Risk/Arbitrage Strategies: An Application to Stock Option Portfolio Management

|

|

|

- Vivian Robertson

- 8 years ago

- Views:

Transcription

1 Risk/Arbitrage Strategies: An Application to Stock Option Portfolio Management Vincenzo Bochicchio, Niklaus Bühlmann, Stephane Junod and Hans-Fredo List Swiss Reinsurance Company Mythenquai 50/60, CH-8022 Zurich Telephone: Facsimile: Mark H.A. Davis Tokyo-Mitsubishi International plc 6 Broadgate, London EC2M 2AA Telephone: Facsimile: Abstract. Asset/Liability management, optimal fund design and optimal portfolio selection have been key issues of interest to the (re)insurance and investment banking communities, respectively, for some years - especially in the design of advanced risktransfer solutions for clients in the Fortune 500 group of companies. Recently, the securitization of (re)insurance claims portfolios has also attracted considerable attention among (re)insurance companies and their clients. It turns out that the new concept of limited risk arbitrage (LRA) investment management in a diffusion type liabilities, securities and derivatives market introduced in our papers Baseline for Exchange Rate Risks of an International Reinsurer, AFIR 1996, Vol. I, p. 395, and Risk/Arbitrage Strategies: A New Concept for Asset/Liability Management, Optimal Fund Design and Optimal Portfolio Selection in a Dynamic, Continuous-Time Framework Part I: Securities Markets and Part II: Securities and Derivatives Markets, AFIR 1997, Vol. II, p. 543, is immediately applicable to all of the above mentioned practical problems. The competitive advantage of applying LRA strategies in the design of advanced risk transfer solutions for Fortune 500 clients lies in the fact that these techniques achieve an efficient allocation of risk in an overall portfolio context rather than eliminating (at a high price) derivatives risk exposure on a singleinstrument basis by replication (hedging) with underlying securities. The main quantities of practical interest (i.e., the optimal LRA asset allocation, etc.) can be derived by solving a (quasi-) linear partial differential equation of the second order (e.g., by using a finite difference approximation with locally uniform convergence properties, see Part III: A Risk/Arbitrage Pricing Theory) or (in our more sophisticated impluse control approach, see Part IV: An Impulse Control Approach to Limited Risk Arbitrage) by using an efficient Markov chain approximation scheme [i.e., essentially the same (formal) finite difference techniques (with weak convergence properties)]. However, in many practical applications there are much simpler numerical solution techniques, see Part V: A Guide to Efficient Numerical Implementations. We present here such an alternative lattice-bared options portfolio 25

insurance and investment banking communities, respectively, for some years")

2 management methodology which allows the determination of the main LRA quantities by simply solving a linear program at each lattice node. Key Words and Phrases. Risk/Arbitrage platform, dynamic programming procedure, contingent claim price/sensitivity forecast, LRA optimization program, state dependent linear optimization. Contents. 1. Introduction Swiss Re Registered Share Model - Risk-free Interest Rate - Volatility - Dividend Yield - European Call Options - European Put Options - One Period LRA Strategies - Base Value Scenario - Minimum Premium Scenario - Maximum Premium Scenario 2. LRA Option Strategies 3. Mitarbeiter-Option Trading Appendix: References Base Value Scenario Minimum Premium Scenario Maximum Premium Scenario Introduction In order to gain a first insight into how limited risk arbitrage (LRA) trading and portfolio management strategies work in practice and can be successfully used in modern (re)insurance and corporate and investment banking applications, we consider long-dated European call and put options on the Swiss Re registered share (RUKN) with a current market value of CHF (as of 18 October 1995, see also Bühlmann, Davis and List [1], [2] and [3]). Swiss Re Registered Share Model. In a first approximation, the Swiss Re registered share can be assumed to follow an Ito process 26

3 risk -averse evolution risk-neutral evolution standard Brownian motions with constant expected rate of return µ = 17% and constant volatility σ (geometric Brownian motion). The risk-free rate of interest r and the dividend yield y can also be assumed to be constant over the 5 year option maturity horizon. Risk-free Interest Rate. The risk-free rate of interest applicable during the 5 year option maturity period is estimated to be 4% p.a. (continuously compounded). The sensitivity of the European call and put option characteristics with respect to changes in the riskfree interest rate is however examined for a rate variation range from 3% to 5% (p.a.). Volatility. The volatility of the Swiss Re registered share applicable during the 5 year option maturity period is estimated to be 22.5% p.a.; the sensitivity of the European call and put option characteristics with respect to changes in RUKN price volatility is however examined for a volatility variation range from 20% to 25% (pa.). Dividend Yield. The dividend yield of the Swiss Re registered share applicable during the 5 year option maturity period is calculated as follows: Current Dividend Value (18 October 1995): CHF Current Share Value (18 October 1995): CHF Recent Dividend Growth Rate Estimates (18 October 1995): UBS SBC Warburg James Capel Average 13.3% pa. 26.0% p.a 21.6% pa 20.3% p.a Dividend Yield: 27

.")

4 dividend in year i futures price of registered share in year i increase in share position in year i (reinvestment of dividends) equation for dividend yield y Note that this equation is simplified for ease of calculation. A more accurate (and more complicated) expression would be The effects of this simplification are compensated yield variation range outlined below. for in the choice of the dividend Numerical Evaluation (Mathematics): With the initial values D0 = and S0 = Mathematica calculates the implied dividend yields for the above interest rate and dividend growth rate scenarios as follows: g= 13% p.a r = 3% p.a 4% p.a 5% p.a y = 1.66% p.a 1.60% p.a 1.55% p.a g = 20% p.a r= 3% p.a 4% p.a 5% p.a y = 2.02% p.a 1.96% p.a 1.89% p.a g = 26% p.a r = 3% p.a 4% p.a 5% p.a y = 2.39% p.a 2.31% p.a 2.23% p.a The dividend yield of the Swiss Re registered share applicable during the 5 year option maturity period is therefore taken to be 2% p.a. (continuously compounded). The sensitivity of the European call and put option characteristics with respect to changes in dividend yield is however examined for a yield variation range from 1.6% to 2.4% (p.a.). European Call Options. With the above (Black & Scholes) stock price model futures prices of the Swiss Re registered share (RUKN) and the values of corresponding European call options can be analytically calculated as follows: 28

5 Futures: T futures maturity European Call: T option maturity X option strike N[ ] standard normal distribution Specifically, we consider the call options (strike schedule) European Call Option Option Price Exercise Price Base Value Minimum Premium Maximum Premium Base Value Minimum Premium: Maximum Premium: volatility = 22.5% volatility = 20% volatility = 25% dividend yield = 2% dividend yield = 2.4% dividend yield = 1.6% interest rate = 4% interest rate = 3% interest rate = 5% or in graphical form 29

6 The associated option risk parameters are 30

7 (note the relatively modest first and second order risk exposure with respect to changes in the value of the underlying Swiss Re registered share, RUKN) 31

8 as a function of the exercise or strike price. While the call option s first and second order risk exposure with respect to changes in the value of the underlying Swiss Re registered share (delta and gamma) is relatively modest, its volatility (vega), interest rate (rho rate) and dividend yield (rho yield) risk exposures are quite significant. European Put Options. The price of a European put option is similarly Like above, we consider the put options (strike schedule) European Put Option Option Price Exercise Price Base Value Maximum Premium Minimum Premium Base Value: Maximum Premium: Minimum Premium: volatility = 22.5% volatility 20% = volatility = 25% dividend yield = 2% dividend yield = 2.4% dividend yield = 1.6% interest rate = 4% interest rate = 3% interest rate = 5% or in graphical form 32

European Put Option Option Price Exercise Price Base Value Maximum Premium Minimum Premium")

9 (note that of course now the maximum and the minimum premium scenarios have the opposite meanings). The associated option risk parameters are 33

.")

10 (note again the relatively modest first and second order risk exposure with respect to changes in the value of the underlying Swiss Re registered share, RUKN) 34

11 as a function of the exercise or strike price. Again, the option s volatility, interest rate and dividend yield risk exposures are quite significant. One Period LRA Strategies. As a next step, therefore, we ask ourselves whether by wisely (i.e., in a limited risk arbitrage sense) choosing among RUKN and all the above European options, significantly better investment opportunities could be created. Specifically, we use the linear program in our analysis (see also Part I: Securities Markets, Part II : Securities and Derivatives Markets and Part V: A Guide to Efficient Numerical Implementations). Furthermore, we consider LRA strategies under the above three scenarios, where we define the maximum premium and the minimum premium scenarios as in the call options case. Base Value Scenario. In the base value scenario, the portfolio components parameters are 35

12 Instrument Parameters Term Period 18, 10, Price 95 Delta Gamma Theta Vega Rho Rate Rho Yield???????? Instrument RUKN C C C C C C C C C C C P P P P P P P P P P P (the position bounds usually implement trading constraints, especially on liquidity; here they are chosen arbitrarily) and a maximum value / maximum theta / minimum vega LRA strategy is Model Parameters a (Value) 1 b Theta 1 c (Delta) 0 d (Gamma) 0 e (Vega) 1 LRA Strategy f (Rho Rate) 0 g (Rho Yield) 0 Minimum Maximum Value Number of Instruments 23 Delta Value Lower Bound Gamma Value Upper Bound Theta Delta Lower Bound Vega Delta Upper Bound Rho Rate Gamma Lower Bound Rho Yield Gamma Upper Bound Theta Lower Bound Result 1 Theta Upper Bound Vega Lower Bound Vega Upper Bound Rho Rate Lower Bound Rho Rate Upper Bound Rho Yield Lower Bound Rho Yield Upper Bound One reason for minimizing the portfolio vega would be to keep the effects of model miss-specification with respect to the volatility of RUKN minimal. In general, however, limited risk arbitrage investment management allows the exact positioning of a securities, futures and options portfolio according to a trader s or portfolio manager's beliefs and expectations about future market moves. 36

13 (result = 1 above means that the LRA strategy is not unique; furthermore, the portfolio value / portfolio theta / portfolio vega constraints are not considered as we maximize portfolio value / maximize portfolio theta / minimize portfolio vega). As interest rate risk and dividend yield risk are the dominating exposures if a purchase of the above European call or put options is considered, an interesting LRA strategy would be one that also minimizes this exposure - to 10%, say: Model Parameters a (Value) 1 b (Theta) 1 c (Delta) 0 d (Gamma) 0 e (Vega) -1 LRA Strategy f (Rho Rate) 0 g (Rho Yield) 0 Minimum Maximum Value Number of Instruments 23 Delta Value Lower Bound Gamma Value upper Bound Theta Delta Lower Bound Vega Delta Upper Bound Rho Rate Gamma Lower Bound Rho Yield Gamma Upper Bound Theta Lower Bound Result 1 Theta Upper Bound Vega Lower Bound Vega Upper Bound Rho Rate Lower Bound Rho Rate Upper Bound Rho Yield Lower Bound Rho Yield Upper Bound

1 b (Theta) 1 c (Delta) 0 d (Gamma) 0 e (Vega) -1 LRA Strategy f (Rho Rate) 0 g (Rho Yield) 0 Minimum Maximum Value 1326.")

14 On the other hand, a significant increase2 in the investor s risk tolerances for the portfolio delta (instantaneous investment risk) and the portfolio gamma (future risk dynamics) has the following effect on the corresponding LRA asset allocation: A. Minimum Vega. Model Parameters a (Value) 1 b (Theta) 1 c (Delta) 0 d (Gamma) 0 e (Vega) -1 LRA Strategy f (Rho Rate) 0 g (Rho Yield) 0 Minimum Maximum Value Number of Instruments 23 Delta Value Lower Bound Gamma Value Upper Bound Theta Delta Lower Bound Vega Delta Upper Bound Rho Rate Gamma Lower Bound Rho Yield Gamma Upper Bound Theta Lower Bound Result 1 Theta Upper Bound Vega Lower Bound Vega Upper Bound Rho Rate Lower Bound Rho Rate Upper Bound Rho Yield Lower Bound Rho Yield Upper Bound ² The new limits for delta and gamma are chosen such that the effects of a 1% change in interest rates and dividend yield are of the same order of magnitude as a 1 CHF change in the value of RUKN. 38

15 The enormous vega (exposure with respect to volatility changes of RUKN) could be quite advantageous in the case where market analysts strongly believe in a decrease in RUKN volatility over the investment period considered: a 1% decrease in RUKN volatility would increase the LRA portfolio value by CHF Such volatility changes could be effects of changes in the underlying fundamentals of RUKN or be implications of changes in the dynamics of the futures and options markets (implied volatility). 5. Constrained Vega. Model parameters a (Value) 1 b (Theta) 1 c (Delta) 0 d (Gamma) 0 e (Vega) 0 LRA Strategy f (Rho Rate) 0 g (Rho Yield) 0 Minimum Maximum Value Number of Instruments 23 Delta Value Lower Bound Gamma Value Upper Bound Theta Delta Lower Bound Vega Delta Upper Bound Rho Rate Gamma Lower Bound Rho Yield Gamma Upper Bound Theta Lower Bound Result Theta Upper Bound Vega Lower Bound Vega Upper Bound Rho Rate Lower Bound Rho Rate Upper Bound Rho Yield Lower Bound Rho Yield Upper Bound

1 b (Theta) 1 c (Delta) 0 d (Gamma) 0 e (Vega) 0 LRA Strategy f (Rho Rate) 0 g (Rho Yield) 0 Minimum Maximum Value 122880.")

16 A constrained vega strategy would not try to position the LRA portfolio with respect to strong expectations about a decrease in RUKN volatility but rather strive to keep the effects of volatility changes (on LRA portfolio value) small: in the above example an adverse (i.e., upward) move in RUKN volatility of 1% over the next trading period would only cost CHF Note in such a context also the following zero exposure (= zero miss-specification error ) LRA strategies for both vega and rho: C. Zero Vega. Model Parameters a (Value) b (Theta) c (Delta) d (Gamma) e (Vega) f (Rho Rate) g (Rho Yield) Number of Instruments Minimum Maximum LRA Strategy Value Delta Value Lower Bound Gamma Value Upper Bound Theta Delta Lower Bound Vega Delta Upper Bound Rho Rate Gamma Lower Bound Rho Yield Gamma Upper Bound Theta Lower Bound Result Theta Upper Bound Vega Lower Bound Vega Upper Bound Rho Rate Lower Bound Rho Rate Upper Bound Rho Yield Lower Bound Rho Yield Upper Bound

b (Theta) c (Delta) d (Gamma) 1 1 0 0 e (Vega) f (Rho Rate) g (Rho Yield) Number of Instruments 0 0 0 23 Minimum Maximum LRA Strategy Value Delta 122881 6516 100 0000 Value")

17 Note the remarkable similarity of the positions held: 41

18 D. Zero Vega, Zero Rho (Rate). Model Parameters a (Value) 1 b (Theta) 1 c (Delta) 0 d (Gamma) 0 e (Vega) 0 LRA Strategy F (Rho Rate) 0 g (Rho yield) 0 Minimum Maximum Value Number of Instruments 23 Delta 100_0000 Value Level Bound Gamma Value upper bound Theta Delta Lower Bound _0000 Vega Delta Upper Bound Rho Rate Gamma Lower Bound Rho Yield Gamma Upper Bound Theta Lower Bound Result Theta Upper Bound Vega Lower Bound Vega Upper Bound Rho Rate Lower Bound Rho Rate Upper Bound Rho Yield Bound Rho Yield Upper Bound

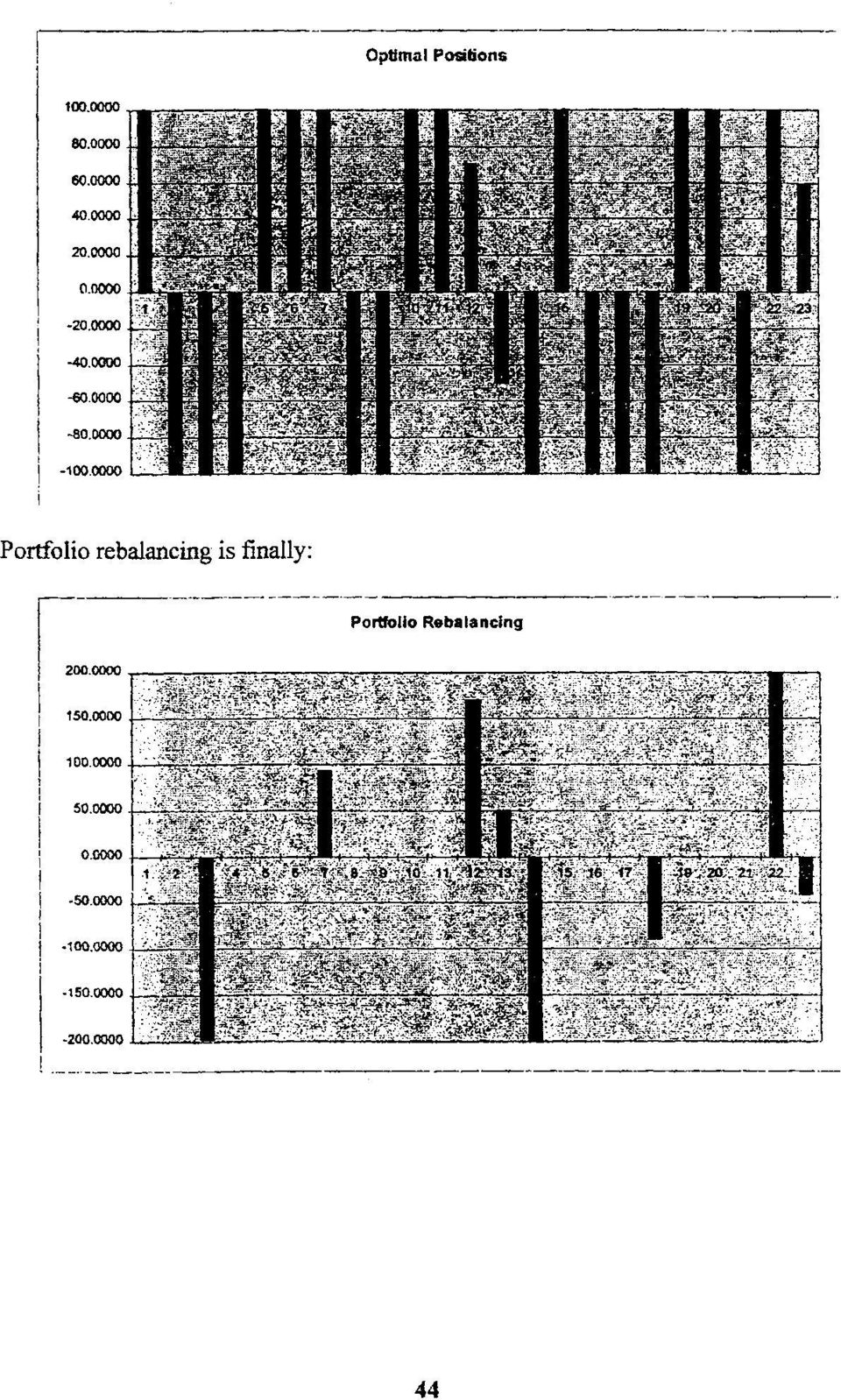

19 Portfolio rebalancing is now: E. Zero Vega. Zero Rho (Rate), Zero Rho (Yield) Model Parameters a (Value) 1 b (Theta) 1 c (Delta) 0 d (Gamma) 0 e (Vega) 0 LRA Strategy f(rho Rate) 0 g (Rho Yield) 0 Minimum Maximum Value Number of Instruments 23 Delta Value Lower Bound Gamma Value Upper Bound Theta Delta Lower Bound Vega Delta Upper Bound Rho Rate Gamma Lower Bound t Rho Yield Gamma Upper Bound Theta Lower Bound Result 1 Theta Upper Bound Vega Lower Bound Vega Upper Bound Rho Rate Lower Bound Rho rate Upper Bound Rho Yield Lower Bound Rho Yield Upper Bound

20 Portfolio rebalancing is finally: 44

21 Minimum Premium Scenario. In the minimum premium scenario, the portfolio components parameters are Instrument Parameters Time Period Fixe Delta Gamma Theta Vega Am Rate Am Yield Low Bound Up Bound?? RLKN C C C C C C C C C C C P P P P P P P t _ P P P _ P and a maximum value / maximum theta / minimum vega LRA strategy is Model Parameters a (Value) 1 b (Theta) c (Delta) 1 0 d (Gamma) 0 e (Vega) -1 LRA Strategy f (Rho Rate) 0 g (Rho Yield) 0 Minimum Maximum Value Number of Instruments 23 Delta Value Lower Bound Gamma Value Upper Bound Theta Delta Lower Bound Vega Delta Upper Bound Rho Rate Gamma Lower Bound Rho Yield Gamma Upper Bound Theta Lower Bound Result 1 Theta Upper Bound Vega Lower Bound Vega Upper Bound Rho Rate Lower Bound Rho Rate Upper Bound Rho Yield Lower Bound Rho Yield Upper Bound

22 Portfolio rebalancing is substantial: 46

23 Maximum Premium Scenario. In the maximum premium scenario, the portfolio components parameters are Instrument Parameters Time Period Price Delta Gamma Theta Vega Rho Rate Rho Yield Roh Low Bond Roh Upper Bound Instrument RKN C C C C C C C C C C C P P P P P P P t 20 P P P t P and a maximum value / maximum theta / minimum vega LRA strategy is Model Parameters a (Value) 1 b (Theta) 1 c (Delta) 0 d (Gamma) 0 e (Vega) -1 LRA Strategy f (Rho Rate) 0 g (Rho Yield) 0 Minimum Maximum Value Number of Instruments 23 Delta Value Lower Bound Gamma Value Upper Bound Theta Delta Lower Bound Vega Delta Upper Bound Rho Rate Gamma Lower Bound Rho Yield Gamma Upper Bound Theta Lower Bound Result Theta Upper Bound Vega Lower Bound Vega Upper Bound Rho Rate Lower Bound Rho Rate Upper Bound Rho Yield Lower Bound Rho Yield Upper Bound

24 Portfolio rebalancing is in this case: Note that quasi-lra buy-and-hold strategies would be one efficient way to control the rebalancing of LRA portfolios over time. We shall now focus our attention on longterm Limited risk arbitrage strategies (that are of a stochastic nature, described by their expected value and their standard deviation). We still use the above simple Black & Scholes approximation of RUKN's value process but now assume American-style call and put options with strike prices ranging from CHF to

25 2. LRA Option Strategies Limited risk arbitrage (LRA) option strategies (see also Part I: Securities Markets, Part II: Securities and Derivatives Markets and Part V: A Guide to Efficient Numerical Implementations) involve shares x(t) of common stock [for example, Swiss Re registered shares S(t) as considered earlier in this paper] as well as corresponding futures contracts and European call and put options [on the stocks themselves or on a stock market index I(t)] and thus generalize the more traditional stock option trading strategies (i.e., covered call strategies, protective put strategies. spreads and combinations). Specifically, in the context of this paper, we assume the canonical Black & Scholes securities market setting risk - averse evolution risk -neutral evolution and consider trading and portfolio management strategies with associated value function position in common stock positions in futures F1 (t),..,fk (t) positions in call options c1 (t),..,cl (t) positions in put options P1 (t),..,pm (t) that are the solutions of the linear program where RA denotes the limited risk arbitrage objectives and AC additional linear constraints. Since the return Rn on the above risk/arbitrage portfolio n = n(t) has the (conditional) variance 49

26 LRA investment management clearly minimizes both instantaneous investment risk³ etc.] future and portfolio risk dynamics consistent with the investor s stated objectives (i.e, the risk tolerances and ). If we now introduce the instantaneous value appreciation rate to a degree that is (lambda) of a contingent claim, then the limited risk arbitrage optimization program RA: maximizes the value appreciation rate of an investor s option portfolio while keeping its derivatives risk exposure within the specified tolerance band. Furthermore, we have which shows that this optimization program at the same time maximizes the (conditionally) expected return of the investor's securities and derivatives portfolio to an extent that is consistent with the stated investment management objectives (RA and AC). Moreover, we can write the moments of the return on the risk/arbitrage portfolio over a given investment period [0, H] in the form ³ In a securities (i.e., stocks and bonds) portfolio context, instantaneous investment risk is usually defined in terms of the variance /standard deviation of return, whereas in a derivatives portfolio context the contingent claim sensitivities (of the first order: delta, etc.) are used. 50

27 and thus limited risk arbitrage investment management is a generalization to the derivatives markets of the myopic portfolio optimization techniques that extend Markowitz portfolio selection in the traditional financial markets. Recall also that in a dynamically complete securities market setting (such as the simple canonical one considered here) contingent claims are redundant and therefore (after appropriate identifications) general limited risk arbitrage investment management only involves solving a linear program in strategy space (see Part I: Securities Markets, Part II: Securities and Derivatives Markets and Part V: A Guide to Efficient Numerical Implementations). In the case of American options the Black & Scholes partial deferential equation can be solved with numerical methods (Brennan and Schwartz [4, 5]). The implicit finite difference method approximates the partial differential operators in this equation by the finite differences that are defined on a two dimensional rectangular grid in time t and state x (see Fig. 1 below) while the corresponding explicit finite difference approximation is A discretization of the above Black & Scholes partial differential equation with the implicit finite difference operators then leads to the (tridiagonal) system of linear equations with (state dependent) coefficients and that can easily be solved backwards in time by using the boundary conditions and early exercise criteria which characterize the given contingent claim v. 51

28 A discretization with the explicit instead of the implicit finite difference operators substantially simplifies these calculations. The corresponding linear equation system is in this case and the (state dependent) coefficients are [where the local consistency conditions and have to be satisfied, see also Part III A Risk/Arbitrage Pricing Theory and Part IV An Impulse Control Approach to Limited Risk Arbitrage]. and Fig 1: Finite Difference Method With the contingent claim sensitivities in an implicit and 52

29 in an explicit finite difference approximation for the market variable x, risk/arbitrage strategies position in common stock positions in futures positions in European call options positions in European put options positions in American call options positions in American put options involving shares of common stock as well as futures contracts and European and American call and put options on the stocks themselves or on a stock market index [where is the associated value function] are the solutions of the state dependent linear programs (variance of return minimization) or 53

30 [expected return maximization, where is the associated option value appreciation rate]. In this way, risk/arbitrage trading and portfolio management systems (see Fig. 3 below) that operate on the basis of the finite difference method support the design of longer-term limited risk arbitrage investment management strategies by determining at any time before or during the relevant investment period the current and all future optimal (state dependent linear optimization) portfolio positions that over the entire investment horizon reduce both the instantaneous investment risk and the future portfolio risk dynamics to values within a specified tolerance band and at the same time achieve a maximum rate of portfolio value appreciation over each single trading period. As noted earlier, the simple canonical (linear optimization in strategy space) setting that we consider here readily extends to any dynamically complete (diffusion type) securities market and any given set of portfolio management objectives of an investor in the form of von Neumann-Morgenstern utility functions. The necessary identifications are (see Part I: Securities Markers and Part II: Securities and Derivatives Markets): Lattice approaches on the other hand work with a discrete representation of the market variable (risk -neutral state evolution) in the form of a binomial lattice (Cox and Ross [6] and Cox, Ross and Rubinstein [7]). 54

31 Fig 2: Lattice Approach The parameters risk -averse risk-neutral P, u state evolution state evolution of such a lattice describing the securities market dynamics in a risk-averse and in a risk-neutral financial economy can be calculated by noting that and with therefore holds. 55

32 The current sensitivities of a contingent claim and their future evolution over the claim s entire lifetime can then be determined together with its current and all future prices by using a dynamic programming procedure that operates on the underlying recombining lattice with root and branching process risk-averse state evolution risk-neutral state evolution Any claim v contingent on the market variable x is uniquely characterized by a function F(j), 0 j m, representing the payments to its holder at maturity (terminal condition), a function X(i,j), 1 i m and 0 j i, representing intertemporal cashflows to which its holder is entitled (payoff function) and boundary conditions L(i,j) vij U(i, j), 0 i m 1 and 0 j i, for its value process. In an arbitrage pricing theory framework the claim s value function consequently satisfies the equation (risk-neutral pricing formula) which provides the basic algorithm for the above mentioned dynamic programming procedure. The claim s sensitivities can now (similar to the explicit finite difference approach) he approximated by where or alternatively by where 56

33 [note that these conditionally expected rates of change of the option value with respect to time t and the market variable x are defined only in the context of a discrete-time lattice approximation of the state dynamics; we have however as Based on this information the current and all future optimal asset positions (that over the entire investment horizon reduce both instantaneous investment risk and future portfolio risk dynamics to values within a given tolerance band and at the same time achieve a maximum rate of portfolio value appreciation over each single trading period) can then be determined by solving (as part of the above mentioned dynamic programming procedure) the state dependent linear programs (variance of return minimization) or (expected return maximization) if the sensitivities of the contingent claims are defined as in an explicit finite difference approximation and or 57

34 in the case where the sensitivity approximations of the contingent claims are defined as conditionally expected rates of change with respect to time and the market variable. Note finally that the futures price of the tradable asset represented by the market variable x satisfies the stochastic differential equation and can therefore be approximated by a binomial lattice with parameters The limited risk arbitrage (LRA) techniques briefly outlined above and developed in detail in the publication series Risk/Arbitrage Strategies.. A New Concept for Asset/Liability Management, Optimal Fund Design and Optimal Portfolio Selection in a Dynamic, Continuous-Time Framework have been implemented in the form of a financial / (re)insurance techniques toolbox (FRT), see Fig. 3 below. The toolbox runs under Windows 3.1, 3.11 and 95 as well as under Windows NT 3.51 and NT

35 Fig.3: Financial / (Re)insurance Techniques Toolbox (FRT) FRT can be used in asset /liability management applications as well as for the rapid development of advanced risk transfer solutions for Fortune 500 companies. An extreme value techniques toolbox (EVT) handels the liability side while on the asset side multivariate stochastic models of the (jump) diffusion type are used for the evolution of the main financial markets variables like interest rates, stocks, stock indices and foreign currencies (for details, see Part V: A Guide to Efficient Numerical Implementations). 3. Mitarbeiter-Option Trading In the final section of our paper we shall now outline how the LRA (lattice) techniques described above can be used to implement a Mitarbeiter-Option trading system along the lines of Bühlmann, Davis and List [3]. We consider an American-style call and put Mitarbeiter-Option schedule with strike prices ranging from CHF to The options are of the forwardstart variety, starting in 3.5 years and maturing in 5 years time. As in the introduction, 59

36 we distinguish between the base value, the minimum premium and the maximum premium scenario (defined as in the European call option case). The LRA strategy considered is of the maximum value / maximum time value maximum theta type with constrained instantaneous investment risk, i.e., and constrained future portfolio risk dynamics, i.e., [where the option sensitivities are defined as conditional (monthly) motes of change of the option value with respect to time t and the market variable x ]. The results model parameters option values and sensitivities positions held investment portfolio characteristics conclude the paper. 60

37 Base Value Scenario. 61

38 62

39 63

40 64

41 LRA Investment Portfolio (Expectations) Time Period Portfolio Value Portfolio Time Value Portfolio Delta Portfolio Gamma Portfolio Theta 0 261' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' '

42 LRA Investment Portfolio (Standard Deviations) Time Period Portfolio Value Portfolio Time Value Portfolio Delta Portfolio Gamma Portfolio Theta ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' Minimum Premium Scenario. 66

43 LRA Investment Portfolio (Expectations) Time Period Portfolio Value Portfolio Time Value Portfolio Delta Portfolio Gamma Portfolio Theta 0 282' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' '

44 LRA Investment Portfolio (Standard Deviations) Time Period Portfolio Value Portfolio Time Value Portfolio Delta Portfolio Gamma Portfolio Theta ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' Maximum Premium Scenario 68

45 LRA Investment Portfolio (Expectations) lime Period Portfolio Value Portfolio Time Value Portfolio Delta Portfolio Gamma Portfolio Theta 0 246' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' ' '

BINOMIAL OPTIONS PRICING MODEL. Mark Ioffe. Abstract

BINOMIAL OPTIONS PRICING MODEL Mark Ioffe Abstract Binomial option pricing model is a widespread numerical method of calculating price of American options. In terms of applied mathematics this is simple

BINOMIAL OPTIONS PRICING MODEL Mark Ioffe Abstract Binomial option pricing model is a widespread numerical method of calculating price of American options. In terms of applied mathematics this is simple

OPTIONS and FUTURES Lecture 2: Binomial Option Pricing and Call Options

OPTIONS and FUTURES Lecture 2: Binomial Option Pricing and Call Options Philip H. Dybvig Washington University in Saint Louis binomial model replicating portfolio single period artificial (risk-neutral)

OPTIONS and FUTURES Lecture 2: Binomial Option Pricing and Call Options Philip H. Dybvig Washington University in Saint Louis binomial model replicating portfolio single period artificial (risk-neutral)

VALUATION IN DERIVATIVES MARKETS

VALUATION IN DERIVATIVES MARKETS September 2005 Rawle Parris ABN AMRO Property Derivatives What is a Derivative? A contract that specifies the rights and obligations between two parties to receive or deliver

VALUATION IN DERIVATIVES MARKETS September 2005 Rawle Parris ABN AMRO Property Derivatives What is a Derivative? A contract that specifies the rights and obligations between two parties to receive or deliver

CS 522 Computational Tools and Methods in Finance Robert Jarrow Lecture 1: Equity Options

CS 5 Computational Tools and Methods in Finance Robert Jarrow Lecture 1: Equity Options 1. Definitions Equity. The common stock of a corporation. Traded on organized exchanges (NYSE, AMEX, NASDAQ). A common

CS 5 Computational Tools and Methods in Finance Robert Jarrow Lecture 1: Equity Options 1. Definitions Equity. The common stock of a corporation. Traded on organized exchanges (NYSE, AMEX, NASDAQ). A common

Week 13 Introduction to the Greeks and Portfolio Management:

Week 13 Introduction to the Greeks and Portfolio Management: Hull, Ch. 17; Poitras, Ch.9: I, IIA, IIB, III. 1 Introduction to the Greeks and Portfolio Management Objective: To explain how derivative portfolios

Week 13 Introduction to the Greeks and Portfolio Management: Hull, Ch. 17; Poitras, Ch.9: I, IIA, IIB, III. 1 Introduction to the Greeks and Portfolio Management Objective: To explain how derivative portfolios

Caput Derivatives: October 30, 2003

Caput Derivatives: October 30, 2003 Exam + Answers Total time: 2 hours and 30 minutes. Note 1: You are allowed to use books, course notes, and a calculator. Question 1. [20 points] Consider an investor

Caput Derivatives: October 30, 2003 Exam + Answers Total time: 2 hours and 30 minutes. Note 1: You are allowed to use books, course notes, and a calculator. Question 1. [20 points] Consider an investor

Hedging Illiquid FX Options: An Empirical Analysis of Alternative Hedging Strategies

Hedging Illiquid FX Options: An Empirical Analysis of Alternative Hedging Strategies Drazen Pesjak Supervised by A.A. Tsvetkov 1, D. Posthuma 2 and S.A. Borovkova 3 MSc. Thesis Finance HONOURS TRACK Quantitative

Hedging Illiquid FX Options: An Empirical Analysis of Alternative Hedging Strategies Drazen Pesjak Supervised by A.A. Tsvetkov 1, D. Posthuma 2 and S.A. Borovkova 3 MSc. Thesis Finance HONOURS TRACK Quantitative

FAIR VALUATION OF THE SURRENDER OPTION EMBEDDED IN A GUARANTEED LIFE INSURANCE PARTICIPATING POLICY. Anna Rita Bacinello

FAIR VALUATION OF THE SURRENDER OPTION EMBEDDED IN A GUARANTEED LIFE INSURANCE PARTICIPATING POLICY Anna Rita Bacinello Dipartimento di Matematica Applicata alle Scienze Economiche, Statistiche ed Attuariali

FAIR VALUATION OF THE SURRENDER OPTION EMBEDDED IN A GUARANTEED LIFE INSURANCE PARTICIPATING POLICY Anna Rita Bacinello Dipartimento di Matematica Applicata alle Scienze Economiche, Statistiche ed Attuariali

Financial Options: Pricing and Hedging

Financial Options: Pricing and Hedging Diagrams Debt Equity Value of Firm s Assets T Value of Firm s Assets T Valuation of distressed debt and equity-linked securities requires an understanding of financial

Financial Options: Pricing and Hedging Diagrams Debt Equity Value of Firm s Assets T Value of Firm s Assets T Valuation of distressed debt and equity-linked securities requires an understanding of financial

On Black-Scholes Equation, Black- Scholes Formula and Binary Option Price

On Black-Scholes Equation, Black- Scholes Formula and Binary Option Price Abstract: Chi Gao 12/15/2013 I. Black-Scholes Equation is derived using two methods: (1) risk-neutral measure; (2) - hedge. II.

On Black-Scholes Equation, Black- Scholes Formula and Binary Option Price Abstract: Chi Gao 12/15/2013 I. Black-Scholes Equation is derived using two methods: (1) risk-neutral measure; (2) - hedge. II.

Option Valuation. Chapter 21

Option Valuation Chapter 21 Intrinsic and Time Value intrinsic value of in-the-money options = the payoff that could be obtained from the immediate exercise of the option for a call option: stock price

Option Valuation Chapter 21 Intrinsic and Time Value intrinsic value of in-the-money options = the payoff that could be obtained from the immediate exercise of the option for a call option: stock price

Black-Scholes-Merton approach merits and shortcomings

Black-Scholes-Merton approach merits and shortcomings Emilia Matei 1005056 EC372 Term Paper. Topic 3 1. Introduction The Black-Scholes and Merton method of modelling derivatives prices was first introduced

Black-Scholes-Merton approach merits and shortcomings Emilia Matei 1005056 EC372 Term Paper. Topic 3 1. Introduction The Black-Scholes and Merton method of modelling derivatives prices was first introduced

Lecture 12: The Black-Scholes Model Steven Skiena. http://www.cs.sunysb.edu/ skiena

Lecture 12: The Black-Scholes Model Steven Skiena Department of Computer Science State University of New York Stony Brook, NY 11794 4400 http://www.cs.sunysb.edu/ skiena The Black-Scholes-Merton Model

Lecture 12: The Black-Scholes Model Steven Skiena Department of Computer Science State University of New York Stony Brook, NY 11794 4400 http://www.cs.sunysb.edu/ skiena The Black-Scholes-Merton Model

Mathematical Finance

Mathematical Finance Option Pricing under the Risk-Neutral Measure Cory Barnes Department of Mathematics University of Washington June 11, 2013 Outline 1 Probability Background 2 Black Scholes for European

Mathematical Finance Option Pricing under the Risk-Neutral Measure Cory Barnes Department of Mathematics University of Washington June 11, 2013 Outline 1 Probability Background 2 Black Scholes for European

Lecture 4: The Black-Scholes model

OPTIONS and FUTURES Lecture 4: The Black-Scholes model Philip H. Dybvig Washington University in Saint Louis Black-Scholes option pricing model Lognormal price process Call price Put price Using Black-Scholes

OPTIONS and FUTURES Lecture 4: The Black-Scholes model Philip H. Dybvig Washington University in Saint Louis Black-Scholes option pricing model Lognormal price process Call price Put price Using Black-Scholes

Does Black-Scholes framework for Option Pricing use Constant Volatilities and Interest Rates? New Solution for a New Problem

Does Black-Scholes framework for Option Pricing use Constant Volatilities and Interest Rates? New Solution for a New Problem Gagan Deep Singh Assistant Vice President Genpact Smart Decision Services Financial

Does Black-Scholes framework for Option Pricing use Constant Volatilities and Interest Rates? New Solution for a New Problem Gagan Deep Singh Assistant Vice President Genpact Smart Decision Services Financial

第 9 讲 : 股 票 期 权 定 价 : B-S 模 型 Valuing Stock Options: The Black-Scholes Model

1 第 9 讲 : 股 票 期 权 定 价 : B-S 模 型 Valuing Stock Options: The Black-Scholes Model Outline 有 关 股 价 的 假 设 The B-S Model 隐 性 波 动 性 Implied Volatility 红 利 与 期 权 定 价 Dividends and Option Pricing 美 式 期 权 定 价 American

1 第 9 讲 : 股 票 期 权 定 价 : B-S 模 型 Valuing Stock Options: The Black-Scholes Model Outline 有 关 股 价 的 假 设 The B-S Model 隐 性 波 动 性 Implied Volatility 红 利 与 期 权 定 价 Dividends and Option Pricing 美 式 期 权 定 价 American

Invesco Great Wall Fund Management Co. Shenzhen: June 14, 2008

: A Stern School of Business New York University Invesco Great Wall Fund Management Co. Shenzhen: June 14, 2008 Outline 1 2 3 4 5 6 se notes review the principles underlying option pricing and some of

: A Stern School of Business New York University Invesco Great Wall Fund Management Co. Shenzhen: June 14, 2008 Outline 1 2 3 4 5 6 se notes review the principles underlying option pricing and some of

Review of Basic Options Concepts and Terminology

Review of Basic Options Concepts and Terminology March 24, 2005 1 Introduction The purchase of an options contract gives the buyer the right to buy call options contract or sell put options contract some

Review of Basic Options Concepts and Terminology March 24, 2005 1 Introduction The purchase of an options contract gives the buyer the right to buy call options contract or sell put options contract some

On Market-Making and Delta-Hedging

On Market-Making and Delta-Hedging 1 Market Makers 2 Market-Making and Bond-Pricing On Market-Making and Delta-Hedging 1 Market Makers 2 Market-Making and Bond-Pricing What to market makers do? Provide

On Market-Making and Delta-Hedging 1 Market Makers 2 Market-Making and Bond-Pricing On Market-Making and Delta-Hedging 1 Market Makers 2 Market-Making and Bond-Pricing What to market makers do? Provide

S 1 S 2. Options and Other Derivatives

Options and Other Derivatives The One-Period Model The previous chapter introduced the following two methods: Replicate the option payoffs with known securities, and calculate the price of the replicating

Options and Other Derivatives The One-Period Model The previous chapter introduced the following two methods: Replicate the option payoffs with known securities, and calculate the price of the replicating

Finance 436 Futures and Options Review Notes for Final Exam. Chapter 9

Finance 436 Futures and Options Review Notes for Final Exam Chapter 9 1. Options: call options vs. put options, American options vs. European options 2. Characteristics: option premium, option type, underlying

Finance 436 Futures and Options Review Notes for Final Exam Chapter 9 1. Options: call options vs. put options, American options vs. European options 2. Characteristics: option premium, option type, underlying

Numerical methods for American options

Lecture 9 Numerical methods for American options Lecture Notes by Andrzej Palczewski Computational Finance p. 1 American options The holder of an American option has the right to exercise it at any moment

Lecture 9 Numerical methods for American options Lecture Notes by Andrzej Palczewski Computational Finance p. 1 American options The holder of an American option has the right to exercise it at any moment

Option pricing. Vinod Kothari

Option pricing Vinod Kothari Notation we use this Chapter will be as follows: S o : Price of the share at time 0 S T : Price of the share at time T T : time to maturity of the option r : risk free rate

Option pricing Vinod Kothari Notation we use this Chapter will be as follows: S o : Price of the share at time 0 S T : Price of the share at time T T : time to maturity of the option r : risk free rate

Jorge Cruz Lopez - Bus 316: Derivative Securities. Week 11. The Black-Scholes Model: Hull, Ch. 13.

Week 11 The Black-Scholes Model: Hull, Ch. 13. 1 The Black-Scholes Model Objective: To show how the Black-Scholes formula is derived and how it can be used to value options. 2 The Black-Scholes Model 1.

Week 11 The Black-Scholes Model: Hull, Ch. 13. 1 The Black-Scholes Model Objective: To show how the Black-Scholes formula is derived and how it can be used to value options. 2 The Black-Scholes Model 1.

Hedging. An Undergraduate Introduction to Financial Mathematics. J. Robert Buchanan. J. Robert Buchanan Hedging

Hedging An Undergraduate Introduction to Financial Mathematics J. Robert Buchanan 2010 Introduction Definition Hedging is the practice of making a portfolio of investments less sensitive to changes in

Hedging An Undergraduate Introduction to Financial Mathematics J. Robert Buchanan 2010 Introduction Definition Hedging is the practice of making a portfolio of investments less sensitive to changes in

Article from: Risk Management. June 2009 Issue 16

Article from: Risk Management June 2009 Issue 16 CHAIRSPERSON S Risk quantification CORNER Structural Credit Risk Modeling: Merton and Beyond By Yu Wang The past two years have seen global financial markets

Article from: Risk Management June 2009 Issue 16 CHAIRSPERSON S Risk quantification CORNER Structural Credit Risk Modeling: Merton and Beyond By Yu Wang The past two years have seen global financial markets

American and European. Put Option

American and European Put Option Analytical Finance I Kinda Sumlaji 1 Table of Contents: 1. Introduction... 3 2. Option Style... 4 3. Put Option 4 3.1 Definition 4 3.2 Payoff at Maturity... 4 3.3 Example

American and European Put Option Analytical Finance I Kinda Sumlaji 1 Table of Contents: 1. Introduction... 3 2. Option Style... 4 3. Put Option 4 3.1 Definition 4 3.2 Payoff at Maturity... 4 3.3 Example

Valuing Stock Options: The Black-Scholes-Merton Model. Chapter 13

Valuing Stock Options: The Black-Scholes-Merton Model Chapter 13 Fundamentals of Futures and Options Markets, 8th Ed, Ch 13, Copyright John C. Hull 2013 1 The Black-Scholes-Merton Random Walk Assumption

Valuing Stock Options: The Black-Scholes-Merton Model Chapter 13 Fundamentals of Futures and Options Markets, 8th Ed, Ch 13, Copyright John C. Hull 2013 1 The Black-Scholes-Merton Random Walk Assumption

Options: Valuation and (No) Arbitrage

Arbitrage") Prof. Alex Shapiro Lecture Notes 15 Options: Valuation and (No) Arbitrage I. Readings and Suggested Practice Problems II. Introduction: Objectives and Notation III. No Arbitrage Pricing Bound IV. The Binomial

Prof. Alex Shapiro Lecture Notes 15 Options: Valuation and (No) Arbitrage I. Readings and Suggested Practice Problems II. Introduction: Objectives and Notation III. No Arbitrage Pricing Bound IV. The Binomial

Martingale Pricing Applied to Options, Forwards and Futures

IEOR E4706: Financial Engineering: Discrete-Time Asset Pricing Fall 2005 c 2005 by Martin Haugh Martingale Pricing Applied to Options, Forwards and Futures We now apply martingale pricing theory to the

IEOR E4706: Financial Engineering: Discrete-Time Asset Pricing Fall 2005 c 2005 by Martin Haugh Martingale Pricing Applied to Options, Forwards and Futures We now apply martingale pricing theory to the

VALUING REAL OPTIONS USING IMPLIED BINOMIAL TREES AND COMMODITY FUTURES OPTIONS

VALUING REAL OPTIONS USING IMPLIED BINOMIAL TREES AND COMMODITY FUTURES OPTIONS TOM ARNOLD TIMOTHY FALCON CRACK* ADAM SCHWARTZ A real option on a commodity is valued using an implied binomial tree (IBT)

VALUING REAL OPTIONS USING IMPLIED BINOMIAL TREES AND COMMODITY FUTURES OPTIONS TOM ARNOLD TIMOTHY FALCON CRACK* ADAM SCHWARTZ A real option on a commodity is valued using an implied binomial tree (IBT)

The Behavior of Bonds and Interest Rates. An Impossible Bond Pricing Model. 780 w Interest Rate Models

780 w Interest Rate Models The Behavior of Bonds and Interest Rates Before discussing how a bond market-maker would delta-hedge, we first need to specify how bonds behave. Suppose we try to model a zero-coupon

780 w Interest Rate Models The Behavior of Bonds and Interest Rates Before discussing how a bond market-maker would delta-hedge, we first need to specify how bonds behave. Suppose we try to model a zero-coupon

Optimal proportional reinsurance and dividend pay-out for insurance companies with switching reserves

Optimal proportional reinsurance and dividend pay-out for insurance companies with switching reserves Abstract: This paper presents a model for an insurance company that controls its risk and dividend

Optimal proportional reinsurance and dividend pay-out for insurance companies with switching reserves Abstract: This paper presents a model for an insurance company that controls its risk and dividend

Tutorial: Structural Models of the Firm

Tutorial: Structural Models of the Firm Peter Ritchken Case Western Reserve University February 16, 2015 Peter Ritchken, Case Western Reserve University Tutorial: Structural Models of the Firm 1/61 Tutorial:

Tutorial: Structural Models of the Firm Peter Ritchken Case Western Reserve University February 16, 2015 Peter Ritchken, Case Western Reserve University Tutorial: Structural Models of the Firm 1/61 Tutorial:

Betting on Volatility: A Delta Hedging Approach. Liang Zhong

Betting on Volatility: A Delta Hedging Approach Liang Zhong Department of Mathematics, KTH, Stockholm, Sweden April, 211 Abstract In the financial market, investors prefer to estimate the stock price

Betting on Volatility: A Delta Hedging Approach Liang Zhong Department of Mathematics, KTH, Stockholm, Sweden April, 211 Abstract In the financial market, investors prefer to estimate the stock price

Master of Mathematical Finance: Course Descriptions

Master of Mathematical Finance: Course Descriptions CS 522 Data Mining Computer Science This course provides continued exploration of data mining algorithms. More sophisticated algorithms such as support

Master of Mathematical Finance: Course Descriptions CS 522 Data Mining Computer Science This course provides continued exploration of data mining algorithms. More sophisticated algorithms such as support

Simplified Option Selection Method

Simplified Option Selection Method Geoffrey VanderPal Webster University Thailand Options traders and investors utilize methods to price and select call and put options. The models and tools range from

Simplified Option Selection Method Geoffrey VanderPal Webster University Thailand Options traders and investors utilize methods to price and select call and put options. The models and tools range from

Consider a European call option maturing at time T

Lecture 10: Multi-period Model Options Black-Scholes-Merton model Prof. Markus K. Brunnermeier 1 Binomial Option Pricing Consider a European call option maturing at time T with ihstrike K: C T =max(s T

Lecture 10: Multi-period Model Options Black-Scholes-Merton model Prof. Markus K. Brunnermeier 1 Binomial Option Pricing Consider a European call option maturing at time T with ihstrike K: C T =max(s T

Valuation of American Options

Valuation of American Options Among the seminal contributions to the mathematics of finance is the paper F. Black and M. Scholes, The pricing of options and corporate liabilities, Journal of Political

Valuation of American Options Among the seminal contributions to the mathematics of finance is the paper F. Black and M. Scholes, The pricing of options and corporate liabilities, Journal of Political

Fundamentals of Futures and Options (a summary)

") Fundamentals of Futures and Options (a summary) Roger G. Clarke, Harindra de Silva, CFA, and Steven Thorley, CFA Published 2013 by the Research Foundation of CFA Institute Summary prepared by Roger G.

Fundamentals of Futures and Options (a summary) Roger G. Clarke, Harindra de Silva, CFA, and Steven Thorley, CFA Published 2013 by the Research Foundation of CFA Institute Summary prepared by Roger G.

Options 1 OPTIONS. Introduction

Options 1 OPTIONS Introduction A derivative is a financial instrument whose value is derived from the value of some underlying asset. A call option gives one the right to buy an asset at the exercise or

Options 1 OPTIONS Introduction A derivative is a financial instrument whose value is derived from the value of some underlying asset. A call option gives one the right to buy an asset at the exercise or

How To Value Options In Black-Scholes Model

Option Pricing Basics Aswath Damodaran Aswath Damodaran 1 What is an option? An option provides the holder with the right to buy or sell a specified quantity of an underlying asset at a fixed price (called

Option Pricing Basics Aswath Damodaran Aswath Damodaran 1 What is an option? An option provides the holder with the right to buy or sell a specified quantity of an underlying asset at a fixed price (called

Monte Carlo Methods and Models in Finance and Insurance

Chapman & Hall/CRC FINANCIAL MATHEMATICS SERIES Monte Carlo Methods and Models in Finance and Insurance Ralf Korn Elke Korn Gerald Kroisandt f r oc) CRC Press \ V^ J Taylor & Francis Croup ^^"^ Boca Raton

Chapman & Hall/CRC FINANCIAL MATHEMATICS SERIES Monte Carlo Methods and Models in Finance and Insurance Ralf Korn Elke Korn Gerald Kroisandt f r oc) CRC Press \ V^ J Taylor & Francis Croup ^^"^ Boca Raton

The Black-Scholes-Merton Approach to Pricing Options

he Black-Scholes-Merton Approach to Pricing Options Paul J Atzberger Comments should be sent to: atzberg@mathucsbedu Introduction In this article we shall discuss the Black-Scholes-Merton approach to determining

he Black-Scholes-Merton Approach to Pricing Options Paul J Atzberger Comments should be sent to: atzberg@mathucsbedu Introduction In this article we shall discuss the Black-Scholes-Merton approach to determining

DETERMINING THE VALUE OF EMPLOYEE STOCK OPTIONS. Report Produced for the Ontario Teachers Pension Plan John Hull and Alan White August 2002

DETERMINING THE VALUE OF EMPLOYEE STOCK OPTIONS 1. Background Report Produced for the Ontario Teachers Pension Plan John Hull and Alan White August 2002 It is now becoming increasingly accepted that companies

DETERMINING THE VALUE OF EMPLOYEE STOCK OPTIONS 1. Background Report Produced for the Ontario Teachers Pension Plan John Hull and Alan White August 2002 It is now becoming increasingly accepted that companies

BINOMIAL OPTION PRICING

Darden Graduate School of Business Administration University of Virginia BINOMIAL OPTION PRICING Binomial option pricing is a simple but powerful technique that can be used to solve many complex option-pricing

Darden Graduate School of Business Administration University of Virginia BINOMIAL OPTION PRICING Binomial option pricing is a simple but powerful technique that can be used to solve many complex option-pricing

How to Value Employee Stock Options

John Hull and Alan White One of the arguments often used against expensing employee stock options is that calculating their fair value at the time they are granted is very difficult. This article presents

John Hull and Alan White One of the arguments often used against expensing employee stock options is that calculating their fair value at the time they are granted is very difficult. This article presents

1 The Black-Scholes model: extensions and hedging

1 The Black-Scholes model: extensions and hedging 1.1 Dividends Since we are now in a continuous time framework the dividend paid out at time t (or t ) is given by dd t = D t D t, where as before D denotes

1 The Black-Scholes model: extensions and hedging 1.1 Dividends Since we are now in a continuous time framework the dividend paid out at time t (or t ) is given by dd t = D t D t, where as before D denotes

Does the Model matter? A Valuation Analysis of Employee Stock Options

1 Does the Model matter? A Valuation Analysis of Employee Stock Options Manuel Ammann Ralf Seiz Working Paper Series in Finance Paper No. 2 www.finance.unisg.ch March 2004 2 DOES THE MODEL MATTER? A VALUATION

1 Does the Model matter? A Valuation Analysis of Employee Stock Options Manuel Ammann Ralf Seiz Working Paper Series in Finance Paper No. 2 www.finance.unisg.ch March 2004 2 DOES THE MODEL MATTER? A VALUATION

Institutional Finance 08: Dynamic Arbitrage to Replicate Non-linear Payoffs. Binomial Option Pricing: Basics (Chapter 10 of McDonald)

") Copyright 2003 Pearson Education, Inc. Slide 08-1 Institutional Finance 08: Dynamic Arbitrage to Replicate Non-linear Payoffs Binomial Option Pricing: Basics (Chapter 10 of McDonald) Originally prepared

Copyright 2003 Pearson Education, Inc. Slide 08-1 Institutional Finance 08: Dynamic Arbitrage to Replicate Non-linear Payoffs Binomial Option Pricing: Basics (Chapter 10 of McDonald) Originally prepared

Valuation, Pricing of Options / Use of MATLAB

CS-5 Computational Tools and Methods in Finance Tom Coleman Valuation, Pricing of Options / Use of MATLAB 1.0 Put-Call Parity (review) Given a European option with no dividends, let t current time T exercise

CS-5 Computational Tools and Methods in Finance Tom Coleman Valuation, Pricing of Options / Use of MATLAB 1.0 Put-Call Parity (review) Given a European option with no dividends, let t current time T exercise

How To Value Options In A Regime Switching Model

NICOLAS P.B. BOLLEN VALUING OPTIONS IN REGIME-SWITCHING MODELS ABSTRACT This paper presents a lattice-based method for valuing both European and American-style options in regime-switching models. In a

NICOLAS P.B. BOLLEN VALUING OPTIONS IN REGIME-SWITCHING MODELS ABSTRACT This paper presents a lattice-based method for valuing both European and American-style options in regime-switching models. In a

6. Foreign Currency Options

6. Foreign Currency Options So far, we have studied contracts whose payoffs are contingent on the spot rate (foreign currency forward and foreign currency futures). he payoffs from these instruments are

6. Foreign Currency Options So far, we have studied contracts whose payoffs are contingent on the spot rate (foreign currency forward and foreign currency futures). he payoffs from these instruments are

Hedging Options In The Incomplete Market With Stochastic Volatility. Rituparna Sen Sunday, Nov 15

Hedging Options In The Incomplete Market With Stochastic Volatility Rituparna Sen Sunday, Nov 15 1. Motivation This is a pure jump model and hence avoids the theoretical drawbacks of continuous path models.

Hedging Options In The Incomplete Market With Stochastic Volatility Rituparna Sen Sunday, Nov 15 1. Motivation This is a pure jump model and hence avoids the theoretical drawbacks of continuous path models.

where N is the standard normal distribution function,

The Black-Scholes-Merton formula (Hull 13.5 13.8) Assume S t is a geometric Brownian motion w/drift. Want market value at t = 0 of call option. European call option with expiration at time T. Payout at

The Black-Scholes-Merton formula (Hull 13.5 13.8) Assume S t is a geometric Brownian motion w/drift. Want market value at t = 0 of call option. European call option with expiration at time T. Payout at

The Binomial Option Pricing Model André Farber

1 Solvay Business School Université Libre de Bruxelles The Binomial Option Pricing Model André Farber January 2002 Consider a non-dividend paying stock whose price is initially S 0. Divide time into small

1 Solvay Business School Université Libre de Bruxelles The Binomial Option Pricing Model André Farber January 2002 Consider a non-dividend paying stock whose price is initially S 0. Divide time into small

Ch 7. Greek Letters and Trading Strategies

Ch 7. Greek Letters and Trading trategies I. Greek Letters II. Numerical Differentiation to Calculate Greek Letters III. Dynamic (Inverted) Delta Hedge IV. elected Trading trategies This chapter introduces

Ch 7. Greek Letters and Trading trategies I. Greek Letters II. Numerical Differentiation to Calculate Greek Letters III. Dynamic (Inverted) Delta Hedge IV. elected Trading trategies This chapter introduces

Stephane Crepey. Financial Modeling. A Backward Stochastic Differential Equations Perspective. 4y Springer

Stephane Crepey Financial Modeling A Backward Stochastic Differential Equations Perspective 4y Springer Part I An Introductory Course in Stochastic Processes 1 Some Classes of Discrete-Time Stochastic

Stephane Crepey Financial Modeling A Backward Stochastic Differential Equations Perspective 4y Springer Part I An Introductory Course in Stochastic Processes 1 Some Classes of Discrete-Time Stochastic

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 Options These notes consider the way put and call options and the underlying can be combined to create hedges, spreads and combinations. We will consider the

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 Options These notes consider the way put and call options and the underlying can be combined to create hedges, spreads and combinations. We will consider the

QUANTIZED INTEREST RATE AT THE MONEY FOR AMERICAN OPTIONS

QUANTIZED INTEREST RATE AT THE MONEY FOR AMERICAN OPTIONS L. M. Dieng ( Department of Physics, CUNY/BCC, New York, New York) Abstract: In this work, we expand the idea of Samuelson[3] and Shepp[,5,6] for

QUANTIZED INTEREST RATE AT THE MONEY FOR AMERICAN OPTIONS L. M. Dieng ( Department of Physics, CUNY/BCC, New York, New York) Abstract: In this work, we expand the idea of Samuelson[3] and Shepp[,5,6] for

OPTIONS CALCULATOR QUICK GUIDE. Reshaping Canada s Equities Trading Landscape

OPTIONS CALCULATOR QUICK GUIDE Reshaping Canada s Equities Trading Landscape OCTOBER 2014 Table of Contents Introduction 3 Valuing options 4 Examples 6 Valuing an American style non-dividend paying stock

OPTIONS CALCULATOR QUICK GUIDE Reshaping Canada s Equities Trading Landscape OCTOBER 2014 Table of Contents Introduction 3 Valuing options 4 Examples 6 Valuing an American style non-dividend paying stock

Pricing Barrier Option Using Finite Difference Method and MonteCarlo Simulation

Pricing Barrier Option Using Finite Difference Method and MonteCarlo Simulation Yoon W. Kwon CIMS 1, Math. Finance Suzanne A. Lewis CIMS, Math. Finance May 9, 000 1 Courant Institue of Mathematical Science,

Pricing Barrier Option Using Finite Difference Method and MonteCarlo Simulation Yoon W. Kwon CIMS 1, Math. Finance Suzanne A. Lewis CIMS, Math. Finance May 9, 000 1 Courant Institue of Mathematical Science,

UCLA Anderson School of Management Daniel Andrei, Derivative Markets 237D, Winter 2014. MFE Midterm. February 2014. Date:

UCLA Anderson School of Management Daniel Andrei, Derivative Markets 237D, Winter 2014 MFE Midterm February 2014 Date: Your Name: Your Equiz.me email address: Your Signature: 1 This exam is open book,

UCLA Anderson School of Management Daniel Andrei, Derivative Markets 237D, Winter 2014 MFE Midterm February 2014 Date: Your Name: Your Equiz.me email address: Your Signature: 1 This exam is open book,

Moreover, under the risk neutral measure, it must be the case that (5) r t = µ t.

r t = µ t.") LECTURE 7: BLACK SCHOLES THEORY 1. Introduction: The Black Scholes Model In 1973 Fisher Black and Myron Scholes ushered in the modern era of derivative securities with a seminal paper 1 on the pricing

LECTURE 7: BLACK SCHOLES THEORY 1. Introduction: The Black Scholes Model In 1973 Fisher Black and Myron Scholes ushered in the modern era of derivative securities with a seminal paper 1 on the pricing

Chapter 11 Options. Main Issues. Introduction to Options. Use of Options. Properties of Option Prices. Valuation Models of Options.

Chapter 11 Options Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. Part C Determination of risk-adjusted discount rate. Part D Introduction to derivatives. Forwards

Chapter 11 Options Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. Part C Determination of risk-adjusted discount rate. Part D Introduction to derivatives. Forwards

CHAPTER 5 OPTION PRICING THEORY AND MODELS

1 CHAPTER 5 OPTION PRICING THEORY AND MODELS In general, the value of any asset is the present value of the expected cash flows on that asset. In this section, we will consider an exception to that rule

1 CHAPTER 5 OPTION PRICING THEORY AND MODELS In general, the value of any asset is the present value of the expected cash flows on that asset. In this section, we will consider an exception to that rule

Black and Scholes - A Review of Option Pricing Model

CAPM Option Pricing Sven Husmann a, Neda Todorova b a Department of Business Administration, European University Viadrina, Große Scharrnstraße 59, D-15230 Frankfurt (Oder, Germany, Email: husmann@europa-uni.de,

CAPM Option Pricing Sven Husmann a, Neda Todorova b a Department of Business Administration, European University Viadrina, Große Scharrnstraße 59, D-15230 Frankfurt (Oder, Germany, Email: husmann@europa-uni.de,

DERIVATIVE SECURITIES Lecture 2: Binomial Option Pricing and Call Options

DERIVATIVE SECURITIES Lecture 2: Binomial Option Pricing and Call Options Philip H. Dybvig Washington University in Saint Louis review of pricing formulas assets versus futures practical issues call options

DERIVATIVE SECURITIES Lecture 2: Binomial Option Pricing and Call Options Philip H. Dybvig Washington University in Saint Louis review of pricing formulas assets versus futures practical issues call options

Black-Scholes Option Pricing Model

Black-Scholes Option Pricing Model Nathan Coelen June 6, 22 1 Introduction Finance is one of the most rapidly changing and fastest growing areas in the corporate business world. Because of this rapid change,

Black-Scholes Option Pricing Model Nathan Coelen June 6, 22 1 Introduction Finance is one of the most rapidly changing and fastest growing areas in the corporate business world. Because of this rapid change,

American Capped Call Options on Dividend-Paying Assets

American Capped Call Options on Dividend-Paying Assets Mark Broadie Columbia University Jerome Detemple McGill University and CIRANO This article addresses the problem of valuing American call options

American Capped Call Options on Dividend-Paying Assets Mark Broadie Columbia University Jerome Detemple McGill University and CIRANO This article addresses the problem of valuing American call options

Black Scholes Merton Approach To Modelling Financial Derivatives Prices Tomas Sinkariovas 0802869. Words: 3441

Black Scholes Merton Approach To Modelling Financial Derivatives Prices Tomas Sinkariovas 0802869 Words: 3441 1 1. Introduction In this paper I present Black, Scholes (1973) and Merton (1973) (BSM) general

Black Scholes Merton Approach To Modelling Financial Derivatives Prices Tomas Sinkariovas 0802869 Words: 3441 1 1. Introduction In this paper I present Black, Scholes (1973) and Merton (1973) (BSM) general

Chapter 21 Valuing Options

Chapter 21 Valuing Options Multiple Choice Questions 1. Relative to the underlying stock, a call option always has: A) A higher beta and a higher standard deviation of return B) A lower beta and a higher

Chapter 21 Valuing Options Multiple Choice Questions 1. Relative to the underlying stock, a call option always has: A) A higher beta and a higher standard deviation of return B) A lower beta and a higher

Options/1. Prof. Ian Giddy

Options/1 New York University Stern School of Business Options Prof. Ian Giddy New York University Options Puts and Calls Put-Call Parity Combinations and Trading Strategies Valuation Hedging Options2

Options/1 New York University Stern School of Business Options Prof. Ian Giddy New York University Options Puts and Calls Put-Call Parity Combinations and Trading Strategies Valuation Hedging Options2

How to use the Options/Warrants Calculator?

How to use the Options/Warrants Calculator? 1. Introduction Options/Warrants Calculator is a tool for users to estimate the theoretical prices of options/warrants in various market conditions by inputting

How to use the Options/Warrants Calculator? 1. Introduction Options/Warrants Calculator is a tool for users to estimate the theoretical prices of options/warrants in various market conditions by inputting

Lectures. Sergei Fedotov. 20912 - Introduction to Financial Mathematics. No tutorials in the first week

Lectures Sergei Fedotov 20912 - Introduction to Financial Mathematics No tutorials in the first week Sergei Fedotov (University of Manchester) 20912 2010 1 / 1 Lecture 1 1 Introduction Elementary economics

Lectures Sergei Fedotov 20912 - Introduction to Financial Mathematics No tutorials in the first week Sergei Fedotov (University of Manchester) 20912 2010 1 / 1 Lecture 1 1 Introduction Elementary economics

Pricing Barrier Options under Local Volatility

Abstract Pricing Barrier Options under Local Volatility Artur Sepp Mail: artursepp@hotmail.com, Web: www.hot.ee/seppar 16 November 2002 We study pricing under the local volatility. Our research is mainly

Abstract Pricing Barrier Options under Local Volatility Artur Sepp Mail: artursepp@hotmail.com, Web: www.hot.ee/seppar 16 November 2002 We study pricing under the local volatility. Our research is mainly

Lecture 11: The Greeks and Risk Management

Lecture 11: The Greeks and Risk Management This lecture studies market risk management from the perspective of an options trader. First, we show how to describe the risk characteristics of derivatives.

Lecture 11: The Greeks and Risk Management This lecture studies market risk management from the perspective of an options trader. First, we show how to describe the risk characteristics of derivatives.

a. What is the portfolio of the stock and the bond that replicates the option?

Practice problems for Lecture 2. Answers. 1. A Simple Option Pricing Problem in One Period Riskless bond (interest rate is 5%): 1 15 Stock: 5 125 5 Derivative security (call option with a strike of 8):?

Practice problems for Lecture 2. Answers. 1. A Simple Option Pricing Problem in One Period Riskless bond (interest rate is 5%): 1 15 Stock: 5 125 5 Derivative security (call option with a strike of 8):?

Option Pricing with S+FinMetrics. PETER FULEKY Department of Economics University of Washington

Option Pricing with S+FinMetrics PETER FULEKY Department of Economics University of Washington August 27, 2007 Contents 1 Introduction 3 1.1 Terminology.............................. 3 1.2 Option Positions...........................

Option Pricing with S+FinMetrics PETER FULEKY Department of Economics University of Washington August 27, 2007 Contents 1 Introduction 3 1.1 Terminology.............................. 3 1.2 Option Positions...........................

Pricing European and American bond option under the Hull White extended Vasicek model

1 Academic Journal of Computational and Applied Mathematics /August 2013/ UISA Pricing European and American bond option under the Hull White extended Vasicek model Eva Maria Rapoo 1, Mukendi Mpanda 2

1 Academic Journal of Computational and Applied Mathematics /August 2013/ UISA Pricing European and American bond option under the Hull White extended Vasicek model Eva Maria Rapoo 1, Mukendi Mpanda 2

Options pricing in discrete systems

UNIVERZA V LJUBLJANI, FAKULTETA ZA MATEMATIKO IN FIZIKO Options pricing in discrete systems Seminar II Mentor: prof. Dr. Mihael Perman Author: Gorazd Gotovac //2008 Abstract This paper is a basic introduction

UNIVERZA V LJUBLJANI, FAKULTETA ZA MATEMATIKO IN FIZIKO Options pricing in discrete systems Seminar II Mentor: prof. Dr. Mihael Perman Author: Gorazd Gotovac //2008 Abstract This paper is a basic introduction

ON DETERMINANTS AND SENSITIVITIES OF OPTION PRICES IN DELAYED BLACK-SCHOLES MODEL

ON DETERMINANTS AND SENSITIVITIES OF OPTION PRICES IN DELAYED BLACK-SCHOLES MODEL A. B. M. Shahadat Hossain, Sharif Mozumder ABSTRACT This paper investigates determinant-wise effect of option prices when

ON DETERMINANTS AND SENSITIVITIES OF OPTION PRICES IN DELAYED BLACK-SCHOLES MODEL A. B. M. Shahadat Hossain, Sharif Mozumder ABSTRACT This paper investigates determinant-wise effect of option prices when

Understanding Options and Their Role in Hedging via the Greeks

Understanding Options and Their Role in Hedging via the Greeks Bradley J. Wogsland Department of Physics and Astronomy, University of Tennessee, Knoxville, TN 37996-1200 Options are priced assuming that

Understanding Options and Their Role in Hedging via the Greeks Bradley J. Wogsland Department of Physics and Astronomy, University of Tennessee, Knoxville, TN 37996-1200 Options are priced assuming that

Introduction to Options. Derivatives

Introduction to Options Econ 422: Investment, Capital & Finance University of Washington Summer 2010 August 18, 2010 Derivatives A derivative is a security whose payoff or value depends on (is derived

Introduction to Options Econ 422: Investment, Capital & Finance University of Washington Summer 2010 August 18, 2010 Derivatives A derivative is a security whose payoff or value depends on (is derived

IAA PAPER VALUATION OF RISK ADJUSTED CASH FLOWS AND THE SETTING OF DISCOUNT RATES THEORY AND PRACTICE

Introduction This document refers to sub-issue 11G of the IASC Insurance Issues paper and proposes a method to value risk-adjusted cash flows (refer to the IAA paper INSURANCE LIABILITIES - VALUATION &

Introduction This document refers to sub-issue 11G of the IASC Insurance Issues paper and proposes a method to value risk-adjusted cash flows (refer to the IAA paper INSURANCE LIABILITIES - VALUATION &

FINANCIAL ECONOMICS OPTION PRICING

OPTION PRICING Options are contingency contracts that specify payoffs if stock prices reach specified levels. A call option is the right to buy a stock at a specified price, X, called the strike price.

OPTION PRICING Options are contingency contracts that specify payoffs if stock prices reach specified levels. A call option is the right to buy a stock at a specified price, X, called the strike price.

American Options. An Undergraduate Introduction to Financial Mathematics. J. Robert Buchanan. J. Robert Buchanan American Options

American Options An Undergraduate Introduction to Financial Mathematics J. Robert Buchanan 2010 Early Exercise Since American style options give the holder the same rights as European style options plus

American Options An Undergraduate Introduction to Financial Mathematics J. Robert Buchanan 2010 Early Exercise Since American style options give the holder the same rights as European style options plus

More on Market-Making and Delta-Hedging

More on Market-Making and Delta-Hedging What do market makers do to delta-hedge? Recall that the delta-hedging strategy consists of selling one option, and buying a certain number shares An example of

More on Market-Making and Delta-Hedging What do market makers do to delta-hedge? Recall that the delta-hedging strategy consists of selling one option, and buying a certain number shares An example of

Ind AS 102 Share-based Payments

Ind AS 102 Share-based Payments Mayur Ankolekar Consulting Actuary Current Issues in Pension Seminar at Mumbai The Institute of Actuaries of India August 21, 2015 Page 1 Session Objectives 1. To appreciate

Ind AS 102 Share-based Payments Mayur Ankolekar Consulting Actuary Current Issues in Pension Seminar at Mumbai The Institute of Actuaries of India August 21, 2015 Page 1 Session Objectives 1. To appreciate

Option pricing in detail

Course #: Title Module 2 Option pricing in detail Topic 1: Influences on option prices - recap... 3 Which stock to buy?... 3 Intrinsic value and time value... 3 Influences on option premiums... 4 Option

Course #: Title Module 2 Option pricing in detail Topic 1: Influences on option prices - recap... 3 Which stock to buy?... 3 Intrinsic value and time value... 3 Influences on option premiums... 4 Option

Session IX: Lecturer: Dr. Jose Olmo. Module: Economics of Financial Markets. MSc. Financial Economics

Session IX: Stock Options: Properties, Mechanics and Valuation Lecturer: Dr. Jose Olmo Module: Economics of Financial Markets MSc. Financial Economics Department of Economics, City University, London Stock

Session IX: Stock Options: Properties, Mechanics and Valuation Lecturer: Dr. Jose Olmo Module: Economics of Financial Markets MSc. Financial Economics Department of Economics, City University, London Stock

Valuation of the Surrender Option Embedded in Equity-Linked Life Insurance. Brennan Schwartz (1976,1979) Brennan Schwartz

Brennan Schwartz") Valuation of the Surrender Option Embedded in Equity-Linked Life Insurance Brennan Schwartz (976,979) Brennan Schwartz 04 2005 6. Introduction Compared to traditional insurance products, one distinguishing

Valuation of the Surrender Option Embedded in Equity-Linked Life Insurance Brennan Schwartz (976,979) Brennan Schwartz 04 2005 6. Introduction Compared to traditional insurance products, one distinguishing

Or part of or all the risk is dynamically hedged trading regularly, with a. frequency that needs to be appropriate for the trade.

Option position (risk) management Correct risk management of option position is the core of the derivatives business industry. Option books bear huge amount of risk with substantial leverage in the position.

Option position (risk) management Correct risk management of option position is the core of the derivatives business industry. Option books bear huge amount of risk with substantial leverage in the position.

GAMMA.0279 THETA 8.9173 VEGA 9.9144 RHO 3.5985

14 Option Sensitivities and Option Hedging Answers to Questions and Problems 1. Consider Call A, with: X $70; r 0.06; T t 90 days; 0.4; and S $60. Compute the price, DELTA, GAMMA, THETA, VEGA, and RHO

14 Option Sensitivities and Option Hedging Answers to Questions and Problems 1. Consider Call A, with: X $70; r 0.06; T t 90 days; 0.4; and S $60. Compute the price, DELTA, GAMMA, THETA, VEGA, and RHO

The Black-Scholes pricing formulas

The Black-Scholes pricing formulas Moty Katzman September 19, 2014 The Black-Scholes differential equation Aim: Find a formula for the price of European options on stock. Lemma 6.1: Assume that a stock

The Black-Scholes pricing formulas Moty Katzman September 19, 2014 The Black-Scholes differential equation Aim: Find a formula for the price of European options on stock. Lemma 6.1: Assume that a stock

Introduction to Binomial Trees