Chapter 11. Long-Term Liabilities Notes, Bonds, and Leases

|

|

|

- Ilene Newton

- 10 years ago

- Views:

Transcription

1 1

2 Chapter 11 Long-Term Liabilities Notes, Bonds, and Leases 2

3 Long-Term Liabilities 3

4 Economic Consequences of Reporting Long-Term Liabilities Improved credit ratings can lead to lower borrowing costs Management has strong incentive to manage the balance sheet by using off-balance-sheet financing 4

5 Basic Definitions and Different Contractual Forms Some contracts, called interest-bearing obligations, require periodic (annual or semiannual) cash payments (called interest) that are determined as a percentage of the face, principal, or maturity value, which must be paid at the end of the contract period. Non-interest-bearing obligations, on the other hand, require no periodic payments, but only a single cash payment at the end of the contract period. These contractual forms may contain additional terms that specify assets pledged as security or collateral in case the required cash payments are not met (default), as well as additional provisions (restrictive covenants). 5

, as")

6 Figure

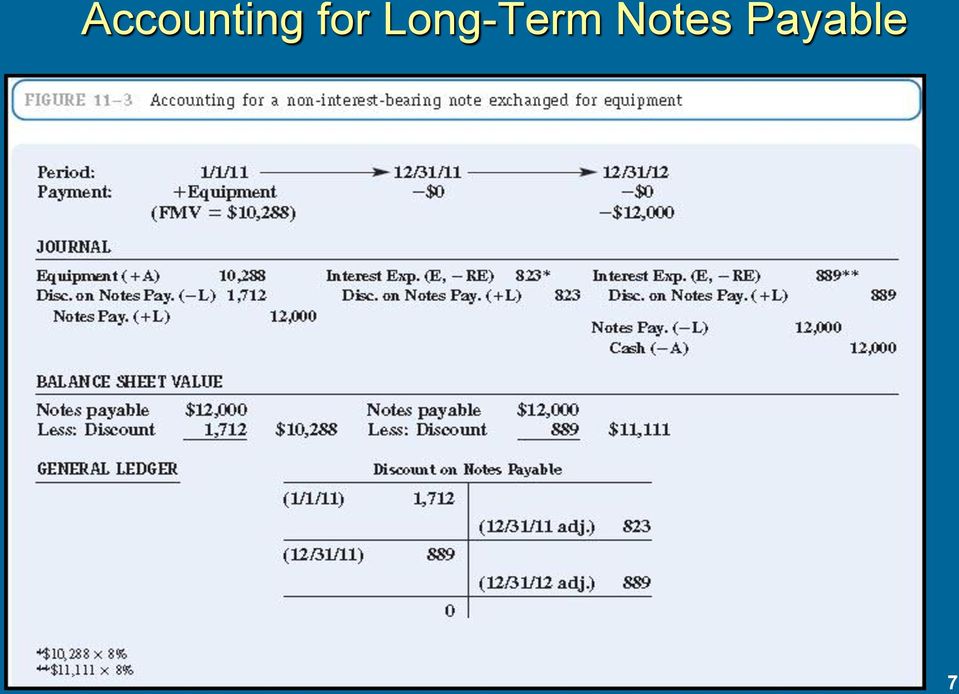

7 Accounting for Long-Term Notes Payable 7

8 Long-Term Liabilities Notes, Bonds, and Leases Long-term liabilities are recorded at the present value of the future cash flows. Two components determine the time value of money: interest (discount) rate number of periods of discounting Types of activities that require PV calculations: notes payable bonds payable and bond investments capital leases 8

9 Present Value of a Single Sum All present value calculations presume a discount rate (i) and a number of periods of discounting (n). There are 3 different ways you can calculate the PV1: 1. Formula: PV1 = FV1 [1/(1+i) n ] 2. Tables: See Page 718, Table 4 3. Financial Calculator (time value of money). 9

n ] 2. Tables: See Page 718, Table 4 3.")

10 Long-term Notes Payable Problem 1: On January 2, 2008, Pearson Company purchases a section of land for its new plant site. Pearson issues a 5 year non-interest bearing note, and promises to pay $50,000 at the end of the 5 year period. What is the cash equivalent price of the land, if a 6 percent discount rate is assumed? PV1 = 50,000 x ( ) = $37,363 [ i=6%, n=5] Journal entry Jan. 2, 2008: Dr. Land 37,363 Dr. Discount on N/P 12,637 Cr. Notes Payable 50,000 10

= $37,363 [ i=6%, n=5] Journal entry Jan. 2, 2008: Dr. Land 37,363 Dr. Discount on N/P 12,637 Cr.")

11 Problem 1 Solution, continued The Effective Interest Method: Interest Expense = Carrying value x Interest rate x Time period (CV) (Per year) (Portion of year) Where carrying value = face - discount. For Example 1, CV= 50,000-12,637 = 37,363 Interest expense = 37,363 x 6% per year x 1year = $2,242 11

12 Problem 1 Solution, continued Journal entry, December 31, 2008: Interest expense 2,242 Discount on N/P 2,242 Carrying value on B/S at 12/31/2008: Notes Payable $50,000 Discount on N/P (10,395) $39,605 (Discount = $12,637-2,242 = $10,395) 12

$39,605 (Discount = $12,637-2,242 =")

13 Problem 1 Solution, continued Interest expense at Dec. 31, 2009: 39,605 x 6% x 1 = $2,376 Journal entry, December 31, 2009: Interest expense 2,376 Discount on N/P 2,376 Carrying value on B/S at 12/31/2009: Notes Payable $50,000 Discount on N/P (8,019) $41,981 (Discount = 10,395-2,376) Carrying value on 12/31/2012 (before retirement)? $50,000 13

$41,981 (Discount = 10,395-2,376) Carrying value on 12/31/2012")

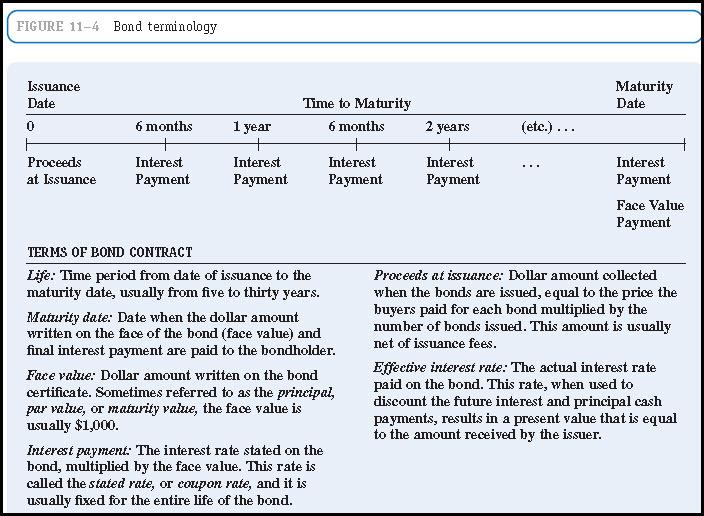

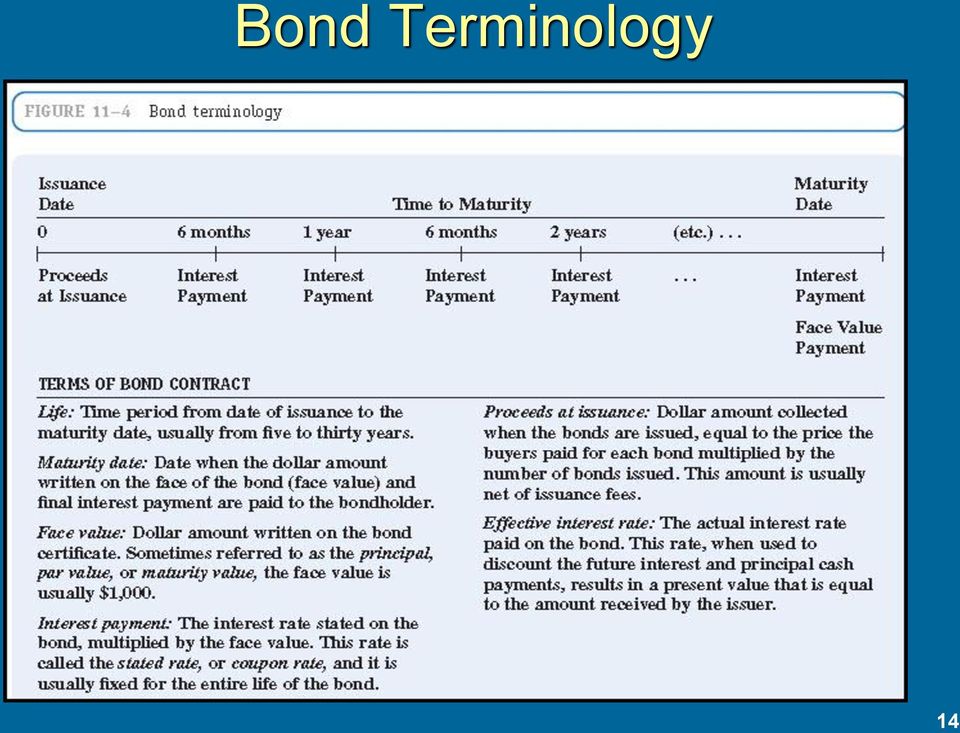

14 Bond Terminology 14

15 Bonds Payable Example 15

16 Bond Prices 16

17 2. Present Value of an Ordinary Annuity(PVOA) PVOA calculations presume a discount rate (i), where (A) = the amount of each annuity, and (n) = the number of annuities (or rents), which is the same as the number of periods of discounting. There are 3 different ways you can calculate PVOA: 1. Formula: PVOA = A [1-(1/(1+i) n )] / i 2. Tables: see page 719, Table 5 3. Financial Calculator (time value of money). 17

n )] / i 2. Tables: see page 719, Table 5 3.")

18 Problem 2: Bonds Payable On July 1, 2007, Mustang Corporation issues $100,000 of its 5-year bonds which have an annual stated rate of 7%, and pay interest semiannually each June 30 and December 31, starting December 31, The bonds were issued to yield 6% annually. Calculate the issue price of the bond: (1) What are the cash flows and factors? Face value at maturity = $100,000 Stated Interest = Face value x stated rate x time period 100,000 x 7% x (1/2) = $3,500 Number of periods = n = 5 years x 2 = 10 Discount rate = 6% / 2 = 3% per period 18

= $3,500 Number of periods")

=$74,409 i=3%, n=10 Total issue price = $104,265 Issued at a premium of $4,265 because the company was offering an interest rate greater than the market rate, and investors were willing")

19 Problem 2 - calculations PV of interest annuity: PVOA Table PVOA = 3,500 ( ) = $29,856 i = 3%, n = 10 PV of face value: PV1 Table PV = 100,000 ( )=$74,409 i=3%, n=10 Total issue price = $104,265 Issued at a premium of $4,265 because the company was offering an interest rate greater than the market rate, and investors were willing to pay more for the higher interest rate. 19

20 Problem 2 - Amortization Schedule To recognize interest expense using the effective interest method, an amortization schedule must be constructed. (This expands the text discussion.) To calculate the columns (see next slide): Cash paid = Face x Stated Rate x Time = 100,000 x 7% x 1/2 year = $3,500 (this is the same amount every period) Int. Expense = CV x Market Rate x Time at 12/31/07 = 104,265 x 6% x 1/2 year = 3,128 at 6/30/08 = 103,893 x 6% x 1/2 year = 3,117 The difference between cash paid and interest expense is the periodic amortization of premium. Note that the carrying value is amortized down to face value by maturity. 20

21 Problem 2 - Amortization Schedule Cash Interest Carrying Date Paid Expense Premium Value 7/01/07 104,265 12/31/07 3,500 3, ,893 6/30/08 3,500 3, ,510 12/31/08 3,500 3, ,115 6/30/09 3,500 3, ,708 12/31/09 3,500 3, ,289 6/30/10 3,500 3, ,858 12/31/10 3,500 3, ,414 6/30/11 3,500 3, ,956 12/31/11 3,500 3, ,485 6/30/12 3,500 3, ,000 21

22 Problem 2 - Journal Entries JE at 7/1/07 to issue the bonds: Cash 104,265 Premium on B/P 4,265 Bonds Payable 100,000 JE at 12/31/07 to pay interest: Interest Expense 3,128 Premium on B/P 372 Cash 3,500 Note that the numbers for each interest payment come from the lines on the amortization schedule. 22

23 Cash Flows for Bonds Payable 23

24 Bonds Issued at Face Value 24

25 Bonds Payable at a Discount If bonds are issued at a discount, the carrying value will be below face value at the date of issue. The Discount on B/P account has a normal debit balance and is a contra to B/P (similar to the Discount on N/P). The Discount account is amortized with a credit. Note that the difference between Cash Paid and Interest Expense is still the amount of amortization. Interest expense for bonds issued at a discount will be greater than cash paid. The amortization table will show the bonds amortized up to face value. 25

26 Bonds Issued at a Discount 26

27 Bond Amortization Table 27

28 Bond Redemptions When bonds are redeemed at the maturity date, the issuing company simply pays cash to the bondholders in the amount of the face value and removes the bond payable from the balance sheet. To illustrate the redemption of a bond issuance prior to maturity at a loss, assume that bonds with a $100,000 face value and a $5,000 unamortized discount are redeemed for $102,000. The $7,000 loss on redemption would decrease net income 28

29 Capital Lease 29

30 Capital Lease Criteria 30

31 Leases FASB issued SFAS No. 13, which requires certain leases to be recorded as capital leases. Capital leases record the leased asset as a capital asset, and reflect the present value of the related payment contract as a liability. Requirements of SFAS No record as capital lease for the lessee if any one of the following is present in the lease: Title transfers at the end of the lease period, The lease contains a bargain purchase option, The lease life is at least 75% of the useful life of the asset, or The lessee pays for at least 90% of the fair market value of the lease. 31

32 International Perspective The accounting disclosure requirements in non-u.s. countries and IFRS are not as comprehensive as those in the United States, partially because the information needs of the major capital providers (i.e., banks) are satisfied in a relatively straightforward way through personal contact and direct visits. A second way in which the heavy reliance on debt affects non-u.s. accounting systems is that the required disclosures and regulations tend to be designed either to protect the creditor or to help in the assessment of solvency. 32

33 Appendix 11A Determine the Effective (Actual) Rate of Return Determine the Required Rate of Return Determine the Risk-Free Return Determine the Risk Premium Compare the Effective Rate to the Required Rate 33

34 Appendix 11B 34

35 Appendix 11C Interest Rate Swaps A common method used by companies to reduce such risks is called hedging, where a company enters into a contract that creates risks that counteract or balance the risks attempted to be hedged (reduced). The most common method of hedging market interest rate risk is called an interest rate swap. 35

36 Copyright Copyright 2011 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein. 36

Appendix C- 1. Time Value of Money. Appendix C- 2. Financial Accounting, Fifth Edition

C- 1 Time Value of Money C- 2 Financial Accounting, Fifth Edition Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount. 3. Solve for future

C- 1 Time Value of Money C- 2 Financial Accounting, Fifth Edition Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount. 3. Solve for future

Appendix. Time Value of Money. Financial Accounting, IFRS Edition Weygandt Kimmel Kieso. Appendix C- 1

C Time Value of Money C- 1 Financial Accounting, IFRS Edition Weygandt Kimmel Kieso C- 2 Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount.

C Time Value of Money C- 1 Financial Accounting, IFRS Edition Weygandt Kimmel Kieso C- 2 Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount.

PREVIEW OF CHAPTER 6-2

6-1 PREVIEW OF CHAPTER 6 6-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 6 Accounting and the Time Value of Money LEARNING OBJECTIVES After studying this chapter, you should

6-1 PREVIEW OF CHAPTER 6 6-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 6 Accounting and the Time Value of Money LEARNING OBJECTIVES After studying this chapter, you should

Bonds. Accounting for Long-Term Debt. Agenda Long-Term Debt. 15.501/516 Accounting Spring 2004

Accounting for Long-Term Debt 15.501/516 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology April 5, 2004 1 Agenda Long-Term Debt Extend our

Accounting for Long-Term Debt 15.501/516 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology April 5, 2004 1 Agenda Long-Term Debt Extend our

CHAPTER 14. Long-Term Liabilities 1, 10, 14, 20 2, 3, 4, 9, 10, 11 1, 2, 3, 4, 5, 6, 7 5, 6, 7, 8, 11 3, 4, 6, 7, 8, 10 12, 13 11 12, 13, 14, 15

CHAPTER 14 Long-Term Liabilities ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Long-term liability; classification; definitions.

CHAPTER 14 Long-Term Liabilities ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Long-term liability; classification; definitions.

In October 1997, Hewlett-Packard issued zero coupon bonds with a face value of $1.8 million, due in 2017, for proceeds of $968 million.

BE11-2 In October 1997, Hewlett-Packard issued zero coupon bonds with a face value of $1.8 million, due in 2017, for proceeds of $968 million. (a) What is the life of these bonds? The life of the bonds

BE11-2 In October 1997, Hewlett-Packard issued zero coupon bonds with a face value of $1.8 million, due in 2017, for proceeds of $968 million. (a) What is the life of these bonds? The life of the bonds

Time Value of Money Concepts

BASIC ANNUITIES There are many accounting transactions that require the payment of a specific amount each period. A payment for a auto loan or a mortgage payment are examples of this type of transaction.

BASIC ANNUITIES There are many accounting transactions that require the payment of a specific amount each period. A payment for a auto loan or a mortgage payment are examples of this type of transaction.

PREVIEW OF CHAPTER 21-1. Intermediate Accounting 15th Edition Kieso Weygandt Warfield

PREVIEW OF CHAPTER 21 21-1 Intermediate Accounting 15th Edition Kieso Weygandt Warfield 21 Accounting for Leases LEARNING OBJECTIVES After studying this chapter, you should be able to: 21-2 1. Explain

PREVIEW OF CHAPTER 21 21-1 Intermediate Accounting 15th Edition Kieso Weygandt Warfield 21 Accounting for Leases LEARNING OBJECTIVES After studying this chapter, you should be able to: 21-2 1. Explain

Long-Term Debt. Objectives: simple present value calculations. Understand the terminology of long-term debt Par value Discount vs.

Objectives: Long-Term Debt! Extend our understanding of valuation methods beyond simple present value calculations. Understand the terminology of long-term debt Par value Discount vs. Premium Mortgages!

Objectives: Long-Term Debt! Extend our understanding of valuation methods beyond simple present value calculations. Understand the terminology of long-term debt Par value Discount vs. Premium Mortgages!

Accounting for Bonds and Long-Term Notes

Accounting for Bonds and Long-Term Notes Bond Premiums and Discounts Effective interest method Bond issuance Interest expense Types of Debt Instruments Zero-Coupon Bonds Convertible Bonds Detachable Warrants

Accounting for Bonds and Long-Term Notes Bond Premiums and Discounts Effective interest method Bond issuance Interest expense Types of Debt Instruments Zero-Coupon Bonds Convertible Bonds Detachable Warrants

Chapter 21 The Statement of Cash Flows Revisited

Chapter 21 The Statement of Cash Flows Revisited AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments,

Chapter 21 The Statement of Cash Flows Revisited AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments,

Unit 6 Receivables. Receivables - Claims resulting from credit sales to customers and others goods or services for money,.

Unit 6 Receivables 7-1 Receivables - Claims resulting from credit sales to customers and others goods or services for money,. Oral promises of the purchaser to pay for goods and services sold (credit sale;

Unit 6 Receivables 7-1 Receivables - Claims resulting from credit sales to customers and others goods or services for money,. Oral promises of the purchaser to pay for goods and services sold (credit sale;

TVM Applications Chapter

Chapter 6 Time of Money UPS, Walgreens, Costco, American Air, Dreamworks Intel (note 10 page 28) TVM Applications Accounting issue Chapter Notes receivable (long-term receivables) 7 Long-term assets 10

Chapter 6 Time of Money UPS, Walgreens, Costco, American Air, Dreamworks Intel (note 10 page 28) TVM Applications Accounting issue Chapter Notes receivable (long-term receivables) 7 Long-term assets 10

CHAPTER 6. Accounting and the Time Value of Money. 2. Use of tables. 13, 14 8 1. a. Unknown future amount. 7, 19 1, 5, 13 2, 3, 4, 7

CHAPTER 6 Accounting and the Time Value of Money ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems 1. Present value concepts. 1, 2, 3, 4, 5, 9, 17 2. Use of

CHAPTER 6 Accounting and the Time Value of Money ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems 1. Present value concepts. 1, 2, 3, 4, 5, 9, 17 2. Use of

Module 8: Current and long-term liabilities

Module 8: Current and long-term liabilities Module 8: Current and long-term liabilities Overview In previous modules, you learned how to account for assets. Assets are what a business uses or sells to

Module 8: Current and long-term liabilities Module 8: Current and long-term liabilities Overview In previous modules, you learned how to account for assets. Assets are what a business uses or sells to

Intercompany Indebtedness. Chapter 8. Intercompany Indebtedness. Consolidation Overview. Consolidation Overview. Intercompany Indebtedness

Chapter 8 Intercompany Indebtedness Intercompany Indebtedness One advantage of having control over other companies is that management has the ability to transfer resources from one legal entity to another

Chapter 8 Intercompany Indebtedness Intercompany Indebtedness One advantage of having control over other companies is that management has the ability to transfer resources from one legal entity to another

ANALYSIS OF FIXED INCOME SECURITIES

ANALYSIS OF FIXED INCOME SECURITIES Valuation of Fixed Income Securities Page 1 VALUATION Valuation is the process of determining the fair value of a financial asset. The fair value of an asset is its

ANALYSIS OF FIXED INCOME SECURITIES Valuation of Fixed Income Securities Page 1 VALUATION Valuation is the process of determining the fair value of a financial asset. The fair value of an asset is its

CHAPTER 6. Accounting and the Time Value of Money. 2. Use of tables. 13, 14 8 1. a. Unknown future amount. 7, 19 1, 5, 13 2, 3, 4, 6

CHAPTER 6 Accounting and the Time Value of Money ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems 1. Present value concepts. 1, 2, 3, 4, 5, 9, 17, 19 2. Use

CHAPTER 6 Accounting and the Time Value of Money ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems 1. Present value concepts. 1, 2, 3, 4, 5, 9, 17, 19 2. Use

Leases. Objectives. Understand the rationale for leasing and the distinction between Operating and capital leases.

Leases Objectives Understand the rationale for leasing and the distinction between Operating and capital leases. Understand the Income Statement and Balance Sheet differences Between operating and capital

Leases Objectives Understand the rationale for leasing and the distinction between Operating and capital leases. Understand the Income Statement and Balance Sheet differences Between operating and capital

TIME VALUE OF MONEY (TVM)

") TIME VALUE OF MONEY (TVM) INTEREST Rate of Return When we know the Present Value (amount today), Future Value (amount to which the investment will grow), and Number of Periods, we can calculate the rate

TIME VALUE OF MONEY (TVM) INTEREST Rate of Return When we know the Present Value (amount today), Future Value (amount to which the investment will grow), and Number of Periods, we can calculate the rate

Chapter 6. Time Value of Money Concepts. Simple Interest 6-1. Interest amount = P i n. Assume you invest $1,000 at 6% simple interest for 3 years.

6-1 Chapter 6 Time Value of Money Concepts 6-2 Time Value of Money Interest is the rent paid for the use of money over time. That s right! A dollar today is more valuable than a dollar to be received in

6-1 Chapter 6 Time Value of Money Concepts 6-2 Time Value of Money Interest is the rent paid for the use of money over time. That s right! A dollar today is more valuable than a dollar to be received in

Short term leases, defined as a lease term of one year or less, are to be accounted for under the same operating lease method that currently exists.

Lease Accounting Updated January 2014 Page 1 Lease Accounting The pending changes in lease accounting have been a hot topic item since 2009, when the Financial Accounting Standards Board (FASB) and International

Lease Accounting Updated January 2014 Page 1 Lease Accounting The pending changes in lease accounting have been a hot topic item since 2009, when the Financial Accounting Standards Board (FASB) and International

Time Value of Money. 15.511 Corporate Accounting Summer 2004. Professor S. P. Kothari Sloan School of Management Massachusetts Institute of Technology

Time Value of Money 15.511 Corporate Accounting Summer 2004 Professor S. P. Kothari Sloan School of Management Massachusetts Institute of Technology July 2, 2004 1 LIABILITIES: Current Liabilities Obligations

Time Value of Money 15.511 Corporate Accounting Summer 2004 Professor S. P. Kothari Sloan School of Management Massachusetts Institute of Technology July 2, 2004 1 LIABILITIES: Current Liabilities Obligations

FinQuiz Notes 2 0 1 4

Reading 5 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Reading 5 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Accounting for and Presentation of Liabilities

7 Accounting for and Presentation of Liabilities Liabilities are obligations of the entity or, as defined by the FASB, probable future sacrifices of economic benefits arising from present obligations of

7 Accounting for and Presentation of Liabilities Liabilities are obligations of the entity or, as defined by the FASB, probable future sacrifices of economic benefits arising from present obligations of

Chapter 16. Debentures: An Introduction. Non-current Liabilities. Horngren, Best, Fraser, Willett: Accounting 6e 2010 Pearson Australia.

PowerPoint to accompany Non-current Liabilities Chapter 16 Learning Objectives 1. Account for debentures payable transactions 2. Measure interest expense by the straight line interest method 3. Account

PowerPoint to accompany Non-current Liabilities Chapter 16 Learning Objectives 1. Account for debentures payable transactions 2. Measure interest expense by the straight line interest method 3. Account

CHAPTER 7 Cash and Receivables

CHAPTER 7 Cash and Receivables 7-1 LECTURE OUTLINE Chapter 7, the first of six asset chapters, covers cash, accounts receivable, and notes receivable. Temporary investments (marketable securities) are

CHAPTER 7 Cash and Receivables 7-1 LECTURE OUTLINE Chapter 7, the first of six asset chapters, covers cash, accounts receivable, and notes receivable. Temporary investments (marketable securities) are

Module 8: Current and long-term liabilities

Page 1 of 35 Module 8: Current and long-term liabilities Overview In previous modules, you learned how to account for assets. Assets are what a business uses or sells to earn revenues. Recall that the

Page 1 of 35 Module 8: Current and long-term liabilities Overview In previous modules, you learned how to account for assets. Assets are what a business uses or sells to earn revenues. Recall that the

Assuming office supplies are charged to the Office Supplies inventory account when purchased:

Adjusting Entries Prepaid Expenses Second Bullet Example - Assuming office supplies are charged to the Office Supplies inventory account when purchased: Office supplies expense 7,800 Office supplies 7,800

Adjusting Entries Prepaid Expenses Second Bullet Example - Assuming office supplies are charged to the Office Supplies inventory account when purchased: Office supplies expense 7,800 Office supplies 7,800

Chapter 8: account receivable

Chapter 8: account receivable Three accounting issues associated with accounts receivable are: 1. Recognizing accounts receivable 2. Valuing accounts receivable 3. Disposing of accounts receivable Recognizing

Chapter 8: account receivable Three accounting issues associated with accounts receivable are: 1. Recognizing accounts receivable 2. Valuing accounts receivable 3. Disposing of accounts receivable Recognizing

Walk Through Balance Sheet. Chapter 7. Learning Objectives. Learning Objectives 1, 2. Learning Objectives 1, 2. Cash and Receivables.

Chapter 7 Walk Through Balance Sheet Cash and Receivables Chapters 1 6 Accounting cycle: JE, AJE, financial stmts Conceptual framework, GAAP, revenue Time value of money concepts Remaining chapters (ACTG

Chapter 7 Walk Through Balance Sheet Cash and Receivables Chapters 1 6 Accounting cycle: JE, AJE, financial stmts Conceptual framework, GAAP, revenue Time value of money concepts Remaining chapters (ACTG

Cash and Receivables. Chapter. Learning Objectives. Nature and Composition of Cash. Additional Cash Issues

Learning Objectives Cash and Receivables No substantial departures from the text, Chapter 7. Chapter 7 7-1 UCSB, Anderson 7-2 UCSB, Anderson Nature and Composition of Cash Cash is classified as a... Current

Learning Objectives Cash and Receivables No substantial departures from the text, Chapter 7. Chapter 7 7-1 UCSB, Anderson 7-2 UCSB, Anderson Nature and Composition of Cash Cash is classified as a... Current

FinQuiz Notes 2 0 1 5

Reading 5 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Reading 5 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

EFFECTIVE-INTEREST METHOD

Chapter 14 Non-Current Liabilities 14 1 CHAPTER 14 NON-CURRENT LIABILITIES This IFRS Supplement provides expanded discussions of accounting guidance under International Financial Reporting Standards (IFRS)

Chapter 14 Non-Current Liabilities 14 1 CHAPTER 14 NON-CURRENT LIABILITIES This IFRS Supplement provides expanded discussions of accounting guidance under International Financial Reporting Standards (IFRS)

Sample Examination Questions CHAPTER 6 ACCOUNTING AND THE TIME VALUE OF MONEY MULTIPLE CHOICE Conceptual Answer No. Description d 1. Definition of present value. c 2. Understanding compound interest tables.

Sample Examination Questions CHAPTER 6 ACCOUNTING AND THE TIME VALUE OF MONEY MULTIPLE CHOICE Conceptual Answer No. Description d 1. Definition of present value. c 2. Understanding compound interest tables.

ASPE AT A GLANCE Section 3856 Financial Instruments

ASPE AT A GLANCE Section 3856 Financial Instruments December 2014 Section 3856 Financial Instruments Effective Date Fiscal years beginning on or after January 1, 2011 1 SCOPE Applies to all financial instruments

ASPE AT A GLANCE Section 3856 Financial Instruments December 2014 Section 3856 Financial Instruments Effective Date Fiscal years beginning on or after January 1, 2011 1 SCOPE Applies to all financial instruments

ACCOUNT DEBIT CREDIT Accounts receivable 10,000 Sales 10,000 To record the sale of merchandise to Sophie Company

CURRENT RECEIVABLES Receivables are the amount owed to the organization by its customers and/or others. Current receivables will be collected within one year or the current operating cycle which ever is

CURRENT RECEIVABLES Receivables are the amount owed to the organization by its customers and/or others. Current receivables will be collected within one year or the current operating cycle which ever is

2 The Mathematics. of Finance. Copyright Cengage Learning. All rights reserved.

2 The Mathematics of Finance Copyright Cengage Learning. All rights reserved. 2.3 Annuities, Loans, and Bonds Copyright Cengage Learning. All rights reserved. Annuities, Loans, and Bonds A typical defined-contribution

2 The Mathematics of Finance Copyright Cengage Learning. All rights reserved. 2.3 Annuities, Loans, and Bonds Copyright Cengage Learning. All rights reserved. Annuities, Loans, and Bonds A typical defined-contribution

The Concept of Present Value

The Concept of Present Value If you could have $100 today or $100 next week which would you choose? Of course you would choose the $100 today. Why? Hopefully you said because you could invest it and make

The Concept of Present Value If you could have $100 today or $100 next week which would you choose? Of course you would choose the $100 today. Why? Hopefully you said because you could invest it and make

Exam 3 Review. FV = PV (1 + i) n. Format. What to Bring/Remember. Time Value of Money. Solving for Other Variables Example. Solving for Other Values

n. Format. What to Bring/Remember. Time Value of Money. Solving for Other Variables Example. Solving for Other Values") Format Exam 3 Review http://fates.cns.muskingum.edu/~ plaube/acct301/default.htm 15 questions Multiple choice (12) Essay (2) Problem (1) What to Bring/Remember What to bring Calculator I ll bring scrap

Format Exam 3 Review http://fates.cns.muskingum.edu/~ plaube/acct301/default.htm 15 questions Multiple choice (12) Essay (2) Problem (1) What to Bring/Remember What to bring Calculator I ll bring scrap

Bonds. Describe Bonds. Define Key Words. Created 2007 By Michael Worthington Elizabeth City State University

Bonds OBJECTIVES Describe bonds Define key words Explain why bond prices fluctuate Compute interest payments Calculate the price of bonds Created 2007 By Michael Worthington Elizabeth City State University

Bonds OBJECTIVES Describe bonds Define key words Explain why bond prices fluctuate Compute interest payments Calculate the price of bonds Created 2007 By Michael Worthington Elizabeth City State University

Present Value Concepts

Present Value Concepts Present value concepts are widely used by accountants in the preparation of financial statements. In fact, under International Financial Reporting Standards (IFRS), these concepts

Present Value Concepts Present value concepts are widely used by accountants in the preparation of financial statements. In fact, under International Financial Reporting Standards (IFRS), these concepts

CHAPTER 5. Examining the Balance Sheet and Statement of Cash Flows 2 4, 5 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11 12, 13, 14, 15, 16

CHAPTER 5 Examining the Balance Sheet and Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Disclosure principles,

CHAPTER 5 Examining the Balance Sheet and Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Disclosure principles,

Income Statements. Accounting for Merchandising Operations

Accounting Principles, 7 th Edition Weygandt Kieso Kimmel Income Statements Accounting for Merchandising Operations Prepared by Naomi Karolinski Monroe Community College and Marianne Bradford Bryant College

Accounting Principles, 7 th Edition Weygandt Kieso Kimmel Income Statements Accounting for Merchandising Operations Prepared by Naomi Karolinski Monroe Community College and Marianne Bradford Bryant College

Chapter The Time Value of Money

Chapter The Time Value of Money PPT 9-2 Chapter 9 - Outline Time Value of Money Future Value and Present Value Annuities Time-Value-of-Money Formulas Adjusting for Non-Annual Compounding Compound Interest

Chapter The Time Value of Money PPT 9-2 Chapter 9 - Outline Time Value of Money Future Value and Present Value Annuities Time-Value-of-Money Formulas Adjusting for Non-Annual Compounding Compound Interest

International Accounting Standard 7 Statement of cash flows *

International Accounting Standard 7 Statement of cash flows * Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

International Accounting Standard 7 Statement of cash flows * Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

Present Value (PV) Tutorial

Tutorial") EYK 15-1 Present Value (PV) Tutorial The concepts of present value are described and applied in Chapter 15. This supplement provides added explanations, illustrations, calculations, present value tables,

EYK 15-1 Present Value (PV) Tutorial The concepts of present value are described and applied in Chapter 15. This supplement provides added explanations, illustrations, calculations, present value tables,

CHAPTER 23. Statement of Cash Flows 1, 2, 7, 8, 12 3, 4, 5, 6, 16, 17, 19 9, 20 4, 5, 9, 10, 11 10, 13, 15, 16. 7. Worksheet adjustments.

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

CHAPTER 6 Accounting and the Time Value of Money

CHAPTER 6 Accounting and the Time Value of Money 6-1 LECTURE OUTLINE This chapter can be covered in two to three class sessions. Most students have had previous exposure to single sum problems and ordinary

CHAPTER 6 Accounting and the Time Value of Money 6-1 LECTURE OUTLINE This chapter can be covered in two to three class sessions. Most students have had previous exposure to single sum problems and ordinary

GUIDE TO ACCOUNTING STANDARDS FOR PRIVATE ENTERPRISES CHAPTER 45 FINANCIAL INSTRUMENTS

GUIDE TO ACCOUNTING STANDARDS FOR PRIVATE ENTERPRISES CHAPTER 45 FINANCIAL INSTRUMENTS DISCLAIMER This publication was prepared by the Chartered Professional Accountants of Canada (CPA Canada). It has

GUIDE TO ACCOUNTING STANDARDS FOR PRIVATE ENTERPRISES CHAPTER 45 FINANCIAL INSTRUMENTS DISCLAIMER This publication was prepared by the Chartered Professional Accountants of Canada (CPA Canada). It has

Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows

7 Statement of Cash Flows") Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

LEASES: ASPE 3065. PMR NOTES HTK Consulting

LEASES: ASPE 3065 Scope The following items are not covered under this section: licensing agreements for items such as motion pictures, videotapes, plays, manuscripts, patents and copyrights Definitions

LEASES: ASPE 3065 Scope The following items are not covered under this section: licensing agreements for items such as motion pictures, videotapes, plays, manuscripts, patents and copyrights Definitions

6. Depreciation is a process of a. asset devaluation. b. cost accumulation. c. cost allocation. d. asset valuation.

1. A company purchased land for $72,000 cash. Real estate brokers' commission was $5,000 and $7,000 was spent for demolishing an old building on the land before construction of a new building could start.

1. A company purchased land for $72,000 cash. Real estate brokers' commission was $5,000 and $7,000 was spent for demolishing an old building on the land before construction of a new building could start.

NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS

NAS 03 NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-3 BENEFITS OF CASH FLOWS INFORMATION 4-5 DEFINITIONS 6-9 Cash and cash equivalents 7-9 PRESENTATION OF A

NAS 03 NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-3 BENEFITS OF CASH FLOWS INFORMATION 4-5 DEFINITIONS 6-9 Cash and cash equivalents 7-9 PRESENTATION OF A

1 CONSOLIDATED FINANCIAL STATEMENTS (1) Consolidated Balance Sheets

Consolidated Balance Sheets") 1 CONSOLIDATED FINANCIAL STATEMENTS (1) Consolidated Balance Sheets As of March 31,2014 As of March 31,2015 Assets Cash and due from banks 478,425 339,266 Call loans and bills bought 23,088 58,740 Monetary

1 CONSOLIDATED FINANCIAL STATEMENTS (1) Consolidated Balance Sheets As of March 31,2014 As of March 31,2015 Assets Cash and due from banks 478,425 339,266 Call loans and bills bought 23,088 58,740 Monetary

Summary of Significant Differences between Japanese GAAP and U.S. GAAP

Summary of Significant Differences between Japanese GAAP and U.S. GAAP The consolidated financial statements of SMFG and its subsidiaries presented in this annual report conform with generally accepted

Summary of Significant Differences between Japanese GAAP and U.S. GAAP The consolidated financial statements of SMFG and its subsidiaries presented in this annual report conform with generally accepted

07:35 CURRENT LIABILITIES & CONTINGENCIES ECON 136A REFRESHER. 136A Concepts. Notes Payable. Chapter 13

CURRENT LIABILITIES & CONTINGENCIES Chapter 13 ECON 136A REFRESHER What is a liability? Present (not necessarily current) unavoidable obligation; Result of a past transaction; What makes a liability current?

CURRENT LIABILITIES & CONTINGENCIES Chapter 13 ECON 136A REFRESHER What is a liability? Present (not necessarily current) unavoidable obligation; Result of a past transaction; What makes a liability current?

Interest Expense Principal

ACCOUNTING BY THE LESSOR AND LESSEE A lease is a contract between a lessor (the owner of the property) and a lessee (the user of the property). Normally the lessee makes periodic payments in exchange for

ACCOUNTING BY THE LESSOR AND LESSEE A lease is a contract between a lessor (the owner of the property) and a lessee (the user of the property). Normally the lessee makes periodic payments in exchange for

IPSAS 2 CASH FLOW STATEMENTS

IPSAS 2 CASH FLOW STATEMENTS Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 7, Cash Flow Statements published

IPSAS 2 CASH FLOW STATEMENTS Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 7, Cash Flow Statements published

Chapter 8 Accounting for Receivables

Chapter 8 Accounting for Receivables Accounts Receivable Accounts Receivables are current assets. They are usually expected to be collected within 30 days. Allowance Method and Bad Debt Expense 2 methods:

Chapter 8 Accounting for Receivables Accounts Receivable Accounts Receivables are current assets. They are usually expected to be collected within 30 days. Allowance Method and Bad Debt Expense 2 methods:

PART III. Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Independent Auditors Report 47

PART III Item 17. Financial Statements Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Schedule: Page Number Independent Auditors Report 47 Consolidated Balance Sheets as of March

PART III Item 17. Financial Statements Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Schedule: Page Number Independent Auditors Report 47 Consolidated Balance Sheets as of March

Sri Lanka Accounting Standard-LKAS 7. Statement of Cash Flows

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

Case Western Reserve University Consolidated Financial Statements for the Year Ending June 30, 2001

Contents Report of Independent Accountants 1 Part 1 Consolidated Financial Statements Consolidated Balance Sheet 2 Consolidated Statement of Activities 3 Consolidated Statement of Cash Flows 4 Part 2 Summary

Contents Report of Independent Accountants 1 Part 1 Consolidated Financial Statements Consolidated Balance Sheet 2 Consolidated Statement of Activities 3 Consolidated Statement of Cash Flows 4 Part 2 Summary

Module 1: Corporate Finance and the Role of Venture Capital Financing TABLE OF CONTENTS

1.0 ALTERNATIVE SOURCES OF FINANCE Module 1: Corporate Finance and the Role of Venture Capital Financing Alternative Sources of Finance TABLE OF CONTENTS 1.1 Short-Term Debt (Short-Term Loans, Line of

1.0 ALTERNATIVE SOURCES OF FINANCE Module 1: Corporate Finance and the Role of Venture Capital Financing Alternative Sources of Finance TABLE OF CONTENTS 1.1 Short-Term Debt (Short-Term Loans, Line of

Cash Flow Statements

Compiled Accounting Standard AASB 107 Cash Flow Statements This compiled Standard applies to annual reporting periods beginning on or after 1 July 2007. Early application is permitted. It incorporates

Compiled Accounting Standard AASB 107 Cash Flow Statements This compiled Standard applies to annual reporting periods beginning on or after 1 July 2007. Early application is permitted. It incorporates

Off-Balance Sheet Financing: Operating Leases & Other Topics

Off-Balance Sheet Financing: Operating Leases & Other Topics Session 7 FIN 551 - Financial Statement Analysis 1 Let s Discuss Leases FIN 551 - Financial Statement Analysis 2 1 Off-Balance-Sheet Obligation

Off-Balance Sheet Financing: Operating Leases & Other Topics Session 7 FIN 551 - Financial Statement Analysis 1 Let s Discuss Leases FIN 551 - Financial Statement Analysis 2 1 Off-Balance-Sheet Obligation

Statement of Cash Flows

HKAS 7 Revised February November 2014 Hong Kong Accounting Standard 7 Statement of Cash Flows HKAS 7 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

HKAS 7 Revised February November 2014 Hong Kong Accounting Standard 7 Statement of Cash Flows HKAS 7 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

T-Account Approach to Preparing a Statement of Cash Flows Indirect Method

266 Part 1 E M Foundations of Financial Accounting With these adjustments to the income statement, we can now present the operating activities section of the statement of cash flows using either the direct

266 Part 1 E M Foundations of Financial Accounting With these adjustments to the income statement, we can now present the operating activities section of the statement of cash flows using either the direct

Basic financial arithmetic

2 Basic financial arithmetic Simple interest Compound interest Nominal and effective rates Continuous discounting Conversions and comparisons Exercise Summary File: MFME2_02.xls 13 This chapter deals

2 Basic financial arithmetic Simple interest Compound interest Nominal and effective rates Continuous discounting Conversions and comparisons Exercise Summary File: MFME2_02.xls 13 This chapter deals

Statement of Cash Flows

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 7 Statement of Cash Flows This version of SB-FRS 7 does not include amendments that are effective for annual periods beginning after 1 January 2014.

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 7 Statement of Cash Flows This version of SB-FRS 7 does not include amendments that are effective for annual periods beginning after 1 January 2014.

Consolidated Balance Sheets March 31, 2001 and 2000

Financial Statements SEIKAGAKU CORPORATION AND CONSOLIDATED SUBSIDIARIES Consolidated Balance Sheets March 31, 2001 and 2000 Assets Current assets: Cash and cash equivalents... Short-term investments (Note

Financial Statements SEIKAGAKU CORPORATION AND CONSOLIDATED SUBSIDIARIES Consolidated Balance Sheets March 31, 2001 and 2000 Assets Current assets: Cash and cash equivalents... Short-term investments (Note

Accounting Building Business Skills. Interest. Interest. Paul D. Kimmel. Appendix B: Time Value of Money

Accounting Building Business Skills Paul D. Kimmel Appendix B: Time Value of Money PowerPoint presentation by Kate Wynn-Williams University of Otago, Dunedin 2003 John Wiley & Sons Australia, Ltd 1 Interest

Accounting Building Business Skills Paul D. Kimmel Appendix B: Time Value of Money PowerPoint presentation by Kate Wynn-Williams University of Otago, Dunedin 2003 John Wiley & Sons Australia, Ltd 1 Interest

Foundation review. Introduction. Learning objectives

Foundation review: Introduction Foundation review Introduction Throughout FN1, you will be expected to apply techniques and concepts that you learned in prerequisite courses. The purpose of this foundation

Foundation review: Introduction Foundation review Introduction Throughout FN1, you will be expected to apply techniques and concepts that you learned in prerequisite courses. The purpose of this foundation

Chapter 14. 1 Copyright 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Chapter 14 1 Identify the purposes of the statement of cash flows Distinguish among operating, investing, and financing cash flows Prepare the statement of cash flows by the indirect method Identify noncash

Chapter 14 1 Identify the purposes of the statement of cash flows Distinguish among operating, investing, and financing cash flows Prepare the statement of cash flows by the indirect method Identify noncash

5-1. Prepared by Coby Harmon University of California, Santa Barbara Westmont College

5-1 Prepared by Coby Harmon University of California, Santa Barbara Westmont College 5 Accounting for Merchandising Operations Learning Objectives After studying this chapter, you should be able to: [1]

5-1 Prepared by Coby Harmon University of California, Santa Barbara Westmont College 5 Accounting for Merchandising Operations Learning Objectives After studying this chapter, you should be able to: [1]

Accounting for Merchandising Operations

Prepared by Coby Harmon University of California, Santa Barbara Westmont College 5-1 5 Accounting for Merchandising Operations Learning Objectives After studying this chapter, you should be able to: [1]

Prepared by Coby Harmon University of California, Santa Barbara Westmont College 5-1 5 Accounting for Merchandising Operations Learning Objectives After studying this chapter, you should be able to: [1]

What Is Other Equity? Marketable Securities. Marketable Securities, Time Value of Money. 15.501/516 Accounting Spring 2004

Marketable Securities, Time Value of Money 15.501/516 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology March 31, 2004 1 Marketable Securities

Marketable Securities, Time Value of Money 15.501/516 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology March 31, 2004 1 Marketable Securities

15.511 Corporate Accounting Recitation 6. July 7, 2004

15.511 Corporate Accounting Recitation 6 July 7, 2004 1 Agenda Marketable Securities (lecture notes) Bonds Leases Deferred tax 2 Accounting for Bonds -Terminology Par value Proceeds from issuance Coupon

15.511 Corporate Accounting Recitation 6 July 7, 2004 1 Agenda Marketable Securities (lecture notes) Bonds Leases Deferred tax 2 Accounting for Bonds -Terminology Par value Proceeds from issuance Coupon

DRAFT. Quarterly Savings and Loan Holding Company Report FR 2320. General Instructions Who Must Report. When to Submit the Report

JOBNAME: No Job Name PAGE: 1 SESS: 378 OUTPUT: Mon Nov 21 10:08:25 2011 /frb/bsr/instructs/fr2320/4_dec11_2320-gen_v3 INSTRUCTIONS FOR PREPARATION OF Quarterly Savings and Loan Holding Company Report General

JOBNAME: No Job Name PAGE: 1 SESS: 378 OUTPUT: Mon Nov 21 10:08:25 2011 /frb/bsr/instructs/fr2320/4_dec11_2320-gen_v3 INSTRUCTIONS FOR PREPARATION OF Quarterly Savings and Loan Holding Company Report General

FINANCIAL STATEMENT 2010

FINANCIAL STATEMENT 2010 CONTENTS Independent Auditors Report------------------------------ 2 Consolidated Balance Sheets ------------------------------ 3 Consolidated Statements of Operations ----------------

FINANCIAL STATEMENT 2010 CONTENTS Independent Auditors Report------------------------------ 2 Consolidated Balance Sheets ------------------------------ 3 Consolidated Statements of Operations ----------------

You just paid $350,000 for a policy that will pay you and your heirs $12,000 a year forever. What rate of return are you earning on this policy?

1 You estimate that you will have $24,500 in student loans by the time you graduate. The interest rate is 6.5%. If you want to have this debt paid in full within five years, how much must you pay each

1 You estimate that you will have $24,500 in student loans by the time you graduate. The interest rate is 6.5%. If you want to have this debt paid in full within five years, how much must you pay each

Assurance and accounting A Guide to Financial Instruments for Private

june 2011 www.bdo.ca Assurance and accounting A Guide to Financial Instruments for Private Enterprises and Private Sector t-for-profit Organizations For many entities adopting the Accounting Standards

june 2011 www.bdo.ca Assurance and accounting A Guide to Financial Instruments for Private Enterprises and Private Sector t-for-profit Organizations For many entities adopting the Accounting Standards

ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL)

") Page 1 ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL) Complete these sample exam problems/objective questions and check your answers with the solutions at the end of the review file and identify where

Page 1 ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL) Complete these sample exam problems/objective questions and check your answers with the solutions at the end of the review file and identify where

AMA202.0035 Prof. Angela Wu

E17-1 For the following investments indentify whether they are: 1. Trading Securities 2. Available-for-Sale Securities 3. Held-to-Maturity Securities Each case is independent of the other. 1 (a) A bond

E17-1 For the following investments indentify whether they are: 1. Trading Securities 2. Available-for-Sale Securities 3. Held-to-Maturity Securities Each case is independent of the other. 1 (a) A bond

Financial Accounting: Liabilities & Equities Class notes Barbara Wyntjes, B.Sc., CGA

Module 5: Leases Part 2: Assignment 17-1 (Chapter 17, page 1080) The lease term is eight years. Guaranteed residual value, none. Unguaranteed residual value, unknown BPO, none. Minimum net lease payment,

Module 5: Leases Part 2: Assignment 17-1 (Chapter 17, page 1080) The lease term is eight years. Guaranteed residual value, none. Unguaranteed residual value, unknown BPO, none. Minimum net lease payment,

ACCOUNTING FOR TROUBLED DEBT

APPENDIX G ACCOUNTING FOR TROUBLED DEBT Illustration G-1 Usual Progression in Troubled Debt Situations Practically every day the Wall Street Journal runs a story about some company in financial difficulty.

APPENDIX G ACCOUNTING FOR TROUBLED DEBT Illustration G-1 Usual Progression in Troubled Debt Situations Practically every day the Wall Street Journal runs a story about some company in financial difficulty.

Practice Problems. Use the following information extracted from present and future value tables to answer question 1 to 4.

PROBLEM 1 MULTIPLE CHOICE Practice Problems Use the following information extracted from present and future value tables to answer question 1 to 4. Type of Table Number of Periods Interest Rate Factor

PROBLEM 1 MULTIPLE CHOICE Practice Problems Use the following information extracted from present and future value tables to answer question 1 to 4. Type of Table Number of Periods Interest Rate Factor

Corporate Finance Fundamentals [FN1]

![Corporate Finance Fundamentals [FN1]](/thumbs/29/13224229.jpg "Corporate Finance Fundamentals [FN1]") Page 1 of 32 Foundation review Introduction Throughout FN1, you encounter important techniques and concepts that you learned in previous courses in the CGA program of professional studies. The purpose

Page 1 of 32 Foundation review Introduction Throughout FN1, you encounter important techniques and concepts that you learned in previous courses in the CGA program of professional studies. The purpose

Accounting Standards for. Transition Middle of the Road

Accounting Standards for Private Enterprises Transition Middle of the Road A DISCLAIMER BEFORE WE BEGIN... Although the presentation and related materials have been carefully prepared, neither the presentation

Accounting Standards for Private Enterprises Transition Middle of the Road A DISCLAIMER BEFORE WE BEGIN... Although the presentation and related materials have been carefully prepared, neither the presentation

West Japan Railway Company

(Translation) Matters to be disclosed on the Internet in accordance with laws and ordinances and the Articles of Incorporation NOTES TO CONSOLIDATED FINANCIAL STATEMENTS NOTES TO NON-CONSOLIDATED FINANCIAL

(Translation) Matters to be disclosed on the Internet in accordance with laws and ordinances and the Articles of Incorporation NOTES TO CONSOLIDATED FINANCIAL STATEMENTS NOTES TO NON-CONSOLIDATED FINANCIAL

LO.a: Interpret interest rates as required rates of return, discount rates, or opportunity costs.

LO.a: Interpret interest rates as required rates of return, discount rates, or opportunity costs. 1. The minimum rate of return that an investor must receive in order to invest in a project is most likely

LO.a: Interpret interest rates as required rates of return, discount rates, or opportunity costs. 1. The minimum rate of return that an investor must receive in order to invest in a project is most likely

Exercise 6 8. Exercise 6 12 PVA = $5,000 x 4.35526* = $21,776

CHAPTER 6: EXERCISES Exercise 6 2 1. FV = $10,000 (2.65330 * ) = $26,533 * Future value of $1: n = 20, i = 5% (from Table 1) 2. FV = $10,000 (1.80611 * ) = $18,061 * Future value of $1: n = 20, i = 3%

CHAPTER 6: EXERCISES Exercise 6 2 1. FV = $10,000 (2.65330 * ) = $26,533 * Future value of $1: n = 20, i = 5% (from Table 1) 2. FV = $10,000 (1.80611 * ) = $18,061 * Future value of $1: n = 20, i = 3%

Statement of Cash Flows. Study Objectives

Statement of Cash Flows Study Objectives Indicate the primary purpose of the statement of cash flows. Distinguish among operating, investing, and financing activities. Explain the impact of the product

Statement of Cash Flows Study Objectives Indicate the primary purpose of the statement of cash flows. Distinguish among operating, investing, and financing activities. Explain the impact of the product

University of Waterloo Final Examination. Term: Fall Year: 2005. Core Concepts of Accounting Information

University of Waterloo Final Examination Term: Fall Year: 2005 Student Name Solution UW Student ID Number Course Abbreviation and Number AFM 101 Course Title Core Concepts of Accounting Information Section(s)

University of Waterloo Final Examination Term: Fall Year: 2005 Student Name Solution UW Student ID Number Course Abbreviation and Number AFM 101 Course Title Core Concepts of Accounting Information Section(s)

AFM 391 Case Concepts

AFM 391 Case Concepts a. Why do companies lease assets rather than buy them? 1. 100% financing at fixed rates. Leases are often signed without requiring any money down from the lessee, which helps to conserve

AFM 391 Case Concepts a. Why do companies lease assets rather than buy them? 1. 100% financing at fixed rates. Leases are often signed without requiring any money down from the lessee, which helps to conserve

CANADIAN TIRE BANK. BASEL PILLAR 3 DISCLOSURES December 31, 2014 (unaudited)

") (unaudited) 1. SCOPE OF APPLICATION Basis of preparation This document represents the Basel Pillar 3 disclosures for Canadian Tire Bank ( the Bank ) and is unaudited. The Basel Pillar 3 disclosures included

(unaudited) 1. SCOPE OF APPLICATION Basis of preparation This document represents the Basel Pillar 3 disclosures for Canadian Tire Bank ( the Bank ) and is unaudited. The Basel Pillar 3 disclosures included