Finding the Payment $20,000 = C[1 1 / ] / C = $488.26

|

|

|

- Sabrina Gloria Clark

- 9 years ago

- Views:

Transcription

1 Quick Quiz: Part 2 You know the payment amount for a loan and you want to know how much was borrowed. Do you compute a present value or a future value? You want to receive $5,000 per month in retirement. If you can earn.75% per month and you expect to need the income for 25 years, how much do you need to have in your account at retirement?

2 Finding the Payment Suppose you want to borrow $20,000 for a new car. You can borrow at 8% per year, compounded monthly (8/12 = % per month). If you take a 4- year loan, what is your monthly payment? $20,000 = C[1 1 / ] / C = $488.26

3 Finding the Number of Payments Example 5.6 Start with the equation and remember your logs. $1,000 = $20(1 1/1.015 t ) / = 1 1 / t 1 / t =.25 1 /.25 = t t = ln(1/.25) / ln(1.015) = months = 7.75 years And this is only true if you don t charge anything more on the card!

/ ln(1.015) = 93.111 months = 7.")

4 Finding the Number of Payments Another Example Suppose you borrow $2,000 at 5% and you are going to make annual payments of $ How long is it before you pay off the loan? $2,000 = $734.42(1 1/1.05 t ) / = 1 1/1.05 t 1/1.05 t = = 1.05 t t = ln( ) / ln(1.05) = 3 years

/.05.136161869 = 1 1/1.05 t 1/1.05 t =.863838131 1.157624287 = 1.")

5 Finding the Rate Suppose you borrow $10,000 from your parents to buy a car. You agree to pay $ per month for 60 months. What is the monthly interest rate?

6 Annuity Finding the Rate Trial and Error Process Choose an interest rate and compute the PV of the payments based on this rate Compare the computed PV with the actual loan amount If the computed PV > loan amount, then the interest rate is too low If the computed PV < loan amount, then the interest rate is too high Adjust the rate and repeat the process until the computed PV and the loan amount are equal

7 Quick Quiz: Part 3 You want to receive $5,000 per month for the next 5 years. How much would you need to deposit today if you can earn.75% per month? What monthly rate would you need to earn if you only have $200,000 to deposit? Suppose you have $200,000 to deposit and can earn.75% per month. How many months could you receive the $5,000 payment? How much could you receive every month for 5 years?

8 Future Values for Annuities Suppose you begin saving for your retirement by depositing $2,000 per year in an IRA. If the interest rate is 7.5%, how much will you have in 40 years? FV(Ordinary) = $2,000( )/.075 = $454, FV(Due) = $454, x = $488,601.52

= $2,000(1.075 40 1)/.075 = $454,513.")

9 Annuity Due You are saving for a new house and you put $10,000 per year in an account paying 8%. The first payment is made today. How much will you have at the end of 3 years? FV = $10,000[( ) /.08](1.08) = $35,061.12

10 Annuity Due Time Line ,464 35,016.12

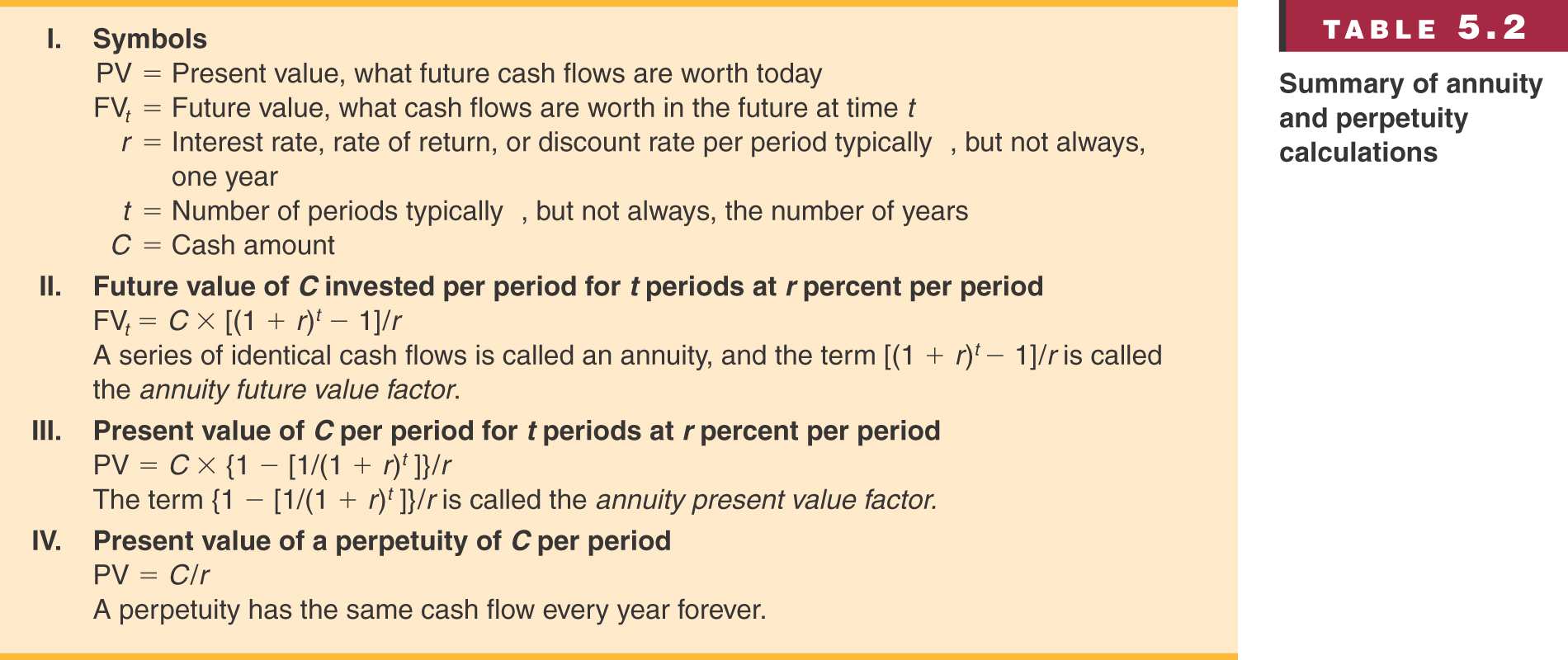

11 Table 5.2

12 Example: Work the Web Another online financial calculator can be found at Moneychimp Click on the Web surfer and work the following example Choose calculator and then annuity You just inherited $5 million. If you can earn 6% on your money, how much can you withdraw each year for the next 40 years? Moneychimp assumes annuity due!!! Payment = $313,497.81

13 Perpetuity Example 5.7 Perpetuity formula: PV = C / r Current required return: $40 = $1 / r r =.025 or 2.5% per quarter Dividend for new preferred: $100 = C /.025 C = $2.50 per quarter

14 Quick Quiz: Part 4 You want to have $1 million to use for retirement in 35 years. If you can earn 1% per month, how much do you need to deposit on a monthly basis if the first payment is made in one month? What if the first payment is made today? You are considering preferred stock that pays a quarterly dividend of $1.50. If your desired return is 3% per quarter, how much would you be willing to pay?

15 Effective Annual Rate (EAR) This is the actual rate paid (or received) after accounting for compounding that occurs during the year If you want to compare two alternative investments with different compounding periods, you need to compute the EAR and use that for comparison.

16 Annual Percentage Rate This is the annual rate that is quoted by law By definition, APR = period rate times the number of periods per year Consequently, to get the period rate we rearrange the APR equation: Period rate = APR / number of periods per year You should NEVER divide the effective rate by the number of periods per year it will NOT give you the period rate

17 Computing APRs What is the APR if the monthly rate is.5%?.5%(12) = 6% What is the APR if the semiannual rate is.5%?.5%(2) = 1% What is the monthly rate if the APR is 12% with monthly compounding? 12% / 12 = 1% Can you divide the above APR by 2 to get the semiannual rate? NO!!! You need an APR based on semiannual compounding to find the semiannual rate.

18 Things to Remember You ALWAYS need to make sure that the interest rate and the time period match. If you are looking at annual periods, you need an annual rate. If you are looking at monthly periods, you need a monthly rate. If you have an APR based on monthly compounding, you have to use monthly periods for lump sums, or adjust the interest rate appropriately if you have payments other than monthly

19 Computing EARs - Example Suppose you can earn 1% per month on $1 invested today. What is the APR? 1%(12) = 12% How much are you effectively earning? FV = 1(1.01) 12 = Rate = ( ) / 1 =.1268 = 12.68% Suppose if you put it in another account, and you earn 3% per quarter. What is the APR? 3%(4) = 12% How much are you effectively earning? FV = 1(1.03) 4 = Rate = ( ) / 1 =.1255 = 12.55%

= 12% How much are you effectively earning? FV = 1(1.03) 4 = 1.1255 Rate = (1.1255 1) / 1 =.")

20 EAR - Formula EAR = 1 + APR m m 1 Remember that the APR is the quoted rate, and m is the number of compounds per year

21 Decisions, Decisions II You are looking at two savings accounts. One pays 5.25%, with daily compounding. The other pays 5.3% with semiannual compounding. Which account should you use? First account: EAR = ( /365) = 5.39% Second account: EAR = ( /2) 2 1 = 5.37% Which account should you choose and why?

22 Decisions, Decisions II Continued Let s verify the choice. Suppose you invest $100 in each account. How much will you have in each account in one year? First Account: Daily rate =.0525 / 365 = FV = $100( ) 365 = $ Second Account: Semiannual rate =.053 / 2 =.0265 FV = $100(1.0265) 2 = $ You have more money in the first account.

23 Computing APRs from EARs If you have an effective rate, how can you compute the APR? Rearrange the EAR equation and you get: APR = m (1 + EAR) m -1 1

24 APR - Example Suppose you want to earn an effective rate of 12% and you are looking at an account that compounds on a monthly basis. What APR must they pay? APR = 12 (1 or 11.39% [ ] +.12) 1/12 1 =

25 Computing Payments with APRs Suppose you want to buy a new computer system. The store will allow you to make monthly payments. The entire computer system costs $3,500. The loan period is for 2 years, and the interest rate is 16.9% with monthly compounding. What is your monthly payment? Monthly rate =.169 / 12 = Number of months = 2(12) = 24 $3,500 = C[1 1 / ( ) 24 ] / C = $172.88

26 Future Values with Monthly Compounding Suppose you deposit $50 per month into an account that has an APR of 9%, based on monthly compounding. How much will you have in the account in 35 years? Monthly rate =.09 / 12 =.0075 Number of months = 35(12) = 420 FV = $50[ ] /.0075 = $147,089.22

27 Present Value with Daily Compounding You need $15,000 in 3 years for a new car. If you can deposit money into an account that pays an APR of 5.5% based on daily compounding, how much would you need to deposit? Daily rate =.055 / 365 = Number of days = 3(365) = 1,095 FV = $15,000 / ( ) 1095 = $12,718.56

28 Quick Quiz: Part 5 What is the definition of an APR? What is the effective annual rate? Which rate should you use to compare alternative investments or loans? Which rate do you need to use in the time value of money calculations?

29 Pure Discount Loans Example 5.11 Treasury bills are excellent examples of pure discount loans. The principal amount is repaid at some future date, without any periodic interest payments. If a T-bill promises to repay $10,000 in one year and the market interest rate is 7 percent, how much will the bill sell for in the market? PV = $10,000 / 1.07 = $9,345.79

30 Interest-Only Loan - Example Consider a 5-year, interest-only loan with a 7% interest rate. The principal amount is $10,000. Interest is paid annually. What would the stream of cash flows be? Years 1 4: Interest payments of.07($10,000) = $700 Year 5: Interest + principal = $10,700 This cash flow stream is similar to the cash flows on corporate bonds. We will talk about them in greater detail later.

31 Amortized Loan with Fixed Payment - Example Each payment covers the interest expense; plus, it reduces principal Consider a 4-year loan with annual payments. The interest rate is 8% and the principal amount is $5,000. What is the annual payment? $5,000 = C[1 1 / ] /.08 C = $1,509.60

32 Quick Quiz: Part 6 What is a pure discount loan? What is a good example of a pure discount loan? What is an interest-only loan? What is a good example of an interest-only loan? What is an amortized loan? What is a good example of an amortized loan?

33 Comprehensive Problem An investment will provide you with $100 at the end of each year for the next 10 years. What is the present value of that annuity if the discount rate is 8% annually? What is the present value of the above if the payments are received at the beginning of each year? If you deposit those payments into an account earning 8%, what will the future value be in 10 years? What will the future value be if you open the account with $1,000 today, and then make the $100 deposits at the end of each year?

Key Concepts and Skills. Multiple Cash Flows Future Value Example 6.1. Chapter Outline. Multiple Cash Flows Example 2 Continued

6 Calculators Discounted Cash Flow Valuation Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

6 Calculators Discounted Cash Flow Valuation Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

Discounted Cash Flow Valuation

6 Formulas Discounted Cash Flow Valuation McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter Outline Future and Present Values of Multiple Cash Flows Valuing

6 Formulas Discounted Cash Flow Valuation McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter Outline Future and Present Values of Multiple Cash Flows Valuing

Discounted Cash Flow Valuation

Discounted Cash Flow Valuation Chapter 5 Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

Discounted Cash Flow Valuation Chapter 5 Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

Chapter 6. Discounted Cash Flow Valuation. Key Concepts and Skills. Multiple Cash Flows Future Value Example 6.1. Answer 6.1

Chapter 6 Key Concepts and Skills Be able to compute: the future value of multiple cash flows the present value of multiple cash flows the future and present value of annuities Discounted Cash Flow Valuation

Chapter 6 Key Concepts and Skills Be able to compute: the future value of multiple cash flows the present value of multiple cash flows the future and present value of annuities Discounted Cash Flow Valuation

DISCOUNTED CASH FLOW VALUATION and MULTIPLE CASH FLOWS

Chapter 5 DISCOUNTED CASH FLOW VALUATION and MULTIPLE CASH FLOWS The basic PV and FV techniques can be extended to handle any number of cash flows. PV with multiple cash flows: Suppose you need $500 one

Chapter 5 DISCOUNTED CASH FLOW VALUATION and MULTIPLE CASH FLOWS The basic PV and FV techniques can be extended to handle any number of cash flows. PV with multiple cash flows: Suppose you need $500 one

The Time Value of Money

The Time Value of Money Time Value Terminology 0 1 2 3 4 PV FV Future value (FV) is the amount an investment is worth after one or more periods. Present value (PV) is the current value of one or more future

The Time Value of Money Time Value Terminology 0 1 2 3 4 PV FV Future value (FV) is the amount an investment is worth after one or more periods. Present value (PV) is the current value of one or more future

Chapter 4. The Time Value of Money

Chapter 4 The Time Value of Money 1 Learning Outcomes Chapter 4 Identify various types of cash flow patterns Compute the future value and the present value of different cash flow streams Compute the return

Chapter 4 The Time Value of Money 1 Learning Outcomes Chapter 4 Identify various types of cash flow patterns Compute the future value and the present value of different cash flow streams Compute the return

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY 1. The simple interest per year is: $5,000.08 = $400 So after 10 years you will have: $400 10 = $4,000 in interest. The total balance will be

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY 1. The simple interest per year is: $5,000.08 = $400 So after 10 years you will have: $400 10 = $4,000 in interest. The total balance will be

5. Time value of money

1 Simple interest 2 5. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

1 Simple interest 2 5. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

Future Value. Basic TVM Concepts. Chapter 2 Time Value of Money. $500 cash flow. On a time line for 3 years: $100. FV 15%, 10 yr.

Chapter Time Value of Money Future Value Present Value Annuities Effective Annual Rate Uneven Cash Flows Growing Annuities Loan Amortization Summary and Conclusions Basic TVM Concepts Interest rate: abbreviated

Chapter Time Value of Money Future Value Present Value Annuities Effective Annual Rate Uneven Cash Flows Growing Annuities Loan Amortization Summary and Conclusions Basic TVM Concepts Interest rate: abbreviated

CHAPTER 6 DISCOUNTED CASH FLOW VALUATION

CHAPTER 6 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. The four pieces are the present value (PV), the periodic cash flow (C), the discount rate (r), and

CHAPTER 6 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. The four pieces are the present value (PV), the periodic cash flow (C), the discount rate (r), and

Chapter 5 Time Value of Money 2: Analyzing Annuity Cash Flows

1. Future Value of Multiple Cash Flows 2. Future Value of an Annuity 3. Present Value of an Annuity 4. Perpetuities 5. Other Compounding Periods 6. Effective Annual Rates (EAR) 7. Amortized Loans Chapter

1. Future Value of Multiple Cash Flows 2. Future Value of an Annuity 3. Present Value of an Annuity 4. Perpetuities 5. Other Compounding Periods 6. Effective Annual Rates (EAR) 7. Amortized Loans Chapter

Business 2019. Fundamentals of Finance, Chapter 6 Solution to Selected Problems

Business 209 Fundamentals of Finance, Chapter 6 Solution to Selected Problems 8. Calculating Annuity Values You want to have $50,000 in your savings account five years from now, and you re prepared to

Business 209 Fundamentals of Finance, Chapter 6 Solution to Selected Problems 8. Calculating Annuity Values You want to have $50,000 in your savings account five years from now, and you re prepared to

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY Answers to Concepts Review and Critical Thinking Questions 1. The four parts are the present value (PV), the future value (FV), the discount

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY Answers to Concepts Review and Critical Thinking Questions 1. The four parts are the present value (PV), the future value (FV), the discount

HOW TO CALCULATE PRESENT VALUES

Chapter 2 HOW TO CALCULATE PRESENT VALUES Brealey, Myers, and Allen Principles of Corporate Finance 11th Edition McGraw-Hill/Irwin Copyright 2014 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 2 HOW TO CALCULATE PRESENT VALUES Brealey, Myers, and Allen Principles of Corporate Finance 11th Edition McGraw-Hill/Irwin Copyright 2014 by The McGraw-Hill Companies, Inc. All rights reserved.

Problem Set: Annuities and Perpetuities (Solutions Below)

") Problem Set: Annuities and Perpetuities (Solutions Below) 1. If you plan to save $300 annually for 10 years and the discount rate is 15%, what is the future value? 2. If you want to buy a boat in 6 years

Problem Set: Annuities and Perpetuities (Solutions Below) 1. If you plan to save $300 annually for 10 years and the discount rate is 15%, what is the future value? 2. If you want to buy a boat in 6 years

1. If you wish to accumulate $140,000 in 13 years, how much must you deposit today in an account that pays an annual interest rate of 14%?

Chapter 2 - Sample Problems 1. If you wish to accumulate $140,000 in 13 years, how much must you deposit today in an account that pays an annual interest rate of 14%? 2. What will $247,000 grow to be in

Chapter 2 - Sample Problems 1. If you wish to accumulate $140,000 in 13 years, how much must you deposit today in an account that pays an annual interest rate of 14%? 2. What will $247,000 grow to be in

Chapter 6. Time Value of Money Concepts. Simple Interest 6-1. Interest amount = P i n. Assume you invest $1,000 at 6% simple interest for 3 years.

6-1 Chapter 6 Time Value of Money Concepts 6-2 Time Value of Money Interest is the rent paid for the use of money over time. That s right! A dollar today is more valuable than a dollar to be received in

6-1 Chapter 6 Time Value of Money Concepts 6-2 Time Value of Money Interest is the rent paid for the use of money over time. That s right! A dollar today is more valuable than a dollar to be received in

You just paid $350,000 for a policy that will pay you and your heirs $12,000 a year forever. What rate of return are you earning on this policy?

1 You estimate that you will have $24,500 in student loans by the time you graduate. The interest rate is 6.5%. If you want to have this debt paid in full within five years, how much must you pay each

1 You estimate that you will have $24,500 in student loans by the time you graduate. The interest rate is 6.5%. If you want to have this debt paid in full within five years, how much must you pay each

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. Assuming positive cash flows and interest rates, the future value increases and the present value

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. Assuming positive cash flows and interest rates, the future value increases and the present value

Chapter 4: Time Value of Money

FIN 301 Homework Solution Ch4 Chapter 4: Time Value of Money 1. a. 10,000/(1.10) 10 = 3,855.43 b. 10,000/(1.10) 20 = 1,486.44 c. 10,000/(1.05) 10 = 6,139.13 d. 10,000/(1.05) 20 = 3,768.89 2. a. $100 (1.10)

FIN 301 Homework Solution Ch4 Chapter 4: Time Value of Money 1. a. 10,000/(1.10) 10 = 3,855.43 b. 10,000/(1.10) 20 = 1,486.44 c. 10,000/(1.05) 10 = 6,139.13 d. 10,000/(1.05) 20 = 3,768.89 2. a. $100 (1.10)

Chapter The Time Value of Money

Chapter The Time Value of Money PPT 9-2 Chapter 9 - Outline Time Value of Money Future Value and Present Value Annuities Time-Value-of-Money Formulas Adjusting for Non-Annual Compounding Compound Interest

Chapter The Time Value of Money PPT 9-2 Chapter 9 - Outline Time Value of Money Future Value and Present Value Annuities Time-Value-of-Money Formulas Adjusting for Non-Annual Compounding Compound Interest

FinQuiz Notes 2 0 1 4

Reading 5 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Reading 5 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Chapter 6. Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams

Chapter 6 Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams 1. Distinguish between an ordinary annuity and an annuity due, and calculate present

Chapter 6 Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams 1. Distinguish between an ordinary annuity and an annuity due, and calculate present

International Financial Strategies Time Value of Money

International Financial Strategies 1 Future Value and Compounding Future value = cash value of the investment at some point in the future Investing for single period: FV. Future Value PV. Present Value

International Financial Strategies 1 Future Value and Compounding Future value = cash value of the investment at some point in the future Investing for single period: FV. Future Value PV. Present Value

Time Value Conepts & Applications. Prof. Raad Jassim

Time Value Conepts & Applications Prof. Raad Jassim Chapter Outline Introduction to Valuation: The Time Value of Money 1 2 3 4 5 6 7 8 Future Value and Compounding Present Value and Discounting More on

Time Value Conepts & Applications Prof. Raad Jassim Chapter Outline Introduction to Valuation: The Time Value of Money 1 2 3 4 5 6 7 8 Future Value and Compounding Present Value and Discounting More on

PowerPoint. to accompany. Chapter 5. Interest Rates

PowerPoint to accompany Chapter 5 Interest Rates 5.1 Interest Rate Quotes and Adjustments To understand interest rates, it s important to think of interest rates as a price the price of using money. When

PowerPoint to accompany Chapter 5 Interest Rates 5.1 Interest Rate Quotes and Adjustments To understand interest rates, it s important to think of interest rates as a price the price of using money. When

Discounted Cash Flow Valuation

BUAD 100x Foundations of Finance Discounted Cash Flow Valuation September 28, 2009 Review Introduction to corporate finance What is corporate finance? What is a corporation? What decision do managers make?

BUAD 100x Foundations of Finance Discounted Cash Flow Valuation September 28, 2009 Review Introduction to corporate finance What is corporate finance? What is a corporation? What decision do managers make?

Oklahoma State University Spears School of Business. Time Value of Money

Oklahoma State University Spears School of Business Time Value of Money Slide 2 Time Value of Money Which would you rather receive as a sign-in bonus for your new job? 1. $15,000 cash upon signing the

Oklahoma State University Spears School of Business Time Value of Money Slide 2 Time Value of Money Which would you rather receive as a sign-in bonus for your new job? 1. $15,000 cash upon signing the

Chapter 6 Contents. Principles Used in Chapter 6 Principle 1: Money Has a Time Value.

Chapter 6 The Time Value of Money: Annuities and Other Topics Chapter 6 Contents Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate present and future values

Chapter 6 The Time Value of Money: Annuities and Other Topics Chapter 6 Contents Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate present and future values

Solutions to Time value of money practice problems

Solutions to Time value of money practice problems Prepared by Pamela Peterson Drake 1. What is the balance in an account at the end of 10 years if $2,500 is deposited today and the account earns 4% interest,

Solutions to Time value of money practice problems Prepared by Pamela Peterson Drake 1. What is the balance in an account at the end of 10 years if $2,500 is deposited today and the account earns 4% interest,

Ch. Ch. 5 Discounted Cash Flows & Valuation In Chapter 5,

Ch. 5 Discounted Cash Flows & Valuation In Chapter 5, we found the PV & FV of single cash flows--either payments or receipts. In this chapter, we will do the same for multiple cash flows. 2 Multiple Cash

Ch. 5 Discounted Cash Flows & Valuation In Chapter 5, we found the PV & FV of single cash flows--either payments or receipts. In this chapter, we will do the same for multiple cash flows. 2 Multiple Cash

2. How would (a) a decrease in the interest rate or (b) an increase in the holding period of a deposit affect its future value? Why?

a decrease in the interest rate or (b) an increase in the holding period of a deposit affect its future value? Why?") CHAPTER 3 CONCEPT REVIEW QUESTIONS 1. Will a deposit made into an account paying compound interest (assuming compounding occurs once per year) yield a higher future value after one period than an equal-sized

CHAPTER 3 CONCEPT REVIEW QUESTIONS 1. Will a deposit made into an account paying compound interest (assuming compounding occurs once per year) yield a higher future value after one period than an equal-sized

Check off these skills when you feel that you have mastered them.

Chapter Objectives Check off these skills when you feel that you have mastered them. Know the basic loan terms principal and interest. Be able to solve the simple interest formula to find the amount of

Chapter Objectives Check off these skills when you feel that you have mastered them. Know the basic loan terms principal and interest. Be able to solve the simple interest formula to find the amount of

The Time Value of Money C H A P T E R N I N E

The Time Value of Money C H A P T E R N I N E Figure 9-1 Relationship of present value and future value PPT 9-1 $1,000 present value $ 10% interest $1,464.10 future value 0 1 2 3 4 Number of periods Figure

The Time Value of Money C H A P T E R N I N E Figure 9-1 Relationship of present value and future value PPT 9-1 $1,000 present value $ 10% interest $1,464.10 future value 0 1 2 3 4 Number of periods Figure

Review for Exam 1. Instructions: Please read carefully

Review for Exam 1 Instructions: Please read carefully The exam will have 20 multiple choice questions and 4 work problems. Questions in the multiple choice section will be either concept or calculation

Review for Exam 1 Instructions: Please read carefully The exam will have 20 multiple choice questions and 4 work problems. Questions in the multiple choice section will be either concept or calculation

Compound Interest Formula

Mathematics of Finance Interest is the rental fee charged by a lender to a business or individual for the use of money. charged is determined by Principle, rate and time Interest Formula I = Prt $100 At

Mathematics of Finance Interest is the rental fee charged by a lender to a business or individual for the use of money. charged is determined by Principle, rate and time Interest Formula I = Prt $100 At

FinQuiz Notes 2 0 1 5

Reading 5 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Reading 5 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Solutions to Questions and Problems NOTE: All-end-of chapter problems were solved using a spreadsheet. Many problems require multiple steps. Due to space and readability

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Solutions to Questions and Problems NOTE: All-end-of chapter problems were solved using a spreadsheet. Many problems require multiple steps. Due to space and readability

Key Concepts and Skills. Chapter Outline. Basic Definitions. Future Values. Future Values: General Formula 1-1. Chapter 4

Key Concepts and Skills Chapter 4 Introduction to Valuation: The Time Value of Money Be able to compute the future value of an investment made today Be able to compute the present value of cash to be received

Key Concepts and Skills Chapter 4 Introduction to Valuation: The Time Value of Money Be able to compute the future value of an investment made today Be able to compute the present value of cash to be received

Present Value and Annuities. Chapter 3 Cont d

Present Value and Annuities Chapter 3 Cont d Present Value Helps us answer the question: What s the value in today s dollars of a sum of money to be received in the future? It lets us strip away the effects

Present Value and Annuities Chapter 3 Cont d Present Value Helps us answer the question: What s the value in today s dollars of a sum of money to be received in the future? It lets us strip away the effects

Chapter 3. Understanding The Time Value of Money. Prentice-Hall, Inc. 1

Chapter 3 Understanding The Time Value of Money Prentice-Hall, Inc. 1 Time Value of Money A dollar received today is worth more than a dollar received in the future. The sooner your money can earn interest,

Chapter 3 Understanding The Time Value of Money Prentice-Hall, Inc. 1 Time Value of Money A dollar received today is worth more than a dollar received in the future. The sooner your money can earn interest,

Chapter 4 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONS

Chapter 4 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONS 4-1 a. PV (present value) is the value today of a future payment, or stream of payments, discounted at the appropriate rate of interest.

Chapter 4 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONS 4-1 a. PV (present value) is the value today of a future payment, or stream of payments, discounted at the appropriate rate of interest.

CHAPTER 4. The Time Value of Money. Chapter Synopsis

CHAPTER 4 The Time Value of Money Chapter Synopsis Many financial problems require the valuation of cash flows occurring at different times. However, money received in the future is worth less than money

CHAPTER 4 The Time Value of Money Chapter Synopsis Many financial problems require the valuation of cash flows occurring at different times. However, money received in the future is worth less than money

Financial Management Spring 2012

3-1 Financial Management Spring 2012 Week 4 How to Calculate Present Values III 4-1 3-2 Topics Covered More Shortcuts Growing Perpetuities and Annuities How Interest Is Paid and Quoted 4-2 Example 3-3

3-1 Financial Management Spring 2012 Week 4 How to Calculate Present Values III 4-1 3-2 Topics Covered More Shortcuts Growing Perpetuities and Annuities How Interest Is Paid and Quoted 4-2 Example 3-3

CHAPTER 2. Time Value of Money 2-1

CHAPTER 2 Time Value of Money 2-1 Time Value of Money (TVM) Time Lines Future value & Present value Rates of return Annuities & Perpetuities Uneven cash Flow Streams Amortization 2-2 Time lines 0 1 2 3

CHAPTER 2 Time Value of Money 2-1 Time Value of Money (TVM) Time Lines Future value & Present value Rates of return Annuities & Perpetuities Uneven cash Flow Streams Amortization 2-2 Time lines 0 1 2 3

1.3.2015 г. D. Dimov. Year Cash flow 1 $3,000 2 $5,000 3 $4,000 4 $3,000 5 $2,000

D. Dimov Most financial decisions involve costs and benefits that are spread out over time Time value of money allows comparison of cash flows from different periods Question: You have to choose one of

D. Dimov Most financial decisions involve costs and benefits that are spread out over time Time value of money allows comparison of cash flows from different periods Question: You have to choose one of

Chapter 5 Discounted Cash Flow Valuation

Chapter Discounted Cash Flow Valuation Compounding Periods Other Than Annual Let s examine monthly compounding problems. Future Value Suppose you invest $9,000 today and get an interest rate of 9 percent

Chapter Discounted Cash Flow Valuation Compounding Periods Other Than Annual Let s examine monthly compounding problems. Future Value Suppose you invest $9,000 today and get an interest rate of 9 percent

PRESENT VALUE ANALYSIS. Time value of money equal dollar amounts have different values at different points in time.

PRESENT VALUE ANALYSIS Time value of money equal dollar amounts have different values at different points in time. Present value analysis tool to convert CFs at different points in time to comparable values

PRESENT VALUE ANALYSIS Time value of money equal dollar amounts have different values at different points in time. Present value analysis tool to convert CFs at different points in time to comparable values

FIN 3000. Chapter 6. Annuities. Liuren Wu

FIN 3000 Chapter 6 Annuities Liuren Wu Overview 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams Learning objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate

FIN 3000 Chapter 6 Annuities Liuren Wu Overview 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams Learning objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate

TIME VALUE OF MONEY. Return of vs. Return on Investment: We EXPECT to get more than we invest!

TIME VALUE OF MONEY Return of vs. Return on Investment: We EXPECT to get more than we invest! Invest $1,000 it becomes $1,050 $1,000 return of $50 return on Factors to consider when assessing Return on

TIME VALUE OF MONEY Return of vs. Return on Investment: We EXPECT to get more than we invest! Invest $1,000 it becomes $1,050 $1,000 return of $50 return on Factors to consider when assessing Return on

Warm-up: Compound vs. Annuity!

Warm-up: Compound vs. Annuity! 1) How much will you have after 5 years if you deposit $500 twice a year into an account yielding 3% compounded semiannually? 2) How much money is in the bank after 3 years

Warm-up: Compound vs. Annuity! 1) How much will you have after 5 years if you deposit $500 twice a year into an account yielding 3% compounded semiannually? 2) How much money is in the bank after 3 years

A = P (1 + r / n) n t

n t") Finance Formulas for College Algebra (LCU - Fall 2013) ---------------------------------------------------------------------------------------------------------------------------------- Formula 1: Amount

Finance Formulas for College Algebra (LCU - Fall 2013) ---------------------------------------------------------------------------------------------------------------------------------- Formula 1: Amount

The time value of money: Part II

The time value of money: Part II A reading prepared by Pamela Peterson Drake O U T L I E 1. Introduction 2. Annuities 3. Determining the unknown interest rate 4. Determining the number of compounding periods

The time value of money: Part II A reading prepared by Pamela Peterson Drake O U T L I E 1. Introduction 2. Annuities 3. Determining the unknown interest rate 4. Determining the number of compounding periods

Topics. Chapter 5. Future Value. Future Value - Compounding. Time Value of Money. 0 r = 5% 1

Chapter 5 Time Value of Money Topics 1. Future Value of a Lump Sum 2. Present Value of a Lump Sum 3. Future Value of Cash Flow Streams 4. Present Value of Cash Flow Streams 5. Perpetuities 6. Uneven Series

Chapter 5 Time Value of Money Topics 1. Future Value of a Lump Sum 2. Present Value of a Lump Sum 3. Future Value of Cash Flow Streams 4. Present Value of Cash Flow Streams 5. Perpetuities 6. Uneven Series

CHAPTER 5. Interest Rates. Chapter Synopsis

CHAPTER 5 Interest Rates Chapter Synopsis 5.1 Interest Rate Quotes and Adjustments Interest rates can compound more than once per year, such as monthly or semiannually. An annual percentage rate (APR)

CHAPTER 5 Interest Rates Chapter Synopsis 5.1 Interest Rate Quotes and Adjustments Interest rates can compound more than once per year, such as monthly or semiannually. An annual percentage rate (APR)

1.2-1.3 Time Value of Money and Discounted Cash Flows

1.-1.3 ime Value of Money and Discounted ash Flows ime Value of Money (VM) - the Intuition A cash flow today is worth more than a cash flow in the future since: Individuals prefer present consumption to

1.-1.3 ime Value of Money and Discounted ash Flows ime Value of Money (VM) - the Intuition A cash flow today is worth more than a cash flow in the future since: Individuals prefer present consumption to

TIME VALUE OF MONEY (TVM)

") TIME VALUE OF MONEY (TVM) INTEREST Rate of Return When we know the Present Value (amount today), Future Value (amount to which the investment will grow), and Number of Periods, we can calculate the rate

TIME VALUE OF MONEY (TVM) INTEREST Rate of Return When we know the Present Value (amount today), Future Value (amount to which the investment will grow), and Number of Periods, we can calculate the rate

Finance 331 Corporate Financial Management Week 1 Week 3 Note: For formulas, a Texas Instruments BAII Plus calculator was used.

Chapter 1 Finance 331 What is finance? - Finance has to do with decisions about money and/or cash flows. These decisions have to do with money being raised or used. General parts of finance include: -

Chapter 1 Finance 331 What is finance? - Finance has to do with decisions about money and/or cash flows. These decisions have to do with money being raised or used. General parts of finance include: -

Key Concepts and Skills

McGraw-Hill/Irwin Copyright 2014 by the McGraw-Hill Companies, Inc. All rights reserved. Key Concepts and Skills Be able to compute: The future value of an investment made today The present value of cash

McGraw-Hill/Irwin Copyright 2014 by the McGraw-Hill Companies, Inc. All rights reserved. Key Concepts and Skills Be able to compute: The future value of an investment made today The present value of cash

Appendix C- 1. Time Value of Money. Appendix C- 2. Financial Accounting, Fifth Edition

C- 1 Time Value of Money C- 2 Financial Accounting, Fifth Edition Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount. 3. Solve for future

C- 1 Time Value of Money C- 2 Financial Accounting, Fifth Edition Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount. 3. Solve for future

3. Time value of money. We will review some tools for discounting cash flows.

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

Chapter 2 Present Value

Chapter 2 Present Value Road Map Part A Introduction to finance. Financial decisions and financial markets. Present value. Part B Valuation of assets, given discount rates. Part C Determination of risk-adjusted

Chapter 2 Present Value Road Map Part A Introduction to finance. Financial decisions and financial markets. Present value. Part B Valuation of assets, given discount rates. Part C Determination of risk-adjusted

How to calculate present values

How to calculate present values Back to the future Chapter 3 Discounted Cash Flow Analysis (Time Value of Money) Discounted Cash Flow (DCF) analysis is the foundation of valuation in corporate finance

How to calculate present values Back to the future Chapter 3 Discounted Cash Flow Analysis (Time Value of Money) Discounted Cash Flow (DCF) analysis is the foundation of valuation in corporate finance

Time Value of Money. Background

Time Value of Money (Text reference: Chapter 4) Topics Background One period case - single cash flow Multi-period case - single cash flow Multi-period case - compounding periods Multi-period case - multiple

Time Value of Money (Text reference: Chapter 4) Topics Background One period case - single cash flow Multi-period case - single cash flow Multi-period case - compounding periods Multi-period case - multiple

Mathematics. Rosella Castellano. Rome, University of Tor Vergata

and Loans Mathematics Rome, University of Tor Vergata and Loans Future Value for Simple Interest Present Value for Simple Interest You deposit E. 1,000, called the principal or present value, into a savings

and Loans Mathematics Rome, University of Tor Vergata and Loans Future Value for Simple Interest Present Value for Simple Interest You deposit E. 1,000, called the principal or present value, into a savings

9. Time Value of Money 1: Present and Future Value

9. Time Value of Money 1: Present and Future Value Introduction The language of finance has unique terms and concepts that are based on mathematics. It is critical that you understand this language, because

9. Time Value of Money 1: Present and Future Value Introduction The language of finance has unique terms and concepts that are based on mathematics. It is critical that you understand this language, because

The Time Value of Money

The following is a review of the Quantitative Methods: Basic Concepts principles designed to address the learning outcome statements set forth by CFA Institute. This topic is also covered in: The Time

The following is a review of the Quantitative Methods: Basic Concepts principles designed to address the learning outcome statements set forth by CFA Institute. This topic is also covered in: The Time

E INV 1 AM 11 Name: INTEREST. There are two types of Interest : and. The formula is. I is. P is. r is. t is

E INV 1 AM 11 Name: INTEREST There are two types of Interest : and. SIMPLE INTEREST The formula is I is P is r is t is NOTE: For 8% use r =, for 12% use r =, for 2.5% use r = NOTE: For 6 months use t =

E INV 1 AM 11 Name: INTEREST There are two types of Interest : and. SIMPLE INTEREST The formula is I is P is r is t is NOTE: For 8% use r =, for 12% use r =, for 2.5% use r = NOTE: For 6 months use t =

Click Here to Buy the Tutorial

FIN 534 Week 4 Quiz 3 (Str) Click Here to Buy the Tutorial http://www.tutorialoutlet.com/fin-534/fin-534-week-4-quiz-3- str/ For more course tutorials visit www.tutorialoutlet.com Which of the following

FIN 534 Week 4 Quiz 3 (Str) Click Here to Buy the Tutorial http://www.tutorialoutlet.com/fin-534/fin-534-week-4-quiz-3- str/ For more course tutorials visit www.tutorialoutlet.com Which of the following

Appendix. Time Value of Money. Financial Accounting, IFRS Edition Weygandt Kimmel Kieso. Appendix C- 1

C Time Value of Money C- 1 Financial Accounting, IFRS Edition Weygandt Kimmel Kieso C- 2 Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount.

C Time Value of Money C- 1 Financial Accounting, IFRS Edition Weygandt Kimmel Kieso C- 2 Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount.

1. Annuity a sequence of payments, each made at equally spaced time intervals.

Ordinary Annuities (Young: 6.2) In this Lecture: 1. More Terminology 2. Future Value of an Ordinary Annuity 3. The Ordinary Annuity Formula (Optional) 4. Present Value of an Ordinary Annuity More Terminology

Ordinary Annuities (Young: 6.2) In this Lecture: 1. More Terminology 2. Future Value of an Ordinary Annuity 3. The Ordinary Annuity Formula (Optional) 4. Present Value of an Ordinary Annuity More Terminology

Chapter 22: Borrowings Models

October 21, 2013 Last Time The Consumer Price Index Real Growth The Consumer Price index The official measure of inflation is the Consumer Price Index (CPI) which is the determined by the Bureau of Labor

October 21, 2013 Last Time The Consumer Price Index Real Growth The Consumer Price index The official measure of inflation is the Consumer Price Index (CPI) which is the determined by the Bureau of Labor

LO.a: Interpret interest rates as required rates of return, discount rates, or opportunity costs.

LO.a: Interpret interest rates as required rates of return, discount rates, or opportunity costs. 1. The minimum rate of return that an investor must receive in order to invest in a project is most likely

LO.a: Interpret interest rates as required rates of return, discount rates, or opportunity costs. 1. The minimum rate of return that an investor must receive in order to invest in a project is most likely

The signing of big-name athletes is often accompanied

ros10765_ch05.qxd 2/26/03 10:24 AM Page 112 5 Discounted Cash Flow Valuation The signing of big-name athletes is often accompanied by great fanfare, but the numbers are sometimes misleading. For example,

ros10765_ch05.qxd 2/26/03 10:24 AM Page 112 5 Discounted Cash Flow Valuation The signing of big-name athletes is often accompanied by great fanfare, but the numbers are sometimes misleading. For example,

How To Value Cash Flow

Lecture: II 1 Time Value of Money (TVM) A dollar today is more valuable than a dollar sometime in the future...! The intuitive basis for present value what determines the effect of timing on the value

Lecture: II 1 Time Value of Money (TVM) A dollar today is more valuable than a dollar sometime in the future...! The intuitive basis for present value what determines the effect of timing on the value

Chapter 4. Time Value of Money. Copyright 2009 Pearson Prentice Hall. All rights reserved.

Chapter 4 Time Value of Money Learning Goals 1. Discuss the role of time value in finance, the use of computational aids, and the basic patterns of cash flow. 2. Understand the concept of future value

Chapter 4 Time Value of Money Learning Goals 1. Discuss the role of time value in finance, the use of computational aids, and the basic patterns of cash flow. 2. Understand the concept of future value

Chapter 4. Time Value of Money. Learning Goals. Learning Goals (cont.)

") Chapter 4 Time Value of Money Learning Goals 1. Discuss the role of time value in finance, the use of computational aids, and the basic patterns of cash flow. 2. Understand the concept of future value

Chapter 4 Time Value of Money Learning Goals 1. Discuss the role of time value in finance, the use of computational aids, and the basic patterns of cash flow. 2. Understand the concept of future value

Bank: The bank's deposit pays 8 % per year with annual compounding. Bond: The price of the bond is $75. You will receive $100 five years later.

ü 4.4 lternative Discounted Cash Flow Decision Rules ü Three Decision Rules (1) Net Present Value (2) Future Value (3) Internal Rate of Return, IRR ü (3) Internal Rate of Return, IRR Internal Rate of Return

ü 4.4 lternative Discounted Cash Flow Decision Rules ü Three Decision Rules (1) Net Present Value (2) Future Value (3) Internal Rate of Return, IRR ü (3) Internal Rate of Return, IRR Internal Rate of Return

Chapter 4. The Time Value of Money

Chapter 4 The Time Value of Money 4-2 Topics Covered Future Values and Compound Interest Present Values Multiple Cash Flows Perpetuities and Annuities Inflation and Time Value Effective Annual Interest

Chapter 4 The Time Value of Money 4-2 Topics Covered Future Values and Compound Interest Present Values Multiple Cash Flows Perpetuities and Annuities Inflation and Time Value Effective Annual Interest

F V P V = F V = P (1 + r) n. n 1. FV n = C (1 + r) i. i=0. = C 1 r. (1 + r) n 1 ]

![F V P V = F V = P (1 + r) n. n 1. FV n = C (1 + r) i. i=0. = C 1 r. (1 + r) n 1 ]](/thumbs/25/5828485.jpg "F V P V = F V = P (1 + r) n. n 1. FV n = C (1 + r) i. i=0. = C 1 r. (1 + r) n 1 ]") 1 Week 2 1.1 Recap Week 1 P V = F V (1 + r) n F V = P (1 + r) n 1.2 FV of Annuity: oncept 1.2.1 Multiple Payments: Annuities Multiple payments over time. A special case of multiple payments: annuities

1 Week 2 1.1 Recap Week 1 P V = F V (1 + r) n F V = P (1 + r) n 1.2 FV of Annuity: oncept 1.2.1 Multiple Payments: Annuities Multiple payments over time. A special case of multiple payments: annuities

DISCOUNTED CASH FLOW VALUATION

6 DISCOUNTED CASH FLOW VALUATION Valuation of Future Cash Flows PART 3 THE SIGNING OF BIG-NAME ATHLETES is often accompanied by great fanfare, but the numbers are often misleading. For example, in 2006,

6 DISCOUNTED CASH FLOW VALUATION Valuation of Future Cash Flows PART 3 THE SIGNING OF BIG-NAME ATHLETES is often accompanied by great fanfare, but the numbers are often misleading. For example, in 2006,

Topics Covered. Ch. 4 - The Time Value of Money. The Time Value of Money Compounding and Discounting Single Sums

Ch. 4 - The Time Value of Money Topics Covered Future Values Present Values Multiple Cash Flows Perpetuities and Annuities Effective Annual Interest Rate For now, we will omit the section 4.5 on inflation

Ch. 4 - The Time Value of Money Topics Covered Future Values Present Values Multiple Cash Flows Perpetuities and Annuities Effective Annual Interest Rate For now, we will omit the section 4.5 on inflation

Example. L.N. Stout () Problems on annuities 1 / 14

Problems on annuities 1 / 14") Example A credit card charges an annual rate of 14% compounded monthly. This month s bill is $6000. The minimum payment is $5. Suppose I keep paying $5 each month. How long will it take to pay off the

Example A credit card charges an annual rate of 14% compounded monthly. This month s bill is $6000. The minimum payment is $5. Suppose I keep paying $5 each month. How long will it take to pay off the

Compounding Quarterly, Monthly, and Daily

126 Compounding Quarterly, Monthly, and Daily So far, you have been compounding interest annually, which means the interest is added once per year. However, you will want to add the interest quarterly,

126 Compounding Quarterly, Monthly, and Daily So far, you have been compounding interest annually, which means the interest is added once per year. However, you will want to add the interest quarterly,

Exercise 1 for Time Value of Money

Exercise 1 for Time Value of Money MULTIPLE CHOICE 1. Which of the following statements is CORRECT? a. A time line is not meaningful unless all cash flows occur annually. b. Time lines are useful for visualizing

Exercise 1 for Time Value of Money MULTIPLE CHOICE 1. Which of the following statements is CORRECT? a. A time line is not meaningful unless all cash flows occur annually. b. Time lines are useful for visualizing

Time Value of Money. Work book Section I True, False type questions. State whether the following statements are true (T) or False (F)

or False (F)") Time Value of Money Work book Section I True, False type questions State whether the following statements are true (T) or False (F) 1.1 Money has time value because you forgo something certain today for

Time Value of Money Work book Section I True, False type questions State whether the following statements are true (T) or False (F) 1.1 Money has time value because you forgo something certain today for

Integrated Case. 5-42 First National Bank Time Value of Money Analysis

Integrated Case 5-42 First National Bank Time Value of Money Analysis You have applied for a job with a local bank. As part of its evaluation process, you must take an examination on time value of money

Integrated Case 5-42 First National Bank Time Value of Money Analysis You have applied for a job with a local bank. As part of its evaluation process, you must take an examination on time value of money

Goals. The Time Value of Money. First example. Compounding. Economics 71a Spring 2007 Mayo, Chapter 7 Lecture notes 3.1

Goals The Time Value of Money Economics 7a Spring 2007 Mayo, Chapter 7 Lecture notes 3. More applications Compounding PV = present or starting value FV = future value R = interest rate n = number of periods

Goals The Time Value of Money Economics 7a Spring 2007 Mayo, Chapter 7 Lecture notes 3. More applications Compounding PV = present or starting value FV = future value R = interest rate n = number of periods

In Section 5.3, we ll modify the worksheet shown above. This will allow us to use Excel to calculate the different amounts in the annuity formula,

Excel has several built in functions for working with compound interest and annuities. To use these functions, we ll start with a standard Excel worksheet. This worksheet contains the variables used throughout

Excel has several built in functions for working with compound interest and annuities. To use these functions, we ll start with a standard Excel worksheet. This worksheet contains the variables used throughout

Topics Covered. Compounding and Discounting Single Sums. Ch. 4 - The Time Value of Money. The Time Value of Money

Ch. 4 - The Time Value of Money Topics Covered Future Values Present Values Multiple Cash Flows Perpetuities and Annuities Effective Annual Interest Rate Inflation & Time Value The Time Value of Money

Ch. 4 - The Time Value of Money Topics Covered Future Values Present Values Multiple Cash Flows Perpetuities and Annuities Effective Annual Interest Rate Inflation & Time Value The Time Value of Money

Finite Mathematics. CHAPTER 6 Finance. Helene Payne. 6.1. Interest. savings account. bond. mortgage loan. auto loan

Finite Mathematics Helene Payne CHAPTER 6 Finance 6.1. Interest savings account bond mortgage loan auto loan Lender Borrower Interest: Fee charged by the lender to the borrower. Principal or Present Value:

Finite Mathematics Helene Payne CHAPTER 6 Finance 6.1. Interest savings account bond mortgage loan auto loan Lender Borrower Interest: Fee charged by the lender to the borrower. Principal or Present Value:

Finance CHAPTER OUTLINE. 5.1 Interest 5.2 Compound Interest 5.3 Annuities; Sinking Funds 5.4 Present Value of an Annuity; Amortization

CHAPTER 5 Finance OUTLINE Even though you re in college now, at some time, probably not too far in the future, you will be thinking of buying a house. And, unless you ve won the lottery, you will need

CHAPTER 5 Finance OUTLINE Even though you re in college now, at some time, probably not too far in the future, you will be thinking of buying a house. And, unless you ve won the lottery, you will need

CHAPTER 8 INTEREST RATES AND BOND VALUATION

CHAPTER 8 INTEREST RATES AND BOND VALUATION Answers to Concept Questions 1. No. As interest rates fluctuate, the value of a Treasury security will fluctuate. Long-term Treasury securities have substantial

CHAPTER 8 INTEREST RATES AND BOND VALUATION Answers to Concept Questions 1. No. As interest rates fluctuate, the value of a Treasury security will fluctuate. Long-term Treasury securities have substantial

Key Concepts and Skills

Chapters 5 and 6 Calculators Time Value of Money and Discounted Cash Flow Valuation McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Key Concepts and Skills Be able

Chapters 5 and 6 Calculators Time Value of Money and Discounted Cash Flow Valuation McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Key Concepts and Skills Be able

A = P [ (1 + r/n) nt 1 ] (r/n)

![A = P [ (1 + r/n) nt 1 ] (r/n)](/thumbs/39/18618972.jpg "A = P [ (1 + r/n) nt 1 ] (r/n)") April 23 8.4 Annuities, Stocks and Bonds ---- Systematic Savings Annuity = sequence of equal payments made at equal time periods i.e. depositing $1000 at the end of every year into an IRA Value of an annuity

April 23 8.4 Annuities, Stocks and Bonds ---- Systematic Savings Annuity = sequence of equal payments made at equal time periods i.e. depositing $1000 at the end of every year into an IRA Value of an annuity

Chapter 3 Present Value

Chapter 3 Present Value MULTIPLE CHOICE 1. Which of the following cannot be calculated? a. Present value of an annuity. b. Future value of an annuity. c. Present value of a perpetuity. d. Future value

Chapter 3 Present Value MULTIPLE CHOICE 1. Which of the following cannot be calculated? a. Present value of an annuity. b. Future value of an annuity. c. Present value of a perpetuity. d. Future value

Regular Annuities: Determining Present Value

8.6 Regular Annuities: Determining Present Value GOAL Find the present value when payments or deposits are made at regular intervals. LEARN ABOUT the Math Harry has money in an account that pays 9%/a compounded

8.6 Regular Annuities: Determining Present Value GOAL Find the present value when payments or deposits are made at regular intervals. LEARN ABOUT the Math Harry has money in an account that pays 9%/a compounded