Term Structure of Commodities Futures. Forecasting and Pricing.

|

|

|

- Shannon Walsh

- 9 years ago

- Views:

Transcription

1 erm Srucure of Commodiies Fuures. Forecasing and Pricing. Marcos Escobar, Nicolás Hernández, Luis Seco RiskLab, Universiy of orono Absrac he developmen of risk managemen mehodologies for non-gaussian markes relies ofen on he assumpion ha he underlying marke facors have a gaussian disribuion. While advances have been made in he modeling of more general marginal disribuions of he risk facors, he modeling of non-gaussian dependence srucures is much less advanced. For commodiies markes ha ofen exhibi sudden changes from backwardaion ino conango (such as energy, agriculural producs and meals), correlaions or linear ransformaions of hem fail o accoun for realisic ransformaions of forward curve convexiy. his paper develops a model ha overcomes his difficuly for scenario generaion purposes. I also provides he risk neural processes needed for derivaives pricing, answering wo leading problems of he financial world (forecasing and pricing), and presens i in he conex of oher developmens for commodiy fuures modeling.

2 I - INRODUCION he developmen of risk managemen mehodologies for non-gaussian markes relies ofen on he assumpion ha he underlying marke facors have a gaussian disribuion. While advances have been made in he developmen of more flexible families of disribuions o model he marginal behavior of he risk facors, he modeling of non-gaussian dependence srucures is much less advanced. Normal rank correlaions (NRC) and Spearman raios, over he underlyngs facors or direcly over he observed curve, in general yield beer resuls han correlaions in markes wih non-gaussian marginals, bu are sill linear-based measures of dependence. For commodiies markes ha ofen exhibi sudden changes from backwardaion ino conango (such as energy, agriculural producs and meals), hey fail o accoun for realisic ransformaions of fuure curve convexiy. Copulas, which in principle will reconsruc he enire dependence srucure, appear o be oo difficul o impracical in specific siuaions. his paper develops a model ha overcomes his difficuly in cerain markes, and presens i in he conex of relaed developmens for commodiy fuures modeling. he firs sep will provide a model o fi commodiy markes for he purpose of scenario generaion in he conex of risk managemen exercises; in order o enhance he scope of he proposed model, as a second sep, non-arbirage condiions will be considered wih purposes of pricing commodiies derivaives. Les firs poin ou he followings pracical facs abou fuures markes in commodiies: A commodiy s fuure conrac is an agreemen o exchange a fixed amoun of physical asse for a specific price a mauriy.

and Spearman raios, over he underlyngs facors or direcly over he observed curve, in general yield beer resuls han correlaions in markes wih non-gaussian marginals, bu")

3 - Fuures conrac are raded in a day-by-day basis, and here are widely known convenions abou how hey should be raded; his is no he case of he forward conrac, which is only found on over he couner markes. One of he mos influen feaures of he fuures markes is ha you can only ge a ime- he fuure prices for a commodiy mauring a i - for fixed values of i, i.e. i are he h of every monh in he case of oil. here are wo popular views of commodiies prices; boh based on he fiing of he observed erm srucure for fuures prices, namely: By modeling he vecor of fuures prices of dimension m ( in Oil case) ha can be obained a any ime- from he marke, filering all ypes of dependencies rough ime in he componens of he vecor and aking care of he mulivariae srucure of he residuals by NRC or Spearman raios. his is he simples way, bu fail o accoun for he arbirage-free condiions. he heory of sorage (S) of Kaldor (99), Brennan (958) and elser (958) explains he difference beween conemporaneous spo and he fuures prices in erms of ineres forgone in soring a commodiy, warehousing coss, and a convenience yield on invenory. his can be also seemed as a muliplicaive model. hey obained processes for he underlyngs under arbiragefree condiions.

4 In his aricle we will presen an alernaive o he previous mehods, bu firs we will basically review S and he saisical feaures of he fuures prices vecors. here is one general way o obain expression for he fuures prices of commodiies under he heory of Sorage: where: F, = S e { r (, ) + u(, ) δ (, )}( ), F, denoes he fuure price, a ime of a conrac for delivery a ime. S is he spo price of he commodiy a ime. r (, ) is he ineres rae a ime for (-) ime o mauriy, boosrapped from he zero curve. δ (, ) is he convenience yield: he flow of services ha accrues o he holder of he physical commodiy, bu no o he owner of a conrac for fuure delivery. In ohers words he benefi from ownership of he physical commodiy ha may include he abiliy o profi from emporary local sorages or he abiliy o keep a producion process running, a ime- for (-)-ime o mauriy. u (, ) is he sorage cos a ime for (-)-ime o mauriy. he insananeous ineres rae and insananeous convenience yield are defined as r = lim r (, ), δ = lim δ (, ) respecively. he erm srucures of forward ineres rae and fuures convenience yields are defined as rf (, s) = lim r(, s, ), δ f (, s) = lim δ (, s, ) respecively. s s 4

is he convenience yield: he flow of services ha accrues o he holder of he physical commodiy, bu no o he owner of a conrac for fuure delivery.")

5 Where r (, s, ) and δ (, s, ) are he ineres rae yield and convenience yield a ime for he period from s o. he relaionship beween he above erms is alernaively described in he following equaions: rs ds = r (, ) = rf (, s) ds ; δ (, ) = δ sds = δf (, s) ds Since fuures prices are funcions of several underlying facors, which have a widely acceped financial inerpreaion, i is ofen more convenien o describe he uncerainy of fuures prices by modelling he sochasic behaviour of hese underlying facors. he main difficuly wih hese facors is ha mos of hem canno be recorded or observed, leading o reliabiliy problems. here are wo main measures ruling ou each underlying sochasic models, he observed one (called P-measure) based on he bes saisical fiing of he daa, and he Q-measure based on arbirage-free condiions. In paricular, when rying o forecas a fuure price, models based on he P-measure for he underlying facors are needed; Q-measure is used for pricing derivaives on eiher spo or fuure price. As for he univariae and mulivariae feaures of commodiies (Oil, Gas, Sugar, Coffee, Meals) fuures prices, we have he following findings (see ): mean reversion and sochasic volailiy, which can be modeled by an AR()-GARCH(,) model (mulivariae GARCH for he whole vecor), wih fa-ail non-normal residuals. he vecor of residuals sill has he conango 5

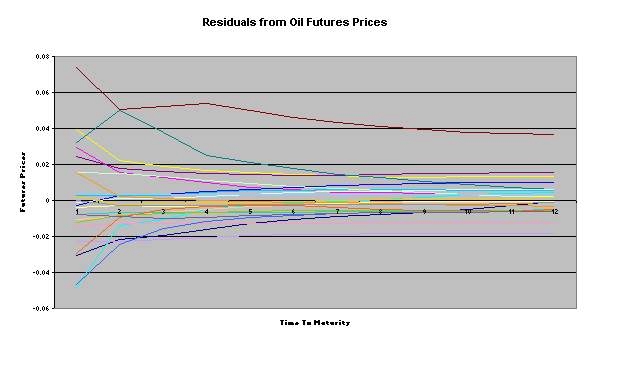

6 and backwardaion feaure (increasing or decreasing curve rough ime-o-mauriy) see figure for Residuals from a Vecor Auoregressive. his paper propose an addiive (quadraic fiing) model for he erm srucure of fuures prices leading o a -dim vecor of underlyngs. hese new facors are sudied, showing simple sochasic behaviour and normal dependency srucures under he real measure. hey are also modelled under arbirage free condiions for purposes of pricing derivaives. his model shows more accurae forecasing han AR-GARCH models, geing a beer and more flexible fiing, for up o year ime-o-mauriy, of he erm srucure of fuures prices, volailiies and correlaions han S models. he paper is organized as follows: he second secion is a survey of some of he mos imporan models (given explicily he Q-measure for he underlying, he P-measure is basically zero marke price of risk, λ=,) in he lieraure, highlighing some of heir drawbacks: Schwarz 997, Milersen and Schwarz 998, homas Urich and Schwarz-Smih. Secion III deals wih he proposed model and some deails abou he esimaion procedure. he fourh secion is dedicaed o he forecasing properies of he model using a es porfolio and measures of risk implemened in RiskWach..6 and HisoRisk.6, sofware developed by Algorihmics Inc for risk managemen purposes he fifh secion deals wih he formalizaion of he pricing framework for he proposed model. Secion sixh deals wih he volailiies and correlaions implied by our model over he fuure prices erm srucure, and las secion goes o he pricing of opions on fuures conracs. 6

7 II - MODELS One of he difficulies in he empirical implemenaion of commodiy price models is ha frequenly he facors or sae variables of hese models are no direcly observable. For some commodiies he spo price is hard o obain, and he fuures conrac closes o mauriy is used as proxy for he spo price. he problems of esimaing he insananeous convenience yield are even more complex; normally, fuures prices wih differen mauriies are used o compue i. he insananeous ineres rae is also no direcly observable. Fuures conracs, however, are widely raded in several exchanges and heir prices are more easily observed. his is why a model based on modelling direcly fuures prices is more convenien and reliable. Schwarz-Smih Model: ln(s ) = χ + ξ dχ = ( kχ λ χ ) d + σ χ dz χ () dξ = µ λ ) d + σ dz ( () ξ ξ ξ ξ Where z ξ and z χ are sandard Brownian moion wih dzξ dz χ = ρd χ will be referred o as he shor-erm deviaion in prices (emporary changes in prices ha are no expeced o persis) and ξ he equilibrium price level (fundamenal changes ha are expeced o persis). hese facors are almos orhogonal in heirs dynamics, which implies a small correlaion beween he sochasic incremens of hose facors. k ( ) ln( F, ) e χ ξ A( ) = + + () Where 7

8 * A ( ) = µ ( ) ( e ξ k( ) λ χ ) + ( e k k( ) σχ ) + σξ ( ) + ( e k k( ) σ χσξρ ) k prices. I assumes only wo sources of randomness, which may barely hold all feaures of fuures he procedure followed o compue he unobserved sae variables in his model is Kalman Filer. he Kalman filer is a recursive procedure for compuing esimaes of unobserved sae variables based on observaions ha depend on hese sae variables. Given a prior disribuion on he iniial values of he sae variables and a model describing he likelihood of he observaions as a funcion of he rue values, he Kalman filer generaes updaed poserior disribuions for hese sae variables in accordance o Bayes rule. Schwarz Model: ds = ( r δ ) S d + σ S dz (4) dδ = k( α δ ) d + σ dz (5) dr = a( m r ) d + σ dz (6) z, z and z are sandard Brownian moion, wih dzdz = ρd. dzdz = ρd, dzdz = ρ d, Where S denoes he ime- curren spo price, δ denoes he insananeous ime- convenience yield (here includes he insananeous cos of carry) and r sands for he insananeous ineres rae. (If he goals is pricing derivaives hen coefficiens m and α ake implicily accoun of λ s marke prices of risk; as for forecasing purposes hey are jus esimae from he observed daa). k ( ) a ( ) e e ln( F, ) = δ + r + X+ C( ) k a 8

9 Here, C( ) is jus a explici funcion on -. X =logs. Commodiy fuure prices may also be affeced by a number of addiional facors no included in he previous model. For example he effec of he sorage cos on fuure prices flucuaions is no considered Milersen and Schwarz model: his model generalizes and combines he wo approaches by using all he informaion in he iniial erm srucures of boh ineres rae and commodiy fuures prices. rf (, s ) = rf (, s ) + µ rf ( u, s ) du + σ rf ( u, s ) dw u (7) δ f (, s ) = δ f (, s ) + µ δ f ( u, s ) du + σ δ f ( u, s ) dw u (8) S ( ) = S () + S u µ s ( u) du + S uσ s ( u) dw u (9) W u is a sandard d-dimensional wiener processes for every differenial equaion. Correlaions among he hree processes come via he specificaion of he diffusion erms (σ s). he no arbirage condiions will compleely deermine he drif erms (µ s): µ s () = rf(,) - δf(,). () s s µ (, s) = σ (, s) σ (, v) dv () rf µ δf (, s) = σ rf (, s)( σ rf (, v) dv) + ( σ rf (, ) σ δ (, ))( σ S ( ) + rf rf ( σ rf (, s) σ (, s)) ds) () he expression for he Fuures prices of he commodiy is given by: δ 9

= rf (, s ) + µ rf ( u, s ) du + σ rf ( u, s ) dw u (7) δ f (, s ) = δ f (, s ) + µ δ f ( u, s ) du + σ δ f ( u, s ) dw u (8) S ( ) = S () + S u µ s ( u) du + S uσ s ( u) dw u (9) W u is a")

10 F (, ) = S exp( ( rf (, s ) δ f (, s )) ds ) () homas Urich Model: his model is an exension o commodiies, specifically meals, of he Garbade (996) work on erm srucure for ineres raes. F, = f ( ) + wi ( ) f i ( ) I i= (4) f i J j ( ) = bij ( ), ( ) = j= J j b j ( ) j= f (5) In paricular F I, = S = b + bi wi ) i= ( which yields he spo price behavior. (6) Here, w i are Gaussian random walks wih zero drif and uni variance per year; he random walks are saisically independen of each oher. he funcion f i are referred o as modes of flucuaions. he degree of he underlying polynomials, for forecasing purposes, can be anyone desired, bu in he case of pricing i should saisfy he following requiremen. I >, I = J (7) J = *J + (8) his model makes a very imporan assumpion in order o esimae is parameers: one should have available, a any ime, he fuure prices for he same ime-o-mauriy; a imes his is

11 no realisic, so approximaions are required o fulfill i. his becomes he main difficuly in he model. III - A PROPOSED MODEL In order o overcome he assumpion of Ulrich, we make a few changes in he esimaion procedure and he srucure of he model, which yields he following model: F, = χ, + ξ, ( + ) + η, ( + ) (9) he model is specified by he coefficiens (ime series χ, ξ, η ), on which saisical assumpions need o be made. In his paper, for forecasing purposes, we propose o deal wih he modeling of he coefficiens as follows: he marginal srucure will be modeled using univariae feaures: a Box-Cox ransformaion, he esimaion of a sochasic rend, and he calibraion of non-normal residuals. log χ = log χ - + res,, ξ = ξ - + res,, η = η - + res, We assume he dependence srucure is deermined by normal correlaions. he way o esimae he parameers (ime series χ, ξ, η ) of he model will be by minimum leas square a every ime-, using he differen ime-o-mauriy ( i -) as he fiing daa (based on he feaures of figure ).

12 IV - EMPIRICAL RESULS he idea of obaining a model wih good forecasing properies is highly useful for he financial world, mainly because measures of marke risk like VaR are obained by esimaing he condiional disribuion of a financial Porfolio (funcion of asses). So he idea of good risk managemen is close relaed o good forecaser models. here are many examples of disasers in financial companies due o heir failure o compue fuure condiional disribuion. he forecasing issue is address by comparing he proposed model o boh views of fiing he observed fuure price curve (see inroducion). Firs we compare our model o high sophisicaed mahemaics mulivariae models by using a porfolio example. As for S models, even when hey are used mainly o pricing commodiy s derivaives, i is heoreically possible o use hem for forecasing purposes. So we may he comparison by assessing he goodness of fi of he observed fuures prices vecor. We worked wih ime series of Oil fuure prices from January 99 ill December ; each series corresponds o a specific mauriy monh i.e. we have he fuure prices for i -, (i=january,,december) ime o mauriy a ime-. Our goal is o provide a good fiing for he condiional disribuion wih one-day-horizons of a porfolio of fuures conracs; in oher words, we ry o forecas he exac values of he perceniles for omorrow s disribuion using pas informaion on he vecor of fuure prices. Due o he fac ha he Value a Risk is he mos imporan measure for risk managemen, which is jus he percenile 95 of he disribuion, we will highligh he resuls regarding his paricular percenile. We also ook ino consideraion

.")

13 oher perceniles han he 95: if a porfolio depends on fuures prices in a non-linear way (i.e. opions on fuures), hen small perceniles may have an influence in he porfolio Var. Les inroduce he following noaion: Dis α (P / -): Percenile α of he condiional disribuion of he Porfolio P for ime, given informaion available a ime -. P - Observed value for Porfolio P a day. he following es is equivalen o he one explained in Diebold, which is based on he iid U(,) properies of he probabiliy inegral ransform series z = Dis ( P, ). P he number of ime ha he real value of he Porfolio (P ) is bigger han Dis α (P / -) for a given perceniles α (i.e. 95%) ou of 5 replicas should be close o 5(-α)/, (.5). So, by he creaion of he following Bernoulli random variable, we will be able o assess how well is every percenile recovered (es of goodness-of-forecasing). B iα = if P i > Dis α (P i / i-) oherwise. Le creae he following graph represenaion, perceniles from. o.99 are allocaed in he 5 X-axis, numbers Y iα = ( 5 i= B α )/ (5*α) are allocaed in he Y-axis. i So pairs (α, Bi α ) or (α,y iα ) show he behaviour of he whole condiional disribuion for he i= Porfolio. We will use (α,y iα ) in able I as a comparaive ools. he closer o one he values of Y iα, he beer he model in is forecasing abiliies. As has been suggesed by Diebold (998),

is bigger han Dis α (P / -) for a given perceniles α (i.e. 95%) ou of 5 replicas should be close o 5(-α)/, (.5).")

14 he previous visual assessmen is more revealing, consrucive and aracive han more sophisicaed procedures such as kernel densiy esimaes. A porfolio was creaed using RiskWach sofware, hree insrumens were creaed, a commodiy forward saring a and mauring a 9 days, he second one saring a he same momen and mauring a days and he las one wih he same sar dae and mauriy 5 (business) days. Fourh ses of scenarios were creaed following differen models. wo of hem come from considering he residuals res o be normal/non-normal or dependen/independen in our model. Also we creaed wo se of scenarios based on differen assumpions for he vecor of fuures prices.. Empirical Disribuion of he residuals (res ) in proposed model, aking ino accoun las 5 values. (EP5). Normal Disribuion of he residuals (res ) in proposed model, aking ino accoun las 5 values. (ND5). Mean reversion and Garch in every univariae fuure prices series, mulivariae normal for he residuals (using principal componens) from he AR()-Garch(,), 5 previous values considered. (MRGN) 4. Mean reversion and Garch in every univariae fuure prices series, Empirical disribuion for he mulivariae residuals from he AR()-Garch(,), 5 previous values considered. (MRGEP) 4

15 he following able shows a comparison among hose differen models considered: able I Proposed Model Classical approaches Perceniles EP5 ND5 MRGN MRGEP.6 Righ Lef Righ Lef Righ Lef Righ Lef Righ Var Lef he bes resuls are in black for each percenile. able I show us very ineresing feaures abou he mulivariae condiional disribuion (from now on MCD), which is he one needed o forecas he vecor of fuures prices. he normal mulivariae disribuion of he vecor of residuals (res i, ND5) give a decen fiing of he MCD of fuures prices vecor, and induced a normal MCD on i!!. he mean vecor and covariance marix of he MCD depend highly non-lineal on previous daa (due o he fac ha he new ime series vecor (χ, ξ, η ) is no a lineal combinaion of he fuures prices vecor ( F,..., F ). his specific form of mulivariae non-saionariy could no be hold by filers,, like Vecor AR, mulivariae GARCH or even by assuming non-normaliy on he residuals form any of hose models (models and 4 in able I). In oher words his model show he dependency rough ime-o-mauriy change according o he ime- chosen and vice versa; rying o capure hose dependencies separaely lead o unreliable 5

give a decen fiing of he MCD of fuures prices vecor, and induced a normal MCD on i!")

16 resuls, leading us o hink ha he behavior in and - should be faced simulaneously using he conango and backwardaion feaures of he fuures price vecor. Regarding S models, he sandard deviaion of he error (obained from he regressions) is smaller for he quadraic polynomial (addiive model) han for he Schwarz model (muliplicaive model). he goodness of fi from exponenial funcion is worse ha he fiing using quadraic polynomials in he ime-o-mauriy considered ( year). V - COMMODIY DERIVAIVE PRICING Les menion a couple of examples ha address he imporance of aking care of he conangobackwardaion feaure in he pricing of derivaives. Mealgesellschaf: 99 I decided o marke long daed fuures conracs o US cliens (up o years), when he marke only had fuures up o 8 monhs. heir sraegy relied on rolling over he conracs a expiraion. A change in he convexiy of he fuures curve gave rise o margin paymens ha hey could no mee. hey los over $B. Orange Couny and Bob Ciron: In December 994, Orange Couny sunned he markes by announcing ha is invesmen pool had suffered a loss of $.6 billion, he larges loss ever recorded by a local governmen invesmen pool, and led o he bankrupcy of he couny. his loss was he resul of unsupervised invesmen aciviy of Bob Ciron, he Couny reasurer, who was enrused wih an $7.5 billion porfolio belonging o couny schools, ciies, special disrics 6

17 and he couny iself. In imes of fiscal resrains, Ciron was viewed as a wizard who could painlessly deliver greaer reurns o invesors. Indeed, Ciron delivered reurns abou % higher han he comparable Sae pool. Ciron's main purpose was o increase curren income by exploiing he fac ha medium-erm mauriies had higher yields han shor-erm invesmens. On December 99, for insance, shorerm yields were less han %, while 5-year yields were around 5.%. Wih such a posiively sloped erm srucure of ineres raes, he endency may be o increase he duraion of he invesmen o pick up an exra yield. his boos, of course, comes a he expense of greaer risk. he sraegy worked fine as long as ineres raes wen down. In February 994, however, he Federal Reserve Bank sared a series of 6 consecuive ineres rae increases, which led o a bloodbah in he bond marke. he large duraion led o a $.6 billion loss In our previous secion we proposed a polynomial fiing of he erm srucure for commodiy fuures prices, which yields he following model: F = χ + ξ ( + ) + η ( + ) + e (),,,,, As i can noiced, he main srucural difference beween his model and he ohers reviewed in he previous secion, lies in he fac ha our sochasic underlying facors are addiive in he fuures prices while facors in he oher models were always muliplicaive, i.e., F, = S e { r(, ) δ (, )}( ) he feaures for hose ime series called (χ, ξ, η ) depend on he analysis goal, eiher forecasing, which was done in previous secion, or pricing, which is he focus of his secion. 7

18 Arbirage pricing always is a case of deermining prices of derivaives in erms of some a priori given underlying price processes. he process in he underlying used o price he derivaive (Q-measure, risk-neural ) is differen o he one obained by any sound saisical ools using hisorical daa (P-measure), oherwise here would be arbirage opporuniies. In our approach, insead of specifying he models and parameers under he P-measure, we will specify he dynamics of he series in he spo decomposiions direcly under he Q- measure. his procedure is known as maringale modeling, and i is widely used in ineres rae modeling (see Bjork 998). So le keep expressing our fuure price F, as a combinaion of hree ime series (sochasic processes). F, = χ + ξ ( + ) + η ( + ) () he ime o mauriy appears on he underlyngs ime series because he drif of heirs diffusion processes depend on under he Q-measure (see Appendix III): dχ ξ = σdz, dξ = d+ σdz + η +, dη = d+ σdz. () Here dz, dz, dz are correlaed incremens of sandard Brownian moion processes wih dz dz = ρ d, dz dz = ρ d, dz dz = ρ d. he specificaion of he drifs for he above diffusion processes under he Q-measure follows from sandard arbirage argumens: he fuures prices process mus saisfy he following 8

.")

19 propery: F(, s) = E Q ( F, / s), s< <, which makes fuures prices a maringale. Milersen- Schwarz (998) also derives he convenience yield erm srucure based on his condiion. A well-known problem wih he maringale-approach lies in he fac ha he series χ, ξ, η ) ( are never observed under he Q-measure bu under he P-measure. his means ha if we apply sandard saisical procedures o our series we will no ge our Q-parameers, bu pure nonsense. In order o overcome his difficuly (see Bjork 998) he process of esimaion is spli in wo pars, he diffusion erm and he drif erm. he diffusion erm is he same under P and under Q (Girsanov ransformaion make his possible), so i is possible o esimae diffusion parameers using P-measure. As for he drif, i would be necessary o follow he yield curve inversion procedure (which is he procedure used on ineres rae). Bu in our case we do no need o worry abou i because our Q- measure models do no have parameers in he drif. hen we have ha, he condiional expecancy, under Q, and volailiy given = is: Q ( + ) ( + ) E [( χ, ξ, η ) / ] = [ χ, ξ, η ] ( + ) ( + ) () Cov[( χ, ξ, η ) / ] = ρ ρ σ σ σ a σ σ c ρ ρ σ σ a σ σ b σ f ρ ρ σ σ c σ σ σ d f (4) (See Appendix I) Each model considered in previous aricles (see papers in References) has differen implicaions no only for he erm srucure of fuures prices (see our previous paper) bu also he erm srucure of volailiies of fuures prices and erm srucure of correlaions of fuures prices. 9

he process of esimaion is spli in wo pars, he diffusion erm and he drif erm.")

20 VI - MODEL FIING OF VOLAILIIES AND CORRELAIONS. We can wrie he fuures prices, under he Q-measure, as: F(, ) E ( S / ) ( ) ( ) Q = = χ + ξ + + η + (5) We are ineresed in modeling no only he erm srucure of fuures prices, bu also he erm srucure of volailiies and correlaions. We can show ha he volailiy of he fuure price F(,) a ime, mauring a, comes up from applying Mulidimensional Io s lemma o equaion (5), so i will be given by: V F V V Cov [ (, )] = [ χ ] + [ ξ ] ( + ) + ( + ) [ χ, ξ ] + V Cov + + Cov 4 [ η ] ( ) ( ) { [ χ, η ] ( ) [ ξ, η ]} = σ + σ 4 ( + ) + ρ σ σ ( + ) + ( σ + ρσ σ ) ( + ) + ρσ σ ( + ) his is a polynomial of order 4, which will fi he volailiy erm srucure of fuures prices; he correlaions beween he new facors χ, ξ, η ) will deermine wheher his curve is increasing ( or decreasing. In pracice, a decreasing paern will characerize mos commodiies. (see Schwarz 998). I is also ineresing o check wheher his model capure he erm srucure of correlaions (which is decreasing in ime-o-mauriy for mos commodiies, see ). We can verify ha correlaions of he fuure price F(,) a ime, mauring a, come up also from applying Mulidimensional Io s lemma o equaion (5), so i will be given by:

a ime, mauring a, comes up from applying Mulidimensional Io s lemma o equaion (5), so i will be given by: V F V V Cov [ (, )] = [ χ ] + [ ξ ] ( + ) +")

21 Cov[ F(, ), F(, S)] Corr[ F(, ), F(, S)] =, where he covariance is given by: / { V[ F(, )] V[ F(, S)]} Cov[ F(, ), F(, S)] = σ + ( + )( S + ) σ + ( + ) ( S + ) σ + ( + [( + S + ) ρ + )( S + ) σ σ + [( S + ) + ( S + )( + ) + ( + ) ] ρ σ σ ] ρ σ σ his is a quoien of polynomial on wo variables of order 4, which will fi he correlaions erm srucure of he fuures prices; he correlaion on he unobserved series will deermine wheher his srucure is increasing or decreasing. For example, les consider a lineal model (only χ, ), no quadraic erm). We will ge he ( ξ following polynomial of order wo for he volailiy of fuures: σ ( + σ, Which means decreasing volailiy in he inerval + ) + ρσ σ ( + ) σ ρ ( + ) [, ( ρ )], and increasing in he inerval σ σ σ σ ( + ) [ σ ( ρ + ρ σ σ ), + ], in case of negaive correlaion. We will also ge he following polynomial of order wo for he correlaions of fuures: {[ σ ( + ) σ + ρ + ( + S + ) ρ σ σ ( + ) + σ ] [ σ σ σ + ( + )( S + ) σ ( S + ) + ρ σ σ ( S + ) + σ ]} / he correlaion for χ, ), using real fuures prices from 996 ill 999, was.89, which ( ξ implies decreasing volailiies and also decreasing correlaions from year ill year ime-omauriy. VII - VALUING OPIONS ON FUURES CONRACS

22 A fuure conrac, sared a, is define as he following coningen claim (also called a -claim due o he dependency only on ime-): S -F(,). A European opion on a spo is a -claim defined as Max{S -K, }; a European opion wih exercise dae on a fuure conrac (mauring a ) is a -claim defined as Max{F(, )-K, }. K is always he accorded price. From he formula for curren fuures prices: F(, ) E ( S / ) ( ) ( ) Q = = χ + ξ + + η +. Given curren sae variables a, because hey are joinly normally disribued a, we ge: Q ( + ) ( + ) µ (, ) = E [ F (, )/] = χ + ξ + η ( + ) ( + ) (7) σ (, ) = V[ F (, )] = V[ χ ] + V[ ξ ]( + ) + ( + ) Cov[ χ, ξ ] + V Cov [ η ] ( ) ( ) [ χ ( ) ξ, η ] (8) he variance and covariance given ime are he resuls shown in marix (4). he value of a European opion on a fuures conrac mauring a ime, wih srike price K, and ime unil he opion expires is (under consan ineres rae): r Q e E [max( F(, ) K,)]. (9) Closed form expression for he price of a European opion on a fuure conrac. Assume ha F(,) ~ N(µ(,), σ (,)), his implies ha σ F + µ ~ N(,). Les call he densiy funcion of a N(,) as ϕ. hen he expeced par, under he equivalen measure, of an opion value a momen is:

23 = [max( σ z + µ K,)] ϕ( z) dz z ( σ z + µ K) e π z σ (, ) dz = e π ( z) + ( µ (, ) K) ( N ( z)) () Where, Z = K µ and N ( x) = σ x ϕ ( z) dz. VIII - CONCLUSIONS. he mos influen characerisic in a Porfolio of Oil forwards (fuures) is he mulivariae dependency srucure; his leaded us o focus in he search for a model holding his feaure.. he models proposed in he lieraure do no focus on boh goals forecasing and pricing, besides hey have, as mains problems: -Inaccuracy in he inpu daa (i.e. errors on he esimaed spo prices, insananeous convenience yields). -Unrealisic assumpions (i.e. fuures prices for he same ime-o-mauriy a every ime-). -Do no ake ino consideraions he sorage cos as a sochasic process and even do no allow new sources of randomness o show up (S).. he proposed model work sraigh wih he spo prices (no he log of spo prices) implying addiion model insead of muliplicaive model for he fuures prices. I is he firs model ha provides an addiive explanaion for he erm srucure of fuures prices of Commodiies.

24 4. Due o being addiive, our model can be used for imes o mauriy up o year, which acually is he sample used in he esimaion procedure. I gives no suppor for asympoic (on ime) conclusions. 5. his model only requires esimaion of six parameers, being more parsimonious han oher S model, which requires more free parameers. 6. I provides arbirage-free underlying models for pricing purposes by mixing resuls from Schwarz and Ineres rae maringale modeling approach. A mulivariae normal disribuion in few facors (he ones underlyngs our model) is able o explain he whole vecor of fuures prices; hese facors are no obained by principal componens because i is no he correlaion wha should be conserved. 8. As for univariae forward (spo) Oil ime series, we realized he following: - If he goal is o ge a good shor-erm forecasing hen i is beer o work wih he reurns (log of differencing). here is no significan presence of lineal correlaion (ARMA) on he reurns, bu here is high correlaion in he reurn square (GARCH(,)), wih non-normal residuals. - As for he medium and long-erm forecasing, here is a marked reversion o he mean, and high correlaion in he residuals square (GARCH(,)). - I was no observed deerminisic or sochasic seasonaliy in any case. 9. We may use his model o price derivaives of several underlyngs (commodiies like sugar, oil, ec), looking a he correlaions among he consan, linear and quadraic series. 4

25 IX Bibliography. Bjork,. 998 Arbirage heory in coninuous ime. Breeden, D.., 98, Consumpion risks in fuures markes, Journal of Finance, 5(): 5 5, May. Brennan, M.J., 958, he supply of sorage, American Economic Review, 48: 5 7, March. Brennan, M. J., 99, he price of conve-nience and he evaluaion of commodiy coningen claims., D. Lund, B. Oksendal, (eds.) Sochasic Models and Opion Values: Applicaions o Resources, Environmen, and Invesmen Problems. New York, NY: Norh-Holland. Campbell, Lo and Mackinlay. 997 he economeric of financial markes. Cooner, P.H., 96, Reurns o speculaors: elser versus Keynes, he Journal of Poliical Economy, 68: Corazar, G. and E. Schwarz, 994, he valuaion of commodiy-coningen claims, he Journal of Derivaives, (4): 7 9. Diebold, F.X.,.A., Gunher and A.S. ay, 998, Evaluaing densiy forecass: Wih applicaions o financial risk managemen, Inernaional Economic Review, 9: Diebold, F.X., J.Y. Hanh and A.S. ay, 999, Mulivariae densiy forecas evaluaion and calibraion in financial risk managemen: High-frequency reurns on foreign exchange, Review of Economics and Saisics, 8: Garbade, K., 996, Fixed Income Analysis, Cambridge, MA: MI Press. 5

26 Gibson, R. and E. S. Schwarz, 99, Sochasic convenience yield and he pricing of oil coningen claims, Journal of Finance, 45(): Hazuka,.B., 984, Fuures markes: Consumpion beas and backwardaion in commodiy markes, Journal of Finance, 9(): , July. Hong, H.,, Sochasic convenience yield, opimal hedging and he erm srucure of open ineres and fuures prices, Working Paper. Hull, John C.,, Opions, Fuures and Oher Derivaives. New Jersey: Prenice Hall. Kaldor, N.,99, Speculaion and economic sabiliy, Review of Economic Sudies, 9: 7, Ocober. Ross, S.A., 995, Hedging long-run commimens: Exercises in incomplee marke pricing, Preliminary draf. Schwarz, E. S., 997, he sochasic behavior of commodiy prices: Implicaions for valuaion and hedging, Journal of Finance, 5(): Schwarz, S., 998, Valuing long-erm commodiy asses, Financial Managemen, 7(): Schwarz, S. and K. Milersen, 998, Pricing of opions on commodiy fuures wih sochasic erm srucures of convenience yield and ineres rae, Journal of Financial and Quaniaive Analysis, (): 59. Schwarz, S. and J. Smih,, Shor-erm variaions and long-erm dynamics in commodiy prices, Managemen Science,46(7): elser, L.G., 958, Fuures rading and he sorage of coon and whea, Journal of Poliical Economy, 66: 55. 6

27 Urich,.,, Modes of flucuaion in meal fuures prices, he Journal of Fuures Markes (): 9 4. X - FIGURES Figure : Oil fuures prices. 7

and backwardaion (posiive")

28 Figure : Behavior hrough ime o mauriy. Conango (negaive slope) and backwardaion (posiive slope). Figure : Behavior hrough ime o mauriy. Conango (negaive slope) and backwardaion (posiive slope) for Residuals. 8

29 APPENDIX I Geing expressions and 4. We proceed by firs finding he mean vecor and covariance marix for a discree-ime approximaion of he process based on he sochasic differenial equaions (), and hen ake he limi as he ime seps are made infiniesimally small. he discree-ime approximaion of he process wih ime seps of lengh = /n can be wrien as X i Q i+ ) X ( i+ ) + = ( ψ, (For i i= o n) where X = [ χ, ξ, η ], = φi, where φi = +, + ( i ) + ϕ Q i i ϕi = + and ψ is a x vecor of serially uncorrelaed, normally disribued + ( i ) + σ disurbance wih E[ψ ]= and Var[ ψ ] = W = ρ σ σ σ ρ σ σ. ρ σ σ ρ σ σ ρ σ σ ρ σ σ σ Wih his process, he i-sep ahead mean vecor ( m i ) and covariance marix ( V i ) are given recursively by m i = Q ( i+ ) m ( i+ ) and V i = Q ( i+ ) V ( i+ ) Q ( i+ ) + W, wih m = X = [ χ, ξ, η ] and V = (see, for example, Harvey 989, p. 9). Applying his recursion, we find: σ ρ σ σ a ρ σ σ c ( ) ( )( ) m [ χ +,, ] ξ = + ( + + )( + ) η ; V = ρ σ σ a σ b ρ σ σ f ρ σ σ c ρ σ σ f σ d les n=/, 9

30 n i a = { ( + )} n ( j n ) + n( + ), i= j= n i c = { ( + )} n ( j n ) + n( + ), i= j= n i f = { ( + )( + )} n ( j n ) + n( + ) ( j n ) + n( + ) i= j= b = + n ( j n ) + n( + ) n i { ( ) }, i= j= d = + n ( j n ) + n( + ) n i { ( ) }, i= j= Working wih hose expressions we found ha: n i+ n( + ) a = ( ), n + n( + ) i= n i+ n( + ) ( i ) + n( + ) c = ( ), n i= + n( + ) n( + ) n i+ n( + ) ( i ) + n( + ) f = {[ ] } n + n( + ) n( + ) i= n i+ n( + ) b = { }, n i= + n( + ) n i+ n( + ) ( i ) + n( + ) d = { }, n + n( + ) n( + ) i= I can be shown ha he limi as n goes infinie is: + + ( + ) a = ; b= + ; c= b; + ( + ) + ( + ) + ( + ) f = 4 +. ( + ) ( ) + + d = 5 + ; 4 ( + ) As can be seen all variables (a,b,c,d,f) depend on and. APPENDIX III he following approach is inspired by he work shown on Milersen-Schwarz (998). We will find he sochasic processes for he underlyngs ha make he process for F(,) a maringale (zero drif, F(, s) = E Q ( F, / s), s< < ):

31 Les dx = b (, s, X ) ds + σ () s dw where i, i i i s s s W s i independen each oher. X X X, s, s, s,,, = (,, ). X X X X = χ = ξ = η s s s. For convenience we will assume Q E [ f( X ) Xs = x] = u( s, x). u (, x) = f( x) By Io s lemma: u u u (, sx ) () s () s u b(, sx, ) s X X X i j i = σ σ + i, j, i,. (*) Bu, under he equivalen measure, our model implies ha,,, u( s, ) = X + X ( s + ) + X ( s + ), so: s s s u,, (, sx ) = + X + X ( s + ) s u u u (, sx ) = ; (, sx ) = s+ ; (, sx ) = ( s+ ),,, X X X his ranslae (*) ino he following equaion:,, + X + X s+ = b s X + b s X s+ + b s X s+. ( ) (,, ) (,, ) ( ) (,, ) ( ) Les assume he following family of expression for k k k, b (, s, X ) = g (, s ) h( X ). In his case, which is he simples one ha we can hink of, he soluion for b is unique, given by: b (, s ) =,,,, c, X g ( s, ) ( s+ ) h( X ) X = g ( s, ) = and h( X ) = s+ c,, d, X g ( s, ) ( s+ ) h( X ) ( s+ ) X = g ( s, ) = and h( X ) = s+ d, Be aware ha, under he previous soluion, he following properies hold:

32 E E E ( χ / s) = χ Q s ( s + ) ( ξ / s) = ξ s ( + ) Q ( s + ) ( η / s) = ηs ( + ) Q. - So we should go deep ino he possible negaiviy of observed values for he fuures prices series. Prof Luis A. Seco Dep. of Mahemaics Phone: (46) Fax: (46) Universiy of orono orono Onario M5S G, CANADA [email protected]

33 Ph.D Marcos Escobar-Anel Dep. of Mahemaics Phone: (46) Universiy of orono orono Onario M5S G, CANADA

Term Structure of Prices of Asian Options

Term Srucure of Prices of Asian Opions Jirô Akahori, Tsuomu Mikami, Kenji Yasuomi and Teruo Yokoa Dep. of Mahemaical Sciences, Risumeikan Universiy 1-1-1 Nojihigashi, Kusasu, Shiga 525-8577, Japan E-mail:

Term Srucure of Prices of Asian Opions Jirô Akahori, Tsuomu Mikami, Kenji Yasuomi and Teruo Yokoa Dep. of Mahemaical Sciences, Risumeikan Universiy 1-1-1 Nojihigashi, Kusasu, Shiga 525-8577, Japan E-mail:

MTH6121 Introduction to Mathematical Finance Lesson 5

26 MTH6121 Inroducion o Mahemaical Finance Lesson 5 Conens 2.3 Brownian moion wih drif........................... 27 2.4 Geomeric Brownian moion........................... 28 2.5 Convergence of random

26 MTH6121 Inroducion o Mahemaical Finance Lesson 5 Conens 2.3 Brownian moion wih drif........................... 27 2.4 Geomeric Brownian moion........................... 28 2.5 Convergence of random

A Note on Using the Svensson procedure to estimate the risk free rate in corporate valuation

A Noe on Using he Svensson procedure o esimae he risk free rae in corporae valuaion By Sven Arnold, Alexander Lahmann and Bernhard Schwezler Ocober 2011 1. The risk free ineres rae in corporae valuaion

A Noe on Using he Svensson procedure o esimae he risk free rae in corporae valuaion By Sven Arnold, Alexander Lahmann and Bernhard Schwezler Ocober 2011 1. The risk free ineres rae in corporae valuaion

Vector Autoregressions (VARs): Operational Perspectives

: Operational Perspectives") Vecor Auoregressions (VARs): Operaional Perspecives Primary Source: Sock, James H., and Mark W. Wason, Vecor Auoregressions, Journal of Economic Perspecives, Vol. 15 No. 4 (Fall 2001), 101-115. Macroeconomericians

Vecor Auoregressions (VARs): Operaional Perspecives Primary Source: Sock, James H., and Mark W. Wason, Vecor Auoregressions, Journal of Economic Perspecives, Vol. 15 No. 4 (Fall 2001), 101-115. Macroeconomericians

DYNAMIC MODELS FOR VALUATION OF WRONGFUL DEATH PAYMENTS

DYNAMIC MODELS FOR VALUATION OF WRONGFUL DEATH PAYMENTS Hong Mao, Shanghai Second Polyechnic Universiy Krzyszof M. Osaszewski, Illinois Sae Universiy Youyu Zhang, Fudan Universiy ABSTRACT Liigaion, exper

DYNAMIC MODELS FOR VALUATION OF WRONGFUL DEATH PAYMENTS Hong Mao, Shanghai Second Polyechnic Universiy Krzyszof M. Osaszewski, Illinois Sae Universiy Youyu Zhang, Fudan Universiy ABSTRACT Liigaion, exper

Journal Of Business & Economics Research September 2005 Volume 3, Number 9

Opion Pricing And Mone Carlo Simulaions George M. Jabbour, (Email: [email protected]), George Washingon Universiy Yi-Kang Liu, ([email protected]), George Washingon Universiy ABSTRACT The advanage of Mone Carlo

Opion Pricing And Mone Carlo Simulaions George M. Jabbour, (Email: [email protected]), George Washingon Universiy Yi-Kang Liu, ([email protected]), George Washingon Universiy ABSTRACT The advanage of Mone Carlo

Cointegration: The Engle and Granger approach

Coinegraion: The Engle and Granger approach Inroducion Generally one would find mos of he economic variables o be non-saionary I(1) variables. Hence, any equilibrium heories ha involve hese variables require

Coinegraion: The Engle and Granger approach Inroducion Generally one would find mos of he economic variables o be non-saionary I(1) variables. Hence, any equilibrium heories ha involve hese variables require

Stochastic Optimal Control Problem for Life Insurance

Sochasic Opimal Conrol Problem for Life Insurance s. Basukh 1, D. Nyamsuren 2 1 Deparmen of Economics and Economerics, Insiue of Finance and Economics, Ulaanbaaar, Mongolia 2 School of Mahemaics, Mongolian

Sochasic Opimal Conrol Problem for Life Insurance s. Basukh 1, D. Nyamsuren 2 1 Deparmen of Economics and Economerics, Insiue of Finance and Economics, Ulaanbaaar, Mongolia 2 School of Mahemaics, Mongolian

Chapter 7. Response of First-Order RL and RC Circuits

Chaper 7. esponse of Firs-Order L and C Circuis 7.1. The Naural esponse of an L Circui 7.2. The Naural esponse of an C Circui 7.3. The ep esponse of L and C Circuis 7.4. A General oluion for ep and Naural

Chaper 7. esponse of Firs-Order L and C Circuis 7.1. The Naural esponse of an L Circui 7.2. The Naural esponse of an C Circui 7.3. The ep esponse of L and C Circuis 7.4. A General oluion for ep and Naural

4. International Parity Conditions

4. Inernaional ariy ondiions 4.1 urchasing ower ariy he urchasing ower ariy ( heory is one of he early heories of exchange rae deerminaion. his heory is based on he concep ha he demand for a counry's currency

4. Inernaional ariy ondiions 4.1 urchasing ower ariy he urchasing ower ariy ( heory is one of he early heories of exchange rae deerminaion. his heory is based on he concep ha he demand for a counry's currency

The Transport Equation

The Transpor Equaion Consider a fluid, flowing wih velociy, V, in a hin sraigh ube whose cross secion will be denoed by A. Suppose he fluid conains a conaminan whose concenraion a posiion a ime will be

The Transpor Equaion Consider a fluid, flowing wih velociy, V, in a hin sraigh ube whose cross secion will be denoed by A. Suppose he fluid conains a conaminan whose concenraion a posiion a ime will be

INTEREST RATE FUTURES AND THEIR OPTIONS: SOME PRICING APPROACHES

INTEREST RATE FUTURES AND THEIR OPTIONS: SOME PRICING APPROACHES OPENGAMMA QUANTITATIVE RESEARCH Absrac. Exchange-raded ineres rae fuures and heir opions are described. The fuure opions include hose paying

INTEREST RATE FUTURES AND THEIR OPTIONS: SOME PRICING APPROACHES OPENGAMMA QUANTITATIVE RESEARCH Absrac. Exchange-raded ineres rae fuures and heir opions are described. The fuure opions include hose paying

A Probability Density Function for Google s stocks

A Probabiliy Densiy Funcion for Google s socks V.Dorobanu Physics Deparmen, Poliehnica Universiy of Timisoara, Romania Absrac. I is an approach o inroduce he Fokker Planck equaion as an ineresing naural

A Probabiliy Densiy Funcion for Google s socks V.Dorobanu Physics Deparmen, Poliehnica Universiy of Timisoara, Romania Absrac. I is an approach o inroduce he Fokker Planck equaion as an ineresing naural

The Greek financial crisis: growing imbalances and sovereign spreads. Heather D. Gibson, Stephan G. Hall and George S. Tavlas

The Greek financial crisis: growing imbalances and sovereign spreads Heaher D. Gibson, Sephan G. Hall and George S. Tavlas The enry The enry of Greece ino he Eurozone in 2001 produced a dividend in he

The Greek financial crisis: growing imbalances and sovereign spreads Heaher D. Gibson, Sephan G. Hall and George S. Tavlas The enry The enry of Greece ino he Eurozone in 2001 produced a dividend in he

Duration and Convexity ( ) 20 = Bond B has a maturity of 5 years and also has a required rate of return of 10%. Its price is $613.

20 = Bond B has a maturity of 5 years and also has a required rate of return of 10%. Its price is $613.") Graduae School of Business Adminisraion Universiy of Virginia UVA-F-38 Duraion and Convexiy he price of a bond is a funcion of he promised paymens and he marke required rae of reurn. Since he promised

Graduae School of Business Adminisraion Universiy of Virginia UVA-F-38 Duraion and Convexiy he price of a bond is a funcion of he promised paymens and he marke required rae of reurn. Since he promised

Modeling VIX Futures and Pricing VIX Options in the Jump Diusion Modeling

Modeling VIX Fuures and Pricing VIX Opions in he Jump Diusion Modeling Faemeh Aramian Maseruppsas i maemaisk saisik Maser hesis in Mahemaical Saisics Maseruppsas 2014:2 Maemaisk saisik April 2014 www.mah.su.se

Modeling VIX Fuures and Pricing VIX Opions in he Jump Diusion Modeling Faemeh Aramian Maseruppsas i maemaisk saisik Maser hesis in Mahemaical Saisics Maseruppsas 2014:2 Maemaisk saisik April 2014 www.mah.su.se

Usefulness of the Forward Curve in Forecasting Oil Prices

Usefulness of he Forward Curve in Forecasing Oil Prices Akira Yanagisawa Leader Energy Demand, Supply and Forecas Analysis Group The Energy Daa and Modelling Cener Summary When people analyse oil prices,

Usefulness of he Forward Curve in Forecasing Oil Prices Akira Yanagisawa Leader Energy Demand, Supply and Forecas Analysis Group The Energy Daa and Modelling Cener Summary When people analyse oil prices,

Hedging with Forwards and Futures

Hedging wih orwards and uures Hedging in mos cases is sraighforward. You plan o buy 10,000 barrels of oil in six monhs and you wish o eliminae he price risk. If you ake he buy-side of a forward/fuures

Hedging wih orwards and uures Hedging in mos cases is sraighforward. You plan o buy 10,000 barrels of oil in six monhs and you wish o eliminae he price risk. If you ake he buy-side of a forward/fuures

Principal components of stock market dynamics. Methodology and applications in brief (to be updated ) Andrei Bouzaev, bouzaev@ya.

Andrei Bouzaev, bouzaev@ya.") Principal componens of sock marke dynamics Mehodology and applicaions in brief o be updaed Andrei Bouzaev, [email protected] Why principal componens are needed Objecives undersand he evidence of more han one

Principal componens of sock marke dynamics Mehodology and applicaions in brief o be updaed Andrei Bouzaev, [email protected] Why principal componens are needed Objecives undersand he evidence of more han one

The Real Business Cycle paradigm. The RBC model emphasizes supply (technology) disturbances as the main source of

disturbances as the main source of") Prof. Harris Dellas Advanced Macroeconomics Winer 2001/01 The Real Business Cycle paradigm The RBC model emphasizes supply (echnology) disurbances as he main source of macroeconomic flucuaions in a world

Prof. Harris Dellas Advanced Macroeconomics Winer 2001/01 The Real Business Cycle paradigm The RBC model emphasizes supply (echnology) disurbances as he main source of macroeconomic flucuaions in a world

Technical Appendix to Risk, Return, and Dividends

Technical Appendix o Risk, Reurn, and Dividends Andrew Ang Columbia Universiy and NBER Jun Liu UC San Diego This Version: 28 Augus, 2006 Columbia Business School, 3022 Broadway 805 Uris, New York NY 10027,

Technical Appendix o Risk, Reurn, and Dividends Andrew Ang Columbia Universiy and NBER Jun Liu UC San Diego This Version: 28 Augus, 2006 Columbia Business School, 3022 Broadway 805 Uris, New York NY 10027,

PROFIT TEST MODELLING IN LIFE ASSURANCE USING SPREADSHEETS PART ONE

Profi Tes Modelling in Life Assurance Using Spreadshees PROFIT TEST MODELLING IN LIFE ASSURANCE USING SPREADSHEETS PART ONE Erik Alm Peer Millingon 2004 Profi Tes Modelling in Life Assurance Using Spreadshees

Profi Tes Modelling in Life Assurance Using Spreadshees PROFIT TEST MODELLING IN LIFE ASSURANCE USING SPREADSHEETS PART ONE Erik Alm Peer Millingon 2004 Profi Tes Modelling in Life Assurance Using Spreadshees

SPEC model selection algorithm for ARCH models: an options pricing evaluation framework

Applied Financial Economics Leers, 2008, 4, 419 423 SEC model selecion algorihm for ARCH models: an opions pricing evaluaion framework Savros Degiannakis a, * and Evdokia Xekalaki a,b a Deparmen of Saisics,

Applied Financial Economics Leers, 2008, 4, 419 423 SEC model selecion algorihm for ARCH models: an opions pricing evaluaion framework Savros Degiannakis a, * and Evdokia Xekalaki a,b a Deparmen of Saisics,

Option Put-Call Parity Relations When the Underlying Security Pays Dividends

Inernaional Journal of Business and conomics, 26, Vol. 5, No. 3, 225-23 Opion Pu-all Pariy Relaions When he Underlying Securiy Pays Dividends Weiyu Guo Deparmen of Finance, Universiy of Nebraska Omaha,

Inernaional Journal of Business and conomics, 26, Vol. 5, No. 3, 225-23 Opion Pu-all Pariy Relaions When he Underlying Securiy Pays Dividends Weiyu Guo Deparmen of Finance, Universiy of Nebraska Omaha,

CHARGE AND DISCHARGE OF A CAPACITOR

REFERENCES RC Circuis: Elecrical Insrumens: Mos Inroducory Physics exs (e.g. A. Halliday and Resnick, Physics ; M. Sernheim and J. Kane, General Physics.) This Laboraory Manual: Commonly Used Insrumens:

REFERENCES RC Circuis: Elecrical Insrumens: Mos Inroducory Physics exs (e.g. A. Halliday and Resnick, Physics ; M. Sernheim and J. Kane, General Physics.) This Laboraory Manual: Commonly Used Insrumens:

ARCH 2013.1 Proceedings

Aricle from: ARCH 213.1 Proceedings Augus 1-4, 212 Ghislain Leveille, Emmanuel Hamel A renewal model for medical malpracice Ghislain Léveillé École d acuaria Universié Laval, Québec, Canada 47h ARC Conference

Aricle from: ARCH 213.1 Proceedings Augus 1-4, 212 Ghislain Leveille, Emmanuel Hamel A renewal model for medical malpracice Ghislain Léveillé École d acuaria Universié Laval, Québec, Canada 47h ARC Conference

= r t dt + σ S,t db S t (19.1) with interest rates given by a mean reverting Ornstein-Uhlenbeck or Vasicek process,

with interest rates given by a mean reverting Ornstein-Uhlenbeck or Vasicek process,") Chaper 19 The Black-Scholes-Vasicek Model The Black-Scholes-Vasicek model is given by a sandard ime-dependen Black-Scholes model for he sock price process S, wih ime-dependen bu deerminisic volailiy σ

Chaper 19 The Black-Scholes-Vasicek Model The Black-Scholes-Vasicek model is given by a sandard ime-dependen Black-Scholes model for he sock price process S, wih ime-dependen bu deerminisic volailiy σ

LIFE INSURANCE WITH STOCHASTIC INTEREST RATE. L. Noviyanti a, M. Syamsuddin b

LIFE ISURACE WITH STOCHASTIC ITEREST RATE L. oviyani a, M. Syamsuddin b a Deparmen of Saisics, Universias Padjadjaran, Bandung, Indonesia b Deparmen of Mahemaics, Insiu Teknologi Bandung, Indonesia Absrac.

LIFE ISURACE WITH STOCHASTIC ITEREST RATE L. oviyani a, M. Syamsuddin b a Deparmen of Saisics, Universias Padjadjaran, Bandung, Indonesia b Deparmen of Mahemaics, Insiu Teknologi Bandung, Indonesia Absrac.

AP Calculus BC 2010 Scoring Guidelines

AP Calculus BC Scoring Guidelines The College Board The College Board is a no-for-profi membership associaion whose mission is o connec sudens o college success and opporuniy. Founded in, he College Board

AP Calculus BC Scoring Guidelines The College Board The College Board is a no-for-profi membership associaion whose mission is o connec sudens o college success and opporuniy. Founded in, he College Board

DYNAMIC ECONOMETRIC MODELS Vol. 7 Nicolaus Copernicus University Toruń 2006. Ryszard Doman Adam Mickiewicz University in Poznań

DYNAMIC ECONOMETRIC MODELS Vol. 7 Nicolaus Copernicus Universiy Toruń 26 1. Inroducion Adam Mickiewicz Universiy in Poznań Measuring Condiional Dependence of Polish Financial Reurns Idenificaion of condiional

DYNAMIC ECONOMETRIC MODELS Vol. 7 Nicolaus Copernicus Universiy Toruń 26 1. Inroducion Adam Mickiewicz Universiy in Poznań Measuring Condiional Dependence of Polish Financial Reurns Idenificaion of condiional

cooking trajectory boiling water B (t) microwave 0 2 4 6 8 101214161820 time t (mins)

microwave 0 2 4 6 8 101214161820 time t (mins)") Alligaor egg wih calculus We have a large alligaor egg jus ou of he fridge (1 ) which we need o hea o 9. Now here are wo accepable mehods for heaing alligaor eggs, one is o immerse hem in boiling waer

Alligaor egg wih calculus We have a large alligaor egg jus ou of he fridge (1 ) which we need o hea o 9. Now here are wo accepable mehods for heaing alligaor eggs, one is o immerse hem in boiling waer

Morningstar Investor Return

Morningsar Invesor Reurn Morningsar Mehodology Paper Augus 31, 2010 2010 Morningsar, Inc. All righs reserved. The informaion in his documen is he propery of Morningsar, Inc. Reproducion or ranscripion

Morningsar Invesor Reurn Morningsar Mehodology Paper Augus 31, 2010 2010 Morningsar, Inc. All righs reserved. The informaion in his documen is he propery of Morningsar, Inc. Reproducion or ranscripion

Stochastic Calculus and Option Pricing

Sochasic Calculus and Opion Pricing Leonid Kogan MIT, Sloan 15.450, Fall 2010 c Leonid Kogan ( MIT, Sloan ) Sochasic Calculus 15.450, Fall 2010 1 / 74 Ouline 1 Sochasic Inegral 2 Iô s Lemma 3 Black-Scholes

Sochasic Calculus and Opion Pricing Leonid Kogan MIT, Sloan 15.450, Fall 2010 c Leonid Kogan ( MIT, Sloan ) Sochasic Calculus 15.450, Fall 2010 1 / 74 Ouline 1 Sochasic Inegral 2 Iô s Lemma 3 Black-Scholes

Pricing Single Name Credit Derivatives

Pricing Single Name Credi Derivaives Vladimir Finkelsein 7h Annual CAP Workshop on Mahemaical Finance Columbia Universiy, New York December 1, 2 Ouline Realiies of he CDS marke Pricing Credi Defaul Swaps

Pricing Single Name Credi Derivaives Vladimir Finkelsein 7h Annual CAP Workshop on Mahemaical Finance Columbia Universiy, New York December 1, 2 Ouline Realiies of he CDS marke Pricing Credi Defaul Swaps

Chapter 8 Student Lecture Notes 8-1

Chaper Suden Lecure Noes - Chaper Goals QM: Business Saisics Chaper Analyzing and Forecasing -Series Daa Afer compleing his chaper, you should be able o: Idenify he componens presen in a ime series Develop

Chaper Suden Lecure Noes - Chaper Goals QM: Business Saisics Chaper Analyzing and Forecasing -Series Daa Afer compleing his chaper, you should be able o: Idenify he componens presen in a ime series Develop

Mathematics in Pharmacokinetics What and Why (A second attempt to make it clearer)

") Mahemaics in Pharmacokineics Wha and Why (A second aemp o make i clearer) We have used equaions for concenraion () as a funcion of ime (). We will coninue o use hese equaions since he plasma concenraions

Mahemaics in Pharmacokineics Wha and Why (A second aemp o make i clearer) We have used equaions for concenraion () as a funcion of ime (). We will coninue o use hese equaions since he plasma concenraions

Optimal Investment and Consumption Decision of Family with Life Insurance

Opimal Invesmen and Consumpion Decision of Family wih Life Insurance Minsuk Kwak 1 2 Yong Hyun Shin 3 U Jin Choi 4 6h World Congress of he Bachelier Finance Sociey Torono, Canada June 25, 2010 1 Speaker

Opimal Invesmen and Consumpion Decision of Family wih Life Insurance Minsuk Kwak 1 2 Yong Hyun Shin 3 U Jin Choi 4 6h World Congress of he Bachelier Finance Sociey Torono, Canada June 25, 2010 1 Speaker

Chapter 8: Regression with Lagged Explanatory Variables

Chaper 8: Regression wih Lagged Explanaory Variables Time series daa: Y for =1,..,T End goal: Regression model relaing a dependen variable o explanaory variables. Wih ime series new issues arise: 1. One

Chaper 8: Regression wih Lagged Explanaory Variables Time series daa: Y for =1,..,T End goal: Regression model relaing a dependen variable o explanaory variables. Wih ime series new issues arise: 1. One

Skewness and Kurtosis Adjusted Black-Scholes Model: A Note on Hedging Performance

Finance Leers, 003, (5), 6- Skewness and Kurosis Adjused Black-Scholes Model: A Noe on Hedging Performance Sami Vähämaa * Universiy of Vaasa, Finland Absrac his aricle invesigaes he dela hedging performance

Finance Leers, 003, (5), 6- Skewness and Kurosis Adjused Black-Scholes Model: A Noe on Hedging Performance Sami Vähämaa * Universiy of Vaasa, Finland Absrac his aricle invesigaes he dela hedging performance

AP Calculus AB 2013 Scoring Guidelines

AP Calculus AB 1 Scoring Guidelines The College Board The College Board is a mission-driven no-for-profi organizaion ha connecs sudens o college success and opporuniy. Founded in 19, he College Board was

AP Calculus AB 1 Scoring Guidelines The College Board The College Board is a mission-driven no-for-profi organizaion ha connecs sudens o college success and opporuniy. Founded in 19, he College Board was

How To Price An Opion

HE PERFORMANE OF OPION PRIING MODEL ON HEDGING EXOI OPION Firs Draf: May 5 003 his Version Oc. 30 003 ommens are welcome Absrac his paper examines he empirical performance of various opion pricing models

HE PERFORMANE OF OPION PRIING MODEL ON HEDGING EXOI OPION Firs Draf: May 5 003 his Version Oc. 30 003 ommens are welcome Absrac his paper examines he empirical performance of various opion pricing models

Distributing Human Resources among Software Development Projects 1

Disribuing Human Resources among Sofware Developmen Proecs Macario Polo, María Dolores Maeos, Mario Piaini and rancisco Ruiz Summary This paper presens a mehod for esimaing he disribuion of human resources

Disribuing Human Resources among Sofware Developmen Proecs Macario Polo, María Dolores Maeos, Mario Piaini and rancisco Ruiz Summary This paper presens a mehod for esimaing he disribuion of human resources

Why Did the Demand for Cash Decrease Recently in Korea?

Why Did he Demand for Cash Decrease Recenly in Korea? Byoung Hark Yoo Bank of Korea 26. 5 Absrac We explores why cash demand have decreased recenly in Korea. The raio of cash o consumpion fell o 4.7% in

Why Did he Demand for Cash Decrease Recenly in Korea? Byoung Hark Yoo Bank of Korea 26. 5 Absrac We explores why cash demand have decreased recenly in Korea. The raio of cash o consumpion fell o 4.7% in

The naive method discussed in Lecture 1 uses the most recent observations to forecast future values. That is, Y ˆ t + 1

Business Condiions & Forecasing Exponenial Smoohing LECTURE 2 MOVING AVERAGES AND EXPONENTIAL SMOOTHING OVERVIEW This lecure inroduces ime-series smoohing forecasing mehods. Various models are discussed,

Business Condiions & Forecasing Exponenial Smoohing LECTURE 2 MOVING AVERAGES AND EXPONENTIAL SMOOTHING OVERVIEW This lecure inroduces ime-series smoohing forecasing mehods. Various models are discussed,

A Generalized Bivariate Ornstein-Uhlenbeck Model for Financial Assets

A Generalized Bivariae Ornsein-Uhlenbeck Model for Financial Asses Romy Krämer, Mahias Richer Technische Universiä Chemniz, Fakulä für Mahemaik, 917 Chemniz, Germany Absrac In his paper, we sudy mahemaical

A Generalized Bivariae Ornsein-Uhlenbeck Model for Financial Asses Romy Krämer, Mahias Richer Technische Universiä Chemniz, Fakulä für Mahemaik, 917 Chemniz, Germany Absrac In his paper, we sudy mahemaical

Stability. Coefficients may change over time. Evolution of the economy Policy changes

Sabiliy Coefficiens may change over ime Evoluion of he economy Policy changes Time Varying Parameers y = α + x β + Coefficiens depend on he ime period If he coefficiens vary randomly and are unpredicable,

Sabiliy Coefficiens may change over ime Evoluion of he economy Policy changes Time Varying Parameers y = α + x β + Coefficiens depend on he ime period If he coefficiens vary randomly and are unpredicable,

Mortality Variance of the Present Value (PV) of Future Annuity Payments

of Future Annuity Payments") Morali Variance of he Presen Value (PV) of Fuure Annui Pamens Frank Y. Kang, Ph.D. Research Anals a Frank Russell Compan Absrac The variance of he presen value of fuure annui pamens plas an imporan role

Morali Variance of he Presen Value (PV) of Fuure Annui Pamens Frank Y. Kang, Ph.D. Research Anals a Frank Russell Compan Absrac The variance of he presen value of fuure annui pamens plas an imporan role

Pricing Fixed-Income Derivaives wih he Forward-Risk Adjused Measure Jesper Lund Deparmen of Finance he Aarhus School of Business DK-8 Aarhus V, Denmark E-mail: [email protected] Homepage: www.hha.dk/~jel/ Firs

Pricing Fixed-Income Derivaives wih he Forward-Risk Adjused Measure Jesper Lund Deparmen of Finance he Aarhus School of Business DK-8 Aarhus V, Denmark E-mail: [email protected] Homepage: www.hha.dk/~jel/ Firs

Credit Index Options: the no-armageddon pricing measure and the role of correlation after the subprime crisis

Second Conference on The Mahemaics of Credi Risk, Princeon May 23-24, 2008 Credi Index Opions: he no-armageddon pricing measure and he role of correlaion afer he subprime crisis Damiano Brigo - Join work

Second Conference on The Mahemaics of Credi Risk, Princeon May 23-24, 2008 Credi Index Opions: he no-armageddon pricing measure and he role of correlaion afer he subprime crisis Damiano Brigo - Join work

APPLICATION OF THE KALMAN FILTER FOR ESTIMATING CONTINUOUS TIME TERM STRUCTURE MODELS: THE CASE OF UK AND GERMANY. January, 2005

APPLICATION OF THE KALMAN FILTER FOR ESTIMATING CONTINUOUS TIME TERM STRUCTURE MODELS: THE CASE OF UK AND GERMANY Somnah Chaeree* Deparmen of Economics Universiy of Glasgow January, 2005 Absrac The purpose

APPLICATION OF THE KALMAN FILTER FOR ESTIMATING CONTINUOUS TIME TERM STRUCTURE MODELS: THE CASE OF UK AND GERMANY Somnah Chaeree* Deparmen of Economics Universiy of Glasgow January, 2005 Absrac The purpose

11/6/2013. Chapter 14: Dynamic AD-AS. Introduction. Introduction. Keeping track of time. The model s elements

Inroducion Chaper 14: Dynamic D-S dynamic model of aggregae and aggregae supply gives us more insigh ino how he economy works in he shor run. I is a simplified version of a DSGE model, used in cuing-edge

Inroducion Chaper 14: Dynamic D-S dynamic model of aggregae and aggregae supply gives us more insigh ino how he economy works in he shor run. I is a simplified version of a DSGE model, used in cuing-edge

Random Walk in 1-D. 3 possible paths x vs n. -5 For our random walk, we assume the probabilities p,q do not depend on time (n) - stationary

- stationary") Random Walk in -D Random walks appear in many cones: diffusion is a random walk process undersanding buffering, waiing imes, queuing more generally he heory of sochasic processes gambling choosing he bes

Random Walk in -D Random walks appear in many cones: diffusion is a random walk process undersanding buffering, waiing imes, queuing more generally he heory of sochasic processes gambling choosing he bes

The option pricing framework

Chaper 2 The opion pricing framework The opion markes based on swap raes or he LIBOR have become he larges fixed income markes, and caps (floors) and swapions are he mos imporan derivaives wihin hese markes.

Chaper 2 The opion pricing framework The opion markes based on swap raes or he LIBOR have become he larges fixed income markes, and caps (floors) and swapions are he mos imporan derivaives wihin hese markes.

Measuring macroeconomic volatility Applications to export revenue data, 1970-2005

FONDATION POUR LES ETUDES ET RERS LE DEVELOPPEMENT INTERNATIONAL Measuring macroeconomic volailiy Applicaions o expor revenue daa, 1970-005 by Joël Cariolle Policy brief no. 47 March 01 The FERDI is a

FONDATION POUR LES ETUDES ET RERS LE DEVELOPPEMENT INTERNATIONAL Measuring macroeconomic volailiy Applicaions o expor revenue daa, 1970-005 by Joël Cariolle Policy brief no. 47 March 01 The FERDI is a

DOES TRADING VOLUME INFLUENCE GARCH EFFECTS? SOME EVIDENCE FROM THE GREEK MARKET WITH SPECIAL REFERENCE TO BANKING SECTOR

Invesmen Managemen and Financial Innovaions, Volume 4, Issue 3, 7 33 DOES TRADING VOLUME INFLUENCE GARCH EFFECTS? SOME EVIDENCE FROM THE GREEK MARKET WITH SPECIAL REFERENCE TO BANKING SECTOR Ahanasios

Invesmen Managemen and Financial Innovaions, Volume 4, Issue 3, 7 33 DOES TRADING VOLUME INFLUENCE GARCH EFFECTS? SOME EVIDENCE FROM THE GREEK MARKET WITH SPECIAL REFERENCE TO BANKING SECTOR Ahanasios

ON THE PRICING OF EQUITY-LINKED LIFE INSURANCE CONTRACTS IN GAUSSIAN FINANCIAL ENVIRONMENT

Teor Imov r.amaem.sais. Theor. Probabiliy and Mah. Sais. Vip. 7, 24 No. 7, 25, Pages 15 111 S 94-9(5)634-4 Aricle elecronically published on Augus 12, 25 ON THE PRICING OF EQUITY-LINKED LIFE INSURANCE

Teor Imov r.amaem.sais. Theor. Probabiliy and Mah. Sais. Vip. 7, 24 No. 7, 25, Pages 15 111 S 94-9(5)634-4 Aricle elecronically published on Augus 12, 25 ON THE PRICING OF EQUITY-LINKED LIFE INSURANCE

BALANCE OF PAYMENTS. First quarter 2008. Balance of payments

BALANCE OF PAYMENTS DATE: 2008-05-30 PUBLISHER: Balance of Paymens and Financial Markes (BFM) Lena Finn + 46 8 506 944 09, [email protected] Camilla Bergeling +46 8 506 942 06, [email protected]

BALANCE OF PAYMENTS DATE: 2008-05-30 PUBLISHER: Balance of Paymens and Financial Markes (BFM) Lena Finn + 46 8 506 944 09, [email protected] Camilla Bergeling +46 8 506 942 06, [email protected]

Acceleration Lab Teacher s Guide

Acceleraion Lab Teacher s Guide Objecives:. Use graphs of disance vs. ime and velociy vs. ime o find acceleraion of a oy car.. Observe he relaionship beween he angle of an inclined plane and he acceleraion

Acceleraion Lab Teacher s Guide Objecives:. Use graphs of disance vs. ime and velociy vs. ime o find acceleraion of a oy car.. Observe he relaionship beween he angle of an inclined plane and he acceleraion

ABSTRACT KEYWORDS. Term structure, duration, uncertain cash flow, variable rates of return JEL codes: C33, E43 1. INTRODUCTION

THE VALUATION AND HEDGING OF VARIABLE RATE SAVINGS ACCOUNTS BY FRANK DE JONG 1 AND JACCO WIELHOUWER ABSTRACT Variable rae savings accouns have wo main feaures. The ineres rae paid on he accoun is variable

THE VALUATION AND HEDGING OF VARIABLE RATE SAVINGS ACCOUNTS BY FRANK DE JONG 1 AND JACCO WIELHOUWER ABSTRACT Variable rae savings accouns have wo main feaures. The ineres rae paid on he accoun is variable

Estimating Time-Varying Equity Risk Premium The Japanese Stock Market 1980-2012

Norhfield Asia Research Seminar Hong Kong, November 19, 2013 Esimaing Time-Varying Equiy Risk Premium The Japanese Sock Marke 1980-2012 Ibboson Associaes Japan Presiden Kasunari Yamaguchi, PhD/CFA/CMA

Norhfield Asia Research Seminar Hong Kong, November 19, 2013 Esimaing Time-Varying Equiy Risk Premium The Japanese Sock Marke 1980-2012 Ibboson Associaes Japan Presiden Kasunari Yamaguchi, PhD/CFA/CMA

The Grantor Retained Annuity Trust (GRAT)

") WEALTH ADVISORY Esae Planning Sraegies for closely-held, family businesses The Granor Reained Annuiy Trus (GRAT) An efficien wealh ransfer sraegy, paricularly in a low ineres rae environmen Family business

WEALTH ADVISORY Esae Planning Sraegies for closely-held, family businesses The Granor Reained Annuiy Trus (GRAT) An efficien wealh ransfer sraegy, paricularly in a low ineres rae environmen Family business

MACROECONOMIC FORECASTS AT THE MOF A LOOK INTO THE REAR VIEW MIRROR

MACROECONOMIC FORECASTS AT THE MOF A LOOK INTO THE REAR VIEW MIRROR The firs experimenal publicaion, which summarised pas and expeced fuure developmen of basic economic indicaors, was published by he Minisry

MACROECONOMIC FORECASTS AT THE MOF A LOOK INTO THE REAR VIEW MIRROR The firs experimenal publicaion, which summarised pas and expeced fuure developmen of basic economic indicaors, was published by he Minisry

ANALYSIS AND COMPARISONS OF SOME SOLUTION CONCEPTS FOR STOCHASTIC PROGRAMMING PROBLEMS

ANALYSIS AND COMPARISONS OF SOME SOLUTION CONCEPTS FOR STOCHASTIC PROGRAMMING PROBLEMS R. Caballero, E. Cerdá, M. M. Muñoz and L. Rey () Deparmen of Applied Economics (Mahemaics), Universiy of Málaga,

ANALYSIS AND COMPARISONS OF SOME SOLUTION CONCEPTS FOR STOCHASTIC PROGRAMMING PROBLEMS R. Caballero, E. Cerdá, M. M. Muñoz and L. Rey () Deparmen of Applied Economics (Mahemaics), Universiy of Málaga,

Individual Health Insurance April 30, 2008 Pages 167-170

Individual Healh Insurance April 30, 2008 Pages 167-170 We have received feedback ha his secion of he e is confusing because some of he defined noaion is inconsisen wih comparable life insurance reserve

Individual Healh Insurance April 30, 2008 Pages 167-170 We have received feedback ha his secion of he e is confusing because some of he defined noaion is inconsisen wih comparable life insurance reserve

The Application of Multi Shifts and Break Windows in Employees Scheduling

The Applicaion of Muli Shifs and Brea Windows in Employees Scheduling Evy Herowai Indusrial Engineering Deparmen, Universiy of Surabaya, Indonesia Absrac. One mehod for increasing company s performance

The Applicaion of Muli Shifs and Brea Windows in Employees Scheduling Evy Herowai Indusrial Engineering Deparmen, Universiy of Surabaya, Indonesia Absrac. One mehod for increasing company s performance

DEMAND FORECASTING MODELS

DEMAND FORECASTING MODELS Conens E-2. ELECTRIC BILLED SALES AND CUSTOMER COUNTS Sysem-level Model Couny-level Model Easside King Couny-level Model E-6. ELECTRIC PEAK HOUR LOAD FORECASTING Sysem-level Forecas

DEMAND FORECASTING MODELS Conens E-2. ELECTRIC BILLED SALES AND CUSTOMER COUNTS Sysem-level Model Couny-level Model Easside King Couny-level Model E-6. ELECTRIC PEAK HOUR LOAD FORECASTING Sysem-level Forecas

RiskMetrics TM Technical Document

.P.Morgan/Reuers RiskMerics TM Technical Documen Fourh Ediion, 1996 New York December 17, 1996.P. Morgan and Reuers have eamed up o enhance RiskMerics. Morgan will coninue o be responsible for enhancing

.P.Morgan/Reuers RiskMerics TM Technical Documen Fourh Ediion, 1996 New York December 17, 1996.P. Morgan and Reuers have eamed up o enhance RiskMerics. Morgan will coninue o be responsible for enhancing

Efficient Pricing of Energy Derivatives

Efficien Pricing of Energy Derivaives Anders B. Trolle EPFL and Swiss Finance Insiue March 1, 2014 Absrac I presen a racable framework, firs developed in Trolle and Schwarz (2009), for pricing energy derivaives

Efficien Pricing of Energy Derivaives Anders B. Trolle EPFL and Swiss Finance Insiue March 1, 2014 Absrac I presen a racable framework, firs developed in Trolle and Schwarz (2009), for pricing energy derivaives

Stochastic Volatility Models: Considerations for the Lay Actuary 1. Abstract

Sochasic Volailiy Models: Consideraions for he Lay Acuary 1 Phil Jouber Coomaren Vencaasawmy (Presened o he Finance & Invesmen Conference, 19-1 June 005) Absrac Sochasic models for asse prices processes

Sochasic Volailiy Models: Consideraions for he Lay Acuary 1 Phil Jouber Coomaren Vencaasawmy (Presened o he Finance & Invesmen Conference, 19-1 June 005) Absrac Sochasic models for asse prices processes

Time Consisency in Porfolio Managemen

1 Time Consisency in Porfolio Managemen Traian A Pirvu Deparmen of Mahemaics and Saisics McMaser Universiy Torono, June 2010 The alk is based on join work wih Ivar Ekeland Time Consisency in Porfolio Managemen

1 Time Consisency in Porfolio Managemen Traian A Pirvu Deparmen of Mahemaics and Saisics McMaser Universiy Torono, June 2010 The alk is based on join work wih Ivar Ekeland Time Consisency in Porfolio Managemen

Appendix A: Area. 1 Find the radius of a circle that has circumference 12 inches.

Appendi A: Area worked-ou s o Odd-Numbered Eercises Do no read hese worked-ou s before aemping o do he eercises ourself. Oherwise ou ma mimic he echniques shown here wihou undersanding he ideas. Bes wa

Appendi A: Area worked-ou s o Odd-Numbered Eercises Do no read hese worked-ou s before aemping o do he eercises ourself. Oherwise ou ma mimic he echniques shown here wihou undersanding he ideas. Bes wa

Table of contents Chapter 1 Interest rates and factors Chapter 2 Level annuities Chapter 3 Varying annuities

Table of conens Chaper 1 Ineres raes and facors 1 1.1 Ineres 2 1.2 Simple ineres 4 1.3 Compound ineres 6 1.4 Accumulaed value 10 1.5 Presen value 11 1.6 Rae of discoun 13 1.7 Consan force of ineres 17

Table of conens Chaper 1 Ineres raes and facors 1 1.1 Ineres 2 1.2 Simple ineres 4 1.3 Compound ineres 6 1.4 Accumulaed value 10 1.5 Presen value 11 1.6 Rae of discoun 13 1.7 Consan force of ineres 17

Option Pricing Under Stochastic Interest Rates

I.J. Engineering and Manufacuring, 0,3, 8-89 ublished Online June 0 in MECS (hp://www.mecs-press.ne) DOI: 0.585/ijem.0.03. Available online a hp://www.mecs-press.ne/ijem Opion ricing Under Sochasic Ineres

I.J. Engineering and Manufacuring, 0,3, 8-89 ublished Online June 0 in MECS (hp://www.mecs-press.ne) DOI: 0.585/ijem.0.03. Available online a hp://www.mecs-press.ne/ijem Opion ricing Under Sochasic Ineres

TEMPORAL PATTERN IDENTIFICATION OF TIME SERIES DATA USING PATTERN WAVELETS AND GENETIC ALGORITHMS

TEMPORAL PATTERN IDENTIFICATION OF TIME SERIES DATA USING PATTERN WAVELETS AND GENETIC ALGORITHMS RICHARD J. POVINELLI AND XIN FENG Deparmen of Elecrical and Compuer Engineering Marquee Universiy, P.O.

TEMPORAL PATTERN IDENTIFICATION OF TIME SERIES DATA USING PATTERN WAVELETS AND GENETIC ALGORITHMS RICHARD J. POVINELLI AND XIN FENG Deparmen of Elecrical and Compuer Engineering Marquee Universiy, P.O.

How To Write A Demand And Price Model For A Supply Chain

Proc. Schl. ITE Tokai Univ. vol.3,no,,pp.37-4 Vol.,No.,,pp. - Paper Demand and Price Forecasing Models for Sraegic and Planning Decisions in a Supply Chain by Vichuda WATTANARAT *, Phounsakda PHIMPHAVONG

Proc. Schl. ITE Tokai Univ. vol.3,no,,pp.37-4 Vol.,No.,,pp. - Paper Demand and Price Forecasing Models for Sraegic and Planning Decisions in a Supply Chain by Vichuda WATTANARAT *, Phounsakda PHIMPHAVONG

4 Convolution. Recommended Problems. x2[n] 1 2[n]

![4 Convolution. Recommended Problems. x2[n] 1 2[n]](/thumbs/40/21827733.jpg "4 Convolution. Recommended Problems. x2[n] 1 2[n]") 4 Convoluion Recommended Problems P4.1 This problem is a simple example of he use of superposiion. Suppose ha a discree-ime linear sysem has oupus y[n] for he given inpus x[n] as shown in Figure P4.1-1.

4 Convoluion Recommended Problems P4.1 This problem is a simple example of he use of superposiion. Suppose ha a discree-ime linear sysem has oupus y[n] for he given inpus x[n] as shown in Figure P4.1-1.

Optimal Time to Sell in Real Estate Portfolio Management

Opimal ime o Sell in Real Esae Porfolio Managemen Fabrice Barhélémy and Jean-Luc Prigen hema, Universiy of Cergy-Ponoise, Cergy-Ponoise, France E-mails: fabricebarhelemy@u-cergyfr; jean-lucprigen@u-cergyfr

Opimal ime o Sell in Real Esae Porfolio Managemen Fabrice Barhélémy and Jean-Luc Prigen hema, Universiy of Cergy-Ponoise, Cergy-Ponoise, France E-mails: fabricebarhelemy@u-cergyfr; jean-lucprigen@u-cergyfr

UNDERSTANDING THE DEATH BENEFIT SWITCH OPTION IN UNIVERSAL LIFE POLICIES. Nadine Gatzert

UNDERSTANDING THE DEATH BENEFIT SWITCH OPTION IN UNIVERSAL LIFE POLICIES Nadine Gazer Conac (has changed since iniial submission): Chair for Insurance Managemen Universiy of Erlangen-Nuremberg Lange Gasse

UNDERSTANDING THE DEATH BENEFIT SWITCH OPTION IN UNIVERSAL LIFE POLICIES Nadine Gazer Conac (has changed since iniial submission): Chair for Insurance Managemen Universiy of Erlangen-Nuremberg Lange Gasse

Lead Lag Relationships between Futures and Spot Prices

Working Paper No. 2/02 Lead Lag Relaionships beween Fuures and Spo Prices by Frank Asche Ale G. Guormsen SNF-projec No. 7220: Gassmarkeder, menneskelig kapial og selskapssraegier The projec is financed

Working Paper No. 2/02 Lead Lag Relaionships beween Fuures and Spo Prices by Frank Asche Ale G. Guormsen SNF-projec No. 7220: Gassmarkeder, menneskelig kapial og selskapssraegier The projec is financed

Analogue and Digital Signal Processing. First Term Third Year CS Engineering By Dr Mukhtiar Ali Unar

Analogue and Digial Signal Processing Firs Term Third Year CS Engineering By Dr Mukhiar Ali Unar Recommended Books Haykin S. and Van Veen B.; Signals and Sysems, John Wiley& Sons Inc. ISBN: 0-7-380-7 Ifeachor

Analogue and Digial Signal Processing Firs Term Third Year CS Engineering By Dr Mukhiar Ali Unar Recommended Books Haykin S. and Van Veen B.; Signals and Sysems, John Wiley& Sons Inc. ISBN: 0-7-380-7 Ifeachor

Dependent Interest and Transition Rates in Life Insurance

Dependen Ineres and ransiion Raes in Life Insurance Krisian Buchard Universiy of Copenhagen and PFA Pension January 28, 2013 Absrac In order o find marke consisen bes esimaes of life insurance liabiliies

Dependen Ineres and ransiion Raes in Life Insurance Krisian Buchard Universiy of Copenhagen and PFA Pension January 28, 2013 Absrac In order o find marke consisen bes esimaes of life insurance liabiliies

Chapter 9 Bond Prices and Yield

Chaper 9 Bond Prices and Yield Deb Classes: Paymen ype A securiy obligaing issuer o pay ineress and principal o he holder on specified daes, Coupon rae or ineres rae, e.g. 4%, 5 3/4%, ec. Face, par value

Chaper 9 Bond Prices and Yield Deb Classes: Paymen ype A securiy obligaing issuer o pay ineress and principal o he holder on specified daes, Coupon rae or ineres rae, e.g. 4%, 5 3/4%, ec. Face, par value

THE FIRM'S INVESTMENT DECISION UNDER CERTAINTY: CAPITAL BUDGETING AND RANKING OF NEW INVESTMENT PROJECTS

VII. THE FIRM'S INVESTMENT DECISION UNDER CERTAINTY: CAPITAL BUDGETING AND RANKING OF NEW INVESTMENT PROJECTS The mos imporan decisions for a firm's managemen are is invesmen decisions. While i is surely

VII. THE FIRM'S INVESTMENT DECISION UNDER CERTAINTY: CAPITAL BUDGETING AND RANKING OF NEW INVESTMENT PROJECTS The mos imporan decisions for a firm's managemen are is invesmen decisions. While i is surely

Key Words: Steel Modelling, ARMA, GARCH, COGARCH, Lévy Processes, Discrete Time Models, Continuous Time Models, Stochastic Modelling

Vol 4, No, 01 ISSN: 1309-8055 (Online STEEL PRICE MODELLING WITH LEVY PROCESS Emre Kahraman Türk Ekonomi Bankası (TEB A.Ş. Direcor / Risk Capial Markes Deparmen [email protected] Gazanfer Unal Yediepe

Vol 4, No, 01 ISSN: 1309-8055 (Online STEEL PRICE MODELLING WITH LEVY PROCESS Emre Kahraman Türk Ekonomi Bankası (TEB A.Ş. Direcor / Risk Capial Markes Deparmen [email protected] Gazanfer Unal Yediepe

Risk Modelling of Collateralised Lending