What Is Other Equity? Marketable Securities. Marketable Securities, Time Value of Money /516 Accounting Spring 2004

|

|

|

- Jonah Evans

- 8 years ago

- Views:

Transcription

1 Marketable Securities, Time Value of Money /516 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology March 31, Marketable Securities Trading securities (debt and equity) Acquired for short-term profit potential Changes in market value reported in the income statement (net of taxes), investment marked to market in the balance sheet Purchases and disposals reported in operating section of SCF Held to maturity (debt only) Acquired with ability and intent to hold to maturity No changes in market value reported in the income statement, thus investment carried at historical cost in the balance sheet Interest income reported in operating section of SCF Available for sale (debt and equity) Securities not classified as either of above Changes in market value reported in Other Equity (net of taxes), instead of the income statement! Purchases and disposals reported in investing section of SCF 2 What Is Other Equity? So far, what have we seen in class? Stockholders Equity (SE) = Contributed capital (CC) + Retained Earnings (RE) The above is a simplification! It is known as the Clean Surplus Equation. In fact, Clean Surplus is often violated SE = CC + RE + Other Equity What causes changes in Other Equity? Changes in the market value of AFS securities, for one! 3

Acquired with ability and intent to hold to maturity No changes in market value reported in the income statement, thus investment carried at historical cost in the balance sheet Interest")

2 An Illustration: Acquisition and Dividends (2002) On Jan. 1, 2002, Ace acquired 500 common shares of security MITCo for $25/share. C MS +MS adj = DTL OE RE Trading: Adjunct account On Nov. 30, 2002, Ace received $625 in dividends ($1.25/share of MITCo) C MS +MSadj = DTL OE RE Trading: 4 An Illustration: Acquisition and Dividends (2002) On Jan. 1, 2002, Ace acquired 500 common shares of security MITCo for $25/share. C MS +MS adj = DTL OE RE Trading: () Same as above On Nov. 30, 2002, Ace received $625 in dividends ($1.25/share of MITCo) C MS +MSadj = DTL OE RE Trading: 5 An Illustration: Acquisition and Dividends (2002) On Jan. 1, 2002, Ace acquired 500 common shares of security MITCo for $25/share. C MS +MS adj = DTL OE RE Trading: () Same as above On Nov. 30, 2002, Ace received $625 in dividends ($1.25/share of MITCo) C MS +MSadj = DTL OE RE Trading: Same as above Investment income on I/S 6

C MS +MSadj = DTL OE RE Trading: 5 An Illustration: Acquisition and Dividends (2002) On Jan.")

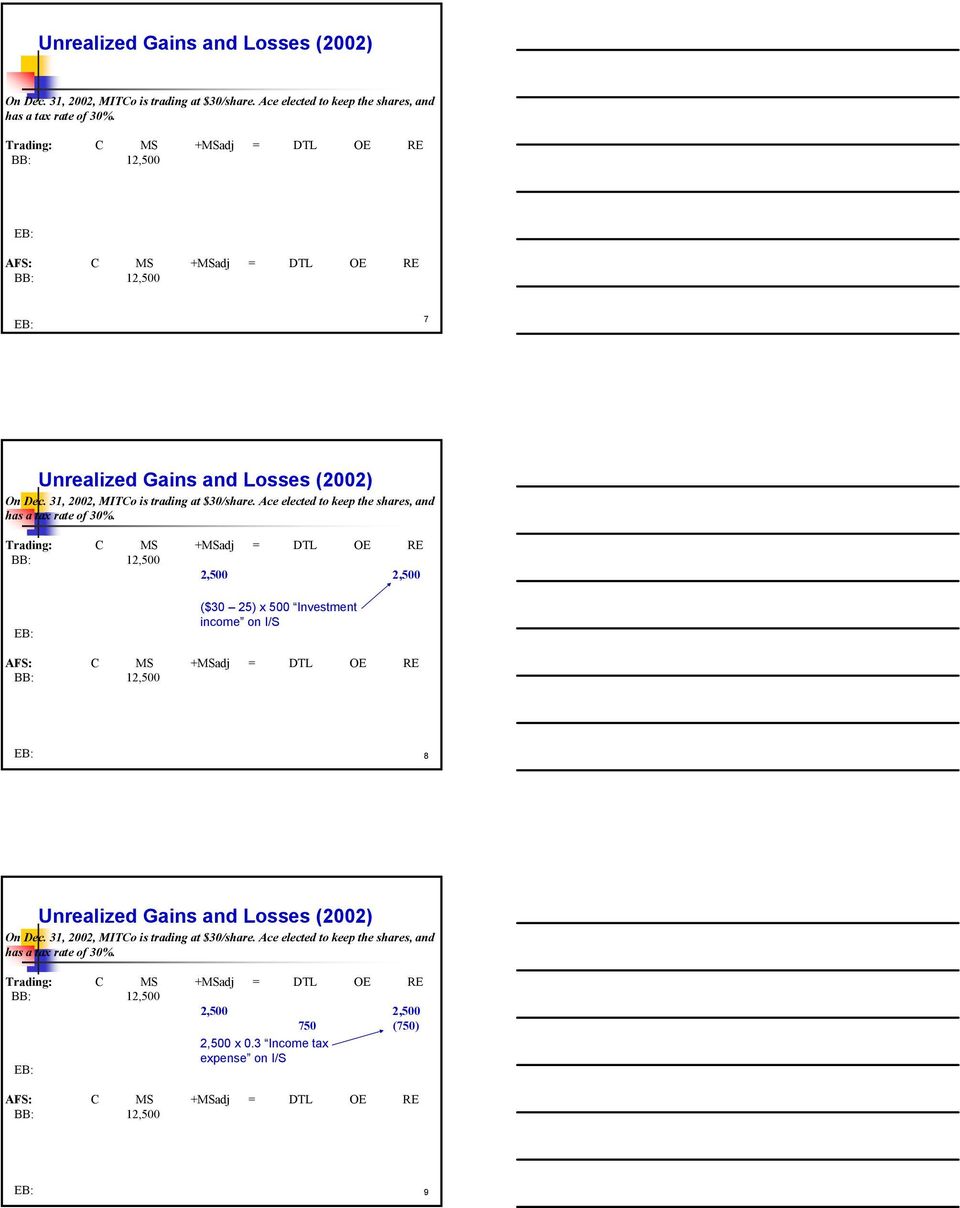

3 Unrealized Gains and Losses (2002) On Dec. 31, 2002, MITCo is trading at $30/share. Ace elected to keep the shares, and has a tax rate of 30%. Trading: C MS +MSadj = DTL OE RE C MS +MSadj = DTL OE RE 7 Unrealized Gains and Losses (2002) On Dec. 31, 2002, MITCo is trading at $30/share. Ace elected to keep the shares, and has a tax rate of 30%. Trading: C MS +MSadj = DTL OE RE ($30 25) x 500 Investment income on I/S C MS +MSadj = DTL OE RE 8 Unrealized Gains and Losses (2002) On Dec. 31, 2002, MITCo is trading at $30/share. Ace elected to keep the shares, and has a tax rate of 30%. Trading: C MS +MSadj = DTL OE RE 750 (750) x 0.3 Income tax expense on I/S C MS +MSadj = DTL OE RE 9

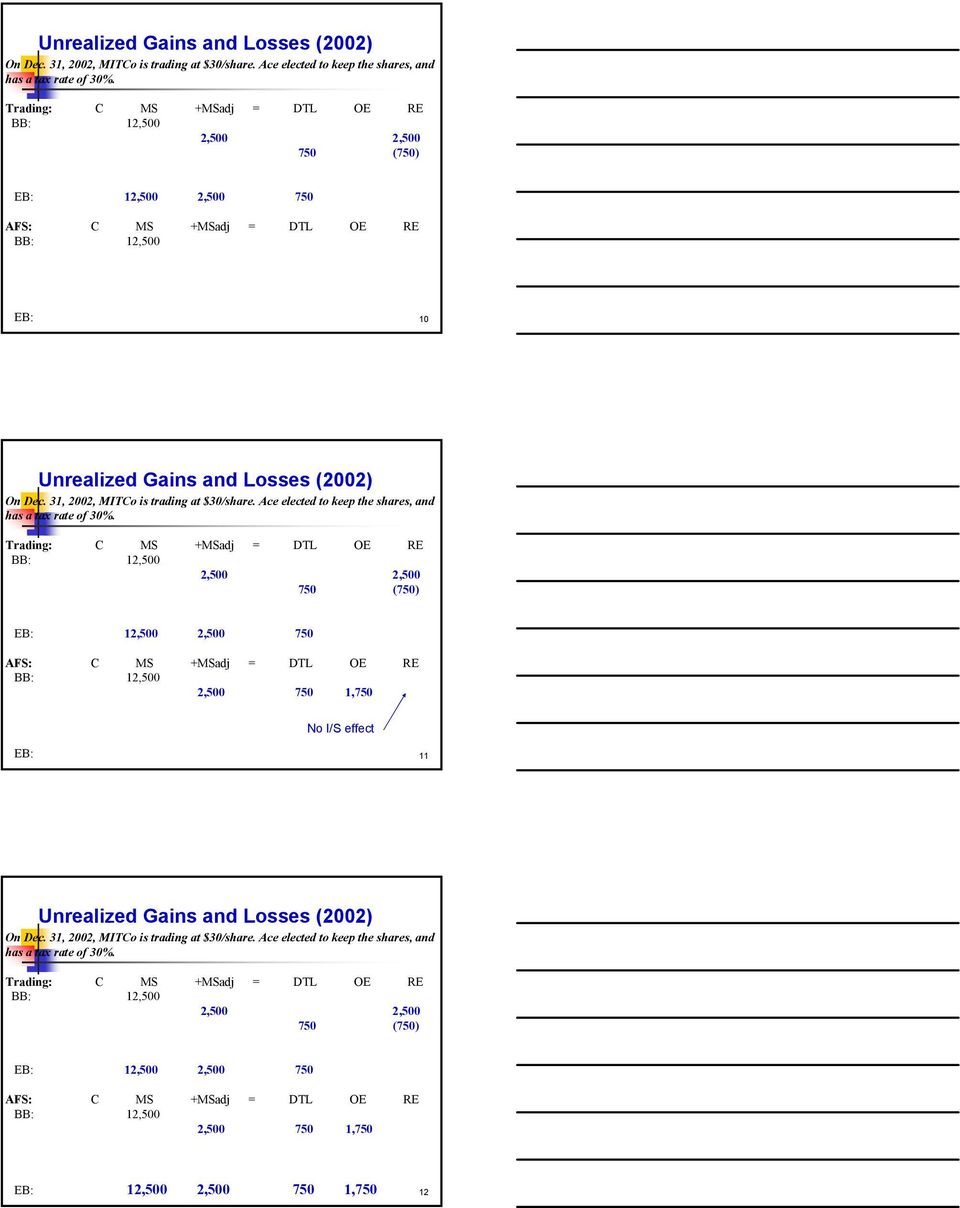

4 Unrealized Gains and Losses (2002) On Dec. 31, 2002, MITCo is trading at $30/share. Ace elected to keep the shares, and has a tax rate of 30%. Trading: C MS +MSadj = DTL OE RE 750 (750) 750 C MS +MSadj = DTL OE RE 10 Unrealized Gains and Losses (2002) On Dec. 31, 2002, MITCo is trading at $30/share. Ace elected to keep the shares, and has a tax rate of 30%. Trading: C MS +MSadj = DTL OE RE 750 (750) 750 C MS +MSadj = DTL OE RE 750 1,750 No I/S effect 11 Unrealized Gains and Losses (2002) On Dec. 31, 2002, MITCo is trading at $30/share. Ace elected to keep the shares, and has a tax rate of 30%. Trading: C MS +MSadj = DTL OE RE 750 (750) 750 C MS +MSadj = DTL 750 OE 1,750 RE 750 1,750 12

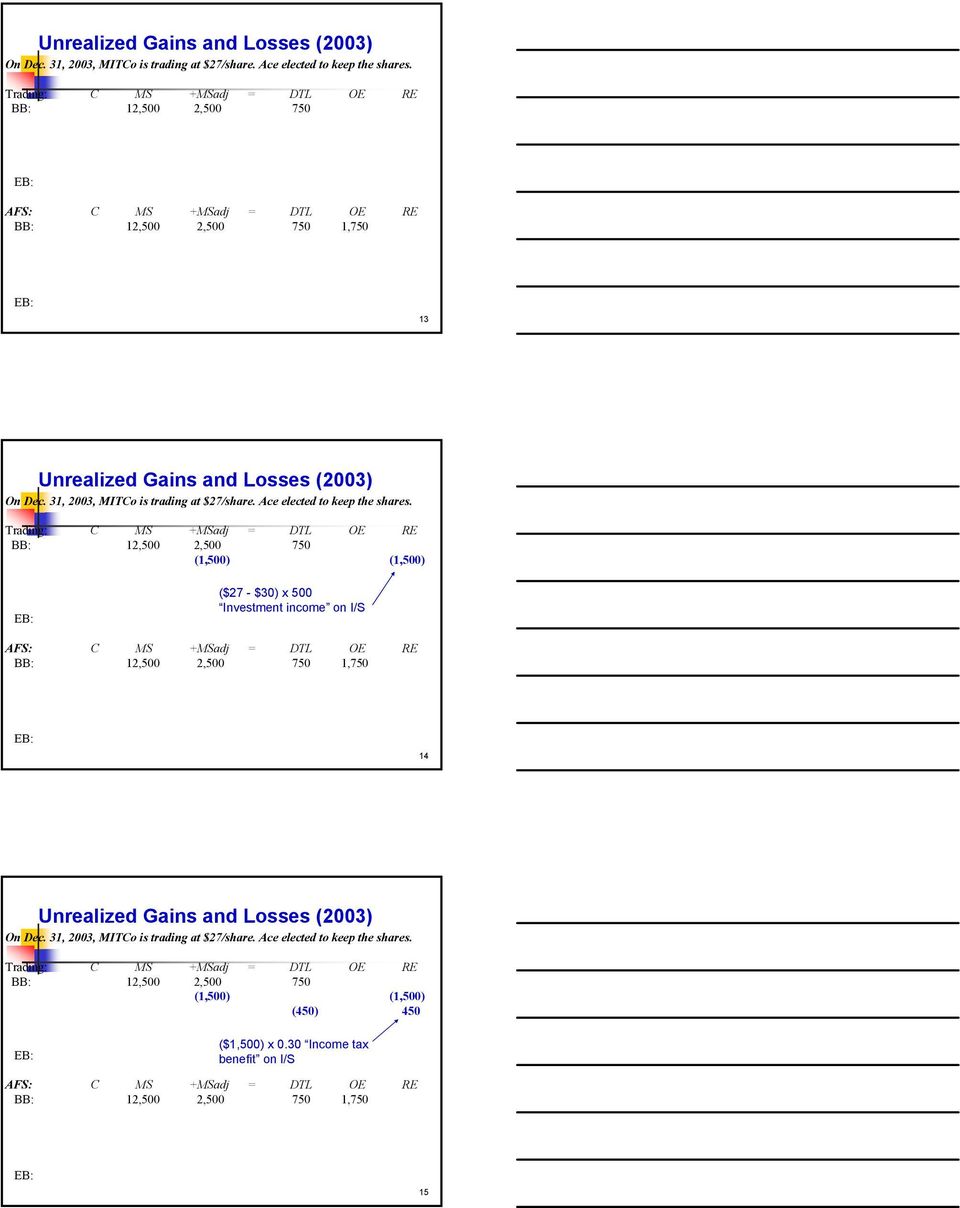

5 Unrealized Gains and Losses (2003) On Dec. 31, 2003, MITCo is trading at $27/share. Ace elected to keep the shares. 750 C MS +MSadj = DTL 750 OE 1,750 RE 13 Unrealized Gains and Losses (2003) On Dec. 31, 2003, MITCo is trading at $27/share. Ace elected to keep the shares. 750 (1,500) (1,500) ($27 - $30) x 500 Investment income on I/S C MS +MSadj = DTL OE RE 750 1, Unrealized Gains and Losses (2003) On Dec. 31, 2003, MITCo is trading at $27/share. Ace elected to keep the shares. 750 (1,500) (1,500) (450) 450 ($1,500) x 0.30 Income tax benefit on I/S C MS +MSadj = DTL OE RE 750 1,750 15

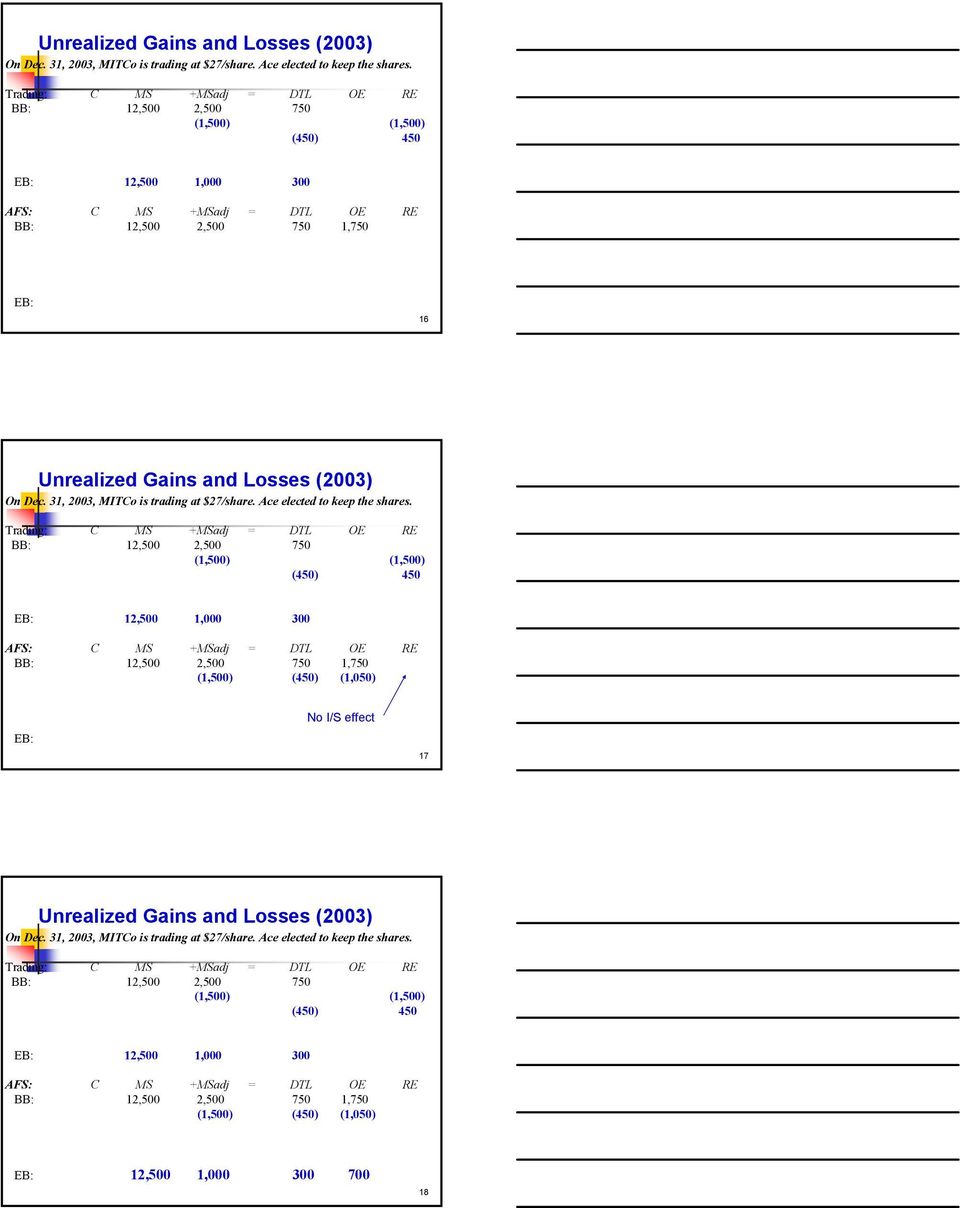

6 Unrealized Gains and Losses (2003) On Dec. 31, 2003, MITCo is trading at $27/share. Ace elected to keep the shares. 750 (1,500) (1,500) (450) 450 1, C MS +MSadj = DTL 750 OE 1,750 RE 16 Unrealized Gains and Losses (2003) On Dec. 31, 2003, MITCo is trading at $27/share. Ace elected to keep the shares. 750 (1,500) (1,500) (450) 450 1, C MS +MSadj = DTL OE RE 750 1,750 (1,500) (450) (1,050) No I/S effect 17 Unrealized Gains and Losses (2003) On Dec. 31, 2003, MITCo is trading at $27/share. Ace elected to keep the shares. 750 (1,500) (1,500) (450) 450 1, C MS +MSadj (1,500) = DTL 750 (450) OE 1,750 (1,050) RE 1,

7 Realized Gains and Losses (2004) On Feb. 14, 2004, Ace sold all of its investment in MITCo, then trading at $36/share. 1, C MS +MSadj 1,000 = DTL 300 OE 700 RE 19 Realized Gains and Losses (2004) On Feb. 14, 2004, Ace sold all of its investment in MITCo, then trading at $36/share. 1, ,000 () (1,000) 4,500 $36 x 500 Plug that equals ($36 - $27) x Remove existing accounts 500 Investment income on I/S C MS +MSadj = DTL OE RE 1, Realized Gains and Losses (2004) On Feb. 14, 2004, Ace sold all of its investment in MITCo, then trading at $36/share. 1, ,000 () (1,000) 4,500 (1,650) (300) (1,350) Pay tax on the full gain Recognize tax expense for gain ($36 - $25) x 500 x 0.30 in this year s I/S, $4,500 x 0.30 C MS +MSadj = DTL OE RE 1,

8 Realized Gains and Losses (2004) On Feb. 14, 2004, Ace sold all of its investment in MITCo, then trading at $36/share. 1, ,000 () (1,000) 4,500 (1,650) (300) (1,350) C MS +MSadj = DTL OE RE 1, ,000 () (1,000) (300) (700) 5,500 $36 x 500 Remove existing accounts Plug that equals ($36 - $25) x 500 Investment income on I/S 22 Realized Gains and Losses (2004) On Feb. 14, 2004, Ace sold all of its investment in MITCo, then trading at $36/share. 1, ,000 () (1,000) 4,500 (1,650) (300) (1,350) C MS +MSadj = DTL OE RE 1, ,000 () (1,000) (300) (700) 5,500 (1,650) (1,650) Pay tax on the full gain Recognize tax expense for the gain ($18,000 - $) x 0.30 in this year s I/S, $5,500 x Marketable Securities: Income patterns Trading Available for Sale 5,500 4,500 5,500 4,500-1, ,

x 0.30 in this year s I/S, $5,500 x 0.")

9 Marketable Securities: Income patterns Trading Available for Sale 5,500 4,500 5,500 4, ,500-1, Marking to market For both Trading and AFS securities Book value of security investments tracks market value Balance sheet effects are the same! Marketable Securities and total Stockholders Equity will be the same. What is different? Income statement effects For trading securities, gains or losses recognized in Income Statement track changes in market value For AFS securities, gains or losses net of taxes are cumulatively recorded in Other Equity till securities are sold At that time, all gains and losses are recognized in Income Statement and the Other Equity account as well as Deferred Tax Liability account is cleared off. 26 Reclassifications of Marketable Securities Trading to Available for sale Gains or losses of the period recognized on reclassification date Subsequent market value changes reported in Other Equity Available for sale to Trading Cumulative gains or losses, including those of current period, recognized on reclassification date Subsequent market value changes reported in the income statement 27

10 Why does recognition of gains/losses matter? Former SEC Chairman Breeden, on mark-to-market (ca 1990): If you are in a volatile business, then your balance sheet and income statement should reflect that volatility. Furthermore, we have seen significant abuse of managed earnings. Too often companies buy securities with an intent to hold them as investments, and then miraculously, when they rise in value, the companies decide it's time to sell them. Meanwhile, their desire to hold those securities that are falling in value grows ever stronger. So companies report the gains and hide the losses. Current SEC Chairman Arthur Levitt, Jr (1997): it is unacceptable to allow American investors to remain in the dark about the consequences of a $23 trillion derivatives exposure. We support the independence of the FASB as they turn on the light. Federal Reserve Chairman Greenspan, on derivatives (ca 1997): Putting the unrealized gains and losses of open derivatives contracts onto companies income statements would introduce "artificial" volatility to their earnings and equity. Shareholders would become confused; management might forego sensible hedging strategies out of purely window dressing concerns. 28 A compromise in GAAP? Recognize all unrealized gains/losses for trading securities in Net Income Mark available for sale securities to market value, but don t report changes in the income statement Reduces earnings volatility Managers dislike income volatility They complain similarly about other accounting method changes that increase reported earnings volatility even though underlying cash flows are unaffected Ignore value changes for held to maturity category 29 Marketable Securities in other countries Canada: LCM for investments classified as current assets; historical cost for noncurrent assets, but recognize permanent declines in value Mexico: Carry marketable securities at net realizable value, report gains/losses in the income statement; LCM for other investments Japan: LCM for marketable securities Others: Typically either LCM or mark-to-market, exclusively International Accounting Standards: Similar to US GAAP 30

11 Summary Valuation adjustment necessary when changes in market values are objectively measurable Lower of cost or market applied to inventory valuation New GAAP in marketable securities: mark-to-market treats gains and losses equally Disclosure vs. Recognition in mark-to-market accounting: Not all gains and losses are reported in the income statement A compromise! 31 LIABILITIES: Current Liabilities Obligations that must be discharged in a short period of time (generally less than one year) Reported on balance sheet at nominal value Examples: Accounts payable Short-term borrowings Current portion of long-term debt Deposits Warranties Deferred Revenues / Income 32 LIABILITIES: Long-term Liabilities Obligations spanning a longer period of time (generally more than one year) Generally reported on the balance sheet at present value based on interest rate when initiated Examples: Bonds Long-term loans Mortgages Capital Leases How do we compute present values? And interest expense? 33

12 Time Value Of Money Refresher Time 1 Interest = 10% $1.00 Time 0 Time 1 $1.00 $1.10 Future value of $ 1.00 today = $1.00 (1+10%) = $1.10 at the end of one year. What is the present value of $1.10 to be received one year from now? Present value of $1.10 one year from now = $1.10/(1+10%) = $1.00 What is the present value of $1.00 to be received one year from now? Present value of $1.00 one year from now = $1.00/(1.10) = $ Time Value Of Money Refresher $0.83 $0.91 $1.00 T=0 T=1 T=2 $1.00 $1.10 $1.21 Future value of $1.00 two years from now = $1.00*(1+10%)*(1+10%) = $1.00*(1.10) 2 = $1.21 Present value of $1.00 to be received two years from now = $1.00/[(1.10) 2 ] = $0.83 RECALL: PV of $1.00 to be received a year from now = $ Calculating present values: An example You have just won a lottery. The lottery board offers you three different options for collecting your winnings: (1) Payments of $500,000 at the end of each year for 20 years. (2) Lump-sum payment of $4,500,000 today. (3) Lump-sum payment of $1 million today, followed by $2,100,000 at the end of years 5, 6, and 7. Assume all earnings can be invested at a 10 percent annual rate. Ignoring any tax effects, which option should you 36 choose and why?

2 ] = $0.83 RECALL: PV of $1.00 to be received a year from now = $0.")

13 Future Value of Option 1: $500,000 at the end of each year for 20 years years $0.5m (1.1) 19 = $3.06m 18 years $0.5m (1.1) 18 = $2.78m 17 years $0.5m (1.1) 17 = $2.53m $0.5m (1.1) 1 = $0.55m $0.5m (1.1) 0 = $0.50m $28.64m 37 Future Value of Option 2: Lump-sum payment of $4,500,000 today years $4.5m (1.1) 20 = $30.27m 38 Future Value of Option 3: $1m today, and $2.1m at the end of years 5, 6, and years 15 years 14 years 13 years $1.0m (1.1) 20 = $3.36m $2.1m (1.1) 15 = $8.77m $2.1m (1.1) 14 = $7.97m $2.1m (1.1) 13 = $7.25m $30.71m 39

14 Future Values If you invest all lottery receipts at 10% peryear, how much will you have in 20 years? 1. $500K (1.10) 19 + $500K (1.10) $500K (1.10) 1 + $500K = $28.64m 2. $4,500,000 (1.10) 20 = $30.27m 3. $1m (1.10) 20 + $2.1m (1.10) 15 + $2.1m (1.10) 14 + $2.1m (1.10) 13 = $30.71m Î FV(Option 1) < FV(Option 2) < FV(Option 3) 40 Present Value of Option 1: $500,000 at the end of each year for 20 years $0.5m (1.1) -1 = $0.45m $0.5m (1.1) -2 = $0.41m $0.5m (1.1) -3 = $0.38m 1 year 2 years 3 years $0.5m (1.1) -19 = $0.08m $0.5m (1.1) -20 = $0.07m $4.26m 19 years 20 years 41 Present Value of Option 2: Lump-sum payment of $4,500,000 today $4.5m 42

-2 = $0.41m $0.5m (1.1) -3 = $0.38m 1 year 2 years 3 years $0.5m (1.1) -19 = $0.08m $0.5m (1.1) -20 = $0.07m $4.")

15 Present Value of Option 3: $1m today, and $2.1m at the end of years 5, 6, and $1.0m (1.1) 0 = $1.00m $2.1m (1.1) -5 = $1.30m $2.1m (1.1) -6 = $1.19m $2.1m (1.1) -7 = $1.08m $4.57m 5 years 6 years 7 years 43 Present Values If all lottery receipts can be invested at 10% per year, what is the present value of each option? 1. $500K (1.10) $500K (1.10) $500K (1.10) -2 + $500K (1.10) -1 = $4.26m 2. $4,500,000 (1.10) 0 = $4.5m 3. $1m (1.10) 0 + $2.1m (1.10) -5 + $2.1m (1.10) -6 + $2.1m (1.10) -7 = $4.57m Î PV(Option 1) < PV(Option 2) < PV(Option 3) 44 Converting Present and Future Values Present Values Future Values Option 1 $4.26m Option 2 $4.50m Option 3 $4.57m FV = = PV = = 4.26 FV = = PV = = 4.50 FV = = PV = = 4.57 Option 1 $28.64m Option 2 $30.27m Option 3 $30.71m 45

< PV(Option 2) < PV(Option 3) 44 Converting Present and Future Values 0 1 2 3 4 5 6 7 19 20 Present Values Future Values Option 1 $4.26m Option 2 $4.50m Option 3 $4.57m FV = 4.26 1.")

16 Using PV and FV Tables Tbl 1: Future Value of $1 A one-time payment to be received now and held (reinvested) for n periods Compounded at interest rate r Multiply the dollar amount received by the factor in Row n, Column r Formula: FV($1) = (1+r) n Pratt, Jamie. Financial Accounting in an Economic Context. 5th ed. John Wiley & Sons, p Using PV and FV Tables Tbl 4: Present Value of $1 A one-time payment to be received n periods from now Discounted at interest rate r Multiply the dollar amount to be received by the factor in Row n, Column r Formula: PV($1) = 1/(1+r) n = (1+r) -n Pratt, Jamie. Financial Accounting in an Economic Context. 5th ed. John Wiley & Sons, p Some PV Terminology Annuity: a stream of fixed-dollar payments made at regular intervals of time Ordinary Annuity (annuity in arrears): payments occur at the end of the period Annuity due (annuity in advance): payments occur at the beginning of the period 48

= 1/(1+r) n = (1+r) -n Pratt, Jamie. Financial Accounting in an Economic Context. 5th ed. John Wiley & Sons, 2003. p. 708.")

17 Using PV and FV Tables Tbl 2: Future Value of $1 ordinary annuity Regular payments to be received at end of year for n years and held (reinvested) until time n Compounded at interest rate r Multiply the dollar amount received by the factor in Row n, Column r Pratt, Jamie. Financial Accounting in an Economic Context. 5th ed. John Wiley & Sons, p Using PV and FV Tables Tbl 3: Future Value of $1 annuity due Regular payments to be received at beginning of year for n years and held (reinvested) until time n Compounded at interest rate r Multiply the dollar amount received by the factor in Row n, Column r Table is redundant Pratt, Jamie. Financial Accounting in an Economic Context. 5th ed. John Wiley & Sons, p Using PV and FV Tables Tbl 5: Present Value of $1 ordinary annuity Regular payments to be received at end of year for n years Compounded at interest rate r Multiply the dollar amount received by the factor in Row n, Column r Pratt, Jamie. Financial Accounting in an Economic Context. 5th ed. John Wiley & Sons, p

18 Using PV and FV Tables Tbl 6: Present Value of $1 annuity due Regular payments to be received at beginning of year for n years Compounded at interest rate r Multiply the dollar amount received by the factor in Row n, Column r Also redundant Pratt, Jamie. Financial Accounting in an Economic Context. 5th ed. John Wiley & Sons, p Annuity Formulas Sum of infinite series : 1 = e. g., = 1 n n =1 k k PV of a perpetuity : = = n n =1 (1 + r ) (1 + r ) 1 r A perpetuity is a constant amount received at the end of each period. 53 Present Values of Lottery Options - Revisited If all lottery receipts can be invested at 10% per year, what is the present value of each option? $500K PVFOrdinaryAnnuity 20 years, 10% = $4.26m $4,500,000 PVF 0 years, 10% = $4.5m $1m PVF 0 years, 10% + Present Value of ordinary annuity of $2.1m for three years starting Year 4 = $1m + ($2.1m x PVFOrdinaryAnnuity 3 years, 10% ) x PVF 4 years, 10% = $1m + (2.1 x ) x = $4.57m PV(Option 1) < PV(Option 2) < PV(Option 3) 54

19 Problem With Time Value of Money The Croziers want to provide for three-year-old son Ryan s future college education. They estimate that it will cost $40,000/year for four years when Ryan enters college 15 years from now. Assuming a 10% interest rate, and college payments due at the start of each year: (a) How much would the parents have to invest today? (b) How much would they have to invest at the end of each year for the next 14 years? (c) How would your answers change if the expected rate of return is only 8% per year? 55 Part (a): How much would the parents have to invest today? Step 1: Calculate how much money they will need 15 years from now. PV 15 = $40,000 PVFactorAnnuityDue 4yrs, 10% = $40, = $139,476 Step 2: Calculate the present value of the amount from Step 1. PV 0 = $139,476 PVFactor 15yrs, 10% = $139, = $33, Part (b): How much would they have to invest at the end of each year for the next 14 years? The PV of the annuity must equal the PV calculated in part (a). $33,389 = Annuity Payments PVFactorAnnuity 14yrs, 10% = Annuity Payments Annuity Payments = $4,532 57

How much would they have to invest at the end of each year for the next 14 years? (c) How would your answers change if the expected rate of return is only 8% per year?")

20 Part (c): How would your answers change if the expected rate of return is only 8%p/a? Step 1: Calculate how much money they will need 15 years from now. PV 15 = $40,000 PVFactorAnnuityDue 4yrs, 8% = $40, = $143,084 Step 2: Calculate the PV at time 0. PV 0 = $143,084 PVFactor 15yrs, 8% = $143, = $45,106 The PV of the annuity must equal $45,106 $45,106 = Annuity Pmts PVFA 14yrs, 8% = Annuity Pmts Annuity Pmts = $

Marketable Securities and Deferred Taxes

Marketable Securities and Deferred Taxes 15.501/516 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology 1 Marketable Securities and Deferred

Marketable Securities and Deferred Taxes 15.501/516 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology 1 Marketable Securities and Deferred

Time Value of Money. 15.511 Corporate Accounting Summer 2004. Professor S. P. Kothari Sloan School of Management Massachusetts Institute of Technology

Time Value of Money 15.511 Corporate Accounting Summer 2004 Professor S. P. Kothari Sloan School of Management Massachusetts Institute of Technology July 2, 2004 1 LIABILITIES: Current Liabilities Obligations

Time Value of Money 15.511 Corporate Accounting Summer 2004 Professor S. P. Kothari Sloan School of Management Massachusetts Institute of Technology July 2, 2004 1 LIABILITIES: Current Liabilities Obligations

Long-Term Debt. Objectives: simple present value calculations. Understand the terminology of long-term debt Par value Discount vs.

Objectives: Long-Term Debt! Extend our understanding of valuation methods beyond simple present value calculations. Understand the terminology of long-term debt Par value Discount vs. Premium Mortgages!

Objectives: Long-Term Debt! Extend our understanding of valuation methods beyond simple present value calculations. Understand the terminology of long-term debt Par value Discount vs. Premium Mortgages!

CHAPTER 6. Accounting and the Time Value of Money. 2. Use of tables. 13, 14 8 1. a. Unknown future amount. 7, 19 1, 5, 13 2, 3, 4, 6

CHAPTER 6 Accounting and the Time Value of Money ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems 1. Present value concepts. 1, 2, 3, 4, 5, 9, 17, 19 2. Use

CHAPTER 6 Accounting and the Time Value of Money ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems 1. Present value concepts. 1, 2, 3, 4, 5, 9, 17, 19 2. Use

Bonds. Accounting for Long-Term Debt. Agenda Long-Term Debt. 15.501/516 Accounting Spring 2004

Accounting for Long-Term Debt 15.501/516 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology April 5, 2004 1 Agenda Long-Term Debt Extend our

Accounting for Long-Term Debt 15.501/516 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology April 5, 2004 1 Agenda Long-Term Debt Extend our

Appendix C- 1. Time Value of Money. Appendix C- 2. Financial Accounting, Fifth Edition

C- 1 Time Value of Money C- 2 Financial Accounting, Fifth Edition Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount. 3. Solve for future

C- 1 Time Value of Money C- 2 Financial Accounting, Fifth Edition Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount. 3. Solve for future

Present Value Concepts

Present Value Concepts Present value concepts are widely used by accountants in the preparation of financial statements. In fact, under International Financial Reporting Standards (IFRS), these concepts

Present Value Concepts Present value concepts are widely used by accountants in the preparation of financial statements. In fact, under International Financial Reporting Standards (IFRS), these concepts

Balance Sheet. 15.501/516 Accounting Spring 2004. Professor S.Roychowdhury. Sloan School of Management Massachusetts Institute of Technology

Balance Sheet 15.501/516 Accounting Spring 2004 Professor S.Roychowdhury Sloan School of Management Massachusetts Institute of Technology Feb 09, 2003 1 Some residual administrative matters Access web

Balance Sheet 15.501/516 Accounting Spring 2004 Professor S.Roychowdhury Sloan School of Management Massachusetts Institute of Technology Feb 09, 2003 1 Some residual administrative matters Access web

Appendix. Time Value of Money. Financial Accounting, IFRS Edition Weygandt Kimmel Kieso. Appendix C- 1

C Time Value of Money C- 1 Financial Accounting, IFRS Edition Weygandt Kimmel Kieso C- 2 Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount.

C Time Value of Money C- 1 Financial Accounting, IFRS Edition Weygandt Kimmel Kieso C- 2 Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount.

CHAPTER 6. Accounting and the Time Value of Money. 2. Use of tables. 13, 14 8 1. a. Unknown future amount. 7, 19 1, 5, 13 2, 3, 4, 7

CHAPTER 6 Accounting and the Time Value of Money ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems 1. Present value concepts. 1, 2, 3, 4, 5, 9, 17 2. Use of

CHAPTER 6 Accounting and the Time Value of Money ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems 1. Present value concepts. 1, 2, 3, 4, 5, 9, 17 2. Use of

Unit 6 Receivables. Receivables - Claims resulting from credit sales to customers and others goods or services for money,.

Unit 6 Receivables 7-1 Receivables - Claims resulting from credit sales to customers and others goods or services for money,. Oral promises of the purchaser to pay for goods and services sold (credit sale;

Unit 6 Receivables 7-1 Receivables - Claims resulting from credit sales to customers and others goods or services for money,. Oral promises of the purchaser to pay for goods and services sold (credit sale;

TVM Applications Chapter

Chapter 6 Time of Money UPS, Walgreens, Costco, American Air, Dreamworks Intel (note 10 page 28) TVM Applications Accounting issue Chapter Notes receivable (long-term receivables) 7 Long-term assets 10

Chapter 6 Time of Money UPS, Walgreens, Costco, American Air, Dreamworks Intel (note 10 page 28) TVM Applications Accounting issue Chapter Notes receivable (long-term receivables) 7 Long-term assets 10

The Time Value of Money

The Time Value of Money Time Value Terminology 0 1 2 3 4 PV FV Future value (FV) is the amount an investment is worth after one or more periods. Present value (PV) is the current value of one or more future

The Time Value of Money Time Value Terminology 0 1 2 3 4 PV FV Future value (FV) is the amount an investment is worth after one or more periods. Present value (PV) is the current value of one or more future

Chapter 6. Time Value of Money Concepts. Simple Interest 6-1. Interest amount = P i n. Assume you invest $1,000 at 6% simple interest for 3 years.

6-1 Chapter 6 Time Value of Money Concepts 6-2 Time Value of Money Interest is the rent paid for the use of money over time. That s right! A dollar today is more valuable than a dollar to be received in

6-1 Chapter 6 Time Value of Money Concepts 6-2 Time Value of Money Interest is the rent paid for the use of money over time. That s right! A dollar today is more valuable than a dollar to be received in

Chapter 6. Discounted Cash Flow Valuation. Key Concepts and Skills. Multiple Cash Flows Future Value Example 6.1. Answer 6.1

Chapter 6 Key Concepts and Skills Be able to compute: the future value of multiple cash flows the present value of multiple cash flows the future and present value of annuities Discounted Cash Flow Valuation

Chapter 6 Key Concepts and Skills Be able to compute: the future value of multiple cash flows the present value of multiple cash flows the future and present value of annuities Discounted Cash Flow Valuation

1. Debt securities are instruments representing a creditor relationship with an enterprise.

Chapter 18 Investments LECTURE OUTLINE The material in this chapter can be covered in three class periods. Students will have some difficulty with the classifications of debt securities into trading, available-for-sale,

Chapter 18 Investments LECTURE OUTLINE The material in this chapter can be covered in three class periods. Students will have some difficulty with the classifications of debt securities into trading, available-for-sale,

15.511 Corporate Accounting Recitation 6. July 7, 2004

15.511 Corporate Accounting Recitation 6 July 7, 2004 1 Agenda Marketable Securities (lecture notes) Bonds Leases Deferred tax 2 Accounting for Bonds -Terminology Par value Proceeds from issuance Coupon

15.511 Corporate Accounting Recitation 6 July 7, 2004 1 Agenda Marketable Securities (lecture notes) Bonds Leases Deferred tax 2 Accounting for Bonds -Terminology Par value Proceeds from issuance Coupon

Discounted Cash Flow Valuation

6 Formulas Discounted Cash Flow Valuation McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter Outline Future and Present Values of Multiple Cash Flows Valuing

6 Formulas Discounted Cash Flow Valuation McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter Outline Future and Present Values of Multiple Cash Flows Valuing

TIME VALUE OF MONEY (TVM)

") TIME VALUE OF MONEY (TVM) INTEREST Rate of Return When we know the Present Value (amount today), Future Value (amount to which the investment will grow), and Number of Periods, we can calculate the rate

TIME VALUE OF MONEY (TVM) INTEREST Rate of Return When we know the Present Value (amount today), Future Value (amount to which the investment will grow), and Number of Periods, we can calculate the rate

Chapter 21 The Statement of Cash Flows Revisited

Chapter 21 The Statement of Cash Flows Revisited AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments,

Chapter 21 The Statement of Cash Flows Revisited AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments,

Chapter 2 Present Value

Chapter 2 Present Value Road Map Part A Introduction to finance. Financial decisions and financial markets. Present value. Part B Valuation of assets, given discount rates. Part C Determination of risk-adjusted

Chapter 2 Present Value Road Map Part A Introduction to finance. Financial decisions and financial markets. Present value. Part B Valuation of assets, given discount rates. Part C Determination of risk-adjusted

Investments and advances... 313,669

Consolidated Financial Statements of the Company The consolidated balance sheet, statement of income, and statement of equity of the Company are as follows. Please note the Company s consolidated financial

Consolidated Financial Statements of the Company The consolidated balance sheet, statement of income, and statement of equity of the Company are as follows. Please note the Company s consolidated financial

PREVIEW OF CHAPTER 6-2

6-1 PREVIEW OF CHAPTER 6 6-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 6 Accounting and the Time Value of Money LEARNING OBJECTIVES After studying this chapter, you should

6-1 PREVIEW OF CHAPTER 6 6-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 6 Accounting and the Time Value of Money LEARNING OBJECTIVES After studying this chapter, you should

Chapter 6. Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams

Chapter 6 Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams 1. Distinguish between an ordinary annuity and an annuity due, and calculate present

Chapter 6 Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams 1. Distinguish between an ordinary annuity and an annuity due, and calculate present

Accounting for Bonds and Long-Term Notes

Accounting for Bonds and Long-Term Notes Bond Premiums and Discounts Effective interest method Bond issuance Interest expense Types of Debt Instruments Zero-Coupon Bonds Convertible Bonds Detachable Warrants

Accounting for Bonds and Long-Term Notes Bond Premiums and Discounts Effective interest method Bond issuance Interest expense Types of Debt Instruments Zero-Coupon Bonds Convertible Bonds Detachable Warrants

Investments and advances... 344,499

Consolidated Financial Statements of the Company The consolidated balance sheet, statement of income, and statement of equity of the Company are as follows. Please note the Company s consolidated financial

Consolidated Financial Statements of the Company The consolidated balance sheet, statement of income, and statement of equity of the Company are as follows. Please note the Company s consolidated financial

HOME PRODUCT CENTER PUBLIC COMPANY LIMITED BALANCE SHEETS AS AT DECEMBER 31, 2003 AND 2002

BALANCE SHEETS AS AT DECEMBER 31, 2003 AND 2002 Assets Note 2003 Baht 2002 Current assets Cash and cash equivalents 2 36,291,871.62 84,051,092.97 Accounts receivable - net 3 121,235,696.40 140,699,262.83

BALANCE SHEETS AS AT DECEMBER 31, 2003 AND 2002 Assets Note 2003 Baht 2002 Current assets Cash and cash equivalents 2 36,291,871.62 84,051,092.97 Accounts receivable - net 3 121,235,696.40 140,699,262.83

Chapter 9, Problem 7 Closing inventory profits Before Tax After tax 40% tax

Chapter 9, Problem 7 Cost of 70% of Simon 900,000 Book value of Simon Common stock 550,000 Retained earnings Jan. 1 400,000 Net income to April 1 (¼ 200,000) 50,000 1,000,000 70% 700,000 Purchase discrepancy

Chapter 9, Problem 7 Cost of 70% of Simon 900,000 Book value of Simon Common stock 550,000 Retained earnings Jan. 1 400,000 Net income to April 1 (¼ 200,000) 50,000 1,000,000 70% 700,000 Purchase discrepancy

Chapter 5 Time Value of Money 2: Analyzing Annuity Cash Flows

1. Future Value of Multiple Cash Flows 2. Future Value of an Annuity 3. Present Value of an Annuity 4. Perpetuities 5. Other Compounding Periods 6. Effective Annual Rates (EAR) 7. Amortized Loans Chapter

1. Future Value of Multiple Cash Flows 2. Future Value of an Annuity 3. Present Value of an Annuity 4. Perpetuities 5. Other Compounding Periods 6. Effective Annual Rates (EAR) 7. Amortized Loans Chapter

Consolidated Interim Earnings Report

Consolidated Interim Earnings Report For the Six Months Ended 30th September, 2003 23th Octorber, 2003 Hitachi Capital Corporation These financial statements were prepared for the interim earnings release

Consolidated Interim Earnings Report For the Six Months Ended 30th September, 2003 23th Octorber, 2003 Hitachi Capital Corporation These financial statements were prepared for the interim earnings release

5. Time value of money

1 Simple interest 2 5. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

1 Simple interest 2 5. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

CHAPTER 2 ACCOUNTING STATEMENTS, TAXES, AND CASH FLOW

CHAPTER 2 ACCOUNTING STATEMENTS, TAXES, AND CASH FLOW Answers to Concepts Review and Critical Thinking Questions 1. True. Every asset can be converted to cash at some price. However, when we are referring

CHAPTER 2 ACCOUNTING STATEMENTS, TAXES, AND CASH FLOW Answers to Concepts Review and Critical Thinking Questions 1. True. Every asset can be converted to cash at some price. However, when we are referring

Discounted Cash Flow Valuation

Discounted Cash Flow Valuation Chapter 5 Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

Discounted Cash Flow Valuation Chapter 5 Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

Consolidated Balance Sheets March 31, 2001 and 2000

Financial Statements SEIKAGAKU CORPORATION AND CONSOLIDATED SUBSIDIARIES Consolidated Balance Sheets March 31, 2001 and 2000 Assets Current assets: Cash and cash equivalents... Short-term investments (Note

Financial Statements SEIKAGAKU CORPORATION AND CONSOLIDATED SUBSIDIARIES Consolidated Balance Sheets March 31, 2001 and 2000 Assets Current assets: Cash and cash equivalents... Short-term investments (Note

Chapter 3 the balance sheet and the statement of changes in stockholder. equity

Full Picture for Intermediate Accounting (I) Chapter 3 the balance sheet ASSET LIABILITY Current Chapter 6 cash and receivables Chapter 7/8 inventories Chapter 12 current liabilities and contingencies

Full Picture for Intermediate Accounting (I) Chapter 3 the balance sheet ASSET LIABILITY Current Chapter 6 cash and receivables Chapter 7/8 inventories Chapter 12 current liabilities and contingencies

Investments and International Operations

A Look at This Appendix This appendix focuses on investments in securities. We explain how to identify, account for, and report investments in both debt and equity securities. We also explain accounting

A Look at This Appendix This appendix focuses on investments in securities. We explain how to identify, account for, and report investments in both debt and equity securities. We also explain accounting

INSTITUTE OF ACTUARIES OF INDIA

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 15 th November 2010 Subject CT1 Financial Mathematics Time allowed: Three Hours (15.00 18.00 Hrs) Total Marks: 100 INSTRUCTIONS TO THE CANDIDATES 1. Please

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 15 th November 2010 Subject CT1 Financial Mathematics Time allowed: Three Hours (15.00 18.00 Hrs) Total Marks: 100 INSTRUCTIONS TO THE CANDIDATES 1. Please

Summary of Financial Results for the Three Months Ended June 30, 2015

Summary of Financial Results for the Three Months Ended June 30, 2015 (Non-Consolidated) August 7, 2015 Company name: JAPAN POST BANK Co., Ltd. Website: http://www.jp-bank.japanpost.jp/

Summary of Financial Results for the Three Months Ended June 30, 2015 (Non-Consolidated) August 7, 2015 Company name: JAPAN POST BANK Co., Ltd. Website: http://www.jp-bank.japanpost.jp/

Introduction to Real Estate Investment Appraisal

Introduction to Real Estate Investment Appraisal Maths of Finance Present and Future Values Pat McAllister INVESTMENT APPRAISAL: INTEREST Interest is a reward or rent paid to a lender or investor who has

Introduction to Real Estate Investment Appraisal Maths of Finance Present and Future Values Pat McAllister INVESTMENT APPRAISAL: INTEREST Interest is a reward or rent paid to a lender or investor who has

The Time Value of Money/ Present Values Appendix C

The Time Value Money/ Present Values Appendix C THIS IS ABOUT THE BASICS You should become familiar with the concept present values and the basics how they work using the tables. This is NOT intended to

The Time Value Money/ Present Values Appendix C THIS IS ABOUT THE BASICS You should become familiar with the concept present values and the basics how they work using the tables. This is NOT intended to

SANYO TRADING COMPANY LIMITED. Financial Statements

Financial Statements Year Ended September 30, 2014 English translation from original Japanese-language documents Balance Sheets As of September 30, 2014 ASSETS Current Assets Cash and deposits US$ 18,509,007

Financial Statements Year Ended September 30, 2014 English translation from original Japanese-language documents Balance Sheets As of September 30, 2014 ASSETS Current Assets Cash and deposits US$ 18,509,007

Chapter 11. Long-Term Liabilities Notes, Bonds, and Leases

1 Chapter 11 Long-Term Liabilities Notes, Bonds, and Leases 2 Long-Term Liabilities 3 Economic Consequences of Reporting Long-Term Liabilities Improved credit ratings can lead to lower borrowing costs

1 Chapter 11 Long-Term Liabilities Notes, Bonds, and Leases 2 Long-Term Liabilities 3 Economic Consequences of Reporting Long-Term Liabilities Improved credit ratings can lead to lower borrowing costs

Chapter The Time Value of Money

Chapter The Time Value of Money PPT 9-2 Chapter 9 - Outline Time Value of Money Future Value and Present Value Annuities Time-Value-of-Money Formulas Adjusting for Non-Annual Compounding Compound Interest

Chapter The Time Value of Money PPT 9-2 Chapter 9 - Outline Time Value of Money Future Value and Present Value Annuities Time-Value-of-Money Formulas Adjusting for Non-Annual Compounding Compound Interest

Time Value of Money (TVM)

") BUSI Financial Management Time Value of Money 1 Time Value of Money (TVM) Present value and future value how much is $1 now worth in the future? how much is $1 in the future worth now? Business planning

BUSI Financial Management Time Value of Money 1 Time Value of Money (TVM) Present value and future value how much is $1 now worth in the future? how much is $1 in the future worth now? Business planning

Chapter 6 Contents. Principles Used in Chapter 6 Principle 1: Money Has a Time Value.

Chapter 6 The Time Value of Money: Annuities and Other Topics Chapter 6 Contents Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate present and future values

Chapter 6 The Time Value of Money: Annuities and Other Topics Chapter 6 Contents Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate present and future values

Financial Management Spring 2012

3-1 Financial Management Spring 2012 Week 4 How to Calculate Present Values III 4-1 3-2 Topics Covered More Shortcuts Growing Perpetuities and Annuities How Interest Is Paid and Quoted 4-2 Example 3-3

3-1 Financial Management Spring 2012 Week 4 How to Calculate Present Values III 4-1 3-2 Topics Covered More Shortcuts Growing Perpetuities and Annuities How Interest Is Paid and Quoted 4-2 Example 3-3

CHAPTER 7: NPV AND CAPITAL BUDGETING

CHAPTER 7: NPV AND CAPITAL BUDGETING I. Introduction Assigned problems are 3, 7, 34, 36, and 41. Read Appendix A. The key to analyzing a new project is to think incrementally. We calculate the incremental

CHAPTER 7: NPV AND CAPITAL BUDGETING I. Introduction Assigned problems are 3, 7, 34, 36, and 41. Read Appendix A. The key to analyzing a new project is to think incrementally. We calculate the incremental

Financial Accounting by Michael P. Licata, Ph.D. Course Syllabus and Learning Objectives by Chapter

Financial Accounting by Michael P. Licata, Ph.D. Course Syllabus and Learning Objectives by Chapter Basic Course Description Financial Accounting by Michael P. Licata, Ph.D. is a first accounting course

Financial Accounting by Michael P. Licata, Ph.D. Course Syllabus and Learning Objectives by Chapter Basic Course Description Financial Accounting by Michael P. Licata, Ph.D. is a first accounting course

1 (a) Net present value of investment in new machinery Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 6,084 6,327 6,580 6,844

Net present value of investment in new machinery Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 6,084 6,327 6,580 6,844") Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2013 Answers 1 (a) Net present value of investment in new machinery Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 6,084

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2013 Answers 1 (a) Net present value of investment in new machinery Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 6,084

Income Statement: Results of Operating Performance

Income Statement: Results of Operating Performance 15.501/516 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology Feb 11, 2004 1 Some administrative

Income Statement: Results of Operating Performance 15.501/516 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology Feb 11, 2004 1 Some administrative

CONSOLIDATED STATEMENTS OF OPERATIONS

CONSOLIDATED STATEMENTS OF OPERATIONS For the years ended December 31, (in millions of Canadian dollars except for per share amounts) 2015 2014 Revenue Premiums Gross $ 16,824 $ 15,499 Less: Ceded 6,429

CONSOLIDATED STATEMENTS OF OPERATIONS For the years ended December 31, (in millions of Canadian dollars except for per share amounts) 2015 2014 Revenue Premiums Gross $ 16,824 $ 15,499 Less: Ceded 6,429

3,000 3,000 2,910 2,910 3,000 3,000 2,940 2,940

1. David Company uses the gross method to record its credit purchases, and it uses the periodic inventory system. On July 21, 20D, the company purchased goods that had an invoice price of $ with terms

1. David Company uses the gross method to record its credit purchases, and it uses the periodic inventory system. On July 21, 20D, the company purchased goods that had an invoice price of $ with terms

Finance 3130 Sample Exam 1B Spring 2012

Finance 3130 Sample Exam 1B Spring 2012 True/False Indicate whether the statement is true or false. 1. A firm s income statement provides information as of a point in time, and represents how management

Finance 3130 Sample Exam 1B Spring 2012 True/False Indicate whether the statement is true or false. 1. A firm s income statement provides information as of a point in time, and represents how management

Accrual Accounting Process

Accrual Accounting Process 15.501 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology Feb 17/18, 2004 1 An accountant s functions include Classifying

Accrual Accounting Process 15.501 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology Feb 17/18, 2004 1 An accountant s functions include Classifying

Introduction. 15.501/516 Accounting Spring 2004. Professor Sugata Roychowdhury Sloan School of Management Massachusetts Institute of Technology

Introduction 15.501/516 Accounting Spring 2004 Professor Sugata Roychowdhury Sloan School of Management Massachusetts Institute of Technology Feb 4, 2004 1 Session 1: Agenda Administrative matters Discussion

Introduction 15.501/516 Accounting Spring 2004 Professor Sugata Roychowdhury Sloan School of Management Massachusetts Institute of Technology Feb 4, 2004 1 Session 1: Agenda Administrative matters Discussion

Chapter 4: Time Value of Money

FIN 301 Homework Solution Ch4 Chapter 4: Time Value of Money 1. a. 10,000/(1.10) 10 = 3,855.43 b. 10,000/(1.10) 20 = 1,486.44 c. 10,000/(1.05) 10 = 6,139.13 d. 10,000/(1.05) 20 = 3,768.89 2. a. $100 (1.10)

FIN 301 Homework Solution Ch4 Chapter 4: Time Value of Money 1. a. 10,000/(1.10) 10 = 3,855.43 b. 10,000/(1.10) 20 = 1,486.44 c. 10,000/(1.05) 10 = 6,139.13 d. 10,000/(1.05) 20 = 3,768.89 2. a. $100 (1.10)

SOLUTIONS. Learning Goal 30

S1 Learning Goal 30 Multiple Choice 1. c A corporation wants to reissue treasury stock at a higher price than it paid. In this way, a greater amount of capital can be obtained than was returned to the

S1 Learning Goal 30 Multiple Choice 1. c A corporation wants to reissue treasury stock at a higher price than it paid. In this way, a greater amount of capital can be obtained than was returned to the

Chapter 16. Debentures: An Introduction. Non-current Liabilities. Horngren, Best, Fraser, Willett: Accounting 6e 2010 Pearson Australia.

PowerPoint to accompany Non-current Liabilities Chapter 16 Learning Objectives 1. Account for debentures payable transactions 2. Measure interest expense by the straight line interest method 3. Account

PowerPoint to accompany Non-current Liabilities Chapter 16 Learning Objectives 1. Account for debentures payable transactions 2. Measure interest expense by the straight line interest method 3. Account

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY Answers to Concepts Review and Critical Thinking Questions 1. The four parts are the present value (PV), the future value (FV), the discount

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY Answers to Concepts Review and Critical Thinking Questions 1. The four parts are the present value (PV), the future value (FV), the discount

Consolidated balance sheet

83 Consolidated balance sheet December 31 Non-current assets Goodwill 14 675.1 978.4 Other intangible assets 14 317.4 303.8 Property, plant, and equipment 15 530.7 492.0 Investment in associates 16 2.5

83 Consolidated balance sheet December 31 Non-current assets Goodwill 14 675.1 978.4 Other intangible assets 14 317.4 303.8 Property, plant, and equipment 15 530.7 492.0 Investment in associates 16 2.5

Consolidated Financial Statements

Consolidated Financial Statements For the year ended February 20, 2016 Nitori Holdings Co., Ltd. Consolidated Balance Sheet Nitori Holdings Co., Ltd. and consolidated subsidiaries As at February 20, 2016

Consolidated Financial Statements For the year ended February 20, 2016 Nitori Holdings Co., Ltd. Consolidated Balance Sheet Nitori Holdings Co., Ltd. and consolidated subsidiaries As at February 20, 2016

Investments in Equity Securities. The Internet research exercise examines Cisco System s strategy of growth through acquisitions.

CHAPTER 8 Investments in Equity Securities SYNOPSIS In this chapter, the author discusses investments in equity securities. The discussion is divided into equity securities classified as current and long-term

CHAPTER 8 Investments in Equity Securities SYNOPSIS In this chapter, the author discusses investments in equity securities. The discussion is divided into equity securities classified as current and long-term

Click Here to Buy the Tutorial

FIN 534 Week 4 Quiz 3 (Str) Click Here to Buy the Tutorial http://www.tutorialoutlet.com/fin-534/fin-534-week-4-quiz-3- str/ For more course tutorials visit www.tutorialoutlet.com Which of the following

FIN 534 Week 4 Quiz 3 (Str) Click Here to Buy the Tutorial http://www.tutorialoutlet.com/fin-534/fin-534-week-4-quiz-3- str/ For more course tutorials visit www.tutorialoutlet.com Which of the following

Chapter 8 Accounting for Receivables

Chapter 8 Accounting for Receivables Accounts Receivable Accounts Receivables are current assets. They are usually expected to be collected within 30 days. Allowance Method and Bad Debt Expense 2 methods:

Chapter 8 Accounting for Receivables Accounts Receivable Accounts Receivables are current assets. They are usually expected to be collected within 30 days. Allowance Method and Bad Debt Expense 2 methods:

CHAPTER 18 ASC TOPIC 320: INVESTMENTS DEBT AND EQUITY SECURITIES

CCH brings you... CHAPTER 18 ASC TOPIC 320: INVESTMENTS DEBT AND EQUITY SECURITIES from the Special Edition GAAP Financial Statement Disclosures Manual Visit CCHGroup.com/AASolutions for an overview of

CCH brings you... CHAPTER 18 ASC TOPIC 320: INVESTMENTS DEBT AND EQUITY SECURITIES from the Special Edition GAAP Financial Statement Disclosures Manual Visit CCHGroup.com/AASolutions for an overview of

TIME VALUE OF MONEY. In following we will introduce one of the most important and powerful concepts you will learn in your study of finance;

In following we will introduce one of the most important and powerful concepts you will learn in your study of finance; the time value of money. It is generally acknowledged that money has a time value.

In following we will introduce one of the most important and powerful concepts you will learn in your study of finance; the time value of money. It is generally acknowledged that money has a time value.

IPSAS 2 CASH FLOW STATEMENTS

IPSAS 2 CASH FLOW STATEMENTS Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 7, Cash Flow Statements published

IPSAS 2 CASH FLOW STATEMENTS Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 7, Cash Flow Statements published

Bond Valuation. What is a bond?

Lecture: III 1 What is a bond? Bond Valuation When a corporation wishes to borrow money from the public on a long-term basis, it usually does so by issuing or selling debt securities called bonds. A bond

Lecture: III 1 What is a bond? Bond Valuation When a corporation wishes to borrow money from the public on a long-term basis, it usually does so by issuing or selling debt securities called bonds. A bond

Accounting 303 Exam 2, Chapters 4, 6, and 18

Accounting 303 Exam 2, Chapters 4, 6, and 18 Spring 2012 Name Row I. Multiple Choice Questions. (2 points each, 34 points in total) Read each question carefully and indicate your answer by circling the

Accounting 303 Exam 2, Chapters 4, 6, and 18 Spring 2012 Name Row I. Multiple Choice Questions. (2 points each, 34 points in total) Read each question carefully and indicate your answer by circling the

Accounting for and Presentation of Liabilities

7 Accounting for and Presentation of Liabilities Liabilities are obligations of the entity or, as defined by the FASB, probable future sacrifices of economic benefits arising from present obligations of

7 Accounting for and Presentation of Liabilities Liabilities are obligations of the entity or, as defined by the FASB, probable future sacrifices of economic benefits arising from present obligations of

Review for Exam 1. Instructions: Please read carefully

Review for Exam 1 Instructions: Please read carefully The exam will have 20 multiple choice questions and 4 work problems. Questions in the multiple choice section will be either concept or calculation

Review for Exam 1 Instructions: Please read carefully The exam will have 20 multiple choice questions and 4 work problems. Questions in the multiple choice section will be either concept or calculation

Contribution 787 1,368 1,813 983. Taxable cash flow 682 1,253 1,688 858 Tax liabilities (205) (376) (506) (257)

(376) (506) (257)") Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2012 Answers 1 (a) Calculation of net present value (NPV) As nominal after-tax cash flows are to be discounted, the nominal

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2012 Answers 1 (a) Calculation of net present value (NPV) As nominal after-tax cash flows are to be discounted, the nominal

Japan Vilene Company, Ltd. and Subsidiaries

- 27 - Japan Vilene Company, Ltd. and Subsidiaries Notes to Consolidated Financial Statements Year Ended March 31, 2015 1. BASIS OF PRESENTATION OF CONSOLIDATED FINANCIAL STATEMENTS The accompanying consolidated

- 27 - Japan Vilene Company, Ltd. and Subsidiaries Notes to Consolidated Financial Statements Year Ended March 31, 2015 1. BASIS OF PRESENTATION OF CONSOLIDATED FINANCIAL STATEMENTS The accompanying consolidated

Walk Through Balance Sheet. Chapter 7. Learning Objectives. Learning Objectives 1, 2. Learning Objectives 1, 2. Cash and Receivables.

Chapter 7 Walk Through Balance Sheet Cash and Receivables Chapters 1 6 Accounting cycle: JE, AJE, financial stmts Conceptual framework, GAAP, revenue Time value of money concepts Remaining chapters (ACTG

Chapter 7 Walk Through Balance Sheet Cash and Receivables Chapters 1 6 Accounting cycle: JE, AJE, financial stmts Conceptual framework, GAAP, revenue Time value of money concepts Remaining chapters (ACTG

FIN 3000. Chapter 6. Annuities. Liuren Wu

FIN 3000 Chapter 6 Annuities Liuren Wu Overview 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams Learning objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate

FIN 3000 Chapter 6 Annuities Liuren Wu Overview 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams Learning objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate

Assurance and accounting A Guide to Financial Instruments for Private

june 2011 www.bdo.ca Assurance and accounting A Guide to Financial Instruments for Private Enterprises and Private Sector t-for-profit Organizations For many entities adopting the Accounting Standards

june 2011 www.bdo.ca Assurance and accounting A Guide to Financial Instruments for Private Enterprises and Private Sector t-for-profit Organizations For many entities adopting the Accounting Standards

Module 8: Current and long-term liabilities

Module 8: Current and long-term liabilities Module 8: Current and long-term liabilities Overview In previous modules, you learned how to account for assets. Assets are what a business uses or sells to

Module 8: Current and long-term liabilities Module 8: Current and long-term liabilities Overview In previous modules, you learned how to account for assets. Assets are what a business uses or sells to

Exercise 6 8. Exercise 6 12 PVA = $5,000 x 4.35526* = $21,776

CHAPTER 6: EXERCISES Exercise 6 2 1. FV = $10,000 (2.65330 * ) = $26,533 * Future value of $1: n = 20, i = 5% (from Table 1) 2. FV = $10,000 (1.80611 * ) = $18,061 * Future value of $1: n = 20, i = 3%

CHAPTER 6: EXERCISES Exercise 6 2 1. FV = $10,000 (2.65330 * ) = $26,533 * Future value of $1: n = 20, i = 5% (from Table 1) 2. FV = $10,000 (1.80611 * ) = $18,061 * Future value of $1: n = 20, i = 3%

Data Compilation Financial Data

Data Compilation Financial Data CONTENTS 1. Transition of Significant Management Indicators, etc. Japan Post Group (Consolidated) 122 Japan Post Holdings Co., Ltd. (Non-consolidated) 122 Japan Post Co.,

Data Compilation Financial Data CONTENTS 1. Transition of Significant Management Indicators, etc. Japan Post Group (Consolidated) 122 Japan Post Holdings Co., Ltd. (Non-consolidated) 122 Japan Post Co.,

Foundation review. Introduction. Learning objectives

Foundation review: Introduction Foundation review Introduction Throughout FN1, you will be expected to apply techniques and concepts that you learned in prerequisite courses. The purpose of this foundation

Foundation review: Introduction Foundation review Introduction Throughout FN1, you will be expected to apply techniques and concepts that you learned in prerequisite courses. The purpose of this foundation

Discounted Cash Flow Valuation

BUAD 100x Foundations of Finance Discounted Cash Flow Valuation September 28, 2009 Review Introduction to corporate finance What is corporate finance? What is a corporation? What decision do managers make?

BUAD 100x Foundations of Finance Discounted Cash Flow Valuation September 28, 2009 Review Introduction to corporate finance What is corporate finance? What is a corporation? What decision do managers make?

The Kansai Electric Power Company, Incorporated and Subsidiaries

The Kansai Electric Power Company, Incorporated and Subsidiaries Consolidated Financial Statements for the Years Ended March 31, 2003 and 2002 and for the Six Months Ended September 30, 2003 and 2002 The

The Kansai Electric Power Company, Incorporated and Subsidiaries Consolidated Financial Statements for the Years Ended March 31, 2003 and 2002 and for the Six Months Ended September 30, 2003 and 2002 The

E2-2: Identifying Financing, Investing and Operating Transactions?

E2-2: Identifying Financing, Investing and Operating Transactions? Listed below are eight transactions. In each case, identify whether the transaction is an example of financing, investing or operating

E2-2: Identifying Financing, Investing and Operating Transactions? Listed below are eight transactions. In each case, identify whether the transaction is an example of financing, investing or operating

How To Calculate Financial Leverage Ratio

What Do Short-Term Liquidity Ratios Measure? What Is Working Capital? HOCK international - 2004 1 HOCK international - 2004 2 How Is the Current Ratio Calculated? How Is the Quick Ratio Calculated? HOCK

What Do Short-Term Liquidity Ratios Measure? What Is Working Capital? HOCK international - 2004 1 HOCK international - 2004 2 How Is the Current Ratio Calculated? How Is the Quick Ratio Calculated? HOCK

Cash is King. cash flow is less likely to be affected

Reading 27: Understanding Cash Flow Statements Relevance of Cash Flow The primary purpose of the statement of cash flows (SCF) is to provide: Info about a firm s cash receipts & cash payments during an

Reading 27: Understanding Cash Flow Statements Relevance of Cash Flow The primary purpose of the statement of cash flows (SCF) is to provide: Info about a firm s cash receipts & cash payments during an

Accounting for Income Taxes

Accounting for Income Taxes Objectives:! Understand the differences between tax accounting and financial accounting P Timing: temporary differences P Scope: permanent differences! Understand the effects

Accounting for Income Taxes Objectives:! Understand the differences between tax accounting and financial accounting P Timing: temporary differences P Scope: permanent differences! Understand the effects

CHAE Review. Capital Leases & Forms of Business

CHAE Review Financial Statements, Capital Leases & Forms of Business This is a complete review of the two volume text book, Certified Hospitality Accountant Executive Study Guide, as published by The Educational

CHAE Review Financial Statements, Capital Leases & Forms of Business This is a complete review of the two volume text book, Certified Hospitality Accountant Executive Study Guide, as published by The Educational

Understand the relationship between financial plans and statements.

#2 Budget Development Your Financial Statements and Plans Learning Goals Understand the relationship between financial plans and statements. Prepare a personal balance sheet. Generate a personal income

#2 Budget Development Your Financial Statements and Plans Learning Goals Understand the relationship between financial plans and statements. Prepare a personal balance sheet. Generate a personal income

Corporate Finance Fundamentals [FN1]

![Corporate Finance Fundamentals [FN1]](/thumbs/29/13224229.jpg "Corporate Finance Fundamentals [FN1]") Page 1 of 32 Foundation review Introduction Throughout FN1, you encounter important techniques and concepts that you learned in previous courses in the CGA program of professional studies. The purpose

Page 1 of 32 Foundation review Introduction Throughout FN1, you encounter important techniques and concepts that you learned in previous courses in the CGA program of professional studies. The purpose

ACER INCORPORATED AND SUBSIDIARIES. Consolidated Balance Sheets

Consolidated Balance Sheets June 30, 2015, December 31, 2014, and (June 30, 2015 and 2014 are reviewed, not audited) Assets 2015.6.30 2014.12.31 2014.6.30 Current assets: Cash and cash equivalents $ 36,400,657

Consolidated Balance Sheets June 30, 2015, December 31, 2014, and (June 30, 2015 and 2014 are reviewed, not audited) Assets 2015.6.30 2014.12.31 2014.6.30 Current assets: Cash and cash equivalents $ 36,400,657

1-3Q of FY2014 87.43 78.77 1-3Q of FY2013 74.47 51.74

January 30, 2015 Resona Holdings, Inc. Consolidated Financial Results for the Third Quarter of Fiscal Year 2014 (Nine months ended December 31, 2014/Unaudited) Code number: 8308 Stock

January 30, 2015 Resona Holdings, Inc. Consolidated Financial Results for the Third Quarter of Fiscal Year 2014 (Nine months ended December 31, 2014/Unaudited) Code number: 8308 Stock

DRAFT. Quarterly Savings and Loan Holding Company Report FR 2320. General Instructions Who Must Report. When to Submit the Report

JOBNAME: No Job Name PAGE: 1 SESS: 378 OUTPUT: Mon Nov 21 10:08:25 2011 /frb/bsr/instructs/fr2320/4_dec11_2320-gen_v3 INSTRUCTIONS FOR PREPARATION OF Quarterly Savings and Loan Holding Company Report General

JOBNAME: No Job Name PAGE: 1 SESS: 378 OUTPUT: Mon Nov 21 10:08:25 2011 /frb/bsr/instructs/fr2320/4_dec11_2320-gen_v3 INSTRUCTIONS FOR PREPARATION OF Quarterly Savings and Loan Holding Company Report General

Most economic transactions involve two unrelated entities, although

139-210.ch04rev.qxd 12/2/03 2:57 PM Page 139 CHAPTER4 INTERCOMPANY TRANSACTIONS LEARNING OBJECTIVES After reading this chapter, you should be able to: Understand the different types of intercompany transactions

139-210.ch04rev.qxd 12/2/03 2:57 PM Page 139 CHAPTER4 INTERCOMPANY TRANSACTIONS LEARNING OBJECTIVES After reading this chapter, you should be able to: Understand the different types of intercompany transactions

Ricoh Company, Ltd. INTERIM REPORT (Non consolidated. Half year ended September 30, 2000)

") Ricoh Company, Ltd. INTERIM REPORT (Non consolidated. Half year ended September 30, 2000) *Date of approval for the financial results for the half year ended September 30, 2000, at the Board of Directors'

Ricoh Company, Ltd. INTERIM REPORT (Non consolidated. Half year ended September 30, 2000) *Date of approval for the financial results for the half year ended September 30, 2000, at the Board of Directors'

International Financial Strategies Time Value of Money

International Financial Strategies 1 Future Value and Compounding Future value = cash value of the investment at some point in the future Investing for single period: FV. Future Value PV. Present Value

International Financial Strategies 1 Future Value and Compounding Future value = cash value of the investment at some point in the future Investing for single period: FV. Future Value PV. Present Value

the Time Value of Money

8658d_c06.qxd 11/8/02 11:00 AM Page 251 mac62 mac62:1st Shift: 6 CHAPTER Accounting and the Time Value of Money he Magic of Interest T Sidney Homer, author of A History of Interest Rates, wrote, $1,000

8658d_c06.qxd 11/8/02 11:00 AM Page 251 mac62 mac62:1st Shift: 6 CHAPTER Accounting and the Time Value of Money he Magic of Interest T Sidney Homer, author of A History of Interest Rates, wrote, $1,000

PART III. Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Independent Auditors Report 47

PART III Item 17. Financial Statements Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Schedule: Page Number Independent Auditors Report 47 Consolidated Balance Sheets as of March

PART III Item 17. Financial Statements Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Schedule: Page Number Independent Auditors Report 47 Consolidated Balance Sheets as of March

CHAPTER 6. Accounting and the Time Value of Money. 2. Use of tables. 13, 14 8 1. a. Unknown future amount. 7, 19 1, 5, 13 2, 4, 6, 7, 11

CHAPTER 6 Accounting and the Time Value of Money ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems 1. Present value concepts. 1, 2, 3, 4, 5, 9, 17 2. Use of

CHAPTER 6 Accounting and the Time Value of Money ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems 1. Present value concepts. 1, 2, 3, 4, 5, 9, 17 2. Use of