An inquiry into the multiplier process in IS-LM model

|

|

|

- Eleanor Mitchell

- 10 years ago

- Views:

Transcription

1 An inquiry into te multiplier process in IS-LM model Autor: Li ziran Address: Li ziran, Room 409, Building 38#, Peing University, Beijing 00.87,PRC. Pone: (86) Internet Address: Abstract Te multiplier teory is still an important analytical tool in many macroeconomic textboos. For example, a number of textboo autors use te teory to explain te process of growt in goods maret by expanding te multiplier process into a geometric series, and tus obtain te route of economic growt. Ten some students raise an interesting question: Can we induce te dynamics of te monetary and fiscal transmission mecanism of IS-LM model troug te multiplier process? (None of te textboos involve tis problem; alternative solutions are available in economics journals, but go beyond te scope of our students nowledge.) If not, wat is te problem in te analysis of te multiplier process? Here I first sow some professor s deduction of te "monetary transmission mecanism", and ten analyze te main problems and discuss te multiplier teory. Finally, I propose a generalization of te monetary transmission mecanism approac. I trace te cange of demand and output in te process of increase respectively, and use a stocastic series of variables to reflect regularity in te teir relationsip, and obtain anoter two curves in IS-LM model representing teir relationsip In conclusion, I demonstrate teoretically tat te economy will ultimately reac its equilibrium point, following te route of LM curve between one static equilibrium point to anoter. Deduction

2 For te sae of numerical calculation, we analyze te multiplier process in a tree-department economy. We ave two important curves in IS-LM model representing te equilibrium contrail of te goods maret and money maret respectively: IS curve: C 0 + ctr 0 + I 0 + G () Y= - c ( - t) LM curve: 0 - br = A 0 - br - c ( - t) (A 0 = C 0 + ctr 0 +I 0 +G 0 ) () M (2) =Y-r, (2) P Te intersection of te two curves determines te equilibrium output of our economy: (3) Y 0 = A 0 - c ( + bm P - Were Y is output or national income; C 0 is autonomous consumption; I represents investment spending r is te interest rate and b measures interest response of investment, I 0 is autonomous investment spending; G is government purcase of goods and services; TR 0 is transfer to te private sector; t is tax rate; c measures marginal propensity to consume out of disposable income; is te interest elasticity of money demand; is te output elasticity of money supply. Some professors old te following deduction of te monetary transmission mecanism in IS-LM model: [I] Initiative effects: ()Te government increases real money stoc by M/p. (2)Good marets adjust relatively slow and Y will not cange in a sort period, wile asset maret adjusts quicly and tus interest rates will be down by M/(p) (M/p=Y-r, M/p=Y- r.oterwise te equation M/p=Y-r will not old after an increase on its left side),. (3) 2

3 (3)Lower interest rate will stimulate te investment demand and consequently increase te aggregate demand. And, te output and national income begin to rise. Te above stages can be demonstrated by te following grap: M/p R= M/P I I=b M/P = AD AD AD= Y Y [II] Induced effects: Round R= Y/ Y R A I D I Y Notes: M/p=Y-r, M/p will remain stable after te monetary policy is applied, and terefore, in order to old te equation, r will rise as a result of te increase in Y. And tis increase can be denoted as Y i Y d = (-t) Y I= - Y/ Y d = (-t) Y Y d C AD Y (Tis increase in Y is induced by increased consumption demand, and tus can be denoted as Y c ) In round, te combination of effects induced by te initiative increase in Y is Y c +Y i, we may denote Y c +Y i by Y, ten Y =[c(-t)-/] Y.Similarly, In round 2, te combination of effects induced by te cange of Y in round (denoted by Y ) is [c(-t)-/]y,or to be more exact, [c(-t)- /] 2 Y(denoted by Y 2 ).And in round 3, [c(-t)-/] 3 Y.. C=c If c(-t) -/ <, te successive terms in te series become progressively smaller, we can write out te successive rounds of increased output, starting wit te initial increase in output, we may obtain a geometric series: Y, [c(-t)-/] Y, [c(-t)-/] 2 Y.. Moreover, te total cange can be obtained by adding tem up: Y d Y Y I = - AD= C Y/ Y i = Y {+[c (-t)-/] +[c(-t)-/] 2 + }= Y/[-c(-t)+/]= Problems: b M p c( 3

Y I= - Y/ Y d = (-t) Y Y d C AD Y (Tis increase in Y is induced by increased consumption demand, and tus can be denoted as Y c ) In round, te")

4 . Tis deduction sees to use te multiplier teory to explain te mecanism. It implies tat an increase in demand will immediately induce a same amount of increase in Y. If te economy is in recession ow can te output gain suc a sarp increase? 2. Te linear discrete dynamical systems can beave in some surprising ways. Wen c(-t) -/ <,a sequence obtained from a linear discrete dynamical system bounces around te equilibrium point and te bounces get smaller so tat te sequence approaces te equilibrium point; but wen c(-t) - / >, it bounces around te equilibrium point but te bounces get larger so tat te sequence does not approac te equilibrium point. If c(-t) -/ > te initial effect is b M/(P), wile te predicted equilibrium output is C b( M + M) + ctr0 + I p, and te predicted final total c( 0 G b M b M p increase of outcome is c(.obviously, p c( < b M/(P). Tat means after te initial increase output exceeds tat of te equilibrium. We can also figure out tat in te second period, te output is below tat of te equilibrium, and in te tird period, te output exceeds tat of te equilibrium again. Just lie a cobweb grap. If te economy is in recession and output is below tat of te sufficient employment, ow can te output gain suc a sarp increase immediately after te increase in money stoc? A number of macroeconomic text-boo autors examine te government purcase multiplier as follows : Suppose te government increases purcase of goods by G, te multiplier process G/(- c), were c is te marginal propensity to consume, can be expanded into G + c G + c 2 G + + for 0< c <, and tus we obtain te route of economic growt. Neverteless, tis applies only for an economy wit a sufficiently large excess capacity to produce, for instance, an economy wit 4

- / >, it bounces around te equilibrium point but te bounces get larger so tat te sequence does not approac te equilibrium point.")

5 only one customer and dozens of barbers sitting around. If we tin about output being say Boeing 747s, te analysis is more complex, and te geometric series will fail, simply because it taes time to build a plane. Te multiplier teory as its strengt, but its assumptions are very strict: () sufficient large excess capacity to produce (2) output sould exactly meet te surplus demand in eac round. (3) One maret. Instructors usually teac te teory (or tey temselves accept it literally) as axioms and leave out tese assumptions. Tus, it is reluctant for tem to use te teory to explain te case were tese assumptions are sligtly violated. Ten ow can we analyze te multiplier process? Te Generalization of te Multiplier Process Approac Wen we explain te multiplier process, te geometric series only give us a logical deduction.in fact; te number value of te increase of eac round is indefinite. We can deduce te multiplier process in anoter way. Here I trace te cange of demand and output in te process of increase respectively: Te government increases purcases of goods by G, wic increases te aggregate demand in our economy by G. In te first round, we suppose te goods maret does not adjust quicly enoug to meet te excessive demand, and income (or output) only increases by Y (<< G). Ten consumption demand will increase by c Y. Since demand still exceeds output, output will continue to increase. Ten we obtain an increase of Y 2 in te second round, and a relevant increase of c Y 2 in consumption demand. Tis cycle repeats until output meet demand. (Note tat in eac round output increases more tan demand: Y i >c Y i, and tus output will ultimately meet demand.)tus we can + obtain te equation on equilibrium point: + Yi = G+ c Y +c Y 2 +c Y 3 + = G+ c Yi, i= i= + and derive te number value of te total income increase: Yi = G /(-c). i= 5

as axioms and leave out tese assumptions.")

6 Te above analysis sows an alternative metod of explaining te multiplier process, and te result is te same as we use te traditional metod of geometric series. However, tere is great difference if we analyze complicated maret. Now let us loo at te multiplier process in IS-LM model: Application in IS-LM Model If we expand te monetary multiplier process G c( (were G is te increased government purcase of goods) into a geometric series and specify a definite cange of eac round: G, [c(-t)-/] G, [c(-t)-/] 2 G.,we cannot explain te case of c(-t)-/ (-, -). Wen we apply te multiplier teory to explain IS-LM model, wic is a model involving bot te money maret and goods maret, result is unsatisfactory. Tis is partly because te multiplier G incorporates te process of cange on two separate marets into a single course, in c( wic individuals beave on money maret and goods maret separately. Tis time te multiplier process fails again. In fact, te aggregate output and aggregate demand of te nation, not te multiplier process, determine te equilibrium point in an economy. If AD>AS, output will increase; if AD<AS, output will decrease; if AD=AS, te economy reaces its equilibrium point. Many macroeconomics textboo autors do not empasize te distinction between demand and output in IS-LM model, and literally tae te equations as axioms. In fact, IS curve represents combination of interest rates and income at wic te goods maret clears. Tus te mat symbols Y, G, I, C etc. represent bot te demand and output, since tey are equal on te equilibrium point. Wen we trace te process of growt, wic is an out-of -equilibrium course, we sould consider te two concepts separately. Now we use te generalization of te multiplier process approac to deduce te dynamics of te government purcase multiplier: 6

-/] G, [c(-t)-/] 2 G.,we cannot explain te case of c(-t)-/ (-, -).")

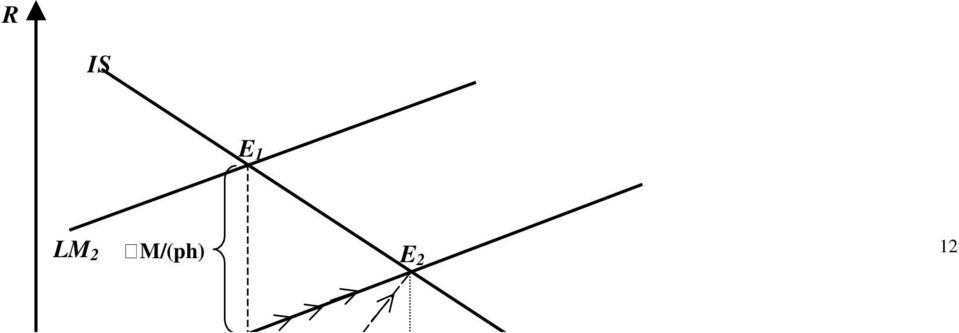

7 First, te government purcase of goods increases AD by G, and te output will increase as a result of te stimulation of excessive demand. Tis time we abandon te ambition to predict te exact value of increase in eac round. Let Y denote an uncertain increase in output in te first round, tus te cange in income is equal to Y. Ten te income increase will induce an increase of c(-t) Y in consumption demand and a decrease of Y / in investment demand. Similarly, we can analyze te cange in te second round: an increase of Y 2 in output and a cange of [c(-t)- /] Y 2 in demand. And tis cycle repeats until AD=AS. Te range of c, t and is (0, ), wile te range of b and is (0,+ ).Tus c(-t)-/ (-, ).If c(-t)-/ (0, ), ten wit te increase in AS, AD will consequently increase but on a smaller scale.( Y i > [c(-t)-/] Y i ) If c(-t)-/ (-,0),wit an increase of Y in AS, AD will decrease by [/-c(-t)] Y. All in all, AS will ultimately meet AD. Table sows te detail of te transmission mecanism, were GAP i denotes te gap between AD and AS in eac round. We obtain a stocastic series of te increase in output: Y, Y 2, Y 3,.. and a relevant series of te cange in demand [c(-t) -/] Y, [c(-t) -/] Y 2, Wen GAP i =0, te economy reaces its equilibrium point. From te equation G -[-c(-t) -/] Y i=0, we derive te total increase in = income: G Yi = = c( i and total increase in interest rate: (/) Yi = = i G i c( Conclusion: te economy will ultimately reac its equilibrium point following te route of E E 2 along te LM curve. 2 (Figure sows te route of te cange in demand and output on condition tat c (-t) -/>0, wile Figure 3 sows te case of c(-t) -/<0) Te case of te monetary transmission mecanism is similar (Figure 2): 7

- /] Y 2 in demand. And tis cycle repeats until AD=AS.")

8 An increase of M/p in te real money stoc sifts te LM scedule to te rigt. Te money maret adjusts immediately, and interest rates decline between point E and E 3 3 by M/(P) according to te following equations: M /p=y-r M/p= - r Te lower interest rate stimulates an increase of b M/(P) in investment demand, and ten te output begins to rise. Y denotes an indefinite increase of output in te first round. Te income increase will induce a decrease of Y / in investment demand by raising te interest rate and an increase of c(-t) Y in consumption demand, according to te following equations: M /p=y-r 0= Y - r, r= Y / I=I 0 -br, I=-b r I= - Y / C=C 0 +c[(-t)y +TR 0 ] C = c(-t) Y Similarly, we can analyze te cange in te second round: an increase of Y 2 in output and a cange of [c(-t)- /] Y 2 in demand. Tis cycle repeats until AD=AS. Finally, we obtain a series of te increase in output: Y, Y 2, Y 3, and a relevant series of te cange in demand: [c(-t) -/] Y, [c(-t) -/] Y 2, [c(-t) -/] Y 3. On te equilibrium point, we ave: b M M/(p) -[-c(-t) -/] Yi=0, p Yi = i= i= c( Advantages of tis Generalization Approac First, te metod still olds if we consider oter parameters tat determine te IS-LM model. For example, in an open economy, we can simply add a equation to modify te deduction: X=g-mY-nr, were X is net export, m is te marginal propensity to export Ten te equilibrium income determined by IS-LM model is: 8

Y in consumption demand, according to te following equations: M /p=y-r 0= Y")

9 C 0 + ctr 0 + I 0 + G 0 + g Y= (b+ n) c( m+ 4 and te series will be more complex to demonstrate te mecanism, but te result is similar. Second, it can, if not very reluctantly, explain te effect of monetary policy wit a orizontal IS curve and te effect of fiscal policy wit a vertical LM curve: ()If b, we obtain a orizontal IS curve.now we trace te monetary policy: Te lower interest rate stimulates an infinitely large increase of b M/(P) in investment demand, Y denotes an increase in output in te first round.te income increase will induce a decrease of Y / in investment demand by raising te interest rate, and an increase of c(-t) Y in consumption demand. Here we ave a flat (or almost orizontal) demand curve AE 2 wit a negative slope, and a relatively steeper supply curve. Since Y only generates infinitely large canges in investment demand, and tus avoid te embarrassment of explaining an infinitely large decrease of M/(p) in output wen applying te traditional metod of geometric series. We obtain: b M p lim Yi M = = b i= c( p (2)If 0, we obtain a vertical LM curve. Let us trace te effect of fiscal policy: First, te excessive government purcase of goods increases AD by G. Y denotes an increase of output in te first round. Ten an increase of c(-t) Y in consumption demand and a decrease of Y / in investment demand. Since an infinitely small Y can be large enoug to mae te decrease of investment demand counteract G, ere we ave a vertical supply curve E E 2 and a demand curve AE 2 wit a negative slope. Tus we avoid te problem of explaining an infinitely large decrease of G / in output. Finally we obtain: (5) G lim Yi = 0 i= c( =0 (6) 9

Y in consumption demand.")

10 NOTES. For example, te following textboos expand te multiplier process into a geometric series: Maniw (996), Gordon (993), Hall and Taylor (993), Dornbusc and Fiscer (994) 2. It seems tat te effects on consumption and investment bot occur witin te same round, in fact, tey are two separate processes. For example, suppose te effect on investment lags m rounds beind tat on consumption demand and tus GAP equals G -[-c(-t)] Y i -/ + Yi. Wit te increase of output,gap still becomes progressively smaller.we can consider te series in anoter way: increased consumption demand c(-t) Y, c(-t) Y 2, c(-t) Y 3 cange of investment demand - / Y, -/ Y 2,-/ Y 3,increase of output Y, Y 2, Y 3 In te long run, we can still add up te aggregate effect of eac round and get te same result: Yi=-/ Yi+ c(-t) = = i= i -m i= i Yi+ G i = 3. Robert J. Gordon explained tat: Finding temselves wit more money tan tey need. Tis raises te prices of stocs and reduces te interest rate. Te initial decline in interest rate is called `liquidity effect` of a monetary expansion. Te lower interest rate raises te desired level of autonomous consumption and investment spending requiring an increase in production. Tis is te `income effect` of a monetary expansion."(gordon 990) Rudiger Dornbusc summarizes te stages in te transmission mecanism as follows:() Cange in real Money supply (2) Portfolio adjustments lead to a cange in asset prices and interest rates (3) Spending adjusts to te cange in interest rate (4) Output adjust to te cange in aggregate demand (Dornbusc and Fiscer 994.) REFERENCES () Dornbusc, R., and S. Fiscer Macroeconomics. 6t. ed. New Yor: McGraw-Hill. 0

![For example, suppose te effect on investment lags m rounds beind tat on consumption demand and tus GAP equals G -[-c(-t)] Y i -/ + Yi.](/docs-images/51/14499457/images/page_10.jpg "Wit te increase of output,gap still becomes progressively smaller.")

11 (2) Froyen, R Macroeconomics: Teories and policies. 5t. ed. Upper Saddle River, N.J.: Pren-tice-Hall. (3) Gordon, R. J Macroeconomics, 5t ed. New Yor: Harper Collins College Publisers. (4) Maniw, N. G.996. Macroeconomics. 3rd. ed. New Yor: Wort. Table Round Effect on C Effect on I Combination effects GAP i of eac period G c(-t) Y (-/) Y c(-t) Y -/ Y G -[-c(-/] Y 2 c(-t) Y 2 (-/) Y 2 c(-t) Y 2 -/ Y 2 G -[-c(-/] ( Y + Y 2 ) m c(-t) Y m (-/) Y m c(-t) Y m -/ Y m m G -[-c(-/ ûyi. c(-t) Y (-/) Y c(-t) Y -/ Y G -[-c(-/] ûyi R IS 2 i= i= IS E 2 E A B G/ c( LM G G

![Table Round Effect on C Effect on I Combination effects GAP i of eac period 0 0 0 0 G c(-t) Y (-/) Y c(-t) Y -/ Y G -[-c(-/] Y 2 c(-t) Y 2 (-/) Y](/docs-images/51/14499457/images/page_11.jpg "2 c(-t) Y 2 -/ Y 2 G -[-c(-/] ( Y + Y 2 ) m c(-t) Y m (-/) Y m c(-t) Y m -/ Y m m G -[-c(-/ ûyi.")

12 R IS E LM 2 M/(p) E 2 2

13 R IS 2 o IS LM E G G c( E 2 Figure 3 Te income increase is smaller tan te government spending if c(-t)-/ <0 B A / Slope= <0 c(- t) Y(AD) 3

-/ <0 B A / Slope= <0 c(- t)")

2 Limits and Derivatives

2 Limits and Derivatives 2.7 Tangent Lines, Velocity, and Derivatives A tangent line to a circle is a line tat intersects te circle at exactly one point. We would like to take tis idea of tangent line

2 Limits and Derivatives 2.7 Tangent Lines, Velocity, and Derivatives A tangent line to a circle is a line tat intersects te circle at exactly one point. We would like to take tis idea of tangent line

EC201 Intermediate Macroeconomics. EC201 Intermediate Macroeconomics Problem set 8 Solution

EC201 Intermediate Macroeconomics EC201 Intermediate Macroeconomics Prolem set 8 Solution 1) Suppose tat te stock of mone in a given econom is given te sum of currenc and demand for current accounts tat

EC201 Intermediate Macroeconomics EC201 Intermediate Macroeconomics Prolem set 8 Solution 1) Suppose tat te stock of mone in a given econom is given te sum of currenc and demand for current accounts tat

Instantaneous Rate of Change:

Instantaneous Rate of Cange: Last section we discovered tat te average rate of cange in F(x) can also be interpreted as te slope of a scant line. Te average rate of cange involves te cange in F(x) over

Instantaneous Rate of Cange: Last section we discovered tat te average rate of cange in F(x) can also be interpreted as te slope of a scant line. Te average rate of cange involves te cange in F(x) over

Tangent Lines and Rates of Change

Tangent Lines and Rates of Cange 9-2-2005 Given a function y = f(x), ow do you find te slope of te tangent line to te grap at te point P(a, f(a))? (I m tinking of te tangent line as a line tat just skims

Tangent Lines and Rates of Cange 9-2-2005 Given a function y = f(x), ow do you find te slope of te tangent line to te grap at te point P(a, f(a))? (I m tinking of te tangent line as a line tat just skims

The EOQ Inventory Formula

Te EOQ Inventory Formula James M. Cargal Matematics Department Troy University Montgomery Campus A basic problem for businesses and manufacturers is, wen ordering supplies, to determine wat quantity of

Te EOQ Inventory Formula James M. Cargal Matematics Department Troy University Montgomery Campus A basic problem for businesses and manufacturers is, wen ordering supplies, to determine wat quantity of

Math 113 HW #5 Solutions

Mat 3 HW #5 Solutions. Exercise.5.6. Suppose f is continuous on [, 5] and te only solutions of te equation f(x) = 6 are x = and x =. If f() = 8, explain wy f(3) > 6. Answer: Suppose we ad tat f(3) 6. Ten

Mat 3 HW #5 Solutions. Exercise.5.6. Suppose f is continuous on [, 5] and te only solutions of te equation f(x) = 6 are x = and x =. If f() = 8, explain wy f(3) > 6. Answer: Suppose we ad tat f(3) 6. Ten

What is Advanced Corporate Finance? What is finance? What is Corporate Finance? Deciding how to optimally manage a firm s assets and liabilities.

Wat is? Spring 2008 Note: Slides are on te web Wat is finance? Deciding ow to optimally manage a firm s assets and liabilities. Managing te costs and benefits associated wit te timing of cas in- and outflows

Wat is? Spring 2008 Note: Slides are on te web Wat is finance? Deciding ow to optimally manage a firm s assets and liabilities. Managing te costs and benefits associated wit te timing of cas in- and outflows

How To Ensure That An Eac Edge Program Is Successful

Introduction Te Economic Diversification and Growt Enterprises Act became effective on 1 January 1995. Te creation of tis Act was to encourage new businesses to start or expand in Newfoundland and Labrador.

Introduction Te Economic Diversification and Growt Enterprises Act became effective on 1 January 1995. Te creation of tis Act was to encourage new businesses to start or expand in Newfoundland and Labrador.

Verifying Numerical Convergence Rates

1 Order of accuracy Verifying Numerical Convergence Rates We consider a numerical approximation of an exact value u. Te approximation depends on a small parameter, suc as te grid size or time step, and

1 Order of accuracy Verifying Numerical Convergence Rates We consider a numerical approximation of an exact value u. Te approximation depends on a small parameter, suc as te grid size or time step, and

Pre-trial Settlement with Imperfect Private Monitoring

Pre-trial Settlement wit Imperfect Private Monitoring Mostafa Beskar University of New Hampsire Jee-Hyeong Park y Seoul National University July 2011 Incomplete, Do Not Circulate Abstract We model pretrial

Pre-trial Settlement wit Imperfect Private Monitoring Mostafa Beskar University of New Hampsire Jee-Hyeong Park y Seoul National University July 2011 Incomplete, Do Not Circulate Abstract We model pretrial

f(x) f(a) x a Our intuition tells us that the slope of the tangent line to the curve at the point P is m P Q =

f(a) x a Our intuition tells us that the slope of the tangent line to the curve at the point P is m P Q =") Lecture 6 : Derivatives and Rates of Cange In tis section we return to te problem of finding te equation of a tangent line to a curve, y f(x) If P (a, f(a)) is a point on te curve y f(x) and Q(x, f(x))

Lecture 6 : Derivatives and Rates of Cange In tis section we return to te problem of finding te equation of a tangent line to a curve, y f(x) If P (a, f(a)) is a point on te curve y f(x) and Q(x, f(x))

Can a Lump-Sum Transfer Make Everyone Enjoy the Gains. from Free Trade?

Can a Lump-Sum Transfer Make Everyone Enjoy te Gains from Free Trade? Yasukazu Icino Department of Economics, Konan University June 30, 2010 Abstract I examine lump-sum transfer rules to redistribute te

Can a Lump-Sum Transfer Make Everyone Enjoy te Gains from Free Trade? Yasukazu Icino Department of Economics, Konan University June 30, 2010 Abstract I examine lump-sum transfer rules to redistribute te

Sections 3.1/3.2: Introducing the Derivative/Rules of Differentiation

Sections 3.1/3.2: Introucing te Derivative/Rules of Differentiation 1 Tangent Line Before looking at te erivative, refer back to Section 2.1, looking at average velocity an instantaneous velocity. Here

Sections 3.1/3.2: Introucing te Derivative/Rules of Differentiation 1 Tangent Line Before looking at te erivative, refer back to Section 2.1, looking at average velocity an instantaneous velocity. Here

Research on the Anti-perspective Correction Algorithm of QR Barcode

Researc on te Anti-perspective Correction Algoritm of QR Barcode Jianua Li, Yi-Wen Wang, YiJun Wang,Yi Cen, Guoceng Wang Key Laboratory of Electronic Tin Films and Integrated Devices University of Electronic

Researc on te Anti-perspective Correction Algoritm of QR Barcode Jianua Li, Yi-Wen Wang, YiJun Wang,Yi Cen, Guoceng Wang Key Laboratory of Electronic Tin Films and Integrated Devices University of Electronic

Derivatives Math 120 Calculus I D Joyce, Fall 2013

Derivatives Mat 20 Calculus I D Joyce, Fall 203 Since we ave a good understanding of its, we can develop derivatives very quickly. Recall tat we defined te derivative f x of a function f at x to be te

Derivatives Mat 20 Calculus I D Joyce, Fall 203 Since we ave a good understanding of its, we can develop derivatives very quickly. Recall tat we defined te derivative f x of a function f at x to be te

SAT Subject Math Level 1 Facts & Formulas

Numbers, Sequences, Factors Integers:..., -3, -2, -1, 0, 1, 2, 3,... Reals: integers plus fractions, decimals, and irrationals ( 2, 3, π, etc.) Order Of Operations: Aritmetic Sequences: PEMDAS (Parenteses

Numbers, Sequences, Factors Integers:..., -3, -2, -1, 0, 1, 2, 3,... Reals: integers plus fractions, decimals, and irrationals ( 2, 3, π, etc.) Order Of Operations: Aritmetic Sequences: PEMDAS (Parenteses

Theoretical calculation of the heat capacity

eoretical calculation of te eat capacity Principle of equipartition of energy Heat capacity of ideal and real gases Heat capacity of solids: Dulong-Petit, Einstein, Debye models Heat capacity of metals

eoretical calculation of te eat capacity Principle of equipartition of energy Heat capacity of ideal and real gases Heat capacity of solids: Dulong-Petit, Einstein, Debye models Heat capacity of metals

CHAPTER TWO. f(x) Slope = f (3) = Rate of change of f at 3. x 3. f(1.001) f(1) Average velocity = 1.1 1 1.01 1. s(0.8) s(0) 0.8 0

Slope = f (3) = Rate of change of f at 3. x 3. f(1.001) f(1) Average velocity = 1.1 1 1.01 1. s(0.8) s(0) 0.8 0") CHAPTER TWO 2.1 SOLUTIONS 99 Solutions for Section 2.1 1. (a) Te average rate of cange is te slope of te secant line in Figure 2.1, wic sows tat tis slope is positive. (b) Te instantaneous rate of cange

CHAPTER TWO 2.1 SOLUTIONS 99 Solutions for Section 2.1 1. (a) Te average rate of cange is te slope of te secant line in Figure 2.1, wic sows tat tis slope is positive. (b) Te instantaneous rate of cange

Lecture 10: What is a Function, definition, piecewise defined functions, difference quotient, domain of a function

Lecture 10: Wat is a Function, definition, piecewise defined functions, difference quotient, domain of a function A function arises wen one quantity depends on anoter. Many everyday relationsips between

Lecture 10: Wat is a Function, definition, piecewise defined functions, difference quotient, domain of a function A function arises wen one quantity depends on anoter. Many everyday relationsips between

Schedulability Analysis under Graph Routing in WirelessHART Networks

Scedulability Analysis under Grap Routing in WirelessHART Networks Abusayeed Saifulla, Dolvara Gunatilaka, Paras Tiwari, Mo Sa, Cenyang Lu, Bo Li Cengjie Wu, and Yixin Cen Department of Computer Science,

Scedulability Analysis under Grap Routing in WirelessHART Networks Abusayeed Saifulla, Dolvara Gunatilaka, Paras Tiwari, Mo Sa, Cenyang Lu, Bo Li Cengjie Wu, and Yixin Cen Department of Computer Science,

A strong credit score can help you score a lower rate on a mortgage

NET GAIN Scoring points for your financial future AS SEEN IN USA TODAY S MONEY SECTION, JULY 3, 2007 A strong credit score can elp you score a lower rate on a mortgage By Sandra Block Sales of existing

NET GAIN Scoring points for your financial future AS SEEN IN USA TODAY S MONEY SECTION, JULY 3, 2007 A strong credit score can elp you score a lower rate on a mortgage By Sandra Block Sales of existing

Average and Instantaneous Rates of Change: The Derivative

9.3 verage and Instantaneous Rates of Cange: Te Derivative 609 OBJECTIVES 9.3 To define and find average rates of cange To define te derivative as a rate of cange To use te definition of derivative to

9.3 verage and Instantaneous Rates of Cange: Te Derivative 609 OBJECTIVES 9.3 To define and find average rates of cange To define te derivative as a rate of cange To use te definition of derivative to

College Planning Using Cash Value Life Insurance

College Planning Using Cas Value Life Insurance CAUTION: Te advisor is urged to be extremely cautious of anoter college funding veicle wic provides a guaranteed return of premium immediately if funded

College Planning Using Cas Value Life Insurance CAUTION: Te advisor is urged to be extremely cautious of anoter college funding veicle wic provides a guaranteed return of premium immediately if funded

Strategic trading and welfare in a dynamic market. Dimitri Vayanos

LSE Researc Online Article (refereed) Strategic trading and welfare in a dynamic market Dimitri Vayanos LSE as developed LSE Researc Online so tat users may access researc output of te Scool. Copyrigt

LSE Researc Online Article (refereed) Strategic trading and welfare in a dynamic market Dimitri Vayanos LSE as developed LSE Researc Online so tat users may access researc output of te Scool. Copyrigt

Comparison between two approaches to overload control in a Real Server: local or hybrid solutions?

Comparison between two approaces to overload control in a Real Server: local or ybrid solutions? S. Montagna and M. Pignolo Researc and Development Italtel S.p.A. Settimo Milanese, ITALY Abstract Tis wor

Comparison between two approaces to overload control in a Real Server: local or ybrid solutions? S. Montagna and M. Pignolo Researc and Development Italtel S.p.A. Settimo Milanese, ITALY Abstract Tis wor

2.1: The Derivative and the Tangent Line Problem

.1.1.1: Te Derivative and te Tangent Line Problem Wat is te deinition o a tangent line to a curve? To answer te diiculty in writing a clear deinition o a tangent line, we can deine it as te iting position

.1.1.1: Te Derivative and te Tangent Line Problem Wat is te deinition o a tangent line to a curve? To answer te diiculty in writing a clear deinition o a tangent line, we can deine it as te iting position

Pretrial Settlement with Imperfect Private Monitoring

Pretrial Settlement wit Imperfect Private Monitoring Mostafa Beskar Indiana University Jee-Hyeong Park y Seoul National University April, 2016 Extremely Preliminary; Please Do Not Circulate. Abstract We

Pretrial Settlement wit Imperfect Private Monitoring Mostafa Beskar Indiana University Jee-Hyeong Park y Seoul National University April, 2016 Extremely Preliminary; Please Do Not Circulate. Abstract We

TRADING AWAY WIDE BRANDS FOR CHEAP BRANDS. Swati Dhingra London School of Economics and CEP. Online Appendix

TRADING AWAY WIDE BRANDS FOR CHEAP BRANDS Swati Dingra London Scool of Economics and CEP Online Appendix APPENDIX A. THEORETICAL & EMPIRICAL RESULTS A.1. CES and Logit Preferences: Invariance of Innovation

TRADING AWAY WIDE BRANDS FOR CHEAP BRANDS Swati Dingra London Scool of Economics and CEP Online Appendix APPENDIX A. THEORETICAL & EMPIRICAL RESULTS A.1. CES and Logit Preferences: Invariance of Innovation

Optimized Data Indexing Algorithms for OLAP Systems

Database Systems Journal vol. I, no. 2/200 7 Optimized Data Indexing Algoritms for OLAP Systems Lucian BORNAZ Faculty of Cybernetics, Statistics and Economic Informatics Academy of Economic Studies, Bucarest

Database Systems Journal vol. I, no. 2/200 7 Optimized Data Indexing Algoritms for OLAP Systems Lucian BORNAZ Faculty of Cybernetics, Statistics and Economic Informatics Academy of Economic Studies, Bucarest

Distances in random graphs with infinite mean degrees

Distances in random graps wit infinite mean degrees Henri van den Esker, Remco van der Hofstad, Gerard Hoogiemstra and Dmitri Znamenski April 26, 2005 Abstract We study random graps wit an i.i.d. degree

Distances in random graps wit infinite mean degrees Henri van den Esker, Remco van der Hofstad, Gerard Hoogiemstra and Dmitri Znamenski April 26, 2005 Abstract We study random graps wit an i.i.d. degree

Torchmark Corporation 2001 Third Avenue South Birmingham, Alabama 35233 Contact: Joyce Lane 972-569-3627 NYSE Symbol: TMK

News Release Torcmark Corporation 2001 Tird Avenue Sout Birmingam, Alabama 35233 Contact: Joyce Lane 972-569-3627 NYSE Symbol: TMK TORCHMARK CORPORATION REPORTS FOURTH QUARTER AND YEAR-END 2004 RESULTS

News Release Torcmark Corporation 2001 Tird Avenue Sout Birmingam, Alabama 35233 Contact: Joyce Lane 972-569-3627 NYSE Symbol: TMK TORCHMARK CORPORATION REPORTS FOURTH QUARTER AND YEAR-END 2004 RESULTS

ACT Math Facts & Formulas

Numbers, Sequences, Factors Integers:..., -3, -2, -1, 0, 1, 2, 3,... Rationals: fractions, tat is, anyting expressable as a ratio of integers Reals: integers plus rationals plus special numbers suc as

Numbers, Sequences, Factors Integers:..., -3, -2, -1, 0, 1, 2, 3,... Rationals: fractions, tat is, anyting expressable as a ratio of integers Reals: integers plus rationals plus special numbers suc as

= C + I + G + NX ECON 302. Lecture 4: Aggregate Expenditures/Keynesian Model: Equilibrium in the Goods Market/Loanable Funds Market

Intermediate Macroeconomics Lecture 4: Introduction to the Goods Market Review of the Aggregate Expenditures model and the Keynesian Cross ECON 302 Professor Yamin Ahmad Components of Aggregate Demand

Intermediate Macroeconomics Lecture 4: Introduction to the Goods Market Review of the Aggregate Expenditures model and the Keynesian Cross ECON 302 Professor Yamin Ahmad Components of Aggregate Demand

The modelling of business rules for dashboard reporting using mutual information

8 t World IMACS / MODSIM Congress, Cairns, Australia 3-7 July 2009 ttp://mssanz.org.au/modsim09 Te modelling of business rules for dasboard reporting using mutual information Gregory Calbert Command, Control,

8 t World IMACS / MODSIM Congress, Cairns, Australia 3-7 July 2009 ttp://mssanz.org.au/modsim09 Te modelling of business rules for dasboard reporting using mutual information Gregory Calbert Command, Control,

Yale ICF Working Paper No. 05-11 May 2005

Yale ICF Working Paper No. 05-11 May 2005 HUMAN CAPITAL, AET ALLOCATION, AND LIFE INURANCE Roger G. Ibbotson, Yale cool of Management, Yale University Peng Cen, Ibbotson Associates Mose Milevsky, culic

Yale ICF Working Paper No. 05-11 May 2005 HUMAN CAPITAL, AET ALLOCATION, AND LIFE INURANCE Roger G. Ibbotson, Yale cool of Management, Yale University Peng Cen, Ibbotson Associates Mose Milevsky, culic

Section 3.3. Differentiation of Polynomials and Rational Functions. Difference Equations to Differential Equations

Difference Equations to Differential Equations Section 3.3 Differentiation of Polynomials an Rational Functions In tis section we begin te task of iscovering rules for ifferentiating various classes of

Difference Equations to Differential Equations Section 3.3 Differentiation of Polynomials an Rational Functions In tis section we begin te task of iscovering rules for ifferentiating various classes of

Computer Science and Engineering, UCSD October 7, 1999 Goldreic-Levin Teorem Autor: Bellare Te Goldreic-Levin Teorem 1 Te problem We æx a an integer n for te lengt of te strings involved. If a is an n-bit

Computer Science and Engineering, UCSD October 7, 1999 Goldreic-Levin Teorem Autor: Bellare Te Goldreic-Levin Teorem 1 Te problem We æx a an integer n for te lengt of te strings involved. If a is an n-bit

FINITE DIFFERENCE METHODS

FINITE DIFFERENCE METHODS LONG CHEN Te best known metods, finite difference, consists of replacing eac derivative by a difference quotient in te classic formulation. It is simple to code and economic to

FINITE DIFFERENCE METHODS LONG CHEN Te best known metods, finite difference, consists of replacing eac derivative by a difference quotient in te classic formulation. It is simple to code and economic to

Note: Principal version Modification Modification Complete version from 1 October 2014 Business Law Corporate and Contract Law

Note: Te following curriculum is a consolidated version. It is legally non-binding and for informational purposes only. Te legally binding versions are found in te University of Innsbruck Bulletins (in

Note: Te following curriculum is a consolidated version. It is legally non-binding and for informational purposes only. Te legally binding versions are found in te University of Innsbruck Bulletins (in

Improved dynamic programs for some batcing problems involving te maximum lateness criterion A P M Wagelmans Econometric Institute Erasmus University Rotterdam PO Box 1738, 3000 DR Rotterdam Te Neterlands

Improved dynamic programs for some batcing problems involving te maximum lateness criterion A P M Wagelmans Econometric Institute Erasmus University Rotterdam PO Box 1738, 3000 DR Rotterdam Te Neterlands

Chapter 11. Limits and an Introduction to Calculus. Selected Applications

Capter Limits and an Introduction to Calculus. Introduction to Limits. Tecniques for Evaluating Limits. Te Tangent Line Problem. Limits at Infinit and Limits of Sequences.5 Te Area Problem Selected Applications

Capter Limits and an Introduction to Calculus. Introduction to Limits. Tecniques for Evaluating Limits. Te Tangent Line Problem. Limits at Infinit and Limits of Sequences.5 Te Area Problem Selected Applications

Catalogue no. 12-001-XIE. Survey Methodology. December 2004

Catalogue no. 1-001-XIE Survey Metodology December 004 How to obtain more information Specific inquiries about tis product and related statistics or services sould be directed to: Business Survey Metods

Catalogue no. 1-001-XIE Survey Metodology December 004 How to obtain more information Specific inquiries about tis product and related statistics or services sould be directed to: Business Survey Metods

2.23 Gambling Rehabilitation Services. Introduction

2.23 Gambling Reabilitation Services Introduction Figure 1 Since 1995 provincial revenues from gambling activities ave increased over 56% from $69.2 million in 1995 to $108 million in 2004. Te majority

2.23 Gambling Reabilitation Services Introduction Figure 1 Since 1995 provincial revenues from gambling activities ave increased over 56% from $69.2 million in 1995 to $108 million in 2004. Te majority

Notes: Most of the material in this chapter is taken from Young and Freedman, Chap. 12.

Capter 6. Fluid Mecanics Notes: Most of te material in tis capter is taken from Young and Freedman, Cap. 12. 6.1 Fluid Statics Fluids, i.e., substances tat can flow, are te subjects of tis capter. But

Capter 6. Fluid Mecanics Notes: Most of te material in tis capter is taken from Young and Freedman, Cap. 12. 6.1 Fluid Statics Fluids, i.e., substances tat can flow, are te subjects of tis capter. But

The Short-Run Macro Model. The Short-Run Macro Model. The Short-Run Macro Model

The Short-Run Macro Model In the short run, spending depends on income, and income depends on spending. The Short-Run Macro Model Short-Run Macro Model A macroeconomic model that explains how changes in

The Short-Run Macro Model In the short run, spending depends on income, and income depends on spending. The Short-Run Macro Model Short-Run Macro Model A macroeconomic model that explains how changes in

Staffing and routing in a two-tier call centre. Sameer Hasija*, Edieal J. Pinker and Robert A. Shumsky

8 Int. J. Operational Researc, Vol. 1, Nos. 1/, 005 Staffing and routing in a two-tier call centre Sameer Hasija*, Edieal J. Pinker and Robert A. Sumsky Simon Scool, University of Rocester, Rocester 1467,

8 Int. J. Operational Researc, Vol. 1, Nos. 1/, 005 Staffing and routing in a two-tier call centre Sameer Hasija*, Edieal J. Pinker and Robert A. Sumsky Simon Scool, University of Rocester, Rocester 1467,

Digital evolution Where next for the consumer facing business?

Were next for te consumer facing business? Cover 2 Digital tecnologies are powerful enablers and lie beind a combination of disruptive forces. Teir rapid continuous development demands a response from

Were next for te consumer facing business? Cover 2 Digital tecnologies are powerful enablers and lie beind a combination of disruptive forces. Teir rapid continuous development demands a response from

ECO209 MACROECONOMIC THEORY. Chapter 11

Prof. Gustavo Indart Department of Economics University of Toronto ECO209 MACROECONOMIC THEORY Chapter 11 MONEY, INTEREST, AND INCOME Discussion Questions: 1. The model in Chapter 9 assumed that both the

Prof. Gustavo Indart Department of Economics University of Toronto ECO209 MACROECONOMIC THEORY Chapter 11 MONEY, INTEREST, AND INCOME Discussion Questions: 1. The model in Chapter 9 assumed that both the

Section 2.3 Solving Right Triangle Trigonometry

Section.3 Solving Rigt Triangle Trigonometry Eample In te rigt triangle ABC, A = 40 and c = 1 cm. Find a, b, and B. sin 40 a a c 1 a 1sin 40 7.7cm cos 40 b c b 1 b 1cos40 9.cm A 40 1 b C B a B = 90 - A

Section.3 Solving Rigt Triangle Trigonometry Eample In te rigt triangle ABC, A = 40 and c = 1 cm. Find a, b, and B. sin 40 a a c 1 a 1sin 40 7.7cm cos 40 b c b 1 b 1cos40 9.cm A 40 1 b C B a B = 90 - A

Math Test Sections. The College Board: Expanding College Opportunity

Taking te SAT I: Reasoning Test Mat Test Sections Te materials in tese files are intended for individual use by students getting ready to take an SAT Program test; permission for any oter use must be sougt

Taking te SAT I: Reasoning Test Mat Test Sections Te materials in tese files are intended for individual use by students getting ready to take an SAT Program test; permission for any oter use must be sougt

Answers to Text Questions and Problems in Chapter 8

Answers to Text Questions and Problems in Chapter 8 Answers to Review Questions 1. The key assumption is that, in the short run, firms meet demand at pre-set prices. The fact that firms produce to meet

Answers to Text Questions and Problems in Chapter 8 Answers to Review Questions 1. The key assumption is that, in the short run, firms meet demand at pre-set prices. The fact that firms produce to meet

Geometric Stratification of Accounting Data

Stratification of Accounting Data Patricia Gunning * Jane Mary Horgan ** William Yancey *** Abstract: We suggest a new procedure for defining te boundaries of te strata in igly skewed populations, usual

Stratification of Accounting Data Patricia Gunning * Jane Mary Horgan ** William Yancey *** Abstract: We suggest a new procedure for defining te boundaries of te strata in igly skewed populations, usual

SAT Math Must-Know Facts & Formulas

SAT Mat Must-Know Facts & Formuas Numbers, Sequences, Factors Integers:..., -3, -2, -1, 0, 1, 2, 3,... Rationas: fractions, tat is, anyting expressabe as a ratio of integers Reas: integers pus rationas

SAT Mat Must-Know Facts & Formuas Numbers, Sequences, Factors Integers:..., -3, -2, -1, 0, 1, 2, 3,... Rationas: fractions, tat is, anyting expressabe as a ratio of integers Reas: integers pus rationas

Pioneer Fund Story. Searching for Value Today and Tomorrow. Pioneer Funds Equities

Pioneer Fund Story Searcing for Value Today and Tomorrow Pioneer Funds Equities Pioneer Fund A Cornerstone of Financial Foundations Since 1928 Te fund s relatively cautious stance as kept it competitive

Pioneer Fund Story Searcing for Value Today and Tomorrow Pioneer Funds Equities Pioneer Fund A Cornerstone of Financial Foundations Since 1928 Te fund s relatively cautious stance as kept it competitive

Tis Problem and Retail Inventory Management

Optimizing Inventory Replenisment of Retail Fasion Products Marsall Fiser Kumar Rajaram Anant Raman Te Warton Scool, University of Pennsylvania, 3620 Locust Walk, 3207 SH-DH, Piladelpia, Pennsylvania 19104-6366

Optimizing Inventory Replenisment of Retail Fasion Products Marsall Fiser Kumar Rajaram Anant Raman Te Warton Scool, University of Pennsylvania, 3620 Locust Walk, 3207 SH-DH, Piladelpia, Pennsylvania 19104-6366

Free Shipping and Repeat Buying on the Internet: Theory and Evidence

Free Sipping and Repeat Buying on te Internet: eory and Evidence Yingui Yang, Skander Essegaier and David R. Bell 1 June 13, 2005 1 Graduate Scool of Management, University of California at Davis ([email protected])

Free Sipping and Repeat Buying on te Internet: eory and Evidence Yingui Yang, Skander Essegaier and David R. Bell 1 June 13, 2005 1 Graduate Scool of Management, University of California at Davis ([email protected])

CHAPTER 8: DIFFERENTIAL CALCULUS

CHAPTER 8: DIFFERENTIAL CALCULUS 1. Rules of Differentiation As we ave seen, calculating erivatives from first principles can be laborious an ifficult even for some relatively simple functions. It is clearly

CHAPTER 8: DIFFERENTIAL CALCULUS 1. Rules of Differentiation As we ave seen, calculating erivatives from first principles can be laborious an ifficult even for some relatively simple functions. It is clearly

2.12 Student Transportation. Introduction

Introduction Figure 1 At 31 Marc 2003, tere were approximately 84,000 students enrolled in scools in te Province of Newfoundland and Labrador, of wic an estimated 57,000 were transported by scool buses.

Introduction Figure 1 At 31 Marc 2003, tere were approximately 84,000 students enrolled in scools in te Province of Newfoundland and Labrador, of wic an estimated 57,000 were transported by scool buses.

For Sale By Owner Program. We can help with our for sale by owner kit that includes:

Dawn Coen Broker/Owner For Sale By Owner Program If you want to sell your ome By Owner wy not:: For Sale Dawn Coen Broker/Owner YOUR NAME YOUR PHONE # Look as professional as possible Be totally prepared

Dawn Coen Broker/Owner For Sale By Owner Program If you want to sell your ome By Owner wy not:: For Sale Dawn Coen Broker/Owner YOUR NAME YOUR PHONE # Look as professional as possible Be totally prepared

CHAPTER 7. Di erentiation

CHAPTER 7 Di erentiation 1. Te Derivative at a Point Definition 7.1. Let f be a function defined on a neigborood of x 0. f is di erentiable at x 0, if te following it exists: f 0 fx 0 + ) fx 0 ) x 0 )=.

CHAPTER 7 Di erentiation 1. Te Derivative at a Point Definition 7.1. Let f be a function defined on a neigborood of x 0. f is di erentiable at x 0, if te following it exists: f 0 fx 0 + ) fx 0 ) x 0 )=.

Model Quality Report in Business Statistics

Model Quality Report in Business Statistics Mats Bergdal, Ole Blac, Russell Bowater, Ray Cambers, Pam Davies, David Draper, Eva Elvers, Susan Full, David Holmes, Pär Lundqvist, Sixten Lundström, Lennart

Model Quality Report in Business Statistics Mats Bergdal, Ole Blac, Russell Bowater, Ray Cambers, Pam Davies, David Draper, Eva Elvers, Susan Full, David Holmes, Pär Lundqvist, Sixten Lundström, Lennart

MATHEMATICS FOR ENGINEERING DIFFERENTIATION TUTORIAL 1 - BASIC DIFFERENTIATION

MATHEMATICS FOR ENGINEERING DIFFERENTIATION TUTORIAL 1 - BASIC DIFFERENTIATION Tis tutorial is essential pre-requisite material for anyone stuing mecanical engineering. Tis tutorial uses te principle of

MATHEMATICS FOR ENGINEERING DIFFERENTIATION TUTORIAL 1 - BASIC DIFFERENTIATION Tis tutorial is essential pre-requisite material for anyone stuing mecanical engineering. Tis tutorial uses te principle of

Asymmetric Trade Liberalizations and Current Account Dynamics

Asymmetric Trade Liberalizations and Current Account Dynamics Alessandro Barattieri January 15, 2015 Abstract Te current account deficits of Spain, Portugal and Greece are te result of large deficits in

Asymmetric Trade Liberalizations and Current Account Dynamics Alessandro Barattieri January 15, 2015 Abstract Te current account deficits of Spain, Portugal and Greece are te result of large deficits in

Bonferroni-Based Size-Correction for Nonstandard Testing Problems

Bonferroni-Based Size-Correction for Nonstandard Testing Problems Adam McCloskey Brown University October 2011; Tis Version: October 2012 Abstract We develop powerful new size-correction procedures for

Bonferroni-Based Size-Correction for Nonstandard Testing Problems Adam McCloskey Brown University October 2011; Tis Version: October 2012 Abstract We develop powerful new size-correction procedures for

0 100 200 300 Real income (Y)

") Lecture 11-1 6.1 The open economy, the multiplier, and the IS curve Assume that the economy is either closed (no foreign trade) or open. Assume that the exchange rates are either fixed or flexible. Assume

Lecture 11-1 6.1 The open economy, the multiplier, and the IS curve Assume that the economy is either closed (no foreign trade) or open. Assume that the exchange rates are either fixed or flexible. Assume

The IS-LM Model Ing. Mansoor Maitah Ph.D.

The IS-LM Model Ing. Mansoor Maitah Ph.D. Constructing the Keynesian Cross Equilibrium is at the point where Y = C + I + G. If firms were producing at Y 1 then Y > E Because actual expenditure exceeds

The IS-LM Model Ing. Mansoor Maitah Ph.D. Constructing the Keynesian Cross Equilibrium is at the point where Y = C + I + G. If firms were producing at Y 1 then Y > E Because actual expenditure exceeds

Note nine: Linear programming CSE 101. 1 Linear constraints and objective functions. 1.1 Introductory example. Copyright c Sanjoy Dasgupta 1

Copyrigt c Sanjoy Dasgupta Figure. (a) Te feasible region for a linear program wit two variables (see tet for details). (b) Contour lines of te objective function: for different values of (profit). Te

Copyrigt c Sanjoy Dasgupta Figure. (a) Te feasible region for a linear program wit two variables (see tet for details). (b) Contour lines of te objective function: for different values of (profit). Te

Welfare, financial innovation and self insurance in dynamic incomplete markets models

Welfare, financial innovation and self insurance in dynamic incomplete markets models Paul Willen Department of Economics Princeton University First version: April 998 Tis version: July 999 Abstract We

Welfare, financial innovation and self insurance in dynamic incomplete markets models Paul Willen Department of Economics Princeton University First version: April 998 Tis version: July 999 Abstract We

THE IMPACT OF INTERLINKED INDEX INSURANCE AND CREDIT CONTRACTS ON FINANCIAL MARKET DEEPENING AND SMALL FARM PRODUCTIVITY

THE IMPACT OF INTERLINKED INDEX INSURANCE AND CREDIT CONTRACTS ON FINANCIAL MARKET DEEPENING AND SMALL FARM PRODUCTIVITY Micael R. Carter Lan Ceng Alexander Sarris University of California, Davis University

THE IMPACT OF INTERLINKED INDEX INSURANCE AND CREDIT CONTRACTS ON FINANCIAL MARKET DEEPENING AND SMALL FARM PRODUCTIVITY Micael R. Carter Lan Ceng Alexander Sarris University of California, Davis University

The Derivative as a Function

Section 2.2 Te Derivative as a Function 200 Kiryl Tsiscanka Te Derivative as a Function DEFINITION: Te derivative of a function f at a number a, denoted by f (a), is if tis limit exists. f (a) f(a+) f(a)

Section 2.2 Te Derivative as a Function 200 Kiryl Tsiscanka Te Derivative as a Function DEFINITION: Te derivative of a function f at a number a, denoted by f (a), is if tis limit exists. f (a) f(a+) f(a)

Predicting the behavior of interacting humans by fusing data from multiple sources

Predicting te beavior of interacting umans by fusing data from multiple sources Erik J. Sclict 1, Ritcie Lee 2, David H. Wolpert 3,4, Mykel J. Kocenderfer 1, and Brendan Tracey 5 1 Lincoln Laboratory,

Predicting te beavior of interacting umans by fusing data from multiple sources Erik J. Sclict 1, Ritcie Lee 2, David H. Wolpert 3,4, Mykel J. Kocenderfer 1, and Brendan Tracey 5 1 Lincoln Laboratory,

FINANCIAL SECTOR INEFFICIENCIES AND THE DEBT LAFFER CURVE

INTERNATIONAL JOURNAL OF FINANCE AND ECONOMICS Int. J. Fin. Econ. 10: 1 13 (2005) Publised online in Wiley InterScience (www.interscience.wiley.com). DOI: 10.1002/ijfe.251 FINANCIAL SECTOR INEFFICIENCIES

INTERNATIONAL JOURNAL OF FINANCE AND ECONOMICS Int. J. Fin. Econ. 10: 1 13 (2005) Publised online in Wiley InterScience (www.interscience.wiley.com). DOI: 10.1002/ijfe.251 FINANCIAL SECTOR INEFFICIENCIES

Keynesian Macroeconomic Theory

2 Keynesian Macroeconomic Theory 2.1. The Keynesian Consumption Function 2.2. The Complete Keynesian Model 2.3. The Keynesian-Cross Model 2.4. The IS-LM Model 2.5. The Keynesian AD-AS Model 2.6. Conclusion

2 Keynesian Macroeconomic Theory 2.1. The Keynesian Consumption Function 2.2. The Complete Keynesian Model 2.3. The Keynesian-Cross Model 2.4. The IS-LM Model 2.5. The Keynesian AD-AS Model 2.6. Conclusion

OPTIMAL FLEET SELECTION FOR EARTHMOVING OPERATIONS

New Developments in Structural Engineering and Construction Yazdani, S. and Sing, A. (eds.) ISEC-7, Honolulu, June 18-23, 2013 OPTIMAL FLEET SELECTION FOR EARTHMOVING OPERATIONS JIALI FU 1, ERIK JENELIUS

New Developments in Structural Engineering and Construction Yazdani, S. and Sing, A. (eds.) ISEC-7, Honolulu, June 18-23, 2013 OPTIMAL FLEET SELECTION FOR EARTHMOVING OPERATIONS JIALI FU 1, ERIK JENELIUS

OPTIMAL DISCONTINUOUS GALERKIN METHODS FOR THE ACOUSTIC WAVE EQUATION IN HIGHER DIMENSIONS

OPTIMAL DISCONTINUOUS GALERKIN METHODS FOR THE ACOUSTIC WAVE EQUATION IN HIGHER DIMENSIONS ERIC T. CHUNG AND BJÖRN ENGQUIST Abstract. In tis paper, we developed and analyzed a new class of discontinuous

OPTIMAL DISCONTINUOUS GALERKIN METHODS FOR THE ACOUSTIC WAVE EQUATION IN HIGHER DIMENSIONS ERIC T. CHUNG AND BJÖRN ENGQUIST Abstract. In tis paper, we developed and analyzed a new class of discontinuous

M.A.PART - I ECONOMIC PAPER - I MACRO ECONOMICS

1 M.A.PART - I ECONOMIC PAPER - I MACRO ECONOMICS 1. Basic Macroeconomics Income and spending The consumption function Savings and investment The Keynesian Multiplier The budget Balanced budget : theorem

1 M.A.PART - I ECONOMIC PAPER - I MACRO ECONOMICS 1. Basic Macroeconomics Income and spending The consumption function Savings and investment The Keynesian Multiplier The budget Balanced budget : theorem

M(0) = 1 M(1) = 2 M(h) = M(h 1) + M(h 2) + 1 (h > 1)

= 1 M(1) = 2 M(h) = M(h 1) + M(h 2) + 1 (h > 1)") Insertion and Deletion in VL Trees Submitted in Partial Fulfillment of te Requirements for Dr. Eric Kaltofen s 66621: nalysis of lgoritms by Robert McCloskey December 14, 1984 1 ackground ccording to Knut

Insertion and Deletion in VL Trees Submitted in Partial Fulfillment of te Requirements for Dr. Eric Kaltofen s 66621: nalysis of lgoritms by Robert McCloskey December 14, 1984 1 ackground ccording to Knut

Writing Mathematics Papers

Writing Matematics Papers Tis essay is intended to elp your senior conference paper. It is a somewat astily produced amalgam of advice I ave given to students in my PDCs (Mat 4 and Mat 9), so it s not

Writing Matematics Papers Tis essay is intended to elp your senior conference paper. It is a somewat astily produced amalgam of advice I ave given to students in my PDCs (Mat 4 and Mat 9), so it s not

These are some practice questions for CHAPTER 23. Each question should have a single answer. But be careful. There may be errors in the answer key!

These are some practice questions for CHAPTER 23. Each question should have a single answer. But be careful. There may be errors in the answer key! 67. Public saving is equal to a. net tax revenues minus

These are some practice questions for CHAPTER 23. Each question should have a single answer. But be careful. There may be errors in the answer key! 67. Public saving is equal to a. net tax revenues minus

His solution? Federal law that requires government agencies and private industry to encrypt, or digitally scramble, sensitive data.

NET GAIN Scoring points for your financial future AS SEEN IN USA TODAY S MONEY SECTION, FEBRUARY 9, 2007 Tec experts plot to catc identity tieves Politicians to security gurus offer ideas to prevent data

NET GAIN Scoring points for your financial future AS SEEN IN USA TODAY S MONEY SECTION, FEBRUARY 9, 2007 Tec experts plot to catc identity tieves Politicians to security gurus offer ideas to prevent data

Channel Allocation in Non-Cooperative Multi-Radio Multi-Channel Wireless Networks

Cannel Allocation in Non-Cooperative Multi-Radio Multi-Cannel Wireless Networks Dejun Yang, Xi Fang, Guoliang Xue Arizona State University Abstract Wile tremendous efforts ave been made on cannel allocation

Cannel Allocation in Non-Cooperative Multi-Radio Multi-Cannel Wireless Networks Dejun Yang, Xi Fang, Guoliang Xue Arizona State University Abstract Wile tremendous efforts ave been made on cannel allocation

Cyber Epidemic Models with Dependences

Cyber Epidemic Models wit Dependences Maocao Xu 1, Gaofeng Da 2 and Souuai Xu 3 1 Department of Matematics, Illinois State University [email protected] 2 Institute for Cyber Security, University of Texas

Cyber Epidemic Models wit Dependences Maocao Xu 1, Gaofeng Da 2 and Souuai Xu 3 1 Department of Matematics, Illinois State University [email protected] 2 Institute for Cyber Security, University of Texas

To motivate the notion of a variogram for a covariance stationary process, { Ys ( ): s R}

: s R}") 4. Variograms Te covariogram and its normalized form, te correlogram, are by far te most intuitive metods for summarizing te structure of spatial dependencies in a covariance stationary process. However,

4. Variograms Te covariogram and its normalized form, te correlogram, are by far te most intuitive metods for summarizing te structure of spatial dependencies in a covariance stationary process. However,

Guide to Cover Letters & Thank You Letters

Guide to Cover Letters & Tank You Letters 206 Strebel Student Center (315) 792-3087 Fax (315) 792-3370 TIPS FOR WRITING A PERFECT COVER LETTER Te resume never travels alone. Eac time you submit your resume

Guide to Cover Letters & Tank You Letters 206 Strebel Student Center (315) 792-3087 Fax (315) 792-3370 TIPS FOR WRITING A PERFECT COVER LETTER Te resume never travels alone. Eac time you submit your resume

8. Simultaneous Equilibrium in the Commodity and Money Markets

Lecture 8-1 8. Simultaneous Equilibrium in the Commodity and Money Markets We now combine the IS (commodity-market equilibrium) and LM (money-market equilibrium) schedules to establish a general equilibrium

Lecture 8-1 8. Simultaneous Equilibrium in the Commodity and Money Markets We now combine the IS (commodity-market equilibrium) and LM (money-market equilibrium) schedules to establish a general equilibrium

SAMPLE DESIGN FOR THE TERRORISM RISK INSURANCE PROGRAM SURVEY

ASA Section on Survey Researc Metods SAMPLE DESIG FOR TE TERRORISM RISK ISURACE PROGRAM SURVEY G. ussain Coudry, Westat; Mats yfjäll, Statisticon; and Marianne Winglee, Westat G. ussain Coudry, Westat,

ASA Section on Survey Researc Metods SAMPLE DESIG FOR TE TERRORISM RISK ISURACE PROGRAM SURVEY G. ussain Coudry, Westat; Mats yfjäll, Statisticon; and Marianne Winglee, Westat G. ussain Coudry, Westat,

Shell and Tube Heat Exchanger

Sell and Tube Heat Excanger MECH595 Introduction to Heat Transfer Professor M. Zenouzi Prepared by: Andrew Demedeiros, Ryan Ferguson, Bradford Powers November 19, 2009 1 Abstract 2 Contents Discussion

Sell and Tube Heat Excanger MECH595 Introduction to Heat Transfer Professor M. Zenouzi Prepared by: Andrew Demedeiros, Ryan Ferguson, Bradford Powers November 19, 2009 1 Abstract 2 Contents Discussion

A system to monitor the quality of automated coding of textual answers to open questions

Researc in Official Statistics Number 2/2001 A system to monitor te quality of automated coding of textual answers to open questions Stefania Maccia * and Marcello D Orazio ** Italian National Statistical

Researc in Official Statistics Number 2/2001 A system to monitor te quality of automated coding of textual answers to open questions Stefania Maccia * and Marcello D Orazio ** Italian National Statistical

Pressure. Pressure. Atmospheric pressure. Conceptual example 1: Blood pressure. Pressure is force per unit area:

Pressure Pressure is force per unit area: F P = A Pressure Te direction of te force exerted on an object by a fluid is toward te object and perpendicular to its surface. At a microscopic level, te force

Pressure Pressure is force per unit area: F P = A Pressure Te direction of te force exerted on an object by a fluid is toward te object and perpendicular to its surface. At a microscopic level, te force

Macroeconomic conditions influence consumers attitudes,

Yu Ma, Kusum L. Ailawadi, Dines K. Gauri, & Druv Grewal An Empirical Investigation of te Impact of Gasoline Prices on Grocery Sopping Beavior Te autors empirically examine te effect of gas prices on grocery

Yu Ma, Kusum L. Ailawadi, Dines K. Gauri, & Druv Grewal An Empirical Investigation of te Impact of Gasoline Prices on Grocery Sopping Beavior Te autors empirically examine te effect of gas prices on grocery