Output, Inflation, and the Quantity Theory of Money. Ref: Chap 20 p454-57, & Chap 21 p481-89

|

|

|

- Christina Walters

- 7 years ago

- Views:

Transcription

1 Oupu, Inflaion, and he Quaniy Theory of Money Ref: Chap 20 p454-57, & Chap 21 p481-89

2 Aggregae Oupu (Income) Aggregae Oupu is measured by GDP, Gross Domesic Produc: The marke value of final goods and services produced in a counry during a year. Aggregae Income is measured by GNI, Gross Naional Income: Toal income of facors of producion (land, capial, labour) during a year. I4-2

3 Aggregae Oupu (Income) Con d GDP versus GNI GDP and GNI are ofen very abou he same magniude. Quesions: Why do hey differ in magniude, and when are hey he same? When is i beer o use GDP? I4-3

4 Aggregae Oupu (Income) Con d Real versus Nominal GDP: - Disinguish changes in prices from changes in quaniies. - Real GDP uses base-year prices and isolaes change in quaniies. GDP Deflaor=100 x Nominal GDP Real GDP I4-3

5 Aggregae Oupu (Income) Con d Y denoes Aggregae Real Oupu Noe: indicaes oupu over a ime period. e.g. year = 2012 so Y 2012 is aggregae real income from he beginning o he end of he year Noe: Oupu is a flow variable (in unis per period of ime) I4-4

6 P denoes he Aggregae Price Level = The Price Level Aggregae Nominal Oupu Aggregae Real Oupu ( ) Y A price is a level variable, so subscrip corresponds o a specific ime in period, usually he end of period. P, like he CPI, is in dollars per uni quaniy of goods and services. I4-5

7 I4-6 π denoes he (ne) π Inflaion P P P P P P P 1 = Inflaion Rae where " " denoes defined as. The inflaion rae for period is he change beween end of period and end of period -1. This inflaion rae is expressed as a fracion. To express as a percenage muliply by 100. The ex denoes he percenage inflaion: P % P x100 P 1 1

8 I4-7 Proporional change in he price level from he previous period. An increase (decrease) in he price level is referred o as inflaion ( deflaion ). Hyperinflaion describes a very high rae of inflaion, usually 100% or more a year i.e. π 1. Inflaion (Con d) e.g. p322, Bolivia in 1985 Ukraine in 1983 π = 110 π = 50 (FYI: my paper, Currency Transacions Coss and Compeing Fia Currencies explains why domesic money coninues o be used in hyperinflaions.)

9 Inflaion (Con d) e.g. In German in 1923, he rae of inflaion hi percen per monh (prices doubled every wo days). Quesion: A his rae, wha is he annual (ne) inflaion rae? (In your calculaions, firs work ou he gross inflaion rae.) Deflaion corresponds o a negaive inflaion rae: π < 0. - In a deflaion, money increases in value! See Inflaion Propaganda Film (up o 9:25) I4-8

10 v v The Value of Money denoes he Value of Money = 1/ P : in unis of goods and services per dollar e.g. A doubling of he price level resuls in he value of money going down by half. Thus, money buys 50% less goods and services. Ex. Wha is he relaionship beween he rae of inflaion,, and he rae of reurn on money, π v v υ υ v 1, where? 1 I4-9

11 Inflaion-Targeing Policy The Bank of Canada (BOC) follows a inflaion-argeing policy, which aims a 2% inflaion and o keep (core) inflaion wihin bounds of 1% o 3% (see Ch. 20). Ex. Wha are he implicaions of his policy for he pah of prices and he value of money. Sar a = 0 wih P 0 = 1. (FYI: For my evaluaion of inflaion polices see When is Price-Level Targeing a Good Idea? ) I4-10

12 Consumer Price Index in Canada CPI Core CPI

13 Equaion of Exchange M V = P Y Quaniy of Money (M ) x Velociy of Money (V ) = Nominal GDP where Nominal GDP = Price level (P ) x Real Oupu (Y ) I4-12

14 Equaion of Exchange (Con d) M V = P Y implicily defines he Velociy of Money: V PY = M V is he average number of imes a year ha a dollar is spen. Cauion: Be careful o disinguish V, v and. υ I4-13

15 Equaion of Exchange (Con d) M V = P Y implies he approximaion ( ) used in Ch. 21: % M + % V % P + % Y (15) %Money Growh + %Velociy Growh %Inflaion + %Real Growh I gives close o he exac value for small changes. e.g Inflaion = 2%; Real Growh = 2.25%; Velociy Growh= 0.75%. Then (15) implies % M 2%+ 2.25%+0.75% = 5%. Quesion: Find he exac rae of money growh? I4-14

16 Daa: Money Growh and Inflaion I4-15

17 I4-16 Money Growh and Inflaion (con d)

18 I4-17

19 Quaniy Theory of Money The Quaniy Theory of Money combines he Equaion of Exchange M V = P Y wih Classical Dichoomy assumpions. I4-18 The basic Quaniy Theory of Money assumes velociy and oupu are consan and implies: V V P = M = M Y Y The price level is deermined solely by he quaniy of money! (Equaion describes AD.)

20 Quaniy Theory of Money (Con d) In urn, his implies V P = M Y The price level changes solely from changes in he quaniy of money. This implies M M 1 π = m M 1 The inflaion is given by he rae of money growh, m! Ex. Show he seps in deriving π = m. I4-19

21 Quaniy Theory of Money (Con d) The basic Quaniy of Theory of Money predics ha inflaion increases a he same rae as money growh rae. - On a plo he daa would lie on he 45% line. - Helps o explain why high inflaion and money growh go ogeher. - I does no explain why low and moderae inflaion counries fall below he 45% line and hyperinflaion counries lie above he line. I4-20

22 I4-21 Quaniy Theory of Money (con d) Inflaion and Money Growh

23 I4-22 Quaniy Theory of Money (Con d) Classical Dichoomy : Only real forces deermine real variables, and only he money supply deermines he price level. Behavioral assumpions. In he long run: a) Aggregae oupu is a he full-employmen (equilibrium) level; b) Velociy is only deermined by he rae of echnological progress. Thus V and Y are independen of money supply M. Money is said o be neural i.e. money neuraliy. In he basic quaniy heory, which is wihou economic growh or echnological progress, velociy and oupu are assumed consan V = V and Y = Y.

24 Quaniy Theory of Money (Con d) I4-23 One of he oldes and mos successful economic heories. Firs described by David Hume (1752), he famous philosopher, in his paper On Money Formulaed by Irving Fisher, Milon Friedman and Rober Lucas, America s greaes economiss. Appropriaely modified, i can explain why: Low inflaion counries have inflaion raes below he 45% line because of posiive oupu growh. High inflaion counries lie above he 45% line velociy increases as people urn over heir money faser o avoid losing purchasing power.

25 Quaniy Theory of Money Demand (con d) The Quaniy Theory yields a ransacion demand for money, ha does no depend on he ineres rae. For example, wih velociy consan, money D demand, M, increases proporionaely wih nominal income: M D = 1 ( PY ) V Wih his heory, Moneariss (e.g. Milon Friedman) recommend argeing money growh, seing arges S for in order o conrol inflaion (see Ch. 21). M I4-24 S Ex. How would you se M o implemen an inflaionarge pah of 2% inflaion?

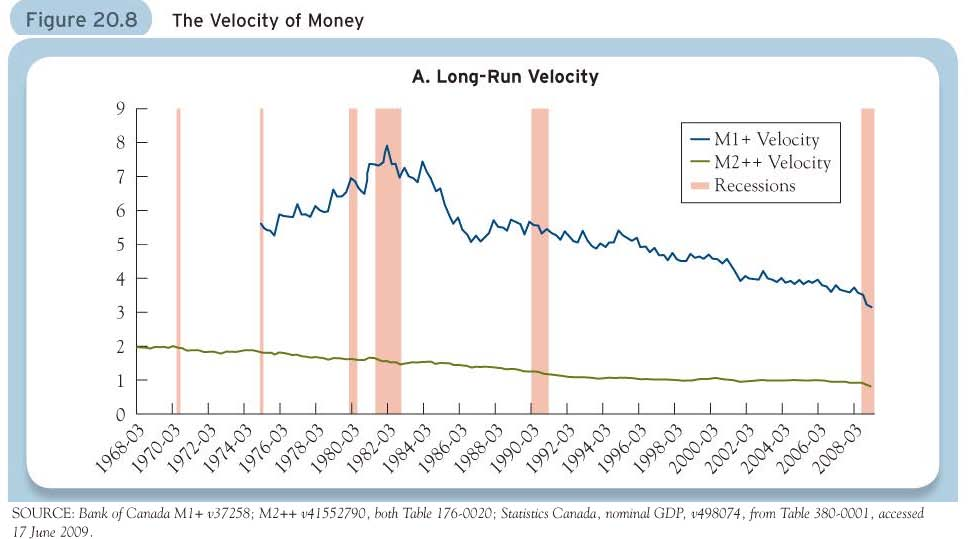

26 Quaniy Theory of Money Demand (con d) I4-25 Canada was he firs counry o adop Milon Friedman s policy of argeing money growh. The policy sared in 1975 bu was considered a failure and abandoned in Velociy became unseady when he BOC ried o arge he money supply. Currenly, he BOC arges inflaion by using an ineres rae, he overnigh rae, raher han money supply o conrol he money marke and inflaion. I is widely believed ha ineres raes affec money demand so ha he Classical Dichoomy doesn hold, a leas in he shor run. Quesion: In he Inflaion Propaganda Film is money neural?

Is he Velociy")

27 I4-26 Quaniy Theory of Money Demand (Con d) Is he Velociy Consan?

11/6/2013. Chapter 14: Dynamic AD-AS. Introduction. Introduction. Keeping track of time. The model s elements

Inroducion Chaper 14: Dynamic D-S dynamic model of aggregae and aggregae supply gives us more insigh ino how he economy works in he shor run. I is a simplified version of a DSGE model, used in cuing-edge

Inroducion Chaper 14: Dynamic D-S dynamic model of aggregae and aggregae supply gives us more insigh ino how he economy works in he shor run. I is a simplified version of a DSGE model, used in cuing-edge

Aggregate Output. Aggregate Output. Topics. Aggregate Output. Aggregate Output. Aggregate Output

Topics (Sandard Measure) GDP vs GPI discussion Macroeconomic Variables (Unemploymen and Inflaion Rae) (naional income and produc accouns, or NIPA) Gross Domesic Produc (GDP) The value of he final goods

Topics (Sandard Measure) GDP vs GPI discussion Macroeconomic Variables (Unemploymen and Inflaion Rae) (naional income and produc accouns, or NIPA) Gross Domesic Produc (GDP) The value of he final goods

BALANCE OF PAYMENTS. First quarter 2008. Balance of payments

BALANCE OF PAYMENTS DATE: 2008-05-30 PUBLISHER: Balance of Paymens and Financial Markes (BFM) Lena Finn + 46 8 506 944 09, lena.finn@scb.se Camilla Bergeling +46 8 506 942 06, camilla.bergeling@scb.se

BALANCE OF PAYMENTS DATE: 2008-05-30 PUBLISHER: Balance of Paymens and Financial Markes (BFM) Lena Finn + 46 8 506 944 09, lena.finn@scb.se Camilla Bergeling +46 8 506 942 06, camilla.bergeling@scb.se

Chapter 6: Business Valuation (Income Approach)

") Chaper 6: Business Valuaion (Income Approach) Cash flow deerminaion is one of he mos criical elemens o a business valuaion. Everyhing may be secondary. If cash flow is high, hen he value is high; if he

Chaper 6: Business Valuaion (Income Approach) Cash flow deerminaion is one of he mos criical elemens o a business valuaion. Everyhing may be secondary. If cash flow is high, hen he value is high; if he

4. International Parity Conditions

4. Inernaional ariy ondiions 4.1 urchasing ower ariy he urchasing ower ariy ( heory is one of he early heories of exchange rae deerminaion. his heory is based on he concep ha he demand for a counry's currency

4. Inernaional ariy ondiions 4.1 urchasing ower ariy he urchasing ower ariy ( heory is one of he early heories of exchange rae deerminaion. his heory is based on he concep ha he demand for a counry's currency

Chapter 7. Response of First-Order RL and RC Circuits

Chaper 7. esponse of Firs-Order L and C Circuis 7.1. The Naural esponse of an L Circui 7.2. The Naural esponse of an C Circui 7.3. The ep esponse of L and C Circuis 7.4. A General oluion for ep and Naural

Chaper 7. esponse of Firs-Order L and C Circuis 7.1. The Naural esponse of an L Circui 7.2. The Naural esponse of an C Circui 7.3. The ep esponse of L and C Circuis 7.4. A General oluion for ep and Naural

CHARGE AND DISCHARGE OF A CAPACITOR

REFERENCES RC Circuis: Elecrical Insrumens: Mos Inroducory Physics exs (e.g. A. Halliday and Resnick, Physics ; M. Sernheim and J. Kane, General Physics.) This Laboraory Manual: Commonly Used Insrumens:

REFERENCES RC Circuis: Elecrical Insrumens: Mos Inroducory Physics exs (e.g. A. Halliday and Resnick, Physics ; M. Sernheim and J. Kane, General Physics.) This Laboraory Manual: Commonly Used Insrumens:

Morningstar Investor Return

Morningsar Invesor Reurn Morningsar Mehodology Paper Augus 31, 2010 2010 Morningsar, Inc. All righs reserved. The informaion in his documen is he propery of Morningsar, Inc. Reproducion or ranscripion

Morningsar Invesor Reurn Morningsar Mehodology Paper Augus 31, 2010 2010 Morningsar, Inc. All righs reserved. The informaion in his documen is he propery of Morningsar, Inc. Reproducion or ranscripion

Lecture Note on the Real Exchange Rate

Lecure Noe on he Real Exchange Rae Barry W. Ickes Fall 2004 0.1 Inroducion The real exchange rae is he criical variable (along wih he rae of ineres) in deermining he capial accoun. As we shall see, his

Lecure Noe on he Real Exchange Rae Barry W. Ickes Fall 2004 0.1 Inroducion The real exchange rae is he criical variable (along wih he rae of ineres) in deermining he capial accoun. As we shall see, his

Economics Honors Exam 2008 Solutions Question 5

Economics Honors Exam 2008 Soluions Quesion 5 (a) (2 poins) Oupu can be decomposed as Y = C + I + G. And we can solve for i by subsiuing in equaions given in he quesion, Y = C + I + G = c 0 + c Y D + I

Economics Honors Exam 2008 Soluions Quesion 5 (a) (2 poins) Oupu can be decomposed as Y = C + I + G. And we can solve for i by subsiuing in equaions given in he quesion, Y = C + I + G = c 0 + c Y D + I

Acceleration Lab Teacher s Guide

Acceleraion Lab Teacher s Guide Objecives:. Use graphs of disance vs. ime and velociy vs. ime o find acceleraion of a oy car.. Observe he relaionship beween he angle of an inclined plane and he acceleraion

Acceleraion Lab Teacher s Guide Objecives:. Use graphs of disance vs. ime and velociy vs. ime o find acceleraion of a oy car.. Observe he relaionship beween he angle of an inclined plane and he acceleraion

Cointegration: The Engle and Granger approach

Coinegraion: The Engle and Granger approach Inroducion Generally one would find mos of he economic variables o be non-saionary I(1) variables. Hence, any equilibrium heories ha involve hese variables require

Coinegraion: The Engle and Granger approach Inroducion Generally one would find mos of he economic variables o be non-saionary I(1) variables. Hence, any equilibrium heories ha involve hese variables require

Chapter 2 Kinematics in One Dimension

Chaper Kinemaics in One Dimension Chaper DESCRIBING MOTION:KINEMATICS IN ONE DIMENSION PREVIEW Kinemaics is he sudy of how hings moe how far (disance and displacemen), how fas (speed and elociy), and how

Chaper Kinemaics in One Dimension Chaper DESCRIBING MOTION:KINEMATICS IN ONE DIMENSION PREVIEW Kinemaics is he sudy of how hings moe how far (disance and displacemen), how fas (speed and elociy), and how

Duration and Convexity ( ) 20 = Bond B has a maturity of 5 years and also has a required rate of return of 10%. Its price is $613.

20 = Bond B has a maturity of 5 years and also has a required rate of return of 10%. Its price is $613.") Graduae School of Business Adminisraion Universiy of Virginia UVA-F-38 Duraion and Convexiy he price of a bond is a funcion of he promised paymens and he marke required rae of reurn. Since he promised

Graduae School of Business Adminisraion Universiy of Virginia UVA-F-38 Duraion and Convexiy he price of a bond is a funcion of he promised paymens and he marke required rae of reurn. Since he promised

A Note on Using the Svensson procedure to estimate the risk free rate in corporate valuation

A Noe on Using he Svensson procedure o esimae he risk free rae in corporae valuaion By Sven Arnold, Alexander Lahmann and Bernhard Schwezler Ocober 2011 1. The risk free ineres rae in corporae valuaion

A Noe on Using he Svensson procedure o esimae he risk free rae in corporae valuaion By Sven Arnold, Alexander Lahmann and Bernhard Schwezler Ocober 2011 1. The risk free ineres rae in corporae valuaion

Education & Human Resource Development

Educaion & Human Resource Developmen New Research Adminisraion Srucure Rerea June 23 & 24, 2006 Where is he Caribbean in Relaion o Oher Counries? Office of he Vice Presiden for Research and Compliance

Educaion & Human Resource Developmen New Research Adminisraion Srucure Rerea June 23 & 24, 2006 Where is he Caribbean in Relaion o Oher Counries? Office of he Vice Presiden for Research and Compliance

The Real Business Cycle paradigm. The RBC model emphasizes supply (technology) disturbances as the main source of

disturbances as the main source of") Prof. Harris Dellas Advanced Macroeconomics Winer 2001/01 The Real Business Cycle paradigm The RBC model emphasizes supply (echnology) disurbances as he main source of macroeconomic flucuaions in a world

Prof. Harris Dellas Advanced Macroeconomics Winer 2001/01 The Real Business Cycle paradigm The RBC model emphasizes supply (echnology) disurbances as he main source of macroeconomic flucuaions in a world

Name: Algebra II Review for Quiz #13 Exponential and Logarithmic Functions including Modeling

Name: Algebra II Review for Quiz #13 Exponenial and Logarihmic Funcions including Modeling TOPICS: -Solving Exponenial Equaions (The Mehod of Common Bases) -Solving Exponenial Equaions (Using Logarihms)

Name: Algebra II Review for Quiz #13 Exponenial and Logarihmic Funcions including Modeling TOPICS: -Solving Exponenial Equaions (The Mehod of Common Bases) -Solving Exponenial Equaions (Using Logarihms)

Chapter 8: Regression with Lagged Explanatory Variables

Chaper 8: Regression wih Lagged Explanaory Variables Time series daa: Y for =1,..,T End goal: Regression model relaing a dependen variable o explanaory variables. Wih ime series new issues arise: 1. One

Chaper 8: Regression wih Lagged Explanaory Variables Time series daa: Y for =1,..,T End goal: Regression model relaing a dependen variable o explanaory variables. Wih ime series new issues arise: 1. One

MTH6121 Introduction to Mathematical Finance Lesson 5

26 MTH6121 Inroducion o Mahemaical Finance Lesson 5 Conens 2.3 Brownian moion wih drif........................... 27 2.4 Geomeric Brownian moion........................... 28 2.5 Convergence of random

26 MTH6121 Inroducion o Mahemaical Finance Lesson 5 Conens 2.3 Brownian moion wih drif........................... 27 2.4 Geomeric Brownian moion........................... 28 2.5 Convergence of random

PROFIT TEST MODELLING IN LIFE ASSURANCE USING SPREADSHEETS PART ONE

Profi Tes Modelling in Life Assurance Using Spreadshees PROFIT TEST MODELLING IN LIFE ASSURANCE USING SPREADSHEETS PART ONE Erik Alm Peer Millingon 2004 Profi Tes Modelling in Life Assurance Using Spreadshees

Profi Tes Modelling in Life Assurance Using Spreadshees PROFIT TEST MODELLING IN LIFE ASSURANCE USING SPREADSHEETS PART ONE Erik Alm Peer Millingon 2004 Profi Tes Modelling in Life Assurance Using Spreadshees

Analysis of tax effects on consolidated household/government debts of a nation in a monetary union under classical dichotomy

MPRA Munich Personal RePEc Archive Analysis of ax effecs on consolidaed household/governmen debs of a naion in a moneary union under classical dichoomy Minseong Kim 8 April 016 Online a hps://mpra.ub.uni-muenchen.de/71016/

MPRA Munich Personal RePEc Archive Analysis of ax effecs on consolidaed household/governmen debs of a naion in a moneary union under classical dichoomy Minseong Kim 8 April 016 Online a hps://mpra.ub.uni-muenchen.de/71016/

Estimating Time-Varying Equity Risk Premium The Japanese Stock Market 1980-2012

Norhfield Asia Research Seminar Hong Kong, November 19, 2013 Esimaing Time-Varying Equiy Risk Premium The Japanese Sock Marke 1980-2012 Ibboson Associaes Japan Presiden Kasunari Yamaguchi, PhD/CFA/CMA

Norhfield Asia Research Seminar Hong Kong, November 19, 2013 Esimaing Time-Varying Equiy Risk Premium The Japanese Sock Marke 1980-2012 Ibboson Associaes Japan Presiden Kasunari Yamaguchi, PhD/CFA/CMA

II.1. Debt reduction and fiscal multipliers. dbt da dpbal da dg. bal

Quarerly Repor on he Euro Area 3/202 II.. Deb reducion and fiscal mulipliers The deerioraion of public finances in he firs years of he crisis has led mos Member Saes o adop sizeable consolidaion packages.

Quarerly Repor on he Euro Area 3/202 II.. Deb reducion and fiscal mulipliers The deerioraion of public finances in he firs years of he crisis has led mos Member Saes o adop sizeable consolidaion packages.

Newton s Laws of Motion

Newon s Laws of Moion MS4414 Theoreical Mechanics Firs Law velociy. In he absence of exernal forces, a body moves in a sraigh line wih consan F = 0 = v = cons. Khan Academy Newon I. Second Law body. The

Newon s Laws of Moion MS4414 Theoreical Mechanics Firs Law velociy. In he absence of exernal forces, a body moves in a sraigh line wih consan F = 0 = v = cons. Khan Academy Newon I. Second Law body. The

Individual Health Insurance April 30, 2008 Pages 167-170

Individual Healh Insurance April 30, 2008 Pages 167-170 We have received feedback ha his secion of he e is confusing because some of he defined noaion is inconsisen wih comparable life insurance reserve

Individual Healh Insurance April 30, 2008 Pages 167-170 We have received feedback ha his secion of he e is confusing because some of he defined noaion is inconsisen wih comparable life insurance reserve

Random Walk in 1-D. 3 possible paths x vs n. -5 For our random walk, we assume the probabilities p,q do not depend on time (n) - stationary

- stationary") Random Walk in -D Random walks appear in many cones: diffusion is a random walk process undersanding buffering, waiing imes, queuing more generally he heory of sochasic processes gambling choosing he bes

Random Walk in -D Random walks appear in many cones: diffusion is a random walk process undersanding buffering, waiing imes, queuing more generally he heory of sochasic processes gambling choosing he bes

Chapter 9 Bond Prices and Yield

Chaper 9 Bond Prices and Yield Deb Classes: Paymen ype A securiy obligaing issuer o pay ineress and principal o he holder on specified daes, Coupon rae or ineres rae, e.g. 4%, 5 3/4%, ec. Face, par value

Chaper 9 Bond Prices and Yield Deb Classes: Paymen ype A securiy obligaing issuer o pay ineress and principal o he holder on specified daes, Coupon rae or ineres rae, e.g. 4%, 5 3/4%, ec. Face, par value

The Greek financial crisis: growing imbalances and sovereign spreads. Heather D. Gibson, Stephan G. Hall and George S. Tavlas

The Greek financial crisis: growing imbalances and sovereign spreads Heaher D. Gibson, Sephan G. Hall and George S. Tavlas The enry The enry of Greece ino he Eurozone in 2001 produced a dividend in he

The Greek financial crisis: growing imbalances and sovereign spreads Heaher D. Gibson, Sephan G. Hall and George S. Tavlas The enry The enry of Greece ino he Eurozone in 2001 produced a dividend in he

AP Calculus BC 2010 Scoring Guidelines

AP Calculus BC Scoring Guidelines The College Board The College Board is a no-for-profi membership associaion whose mission is o connec sudens o college success and opporuniy. Founded in, he College Board

AP Calculus BC Scoring Guidelines The College Board The College Board is a no-for-profi membership associaion whose mission is o connec sudens o college success and opporuniy. Founded in, he College Board

AP Calculus AB 2013 Scoring Guidelines

AP Calculus AB 1 Scoring Guidelines The College Board The College Board is a mission-driven no-for-profi organizaion ha connecs sudens o college success and opporuniy. Founded in 19, he College Board was

AP Calculus AB 1 Scoring Guidelines The College Board The College Board is a mission-driven no-for-profi organizaion ha connecs sudens o college success and opporuniy. Founded in 19, he College Board was

Chapter 8 Student Lecture Notes 8-1

Chaper Suden Lecure Noes - Chaper Goals QM: Business Saisics Chaper Analyzing and Forecasing -Series Daa Afer compleing his chaper, you should be able o: Idenify he componens presen in a ime series Develop

Chaper Suden Lecure Noes - Chaper Goals QM: Business Saisics Chaper Analyzing and Forecasing -Series Daa Afer compleing his chaper, you should be able o: Idenify he componens presen in a ime series Develop

BALANCE OF PAYMENTS AND FINANCIAL MA REPORT 2015. All officiell statistik finns på: www.scb.se Statistikservice: tfn 08-506 948 01

RKET BALANCE OF PAYMENTS AND FINANCIAL MA REPORT 2015 All officiell saisik finns på: www.scb.se Saisikservice: fn 08-506 948 01 All official saisics can be found a: www.scb.se Saisics service, phone +46

RKET BALANCE OF PAYMENTS AND FINANCIAL MA REPORT 2015 All officiell saisik finns på: www.scb.se Saisikservice: fn 08-506 948 01 All official saisics can be found a: www.scb.se Saisics service, phone +46

I. Basic Concepts (Ch. 1-4)

") (Ch. 1-4) A. Real vs. Financial Asses (Ch 1.2) Real asses (buildings, machinery, ec.) appear on he asse side of he balance shee. Financial asses (bonds, socks) appear on boh sides of he balance shee. Creaing

(Ch. 1-4) A. Real vs. Financial Asses (Ch 1.2) Real asses (buildings, machinery, ec.) appear on he asse side of he balance shee. Financial asses (bonds, socks) appear on boh sides of he balance shee. Creaing

Present Value Methodology

Presen Value Mehodology Econ 422 Invesmen, Capial & Finance Universiy of Washingon Eric Zivo Las updaed: April 11, 2010 Presen Value Concep Wealh in Fisher Model: W = Y 0 + Y 1 /(1+r) The consumer/producer

Presen Value Mehodology Econ 422 Invesmen, Capial & Finance Universiy of Washingon Eric Zivo Las updaed: April 11, 2010 Presen Value Concep Wealh in Fisher Model: W = Y 0 + Y 1 /(1+r) The consumer/producer

MACROECONOMIC FORECASTS AT THE MOF A LOOK INTO THE REAR VIEW MIRROR

MACROECONOMIC FORECASTS AT THE MOF A LOOK INTO THE REAR VIEW MIRROR The firs experimenal publicaion, which summarised pas and expeced fuure developmen of basic economic indicaors, was published by he Minisry

MACROECONOMIC FORECASTS AT THE MOF A LOOK INTO THE REAR VIEW MIRROR The firs experimenal publicaion, which summarised pas and expeced fuure developmen of basic economic indicaors, was published by he Minisry

Vector Autoregressions (VARs): Operational Perspectives

: Operational Perspectives") Vecor Auoregressions (VARs): Operaional Perspecives Primary Source: Sock, James H., and Mark W. Wason, Vecor Auoregressions, Journal of Economic Perspecives, Vol. 15 No. 4 (Fall 2001), 101-115. Macroeconomericians

Vecor Auoregressions (VARs): Operaional Perspecives Primary Source: Sock, James H., and Mark W. Wason, Vecor Auoregressions, Journal of Economic Perspecives, Vol. 15 No. 4 (Fall 2001), 101-115. Macroeconomericians

Chapter Four: Methodology

Chaper Four: Mehodology 1 Assessmen of isk Managemen Sraegy Comparing Is Cos of isks 1.1 Inroducion If we wan o choose a appropriae risk managemen sraegy, no only we should idenify he influence ha risks

Chaper Four: Mehodology 1 Assessmen of isk Managemen Sraegy Comparing Is Cos of isks 1.1 Inroducion If we wan o choose a appropriae risk managemen sraegy, no only we should idenify he influence ha risks

DYNAMIC MODELS FOR VALUATION OF WRONGFUL DEATH PAYMENTS

DYNAMIC MODELS FOR VALUATION OF WRONGFUL DEATH PAYMENTS Hong Mao, Shanghai Second Polyechnic Universiy Krzyszof M. Osaszewski, Illinois Sae Universiy Youyu Zhang, Fudan Universiy ABSTRACT Liigaion, exper

DYNAMIC MODELS FOR VALUATION OF WRONGFUL DEATH PAYMENTS Hong Mao, Shanghai Second Polyechnic Universiy Krzyszof M. Osaszewski, Illinois Sae Universiy Youyu Zhang, Fudan Universiy ABSTRACT Liigaion, exper

CLASSIFICATION OF REINSURANCE IN LIFE INSURANCE

CLASSIFICATION OF REINSURANCE IN LIFE INSURANCE Kaarína Sakálová 1. Classificaions of reinsurance There are many differen ways in which reinsurance may be classified or disinguished. We will discuss briefly

CLASSIFICATION OF REINSURANCE IN LIFE INSURANCE Kaarína Sakálová 1. Classificaions of reinsurance There are many differen ways in which reinsurance may be classified or disinguished. We will discuss briefly

The Time Value of Money

THE TIME VALUE OF MONEY CALCULATING PRESENT AND FUTURE VALUES Fuure Value: FV = PV 0 ( + r) Presen Value: PV 0 = FV ------------------------------- ( + r) THE EFFECTS OF COMPOUNDING The effecs/benefis

THE TIME VALUE OF MONEY CALCULATING PRESENT AND FUTURE VALUES Fuure Value: FV = PV 0 ( + r) Presen Value: PV 0 = FV ------------------------------- ( + r) THE EFFECTS OF COMPOUNDING The effecs/benefis

Answer, Key Homework 2 David McIntyre 45123 Mar 25, 2004 1

Answer, Key Homework 2 Daid McInyre 4123 Mar 2, 2004 1 This prin-ou should hae 1 quesions. Muliple-choice quesions may coninue on he ne column or page find all choices before making your selecion. The

Answer, Key Homework 2 Daid McInyre 4123 Mar 2, 2004 1 This prin-ou should hae 1 quesions. Muliple-choice quesions may coninue on he ne column or page find all choices before making your selecion. The

The effects of stock market movements on consumption and investment: does the shock matter?

The effecs of sock marke movemens on consumpion and invesmen: does he shock maer? Sephen Millard and John Power Working paper no. 236 Bank of England, Threadneedle Sree, London, EC2R 8AH. E-mail: sephen.millard@bankofengland.co.uk

The effecs of sock marke movemens on consumpion and invesmen: does he shock maer? Sephen Millard and John Power Working paper no. 236 Bank of England, Threadneedle Sree, London, EC2R 8AH. E-mail: sephen.millard@bankofengland.co.uk

Equities: Positions and Portfolio Returns

Foundaions of Finance: Equiies: osiions and orfolio Reurns rof. Alex Shapiro Lecure oes 4b Equiies: osiions and orfolio Reurns I. Readings and Suggesed racice roblems II. Sock Transacions Involving Credi

Foundaions of Finance: Equiies: osiions and orfolio Reurns rof. Alex Shapiro Lecure oes 4b Equiies: osiions and orfolio Reurns I. Readings and Suggesed racice roblems II. Sock Transacions Involving Credi

Pulse-Width Modulation Inverters

SECTION 3.6 INVERTERS 189 Pulse-Widh Modulaion Inverers Pulse-widh modulaion is he process of modifying he widh of he pulses in a pulse rain in direc proporion o a small conrol signal; he greaer he conrol

SECTION 3.6 INVERTERS 189 Pulse-Widh Modulaion Inverers Pulse-widh modulaion is he process of modifying he widh of he pulses in a pulse rain in direc proporion o a small conrol signal; he greaer he conrol

Chapter 4: Exponential and Logarithmic Functions

Chaper 4: Eponenial and Logarihmic Funcions Secion 4.1 Eponenial Funcions... 15 Secion 4. Graphs of Eponenial Funcions... 3 Secion 4.3 Logarihmic Funcions... 4 Secion 4.4 Logarihmic Properies... 53 Secion

Chaper 4: Eponenial and Logarihmic Funcions Secion 4.1 Eponenial Funcions... 15 Secion 4. Graphs of Eponenial Funcions... 3 Secion 4.3 Logarihmic Funcions... 4 Secion 4.4 Logarihmic Properies... 53 Secion

INTRODUCTION TO EMAIL MARKETING PERSONALIZATION. How to increase your sales with personalized triggered emails

INTRODUCTION TO EMAIL MARKETING PERSONALIZATION How o increase your sales wih personalized riggered emails ECOMMERCE TRIGGERED EMAILS BEST PRACTICES Triggered emails are generaed in real ime based on each

INTRODUCTION TO EMAIL MARKETING PERSONALIZATION How o increase your sales wih personalized riggered emails ECOMMERCE TRIGGERED EMAILS BEST PRACTICES Triggered emails are generaed in real ime based on each

Forecasting, Ordering and Stock- Holding for Erratic Demand

ISF 2002 23 rd o 26 h June 2002 Forecasing, Ordering and Sock- Holding for Erraic Demand Andrew Eaves Lancaser Universiy / Andalus Soluions Limied Inroducion Erraic and slow-moving demand Demand classificaion

ISF 2002 23 rd o 26 h June 2002 Forecasing, Ordering and Sock- Holding for Erraic Demand Andrew Eaves Lancaser Universiy / Andalus Soluions Limied Inroducion Erraic and slow-moving demand Demand classificaion

Interest Rates, Inflation, and Federal Reserve Policy Since 1980. Peter N. Ireland * Boston College. March 1999

Ineres Raes, Inflaion, and Federal Reserve Policy Since 98 Peer N. Ireland * Boson College March 999 Absrac: This paper characerizes Federal Reserve policy since 98 as one ha acively manages shor-erm nominal

Ineres Raes, Inflaion, and Federal Reserve Policy Since 98 Peer N. Ireland * Boson College March 999 Absrac: This paper characerizes Federal Reserve policy since 98 as one ha acively manages shor-erm nominal

Mathematics in Pharmacokinetics What and Why (A second attempt to make it clearer)

") Mahemaics in Pharmacokineics Wha and Why (A second aemp o make i clearer) We have used equaions for concenraion () as a funcion of ime (). We will coninue o use hese equaions since he plasma concenraions

Mahemaics in Pharmacokineics Wha and Why (A second aemp o make i clearer) We have used equaions for concenraion () as a funcion of ime (). We will coninue o use hese equaions since he plasma concenraions

Return Calculation of U.S. Treasury Constant Maturity Indices

Reurn Calculaion of US Treasur Consan Mauri Indices Morningsar Mehodolog Paper Sepeber 30 008 008 Morningsar Inc All righs reserved The inforaion in his docuen is he proper of Morningsar Inc Reproducion

Reurn Calculaion of US Treasur Consan Mauri Indices Morningsar Mehodolog Paper Sepeber 30 008 008 Morningsar Inc All righs reserved The inforaion in his docuen is he proper of Morningsar Inc Reproducion

Why Did the Demand for Cash Decrease Recently in Korea?

Why Did he Demand for Cash Decrease Recenly in Korea? Byoung Hark Yoo Bank of Korea 26. 5 Absrac We explores why cash demand have decreased recenly in Korea. The raio of cash o consumpion fell o 4.7% in

Why Did he Demand for Cash Decrease Recenly in Korea? Byoung Hark Yoo Bank of Korea 26. 5 Absrac We explores why cash demand have decreased recenly in Korea. The raio of cash o consumpion fell o 4.7% in

The Grantor Retained Annuity Trust (GRAT)

") WEALTH ADVISORY Esae Planning Sraegies for closely-held, family businesses The Granor Reained Annuiy Trus (GRAT) An efficien wealh ransfer sraegy, paricularly in a low ineres rae environmen Family business

WEALTH ADVISORY Esae Planning Sraegies for closely-held, family businesses The Granor Reained Annuiy Trus (GRAT) An efficien wealh ransfer sraegy, paricularly in a low ineres rae environmen Family business

9. Capacitor and Resistor Circuits

ElecronicsLab9.nb 1 9. Capacior and Resisor Circuis Inroducion hus far we have consider resisors in various combinaions wih a power supply or baery which provide a consan volage source or direc curren

ElecronicsLab9.nb 1 9. Capacior and Resisor Circuis Inroducion hus far we have consider resisors in various combinaions wih a power supply or baery which provide a consan volage source or direc curren

cooking trajectory boiling water B (t) microwave 0 2 4 6 8 101214161820 time t (mins)

microwave 0 2 4 6 8 101214161820 time t (mins)") Alligaor egg wih calculus We have a large alligaor egg jus ou of he fridge (1 ) which we need o hea o 9. Now here are wo accepable mehods for heaing alligaor eggs, one is o immerse hem in boiling waer

Alligaor egg wih calculus We have a large alligaor egg jus ou of he fridge (1 ) which we need o hea o 9. Now here are wo accepable mehods for heaing alligaor eggs, one is o immerse hem in boiling waer

Long-Run Stock Returns: Participating in the Real Economy

Long-Run Sock Reurns: Paricipaing in he Real Economy Roger G. Ibboson and Peng Chen In he sudy repored here, we esimaed he forward-looking long-erm equiy risk premium by exrapolaing he way i has paricipaed

Long-Run Sock Reurns: Paricipaing in he Real Economy Roger G. Ibboson and Peng Chen In he sudy repored here, we esimaed he forward-looking long-erm equiy risk premium by exrapolaing he way i has paricipaed

Diagnostic Examination

Diagnosic Examinaion TOPIC XV: ENGINEERING ECONOMICS TIME LIMIT: 45 MINUTES 1. Approximaely how many years will i ake o double an invesmen a a 6% effecive annual rae? (A) 10 yr (B) 12 yr (C) 15 yr (D)

Diagnosic Examinaion TOPIC XV: ENGINEERING ECONOMICS TIME LIMIT: 45 MINUTES 1. Approximaely how many years will i ake o double an invesmen a a 6% effecive annual rae? (A) 10 yr (B) 12 yr (C) 15 yr (D)

Table of contents Chapter 1 Interest rates and factors Chapter 2 Level annuities Chapter 3 Varying annuities

Table of conens Chaper 1 Ineres raes and facors 1 1.1 Ineres 2 1.2 Simple ineres 4 1.3 Compound ineres 6 1.4 Accumulaed value 10 1.5 Presen value 11 1.6 Rae of discoun 13 1.7 Consan force of ineres 17

Table of conens Chaper 1 Ineres raes and facors 1 1.1 Ineres 2 1.2 Simple ineres 4 1.3 Compound ineres 6 1.4 Accumulaed value 10 1.5 Presen value 11 1.6 Rae of discoun 13 1.7 Consan force of ineres 17

Investigating the Relationship between Exchange Rate and Inflation Targeting

Applied Mahemaical Sciences, Vol. 6, 2012, no. 32, 1571-1583 Invesigaing he Relaionship beween Exchange Rae and Inflaion Targeing Siok Kun Sek School of Mahemaical Sciences Universii Sains Malasia 11800

Applied Mahemaical Sciences, Vol. 6, 2012, no. 32, 1571-1583 Invesigaing he Relaionship beween Exchange Rae and Inflaion Targeing Siok Kun Sek School of Mahemaical Sciences Universii Sains Malasia 11800

Working Paper No. 482. Net Intergenerational Transfers from an Increase in Social Security Benefits

Working Paper No. 482 Ne Inergeneraional Transfers from an Increase in Social Securiy Benefis By Li Gan Texas A&M and NBER Guan Gong Shanghai Universiy of Finance and Economics Michael Hurd RAND Corporaion

Working Paper No. 482 Ne Inergeneraional Transfers from an Increase in Social Securiy Benefis By Li Gan Texas A&M and NBER Guan Gong Shanghai Universiy of Finance and Economics Michael Hurd RAND Corporaion

Hedging with Forwards and Futures

Hedging wih orwards and uures Hedging in mos cases is sraighforward. You plan o buy 10,000 barrels of oil in six monhs and you wish o eliminae he price risk. If you ake he buy-side of a forward/fuures

Hedging wih orwards and uures Hedging in mos cases is sraighforward. You plan o buy 10,000 barrels of oil in six monhs and you wish o eliminae he price risk. If you ake he buy-side of a forward/fuures

Outline. Role of Aggregate Planning. Role of Aggregate Planning. Logistics and Supply Chain Management. Aggregate Planning

Logisics and upply Chain Managemen Aggregae Planning 1 Ouline Role of aggregae planning in a supply chain The aggregae planning problem Aggregae planning sraegies mplemening aggregae planning in pracice

Logisics and upply Chain Managemen Aggregae Planning 1 Ouline Role of aggregae planning in a supply chain The aggregae planning problem Aggregae planning sraegies mplemening aggregae planning in pracice

Chapter 1.6 Financial Management

Chaper 1.6 Financial Managemen Par I: Objecive ype quesions and answers 1. Simple pay back period is equal o: a) Raio of Firs cos/ne yearly savings b) Raio of Annual gross cash flow/capial cos n c) = (1

Chaper 1.6 Financial Managemen Par I: Objecive ype quesions and answers 1. Simple pay back period is equal o: a) Raio of Firs cos/ne yearly savings b) Raio of Annual gross cash flow/capial cos n c) = (1

Can Austerity Be Self-defeating?

DOI: 0.007/s07-0-0-7 Auseriy Can Auseriy Be Self-defeaing? Wih European governmens cuing back on spending, many are asking wheher his could make maers worse. In he UK for insance, recen OECD esimaes sugges

DOI: 0.007/s07-0-0-7 Auseriy Can Auseriy Be Self-defeaing? Wih European governmens cuing back on spending, many are asking wheher his could make maers worse. In he UK for insance, recen OECD esimaes sugges

Appendix A: Area. 1 Find the radius of a circle that has circumference 12 inches.

Appendi A: Area worked-ou s o Odd-Numbered Eercises Do no read hese worked-ou s before aemping o do he eercises ourself. Oherwise ou ma mimic he echniques shown here wihou undersanding he ideas. Bes wa

Appendi A: Area worked-ou s o Odd-Numbered Eercises Do no read hese worked-ou s before aemping o do he eercises ourself. Oherwise ou ma mimic he echniques shown here wihou undersanding he ideas. Bes wa

Information technology and economic growth in Canada and the U.S.

Canada U.S. Economic Growh Informaion echnology and economic growh in Canada and he U.S. Informaion and communicaion echnology was he larges conribuor o growh wihin capial services for boh Canada and he

Canada U.S. Economic Growh Informaion echnology and economic growh in Canada and he U.S. Informaion and communicaion echnology was he larges conribuor o growh wihin capial services for boh Canada and he

Permutations and Combinations

Permuaions and Combinaions Combinaorics Copyrigh Sandards 006, Tes - ANSWERS Barry Mabillard. 0 www.mah0s.com 1. Deermine he middle erm in he expansion of ( a b) To ge he k-value for he middle erm, divide

Permuaions and Combinaions Combinaorics Copyrigh Sandards 006, Tes - ANSWERS Barry Mabillard. 0 www.mah0s.com 1. Deermine he middle erm in he expansion of ( a b) To ge he k-value for he middle erm, divide

INFLATION AND UNEMPLOYMENT IN ICELAND IN THE LIGHT OF NATURAL-RATE THEORY

CENTRAL BANK OF ICELAND WORKING PAPERS No. 17 INFLATION AND UNEMPLOYMENT IN ICELAND IN THE LIGHT OF NATURAL-RATE THEORY by Gylfi Zoega March 22 CENTRAL BANK OF ICELAND Economics Deparmen Cenral Bank of

CENTRAL BANK OF ICELAND WORKING PAPERS No. 17 INFLATION AND UNEMPLOYMENT IN ICELAND IN THE LIGHT OF NATURAL-RATE THEORY by Gylfi Zoega March 22 CENTRAL BANK OF ICELAND Economics Deparmen Cenral Bank of

The Euro. Optimal Currency Areas. The Problem. The Euro. The Proposal. The Proposal

The Euro E Opial Currency Areas ( σ ( r The Euro is an exaple of a currency union. The naions abandoned independen oneary auhoriy o ge a coon currency. Lecures in Macroeconoics- Charles W. Upon Opial Currency

The Euro E Opial Currency Areas ( σ ( r The Euro is an exaple of a currency union. The naions abandoned independen oneary auhoriy o ge a coon currency. Lecures in Macroeconoics- Charles W. Upon Opial Currency

CRISES AND THE FLEXIBLE PRICE MONETARY MODEL. Sarantis Kalyvitis

CRISES AND THE FLEXIBLE PRICE MONETARY MODEL Saranis Kalyviis Currency Crises In fixed exchange rae regimes, counries rarely abandon he regime volunarily. In mos cases, raders (or speculaors) exchange

CRISES AND THE FLEXIBLE PRICE MONETARY MODEL Saranis Kalyviis Currency Crises In fixed exchange rae regimes, counries rarely abandon he regime volunarily. In mos cases, raders (or speculaors) exchange

AP Calculus AB 2007 Scoring Guidelines

AP Calculus AB 7 Scoring Guidelines The College Board: Connecing Sudens o College Success The College Board is a no-for-profi membership associaion whose mission is o connec sudens o college success and

AP Calculus AB 7 Scoring Guidelines The College Board: Connecing Sudens o College Success The College Board is a no-for-profi membership associaion whose mission is o connec sudens o college success and

Energy prices and business cycles: Lessons from a simulated small open economy. Torsten Schmidt, RWI Essen * Tobias Zimmermann, RWI Essen *

Energy prices and business cycles: Lessons from a simulaed small open economy model Torsen Schmid, RWI Essen * Tobias Zimmermann, RWI Essen * Preliminary Version, Ocober 2008 Absrac Despie energy price

Energy prices and business cycles: Lessons from a simulaed small open economy model Torsen Schmid, RWI Essen * Tobias Zimmermann, RWI Essen * Preliminary Version, Ocober 2008 Absrac Despie energy price

The Determinants of Trade Credit: Vietnam Experience

Proceedings of he Second Asia-Pacific Conference on Global Business, Economics, Finance and Social Sciences (AP15Vienam Conference) ISBN: 978-1-63415-833-6 Danang, Vienam, 10-12 July 2015 Paper ID: V536

Proceedings of he Second Asia-Pacific Conference on Global Business, Economics, Finance and Social Sciences (AP15Vienam Conference) ISBN: 978-1-63415-833-6 Danang, Vienam, 10-12 July 2015 Paper ID: V536

Debt Accumulation, Debt Reduction, and Debt Spillovers in Canada, 1974-98*

Deb Accumulaion, Deb Reducion, and Deb Spillovers in Canada, 1974-98* Ron Kneebone Deparmen of Economics Universiy of Calgary John Leach Deparmen of Economics McMaser Universiy Ocober, 2000 Absrac Wha

Deb Accumulaion, Deb Reducion, and Deb Spillovers in Canada, 1974-98* Ron Kneebone Deparmen of Economics Universiy of Calgary John Leach Deparmen of Economics McMaser Universiy Ocober, 2000 Absrac Wha

Relationships between Stock Prices and Accounting Information: A Review of the Residual Income and Ohlson Models. Scott Pirie* and Malcolm Smith**

Relaionships beween Sock Prices and Accouning Informaion: A Review of he Residual Income and Ohlson Models Sco Pirie* and Malcolm Smih** * Inernaional Graduae School of Managemen, Universiy of Souh Ausralia

Relaionships beween Sock Prices and Accouning Informaion: A Review of he Residual Income and Ohlson Models Sco Pirie* and Malcolm Smih** * Inernaional Graduae School of Managemen, Universiy of Souh Ausralia

Making Use of Gate Charge Information in MOSFET and IGBT Data Sheets

Making Use of ae Charge Informaion in MOSFET and IBT Daa Shees Ralph McArhur Senior Applicaions Engineer Advanced Power Technology 405 S.W. Columbia Sree Bend, Oregon 97702 Power MOSFETs and IBTs have

Making Use of ae Charge Informaion in MOSFET and IBT Daa Shees Ralph McArhur Senior Applicaions Engineer Advanced Power Technology 405 S.W. Columbia Sree Bend, Oregon 97702 Power MOSFETs and IBTs have

JEL classifications: Q43;E44 Keywords: Oil shocks, Stock market reaction.

Applied Economerics and Inernaional Developmen. AEID.Vol. 5-3 (5) EFFECT OF OIL PRICE SHOCKS IN THE U.S. FOR 1985-4 USING VAR, MIXED DYNAMIC AND GRANGER CAUSALITY APPROACHES AL-RJOUB, Samer AM * Absrac

Applied Economerics and Inernaional Developmen. AEID.Vol. 5-3 (5) EFFECT OF OIL PRICE SHOCKS IN THE U.S. FOR 1985-4 USING VAR, MIXED DYNAMIC AND GRANGER CAUSALITY APPROACHES AL-RJOUB, Samer AM * Absrac

Risk Modelling of Collateralised Lending

Risk Modelling of Collaeralised Lending Dae: 4-11-2008 Number: 8/18 Inroducion This noe explains how i is possible o handle collaeralised lending wihin Risk Conroller. The approach draws on he faciliies

Risk Modelling of Collaeralised Lending Dae: 4-11-2008 Number: 8/18 Inroducion This noe explains how i is possible o handle collaeralised lending wihin Risk Conroller. The approach draws on he faciliies

The Optimal Instrument Rule of Indonesian Monetary Policy

The Opimal Insrumen Rule of Indonesian Moneary Policy Dr. Muliadi Widjaja Dr. Eugenia Mardanugraha Absrac Since 999, according o Law No. 3/999, Bank Indonesia (BI- he Indonesian Cenral Bank) se inflaion

The Opimal Insrumen Rule of Indonesian Moneary Policy Dr. Muliadi Widjaja Dr. Eugenia Mardanugraha Absrac Since 999, according o Law No. 3/999, Bank Indonesia (BI- he Indonesian Cenral Bank) se inflaion

Forecasting Sales: A Model and Some Evidence from the Retail Industry. Russell Lundholm Sarah McVay Taylor Randall

Forecasing Sales: A odel and Some Evidence from he eail Indusry ussell Lundholm Sarah cvay aylor andall Why forecas financial saemens? Seems obvious, bu wo common criicisms: Who cares, can we can look

Forecasing Sales: A odel and Some Evidence from he eail Indusry ussell Lundholm Sarah cvay aylor andall Why forecas financial saemens? Seems obvious, bu wo common criicisms: Who cares, can we can look

Understanding China s High Investment Rate and FDI Levels: A Comparative Analysis of the Return to Capital in China, the United States, and Japan

Undersanding China s High Invesmen Rae and FDI Levels: A Comparaive Analysis of he Reurn o Capial in China, he Unied Saes, and Japan Wenkai Sun, Renmin Universiy of China Xiuke Yang, Peking Universiy Geng

Undersanding China s High Invesmen Rae and FDI Levels: A Comparaive Analysis of he Reurn o Capial in China, he Unied Saes, and Japan Wenkai Sun, Renmin Universiy of China Xiuke Yang, Peking Universiy Geng

THE PRESSURE DERIVATIVE

Tom Aage Jelmer NTNU Dearmen of Peroleum Engineering and Alied Geohysics THE PRESSURE DERIVATIVE The ressure derivaive has imoran diagnosic roeries. I is also imoran for making ye curve analysis more reliable.

Tom Aage Jelmer NTNU Dearmen of Peroleum Engineering and Alied Geohysics THE PRESSURE DERIVATIVE The ressure derivaive has imoran diagnosic roeries. I is also imoran for making ye curve analysis more reliable.

µ r of the ferrite amounts to 1000...4000. It should be noted that the magnetic length of the + δ

Page 9 Design of Inducors and High Frequency Transformers Inducors sore energy, ransformers ransfer energy. This is he prime difference. The magneic cores are significanly differen for inducors and high

Page 9 Design of Inducors and High Frequency Transformers Inducors sore energy, ransformers ransfer energy. This is he prime difference. The magneic cores are significanly differen for inducors and high

Valuation Beyond NPV

FIN 673 Alernaive Valuaion Approaches Professor Rober B.H. Hauswald Kogod School of Business, AU Valuaion Beyond NPV Corporae Finance revolves around hree fundamenal quesions: wha long-erm invesmens should

FIN 673 Alernaive Valuaion Approaches Professor Rober B.H. Hauswald Kogod School of Business, AU Valuaion Beyond NPV Corporae Finance revolves around hree fundamenal quesions: wha long-erm invesmens should

Chapter 2 Problems. 3600s = 25m / s d = s t = 25m / s 0.5s = 12.5m. Δx = x(4) x(0) =12m 0m =12m

x(0) =12m 0m =12m") Chaper 2 Problems 2.1 During a hard sneeze, your eyes migh shu for 0.5s. If you are driving a car a 90km/h during such a sneeze, how far does he car move during ha ime s = 90km 1000m h 1km 1h 3600s = 25m

Chaper 2 Problems 2.1 During a hard sneeze, your eyes migh shu for 0.5s. If you are driving a car a 90km/h during such a sneeze, how far does he car move during ha ime s = 90km 1000m h 1km 1h 3600s = 25m

Migration, Spillovers, and Trade Diversion: The Impact of Internationalization on Domestic Stock Market Activity

Migraion, Spillovers, and Trade Diversion: The mpac of nernaionalizaion on Domesic Sock Marke Aciviy Ross Levine and Sergio L. Schmukler Firs Draf: February 10, 003 This draf: April 8, 004 Absrac Wha is

Migraion, Spillovers, and Trade Diversion: The mpac of nernaionalizaion on Domesic Sock Marke Aciviy Ross Levine and Sergio L. Schmukler Firs Draf: February 10, 003 This draf: April 8, 004 Absrac Wha is

PREMIUM INDEXING IN LIFELONG HEALTH INSURANCE

Far Eas Journal of Mahemaical Sciences (FJMS 203 Pushpa Publishing House, Allahabad, India Published Online: Sepember 203 Available online a hp://pphm.com/ournals/fms.hm Special Volume 203, Par IV, Pages

Far Eas Journal of Mahemaical Sciences (FJMS 203 Pushpa Publishing House, Allahabad, India Published Online: Sepember 203 Available online a hp://pphm.com/ournals/fms.hm Special Volume 203, Par IV, Pages

Finance and Economics Discussion Series Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board, Washington, D.C.

Finance and Economics Discussion Series Divisions of Research & Saisics and Moneary Affairs Federal Reserve Board, Washingon, D.C. The Effecs of Unemploymen Benefis on Unemploymen and Labor Force Paricipaion:

Finance and Economics Discussion Series Divisions of Research & Saisics and Moneary Affairs Federal Reserve Board, Washingon, D.C. The Effecs of Unemploymen Benefis on Unemploymen and Labor Force Paricipaion:

Task is a schedulable entity, i.e., a thread

Real-Time Scheduling Sysem Model Task is a schedulable eniy, i.e., a hread Time consrains of periodic ask T: - s: saring poin - e: processing ime of T - d: deadline of T - p: period of T Periodic ask T

Real-Time Scheduling Sysem Model Task is a schedulable eniy, i.e., a hread Time consrains of periodic ask T: - s: saring poin - e: processing ime of T - d: deadline of T - p: period of T Periodic ask T

THE FIRM'S INVESTMENT DECISION UNDER CERTAINTY: CAPITAL BUDGETING AND RANKING OF NEW INVESTMENT PROJECTS

VII. THE FIRM'S INVESTMENT DECISION UNDER CERTAINTY: CAPITAL BUDGETING AND RANKING OF NEW INVESTMENT PROJECTS The mos imporan decisions for a firm's managemen are is invesmen decisions. While i is surely

VII. THE FIRM'S INVESTMENT DECISION UNDER CERTAINTY: CAPITAL BUDGETING AND RANKING OF NEW INVESTMENT PROJECTS The mos imporan decisions for a firm's managemen are is invesmen decisions. While i is surely

Total factor productivity growth in the Canadian life insurance industry: 1979-1989

Toal facor produciviy growh in he Canadian life insurance indusry: 1979-1989 J E F F R E Y I. B E R N S T E I N Carleon Universiy and Naional Bureau of Economic Research 1. Inroducion Produciviy growh

Toal facor produciviy growh in he Canadian life insurance indusry: 1979-1989 J E F F R E Y I. B E R N S T E I N Carleon Universiy and Naional Bureau of Economic Research 1. Inroducion Produciviy growh

Working Paper Monetary aggregates, financial intermediate and the business cycle

econsor www.econsor.eu Der Open-Access-Publikaionsserver der ZBW Leibniz-Informaionszenrum Wirschaf The Open Access Publicaion Server of he ZBW Leibniz Informaion Cenre for Economics Hong, Hao Working

econsor www.econsor.eu Der Open-Access-Publikaionsserver der ZBW Leibniz-Informaionszenrum Wirschaf The Open Access Publicaion Server of he ZBW Leibniz Informaion Cenre for Economics Hong, Hao Working

Inflation and Economic Growth: Inflation Threshold Level Analysis for Ethiopia

Inernaional Journal of Ehics in Engineering & Managemen Educaion Websie: www.ijeee.in (ISSN: 2348-4748, Volume 2, Issue 5, May 2015) Inflaion and Economic Growh: Inflaion Threshold Level Analysis for Ehiopia

Inernaional Journal of Ehics in Engineering & Managemen Educaion Websie: www.ijeee.in (ISSN: 2348-4748, Volume 2, Issue 5, May 2015) Inflaion and Economic Growh: Inflaion Threshold Level Analysis for Ehiopia

A Probability Density Function for Google s stocks

A Probabiliy Densiy Funcion for Google s socks V.Dorobanu Physics Deparmen, Poliehnica Universiy of Timisoara, Romania Absrac. I is an approach o inroduce he Fokker Planck equaion as an ineresing naural

A Probabiliy Densiy Funcion for Google s socks V.Dorobanu Physics Deparmen, Poliehnica Universiy of Timisoara, Romania Absrac. I is an approach o inroduce he Fokker Planck equaion as an ineresing naural

THE ROLE OF ASYMMETRIC INFORMATION AMONG INVESTORS IN THE FOREIGN EXCHANGE MARKET

INTERNATIONAL JOURNAL OF FINANCE & ECONOMICS In. J. Fin. Econ. (2008) Published online in Wiley InerScience (www.inerscience.wiley.com)..367 THE ROLE OF ASYMMETRIC INFORMATION AMONG INVESTORS IN THE FOREIGN

INTERNATIONAL JOURNAL OF FINANCE & ECONOMICS In. J. Fin. Econ. (2008) Published online in Wiley InerScience (www.inerscience.wiley.com)..367 THE ROLE OF ASYMMETRIC INFORMATION AMONG INVESTORS IN THE FOREIGN

A One-Sector Neoclassical Growth Model with Endogenous Retirement. By Kiminori Matsuyama. Final Manuscript. Abstract

A One-Secor Neoclassical Growh Model wih Endogenous Reiremen By Kiminori Masuyama Final Manuscrip Absrac This paper exends Diamond s OG model by allowing he agens o make he reiremen decision. Earning a

A One-Secor Neoclassical Growh Model wih Endogenous Reiremen By Kiminori Masuyama Final Manuscrip Absrac This paper exends Diamond s OG model by allowing he agens o make he reiremen decision. Earning a

Fiscal Consolidation in an Open Economy

Fiscal Consolidaion in an Open Economy Chrisopher J. Erceg Federal Reserve Board Jesper Lindé Federal Reserve Board and CEPR December 29, 2 Absrac This paper uses a New Keynesian small open economy model

Fiscal Consolidaion in an Open Economy Chrisopher J. Erceg Federal Reserve Board Jesper Lindé Federal Reserve Board and CEPR December 29, 2 Absrac This paper uses a New Keynesian small open economy model

ESTIMATE OF POTENTIAL GROSS DOMESTIC PRODUCT USING THE PRODUCTION FUNCTION METHOD

Economeric Modelling Deparmen Igea Vrbanc June 2006 ESTIMATE OF POTENTIAL GROSS DOMESTIC PRODUCT USING THE PRODUCTION FUNCTION METHOD CONTENTS SUMMARY 1. INTRODUCTION 2. ESTIMATE OF THE PRODUCTION FUNCTION

Economeric Modelling Deparmen Igea Vrbanc June 2006 ESTIMATE OF POTENTIAL GROSS DOMESTIC PRODUCT USING THE PRODUCTION FUNCTION METHOD CONTENTS SUMMARY 1. INTRODUCTION 2. ESTIMATE OF THE PRODUCTION FUNCTION

Consumer sentiment is arguably the

Does Consumer Senimen Predic Regional Consumpion? Thomas A. Garre, Rubén Hernández-Murillo, and Michael T. Owyang This paper ess he abiliy of consumer senimen o predic reail spending a he sae level. The

Does Consumer Senimen Predic Regional Consumpion? Thomas A. Garre, Rubén Hernández-Murillo, and Michael T. Owyang This paper ess he abiliy of consumer senimen o predic reail spending a he sae level. The