Do Recent Rulings Herald The Divorce Of Oil And Natural Gas Prices, And Who Will Benefit?

|

|

|

- Avice Roberts

- 8 years ago

- Views:

Transcription

1 Credit FAQ: Do Recent Rulings Herald The Divorce Of Oil And Natural Gas Prices, And Who Will Benefit? Primary Credit Analyst: Karim Nassif, Dubai (971) ; Secondary Contacts: Tuomas E Ekholm, CFA, Frankfurt (49) ; Tuomas_Ekholm@standardandpoors.com Elena Anankina, CFA, Moscow (7) ; elena_anankina@standardandpoors.com Mark Habib, New York (1) ; mark_habib@standardandpoors.com Research Contributors: Sapna Jagtiani, Dubai (971) ; Sapna_Jagtiani@standardandpoors.com Ekaterina Kulikova, Moscow (7) ; ekaterina_kulikova@standardandpoors.com Table Of Contents Frequently Asked Questions FEBRUARY 4,

495-783-4130; elena_anankina@standardandpoors.com Mark Habib, New York (1) 212-438-1000; mark_habib@standardandpoors.")

2 Credit FAQ: Do Recent Rulings Herald The Divorce Of Oil And Natural Gas Prices, And Who Will Benefit? Recent arbitration cases and commercial agreements have highlighted controversies in the formulation of gas contract pricing, leading market commentators to point to the possibility of oil prices and gas contract prices being gradually decoupled. Notable cases include those between gas suppliers like Qatar's Ras Laffan Liquefied Natural Gas Co. Ltd. 2 & 3 (collectively known as RasGas), Russia's Gazprom OAO, Norway's Statoil ASA, and the Netherlands' GasTerra B.V. and gas importers like Italy's Edison SpA, Germany's E.ON SE, and Spain's Gas Natural SDG S.A. Some of them have led to compensation being paid by the suppliers. Standard & Poor's Ratings Services answers below the most frequently asked questions about the arbitration and what it may mean for the credit quality of our rated gas suppliers and importers. We also address the dynamics that are driving the decoupling of oil and gas supply contract prices and what this could mean for gas supply contracts and gas markets in general in future. Frequently Asked Questions What have the recent arbitration awards and commercial agreements been about? Gazprom and other European gas market suppliers' contract prices have historically been linked to oil products. Traditional European long-term gas import contracts include price review clauses, which allow base prices and indexation formulas to be reset every three years based on market changes. In the current context of high oil prices and oversupply of gas in the European market, oil-indexed gas import prices have been well above European spot prices and parity levels for alternative fuels such as coal. With oil-indexed import contracts permanently "out of the money" importers have been forced to incur losses in their trading segments to be able to place contracted import volumes in the marketplace. This has pushed Central and Western European importers to file arbitration cases and renegotiate long-term supply contracts with base price revisions outside the normal contract review cycle. It has also led to changes in pricing formula in the form of the introduction of a spot component, and some retroactive payments to importers to recover past losses, higher flexibility in volume, and higher destination flexibility, thus increasing the ability to divert volumes, notably for liquefied natural gas (LNG). Details on base price discounts and changes in pricing formulas are not generally disclosed. The European Commission has started an antitrust investigation against Gazprom. We understand that customers in the Commonwealth of Independent States (CIS), notably Ukraine, are also trying to renegotiate their contracts. What have been the key legal developments in the past year? They all concern gas supplier RasGas. On Sept. 11, 2012, the court of arbitration of the International Chamber of Commerce ruled against RasGas in a dispute with Italian utility, Edison, over their long-term LNG Sales and Purchase Agreement (SPA) contract. The LNG SPA sets out the pricing formula and quantity of LNG to be purchased over the term of the SPA by Edison, subject to FEBRUARY 4,

, Russia's Gazprom OAO, Norway's Statoil ASA, and the Netherlands' GasTerra B.V. and gas importers like Italy's Edison SpA, Germany's E.")

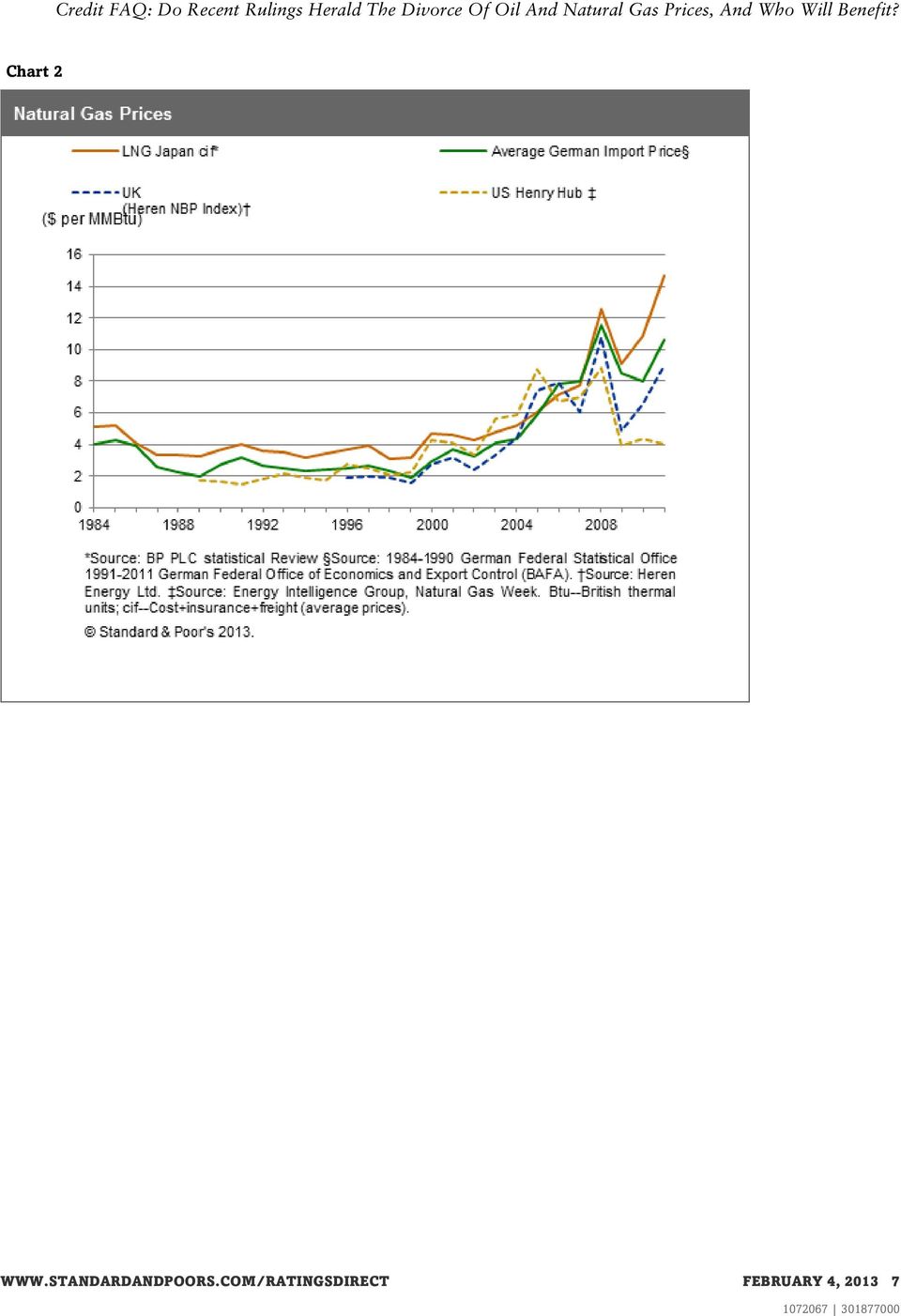

3 RasGas making the LNG available. The RasGas LNG contracts will typically involve a mixture of crude oil and gas based indices that govern the final price. The relative exposure to crude versus gas based indices will depend on the particular contract. The court ruled against RasGas in the dispute relating to their SPA contract with Edison, which ended with RasGas paying about 450 million in compensation. RasGas is still in arbitration with Distrigas over oil indexation of gas prices in their SPA contract. RasGas entered into arbitration with Spanish utility Endesa S.A. in July 2012 over oil indexation of gas prices in their SPA contracts. What is driving the decoupling of U.S., and now increasingly European, natural gas and crude oil prices? The dramatic increase in unconventional production techniques in the last five years, especially shale. Natural gas and crude oil prices have effectively already decoupled in the U.S. market, resulting in the price ratio of a barrel of crude oil to a million metric British thermal unit (mmbtu) of natural gas rising to over 25:1 on a sustained basis, well in excess of 6:1, the ratio based on pricing energy content at parity. Technology advancements and widespread adoption of horizontal drilling and hydraulic fracturing have lowered development costs and increased production efficiency, flooding the U.S. market with natural gas and natural gas liquids (NGLs). This has helped to drive renewed competitiveness in several industries, like petrochemical production, refining, and other natural gas-fueled manufacturing sectors that rely on these feedstocks. Until the development of large-scale liquefaction that would make natural gas exports viable, U.S. production will remain stranded in North America. This has already led to a sharp decline in Henry Hub prices over the past 12 months (see chart 1). Prices hit a 10-year low in the second quarter of 2012, and have fallen sharply since their 2008 peak over $10 per mmbtu. The decoupling in the U.S. as a result of shale also has consequences for the decoupling taking place in Europe: U.S. LNG import facilities are sitting virtually idle with suppliers rerouting capacity to more lucrative markets like Asia and Europe. LNG that would have been destined for the U.S., from the Middle East and elsewhere, is increasingly being diverted to other markets such as Europe. In addition, following the shale gas growth phenonmenon, the U.S. has found itself with excess coal. Some of this cheap goal is finding a home in Europe. Europe, given the current macroeconomic climate, is happy tapping into the additional coal resources from North America as a short term and cost advantageous way of fueling its power plants. These developments are expounded by the relatively loose implementation of carbon-pricing policy in Europe. Additional supplies of LNG and imported coal from the U.S. have therefore helped tip the supply-demand dynamics in Europe in favor of supply, which is also putting pressure on Europe gas hub prices. Gas demand in the EU fell by 10% between 2010 and 2011, and a further fall is expected for 2012, along with increased pressure in Having witnessed the decline in North American gas prices, buyers of LNG in Europe are looking for substantial FEBRUARY 4,

4 changes in their SPA LNG contracts, and this has prompted importers of pipeline gas from Russia and Algeria in Europe, who have traditionally signed contracts indexed to oil prices to try to renegotiate their contracts. Henry Hub is increasingly being used as a benchmark on which to price gas contracts in Europe. For example, Spain's Gas Natural Fenosa has introduced Henry Hub-based indexation for its Sabene Pass project. This follows developments elsewhere around the globe where Henry Hub is increasingly being introduced to benchmark gas contract prices. In addition to the effect of U.S shale on pricing in Europe, decoupling in Europe has been promulgated through regulatory reform over the past decade. For example, Europe's businesses have gone through considerable structural change as regulatory pressures have grown, mainly because of the determination of policy makers to create a single competitive internal market. Contractual tensions have led to financial losses among companies forced to buy imported gas under oil-indexed contracts and to sell it on at lower hub-based prices. What short- to medium-term effects does Standard & Poor's think the recent trends in decoupling will have on the ratings on EMEA gas suppliers and importers? Little effect for suppliers and a positive effect for importers because they've managed to significantly cut risk in their portfolios. For importers our view is that the recent changes in contract structures toward a higher share of hub-based pricing elements instead of oil indexation, following the decoupling of the market, is likely to be a credit supportive as it lowers the likelihood that an importer will run into a structural deficit in the midstream gas business. At the same time we acknowledge that gas wholesale is likely to be a relatively low-margin activity for the importers going forward. We would expect the effects on gas producers' RasGas' and Gazprom's credit quality to be limited because their ratings already factor in a degree of price volatility and are not tied to currently high oil prices. Our ratings are currently based on a midterm price scenario of Brent at $80 per barrel (bbl), which is about 25% below the current Brent crude price, and factor in that the conditions we see today in the market in relation to the decoupling of oil and gas persisting over the short to medium term. For example, supplier Gazprom's EBITDA would be about $40 billion over the short to medium term if the decoupling persisted, significantly lower than 2011's record levels of $66 billion, but still sufficient to support adjusted debt to EBITDA of about 1.5x, in our view. This is still comfortable for our assessment of the company's stand-alone credit profile at 'bbb-'. Gazprom might need to make compensation payments to its customers of up to $7 billion, $4.4 billion of which would have already been paid in the first half of Compared with gross revenues from sales to Europe of $29.7 billion and $28.8 billion over the same period, and bearing in mind the group's low leverage, this amount in our view is comfortable at the existing stand-alone credit profile over the short to medium term. Supplier RasGas' debt service coverage ratios would be expected to remain comfortably above 3x under this scenario, given the compellingly low break-evens in the transaction. For example, Brent would have to drop to $12.7/bbl and Henry Hub would to $1.62/bbl for break even under the financing. We also note that deliveries to Edison, Endesa, and Distrigas are continuing with no interruptions and that the combined amount sold to all three represented less than 20% of RasGas' total cargo sales for The arbitration award was high but not material, in our view, in the context FEBRUARY 4,

5 of RasGas' overall financial performance in To take two importers as examples, we would expect the ruling against RasGas to have a 2012 financial impact of 450 million for Edison's contract with RasGas, and 250 million for Edison's contract with ENI. About half relates to previous years. These are the first gas contracts for Edison being ruled on by a Court of Arbitration, previously we have only seen out of court renegotiations. This legal precedent provides a positive signal, in our opinion, for Edison and others ability to recoup midstream gas losses. The arbitration rulings secure, in our view, a significant share of Edison's cash flows. Although the magnitude and timing of the arbitration proceeds to Edison are uncertain, they support our view that the improvement in Edison's earnings and credit metrics in 2012 is sustainable in the medium term across the arbitration cycle. E.ON has publicly stated that it has completed a round of renegotiations with all of its gas suppliers, including Gazprom. We do not expect any ratings implications in the short to medium term as a result of these negotiations. What medium- to long-term effects would continued decoupling have on the ratings on EMEA gas suppliers and importers? For suppliers the rating impact would depend on eventual gas prices rather than whether or not they were linked to oil. We also derive our view over the medium to long term based on a price scenario of Brent at $80 bbl, which is about 25% below the current Brent crude price. For importers our medium to long term view is similar to that over the short to medium term. Namely, that the changes as a result of continued decoupling are likely to be credit supportive in that they help remove the structural deficit in the midstream gas business. In practice total effective de-coupling across the market will be closely monitored as this will ultimately determine the impact on credit quality. Thus, speedy change in gas supply contracts towards hub-based prices such that this matches the pace at which liberalization towards hub based pricing on the wholesale side is occurring will be key, in our view, in limiting continued exposure by importers to the structural deficit and in supporting their credit quality over this time horizon. As an example, decoupling of oil and gas prices over the medium to long term, at levels witnessed today, would be unlikely to lead us to take any rating action on the ratings on RasGas over the same time horizon. Based on our analysis undertaken of RasGas' financing, it would take a 65% or more decline in revenues across RasGas' businesses for the project to reach break-even with a debt service coverage ratio of 1x. For Gazprom, our expectation of an "extremely high" likelihood of government support should provide resilience for the rating. Under our methodology for rating government-related entities, assuming that Russia's sovereign rating and Gazprom's critical role for the Russian economy and very strong links with the government remain unchanged, the rating would remain at 'BBB' even if the stand-alone credit profile fell to 'bb-', which we view as very unlikely. An important additional element in the analysis of the impact for an importer over the longer term is the degree to which there is risk sharing under the long-term contract. For example, the typical long-term gas supply contract involves the supplier taking the price risk and the importer only exposed to volume risk. We expect this to continue to provide some protection in the form of potential recovery of past losses for these importers in the event that decoupling results in adverse movements in hub-based pricing and ultimately wholesale prices for importers in their FEBRUARY 4,

6 domestic markets. However, as a business model this does not look sustainable for the importers. We note also that while there continues to be forward momentum in the market toward continued decoupling, there are nonetheless some opposing forces that may limit the degree of that decoupling over the short, medium, and long term. These include challenges in exporting LNG from the U.S. to Europe, the uncertain environmental impact of shale technology, the security of supply offered by gas, political priorities to support clean fuel in Europe, and significant power needs in emerging markets like Southeast Asia, Saudi Arabia, and the UAE, all of which are basing their plants on gas as the principle fuel. Chart 1 FEBRUARY 4,

7 Chart 2 FEBRUARY 4,

02-72111-207; vittoria_ferraris@standardandpoors.com Tommy J Trask, Dubai (971) 4-372-7151; Tommy_Trask@standardandpoors.com WWW.STANDARDANDPOORS.")

8 Chart 3 Additional Contacts: Nicolas Riviere, Paris (33) ; nicolas_riviere@standardandpoors.com Simon Redmond, London (44) ; simon_redmond@standardandpoors.com Vittoria Ferraris, Milan (39) ; vittoria_ferraris@standardandpoors.com Tommy J Trask, Dubai (971) ; Tommy_Trask@standardandpoors.com FEBRUARY 4,

02-72111-207; vittoria_ferraris@standardandpoors.")

9 Copyright 2013 by Standard & Poor's Financial Services LLC. All rights reserved. No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part thereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of Standard & Poor's Financial Services LLC or its affiliates (collectively, S&P). The Content shall not be used for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees or agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for the security or maintenance of any data input by the user. The Content is provided on an "as is" basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT'S FUNCTIONING WILL BE UNINTERRUPTED, OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by negligence) in connection with any use of the Content even if advised of the possibility of such damages. Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and not statements of fact. S&P's opinions, analyses, and rating acknowledgment decisions (described below) are not recommendations to purchase, hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation to update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does not act as a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be reliable, S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives. To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain regulatory purposes, S&P reserves the right to assign, withdraw, or suspend such acknowledgement at any time and in its sole discretion. S&P Parties disclaim any duty whatsoever arising out of the assignment, withdrawal, or suspension of an acknowledgment as well as any liability for any damage alleged to have been suffered on account thereof. S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain business units of S&P may have information that is not available to other S&P business units. S&P has established policies and procedures to maintain the confidentiality of certain nonpublic information received in connection with each analytical process. S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites, (free of charge), and and (subscription) and (subscription) and may be distributed through other means, including via S&P publications and third-party redistributors. Additional information about our ratings fees is available at FEBRUARY 4,

. The Content shall not be used for any unlawful or unauthorized purposes.")

AEG Power Solutions Downgraded To 'CC' On Intended Debt Restructuring; Outlook Negative

Research Update: AEG Power Solutions Downgraded To 'CC' On Intended Debt Restructuring; Outlook Negative Primary Credit Analyst: Abigail Klimovich, CFA, London (44) 20-7176-3554; abigail.klimovich@standardandpoors.com

Research Update: AEG Power Solutions Downgraded To 'CC' On Intended Debt Restructuring; Outlook Negative Primary Credit Analyst: Abigail Klimovich, CFA, London (44) 20-7176-3554; abigail.klimovich@standardandpoors.com

AEG Power Solutions Downgraded To 'CCC-' On Heightened Risk Of Missing An Interest Payment; Outlook Negative

Research Update: AEG Power Solutions Downgraded To 'CCC-' On Heightened Risk Of Missing An Interest Payment; Outlook Negative Primary Credit Analyst: Abigail Klimovich, CFA, London (44) 20-7176-3554; abigail.klimovich@standardandpoors.com

Research Update: AEG Power Solutions Downgraded To 'CCC-' On Heightened Risk Of Missing An Interest Payment; Outlook Negative Primary Credit Analyst: Abigail Klimovich, CFA, London (44) 20-7176-3554; abigail.klimovich@standardandpoors.com

AEG Power Solutions Downgraded To 'CCC+' On Weak Earnings And Delays In Customer Payments; Outlook Negative

Research Update: AEG Power Solutions Downgraded To 'CCC+' On Weak Earnings And Delays In Customer Payments; Outlook Negative Primary Credit Analyst: Abigail Klimovich, CFA, London (44) 20-7176-3554; abigail_klimovich@standardandpoors.com

Research Update: AEG Power Solutions Downgraded To 'CCC+' On Weak Earnings And Delays In Customer Payments; Outlook Negative Primary Credit Analyst: Abigail Klimovich, CFA, London (44) 20-7176-3554; abigail_klimovich@standardandpoors.com

Spain-Based IT Service Provider Amadeus IT Holding Rating Raised To 'BBB/A-2' On Strong Financials, Outlook Stable

Research Update: Spain-Based IT Service Provider Amadeus IT Holding Rating Raised To 'BBB/A-2' On Strong Financials, Outlook Stable Primary Credit Analyst: Stefan Kirschner, Frankfurt (49) 69-33-999-281;

Research Update: Spain-Based IT Service Provider Amadeus IT Holding Rating Raised To 'BBB/A-2' On Strong Financials, Outlook Stable Primary Credit Analyst: Stefan Kirschner, Frankfurt (49) 69-33-999-281;

Fibria Celulose S.A. Upgraded To 'BB+ From 'BB' On Debt Reduction, Outlook Stable

Research Update: Fibria Celulose S.A. Upgraded To 'BB+ From 'BB' On Debt Reduction, Outlook Stable Primary Credit Analyst: Diego H Ocampo, Buenos Aires (54) 114-891-2124; diego_ocampo@standardandpoors.com

Research Update: Fibria Celulose S.A. Upgraded To 'BB+ From 'BB' On Debt Reduction, Outlook Stable Primary Credit Analyst: Diego H Ocampo, Buenos Aires (54) 114-891-2124; diego_ocampo@standardandpoors.com

Electricity Transmission System Operator TenneT's Hybrid Equity Content Revised To Intermediate; 'A-' Ratings Affirmed

Research Update: Electricity Transmission System Operator TenneT's Hybrid Equity Content Revised To Intermediate; 'A-' Ratings Affirmed Primary Credit Analyst: Beatrice de Taisne, CFA, London (44) 20-7176-3938;

Research Update: Electricity Transmission System Operator TenneT's Hybrid Equity Content Revised To Intermediate; 'A-' Ratings Affirmed Primary Credit Analyst: Beatrice de Taisne, CFA, London (44) 20-7176-3938;

Residential Real Estate Company Deutsche Wohnen 'BBB+' Ratings Placed On CreditWatch Negative On Conwert Takeover Offer

Research Update: Residential Real Estate Company Deutsche Wohnen 'BBB+' Ratings Placed On CreditWatch Negative On Conwert Takeover Offer Primary Credit Analyst: Marie-Aude Vialle, London (44) 20-7176-3655;

Research Update: Residential Real Estate Company Deutsche Wohnen 'BBB+' Ratings Placed On CreditWatch Negative On Conwert Takeover Offer Primary Credit Analyst: Marie-Aude Vialle, London (44) 20-7176-3655;

Research Update: Ratings On Russian Independent Gas Producer OAO NOVATEK Raised To 'BB+/ruAA+'; Outlook Stable

July 11, 2008 Research Update: Ratings On Russian Independent Gas Producer OAO NOVATEK Raised To 'BB+/ruAA+'; Outlook Stable Primary Credit Analyst: Elena Anankina, Moscow (7) 495-783-4130;elena_anankina@standardandpoors.com

July 11, 2008 Research Update: Ratings On Russian Independent Gas Producer OAO NOVATEK Raised To 'BB+/ruAA+'; Outlook Stable Primary Credit Analyst: Elena Anankina, Moscow (7) 495-783-4130;elena_anankina@standardandpoors.com

German Utility RWE Downgraded To 'BBB-/A-3'; Outlook Negative

Research Update: German Utility RWE Downgraded To 'BBB-/A-3'; Outlook Negative Primary Credit Analyst: Vittoria Ferraris, Milan (39) 02-72111-207; vittoria.ferraris@spglobal.com Secondary Contact: Tobias

Research Update: German Utility RWE Downgraded To 'BBB-/A-3'; Outlook Negative Primary Credit Analyst: Vittoria Ferraris, Milan (39) 02-72111-207; vittoria.ferraris@spglobal.com Secondary Contact: Tobias

Dominion Gas Holdings LLC

Summary: Dominion Gas Holdings LLC Primary Credit Analyst: Todd A Shipman, CFA, New York (1) 212-438-7676; todd.shipman@standardandpoors.com Secondary Contact: Dimitri Nikas, New York (1) 212-438-7807;

Summary: Dominion Gas Holdings LLC Primary Credit Analyst: Todd A Shipman, CFA, New York (1) 212-438-7676; todd.shipman@standardandpoors.com Secondary Contact: Dimitri Nikas, New York (1) 212-438-7807;

Pohjola Non-Life Insurance Downgraded To 'A+' After Government Support Review Of Pohjola Bank; Outlook Remains Negative

Research Update: Pohjola Non-Life Insurance Downgraded To 'A+' After Government Support Review Of Pohjola Bank; Outlook Remains Negative Primary Credit Analyst: Anna Glennmar, Stockholm (46) 8-440-5922;

Research Update: Pohjola Non-Life Insurance Downgraded To 'A+' After Government Support Review Of Pohjola Bank; Outlook Remains Negative Primary Credit Analyst: Anna Glennmar, Stockholm (46) 8-440-5922;

Kuwait Projects Co. (Holding) Affirmed At 'BBB-/A-3'; Outlook Stable

Affirmed At 'BBB-/A-3'; Outlook Stable") Research Update: Kuwait Projects Co. (Holding) Affirmed At 'BBB-/A-3'; Outlook Stable Primary Credit Analyst: Per Karlsson, Stockholm (46) 8-440-5927; per.karlsson@standardandpoors.com Secondary Contact:

Research Update: Kuwait Projects Co. (Holding) Affirmed At 'BBB-/A-3'; Outlook Stable Primary Credit Analyst: Per Karlsson, Stockholm (46) 8-440-5927; per.karlsson@standardandpoors.com Secondary Contact:

Income Inequality And State Tax Revenue Trends

Income Inequality And State Tax Revenue Trends Gabe Petek, CFA Managing Director U.S. Public Finance August 2015 Permission to reprint or distribute any content from this presentation requires the prior

Income Inequality And State Tax Revenue Trends Gabe Petek, CFA Managing Director U.S. Public Finance August 2015 Permission to reprint or distribute any content from this presentation requires the prior

Insurer Mapfre Ratings Raised To 'A' On Spain Upgrade; Outlook Stable

Research Update: Insurer Mapfre Ratings Raised To 'A' On Spain Upgrade; Outlook Stable Primary Credit Analyst: Marco Sindaco, London (44) 20-7176-7095; marco.sindaco@standardandpoors.com Secondary Contact:

Research Update: Insurer Mapfre Ratings Raised To 'A' On Spain Upgrade; Outlook Stable Primary Credit Analyst: Marco Sindaco, London (44) 20-7176-7095; marco.sindaco@standardandpoors.com Secondary Contact:

Healthcare Support (North Staffs) Finance Outlook Revised To Stable On Operating Risk; 'BBB-' Issue Ratings Affirmed

Finance Outlook Revised To Stable On Operating Risk; 'BBB-' Issue Ratings Affirmed") Research Update: Healthcare Support (North Staffs) Finance Outlook Revised To Stable On Operating Risk; 'BBB-' Issue Ratings Affirmed Primary Credit Analyst: Manuel Dusina, London (44) 20-7176-5530; manuel.dusina@standardandpoors.com

Research Update: Healthcare Support (North Staffs) Finance Outlook Revised To Stable On Operating Risk; 'BBB-' Issue Ratings Affirmed Primary Credit Analyst: Manuel Dusina, London (44) 20-7176-5530; manuel.dusina@standardandpoors.com

Interactive Brokers LLC

Summary: Interactive Brokers LLC Primary Credit Analyst: Clayton D Montgomery, New York (1) 212-438-5079; clayton.montgomery@standardandpoors.com Secondary Contact: Robert B Hoban, New York (1) 212-438-7385;

Summary: Interactive Brokers LLC Primary Credit Analyst: Clayton D Montgomery, New York (1) 212-438-5079; clayton.montgomery@standardandpoors.com Secondary Contact: Robert B Hoban, New York (1) 212-438-7385;

Polish TV Operator TVN S.A. And Parent Ratings Placed On CreditWatch Positive On Announced Acquisition By Scripps

Research Update: Polish TV Operator TVN S.A. And Parent Ratings Placed On CreditWatch Positive On Announced Acquisition By Scripps Primary Credit Analyst: Florence Devevey, Madrid (34) 91-788-7236; florence.devevey@standardandpoors.com

Research Update: Polish TV Operator TVN S.A. And Parent Ratings Placed On CreditWatch Positive On Announced Acquisition By Scripps Primary Credit Analyst: Florence Devevey, Madrid (34) 91-788-7236; florence.devevey@standardandpoors.com

Denmark-Based Life Insurer Danica Pension Livsforsikringsaktieselskab Rated 'A-'; Outlook Stable

Research Update: Denmark-Based Life Insurer Danica Pension Livsforsikringsaktieselskab Rated 'A-'; Outlook Primary Credit Analyst: Alexander Altinisik, Stockholm (46) 8-440-5902; alexander.altinisik@standardandpoors.com

Research Update: Denmark-Based Life Insurer Danica Pension Livsforsikringsaktieselskab Rated 'A-'; Outlook Primary Credit Analyst: Alexander Altinisik, Stockholm (46) 8-440-5902; alexander.altinisik@standardandpoors.com

Selective Insurance Group Inc. And Operating Companies Ratings Affirmed; Outlook Revised To Negative

Research Update: Selective Insurance Group Inc. And Operating Companies Ratings Affirmed; Outlook Revised To Primary Credit Analyst: David S Veno, New York (1) 212-438-2108; david_veno@standardandpoors.com

Research Update: Selective Insurance Group Inc. And Operating Companies Ratings Affirmed; Outlook Revised To Primary Credit Analyst: David S Veno, New York (1) 212-438-2108; david_veno@standardandpoors.com

Sirius International Group Outlook Revised To Stable On Plans To Retain Its Strategy Post Acquisition; Ratings Affirmed

Research Update: Sirius International Group Outlook Revised To Stable On Plans To Retain Its Strategy Post Acquisition; Ratings Affirmed Primary Credit Analyst: Anvar Gabidullin, CFA, London (44) 20-7176-7047;

Research Update: Sirius International Group Outlook Revised To Stable On Plans To Retain Its Strategy Post Acquisition; Ratings Affirmed Primary Credit Analyst: Anvar Gabidullin, CFA, London (44) 20-7176-7047;

Turkey-Based Appliance Manufacturer Vestel Outlook Revised To Positive; 'B-' Rating Affirmed

Research Update: Turkey-Based Appliance Manufacturer Vestel Outlook Revised To Positive; 'B-' Rating Affirmed Primary Credit Analyst: Alexander Griaznov, Moscow (7) 495-783-4109; alexander.griaznov@standardandpoors.com

Research Update: Turkey-Based Appliance Manufacturer Vestel Outlook Revised To Positive; 'B-' Rating Affirmed Primary Credit Analyst: Alexander Griaznov, Moscow (7) 495-783-4109; alexander.griaznov@standardandpoors.com

Lloyds Banking Group Life Insurance Operations 'A' Ratings Affirmed And Removed From CreditWatch; Outlook Stable

Research Update: Lloyds Banking Group Life Insurance Operations 'A' Ratings Affirmed And Removed From CreditWatch; Outlook Stable Primary Credit Analyst: Oluwatosin S Adesiyan, London (44) 20-7176-3279;

Research Update: Lloyds Banking Group Life Insurance Operations 'A' Ratings Affirmed And Removed From CreditWatch; Outlook Stable Primary Credit Analyst: Oluwatosin S Adesiyan, London (44) 20-7176-3279;

Research Update: Danish Mortgage Bank DLR Kredit A/S Assigned 'BBB+/A-2' Ratings. Table Of Contents

May 31, 2012 Research Update: Danish Mortgage Bank DLR Kredit A/S Assigned 'BBB+/A-2' Ratings Primary Credit Analyst: Per Tornqvist, Stockholm (46) 8-440-5904;per_tornqvist@standardandpoors.com Secondary

May 31, 2012 Research Update: Danish Mortgage Bank DLR Kredit A/S Assigned 'BBB+/A-2' Ratings Primary Credit Analyst: Per Tornqvist, Stockholm (46) 8-440-5904;per_tornqvist@standardandpoors.com Secondary

Lear Corp.'s Recovery Rating Profile

Recovery Report: Lear Corp.'s Recovery Rating Profile Primary Credit Analyst: Lawrence Orlowski, CFA, New York (1) 212-438-1000; lawrence_orlowski@standardandpoors.com Recovery Analyst: Greg Maddock, New

Recovery Report: Lear Corp.'s Recovery Rating Profile Primary Credit Analyst: Lawrence Orlowski, CFA, New York (1) 212-438-1000; lawrence_orlowski@standardandpoors.com Recovery Analyst: Greg Maddock, New

Icelandic Utility Landsvirkjun Outlook Revised To Stable After Similar Action On Iceland; 'BB/B' Ratings Affirmed

Research Update: Icelandic Utility Landsvirkjun Outlook Revised To Stable After Similar Action On Iceland; Primary Credit Analyst: Alf Stenqvist, Stockholm (46) 8-440-5925; alf.stenqvist@standardandpoors.com

Research Update: Icelandic Utility Landsvirkjun Outlook Revised To Stable After Similar Action On Iceland; Primary Credit Analyst: Alf Stenqvist, Stockholm (46) 8-440-5925; alf.stenqvist@standardandpoors.com

Bertelsmann SE & Co. KGaA's Hybrid Equity Content Revised To "Intermediate"; 'BBB+/A-2' Ratings Affirmed

Research Update: Bertelsmann SE & Co. KGaA's Hybrid Equity Content Revised To "Intermediate"; 'BBB+/A-2' Ratings Affirmed Primary Credit Analyst: Florence Devevey, Madrid (34) 91-788-7236; florence.devevey@standardandpoors.com

Research Update: Bertelsmann SE & Co. KGaA's Hybrid Equity Content Revised To "Intermediate"; 'BBB+/A-2' Ratings Affirmed Primary Credit Analyst: Florence Devevey, Madrid (34) 91-788-7236; florence.devevey@standardandpoors.com

Four Ratings Raised From GreatAmerica Leasing Receivables Funding L.L.C.; 10 Ratings Affirmed

Four s Raised From GreatAmerica Leasing Receivables Funding L.L.C.; 10 s Affirmed Primary Credit Analyst: Srabani C Chandra-Lal, New York (1) 212-438-5036; srabani.chandra-lal@standardandpoors.com Secondary

Four s Raised From GreatAmerica Leasing Receivables Funding L.L.C.; 10 s Affirmed Primary Credit Analyst: Srabani C Chandra-Lal, New York (1) 212-438-5036; srabani.chandra-lal@standardandpoors.com Secondary

Asia Insurance Co. Ltd.

Primary Credit Analyst: Eunice Tan, Hong Kong (852) 2533-3553; eunice.tan@standardandpoors.com Secondary Contact: Mark Li, Beijing (861) 6569-2998; mark.haihu.li@standardandpoors.com Table Of Contents

Primary Credit Analyst: Eunice Tan, Hong Kong (852) 2533-3553; eunice.tan@standardandpoors.com Secondary Contact: Mark Li, Beijing (861) 6569-2998; mark.haihu.li@standardandpoors.com Table Of Contents

A Financial Analysis of Energies and Gas Pipelines

Research Update: Interconexion Electrica S.A. E.S.P. (ISA) 'BBB' Credit Rating Affirmed, Outlook Remains Stable Primary Credit Analyst: Maria del Sol S Gonzalez, CFA, New York (1) 212-438-4443; maria.gonzalezcosio@standardandpoors.com

Research Update: Interconexion Electrica S.A. E.S.P. (ISA) 'BBB' Credit Rating Affirmed, Outlook Remains Stable Primary Credit Analyst: Maria del Sol S Gonzalez, CFA, New York (1) 212-438-4443; maria.gonzalezcosio@standardandpoors.com

Workshop B: Credit Spread Trends In The Energy Sector

Workshop B: Credit Spread Trends In The Energy Sector James West Director, FIOTC Product Management 26 November, 2014 Permission to reprint or distribute any content from this presentation requires the

Workshop B: Credit Spread Trends In The Energy Sector James West Director, FIOTC Product Management 26 November, 2014 Permission to reprint or distribute any content from this presentation requires the

SNS REAAL Insurance Operations (SRIO) On Watch Developing After Announced Sale News

On Watch Developing After Announced Sale News") Research Update: SNS REAAL Insurance Operations (SRIO) On Watch Developing After Announced Sale News Primary Credit Analyst: Mark D Nicholson, London (44) 20-7176-7991; mark.nicholson@standardandpoors.com

Research Update: SNS REAAL Insurance Operations (SRIO) On Watch Developing After Announced Sale News Primary Credit Analyst: Mark D Nicholson, London (44) 20-7176-7991; mark.nicholson@standardandpoors.com

Swedbank Outlook Revised To Stable From Negative On Improved Business Position; Ratings Affirmed At 'A+/A-1'

Research Update: Swedbank Outlook Revised To Stable From Negative On Improved Business Position; Ratings Primary Credit Analyst: Alexander Ekbom, Stockholm (46) 8-440-5911; alexander.ekbom@standardandpoors.com

Research Update: Swedbank Outlook Revised To Stable From Negative On Improved Business Position; Ratings Primary Credit Analyst: Alexander Ekbom, Stockholm (46) 8-440-5911; alexander.ekbom@standardandpoors.com

Nationale Borg Group Outlook Revised To Developing On Uncertainties Related To Sale News; 'A-' Ratings Affirmed

Research Update: Nationale Borg Group Outlook Revised To Developing On Uncertainties Related To Sale News; 'A-' Ratings Affirmed Primary Credit Analyst: Thomas Benhamou, London (44) 20-7176-3216; thomas.benhamou@standardandpoors.com

Research Update: Nationale Borg Group Outlook Revised To Developing On Uncertainties Related To Sale News; 'A-' Ratings Affirmed Primary Credit Analyst: Thomas Benhamou, London (44) 20-7176-3216; thomas.benhamou@standardandpoors.com

Market Data Analysis - Pacific Life

Research Update: 'A+', Pacific LifeCorp 'BBB+' Ratings Affirmed; Outlook Stable; New Senior Notes Rated 'BBB+' Primary Credit Analyst: Carmi Margalit, CFA, New York (1) 212-438-1000; carmi_margalit@standardandpoors.com

Research Update: 'A+', Pacific LifeCorp 'BBB+' Ratings Affirmed; Outlook Stable; New Senior Notes Rated 'BBB+' Primary Credit Analyst: Carmi Margalit, CFA, New York (1) 212-438-1000; carmi_margalit@standardandpoors.com

R.V.I. Guaranty Co. Ltd. And Subsidiaries 'BBB' Ratings Affirmed After Insurance Criteria Change; The Outlook Is Stable

Research Update: R.V.I. Guaranty Co. Ltd. And Subsidiaries 'BBB' Ratings Affirmed After Insurance Criteria Change; The Outlook Is Stable Primary Credit Analyst: David S Veno, New York (1) 212-438-2108;

Research Update: R.V.I. Guaranty Co. Ltd. And Subsidiaries 'BBB' Ratings Affirmed After Insurance Criteria Change; The Outlook Is Stable Primary Credit Analyst: David S Veno, New York (1) 212-438-2108;

Danish Bank DLR Kredit Affirmed At 'BBB+/A-2'; Junior Subordinated Debt Downgraded To 'BB'; Outlook Remains Stable

Research Update: Danish Bank DLR Kredit Affirmed At 'BBB+/A-2'; Junior Subordinated Debt Downgraded To 'BB'; Outlook Remains Stable Primary Credit Analyst: Sean Cotten, Stockholm (46) 8-440-5928; sean.cotten@standardandpoors.com

Research Update: Danish Bank DLR Kredit Affirmed At 'BBB+/A-2'; Junior Subordinated Debt Downgraded To 'BB'; Outlook Remains Stable Primary Credit Analyst: Sean Cotten, Stockholm (46) 8-440-5928; sean.cotten@standardandpoors.com

Lloyds Banking Group Life Insurance Operations 'A' Ratings Affirmed; Outlook Negative

Research Update: Lloyds Banking Group Life Insurance Operations 'A' Ratings Affirmed; Outlook Negative Primary Credit Analyst: Oliver Herbert, London (44) 20-7176-7054; oliver.herbert@standardandpoors.com

Research Update: Lloyds Banking Group Life Insurance Operations 'A' Ratings Affirmed; Outlook Negative Primary Credit Analyst: Oliver Herbert, London (44) 20-7176-7054; oliver.herbert@standardandpoors.com

Companhia Energetica de Minas Gerais Upgraded To 'BB+' From 'BB' On Stronger Business Risk Profile, Outlook Stable

Research Update: Companhia Energetica de Minas Gerais Upgraded To 'BB+' From 'BB' On Stronger Business Risk Profile, Outlook Stable Primary Credit Analyst: Alejandro Gomez Abente, Sao Paulo (55) 11-3039-9741;

Research Update: Companhia Energetica de Minas Gerais Upgraded To 'BB+' From 'BB' On Stronger Business Risk Profile, Outlook Stable Primary Credit Analyst: Alejandro Gomez Abente, Sao Paulo (55) 11-3039-9741;

Iceland-Based Non-Life Insurer Tryggingamidstodin Ratings Affirmed at 'BBB-'; Outlook Stable

Research Update: Iceland-Based Non-Life Insurer Tryggingamidstodin Ratings Affirmed at 'BBB-'; Outlook Stable Primary Credit Analyst: Anna Glennmar, Milan (39) 02-72111-252; anna.glennmar@standardandpoors.com

Research Update: Iceland-Based Non-Life Insurer Tryggingamidstodin Ratings Affirmed at 'BBB-'; Outlook Stable Primary Credit Analyst: Anna Glennmar, Milan (39) 02-72111-252; anna.glennmar@standardandpoors.com

Three Spanish Government-Related Entities Upgraded To 'BBB/A-2' Following Similar Sovereign Action; Outlook Stable

Research Update: Three Spanish Government-Related Entities Upgraded To 'BBB/A-2' Following Similar Sovereign Action; Outlook Stable Primary Credit Analysts: Ines Olondriz, Madrid (34) 91-788-7202; ines.olondriz@standardandpoors.com

Research Update: Three Spanish Government-Related Entities Upgraded To 'BBB/A-2' Following Similar Sovereign Action; Outlook Stable Primary Credit Analysts: Ines Olondriz, Madrid (34) 91-788-7202; ines.olondriz@standardandpoors.com

French Social Security Agency ACOSS Short-Term 'A-1+' Rating Affirmed On Integral Link, Critical Role To French State

Research Update: French Social Security Agency ACOSS Short-Term 'A-1+' Rating Affirmed On Integral Link, Critical Role To French State Primary Credit Analyst: Mehdi Fadli, Paris (33) 1-4420-6706; mehdi_fadli@standardandpoors.com

Research Update: French Social Security Agency ACOSS Short-Term 'A-1+' Rating Affirmed On Integral Link, Critical Role To French State Primary Credit Analyst: Mehdi Fadli, Paris (33) 1-4420-6706; mehdi_fadli@standardandpoors.com

Global Energy Group GDF SUEZ's 'A/A-1' Ratings On CreditWatch Negative On Adverse Business Outlook

Research Update: Global Energy Group GDF SUEZ's 'A/A-1' Ratings On CreditWatch Negative On Adverse Business Outlook Primary Credit Analyst: Nicolas Riviere, Paris (33) 1-4420-6709; nicolas_riviere@standardandpoors.com

Research Update: Global Energy Group GDF SUEZ's 'A/A-1' Ratings On CreditWatch Negative On Adverse Business Outlook Primary Credit Analyst: Nicolas Riviere, Paris (33) 1-4420-6709; nicolas_riviere@standardandpoors.com

Dogus Holding 'BB/B' Ratings Affirmed On Sustained Investments And Expected Completion Of Garanti Sale; Outlook Negative

Research Update: Dogus Holding 'BB/B' Ratings Affirmed On Sustained Investments And Expected Completion Of Garanti Sale; Outlook Negative Primary Credit Analyst: Renato Panichi, Milan (39) 02-72111-215;

Research Update: Dogus Holding 'BB/B' Ratings Affirmed On Sustained Investments And Expected Completion Of Garanti Sale; Outlook Negative Primary Credit Analyst: Renato Panichi, Milan (39) 02-72111-215;

Lake Oswego, Oregon; Water/Sewer

Summary: Lake Oswego, Oregon; Water/Sewer Primary Credit Analyst: Aaron Lee, San Francisco (1) 415-371-5066; aaron.lee@standardandpoors.com Secondary Contact: Tim Tung, San Francisco (415) 371-5041; tim.tung@standardandpoors.com

Summary: Lake Oswego, Oregon; Water/Sewer Primary Credit Analyst: Aaron Lee, San Francisco (1) 415-371-5066; aaron.lee@standardandpoors.com Secondary Contact: Tim Tung, San Francisco (415) 371-5041; tim.tung@standardandpoors.com

Six Russian Real Estate Companies On CreditWatch Amid Higher Interest Rates, Weakening Demand, Sharp Ruble Depreciation

Research Update: Six Russian Real Estate Companies On CreditWatch Amid Higher Interest Rates, Weakening Demand, Sharp Ruble Depreciation Primary Credit Analyst: Anton Geyze, Moscow (7) 495-783-4134; anton.geyze@standardandpoors.com

Research Update: Six Russian Real Estate Companies On CreditWatch Amid Higher Interest Rates, Weakening Demand, Sharp Ruble Depreciation Primary Credit Analyst: Anton Geyze, Moscow (7) 495-783-4134; anton.geyze@standardandpoors.com

ASR Nederland NV Assigned 'BBB+' Rating; Ratings On Core Insurance Operations Affirmed; Outlook Stable

Research Update: ASR Nederland NV Assigned 'BBB+' Rating; Ratings On Core Insurance Operations Affirmed; Primary Credit Analyst: Oliver Herbert, London (44) 20-7176-7054; oliver.herbert@standardandpoors.com

Research Update: ASR Nederland NV Assigned 'BBB+' Rating; Ratings On Core Insurance Operations Affirmed; Primary Credit Analyst: Oliver Herbert, London (44) 20-7176-7054; oliver.herbert@standardandpoors.com

Vienna Insurance Group AG Wiener Versicherung Gruppe

Summary: Vienna Insurance Group AG Wiener Versicherung Gruppe Primary Credit Analyst: Johannes Bender, Frankfurt (49) 69-33-999-196; johannes_bender@standardandpoors.com Secondary Contact: Ralf Bender,

Summary: Vienna Insurance Group AG Wiener Versicherung Gruppe Primary Credit Analyst: Johannes Bender, Frankfurt (49) 69-33-999-196; johannes_bender@standardandpoors.com Secondary Contact: Ralf Bender,

Guardian Life Insurance, Core Operating Subsidiaries 'AA+' Ratings Affirmed On Criteria Review, Outlook Negative

Research Update: Guardian Life Insurance, Core Operating Subsidiaries 'AA+' Ratings Affirmed On Criteria Review, Outlook Negative Primary Credit Analyst: Neal I Freedman, New York (1) 212-438-1274; neal.freedman@standardandpoors.com

Research Update: Guardian Life Insurance, Core Operating Subsidiaries 'AA+' Ratings Affirmed On Criteria Review, Outlook Negative Primary Credit Analyst: Neal I Freedman, New York (1) 212-438-1274; neal.freedman@standardandpoors.com

Outlooks On Six Insurance Groups Revised To Stable From Negative After Outlook On U.S. Revised To Stable

Outlooks On Six Insurance Groups Revised To Stable From Negative After Outlook On U.S. Revised To Stable Primary Credit Analyst: Rodney A Clark, FSA, New York (1) 212-438-7245; rodney.clark@standardandpoors.com

Outlooks On Six Insurance Groups Revised To Stable From Negative After Outlook On U.S. Revised To Stable Primary Credit Analyst: Rodney A Clark, FSA, New York (1) 212-438-7245; rodney.clark@standardandpoors.com

Research Update: Russia-Based HMS Hydraulic Machines & Systems Group Assigned 'BB-' Corporate Credit Rating; Outlook Stable.

June 16, 2011 Research Update: Russia-Based HMS Hydraulic Machines & Systems Group Assigned 'BB-' Corporate Credit Primary Credit Analyst: Antoine Cornu, Paris (33) 1-4420-6796;antoine_cornu@standardandpoors.com

June 16, 2011 Research Update: Russia-Based HMS Hydraulic Machines & Systems Group Assigned 'BB-' Corporate Credit Primary Credit Analyst: Antoine Cornu, Paris (33) 1-4420-6796;antoine_cornu@standardandpoors.com

U.K. Broadcaster ITV Upgraded To 'BBB-/A-3' On Expected Solid Credit Metrics, Moderate Financial Policy; Outlook Stable

Research Update: U.K. Broadcaster ITV Upgraded To 'BBB-/A-3' On Expected Solid Credit Metrics, Moderate Financial Policy; Outlook Stable Primary Credit Analyst: Patrizia D'Amico, Milan (39) 02-72111-206;

Research Update: U.K. Broadcaster ITV Upgraded To 'BBB-/A-3' On Expected Solid Credit Metrics, Moderate Financial Policy; Outlook Stable Primary Credit Analyst: Patrizia D'Amico, Milan (39) 02-72111-206;

Belgium-Based Insurance Group Ageas Upgraded To 'A' On Strengthened Financial Risk Profile; Outlook Stable

Research Update: Belgium-Based Insurance Group Ageas Upgraded To 'A' On Strengthened Financial Risk Profile; Primary Credit Analyst: Merryleas J Rousseau, Paris (33) 1-4420-6729; merryleas.rousseau@standardandpoors.com

Research Update: Belgium-Based Insurance Group Ageas Upgraded To 'A' On Strengthened Financial Risk Profile; Primary Credit Analyst: Merryleas J Rousseau, Paris (33) 1-4420-6729; merryleas.rousseau@standardandpoors.com

Research Update: Iceland-Based Utility Landsvirkjun Rating Raised To 'BB+' On Improved Stand-Alone Credit Profile; Outlook Negative.

October 20, 2010 Research Update: Iceland-Based Utility Landsvirkjun Rating Raised To 'BB+' On Improved Stand-Alone Credit Primary Credit Analyst: Andreas Kindahl, Stockholm (46) 8-440-5907;andreas_kindahl@standardandpoors.com

October 20, 2010 Research Update: Iceland-Based Utility Landsvirkjun Rating Raised To 'BB+' On Improved Stand-Alone Credit Primary Credit Analyst: Andreas Kindahl, Stockholm (46) 8-440-5907;andreas_kindahl@standardandpoors.com

Spanish Multi-Cedulas Rating Actions As Of Aug. 2, 2012

Spanish Multi-Cedulas Rating Actions As Of Aug. 2, 2012 Covered Bonds Frankfurt: Karlo S Fuchs, Analytical Manager, Frankfurt (49) 69-33-999-156; karlo_fuchs@standardandpoors.com Covered Bonds London:

Spanish Multi-Cedulas Rating Actions As Of Aug. 2, 2012 Covered Bonds Frankfurt: Karlo S Fuchs, Analytical Manager, Frankfurt (49) 69-33-999-156; karlo_fuchs@standardandpoors.com Covered Bonds London:

SNS REAAL Insurance Operations Ratings Raised To 'A-'; Outlook Negative

Research Update: SNS REAAL Insurance Operations Ratings Raised To 'A-'; Outlook Negative Primary Credit Analyst: Mark D Nicholson, London (44) 20-7176-7991; mark_nicholson@standardandpoors.com Secondary

Research Update: SNS REAAL Insurance Operations Ratings Raised To 'A-'; Outlook Negative Primary Credit Analyst: Mark D Nicholson, London (44) 20-7176-7991; mark_nicholson@standardandpoors.com Secondary

UBI Banca Ratings Lowered To 'BBB-/A-3' On Heightened Economic And Industry Risks In Italy; Outlook Negative

Research Update: UBI Banca Ratings Lowered To 'BBB-/A-3' On Heightened Economic And Industry Risks In Italy; Outlook Negative Analytical Group Contact: Financial Institutions Ratings Europe; FIG_Europe@standardandpoors.com

Research Update: UBI Banca Ratings Lowered To 'BBB-/A-3' On Heightened Economic And Industry Risks In Italy; Outlook Negative Analytical Group Contact: Financial Institutions Ratings Europe; FIG_Europe@standardandpoors.com

Health Care Service Corp. Outlook Revised To Negative From Stable; Ratings Affirmed

Research Update: Health Care Service Corp. Outlook Revised To Negative From Stable; Ratings Affirmed Primary Credit Analyst: Neal I Freedman, New York (1) 212-438-1274; neal.freedman@standardandpoors.com

Research Update: Health Care Service Corp. Outlook Revised To Negative From Stable; Ratings Affirmed Primary Credit Analyst: Neal I Freedman, New York (1) 212-438-1274; neal.freedman@standardandpoors.com

RBS Citizens Financial Group Ratings Affirmed; Outlook Remains Negative; Stand-Alone Credit Profile Lowered To 'a-'

Research Update: RBS Citizens Financial Group Ratings Affirmed; Outlook Remains Negative; Stand-Alone Credit Profile Lowered To 'a-' Primary Credit Analyst: Barbara Duberstein, New York (1) 212-438-5656;

Research Update: RBS Citizens Financial Group Ratings Affirmed; Outlook Remains Negative; Stand-Alone Credit Profile Lowered To 'a-' Primary Credit Analyst: Barbara Duberstein, New York (1) 212-438-5656;

Factory Mutual Insurance Co. And Core Subsidiaries Assigned 'A+' Rating; Outlook Stable

Research Update: Factory Mutual Insurance Co. And Core Subsidiaries Assigned 'A+' Rating; Outlook Stable Primary Credit Analyst: Jeff Pusey, San Francisco (1) 415-371-5016; jeff.pusey@standardandpoors.com

Research Update: Factory Mutual Insurance Co. And Core Subsidiaries Assigned 'A+' Rating; Outlook Stable Primary Credit Analyst: Jeff Pusey, San Francisco (1) 415-371-5016; jeff.pusey@standardandpoors.com

MBIA U.K. Insurance Ltd.

Primary Credit Analyst: David S Veno, Hightstown (1) 212-438-2108; david.veno@standardandpoors.com Secondary Credit Analyst: Olga Ryabaya, New York (1) 212-438-3843; olga.ryabaya@standardandpoors.com Table

Primary Credit Analyst: David S Veno, Hightstown (1) 212-438-2108; david.veno@standardandpoors.com Secondary Credit Analyst: Olga Ryabaya, New York (1) 212-438-3843; olga.ryabaya@standardandpoors.com Table

Evaluating Insurers Enterprise Risk Management Practice

Evaluating Insurers Enterprise Risk Management Practice Li Cheng, CFA, FRM, FSA Director Financial Services Ratings October 3, 2013 Permission to reprint or distribute any content from this presentation

Evaluating Insurers Enterprise Risk Management Practice Li Cheng, CFA, FRM, FSA Director Financial Services Ratings October 3, 2013 Permission to reprint or distribute any content from this presentation

GCC Infrastructure Credit Quality

GCC Infrastructure Credit Quality Karim Nassif Associate Director Corporate and Infrastructure Ratings 18 February 2014 Permission to reprint or distribute any content from this presentation requires the

GCC Infrastructure Credit Quality Karim Nassif Associate Director Corporate and Infrastructure Ratings 18 February 2014 Permission to reprint or distribute any content from this presentation requires the

Duke Energy International Geracao Paranapanema 'BBB-' Global And 'braaa' National Scale Ratings Affirmed

Research Update: Duke Energy International Geracao Paranapanema 'BBB-' Global And 'braaa' National Scale Ratings Affirmed Primary Credit Analyst: Sergio Fuentes, Buenos Aires (54) 114-891-2131; sergio.fuentes@standardandpoors.com

Research Update: Duke Energy International Geracao Paranapanema 'BBB-' Global And 'braaa' National Scale Ratings Affirmed Primary Credit Analyst: Sergio Fuentes, Buenos Aires (54) 114-891-2131; sergio.fuentes@standardandpoors.com

Research Update: Belgian Community of Flanders Outlook Revised To Negative After Same Action On Sovereign; 'AA+' Rating Affirmed.

December 15, 2010 Research Update: Belgian Community of Flanders Outlook Revised To Negative After Same Action On Sovereign; 'AA+' Rating Affirmed Primary Credit Analyst: Bertrand de Dianous, Paris (33)

December 15, 2010 Research Update: Belgian Community of Flanders Outlook Revised To Negative After Same Action On Sovereign; 'AA+' Rating Affirmed Primary Credit Analyst: Bertrand de Dianous, Paris (33)

Long-Term Rating On Heartland Bank Ltd. Raised To 'BBB'; Outlook Negative

Research Update: Long-Term Rating On Heartland Bank Ltd. Raised To 'BBB'; Outlook Negative Primary Credit Analyst: Nico N DeLange, Sydney (61) 2-9255-9887; nico.delange@standardandpoors.com Secondary Contact:

Research Update: Long-Term Rating On Heartland Bank Ltd. Raised To 'BBB'; Outlook Negative Primary Credit Analyst: Nico N DeLange, Sydney (61) 2-9255-9887; nico.delange@standardandpoors.com Secondary Contact:

Research Update: Klabin Ratings Raised To 'BB+' On Improving Financial Profile. Table Of Contents

December 8, 2010 Research Update: Klabin Ratings Raised To 'BB+' On Improving Financial Profile Primary Credit Analyst: Reginaldo Takara, Sao Paulo (55) 11 3039-9740;reginaldo_takara@standardandpoors.com

December 8, 2010 Research Update: Klabin Ratings Raised To 'BB+' On Improving Financial Profile Primary Credit Analyst: Reginaldo Takara, Sao Paulo (55) 11 3039-9740;reginaldo_takara@standardandpoors.com

Constellium Holdco B.V. Recovery Rating Profile

Recovery Report: Constellium Holdco B.V. Recovery Rating Profile Recovery Analyst: Franck Rizzoli, London (44) 20-7176-3934; Franck_Rizzoli@standardandpoors.com Primary Credit Analyst: Tatjana Lescova,

Recovery Report: Constellium Holdco B.V. Recovery Rating Profile Recovery Analyst: Franck Rizzoli, London (44) 20-7176-3934; Franck_Rizzoli@standardandpoors.com Primary Credit Analyst: Tatjana Lescova,

Sul America Upgraded To 'BBB-' And Sul America Companhia Nacional de Seguros To 'BBB+' Under New Criteria Review

Research Update: Sul America Upgraded To 'BBB-' And Sul America Companhia Nacional de Seguros To 'BBB+' Under New Criteria Review Primary Credit Analyst: Suzane M Iamamoto, Sao Paulo (55) 11-3039-9728;

Research Update: Sul America Upgraded To 'BBB-' And Sul America Companhia Nacional de Seguros To 'BBB+' Under New Criteria Review Primary Credit Analyst: Suzane M Iamamoto, Sao Paulo (55) 11-3039-9728;

Swedish Housing Company Willhem Affirmed At 'A-/A-2'; Outlook Stable

Research Update: Swedish Housing Company Willhem Affirmed At 'A-/A-2'; Outlook Stable Primary Credit Analyst: Carl Nyrerod, Stockholm (46) 8-440-5919; carl.nyrerod@standardandpoors.com Secondary Contact:

Research Update: Swedish Housing Company Willhem Affirmed At 'A-/A-2'; Outlook Stable Primary Credit Analyst: Carl Nyrerod, Stockholm (46) 8-440-5919; carl.nyrerod@standardandpoors.com Secondary Contact:

New York Life Insurance Co. 'AA+/A-1+' Rating Affirmed On Criteria Review; Outlook Stable

Research Update: New York Life Insurance Co. 'AA+/A-1+' Rating Affirmed On Criteria Review; Outlook Stable Primary Credit Analyst: Michael E Gross, San Francisco (1) 415-371-5003; michael.gross@standardandpoors.com

Research Update: New York Life Insurance Co. 'AA+/A-1+' Rating Affirmed On Criteria Review; Outlook Stable Primary Credit Analyst: Michael E Gross, San Francisco (1) 415-371-5003; michael.gross@standardandpoors.com

Volkswagen Bank Ratings Lowered To 'A-/A-2'; Outlook Negative

Research Update: Volkswagen Bank Ratings Lowered To 'A-/A-2'; Outlook Negative Primary Credit Analyst: Salla von Steinaecker, Frankfurt (49) 69-33-999-164; salla.vonsteinaecker@standardandpoors.com Secondary

Research Update: Volkswagen Bank Ratings Lowered To 'A-/A-2'; Outlook Negative Primary Credit Analyst: Salla von Steinaecker, Frankfurt (49) 69-33-999-164; salla.vonsteinaecker@standardandpoors.com Secondary

Business Development Bank of Canada 'AAA' Rating Affirmed On Continuing Federal Government Support

Research Update: Business Development Bank of Canada 'AAA' Rating Affirmed On Continuing Federal Government Support Primary Credit Analyst: Bhavini Patel, CFA, Toronto (1) 416-507-2558; bhavini.patel@standardandpoors.com

Research Update: Business Development Bank of Canada 'AAA' Rating Affirmed On Continuing Federal Government Support Primary Credit Analyst: Bhavini Patel, CFA, Toronto (1) 416-507-2558; bhavini.patel@standardandpoors.com

Molibdenos y Metales 'BBB-' Rating Affirmed On Improving Leverage, Outlook Still Stable

Research Update: Molibdenos y Metales 'BBB-' Rating Affirmed On Improving Leverage, Outlook Still Stable Primary Credit Analyst: Diego H Ocampo, Buenos Aires (54) 114-891-2124; diego.ocampo@standardandpoors.com

Research Update: Molibdenos y Metales 'BBB-' Rating Affirmed On Improving Leverage, Outlook Still Stable Primary Credit Analyst: Diego H Ocampo, Buenos Aires (54) 114-891-2124; diego.ocampo@standardandpoors.com

Research Update: PRI Pensionsgaranti Mutual Insurance Company Assigned 'A' Ratings; Outlook Stable. Table Of Contents

December 8, 2010 Research Update: PRI Pensionsgaranti Mutual Insurance Company Assigned 'A' Ratings; Outlook Stable Primary Credit Analyst: Anna Glennmar, Milan (39) 02-72111252;anna_glennmar@standardandpoors.com

December 8, 2010 Research Update: PRI Pensionsgaranti Mutual Insurance Company Assigned 'A' Ratings; Outlook Stable Primary Credit Analyst: Anna Glennmar, Milan (39) 02-72111252;anna_glennmar@standardandpoors.com

NorthStar Education Finance Inc. Series 2006-A Ratings Affirmed

NorthStar Education Finance Inc. Series 2006-A Ratings Affirmed Primary Credit Analyst: Ronald G Burt, New York (1) 212-438-4011; ronald.burt@standardandpoors.com Analytical Manager--Term ABS: Frank J

NorthStar Education Finance Inc. Series 2006-A Ratings Affirmed Primary Credit Analyst: Ronald G Burt, New York (1) 212-438-4011; ronald.burt@standardandpoors.com Analytical Manager--Term ABS: Frank J

Covea Group Core And Guaranteed Companies Outlooks Revised To Positive; 'A' Ratings Affirmed

Research Update: Covea Group Core And Guaranteed Companies Outlooks Revised To Positive; 'A' Ratings Affirmed Primary Credit Analyst: David D Anthony, London (44) 20-7176-7010; david.anthony@standardandpoors.com

Research Update: Covea Group Core And Guaranteed Companies Outlooks Revised To Positive; 'A' Ratings Affirmed Primary Credit Analyst: David D Anthony, London (44) 20-7176-7010; david.anthony@standardandpoors.com

Research Update: Ratings Lowered On Netherlands-Based SNS REAAL N.V. Group And Core Subs On Slower Recovery Prospects; Outlook Stable

March 1, 2012 Research Update: Ratings Lowered On Netherlands-Based SNS REAAL N.V. Group And Core Subs On Slower Recovery Prospects; Outlook Stable Primary Credit Analysts: Alexandre Birry, London 44 (0)

March 1, 2012 Research Update: Ratings Lowered On Netherlands-Based SNS REAAL N.V. Group And Core Subs On Slower Recovery Prospects; Outlook Stable Primary Credit Analysts: Alexandre Birry, London 44 (0)

Millenniumbcp Ageas Core Non-Life Insurance Entity 'BB' Ratings On CreditWatch Positive On Announced Ownership Change

Research Update: Millenniumbcp Ageas Core Non-Life Insurance Entity 'BB' Ratings On CreditWatch Positive On Announced Ownership Change Primary Credit Analyst: Gwenaelle Gibert, Paris (33) 1-4420-6693;

Research Update: Millenniumbcp Ageas Core Non-Life Insurance Entity 'BB' Ratings On CreditWatch Positive On Announced Ownership Change Primary Credit Analyst: Gwenaelle Gibert, Paris (33) 1-4420-6693;

Methodology: Business Risk/Financial Risk Matrix Expanded

Criteria Corporates General: Methodology: Business Risk/Financial Risk Matrix Expanded Criteria Officer: Mark Puccia, Managing Director, New York (1) 212-438-7233; mark.puccia@standardandpoors.com Table

Criteria Corporates General: Methodology: Business Risk/Financial Risk Matrix Expanded Criteria Officer: Mark Puccia, Managing Director, New York (1) 212-438-7233; mark.puccia@standardandpoors.com Table

How To Rate Spain

April 28, 2010 Research Update: Spain Downgraded To 'AA' On Protracted Economic Adjustment And Risks To Budgetary Position; Outlook Negative Primary Credit Analyst: Marko Mrsnik, Madrid +34 913 896 953;marko_mrsnik@standardandpoors.com

April 28, 2010 Research Update: Spain Downgraded To 'AA' On Protracted Economic Adjustment And Risks To Budgetary Position; Outlook Negative Primary Credit Analyst: Marko Mrsnik, Madrid +34 913 896 953;marko_mrsnik@standardandpoors.com

FWD Life Insurance Co. (Bermuda) Ltd. Assigned 'A-' And 'cnaa' Ratings; Outlook Stable

Ltd. Assigned 'A-' And 'cnaa' Ratings; Outlook Stable") Research Update: FWD Life Insurance Co. (Bermuda) Ltd. Assigned 'A-' And 'cnaa' Ratings; Outlook Stable Primary Credit Analyst: Anna Kong, FSA, FRM, Hong Kong (852) 2533-3571; anna.kong@standardandpoors.com

Research Update: FWD Life Insurance Co. (Bermuda) Ltd. Assigned 'A-' And 'cnaa' Ratings; Outlook Stable Primary Credit Analyst: Anna Kong, FSA, FRM, Hong Kong (852) 2533-3571; anna.kong@standardandpoors.com

Research Update: Ratings On The Republic Of Iceland Placed On Watch Negative After The Electorate Rejects Icesave Agreement A Second Time

April 13, 2011 Research Update: Ratings On The Republic Of Iceland Placed On Watch Negative After The Electorate Rejects Icesave Agreement A Second Time Primary Credit Analyst: Eileen X Zhang, CFA, London

April 13, 2011 Research Update: Ratings On The Republic Of Iceland Placed On Watch Negative After The Electorate Rejects Icesave Agreement A Second Time Primary Credit Analyst: Eileen X Zhang, CFA, London

China Life Insurance Co. Ltd.

Primary Credit Analyst: Connie Wong, Singapore (65) 6239-6353; connie_wong@standardandpoors.com Secondary Contact: Philip P Chung, CFA, Singapore (65) 6239-6343; philip_chung@standardandpoors.com Table

Primary Credit Analyst: Connie Wong, Singapore (65) 6239-6353; connie_wong@standardandpoors.com Secondary Contact: Philip P Chung, CFA, Singapore (65) 6239-6343; philip_chung@standardandpoors.com Table

Research Update: Banco Monex S.A. Rated Global Scale 'BB+/B', National Scale 'mxa+/mxa-1' Rating Affirmed. Table Of Contents

May 17, 2012 Research Update: Banco Monex S.A. Rated Global Scale 'BB+/B', National Scale 'mxa+/mxa-1' Rating Affirmed Primary Credit Analyst: Arturo Sanchez, Mexico City (52) 55-5081-4468;arturo_sanchez@standardandpoors.com

May 17, 2012 Research Update: Banco Monex S.A. Rated Global Scale 'BB+/B', National Scale 'mxa+/mxa-1' Rating Affirmed Primary Credit Analyst: Arturo Sanchez, Mexico City (52) 55-5081-4468;arturo_sanchez@standardandpoors.com

Codelco Rating Outlook Revised To Negative On Lower Copper Prices, 'AA-' Rating Affirmed

Research Update: Codelco Rating Outlook Revised To Negative On Lower Copper Prices, 'AA-' Rating Affirmed Primary Credit Analyst: Diego H Ocampo, Sao Paulo (55) 11-3039-9769; diego.ocampo@standardandpoors.com

Research Update: Codelco Rating Outlook Revised To Negative On Lower Copper Prices, 'AA-' Rating Affirmed Primary Credit Analyst: Diego H Ocampo, Sao Paulo (55) 11-3039-9769; diego.ocampo@standardandpoors.com

Russia-Based EvrazHolding Finance And Sibmetinvest Rated 'B+', Unsecured Notes Rated 'B+'; Outlook Stable

November 24, 2011 Russia-Based EvrazHolding Finance And Sibmetinvest Rated 'B+', Unsecured Notes Rated 'B+'; Outlook Stable Primary Credit Analyst: Andrey Nikolaev, Paris (33) 1-4420-7329; andrey_nikolaev@standardandpoors.com

November 24, 2011 Russia-Based EvrazHolding Finance And Sibmetinvest Rated 'B+', Unsecured Notes Rated 'B+'; Outlook Stable Primary Credit Analyst: Andrey Nikolaev, Paris (33) 1-4420-7329; andrey_nikolaev@standardandpoors.com

Italian Construction Company Salini Impregilo Upgraded To 'BB+' On Strong Credit Ratios; Outlook Stable

Research Update: Italian Construction Company Salini Impregilo Upgraded To 'BB+' On Strong Credit Ratios; Primary Credit Analyst: Vincent Gusdorf, CFA, Paris (33) 1-4420-6667; vincent.gusdorf@standardandpoors.com

Research Update: Italian Construction Company Salini Impregilo Upgraded To 'BB+' On Strong Credit Ratios; Primary Credit Analyst: Vincent Gusdorf, CFA, Paris (33) 1-4420-6667; vincent.gusdorf@standardandpoors.com

Standard & Poor's Base-Case Scenario. Related Criteria And Research

Summary: Valeo S.A. Primary Credit Analyst: Vincent Gusdorf, CFA, Paris (33) 1-4420-6667; vincent.gusdorf@standardandpoors.com Secondary Contact: Barbara Castellano, Milan (39) 02-72111-253; barbara.castellano@standardandpoors.com

Summary: Valeo S.A. Primary Credit Analyst: Vincent Gusdorf, CFA, Paris (33) 1-4420-6667; vincent.gusdorf@standardandpoors.com Secondary Contact: Barbara Castellano, Milan (39) 02-72111-253; barbara.castellano@standardandpoors.com

Cook County Community College District No. 508 (City Colleges of Chicago). Illinois; General Obligation

. Illinois; General Obligation") Summary: Cook County Community College District No. 508 (City Colleges of Chicago). Illinois; General Primary Credit Analyst: John A Kenward, Chicago (1) 312-233-7003; john.kenward@standardandpoors.com

Summary: Cook County Community College District No. 508 (City Colleges of Chicago). Illinois; General Primary Credit Analyst: John A Kenward, Chicago (1) 312-233-7003; john.kenward@standardandpoors.com

South Padre Island, Texas; General Obligation

Summary: South Padre Island, Texas; General Obligation Primary Credit Analyst: Jim Tchou, New York (1) 212-438-3821; jim.tchou@standardandpoors.com Secondary Contact: Sarah L Smaardyk, Dallas (1) 214-871-1428;

Summary: South Padre Island, Texas; General Obligation Primary Credit Analyst: Jim Tchou, New York (1) 212-438-3821; jim.tchou@standardandpoors.com Secondary Contact: Sarah L Smaardyk, Dallas (1) 214-871-1428;

Italian Veneto Banca 'BB/B' Ratings Affirmed And Removed From CreditWatch Negative Following Review; Outlook Negative

Research Update: Italian Veneto Banca 'BB/B' Ratings Affirmed And Removed From CreditWatch Negative Following Review; Outlook Negative Table Of Contents Overview Rating Action Rationale Outlook Ratings

Research Update: Italian Veneto Banca 'BB/B' Ratings Affirmed And Removed From CreditWatch Negative Following Review; Outlook Negative Table Of Contents Overview Rating Action Rationale Outlook Ratings

Islamic Development Bank 'AAA/A-1+' Ratings Affirmed On Criteria Revision; Outlook Stable

Research Update: Islamic Development Bank 'AAA/A-1+' Ratings Affirmed On Criteria Revision; Outlook Stable Primary Credit Analyst: Dima B Jardaneh, Dubai (971) 4-372-7154; Dima_Jardaneh@standardandpoors.com

Research Update: Islamic Development Bank 'AAA/A-1+' Ratings Affirmed On Criteria Revision; Outlook Stable Primary Credit Analyst: Dima B Jardaneh, Dubai (971) 4-372-7154; Dima_Jardaneh@standardandpoors.com

S&P Takes Rating Actions On Section 15 Bonds Issued By Various Danish Mortgage Banks

S&P Takes Rating Actions On Section 15 Bonds Issued By Various Danish Mortgage Banks Primary Credit Analyst: Casper R Andersen, London (44) 20-7176-6757; casper.andersen@standardandpoors.com Secondary

S&P Takes Rating Actions On Section 15 Bonds Issued By Various Danish Mortgage Banks Primary Credit Analyst: Casper R Andersen, London (44) 20-7176-6757; casper.andersen@standardandpoors.com Secondary

Summary: Svenska Cellulosa Aktiebolaget SCA. Table Of Contents. Rationale Outlook Related Criteria And Research. May 28, 2012

May 28, 2012 Summary: Svenska Cellulosa Aktiebolaget SCA Primary Credit Analyst: Gustav Liedgren, Stockholm (46) 8-440-5916; gustav_liedgren@standardandpoors.com Secondary Contact: Dionisio Luiz, London

May 28, 2012 Summary: Svenska Cellulosa Aktiebolaget SCA Primary Credit Analyst: Gustav Liedgren, Stockholm (46) 8-440-5916; gustav_liedgren@standardandpoors.com Secondary Contact: Dionisio Luiz, London

Stand-Alone Credit Profiles: One Component Of A Rating

General Criteria: Stand-Alone Credit Profiles: One Component Of A Rating Criteria Officer, EMEA Corporates: Emmanuel Dubois-Pelerin, Paris (33) 1-4420-6673; emmanuel.dubois-pelerin@standardandpoors.com

General Criteria: Stand-Alone Credit Profiles: One Component Of A Rating Criteria Officer, EMEA Corporates: Emmanuel Dubois-Pelerin, Paris (33) 1-4420-6673; emmanuel.dubois-pelerin@standardandpoors.com

Economic Research: Spain's Housing Market May Need Four More Years To Rebalance. Table Of Contents

June 14, 2012 Economic Research: Spain's Housing Market May Need Four More Years To Rebalance Credit Market Services: Jean-Michel Six, EMEA Chief Economist, Paris (33) 1-4420-6705; jean-michel_six@standardandpoors.com

June 14, 2012 Economic Research: Spain's Housing Market May Need Four More Years To Rebalance Credit Market Services: Jean-Michel Six, EMEA Chief Economist, Paris (33) 1-4420-6705; jean-michel_six@standardandpoors.com

Espírito Santo Centrais Elétricas S.A. 'BB+' Global Scale And 'braa+' National Scale Ratings Affirmed, Outlook Stable

Research Update: Espírito Santo Centrais Elétricas S.A. 'BB+' Global Scale And 'braa+' National Scale Ratings Affirmed, Outlook Stable Primary Credit Analyst: Alejandro Gomez Abente, Sao Paulo (55) 11-3039-9741;

Research Update: Espírito Santo Centrais Elétricas S.A. 'BB+' Global Scale And 'braa+' National Scale Ratings Affirmed, Outlook Stable Primary Credit Analyst: Alejandro Gomez Abente, Sao Paulo (55) 11-3039-9741;

Avianca Holdings Outlook Revised To Stable From Positive, 'B+' Credit Rating Affirmed On Weaker Credit Metrics

Research Update: Avianca Holdings Outlook Revised To Stable From Positive, 'B+' Credit Rating Affirmed On Weaker Credit Metrics Primary Credit Analyst: Francisco Gutierrez, Mexico City (52) 55-5081-4407;

Research Update: Avianca Holdings Outlook Revised To Stable From Positive, 'B+' Credit Rating Affirmed On Weaker Credit Metrics Primary Credit Analyst: Francisco Gutierrez, Mexico City (52) 55-5081-4407;

Tri-Township Consolidated School Building Corp., Indiana Tri-Township Consolidate School Corp.; School State Program

Summary: Tri-Township Consolidated School Building Corp., Indiana Tri-Township Consolidate School Corp.; School State Program Primary Credit Analyst: Ryan Schultz, Chicago (1) 312-233-7066; ryan.schultz@standardandpoors.com

Summary: Tri-Township Consolidated School Building Corp., Indiana Tri-Township Consolidate School Corp.; School State Program Primary Credit Analyst: Ryan Schultz, Chicago (1) 312-233-7066; ryan.schultz@standardandpoors.com

Four Subsidiaries Of Covea Assigned Ratings On High Integration Within Group; Outlook Stable

Research Update: Four Subsidiaries Of Covea Assigned Ratings On High Integration Within Group; Outlook Stable Primary Credit Analyst: Gwenaelle Gibert, Paris (33) 1-4420-6693; gwenaelle.gibert@standardandpoors.com

Research Update: Four Subsidiaries Of Covea Assigned Ratings On High Integration Within Group; Outlook Stable Primary Credit Analyst: Gwenaelle Gibert, Paris (33) 1-4420-6693; gwenaelle.gibert@standardandpoors.com