Understand the relationship between financial plans and statements.

|

|

|

- Leonard Harvey

- 10 years ago

- Views:

Transcription

1 #2 Budget Development Your Financial Statements and Plans

2 Learning Goals Understand the relationship between financial plans and statements. Prepare a personal balance sheet. Generate a personal income and expense statement. Develop a good record-keeping system and use ratios to evaluate personal financial statements. Construct a cash budget and use it to monitor and control spending. Apply time vale of money concepts to put a monetary value on financial goals.

3 Mapping Out Your Financial Future Financial planning facilitates: Greater Wealth Financial Security Attainment of Financial Goals

4 The Interlocking Network of Financial Plans and Statements

5 Balance Sheet A statement of your financial position at a given point in time

6 Balance Sheet Equation Total Liabilities Total Assets = + Net Worth

7 Assets: Things You Own Liquid assets low-risk, cash or investments that can be converted to cash with little or no loss in value Investments acquired to earn a return Real property immovable property including land or a house Personal Property movable property such as autos and home furnishings

8 Liabilities: Money You Owe Classification by Maturity Current or short-term -- due within a year such as utility or repair bills Long-term -- due in a year or more including mortgages, education and consumer installment loans

9 Net Worth: Measure of Your Financial Worth Actual wealth or equity that individuals have in owned assets Net worth = total assets total liabilities Net worth > 0 = SOLVENT Net worth < 0 = INSOLVENT

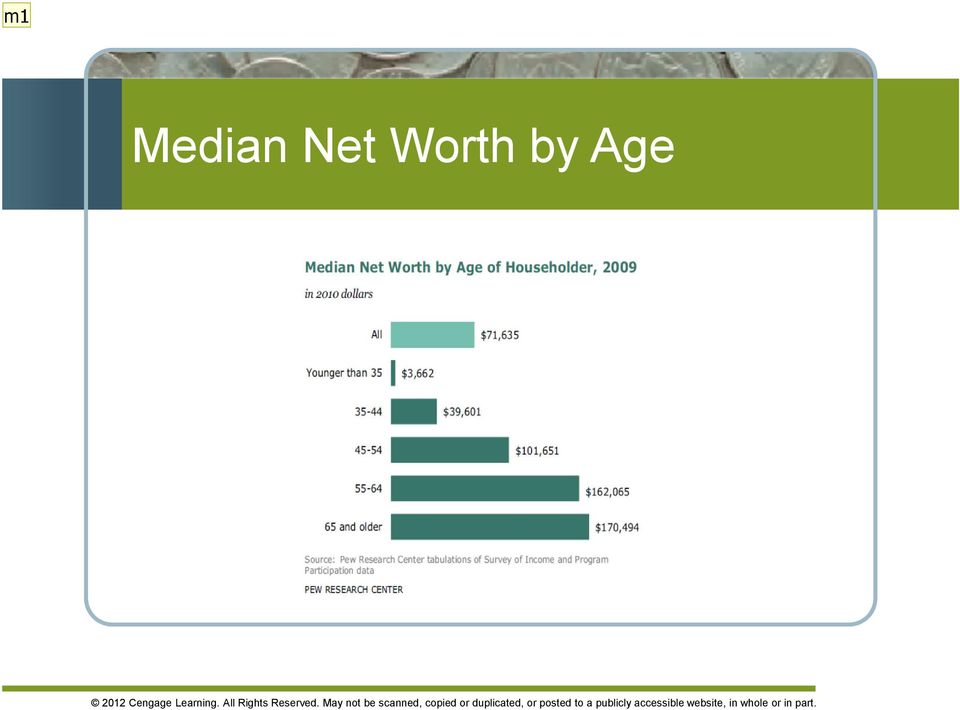

10 m1 Median Net Worth by Age

11 Slide 10 m1 This misuracajia, 11/18/2012

12 The Income and Expense Statement A measure of financial performance over a given time period income (cash in) expenses (cash out) cash surplus (or deficit)

cash surplus (or")

13 Income and Expense Statement Total Income Total Expenses = CASH SURPLUS OR (CASH DEFICIT)

14 Income: Cash In Wages and salaries Bonuses and commissions Interest and dividends Child support Tax refunds Gifts

15 Expenses: Cash Out Living Expenses -- Housing, utilities, food, insurance Tax Payments -- Federal, state, local Asset Purchases -- Autos, furniture, appliances Other Payments -- Personal care, recreation, entertainment

16 Expenses: Cash Out Fixed Contractual, equal payments fixed rent or mortgage, insurance, cable TV payments Variable Amounts change from one period to the next credit card payments

17 Preparing the Income and Expense Statements Record your income from all sources for the chosen period. Establish meaningful expense categories. Subtract total expenses from total income to get cash surplus or deficit.

18 How We Spend Our Income

19 Using Your Personal Financial Statements Keeping good records Organize records Tracking financial progress Ratio Analysis Balance Sheet Ratios Income and Expense Statement Ratios

20 Balance Sheet Ratios Solvency Ratio hnet worth at a given point in time hindicates potential to withstand financial problems Total net worth Total assets

21 Liquidity Ratios hmeasures ability to pay current debts with existing liquid assets h Current = payment within one year Total Liquid assets Total current debts

22 Income & Expense Statement Ratios Savings Ratio hshows percentage of after-tax income saved during a time period Cash surplus Income after taxes

23 Debt Service Ratio Indicates ability to repay loan obligations promptly with before-tax income Total monthly loan payments Monthly gross (before-tax) income

24 Preparing & Using Budgets Budget Short-term financial planning report that helps you achieve short-term financial goals Achieving short-term goals helps you achieve longer-term goals

25 Using Budgets Monitor and control finances Allocate income to reach goals Implement disciplined spending Reduce needless spending Achieve long-term financial goals

26 The Budgeting Process Estimating Income Estimating Expenses Finalize the Cash Budget

27 Dealing with Deficits Shift expenses from months with deficits to months with surpluses Use savings, investments, or borrowing to cover temporary deficits

28 If You End the Year in a Deficit Liquidate savings/investments Borrow to cover the deficit Cut low priority expenses; alter spending habits Increase income

29 Using Your Budgets Budget Control Schedule compares actual figures with various budget categories and shows variances Continually update your budget based upon the actual figures.

30 Time Value of Money Putting a Dollar Value on Financial Goals A dollar today is worth more than a dollar received in the future because it can be invested and earn interest.

31 Types of TVM Calculations Single sum one lump sum investment with no additions or subtractions Annuity series of equal payments made at fixed time intervals for a specified number of periods

32 Future Value Value invested money will grow to become earning a specific rate of interest over a given time period Process of growing today s present value to a larger future value by applying compound interest known as compounding.

33 Calculating the Future Value of a Single Sum Example: What will $5,000 grow to become if invested at 5% for 6 years?

34 Calculating the Future Value of a Single Sum Tables (Find Future Value Factor for 6 years and 5% in Appendix A) FV = PV x Factor $5,000 x = $6,700

35 Calculating the Future Value of an Annuity Example: What would you accumulate if you could invest $5, every year for the next 6 years at 5%?

36 Calculating the Future Value of an Annuity Tables (Find Future Value Annuity Factor for 6 years and 5% in Appendix B) FV = PMT x Factor $5, x = $38,300

37 Present Value Amount needed today to invest at a specific rate of interest over a given time period to accumulate a desired future amount Discounting is the reverse of compounding - process of working from the future value back to present value

38 Calculating the Present Value of a Single Sum Example: You wish to accumulate a retirement fund of $300,000 in 25 years. If you can invest at 5%, what single lumpsum deposit must you make today in order to achieve your goal?

39 Calculating the Present Value of a Single Sum Tables (Find Present Value Factor for 25 years and 5% in Appendix C) PV = FV x Factor $300,000 x.295 = $88,500 Calculator (Set on 1 P/YR and END mode.) FV 25 N 5 I PV $88,590.83

40 Calculating the Present Value of an Annuity Example: You have a $300,000 retirement fund and wish to take out equal annual withdrawals over the next 30 years. How much can you withdraw if interest rates are 5% on the investment?

41 Calculating the Present Value of an Annuity Tables (Find Present Value Annuity Factor for 30 years and 5% in Appendix D.) Annual withdrawal= $300,000/ = $19,514.73

Chapter 6. Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams

Chapter 6 Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams 1. Distinguish between an ordinary annuity and an annuity due, and calculate present

Chapter 6 Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams 1. Distinguish between an ordinary annuity and an annuity due, and calculate present

Chapter 6 Contents. Principles Used in Chapter 6 Principle 1: Money Has a Time Value.

Chapter 6 The Time Value of Money: Annuities and Other Topics Chapter 6 Contents Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate present and future values

Chapter 6 The Time Value of Money: Annuities and Other Topics Chapter 6 Contents Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate present and future values

A financial statement captures a person s overall wealth at a specific point in time. In this lesson, students will:

PROJECT 3 CASH FLOW AND BALANCE SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

PROJECT 3 CASH FLOW AND BALANCE SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

A financial statement captures a person s overall wealth at a specific point in time. In this lesson, students will:

PROJECT 3 CASH FLOW AND BALANC E SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

PROJECT 3 CASH FLOW AND BALANC E SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

1. If you wish to accumulate $140,000 in 13 years, how much must you deposit today in an account that pays an annual interest rate of 14%?

Chapter 2 - Sample Problems 1. If you wish to accumulate $140,000 in 13 years, how much must you deposit today in an account that pays an annual interest rate of 14%? 2. What will $247,000 grow to be in

Chapter 2 - Sample Problems 1. If you wish to accumulate $140,000 in 13 years, how much must you deposit today in an account that pays an annual interest rate of 14%? 2. What will $247,000 grow to be in

Developing Your Financial Statements and Plans

22865_02_c02_p030-068.qxd 9/26/06 5:32 PM Page 30 Developing Your Financial Statements and Plans CHAPTER 2 L E A R N I N G G O A L S LG1 Understand the interlocking network of financial plans and statements.

22865_02_c02_p030-068.qxd 9/26/06 5:32 PM Page 30 Developing Your Financial Statements and Plans CHAPTER 2 L E A R N I N G G O A L S LG1 Understand the interlocking network of financial plans and statements.

FIN 3000. Chapter 6. Annuities. Liuren Wu

FIN 3000 Chapter 6 Annuities Liuren Wu Overview 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams Learning objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate

FIN 3000 Chapter 6 Annuities Liuren Wu Overview 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams Learning objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate

Chris Leung, Ph.D., CFA, FRM

FNE 215 Financial Planning Chris Leung, Ph.D., CFA, FRM Email: [email protected] Chapter 2 Planning with Personal Financial Statements Chapter Objectives Explain how to create your personal cash flow

FNE 215 Financial Planning Chris Leung, Ph.D., CFA, FRM Email: [email protected] Chapter 2 Planning with Personal Financial Statements Chapter Objectives Explain how to create your personal cash flow

DISCOUNTED CASH FLOW VALUATION and MULTIPLE CASH FLOWS

Chapter 5 DISCOUNTED CASH FLOW VALUATION and MULTIPLE CASH FLOWS The basic PV and FV techniques can be extended to handle any number of cash flows. PV with multiple cash flows: Suppose you need $500 one

Chapter 5 DISCOUNTED CASH FLOW VALUATION and MULTIPLE CASH FLOWS The basic PV and FV techniques can be extended to handle any number of cash flows. PV with multiple cash flows: Suppose you need $500 one

MAT116 Project 2 Chapters 8 & 9

MAT116 Project 2 Chapters 8 & 9 1 8-1: The Project In Project 1 we made a loan workout decision based only on data from three banks that had merged into one. We did not consider issues like: What was the

MAT116 Project 2 Chapters 8 & 9 1 8-1: The Project In Project 1 we made a loan workout decision based only on data from three banks that had merged into one. We did not consider issues like: What was the

Chapter 4. The Time Value of Money

Chapter 4 The Time Value of Money 1 Learning Outcomes Chapter 4 Identify various types of cash flow patterns Compute the future value and the present value of different cash flow streams Compute the return

Chapter 4 The Time Value of Money 1 Learning Outcomes Chapter 4 Identify various types of cash flow patterns Compute the future value and the present value of different cash flow streams Compute the return

Chapter 6. Time Value of Money Concepts. Simple Interest 6-1. Interest amount = P i n. Assume you invest $1,000 at 6% simple interest for 3 years.

6-1 Chapter 6 Time Value of Money Concepts 6-2 Time Value of Money Interest is the rent paid for the use of money over time. That s right! A dollar today is more valuable than a dollar to be received in

6-1 Chapter 6 Time Value of Money Concepts 6-2 Time Value of Money Interest is the rent paid for the use of money over time. That s right! A dollar today is more valuable than a dollar to be received in

Personal Finance Unit 1 Chapter 3 2007 Glencoe/McGraw-Hill

0 Chapter 3 Money Management Strategy What You ll Learn Section 3.1 Discuss the relationship between opportunity costs and money management. Explain the benefits of keeping financial records and documents.

0 Chapter 3 Money Management Strategy What You ll Learn Section 3.1 Discuss the relationship between opportunity costs and money management. Explain the benefits of keeping financial records and documents.

Synthesis of Financial Planning

P 7A R T Synthesis of Financial Planning 1. Tools for Financial Planning Budgeting (Chapter 2) Planned Savings (Chapter 3) Tax Planning (Chapter 4) 2. Managing Your Liquidity Bank Services (Chapter 5)

P 7A R T Synthesis of Financial Planning 1. Tools for Financial Planning Budgeting (Chapter 2) Planned Savings (Chapter 3) Tax Planning (Chapter 4) 2. Managing Your Liquidity Bank Services (Chapter 5)

Budgeting and Measuring Your Financial Health. Assignments

Financial Plan Assignments Assignments While the previous chapter helped you determine where you wanted to be, this chapter helps you see where you are right now. Financial statements help you understand

Financial Plan Assignments Assignments While the previous chapter helped you determine where you wanted to be, this chapter helps you see where you are right now. Financial statements help you understand

Time Value of Money. 15.511 Corporate Accounting Summer 2004. Professor S. P. Kothari Sloan School of Management Massachusetts Institute of Technology

Time Value of Money 15.511 Corporate Accounting Summer 2004 Professor S. P. Kothari Sloan School of Management Massachusetts Institute of Technology July 2, 2004 1 LIABILITIES: Current Liabilities Obligations

Time Value of Money 15.511 Corporate Accounting Summer 2004 Professor S. P. Kothari Sloan School of Management Massachusetts Institute of Technology July 2, 2004 1 LIABILITIES: Current Liabilities Obligations

Chapter 5 Time Value of Money 2: Analyzing Annuity Cash Flows

1. Future Value of Multiple Cash Flows 2. Future Value of an Annuity 3. Present Value of an Annuity 4. Perpetuities 5. Other Compounding Periods 6. Effective Annual Rates (EAR) 7. Amortized Loans Chapter

1. Future Value of Multiple Cash Flows 2. Future Value of an Annuity 3. Present Value of an Annuity 4. Perpetuities 5. Other Compounding Periods 6. Effective Annual Rates (EAR) 7. Amortized Loans Chapter

CHAPTER 2. Time Value of Money 2-1

CHAPTER 2 Time Value of Money 2-1 Time Value of Money (TVM) Time Lines Future value & Present value Rates of return Annuities & Perpetuities Uneven cash Flow Streams Amortization 2-2 Time lines 0 1 2 3

CHAPTER 2 Time Value of Money 2-1 Time Value of Money (TVM) Time Lines Future value & Present value Rates of return Annuities & Perpetuities Uneven cash Flow Streams Amortization 2-2 Time lines 0 1 2 3

Discounted Cash Flow Valuation

Discounted Cash Flow Valuation Chapter 5 Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

Discounted Cash Flow Valuation Chapter 5 Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

Chapter The Time Value of Money

Chapter The Time Value of Money PPT 9-2 Chapter 9 - Outline Time Value of Money Future Value and Present Value Annuities Time-Value-of-Money Formulas Adjusting for Non-Annual Compounding Compound Interest

Chapter The Time Value of Money PPT 9-2 Chapter 9 - Outline Time Value of Money Future Value and Present Value Annuities Time-Value-of-Money Formulas Adjusting for Non-Annual Compounding Compound Interest

rate nper pmt pv Interest Number of Payment Present Future Rate Periods Amount Value Value 12.00% 1 0 $100.00 $112.00

In Excel language, if the initial cash flow is an inflow (positive), then the future value must be an outflow (negative). Therefore you must add a negative sign before the FV (and PV) function. The inputs

In Excel language, if the initial cash flow is an inflow (positive), then the future value must be an outflow (negative). Therefore you must add a negative sign before the FV (and PV) function. The inputs

Time Value of Money (TVM)

") BUSI Financial Management Time Value of Money 1 Time Value of Money (TVM) Present value and future value how much is $1 now worth in the future? how much is $1 in the future worth now? Business planning

BUSI Financial Management Time Value of Money 1 Time Value of Money (TVM) Present value and future value how much is $1 now worth in the future? how much is $1 in the future worth now? Business planning

Definition of Accounting

SOLUTIONS TO EXERCISES Lesson 1: Definition of Accounting 1. What is accounting? What are its main functions? Accounting is the process of financially measuring, recording, summarizing and communicating

SOLUTIONS TO EXERCISES Lesson 1: Definition of Accounting 1. What is accounting? What are its main functions? Accounting is the process of financially measuring, recording, summarizing and communicating

The Time Value of Money

The Time Value of Money Time Value Terminology 0 1 2 3 4 PV FV Future value (FV) is the amount an investment is worth after one or more periods. Present value (PV) is the current value of one or more future

The Time Value of Money Time Value Terminology 0 1 2 3 4 PV FV Future value (FV) is the amount an investment is worth after one or more periods. Present value (PV) is the current value of one or more future

hp calculators HP 20b Time value of money basics The time value of money The time value of money application Special settings

The time value of money The time value of money application Special settings Clearing the time value of money registers Begin / End mode Periods per year Cash flow diagrams and sign conventions Practice

The time value of money The time value of money application Special settings Clearing the time value of money registers Begin / End mode Periods per year Cash flow diagrams and sign conventions Practice

Understanding Financial Statements. For Your Business

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

UNDERSTANDING FINANCIAL STATEMENTS

UNDERSTANDING FINANCIAL STATEMENTS ITEM 8 It is important that the directors of any business, cooperative or otherwise, understand the financial statements of the business. Without a basic understanding

UNDERSTANDING FINANCIAL STATEMENTS ITEM 8 It is important that the directors of any business, cooperative or otherwise, understand the financial statements of the business. Without a basic understanding

Chapter 2 Applying Time Value Concepts

Chapter 2 Applying Time Value Concepts Chapter Overview Albert Einstein, the renowned physicist whose theories of relativity formed the theoretical base for the utilization of atomic energy, called the

Chapter 2 Applying Time Value Concepts Chapter Overview Albert Einstein, the renowned physicist whose theories of relativity formed the theoretical base for the utilization of atomic energy, called the

THE TIME VALUE OF MONEY

QUANTITATIVE METHODS THE TIME VALUE OF MONEY Reading 5 http://proschool.imsindia.com/ 1 Learning Objective Statements (LOS) a. Interest Rates as Required rate of return, Discount Rate and Opportunity Cost

QUANTITATIVE METHODS THE TIME VALUE OF MONEY Reading 5 http://proschool.imsindia.com/ 1 Learning Objective Statements (LOS) a. Interest Rates as Required rate of return, Discount Rate and Opportunity Cost

Future Value. Basic TVM Concepts. Chapter 2 Time Value of Money. $500 cash flow. On a time line for 3 years: $100. FV 15%, 10 yr.

Chapter Time Value of Money Future Value Present Value Annuities Effective Annual Rate Uneven Cash Flows Growing Annuities Loan Amortization Summary and Conclusions Basic TVM Concepts Interest rate: abbreviated

Chapter Time Value of Money Future Value Present Value Annuities Effective Annual Rate Uneven Cash Flows Growing Annuities Loan Amortization Summary and Conclusions Basic TVM Concepts Interest rate: abbreviated

Chapter F: Finance. Section F.1-F.4

Chapter F: Finance Section F.1-F.4 F.1 Simple Interest Suppose a sum of money P, called the principal or present value, is invested for t years at an annual simple interest rate of r, where r is given

Chapter F: Finance Section F.1-F.4 F.1 Simple Interest Suppose a sum of money P, called the principal or present value, is invested for t years at an annual simple interest rate of r, where r is given

Practice Problems. Use the following information extracted from present and future value tables to answer question 1 to 4.

PROBLEM 1 MULTIPLE CHOICE Practice Problems Use the following information extracted from present and future value tables to answer question 1 to 4. Type of Table Number of Periods Interest Rate Factor

PROBLEM 1 MULTIPLE CHOICE Practice Problems Use the following information extracted from present and future value tables to answer question 1 to 4. Type of Table Number of Periods Interest Rate Factor

Learning Objectives: Quick answer key: Question # Multiple Choice True/False. 14.1 Describe the important of accounting and financial information.

0 Learning Objectives: 14.1 Describe the important of accounting and financial information. 14.2 Differentiate between managerial and financial accounting. 14.3 Identify the six steps of the accounting

0 Learning Objectives: 14.1 Describe the important of accounting and financial information. 14.2 Differentiate between managerial and financial accounting. 14.3 Identify the six steps of the accounting

Appendix C- 1. Time Value of Money. Appendix C- 2. Financial Accounting, Fifth Edition

C- 1 Time Value of Money C- 2 Financial Accounting, Fifth Edition Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount. 3. Solve for future

C- 1 Time Value of Money C- 2 Financial Accounting, Fifth Edition Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount. 3. Solve for future

PRESENT VALUE ANALYSIS. Time value of money equal dollar amounts have different values at different points in time.

PRESENT VALUE ANALYSIS Time value of money equal dollar amounts have different values at different points in time. Present value analysis tool to convert CFs at different points in time to comparable values

PRESENT VALUE ANALYSIS Time value of money equal dollar amounts have different values at different points in time. Present value analysis tool to convert CFs at different points in time to comparable values

Preparing Family Net Worth and Income Statements

Family and Consumer Sciences FSFCS49 Preparing Family Net Worth and Income Statements Laura Connerly Instructor - Family Resource Management Arkansas Is Our Campus Visit our web site at: http://www.uaex.edu

Family and Consumer Sciences FSFCS49 Preparing Family Net Worth and Income Statements Laura Connerly Instructor - Family Resource Management Arkansas Is Our Campus Visit our web site at: http://www.uaex.edu

Key Concepts and Skills. Multiple Cash Flows Future Value Example 6.1. Chapter Outline. Multiple Cash Flows Example 2 Continued

6 Calculators Discounted Cash Flow Valuation Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

6 Calculators Discounted Cash Flow Valuation Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

Finance 331 Corporate Financial Management Week 1 Week 3 Note: For formulas, a Texas Instruments BAII Plus calculator was used.

Chapter 1 Finance 331 What is finance? - Finance has to do with decisions about money and/or cash flows. These decisions have to do with money being raised or used. General parts of finance include: -

Chapter 1 Finance 331 What is finance? - Finance has to do with decisions about money and/or cash flows. These decisions have to do with money being raised or used. General parts of finance include: -

TVM Applications Chapter

Chapter 6 Time of Money UPS, Walgreens, Costco, American Air, Dreamworks Intel (note 10 page 28) TVM Applications Accounting issue Chapter Notes receivable (long-term receivables) 7 Long-term assets 10

Chapter 6 Time of Money UPS, Walgreens, Costco, American Air, Dreamworks Intel (note 10 page 28) TVM Applications Accounting issue Chapter Notes receivable (long-term receivables) 7 Long-term assets 10

Present Value Concepts

Present Value Concepts Present value concepts are widely used by accountants in the preparation of financial statements. In fact, under International Financial Reporting Standards (IFRS), these concepts

Present Value Concepts Present value concepts are widely used by accountants in the preparation of financial statements. In fact, under International Financial Reporting Standards (IFRS), these concepts

The Time Value of Money C H A P T E R N I N E

The Time Value of Money C H A P T E R N I N E Figure 9-1 Relationship of present value and future value PPT 9-1 $1,000 present value $ 10% interest $1,464.10 future value 0 1 2 3 4 Number of periods Figure

The Time Value of Money C H A P T E R N I N E Figure 9-1 Relationship of present value and future value PPT 9-1 $1,000 present value $ 10% interest $1,464.10 future value 0 1 2 3 4 Number of periods Figure

Brief Report on Closing of Accounts (connection) for the Term Ended March 31, 2007

for the Term Ended March 31, 2007") MARUHAN Co., Ltd. Brief Report on Closing of (connection) for the Term Ended March 31, 2007 (Amounts less than 1 million yen omitted) 1.Business Results for the term ended on March, 2007 (From April 1,

MARUHAN Co., Ltd. Brief Report on Closing of (connection) for the Term Ended March 31, 2007 (Amounts less than 1 million yen omitted) 1.Business Results for the term ended on March, 2007 (From April 1,

Purpose EL-773A HP-10B BA-II PLUS Clear memory 0 n registers

D-How to Use a Financial Calculator* Most personal finance decisions involve calculations of the time value of money. Three methods are used to compute this value: time value of money tables (such as those

D-How to Use a Financial Calculator* Most personal finance decisions involve calculations of the time value of money. Three methods are used to compute this value: time value of money tables (such as those

Discounted Cash Flow Valuation

6 Formulas Discounted Cash Flow Valuation McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter Outline Future and Present Values of Multiple Cash Flows Valuing

6 Formulas Discounted Cash Flow Valuation McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter Outline Future and Present Values of Multiple Cash Flows Valuing

TIME VALUE OF MONEY (TVM)

") TIME VALUE OF MONEY (TVM) INTEREST Rate of Return When we know the Present Value (amount today), Future Value (amount to which the investment will grow), and Number of Periods, we can calculate the rate

TIME VALUE OF MONEY (TVM) INTEREST Rate of Return When we know the Present Value (amount today), Future Value (amount to which the investment will grow), and Number of Periods, we can calculate the rate

National Black Law Journal UCLA

National Black Law Journal UCLA Peer Reviewed Title: An Introduction to Financial Statements for the Practicing Lawyer Journal Issue: National Black Law Journal, 4(1) Author: Edmonds, Thom Publication

National Black Law Journal UCLA Peer Reviewed Title: An Introduction to Financial Statements for the Practicing Lawyer Journal Issue: National Black Law Journal, 4(1) Author: Edmonds, Thom Publication

Accounts payable Money which you owe to an individual or business for goods or services that have been received but not yet paid for.

A Account A record of a business transaction. A contract arrangement, written or unwritten, to purchase and take delivery with payment to be made later as arranged. Accounts payable Money which you owe

A Account A record of a business transaction. A contract arrangement, written or unwritten, to purchase and take delivery with payment to be made later as arranged. Accounts payable Money which you owe

Guide to Financial Ratios Analysis A Step by Step Guide to Balance Sheet and Profit and Loss Statement Analysis

Guide to Financial Ratios Analysis A Step by Step Guide to Balance Sheet and Profit and Loss Statement Analysis By BizMove Management Training Institute Other free books by BizMove that may interest you:

Guide to Financial Ratios Analysis A Step by Step Guide to Balance Sheet and Profit and Loss Statement Analysis By BizMove Management Training Institute Other free books by BizMove that may interest you:

Effective Strategies for Personal Money Management

Effective Strategies for Personal Money Management The key to successful money management is developing and following a personal financial plan. Research has shown that people with a financial plan tend

Effective Strategies for Personal Money Management The key to successful money management is developing and following a personal financial plan. Research has shown that people with a financial plan tend

Oklahoma State University Spears School of Business. Time Value of Money

Oklahoma State University Spears School of Business Time Value of Money Slide 2 Time Value of Money Which would you rather receive as a sign-in bonus for your new job? 1. $15,000 cash upon signing the

Oklahoma State University Spears School of Business Time Value of Money Slide 2 Time Value of Money Which would you rather receive as a sign-in bonus for your new job? 1. $15,000 cash upon signing the

REVIEW MATERIALS FOR REAL ESTATE ANALYSIS

REVIEW MATERIALS FOR REAL ESTATE ANALYSIS 1997, Roy T. Black REAE 5311, Fall 2005 University of Texas at Arlington J. Andrew Hansz, Ph.D., CFA CONTENTS ITEM ANNUAL COMPOUND INTEREST TABLES AT 10% MATERIALS

REVIEW MATERIALS FOR REAL ESTATE ANALYSIS 1997, Roy T. Black REAE 5311, Fall 2005 University of Texas at Arlington J. Andrew Hansz, Ph.D., CFA CONTENTS ITEM ANNUAL COMPOUND INTEREST TABLES AT 10% MATERIALS

Dick Schwanke Finite Math 111 Harford Community College Fall 2013

Annuities and Amortization Finite Mathematics 111 Dick Schwanke Session #3 1 In the Previous Two Sessions Calculating Simple Interest Finding the Amount Owed Computing Discounted Loans Quick Review of

Annuities and Amortization Finite Mathematics 111 Dick Schwanke Session #3 1 In the Previous Two Sessions Calculating Simple Interest Finding the Amount Owed Computing Discounted Loans Quick Review of

2. How would (a) a decrease in the interest rate or (b) an increase in the holding period of a deposit affect its future value? Why?

a decrease in the interest rate or (b) an increase in the holding period of a deposit affect its future value? Why?") CHAPTER 3 CONCEPT REVIEW QUESTIONS 1. Will a deposit made into an account paying compound interest (assuming compounding occurs once per year) yield a higher future value after one period than an equal-sized

CHAPTER 3 CONCEPT REVIEW QUESTIONS 1. Will a deposit made into an account paying compound interest (assuming compounding occurs once per year) yield a higher future value after one period than an equal-sized

Personal Financial Planning Questionnaire

MULHOLLAND FINANCIAL SERVICES Personal Financial Planning Questionnaire Conservative Financial Advice This comprehensive, personal financial planning summary is designed to help you take inventory and

MULHOLLAND FINANCIAL SERVICES Personal Financial Planning Questionnaire Conservative Financial Advice This comprehensive, personal financial planning summary is designed to help you take inventory and

Dick Schwanke Finite Math 111 Harford Community College Fall 2013

Annuities and Amortization Finite Mathematics 111 Dick Schwanke Session #3 1 In the Previous Two Sessions Calculating Simple Interest Finding the Amount Owed Computing Discounted Loans Quick Review of

Annuities and Amortization Finite Mathematics 111 Dick Schwanke Session #3 1 In the Previous Two Sessions Calculating Simple Interest Finding the Amount Owed Computing Discounted Loans Quick Review of

Completing the Accounting Cycle

C H A P T E R 4 Completing the Accounting Cycle Financial Accounting 14e Warren Reeve Duchac human/istock/360/getty Images Flow of Accounting Information (slide 1 of 5) End-of-Period Spreadsheet (Work

C H A P T E R 4 Completing the Accounting Cycle Financial Accounting 14e Warren Reeve Duchac human/istock/360/getty Images Flow of Accounting Information (slide 1 of 5) End-of-Period Spreadsheet (Work

Personal Financial Statements

Personal Financial Statements Overview Personal financial statements provide a summary of an individual s financial situation. The most commonly used financial statements are the Net Worth Statement and

Personal Financial Statements Overview Personal financial statements provide a summary of an individual s financial situation. The most commonly used financial statements are the Net Worth Statement and

Sample problems from Chapter 10.1

Sample problems from Chapter 10.1 This is the annuities sinking funds formula. This formula is used in most cases for annuities. The payments for this formula are made at the end of a period. Your book

Sample problems from Chapter 10.1 This is the annuities sinking funds formula. This formula is used in most cases for annuities. The payments for this formula are made at the end of a period. Your book

Lesson 1. Key Financial Concepts INTRODUCTION

Key Financial Concepts INTRODUCTION Welcome to Financial Management! One of the most important components of every business operation is financial decision making. Business decisions at all levels have

Key Financial Concepts INTRODUCTION Welcome to Financial Management! One of the most important components of every business operation is financial decision making. Business decisions at all levels have

Creating a Successful Financial Plan

Creating a Successful Financial Plan Basic Financial Reports Balance Sheet - Estimates the firm s worth on a given date; built on the accounting equation: Assets = Liabilities + Owner s Equity Income Statement

Creating a Successful Financial Plan Basic Financial Reports Balance Sheet - Estimates the firm s worth on a given date; built on the accounting equation: Assets = Liabilities + Owner s Equity Income Statement

Report Description. Business Counts. Top 10 States (by Business Counts) Page 1 of 16

Page 1 of 16") 5-Year County-Level Financial Profile Industry Report Architectural Services (SIC Code: 8712) in Prince George County, Maryland Sales Range: $500,000 - $999,999 Date: 11/07/08 Report Description This 5-Year

5-Year County-Level Financial Profile Industry Report Architectural Services (SIC Code: 8712) in Prince George County, Maryland Sales Range: $500,000 - $999,999 Date: 11/07/08 Report Description This 5-Year

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY 1. The simple interest per year is: $5,000.08 = $400 So after 10 years you will have: $400 10 = $4,000 in interest. The total balance will be

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY 1. The simple interest per year is: $5,000.08 = $400 So after 10 years you will have: $400 10 = $4,000 in interest. The total balance will be

Appendix. Time Value of Money. Financial Accounting, IFRS Edition Weygandt Kimmel Kieso. Appendix C- 1

C Time Value of Money C- 1 Financial Accounting, IFRS Edition Weygandt Kimmel Kieso C- 2 Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount.

C Time Value of Money C- 1 Financial Accounting, IFRS Edition Weygandt Kimmel Kieso C- 2 Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount.

Financial Planning Questionnaire

Please fill out this questionnaire as accurately and completely as possible. In some cases, a statement from your bank, broker/custodian, mutual fund company, etc. will suffice. Complete only those sections

Please fill out this questionnaire as accurately and completely as possible. In some cases, a statement from your bank, broker/custodian, mutual fund company, etc. will suffice. Complete only those sections

Ratios and interpretation

Unit Ratios and interpretation As we learnt in our earlier studies, accounting information is used to answer two key questions about a business: Is it making a profit? Are its assets sufficient to meet

Unit Ratios and interpretation As we learnt in our earlier studies, accounting information is used to answer two key questions about a business: Is it making a profit? Are its assets sufficient to meet

1.3.2015 г. D. Dimov. Year Cash flow 1 $3,000 2 $5,000 3 $4,000 4 $3,000 5 $2,000

D. Dimov Most financial decisions involve costs and benefits that are spread out over time Time value of money allows comparison of cash flows from different periods Question: You have to choose one of

D. Dimov Most financial decisions involve costs and benefits that are spread out over time Time value of money allows comparison of cash flows from different periods Question: You have to choose one of

account statement a record of transactions in an account at a financial institution, usually provided each month

GLOSSARY GLOSSARY Following are definitions for key words as they are used in the financial life skills resource. They may have different or additional meanings in other contexts. A account an arrangement

GLOSSARY GLOSSARY Following are definitions for key words as they are used in the financial life skills resource. They may have different or additional meanings in other contexts. A account an arrangement

Compounding Quarterly, Monthly, and Daily

126 Compounding Quarterly, Monthly, and Daily So far, you have been compounding interest annually, which means the interest is added once per year. However, you will want to add the interest quarterly,

126 Compounding Quarterly, Monthly, and Daily So far, you have been compounding interest annually, which means the interest is added once per year. However, you will want to add the interest quarterly,

baj01275_app_433-454 02/09/2007 17:10PM Page 433 EPG_Team-C 105:JWQD032:bajapp: APPENDIX PERSONAL FINANCE WORKSHEETS

baj01275_app_433-454 02/09/2007 17:10PM Page 433 EPG_Team-C 105:JWQD032:bajapp: APPENDIX PERSONAL FINANCE WORKSHEETS baj01275_app_433-454 02/09/2007 17:10PM Page 434 EPG_Team-C 105:JWQD032:bajapp: 434

baj01275_app_433-454 02/09/2007 17:10PM Page 433 EPG_Team-C 105:JWQD032:bajapp: APPENDIX PERSONAL FINANCE WORKSHEETS baj01275_app_433-454 02/09/2007 17:10PM Page 434 EPG_Team-C 105:JWQD032:bajapp: 434

Problem Set: Annuities and Perpetuities (Solutions Below)

") Problem Set: Annuities and Perpetuities (Solutions Below) 1. If you plan to save $300 annually for 10 years and the discount rate is 15%, what is the future value? 2. If you want to buy a boat in 6 years

Problem Set: Annuities and Perpetuities (Solutions Below) 1. If you plan to save $300 annually for 10 years and the discount rate is 15%, what is the future value? 2. If you want to buy a boat in 6 years

Financial Plan. A) Estimated One-Time Financial Requirements. Part One

Estimated One-Time Financial Requirements. Part One") Financial Plan The Financial Plan is perhaps one of the most important components of your Business Plan (see Business Plan Handout). Not only is it essential if you are seeking external financing it is

Financial Plan The Financial Plan is perhaps one of the most important components of your Business Plan (see Business Plan Handout). Not only is it essential if you are seeking external financing it is

BACKGROUND KNOWLEDGE for Teachers and Students

Pathway: Business, Marketing, and Computer Education Lesson: BMM C6 4: Financial Statements and Reports Common Core State Standards for Mathematics: N.Q.2 Domain: Quantities Cluster: Reason quantitatively

Pathway: Business, Marketing, and Computer Education Lesson: BMM C6 4: Financial Statements and Reports Common Core State Standards for Mathematics: N.Q.2 Domain: Quantities Cluster: Reason quantitatively

Topics. Chapter 5. Future Value. Future Value - Compounding. Time Value of Money. 0 r = 5% 1

Chapter 5 Time Value of Money Topics 1. Future Value of a Lump Sum 2. Present Value of a Lump Sum 3. Future Value of Cash Flow Streams 4. Present Value of Cash Flow Streams 5. Perpetuities 6. Uneven Series

Chapter 5 Time Value of Money Topics 1. Future Value of a Lump Sum 2. Present Value of a Lump Sum 3. Future Value of Cash Flow Streams 4. Present Value of Cash Flow Streams 5. Perpetuities 6. Uneven Series

Consolidated Interim Earnings Report

Consolidated Interim Earnings Report For the Six Months Ended 30th September, 2003 23th Octorber, 2003 Hitachi Capital Corporation These financial statements were prepared for the interim earnings release

Consolidated Interim Earnings Report For the Six Months Ended 30th September, 2003 23th Octorber, 2003 Hitachi Capital Corporation These financial statements were prepared for the interim earnings release

Cash is King. cash flow is less likely to be affected

Reading 27: Understanding Cash Flow Statements Relevance of Cash Flow The primary purpose of the statement of cash flows (SCF) is to provide: Info about a firm s cash receipts & cash payments during an

Reading 27: Understanding Cash Flow Statements Relevance of Cash Flow The primary purpose of the statement of cash flows (SCF) is to provide: Info about a firm s cash receipts & cash payments during an

Regular Annuities: Determining Present Value

8.6 Regular Annuities: Determining Present Value GOAL Find the present value when payments or deposits are made at regular intervals. LEARN ABOUT the Math Harry has money in an account that pays 9%/a compounded

8.6 Regular Annuities: Determining Present Value GOAL Find the present value when payments or deposits are made at regular intervals. LEARN ABOUT the Math Harry has money in an account that pays 9%/a compounded

Chapter 2 Present Value

Chapter 2 Present Value Road Map Part A Introduction to finance. Financial decisions and financial markets. Present value. Part B Valuation of assets, given discount rates. Part C Determination of risk-adjusted

Chapter 2 Present Value Road Map Part A Introduction to finance. Financial decisions and financial markets. Present value. Part B Valuation of assets, given discount rates. Part C Determination of risk-adjusted

Chapter 3 Present Value

Chapter 3 Present Value MULTIPLE CHOICE 1. Which of the following cannot be calculated? a. Present value of an annuity. b. Future value of an annuity. c. Present value of a perpetuity. d. Future value

Chapter 3 Present Value MULTIPLE CHOICE 1. Which of the following cannot be calculated? a. Present value of an annuity. b. Future value of an annuity. c. Present value of a perpetuity. d. Future value

2 The Mathematics. of Finance. Copyright Cengage Learning. All rights reserved.

2 The Mathematics of Finance Copyright Cengage Learning. All rights reserved. 2.3 Annuities, Loans, and Bonds Copyright Cengage Learning. All rights reserved. Annuities, Loans, and Bonds A typical defined-contribution

2 The Mathematics of Finance Copyright Cengage Learning. All rights reserved. 2.3 Annuities, Loans, and Bonds Copyright Cengage Learning. All rights reserved. Annuities, Loans, and Bonds A typical defined-contribution

Module 8: Current and long-term liabilities

Module 8: Current and long-term liabilities Module 8: Current and long-term liabilities Overview In previous modules, you learned how to account for assets. Assets are what a business uses or sells to

Module 8: Current and long-term liabilities Module 8: Current and long-term liabilities Overview In previous modules, you learned how to account for assets. Assets are what a business uses or sells to

Cash Flow Forecasting & Break-Even Analysis

Cash Flow Forecasting & Break-Even Analysis 1. Cash Flow Cash Flow Projections What is cash flow? Cash flow is an estimate of the timing of when the cash associated with sales will be received and when

Cash Flow Forecasting & Break-Even Analysis 1. Cash Flow Cash Flow Projections What is cash flow? Cash flow is an estimate of the timing of when the cash associated with sales will be received and when

Statistical Models for Forecasting and Planning

Part 5 Statistical Models for Forecasting and Planning Chapter 16 Financial Calculations: Interest, Annuities and NPV chapter 16 Financial Calculations: Interest, Annuities and NPV Outcomes Financial information

Part 5 Statistical Models for Forecasting and Planning Chapter 16 Financial Calculations: Interest, Annuities and NPV chapter 16 Financial Calculations: Interest, Annuities and NPV Outcomes Financial information

Guide to Financial Statements Study Guide

Guide to Financial Statements Study Guide Overview (Topic 1) Three major financial statements: The Income Statement The Balance Sheet The Cash Flow Statement Objectives: Explain the underlying equation

Guide to Financial Statements Study Guide Overview (Topic 1) Three major financial statements: The Income Statement The Balance Sheet The Cash Flow Statement Objectives: Explain the underlying equation

EXAM 2 OVERVIEW. Binay Adhikari

EXAM 2 OVERVIEW Binay Adhikari FEDERAL RESERVE & MARKET ACTIVITY (BS38) Definition 4.1 Discount Rate The discount rate is the periodic percentage return subtracted from the future cash flow for computing

EXAM 2 OVERVIEW Binay Adhikari FEDERAL RESERVE & MARKET ACTIVITY (BS38) Definition 4.1 Discount Rate The discount rate is the periodic percentage return subtracted from the future cash flow for computing

Activity 3.1 Annuities & Installment Payments

Activity 3.1 Annuities & Installment Payments A Tale of Twins Amy and Amanda are identical twins at least in their external appearance. They have very different investment plans to provide for their retirement.

Activity 3.1 Annuities & Installment Payments A Tale of Twins Amy and Amanda are identical twins at least in their external appearance. They have very different investment plans to provide for their retirement.

Compound Interest Formula

Mathematics of Finance Interest is the rental fee charged by a lender to a business or individual for the use of money. charged is determined by Principle, rate and time Interest Formula I = Prt $100 At

Mathematics of Finance Interest is the rental fee charged by a lender to a business or individual for the use of money. charged is determined by Principle, rate and time Interest Formula I = Prt $100 At

Finding the Payment $20,000 = C[1 1 / 1.0066667 48 ] /.0066667 C = $488.26

![Finding the Payment $20,000 = C[1 1 / 1.0066667 48 ] /.0066667 C = $488.26](/thumbs/17/134163.jpg "Finding the Payment $20,000 = C[1 1 / 1.0066667 48 ] /.0066667 C = $488.26") Quick Quiz: Part 2 You know the payment amount for a loan and you want to know how much was borrowed. Do you compute a present value or a future value? You want to receive $5,000 per month in retirement.

Quick Quiz: Part 2 You know the payment amount for a loan and you want to know how much was borrowed. Do you compute a present value or a future value? You want to receive $5,000 per month in retirement.

Present Value and Annuities. Chapter 3 Cont d

Present Value and Annuities Chapter 3 Cont d Present Value Helps us answer the question: What s the value in today s dollars of a sum of money to be received in the future? It lets us strip away the effects

Present Value and Annuities Chapter 3 Cont d Present Value Helps us answer the question: What s the value in today s dollars of a sum of money to be received in the future? It lets us strip away the effects

Module 5: Interest concepts of future and present value

file:///f /Courses/2010-11/CGA/FA2/06course/m05intro.htm Module 5: Interest concepts of future and present value Overview In this module, you learn about the fundamental concepts of interest and present

file:///f /Courses/2010-11/CGA/FA2/06course/m05intro.htm Module 5: Interest concepts of future and present value Overview In this module, you learn about the fundamental concepts of interest and present

first complete "prior knowlegde" -- to refresh knowledge of Simple and Compound Interest.

ORDINARY SIMPLE ANNUITIES first complete "prior knowlegde" -- to refresh knowledge of Simple and Compound Interest. LESSON OBJECTIVES: students will learn how to determine the Accumulated Value of Regular

ORDINARY SIMPLE ANNUITIES first complete "prior knowlegde" -- to refresh knowledge of Simple and Compound Interest. LESSON OBJECTIVES: students will learn how to determine the Accumulated Value of Regular

APPENDIX. Interest Concepts of Future and Present Value. Concept of Interest TIME VALUE OF MONEY BASIC INTEREST CONCEPTS

CHAPTER 8 Current Monetary Balances 395 APPENDIX Interest Concepts of Future and Present Value TIME VALUE OF MONEY In general business terms, interest is defined as the cost of using money over time. Economists

CHAPTER 8 Current Monetary Balances 395 APPENDIX Interest Concepts of Future and Present Value TIME VALUE OF MONEY In general business terms, interest is defined as the cost of using money over time. Economists

CHAPTER 4. FINANCIAL STATEMENTS

CHAPTER 4. FINANCIAL STATEMENTS Accounting standards require statements that show the financial position, earnings, cash flows, and investment (distribution) by (to) owners. These measurements are reported,

CHAPTER 4. FINANCIAL STATEMENTS Accounting standards require statements that show the financial position, earnings, cash flows, and investment (distribution) by (to) owners. These measurements are reported,

10. Time Value of Money 2: Inflation, Real Returns, Annuities, and Amortized Loans

10. Time Value of Money 2: Inflation, Real Returns, Annuities, and Amortized Loans Introduction This chapter continues the discussion on the time value of money. In this chapter, you will learn how inflation

10. Time Value of Money 2: Inflation, Real Returns, Annuities, and Amortized Loans Introduction This chapter continues the discussion on the time value of money. In this chapter, you will learn how inflation

PowerPoint. to accompany. Chapter 5. Interest Rates

PowerPoint to accompany Chapter 5 Interest Rates 5.1 Interest Rate Quotes and Adjustments To understand interest rates, it s important to think of interest rates as a price the price of using money. When

PowerPoint to accompany Chapter 5 Interest Rates 5.1 Interest Rate Quotes and Adjustments To understand interest rates, it s important to think of interest rates as a price the price of using money. When

Finance 3130 Sample Exam 1B Spring 2012

Finance 3130 Sample Exam 1B Spring 2012 True/False Indicate whether the statement is true or false. 1. A firm s income statement provides information as of a point in time, and represents how management

Finance 3130 Sample Exam 1B Spring 2012 True/False Indicate whether the statement is true or false. 1. A firm s income statement provides information as of a point in time, and represents how management

UNDERSTANDING WHERE YOU STAND. A Simple Guide to Your Company s Financial Statements

UNDERSTANDING WHERE YOU STAND A Simple Guide to Your Company s Financial Statements Contents INTRODUCTION One statement cannot diagnose your company s financial health. Put several statements together

UNDERSTANDING WHERE YOU STAND A Simple Guide to Your Company s Financial Statements Contents INTRODUCTION One statement cannot diagnose your company s financial health. Put several statements together