Chapter 4. The Time Value of Money

|

|

|

- Alfred Owens

- 10 years ago

- Views:

Transcription

1 Chapter 4 The Time Value of Money 1

2 Learning Outcomes Chapter 4 Identify various types of cash flow patterns Compute the future value and the present value of different cash flow streams Compute the return on an investment and how long it takes to reach a financial goal Explain the difference between the Annual Percentage Rate and the Effective Annual Rate Describe an amortized loan. Compute amortized loan payments and the amount that must be paid at a specific point during the life of the loan 2

3 Time Value of Money The principles and computations used to revalue cash payoffs from different times so they are stated in dollars of the same time period. 3

4 Cash Flow Time Lines Graphical representations used to show timing of cash flows PV = Present Value the beginning amount that can be invested. PV also represents the current value of some future amount. FV = Future Value the value to which an amount invested today will grow at the end of n periods. 4

5 Types of Cash Flow Patterns Lump Sum Amount a single payment (received or made) that occurs either today or at some date in the future. Annuity Multiple payments of the same amount over equal time periods. Uneven Cash Flows Multiple payments of different amounts over a period of time. 5

6 Future Value Compounding To compute the future value of an amount we push forward the current amount by adding interest for each period in which the money can earn interest in the future. 6

7 Future Value of a Lump-Sum Amount FV n 7

8 Four Ways to Solve Time Value of Money Problems Use Cash Flow Time Line Use Equations Use Financial Calculator Use Electronic Spreadsheet 8

9 Time Line Solution The Future Value of $700 invested at 10% per year for 3 years 9

10 Equation Solution FV 3 = $700(1.10) 3 = $700( ) = $

3 = 33100) =")

11 Financial Calculator Solution 11

12 Spreadsheet Solution - MS Excel 1. Set up a table that contains the data used to solve the problem 2. Click f x and choose function 3. Click the cells containing the appropriate data to calculate the answer Rate (B2) Number of periods (B1) Present value (B3) Payment (B4) (not used) Type (B5) (not used) 12

13 Future Value of an Annuity Annuity - A series of payments of equal amounts at fixed intervals for a specified number of periods. Ordinary (deferred) Annuity - An annuity whose payments occur at the end of each period. Annuity Due - An annuity whose payments occur at the beginning of each period. 13

14 What s the FV of a 3-year Ordinary Annuity of $400 at 5%? 14

15 Equation Solution: 15

16 Financial Calculator Solution 16

17 Find the FV of an Annuity Due 17

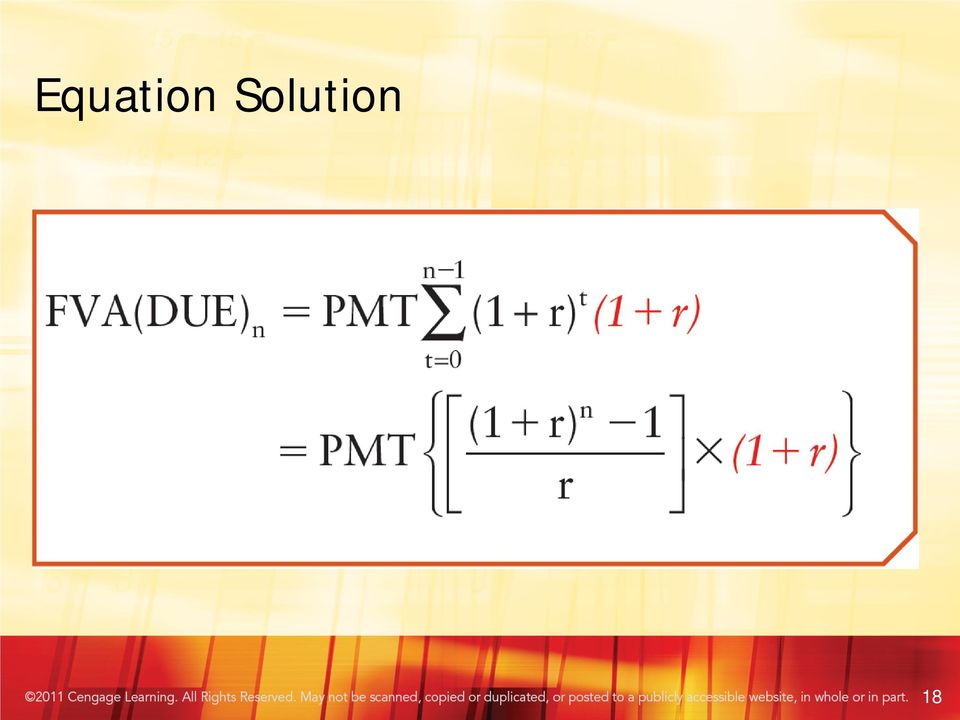

18 Equation Solution 18

19 Financial Calculator Solution 19

20 Find the FV of an Uneven Cash Flow Stream FVCF n 20

21 Equation Solution 21

22 Present Value Present value is the value today of a future cash flow or series of cash flows. Discounting is the process of finding the present value of a future cash flow or series of future cash flows; it is the reverse of compounding. 22

23 Present Value of a Lump-Sum Amount PV 23

24 PV of a Lump-Sum Amount Financial Calculator 24

25 Present Value of an Annuity (Ordinary) PVA n = the present value of an annuity with n payments. Each payment is discounted, and the sum of the discounted payments is the present value of the annuity. 25

26 What is the PV of $400 due in 3 years if r = 5%? 26

27 Equation Solution 27

28 Financial Calculator Solution 28

29 Present Value of an Annuity Due 29

30 Equation Solution 30

31 Financial Calculator Solution 31

32 Perpetuities Streams of equal payments that are expected to go on forever 32

33 Uneven Cash Flow Streams A series of cash flows in which the amount varies from one period to the next: Payment (PMT) designates constant cash flows that is, an annuity stream. Cash flow (CF) designates cash flows in general, both constant cash flows and uneven cash flows. 33

34 PV of an Uneven Cash Flow Stream PVCF n 34

35 Equation Solution 35

36 Financial Calculator Solution Input in CF register: CF0 = 0 CF1 = 400 CF2 = 300 CF3 = 250 Enter I = 5, then press NPV button to get NPV =

37 Solving for Interest Rates (r) You pay $78.35 for an investment that promises to pay you $100 per year for the next five years. What annual rate of return will you earn on this investment? 37

38 Financial Calculator Solution 38

39 Solving for Time (n) A security costing $68.30 will provide a return of 10% per year and you want to keep the investment until it grows to a value of $100. How long will it take the investment to grow to $100? 39

40 Financial Calculator Solution 40

41 Semiannual and Other Compounding Periods Annual compounding is the process of determining the future value of a cash flow or series of cash flows when interest is added once a year. Semiannual compounding is the process of determining the future value of a cash flow or series of cash flows when interest is added twice a year. 41

42 The FV of a lump sum be larger if we compound more often, holding the stated r constant? Why? If compounding is more frequent than once a year for example, semi-annually, quarterly, or daily interest is earned on interest that is, compounded more often. 42

43 Distinguishing Between Different Interest Rates r SIMPLE = Simple (Quoted) Rate used to compute the interest paid per period r EAR = Effective Annual Rate the annual rate of interest actually being earned APR = Annual Percentage Rate = r SIMPLE periodic rate X the number of periods per year 43

44 Comparison of Different Types of Interest Rates r SIMPLE : Written into contracts, quoted by banks and brokers. Not used in calculations or shown on time lines. r PER : Used in calculations, shown on time lines. r EAR : Used to compare returns on investments with different payments per year. 44

45 Simple (Quoted) Rate r SIMPLE is stated in contracts Periods per year (m) must also be given Examples: 8%, compounded quarterly 8%, compounded daily (365 days) 45

46 Periodic Rate Periodic rate = r PER = r SIMPLE /m, where m is number of compounding periods per year. m = 4 for quarterly, 12 for monthly, and 360 or 365 for daily compounding. Examples: 8% quarterly: r PER = 8/4 = 2% 8% daily (365): r PER = 8/365 = % 46

47 Effective Annual Rate The annual rate that causes PV to grow to the same FV as under multi-period compounding. 47

48 How do we find r EAR for a simple rate of 10%, compounded semi-annually? r = 1 + r SIMPLE EAR m = = m ( 1.05) = = 10.25% 48

49 Amortized Loans Amortized Loan - A loan that is repaid in equal payments over its life Amortization tables are widely used for home mortgages, auto loans, business loans, retirement plans, and so forth to determine how much of each payment represents principal repayment and how much represents interest 49

50 An amortization schedule for a $15,000, 8 percent loan that requires three equal annual payments. 50

51 Financial Calculator Solution 51

52 Amortization Schedule 52

CHAPTER 2. Time Value of Money 2-1

CHAPTER 2 Time Value of Money 2-1 Time Value of Money (TVM) Time Lines Future value & Present value Rates of return Annuities & Perpetuities Uneven cash Flow Streams Amortization 2-2 Time lines 0 1 2 3

CHAPTER 2 Time Value of Money 2-1 Time Value of Money (TVM) Time Lines Future value & Present value Rates of return Annuities & Perpetuities Uneven cash Flow Streams Amortization 2-2 Time lines 0 1 2 3

Finance 331 Corporate Financial Management Week 1 Week 3 Note: For formulas, a Texas Instruments BAII Plus calculator was used.

Chapter 1 Finance 331 What is finance? - Finance has to do with decisions about money and/or cash flows. These decisions have to do with money being raised or used. General parts of finance include: -

Chapter 1 Finance 331 What is finance? - Finance has to do with decisions about money and/or cash flows. These decisions have to do with money being raised or used. General parts of finance include: -

Key Concepts and Skills. Multiple Cash Flows Future Value Example 6.1. Chapter Outline. Multiple Cash Flows Example 2 Continued

6 Calculators Discounted Cash Flow Valuation Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

6 Calculators Discounted Cash Flow Valuation Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

Discounted Cash Flow Valuation

Discounted Cash Flow Valuation Chapter 5 Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

Discounted Cash Flow Valuation Chapter 5 Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

DISCOUNTED CASH FLOW VALUATION and MULTIPLE CASH FLOWS

Chapter 5 DISCOUNTED CASH FLOW VALUATION and MULTIPLE CASH FLOWS The basic PV and FV techniques can be extended to handle any number of cash flows. PV with multiple cash flows: Suppose you need $500 one

Chapter 5 DISCOUNTED CASH FLOW VALUATION and MULTIPLE CASH FLOWS The basic PV and FV techniques can be extended to handle any number of cash flows. PV with multiple cash flows: Suppose you need $500 one

Integrated Case. 5-42 First National Bank Time Value of Money Analysis

Integrated Case 5-42 First National Bank Time Value of Money Analysis You have applied for a job with a local bank. As part of its evaluation process, you must take an examination on time value of money

Integrated Case 5-42 First National Bank Time Value of Money Analysis You have applied for a job with a local bank. As part of its evaluation process, you must take an examination on time value of money

Chapter The Time Value of Money

Chapter The Time Value of Money PPT 9-2 Chapter 9 - Outline Time Value of Money Future Value and Present Value Annuities Time-Value-of-Money Formulas Adjusting for Non-Annual Compounding Compound Interest

Chapter The Time Value of Money PPT 9-2 Chapter 9 - Outline Time Value of Money Future Value and Present Value Annuities Time-Value-of-Money Formulas Adjusting for Non-Annual Compounding Compound Interest

HOW TO CALCULATE PRESENT VALUES

Chapter 2 HOW TO CALCULATE PRESENT VALUES Brealey, Myers, and Allen Principles of Corporate Finance 11th Edition McGraw-Hill/Irwin Copyright 2014 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 2 HOW TO CALCULATE PRESENT VALUES Brealey, Myers, and Allen Principles of Corporate Finance 11th Edition McGraw-Hill/Irwin Copyright 2014 by The McGraw-Hill Companies, Inc. All rights reserved.

1. If you wish to accumulate $140,000 in 13 years, how much must you deposit today in an account that pays an annual interest rate of 14%?

Chapter 2 - Sample Problems 1. If you wish to accumulate $140,000 in 13 years, how much must you deposit today in an account that pays an annual interest rate of 14%? 2. What will $247,000 grow to be in

Chapter 2 - Sample Problems 1. If you wish to accumulate $140,000 in 13 years, how much must you deposit today in an account that pays an annual interest rate of 14%? 2. What will $247,000 grow to be in

CHAPTER 9 Time Value Analysis

Copyright 2008 by the Foundation of the American College of Healthcare Executives 6/11/07 Version 9-1 CHAPTER 9 Time Value Analysis Future and present values Lump sums Annuities Uneven cash flow streams

Copyright 2008 by the Foundation of the American College of Healthcare Executives 6/11/07 Version 9-1 CHAPTER 9 Time Value Analysis Future and present values Lump sums Annuities Uneven cash flow streams

Finding the Payment $20,000 = C[1 1 / 1.0066667 48 ] /.0066667 C = $488.26

![Finding the Payment $20,000 = C[1 1 / 1.0066667 48 ] /.0066667 C = $488.26](/thumbs/17/134163.jpg "Finding the Payment $20,000 = C[1 1 / 1.0066667 48 ] /.0066667 C = $488.26") Quick Quiz: Part 2 You know the payment amount for a loan and you want to know how much was borrowed. Do you compute a present value or a future value? You want to receive $5,000 per month in retirement.

Quick Quiz: Part 2 You know the payment amount for a loan and you want to know how much was borrowed. Do you compute a present value or a future value? You want to receive $5,000 per month in retirement.

Chapter 4 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONS

Chapter 4 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONS 4-1 a. PV (present value) is the value today of a future payment, or stream of payments, discounted at the appropriate rate of interest.

Chapter 4 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONS 4-1 a. PV (present value) is the value today of a future payment, or stream of payments, discounted at the appropriate rate of interest.

Discounted Cash Flow Valuation

6 Formulas Discounted Cash Flow Valuation McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter Outline Future and Present Values of Multiple Cash Flows Valuing

6 Formulas Discounted Cash Flow Valuation McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter Outline Future and Present Values of Multiple Cash Flows Valuing

Chapter 5 Time Value of Money 2: Analyzing Annuity Cash Flows

1. Future Value of Multiple Cash Flows 2. Future Value of an Annuity 3. Present Value of an Annuity 4. Perpetuities 5. Other Compounding Periods 6. Effective Annual Rates (EAR) 7. Amortized Loans Chapter

1. Future Value of Multiple Cash Flows 2. Future Value of an Annuity 3. Present Value of an Annuity 4. Perpetuities 5. Other Compounding Periods 6. Effective Annual Rates (EAR) 7. Amortized Loans Chapter

Ehrhardt Chapter 8 Page 1

Chapter 2 Time Value of Money 1 Time Value Topics Future value Present value Rates of return Amortization 2 Time lines show timing of cash flows. 0 1 2 3 I% CF 0 CF 1 CF 2 CF 3 Tick marks at ends of periods,

Chapter 2 Time Value of Money 1 Time Value Topics Future value Present value Rates of return Amortization 2 Time lines show timing of cash flows. 0 1 2 3 I% CF 0 CF 1 CF 2 CF 3 Tick marks at ends of periods,

Ch. Ch. 5 Discounted Cash Flows & Valuation In Chapter 5,

Ch. 5 Discounted Cash Flows & Valuation In Chapter 5, we found the PV & FV of single cash flows--either payments or receipts. In this chapter, we will do the same for multiple cash flows. 2 Multiple Cash

Ch. 5 Discounted Cash Flows & Valuation In Chapter 5, we found the PV & FV of single cash flows--either payments or receipts. In this chapter, we will do the same for multiple cash flows. 2 Multiple Cash

How to calculate present values

How to calculate present values Back to the future Chapter 3 Discounted Cash Flow Analysis (Time Value of Money) Discounted Cash Flow (DCF) analysis is the foundation of valuation in corporate finance

How to calculate present values Back to the future Chapter 3 Discounted Cash Flow Analysis (Time Value of Money) Discounted Cash Flow (DCF) analysis is the foundation of valuation in corporate finance

Solutions to Time value of money practice problems

Solutions to Time value of money practice problems Prepared by Pamela Peterson Drake 1. What is the balance in an account at the end of 10 years if $2,500 is deposited today and the account earns 4% interest,

Solutions to Time value of money practice problems Prepared by Pamela Peterson Drake 1. What is the balance in an account at the end of 10 years if $2,500 is deposited today and the account earns 4% interest,

Chapter 6. Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams

Chapter 6 Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams 1. Distinguish between an ordinary annuity and an annuity due, and calculate present

Chapter 6 Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams 1. Distinguish between an ordinary annuity and an annuity due, and calculate present

Chapter 4: Time Value of Money

FIN 301 Homework Solution Ch4 Chapter 4: Time Value of Money 1. a. 10,000/(1.10) 10 = 3,855.43 b. 10,000/(1.10) 20 = 1,486.44 c. 10,000/(1.05) 10 = 6,139.13 d. 10,000/(1.05) 20 = 3,768.89 2. a. $100 (1.10)

FIN 301 Homework Solution Ch4 Chapter 4: Time Value of Money 1. a. 10,000/(1.10) 10 = 3,855.43 b. 10,000/(1.10) 20 = 1,486.44 c. 10,000/(1.05) 10 = 6,139.13 d. 10,000/(1.05) 20 = 3,768.89 2. a. $100 (1.10)

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY 1. The simple interest per year is: $5,000.08 = $400 So after 10 years you will have: $400 10 = $4,000 in interest. The total balance will be

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY 1. The simple interest per year is: $5,000.08 = $400 So after 10 years you will have: $400 10 = $4,000 in interest. The total balance will be

2. How would (a) a decrease in the interest rate or (b) an increase in the holding period of a deposit affect its future value? Why?

a decrease in the interest rate or (b) an increase in the holding period of a deposit affect its future value? Why?") CHAPTER 3 CONCEPT REVIEW QUESTIONS 1. Will a deposit made into an account paying compound interest (assuming compounding occurs once per year) yield a higher future value after one period than an equal-sized

CHAPTER 3 CONCEPT REVIEW QUESTIONS 1. Will a deposit made into an account paying compound interest (assuming compounding occurs once per year) yield a higher future value after one period than an equal-sized

The Time Value of Money

The Time Value of Money Time Value Terminology 0 1 2 3 4 PV FV Future value (FV) is the amount an investment is worth after one or more periods. Present value (PV) is the current value of one or more future

The Time Value of Money Time Value Terminology 0 1 2 3 4 PV FV Future value (FV) is the amount an investment is worth after one or more periods. Present value (PV) is the current value of one or more future

Chapter 6. Discounted Cash Flow Valuation. Key Concepts and Skills. Multiple Cash Flows Future Value Example 6.1. Answer 6.1

Chapter 6 Key Concepts and Skills Be able to compute: the future value of multiple cash flows the present value of multiple cash flows the future and present value of annuities Discounted Cash Flow Valuation

Chapter 6 Key Concepts and Skills Be able to compute: the future value of multiple cash flows the present value of multiple cash flows the future and present value of annuities Discounted Cash Flow Valuation

The Time Value of Money C H A P T E R N I N E

The Time Value of Money C H A P T E R N I N E Figure 9-1 Relationship of present value and future value PPT 9-1 $1,000 present value $ 10% interest $1,464.10 future value 0 1 2 3 4 Number of periods Figure

The Time Value of Money C H A P T E R N I N E Figure 9-1 Relationship of present value and future value PPT 9-1 $1,000 present value $ 10% interest $1,464.10 future value 0 1 2 3 4 Number of periods Figure

Time Value of Money. If you deposit $100 in an account that pays 6% annual interest, what amount will you expect to have in

Time Value of Money Future value Present value Rates of return 1 If you deposit $100 in an account that pays 6% annual interest, what amount will you expect to have in the account at the end of the year.

Time Value of Money Future value Present value Rates of return 1 If you deposit $100 in an account that pays 6% annual interest, what amount will you expect to have in the account at the end of the year.

Chapter 6 Contents. Principles Used in Chapter 6 Principle 1: Money Has a Time Value.

Chapter 6 The Time Value of Money: Annuities and Other Topics Chapter 6 Contents Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate present and future values

Chapter 6 The Time Value of Money: Annuities and Other Topics Chapter 6 Contents Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate present and future values

5. Time value of money

1 Simple interest 2 5. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

1 Simple interest 2 5. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

MHSA 8630 -- Healthcare Financial Management Time Value of Money Analysis

MHSA 8630 -- Healthcare Financial Management Time Value of Money Analysis ** One of the most fundamental tenets of financial management relates to the time value of money. The old adage that a dollar in

MHSA 8630 -- Healthcare Financial Management Time Value of Money Analysis ** One of the most fundamental tenets of financial management relates to the time value of money. The old adage that a dollar in

Future Value. Basic TVM Concepts. Chapter 2 Time Value of Money. $500 cash flow. On a time line for 3 years: $100. FV 15%, 10 yr.

Chapter Time Value of Money Future Value Present Value Annuities Effective Annual Rate Uneven Cash Flows Growing Annuities Loan Amortization Summary and Conclusions Basic TVM Concepts Interest rate: abbreviated

Chapter Time Value of Money Future Value Present Value Annuities Effective Annual Rate Uneven Cash Flows Growing Annuities Loan Amortization Summary and Conclusions Basic TVM Concepts Interest rate: abbreviated

Solutions to Problems: Chapter 5

Solutions to Problems: Chapter 5 P5-1. Using a time line LG 1; Basic a, b, and c d. Financial managers rely more on present value than future value because they typically make decisions before the start

Solutions to Problems: Chapter 5 P5-1. Using a time line LG 1; Basic a, b, and c d. Financial managers rely more on present value than future value because they typically make decisions before the start

The time value of money: Part II

The time value of money: Part II A reading prepared by Pamela Peterson Drake O U T L I E 1. Introduction 2. Annuities 3. Determining the unknown interest rate 4. Determining the number of compounding periods

The time value of money: Part II A reading prepared by Pamela Peterson Drake O U T L I E 1. Introduction 2. Annuities 3. Determining the unknown interest rate 4. Determining the number of compounding periods

3. Time value of money. We will review some tools for discounting cash flows.

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

How To Calculate The Value Of A Project

Chapter 02 How to Calculate Present Values Multiple Choice Questions 1. The present value of $100 expected in two years from today at a discount rate of 6% is: A. $116.64 B. $108.00 C. $100.00 D. $89.00

Chapter 02 How to Calculate Present Values Multiple Choice Questions 1. The present value of $100 expected in two years from today at a discount rate of 6% is: A. $116.64 B. $108.00 C. $100.00 D. $89.00

TIME VALUE OF MONEY (TVM)

") TIME VALUE OF MONEY (TVM) INTEREST Rate of Return When we know the Present Value (amount today), Future Value (amount to which the investment will grow), and Number of Periods, we can calculate the rate

TIME VALUE OF MONEY (TVM) INTEREST Rate of Return When we know the Present Value (amount today), Future Value (amount to which the investment will grow), and Number of Periods, we can calculate the rate

1.3.2015 г. D. Dimov. Year Cash flow 1 $3,000 2 $5,000 3 $4,000 4 $3,000 5 $2,000

D. Dimov Most financial decisions involve costs and benefits that are spread out over time Time value of money allows comparison of cash flows from different periods Question: You have to choose one of

D. Dimov Most financial decisions involve costs and benefits that are spread out over time Time value of money allows comparison of cash flows from different periods Question: You have to choose one of

Chapter 4. Time Value of Money. Copyright 2009 Pearson Prentice Hall. All rights reserved.

Chapter 4 Time Value of Money Learning Goals 1. Discuss the role of time value in finance, the use of computational aids, and the basic patterns of cash flow. 2. Understand the concept of future value

Chapter 4 Time Value of Money Learning Goals 1. Discuss the role of time value in finance, the use of computational aids, and the basic patterns of cash flow. 2. Understand the concept of future value

Chapter 4. Time Value of Money. Learning Goals. Learning Goals (cont.)

") Chapter 4 Time Value of Money Learning Goals 1. Discuss the role of time value in finance, the use of computational aids, and the basic patterns of cash flow. 2. Understand the concept of future value

Chapter 4 Time Value of Money Learning Goals 1. Discuss the role of time value in finance, the use of computational aids, and the basic patterns of cash flow. 2. Understand the concept of future value

Chapter 7 SOLUTIONS TO END-OF-CHAPTER PROBLEMS

Chapter 7 SOLUTIONS TO END-OF-CHAPTER PROBLEMS 7-1 0 1 2 3 4 5 10% PV 10,000 FV 5? FV 5 $10,000(1.10) 5 $10,000(FVIF 10%, 5 ) $10,000(1.6105) $16,105. Alternatively, with a financial calculator enter the

Chapter 7 SOLUTIONS TO END-OF-CHAPTER PROBLEMS 7-1 0 1 2 3 4 5 10% PV 10,000 FV 5? FV 5 $10,000(1.10) 5 $10,000(FVIF 10%, 5 ) $10,000(1.6105) $16,105. Alternatively, with a financial calculator enter the

CHAPTER 4. The Time Value of Money. Chapter Synopsis

CHAPTER 4 The Time Value of Money Chapter Synopsis Many financial problems require the valuation of cash flows occurring at different times. However, money received in the future is worth less than money

CHAPTER 4 The Time Value of Money Chapter Synopsis Many financial problems require the valuation of cash flows occurring at different times. However, money received in the future is worth less than money

CHAPTER 6 DISCOUNTED CASH FLOW VALUATION

CHAPTER 6 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. The four pieces are the present value (PV), the periodic cash flow (C), the discount rate (r), and

CHAPTER 6 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. The four pieces are the present value (PV), the periodic cash flow (C), the discount rate (r), and

Chapter 2 Present Value

Chapter 2 Present Value Road Map Part A Introduction to finance. Financial decisions and financial markets. Present value. Part B Valuation of assets, given discount rates. Part C Determination of risk-adjusted

Chapter 2 Present Value Road Map Part A Introduction to finance. Financial decisions and financial markets. Present value. Part B Valuation of assets, given discount rates. Part C Determination of risk-adjusted

CALCULATOR TUTORIAL. Because most students that use Understanding Healthcare Financial Management will be conducting time

CALCULATOR TUTORIAL INTRODUCTION Because most students that use Understanding Healthcare Financial Management will be conducting time value analyses on spreadsheets, most of the text discussion focuses

CALCULATOR TUTORIAL INTRODUCTION Because most students that use Understanding Healthcare Financial Management will be conducting time value analyses on spreadsheets, most of the text discussion focuses

FIN 3000. Chapter 6. Annuities. Liuren Wu

FIN 3000 Chapter 6 Annuities Liuren Wu Overview 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams Learning objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate

FIN 3000 Chapter 6 Annuities Liuren Wu Overview 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams Learning objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate

Discounted Cash Flow Valuation

BUAD 100x Foundations of Finance Discounted Cash Flow Valuation September 28, 2009 Review Introduction to corporate finance What is corporate finance? What is a corporation? What decision do managers make?

BUAD 100x Foundations of Finance Discounted Cash Flow Valuation September 28, 2009 Review Introduction to corporate finance What is corporate finance? What is a corporation? What decision do managers make?

Topics. Chapter 5. Future Value. Future Value - Compounding. Time Value of Money. 0 r = 5% 1

Chapter 5 Time Value of Money Topics 1. Future Value of a Lump Sum 2. Present Value of a Lump Sum 3. Future Value of Cash Flow Streams 4. Present Value of Cash Flow Streams 5. Perpetuities 6. Uneven Series

Chapter 5 Time Value of Money Topics 1. Future Value of a Lump Sum 2. Present Value of a Lump Sum 3. Future Value of Cash Flow Streams 4. Present Value of Cash Flow Streams 5. Perpetuities 6. Uneven Series

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. Assuming positive cash flows and interest rates, the future value increases and the present value

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. Assuming positive cash flows and interest rates, the future value increases and the present value

Learning Objectives. Learning Objectives. Learning Objectives. Principles Used in this Chapter. Simple Interest. Principle 2:

Learning Objectives Chapter 5 The Time Value of Money Explain the mechanics of compounding, which is how money grows over a time when it is invested. Be able to move money through time using time value

Learning Objectives Chapter 5 The Time Value of Money Explain the mechanics of compounding, which is how money grows over a time when it is invested. Be able to move money through time using time value

Key Concepts and Skills

Chapters 5 and 6 Calculators Time Value of Money and Discounted Cash Flow Valuation McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Key Concepts and Skills Be able

Chapters 5 and 6 Calculators Time Value of Money and Discounted Cash Flow Valuation McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Key Concepts and Skills Be able

Chapter 4. The Time Value of Money

Chapter 4 The Time Value of Money 4-2 Topics Covered Future Values and Compound Interest Present Values Multiple Cash Flows Perpetuities and Annuities Inflation and Time Value Effective Annual Interest

Chapter 4 The Time Value of Money 4-2 Topics Covered Future Values and Compound Interest Present Values Multiple Cash Flows Perpetuities and Annuities Inflation and Time Value Effective Annual Interest

Time Value of Money. Background

Time Value of Money (Text reference: Chapter 4) Topics Background One period case - single cash flow Multi-period case - single cash flow Multi-period case - compounding periods Multi-period case - multiple

Time Value of Money (Text reference: Chapter 4) Topics Background One period case - single cash flow Multi-period case - single cash flow Multi-period case - compounding periods Multi-period case - multiple

UNDERSTANDING HEALTHCARE FINANCIAL MANAGEMENT, 5ed. Time Value Analysis

This is a sample of the instructor resources for Understanding Healthcare Financial Management, Fifth Edition, by Louis Gapenski. This sample contains the chapter models, end-of-chapter problems, and end-of-chapter

This is a sample of the instructor resources for Understanding Healthcare Financial Management, Fifth Edition, by Louis Gapenski. This sample contains the chapter models, end-of-chapter problems, and end-of-chapter

EXAM 2 OVERVIEW. Binay Adhikari

EXAM 2 OVERVIEW Binay Adhikari FEDERAL RESERVE & MARKET ACTIVITY (BS38) Definition 4.1 Discount Rate The discount rate is the periodic percentage return subtracted from the future cash flow for computing

EXAM 2 OVERVIEW Binay Adhikari FEDERAL RESERVE & MARKET ACTIVITY (BS38) Definition 4.1 Discount Rate The discount rate is the periodic percentage return subtracted from the future cash flow for computing

Problem Set: Annuities and Perpetuities (Solutions Below)

") Problem Set: Annuities and Perpetuities (Solutions Below) 1. If you plan to save $300 annually for 10 years and the discount rate is 15%, what is the future value? 2. If you want to buy a boat in 6 years

Problem Set: Annuities and Perpetuities (Solutions Below) 1. If you plan to save $300 annually for 10 years and the discount rate is 15%, what is the future value? 2. If you want to buy a boat in 6 years

PRESENT VALUE ANALYSIS. Time value of money equal dollar amounts have different values at different points in time.

PRESENT VALUE ANALYSIS Time value of money equal dollar amounts have different values at different points in time. Present value analysis tool to convert CFs at different points in time to comparable values

PRESENT VALUE ANALYSIS Time value of money equal dollar amounts have different values at different points in time. Present value analysis tool to convert CFs at different points in time to comparable values

Ordinary Annuities Chapter 10

Ordinary Annuities Chapter 10 Learning Objectives After completing this chapter, you will be able to: > Define and distinguish between ordinary simple annuities and ordinary general annuities. > Calculate

Ordinary Annuities Chapter 10 Learning Objectives After completing this chapter, you will be able to: > Define and distinguish between ordinary simple annuities and ordinary general annuities. > Calculate

Chapter 5 Discounted Cash Flow Valuation

Chapter Discounted Cash Flow Valuation Compounding Periods Other Than Annual Let s examine monthly compounding problems. Future Value Suppose you invest $9,000 today and get an interest rate of 9 percent

Chapter Discounted Cash Flow Valuation Compounding Periods Other Than Annual Let s examine monthly compounding problems. Future Value Suppose you invest $9,000 today and get an interest rate of 9 percent

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY Answers to Concepts Review and Critical Thinking Questions 1. The four parts are the present value (PV), the future value (FV), the discount

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY Answers to Concepts Review and Critical Thinking Questions 1. The four parts are the present value (PV), the future value (FV), the discount

FinQuiz Notes 2 0 1 4

Reading 5 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Reading 5 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Week 4. Chonga Zangpo, DFB

Week 4 Time Value of Money Chonga Zangpo, DFB What is time value of money? It is based on the belief that people have a positive time preference for consumption. It reflects the notion that people prefer

Week 4 Time Value of Money Chonga Zangpo, DFB What is time value of money? It is based on the belief that people have a positive time preference for consumption. It reflects the notion that people prefer

Chapter 4. Time Value of Money

Chapter 4 Time Value of Money Learning Goals 1. Discuss the role of time value in finance, the use of computational aids, and the basic patterns of cash flow. 2. Understand the concept of future value

Chapter 4 Time Value of Money Learning Goals 1. Discuss the role of time value in finance, the use of computational aids, and the basic patterns of cash flow. 2. Understand the concept of future value

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Solutions to Questions and Problems NOTE: All-end-of chapter problems were solved using a spreadsheet. Many problems require multiple steps. Due to space and readability

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Solutions to Questions and Problems NOTE: All-end-of chapter problems were solved using a spreadsheet. Many problems require multiple steps. Due to space and readability

rate nper pmt pv Interest Number of Payment Present Future Rate Periods Amount Value Value 12.00% 1 0 $100.00 $112.00

In Excel language, if the initial cash flow is an inflow (positive), then the future value must be an outflow (negative). Therefore you must add a negative sign before the FV (and PV) function. The inputs

In Excel language, if the initial cash flow is an inflow (positive), then the future value must be an outflow (negative). Therefore you must add a negative sign before the FV (and PV) function. The inputs

Chapter 8. 48 Financial Planning Handbook PDP

Chapter 8 48 Financial Planning Handbook PDP The Financial Planner's Toolkit As a financial planner, you will be doing a lot of mathematical calculations for your clients. Doing these calculations for

Chapter 8 48 Financial Planning Handbook PDP The Financial Planner's Toolkit As a financial planner, you will be doing a lot of mathematical calculations for your clients. Doing these calculations for

Chapter 1: Time Value of Money

1 Chapter 1: Time Value of Money Study Unit 1: Time Value of Money Concepts Basic Concepts Cash Flows A cash flow has 2 components: 1. The receipt or payment of money: This differs from the accounting

1 Chapter 1: Time Value of Money Study Unit 1: Time Value of Money Concepts Basic Concepts Cash Flows A cash flow has 2 components: 1. The receipt or payment of money: This differs from the accounting

NPV calculation. Academic Resource Center

NPV calculation Academic Resource Center 1 NPV calculation PV calculation a. Constant Annuity b. Growth Annuity c. Constant Perpetuity d. Growth Perpetuity NPV calculation a. Cash flow happens at year

NPV calculation Academic Resource Center 1 NPV calculation PV calculation a. Constant Annuity b. Growth Annuity c. Constant Perpetuity d. Growth Perpetuity NPV calculation a. Cash flow happens at year

Hewlett-Packard 10BII Tutorial

This tutorial has been developed to be used in conjunction with Brigham and Houston s Fundamentals of Financial Management 11 th edition and Fundamentals of Financial Management: Concise Edition. In particular,

This tutorial has been developed to be used in conjunction with Brigham and Houston s Fundamentals of Financial Management 11 th edition and Fundamentals of Financial Management: Concise Edition. In particular,

Exercise 1 for Time Value of Money

Exercise 1 for Time Value of Money MULTIPLE CHOICE 1. Which of the following statements is CORRECT? a. A time line is not meaningful unless all cash flows occur annually. b. Time lines are useful for visualizing

Exercise 1 for Time Value of Money MULTIPLE CHOICE 1. Which of the following statements is CORRECT? a. A time line is not meaningful unless all cash flows occur annually. b. Time lines are useful for visualizing

Oklahoma State University Spears School of Business. Time Value of Money

Oklahoma State University Spears School of Business Time Value of Money Slide 2 Time Value of Money Which would you rather receive as a sign-in bonus for your new job? 1. $15,000 cash upon signing the

Oklahoma State University Spears School of Business Time Value of Money Slide 2 Time Value of Money Which would you rather receive as a sign-in bonus for your new job? 1. $15,000 cash upon signing the

Compound Interest Formula

Mathematics of Finance Interest is the rental fee charged by a lender to a business or individual for the use of money. charged is determined by Principle, rate and time Interest Formula I = Prt $100 At

Mathematics of Finance Interest is the rental fee charged by a lender to a business or individual for the use of money. charged is determined by Principle, rate and time Interest Formula I = Prt $100 At

Chapter 3. Understanding The Time Value of Money. Prentice-Hall, Inc. 1

Chapter 3 Understanding The Time Value of Money Prentice-Hall, Inc. 1 Time Value of Money A dollar received today is worth more than a dollar received in the future. The sooner your money can earn interest,

Chapter 3 Understanding The Time Value of Money Prentice-Hall, Inc. 1 Time Value of Money A dollar received today is worth more than a dollar received in the future. The sooner your money can earn interest,

Key Concepts and Skills

McGraw-Hill/Irwin Copyright 2014 by the McGraw-Hill Companies, Inc. All rights reserved. Key Concepts and Skills Be able to compute: The future value of an investment made today The present value of cash

McGraw-Hill/Irwin Copyright 2014 by the McGraw-Hill Companies, Inc. All rights reserved. Key Concepts and Skills Be able to compute: The future value of an investment made today The present value of cash

Chapter 6. Time Value of Money Concepts. Simple Interest 6-1. Interest amount = P i n. Assume you invest $1,000 at 6% simple interest for 3 years.

6-1 Chapter 6 Time Value of Money Concepts 6-2 Time Value of Money Interest is the rent paid for the use of money over time. That s right! A dollar today is more valuable than a dollar to be received in

6-1 Chapter 6 Time Value of Money Concepts 6-2 Time Value of Money Interest is the rent paid for the use of money over time. That s right! A dollar today is more valuable than a dollar to be received in

The Time Value of Money

The following is a review of the Quantitative Methods: Basic Concepts principles designed to address the learning outcome statements set forth by CFA Institute. This topic is also covered in: The Time

The following is a review of the Quantitative Methods: Basic Concepts principles designed to address the learning outcome statements set forth by CFA Institute. This topic is also covered in: The Time

Present Value and Annuities. Chapter 3 Cont d

Present Value and Annuities Chapter 3 Cont d Present Value Helps us answer the question: What s the value in today s dollars of a sum of money to be received in the future? It lets us strip away the effects

Present Value and Annuities Chapter 3 Cont d Present Value Helps us answer the question: What s the value in today s dollars of a sum of money to be received in the future? It lets us strip away the effects

The Time Value of Money

The Time Value of Money Future Value - Amount to which an investment will grow after earning interest. Compound Interest - Interest earned on interest. Simple Interest - Interest earned only on the original

The Time Value of Money Future Value - Amount to which an investment will grow after earning interest. Compound Interest - Interest earned on interest. Simple Interest - Interest earned only on the original

HOW TO CALCULATE PRESENT VALUES

Chapter 2 HOW TO CALCULATE PRESENT VALUES Brealey, Myers, and Allen Principles of Corporate Finance 11 th Global Edition McGraw-Hill Education Copyright 2014 by The McGraw-Hill Companies, Inc. All rights

Chapter 2 HOW TO CALCULATE PRESENT VALUES Brealey, Myers, and Allen Principles of Corporate Finance 11 th Global Edition McGraw-Hill Education Copyright 2014 by The McGraw-Hill Companies, Inc. All rights

Texas Instruments BAII Plus Tutorial for Use with Fundamentals 11/e and Concise 5/e

Texas Instruments BAII Plus Tutorial for Use with Fundamentals 11/e and Concise 5/e This tutorial was developed for use with Brigham and Houston s Fundamentals of Financial Management, 11/e and Concise,

Texas Instruments BAII Plus Tutorial for Use with Fundamentals 11/e and Concise 5/e This tutorial was developed for use with Brigham and Houston s Fundamentals of Financial Management, 11/e and Concise,

FinQuiz Notes 2 0 1 5

Reading 5 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Reading 5 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

FNCE 301, Financial Management H Guy Williams, 2006

Review In the first class we looked at the value today of future payments (introduction), how to value projects and investments. Present Value = Future Payment * 1 Discount Factor. The discount factor

Review In the first class we looked at the value today of future payments (introduction), how to value projects and investments. Present Value = Future Payment * 1 Discount Factor. The discount factor

This is Time Value of Money: Multiple Flows, chapter 7 from the book Finance for Managers (index.html) (v. 0.1).

(v. 0.1).") This is Time Value of Money: Multiple Flows, chapter 7 from the book Finance for Managers (index.html) (v. 0.1). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/

This is Time Value of Money: Multiple Flows, chapter 7 from the book Finance for Managers (index.html) (v. 0.1). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/

Time Value of Money. 15.511 Corporate Accounting Summer 2004. Professor S. P. Kothari Sloan School of Management Massachusetts Institute of Technology

Time Value of Money 15.511 Corporate Accounting Summer 2004 Professor S. P. Kothari Sloan School of Management Massachusetts Institute of Technology July 2, 2004 1 LIABILITIES: Current Liabilities Obligations

Time Value of Money 15.511 Corporate Accounting Summer 2004 Professor S. P. Kothari Sloan School of Management Massachusetts Institute of Technology July 2, 2004 1 LIABILITIES: Current Liabilities Obligations

Lease Analysis Tools

Lease Analysis Tools 2009 ELFA Lease Accountants Conference Presenter: Bill Bosco, Pres. [email protected] Leasing 101 914-522-3233 Overview Math of Finance Theory Glossary of terms Common calculations

Lease Analysis Tools 2009 ELFA Lease Accountants Conference Presenter: Bill Bosco, Pres. [email protected] Leasing 101 914-522-3233 Overview Math of Finance Theory Glossary of terms Common calculations

Financial Markets and Valuation - Tutorial 1: SOLUTIONS. Present and Future Values, Annuities and Perpetuities

Financial Markets and Valuation - Tutorial 1: SOLUTIONS Present and Future Values, Annuities and Perpetuities (*) denotes those problems to be covered in detail during the tutorial session (*) Problem

Financial Markets and Valuation - Tutorial 1: SOLUTIONS Present and Future Values, Annuities and Perpetuities (*) denotes those problems to be covered in detail during the tutorial session (*) Problem

Solutions to Problems

Solutions to Problems P4-1. LG 1: Using a time line Basic a. b. and c. d. Financial managers rely more on present value than future value because they typically make decisions before the start of a project,

Solutions to Problems P4-1. LG 1: Using a time line Basic a. b. and c. d. Financial managers rely more on present value than future value because they typically make decisions before the start of a project,

Chapter 3 Present Value

Chapter 3 Present Value MULTIPLE CHOICE 1. Which of the following cannot be calculated? a. Present value of an annuity. b. Future value of an annuity. c. Present value of a perpetuity. d. Future value

Chapter 3 Present Value MULTIPLE CHOICE 1. Which of the following cannot be calculated? a. Present value of an annuity. b. Future value of an annuity. c. Present value of a perpetuity. d. Future value

Financial Management Spring 2012

3-1 Financial Management Spring 2012 Week 4 How to Calculate Present Values III 4-1 3-2 Topics Covered More Shortcuts Growing Perpetuities and Annuities How Interest Is Paid and Quoted 4-2 Example 3-3

3-1 Financial Management Spring 2012 Week 4 How to Calculate Present Values III 4-1 3-2 Topics Covered More Shortcuts Growing Perpetuities and Annuities How Interest Is Paid and Quoted 4-2 Example 3-3

Exercise 6 8. Exercise 6 12 PVA = $5,000 x 4.35526* = $21,776

CHAPTER 6: EXERCISES Exercise 6 2 1. FV = $10,000 (2.65330 * ) = $26,533 * Future value of $1: n = 20, i = 5% (from Table 1) 2. FV = $10,000 (1.80611 * ) = $18,061 * Future value of $1: n = 20, i = 3%

CHAPTER 6: EXERCISES Exercise 6 2 1. FV = $10,000 (2.65330 * ) = $26,533 * Future value of $1: n = 20, i = 5% (from Table 1) 2. FV = $10,000 (1.80611 * ) = $18,061 * Future value of $1: n = 20, i = 3%

first complete "prior knowlegde" -- to refresh knowledge of Simple and Compound Interest.

ORDINARY SIMPLE ANNUITIES first complete "prior knowlegde" -- to refresh knowledge of Simple and Compound Interest. LESSON OBJECTIVES: students will learn how to determine the Accumulated Value of Regular

ORDINARY SIMPLE ANNUITIES first complete "prior knowlegde" -- to refresh knowledge of Simple and Compound Interest. LESSON OBJECTIVES: students will learn how to determine the Accumulated Value of Regular

Calculator (Hewlett-Packard 10BII) Tutorial

Tutorial") UNDERSTANDING HEALTHCARE FINANCIAL MANAGEMENT Calculator (Hewlett-Packard 10BII) Tutorial To begin, look at the face of the calculator. Most keys (except a few) have two functions: Each key s primary function

UNDERSTANDING HEALTHCARE FINANCIAL MANAGEMENT Calculator (Hewlett-Packard 10BII) Tutorial To begin, look at the face of the calculator. Most keys (except a few) have two functions: Each key s primary function

How To Value Cash Flow

Lecture: II 1 Time Value of Money (TVM) A dollar today is more valuable than a dollar sometime in the future...! The intuitive basis for present value what determines the effect of timing on the value

Lecture: II 1 Time Value of Money (TVM) A dollar today is more valuable than a dollar sometime in the future...! The intuitive basis for present value what determines the effect of timing on the value

Appendix C- 1. Time Value of Money. Appendix C- 2. Financial Accounting, Fifth Edition

C- 1 Time Value of Money C- 2 Financial Accounting, Fifth Edition Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount. 3. Solve for future

C- 1 Time Value of Money C- 2 Financial Accounting, Fifth Edition Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount. 3. Solve for future

Time Value of Money (TVM)

") BUSI Financial Management Time Value of Money 1 Time Value of Money (TVM) Present value and future value how much is $1 now worth in the future? how much is $1 in the future worth now? Business planning

BUSI Financial Management Time Value of Money 1 Time Value of Money (TVM) Present value and future value how much is $1 now worth in the future? how much is $1 in the future worth now? Business planning

Click Here to Buy the Tutorial

FIN 534 Week 4 Quiz 3 (Str) Click Here to Buy the Tutorial http://www.tutorialoutlet.com/fin-534/fin-534-week-4-quiz-3- str/ For more course tutorials visit www.tutorialoutlet.com Which of the following

FIN 534 Week 4 Quiz 3 (Str) Click Here to Buy the Tutorial http://www.tutorialoutlet.com/fin-534/fin-534-week-4-quiz-3- str/ For more course tutorials visit www.tutorialoutlet.com Which of the following

Financial Math on Spreadsheet and Calculator Version 4.0

Financial Math on Spreadsheet and Calculator Version 4.0 2002 Kent L. Womack and Andrew Brownell Tuck School of Business Dartmouth College Table of Contents INTRODUCTION...1 PERFORMING TVM CALCULATIONS

Financial Math on Spreadsheet and Calculator Version 4.0 2002 Kent L. Womack and Andrew Brownell Tuck School of Business Dartmouth College Table of Contents INTRODUCTION...1 PERFORMING TVM CALCULATIONS

HP 12C Calculations. 2. If you are given the following set of cash flows and discount rates, can you calculate the PV? (pg.

HP 12C Calculations This handout has examples for calculations on the HP12C: 1. Present Value (PV) 2. Present Value with cash flows and discount rate constant over time 3. Present Value with uneven cash

HP 12C Calculations This handout has examples for calculations on the HP12C: 1. Present Value (PV) 2. Present Value with cash flows and discount rate constant over time 3. Present Value with uneven cash

REVIEW MATERIALS FOR REAL ESTATE ANALYSIS

REVIEW MATERIALS FOR REAL ESTATE ANALYSIS 1997, Roy T. Black REAE 5311, Fall 2005 University of Texas at Arlington J. Andrew Hansz, Ph.D., CFA CONTENTS ITEM ANNUAL COMPOUND INTEREST TABLES AT 10% MATERIALS

REVIEW MATERIALS FOR REAL ESTATE ANALYSIS 1997, Roy T. Black REAE 5311, Fall 2005 University of Texas at Arlington J. Andrew Hansz, Ph.D., CFA CONTENTS ITEM ANNUAL COMPOUND INTEREST TABLES AT 10% MATERIALS

Time Value of Money Concepts

BASIC ANNUITIES There are many accounting transactions that require the payment of a specific amount each period. A payment for a auto loan or a mortgage payment are examples of this type of transaction.

BASIC ANNUITIES There are many accounting transactions that require the payment of a specific amount each period. A payment for a auto loan or a mortgage payment are examples of this type of transaction.