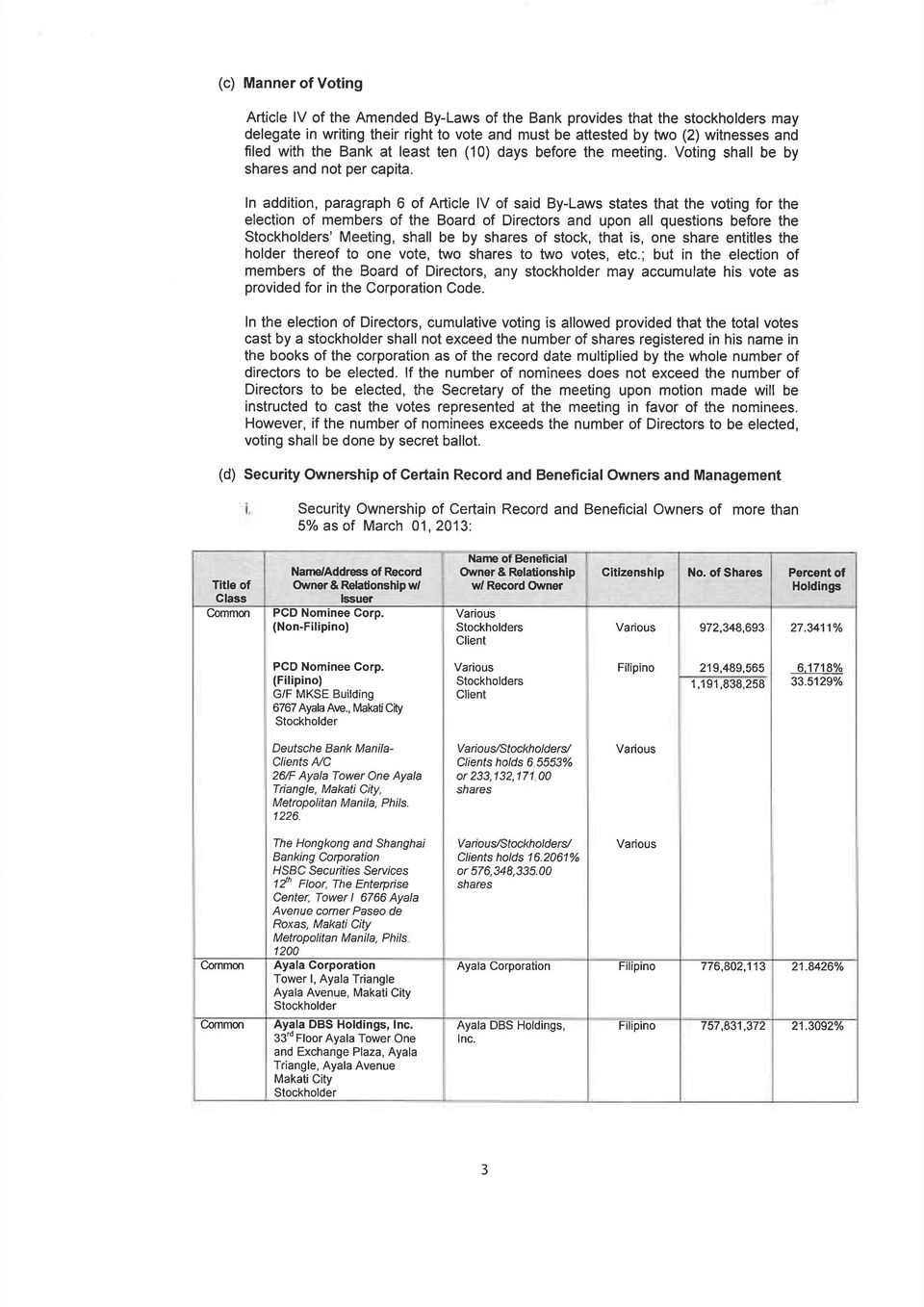

|

|

|

- Stephen Woods

- 7 years ago

- Views:

Transcription

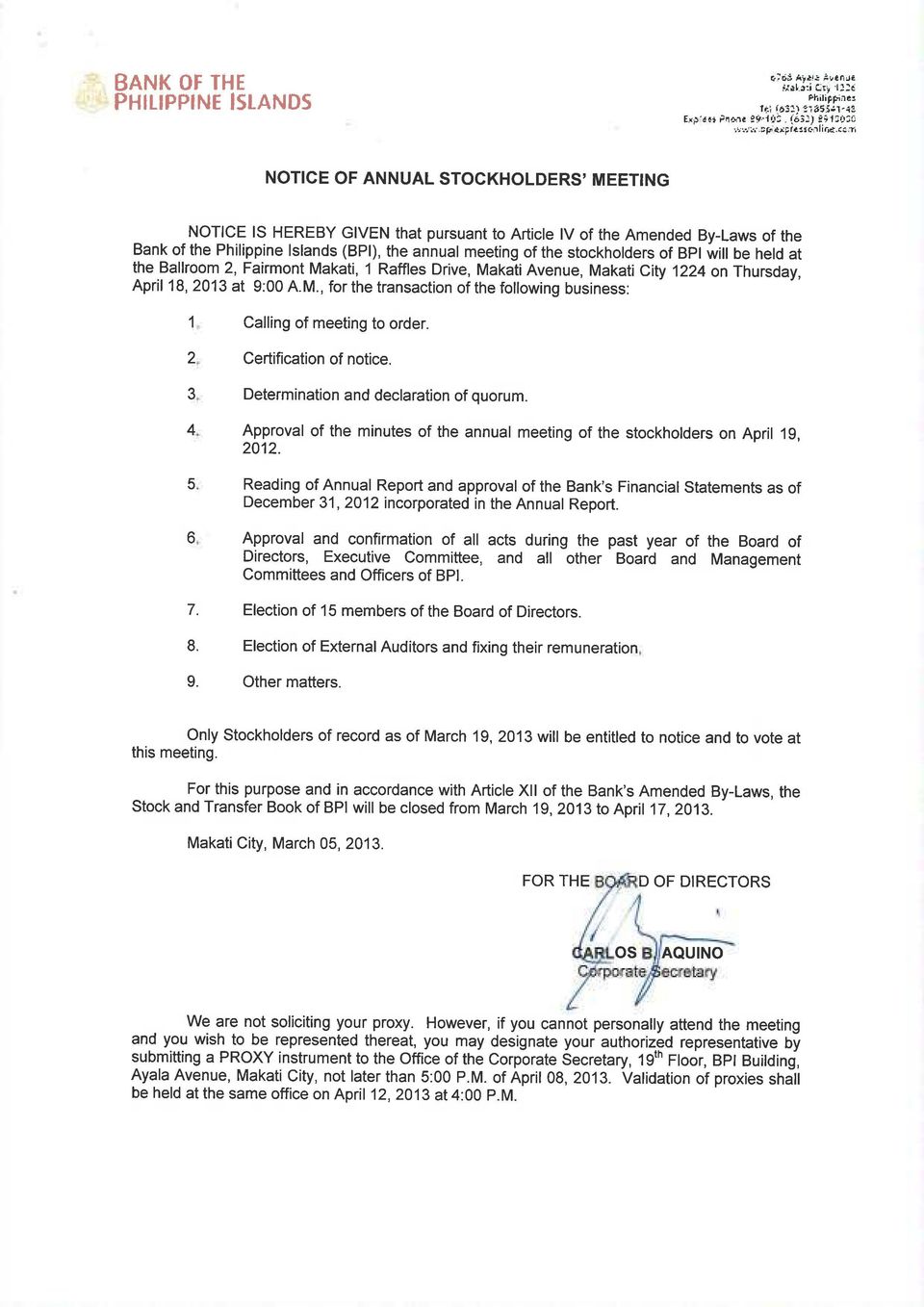

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40 BANK OF THE PHILIPPINE ISLANDS STATEMENTS OF CONDITION DECEMBER 31, 2012 AND 2011 Consolidated Parent Notes R E S O U R C E S CASH AND OTHER CASH ITEMS 7 23,293 22,395 22,518 21,661 DUE FROM BANGKO SENTRAL NG PILIPINAS 7 119,079 83, ,244 70,807 DUE FROM OTHER BANKS 7 7,582 9,297 4,724 5,567 INTERBANK LOANS RECEIVABLE AND SECURITIES PURCHASED UNDER AGREEMENTS TO RESELL 7, 8 38,927 35,277 10,843 24,867 FINANCIAL ASSETS AT FAIR VALUE THROUGH PROFIT OR LOSS - DERIVATIVE FINANCIAL ASSETS 9 5,920 5,389 5,920 5,389 - TRADING SECURITIES 10 22,098 12,275 19,055 11,638 AVAILABLE-FOR-SALE SECURITIES, net ,403 74,084 92,845 64,500 HELD-TO-MATURITY SECURITIES, net 12 76,243 89,742 67,822 79,723 LOANS AND ADVANCES, net , , , ,425 ASSETS HELD FOR SALE, net 6,887 9,148 4,380 6,431 BANK PREMISES, FURNITURE, FIXTURES AND EQUIPMENT, net 14 12,421 12,322 8,101 8,199 INVESTMENT PROPERTIES, net 15 2,582 2,637 2,575 2,630 INVESTMENTS IN SUBSIDIARIES AND ASSOCIATES, net 16 3,680 3,069 7,088 7,008 ASSETS ATTRIBUTABLE TO INSURANCE OPERATIONS 5, 7 13,451 12, DEFERRED INCOME TAX ASSETS, net 17 4,915 4,335 3,421 2,958 OTHER RESOURCES, net 18 14,948 12,148 10,929 8,099 Total resources 985, , , ,902 (forward)

41 BANK OF THE PHILIPPINE ISLANDS STATEMENTS OF CONDITION DECEMBER 31, 2012 AND 2011 Consolidated Parent Notes LIABILITIES AND CAPITAL FUNDS DEPOSIT LIABILITIES , , , ,414 DERIVATIVE FINANCIAL LIABILITIES 9 5,827 4,814 5,827 4,814 BILLS PAYABLE 20 26,280 19,136 16,963 9,887 DUE TO BANGKO SENTRAL NG PILIPINAS AND OTHER BANKS 2,035 1,717 2,036 1,717 MANAGER S CHECKS AND DEMAND DRAFTS OUTSTANDING 5,794 4,131 4,508 3,389 ACCRUED TAXES, INTEREST AND OTHER EXPENSES 4,819 4,025 3,456 2,709 UNSECURED SUBORDINATED DEBT 21 5,000 5,000 5,000 5,000 LIABILITIES ATTRIBUTABLE TO INSURANCE OPERATIONS 5 10,793 9, DEFERRED CREDITS AND OTHER LIABILITIES 22 23,725 22,225 19,216 18,569 Total liabilities 886, , , ,499 CAPITAL FUNDS ATTRIBUTABLE TO THE EQUITY HOLDERS OF BPI 23 Share capital 35,562 35,562 35,562 35,562 Share premium 8,317 8,317 8,317 8,317 Reserves 1,603 1,462 1,603 1,462 Surplus 49,613 41,643 23,932 19,870 Accumulated other comprehensive income 2,000 2, ,192 97,095 89,152 70,056 66,403 NON-CONTROLLING INTERESTS 1,427 1, Total capital funds 98,522 90,530 70,056 66,403 Total liabilities and capital funds 985, , , ,902 (The notes on pages 1 to 96 are an integral part of these financial statements.)

42 BANK OF THE PHILIPPINE ISLANDS STATEMENTS OF INCOME FOR EACH OF THE THREE YEARS IN THE PERIOD ENDED DECEMBER 31, 2012 (In Millions of Pesos, Except Per Share Amounts) Consolidated Parent Notes INTEREST INCOME On loans and advances 30,790 27,156 25,270 19,356 16,762 15,944 On held-to-maturity securities 5,191 6,023 5,787 4,638 5,383 5,017 On available-for-sale securities 3,424 3,592 3,333 3,126 3,374 3,113 On deposits with BSP and other banks 1,229 2,488 3, ,001 2,952 On trading securities Gross receipts tax (1,373) (1,382) (1,394) (963) (1,009) (1,063) 40,108 38,689 36,987 27,622 27,278 26,502 INTEREST EXPENSE On deposits 19 11,648 11,721 12,069 6,929 7,601 8,081 On bills payable and other borrowings 20, 21 1,007 1,102 1, ,655 12,823 13,359 7,517 8,269 9,052 NET INTEREST INCOME 27,453 25,866 23,628 20,105 19,009 17,450 IMPAIRMENT LOSSES 11, 13, 18 2,923 2,150 3,454 2,003 1,583 2,165 NET INTEREST INCOME AFTER IMPAIRMENT LOSSES 24,530 23,716 20,174 18,102 17,426 15,285 OTHER INCOME Trading gain on securities 5,908 2,948 2,946 4,717 2,712 2,652 Fees and commissions 5,111 4,607 4,160 4,256 3,777 2,834 Income from foreign exchange trading 1,682 1,770 2,204 1,372 1,596 2,089 Income attributable to insurance operations Other operating income 25 7,878 6,688 5,825 6,771 5,917 4,430 Gross receipts tax (1,342) (1,070) (1,158) (1,122) (943) (1,039) 19,931 15,892 14,779 15,994 13,059 10,966 OTHER EXPENSES Compensation and fringe benefits 27 10,556 10,379 9,137 8,326 7,994 6,664 Occupancy and equipment-related expenses 14, 15, 26 7,193 6,476 6,083 5,798 5,080 4,714 Other operating expenses 27 7,139 6,610 5,734 5,377 5,296 4,407 24,888 23,465 20,954 19,501 18,370 15,785 INCOME BEFORE INCOME TAX 19,573 16,143 13,999 14,595 12,115 10,466 PROVISION FOR INCOME TAX Current Deferred ,576 (444) 3,570 (440) 2,866 (346) 2,444 (232) 2,556 (297) 3,132 3,130 2,520 2,212 2,259 2,160 NET INCOME FOR THE YEAR 16,441 13,013 11,479 12,383 9,856 8,306 Attributable to: Equity holders of BPI 16,291 12,822 11,312 12,383 9,856 8,306 Non-controlling interests ,441 13,013 11,479 12,383 9,856 8,306 Earnings per share for net income attributable to the equity holders of BPI during the year: Basic and diluted (The notes on pages 1 to 96 are an integral part of these financial statements.) 2,

43 BANK OF THE PHILIPPINE ISLANDS STATEMENTS OF TOTAL COMPREHENSIVE INCOME FOR EACH OF THE THREE YEARS IN THE PERIOD ENDED DECEMBER 31, 2012 Consolidated Parent Note NET INCOME FOR THE YEAR 16,441 13,013 11,479 12,383 9,856 8,306 OTHER COMPREHENSIVE INCOME 23 Net change in fair value reserve on available-for-sale securities, net of tax effect (718) 1,420 1,207 (550) 1,495 1,021 Fair value reserve on investments of insurance subsidiaries, net of tax effect 161 (63) Share in other comprehensive income of associates Currency translation differences (104) (5) (215) Total other comprehensive (loss) income, net of tax effect (159) 1,703 2,145 (550) 1,495 1,021 TOTAL COMPREHENSIVE INCOME FOR THE YEAR 16,282 14,716 13,624 11,833 11,351 9,327 Attributable to: Equity holders of BPI 16,123 14,523 13,414 11,833 11,351 9,327 Non-controlling interests ,282 14,716 13,624 11,833 11,351 9,327 (The notes on pages 1 to 96 are an integral part of these financial statements.)

44 BANK OF THE PHILIPPINE ISLANDS STATEMENTS OF CHANGES IN CAPITAL FUNDS FOR EACH OF THE THREE YEARS IN THE PERIOD ENDED DECEMBER 31, 2012 Consolidated Attributable to equity holders of BPI (Note 23) Accumulated Share capital Share premium Reserves Surplus other comprehensive income (loss) Total Noncontrolling interests Total equity Balance, January 1, ,467 1,412 1,394 33,160 (1,635) 66, ,765 Comprehensive income Net income for the year ,312-11, ,479 Other comprehensive income for the year ,102 2, ,145 Total comprehensive income for the year ,312 2,102 13, ,624 Transactions with owners Issuance of shares 3,077 6, ,906-9,906 Employee stock option plan: Exercise of options (137) - - (43) - (43) Cash dividends (9,044) - (9,044) - (9,044) Transfer from surplus to reserves (110) Other changes in non-controlling interests Total transactions with owners 3,095 6,905 (27) (9,154) Balance, December 31, ,562 8,317 1,367 35, ,031 1,244 82,275 Comprehensive income Net income for the year ,822-12, ,013 Other comprehensive income for the year ,701 1, ,703 Total comprehensive income for the year ,822 1,701 14, ,716 Transactions with owners Issuance of shares Employee stock option plan: Expiration of options - - (42) Cash dividends (6,402) - (6,402) - (6,402) Transfer from surplus to reserves (137) Other changes in non-controlling interests (59) (59) Total transactions with owners (6,497) - (6,402) (59) (6,461) Balance, December 31, ,562 8,317 1,462 41,643 2,168 89,152 1,378 90,530 Comprehensive income Net income for the year ,291-16, ,441 Other comprehensive loss for the year (168) (168) 9 (159) Total comprehensive income (loss) for the year ,291 (168) 16, ,282 Transactions with owners Issuance of shares Employee stock option plan: Expiration of options Cash dividends (8,180) - (8,180) - (8,180) Transfer from surplus to reserves (141) Other changes in non-controlling interests (110) (110) Total transactions with owners (8,321) - (8,180) (110) (8,290) Balance, December 31, ,562 8,317 1,603 49,613 2,000 97,095 1,427 98,522 (The notes on pages 1 to 96 are an integral part of these financial statements.)

45 BANK OF THE PHILIPPINE ISLANDS STATEMENTS OF CHANGES IN CAPITAL FUNDS FOR EACH OF THE THREE YEARS IN THE PERIOD ENDED DECEMBER 31, 2012 Parent (Note 23) Share capital Share premium Reserves Surplus Accumulated other comprehensive income (loss) Total Balance, January 1, ,467 1,412 1,351 17,390 (1,324) 51,296 Comprehensive income Net income for the year ,306-8,306 Other comprehensive income for the year ,021 1,021 Total comprehensive income for the year ,306 1,021 9,327 Transactions with owners Issuance of shares 3,077 6, ,906 Employee stock option plan: Exercise of options (125) - - (31) Cash dividends (9,044) - (9,044) Transfer from surplus to reserves (110) - - Total transactions with owners 3,095 6,905 (15) (9,154) Balance, December 31, ,562 8,317 1,336 16,542 (303) 61,454 Comprehensive income Net income for the year ,856-9,856 Other comprehensive income for the year ,495 1,495 Total comprehensive income for the year ,856 1,495 11,351 Transactions with owners Issuance of shares Employee stock option plan: Expiration of options - - (11) Cash dividends (6,402) - (6,402) Transfer from surplus to reserves (137) - - Total transactions with owners (6,528) - (6,402) Balance, December 31, ,562 8,317 1,462 19,870 1,192 66,403 Comprehensive income Net income for the year ,383-12,383 Other comprehensive income for the year (550) (550) Total comprehensive income for the year ,383 (550) 11,833 Transactions with owners Employee stock option plan: Expiration of options Cash dividends (8,180) - (8,180) Transfer from surplus to reserves (141) - - Total transactions with owners (8,321) - (8,180) Balance, December 31, ,562 8,317 1,603 23, ,056 (The notes on pages 1 to 96 are an integral part of these financial statements.)

46 BANK OF THE PHILIPPINE ISLANDS STATEMENTS OF CASH FLOWS FOR EACH OF THE THREE YEARS IN THE PERIOD ENDED DECEMBER 31, 2012 Consolidated Parent Notes CASH FLOWS FROM OPERATING ACTIVITIES Income before income tax 19,573 16,143 13,999 14,595 12,115 10,466 Adjustments for: Impairment losses 11,13, 18 2,923 2,150 3,454 2,003 1,583 2,165 Depreciation and amortization 14, 15 3,346 3,040 2,586 2,188 1,920 1,549 Share in net income of associates (138) (216) (195) Dividend income 25 (27) (47) (85) (1,383) (1,210) (206) Interest income (41,481) (40,071) (38,381) (28,585) (28,287) (27,565) Interest expense 12,655 12,823 13,359 7,517 8,269 9,052 Operating loss before changes in operating assets and liabilities (3,149) (6,178) (5,263) (3,665) (5,610) (4,539) Changes in operating assets and liabilities (Increase) decrease in: Due from Bangko Sentral ng Pilipinas - 54,303 (12,731) - 52,010 (12,300) Interbank loans receivable and securities purchased under agreements to resell - 3,859 20,403-3,861 20,958 Trading securities, net (9,742) (721) 41,760 (7,593) (1,236) 41,829 Loans and advances, net (74,345) (77,418) (54,907) (53,800) (62,188) (38,573) Assets held for sale 1,868 2,327 2,467 1,759 2,136 2,260 Assets attributable to insurance operations (724) (328) (209) Other resources (3,661) (4,185) (539) (3,603) (3,006) (30) Increase (decrease) in: Deposit liabilities 121,173 (38,665) 140,295 83,951 (47,522) 119,905 Due to Bangko Sentral ng Pilipinas and other banks 318 (283) (285) 68 Manager s checks and demand drafts outstanding 1,663 (56) 1,128 1,119 (95) 977 Accrued taxes, interest and other expenses 557 (536) (654) 226 Liabilities attributable to insurance operations Derivative financial instruments (176) (176) Deferred credits and other liabilities 4,699 (1,364) (35) 3,849 (1,547) (859) Net cash from (used in) operations 39,901 (68,367) 133,051 23,596 (63,982) 129,746 Interest received 40,410 40,467 37,099 27,479 28,623 26,485 Interest paid (12,418) (13,380) (13,029) (7,423) (8,780) (8,703) Income taxes paid (3,711) (2,442) (2,670) (2,675) (1,415) (1,824) Net cash from (used in) operating activities 64,182 (43,722) 154,451 40,977 (45,554) 145,704 CASH FLOWS FROM INVESTING ACTIVITIES (Increase) decrease in: Available-for-sale securities, net 11 (32,454) 39,147 (38,596) (28,286) 35,311 (36,533) Held-to-maturity securities, net 12 13,905 5,693 (20,259) 12,165 5,363 (20,187) Bank premises, furniture, fixtures and equipment, net 14 (2,748) (3,246) (2,531) (1,416) (1,784) (1,376) Investment properties, net (12) 3 (10) (12) (1) (10) Investment in subsidiaries and associates, net (24) (120) 407 (80) (39) (17) Assets attributable to insurance operations (614) 183 (787) - - Dividends received ,383 1, Net cash (used in) from investing activities (21,920) 41,707 (61,691) (16,246) 40,060 (57,687) (forward)

47 BANK OF THE PHILIPPINE ISLANDS STATEMENTS OF CASH FLOWS FOR EACH OF THE THREE YEARS IN THE PERIOD ENDED DECEMBER 31, 2012 Consolidated Parent Notes CASH FLOWS FROM FINANCING ACTIVITIES Cash dividends paid (11,380) (3,201) (9,044) (11,380) (3,201) (9,044) Proceeds from stock rights offering , ,906 Increase (decrease) in bills payable 7,144 (5,733) (7,141) 7,076 (7,357) (7,372) Net cash used in financing activities (4,236) (8,934) (6,279) (4,304) (10,558) (6,510) NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS 38,026 (10,949) 86,481 20,427 (16,052) 81,507 CASH AND CASH EQUIVALENTS 7 January 1 150, ,910 75, , ,954 57,447 December , , , , , ,954 (The notes on pages 1 to 96 are an integral part of these financial statements.)

48 BANK OF THE PHILIPPINE ISLANDS NOTES TO FINANCIAL STATEMENTS AS AT DECEMBER 31, 2012 AND 2011 AND FOR EACH OF THE THREE YEARS IN THE PERIOD ENDED DECEMBER 31, 2012 Note 1 - General Information Bank of the Philippine Islands ( BPI or the Parent Bank ) is a domestic commercial bank with an expanded banking license and has its registered office address, which is also its principal place of business, at BPI Building, Ayala Avenue corner Paseo de Roxas, Makati City. BPI and its subsidiaries as detailed in Note 2.3 (collectively referred to as the BPI Group ) offer a whole breadth of financial services that include corporate banking, consumer banking, investment banking, asset management, corporate finance, securities distribution, and insurance services. At December 31, 2012, the BPI Group has 12,406 employees ( ,355 employees) and operates 820 branches and 2,068 ATMs ( branches and 1,868 ATMs) to support its delivery of services. The BPI Group also serves its customers through alternative electronic banking channels such as telephone, mobile phone and the internet. The BPI shares have been traded in the Philippine Stock Exchange (PSE) since October 12, The Parent Bank was registered with the Securities and Exchange Commission (SEC) on January 4, This license was extended for another 50 years on January 4, These financial statements have been approved and authorized for issuance by the Board of Directors of the Parent Bank on February 20, There are no material events that occurred subsequent to February 20, 2013 until February 22, Note 2 - Summary of Significant Accounting Policies The principal accounting policies applied in the preparation of these financial statements are set out below. These policies have been consistently applied to all the years presented, unless otherwise stated. 2.1 Basis of preparation The financial statements of the BPI Group have been prepared in accordance with Philippine Financial Reporting Standards (PFRS). The term PFRS in general includes all applicable PFRS, Philippine Accounting Standards (PAS), interpretations of the Philippine Interpretations Committee (PIC), Standing Interpretations Committee (SIC) and International Financial Reporting Interpretations Committee (IFRIC) which have been approved by the Financial Reporting Standards Council (FRSC) and adopted by the SEC. As allowed by the SEC, the pre-need subsidiary of the Parent Bank continues to follow the provisions of the Pre-Need Uniform Chart of Accounts (PNUCA) prescribed by the SEC and adopted by the Insurance Commission. The financial statements comprise the statement of condition, statement of income and statement of total comprehensive income shown as two statements, statement of changes in capital funds, statement of cash flows and the notes. These financial statements have been prepared under the historical cost convention, as modified by the revaluation of trading securities, available-for-sale financial assets and all derivative contracts. The preparation of financial statements in conformity with PFRS requires the use of certain critical accounting estimates. It also requires management to exercise its judgment in the process of applying the BPI Group s accounting policies. Changes in assumptions may have a significant impact on the financial statements in the period the assumptions changed. Management believes that the underlying assumptions are appropriate and that the financial statements therefore fairly present the financial position and results of the BPI Group. The areas involving a higher degree of judgment or complexity, or areas where assumptions and estimates are significant to the financial statements, are disclosed in Note 4.

49 2.2 New standards, interpretations and amendments to published standards The BPI Group adopted the following amendments to existing standards and interpretations approved by the FRSC which are effective for the BPI Group beginning January 1, 2012: PAS 12 (Amendment), Income Taxes - Deferred Tax (effective January 1, 2012). PAS 12 currently requires an entity to measure the deferred tax relating to an asset depending on whether the entity expects to recover the carrying amount of the asset through use or sale. It can be difficult and subjective to assess whether recovery will be through use or through sale when the asset is measured using the fair value model in PAS 40, Investment Property. This amendment therefore introduces an exception to the existing principle for the measurement of deferred tax assets or liabilities arising on investment property measured at fair value. As a result of the amendments, SIC 21, Income Taxes - Recovery of Revalued Non-Depreciable Assets, will no longer apply to investment properties carried at fair value. The amendments also incorporate into PAS 12 the remaining guidance previously contained in SIC 21, which is withdrawn. The BPI Group applied the amendments beginning January 1, 2012 but this did not have a material impact on the financial statements as investment properties are measured using the cost model. PFRS 7 (Amendment), Financial Instruments: Disclosures - Derecognition (effective July 1, 2011). This amendment will promote transparency in the reporting of transfer transactions and improve users understanding of the risk exposures relating to transfers of financial assets and the effect of those risks on an entity s financial position, particularly those involving securitization of financial assets. The BPI Group applied the amendments beginning January 1, 2012 but this did not have a material impact on the financial statements as there were no securities transferred that have not been derecognized in the current year. New standards, amendments and interpretations to existing standards that are not yet effective and not early adopted by the BPI Group PAS 1 (Amendment), Financial Statement Presentation - Other Comprehensive Income (effective July 1, 2012). The main change resulting from these amendments is a requirement for entities to group items presented in other comprehensive income on the basis of whether they are potentially reclassifiable to profit or loss subsequently (reclassification adjustments). The amendments do not address which items are presented in other comprehensive income. The BPI Group will apply the amendment beginning January 1, The adoption is not expected to have a significant impact on the financial statements but will result in changes in presentation in the statement of total comprehensive income. PAS 19 (Amendment), Employee Benefits (effective January 1, 2013). These amendments eliminate the corridor approach and calculate finance costs on a net funding basis. The amendments would also require recognition of all actuarial gains and losses in other comprehensive income as they occur and of all past service costs in profit or loss. The amendments replace interest cost and expected return on plan assets with a net interest amount that is calculated by applying the discount rate to the net defined benefit liability (asset). As at December 31, 2012, the BPI Group has unrecognized actuarial loss of P514.5 million (Note 30) which will be recognized in other comprehensive income upon adoption of the amendments. PAS 28 (Revised), Investments in Associates and Joint Ventures (effective January 1, 2013). This revised standard includes the requirements for joint ventures, as well as associates, to be accounted for using the equity method following the issuance of PFRS 11. The BPI Group will apply the revised standard beginning January 1, The BPI Group is currently assessing the full impact on the financial statements as investments in associates are currently accounted for using the cost method in the Parent Bank s separate financial statements. The BPI Group has no investments in joint ventures. PAS 32 (Amendment), Financial Instruments: Presentation Asset and Liability Offsetting (effective January 1, 2014). These amendments are to the application guidance in PAS 32, Financial Instruments: Presentation, and clarify some of the requirements for offsetting financial assets and financial liabilities on the statement of condition. The BPI Group will apply the amendment beginning January 1, The adoption is not expected to have a significant impact on the financial statements but will result in changes in presentation of financial assets and financial liabilities subject to offsetting in the statement of condition. (2)

50 PFRS 9, Financial Instruments (effective January 1, 2015). This new standard addresses the classification, measurement and recognition of financial assets and financial liabilities. It replaces the parts of PAS 39 that relate to the classification and measurement of financial instruments. PFRS 9 requires financial assets to be classified into two measurement categories: those measured at fair value and those measured at amortized cost. The determination is made at initial recognition. The classification depends on the entity s business model for managing its financial instruments and the contractual cash flow characteristics of the instrument. For financial liabilities, the standard retains most of the PAS 39 requirements. The main change is that, in cases where the fair value option is taken for financial liabilities, part of the fair value change due to an entity s own credit risk is recorded in other comprehensive income rather than in profit or loss, unless this creates an accounting mismatch. The BPI Group will apply this new standard beginning January 1, The adoption of PFRS 9 will affect the BPI Group s accounting for its available-for-sale debt securities as the standard will only allow the recognition of fair value gains and losses in other comprehensive income if they relate to equity investments that are not held for trading. Fair value gains and losses on available-for-sale debt securities will therefore have to be recognized directly in profit or loss. The BPI Group is currently assessing the full impact on the financial statements upon adoption of the new standard. PFRS 10, Consolidated Financial Statements (effective January 1, 2013). This new standard builds on existing principles by identifying the concept of control as the determining factor in whether an entity should be included in the consolidated financial statements of the parent company. The standard provides additional guidance to assist in the determination of control where this is difficult to assess. The BPI Group will adopt this new standard beginning January 1, 2013 and is currently assessing the full impact on the financial statements upon adoption. PFRS 12, Disclosures of Interests in Other Entities (effective January 1, 2013). This new standard includes the disclosure requirements for all forms of interests in other entities, including joint arrangements, associates, special purpose vehicles and other off balance sheet vehicles. The BPI Group will apply this new standard beginning January 1, 2013 but the adoption is not expected to have a significant impact on the financial statements other than the required disclosure requirements for interests in associates. PFRS 13, Fair Value Measurement (effective January 1, 2013). This new standard aims to improve consistency and reduce complexity by providing a clarified definition of fair value and a single source of fair value measurement and disclosure requirements for use across PFRS. The requirements, which are largely aligned between IFRS and US GAAP, do not extend the use of fair value accounting but provide guidance on how it should be applied where its use is already required or permitted by other standards within IFRS or US GAAP. The BPI Group will apply this new standard beginning January 1, 2013 but the adoption is not expected to have a significant impact on the financial statements as the current fair value measurement of its financial instruments carried at fair value is already consistent with requirements of the new standard. There are no other standards, amendments or interpretations that are not yet effective that would be expected to have a material impact on the BPI Group. (3)

51 2.3 Consolidation The consolidated financial statements comprise the financial statements of the BPI Group as at December 31, The subsidiaries financial statements are prepared for the same reporting period as the Parent Bank. The consolidated financial statements include the financial statements of the Parent Bank and the following subsidiaries as at December 31: Country of % of ownership Subsidiaries incorporation Principal activities BPI Family Savings Bank, Inc. Philippines Banking BPI Capital Corporation Philippines Investment house BPI Leasing Corporation Philippines Leasing BPI Direct Savings Bank, Inc. Philippines Banking BPI International Finance Limited Hong Kong Financing BPI Europe Plc. England and Wales Banking (deposit) BPI Securities Corp. Philippines Securities dealer BPI Card Finance Corp. Philippines Financing Filinvest Algo Financial Corp. Philippines Financing BPI Rental Corporation. Philippines Rental BPI Investment Management Inc. Philippines Investment management Santiago Land Dev. Corp. Philippines Land holding BPI Operations Management Corp. Philippines Operations management BPI Computer Systems Corp. Philippines Business systems service BPI Foreign Exchange Corp. Philippines Foreign exchange BPI Express Remittance Corp. USA USA Remittance BPI Express Remittance Corp. Nevada USA Remittance BPI Express Remittance Center HK (Ltd.) Hong Kong Remittance Green Enterprises S. R. L. in Liquidation (formerly BPI Express Remittance Europe, S.p.A.) Italy Remittance Prudential Investments, Inc. Philippines Investment house First Far - East Development Corporation Philippines Real estate FEB Stock Brokers, Inc. Philippines Securities dealer Citytrust Securities Corporation Philippines Securities dealer BPI Express Remittance Spain S.A Spain Remittance FEB Speed International Philippines Remittance AF Holdings and Management Corp. Philippines Financial management consultancy Ayala Plans, Inc Philippines Pre-need FGU Insurance Corporation Philippines Non-life insurance BPI/MS Insurance Corporation Philippines Non-life insurance BPI Globe BanKO, Inc. Philippines Banking BPI has control over BPI Globe BanKO, Inc. since BPI is largely involved in key decisions concerning financial and operating policies and activities of, and provision of technological support and technical knowhow to BPI Globe BanKO, Inc. (4)

52 (a) Subsidiaries Subsidiaries are all entities over which the BPI Group has the power to govern the financial and operating policies generally accompanying a shareholding of more than one half of the voting rights. The existence and effect of potential voting rights that are currently exercisable or convertible are considered when assessing whether the BPI Group controls another entity. The BPI Group also assesses existence of control where it does not have more than 50% of the voting power but is able to govern the financial and operating policies by virtue of de-facto control. De-facto control may arise in circumstances where the size of the BPI Group s voting rights relative to the size and dispersion of holdings of other shareholders give the BPI Group the power to govern the financial and operating policies. Subsidiaries are fully consolidated from the date on which control is transferred to the BPI Group. They are de-consolidated from the date that control ceases. The BPI Group applies the acquisition method of accounting to account for business combinations. The consideration transferred for the acquisition of a subsidiary is the fair values of the assets transferred, the liabilities incurred and the equity interests issued by the BPI Group. The consideration transferred includes the fair value of any asset or liability resulting from a contingent consideration arrangement. Acquisitionrelated costs are expensed as incurred. Identifiable assets acquired and liabilities and contingent liabilities assumed in a business combination are measured initially at their fair values at the acquisition date. On an acquisition-by-acquisition basis, the BPI Group recognizes any non-controlling interest in the acquiree either at fair value or at the non-controlling interest s proportionate share of the acquiree s identifiable net assets. The excess of the aggregate of the consideration transferred, the amount of any non-controlling interest in the acquiree and the acquisition-date fair value of any previous equity interest in the acquiree over the fair value of the BPI Group s share of the identifiable net assets acquired is recorded as goodwill. If this consideration is lower than the fair value of the net assets of the subsidiary acquired in the case of a bargain purchase, the difference is recognized directly in profit or loss. Inter-company transactions, balances and income and expenses on transactions between group companies are eliminated. Profits and losses resulting from inter-company transactions that are recognized in assets are also eliminated. Accounting policies of subsidiaries have been changed where necessary to ensure consistency with the policies adopted by the BPI Group, except for the pre-need subsidiary which follows the provisions of the PNUCA as allowed by the SEC. When the BPI Group ceases to have control, any retained interest in the entity is re-measured to its fair value at the date when control is lost, with the change in carrying amount recognized in profit or loss. The fair value is the initial carrying amount for the purposes of subsequently accounting for the retained interest as an associate, joint venture or financial asset. In addition, any amounts previously recognized in other comprehensive income in respect of that entity are accounted for as if the BPI Group had directly disposed of the related assets or liabilities. This may mean that amounts previously recognized in other comprehensive income are reclassified to profit or loss. (b) Transactions with non-controlling interests Transactions with non-controlling interests that do not result in loss of control are accounted for as equity transactions - that is, as transactions with the owners in their capacity as owners. For purchases from noncontrolling interests, the difference between any consideration paid and the relevant share acquired of the carrying value of net assets of the subsidiary is recorded in equity. Gains or losses on disposals to noncontrolling interests are also recorded in equity. Interests in the equity of subsidiaries not attributable to the Parent Bank are reported in consolidated equity as non-controlling interests. Profits or losses attributable to non-controlling interests are reported in the statement of income as net income (loss) attributable to non-controlling interests. (5)

53 (c) Associates Associates are all entities over which the BPI Group has significant influence but not control, generally accompanying a shareholding of between 20% and 50% of the voting rights. Investments in associates in the consolidated financial statements are accounted for using the equity method of accounting. Under the equity method, the investment is initially recognized at cost and the carrying amount is increased or decreased to recognize the investor s share of the profit or loss of the investee after the date of acquisition. The BPI Group s investment in associates includes goodwill identified on acquisition (net of any accumulated impairment loss). If the ownership interest in an associate is reduced but significant influence is retained, a proportionate share of the amounts previously recognized in other comprehensive income is reclassified to profit or loss where appropriate. The BPI Group s share of its associates post-acquisition profits or losses is recognized in profit or loss, and its share of post-acquisition movements in reserves is recognized in other comprehensive income. The cumulative post-acquisition movements are adjusted against the carrying amount of the investment. When the BPI Group s share of losses in an associate equals or exceeds its interest in the associate, including any other unsecured receivables, the BPI Group does not recognize further losses, unless it has incurred legal or constructive obligations or made payments on behalf of the associate. The BPI Group determines at each reporting date whether there is any indicator of impairment that the investment in the associate is impaired. If this is the case, the BPI Group calculates the amount of impairment as the difference between the recoverable amount of the associate and its carrying value and recognizes the amount adjacent to share of profit (loss) of an associate in profit or loss. Unrealized gains on transactions between the BPI Group and its associates are eliminated to the extent of the BPI Group s interest in the associates. Unrealized losses are also eliminated unless the transaction provides evidence of an impairment of the asset transferred. Accounting policies of associates have been changed where necessary to ensure consistency with the policies adopted by the BPI Group. 2.4 Investments in subsidiaries and associates Investments in subsidiaries and associates in the Parent Bank s separate financial statements are accounted for using the cost method in accordance with PAS 27. Under this method, income from investment is recognized in profit or loss only to the extent that the investor receives distributions from accumulated profits of the investee arising after the acquisition date. Distributions received in excess of such profits are regarded as a recovery of investment and are recognized as reduction of the cost of the investment. The Parent Bank recognizes a dividend from a subsidiary or associate in profit or loss in its separate financial statements when its right to receive the dividend is established. The Parent Bank determines at each reporting date whether there is any indicator of impairment that the investment in the subsidiary or associate is impaired. If this is the case, the Parent Bank calculates the amount of impairment as the difference between the recoverable amount and carrying value and the difference is recognized in profit or loss. Investments in subsidiaries and associates are derecognized upon disposal or when no future economic benefits are expected to be derived from the subsidiaries and associates at which time the cost and the related accumulated impairment loss are removed in the statement of condition. Any gains and losses on disposal is determined by comparing the proceeds with the carrying amount of the investment and recognized in profit or loss. 2.5 Segment reporting Operating segments are reported in a manner consistent with the internal reporting provided to the chief executive officer who allocates resources to, and assesses the performance of the operating segments of the BPI Group. (6)

54 All transactions between business segments are conducted on an arm s length basis, with intra-segment revenue and costs being eliminated upon consolidation. Income and expenses directly associated with each segment are included in determining business segment performance. In accordance with PFRS 8, the BPI Group has the following main banking business segments: consumer banking, corporate banking and investment banking. Its insurance business is assessed separately from these banking business segments (Note 5). 2.6 Cash and cash equivalents Cash and cash equivalents consist of Cash and other cash items, Due from Bangko Sentral ng Pilipinas (BSP), Due from other banks, and Interbank loans receivable and securities purchased under agreements to resell with maturities of less than three months from the date of acquisition and that are subject to insignificant risk of changes in value. 2.7 Repurchase and reverse repurchase agreements Securities sold subject to repurchase agreements ( repos ) are reclassified in the financial statements as pledged assets when the transferee has the right by contract or custom to sell or repledge the collateral; the counterparty liability is included in deposits from banks or deposits from customers, as appropriate. The difference between sale and repurchase price is treated as interest and accrued over the life of the agreements using the effective interest method. Securities purchased under agreements to resell ( reverse repos ) are recorded as loans and advances to other banks and customers and included in the statement of condition under Interbank loans receivable and securities purchased under agreements to resell. Securities lent to counterparties are also retained in the financial statements. 2.8 Financial assets Classification The BPI Group classifies its financial assets in the following categories: financial assets at fair value through profit or loss, loans and receivables, held-to-maturity securities and available-for-sale securities. The classification depends on the purpose for which the financial assets are acquired. Management determines the classification of its financial assets at initial recognition. (a) Financial assets at fair value through profit or loss This category has two sub-categories: financial assets held for trading and those designated at fair value through profit or loss at inception. A financial asset is classified as held for trading if it is acquired principally for the purpose of selling or repurchasing it in the near term or if it is part of a portfolio of identified financial instruments that are managed together and for which there is evidence of a recent actual pattern of short-term profit-taking. Financial assets held for trading (other than derivatives) are shown as Trading securities in the statement of condition. Derivatives are also categorized as held for trading unless they are designated as hedging instruments. Financial assets designated at fair value through profit or loss at inception are those that are managed and their performance is evaluated on a fair value basis, in accordance with a documented investment strategy. Information about these financial assets is provided internally on a fair value basis to the BPI Group s key management personnel. The BPI Group has no financial assets that are specifically designated at fair value through profit or loss. (7)

55 (b) Loans and receivables Loans and receivables are non-derivative financial assets with fixed or determinable payments: (i) that are not quoted in an active market, (ii) with no intention of being traded, and (iii) that are not designated as available-for-sale. Significant accounts falling under this category include loans and advances, cash and other cash items, due from BSP and other banks, interbank loans receivable and securities purchased under agreements to resell and accounts receivable included under other resources. (c) Held-to-maturity securities Held-to-maturity securities are non-derivative financial assets with fixed or determinable payments and fixed maturities that the BPI Group s management has the positive intention and ability to hold to maturity. If the BPI Group were to sell other than an insignificant amount of held-to-maturity assets, the entire category would be tainted and reclassified as available-for-sale. (d) Available-for-sale securities Available-for-sale securities are non-derivative financial assets that are either designated in this category or not classified in any of the other categories Recognition and measurement (a) Initial recognition and measurement Regular-way purchases and sales of financial assets at fair value through profit or loss, held-to-maturity securities and available-for-sale securities are recognized on trade date, the date on which the BPI Group commits to purchase or sell the asset. Loans and receivables are recognized upon origination when cash is advanced to the borrowers or when the right to receive payment is established. Financial assets not carried at fair value through profit or loss are initially recognized at fair value plus transaction costs. Financial assets carried at fair value through profit or loss are initially recognized at fair value; and transaction costs are recognized in profit or loss. (b) Subsequent measurement Available-for-sale securities and financial assets at fair value through profit or loss are subsequently carried at fair value. Loans and receivables and held-to-maturity securities are subsequently carried at amortized cost using the effective interest method. Gains and losses arising from changes in the fair value of the financial assets at fair value through profit or loss are included in the statement of income (as Trading gain/loss on securities ) in the year in which they arise. Gains and losses arising from changes in the fair value of available-for-sale securities are recognized directly in other comprehensive income, until the financial asset is derecognized or impaired at which time the cumulative gain or loss previously recognized in other comprehensive income should be recognized in profit or loss. However, interest is calculated on these securities using the effective interest method and foreign currency gains and losses on monetary assets classified as available-for-sale are recognized in profit or loss. Dividends on equity instruments are recognized in profit or loss when the BPI Group s right to receive payment is established Reclassification The BPI Group may choose to reclassify a non-derivative financial asset held for trading out of the held-fortrading category if the financial asset is no longer held for the purpose of selling it in the near term. Financial assets other than loans and receivables are permitted to be reclassified out of the held-for-trading category only in rare circumstances arising from a single event that is unusual and highly unlikely to recur in the near term. In addition, the BPI Group may choose to reclassify financial assets that would meet the definition of loans and receivables out of the held-for-trading or available-for-sale categories if the BPI Group has the intention and ability to hold these financial assets for the foreseeable future or until maturity at the date of reclassification. (8)

56 Reclassifications are made at fair value as of the reclassification date. Fair value becomes the new cost or amortized cost as applicable, and no reversals of fair value gains or losses recorded before reclassification date are subsequently made. Effective interest rates for financial assets reclassified to loans and receivables and held-to-maturity categories are determined at the reclassification date. Further increases in estimates of cash flows adjust effective interest rates prospectively Derecognition Financial assets are derecognized when the contractual rights to receive the cash flows from these assets have ceased to exist or the assets have been transferred and substantially all the risks and rewards of ownership of the assets are also transferred (that is, if substantially all the risks and rewards have not been transferred, the BPI Group tests control to ensure that continuing involvement on the basis of any retained powers of control does not prevent derecognition). 2.9 Impairment of financial assets (a) Assets carried at amortized cost The BPI Group assesses at each reporting date whether there is objective evidence that a financial asset or group of financial assets is impaired. A financial asset or a group of financial assets is impaired and impairment losses are incurred only if there is objective evidence of impairment as a result of one or more events that occurred after the initial recognition of the asset (a loss event ) and that loss event (or events) has an impact on the estimated future cash flows of the financial asset or group of financial assets that can be reliably estimated. The criteria that the BPI Group uses to determine that there is objective evidence of an impairment loss include: Delinquency in contractual payments of principal or interest; Cash flow difficulties experienced by the borrower; Breach of loan covenants or conditions; Initiation of bankruptcy proceedings; Deterioration of the borrower s competitive position; and Deterioration in the value of collateral. The BPI Group first assesses whether objective evidence of impairment exists individually for financial assets that are individually significant, and collectively for financial assets that are not individually significant. If the BPI Group determines that no objective evidence of impairment exists for an individually assessed financial asset, whether significant or not, it includes the asset in a group of financial assets with similar credit risk characteristics and collectively assesses them for impairment. Financial assets that are individually assessed for impairment and for which an impairment loss is or continues to be recognized are not included in a collective assessment of impairment. The amount of impairment loss is measured as the difference between the asset s carrying amount and the present value of estimated future cash flows (excluding future credit losses that have not been incurred) discounted at the financial asset s original effective interest rate (recoverable amount). The calculation of recoverable amount of a collateralized financial asset reflects the cash flows that may result from foreclosure less costs of obtaining and selling the collateral, whether or not foreclosure is probable. If a loan or held-tomaturity investment has a variable interest rate, the discount rate for measuring any impairment loss is the current effective interest rate determined under the contract. The carrying amount of the asset is reduced through the use of an allowance account and the amount of loss is recognized in profit or loss. For the purposes of a collective evaluation of impairment, financial assets are grouped on the basis of similar credit risk characteristics (i.e., on the basis of the BPI Group s grading process that considers asset type, industry, geographical location, collateral type, past-due status and other relevant factors). Those characteristics are relevant to the estimation of future cash flows for groups of such assets by being indicative of the debtors ability to pay all amounts due according to the contractual terms of the assets being evaluated. (9)

57 Future cash flows in a group of financial assets that are collectively evaluated for impairment are estimated on the basis of the contractual cash flows of the assets in the BPI Group and historical loss experience for assets with credit risk characteristics similar to those in the BPI Group. Historical loss experience is adjusted on the basis of current observable data to reflect the effects of current conditions that did not affect the period on which the historical loss experience is based and to remove the effects of conditions in the historical period that do not currently exist. The methodology and assumptions used for estimating future cash flows are reviewed regularly to reduce any differences between loss estimates and actual loss experience. When a loan is uncollectible, it is written off against the related allowance for loan impairment. Such loans are written off after all the necessary procedures have been completed and the amount of the loss has been determined. If in a subsequent period, the amount of the impairment loss decreases and the decrease can be related objectively to an event occurring after the impairment was recognized (such as an improvement in the debtor s credit rating), the previously recognized impairment loss is reversed by adjusting the allowance account. Subsequent recoveries of amounts previously written-off are credited to impairment loss in the statement of income. (b) Assets classified as available-for-sale The BPI Group assesses at each reporting date whether there is an objective evidence that a security classified as available-for-sale is impaired. For debt securities, the BPI Group uses the criteria mentioned in (a) above. For an equity security classified as available-for-sale, a significant or prolonged decline in the fair value below cost is considered in determining whether the securities are impaired. Generally, the BPI Group treats significant as 20% or more and prolonged as greater than twelve months. The cumulative loss (difference between the acquisition cost and the current fair value less any impairment loss on that financial asset previously recognized in profit or loss) is removed from other comprehensive income and recognized in profit or loss when the asset is determined to be impaired. If in a subsequent period, the fair value of a debt instrument previously impaired increases and the increase can be objectively related to an event occurring after the impairment loss was recognized, the impairment loss is reversed through profit or loss. Reversal of impairment losses recognized previously on equity instruments is made directly to other comprehensive income. (c) Renegotiated loans Loans that are either subject to individual or collective impairment assessment and whose terms have been renegotiated are no longer considered to be past due but are treated as new loans Financial liabilities Classification The BPI Group classifies its financial liabilities in the following categories: financial liabilities at fair value through profit or loss and financial liabilities at amortized cost. (a) Financial liabilities at fair value through profit or loss This category comprises two sub-categories: financial liabilities classified as held for trading, and financial liabilities designated by the BPI Group as at fair value through profit or loss upon initial recognition. A financial liability is classified as held for trading if it is acquired or incurred principally for the purpose of selling or repurchasing it in the near term or if it is part of a portfolio of identified financial instruments that are managed together and for which there is evidence of a recent actual pattern of short-term profit-taking. Derivatives are also categorized as held for trading unless they are designated and effective as hedging instruments. Gains and losses arising from changes in fair value of financial liabilities classified as held for trading are included in the statement of income and are reported as Trading gains/losses. The BPI Group has no financial liabilities that are designated at fair value through profit loss. (10)

FUBON LIFE INSURANCE CO., LTD. AND SUBSIDIARIES. CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS JUNE 30, 2013 and 2012

FUBON LIFE INSURANCE CO., LTD. AND SUBSIDIARIES CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS JUNE 30, 2013 and 2012 (with Independent Auditors Report Thereon) Address: 14F, No. 108, Sec. 1, Tun

FUBON LIFE INSURANCE CO., LTD. AND SUBSIDIARIES CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS JUNE 30, 2013 and 2012 (with Independent Auditors Report Thereon) Address: 14F, No. 108, Sec. 1, Tun

KOREAN AIR LINES CO., LTD. AND SUBSIDIARIES. Consolidated Financial Statements

Consolidated Financial Statements December 31, 2015 (With Independent Auditors Report Thereon) Contents Page Independent Auditors Report 1 Consolidated Statements of Financial Position 3 Consolidated Statements

Consolidated Financial Statements December 31, 2015 (With Independent Auditors Report Thereon) Contents Page Independent Auditors Report 1 Consolidated Statements of Financial Position 3 Consolidated Statements

NOTES TO THE FINANCIAL STATEMENTS

1. Principal activities The Company is an investment holding company and its subsidiaries are principally engaged in the provision of banking and related financial services in Hong Kong. The Company is

1. Principal activities The Company is an investment holding company and its subsidiaries are principally engaged in the provision of banking and related financial services in Hong Kong. The Company is

Principal Accounting Policies

1. Basis of Preparation The accounts have been prepared in accordance with Hong Kong Financial Reporting Standards ( HKFRS ). The accounts have been prepared under the historical cost convention as modified

1. Basis of Preparation The accounts have been prepared in accordance with Hong Kong Financial Reporting Standards ( HKFRS ). The accounts have been prepared under the historical cost convention as modified

Note 2 SIGNIFICANT ACCOUNTING

Note 2 SIGNIFICANT ACCOUNTING POLICIES BASIS FOR THE PREPARATION OF THE FINANCIAL STATEMENTS The consolidated financial statements have been prepared in accordance with International Financial Reporting

Note 2 SIGNIFICANT ACCOUNTING POLICIES BASIS FOR THE PREPARATION OF THE FINANCIAL STATEMENTS The consolidated financial statements have been prepared in accordance with International Financial Reporting

Samsung Life Insurance Co., Ltd. Separate Financial Statements March 31, 2013 and 2012

Separate Financial Statements Index Page(s) Report of Independent Auditors 1-2 Separate Financial Statements Statements of Financial Position 3 Statements of Comprehensive Income 4 5 Statements of Changes

Separate Financial Statements Index Page(s) Report of Independent Auditors 1-2 Separate Financial Statements Statements of Financial Position 3 Statements of Comprehensive Income 4 5 Statements of Changes

DBS BANK LTD (Incorporated in Singapore. Registration Number: 196800306E) AND ITS SUBSIDIARIES

AND ITS SUBSIDIARIES") DBS BANK LTD (Incorporated in Singapore. Registration Number: 196800306E) AND ITS SUBSIDIARIES FINANCIAL STATEMENTS For the financial year ended 31 December 2013 Financial Statements Table of Contents

DBS BANK LTD (Incorporated in Singapore. Registration Number: 196800306E) AND ITS SUBSIDIARIES FINANCIAL STATEMENTS For the financial year ended 31 December 2013 Financial Statements Table of Contents

Türkiye İş Bankası A.Ş. Separate Financial Statements As at and for the Year Ended 31 December 2015

Türkiye İş Bankası A.Ş. Separate Financial Statements As at and for the Year Ended 2015 29 April 2016 This report includes 93 pages of separate financial statements together with their explanatory notes.

Türkiye İş Bankası A.Ş. Separate Financial Statements As at and for the Year Ended 2015 29 April 2016 This report includes 93 pages of separate financial statements together with their explanatory notes.

International Accounting Standard 39 Financial Instruments: Recognition and Measurement

EC staff consolidated version as of 18 February 2011 FOR INFORMATION PURPOSES ONLY International Accounting Standard 39 Financial Instruments: Recognition and Measurement Objective 1 The objective of this

EC staff consolidated version as of 18 February 2011 FOR INFORMATION PURPOSES ONLY International Accounting Standard 39 Financial Instruments: Recognition and Measurement Objective 1 The objective of this

FUBON LIFE INSURANCE CO., LTD. AND SUBSIDIARIES. CONSOLIDATED INTERIM FINANCIAL STATEMENTS June 30, 2014 and 2013

CONSOLIDATED INTERIM FINANCIAL STATEMENTS 2014 and (with Independent Accountants Report Thereon) Address: 14F, No. 108, Sec. 1, Tun Hua S. Road, Taipei, Taiwan Telephone: 886-2-8771-6699 - 1 - 2014 and

CONSOLIDATED INTERIM FINANCIAL STATEMENTS 2014 and (with Independent Accountants Report Thereon) Address: 14F, No. 108, Sec. 1, Tun Hua S. Road, Taipei, Taiwan Telephone: 886-2-8771-6699 - 1 - 2014 and

(Amounts in millions of Canadian dollars except for per share amounts and where otherwise stated. All amounts stated in US dollars are in millions.

Notes to the Consolidated Financial Statements (Amounts in millions of Canadian dollars except for per share amounts and where otherwise stated. All amounts stated in US dollars are in millions.) 1. Significant

Notes to the Consolidated Financial Statements (Amounts in millions of Canadian dollars except for per share amounts and where otherwise stated. All amounts stated in US dollars are in millions.) 1. Significant

Arab National Bank Saudi Joint Stock Company

CONSOLIDATED STATEMENT OF FINANCIAL POSITION As at December 31, 2013 and 2012 ASSETS Note 2013 SAR 000 2012 SAR 000 Cash and balances with SAMA 4 14,971,749 20,334,429 Due from banks and other financial

CONSOLIDATED STATEMENT OF FINANCIAL POSITION As at December 31, 2013 and 2012 ASSETS Note 2013 SAR 000 2012 SAR 000 Cash and balances with SAMA 4 14,971,749 20,334,429 Due from banks and other financial

Notes to Consolidated Financial Statements Note 1: Basis of Presentation

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS to Consolidated Financial Statements Note 1: Basis of Presentation Bank of Montreal ( the bank ) is a public company incorporated in Canada having its registered

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS to Consolidated Financial Statements Note 1: Basis of Presentation Bank of Montreal ( the bank ) is a public company incorporated in Canada having its registered

Jollibee Foods Corporation and Subsidiaries

Jollibee Foods Corporation and Subsidiaries Consolidated Financial Statements December 31, 2013 and 2012 and Years Ended December 31, 2013, 2012 and 2011 and Independent Auditors Report SyCip Gorres Velayo

Jollibee Foods Corporation and Subsidiaries Consolidated Financial Statements December 31, 2013 and 2012 and Years Ended December 31, 2013, 2012 and 2011 and Independent Auditors Report SyCip Gorres Velayo

Notes to the Consolidated Financial Statements

1. General The Company is a public limited company incorporated in Hong Kong and its shares are listed on The Stock Exchange of Hong Kong Limited (the Stock Exchange ). The address of the registered office

1. General The Company is a public limited company incorporated in Hong Kong and its shares are listed on The Stock Exchange of Hong Kong Limited (the Stock Exchange ). The address of the registered office

Summary of Significant Accounting Policies FOR THE FINANCIAL YEAR ENDED 31 MARCH 2014

46 Unless otherwise stated, the following accounting policies have been applied consistently in dealing with items which are considered material in relation to the financial statements. The Company and

46 Unless otherwise stated, the following accounting policies have been applied consistently in dealing with items which are considered material in relation to the financial statements. The Company and

G8 Education Limited ABN: 95 123 828 553. Accounting Policies

G8 Education Limited ABN: 95 123 828 553 Accounting Policies Table of Contents Note 1: Summary of significant accounting policies... 3 (a) Basis of preparation... 3 (b) Principles of consolidation... 3

G8 Education Limited ABN: 95 123 828 553 Accounting Policies Table of Contents Note 1: Summary of significant accounting policies... 3 (a) Basis of preparation... 3 (b) Principles of consolidation... 3

Notes to the Consolidated Financial Statements

Deutsche Bank 2 Consolidated Financial Statements 289 Notes to the Consolidated Financial Statements 1 Significant Accounting Policies and Critical Accounting Estimates Notes to the Consolidated Financial

Deutsche Bank 2 Consolidated Financial Statements 289 Notes to the Consolidated Financial Statements 1 Significant Accounting Policies and Critical Accounting Estimates Notes to the Consolidated Financial

Cathay Life Insurance Co., Ltd. Financial Statements As of December 31, 2006 and 2007 With Independent Auditors Report

Financial Statements With Independent Auditors Report The reader is advised that these financial statements have been prepared originally in Chinese. These financial statements do not include additional

Financial Statements With Independent Auditors Report The reader is advised that these financial statements have been prepared originally in Chinese. These financial statements do not include additional

MATRIX IT LTD. AND ITS SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL STATEMENTS AS OF DECEMBER 31, 2013 CONSOLIDATED FINANCIAL STATEMENTS AS OF DECEMBER 31, 2013 NIS IN THOUSANDS INDEX Page Auditors' Reports 2-4 Consolidated Statements of Financial

CONSOLIDATED FINANCIAL STATEMENTS AS OF DECEMBER 31, 2013 CONSOLIDATED FINANCIAL STATEMENTS AS OF DECEMBER 31, 2013 NIS IN THOUSANDS INDEX Page Auditors' Reports 2-4 Consolidated Statements of Financial

ANNUAL FINANCIAL RESULTS FOR THE YEAR ENDED 31 JULY 2014 FONTERRA ANNUAL FINANCIAL RESULTS 2014 A

ANNUAL FINANCIAL RESULTS FOR THE YEAR ENDED 31 JULY 2014 FONTERRA ANNUAL FINANCIAL RESULTS 2014 A CONTENTS DIRECTORS STATEMENT 1 INCOME STATEMENT 2 STATEMENT OF COMPREHENSIVE INCOME 3 STATEMENT OF FINANCIAL

ANNUAL FINANCIAL RESULTS FOR THE YEAR ENDED 31 JULY 2014 FONTERRA ANNUAL FINANCIAL RESULTS 2014 A CONTENTS DIRECTORS STATEMENT 1 INCOME STATEMENT 2 STATEMENT OF COMPREHENSIVE INCOME 3 STATEMENT OF FINANCIAL

Financial Instruments: Recognition and Measurement

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 39 Financial Instruments: Recognition and Measurement This version of the Statutory Board Financial Reporting Standard does not include amendments that

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 39 Financial Instruments: Recognition and Measurement This version of the Statutory Board Financial Reporting Standard does not include amendments that

How To Account In Indian Accounting Standards

Indian Accounting Standard (Ind AS) 39 Financial Instruments: Recognition and Measurement Contents Paragraphs Objective 1 Scope 2 7 Definitions 8 9 Embedded derivatives 10 13 Recognition and derecognition

Indian Accounting Standard (Ind AS) 39 Financial Instruments: Recognition and Measurement Contents Paragraphs Objective 1 Scope 2 7 Definitions 8 9 Embedded derivatives 10 13 Recognition and derecognition

Cathay Life Insurance Co., Ltd. Financial Statements For The Three Months Ended March 31, 2012 and 2011 With Independent Auditors Review Report

Financial Statements For The Three Months Ended March 31, 2012 and 2011 With Independent Auditors Review Report The reader is advised that these financial statements have been prepared originally in Chinese.

Financial Statements For The Three Months Ended March 31, 2012 and 2011 With Independent Auditors Review Report The reader is advised that these financial statements have been prepared originally in Chinese.

Consolidated Statement of Financial Position

18 Consolidated Statement of Financial Position As at December 31, 2010 and 2009 Notes SAR 000 SAR 000 Assets Cash and balances with SAMA 4 11,997,395 10,457,455 Due from banks and other financial institutions

18 Consolidated Statement of Financial Position As at December 31, 2010 and 2009 Notes SAR 000 SAR 000 Assets Cash and balances with SAMA 4 11,997,395 10,457,455 Due from banks and other financial institutions

ATS AUTOMATION TOOLING SYSTEMS INC. Annual Audited Consolidated Financial Statements

Annual Audited Consolidated Financial Statements For the year ended March 31, 2014 MANAGEMENT S RESPONSIBILITY FOR FINANCIAL REPORTING The preparation and presentation of the Company s consolidated financial

Annual Audited Consolidated Financial Statements For the year ended March 31, 2014 MANAGEMENT S RESPONSIBILITY FOR FINANCIAL REPORTING The preparation and presentation of the Company s consolidated financial

Address: 296, Jen Ai Road, Sec. 4, Taipei, Taiwan, R.O.C. Telephone: 886-2-2755-1399

Consolidated Statements For The Years Ended 2013 and With Independent Auditors Report The reader is advised that these financial statements have been prepared originally in Chinese. These financial statements

Consolidated Statements For The Years Ended 2013 and With Independent Auditors Report The reader is advised that these financial statements have been prepared originally in Chinese. These financial statements

Kilikia Universal Credit Organization LLC. Financial Statements for the year ended 31 December 2014

Financial Statements for the year ended 31 December Contents Independent Auditors Report... 3 Statement of profit or loss and other comprehensive income... 4 Statement of financial position... 5 Statement

Financial Statements for the year ended 31 December Contents Independent Auditors Report... 3 Statement of profit or loss and other comprehensive income... 4 Statement of financial position... 5 Statement

ASPE at a Glance. Standards Included in Topic

ASPE AT A GLANCE ASPE AT A GLANCE This publication has been compiled to assist users in gaining a high level overview of Accounting Standards for Private Enterprises (ASPE) included in Part II of the CPA

ASPE AT A GLANCE ASPE AT A GLANCE This publication has been compiled to assist users in gaining a high level overview of Accounting Standards for Private Enterprises (ASPE) included in Part II of the CPA

IPSAS 29 FINANCIAL INSTRUMENTS: RECOGNITION AND MEASUREMENT

IPSAS 29 FINANCIAL INSTRUMENTS: RECOGNITION AND MEASUREMENT Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 39,

IPSAS 29 FINANCIAL INSTRUMENTS: RECOGNITION AND MEASUREMENT Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 39,

Consolidated financial statements

Consolidated financial statements 88 Financial reporting responsibility 89 Independent auditors report of registered public accounting firm to shareholders 91 Consolidated balance sheet 92 Consolidated

Consolidated financial statements 88 Financial reporting responsibility 89 Independent auditors report of registered public accounting firm to shareholders 91 Consolidated balance sheet 92 Consolidated

Shin Kong Investment Trust Co., Ltd. Financial Statements for the Years Ended December 31, 2014 and 2013 and Independent Auditors Report

Shin Kong Investment Trust Co., Ltd. Financial Statements for the Years Ended, 2014 and 2013 and Independent Auditors Report INDEPENDENT AUDITORS REPORT The Board of Directors and stockholder Shin Kong

Shin Kong Investment Trust Co., Ltd. Financial Statements for the Years Ended, 2014 and 2013 and Independent Auditors Report INDEPENDENT AUDITORS REPORT The Board of Directors and stockholder Shin Kong

FINCA International, Inc. Consolidated Financial Statements as of and for the Years Ended December 31, 2013 and 2012, and Independent Auditors Report

FINCA International, Inc. Consolidated Financial Statements as of and for the Years Ended December 31, 2013 and 2012, and Independent Auditors Report FINCA INTERNATIONAL, INC. TABLE OF CONTENTS INDEPENDENT

FINCA International, Inc. Consolidated Financial Statements as of and for the Years Ended December 31, 2013 and 2012, and Independent Auditors Report FINCA INTERNATIONAL, INC. TABLE OF CONTENTS INDEPENDENT

STANDARD DOCUMENT COVER SHEET FOR SEC FILINGS. SEC Number 121 File Number

STANDARD DOCUMENT COVER SHEET FOR SEC FILINGS All documents should be submitted under a cover page which clearly identifies the company and the specific document form as follows: SEC Number 121 File Number

STANDARD DOCUMENT COVER SHEET FOR SEC FILINGS All documents should be submitted under a cover page which clearly identifies the company and the specific document form as follows: SEC Number 121 File Number

Consolidated Financial Statements For the Year Ended 31 December 2015

Consolidated Financial Statements For the Year Ended 31 December 2015 Consolidated Statement of Financial Position As at 31 December 2015 2015 2014 ASSETS Notes QR000 QR000 Cash and Balances with Central

Consolidated Financial Statements For the Year Ended 31 December 2015 Consolidated Statement of Financial Position As at 31 December 2015 2015 2014 ASSETS Notes QR000 QR000 Cash and Balances with Central

Near East Bank Limited And its Subsidiary. Consolidated financial statements as at and for the year ended December 31, 2012

Near East Bank Limited And its Subsidiary Consolidated financial statements as at and for the year ended 2012 Consolidated statement of income...1 Consolidated statement of comprehensive income......2

Near East Bank Limited And its Subsidiary Consolidated financial statements as at and for the year ended 2012 Consolidated statement of income...1 Consolidated statement of comprehensive income......2

CEZ GROUP CONSOLIDATED FINANCIAL STATEMENTS PREPARED IN ACCORDANCE WITH INTERNATIONAL FINANCIAL REPORTING STANDARDS AS OF DECEMBER 31, 2015

CEZ GROUP CONSOLIDATED FINANCIAL STATEMENTS PREPARED IN ACCORDANCE WITH INTERNATIONAL FINANCIAL REPORTING STANDARDS AS OF DECEMBER 31, 2015 PRELIMINARY UNAUDITED ACCOUNTS Prepared as of March 14, 2016

CEZ GROUP CONSOLIDATED FINANCIAL STATEMENTS PREPARED IN ACCORDANCE WITH INTERNATIONAL FINANCIAL REPORTING STANDARDS AS OF DECEMBER 31, 2015 PRELIMINARY UNAUDITED ACCOUNTS Prepared as of March 14, 2016

Consolidated Financial Statements

Consolidated Financial Statements Table of Contents CONSOLIDATED FINANCIAL STATEMENTS 102 Management s Responsibility for Financial Information 103 Independent Auditors Report of Registered Public Accounting

Consolidated Financial Statements Table of Contents CONSOLIDATED FINANCIAL STATEMENTS 102 Management s Responsibility for Financial Information 103 Independent Auditors Report of Registered Public Accounting

CAE INC. CONSOLIDATED FINANCIAL STATEMENTS

CAE INC. CONSOLIDATED FINANCIAL STATEMENTS Management s Report on Internal Control Over Financial Reporting 1 Report of Independent Registered Public Accounting Firm 1 Consolidated Financial Statements

CAE INC. CONSOLIDATED FINANCIAL STATEMENTS Management s Report on Internal Control Over Financial Reporting 1 Report of Independent Registered Public Accounting Firm 1 Consolidated Financial Statements

JOINT STOCK COMPANY "SAVINGS BANK "BELARUSBANK" Consolidated Financial Statements

JOINT STOCK COMPANY "SAVINGS BANK "BELARUSBANK" Consolidated Financial Statements Year ended 31 December 2012 Together with Independent Auditors' Report "Savings Bank "Belarusbank" Consolidated financial

JOINT STOCK COMPANY "SAVINGS BANK "BELARUSBANK" Consolidated Financial Statements Year ended 31 December 2012 Together with Independent Auditors' Report "Savings Bank "Belarusbank" Consolidated financial

Summary of Significant Differences between Japanese GAAP and U.S. GAAP

Summary of Significant Differences between Japanese GAAP and U.S. GAAP The consolidated financial statements of SMFG and its subsidiaries presented in this annual report conform with generally accepted

Summary of Significant Differences between Japanese GAAP and U.S. GAAP The consolidated financial statements of SMFG and its subsidiaries presented in this annual report conform with generally accepted

IFRS Illustrative Consolidated Financial Statements 2014

IFRS Illustrative Consolidated Financial Statements 2014 1 PKF International Limited administers a network of legally independent member firms which carry on separate businesses under the PKF Name. PKF

IFRS Illustrative Consolidated Financial Statements 2014 1 PKF International Limited administers a network of legally independent member firms which carry on separate businesses under the PKF Name. PKF

Consolidated financial statements 2014. Zurich Insurance Group Annual Report 2014

Consolidated financial statements 2014 Annual Report 2014 2 Annual results 2014 Consolidated financial statements Contents Consolidated income statements 3 Consolidated statements of comprehensive income

Consolidated financial statements 2014 Annual Report 2014 2 Annual results 2014 Consolidated financial statements Contents Consolidated income statements 3 Consolidated statements of comprehensive income

ANNUAL FINANCIAL RESULTS

ANNUAL FINANCIAL RESULTS For the year ended 31 July 2013 ANNUAL FINANCIAL RESULTS 2013 FONTERRA CO-OPERATIVE GROUP LIMITED Contents: DIRECTORS STATEMENT... 1 INCOME STATEMENT... 2 STATEMENT OF COMPREHENSIVE

ANNUAL FINANCIAL RESULTS For the year ended 31 July 2013 ANNUAL FINANCIAL RESULTS 2013 FONTERRA CO-OPERATIVE GROUP LIMITED Contents: DIRECTORS STATEMENT... 1 INCOME STATEMENT... 2 STATEMENT OF COMPREHENSIVE

SSAP 24 STATEMENT OF STANDARD ACCOUNTING PRACTICE 24 ACCOUNTING FOR INVESTMENTS IN SECURITIES

SSAP 24 STATEMENT OF STANDARD ACCOUNTING PRACTICE 24 ACCOUNTING FOR INVESTMENTS IN SECURITIES (Issued April 1999) The standards, which have been set in bold italic type, should be read in the context of

SSAP 24 STATEMENT OF STANDARD ACCOUNTING PRACTICE 24 ACCOUNTING FOR INVESTMENTS IN SECURITIES (Issued April 1999) The standards, which have been set in bold italic type, should be read in the context of

NOTES TO THE COMPANY FINANCIAL STATEMENTS

FINANCIAL S 78 79 80 81 82 CONSOLIDATED INCOME CONSOLIDATED OF COMPREHENSIVE INCOME CONSOLIDATED OF FINANCIAL POSITION CONSOLIDATED OF CONSOLIDATED OF CHANGES IN EQUITY 83 NOTES TO THE CONSOLIDATED FINANCIAL

FINANCIAL S 78 79 80 81 82 CONSOLIDATED INCOME CONSOLIDATED OF COMPREHENSIVE INCOME CONSOLIDATED OF FINANCIAL POSITION CONSOLIDATED OF CONSOLIDATED OF CHANGES IN EQUITY 83 NOTES TO THE CONSOLIDATED FINANCIAL

Acal plc. Accounting policies March 2006

Acal plc Accounting policies March 2006 Basis of preparation The consolidated financial statements of Acal plc and all its subsidiaries have been prepared in accordance with International Financial Reporting

Acal plc Accounting policies March 2006 Basis of preparation The consolidated financial statements of Acal plc and all its subsidiaries have been prepared in accordance with International Financial Reporting

Consolidated financial statements

Summary of significant accounting policies Basis of preparation DSM s consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) as adopted

Summary of significant accounting policies Basis of preparation DSM s consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) as adopted

TAKASHIMAYA FINANCIAL STATEMENTS

TAKASHIMAYA FINANCIAL STATEMENTS Years ended February 29, and February 28, 2011 CONSOLIDATED BALANCE SHEETS Takashimaya Company, Limited and Consolidated Subsidiaries February 29, and February 28, 2011

TAKASHIMAYA FINANCIAL STATEMENTS Years ended February 29, and February 28, 2011 CONSOLIDATED BALANCE SHEETS Takashimaya Company, Limited and Consolidated Subsidiaries February 29, and February 28, 2011

Consolidated Financial Statements

Consolidated Financial Statements Reports 111 Management s responsibility for financial reporting 111 Report of Independent Registered Chartered Accountants 112 Management s report on internal control

Consolidated Financial Statements Reports 111 Management s responsibility for financial reporting 111 Report of Independent Registered Chartered Accountants 112 Management s report on internal control

OJSC «OTP Bank» Financial Statements For the Year Ended December 31, 2009

OJSC «OTP Bank» Financial Statements For the Year Ended OJSC «OTP Bank» TABLE OF CONTENTS Page STATEMENT OF MANAGEMENT S RESPONSIBILITIES FOR THE PREPARATION AND APPROVAL OF THE FINANCIAL STATEMENTS 1

OJSC «OTP Bank» Financial Statements For the Year Ended OJSC «OTP Bank» TABLE OF CONTENTS Page STATEMENT OF MANAGEMENT S RESPONSIBILITIES FOR THE PREPARATION AND APPROVAL OF THE FINANCIAL STATEMENTS 1

ILLUSTRATIVE FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2013 International Financial Reporting Standards

ILLUSTRATIVE FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2013 International Financial Reporting Standards 2 A Layout (International) Group Ltd Annual report and financial statements For the year ended

ILLUSTRATIVE FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2013 International Financial Reporting Standards 2 A Layout (International) Group Ltd Annual report and financial statements For the year ended

INGENICO GROUP Consolidated Financial Statements

INGENICO GROUP Consolidated Financial Statements December 31, 2014 Ingenico Consolidated Financial Statements December 31, 2014 I. CONSOLIDATED INCOME STATEMENTS For the years ended December 31, 2014 and

INGENICO GROUP Consolidated Financial Statements December 31, 2014 Ingenico Consolidated Financial Statements December 31, 2014 I. CONSOLIDATED INCOME STATEMENTS For the years ended December 31, 2014 and

Consolidated Financial Statements. FUJIFILM Holdings Corporation and Subsidiaries. March 31, 2015 with Report of Independent Auditors

Consolidated Financial Statements FUJIFILM Holdings Corporation and Subsidiaries March 31, 2015 with Report of Independent Auditors Consolidated Financial Statements March 31, 2015 Contents Report of Independent

Consolidated Financial Statements FUJIFILM Holdings Corporation and Subsidiaries March 31, 2015 with Report of Independent Auditors Consolidated Financial Statements March 31, 2015 Contents Report of Independent

CSCBANK S.A.L. (FORMERLY CREDITCARD SERVICES COMPANY S.A.L.)

") CSCBANK S.A.L. (FORMERLY CREDITCARD SERVICES COMPANY S.A.L.) CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS REPORT YEAR ENDED DECEMBER 31, 2010 CSCBANK S.A.L. (FORMERLY CREDITCARD SERVICES

CSCBANK S.A.L. (FORMERLY CREDITCARD SERVICES COMPANY S.A.L.) CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS REPORT YEAR ENDED DECEMBER 31, 2010 CSCBANK S.A.L. (FORMERLY CREDITCARD SERVICES

Preliminary Final report

Appendix 4E Rule 4.3A Preliminary Final report AMCOR LIMITED ABN 62 000 017 372 1. Details of the reporting period and the previous corresponding period Reporting Period: Year Ended Previous Corresponding