Financial Liberalization and Capital Flows: Facts

|

|

|

- Agatha Chandler

- 8 years ago

- Views:

Transcription

1 Financial Liberalization and Capital Flows: Facts Alberto Martin CREI, Universitat Pompeu Fabra and Barcelona GSE July 2014

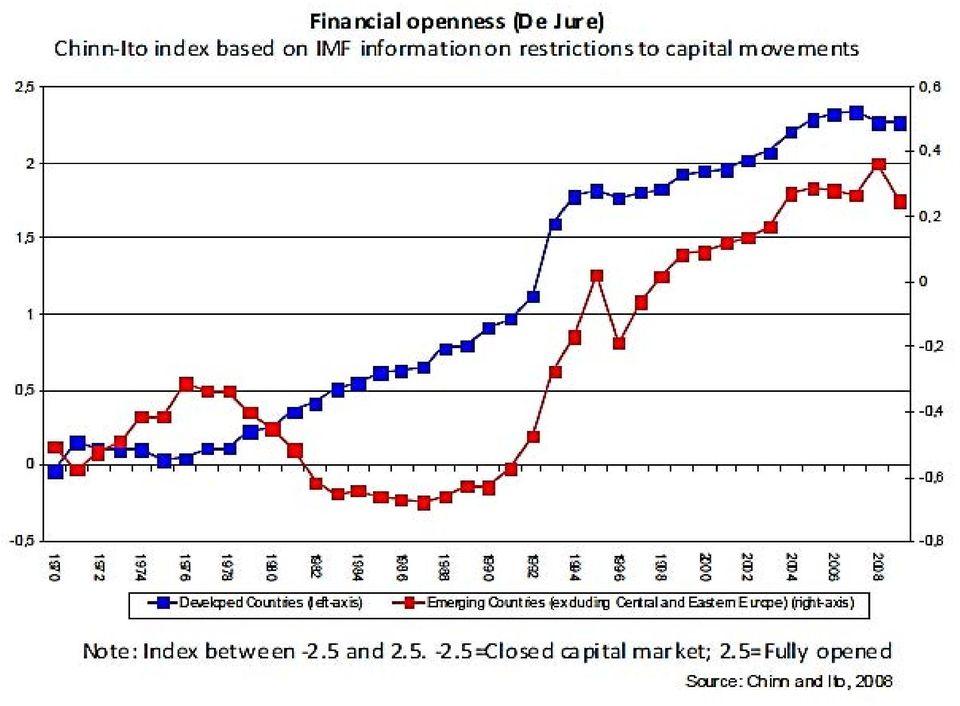

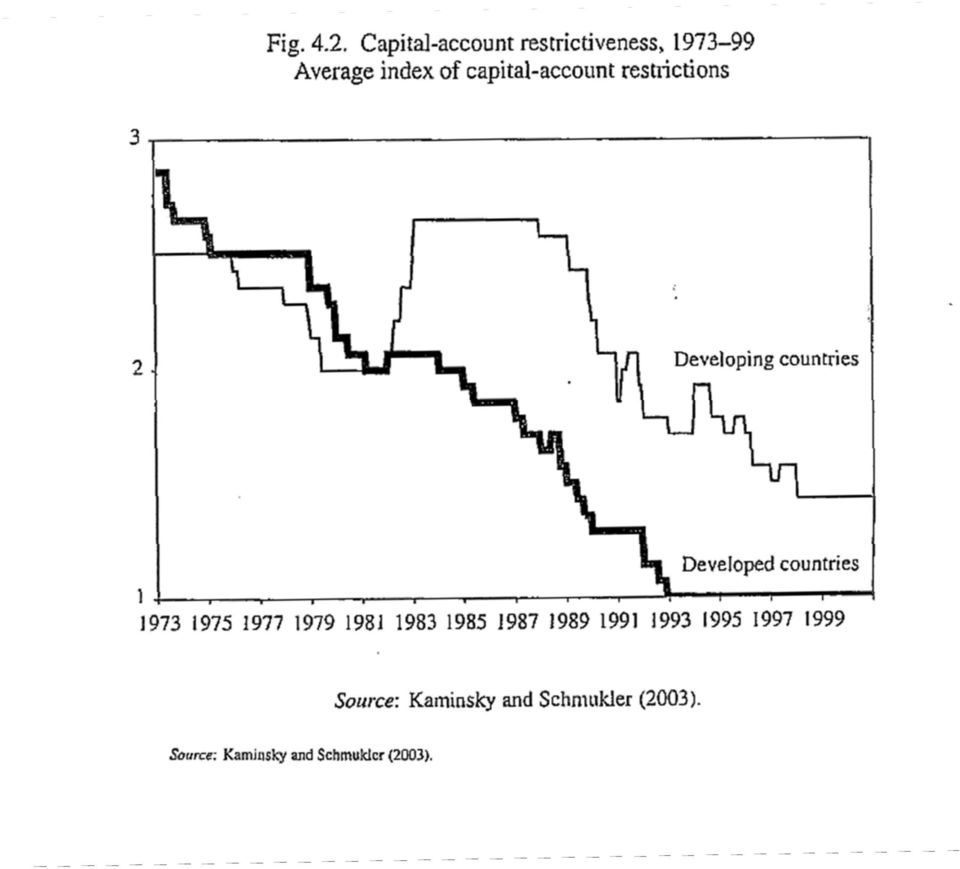

2 The rise of nancial globalization Since the late 1970s Dramatic increase in nancial openness across countries De jure: lower legal and regulatory restrictions to capital ows Based on information from IMF s Annual Report on Exchange Arrangements and Exchange Restrictions (AREAER) De facto: increase in capital ows, foreign assets and liabilities

De facto: increase in capital ows, foreign assets and")

3

4

5 The rise of nancial globalization Since the late 1970s Dramatic increase in nancial openness across countries De jure: lower legal and regulatory restrictions to capital ows De facto: increase in capital ows, foreign assets and liabilities

6 De facto measure of nancial openness Stocks: the value of assets held in a given year foreign assets held by domestics, domestic assets held by foreigners the di erence between the two is the country s net foreign asset position (NF A) important issue of valuation Flows: the value of assets traded for a given year in ows: net purchases of domestic assets by foreign investors (e.g., a loan by a foreign bank to a domestic rm) out ows: net purchases of foreign assets by domestic investors (e.g., a domestic household buying a bond issued by a foreign government) outflows t inflows t = NF A t

outflows t inflows t = NF A t")

7

8 Source: Lane and Milesi Ferretti (2014)

9

10 In some sense, back to where we were... Financial globalization was strong at the end of the 19th century World capital markets were highly integrated Share of UK wealth invested abroad: 17% in 1870 and 33% in 1913 (larger than any country today). This wealth was mostly invested in natural resource-abundant, high growing regions UK composition of foreign assets: Canada + Australia (28%), US (15%), Latin America (24%) This process was interrupted during the world wars, and reversed after World War II

11

12 What are the consequences/expected gains of nancial globalization? Standard narrative predicts di erent types of bene ts from nancial globalization Improved allocation of capital Capital ows towards its more productive uses: capital-scarce, high-productivity countries Higher growth for receiving countries (and for world as a whole) Risk sharing Local risks can be diversi ed through the trade of assets Decreased volatility of consumption relative to output Other e ects Risk shifting Possibility of risk sharing makes it possible to adopt risky, high-return technologies Increased growth and volatility of output Miscellanea: market discipline on domestic policy makers, spillover e ects of FDI, etc...

13 A simple model to x ideas Small country: overlapping generations of size 1 Representative member of generation t maximizes: u (c t;t ) + E t [u (c t;t+1 )] with u() = ln() when young: supplies one unit of labor, earns wage w t, invests with productivity A to produce capital k t+1, k t+1 = A t i t consumes k t+1 c t;t = w t A when old: receives return to capital (full depreciation), consumes c t;t+1 = r t+1 k t+1

, consumes c t;t+1")

14 A simple model to x ideas Small country: overlapping generations of size 1 Representative member of generation t maximizes: u (c t;t ) + E t [u (c t;t+1 )] with u() = ln() when young: supplies one unit of labor, earns wage w t, invests with productivity A to produce capital k t+1, k t+1 = A t i t consumes k t+1 c t;t = w t A when old: receives return to capital (full depreciation), consumes Cobb-Douglas production function: Competitive factor markets: c t;t+1 = r t+1 k t+1 y t = k t w t = (1 ) k t and r t = k 1 t

k t and r t = k")

15 Conventional view: Autarky The law of motion of the capital stock is where s 1 + k t+1 = s A k t (1 ) is the (gross) savings rate

is the (gross) savings")

16 Conventional view: Autarky The law of motion of the capital stock is where s 1 + k t+1 = s A k t (1 ) is the (gross) savings rate These are the dynamics of the Solow model The steady state is k A SS = (s A) 1 1 and A r A SS = s 1

1 1 and A r A SS")

17 Conventional view: Financial liberalization Removes barriers to access international nancial market (IFM) IFM has commitment and buys and sells any bonds with expected gross return 1. Assume country also has commitment to repay its debts. Thus, The budget constraints of generation t are c t;t = w t k t+1 A R t+1 = R t+1 = 1 b t+1 Rt+1 b t+1 R t+1, c t;t+1 = r t+1 k t+1 + b t+1 + b t+1, where b t+1 and b t+1 respectively denote domestic holdings of foreign and domestic bonds. Domestic and foreign bonds are perfect substitutes

18 Conventional view: Financial liberalization Observations savings are una ected due to log utility: k t+1 A + b t+1 R t+1 + b t+1 R t+1 = s k t in this simple model, gross positions are indetermined in equilibrium: only net positions b t+1 + b t+1 are pinned down

19 Conventional view: Financial liberalization The new law of motion of the capital stock is A k 1 t+1 1 = 0, i.e. the marginal return to investment equals the marginal cost of funds (R t+1) There is immediate convergence to current account: s t k SS = ( A) 1 1 i t = s k t k SS A Main e ects of nancial liberalization Capital stock and output grow in capital scarce-countries (i.e., kss A < k SS) Response to shocks? Sensitivity to savings shocks () is reduced lower e ect of savings on output Sensititivity to (anticipated) productivity shocks (A) is enhanced greater investment can be nanced with foreign borrowing In the face of uncertainty, correlation between consumption and output is reduced domestic shocks can be insured with the IFM (risk sharing)

20 What are the consequences/expected gains of nancial globalization? Standard narrative predicts di erent types of bene ts from nancial globalization Improved allocation of capital (mixed evidence) Capital ows towards its more productive uses: capital-scarce, high-productivity countries Higher growth for receiving countries (and for world as a whole) Risk sharing (mixed evidence) Local risks can be diversi ed through the trade of assets Decreased volatility of consumption relative to output Other e ects (perhaps...) In a nutshell, the evidence points to: Small size and wrong direction of capital ows Mixed e ects of nancial liberalization Imperfect degree of risk-sharing among countries Two strands of evidence: nancial liberalization and data on capital ows

21 Evidence on Financial Liberalization: Kose, Prasad, Rogo and Wei (2009) Recap of theory: nancial liberalization should have positive e ects on Growth: more capital should ow to capital-scarce countries, with potential spillovers on TFP Volatility: prediction on output volatility is not obvious, but it should unambiguously decrease consumption volatility by allowing for diversi cation Comovement: related to previous, consumption correlation among countries should increase Analyze evidence and existing literature: what are the conclusions? Measurement of nancial openess: De jure De facto: domestic and foreign prices of similar assets (capital in ows + capital out ows)/gdp (foreign assets + foreign liabilities)/gdp

22 Impact of nancial liberalization on growth No relationship between level of nancial openness and GDP growth ( ) Weak positive relationship between change in nancial openness and growth But it disappears when other controls are introduced Beware of endogeneity throughout!: in this regard, case studies might be informative, but they are equally unconclusive

23 Figure 5A. Level of Financial Openness and GDP Growth, Unconditional Relationship Conditional Relationship 0.06 KOR 0.06 Growth rate of per capita GDP 0.05 THA MUS CHL 0.04 IND IDN MYS LKA 0.03 PRT DOM TUN ESP BGD TUREGYAUS NOR 0.02 PAK NPLJPN CRI GRC USA GHA DEU FIN AUT ITAURY CAN TTO ISR FRA DNK SWE IRN COL SLV TZA NZL GTM BRAFJI JAM 0.01 MEXPHL PER ARGBOL SEN ECUPNG HND DZA KEN 0 MWI PRY ZAF VEN NER TGO ZWE CMR Mean financial openness Growth rate of per capita GDP MUS CHL 0.02 EGY DOM CRI MYS IND KOR TUN 0.01 GTM TUR SLV ISR USATTO AUS BGDCOL LKA GHA PAK IDN URY 0 ZAF THA SEN ESP BRA MEX TZA IRN VEN ITA NOR CANPRT FIN AUT FRA SWE ARG GRC BOL FJI HND DNK NPL DZA PRY KEN NER NZL DEU ZMB ECU CMR JPNPHL JAM PER MWI TGO ZWE Mean financial openness Figure 5B. Change in Financial Openness and GDP Growth, Unconditional Relationship Conditional Relationship 0.06 KOR 0.06 Growth rate of per capita GDP 0.05 THA MUS CHL 0.04 IND IDNMYS LKA 0.03 PRT DOM TUN ESP BGD NOR EGY TUR AUS 0.02 CRI PAK NPL JPNUSA DEU AUT CAN ITA DNK FRA FIN URY GHA GRC ISR SWE TZA TTO COL SLV JAM IRN ZMB NZL 0.01 BRA GTM MEX PHL SEN PER BOL ECU FJI ARG HND 0 MWI DZA PRY ZAF VEN TGONER CMR ZWE Change in financial openness Growth rate of per capita GDP MUS CHL 0.02 EGYMYS CRI DOM TUN IND KOR 0.01 GTM ISRSLV TUR GHA TTO USA COL AUS BGD LKA PAK IDN URY 0 TZA SEN MEX ZAF THA IRN BOL FJI BRA VEN CAN ITA AUT ESPPRT HND DNKFRA NOR FIN SWE KEN PRY GRC ARG NZL DEU JAMZMB NER ECU DZA NPL CMR PHLJPN PER TGOMWI ZWE Change in financial openness Notes: Growth refers to the average real per capita GDP growth. Financial openness is defined as the ratio of gross stocks of foreign assets and liabilities to GDP and is based on a dataset constructed by Lane and Milesi- Ferretti (2006). The second panel uses residuals from a cross-section regression of growth on initial income, population growth, human capital and the investment rate. See Appendix II for abbreviated country names.

24 Interpreting this evidence with care... Henry (2007) casts doubts on these results the standard neoclassical model predicts temporary, not permanent increase in growth after liberalization in steady state, k ss = A R 1 1 nancial liberalization provides temporary growth by lowering the interest rate in the long run, growth in k depends on growth in A Theoretical predictions of liberalization on growth (assuming some gradual adjustment)

25 892 Journal of Economic Literature, Vol. XLV (December 2007) Interest Rate Panel A: The Cost of Capital r r t o t Growth Rate of K Panel B: Investment n + g t o t Growth Rate of Y L Panel C: Growth Rate of GDP per Worker g t o t ln ( Y L ) Panel D: Level of GDP Per Worker Permanent effect of liberalization t o t Figure 2. The Impact of Liberalization on the Cost of Capital, Investment, and Growth

26 Interpreting this evidence with care... In regressing growth on openness, Henry (2007) argues that we should look at time, not cross-country variation (temporary e ects) we should distinguish between developing and developed countries (opposite implications of openness for growth) be careful on how we measure liberalization (de jure vs. de facto) He looks at instances of stock market liberalization (di. measures): ndings fall in the cost of capital (measured through stock prices) increase in investment and in output growth Problems endogeneity (is liberalization undertaken when gains are high?) identi cation (many reforms simultaneous) even then, e ect is signi cant but small (i.e., increase in stock market value of 30%)

27

28

29

30 Interpreting this evidence with care... In regressing growth on openness, Henry (2007) argues that we should look at time, not cross-country variation (temporary e ects) we should distinguish between developing and developed countries (opposite implications of openness for growth) be careful on how we measure liberalization (de jure vs. de facto) He looks at instances of stock market liberalization and nds... fall in the cost of capital increase in investment and in output growth Problems endogeneity (is liberalization undertaken when gains are high?) identi cation (many reforms simultaneous) At the end of the day, e ect is signi cant but small (i.e., increase in stock market value of 30%) perhaps return to foreign investors not so high weak institutions, nancial frictions

31 Impact of nancial liberalization on volatility (Kose et al.) No evidence that nancial liberalization has reduced consumption volatility No systematic evidence of relationship between liberalization and output volatility Evidence that ratio of consumption growth volatility to output growth volatility has actually increased in recent period of nancial globalization moreover, this increase in consumption volatility tends to increase with nancial openness, at least up to a level Mixed evidence on the impact of nancial liberalization on cross-country correlation of consumption growth

32 Distinction between portfolio ows, debt ows, and FDI Portfolio ows (equity market liberalization) FDI Evidence from micro data seems to support the notion that liberalization helps industries that are dependent on external nance Strongest evidence comes from micro data: consistent with the existence of transfer of knowledge to suppliers and custormers, i.e. of vertical spillovers Debt ows (porfolio bond ows and bank loans) These ows are highly volatile and procyclical Also, weaker countries tend to rely on short-term debt denominated in foreign currency, which can increase the likelihood of a crisis

33 A di erent perspective is to look at other, collateral bene ts of capital ows In this view, it is not nancial liberalization per se, but rather its collateral bene ts, that may increase growth Threshold e ects: might be important to have good institutions in place to reap these bene ts Financial sector development For example, bene ts of foreign-owned banks Improved institutional quality and governance Improved corporate governance (due to better monitoring, decreased cost of external nance, etc...) Relationship to public governance: for example, allowing rms to be listed abroad might increase their value Improved macroeconomic policies Once again, beware of endogeneity!

34 Figure 6A. Financial Openness and Financial Development, Private Credit/ GDP Stock Market Capitalization/ GDP JPN DEU 1.4 ZAF MYS Private Credit/ GDP AUT PRTFRA 0.8 ESP NZL MYS THA AUS ISR FIN 0.6 ITA NOR DNK KORZAF CAN TUN SWE CHL 0.4 MUS GRC USA SLVIDN EGY FJI TTO BOL URY BRA PHL IND HND BGD PAK DZA ECU IRN LKA KEN 0.2 SEN COLCRI DOM MEX PNGTGO JAM ZWE GTM NPL PRYPER ARG TUR CMR VEN NER GHA TZA MWI ZMB Mean financial openness Stock Market Capitalization/ GDP 1.2 USA FIN SWE JPN AUS CAN CHL 0.6 FRA ESP JAM DNK 0.4 THA PHLISR NZL KOR TTO GRC DEU MUS ITA NOR INDCHN ZWE BRA ARG PRT 0.2 MEX IRN TUR EGY AUT COL SLV KEN PAK LKA IDN PERGHA NPL CRI ECU VEN TUN FJI BOL MWI HND ZMB 0 BGD GTM PRY TZA URY Mean financial openness Figure 6B. Financial Openness and Institutional Quality, Institutional Quality Control of Corruption Institutional Quality FIN NOR DNK SWE AUS NZL CAN DEUAUT USA PRTFRA JPN ESP CHL CRIITA MUS GRC ISR URY KOR TTO MYS ZAF THA TUN BRA MEX SLVARG JAM IND DOMFJIPHL GHA TURLKA EGY PER BOL CHN SEN HND GTM COL TZA MWI ZMB BGDNPL ECUPNG PRY NER VEN IRN IDN PAKCMR KEN TGO ZWE DZA Control of Corruption FIN NZL DNK SWE NOR CAN AUS AUT USA DEU FRA ESP CHL PRT JPN ISR CRI ITA GRC URY MUS ZAF MYS KOR TUN FJI TTO BRA TURLKA EGY PER INDCHNMEXTHA COL DOM SLVARG SEN JAM NPL PHL GHA IRN DZA BGD ZWE GTM BOL PNG MWI PAK NER ECU VENHND PRYIDN TZA TGO ZMB CMR KEN Mean financial openness Mean financial openness

35 Figure 6C. Financial Openness and Macroeconomic Policies, Monetary Policy Fiscal Policy Log Inflation TUR ZMB -1 ZWE VEN ECU URY -1.5 BRA GHA MEX MWI IRN COL -2 DOM PRY CRI JAM PER GTM BOL TZA ISRHND ZAFARG LKA KEN -2.5 IDN EGY SLV GRC CHL IND NPL DZA PHL PAK PNG TTO BGDMUS PRT -3 CHN KOR TUN NERESP ITA FJI -3.5 CMR THA USAUSNOR NZL DNK CAN SWE SEN TGO MYSFIN AUT FRA -4 DEU -4.5 JPN Mean financial openness Government Budget Balance (%GDP) 10 DZA 5 NOR KOR CHL 0 DOM PRY CMR THA ECU DNK CHN BRA SLVIDN VEN AUS NZL DEU JAM GTM IRN BGDMUS PHL TTO AUT COLCRI USAESP URY IND CAN FIN SWE MEXPERGHA TUN TZATGO MYS PAKZAF EGY HND FRA KEN -5 JPN ARG BOL PNG ZWE FJI PRT TUR SEN NPL NER ITAISR LKA -10 MWI ZMB GRC Mean financial openness Notes: The financial integration data are based on a dataset constructed by Lane and Milesi-Ferretti (2006). Financial Development data are taken from Beck and Al-Hussainy (2006). Private Credit refers to credit given to the private sector by deposit money banks and Stock Market Capitalization is defined as the value of listed shares. Institutional quality data are from Daniel Kaufmann, Aart Kraay and Massimo Mastruzzi (2005) and cover the period Institutional Quality is the average of the following indicators: Voice and Accountability, Political Stability, Government Effectiveness, Regulatory Quality, Rule of Law, and Control of Corruption. Monetary and fiscal data are from the World Bank's World Development Indicators and the IMF's International Financial Statistics and World Economic Outlook databases. Inflation is defined as the annual change in CPI. Government Budget Balance is the difference between government revenues and government expenditures. See Appendix II for abbreviated country names.

36 Evidence on Financial Liberalization: Bon glioli (2008) Analyzes e ects of nancial liberalization on Growth in the capital stock Growth in TFP Sample of 70 countries between 1975 and 1999 Main nding: de jure and de facto measures of nancial liberalization Do not seem to explain growth in the capital stock Seem to be signi cantly and positively correlated with growth in TFP Moreover, nancial liberalization seems to raise likelihood of banking crises We shall return to this point

37 Evidence on Size and Direction of Capital Flows Capital ows between developed and developing countries: much smaller than would be predicted by neo-classical models (Lucas 1990) According to the benchmark model, nancial liberalization should lead to... capital ows towards capital-scarce countries (and decrease in R) at least temporarily, higher growth Consider the production function y t = k t According to theory, capital should ow until return to investment (A kt 1 ) is equalized across countries A simple calibration of India and the US shows k US 15 k INDIA : should lead to massive capital ows! Yet, we do not seem to observe this.... WHY?

38 Alternative explanations... Di erences in human capital? Maybe this makes capital more productive in developed countries, or... Human capital increases TFP because of spillovers Mismeasurements? Maybe the return to capital is actually equalized across countries Even if capital is scarce in developing countries, it is also less productive there Caselli-Feyrer (2007): once income of nonrenewable capital is accounted for, return to renewable capital seems similar between developed and developing countries Financial frictions? Sovereign risk: di culty of enforcing contracts across borders limits ows Or maybe, bad nancial systems limit how much capital an economy may intermediate...

39 In some sense, back to where we were... But current patterns of capital ows are di erent from what they were...

40

41

42

43

44 On direction of capital ows... Recently, global imbalances have caught the attention of economists (Caballero et al., Zilibotti et al.) High growth developing countries (especially China) are actually exporting capital to the rest of the world Hard to interpret according to standard theory And, even if you look at developing countries as a group... Low-growth countries seem to be importing too much capital whereas high-growth countries seem to be exporting too much of it (Prasad et al. (2007), Gourinchas and Jeanne (2009))

45 On direction of capital ows... Recently, global imbalances have caught the attention of economists (Caballero et al., Zilibotti et al.) High growth developing countries (especially China) are actually exporting capital to the rest of the world And, even if you look at developing countries as a group... Low-growth countries seem to be importing too much capital whereas high-growth countries seem to be exporting too much of it (Prasad et al. (2007), Gourinchas and Jeanne (2012)) Do governments play a role? (Kalemli-Ozcan et al. (2012))

46 Current account balances

47 Current account balances

48

49

50 Concluding Remarks Dramatic rise of nancial globalization Large cross-holdings of assets among developed countries Less signi cant for the developing world Size/direction of capital ows seem hard to account for with standard theory Basic predictions of standard model seem at odds with the data No systematic evidence that nancial liberalization leads to capital in ows and faster growth Threshold e ects? No systematic evidence that nancial liberalization reduces volatility of consumption Can nancial frictions help us to reconcile the standard model with the evidence? Contractual frictions: implications in closed vs. open economy Sovereign risk: speci c to the open economy

Financial Liberalization and Capital Flows: Facts

Financial Liberalization and Capital Flows: Facts Alberto Martin CRE, UPF, Barcelona GSE, MF July 6, 2015 Martin (CRE, UPF, Barcelona GSE, MF) CRE Macroeconomics Summer School July 6, 2015 1 / 46 The rise

Financial Liberalization and Capital Flows: Facts Alberto Martin CRE, UPF, Barcelona GSE, MF July 6, 2015 Martin (CRE, UPF, Barcelona GSE, MF) CRE Macroeconomics Summer School July 6, 2015 1 / 46 The rise

The Macroeconomic Implications of Financial Globalization

The Macroeconomic Implications of Financial Globalization Eswar Prasad, IMF Research Department November 10, 2006 The views expressed in this paper are those of the author(s) ) only, and the presence of

The Macroeconomic Implications of Financial Globalization Eswar Prasad, IMF Research Department November 10, 2006 The views expressed in this paper are those of the author(s) ) only, and the presence of

A Pragmatic Approach to Capital Account Liberalization. Eswar Prasad Cornell University

A Pragmatic Approach to Capital Account Liberalization Eswar Prasad Cornell University Presentation partly based on my joint work with: Ayhan Kose, Kenneth Rogoff, Shang-Jin Wei (2003, 2006) Raghuram Rajan

A Pragmatic Approach to Capital Account Liberalization Eswar Prasad Cornell University Presentation partly based on my joint work with: Ayhan Kose, Kenneth Rogoff, Shang-Jin Wei (2003, 2006) Raghuram Rajan

Finance, Growth & Opportunity. Implications for policy

Finance, Growth & Opportunity Implications for policy Today, I will make three points 1) Finance matters for human welfare beyond crises. 2) Financial innovation is associated with arguably necessary for

Finance, Growth & Opportunity Implications for policy Today, I will make three points 1) Finance matters for human welfare beyond crises. 2) Financial innovation is associated with arguably necessary for

Lecture 12 The Solow Model and Convergence. Noah Williams

Lecture 12 The Solow Model and Convergence Noah Williams University of Wisconsin - Madison Economics 312 Spring 2010 Recall: Balanced Growth Path All per-capita variables grow at rate g. All level variables

Lecture 12 The Solow Model and Convergence Noah Williams University of Wisconsin - Madison Economics 312 Spring 2010 Recall: Balanced Growth Path All per-capita variables grow at rate g. All level variables

Addressing The Marketing Problem of the Social Market Economy

Addressing The Marketing Problem of the Social Prepared for: KAS-Conference on 60 Years of Social Market Economy Sankt Augustin, November 30, 2009 Marcus Marktanner, American University of Beirut Outline

Addressing The Marketing Problem of the Social Prepared for: KAS-Conference on 60 Years of Social Market Economy Sankt Augustin, November 30, 2009 Marcus Marktanner, American University of Beirut Outline

In Defense of Wall Street - Does Finance Cause Creative Destruction?

In Defense of Wall Street The Social Productivity of the Financial System Finance is powerful Mobilizes Researches and allocates Monitors and exerts corporate control Provides risk diversification and

In Defense of Wall Street The Social Productivity of the Financial System Finance is powerful Mobilizes Researches and allocates Monitors and exerts corporate control Provides risk diversification and

Financial services and economic development

GDP per capita growth 03/11/2014 Financial services and economic development Thorsten Beck Finance why do we care? 0.04 BWA 0.02 0.00-0.02 COG SLE ALB GAB IND KOR TUR SGP MUS SDN MOZ IRLLUX IDN MAR EGY

GDP per capita growth 03/11/2014 Financial services and economic development Thorsten Beck Finance why do we care? 0.04 BWA 0.02 0.00-0.02 COG SLE ALB GAB IND KOR TUR SGP MUS SDN MOZ IRLLUX IDN MAR EGY

Export Survival and Comparative Advantage

Export Survival and Comparative Advantage (Work in progress) Regional Seminar on Export Diversification, October 27-28, 2010 Bolormaa Tumurchudur, UNCTAD Miho Shirotori, UNCTAD Alessandro Nicita, UNCTAD

Export Survival and Comparative Advantage (Work in progress) Regional Seminar on Export Diversification, October 27-28, 2010 Bolormaa Tumurchudur, UNCTAD Miho Shirotori, UNCTAD Alessandro Nicita, UNCTAD

Figure 1.1 The Parade of World Income. Copyright 2005 Pearson Addison-Wesley. All rights reserved. 1-1

Figure 1.1 The Parade of World Income Copyright 2005 Pearson Addison-Wesley. All rights reserved. 1-1 Copyright 2005 Pearson Addison-Wesley. All rights reserved. 1-2 Growth and Development: The Questions

Figure 1.1 The Parade of World Income Copyright 2005 Pearson Addison-Wesley. All rights reserved. 1-1 Copyright 2005 Pearson Addison-Wesley. All rights reserved. 1-2 Growth and Development: The Questions

Economic Growth: the role of institutions

ECON 184 Economic Growth: the role of institutions ECON 184: Institutions and Growth January 26, 2010 1 Contents 1 Institutions and growth: initial analysis 3 2 How can institutions affect economic growth?

ECON 184 Economic Growth: the role of institutions ECON 184: Institutions and Growth January 26, 2010 1 Contents 1 Institutions and growth: initial analysis 3 2 How can institutions affect economic growth?

Macroeconomics II. Growth

Macroeconomics II Growth Growth Possibilities We previously referred to the aggregate production function Y = A K α L 1- α. The growth rate of real GDP, Y, is generated by the contributions of A, K and

Macroeconomics II Growth Growth Possibilities We previously referred to the aggregate production function Y = A K α L 1- α. The growth rate of real GDP, Y, is generated by the contributions of A, K and

Accounting For Cross-Country Income Di erences

Accounting For Cross-Country Income Di erences January 2011 () Aggregation January 2011 1 / 10 Standard Primal Growth Accounting Aggregate production possibilities frontier: where Change in output is )

Accounting For Cross-Country Income Di erences January 2011 () Aggregation January 2011 1 / 10 Standard Primal Growth Accounting Aggregate production possibilities frontier: where Change in output is )

The new gold standard? Empirically situating the TPP in the investment treaty universe

Graduate Institute of International and Development Studies Center for Trade and Economic Integration Working Paper Series Working Paper N IHEIDCTEI2015-08 The new gold standard? Empirically situating

Graduate Institute of International and Development Studies Center for Trade and Economic Integration Working Paper Series Working Paper N IHEIDCTEI2015-08 The new gold standard? Empirically situating

Overview of Growth Research in the Past Two Decades

Overview of Growth Research in the Past Two Decades by Pete Klenow Stanford University and NBER September 21, 2010 Early Growth Research 1950s Solow (1956) 1960s Nelson and Phelps (1966) 1970s Dark Ages

Overview of Growth Research in the Past Two Decades by Pete Klenow Stanford University and NBER September 21, 2010 Early Growth Research 1950s Solow (1956) 1960s Nelson and Phelps (1966) 1970s Dark Ages

Bringing Up Incentives: A Look at the Determinants of Poverty. Alice Sheehan

Bringing Up Incentives: A Look at the Determinants of Poverty Alice Sheehan Outline presentation What s going on out there? Growth, Human Development indicators, Poverty rates, etc. A look at determinants

Bringing Up Incentives: A Look at the Determinants of Poverty Alice Sheehan Outline presentation What s going on out there? Growth, Human Development indicators, Poverty rates, etc. A look at determinants

Lecture 21: Institutions II

Lecture 21: Institutions II Dave Donaldson and Esther Duflo 14.73 Challenges of World Poverty Institutions II: Plan for the lecture Discussion of assigned reading (Acemoglu, Johnson and Robinson) Causes

Lecture 21: Institutions II Dave Donaldson and Esther Duflo 14.73 Challenges of World Poverty Institutions II: Plan for the lecture Discussion of assigned reading (Acemoglu, Johnson and Robinson) Causes

A new metrics for the Economic Complexity of countries and products

A new metrics for the Economic Complexity of countries and products Andrea Tacchella Dept. of Physics, La Sapienza - University of Rome Istituto dei Sistemi Complessi, CNR Roma CRISISLAB ANALYTICS FOR

A new metrics for the Economic Complexity of countries and products Andrea Tacchella Dept. of Physics, La Sapienza - University of Rome Istituto dei Sistemi Complessi, CNR Roma CRISISLAB ANALYTICS FOR

Measuring the Pollution Terms of Trade with Technique Effects

Measuring the Pollution Terms of Trade with Technique Effects Jean-Marie Grether, University of Neuchâtel Nicole Mathys, Swiss Federal Office of Energy and University of Neuchâtel Conference on the International

Measuring the Pollution Terms of Trade with Technique Effects Jean-Marie Grether, University of Neuchâtel Nicole Mathys, Swiss Federal Office of Energy and University of Neuchâtel Conference on the International

Life-cycle Human Capital Accumulation Across Countries: Lessons From U.S. Immigrants

Life-cycle Human Capital Accumulation Across Countries: Lessons From U.S. Immigrants David Lagakos, UCSD and NBER Benjamin Moll, Princeton and NBER Tommaso Porzio, Yale Nancy Qian, Yale and NBER Todd Schoellman,

Life-cycle Human Capital Accumulation Across Countries: Lessons From U.S. Immigrants David Lagakos, UCSD and NBER Benjamin Moll, Princeton and NBER Tommaso Porzio, Yale Nancy Qian, Yale and NBER Todd Schoellman,

Economic Complexity and the Wealth of Nations

Economic Complexity and the Wealth of Nations Cesar A. Hidalgo ABC Career Development Professor MIT Media Lab Faculty Associate, Center for International Development Harvard University EARTH WIND WATER

Economic Complexity and the Wealth of Nations Cesar A. Hidalgo ABC Career Development Professor MIT Media Lab Faculty Associate, Center for International Development Harvard University EARTH WIND WATER

Trade and International Integration: A Developing Program of Research

Trade and International Integration: A Developing Program of Research World Bank Development Economics Research Group Geneva, June 2013 Three areas of focus I. Implications of the changing patterns of

Trade and International Integration: A Developing Program of Research World Bank Development Economics Research Group Geneva, June 2013 Three areas of focus I. Implications of the changing patterns of

Addressing institutional issues in the Poverty Reduction Strategy Paper process

SESSION 1 Addressing institutional issues in the Poverty Reduction Strategy Paper process Scoping notes, detailed diagnostics, and participatory processes Public Sector Reform and Capacity Building Unit

SESSION 1 Addressing institutional issues in the Poverty Reduction Strategy Paper process Scoping notes, detailed diagnostics, and participatory processes Public Sector Reform and Capacity Building Unit

Ken Jackson. January 31st, 2013

Wilfrid Laurier University January 31st, 2013 Recap of the technology models Do the models match historical data? growth accounting Estimating technology change through history A revised model of technology

Wilfrid Laurier University January 31st, 2013 Recap of the technology models Do the models match historical data? growth accounting Estimating technology change through history A revised model of technology

The Effects of Infrastructure Development on Growth and Income Distribution

The Effects of Infrastructure Development on Growth and Income Distribution César Calderón Luis Servén (Central Bank of Chile) (The World Bank) ALIDE - The World Bank - Banco BICE Reunión Latinoamericana

The Effects of Infrastructure Development on Growth and Income Distribution César Calderón Luis Servén (Central Bank of Chile) (The World Bank) ALIDE - The World Bank - Banco BICE Reunión Latinoamericana

Institutional Change and Growth-Enabling Governance Capabilities

Institutional Change and Growth-Enabling Governance Capabilities Nicolas Meisel Strategy and Research Dept - French Development Agency (AFD) Jacques Ould Aoudia Treasury and Economic Policy Directorate

Institutional Change and Growth-Enabling Governance Capabilities Nicolas Meisel Strategy and Research Dept - French Development Agency (AFD) Jacques Ould Aoudia Treasury and Economic Policy Directorate

The Marginal Product of Capital. Francesco Caselli. Discussion by

7 TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 9-10, 2006 The Marginal Product of Capital Francesco Caselli Discussion by Chang-Tai Hsieh University of California, Berkeley The views expressed

7 TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 9-10, 2006 The Marginal Product of Capital Francesco Caselli Discussion by Chang-Tai Hsieh University of California, Berkeley The views expressed

The contribution of trade in financial services to economic growth and development. Thorsten Beck

The contribution of trade in financial services to economic growth and development Thorsten Beck Finance why do we care? 0.04 BWA GDP per capita growth 0.02 0.00-0.02 COG SLE ALB GAB IND KOR TUR SGP MUS

The contribution of trade in financial services to economic growth and development Thorsten Beck Finance why do we care? 0.04 BWA GDP per capita growth 0.02 0.00-0.02 COG SLE ALB GAB IND KOR TUR SGP MUS

Building Capacity in PFM

Building Capacity in PFM Measuring economic governance in the context of national development planning LAMIA MOUBAYED BISSAT Beirut, Lebanon, 13 June 2014 The Institut des Finances Basil Fuleihan 1996

Building Capacity in PFM Measuring economic governance in the context of national development planning LAMIA MOUBAYED BISSAT Beirut, Lebanon, 13 June 2014 The Institut des Finances Basil Fuleihan 1996

Natural Resources and Development in the Middle East and North Africa: An Alternative Perspective

Natural Resources and Development in the Middle East and North Africa: An Alternative Perspective Daniel Lederman and Mustapha K. Nabli The World Bank Presentation at the Workshop on Natural Resources

Natural Resources and Development in the Middle East and North Africa: An Alternative Perspective Daniel Lederman and Mustapha K. Nabli The World Bank Presentation at the Workshop on Natural Resources

Economic Growth: The Neo-classical & Endogenous Story

Density of countries Economic Growth: The Neo-classical & Endogenous Story EC307 ECONOMIC DEVELOPMENT 1960 Dr. Kumar Aniet University of Cambridge & LSE Summer School Lecture 4 1980 2000 created on July

Density of countries Economic Growth: The Neo-classical & Endogenous Story EC307 ECONOMIC DEVELOPMENT 1960 Dr. Kumar Aniet University of Cambridge & LSE Summer School Lecture 4 1980 2000 created on July

Infrastructure and Economic. Norman V. Loayza, World ldbank Rei Odawara, World Bank

Infrastructure and Economic Growth thin Egypt Norman V. Loayza, World ldbank Rei Odawara, World Bank Motivation Questions How does Egypt compare internationally regarding public infrastructure? Is Egypt

Infrastructure and Economic Growth thin Egypt Norman V. Loayza, World ldbank Rei Odawara, World Bank Motivation Questions How does Egypt compare internationally regarding public infrastructure? Is Egypt

Employment, Structural Change, and Economic Development. Dani Rodrik March 15, 2012

Employment, Structural Change, and Economic Development Dani Rodrik March 15, 2012 A remarkable reversal in fortunes since 1990s -.04 -.02 0.02.04.06 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

Employment, Structural Change, and Economic Development Dani Rodrik March 15, 2012 A remarkable reversal in fortunes since 1990s -.04 -.02 0.02.04.06 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

How To Explain Euro Area Imbalances

GLOBAL IMBALANCES, CAPITAL FLOWS, AND THE CRISIS Gian Maria Milesi-Ferretti International Monetary Fund Global imbalances have declined.. Even though stock positions are still expanding 20 15 Net foreign

GLOBAL IMBALANCES, CAPITAL FLOWS, AND THE CRISIS Gian Maria Milesi-Ferretti International Monetary Fund Global imbalances have declined.. Even though stock positions are still expanding 20 15 Net foreign

The Fall of the Final Mercantilism

The Fall of the Final Mercantilism Labour Mobility in the Caribbean and the World, from Arthur Lewis to the 21 st Century Eastern Caribbean Central Bank Michael Clemens November 3, 2010 1 2 Migration

The Fall of the Final Mercantilism Labour Mobility in the Caribbean and the World, from Arthur Lewis to the 21 st Century Eastern Caribbean Central Bank Michael Clemens November 3, 2010 1 2 Migration

Incen%ves The Good, the Bad and the Ugly

Incen%ves The Good, the Bad and the Ugly Vale Columbia Center Interna%onal Investment Conference New York, Nov 13-14, 2013 Sebas%an James The World Bank Group 1 Prevalence of Tax Incen%ves around the Number

Incen%ves The Good, the Bad and the Ugly Vale Columbia Center Interna%onal Investment Conference New York, Nov 13-14, 2013 Sebas%an James The World Bank Group 1 Prevalence of Tax Incen%ves around the Number

How To Account For Differences In Intermediate Input To Output Ratios Across Countries

Agriculture and Aggregate Productivity: A Quantitative Cross-Country Analysis Diego Restuccia University of Toronto Dennis Tao Yang Virginia Polytechnic Institute Xiaodong Zhu University of Toronto March

Agriculture and Aggregate Productivity: A Quantitative Cross-Country Analysis Diego Restuccia University of Toronto Dennis Tao Yang Virginia Polytechnic Institute Xiaodong Zhu University of Toronto March

China: How to maintain balanced growth? Ricardo Hausmann Kennedy School of Government Harvard University

China: How to maintain balanced growth? Ricardo Hausmann Kennedy School of Government Harvard University China s growth process An unprecedented miracle China has been the fastest growing country in the

China: How to maintain balanced growth? Ricardo Hausmann Kennedy School of Government Harvard University China s growth process An unprecedented miracle China has been the fastest growing country in the

Deep Roots of Comparative Development

Deep Roots of Comparative Development Oded Galor AEA Continuing Education Program Lecture III - AEA 2014 Oded Galor Roots of Comparative Development Lecture III - AEA 2014 1 / 41 Deep Roots of Comparative

Deep Roots of Comparative Development Oded Galor AEA Continuing Education Program Lecture III - AEA 2014 Oded Galor Roots of Comparative Development Lecture III - AEA 2014 1 / 41 Deep Roots of Comparative

Today s tips for the Country Buy Report

High level outline Today s tips for the Country Buy Report Stephen Malpezzi Introduction Overview of the country and economy Basic indicators (GDP, employment, etc.) Key institutions, the setting How does

High level outline Today s tips for the Country Buy Report Stephen Malpezzi Introduction Overview of the country and economy Basic indicators (GDP, employment, etc.) Key institutions, the setting How does

Outline 4/22/2011. Koc University April, 2011

4/22/211 Koc University April, 211 Outline Main messages Crisis experience and focus Reserves trends Review of existing approaches Proposed new approach and metric Cost of reserves Reserve alternatives

4/22/211 Koc University April, 211 Outline Main messages Crisis experience and focus Reserves trends Review of existing approaches Proposed new approach and metric Cost of reserves Reserve alternatives

Human Rights and Governance: The Empirical Challenge. Daniel Kaufmann World Bank Institute. www.worldbank.org/wbi/governance/

Human Rights and Governance: The Empirical Challenge Daniel Kaufmann World Bank Institute www.worldbank.org/wbi/governance/ Presentation at Human Rights and Development: Towards Mutual Reinforcement Conference,

Human Rights and Governance: The Empirical Challenge Daniel Kaufmann World Bank Institute www.worldbank.org/wbi/governance/ Presentation at Human Rights and Development: Towards Mutual Reinforcement Conference,

Lecture 9: Institutions, Geography and Culture. Based on Acemoglu s L. Robbins lectures

Lecture 9: Institutions, Geography and Culture Based on Acemoglu s L. Robbins lectures 1 The Wealth of Nations Vast differences in prosperity across countries today. Income per capita in sub-saharan Africa

Lecture 9: Institutions, Geography and Culture Based on Acemoglu s L. Robbins lectures 1 The Wealth of Nations Vast differences in prosperity across countries today. Income per capita in sub-saharan Africa

Technology Choice. Francesco Caselli. Summer School 2005

Technology Choice Francesco Caselli Summer School 2005 1 Motivation All of the evidence and all of the models we have studied so far assume that cross-country technology differences are factor-neutral.

Technology Choice Francesco Caselli Summer School 2005 1 Motivation All of the evidence and all of the models we have studied so far assume that cross-country technology differences are factor-neutral.

Political Economy of Growth

1 Political Economy of Growth Daron Acemoglu Department of Economics, MIT Milan, DEFAP June 11, 2007 The Wealth of Nations Vast differences in prosperity across countries today. Income per capita in sub-saharan

1 Political Economy of Growth Daron Acemoglu Department of Economics, MIT Milan, DEFAP June 11, 2007 The Wealth of Nations Vast differences in prosperity across countries today. Income per capita in sub-saharan

Governance, Rule of Law and Transparency Matters: BRICs in Global Perspective

Governance, Rule of Law and Transparency Matters: BRICs in Global Perspective Daniel Kaufmann * Senior Fellow, Brookings Institution http://www.brookings.edu/experts/kaufmannd.aspx Panel on Transparency

Governance, Rule of Law and Transparency Matters: BRICs in Global Perspective Daniel Kaufmann * Senior Fellow, Brookings Institution http://www.brookings.edu/experts/kaufmannd.aspx Panel on Transparency

THE QUALITY OF GOVERNMENT CA FOSCARI INTERNATIONAL LECTURE

THE QUALITY OF GOVERNMENT CA FOSCARI INTERNATIONAL LECTURE Andrei Shleifer December 12, 2012 1 Richer countries almost always have better governments Less corrupt More efficient Quality of government improves

THE QUALITY OF GOVERNMENT CA FOSCARI INTERNATIONAL LECTURE Andrei Shleifer December 12, 2012 1 Richer countries almost always have better governments Less corrupt More efficient Quality of government improves

DEPENDENT ELITES IN POST- SOCIALISM: ARE LAND-BASED POST- COLONIAL SYSTEMS SO DIFFERENT FROM THE TRANSCONTINENTAL ONES? by Pal TAMAS [Institute of

DEPENDENT ELITES IN POST- SOCIALISM: ARE LAND-BASED POST- COLONIAL SYSTEMS SO DIFFERENT FROM THE TRANSCONTINENTAL ONES? by Pal TAMAS [Institute of Sociology, HAS Budapest] STRUCTURE OF THE PAPER 1. STATE

DEPENDENT ELITES IN POST- SOCIALISM: ARE LAND-BASED POST- COLONIAL SYSTEMS SO DIFFERENT FROM THE TRANSCONTINENTAL ONES? by Pal TAMAS [Institute of Sociology, HAS Budapest] STRUCTURE OF THE PAPER 1. STATE

The Shift to Government Banking:

The Shift to Government Banking: Risks for the Netherlands and other Developed Countries Prof. Florencio Lopez de Silanes EDHEC Business School, NBER and DSF April 28, 2011 Amsterdam Outline I. The Policy

The Shift to Government Banking: Risks for the Netherlands and other Developed Countries Prof. Florencio Lopez de Silanes EDHEC Business School, NBER and DSF April 28, 2011 Amsterdam Outline I. The Policy

Rodolfo Debenedetti Lecture

Rodolfo Debenedetti Lecture Andrei Shleifer March 2005 Legal Origin Distribution Legal Origins = English = French = German = Scandinavian = Socialist Institution Procedural Formalism Outcomes Time to evict

Rodolfo Debenedetti Lecture Andrei Shleifer March 2005 Legal Origin Distribution Legal Origins = English = French = German = Scandinavian = Socialist Institution Procedural Formalism Outcomes Time to evict

Trade Policy Restrictiveness in Transportation Services

Trade Policy Restrictiveness in Transportation Services Ingo Borchert, Batshur Gootiiz and Aaditya Mattoo Development Research Group Trade and International Integration, The World Bank OECD Expert Meeting

Trade Policy Restrictiveness in Transportation Services Ingo Borchert, Batshur Gootiiz and Aaditya Mattoo Development Research Group Trade and International Integration, The World Bank OECD Expert Meeting

How To Understand The World'S Governance

Metrics Matters: Measures of Governance and Security and the Business Perspective An initial empirical exploration Daniel Kaufmann, World Bank Institute www.worldbank.org/wbi/governance For presentation

Metrics Matters: Measures of Governance and Security and the Business Perspective An initial empirical exploration Daniel Kaufmann, World Bank Institute www.worldbank.org/wbi/governance For presentation

Fear of flying: Policy stances in a troubled world economy

Fear of flying: Policy stances in a troubled world economy UNCTAD G-24 Technical Meeting Luxor, 10-11 March 2014 Session 1 Global Economy A weakening economic performance reflects inability to address

Fear of flying: Policy stances in a troubled world economy UNCTAD G-24 Technical Meeting Luxor, 10-11 March 2014 Session 1 Global Economy A weakening economic performance reflects inability to address

NGO PERSPECTIVE: FROM WORDS TO DEEDS

MMSD & IIED Managing Mineral Wealth NGO PERSPECTIVE: FROM WORDS TO DEEDS Miguel Schloss Executive Director Transparency International Issues Policy distortions Institutional incentives Governance Implications

MMSD & IIED Managing Mineral Wealth NGO PERSPECTIVE: FROM WORDS TO DEEDS Miguel Schloss Executive Director Transparency International Issues Policy distortions Institutional incentives Governance Implications

Does Absolute Latitude Explain Underdevelopment?

AREC 345: Global Poverty and Economic Development Lecture 4 Professor: Pamela Jakiela Department of Agricultural and Resource Economics University of Maryland, College Park Does Absolute Latitude Explain

AREC 345: Global Poverty and Economic Development Lecture 4 Professor: Pamela Jakiela Department of Agricultural and Resource Economics University of Maryland, College Park Does Absolute Latitude Explain

TRADE WATCH DATA JANUARY T RVSFRRTVL

Public Disclosure Authorized TRADE WATCH DATA JANUARY T RVSFRRTVL Public Disclosure Authorized A C F D H T W B DECRG Public Disclosure Authorized Public Disclosure Authorized *TRADE WATCH is a monthly

Public Disclosure Authorized TRADE WATCH DATA JANUARY T RVSFRRTVL Public Disclosure Authorized A C F D H T W B DECRG Public Disclosure Authorized Public Disclosure Authorized *TRADE WATCH is a monthly

A Survey of Securities Laws and Enforcement

A Survey of Securities Laws and Enforcement Preliminary Draft By Florencio Lopez-de-Silanes YALE University and NBER October 2003 *I am indebted to Patricio Amador, Jose Caballero and Manuel Garcia-Huitron

A Survey of Securities Laws and Enforcement Preliminary Draft By Florencio Lopez-de-Silanes YALE University and NBER October 2003 *I am indebted to Patricio Amador, Jose Caballero and Manuel Garcia-Huitron

Gender Inequality, Income, and Growth: Are Good Times Good for Women?

POLICY RESEARCH REPORT ON GENDER AND DEVELOPMENT Working Paper Series, No. 1 Gender Inequality, Income, and Growth: Are Good Times Good for Women? David Dollar Roberta Gatti Gender differentials in education

POLICY RESEARCH REPORT ON GENDER AND DEVELOPMENT Working Paper Series, No. 1 Gender Inequality, Income, and Growth: Are Good Times Good for Women? David Dollar Roberta Gatti Gender differentials in education

Estimating Global Migration Flow Tables Using Place of Birth Data

Estimating Global Migration Flow Tables Using Place of Birth Data Guy J. Abel Wittgenstein Centre (IIASA, VID/ÖAW, WU) Vienna Institute of Demography/Austrian Academy of Sciences 1 Introduction International

Estimating Global Migration Flow Tables Using Place of Birth Data Guy J. Abel Wittgenstein Centre (IIASA, VID/ÖAW, WU) Vienna Institute of Demography/Austrian Academy of Sciences 1 Introduction International

Tripartite Agreements for MEPC.2/Circ. Lists 1, 3, 4 received by IMO following issuance of MEPC.2/Circ.20

The following is a list of tripartite agreements reported to IMO during the period between the issuance of the annual MEPC.2/Circular, disseminated in December of each year. Any countries wishing to join

The following is a list of tripartite agreements reported to IMO during the period between the issuance of the annual MEPC.2/Circular, disseminated in December of each year. Any countries wishing to join

Geography and Economic Transition

Global Spatial Analysis at the Grid Cell Level Mesbah Motamed Raymond Florax Will Masters Department of Agricultural Economics Purdue University March 2009 Urbanization at the grid cell level Growth regimes

Global Spatial Analysis at the Grid Cell Level Mesbah Motamed Raymond Florax Will Masters Department of Agricultural Economics Purdue University March 2009 Urbanization at the grid cell level Growth regimes

Subjective Well-Being, Income, Economic Development and Growth

Subjective Well-Being, Income, Economic Development and Growth Dan Sacks, Betsey Stevenson and Justin Wolfers Wharton School, University of Pennsylvania and NBER Annual Bank Conference on Development Economics--Stockholm,

Subjective Well-Being, Income, Economic Development and Growth Dan Sacks, Betsey Stevenson and Justin Wolfers Wharton School, University of Pennsylvania and NBER Annual Bank Conference on Development Economics--Stockholm,

2006/SOM1/ACT/WKSP/007a Recasting Governance for the XXI Century - Presentation

2006/SOM1/ACT/WKSP/007a Recasting Governance for the XXI Century - Presentation Submitted by: Miguel Schloss, Managing Partner DamConsult Ltd. APEC Workshop on Anti-Corruption Measures for the Development

2006/SOM1/ACT/WKSP/007a Recasting Governance for the XXI Century - Presentation Submitted by: Miguel Schloss, Managing Partner DamConsult Ltd. APEC Workshop on Anti-Corruption Measures for the Development

Globalization, Technology and Inequality

Globalization, Technology and nequality Lecture 4: Trade, O shoring and nequality Gino Gancia July 5, 2012 Gino Gancia () Lecture 4 July 5, 2012 1 / 26 Trends in Wage nequality within-country wage inequality

Globalization, Technology and nequality Lecture 4: Trade, O shoring and nequality Gino Gancia July 5, 2012 Gino Gancia () Lecture 4 July 5, 2012 1 / 26 Trends in Wage nequality within-country wage inequality

Rethinking the Wealth of Nations. Daron Acemoglu, MIT FEEM Lecture, December 14, 2009.

Rethinking the Wealth of Nations Daron Acemoglu, MIT FEEM Lecture, December 14, 2009. 1 The Failure of Nations Vast differences in prosperity across countries today. Income per capita in sub-saharan Africa

Rethinking the Wealth of Nations Daron Acemoglu, MIT FEEM Lecture, December 14, 2009. 1 The Failure of Nations Vast differences in prosperity across countries today. Income per capita in sub-saharan Africa

Informality in Latin America and the Caribbean

WPS4888 Policy Research Working Paper 4888 Informality in Latin America and the Caribbean Norman V. Loayza Luis Servén Naotaka Sugawara The World Bank Development Research Group Macroeconomics and Growth

WPS4888 Policy Research Working Paper 4888 Informality in Latin America and the Caribbean Norman V. Loayza Luis Servén Naotaka Sugawara The World Bank Development Research Group Macroeconomics and Growth

ECON 260 Theories of Economic Development. Instructor: Jorge Agüero. Fall 2008. Lecture 1 September 29, 2008 1

ECON 260 Theories of Economic Development. Instructor: Jorge Agüero. Fall 2008. Lecture 1 September 29, 2008 1 General information Time and location: TR 2:10-3:30 p.m. SPR 3123 Office hours: T 10am-11am,

ECON 260 Theories of Economic Development. Instructor: Jorge Agüero. Fall 2008. Lecture 1 September 29, 2008 1 General information Time and location: TR 2:10-3:30 p.m. SPR 3123 Office hours: T 10am-11am,

14.452 Economic Growth: Lecture 4, The Solow Growth Model and the Data

14.452 Economic Growth: Lecture 4, The Solow Growth Model and the Data Daron Acemoglu MIT November 8, 2011. Daron Acemoglu (MIT) Economic Growth Lecture 4 November 8, 2011. 1 / 52 Mapping the Model to

14.452 Economic Growth: Lecture 4, The Solow Growth Model and the Data Daron Acemoglu MIT November 8, 2011. Daron Acemoglu (MIT) Economic Growth Lecture 4 November 8, 2011. 1 / 52 Mapping the Model to

Tripartite Agreements for MEPC.2/Circ. Lists 1, 3, 4 received by IMO following issuance of MEPC.2/Circ.21

The following is a list of tripartite agreements reported to IMO during the period between the issuance of the annual MEPC.2/Circular, disseminated in December of each year. Any countries wishing to join

The following is a list of tripartite agreements reported to IMO during the period between the issuance of the annual MEPC.2/Circular, disseminated in December of each year. Any countries wishing to join

Subjective Well Being, Income, Economic Development and Growth

Subjective Well Being, Income, Economic Development and Growth Dan Sacks, Betsey Stevenson and Justin Wolfers Wharton School, University of Pennsylvania and NBER CSLS ICP Conference on Happiness December

Subjective Well Being, Income, Economic Development and Growth Dan Sacks, Betsey Stevenson and Justin Wolfers Wharton School, University of Pennsylvania and NBER CSLS ICP Conference on Happiness December

Infrastructure and Economic Growth in Egypt

Public Disclosure Authorized Policy Research Working Paper 5177 WPS5177 Public Disclosure Authorized Public Disclosure Authorized Infrastructure and Economic Growth in Egypt Norman V. Loayza Rei Odawara

Public Disclosure Authorized Policy Research Working Paper 5177 WPS5177 Public Disclosure Authorized Public Disclosure Authorized Infrastructure and Economic Growth in Egypt Norman V. Loayza Rei Odawara

Informality in Latin America and the Caribbean

Public Disclosure Authorized Policy Research Working Paper 4888 WPS4888 Public Disclosure Authorized Public Disclosure Authorized Informality in Latin America and the Caribbean Norman V. Loayza Luis Servén

Public Disclosure Authorized Policy Research Working Paper 4888 WPS4888 Public Disclosure Authorized Public Disclosure Authorized Informality in Latin America and the Caribbean Norman V. Loayza Luis Servén

FEDERAL RESERVE BANK of ATLANTA

FEDERAL RESERVE BANK of ATLANTA Financial and Real Integration Scott L. Baier and Gerald P. Dwyer Jr. Working Paper 2008-14 May 2008 WORKING PAPER SERIES FEDERAL RESERVE BANK of ATLANTA WORKING PAPER SERIES

FEDERAL RESERVE BANK of ATLANTA Financial and Real Integration Scott L. Baier and Gerald P. Dwyer Jr. Working Paper 2008-14 May 2008 WORKING PAPER SERIES FEDERAL RESERVE BANK of ATLANTA WORKING PAPER SERIES

Fiscal Management: Lessons from. Koshy Mathai 10 July 2013

Fiscal Management: Lessons from Emerging Market Economies Koshy Mathai 10 July 2013 1 Outline 1. Importance of fiscal discipline 2. Sri Lanka overview 3. Revenue 4. Expenditure 5. Fiscal space and countercylical

Fiscal Management: Lessons from Emerging Market Economies Koshy Mathai 10 July 2013 1 Outline 1. Importance of fiscal discipline 2. Sri Lanka overview 3. Revenue 4. Expenditure 5. Fiscal space and countercylical

Econ 1340: World Economic History

Econ 1340: World Economic History Lecture 16 Camilo Gracía-Jimeno University of Pennsylvania April 4, 2011 Camilo Gracía-Jimeno (University of Pennsylvania)Econ 1340: World Economic History April 4, 2011

Econ 1340: World Economic History Lecture 16 Camilo Gracía-Jimeno University of Pennsylvania April 4, 2011 Camilo Gracía-Jimeno (University of Pennsylvania)Econ 1340: World Economic History April 4, 2011

Institute for Development Policy and Management (IDPM)

") Institute for Development Policy and Management (IDPM) Development Economics and Public Policy Working Paper Series WP No. 33/212 Published by: Development Economics and Public Policy Cluster, Institute

Institute for Development Policy and Management (IDPM) Development Economics and Public Policy Working Paper Series WP No. 33/212 Published by: Development Economics and Public Policy Cluster, Institute

EC 2725 April 2009. Law and Finance. Effi Benmelech Harvard & NBER

EC 2725 April 2009 Law and Finance Effi Benmelech Harvard & NBER Broad Picture A market economy is not only laissez faire but it also requires a set of institutions that allow markets to work their magic.

EC 2725 April 2009 Law and Finance Effi Benmelech Harvard & NBER Broad Picture A market economy is not only laissez faire but it also requires a set of institutions that allow markets to work their magic.

The distribution of household financial contributions to the health system: A look outside Latin America and the Caribbean

The distribution of household financial contributions to the health system: A look outside Latin America and the Caribbean Priyanka Saksena and Ke Xu 3 November, 2008 Santiago 1 The distribution of household

The distribution of household financial contributions to the health system: A look outside Latin America and the Caribbean Priyanka Saksena and Ke Xu 3 November, 2008 Santiago 1 The distribution of household

Discussion of Growing Like China

Discussion of Growing Like China by Song, Storesletten and Zilibotti Alberto Martin CREI and UPF December 2008 Alberto Martin (CREI and UPF) Discussion of Growing Like China December 2008 1 / 10 This paper

Discussion of Growing Like China by Song, Storesletten and Zilibotti Alberto Martin CREI and UPF December 2008 Alberto Martin (CREI and UPF) Discussion of Growing Like China December 2008 1 / 10 This paper

Movement and development. Australian National University Jan. 17, 2013 Michael Clemens

Movement and development Australian National University Jan. 17, 2013 Michael Clemens ? 60% Benefits Little Haiti Cap-Haïtien Gibson and McKenzie 2010 Tongan seasonal workers in NZ NZ$1,400/family

Movement and development Australian National University Jan. 17, 2013 Michael Clemens ? 60% Benefits Little Haiti Cap-Haïtien Gibson and McKenzie 2010 Tongan seasonal workers in NZ NZ$1,400/family

Non-market strategy under weak institutions

Lectures 5-6 Non-market strategy under weak institutions 1 Outline 1. Does weakness of institutions matter for business and economic performance? 2. Which institutions matter most? 3. Why institutions

Lectures 5-6 Non-market strategy under weak institutions 1 Outline 1. Does weakness of institutions matter for business and economic performance? 2. Which institutions matter most? 3. Why institutions

Are «Good Governance» reforms a priority? Conceptual, measurement, and policy issues

SOAS & Mo Ibrahim Residential School on Governance in Africa Are «Good Governance» reforms a priority? Conceptual, measurement, and policy issues Nicolas Meisel (meiseln@afd.fr) Research Department - French

SOAS & Mo Ibrahim Residential School on Governance in Africa Are «Good Governance» reforms a priority? Conceptual, measurement, and policy issues Nicolas Meisel (meiseln@afd.fr) Research Department - French

The Role of Trade in Structural Transformation

1 The Role of Trade in Structural Transformation Marc Teignier UNIVERSIDAD DE ALICANTE European Summer Symposium in International Macroeconomics 23 May 2012, Tarragona Question Contributions Road Map Motivation

1 The Role of Trade in Structural Transformation Marc Teignier UNIVERSIDAD DE ALICANTE European Summer Symposium in International Macroeconomics 23 May 2012, Tarragona Question Contributions Road Map Motivation

Capital Flows between Rich and Poor Countries

Capital Flows between Rich and Poor Countries Francesco Caselli Summer School 2005 Lucas (1990) Big differences in y. Suppose they are due to differences in k (physical only). Then MPK differences must

Capital Flows between Rich and Poor Countries Francesco Caselli Summer School 2005 Lucas (1990) Big differences in y. Suppose they are due to differences in k (physical only). Then MPK differences must

Growing Together with Growth Polarization and Income Inequality

Growing Together with Growth Polarization and Income Inequality Sudip Ranjan Basu, Ph.D. Economist, United Nations ESCAP UN DESA Expert Group Meeting on the World Economy (LINK Project) United Nations

Growing Together with Growth Polarization and Income Inequality Sudip Ranjan Basu, Ph.D. Economist, United Nations ESCAP UN DESA Expert Group Meeting on the World Economy (LINK Project) United Nations

Human Resources for Health Why we need to act now

Human Resources for Health Why we need to act now Progress towards the MDGs, particularly in Africa is slow, or even stagnating. Poor people cannot access basic services for want of doctors, nurses and

Human Resources for Health Why we need to act now Progress towards the MDGs, particularly in Africa is slow, or even stagnating. Poor people cannot access basic services for want of doctors, nurses and

Specialization Patterns in International Trade

Specialization Patterns in International Trade Walter Steingress November 16, 2015 Abstract The pattern of specialization is key to understanding how trade affects the production structure of an economy.

Specialization Patterns in International Trade Walter Steingress November 16, 2015 Abstract The pattern of specialization is key to understanding how trade affects the production structure of an economy.

The geography of development within countries

The geography of development within countries J. Vernon Henderson Brown University & NBER June 2012 GDN 13TH ANNUAL GLOBAL DEVELOPMENT CONFERENCE Urbanization and Development: Delving Deeper into the Nexus

The geography of development within countries J. Vernon Henderson Brown University & NBER June 2012 GDN 13TH ANNUAL GLOBAL DEVELOPMENT CONFERENCE Urbanization and Development: Delving Deeper into the Nexus

Does Export Concentration Cause Volatility?

Does Export Concentration Cause Volatility? Christian Busch 14. Januar 2010 Overview Countries with undiversified export structure are plausibly more vulnerable to external shocks. But difficult to evaluate

Does Export Concentration Cause Volatility? Christian Busch 14. Januar 2010 Overview Countries with undiversified export structure are plausibly more vulnerable to external shocks. But difficult to evaluate

Diversification versus Polarization: Role of industrial policy in Asia and the Pacific

TOWARDS A RETURN OF INDUSTRIAL POLICY? ARTNeT SYMPOSIUM 25-26 JULY 211 ESCAP, BANGKOK Diversification versus Polarization: Role of industrial policy in Asia and the Pacific Sudip Ranjan Basu* International

TOWARDS A RETURN OF INDUSTRIAL POLICY? ARTNeT SYMPOSIUM 25-26 JULY 211 ESCAP, BANGKOK Diversification versus Polarization: Role of industrial policy in Asia and the Pacific Sudip Ranjan Basu* International

Relative Prices and Sectoral Productivity

Relative Prices and Sectoral Productivity Margarida Duarte University of Toronto Diego Restuccia University of Toronto August 2012 Abstract The relative price of services rises with development. A standard

Relative Prices and Sectoral Productivity Margarida Duarte University of Toronto Diego Restuccia University of Toronto August 2012 Abstract The relative price of services rises with development. A standard

Sovereign Defaults: The Price of Haircuts

Sovereign Defaults: The Price of Haircuts Juan Cruces Univ. Torcuato Di Tella Christoph Trebesch University of Munich and CESIfo Debt Crisis Conference, Reykjavik University, 08.10.2011 1 INTRODUCTION

Sovereign Defaults: The Price of Haircuts Juan Cruces Univ. Torcuato Di Tella Christoph Trebesch University of Munich and CESIfo Debt Crisis Conference, Reykjavik University, 08.10.2011 1 INTRODUCTION

International Investment Patterns. Philip R. Lane WBI Seminar, Paris, April 2006

International Investment Patterns Philip R. Lane WBI Seminar, Paris, April 2006 Introduction What determines aggregate capital inflows and outflows? What determines bilateral patterns in international

International Investment Patterns Philip R. Lane WBI Seminar, Paris, April 2006 Introduction What determines aggregate capital inflows and outflows? What determines bilateral patterns in international

COMPLEXITY AND INDUSTRIAL POLICY

IPD/JICA Task Force on Industrial Policy and Transformation Amman, Jordan, June 5-6, 2014 COMPLEXITY AND INDUSTRIAL POLICY Luciano Pietronero Measuring the Intangible Growth Potential of Countries Collaborators:

IPD/JICA Task Force on Industrial Policy and Transformation Amman, Jordan, June 5-6, 2014 COMPLEXITY AND INDUSTRIAL POLICY Luciano Pietronero Measuring the Intangible Growth Potential of Countries Collaborators:

F L O O R FINANCIAL ASSISTANCE, LAND POLICY, AND GLOBAL SOCIAL RIGHTS

Lutz Leisering, Tobias Böger Measuring Social Citizenship in Developing Countries DFG-Research Project FLOOR-B www.floorgroup.de Principal Investigator: Lutz Leisering F L O O R FINANCIAL ASSISTANCE, LAND

Lutz Leisering, Tobias Böger Measuring Social Citizenship in Developing Countries DFG-Research Project FLOOR-B www.floorgroup.de Principal Investigator: Lutz Leisering F L O O R FINANCIAL ASSISTANCE, LAND

Trends in global income inequality and their political implications

Trends in global income inequality and their political implications LIS Center; Graduate School City University of New York Talk at the Stockholm School of Economics, September 1, 2014 A. National inequalities

Trends in global income inequality and their political implications LIS Center; Graduate School City University of New York Talk at the Stockholm School of Economics, September 1, 2014 A. National inequalities

Services Trade: Recent Policy Trends and Incentives

Services Trade: Recent Policy Trends and Incentives Bernard Hoekman World Bank Based on papers by Borchert and Mattoo (services overall) and Dhar and Srivasta (mode 4) May 27, 2009 Services (should) matter

Services Trade: Recent Policy Trends and Incentives Bernard Hoekman World Bank Based on papers by Borchert and Mattoo (services overall) and Dhar and Srivasta (mode 4) May 27, 2009 Services (should) matter

Political Economy of Development and Underdevelopment

Political Economy of Development and Underdevelopment Daron Acemoglu Department of Economics Massachusetts Institute of Technology October 10, 2005 The State of the World Economy Vast differences in prosperity

Political Economy of Development and Underdevelopment Daron Acemoglu Department of Economics Massachusetts Institute of Technology October 10, 2005 The State of the World Economy Vast differences in prosperity

First Credit Bureau Conference

First Credit Bureau Conference Riga, Latvia 13.1.15 Presentation by: Leora Klapper Lead Economist Development Research Group, World Bank DEVELOPING A NATIONAL CREDIT BUREAU Financial Development What is

First Credit Bureau Conference Riga, Latvia 13.1.15 Presentation by: Leora Klapper Lead Economist Development Research Group, World Bank DEVELOPING A NATIONAL CREDIT BUREAU Financial Development What is

Law and Finance: Would Improved Investor Protection help the ECMU?

Law and Finance: Would Improved Investor Protection help the ECMU? Professor Florencio Lopez de Silanes EDHEC Business School U.S. National Bureau of Economic Research October, 2015 Brussels Why do some

Law and Finance: Would Improved Investor Protection help the ECMU? Professor Florencio Lopez de Silanes EDHEC Business School U.S. National Bureau of Economic Research October, 2015 Brussels Why do some