Financial Mathematics for Actuaries. Chapter 2 Annuities

|

|

|

- Cameron Warner

- 10 years ago

- Views:

Transcription

1 Financial Mathematics for Actuaries Chapter 2 Annuities

2 Learning Objectives 1. Annuity-immediate and annuity-due 2. Present and future values of annuities 3. Perpetuities and deferred annuities 4. Other accumulation methods 5. Payment periods and compounding periods 6. Varying annuities 2

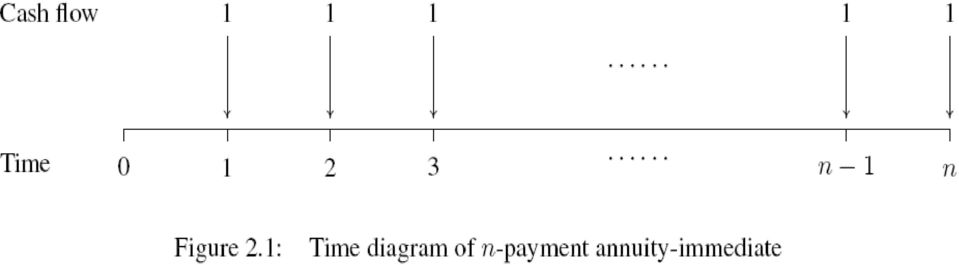

3 2.1 Annuity-Immediate Consider an annuity with payments of 1 unit each, made at the end of every year for n years. This kind of annuity is called an annuity-immediate (also called an ordinary annuity or an annuity in arrears). The present value of an annuity is the sum of the present values of each payment. Example 2.1: Calculate the present value of an annuity-immediate of amount $100 paid annually for 5 years at the rate of interest of 9%. Solution: Table 2.1 summarizes the present values of the payments as well as their total. 3

4 Table 2.1: Present value of annuity Year Payment ($) Present value ($) (1.09) 1 = (1.09) 2 = (1.09) 3 = (1.09) 4 = (1.09) 5 =64.99 Total Weareinterestedinthevalueoftheannuityattime0,calledthe present value, and the accumulated value of the annuity at time n, called the future value. 4

5 Suppose the rate of interest per period is i, and we assume the compound-interest method applies. Let a n ei denote the present value of the annuity, which is sometimes denoted as a n e when the rate of interest is understood. As the present value of the jth payment is v j,wherev =1/(1 + i) is the discount factor, the present value of the annuity is (see Appendix A.5 for the sum of a geometric progression) a n e = v + v 2 + v v n 1 v n = v 1 v = 1 vn i 1 (1 + i) n =. (2.1) i 5

is the discount factor, the present value of the annuity")

6

7 The accumulated value of the annuity at time n is denoted by s n ei or s n e. This is the future value of a n e at time n. Thus,wehave s n e = a n e (1 + i) n = (1 + i)n 1. (2.2) i If the annuity is of level payments of P, the present and future values of the annuity are Pa n e and Ps n e, respectively. Example 2.2: Calculate the present value of an annuity-immediate of amount $100 paid annually for 5 years at the rate of interest of 9% using formula (2.1). Also calculate its future value at time 5. 6

8 Solution: From (2.1), the present value of the annuity is " 1 (1.09) a 5 e = # =$388.97, which agrees with the solution of Example 2.1. The future value of the annuity is (1.09) 5 (100 a 5 e)=(1.09) = $ Alternatively, the future value can be calculated as 100 s 5 e =100 " (1.09) # =$ Example 2.3: Calculate the present value of an annuity-immediate of amount $100 payable quarterly for 10 years at the annual rate of interest 7

9 of 8% convertible quarterly. Also calculate its future value at the end of 10 years. Solution: Note that the rate of interest per payment period (quarter) is (8/4)% = 2%, andthereare4 10 = 40 payments. Thus, from (2.1) thepresentvalueoftheannuity-immediateis " 1 (1.02) a 40 e0.02 = # =$2,735.55, and the future value of the annuity-immediate is (1.02) 40 =$6, A common problem in financial management is to determine the installments required to pay back a loan. We may use (2.1) to calculate the amount of level installments required. 8

40 =$6,040.20.")

10 Example 2.4: A man borrows a loan of $20,000 to purchase a car at annual rate of interest of 6%. He will pay back the loan through monthly installments over 5 years, with the first installment to be made one month after the release of the loan. What is the monthly installment he needs to pay? Solution: The rate of interest per payment period is (6/12)% = 0.5%. Let P be the monthly installment. As there are 5 12 = 60 payments, from (2.1) we have 20,000 = Pa 60 e0.005 " 1 (1.005) 60 = P = P , # 9

% = 0.5%. Let P be the monthly installment.")

11 so that P = 20, =$ The example below illustrates the calculation of the required installment for a targeted future value. Example 2.5: A man wants to save $100,000 to pay for his son s education in 10 years time. An education fund requires the investors to deposit equal installments annually at the end of each year. If interest of 7.5% is paid, how much does the man need to save each year in order to meet his target? Solution: We first calculate s 10 e, which is equal to (1.075) =

12 Then the required amount of installment is P = 100,000 s 10 e = 100, =$7,

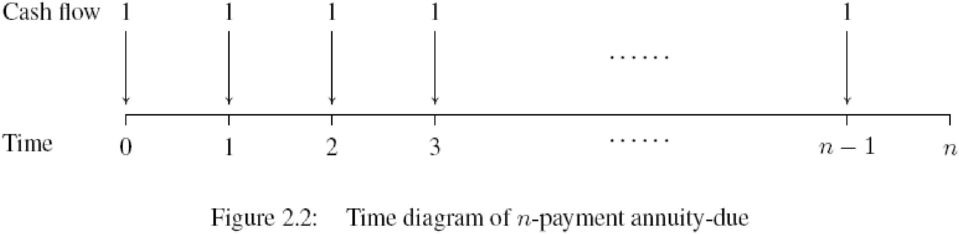

13 2.2 Annuity-Due An annuity-due is an annuity for which the payments are made at the beginning of the payment periods The first payment is made at time 0, and the last payment is made at time n 1. We denote the present value of the annuity-due at time 0 by ä n ei (or ä n e), and the future value of the annuity at time n by s n ei (or s ne). The formula for ä n e can be derived as follows ä n e = 1+v + + v n 1 = 1 vn 1 v = 1 vn d 12. (2.3)

.")

14

15 Also, we have s n e = ä n e (1 + i) n = (1 + i)n 1. (2.4) d As each payment in an annuity-due is paid one period ahead of the corresponding payment of an annuity-immediate, the present value of each payment in an annuity-due is (1+i) times of the present value of the corresponding payment in an annuity-immediate. Hence, ä n e =(1+i) a n e (2.5) and, similarly, s n e =(1+i) s n e. (2.6) 13

a n e (2.")

16 As an annuity-due of n payments consists of a payment at time 0 and an annuity-immediate of n 1 payments, the first payment of whichistobemadeattime1,wehave ä n e =1+a n 1 e. (2.7) Similarly, if we consider an annuity-immediate with n +1 payments at time 1, 2,, n +1as an annuity-due of n payments starting at time 1 plus a final payment at time n +1, we can conclude s n+1 e = s n e +1. (2.8) Example 2.6: A company wants to provide a retirement plan for an employee who is aged 55 now. The plan will provide her with an annuityimmediate of $7,000 every year for 15 years upon her retirement at the 14

Example 2.")

17 age of 65. The company is funding this plan with an annuity-due of 10 years.iftherateofinterestis5%,whatistheamountofinstallmentthe company should pay? Solution: We first calculate the present value of the retirement annuity. This is equal to " # 1 (1.05) 15 7,000 a 15 e = 7,000 =$72, This amount should be equal to the future value of the company s installments P,whichisP s 10 e.nowfrom(2.4),wehave s 10 e = (1.05)10 1 = , 1 (1.05) 1 so that P = 72, =$5,

15 7,000 a 15 e = 7,000 =$72,657.61. 0.")

18 2.3 Perpetuity, Deferred Annuity and Annuity Values at Other Times A perpetuity is an annuity with no termination date, i.e., n. An example that resembles a perpetuity is the dividends of a preferred stock. To calculate the present value of a perpetuity, we note that, as v<1, v n 0 as n. Thus, from (2.1), we have a e = 1 i. (2.9) For the case when the first payment is made immediately, we have, from (2.3), ä e = 1 d. (2.10) 16

, we have a e = 1 i. (2.9) For the case when the first payment is made immediately, we have, from (2.")

19 A deferred annuity is one for which the first payment starts some time in the future. Consider an annuity with n unit payments for which the first payment is due at time m +1. This can be regarded as an n-period annuity-immediate to start at time m,anditspresentvalueisdenotedby m a n ei (or m a n e for short). Thus, we have m a n e = v m a n e 1 v = v m n i = vm v m+n i = (1 vm+n ) (1 v m ) i 17

.")

20 = a m+n e a m e. (2.11) To understand the above equation, see Figure 2.3. From (2.11), we have a m+n e = a m e + v m a n e = a n e + v n a m e. (2.12) Multiplying the above equations throughout by 1+i, we have ä m+n e = ä m e + v m ä n e = ä n e + v n ä m e. (2.13) We also denote v m ä n e as m ä n e,whichisthepresentvalueofanpayment annuity of unit amounts due at time m, m+1,,m+n 1. 18

21

22 If we multiply the equations in (2.12) throughout by (1 + i) m+n,we obtain s m+n e = (1+i) n s m e + s n e = (1+i) m s n e + s m e. (2.14) See Figure 2.4 for illustration. It is also straightforward to see that s m+n e = (1+i) n s m e + s n e = (1+i) m s n e + s m e. (2.15) We now return to (2.2) and write it as s m+n e =(1+i) m+n a m+n e, 19

23

24 so that v m s m+n e =(1+i) n a m+n e, (2.16) for arbitrary positive integers m and n. How do you interpret this equation? 20

25

26 2.4 Annuities Under Other Accumulation Methods We have so far discussed the calculations of the present and future values of annuities assuming compound interest. We now extend our discussion to other interest-accumulation methods. We consider a general accumulation function a( ) and assume that the function applies to any cash-flow transactions in the future. As stated in Section 1.7, any payment at time t>0 starts to accumulate interest according to a( ) as a payment made at time 0. Given the accumulation function a( ), the present value of a unit payment due at time t is 1/a(t), so that the present value of a n- 21

27 period annuity-immediate of unit payments is a n e = nx t=1 1 a(t). (2.17) The future value at time n of a unit payment at time t < n is a(n t), so that the future value of a n-period annuity-immediate of unit payments is s n e = nx t=1 a(n t). (2.18) If (1.35) is satisfied so that a(n t) =a(n)/a(t) for n>t>0, then s n e = nx t=1 a(n) a(t) = a(n) n X t=1 1 a(t) = a(n) a ne. (2.19) This result is satisfied for the compound-interest method, but not the simple-interest method or other accumulation schemes for which equation (1.35) does not hold. 22

28 Example 2.7: Suppose δ(t) =0.02t for 0 t 5, find a 5 e and s 5 e. Solution: We first calculate a(t), which, from (1.26), is µz t a(t) = exp 0.02s ds 0 = exp(0.01t 2 ). Hence, from (2.17), a 5 e = 1 e e e e + 1 =4.4957, 0.16 e0.25 and, from (2.18), s 5 e =1+e e e e 0.16 = Note that a(5) = e 0.25 =1.2840, sothat a(5) a 5 e = = = s 5 e. 23

29 2 Note that in the above example, a(n t) =exp[0.01(n t) 2 ] and a(n) a(t) =exp[0.01(n2 t 2 )], so that a(n t) 6= a(n)/a(t) and (2.19) does not hold. Example 2.8: Calculate a 3 e and s 3 e if the nominal rate of interest is 5% per annum, assuming (a) compound interest, and (b) simple interest. Solution: (a) Assuming compound interest, we have a 3 e = 1 (1.05) =2.723, and s 3 e =(1.05) =

30 (b) For simple interest, the present value is a 3 e = 3X t=1 1 a(t) = 3X t=1 1 1+rt = =2.731, andthefuturevalueattime3is s 3 e = 3X t=1 a(3 t) = 3X t=1 (1 + r(3 t)) = = At the same nominal rate of interest, the compound-interest method generates higher interest than the simple-interest method. Therefore, the future value under the compound-interest method is higher, while its present value is lower. Also, note that for the simple-interest method, a(3) a 3 e = = 3.141, which is different from s 3 e =

31 2.5 Payment Periods, Compounding Periods and Continuous Annuities We now consider the case where the payment period differs from the interest-conversion period. Example 2.9: Find the present value of an annuity-due of $200 per quarter for 2 years, if interest is compounded monthly at the nominal rate of 8%. Solution: Thisisthesituationwherethepaymentsaremadeless frequently than interest is converted. We first calculate the effective rate of interest per quarter, which is =2.01%. 26

32 As there are n =8payments, the required present value is " # 1 (1.0201) ä 8 e =200 =$1, (1.0201) 1 2 Example 2.10: Find the present value of an annuity-immediate of $100 per quarter for 4 years, if interest is compounded semiannually at the nominal rate of 6%. Solution: This is the situation where payments are made more frequently than interest is converted. We first calculate the effective rate of interest per quarter, which is =1.49%. 27

33 Thus, the required present value is " 1 (1.0149) a 16 e = # =$1, It is possible to derive algebraic formulas to compute the present and future values of annuities for which the period of installment is different from the period of compounding. We first consider the case where payments are made less frequently than interest conversion, which occurs at time 1, 2,,etc. Let i denote the effective rate of interest per interest-conversion period. Suppose a m-payment annuity-immediate consists of unit payments at time k, 2k,, mk. We denote n = mk, whichisthe number of interest-conversion periods for the annuity. 28

34 Figure 2.6 illustrates the cash flows for the case of k =2. Thepresentvalueoftheaboveannuity-immediateis(weletw = v k ) v k + v 2k + + v mk = w + w w m 1 w m = w 1 w 1 v = v k n 1 v k 1 v n = (1 + i) k 1 and the future value of the annuity is = a ne, (2.20) s k e (1 + i) n a ne s k e = s ne. (2.21) s k e 29

35

36 We now consider the case where the payments are made more frequently than interest conversion. Let there be mn payments for an annuity-immediate occurring at time 1/m, 2/m,, 1, 1+1/m,, 2,, n, andleti be the effective rate of interest per interest-conversion period. Thus, there are mn payments over n interest-conversion periods. Suppose each payment is of the amount 1/m, so that there is a nominal amount of unit payment in each interest-conversion period. Figure 2.7 illustrates the cash flows for the case of m =4. We denote the present value of this annuity at time 0 by a (m) nei,which can be computed as follows (we let w = v 1 m ) a (m) nei = 1 m ³ v 1 m + v 2 m + + v + v 1+ 1 m + + v n 30

37

38 = 1 m (w + w2 + + w mn ) w 1 wmn where = 1 m = 1 m = 1 m " " 1 w v 1 1 v n m 1 v 1 m 1 v n (1 + i) 1 m 1 # # = 1 vn r (m), (2.22) r (m) = m h (1 + i) 1 m 1 i (2.23) is the equivalent nominal rate of interest compounded m times per interest-conversion period (see (1.19)). 31

39 The future value of the annuity-immediate is s (m) nei = (1+i) n a (m) nei = (1 + i)n 1 = r (m) i r (m) s ne. (2.24) The above equation parallels (2.22), which can also be written as a (m) nei = i r (m) a ne. If the mn-payment annuity is due at time 0, 1/m, 2/m,,n 1/m, we denote its present value at time 0 by ä (m) ne,whichisgivenby ä (m) ne =(1+i) 1 m a (m) ne 32 =(1+i) 1 m 1 v n r (m). (2.25)

40 Thus, from (1.22) we conclude ä (m) ne = 1 vn d (m) = d d (m) äne. (2.26) The future value of this annuity at time n is s (m) ne =(1+i) n ä (m) ne = d d (m) s ne. (2.27) For deferred annuities, the following results apply and q a (m) ne q ä (m) ne = v q a (m) ne, (2.28) = v q ä (m) ne. (2.29) Example 2.11: Solve the problem in Example 2.9 using (2.20). 33

41 Solution: We first note that i = 0.08/12 = Nowk = 3and n =24so that from (2.20), the present value of the annuity-immediate is 200 a 24e s 3 e " 1 (1.0067) 24 = 200 (1.0067) 3 1 = $1, # Finally, the present value of the annuity-due is (1.0067) 3 1, =$1, Example 2.12: (2.23). Solve the problem in Example 2.10 using (2.22) and 2 Solution: Note that m =2and n =8. With i =0.03, wehave,from 34

42 (2.23) r (2) =2 [ ] = Therefore, from (2.22), we have a (2) = 1 (1.03) 8 = e As the total payment in each interest-conversion period is $200, the required present value is = $1, Now we consider (2.22) again. Suppose the annuities are paid continuously attherateof1unitperinterest-conversionperiodover n periods. Thus, m and we denote the present value of this continuous annuity by ā n e. 35 2

43 As lim m r (m) = δ, wehave,from(2.22), ā n e = 1 vn δ = 1 vn ln(1 + i) = i δ a ne. (2.30) Thepresentvalue ofan-period continuous annuity of unit payment perperiodwithadeferredperiodofq is given by q ā n e = v q ā n e =ā q+n e ā q e. (2.31) To compute the future value of a continuous annuity of unit payment per period over n periods, we use the following formula s n e =(1+i) n ā n e = (1 + i)n 1 ln(1 + i) = i δ s ne. (2.32) Wenowgeneralizetheaboveresultstothecaseofageneralaccumulation function a( ). The present value of a continuous annuity 36

44 of unit payment per period over n periods is ā n e = Z n 0 v(t) dt = Z n 0 exp µ Z t δ(s) ds dt. (2.33) 0 To compute the future value of the annuity at time n, weassume that, as in Section 1.7, a unit payment at time t accumulates to a(n t) at time n, forn>t 0. Thus, the future value of the annuity at time n is s n e = Z n 0 a(n t) dt = Z n 0 exp µz n t 0 δ(s) ds dt. (2.34) 37

45 2.6 Varying Annuities We consider annuities the payments of which vary according to an arithmetic progression. Thus, we consider an annuity-immediate and assume the initial payment is P, with subsequent payments P + D, P +2D,,etc.,so that the jth payment is P +(j 1)D. We allow D to be negative so that the annuity can be either stepping up or stepping down. However, for a n-payment annuity, P +(n 1)D must be positive so that negative cash flow is ruled out. We can see that the annuity can be regarded as the sum of the following annuities: (a) a n-period annuity-immediate with constant 38

46 amount P,and(b)n 1 deferred annuities, where the jth deferred annuity is a (n j)-period annuity-immediate with level amount D tostartattimej, forj =1,,n 1. Thus, the present value of the varying annuity is Pa n e + D n 1 X j=1 v j a n j e = Pa n e + D = Pa n e + D = Pa n e + D n 1 X j=1 v j (1 vn j ) i ³ Pn 1 j=1 v j ³ Pnj=1 v j " an e nv n = Pa n e + D i i (n 1)v n i nv n #. (2.35) 39

47

48 For a n-period increasing annuity with P = D =1,wedenoteits present and future values by (Ia) n e and (Is) n e, respectively. It can be shown that and (Ia) n e = äne nv n (Is) n e = s n+1e (n +1) i i (2.36) = s ne n. (2.37) i For an increasing n-payment annuity-due with payments of 1, 2,,n at time 0, 1,,n 1, the present value of the annuity is (Iä) n e =(1+i)(Ia) n e. (2.38) This is the sum of a n-period level annuity-due of unit payments and a (n 1)-payment increasing annuity-immediate with starting and incremental payments of 1. 40

49 Thus, we have (Iä) n e =ä n e +(Ia) n 1 e. (2.39) For the case of a n-period decreasing annuity with P = n and D = 1, we denote its present and future values by (Da) n e and (Ds) n e, respectively. Figure 2.9 presents the time diagram of this annuity. It can be shown that (Da) n e = n a ne i (2.40) and (Ds) n e = n(1 + i)n s n e i. (2.41) 41

50

51 We consider two types of increasing continuous annuities. First, we consider the case of a continuous n-period annuity with level payment (i.e., at a constant rate) of τ units from time τ 1 through time τ. We denote the present value of this annuity by (Iā) n e,whichisgiven by (Iā) n e = nx τ=1 τ Z τ τ 1 v s ds = nx τ=1 τ Z τ τ 1 e δs ds. (2.42) The above equation can be simplified to (Iā) n e = äne nv n. (2.43) δ Second, we may consider a continuous n-period annuity for which thepaymentintheintervalt to t + t is t t, i.e., the instantaneous rateofpaymentattimet is t. 42

52 We denote the present value of this annuity by (Īā) ne, whichisgiven by Z n Z n (Īā) ne = tv t dt = te δt dt = āne nv n. (2.44) 0 0 δ We now consider an annuity-immediate with payments following a geometric progression. Let the first payment be 1, with subsequent payments being 1+k times the previous one. Thus, the present value of an annuity with n payments is (for k 6= i) v + v 2 (1 + k)+ + v n (1 + k) n 1 = v = v n 1 X t=0 n 1 X t=0 [v(1 + k)] t " # t 1+k 1+i 43

53 = v = 1 Ã! n 1+k 1+i 1 1+k 1+i Ã! n 1+k 1 1+i i k. (2.45) Example 2.13: An annuity-immediate consists of a first payment of $100, with subsequent payments increased by 10% over the previous one until the 10th payment, after which subsequent payments decreases by 5% over the previous one. If the effective rate of interest is 10% per payment period, what is the present value of this annuity with 20 payments? Solution: Thepresentvalueofthefirst10paymentsis(usethesecond 44

54 line of (2.45)) (1.1) 1 = $ For the next 10 payments, k = 0.05 and their present value at time 10 is µ (1.10) 9 (0.95) 1.1 =1, Hence, the present value of the 20 payments is ,148.64(1.10) 10 =$1, Example 2.14: An investor wishes to accumulate $1,000 at the end of year 5. He makes level deposits at the beginning of each year for 5 years. The deposits earn a 6% annual effective rate of interest, which is credited 45

55 at the end of each year. The interests on the deposits earn 5% effective interest rate annually. How much does he have to deposit each year? Solution: Let the level annual deposit be A. The interest received at the end of year 1 is 0.06A, which increases by 0.06A annually to A at the end of year 5. Thus, the interest is a 5-payment increasing annuity with P = D =0.06A, earning annual interest of 5%. Hence, we have the equation 1,000 = 5A +0.06A(Is) 5 e0.05. From (2.37) we obtain (Is) 5 e0.05 = , sothat A = 1, =$

56 2.7 Term of Annuity We now consider the case where the annuity period may not be an integer. We consider a n+k e,wheren is an integer and 0 <k<1. We note that a n+k e = 1 vn+k i = (1 vn )+ ³ v n v n+k " i (1 + i) = a n e + v n+k k 1 i = a n e + v n+k s k e. (2.46) Thus, a n+k e is the sum of the present value of a n-period annuityimmediate with unit amount and the present value of an amount s k e 47 #

57 paid at time n + k. Example 2.15: A principal of $5,000 generates income of $500 at the end of every year at an effective rate of interest of 4.5% for as long as possible. Calculate the term of the annuity and discuss the possibilities of settling the last payment. Solution: The equation of value 500 a n e0.045 = 5,000 implies a n e0.045 =10. As a 13e0.045 =9.68 and a 14e0.045 =10.22, the principal can generate 13 regular payments. The investment may be paid off with an additional amount A at the end of year 13, in which case 500 s 13 e A = 5,000 (1.045)13, 48

58 which implies A = $281.02, so that the last payment is $ Alternatively, the last payment B may be made at the end of year 14, which is B = = $ If we adopt the approach in (2.46), we solve k from the equation which implies from which we obtain k = 1 (1.045) (13+k) =10, (1.045) 13+k = , µ 1 ln 0.55 ln(1.045) 13 =

59 Hence, the last payment C to be paid at time years is C =500 " (1.045) # =$ Note that A<C<B, which is as expected, as this follows the order of the occurrence of the payments. In principle, all three approaches are justified. 2 Generally, the effective rate of interest cannot be solved analytically from the equation of value. Numerical methods must be used for this purpose. Example 2.16: A principal of $5,000 generates income of $500 at the end of every year for 15 years. What is the effective rate of interest? 50

60 Solution: so that The equation of value is a 15 ei = 5, =10, 1 (1 + i) 15 a 15 ei = =10. i A simple grid search provides the following results i a 15 ei A finer search provides the answer 5.556%. 2 The Excel Solver may be used to calculate the effectiverateofinterest in Example

61 The computation is illustrated in Exhibit 2.1. We enter a guessed value of 0.05 in Cell A1 in the Excel worksheet. The following expression is then entered in Cell A2: (1 (1 + A1)ˆ( 15))/A1, which computes a 15 ei with i equal to the value at A1. We can also use the Excel function RATE to calculate the rate of interest that equates the present value of an annuity-immediate to a given value. Specifically, consider the equations a n ei A =0 and ä nei A =0. Given n and A, wewishtosolvefori, whichistherateofinterest per payment period of the annuity-immediate or annuity-due. The use of the Excel function RATE to compute i is described as follows: 52

62 Exhibit 2.1: Use of Excel Solver for Example 2.16

63 Excel function: RATE(np,1,pv,type,guess) np = n, pv = A, type = 0 (or omitted) for annuity-immediate, 1 for annuity-due guess = starting value, set to 0.1 if omitted Output = i, rate of interest per payment period of the annuity To use RATE tosolveforexample2.16wekeyinthefollowing: =RATE(15,1,-10). 53

Financial Mathematics for Actuaries. Chapter 1 Interest Accumulation and Time Value of Money

Financial Mathematics for Actuaries Chapter 1 Interest Accumulation and Time Value of Money 1 Learning Objectives 1. Basic principles in calculation of interest accumulation 2. Simple and compound interest

Financial Mathematics for Actuaries Chapter 1 Interest Accumulation and Time Value of Money 1 Learning Objectives 1. Basic principles in calculation of interest accumulation 2. Simple and compound interest

Chapter 04 - More General Annuities

Chapter 04 - More General Annuities 4-1 Section 4.3 - Annuities Payable Less Frequently Than Interest Conversion Payment 0 1 0 1.. k.. 2k... n Time k = interest conversion periods before each payment n

Chapter 04 - More General Annuities 4-1 Section 4.3 - Annuities Payable Less Frequently Than Interest Conversion Payment 0 1 0 1.. k.. 2k... n Time k = interest conversion periods before each payment n

Nominal rates of interest and discount

1 Nominal rates of interest and discount i (m) : The nominal rate of interest payable m times per period, where m is a positive integer > 1. By a nominal rate of interest i (m), we mean a rate payable

1 Nominal rates of interest and discount i (m) : The nominal rate of interest payable m times per period, where m is a positive integer > 1. By a nominal rate of interest i (m), we mean a rate payable

2. Annuities. 1. Basic Annuities 1.1 Introduction. Annuity: A series of payments made at equal intervals of time.

2. Annuities 1. Basic Annuities 1.1 Introduction Annuity: A series of payments made at equal intervals of time. Examples: House rents, mortgage payments, installment payments on automobiles, and interest

2. Annuities 1. Basic Annuities 1.1 Introduction Annuity: A series of payments made at equal intervals of time. Examples: House rents, mortgage payments, installment payments on automobiles, and interest

MATHEMATICS OF FINANCE AND INVESTMENT

MATHEMATICS OF FINANCE AND INVESTMENT G. I. FALIN Department of Probability Theory Faculty of Mechanics & Mathematics Moscow State Lomonosov University Moscow 119992 [email protected] 2 G.I.Falin. Mathematics

MATHEMATICS OF FINANCE AND INVESTMENT G. I. FALIN Department of Probability Theory Faculty of Mechanics & Mathematics Moscow State Lomonosov University Moscow 119992 [email protected] 2 G.I.Falin. Mathematics

Annuity is defined as a sequence of n periodical payments, where n can be either finite or infinite.

1 Annuity Annuity is defined as a sequence of n periodical payments, where n can be either finite or infinite. In order to evaluate an annuity or compare annuities, we need to calculate their present value

1 Annuity Annuity is defined as a sequence of n periodical payments, where n can be either finite or infinite. In order to evaluate an annuity or compare annuities, we need to calculate their present value

Financial Mathematics for Actuaries. Chapter 5 LoansandCostsofBorrowing

Financial Mathematics for Actuaries Chapter 5 LoansandCostsofBorrowing 1 Learning Objectives 1. Loan balance: prospective method and retrospective method 2. Amortization schedule 3. Sinking fund 4. Varying

Financial Mathematics for Actuaries Chapter 5 LoansandCostsofBorrowing 1 Learning Objectives 1. Loan balance: prospective method and retrospective method 2. Amortization schedule 3. Sinking fund 4. Varying

Lecture Notes on Actuarial Mathematics

Lecture Notes on Actuarial Mathematics Jerry Alan Veeh May 1, 2006 Copyright 2006 Jerry Alan Veeh. All rights reserved. 0. Introduction The objective of these notes is to present the basic aspects of the

Lecture Notes on Actuarial Mathematics Jerry Alan Veeh May 1, 2006 Copyright 2006 Jerry Alan Veeh. All rights reserved. 0. Introduction The objective of these notes is to present the basic aspects of the

n(n + 1) 2 1 + 2 + + n = 1 r (iii) infinite geometric series: if r < 1 then 1 + 2r + 3r 2 1 e x = 1 + x + x2 3! + for x < 1 ln(1 + x) = x x2 2 + x3 3

2 1 + 2 + + n = 1 r (iii) infinite geometric series: if r < 1 then 1 + 2r + 3r 2 1 e x = 1 + x + x2 3! + for x < 1 ln(1 + x) = x x2 2 + x3 3") ACTS 4308 FORMULA SUMMARY Section 1: Calculus review and effective rates of interest and discount 1 Some useful finite and infinite series: (i) sum of the first n positive integers: (ii) finite geometric

ACTS 4308 FORMULA SUMMARY Section 1: Calculus review and effective rates of interest and discount 1 Some useful finite and infinite series: (i) sum of the first n positive integers: (ii) finite geometric

Level Annuities with Payments More Frequent than Each Interest Period

Level Annuities with Payments More Frequent than Each Interest Period 1 Examples 2 Annuity-immediate 3 Annuity-due Level Annuities with Payments More Frequent than Each Interest Period 1 Examples 2 Annuity-immediate

Level Annuities with Payments More Frequent than Each Interest Period 1 Examples 2 Annuity-immediate 3 Annuity-due Level Annuities with Payments More Frequent than Each Interest Period 1 Examples 2 Annuity-immediate

Lecture Notes on the Mathematics of Finance

Lecture Notes on the Mathematics of Finance Jerry Alan Veeh February 20, 2006 Copyright 2006 Jerry Alan Veeh. All rights reserved. 0. Introduction The objective of these notes is to present the basic aspects

Lecture Notes on the Mathematics of Finance Jerry Alan Veeh February 20, 2006 Copyright 2006 Jerry Alan Veeh. All rights reserved. 0. Introduction The objective of these notes is to present the basic aspects

Chapter 03 - Basic Annuities

3-1 Chapter 03 - Basic Annuities Section 7.0 - Sum of a Geometric Sequence The form for the sum of a geometric sequence is: Sum(n) a + ar + ar 2 + ar 3 + + ar n 1 Here a = (the first term) n = (the number

3-1 Chapter 03 - Basic Annuities Section 7.0 - Sum of a Geometric Sequence The form for the sum of a geometric sequence is: Sum(n) a + ar + ar 2 + ar 3 + + ar n 1 Here a = (the first term) n = (the number

More on annuities with payments in arithmetic progression and yield rates for annuities

More on annuities with payments in arithmetic progression and yield rates for annuities 1 Annuities-due with payments in arithmetic progression 2 Yield rate examples involving annuities More on annuities

More on annuities with payments in arithmetic progression and yield rates for annuities 1 Annuities-due with payments in arithmetic progression 2 Yield rate examples involving annuities More on annuities

Introduction to Real Estate Investment Appraisal

Introduction to Real Estate Investment Appraisal Maths of Finance Present and Future Values Pat McAllister INVESTMENT APPRAISAL: INTEREST Interest is a reward or rent paid to a lender or investor who has

Introduction to Real Estate Investment Appraisal Maths of Finance Present and Future Values Pat McAllister INVESTMENT APPRAISAL: INTEREST Interest is a reward or rent paid to a lender or investor who has

1 Cash-flows, discounting, interest rate models

Assignment 1 BS4a Actuarial Science Oxford MT 2014 1 1 Cash-flows, discounting, interest rate models Please hand in your answers to questions 3, 4, 5 and 8 for marking. The rest are for further practice.

Assignment 1 BS4a Actuarial Science Oxford MT 2014 1 1 Cash-flows, discounting, interest rate models Please hand in your answers to questions 3, 4, 5 and 8 for marking. The rest are for further practice.

Annuities Certain. 1 Introduction. 2 Annuities-immediate. 3 Annuities-due

Annuities Certain 1 Introduction 2 Annuities-immediate 3 Annuities-due Annuities Certain 1 Introduction 2 Annuities-immediate 3 Annuities-due General terminology An annuity is a series of payments made

Annuities Certain 1 Introduction 2 Annuities-immediate 3 Annuities-due Annuities Certain 1 Introduction 2 Annuities-immediate 3 Annuities-due General terminology An annuity is a series of payments made

Vilnius University. Faculty of Mathematics and Informatics. Gintautas Bareikis

Vilnius University Faculty of Mathematics and Informatics Gintautas Bareikis CONTENT Chapter 1. SIMPLE AND COMPOUND INTEREST 1.1 Simple interest......................................................................

Vilnius University Faculty of Mathematics and Informatics Gintautas Bareikis CONTENT Chapter 1. SIMPLE AND COMPOUND INTEREST 1.1 Simple interest......................................................................

Let P denote the payment amount. Then the accumulated value of the annuity on the daughter s eighteenth birthday is. P s 18.

MATH 3060 Introduction to Financial Mathematics February 2, 205 Example. (Annuity-immediate with unknown payment and a given discount rate. From Vaaler and Daniel, Example 3.2.5, p. 5. ) Mr. Liang wishes

MATH 3060 Introduction to Financial Mathematics February 2, 205 Example. (Annuity-immediate with unknown payment and a given discount rate. From Vaaler and Daniel, Example 3.2.5, p. 5. ) Mr. Liang wishes

Finding the Payment $20,000 = C[1 1 / 1.0066667 48 ] /.0066667 C = $488.26

![Finding the Payment $20,000 = C[1 1 / 1.0066667 48 ] /.0066667 C = $488.26](/thumbs/17/134163.jpg "Finding the Payment $20,000 = C[1 1 / 1.0066667 48 ] /.0066667 C = $488.26") Quick Quiz: Part 2 You know the payment amount for a loan and you want to know how much was borrowed. Do you compute a present value or a future value? You want to receive $5,000 per month in retirement.

Quick Quiz: Part 2 You know the payment amount for a loan and you want to know how much was borrowed. Do you compute a present value or a future value? You want to receive $5,000 per month in retirement.

Chapter 6. Discounted Cash Flow Valuation. Key Concepts and Skills. Multiple Cash Flows Future Value Example 6.1. Answer 6.1

Chapter 6 Key Concepts and Skills Be able to compute: the future value of multiple cash flows the present value of multiple cash flows the future and present value of annuities Discounted Cash Flow Valuation

Chapter 6 Key Concepts and Skills Be able to compute: the future value of multiple cash flows the present value of multiple cash flows the future and present value of annuities Discounted Cash Flow Valuation

Solutions to Supplementary Questions for HP Chapter 5 and Sections 1 and 2 of the Supplementary Material. i = 0.75 1 for six months.

Solutions to Supplementary Questions for HP Chapter 5 and Sections 1 and 2 of the Supplementary Material 1. a) Let P be the recommended retail price of the toy. Then the retailer may purchase the toy at

Solutions to Supplementary Questions for HP Chapter 5 and Sections 1 and 2 of the Supplementary Material 1. a) Let P be the recommended retail price of the toy. Then the retailer may purchase the toy at

5. Time value of money

1 Simple interest 2 5. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

1 Simple interest 2 5. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

1 Interest rates, and risk-free investments

Interest rates, and risk-free investments Copyright c 2005 by Karl Sigman. Interest and compounded interest Suppose that you place x 0 ($) in an account that offers a fixed (never to change over time)

Interest rates, and risk-free investments Copyright c 2005 by Karl Sigman. Interest and compounded interest Suppose that you place x 0 ($) in an account that offers a fixed (never to change over time)

ST334 ACTUARIAL METHODS

ST334 ACTUARIAL METHODS version 214/3 These notes are for ST334 Actuarial Methods. The course covers Actuarial CT1 and some related financial topics. Actuarial CT1 which is called Financial Mathematics

ST334 ACTUARIAL METHODS version 214/3 These notes are for ST334 Actuarial Methods. The course covers Actuarial CT1 and some related financial topics. Actuarial CT1 which is called Financial Mathematics

INSTITUTE OF ACTUARIES OF INDIA

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 15 th November 2010 Subject CT1 Financial Mathematics Time allowed: Three Hours (15.00 18.00 Hrs) Total Marks: 100 INSTRUCTIONS TO THE CANDIDATES 1. Please

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 15 th November 2010 Subject CT1 Financial Mathematics Time allowed: Three Hours (15.00 18.00 Hrs) Total Marks: 100 INSTRUCTIONS TO THE CANDIDATES 1. Please

A) 1.8% B) 1.9% C) 2.0% D) 2.1% E) 2.2%

1.8% B) 1.9% C) 2.0% D) 2.1% E) 2.2%") 1 Exam FM Questions Practice Exam 1 1. Consider the following yield curve: Year Spot Rate 1 5.5% 2 5.0% 3 5.0% 4 4.5% 5 4.0% Find the four year forward rate. A) 1.8% B) 1.9% C) 2.0% D) 2.1% E) 2.2% 2.

1 Exam FM Questions Practice Exam 1 1. Consider the following yield curve: Year Spot Rate 1 5.5% 2 5.0% 3 5.0% 4 4.5% 5 4.0% Find the four year forward rate. A) 1.8% B) 1.9% C) 2.0% D) 2.1% E) 2.2% 2.

Discounted Cash Flow Valuation

6 Formulas Discounted Cash Flow Valuation McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter Outline Future and Present Values of Multiple Cash Flows Valuing

6 Formulas Discounted Cash Flow Valuation McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter Outline Future and Present Values of Multiple Cash Flows Valuing

International Financial Strategies Time Value of Money

International Financial Strategies 1 Future Value and Compounding Future value = cash value of the investment at some point in the future Investing for single period: FV. Future Value PV. Present Value

International Financial Strategies 1 Future Value and Compounding Future value = cash value of the investment at some point in the future Investing for single period: FV. Future Value PV. Present Value

Payment streams and variable interest rates

Chapter 4 Payment streams and variable interest rates In this chapter we consider two extensions of the theory Firstly, we look at payment streams A payment stream is a payment that occurs continuously,

Chapter 4 Payment streams and variable interest rates In this chapter we consider two extensions of the theory Firstly, we look at payment streams A payment stream is a payment that occurs continuously,

E INV 1 AM 11 Name: INTEREST. There are two types of Interest : and. The formula is. I is. P is. r is. t is

E INV 1 AM 11 Name: INTEREST There are two types of Interest : and. SIMPLE INTEREST The formula is I is P is r is t is NOTE: For 8% use r =, for 12% use r =, for 2.5% use r = NOTE: For 6 months use t =

E INV 1 AM 11 Name: INTEREST There are two types of Interest : and. SIMPLE INTEREST The formula is I is P is r is t is NOTE: For 8% use r =, for 12% use r =, for 2.5% use r = NOTE: For 6 months use t =

Bond Price Arithmetic

1 Bond Price Arithmetic The purpose of this chapter is: To review the basics of the time value of money. This involves reviewing discounting guaranteed future cash flows at annual, semiannual and continuously

1 Bond Price Arithmetic The purpose of this chapter is: To review the basics of the time value of money. This involves reviewing discounting guaranteed future cash flows at annual, semiannual and continuously

Chapter 4: Time Value of Money

FIN 301 Homework Solution Ch4 Chapter 4: Time Value of Money 1. a. 10,000/(1.10) 10 = 3,855.43 b. 10,000/(1.10) 20 = 1,486.44 c. 10,000/(1.05) 10 = 6,139.13 d. 10,000/(1.05) 20 = 3,768.89 2. a. $100 (1.10)

FIN 301 Homework Solution Ch4 Chapter 4: Time Value of Money 1. a. 10,000/(1.10) 10 = 3,855.43 b. 10,000/(1.10) 20 = 1,486.44 c. 10,000/(1.05) 10 = 6,139.13 d. 10,000/(1.05) 20 = 3,768.89 2. a. $100 (1.10)

The Basics of Interest Theory

Contents Preface 3 The Basics of Interest Theory 9 1 The Meaning of Interest................................... 10 2 Accumulation and Amount Functions............................ 14 3 Effective Interest

Contents Preface 3 The Basics of Interest Theory 9 1 The Meaning of Interest................................... 10 2 Accumulation and Amount Functions............................ 14 3 Effective Interest

Percent, Sales Tax, & Discounts

Percent, Sales Tax, & Discounts Many applications involving percent are based on the following formula: Note that of implies multiplication. Suppose that the local sales tax rate is 7.5% and you purchase

Percent, Sales Tax, & Discounts Many applications involving percent are based on the following formula: Note that of implies multiplication. Suppose that the local sales tax rate is 7.5% and you purchase

Topics Covered. Ch. 4 - The Time Value of Money. The Time Value of Money Compounding and Discounting Single Sums

Ch. 4 - The Time Value of Money Topics Covered Future Values Present Values Multiple Cash Flows Perpetuities and Annuities Effective Annual Interest Rate For now, we will omit the section 4.5 on inflation

Ch. 4 - The Time Value of Money Topics Covered Future Values Present Values Multiple Cash Flows Perpetuities and Annuities Effective Annual Interest Rate For now, we will omit the section 4.5 on inflation

Basic financial arithmetic

2 Basic financial arithmetic Simple interest Compound interest Nominal and effective rates Continuous discounting Conversions and comparisons Exercise Summary File: MFME2_02.xls 13 This chapter deals

2 Basic financial arithmetic Simple interest Compound interest Nominal and effective rates Continuous discounting Conversions and comparisons Exercise Summary File: MFME2_02.xls 13 This chapter deals

Statistical Models for Forecasting and Planning

Part 5 Statistical Models for Forecasting and Planning Chapter 16 Financial Calculations: Interest, Annuities and NPV chapter 16 Financial Calculations: Interest, Annuities and NPV Outcomes Financial information

Part 5 Statistical Models for Forecasting and Planning Chapter 16 Financial Calculations: Interest, Annuities and NPV chapter 16 Financial Calculations: Interest, Annuities and NPV Outcomes Financial information

Topics Covered. Compounding and Discounting Single Sums. Ch. 4 - The Time Value of Money. The Time Value of Money

Ch. 4 - The Time Value of Money Topics Covered Future Values Present Values Multiple Cash Flows Perpetuities and Annuities Effective Annual Interest Rate For now, we will omit the section 4.5 on inflation

Ch. 4 - The Time Value of Money Topics Covered Future Values Present Values Multiple Cash Flows Perpetuities and Annuities Effective Annual Interest Rate For now, we will omit the section 4.5 on inflation

TIME VALUE OF MONEY (TVM)

") TIME VALUE OF MONEY (TVM) INTEREST Rate of Return When we know the Present Value (amount today), Future Value (amount to which the investment will grow), and Number of Periods, we can calculate the rate

TIME VALUE OF MONEY (TVM) INTEREST Rate of Return When we know the Present Value (amount today), Future Value (amount to which the investment will grow), and Number of Periods, we can calculate the rate

A = P (1 + r / n) n t

n t") Finance Formulas for College Algebra (LCU - Fall 2013) ---------------------------------------------------------------------------------------------------------------------------------- Formula 1: Amount

Finance Formulas for College Algebra (LCU - Fall 2013) ---------------------------------------------------------------------------------------------------------------------------------- Formula 1: Amount

Problem Set: Annuities and Perpetuities (Solutions Below)

") Problem Set: Annuities and Perpetuities (Solutions Below) 1. If you plan to save $300 annually for 10 years and the discount rate is 15%, what is the future value? 2. If you want to buy a boat in 6 years

Problem Set: Annuities and Perpetuities (Solutions Below) 1. If you plan to save $300 annually for 10 years and the discount rate is 15%, what is the future value? 2. If you want to buy a boat in 6 years

Manual for SOA Exam FM/CAS Exam 2.

Manual for SOA Exam FM/CAS Exam 2. Chapter 3. Annuities. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics. Fall 2009 Edition,

Manual for SOA Exam FM/CAS Exam 2. Chapter 3. Annuities. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics. Fall 2009 Edition,

Appendix C- 1. Time Value of Money. Appendix C- 2. Financial Accounting, Fifth Edition

C- 1 Time Value of Money C- 2 Financial Accounting, Fifth Edition Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount. 3. Solve for future

C- 1 Time Value of Money C- 2 Financial Accounting, Fifth Edition Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount. 3. Solve for future

The Institute of Chartered Accountants of India

CHAPTER 4 SIMPLE AND COMPOUND INTEREST INCLUDING ANNUITY APPLICATIONS SIMPLE AND COMPOUND INTEREST INCLUDING ANNUITY- APPLICATIONS LEARNING OBJECTIVES After studying this chapter students will be able

CHAPTER 4 SIMPLE AND COMPOUND INTEREST INCLUDING ANNUITY APPLICATIONS SIMPLE AND COMPOUND INTEREST INCLUDING ANNUITY- APPLICATIONS LEARNING OBJECTIVES After studying this chapter students will be able

Business 2019. Fundamentals of Finance, Chapter 6 Solution to Selected Problems

Business 209 Fundamentals of Finance, Chapter 6 Solution to Selected Problems 8. Calculating Annuity Values You want to have $50,000 in your savings account five years from now, and you re prepared to

Business 209 Fundamentals of Finance, Chapter 6 Solution to Selected Problems 8. Calculating Annuity Values You want to have $50,000 in your savings account five years from now, and you re prepared to

MATH1510 Financial Mathematics I. Jitse Niesen University of Leeds

MATH1510 Financial Mathematics I Jitse Niesen University of Leeds January May 2012 Description of the module This is the description of the module as it appears in the module catalogue. Objectives Introduction

MATH1510 Financial Mathematics I Jitse Niesen University of Leeds January May 2012 Description of the module This is the description of the module as it appears in the module catalogue. Objectives Introduction

1. Annuity a sequence of payments, each made at equally spaced time intervals.

Ordinary Annuities (Young: 6.2) In this Lecture: 1. More Terminology 2. Future Value of an Ordinary Annuity 3. The Ordinary Annuity Formula (Optional) 4. Present Value of an Ordinary Annuity More Terminology

Ordinary Annuities (Young: 6.2) In this Lecture: 1. More Terminology 2. Future Value of an Ordinary Annuity 3. The Ordinary Annuity Formula (Optional) 4. Present Value of an Ordinary Annuity More Terminology

Time Value of Money. Work book Section I True, False type questions. State whether the following statements are true (T) or False (F)

or False (F)") Time Value of Money Work book Section I True, False type questions State whether the following statements are true (T) or False (F) 1.1 Money has time value because you forgo something certain today for

Time Value of Money Work book Section I True, False type questions State whether the following statements are true (T) or False (F) 1.1 Money has time value because you forgo something certain today for

Manual for SOA Exam FM/CAS Exam 2.

Manual for SOA Exam FM/CAS Exam 2. Chapter 2. Cashflows. c 29. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics. Fall 29 Edition,

Manual for SOA Exam FM/CAS Exam 2. Chapter 2. Cashflows. c 29. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics. Fall 29 Edition,

Chapter 2. CASH FLOW Objectives: To calculate the values of cash flows using the standard methods.. To evaluate alternatives and make reasonable

Chapter 2 CASH FLOW Objectives: To calculate the values of cash flows using the standard methods To evaluate alternatives and make reasonable suggestions To simulate mathematical and real content situations

Chapter 2 CASH FLOW Objectives: To calculate the values of cash flows using the standard methods To evaluate alternatives and make reasonable suggestions To simulate mathematical and real content situations

Chapter 6. Time Value of Money Concepts. Simple Interest 6-1. Interest amount = P i n. Assume you invest $1,000 at 6% simple interest for 3 years.

6-1 Chapter 6 Time Value of Money Concepts 6-2 Time Value of Money Interest is the rent paid for the use of money over time. That s right! A dollar today is more valuable than a dollar to be received in

6-1 Chapter 6 Time Value of Money Concepts 6-2 Time Value of Money Interest is the rent paid for the use of money over time. That s right! A dollar today is more valuable than a dollar to be received in

FIN 3000. Chapter 6. Annuities. Liuren Wu

FIN 3000 Chapter 6 Annuities Liuren Wu Overview 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams Learning objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate

FIN 3000 Chapter 6 Annuities Liuren Wu Overview 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams Learning objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate

PRESENT VALUE ANALYSIS. Time value of money equal dollar amounts have different values at different points in time.

PRESENT VALUE ANALYSIS Time value of money equal dollar amounts have different values at different points in time. Present value analysis tool to convert CFs at different points in time to comparable values

PRESENT VALUE ANALYSIS Time value of money equal dollar amounts have different values at different points in time. Present value analysis tool to convert CFs at different points in time to comparable values

DISCOUNTED CASH FLOW VALUATION and MULTIPLE CASH FLOWS

Chapter 5 DISCOUNTED CASH FLOW VALUATION and MULTIPLE CASH FLOWS The basic PV and FV techniques can be extended to handle any number of cash flows. PV with multiple cash flows: Suppose you need $500 one

Chapter 5 DISCOUNTED CASH FLOW VALUATION and MULTIPLE CASH FLOWS The basic PV and FV techniques can be extended to handle any number of cash flows. PV with multiple cash flows: Suppose you need $500 one

Chapter 6 Contents. Principles Used in Chapter 6 Principle 1: Money Has a Time Value.

Chapter 6 The Time Value of Money: Annuities and Other Topics Chapter 6 Contents Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate present and future values

Chapter 6 The Time Value of Money: Annuities and Other Topics Chapter 6 Contents Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate present and future values

Appendix. Time Value of Money. Financial Accounting, IFRS Edition Weygandt Kimmel Kieso. Appendix C- 1

C Time Value of Money C- 1 Financial Accounting, IFRS Edition Weygandt Kimmel Kieso C- 2 Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount.

C Time Value of Money C- 1 Financial Accounting, IFRS Edition Weygandt Kimmel Kieso C- 2 Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount.

SOCIETY OF ACTUARIES/CASUALTY ACTUARIAL SOCIETY EXAM FM SAMPLE QUESTIONS

SOCIETY OF ACTUARIES/CASUALTY ACTUARIAL SOCIETY EXAM FM FINANCIAL MATHEMATICS EXAM FM SAMPLE QUESTIONS Copyright 2005 by the Society of Actuaries and the Casualty Actuarial Society Some of the questions

SOCIETY OF ACTUARIES/CASUALTY ACTUARIAL SOCIETY EXAM FM FINANCIAL MATHEMATICS EXAM FM SAMPLE QUESTIONS Copyright 2005 by the Society of Actuaries and the Casualty Actuarial Society Some of the questions

Chapter 1: Time Value of Money

1 Chapter 1: Time Value of Money Study Unit 1: Time Value of Money Concepts Basic Concepts Cash Flows A cash flow has 2 components: 1. The receipt or payment of money: This differs from the accounting

1 Chapter 1: Time Value of Money Study Unit 1: Time Value of Money Concepts Basic Concepts Cash Flows A cash flow has 2 components: 1. The receipt or payment of money: This differs from the accounting

SOCIETY OF ACTUARIES FINANCIAL MATHEMATICS EXAM FM SAMPLE QUESTIONS

SOCIETY OF ACTUARIES EXAM FM FINANCIAL MATHEMATICS EXAM FM SAMPLE QUESTIONS This page indicates changes made to Study Note FM-09-05. April 28, 2014: Question and solutions 61 were added. January 14, 2014:

SOCIETY OF ACTUARIES EXAM FM FINANCIAL MATHEMATICS EXAM FM SAMPLE QUESTIONS This page indicates changes made to Study Note FM-09-05. April 28, 2014: Question and solutions 61 were added. January 14, 2014:

How to calculate present values

How to calculate present values Back to the future Chapter 3 Discounted Cash Flow Analysis (Time Value of Money) Discounted Cash Flow (DCF) analysis is the foundation of valuation in corporate finance

How to calculate present values Back to the future Chapter 3 Discounted Cash Flow Analysis (Time Value of Money) Discounted Cash Flow (DCF) analysis is the foundation of valuation in corporate finance

In Section 5.3, we ll modify the worksheet shown above. This will allow us to use Excel to calculate the different amounts in the annuity formula,

Excel has several built in functions for working with compound interest and annuities. To use these functions, we ll start with a standard Excel worksheet. This worksheet contains the variables used throughout

Excel has several built in functions for working with compound interest and annuities. To use these functions, we ll start with a standard Excel worksheet. This worksheet contains the variables used throughout

Time Value of Money Concepts

BASIC ANNUITIES There are many accounting transactions that require the payment of a specific amount each period. A payment for a auto loan or a mortgage payment are examples of this type of transaction.

BASIC ANNUITIES There are many accounting transactions that require the payment of a specific amount each period. A payment for a auto loan or a mortgage payment are examples of this type of transaction.

CHAPTER 1. Compound Interest

CHAPTER 1 Compound Interest 1. Compound Interest The simplest example of interest is a loan agreement two children might make: I will lend you a dollar, but every day you keep it, you owe me one more penny.

CHAPTER 1 Compound Interest 1. Compound Interest The simplest example of interest is a loan agreement two children might make: I will lend you a dollar, but every day you keep it, you owe me one more penny.

SOCIETY OF ACTUARIES FINANCIAL MATHEMATICS. EXAM FM SAMPLE QUESTIONS Interest Theory

SOCIETY OF ACTUARIES EXAM FM FINANCIAL MATHEMATICS EXAM FM SAMPLE QUESTIONS Interest Theory This page indicates changes made to Study Note FM-09-05. January 14, 2014: Questions and solutions 58 60 were

SOCIETY OF ACTUARIES EXAM FM FINANCIAL MATHEMATICS EXAM FM SAMPLE QUESTIONS Interest Theory This page indicates changes made to Study Note FM-09-05. January 14, 2014: Questions and solutions 58 60 were

Chapter 6. Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams

Chapter 6 Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams 1. Distinguish between an ordinary annuity and an annuity due, and calculate present

Chapter 6 Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams 1. Distinguish between an ordinary annuity and an annuity due, and calculate present

Key Concepts and Skills

McGraw-Hill/Irwin Copyright 2014 by the McGraw-Hill Companies, Inc. All rights reserved. Key Concepts and Skills Be able to compute: The future value of an investment made today The present value of cash

McGraw-Hill/Irwin Copyright 2014 by the McGraw-Hill Companies, Inc. All rights reserved. Key Concepts and Skills Be able to compute: The future value of an investment made today The present value of cash

Oklahoma State University Spears School of Business. Time Value of Money

Oklahoma State University Spears School of Business Time Value of Money Slide 2 Time Value of Money Which would you rather receive as a sign-in bonus for your new job? 1. $15,000 cash upon signing the

Oklahoma State University Spears School of Business Time Value of Money Slide 2 Time Value of Money Which would you rather receive as a sign-in bonus for your new job? 1. $15,000 cash upon signing the

Chapter 5 Discounted Cash Flow Valuation

Chapter Discounted Cash Flow Valuation Compounding Periods Other Than Annual Let s examine monthly compounding problems. Future Value Suppose you invest $9,000 today and get an interest rate of 9 percent

Chapter Discounted Cash Flow Valuation Compounding Periods Other Than Annual Let s examine monthly compounding problems. Future Value Suppose you invest $9,000 today and get an interest rate of 9 percent

Key Concepts and Skills. Multiple Cash Flows Future Value Example 6.1. Chapter Outline. Multiple Cash Flows Example 2 Continued

6 Calculators Discounted Cash Flow Valuation Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

6 Calculators Discounted Cash Flow Valuation Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

2. How would (a) a decrease in the interest rate or (b) an increase in the holding period of a deposit affect its future value? Why?

a decrease in the interest rate or (b) an increase in the holding period of a deposit affect its future value? Why?") CHAPTER 3 CONCEPT REVIEW QUESTIONS 1. Will a deposit made into an account paying compound interest (assuming compounding occurs once per year) yield a higher future value after one period than an equal-sized

CHAPTER 3 CONCEPT REVIEW QUESTIONS 1. Will a deposit made into an account paying compound interest (assuming compounding occurs once per year) yield a higher future value after one period than an equal-sized

Discounted Cash Flow Valuation

Discounted Cash Flow Valuation Chapter 5 Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

Discounted Cash Flow Valuation Chapter 5 Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY 1. The simple interest per year is: $5,000.08 = $400 So after 10 years you will have: $400 10 = $4,000 in interest. The total balance will be

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY 1. The simple interest per year is: $5,000.08 = $400 So after 10 years you will have: $400 10 = $4,000 in interest. The total balance will be

first complete "prior knowlegde" -- to refresh knowledge of Simple and Compound Interest.

ORDINARY SIMPLE ANNUITIES first complete "prior knowlegde" -- to refresh knowledge of Simple and Compound Interest. LESSON OBJECTIVES: students will learn how to determine the Accumulated Value of Regular

ORDINARY SIMPLE ANNUITIES first complete "prior knowlegde" -- to refresh knowledge of Simple and Compound Interest. LESSON OBJECTIVES: students will learn how to determine the Accumulated Value of Regular

Time Value of Money. Background

Time Value of Money (Text reference: Chapter 4) Topics Background One period case - single cash flow Multi-period case - single cash flow Multi-period case - compounding periods Multi-period case - multiple

Time Value of Money (Text reference: Chapter 4) Topics Background One period case - single cash flow Multi-period case - single cash flow Multi-period case - compounding periods Multi-period case - multiple

Present Value (PV) Tutorial

Tutorial") EYK 15-1 Present Value (PV) Tutorial The concepts of present value are described and applied in Chapter 15. This supplement provides added explanations, illustrations, calculations, present value tables,

EYK 15-1 Present Value (PV) Tutorial The concepts of present value are described and applied in Chapter 15. This supplement provides added explanations, illustrations, calculations, present value tables,

Chapter The Time Value of Money

Chapter The Time Value of Money PPT 9-2 Chapter 9 - Outline Time Value of Money Future Value and Present Value Annuities Time-Value-of-Money Formulas Adjusting for Non-Annual Compounding Compound Interest

Chapter The Time Value of Money PPT 9-2 Chapter 9 - Outline Time Value of Money Future Value and Present Value Annuities Time-Value-of-Money Formulas Adjusting for Non-Annual Compounding Compound Interest

Dick Schwanke Finite Math 111 Harford Community College Fall 2013

Annuities and Amortization Finite Mathematics 111 Dick Schwanke Session #3 1 In the Previous Two Sessions Calculating Simple Interest Finding the Amount Owed Computing Discounted Loans Quick Review of

Annuities and Amortization Finite Mathematics 111 Dick Schwanke Session #3 1 In the Previous Two Sessions Calculating Simple Interest Finding the Amount Owed Computing Discounted Loans Quick Review of

3. Time value of money. We will review some tools for discounting cash flows.

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

Chapter 8. 48 Financial Planning Handbook PDP

Chapter 8 48 Financial Planning Handbook PDP The Financial Planner's Toolkit As a financial planner, you will be doing a lot of mathematical calculations for your clients. Doing these calculations for

Chapter 8 48 Financial Planning Handbook PDP The Financial Planner's Toolkit As a financial planner, you will be doing a lot of mathematical calculations for your clients. Doing these calculations for

Essential Topic: Continuous cash flows

Essential Topic: Continuous cash flows Chapters 2 and 3 The Mathematics of Finance: A Deterministic Approach by S. J. Garrett CONTENTS PAGE MATERIAL Continuous payment streams Example Continuously paid

Essential Topic: Continuous cash flows Chapters 2 and 3 The Mathematics of Finance: A Deterministic Approach by S. J. Garrett CONTENTS PAGE MATERIAL Continuous payment streams Example Continuously paid

Chapter 1. Theory of Interest 1. The measurement of interest 1.1 Introduction

Chapter 1. Theory of Interest 1. The measurement of interest 1.1 Introduction Interest may be defined as the compensation that a borrower of capital pays to lender of capital for its use. Thus, interest

Chapter 1. Theory of Interest 1. The measurement of interest 1.1 Introduction Interest may be defined as the compensation that a borrower of capital pays to lender of capital for its use. Thus, interest

HOW TO CALCULATE PRESENT VALUES

Chapter 2 HOW TO CALCULATE PRESENT VALUES Brealey, Myers, and Allen Principles of Corporate Finance 11th Edition McGraw-Hill/Irwin Copyright 2014 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 2 HOW TO CALCULATE PRESENT VALUES Brealey, Myers, and Allen Principles of Corporate Finance 11th Edition McGraw-Hill/Irwin Copyright 2014 by The McGraw-Hill Companies, Inc. All rights reserved.

5 More on Annuities and Loans

5 More on Annuities and Loans 5.1 Introduction This section introduces Annuities. Much of the mathematics of annuities is similar to that of loans. Indeed, we will see that a loan and an annuity are just

5 More on Annuities and Loans 5.1 Introduction This section introduces Annuities. Much of the mathematics of annuities is similar to that of loans. Indeed, we will see that a loan and an annuity are just

The Time Value of Money (contd.)

") The Time Value of Money (contd.) February 11, 2004 Time Value Equivalence Factors (Discrete compounding, discrete payments) Factor Name Factor Notation Formula Cash Flow Diagram Future worth factor (compound

The Time Value of Money (contd.) February 11, 2004 Time Value Equivalence Factors (Discrete compounding, discrete payments) Factor Name Factor Notation Formula Cash Flow Diagram Future worth factor (compound

The Time Value of Money

The Time Value of Money Time Value Terminology 0 1 2 3 4 PV FV Future value (FV) is the amount an investment is worth after one or more periods. Present value (PV) is the current value of one or more future

The Time Value of Money Time Value Terminology 0 1 2 3 4 PV FV Future value (FV) is the amount an investment is worth after one or more periods. Present value (PV) is the current value of one or more future

Chapter 5 Time Value of Money 2: Analyzing Annuity Cash Flows

1. Future Value of Multiple Cash Flows 2. Future Value of an Annuity 3. Present Value of an Annuity 4. Perpetuities 5. Other Compounding Periods 6. Effective Annual Rates (EAR) 7. Amortized Loans Chapter

1. Future Value of Multiple Cash Flows 2. Future Value of an Annuity 3. Present Value of an Annuity 4. Perpetuities 5. Other Compounding Periods 6. Effective Annual Rates (EAR) 7. Amortized Loans Chapter

Module 5: Interest concepts of future and present value

Page 1 of 23 Module 5: Interest concepts of future and present value Overview In this module, you learn about the fundamental concepts of interest and present and future values, as well as ordinary annuities

Page 1 of 23 Module 5: Interest concepts of future and present value Overview In this module, you learn about the fundamental concepts of interest and present and future values, as well as ordinary annuities

Discounted Cash Flow Valuation

BUAD 100x Foundations of Finance Discounted Cash Flow Valuation September 28, 2009 Review Introduction to corporate finance What is corporate finance? What is a corporation? What decision do managers make?

BUAD 100x Foundations of Finance Discounted Cash Flow Valuation September 28, 2009 Review Introduction to corporate finance What is corporate finance? What is a corporation? What decision do managers make?

CHAPTER 6 Accounting and the Time Value of Money

CHAPTER 6 Accounting and the Time Value of Money 6-1 LECTURE OUTLINE This chapter can be covered in two to three class sessions. Most students have had previous exposure to single sum problems and ordinary

CHAPTER 6 Accounting and the Time Value of Money 6-1 LECTURE OUTLINE This chapter can be covered in two to three class sessions. Most students have had previous exposure to single sum problems and ordinary

Dick Schwanke Finite Math 111 Harford Community College Fall 2013

Annuities and Amortization Finite Mathematics 111 Dick Schwanke Session #3 1 In the Previous Two Sessions Calculating Simple Interest Finding the Amount Owed Computing Discounted Loans Quick Review of

Annuities and Amortization Finite Mathematics 111 Dick Schwanke Session #3 1 In the Previous Two Sessions Calculating Simple Interest Finding the Amount Owed Computing Discounted Loans Quick Review of

Time Value of Money. 15.511 Corporate Accounting Summer 2004. Professor S. P. Kothari Sloan School of Management Massachusetts Institute of Technology

Time Value of Money 15.511 Corporate Accounting Summer 2004 Professor S. P. Kothari Sloan School of Management Massachusetts Institute of Technology July 2, 2004 1 LIABILITIES: Current Liabilities Obligations

Time Value of Money 15.511 Corporate Accounting Summer 2004 Professor S. P. Kothari Sloan School of Management Massachusetts Institute of Technology July 2, 2004 1 LIABILITIES: Current Liabilities Obligations

Accounting Building Business Skills. Interest. Interest. Paul D. Kimmel. Appendix B: Time Value of Money

Accounting Building Business Skills Paul D. Kimmel Appendix B: Time Value of Money PowerPoint presentation by Kate Wynn-Williams University of Otago, Dunedin 2003 John Wiley & Sons Australia, Ltd 1 Interest

Accounting Building Business Skills Paul D. Kimmel Appendix B: Time Value of Money PowerPoint presentation by Kate Wynn-Williams University of Otago, Dunedin 2003 John Wiley & Sons Australia, Ltd 1 Interest

Finance CHAPTER OUTLINE. 5.1 Interest 5.2 Compound Interest 5.3 Annuities; Sinking Funds 5.4 Present Value of an Annuity; Amortization

CHAPTER 5 Finance OUTLINE Even though you re in college now, at some time, probably not too far in the future, you will be thinking of buying a house. And, unless you ve won the lottery, you will need

CHAPTER 5 Finance OUTLINE Even though you re in college now, at some time, probably not too far in the future, you will be thinking of buying a house. And, unless you ve won the lottery, you will need

Engineering Economy. Time Value of Money-3

Engineering Economy Time Value of Money-3 Prof. Kwang-Kyu Seo 1 Chapter 2 Time Value of Money Interest: The Cost of Money Economic Equivalence Interest Formulas Single Cash Flows Equal-Payment Series Dealing

Engineering Economy Time Value of Money-3 Prof. Kwang-Kyu Seo 1 Chapter 2 Time Value of Money Interest: The Cost of Money Economic Equivalence Interest Formulas Single Cash Flows Equal-Payment Series Dealing

substantially more powerful. The internal rate of return feature is one of the most useful of the additions. Using the TI BA II Plus

for Actuarial Finance Calculations Introduction. This manual is being written to help actuarial students become more efficient problem solvers for the Part II examination of the Casualty Actuarial Society

for Actuarial Finance Calculations Introduction. This manual is being written to help actuarial students become more efficient problem solvers for the Part II examination of the Casualty Actuarial Society

LO.a: Interpret interest rates as required rates of return, discount rates, or opportunity costs.

LO.a: Interpret interest rates as required rates of return, discount rates, or opportunity costs. 1. The minimum rate of return that an investor must receive in order to invest in a project is most likely

LO.a: Interpret interest rates as required rates of return, discount rates, or opportunity costs. 1. The minimum rate of return that an investor must receive in order to invest in a project is most likely

FinQuiz Notes 2 0 1 4

Reading 5 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Reading 5 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Continuous Compounding and Discounting

Continuous Compounding and Discounting Philip A. Viton October 5, 2011 Continuous October 5, 2011 1 / 19 Introduction Most real-world project analysis is carried out as we ve been doing it, with the present

Continuous Compounding and Discounting Philip A. Viton October 5, 2011 Continuous October 5, 2011 1 / 19 Introduction Most real-world project analysis is carried out as we ve been doing it, with the present

Mathematics. Rosella Castellano. Rome, University of Tor Vergata

and Loans Mathematics Rome, University of Tor Vergata and Loans Future Value for Simple Interest Present Value for Simple Interest You deposit E. 1,000, called the principal or present value, into a savings

and Loans Mathematics Rome, University of Tor Vergata and Loans Future Value for Simple Interest Present Value for Simple Interest You deposit E. 1,000, called the principal or present value, into a savings