AGGREGATE CLAIMS, SOLVENCY AND REINSURANCE. David Dickson, Centre for Actuarial Studies, University of Melbourne. Cherry Bud Workshop

|

|

|

- Kelley Chase

- 8 years ago

- Views:

Transcription

1 AGGREGATE CLAIMS, SOLVENCY AND REINSURANCE David Dickson, Centre for Actuarial Studies, University of Melbourne Cherry Bud Workshop Keio University, 27 March 2006

2 Basic General Insurance Risk Model where S= N X i i=1 Srepresentstheaggregateamountofclaimsinafixedperiod,e.g. oneyear N isacountingvariablerepresentingthenumberofclaims X i =amountofthei-thclaim {X i } i=1 isasequenceofi.i.d. randomvariables

3 Standard Problem- find the distribution function of S Reasons Premium setting Setting appropriate levels of reinsurance Solvency,e.g. foragivenpremiump,findthecapitalusuchthat Pr(u+P >S)=0.99

4 Howtofitourmodelforaggregateclaims? Model for the number of claims, e.g. Poisson, negative binomial, or zeromodified versions Model for claim amounts, e.g. lognormal, Pareto Parameter estimation by maximum likelihood, standard goodness of fit tests Excellent reference: Loss Models- from Data to Decisions by Klugman, Panjer &Willmot

5 Computational Issues Distribution function of S is Pr(S x)= n=0 Pr(N =n)f n (x) wheref(x)=pr(x i x),andf n isthen-foldconvolution Exact computation is difficult Approximations are often used- especially moment based approximationsbut estimation of counting and claim amount distributions is important

6 Insurer s surplus process before reinsurance u = initial surplus, U(t)=u+ct N(t) i=1 X i c=rateofpremiumincomeperunittime(year), N(t)=numberofclaimsin[0,t],N(t) Poisson(λt), X i =amountofthei-thclaim.

=numberofclaimsin[0,t],N(t) Poisson(λt), X i")

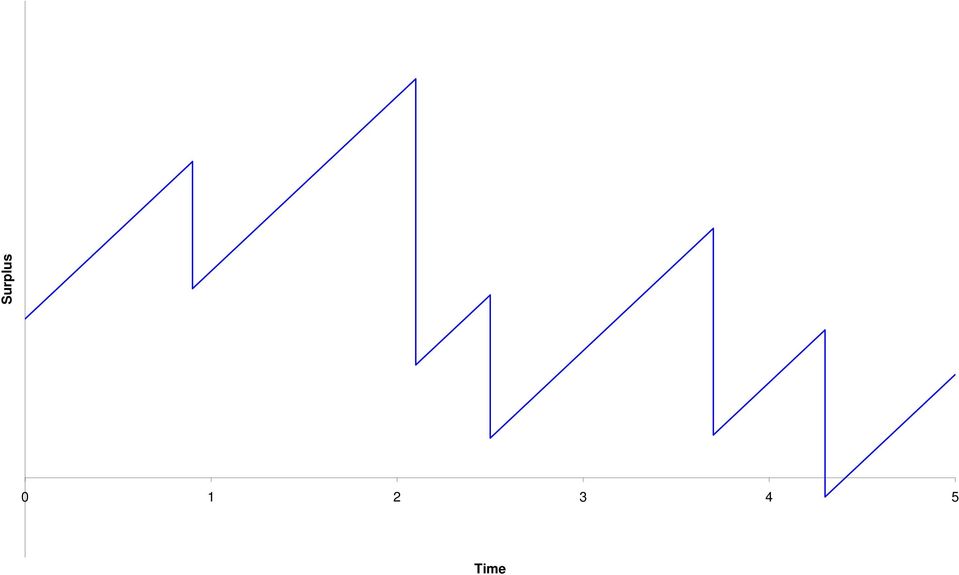

7 Time Surplus

8 Let θ denote a general reinsurance arrangement. Then the insurer s surplus process after reinsurance is where U θ (t)=u+c θ t S θ (t) U θ (t)=insurer ssurplusattimet, c θ =rateofpremiumincometotheinsurernetofreinsurance, S θ (t)=netaggregateclaimsfortheinsurerin[0,t], S θ (t)hascdfg θ (x;t)andpdfg θ (x;t)forx>0.

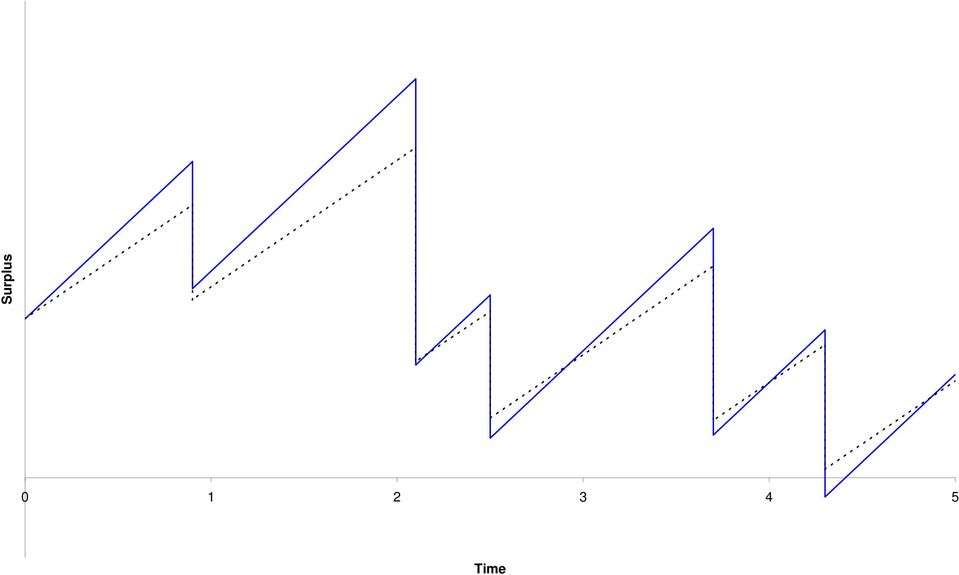

9 Time Surplus

10 Probability of ruin- definitions Discrete time: ψ θ (u,t)=pr[u θ (s)<0forsomes,s=1,2,...,t] Continuous time: ψ θ (u,t)=pr[u θ (s)<0forsomes,s (0,t]]

11 Time Surplus

12 The problem: Determine: where: ˆψ(u,t)= inf θ Θ ψ θ(u,t) Θ is a set of admissible reinsurance arrangements. In our study, admissible means: either proportional or excess of loss reinsurance throughout the period, the insurer s annual net income exceeds net expected claims. θcanbechangedatthestartofeachyear. Ruincanbeindiscreteorcontinuoustime.

13 Proportional reinsurance Let X i denote the amount of the i-th individual claim. Under a proportional reinsurance arrangement with proportion retained a, theinsurerpaysax i thereinsurerpays(1 a)x i.

14 Excess of Loss Reinsurance LetX i denotetheamountofthei-thindividualclaim. Underanexcessofloss reinsurance arrangement with retention level M, theinsurerpaysmin(x i,m) thereinsurerpaysmax(0,x i M).

")

15 Discrete time formulae ˆψ(u,1) = inf θ Θ (1 G θ(u+c θ ;1)) ψ θ (u,n) = ψ θ (u,1) + u+cθ 0 g θ (u+c θ x;1)ˆψ(x,n 1)dx +e λˆψ(u+cθ,n 1) ˆψ(u,n) = inf θ Θ ψ θ(u,n) (Bellman Principle)

ˆψ(u,n) = inf θ Θ ψ θ(u,n) (Bellman")

16 Calculating ruin probabilities Translatedgammadistribution: Foreachθcalculateα θ,β θ,κ θ suchthat: E[(Y θ +κ θ ) i ]=E[(S θ (1)) i ] i=1,2,3 wherey θ Γ(α θ,β θ )withcdf Γ θ (x;α θ,β θ )andpdf γ θ (x;α θ,β θ ). Thenforx 0 In particular, G θ (x;1) Pr[Y θ +κ θ x] = Γ θ (x κ θ ;α θ,β θ ). G θ (0;1)=e λ Pr[Y θ +κ θ 0]=Γ θ ( κ θ ;α θ,β θ ). Thepdfapproximationisg θ (x;1) γ θ (x κ θ ;α θ,β θ ).

Pr[Y θ +κ θ x] = Γ θ (x κ θ ;α θ,β θ ).")

17 Translatedgammadistributionapproximationtoψ θ (u,n) 1. Original(compound Poisson) process: ψ θ (u,1) + u+cθ 0 g θ (u+c θ x;1)ˆψ(x,n 1)dx +e λˆψ(u+c θ,n 1) 2. Translated gamma distribution approximation: 1 Γ θ (u+c θ κ θ ;α θ,β θ ) + u+cθ 0 γ θ (u+c θ κ θ x;α θ,β θ )ˆψ(x,n 1)dx +Γ θ ( κ θ ;α θ,β θ )ˆψ(u+c θ,n 1)

+")

18 Computational Issues Need to use numerical integration. Can reduce the amount of calculation required by introducing a truncation procedure- essentially we set very small ruin probabilities to zero. A grid search is required for the optimal retention level - we limit our set of possible retention levels, e.g. 0.01,0.02,...,0.99,1 for proportional reinsurance. Computations for discrete time ruin are considerably faster than for continuous time- factor may depend on programming language. It does not appear possible to find explicit solutions!

19 Questions to be answered To what extent is a dynamic reinsurance policy better than a static policy? To what extent does the time horizon affect the optimal reinsurance strategy? Is minimising the probability of ruin(in finite time) a sensible optimisation criterion?

20 Numerical example Individual claim amount distribution is Exponential(1) Premium loading factors: 0.1(insurer)& 0.2(reinsurer) Poissonparameter: λ=100 Initialsurplusis u=23ingraphicalillustration

Poissonparameter: λ=100")

21 Surplus, Remaining term, t u M ˆψ(u, t) M ˆψ(u, t) M ˆψ(u, t) M ˆψ(u, t) Optimal strategy: Exponential claims, loadings 10%/20%, excess loss, discrete time ruin, distributional approximation.

22 Ruin probability No reinsurance Static ppn Dynamic ppn Static XL Dynamic XL Time

23 Questions to be answered To what extent is a dynamic reinsurance policy better than a static policy? Significantly. To what extent does the time horizon affect the optimal reinsurance strategy? Significantly. Is minimising the probability of ruin(in finite time) a sensible optimisation criterion? Answered later!

24 Continuous time formulae Letδ θ (u,t)=1 ψ θ (u,t)bethesurvivalprobabilitytotimet(years). Prahbu s formula is with δ θ (u,1)=g θ (u+c θ,1) c θ 1 δ θ (0,t)= 1 c θ t 0 δ θ(0,1 s)g θ (u+c θ s,s)ds cθ t 0 G θ (y,t)dy.

25 Thenforn>1wehave ˆψ(u,n)=inf ψ θ(u,n), θ where,foragivenvalueofθ, ψ θ (u,n) = ψ θ (u,1)+e λˆψ(u+cθ,n 1)+ and with + u+cθ c θ cθ g θ (u+c θ y,1)ˆψ(y,n 1)dy δ θ (u,1,y)=g θ (u+c θ y,1) c θ 1 y/cθ 0 δ θ (0,t,y)= y c θ t g θ(c θ t y,t). 0 δ θ (u,1,y)ˆψ(y,n 1)dy g θ (u+c θ s,s)δ θ (0,1 s,y)ds

26 Translated gamma distribution approximation Thiscanbeappliedwithease Formulae are relatively straightforward. Numerical example Initialsurplusisu=49 Individual claim amount distribution is Pareto(4,3)(mean is 1) Premium loading factors: 0.1(insurer)& 0.2 or 0.3(reinsurer) Poissonparameter: λ=100

27 Ruin probability No reinsurance Dynamic ppn Static ppn Dynamic XL (10%/20%) Static XL (10%/20%) Dynamic XL (10%/30%) Static XL (10%/30%) Time

28 Questions to be answered To what extent is a dynamic reinsurance policy better than a static policy? Clearly better for proportional reinsurance, but only at the longer time horizons. Marginally better for excess loss reinsurance for both reinsurance loadings. To what extent does the time horizon affect the optimal reinsurance strategy? Significantly: for example, with excess of loss reinsurance and a 30% reinsuranceloadingfactorwegetthefollowingvaluesofm forthefirstyear: Term Dynamic Static

29 Questions to be answered Is minimising the probability of ruin(in finite time) a sensible optimisation criterion? Yes,butitcanleadtostrategiesthatmightnotappearsensible. Forexample,intheprevioustable,withu=49andaremainingtermof1year, whyshouldtheinsurercedesomuchrisk? Alternative criteria, e.g. minimise the ruin probability over a fixed but rolling time horizon? Cannot reduce the ruin probability over the original time horizon.

30 Concluding Remarks A dynamic strategy appears to have a greater effect if we consider discrete time ruin. If we consider discrete time only, the translated gamma approximation still applies for other models, e.g. in the case of a compound negative binomial distribution for claim numbers. It is computationally much faster to compute the optimal static strategy, especially in continuous time. Ruin probabilities under a static strategy bound those under a dynamic strategy.

31 Our study contained a second approach to calculation using translated gamma processes. Results were virtually identical - confidence in robustness of approaches. Acknowledgement: co-author is Prof Howard Waters, Heriot-Watt University, Edinburgh Paper is at

α α λ α = = λ λ α ψ = = α α α λ λ ψ α = + β = > θ θ β > β β θ θ θ β θ β γ θ β = γ θ > β > γ θ β γ = θ β = θ β = θ β = β θ = β β θ = = = β β θ = + α α α α α = = λ λ λ λ λ λ λ = λ λ α α α α λ ψ + α =

α α λ α = = λ λ α ψ = = α α α λ λ ψ α = + β = > θ θ β > β β θ θ θ β θ β γ θ β = γ θ > β > γ θ β γ = θ β = θ β = θ β = β θ = β β θ = = = β β θ = + α α α α α = = λ λ λ λ λ λ λ = λ λ α α α α λ ψ + α =

Aggregate Loss Models

Aggregate Loss Models Chapter 9 Stat 477 - Loss Models Chapter 9 (Stat 477) Aggregate Loss Models Brian Hartman - BYU 1 / 22 Objectives Objectives Individual risk model Collective risk model Computing

Aggregate Loss Models Chapter 9 Stat 477 - Loss Models Chapter 9 (Stat 477) Aggregate Loss Models Brian Hartman - BYU 1 / 22 Objectives Objectives Individual risk model Collective risk model Computing

Optimal reinsurance with ruin probability target

Optimal reinsurance with ruin probability target Arthur Charpentier 7th International Workshop on Rare Event Simulation, Sept. 2008 http ://blogperso.univ-rennes1.fr/arthur.charpentier/ 1 Ruin, solvency

Optimal reinsurance with ruin probability target Arthur Charpentier 7th International Workshop on Rare Event Simulation, Sept. 2008 http ://blogperso.univ-rennes1.fr/arthur.charpentier/ 1 Ruin, solvency

A note on the distribution of the aggregate claim amount at ruin

A note on the distribution of the aggregate claim amount at ruin Jingchao Li, David C M Dickson, Shuanming Li Centre for Actuarial Studies, Department of Economics, University of Melbourne, VIC 31, Australia

A note on the distribution of the aggregate claim amount at ruin Jingchao Li, David C M Dickson, Shuanming Li Centre for Actuarial Studies, Department of Economics, University of Melbourne, VIC 31, Australia

Errata and updates for ASM Exam C/Exam 4 Manual (Sixteenth Edition) sorted by page

sorted by page") Errata for ASM Exam C/4 Study Manual (Sixteenth Edition) Sorted by Page 1 Errata and updates for ASM Exam C/Exam 4 Manual (Sixteenth Edition) sorted by page Practice exam 1:9, 1:22, 1:29, 9:5, and 10:8

Errata for ASM Exam C/4 Study Manual (Sixteenth Edition) Sorted by Page 1 Errata and updates for ASM Exam C/Exam 4 Manual (Sixteenth Edition) sorted by page Practice exam 1:9, 1:22, 1:29, 9:5, and 10:8

Approximation of Aggregate Losses Using Simulation

Journal of Mathematics and Statistics 6 (3): 233-239, 2010 ISSN 1549-3644 2010 Science Publications Approimation of Aggregate Losses Using Simulation Mohamed Amraja Mohamed, Ahmad Mahir Razali and Noriszura

Journal of Mathematics and Statistics 6 (3): 233-239, 2010 ISSN 1549-3644 2010 Science Publications Approimation of Aggregate Losses Using Simulation Mohamed Amraja Mohamed, Ahmad Mahir Razali and Noriszura

Past and present trends in aggregate claims analysis

Past and present trends in aggregate claims analysis Gordon E. Willmot Munich Re Professor of Insurance Department of Statistics and Actuarial Science University of Waterloo 1st Quebec-Ontario Workshop

Past and present trends in aggregate claims analysis Gordon E. Willmot Munich Re Professor of Insurance Department of Statistics and Actuarial Science University of Waterloo 1st Quebec-Ontario Workshop

INSURANCE RISK THEORY (Problems)

") INSURANCE RISK THEORY (Problems) 1 Counting random variables 1. (Lack of memory property) Let X be a geometric distributed random variable with parameter p (, 1), (X Ge (p)). Show that for all n, m =,

INSURANCE RISK THEORY (Problems) 1 Counting random variables 1. (Lack of memory property) Let X be a geometric distributed random variable with parameter p (, 1), (X Ge (p)). Show that for all n, m =,

From Ruin Theory to Solvency in Non-Life Insurance

From Ruin Theory to Solvency in Non-Life Insurance Mario V. Wüthrich RiskLab ETH Zurich & Swiss Finance Institute SFI January 23, 2014 LUH Colloquium Versicherungs- und Finanzmathematik Leibniz Universität

From Ruin Theory to Solvency in Non-Life Insurance Mario V. Wüthrich RiskLab ETH Zurich & Swiss Finance Institute SFI January 23, 2014 LUH Colloquium Versicherungs- und Finanzmathematik Leibniz Universität

Cover. Optimal Retentions with Ruin Probability Target in The case of Fire. Insurance in Iran

Cover Optimal Retentions with Ruin Probability Target in The case of Fire Insurance in Iran Ghadir Mahdavi Ass. Prof., ECO College of Insurance, Allameh Tabataba i University, Iran Omid Ghavibazoo MS in

Cover Optimal Retentions with Ruin Probability Target in The case of Fire Insurance in Iran Ghadir Mahdavi Ass. Prof., ECO College of Insurance, Allameh Tabataba i University, Iran Omid Ghavibazoo MS in

EXAM 3, FALL 003 Please note: On a one-time basis, the CAS is releasing annotated solutions to Fall 003 Examination 3 as a study aid to candidates. It is anticipated that for future sittings, only the

EXAM 3, FALL 003 Please note: On a one-time basis, the CAS is releasing annotated solutions to Fall 003 Examination 3 as a study aid to candidates. It is anticipated that for future sittings, only the

Analyzing the Surrender Rate of Limited Reimbursement Long-Term Individual Health Insurance

Analyzing the Surrender Rate of Limited Reimbursement Long-Term Individual Health Insurance Chih-Hua Chiao, Shing-Her Juang, Pin-Hsun Chen, Chen-Ting Chueh Department of Financial Engineering and Actuarial

Analyzing the Surrender Rate of Limited Reimbursement Long-Term Individual Health Insurance Chih-Hua Chiao, Shing-Her Juang, Pin-Hsun Chen, Chen-Ting Chueh Department of Financial Engineering and Actuarial

Department of Mathematics, Indian Institute of Technology, Kharagpur Assignment 2-3, Probability and Statistics, March 2015. Due:-March 25, 2015.

Department of Mathematics, Indian Institute of Technology, Kharagpur Assignment -3, Probability and Statistics, March 05. Due:-March 5, 05.. Show that the function 0 for x < x+ F (x) = 4 for x < for x

Department of Mathematics, Indian Institute of Technology, Kharagpur Assignment -3, Probability and Statistics, March 05. Due:-March 5, 05.. Show that the function 0 for x < x+ F (x) = 4 for x < for x

A LOGNORMAL MODEL FOR INSURANCE CLAIMS DATA

REVSTAT Statistical Journal Volume 4, Number 2, June 2006, 131 142 A LOGNORMAL MODEL FOR INSURANCE CLAIMS DATA Authors: Daiane Aparecida Zuanetti Departamento de Estatística, Universidade Federal de São

REVSTAT Statistical Journal Volume 4, Number 2, June 2006, 131 142 A LOGNORMAL MODEL FOR INSURANCE CLAIMS DATA Authors: Daiane Aparecida Zuanetti Departamento de Estatística, Universidade Federal de São

Lecture 2 of 4-part series. Spring School on Risk Management, Insurance and Finance European University at St. Petersburg, Russia.

Principles and Lecture 2 of 4-part series Capital Spring School on Risk, Insurance and Finance European University at St. Petersburg, Russia 2-4 April 2012 Fair Wang s University of Connecticut, USA page

Principles and Lecture 2 of 4-part series Capital Spring School on Risk, Insurance and Finance European University at St. Petersburg, Russia 2-4 April 2012 Fair Wang s University of Connecticut, USA page

Optimisation Problems in Non-Life Insurance

Frankfurt, 6. Juli 2007 1 The de Finetti Problem The Optimal Strategy De Finetti s Example 2 Minimal Ruin Probabilities The Hamilton-Jacobi-Bellman Equation Two Examples 3 Optimal Dividends Dividends in

Frankfurt, 6. Juli 2007 1 The de Finetti Problem The Optimal Strategy De Finetti s Example 2 Minimal Ruin Probabilities The Hamilton-Jacobi-Bellman Equation Two Examples 3 Optimal Dividends Dividends in

EXTREMES ON THE DISCOUNTED AGGREGATE CLAIMS IN A TIME DEPENDENT RISK MODEL

EXTREMES ON THE DISCOUNTED AGGREGATE CLAIMS IN A TIME DEPENDENT RISK MODEL Alexandru V. Asimit 1 Andrei L. Badescu 2 Department of Statistics University of Toronto 100 St. George St. Toronto, Ontario,

EXTREMES ON THE DISCOUNTED AGGREGATE CLAIMS IN A TIME DEPENDENT RISK MODEL Alexandru V. Asimit 1 Andrei L. Badescu 2 Department of Statistics University of Toronto 100 St. George St. Toronto, Ontario,

A Uniform Asymptotic Estimate for Discounted Aggregate Claims with Subexponential Tails

12th International Congress on Insurance: Mathematics and Economics July 16-18, 2008 A Uniform Asymptotic Estimate for Discounted Aggregate Claims with Subexponential Tails XUEMIAO HAO (Based on a joint

12th International Congress on Insurance: Mathematics and Economics July 16-18, 2008 A Uniform Asymptotic Estimate for Discounted Aggregate Claims with Subexponential Tails XUEMIAO HAO (Based on a joint

Probability and Statistics Prof. Dr. Somesh Kumar Department of Mathematics Indian Institute of Technology, Kharagpur

Probability and Statistics Prof. Dr. Somesh Kumar Department of Mathematics Indian Institute of Technology, Kharagpur Module No. #01 Lecture No. #15 Special Distributions-VI Today, I am going to introduce

Probability and Statistics Prof. Dr. Somesh Kumar Department of Mathematics Indian Institute of Technology, Kharagpur Module No. #01 Lecture No. #15 Special Distributions-VI Today, I am going to introduce

OPTIMAl PREMIUM CONTROl IN A NON-liFE INSURANCE BUSINESS

ONDERZOEKSRAPPORT NR 8904 OPTIMAl PREMIUM CONTROl IN A NON-liFE INSURANCE BUSINESS BY M. VANDEBROEK & J. DHAENE D/1989/2376/5 1 IN A OPTIMAl PREMIUM CONTROl NON-liFE INSURANCE BUSINESS By Martina Vandebroek

ONDERZOEKSRAPPORT NR 8904 OPTIMAl PREMIUM CONTROl IN A NON-liFE INSURANCE BUSINESS BY M. VANDEBROEK & J. DHAENE D/1989/2376/5 1 IN A OPTIMAl PREMIUM CONTROl NON-liFE INSURANCE BUSINESS By Martina Vandebroek

Lloyd Spencer Lincoln Re

AN OVERVIEW OF THE PANJER METHOD FOR DERIVING THE AGGREGATE CLAIMS DISTRIBUTION Lloyd Spencer Lincoln Re Harry H. Panjer derives a recursive method for deriving the aggregate distribution of claims in

AN OVERVIEW OF THE PANJER METHOD FOR DERIVING THE AGGREGATE CLAIMS DISTRIBUTION Lloyd Spencer Lincoln Re Harry H. Panjer derives a recursive method for deriving the aggregate distribution of claims in

Math 370/408, Spring 2008 Prof. A.J. Hildebrand. Actuarial Exam Practice Problem Set 2 Solutions

Math 70/408, Spring 2008 Prof. A.J. Hildebrand Actuarial Exam Practice Problem Set 2 Solutions About this problem set: These are problems from Course /P actuarial exams that I have collected over the years,

Math 70/408, Spring 2008 Prof. A.J. Hildebrand Actuarial Exam Practice Problem Set 2 Solutions About this problem set: These are problems from Course /P actuarial exams that I have collected over the years,

Stochastic Loss Reserving with the Collective Risk Model

Glenn Meyers, FCAS, MAAA, Ph.D. Abstract This paper presents a Bayesian stochastic loss reserve model with the following features. 1. The model for expected loss payments depends upon unknown parameters

Glenn Meyers, FCAS, MAAA, Ph.D. Abstract This paper presents a Bayesian stochastic loss reserve model with the following features. 1. The model for expected loss payments depends upon unknown parameters

Maximum Likelihood Estimation

Math 541: Statistical Theory II Lecturer: Songfeng Zheng Maximum Likelihood Estimation 1 Maximum Likelihood Estimation Maximum likelihood is a relatively simple method of constructing an estimator for

Math 541: Statistical Theory II Lecturer: Songfeng Zheng Maximum Likelihood Estimation 1 Maximum Likelihood Estimation Maximum likelihood is a relatively simple method of constructing an estimator for

Premium Calculation. Lecture: Weeks 12-14. Lecture: Weeks 12-14 (Math 3630) Annuities Fall 2015 - Valdez 1 / 32

Annuities Fall 2015 - Valdez 1 / 32") Premium Calculation Lecture: Weeks 12-14 Lecture: Weeks 12-14 (Math 3630) Annuities Fall 2015 - Valdez 1 / 32 Preliminaries Preliminaries An insurance policy (life insurance or life annuity) is funded

Premium Calculation Lecture: Weeks 12-14 Lecture: Weeks 12-14 (Math 3630) Annuities Fall 2015 - Valdez 1 / 32 Preliminaries Preliminaries An insurance policy (life insurance or life annuity) is funded

Benchmark Rates for XL Reinsurance Revisited: Model Comparison for the Swiss MTPL Market

Benchmark Rates for XL Reinsurance Revisited: Model Comparison for the Swiss MTPL Market W. Hürlimann 1 Abstract. We consider the dynamic stable benchmark rate model introduced in Verlaak et al. (005),

Benchmark Rates for XL Reinsurance Revisited: Model Comparison for the Swiss MTPL Market W. Hürlimann 1 Abstract. We consider the dynamic stable benchmark rate model introduced in Verlaak et al. (005),

The Exponential Distribution

21 The Exponential Distribution From Discrete-Time to Continuous-Time: In Chapter 6 of the text we will be considering Markov processes in continuous time. In a sense, we already have a very good understanding

21 The Exponential Distribution From Discrete-Time to Continuous-Time: In Chapter 6 of the text we will be considering Markov processes in continuous time. In a sense, we already have a very good understanding

Stop Loss Reinsurance

Stop Loss Reinsurance Stop loss is a nonproportional type of reinsurance and works similarly to excess-of-loss reinsurance. While excess-of-loss is related to single loss amounts, either per risk or per

Stop Loss Reinsurance Stop loss is a nonproportional type of reinsurance and works similarly to excess-of-loss reinsurance. While excess-of-loss is related to single loss amounts, either per risk or per

**BEGINNING OF EXAMINATION**

November 00 Course 3 Society of Actuaries **BEGINNING OF EXAMINATION**. You are given: R = S T µ x 0. 04, 0 < x < 40 0. 05, x > 40 Calculate e o 5: 5. (A) 4.0 (B) 4.4 (C) 4.8 (D) 5. (E) 5.6 Course 3: November

November 00 Course 3 Society of Actuaries **BEGINNING OF EXAMINATION**. You are given: R = S T µ x 0. 04, 0 < x < 40 0. 05, x > 40 Calculate e o 5: 5. (A) 4.0 (B) 4.4 (C) 4.8 (D) 5. (E) 5.6 Course 3: November

Computation of the Aggregate Claim Amount Distribution Using R and actuar. Vincent Goulet, Ph.D.

Computation of the Aggregate Claim Amount Distribution Using R and actuar Vincent Goulet, Ph.D. Actuarial Risk Modeling Process 1 Model costs at the individual level Modeling of loss distributions 2 Aggregate

Computation of the Aggregate Claim Amount Distribution Using R and actuar Vincent Goulet, Ph.D. Actuarial Risk Modeling Process 1 Model costs at the individual level Modeling of loss distributions 2 Aggregate

Asymptotics of discounted aggregate claims for renewal risk model with risky investment

Appl. Math. J. Chinese Univ. 21, 25(2: 29-216 Asymptotics of discounted aggregate claims for renewal risk model with risky investment JIANG Tao Abstract. Under the assumption that the claim size is subexponentially

Appl. Math. J. Chinese Univ. 21, 25(2: 29-216 Asymptotics of discounted aggregate claims for renewal risk model with risky investment JIANG Tao Abstract. Under the assumption that the claim size is subexponentially

SOCIETY OF ACTUARIES/CASUALTY ACTUARIAL SOCIETY EXAM C CONSTRUCTION AND EVALUATION OF ACTUARIAL MODELS EXAM C SAMPLE QUESTIONS

SOCIETY OF ACTUARIES/CASUALTY ACTUARIAL SOCIETY EXAM C CONSTRUCTION AND EVALUATION OF ACTUARIAL MODELS EXAM C SAMPLE QUESTIONS Copyright 005 by the Society of Actuaries and the Casualty Actuarial Society

SOCIETY OF ACTUARIES/CASUALTY ACTUARIAL SOCIETY EXAM C CONSTRUCTION AND EVALUATION OF ACTUARIAL MODELS EXAM C SAMPLE QUESTIONS Copyright 005 by the Society of Actuaries and the Casualty Actuarial Society

An exact formula for default swaptions pricing in the SSRJD stochastic intensity model

An exact formula for default swaptions pricing in the SSRJD stochastic intensity model Naoufel El-Bachir (joint work with D. Brigo, Banca IMI) Radon Institute, Linz May 31, 2007 ICMA Centre, University

An exact formula for default swaptions pricing in the SSRJD stochastic intensity model Naoufel El-Bachir (joint work with D. Brigo, Banca IMI) Radon Institute, Linz May 31, 2007 ICMA Centre, University

Pricing Alternative forms of Commercial Insurance cover

Pricing Alternative forms of Commercial Insurance cover Prepared by Andrew Harford Presented to the Institute of Actuaries of Australia Biennial Convention 23-26 September 2007 Christchurch, New Zealand

Pricing Alternative forms of Commercial Insurance cover Prepared by Andrew Harford Presented to the Institute of Actuaries of Australia Biennial Convention 23-26 September 2007 Christchurch, New Zealand

Pricing Alternative forms of Commercial insurance cover. Andrew Harford

Pricing Alternative forms of Commercial insurance cover Andrew Harford Pricing alternative covers Types of policies Overview of Pricing Approaches Total claim cost distribution Discounting Cash flows Adjusting

Pricing Alternative forms of Commercial insurance cover Andrew Harford Pricing alternative covers Types of policies Overview of Pricing Approaches Total claim cost distribution Discounting Cash flows Adjusting

Math 370, Spring 2008 Prof. A.J. Hildebrand. Practice Test 1 Solutions

Math 70, Spring 008 Prof. A.J. Hildebrand Practice Test Solutions About this test. This is a practice test made up of a random collection of 5 problems from past Course /P actuarial exams. Most of the

Math 70, Spring 008 Prof. A.J. Hildebrand Practice Test Solutions About this test. This is a practice test made up of a random collection of 5 problems from past Course /P actuarial exams. Most of the

Exam MFE Spring 2007 FINAL ANSWER KEY 1 B 2 A 3 C 4 E 5 D 6 C 7 E 8 C 9 A 10 B 11 D 12 A 13 E 14 E 15 C 16 D 17 B 18 A 19 D

Exam MFE Spring 2007 FINAL ANSWER KEY Question # Answer 1 B 2 A 3 C 4 E 5 D 6 C 7 E 8 C 9 A 10 B 11 D 12 A 13 E 14 E 15 C 16 D 17 B 18 A 19 D **BEGINNING OF EXAMINATION** ACTUARIAL MODELS FINANCIAL ECONOMICS

Exam MFE Spring 2007 FINAL ANSWER KEY Question # Answer 1 B 2 A 3 C 4 E 5 D 6 C 7 E 8 C 9 A 10 B 11 D 12 A 13 E 14 E 15 C 16 D 17 B 18 A 19 D **BEGINNING OF EXAMINATION** ACTUARIAL MODELS FINANCIAL ECONOMICS

A Model of Optimum Tariff in Vehicle Fleet Insurance

A Model of Optimum Tariff in Vehicle Fleet Insurance. Bouhetala and F.Belhia and R.Salmi Statistics and Probability Department Bp, 3, El-Alia, USTHB, Bab-Ezzouar, Alger Algeria. Summary: An approach about

A Model of Optimum Tariff in Vehicle Fleet Insurance. Bouhetala and F.Belhia and R.Salmi Statistics and Probability Department Bp, 3, El-Alia, USTHB, Bab-Ezzouar, Alger Algeria. Summary: An approach about

ON SOME ANALOGUE OF THE GENERALIZED ALLOCATION SCHEME

ON SOME ANALOGUE OF THE GENERALIZED ALLOCATION SCHEME Alexey Chuprunov Kazan State University, Russia István Fazekas University of Debrecen, Hungary 2012 Kolchin s generalized allocation scheme A law of

ON SOME ANALOGUE OF THE GENERALIZED ALLOCATION SCHEME Alexey Chuprunov Kazan State University, Russia István Fazekas University of Debrecen, Hungary 2012 Kolchin s generalized allocation scheme A law of

Financial Simulation Models in General Insurance

Financial Simulation Models in General Insurance By - Peter D. England Abstract Increases in computer power and advances in statistical modelling have conspired to change the way financial modelling is

Financial Simulation Models in General Insurance By - Peter D. England Abstract Increases in computer power and advances in statistical modelling have conspired to change the way financial modelling is

UNIVERSITY OF OSLO. The Poisson model is a common model for claim frequency.

UNIVERSITY OF OSLO Faculty of mathematics and natural sciences Candidate no Exam in: STK 4540 Non-Life Insurance Mathematics Day of examination: December, 9th, 2015 Examination hours: 09:00 13:00 This

UNIVERSITY OF OSLO Faculty of mathematics and natural sciences Candidate no Exam in: STK 4540 Non-Life Insurance Mathematics Day of examination: December, 9th, 2015 Examination hours: 09:00 13:00 This

The Heat Equation. Lectures INF2320 p. 1/88

The Heat Equation Lectures INF232 p. 1/88 Lectures INF232 p. 2/88 The Heat Equation We study the heat equation: u t = u xx for x (,1), t >, (1) u(,t) = u(1,t) = for t >, (2) u(x,) = f(x) for x (,1), (3)

The Heat Equation Lectures INF232 p. 1/88 Lectures INF232 p. 2/88 The Heat Equation We study the heat equation: u t = u xx for x (,1), t >, (1) u(,t) = u(1,t) = for t >, (2) u(x,) = f(x) for x (,1), (3)

STAT2400 STAT2400 STAT2400 STAT2400 STAT2400 STAT2400 STAT2400 STAT2400&3400 STAT2400&3400 STAT2400&3400 STAT2400&3400 STAT3400 STAT3400

Exam P Learning Objectives All 23 learning objectives are covered. General Probability STAT2400 STAT2400 STAT2400 STAT2400 STAT2400 STAT2400 STAT2400 1. Set functions including set notation and basic elements

Exam P Learning Objectives All 23 learning objectives are covered. General Probability STAT2400 STAT2400 STAT2400 STAT2400 STAT2400 STAT2400 STAT2400 1. Set functions including set notation and basic elements

Mixing internal and external data for managing operational risk

Mixing internal and external data for managing operational risk Antoine Frachot and Thierry Roncalli Groupe de Recherche Opérationnelle, Crédit Lyonnais, France This version: January 29, 2002 Introduction

Mixing internal and external data for managing operational risk Antoine Frachot and Thierry Roncalli Groupe de Recherche Opérationnelle, Crédit Lyonnais, France This version: January 29, 2002 Introduction

b g is the future lifetime random variable.

**BEGINNING OF EXAMINATION** 1. Given: (i) e o 0 = 5 (ii) l = ω, 0 ω (iii) is the future lifetime random variable. T Calculate Var Tb10g. (A) 65 (B) 93 (C) 133 (D) 178 (E) 333 COURSE/EXAM 3: MAY 000-1

**BEGINNING OF EXAMINATION** 1. Given: (i) e o 0 = 5 (ii) l = ω, 0 ω (iii) is the future lifetime random variable. T Calculate Var Tb10g. (A) 65 (B) 93 (C) 133 (D) 178 (E) 333 COURSE/EXAM 3: MAY 000-1

Actuarial Applications of a Hierarchical Insurance Claims Model

Actuarial Applications of a Hierarchical Insurance Claims Model Edward W. Frees Peng Shi University of Wisconsin University of Wisconsin Emiliano A. Valdez University of Connecticut February 17, 2008 Abstract

Actuarial Applications of a Hierarchical Insurance Claims Model Edward W. Frees Peng Shi University of Wisconsin University of Wisconsin Emiliano A. Valdez University of Connecticut February 17, 2008 Abstract

STATISTICAL METHODS IN GENERAL INSURANCE. Philip J. Boland National University of Ireland, Dublin philip.j.boland@ucd.ie

STATISTICAL METHODS IN GENERAL INSURANCE Philip J. Boland National University of Ireland, Dublin philip.j.boland@ucd.ie The Actuarial profession appeals to many with excellent quantitative skills who aspire

STATISTICAL METHODS IN GENERAL INSURANCE Philip J. Boland National University of Ireland, Dublin philip.j.boland@ucd.ie The Actuarial profession appeals to many with excellent quantitative skills who aspire

ECON20310 LECTURE SYNOPSIS REAL BUSINESS CYCLE

ECON20310 LECTURE SYNOPSIS REAL BUSINESS CYCLE YUAN TIAN This synopsis is designed merely for keep a record of the materials covered in lectures. Please refer to your own lecture notes for all proofs.

ECON20310 LECTURE SYNOPSIS REAL BUSINESS CYCLE YUAN TIAN This synopsis is designed merely for keep a record of the materials covered in lectures. Please refer to your own lecture notes for all proofs.

e.g. arrival of a customer to a service station or breakdown of a component in some system.

Poisson process Events occur at random instants of time at an average rate of λ events per second. e.g. arrival of a customer to a service station or breakdown of a component in some system. Let N(t) be

Poisson process Events occur at random instants of time at an average rate of λ events per second. e.g. arrival of a customer to a service station or breakdown of a component in some system. Let N(t) be

Institute of Actuaries of India Subject CT3 Probability and Mathematical Statistics

Institute of Actuaries of India Subject CT3 Probability and Mathematical Statistics For 2015 Examinations Aim The aim of the Probability and Mathematical Statistics subject is to provide a grounding in

Institute of Actuaries of India Subject CT3 Probability and Mathematical Statistics For 2015 Examinations Aim The aim of the Probability and Mathematical Statistics subject is to provide a grounding in

Section 5.1 Continuous Random Variables: Introduction

Section 5. Continuous Random Variables: Introduction Not all random variables are discrete. For example:. Waiting times for anything (train, arrival of customer, production of mrna molecule from gene,

Section 5. Continuous Random Variables: Introduction Not all random variables are discrete. For example:. Waiting times for anything (train, arrival of customer, production of mrna molecule from gene,

Properties of Future Lifetime Distributions and Estimation

Properties of Future Lifetime Distributions and Estimation Harmanpreet Singh Kapoor and Kanchan Jain Abstract Distributional properties of continuous future lifetime of an individual aged x have been studied.

Properties of Future Lifetime Distributions and Estimation Harmanpreet Singh Kapoor and Kanchan Jain Abstract Distributional properties of continuous future lifetime of an individual aged x have been studied.

Actuarial Risk Management

ARA syllabus Actuarial Risk Management Aim: To provide the technical skills to apply the principles and methodologies studied under actuarial technical subjects for the identification, quantification and

ARA syllabus Actuarial Risk Management Aim: To provide the technical skills to apply the principles and methodologies studied under actuarial technical subjects for the identification, quantification and

TABLE OF CONTENTS. 4. Daniel Markov 1 173

TABLE OF CONTENTS 1. Survival A. Time of Death for a Person Aged x 1 B. Force of Mortality 7 C. Life Tables and the Deterministic Survivorship Group 19 D. Life Table Characteristics: Expectation of Life

TABLE OF CONTENTS 1. Survival A. Time of Death for a Person Aged x 1 B. Force of Mortality 7 C. Life Tables and the Deterministic Survivorship Group 19 D. Life Table Characteristics: Expectation of Life

Asymptotics for a discrete-time risk model with Gamma-like insurance risks. Pokfulam Road, Hong Kong

Asymptotics for a discrete-time risk model with Gamma-like insurance risks Yang Yang 1,2 and Kam C. Yuen 3 1 Department of Statistics, Nanjing Audit University, Nanjing, 211815, China 2 School of Economics

Asymptotics for a discrete-time risk model with Gamma-like insurance risks Yang Yang 1,2 and Kam C. Yuen 3 1 Department of Statistics, Nanjing Audit University, Nanjing, 211815, China 2 School of Economics

Risk/Arbitrage Strategies: An Application to Stock Option Portfolio Management

Risk/Arbitrage Strategies: An Application to Stock Option Portfolio Management Vincenzo Bochicchio, Niklaus Bühlmann, Stephane Junod and Hans-Fredo List Swiss Reinsurance Company Mythenquai 50/60, CH-8022

Risk/Arbitrage Strategies: An Application to Stock Option Portfolio Management Vincenzo Bochicchio, Niklaus Bühlmann, Stephane Junod and Hans-Fredo List Swiss Reinsurance Company Mythenquai 50/60, CH-8022

Exam C, Fall 2006 PRELIMINARY ANSWER KEY

Exam C, Fall 2006 PRELIMINARY ANSWER KEY Question # Answer Question # Answer 1 E 19 B 2 D 20 D 3 B 21 A 4 C 22 A 5 A 23 E 6 D 24 E 7 B 25 D 8 C 26 A 9 E 27 C 10 D 28 C 11 E 29 C 12 B 30 B 13 C 31 C 14

Exam C, Fall 2006 PRELIMINARY ANSWER KEY Question # Answer Question # Answer 1 E 19 B 2 D 20 D 3 B 21 A 4 C 22 A 5 A 23 E 6 D 24 E 7 B 25 D 8 C 26 A 9 E 27 C 10 D 28 C 11 E 29 C 12 B 30 B 13 C 31 C 14

Premium calculation. summer semester 2013/2014. Technical University of Ostrava Faculty of Economics department of Finance

Technical University of Ostrava Faculty of Economics department of Finance summer semester 2013/2014 Content 1 Fundamentals Insurer s expenses 2 Equivalence principles Calculation principles 3 Equivalence

Technical University of Ostrava Faculty of Economics department of Finance summer semester 2013/2014 Content 1 Fundamentals Insurer s expenses 2 Equivalence principles Calculation principles 3 Equivalence

An Internal Model for Operational Risk Computation

An Internal Model for Operational Risk Computation Seminarios de Matemática Financiera Instituto MEFF-RiskLab, Madrid http://www.risklab-madrid.uam.es/ Nicolas Baud, Antoine Frachot & Thierry Roncalli

An Internal Model for Operational Risk Computation Seminarios de Matemática Financiera Instituto MEFF-RiskLab, Madrid http://www.risklab-madrid.uam.es/ Nicolas Baud, Antoine Frachot & Thierry Roncalli

3 The Standard Real Business Cycle (RBC) Model. Optimal growth model + Labor decisions

Model. Optimal growth model + Labor decisions") Franck Portier TSE Macro II 29-21 Chapter 3 Real Business Cycles 36 3 The Standard Real Business Cycle (RBC) Model Perfectly competitive economy Optimal growth model + Labor decisions 2 types of agents

Franck Portier TSE Macro II 29-21 Chapter 3 Real Business Cycles 36 3 The Standard Real Business Cycle (RBC) Model Perfectly competitive economy Optimal growth model + Labor decisions 2 types of agents

Exam P - Total 23/23 - 1 -

Exam P Learning Objectives Schools will meet 80% of the learning objectives on this examination if they can show they meet 18.4 of 23 learning objectives outlined in this table. Schools may NOT count a

Exam P Learning Objectives Schools will meet 80% of the learning objectives on this examination if they can show they meet 18.4 of 23 learning objectives outlined in this table. Schools may NOT count a

An Extension Model of Financially-balanced Bonus-Malus System

An Extension Model of Financially-balanced Bonus-Malus System Other : Ratemaking, Experience Rating XIAO, Yugu Center for Applied Statistics, Renmin University of China, Beijing, 00872, P.R. China Phone:

An Extension Model of Financially-balanced Bonus-Malus System Other : Ratemaking, Experience Rating XIAO, Yugu Center for Applied Statistics, Renmin University of China, Beijing, 00872, P.R. China Phone:

RISKY LOSS DISTRIBUTIONS AND MODELING THE LOSS RESERVE PAY-OUT TAIL

Review of Applied Economics, Vol. 3, No. 1-2, (2007) : 1-23 RISKY LOSS DISTRIBUTIONS AND MODELING THE LOSS RESERVE PAY-OUT TAIL J. David Cummins *, James B. McDonald ** & Craig Merrill *** Although an

Review of Applied Economics, Vol. 3, No. 1-2, (2007) : 1-23 RISKY LOSS DISTRIBUTIONS AND MODELING THE LOSS RESERVE PAY-OUT TAIL J. David Cummins *, James B. McDonald ** & Craig Merrill *** Although an

Premium Calculation. Lecture: Weeks 12-14. Lecture: Weeks 12-14 (STT 455) Premium Calculation Fall 2014 - Valdez 1 / 31

Premium Calculation Fall 2014 - Valdez 1 / 31") Premium Calculation Lecture: Weeks 12-14 Lecture: Weeks 12-14 (STT 455) Premium Calculation Fall 2014 - Valdez 1 / 31 Preliminaries Preliminaries An insurance policy (life insurance or life annuity) is

Premium Calculation Lecture: Weeks 12-14 Lecture: Weeks 12-14 (STT 455) Premium Calculation Fall 2014 - Valdez 1 / 31 Preliminaries Preliminaries An insurance policy (life insurance or life annuity) is

( ) is proportional to ( 10 + x)!2. Calculate the

is proportional to ( 10 + x)!2. Calculate the") PRACTICE EXAMINATION NUMBER 6. An insurance company eamines its pool of auto insurance customers and gathers the following information: i) All customers insure at least one car. ii) 64 of the customers

PRACTICE EXAMINATION NUMBER 6. An insurance company eamines its pool of auto insurance customers and gathers the following information: i) All customers insure at least one car. ii) 64 of the customers

Using the Delta Method to Construct Confidence Intervals for Predicted Probabilities, Rates, and Discrete Changes

Using the Delta Method to Construct Confidence Intervals for Predicted Probabilities, Rates, Discrete Changes JunXuJ.ScottLong Indiana University August 22, 2005 The paper provides technical details on

Using the Delta Method to Construct Confidence Intervals for Predicted Probabilities, Rates, Discrete Changes JunXuJ.ScottLong Indiana University August 22, 2005 The paper provides technical details on

COURSE 3 SAMPLE EXAM

COURSE 3 SAMPLE EXAM Although a multiple choice format is not provided for some questions on this sample examination, the initial Course 3 examination will consist entirely of multiple choice type questions.

COURSE 3 SAMPLE EXAM Although a multiple choice format is not provided for some questions on this sample examination, the initial Course 3 examination will consist entirely of multiple choice type questions.

MATH4427 Notebook 2 Spring 2016. 2 MATH4427 Notebook 2 3. 2.1 Definitions and Examples... 3. 2.2 Performance Measures for Estimators...

MATH4427 Notebook 2 Spring 2016 prepared by Professor Jenny Baglivo c Copyright 2009-2016 by Jenny A. Baglivo. All Rights Reserved. Contents 2 MATH4427 Notebook 2 3 2.1 Definitions and Examples...................................

MATH4427 Notebook 2 Spring 2016 prepared by Professor Jenny Baglivo c Copyright 2009-2016 by Jenny A. Baglivo. All Rights Reserved. Contents 2 MATH4427 Notebook 2 3 2.1 Definitions and Examples...................................

ACTS 4301 FORMULA SUMMARY Lesson 1: Probability Review. Name f(x) F (x) E[X] Var(X) Name f(x) E[X] Var(X) p x (1 p) m x mp mp(1 p)

![ACTS 4301 FORMULA SUMMARY Lesson 1: Probability Review. Name f(x) F (x) E[X] Var(X) Name f(x) E[X] Var(X) p x (1 p) m x mp mp(1 p)](/thumbs/39/20405687.jpg "ACTS 4301 FORMULA SUMMARY Lesson 1: Probability Review. Name f(x) F (x) E[X] Var(X) Name f(x) E[X] Var(X) p x (1 p) m x mp mp(1 p)") ACTS 431 FORMULA SUMMARY Lesson 1: Probability Review 1. VarX)= E[X 2 ]- E[X] 2 2. V arax + by ) = a 2 V arx) + 2abCovX, Y ) + b 2 V ary ) 3. V ar X) = V arx) n 4. E X [X] = E Y [E X [X Y ]] Double expectation

ACTS 431 FORMULA SUMMARY Lesson 1: Probability Review 1. VarX)= E[X 2 ]- E[X] 2 2. V arax + by ) = a 2 V arx) + 2abCovX, Y ) + b 2 V ary ) 3. V ar X) = V arx) n 4. E X [X] = E Y [E X [X Y ]] Double expectation

Dependence in non-life insurance

Dependence in non-life insurance Hanna Arvidsson and Sofie Francke U.U.D.M. Project Report 2007:23 Examensarbete i matematisk statistik, 20 poäng Handledare och examinator: Ingemar Kaj Juni 2007 Department

Dependence in non-life insurance Hanna Arvidsson and Sofie Francke U.U.D.M. Project Report 2007:23 Examensarbete i matematisk statistik, 20 poäng Handledare och examinator: Ingemar Kaj Juni 2007 Department

The Black-Scholes-Merton Approach to Pricing Options

he Black-Scholes-Merton Approach to Pricing Options Paul J Atzberger Comments should be sent to: atzberg@mathucsbedu Introduction In this article we shall discuss the Black-Scholes-Merton approach to determining

he Black-Scholes-Merton Approach to Pricing Options Paul J Atzberger Comments should be sent to: atzberg@mathucsbedu Introduction In this article we shall discuss the Black-Scholes-Merton approach to determining

1 The Black-Scholes model: extensions and hedging

1 The Black-Scholes model: extensions and hedging 1.1 Dividends Since we are now in a continuous time framework the dividend paid out at time t (or t ) is given by dd t = D t D t, where as before D denotes

1 The Black-Scholes model: extensions and hedging 1.1 Dividends Since we are now in a continuous time framework the dividend paid out at time t (or t ) is given by dd t = D t D t, where as before D denotes

Modern Actuarial Risk Theory

Modern Actuarial Risk Theory Modern Actuarial Risk Theory by Rob Kaas University of Amsterdam, The Netherlands Marc Goovaerts Catholic University of Leuven, Belgium and University of Amsterdam, The Netherlands

Modern Actuarial Risk Theory Modern Actuarial Risk Theory by Rob Kaas University of Amsterdam, The Netherlands Marc Goovaerts Catholic University of Leuven, Belgium and University of Amsterdam, The Netherlands

Revenue Management & Insurance Cycle J-B Crozet, FIA, CFA

J-B Crozet, FIA, CFA Abstract: This paper investigates how an insurer s pricing strategy can be adapted to respond to market conditions, and in particular the insurance cycle. For this purpose, we explore

J-B Crozet, FIA, CFA Abstract: This paper investigates how an insurer s pricing strategy can be adapted to respond to market conditions, and in particular the insurance cycle. For this purpose, we explore

Week 2: Exponential Functions

Week 2: Exponential Functions Goals: Introduce exponential functions Study the compounded interest and introduce the number e Suggested Textbook Readings: Chapter 4: 4.1, and Chapter 5: 5.1. Practice Problems:

Week 2: Exponential Functions Goals: Introduce exponential functions Study the compounded interest and introduce the number e Suggested Textbook Readings: Chapter 4: 4.1, and Chapter 5: 5.1. Practice Problems:

Modeling Individual Claims for Motor Third Party Liability of Insurance Companies in Albania

Modeling Individual Claims for Motor Third Party Liability of Insurance Companies in Albania Oriana Zacaj Department of Mathematics, Polytechnic University, Faculty of Mathematics and Physics Engineering

Modeling Individual Claims for Motor Third Party Liability of Insurance Companies in Albania Oriana Zacaj Department of Mathematics, Polytechnic University, Faculty of Mathematics and Physics Engineering

A revisit of the hierarchical insurance claims modeling

A revisit of the hierarchical insurance claims modeling Emiliano A. Valdez Michigan State University joint work with E.W. Frees* * University of Wisconsin Madison Statistical Society of Canada (SSC) 2014

A revisit of the hierarchical insurance claims modeling Emiliano A. Valdez Michigan State University joint work with E.W. Frees* * University of Wisconsin Madison Statistical Society of Canada (SSC) 2014

Nonparametric adaptive age replacement with a one-cycle criterion

Nonparametric adaptive age replacement with a one-cycle criterion P. Coolen-Schrijner, F.P.A. Coolen Department of Mathematical Sciences University of Durham, Durham, DH1 3LE, UK e-mail: Pauline.Schrijner@durham.ac.uk

Nonparametric adaptive age replacement with a one-cycle criterion P. Coolen-Schrijner, F.P.A. Coolen Department of Mathematical Sciences University of Durham, Durham, DH1 3LE, UK e-mail: Pauline.Schrijner@durham.ac.uk

GLMs: Gompertz s Law. GLMs in R. Gompertz s famous graduation formula is. or log µ x is linear in age, x,

Computing: an indispensable tool or an insurmountable hurdle? Iain Currie Heriot Watt University, Scotland ATRC, University College Dublin July 2006 Plan of talk General remarks The professional syllabus

Computing: an indispensable tool or an insurmountable hurdle? Iain Currie Heriot Watt University, Scotland ATRC, University College Dublin July 2006 Plan of talk General remarks The professional syllabus

The Dirichlet-Multinomial and Dirichlet-Categorical models for Bayesian inference

The Dirichlet-Multinomial and Dirichlet-Categorical models for Bayesian inference Stephen Tu tu.stephenl@gmail.com 1 Introduction This document collects in one place various results for both the Dirichlet-multinomial

The Dirichlet-Multinomial and Dirichlet-Categorical models for Bayesian inference Stephen Tu tu.stephenl@gmail.com 1 Introduction This document collects in one place various results for both the Dirichlet-multinomial

c u @ college College is for everyone! When: Sunday, February 20, 2011 2:00 p.m. - 6:30 p.m.

Evaluating Liquidation Strategies for Insurance Companies 1

Evaluating Liquidation Strategies for Insurance Companies 1 Thomas Berry-Stölzle Graduate School of Risk Management University of Cologne Albertus-Magnus-Platz 50923 Koeln GERMANY Tel. +49-(0)221-470-7703

Evaluating Liquidation Strategies for Insurance Companies 1 Thomas Berry-Stölzle Graduate School of Risk Management University of Cologne Albertus-Magnus-Platz 50923 Koeln GERMANY Tel. +49-(0)221-470-7703

Internet Dial-Up Traffic Modelling

NTS 5, Fifteenth Nordic Teletraffic Seminar Lund, Sweden, August 4, Internet Dial-Up Traffic Modelling Villy B. Iversen Arne J. Glenstrup Jens Rasmussen Abstract This paper deals with analysis and modelling

NTS 5, Fifteenth Nordic Teletraffic Seminar Lund, Sweden, August 4, Internet Dial-Up Traffic Modelling Villy B. Iversen Arne J. Glenstrup Jens Rasmussen Abstract This paper deals with analysis and modelling

Valuation, Pricing of Options / Use of MATLAB

CS-5 Computational Tools and Methods in Finance Tom Coleman Valuation, Pricing of Options / Use of MATLAB 1.0 Put-Call Parity (review) Given a European option with no dividends, let t current time T exercise

CS-5 Computational Tools and Methods in Finance Tom Coleman Valuation, Pricing of Options / Use of MATLAB 1.0 Put-Call Parity (review) Given a European option with no dividends, let t current time T exercise

Fluid Approximation of Smart Grid Systems: Optimal Control of Energy Storage Units

Fluid Approximation of Smart Grid Systems: Optimal Control of Energy Storage Units by Rasha Ibrahim Sakr, B.Sc. A thesis submitted to the Faculty of Graduate and Postdoctoral Affairs in partial fulfillment

Fluid Approximation of Smart Grid Systems: Optimal Control of Energy Storage Units by Rasha Ibrahim Sakr, B.Sc. A thesis submitted to the Faculty of Graduate and Postdoctoral Affairs in partial fulfillment

Overview of Monte Carlo Simulation, Probability Review and Introduction to Matlab

Monte Carlo Simulation: IEOR E4703 Fall 2004 c 2004 by Martin Haugh Overview of Monte Carlo Simulation, Probability Review and Introduction to Matlab 1 Overview of Monte Carlo Simulation 1.1 Why use simulation?

Monte Carlo Simulation: IEOR E4703 Fall 2004 c 2004 by Martin Haugh Overview of Monte Carlo Simulation, Probability Review and Introduction to Matlab 1 Overview of Monte Carlo Simulation 1.1 Why use simulation?

Math 461 Fall 2006 Test 2 Solutions

Math 461 Fall 2006 Test 2 Solutions Total points: 100. Do all questions. Explain all answers. No notes, books, or electronic devices. 1. [105+5 points] Assume X Exponential(λ). Justify the following two

Math 461 Fall 2006 Test 2 Solutions Total points: 100. Do all questions. Explain all answers. No notes, books, or electronic devices. 1. [105+5 points] Assume X Exponential(λ). Justify the following two

ACTS 4302 SOLUTION TO MIDTERM EXAM Derivatives Markets, Chapters 9, 10, 11, 12, 18. October 21, 2010 (Thurs)

") Problem ACTS 4302 SOLUTION TO MIDTERM EXAM Derivatives Markets, Chapters 9, 0,, 2, 8. October 2, 200 (Thurs) (i) The current exchange rate is 0.0$/. (ii) A four-year dollar-denominated European put option

Problem ACTS 4302 SOLUTION TO MIDTERM EXAM Derivatives Markets, Chapters 9, 0,, 2, 8. October 2, 200 (Thurs) (i) The current exchange rate is 0.0$/. (ii) A four-year dollar-denominated European put option

Fundamentals of Actuarial Mathematics. 3rd Edition

Brochure More information from http://www.researchandmarkets.com/reports/2866022/ Fundamentals of Actuarial Mathematics. 3rd Edition Description: - Provides a comprehensive coverage of both the deterministic

Brochure More information from http://www.researchandmarkets.com/reports/2866022/ Fundamentals of Actuarial Mathematics. 3rd Edition Description: - Provides a comprehensive coverage of both the deterministic

MATH 425, PRACTICE FINAL EXAM SOLUTIONS.

MATH 45, PRACTICE FINAL EXAM SOLUTIONS. Exercise. a Is the operator L defined on smooth functions of x, y by L u := u xx + cosu linear? b Does the answer change if we replace the operator L by the operator

MATH 45, PRACTICE FINAL EXAM SOLUTIONS. Exercise. a Is the operator L defined on smooth functions of x, y by L u := u xx + cosu linear? b Does the answer change if we replace the operator L by the operator

MINIMUM SOLVENCY MARGIN OF A GENERAL INSURANCE COMPANY: PROPOSALS AND CURIOSITIES ROBERTO DARIS GIANNI BOSI

Insurance Convention 1998 General & ASTIN Colloquium MINIMUM SOLVENCY MARGIN OF A GENERAL INSURANCE COMPANY: PROPOSALS AND CURIOSITIES ROBERTO DARIS GIANNI BOSI 1998 GENERAL INSURANCE CONVENTION AND ASTIN

Insurance Convention 1998 General & ASTIN Colloquium MINIMUM SOLVENCY MARGIN OF A GENERAL INSURANCE COMPANY: PROPOSALS AND CURIOSITIES ROBERTO DARIS GIANNI BOSI 1998 GENERAL INSURANCE CONVENTION AND ASTIN

ACTUARIAL MATHEMATICS FOR LIFE CONTINGENT RISKS

ACTUARIAL MATHEMATICS FOR LIFE CONTINGENT RISKS DAVID C. M. DICKSON University of Melbourne MARY R. HARDY University of Waterloo, Ontario V HOWARD R. WATERS Heriot-Watt University, Edinburgh CAMBRIDGE

ACTUARIAL MATHEMATICS FOR LIFE CONTINGENT RISKS DAVID C. M. DICKSON University of Melbourne MARY R. HARDY University of Waterloo, Ontario V HOWARD R. WATERS Heriot-Watt University, Edinburgh CAMBRIDGE

Practical Calculation of Expected and Unexpected Losses in Operational Risk by Simulation Methods

Practical Calculation of Expected and Unexpected Losses in Operational Risk by Simulation Methods Enrique Navarrete 1 Abstract: This paper surveys the main difficulties involved with the quantitative measurement

Practical Calculation of Expected and Unexpected Losses in Operational Risk by Simulation Methods Enrique Navarrete 1 Abstract: This paper surveys the main difficulties involved with the quantitative measurement

Exact Confidence Intervals

Math 541: Statistical Theory II Instructor: Songfeng Zheng Exact Confidence Intervals Confidence intervals provide an alternative to using an estimator ˆθ when we wish to estimate an unknown parameter

Math 541: Statistical Theory II Instructor: Songfeng Zheng Exact Confidence Intervals Confidence intervals provide an alternative to using an estimator ˆθ when we wish to estimate an unknown parameter

University of Maryland Fraternity & Sorority Life Spring 2015 Academic Report

University of Maryland Fraternity & Sorority Life Academic Report Academic and Population Statistics Population: # of Students: # of New Members: Avg. Size: Avg. GPA: % of the Undergraduate Population

University of Maryland Fraternity & Sorority Life Academic Report Academic and Population Statistics Population: # of Students: # of New Members: Avg. Size: Avg. GPA: % of the Undergraduate Population

Statistical Analysis of Life Insurance Policy Termination and Survivorship

Statistical Analysis of Life Insurance Policy Termination and Survivorship Emiliano A. Valdez, PhD, FSA Michigan State University joint work with J. Vadiveloo and U. Dias Session ES82 (Statistics in Actuarial

Statistical Analysis of Life Insurance Policy Termination and Survivorship Emiliano A. Valdez, PhD, FSA Michigan State University joint work with J. Vadiveloo and U. Dias Session ES82 (Statistics in Actuarial

INCREASED LIMITS RATEMAKING FOR LIABILITY INSURANCE

INCREASED LIMITS RATEMAKING FOR LIABILITY INSURANCE July 2006 By Joseph M. Palmer, FCAS, MAAA, CPCU INCREASED LIMITS RATEMAKING FOR LIABILITY INSURANCE By Joseph M. Palmer, FCAS, MAAA, CPCU 1. INTRODUCTION

INCREASED LIMITS RATEMAKING FOR LIABILITY INSURANCE July 2006 By Joseph M. Palmer, FCAS, MAAA, CPCU INCREASED LIMITS RATEMAKING FOR LIABILITY INSURANCE By Joseph M. Palmer, FCAS, MAAA, CPCU 1. INTRODUCTION

November 2000 Course 3

November Course 3 Society of Actuaries/Casualty Actuarial Society November - - GO ON TO NEXT PAGE Questions through 36 are each worth points; questions 37 through 44 are each worth point.. For independent

November Course 3 Society of Actuaries/Casualty Actuarial Society November - - GO ON TO NEXT PAGE Questions through 36 are each worth points; questions 37 through 44 are each worth point.. For independent