The Reverse Mortgage Analyst

|

|

|

- Clarence Clark

- 10 years ago

- Views:

Transcription

1 The Reverse Mortgage Analyst Illustrated User Manual May 26, 2009 version Christena Schafale, Consultant, AARP Foundation

2 Table of Contents Using this Manual... 1 Getting Started... 1 The Navigator... 2 Entering Counselor Information... 3 Entering New Client Information... 4 Get Client... 6 Loan Estimates... 7 Payment Options Creditline Tenure Modified Tenure Term Modified Term Creditline Scenarios Amortization Schedule Creditline Draw Estimates Comparing Loan Costs and Benefits Using the Charts Function TALC HECM Certificates HECM Refinance Counseling Comparing Refinance Costs and Benefits Refi Disclosure Sell & Move Annuity Comparison HECM for Purchase Print & Technical Specifications User Support... 30

3 Using this Manual If you are just getting started using Ibis RMA, it will be helpful to try out all the features and see how they work. This manual will lead you through an exploration of the program, with illustrations showing how the screens will look as you go along. You may want to read through the text once first, then sit down at the computer, open Ibis RMA, and follow along, entering sample client data and trying out features. Getting Started To access the Ibis Reverse Mortgage Analyst, open your browser and go to: You will see the login screen, where you will enter your username and password. 1

4 The Navigator When you open the software, you will find yourself at the Navigator screen. The Navigator is a roadmap to all the other places in the program. The initial Navigator screen that you see is a simplified one. Once you have entered client data, you will see a Navigator screen with many more options. Tip: When selecting a button on the Navigator screen, click the text inside the button, not the blank areas. You will know you are in the right place when the words appear underlined. 2

5 Entering Counselor Information The first time you use the Ibis RMA, you will need to enter information about yourself and your agency. This information is used to generate printable counseling certificates. Once you have entered and saved this information, you won t have to do it again. To enter counselor information, click on on the Navigator screen. Now fill in the blanks. Click Save at the bottom of the screen, which will save your information and return you to the Navigator. If the counselor is based at a different physical location from the agency they work for, the counselor s info would be placed in the first section, and the agency s information (which will appear on the certificate) would appear in the second section. 3

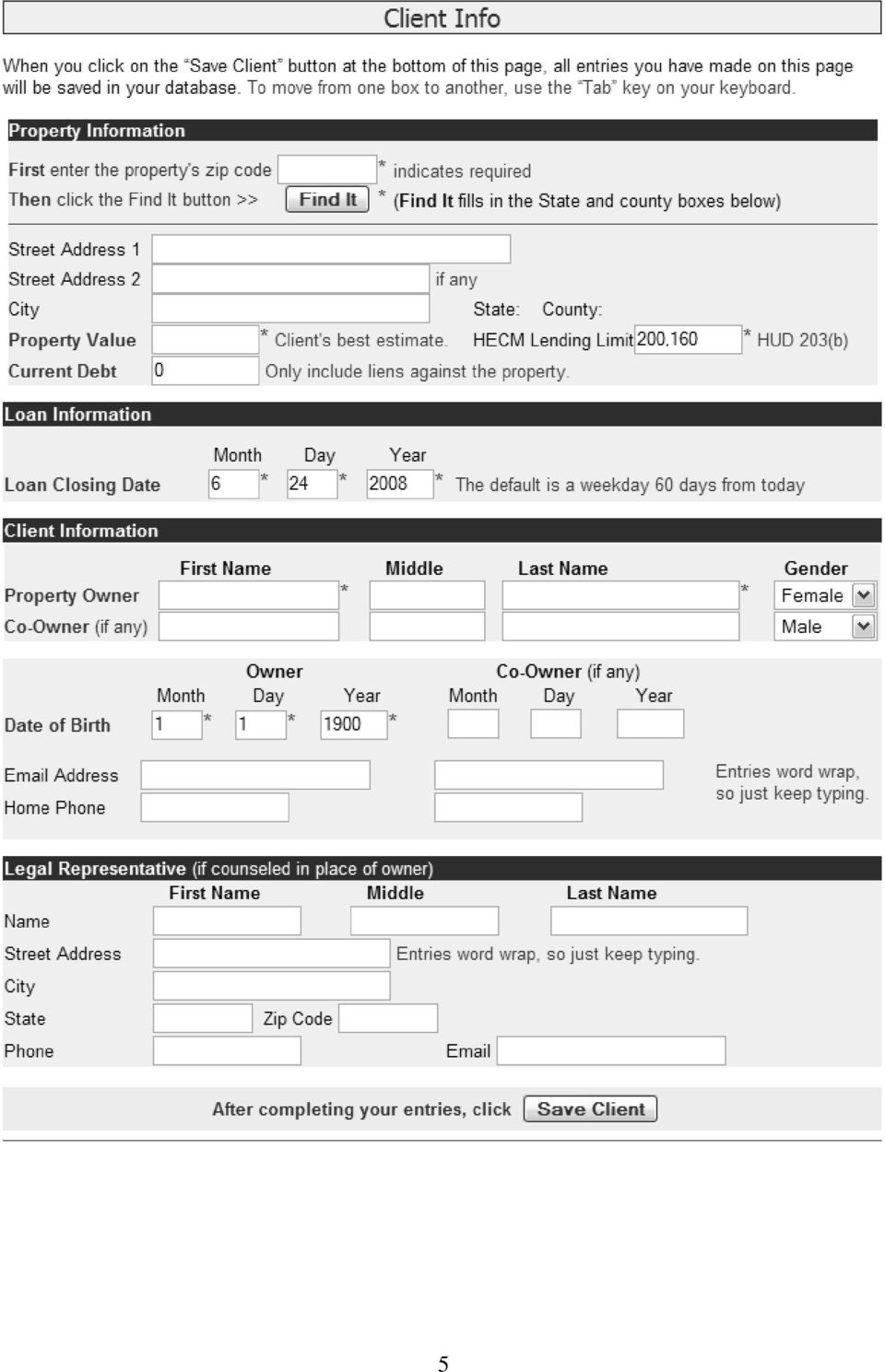

6 Entering New Client Information Click on (at the top left of the Navigator page). This will take you to the Client Info page, where you will enter data about your clients. Data Entry Tips: Use the Tab key to move from one field to another. You cannot enter the client s state and county info manually. You must enter the zip code and use the Find It button. When entering the Month of the client s Date of Birth, use the month s number. For example, for March enter 3. Word wrap means that you can type in more than appears to fit in the box; so just keep typing. Required fields are marked with a red asterisk. First, enter the 5-digit zip code in which this client s home is located. Then click on the boxes. button. This will cause the home s state and county to be entered into those Some zip codes cover more than one county. If the zip code you enter is one of these, you will be shown a list of counties in that zip code. Select the county where the home is located. Note that the zip code is needed despite the national lending limit, because Ibis uses the zip code to provide localized estimates of third-party closing costs. Required Entries: The boxes marked with a red asterisk (*) must be completed, or you will not be able to save the data you have entered. To be sure that estimates are calculated correctly, be sure to enter info for the co-owner, if there is one. If a legal representative (guardian, conservator, or power of attorney) is being counseled instead of the owner, you may enter this information as well. In the Current Debt box, enter the total amount of any current debt against the home, for example, mortgages or outstanding balances on home equity lines of credit. Do not include any other debt such as credit cards or car loans. When all required boxes are complete, click on at the bottom of the page. This will save all of the client data you have entered to the secure online database associated with your User ID. If you have entered all the required data, clicking on Save Client will also take you to the Loan Estimates page. If you are missing any required info, an error message will remind you what you need to enter. DON T FORGET TO SAVE YOUR CLIENT! 4

7 5

8 Get Client If you have already entered client data and want to retrieve it, click on on the Navigator page. This takes you to the Select a Client page, where you can open a client s record by clicking on the borrower s name. Clicking on the client s name selects that client and takes you to the Estimates page for that client. The selected client s name and age will now appear at the top of any page you go to. By default, the clients are listed by the date of the most recent revision, with the most recentlyedited records at the top.. You can change this by clicking on the heading at the top of each column, if you would prefer to search the list by the client s name, by the date they were originally entered, or by the user who entered them. If a client name appears at the top of this page, that client s current Client Info and Settings data will automatically be saved when you click anything on this page. If you delete one of your clients from the Select a Client page, the client s name will disappear from the list, but their data will be archived with your User ID. A site administrator would be able to reactivate the client at your request, in case of an accidental deletion. 6

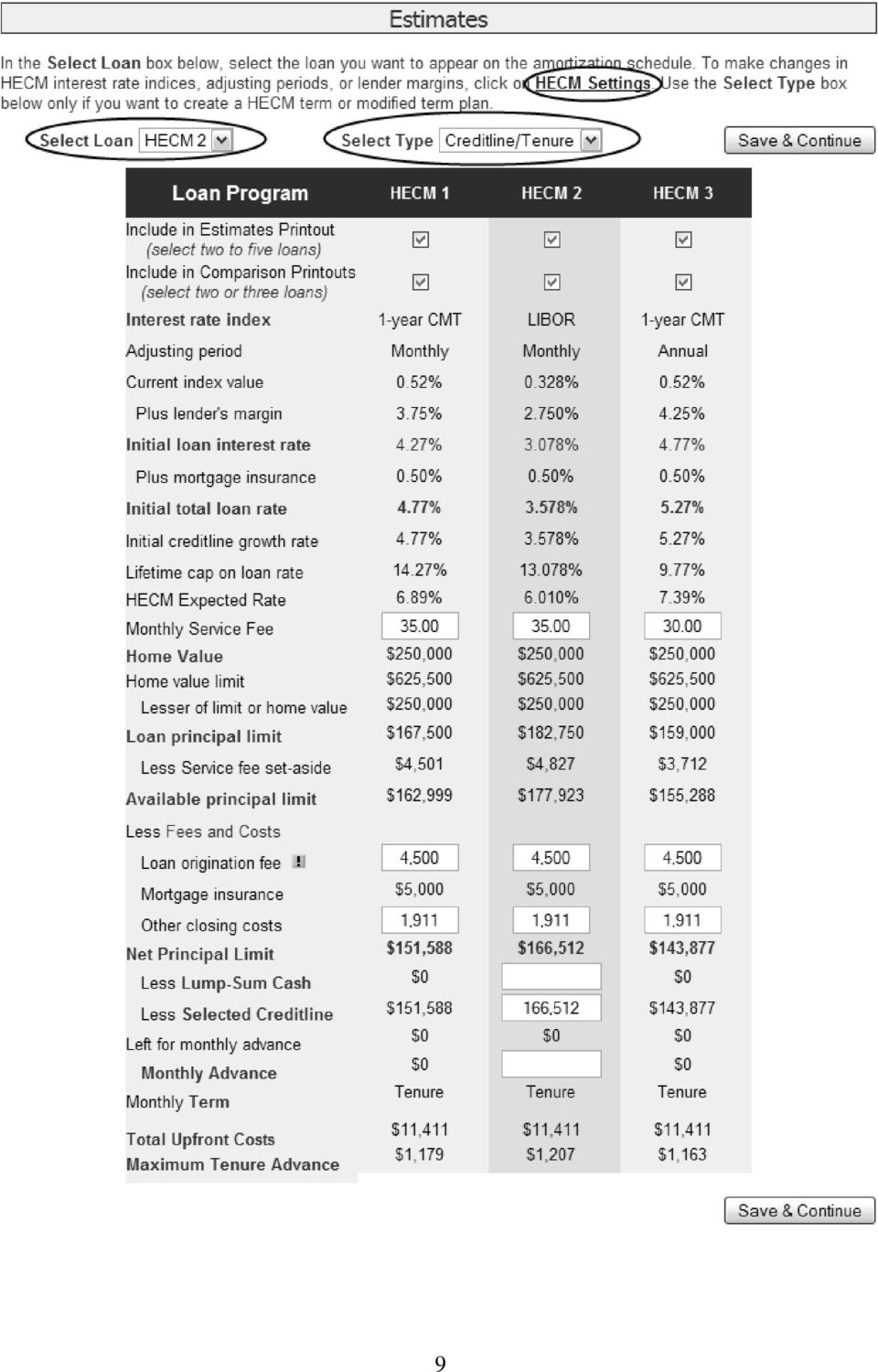

9 Loan Estimates Here you will see three sample HECM loans and two empty columns into which you can enter data for non-hecm loans. The three HECMs shown by default are based on three different combinations of interest rate type, index, and margin. These default settings are subject to change as prevailing interest rates change. Changing Margins: If you need to change the margins or select a different index, click on HECM Settings at the top of the page. This will take you to a page where you can make these choices. Note that, for previously entered clients, the system will retain the index rates used the last time you did calculations for this client. If you want to update to current rates, click the Current Rates button at the bottom of the screen. Choosing a Fixed Rate: The dropdown boxes next to Adjusting Period allow you to select Monthly-adjusting, Annual-adjusting, or Fixed Rate loans. If you select Fixed Rate, click Current Rate, which will refresh the screen so that you can see the current default rate, which you can change if needed. Take note of which column (HECM 1, 2 or 3) you are using for Fixed Rate; this will be reflected on the Estimates page. You will need to select this column in order to have the fixed rate reflected in the Amortization schedule and other printouts. 7

10 The checkboxes at the top of the Estimates page allow you to specify which loans will appear on loan printouts and comparisons. (See page 25 for directions on creating, printing, saving, and ing PDF printouts.) The Select Loan box: appears just above the words Loan Program in the upper left of the page. It is used to choose and highlight a specific loan on the page, which allows you to place some or all of the Net Principal Limit into an initial Lump-Sum Cash advance or a Monthly Advance. It also allows you to select which loan will be reflected in an amortization schedule. The Select Type box: (just to the right of the Select Loan box) displays Creditline/Tenure by default. You can change this setting if you want to generate a HECM term or modified term loan with monthly payments for a specific period of time, or specific monthly payments that are larger than those allowed by a tenure plan. Leave it as is if you want to show tenure or creditline options. Data Entry Tip: You can change data that appears in any box with a white background. Enter your new data, then hit the Tab key on your keyboard or click on any other data entry box on the page to recalculate. Don t forget to click the Save & Continue button at the top or bottom before you leave this page! If you don t, you will lose the information you just entered. Hitting the Enter key has the same effect as clicking Save & Continue, taking you to the Scenarios page. Use your Back button or the Estimates link at the top of the page to get back to the Estimates page. Non-HECM Loans You can also enter data about any non-hecm loan in the columns called OTHER-1 and OTHER-2. To do this, you will need to obtain the data from printouts or other information provided to your client by a lender. Entering data on non-hecm loans will allow you to generate amortization schedules and side-by-side loan comparisons with HECM loans. If a non-hecm loan does not have a given feature (for example, if it does not provide any creditline growth, or doesn t have a servicing fee set-aside), just leave the entry box blank. If a loan has a "teaser" interest rate (for example, a lower rate for the first six months), do not enter the teaser rate as the "Initial Total Loan Rate." Instead, enter the rate that will be in effect when the teaser rate ends. For example, if the initial teaser rate is 7% but it will increase to 7.5% after six months, enter 7.5% as the "Initial Total Loan Rate" because that's the rate that will be in effect for all but six months of the loan. 8

displays Creditline/Tenure by default.")

11 9

12 Payment options Creditline: By default, all funds will be placed in a creditline. If that s what your client wants, leave things as is. Click the Save & Continue button at the top of the page to proceed to the Scenarios page to specify a pattern of creditline draws. See below for details. Tenure: The maximum tenure payment is displayed at the bottom of the column for all clients. If your client is interested in receiving the maximum tenure payment, simply delete the Selected Creditline amount and click anywhere on the page to recalculate. The program will then fill in the maximum tenure amount in the Monthly Advance box. 10

13 Modified Tenure: To show a specific monthly payment and calculate what would be left in the line of credit, put the desired monthly amount in the Monthly Advance box. The available line of credit will now show up in the Less Selected Creditline box. To show a specific creditline amount and calculate the tenure payment that would be available, enter the desired creditline in the Selected Creditline box. The maximum monthly tenure payment that could be combined with that creditline will now appear in the Monthly Advance box. 11

14 Term: Go to the Select Type box: at the top of the screen. Choose HECM Term Plan from the dropdown menu. There are three pieces of information that will determine how much the term payment will be: 1. Selected Creditline, if any 2. Monthly Advance 3. Monthly Term in Years (how many years the borrower wants to receive monthly advances) You will need to specify two out of three in order to calculate the third. To calculate a term payment for a fixed number of years with nothing reserved in a creditline, o Enter 0 in the Selected Creditline box o Fill in the desired number of years in the Monthly Term in Years box. o Click the calculator icon next to the Monthly Advance box to calculate how much the monthly payment will be. To calculate a term payment based on a specific amount each month, with nothing reserved in a creditline, o Enter 0 in the Selected Creditline box o Fill in the desired monthly payment in the Monthly Advance box o Click the calculator icon next to the Monthly Term in Years box to calculate how many years payments will last. o Results will display the term in years and in months. There may be a small remainder left in the creditline. (Click again if number of months does not display correctly.) 12

15 Modified Term: There are three different ways to display a modified term plan. Specify creditline and monthly advance, then calculate term in years: o Enter the desired creditline amount in the Selected Creditline box o Enter the desired monthly payment amount o Click the calculator button next to Monthly Term in Years. Specify creditline and term in years, then calculate monthly advance o Enter the desired creditline amount in the Selected Creditline box o Enter the desired term in years in the Monthly Term in Years box o Click the calculator button next to Monthly Advance Specify monthly advance and term in years, calculate remaining creditline o Enter 0 in the Selected Creditline box o Enter the desired monthly advance o Enter the desired term in years o Click the calculator button next to Selected Creditline The button at the top or bottom of the page will save your work. It will also automatically take you to the Creditline Draw Scenarios page. 13

16 Creditline Scenarios If you have entered a creditline for your client, this page allows you to select the draw pattern and specify the dollar amounts that best approximate your client s intended or expected use of the creditline. The draws you specify here will be transferred into three key reports and make them more realistic for your client. You can show monthly or annual draws of any amount you select, or monthly or annual draws equal to projected creditline growth. You can also show up to 5 draws of different amounts at particular future times. For instance, your client might specify that he wants to take a trip costing $5000 in year 2 of the loan, then buy a car costing $15,000 in year 3, then give $10,000 to his grandchildren in year 5. You can then look at the results in several ways, by clicking on one of the three report buttons at the bottom of the page. 14

17 Amortization Schedule The Loan Amortization Schedule projects into the future the single loan you selected in the Select a Loan Program menu on the Loan Estimates page, using the draws you specified on the Scenarios page. 15

18 Assumptions The text at the top of the page explains the assumptions that go into the amortization schedule. These assumptions should be pointed out whenever you provide an amortization schedule, because the projected loan balances are only as accurate as the assumptions they are based on. By default, the schedule uses the initial interest rate and a predicted 4% appreciation rate. However, you can change these assumptions to better fit the client s situation, or to illustrate what would happen if the home did not appreciate as expected, for instance. o You can select one of four interest rates for projecting the loan s future balance: the loan s initial rate, that rate plus 2 points, or plus 4 points, or the loan s expected rate. o Appreciation rate can be changed to any percentage between -10% and +10%. Explanations The definitions at the bottom of the page provide an explanation of each column on the amortization schedule. Note that the net home value takes into account the projected costs of selling the home. (This is different from the home value column in FFRMA amortization schedules, which does not reflect costs of sale.) 16

19 Creditline Draw Estimates For each loan you select on the Estimates page, this report displays the client s selected creditline draws and the amount of funds remaining available in the creditline. To change the draws that are illustrated, click on Scenarios at the top or bottom of the page. To change which loans are selected, click on Estimates. 17

20 Comparing Loan Costs and Benefits The Comparison button on the Scenarios page or the Navigator takes you to the Reverse Mortgage Comparisons report. This report is similar to the Performance report found in the FFRMA software. It projects the loan into the future and shows the three basic facts about any reverse mortgage: Loan advances (what the borrower got) Loan costs (what it cost them to get it) Leftover equity (what the borrower or their estate has left after the loan is paid off) The Comparisons report allows you to compare these projections side-by-side for three different loans or loan variations, at five future points in time. The five points in time are the median projected remaining life expectancy for the youngest borrower, and 20%, 60%, 140%, and 180% of this median life expectancy. The report also includes a Total Annual Rate at each point in time, which is similar to the official Total Annual Loan Cost (TALC) rate, but takes into account client-specific creditline draws and other factors which may make it more useful to the borrower. This single percentage, like an APR, includes both interest charges and closing costs, and allows side-by-side comparison of loans with different kinds of costs. Assumptions Like the Amortization schedule, the Comparison report relies on some assumptions, including projected interest rate and appreciation rate. These assumptions can be changed using the boxes on the upper right hand side of the page. Explanations The software provides a 2-page handout that explains the Comparison report in detail. The handout should be given to clients whenever you provide the Comparison report. To review the handout, click on the button at the bottom of the page, which takes you to the first page. A link at the bottom of the first page leads to the second page of the handout. Charts To show your client a visual representation of the numerical information presented on the Comparisons page, Ibis RMA provides pie charts. Click on the link at the top of the Comparisons page to access the charts. There is also a link to the charts on the Navigator page, at the far right. 18

The Comparisons report allows you to compare these projections side-by-side for three different loans or loan variations, at five")

21 19

22 Using the Charts Function Clicking the Charts link on the Navigation page or from the Comparisons page takes you to the Charts page. Here you will have the opportunity to display pie charts showing a visual representation of the same data that is displayed numerically on the Comparisons page. Pie charts like these can make it much easier for some clients to grasp the growth of their loan balance and the shrinkage of their remaining equity. First, check the assumptions that you want to use. By default, the Charts page will pick up the assumptions you used on the Comparisons page (by default, a 4% appreciation rate and projecting the loan at the initial interest rate), but you can change these assumptions at the top right. Next, you have a number of choices about which comparisons to display. First, you ll want to think about whether you want to show one loan program compared to another (e.g., two HECM loans with different interest rates), or comparing two different points in time for the same loan (e.g., year 2 vs. year 14). Make that selection at the top left. If you decide to show two loans in one period, then you will need to select what time period you want to show, and then which two loans you want to compare. If, instead, you want to show one loan at two different time points, you ll first select the loan program, then select the two time periods. After making changes to these options, you may see a Refresh Charts button. Click it to make the charts reflect your new choices. To print out the charts, click the Print Charts button at the bottom of the page. 20

23 21

24 TALC To meet HUD specifications for a pre-counseling package to be sent to all clients, Ibis RMA includes the ability to generate a TALC disclosure similar to the one that clients must receive from their lender. This gives the counselor an opportunity to educate the client about the meaning of this complex disclosure. The TALC disclosure can be accessed using the Navigator page. Look for the TALC button on the far right side. The TALC disclosure is also included by default in the pre-counseling package generated by Ibis. The TALC calculation will be based on your selected loan product and payment plan, so be sure these options are selected correctly before you generate the TALC disclosure. 22

25 HECM Certificates Ibis RMA can generate your HECM counseling certificates for you, with all the counselor, client, and session info inserted. Session Info At the Navigator, click on. Enter the information about your session, including the amount of time it took and what fees were/should be charged. When you are finished, click the Save Session button, which will save your information and take you back to the Navigator. Certificate From the Navigator, click on the button to create a HECM counseling certificate in PDF format. The certificate will open with Adobe Acrobat Reader. Depending on your browser settings, Reader may appear as a separate program window, or it may appear inside your browser window. Use the printer icon or the Print command on the File menu to print out as many copies as you need. If you have made changes in your session info, be sure to check the certificate before printing to be sure that the counseling date and amount of time are shown correctly. 23

26 HECM Refinance Counseling Ibis RMA provides support for the special calculations that are needed when a client is considering a refinance of a HECM Loan. To access these calculations, go to the Navigator and click on The text at the top of the Refinancing a HECM with a HECM page explains how the mortgage insurance premium is calculated for a HECM refi, and the conditions under which clients are permitted to waive the counseling requirement. To calculate the costs and benefits of a refi for your client, you will need several pieces of information: Maximum Claim Amount from the original HECM Current Principal Limit Current Payoff on Existing HECM This information can be obtained from the client s loan servicer or from the original loan documents and a recent loan statement. Enter this information into the boxes at the bottom of the page. Then click on the button, which takes you to the Comparing Refinance Costs & Benefits page. 24

27 Comparing Refinance Costs & Benefits This page provides calculations of the new Principal Limit and the costs associated with refinancing. Note that the Upfront Cash on the new HECM figure includes the lien payoff for the old HECM plus any lump-sum cash draw that you may have entered on the Estimates page. The Ratio of PL Increase/Total Cost is an indicator of how well the benefits of a refi compare to the costs. A ratio of 5:1 or greater indicates that there is substantial benefit to the borrower, and is also one of the criteria that must be met if the borrower wishes to waive the counseling requirement. The Current Principal Limit minus Total Costs of Refinancing, minus the Current Payoff on Existing HECM, would give you the cash available to the borrower from the new HECM. This figure appears on the Refi Disclosure page. Refi Disclosure The button will take you to a Sample Refinance Disclosure. This is a copy of the official HUD Anti-Churning Disclosure, which the lender is required to provide to the borrower. Since the lender may not actually provide the official disclosure until the closing, it can be helpful for the counselor to prepare a sample disclosure using the best information available at the time of counseling. 25

28 Sell & Move Selling and moving is an important option to consider, because it helps clients evaluate how important it is to them to continue living in their current homes. The Reverse Mortgage Analyst provides an individually-customized one-page handout on this choice. To access it, a client name must appear in the upper left-hand part of the Navigator. Click on Sell & Move, which takes you to the Selling Your Home page. The figures in the second paragraph of this page are based on your current client s information. These figures do not take tax considerations into account, but they provide a general sense of the economics of selling and moving. Annuity Comparison If your client is considering the purchase of an annuity with reverse mortgage proceeds, a 3-page handout on this topic is available in HUD s HECM Counseling Protocol. The second page of that 3-page handout explains that software meeting the model specifications cited above can generate a side-by-side comparison of the costs and benefits of using a HECM to purchase an annuity versus a HECM tenure plan. The Reverse Mortgage Analyst has an annuity comparison feature that is currently available to site administrators only. 26

29 HECM for Purchase Ibis does not have a special module for calculating HECM for Purchase transactions, but it can certainly be used to generate the numbers you need. Here s how: As with any HECM, the loan amount depends on the value of the property, the age of the youngest borrower, and the expected interest rate. However, what most borrowers really want to know is, how much money they will need to bring to the table in order to complete the transaction. Using the Ibis Reverse Mortgage Analyst, the HECM loan amount, and the borrower s required investment on a HECM for Purchase can be calculated as follows: Initial input: Zip code Property value = Estimated appraised value or negotiated purchase price of the subject property, whichever is lower Current liens = Property value as above PLUS estimated purchase costs such as recordation fees and transfer taxes (if known). Name and date of birth of each borrower (everyone who will be on title) Output: Principal Limit = total amount of HECM Net Principal Limit = amount the HECM will provide toward the purchase Program is Short By = minimum required monetary investment. If they have already paid earnest money, subtract that figure to get the amount they must bring to closing. If the client has not yet found a house they want to buy,and wants to know how much house they could afford to buy using a HECM, based on a set amount of money they have to contribute, the counselor will need to take a guess at the purchase price that might work, and then redo the calculations as needed to come as close as possible to the client s desired scenario. For instance, borrower has $100,000 to spend. Counselor might start by using a $200,000 home value, and see what figure they get in the Program is Short By field. If it s higher than $100,000, try a lower home value. If it s lower than $100,000, try a higher home value. Keep doing this until you get as close as you need to be. In future, Ibis may add a HECM for Purchase feature that will make this easier, but this approach will work until that time. 27

30 Print & Click on Navigator and then on. Follow the instructions on this page to generate, view, print out, save, and a PDF file that includes whichever reports you select for your current client. You can also print individual pages at any point while using Ibis, by using the Print menu in your browser, or the Print Page link at the bottom of each page; however, the output that you will get may not look as good as what you get from the Print & page. For example, the Estimates page may print across two pages instead of being sized to fit a single sheet. On the Print & page, you can select which reports you would like to print or . The three reports required by HUD for the pre-counseling package are pre-selected by default. Once you have chosen which reports to generate, click Build Package. A notification will pop up, telling you that your package is complete. Click OK to view the package immediately, or close the window if you don t want to view the package right away. Clicking OK should cause a new window to open, displaying the first page of your package in Adobe Reader. If no window appears, check your browser settings to be sure you haven t blocked all popups. If so, change your settings to allow popups from IbisRMA.com. 28

31 Once the new window is showing, you can enlarge it, review the printouts, and decide if everything looks right. If you build a package more than once, you will see a list of all packages built for that client. Each one is dated so you can tell them apart. The most recent one will appear at the top of the list by default. From the list of packages, you can view any package, or set up an to send the package to yourself or someone else. If you click on the icon, you will have the opportunity to insert addresses and personalize a message to the recipients. 29

32 Technical Specifications The Reverse Mortgage Analyst software meets the "Model Specifications for Analyzing and Comparing Reverse Mortgages" developed by the AARP Foundation s Reverse Mortgage Education Project with support from HUD. General information on the model specifications can be found at and a copy of the specifications at: assets.aarp.org/ User Support Call Ibis Customer Service between 1 PM and 2 PM Pacific time (4-5 PM Eastern), Monday- Friday at or send an to [email protected] with a question or a requested time for us to call you. Exam-qualified counselors who have access to hecmcounselors.org can also use the Ibis Forum to ask question. Check the forum archives to see if your question has already been answered. 30

Table of Contents Reverse Mortgage O verview... Reverse Mortgage K ey Questions... 5 Reverse Mortgage Pros and Cons... 7 Reverse Mortgage Borr

1 Table of Contents Reverse Mortgage Overview... Reverse Mortgage Key Questions... Reverse Mortgage Pros and Cons... Reverse Mortgage Borrower Qualification... Reverse Mortgage Key Items... Reverse Mortgage

1 Table of Contents Reverse Mortgage Overview... Reverse Mortgage Key Questions... Reverse Mortgage Pros and Cons... Reverse Mortgage Borrower Qualification... Reverse Mortgage Key Items... Reverse Mortgage

How To Compare Reverse Mortgages

Model Specifications for Analyzing and Comparing Reverse Mortgages To help consumers and their advisors make informed decisions about reverse mortgages, AARP has developed these model specifications for

Model Specifications for Analyzing and Comparing Reverse Mortgages To help consumers and their advisors make informed decisions about reverse mortgages, AARP has developed these model specifications for

housing information www.housing-information.org Reverse Mortgages A project of Consumer Action

housing information www.housing-information.org Reverse Mortgages A project of Consumer Action One of the major benefits of buying a home is the opportunity to build equity, or ownership, in the property.

housing information www.housing-information.org Reverse Mortgages A project of Consumer Action One of the major benefits of buying a home is the opportunity to build equity, or ownership, in the property.

Refinance Info Online Application Steps and Helpful Hints

Refinance Info Online Application Steps and Helpful Hints Get Started: Select a type of loan Select Refinance. The property you are looking to refinance must be located in Florida in order to utilize GTE

Refinance Info Online Application Steps and Helpful Hints Get Started: Select a type of loan Select Refinance. The property you are looking to refinance must be located in Florida in order to utilize GTE

Reverse Mortgage Counseling Checklist

Reverse Mortgage Counseling Checklist Have these items available for your counseling session... - Loan Comparison Page The calculator loan results is an estimate of available reverse mortgage programs

Reverse Mortgage Counseling Checklist Have these items available for your counseling session... - Loan Comparison Page The calculator loan results is an estimate of available reverse mortgage programs

Payco, Inc. Evolution and Employee Portal. Payco Services, Inc.., 2013. 1 Home

Payco, Inc. Evolution and Employee Portal Payco Services, Inc.., 2013 1 Table of Contents Payco Services, Inc.., 2013 Table of Contents Installing Evolution... 4 Commonly Used Buttons... 5 Employee Information...

Payco, Inc. Evolution and Employee Portal Payco Services, Inc.., 2013 1 Table of Contents Payco Services, Inc.., 2013 Table of Contents Installing Evolution... 4 Commonly Used Buttons... 5 Employee Information...

Section D. Reverse Mortgage Loan Features and Costs Overview

Section D. Reverse Mortgage Loan Features and Costs Overview Contents This section contains the following topics: Topic See Page 1. Types of Reverse Mortgage Products 5-D-2 2. Reverse Mortgage Loan Limits

Section D. Reverse Mortgage Loan Features and Costs Overview Contents This section contains the following topics: Topic See Page 1. Types of Reverse Mortgage Products 5-D-2 2. Reverse Mortgage Loan Limits

eboutique TM Reverse Mortgage Servicing User s Guide

eboutique TM Reverse Mortgage Servicing User s Guide January 2008 2007-2008 Fannie Mae. Trademarks of Fannie Mae. eboutique User Guide 1 2007-2008 Fannie Mae. All rights reserved. eboutique is a trademark

eboutique TM Reverse Mortgage Servicing User s Guide January 2008 2007-2008 Fannie Mae. Trademarks of Fannie Mae. eboutique User Guide 1 2007-2008 Fannie Mae. All rights reserved. eboutique is a trademark

Complete Guide to Reverse Mortgages

Complete Guide to Reverse Mortgages Contents I. What Is a Reverse Mortgage? 2 Reasons for taking out a reverse mortgage 2 Differences between reverse and traditional mortgages 2 II. Where to Get Reverse

Complete Guide to Reverse Mortgages Contents I. What Is a Reverse Mortgage? 2 Reasons for taking out a reverse mortgage 2 Differences between reverse and traditional mortgages 2 II. Where to Get Reverse

OSP User Guide. 1 P a g e

Online School Payments (OSP) User Guide February, 2014 OSP User Guide Table of Contents Overview...3 Site Information...3 Login to Portal...4 Activity Setup...6 OSP Activity Setup Form...6 Add Activity...7

Online School Payments (OSP) User Guide February, 2014 OSP User Guide Table of Contents Overview...3 Site Information...3 Login to Portal...4 Activity Setup...6 OSP Activity Setup Form...6 Add Activity...7

Online School Payments (OSP) User Guide

User Guide") Online School Payments (OSP) User Guide November, 2013 OSP User Guide Table of Contents Overview...3 Site Information...3 Login to Portal...4 Activity Setup...6 OSP Activity Setup Form...6 Add Activity...7

Online School Payments (OSP) User Guide November, 2013 OSP User Guide Table of Contents Overview...3 Site Information...3 Login to Portal...4 Activity Setup...6 OSP Activity Setup Form...6 Add Activity...7

How To Understand A Reverse Mortgage

Introduction to Home Equity Conversion Mortgages (HECM) HO 111 COPYRIGHT REPRINT PERMISSION Copyright 2010NeighborhoodReinvestmentCorporation d/b/aneighborworks America. Allrightsreserved.Requestsforpermissiontoreproduce

Introduction to Home Equity Conversion Mortgages (HECM) HO 111 COPYRIGHT REPRINT PERMISSION Copyright 2010NeighborhoodReinvestmentCorporation d/b/aneighborworks America. Allrightsreserved.Requestsforpermissiontoreproduce

Wrightstown School District

Wrightstown School District Overview E-help desk gives you the ability to create your own Help Desk tickets. It also allows you to be able to check the status of your requests, and add updates (comments)

Wrightstown School District Overview E-help desk gives you the ability to create your own Help Desk tickets. It also allows you to be able to check the status of your requests, and add updates (comments)

Endorsing a HECM Case

Endorsing a HECM Case FHA-approved lenders may submit a request for FHA mortgage insurance for a Home Equity Conversion Mortgage (HECM) direct endorsement (DE) case using HECM Insurance Application. HECM

Endorsing a HECM Case FHA-approved lenders may submit a request for FHA mortgage insurance for a Home Equity Conversion Mortgage (HECM) direct endorsement (DE) case using HECM Insurance Application. HECM

Submitting a Loan to DO through Point

Submitting a Loan to DO through Point This document shows you how to work with a loan in Calyx Point and submit it to Fannie Mae Desktop Originator or Desktop Underwriter for underwriting. It is not intended

Submitting a Loan to DO through Point This document shows you how to work with a loan in Calyx Point and submit it to Fannie Mae Desktop Originator or Desktop Underwriter for underwriting. It is not intended

rbweb RB Web 8 online office for attorneys, paralegals and secretaries User Guide

rbweb RB Web 8 online office for attorneys, paralegals and secretaries User Guide Table of Contents Program Basics Logging in.... 1 Resetting password for security reasons.... 1 Navigating the site...

rbweb RB Web 8 online office for attorneys, paralegals and secretaries User Guide Table of Contents Program Basics Logging in.... 1 Resetting password for security reasons.... 1 Navigating the site...

GUIDE TO THE TRADING PLATFORM CONTENTS. Page OVERVIEW 2. ACCOUNT SUMMARY Transfer funds Account details

GUIDE TO THE TRADING PLATFORM CONTENTS OVERVIEW 2 Page ACCOUNT SUMMARY Transfer funds Account details 3 SPREAD & BINARY MARKETS Finding your market Opening and closing trades Opening Orders Closing Orders

GUIDE TO THE TRADING PLATFORM CONTENTS OVERVIEW 2 Page ACCOUNT SUMMARY Transfer funds Account details 3 SPREAD & BINARY MARKETS Finding your market Opening and closing trades Opening Orders Closing Orders

Chapter 14: Links. Types of Links. 1 Chapter 14: Links

1 Unlike a word processor, the pages that you create for a website do not really have any order. You can create as many pages as you like, in any order that you like. The way your website is arranged and

1 Unlike a word processor, the pages that you create for a website do not really have any order. You can create as many pages as you like, in any order that you like. The way your website is arranged and

DarwiNet Client Level

DarwiNet Client Level Table Of Contents Welcome to the Help area for your online payroll system.... 1 Getting Started... 3 Welcome to the Help area for your online payroll system.... 3 Logging In... 4

DarwiNet Client Level Table Of Contents Welcome to the Help area for your online payroll system.... 1 Getting Started... 3 Welcome to the Help area for your online payroll system.... 3 Logging In... 4

Online Banking User Guide

TABLE OF CONTENTS TABLE OF CONTENTS... 1 INTRODUCTION... 4 QUICK REFERENCE... 4 LOG ON... 4 SECURITY PROFILE... 4 ENTITLEMENTS... 4 LOG ON... 5 ENTER YOUR USERNAME... 5 REVIEW SECURE IMAGE AND PHRASE,

TABLE OF CONTENTS TABLE OF CONTENTS... 1 INTRODUCTION... 4 QUICK REFERENCE... 4 LOG ON... 4 SECURITY PROFILE... 4 ENTITLEMENTS... 4 LOG ON... 5 ENTER YOUR USERNAME... 5 REVIEW SECURE IMAGE AND PHRASE,

Creating a Digital Signature in Adobe Acrobat Created on 1/11/2013 2:48:00 PM

Creating a Digital Signature in Adobe Acrobat Created on 1/11/2013 2:48:00 PM Table of Contents Creating a Digital Signature in Adobe Acrobat... 1 Page ii Creating a Digital Signature in Adobe Acrobat

Creating a Digital Signature in Adobe Acrobat Created on 1/11/2013 2:48:00 PM Table of Contents Creating a Digital Signature in Adobe Acrobat... 1 Page ii Creating a Digital Signature in Adobe Acrobat

WEBSITE USER GUIDE. Undebt.it User Guide. May 2015. Version 1.0

WEBSITE USER GUIDE Undebt.it User Guide May 2015 Version 1.0 USER GUIDE Undebt.it is an online, mobile-friendly debt management tool There are various payment methods which can be very effective ways to

WEBSITE USER GUIDE Undebt.it User Guide May 2015 Version 1.0 USER GUIDE Undebt.it is an online, mobile-friendly debt management tool There are various payment methods which can be very effective ways to

Reverse Mortgage Glossary of Terms

Reverse Mortgage Glossary of Terms Acceleration Clause Adjustable Rate Annuity Appraisal Appreciation Available Principle Limit Change of Circumstance Closing Condemnation Correspondent Cost to Cure Credit

Reverse Mortgage Glossary of Terms Acceleration Clause Adjustable Rate Annuity Appraisal Appreciation Available Principle Limit Change of Circumstance Closing Condemnation Correspondent Cost to Cure Credit

How To Use Thecontinuus Provider Portal

PROVIDER PORTAL USER GUIDE OCTOBER 13, 2014 TOGETHER ADMINISTRATION OFFICE phone: 608-647-4729 toll free: 1-877-376-6113 fax: 608-647-4754 web: www.continuus.org email: [email protected] CONTENTS System

PROVIDER PORTAL USER GUIDE OCTOBER 13, 2014 TOGETHER ADMINISTRATION OFFICE phone: 608-647-4729 toll free: 1-877-376-6113 fax: 608-647-4754 web: www.continuus.org email: [email protected] CONTENTS System

Guide to Reverse Mortgages

Guide to Reverse Mortgages Prepared by Steve Juetten, CFP Juetten Personal Financial Planning, LLC. www.finpath.com 425-373-9393 Disclaimer: the information in this report was prepared from reliable sources;

Guide to Reverse Mortgages Prepared by Steve Juetten, CFP Juetten Personal Financial Planning, LLC. www.finpath.com 425-373-9393 Disclaimer: the information in this report was prepared from reliable sources;

NYS OCFS CMS Manual CHAPTER 1...1-1 CHAPTER 2...2-1 CHAPTER 3...3-1 CHAPTER 4...4-1. Contract Management System

NYS OCFS CMS Manual C O N T E N T S CHAPTER 1...1-1 Chapter 1: Introduction to the Contract Management System...1-2 Using the Contract Management System... 1-2 Accessing the Contract Management System...

NYS OCFS CMS Manual C O N T E N T S CHAPTER 1...1-1 Chapter 1: Introduction to the Contract Management System...1-2 Using the Contract Management System... 1-2 Accessing the Contract Management System...

Chapter 16: Squeezing the Last Drop Additional Material

Chapter 16: Squeezing the Last Drop Additional Material In my original manuscript, I had a more extensive discussion on reverse mortgages. Here s the full version. What about reverse mortgages? These are

Chapter 16: Squeezing the Last Drop Additional Material In my original manuscript, I had a more extensive discussion on reverse mortgages. Here s the full version. What about reverse mortgages? These are

Beginner s Guide to AIA Contract Documents Online Service for Single-Seat Users

Beginner s Guide to AIA Contract Documents Online Service for Single-Seat Users Table of Contents Getting Started - Introducing ACD5- AIA Contract Documents New Online Service System Requirements Transitioning

Beginner s Guide to AIA Contract Documents Online Service for Single-Seat Users Table of Contents Getting Started - Introducing ACD5- AIA Contract Documents New Online Service System Requirements Transitioning

Business Online Banking ACH Reference Guide

Business Online Banking ACH Reference Guide Creating an ACH Batch Select ACH Payments on the left-hand side of the screen. On the Database List screen, locate the Database to be processed, and place a

Business Online Banking ACH Reference Guide Creating an ACH Batch Select ACH Payments on the left-hand side of the screen. On the Database List screen, locate the Database to be processed, and place a

Table of Contents. zipform 6 User Guide

Table of Contents Welcome 4 Creating and Using Transactions.. 4 How to Create a Transaction...... 4 Creating a Transaction Using a Template....... 5 Adding and Removing Forms from a Transaction.......

Table of Contents Welcome 4 Creating and Using Transactions.. 4 How to Create a Transaction...... 4 Creating a Transaction Using a Template....... 5 Adding and Removing Forms from a Transaction.......

Frequently asked questions for advisors

1. How does your client qualify for a reverse mortgage? To become eligible for a reverse mortgage, the borrower must be at least 62 years old and own their home And have enough equity in the house to pay

1. How does your client qualify for a reverse mortgage? To become eligible for a reverse mortgage, the borrower must be at least 62 years old and own their home And have enough equity in the house to pay

The following information is provided to you by U.S. Department of Housing and Urban Development.

The following information is provided to you by U.S. Department of Housing and Urban Development. Attachment C: Resources for Clients C.1 Important Information about Reverse Mortgage Counselors C.2 Reverse

The following information is provided to you by U.S. Department of Housing and Urban Development. Attachment C: Resources for Clients C.1 Important Information about Reverse Mortgage Counselors C.2 Reverse

Moneyspire Help Manual. 2015 Moneyspire Inc. All rights reserved.

Moneyspire Help Manual 2015 Moneyspire Inc. All rights reserved. Getting Started Getting started with Moneyspire is easy. When you first start the program, you will be greeted with the welcome screen.

Moneyspire Help Manual 2015 Moneyspire Inc. All rights reserved. Getting Started Getting started with Moneyspire is easy. When you first start the program, you will be greeted with the welcome screen.

If you re 62 or older and looking for money

April 2009 Reverse Mortgages: Get the Facts Before Cashing in on Your Home s Equity If you re 62 or older and looking for money to finance a home improvement, pay off your current mortgage, supplement

April 2009 Reverse Mortgages: Get the Facts Before Cashing in on Your Home s Equity If you re 62 or older and looking for money to finance a home improvement, pay off your current mortgage, supplement

Contact Treasury Management Support: 866-563-1010 (toll free) Monday through Friday, 7:30 am 5:30 pm (Pacific Time) TreasuryManagement@umpquabank.

Monday through Friday, 7:30 am 5:30 pm (Pacific Time) TreasuryManagement@umpquabank.") Contact Treasury Management Support: 866-563-1010 (toll free) Monday through Friday, 7:30 am 5:30 pm (Pacific Time) [email protected] Updated November 2013 - TreasuryPro 3.8 Contents Welcome...

Contact Treasury Management Support: 866-563-1010 (toll free) Monday through Friday, 7:30 am 5:30 pm (Pacific Time) [email protected] Updated November 2013 - TreasuryPro 3.8 Contents Welcome...

Nationwide Mortgage Licensing System #222955

Nationwide Mortgage Licensing System #222955 Senior Concerns Is your mortgage paid off? Is your Social Security and/or pension sufficient? Rising costs of living: gas, health care, food, utilities, medications,

Nationwide Mortgage Licensing System #222955 Senior Concerns Is your mortgage paid off? Is your Social Security and/or pension sufficient? Rising costs of living: gas, health care, food, utilities, medications,

1 CoverMyMeds User s Guide User s Guide

1 CoverMyMeds User s Guide User s Guide 2 CoverMyMeds User s Guide TABLE OF CONTENTS Overview 3 Starting a Request 3 Using a Key 4 Completing the Request 5 Address Books 5 Required and Important Tags 5

1 CoverMyMeds User s Guide User s Guide 2 CoverMyMeds User s Guide TABLE OF CONTENTS Overview 3 Starting a Request 3 Using a Key 4 Completing the Request 5 Address Books 5 Required and Important Tags 5

Is A Reverse Mortgage Right for You?

Is A Reverse Mortgage Right for You? NewRetirement s Guide to Reverse Mortgages www.newretirement.com (877) 394-1305 Table of Contents What is a Reverse Mortgage? Are You Eligible For a Reverse Mortgage?

Is A Reverse Mortgage Right for You? NewRetirement s Guide to Reverse Mortgages www.newretirement.com (877) 394-1305 Table of Contents What is a Reverse Mortgage? Are You Eligible For a Reverse Mortgage?

THANK YOU FOR CHOOSING CAPITAL ONE BANK

KNOW ALL THE STEPS THANK YOU FOR CHOOSING CAPITAL ONE BANK WE RE HAPPY THAT YOU VE COME TO US FOR YOUR HOME LOAN NEEDS, AND WE LOOK FORWARD TO MAKING THE APPLICATION PROCESS AS CLEAR AS POSSIBLE. THIS

KNOW ALL THE STEPS THANK YOU FOR CHOOSING CAPITAL ONE BANK WE RE HAPPY THAT YOU VE COME TO US FOR YOUR HOME LOAN NEEDS, AND WE LOOK FORWARD TO MAKING THE APPLICATION PROCESS AS CLEAR AS POSSIBLE. THIS

FHA Reverse Mortgages for People 62 Years and Older

FHA Reverse Mortgages for People 62 Years and Older If you are age 62 or older you may want to participate in FHA's Home Equity Conversion Mortgage (HECM), better known as the Reverse Mortgage, program.

FHA Reverse Mortgages for People 62 Years and Older If you are age 62 or older you may want to participate in FHA's Home Equity Conversion Mortgage (HECM), better known as the Reverse Mortgage, program.

An Introduction to K12 s Online School (OLS)

") An Introduction to K12 s Online School (OLS) 1 Introducing the Online School (OLS)... 6 Logging In... 6 OLS Home page... 8 My Account Menu... 9 To Edit Basic Account Information for Yourself... 9 Tip:

An Introduction to K12 s Online School (OLS) 1 Introducing the Online School (OLS)... 6 Logging In... 6 OLS Home page... 8 My Account Menu... 9 To Edit Basic Account Information for Yourself... 9 Tip:

Student Loan Guide And Loan Request Form 2014-2015

THE LOS ANGELES COMMUNITY COLLEGE DISTRICT Student Loan Guide And Loan Request Form 2014-2015 2014-2015 Student Loan Guide and Request Form Page 1 LACCD and West Los Angeles College Loan Philosophy As

THE LOS ANGELES COMMUNITY COLLEGE DISTRICT Student Loan Guide And Loan Request Form 2014-2015 2014-2015 Student Loan Guide and Request Form Page 1 LACCD and West Los Angeles College Loan Philosophy As

HOME EQUITY LINES OF CREDIT

HOME EQUITY LINES OF CREDIT WHAT YOU SHOULD KNOW ABOUT HOME EQUITY LINES OF CREDIT: More and more lenders are offering home equity lines of credit. By using the equity in your home, you may qualify for

HOME EQUITY LINES OF CREDIT WHAT YOU SHOULD KNOW ABOUT HOME EQUITY LINES OF CREDIT: More and more lenders are offering home equity lines of credit. By using the equity in your home, you may qualify for

Guide to BMO Harris Online Banking SM

L O G G I N G I N Guide to BMO Harris Online Banking SM T A B L E O F C O N T E N T S Security & Bill Payment...4 Getting Started...5 Forgotten Password & User ID...6 BMO HARRIS ONLINE BANKING OVERVIEW...7

L O G G I N G I N Guide to BMO Harris Online Banking SM T A B L E O F C O N T E N T S Security & Bill Payment...4 Getting Started...5 Forgotten Password & User ID...6 BMO HARRIS ONLINE BANKING OVERVIEW...7

Introduction to Client Online. Factoring Guide

Introduction to Client Online Factoring Guide Contents Introduction 3 Preparing for Go live 3 If you have any questions 4 Logging In 5 Welcome Screen 6 Navigation 7 Navigation continued 8 Viewing Your

Introduction to Client Online Factoring Guide Contents Introduction 3 Preparing for Go live 3 If you have any questions 4 Logging In 5 Welcome Screen 6 Navigation 7 Navigation continued 8 Viewing Your

Outlook XP Email Only

Outlook XP Email Only Table of Contents OUTLOOK XP EMAIL 5 HOW EMAIL WORKS: 5 POP AND SMTP: 5 TO SET UP THE POP AND SMTP ADDRESSES: 6 TO SET THE DELIVERY PROPERTY: 8 STARTING OUTLOOK: 10 THE OUTLOOK BAR:

Outlook XP Email Only Table of Contents OUTLOOK XP EMAIL 5 HOW EMAIL WORKS: 5 POP AND SMTP: 5 TO SET UP THE POP AND SMTP ADDRESSES: 6 TO SET THE DELIVERY PROPERTY: 8 STARTING OUTLOOK: 10 THE OUTLOOK BAR:

ARIBA Contract Management System. User Guide to Accompany Training

ARIBA Contract Management System User Guide to Accompany Training Technical Training Team 6/29/2010 Table of Contents How to use this Guide... 4 Contract Management Process... 5 ARIBA- Getting Started...

ARIBA Contract Management System User Guide to Accompany Training Technical Training Team 6/29/2010 Table of Contents How to use this Guide... 4 Contract Management Process... 5 ARIBA- Getting Started...

Integrated Accounting System for Mac OS X

Integrated Accounting System for Mac OS X Program version: 6.3 110401 2011 HansaWorld Ireland Limited, Dublin, Ireland Preface Standard Accounts is a powerful accounting system for Mac OS X. Text in square

Integrated Accounting System for Mac OS X Program version: 6.3 110401 2011 HansaWorld Ireland Limited, Dublin, Ireland Preface Standard Accounts is a powerful accounting system for Mac OS X. Text in square

Reverse Mortgage Loans Borrowing Against Your Home

Reverse Mortgage Loans Borrowing Against Your Home AARP does not endorse any reverse mortgage lender or product, but wants you to have the information you need to make an informed decision about these

Reverse Mortgage Loans Borrowing Against Your Home AARP does not endorse any reverse mortgage lender or product, but wants you to have the information you need to make an informed decision about these

HOME A LOAN? A Quick Guide on Reverse Mortgages for Senior Advocates

HOME A LOAN? A Quick Guide on Reverse Mortgages for Senior Advocates At first glance, it seems there is a lot for a senior citizen to love about a reverse mortgage. It s a way to turn home equity into

HOME A LOAN? A Quick Guide on Reverse Mortgages for Senior Advocates At first glance, it seems there is a lot for a senior citizen to love about a reverse mortgage. It s a way to turn home equity into

MyCaseInfo Attorney Administration Users Guide. A Best Case Bankruptcy Add-on Tool

MyCaseInfo Attorney Administration Users Guide A Best Case Bankruptcy Add-on Tool 2 Table of Contents I. ATTORNEY ADMINISTRATION OVERVIEW... 4 II. HELP CENTER... 5 Documents Web Tutorials Online Seminar

MyCaseInfo Attorney Administration Users Guide A Best Case Bankruptcy Add-on Tool 2 Table of Contents I. ATTORNEY ADMINISTRATION OVERVIEW... 4 II. HELP CENTER... 5 Documents Web Tutorials Online Seminar

Guarantee Trust Life Insurance Company. Agent Portal www.gtlic.com. Agent Portal Guide

Guarantee Trust Life Insurance Company Agent Portal www.gtlic.com Agent Portal Guide Rev. 3/2014 Table of Contents Log in to Agent Portal... 3 Obtain Quote... 4 Print Quote... 5 Save and Retrieve Quote...

Guarantee Trust Life Insurance Company Agent Portal www.gtlic.com Agent Portal Guide Rev. 3/2014 Table of Contents Log in to Agent Portal... 3 Obtain Quote... 4 Print Quote... 5 Save and Retrieve Quote...

NYS OCFS CMS Contractor Manual

NYS OCFS CMS Contractor Manual C O N T E N T S CHAPTER 1... 1-1 Chapter 1: Introduction to the Contract Management System... 1-2 CHAPTER 2... 2-1 Accessing the Contract Management System... 2-2 Shortcuts

NYS OCFS CMS Contractor Manual C O N T E N T S CHAPTER 1... 1-1 Chapter 1: Introduction to the Contract Management System... 1-2 CHAPTER 2... 2-1 Accessing the Contract Management System... 2-2 Shortcuts

Renewing and Renegotiating Your Mortgage

ABCs of Mortgages Series Renewing and Renegotiating Your Mortgage Smart mortgage decisions start here table of contents overview 1 the renewal process 2 renegotiating your mortgage agreement: breaking

ABCs of Mortgages Series Renewing and Renegotiating Your Mortgage Smart mortgage decisions start here table of contents overview 1 the renewal process 2 renegotiating your mortgage agreement: breaking

Using Credit to Your Advantage.

Using Credit to Your Advantage. Topic Overview. The Using Credit To Your Advantage topic will provide participants with all the basic information they need to understand credit what it is and how to make

Using Credit to Your Advantage. Topic Overview. The Using Credit To Your Advantage topic will provide participants with all the basic information they need to understand credit what it is and how to make

Explain vital application doc calculations, including: Amortization Schedule TALC TIL (Fixed Rate)

") Illustrate how reverse mortgage interest rates are calculated. Explain vital application doc calculations, including: Amortization Schedule TALC TIL (Fixed Rate) Describe reverse mortgage loan growth Loan

Illustrate how reverse mortgage interest rates are calculated. Explain vital application doc calculations, including: Amortization Schedule TALC TIL (Fixed Rate) Describe reverse mortgage loan growth Loan

Loan Comparison. With this program, the user can compare two loan alternatives or evaluate the potential refinancing of an existing loan.

Loan Comparison With this program, the user can compare two loan alternatives or evaluate the potential refinancing of an existing loan. Fast Tools & Resources Loans may differ in their interest rates,

Loan Comparison With this program, the user can compare two loan alternatives or evaluate the potential refinancing of an existing loan. Fast Tools & Resources Loans may differ in their interest rates,

CORE K-Nect Web Portal

CORE K-Nect Web Portal Training October 2015 KIOSK Information Systems www.kiosk.com October 2015 Table of Contents Table of Contents 1 Getting Started 2 Logging In 2 Your Account Settings 3 My Profile

CORE K-Nect Web Portal Training October 2015 KIOSK Information Systems www.kiosk.com October 2015 Table of Contents Table of Contents 1 Getting Started 2 Logging In 2 Your Account Settings 3 My Profile

Quick Reference Guide: Corporate Card Changes

Quick Reference Guide: Corporate Card Changes In the USC Kuali system, every type of transaction is created and submitted in the form of an electronic document referred to as an edoc. This guide presents

Quick Reference Guide: Corporate Card Changes In the USC Kuali system, every type of transaction is created and submitted in the form of an electronic document referred to as an edoc. This guide presents

ROI Study: Leveraged versus Cash Investments by Max Wilson, Real Estate Investment Strategist Max Business Group Real Estate Services 724-368-3650

ROI Study: Leveraged versus Cash Investments by Max Wilson, Real Estate Investment Strategist Max Business Group Real Estate Services 724-368-3650 There is no doubt one of the attributes by Max Wilson,

ROI Study: Leveraged versus Cash Investments by Max Wilson, Real Estate Investment Strategist Max Business Group Real Estate Services 724-368-3650 There is no doubt one of the attributes by Max Wilson,

Managing your Joomla! 3 Content Management System (CMS) Website Websites For Small Business

Website Websites For Small Business") 2015 Managing your Joomla! 3 Content Management System (CMS) Website Websites For Small Business This manual will take you through all the areas that you are likely to use in order to maintain, update

2015 Managing your Joomla! 3 Content Management System (CMS) Website Websites For Small Business This manual will take you through all the areas that you are likely to use in order to maintain, update

Personal Online Banking & Bill Pay. Guide to Getting Started

Personal Online Banking & Bill Pay Guide to Getting Started What s Inside Contents Security at Vectra Bank... 4 Getting Started Online... 5 Welcome to Vectra Bank Online Banking. Whether you re at home,

Personal Online Banking & Bill Pay Guide to Getting Started What s Inside Contents Security at Vectra Bank... 4 Getting Started Online... 5 Welcome to Vectra Bank Online Banking. Whether you re at home,

Guide for Homebuyers

Guide for Homebuyers Tips for Getting a Safe Mortgage You Can Afford Q u i c k S u m m a ry Figure out what you can afford. Contact at least 3 different lenders or brokers. When you call, say: I m buying

Guide for Homebuyers Tips for Getting a Safe Mortgage You Can Afford Q u i c k S u m m a ry Figure out what you can afford. Contact at least 3 different lenders or brokers. When you call, say: I m buying

Mortgage Fraud. Table of Contents. Home Equity Scams Choosing a Loan Home Equity Dos Home Equity Don ts

Mortgage Fraud Table of Contents Home Equity Scams Choosing a Loan Home Equity Dos Home Equity Don ts Reverse Mortgages Home Loan Law HOEPA Prevents For more information on Mortgage Fraud visit: You could

Mortgage Fraud Table of Contents Home Equity Scams Choosing a Loan Home Equity Dos Home Equity Don ts Reverse Mortgages Home Loan Law HOEPA Prevents For more information on Mortgage Fraud visit: You could

A GUIDE TO. reverse mortgages. Live the retirement you dreamed

A GUIDE TO reverse mortgages Live the retirement you dreamed Guide Content 14What Is A Reverse Mortgage? 24How Do I Qualify? 34 What Can A Reverse Mortgage Be Used For? 44How Much Money Could I Qualify

A GUIDE TO reverse mortgages Live the retirement you dreamed Guide Content 14What Is A Reverse Mortgage? 24How Do I Qualify? 34 What Can A Reverse Mortgage Be Used For? 44How Much Money Could I Qualify

CheckBook Pro 2 Help

Get started with CheckBook Pro 9 Introduction 9 Create your Accounts document 10 Name your first Account 11 Your Starting Balance 12 Currency 13 Optional password protection 14 We're not done yet! 15 AutoCompletion

Get started with CheckBook Pro 9 Introduction 9 Create your Accounts document 10 Name your first Account 11 Your Starting Balance 12 Currency 13 Optional password protection 14 We're not done yet! 15 AutoCompletion

HELP CONTENTS INTRODUCTION...

HELP CONTENTS INTRODUCTION... 1 What is GMATPrep... 1 GMATPrep tip: to get the most from GMATPrep software, think about how you study best... 1 Navigating around... 2 The top navigation... 2 Breadcrumbs,

HELP CONTENTS INTRODUCTION... 1 What is GMATPrep... 1 GMATPrep tip: to get the most from GMATPrep software, think about how you study best... 1 Navigating around... 2 The top navigation... 2 Breadcrumbs,

How To Get A Home Equity Line Of Credit

A GUIDE TO HOME EQUITY LINES OF CREDIT Call or visit one of our offices today to see what products in this guide we have to offer you! TABLE OF CONTENTS Introduction What is a home equity line of credit

A GUIDE TO HOME EQUITY LINES OF CREDIT Call or visit one of our offices today to see what products in this guide we have to offer you! TABLE OF CONTENTS Introduction What is a home equity line of credit

Reference Guide to the Attorney Registration System

Reference Guide to the Attorney Registration System What is the Attorney Registration System? The Attorney Registration System allows attorneys to register for a secure user account. Upon registration

Reference Guide to the Attorney Registration System What is the Attorney Registration System? The Attorney Registration System allows attorneys to register for a secure user account. Upon registration

A SMART WAY TO PAY. AN EASY WAY TO SAVE. Fifth Third Bank Health Savings Account

A SMART WAY TO PAY. AN EASY WAY TO SAVE. Fifth Third Bank Health Savings Account Contents Welcome 3 Getting Started 4 Logging in for the First Time 4 Forget your Username or Password? 4 Home Page 5 Make

A SMART WAY TO PAY. AN EASY WAY TO SAVE. Fifth Third Bank Health Savings Account Contents Welcome 3 Getting Started 4 Logging in for the First Time 4 Forget your Username or Password? 4 Home Page 5 Make

If you re 62 or older and looking for money

March 2011 Reverse Mortgages: Get the Facts Before Cashing in on Your Home s Equity If you re 62 or older and looking for money to finance a home improvement, pay off your current mortgage, supplement

March 2011 Reverse Mortgages: Get the Facts Before Cashing in on Your Home s Equity If you re 62 or older and looking for money to finance a home improvement, pay off your current mortgage, supplement

FedEx Billing Online User Guide

FedEx Billing Online User Guide Introduction FedEx Billing Online allows you to efficiently manage and pay your FedEx invoices online. It s free, easy and secure. FedEx Billing Online helps you streamline

FedEx Billing Online User Guide Introduction FedEx Billing Online allows you to efficiently manage and pay your FedEx invoices online. It s free, easy and secure. FedEx Billing Online helps you streamline

Enhance Your Financial Security. With a Home Equity Conversion Mortgage

Enhance Your Financial Security With a Home Equity Conversion Mortgage 1 Call for Additional Information 925-258-0386 1 Unlock Your Home s Equity We understand that you want to transition easily into the

Enhance Your Financial Security With a Home Equity Conversion Mortgage 1 Call for Additional Information 925-258-0386 1 Unlock Your Home s Equity We understand that you want to transition easily into the

Reverse Mortgage Loans Borrowing Against Your Home

Reverse Mortgage Loans Borrowing Against Your Home AARP does not endorse any reverse mortgage lender or product, but wants you to have the information you need to make an informed decision about these

Reverse Mortgage Loans Borrowing Against Your Home AARP does not endorse any reverse mortgage lender or product, but wants you to have the information you need to make an informed decision about these

Reverse Mortgages. Federal Trade Commission ftc.gov

Reverse Mortgages Federal Trade Commission ftc.gov If you re 62 or older and looking for money to finance a home improvement, pay off your current mortgage, supplement your retirement income, or pay for

Reverse Mortgages Federal Trade Commission ftc.gov If you re 62 or older and looking for money to finance a home improvement, pay off your current mortgage, supplement your retirement income, or pay for

ibank Quick Start Guide

ibank Quick Start Guide An introductory tutorial for ibank 3, a personal financial management application. 2008 IGG Software, LLC Overview This tutorial will cover these basic program concepts: 1 2 3 4

ibank Quick Start Guide An introductory tutorial for ibank 3, a personal financial management application. 2008 IGG Software, LLC Overview This tutorial will cover these basic program concepts: 1 2 3 4

The Facts. About Reverse Mortgages. without the hype

The Facts About Reverse Mortgages without the hype A reverse mortgage... Will it help me? Is it a good fit for my needs? Will I own my home? Do I qualify? Am I protected? These may be some of the thoughts

The Facts About Reverse Mortgages without the hype A reverse mortgage... Will it help me? Is it a good fit for my needs? Will I own my home? Do I qualify? Am I protected? These may be some of the thoughts

Integrated Invoicing and Debt Management System for Mac OS X

Integrated Invoicing and Debt Management System for Mac OS X Program version: 6.3 110401 2011 HansaWorld Ireland Limited, Dublin, Ireland Preface Standard Invoicing is a powerful invoicing and debt management

Integrated Invoicing and Debt Management System for Mac OS X Program version: 6.3 110401 2011 HansaWorld Ireland Limited, Dublin, Ireland Preface Standard Invoicing is a powerful invoicing and debt management

Campus Solutions Self Service: Student Quick Reference Guide

Campus Solutions Self Service: Student Table of Contents Introduction to Step Sheets... 4 Getting Started in CUNYfirst... 5 Activate My CUNYfirst Account... 6 Log into My CUNYfirst Account... 10 Sign Out

Campus Solutions Self Service: Student Table of Contents Introduction to Step Sheets... 4 Getting Started in CUNYfirst... 5 Activate My CUNYfirst Account... 6 Log into My CUNYfirst Account... 10 Sign Out

Texas Woman s University RedDot Webspinner s Manual Revised 7/23/2015. [email protected]

Texas Woman s University RedDot Webspinner s Manual Revised 7/23/2015 [email protected] 1 Contents CONNECTING TO YOUR SITE... 3 MAIN MENU... 4 REPEATED CONTENT AREAS... 4 OPENING PAGE LAYOUTS AND EXISTING

Texas Woman s University RedDot Webspinner s Manual Revised 7/23/2015 [email protected] 1 Contents CONNECTING TO YOUR SITE... 3 MAIN MENU... 4 REPEATED CONTENT AREAS... 4 OPENING PAGE LAYOUTS AND EXISTING

Adobe Acrobat 6.0 Professional

Adobe Acrobat 6.0 Professional Manual Adobe Acrobat 6.0 Professional Manual Purpose The will teach you to create, edit, save, and print PDF files. You will also learn some of Adobe s collaborative functions,

Adobe Acrobat 6.0 Professional Manual Adobe Acrobat 6.0 Professional Manual Purpose The will teach you to create, edit, save, and print PDF files. You will also learn some of Adobe s collaborative functions,

ReverseVision Handbook. 2011 ReverseVision

ReverseVision Handbook ReverseVision by ReverseVision ReverseVision is an enterprise level reverse mortgage origination platform that supports inter-company and intra-company workflow. ReverseVision Handbook

ReverseVision Handbook ReverseVision by ReverseVision ReverseVision is an enterprise level reverse mortgage origination platform that supports inter-company and intra-company workflow. ReverseVision Handbook

Apple Bank Online Banking Guide

Apple Bank Online Banking Guide 24/7 Banking Financial Management Funds Transfer Bill Payment Convenient, Easy to Use Secure Table of Contents Online Banking Overview - Convenient, Easy, Secure 1 Registration

Apple Bank Online Banking Guide 24/7 Banking Financial Management Funds Transfer Bill Payment Convenient, Easy to Use Secure Table of Contents Online Banking Overview - Convenient, Easy, Secure 1 Registration

INTRODUCTION TO EMAIL: & BASICS

University of North Carolina at Chapel Hill Libraries Chapel Hill Public Library Carrboro Branch Library Carrboro Cybrary Durham Public Library INTRODUCTION TO EMAIL: & BASICS Getting Started Page 02 Prerequisites

University of North Carolina at Chapel Hill Libraries Chapel Hill Public Library Carrboro Branch Library Carrboro Cybrary Durham Public Library INTRODUCTION TO EMAIL: & BASICS Getting Started Page 02 Prerequisites

Microsoft Outlook. KNOW HOW: Outlook. Using. Guide for using E-mail, Contacts, Personal Distribution Lists, Signatures and Archives

Trust Library Services http://www.mtwlibrary.nhs.uk http://mtwweb/cgt/library/default.htm http://mtwlibrary.blogspot.com KNOW HOW: Outlook Using Microsoft Outlook Guide for using E-mail, Contacts, Personal

Trust Library Services http://www.mtwlibrary.nhs.uk http://mtwweb/cgt/library/default.htm http://mtwlibrary.blogspot.com KNOW HOW: Outlook Using Microsoft Outlook Guide for using E-mail, Contacts, Personal

Intellect Platform - The Workflow Engine Basic HelpDesk Troubleticket System - A102

Intellect Platform - The Workflow Engine Basic HelpDesk Troubleticket System - A102 Interneer, Inc. Updated on 2/22/2012 Created by Erika Keresztyen Fahey 2 Workflow - A102 - Basic HelpDesk Ticketing System

Intellect Platform - The Workflow Engine Basic HelpDesk Troubleticket System - A102 Interneer, Inc. Updated on 2/22/2012 Created by Erika Keresztyen Fahey 2 Workflow - A102 - Basic HelpDesk Ticketing System

The Facts About Reverse Mortgages. without the hype

The Facts About Reverse Mortgages without the hype A reverse mortgage... Will it help me? Is it a good fit for my needs? Will I own my home? Do I qualify? Am I protected? These may be some of the thoughts

The Facts About Reverse Mortgages without the hype A reverse mortgage... Will it help me? Is it a good fit for my needs? Will I own my home? Do I qualify? Am I protected? These may be some of the thoughts

Lesson Description. Texas Essential Knowledge and Skills (Target standards) National Standards (Supporting standards) PFL Terms Interest rate

National Standards (Supporting standards) PFL Terms Interest rate") Lesson Description This lesson focuses on the various sources people use for borrowing money or using credit. Some people, especially those who do not know all their options, borrow money from lenders

Lesson Description This lesson focuses on the various sources people use for borrowing money or using credit. Some people, especially those who do not know all their options, borrow money from lenders

User Guide. A guide to online services available through Sircon for Education Providers. DOC CX 08/13/10 02/02 v5

User Guide A guide to online services available through Sircon for Education Providers DOC CX 08/13/10 02/02 v5 Contents Contents Contents... 2 Introduction... 4 About this Guide... 4 Getting Started...

User Guide A guide to online services available through Sircon for Education Providers DOC CX 08/13/10 02/02 v5 Contents Contents Contents... 2 Introduction... 4 About this Guide... 4 Getting Started...

ADOBE ACROBAT 7.0 CREATING FORMS

ADOBE ACROBAT 7.0 CREATING FORMS ADOBE ACROBAT 7.0: CREATING FORMS ADOBE ACROBAT 7.0: CREATING FORMS...2 Getting Started...2 Creating the Adobe Form...3 To insert a Text Field...3 To insert a Check Box/Radio

ADOBE ACROBAT 7.0 CREATING FORMS ADOBE ACROBAT 7.0: CREATING FORMS ADOBE ACROBAT 7.0: CREATING FORMS...2 Getting Started...2 Creating the Adobe Form...3 To insert a Text Field...3 To insert a Check Box/Radio

Reverse Mortgages: A Guide for Consumers. A New Report from THE AMERICAN ADVISORY COUNCIL

Reverse Mortgages: A Guide for Consumers A New Report from THE AMERICAN ADVISORY COUNCIL This publication is designed to provide accurate and authoritative information regarding the subject matter covered.

Reverse Mortgages: A Guide for Consumers A New Report from THE AMERICAN ADVISORY COUNCIL This publication is designed to provide accurate and authoritative information regarding the subject matter covered.

Office of Fleet and Asset Management (OFAM) www.dgs.ca.gov/ofam (Reserve a State Vehicle) Online Vehicle Reservation Instructions

www.dgs.ca.gov/ofam (Reserve a State Vehicle) Online Vehicle Reservation Instructions") Office of Fleet and Asset Management (OFAM) www.dgs.ca.gov/ofam (Reserve a State Vehicle) Online Vehicle Reservation Instructions Revised March 2, 2012 1 You must be an active California State Employee

Office of Fleet and Asset Management (OFAM) www.dgs.ca.gov/ofam (Reserve a State Vehicle) Online Vehicle Reservation Instructions Revised March 2, 2012 1 You must be an active California State Employee

RealTAG User Documentation ABOUT REALTAG... 4 HOW TO ACCESS REALTAG... 4 HOW TO RETRIEVE YOUR USERNAME AND PASSWORD... 5

Office Edition RealTAG User Documentation ABOUT REALTAG... 4 HOW TO ACCESS REALTAG... 4 HOW TO RETRIEVE YOUR USERNAME AND PASSWORD... 5 LOGGING IN FOR THE FIRST TIME... 5 HOW TO SETUP AGENTS... 6 HOW TO

Office Edition RealTAG User Documentation ABOUT REALTAG... 4 HOW TO ACCESS REALTAG... 4 HOW TO RETRIEVE YOUR USERNAME AND PASSWORD... 5 LOGGING IN FOR THE FIRST TIME... 5 HOW TO SETUP AGENTS... 6 HOW TO

Shopping Cart Manual. Written by Shawn Xavier Mendoza

Shopping Cart Manual Written by Shawn Xavier Mendoza Table of Contents 1 Disclaimer This manual assumes that you are using Wix.com for website creation, and so this method may not work for all other online

Shopping Cart Manual Written by Shawn Xavier Mendoza Table of Contents 1 Disclaimer This manual assumes that you are using Wix.com for website creation, and so this method may not work for all other online

Outstanding mortgage balance

Using Home Equity There are numerous benefits to owning your own home. Not only does it provide a place to live, where you can decorate as you want, but it also provides a source of wealth. Over time,

Using Home Equity There are numerous benefits to owning your own home. Not only does it provide a place to live, where you can decorate as you want, but it also provides a source of wealth. Over time,