INVESTMENT OBJECTIVES AND VISION

|

|

|

- Hector Hancock

- 10 years ago

- Views:

Transcription

Investment Objectives: The investment objectives of the Company are to maximize the risk adjusted returns and ensure reasonable liquidity at all times.")

1 Monthly Investment Update: Volume 6, Issue 4 July, 2013 UNIT LINKED PRODUCTS FROM SBI LIFE INSURANCE CO. LTD INVESTMENT OBJECTIVES AND VISION (A) Investment Objectives: The investment objectives of the Company are to maximize the risk adjusted returns and ensure reasonable liquidity at all times. Management of the investment portfolio is a crucial function as investment risk and returns, inter alia, determine the ability of the Company to competitively price its products, ensure solvency at all times and earn the expected profitability. The investment policy outlined in this document seeks to set the direction and philosophy for the Company s investment operations. The Policy outlined below conforms to the IRDA Investment Regulations and the Insurance Act. The Policy covers investment parameters, exposure norms and other relevant factors that will assist in taking prudent investment decisions. The Policy framework also takes into account asset liability management, market risks, portfolio duration, liquidity considerations, and credit risk. To summarize the investment policy aims to achieve the following Investment Objectives: a) To acquire and maintain quality assets that will meet the liabilities accepted by the Company; b) To be able to meet the reasonable expectations of the policyholders taking into account the safety of their funds with optimum Return; c) To adhere to all Regulatory provisions; d) To conduct all the related activities in a cost effective and efficient manner; and e) To achieve performance in line with benchmarks identified for the different investment portfolios. The Company has also defined the Investment Objectives for each Fund separately, on the basis of aforesaid broader Investment objectives. (B) Investment Vision: To invest the funds on the prudent principles of Safety, Liquidity & Returns, with an overall vision of meeting reasonable expectations of policy holders. Source: SBI Life Investment Policy 1

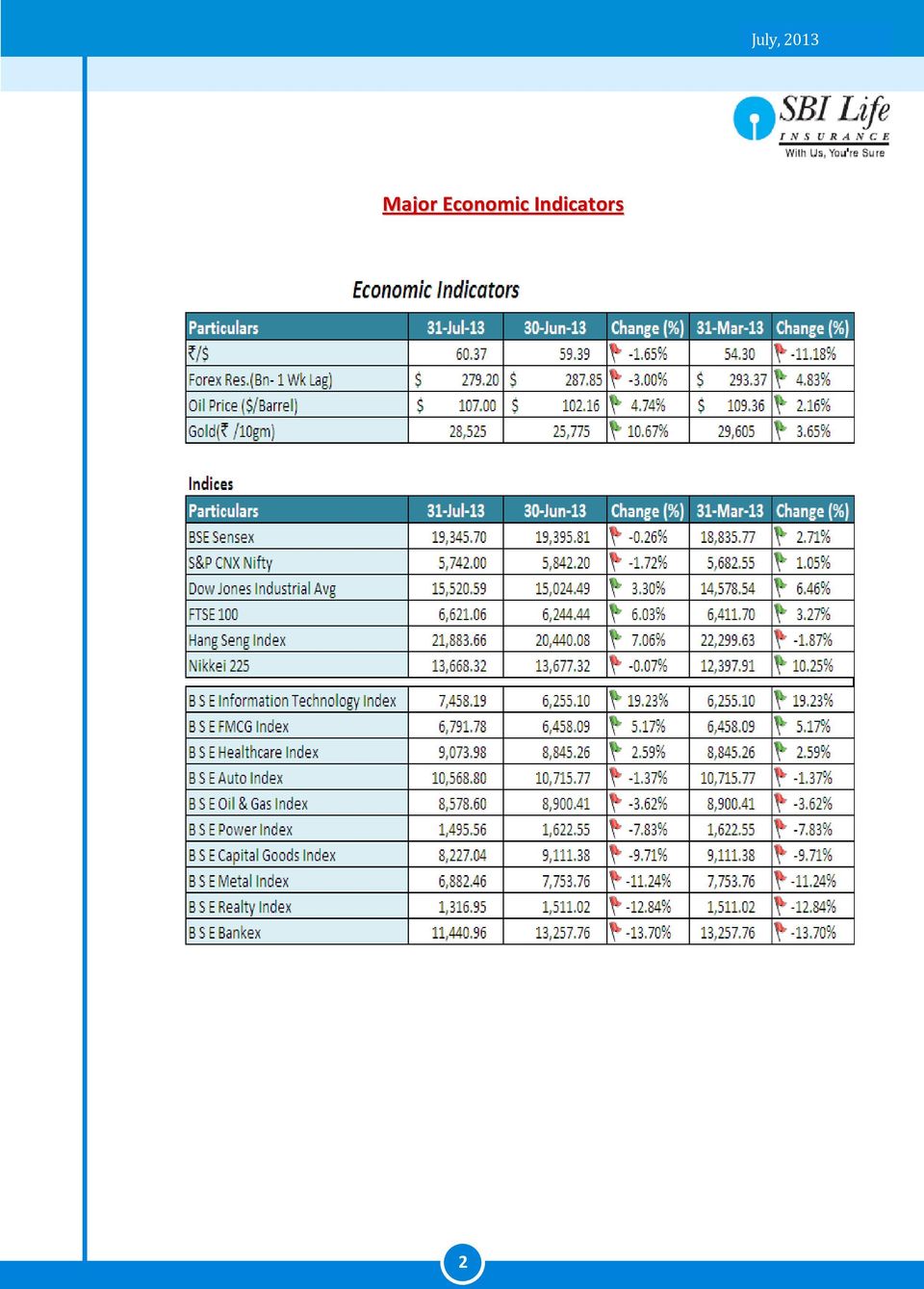

2 Major Economic Indicators 2

3 * w e f May 03, 2013 # w e f Feb 09, 2013 Data Sources NSE BSE RBI FIMMDA Bloomberg & Reuters 3

4 DEBT MARKET REVIEW AND OUTLOOK MARKET REVIEW The benchmark 10 yr. Gsec yields hardened an outrageous 75 basis points in July and all of it coming overnight on 16 th July after the RBI announced first set of liquidity tightening measures to curb speculation and volatility in INR currency. These measures were as a result of record depreciation of INR from ` 56 to `. 60 against Dollar in just one month. The summary of measures is as under: The RBI on 15 th July had announced following unconventional measures 1. Hiked marginal standing facility (MSF) rate by 200 bps to 10.25%. This is the penalty rate at which banks can borrow over Repo rate (7.25%) 2. Restricted borrowing under LAF to 1 percent of NDTL or approx INR 75,000 crores. 3. Conducted OMO sale to draw out excess INR liquidity. On 23rd July RBI introduced additional measures to arrest INR volatility 1. Restricted borrowing under LAF to 0.5 % percent of NDTL per bank from the earlier 1% limit on the overall system. 2. Require banks to maintain 99% of the CRR requirement on a daily basis with the RBI against the existing 70% 3. Conduct 6000 crores of Cash management bills These measures, intended to reduce the rupee volatility, not only pushed the short end yields but also longer tenor yields. The Quarterly Monetary policy statement announced on 30 th July re-iterated the risk emanating from the global development and the weakening of the CAD (Current Account Deficit). While the report acknowledged moderating inflation and reduced growth, it stressed on the stable macroeconomic environment as a prerequisite condition to bring back growth in a sustained manner. Markets expected RBI to hint that the measures announced to be temporary but RBI chose not to give any time lines for reversal and made it dependent on future data. It also ruled out the possibility of rate hike, but warned of all possible arsenals to be used in future to reign in the rupee volatility. Key rate movements are as under: Instrument Jul '13 Jun '13 Mar '13 Mar '12 Change MOM Change (YTD) 10 Yr Gsec 8.33% 7.61% 7.95% 8.57% 0.72% 0.38% 30 Yr Gsec 8.74% 7.86% 8.17% 8.74% 0.88% 0.57% 3 Yr AAA Bond 10.00% 8.60% 8.80% 9.60% 1.40% 1.20% 5 Yr AAA Bond 9.75% 8.65% 8.85% 9.50% 1.10% 0.90% 10 Yr AAA Bond 9.45% 8.56% 8.85% 9.45% 0.89% 0.60% 364 Days T-bill 10.46% 7.46% 7.80% 8.48% 3.00% 2.66% 91 Days T-bill 11.26% 7.48% 8.10% 9.02% 3.78% 3.16% 1 Yr Certificate of Deposit 9.85% 8.30% 9.25% 10.35% 1.55% 0.60% Credit spreads Crude $/barrel (Source: Bloomberg, Reuters & RBI) 4

rate by 200 bps to 10.25%.")

5 Macro Indicators The IIP saw a drop of 1.6% in May 2013 vs. the revised 1.9% in April The mfg sector showed a decline after few months of positive movement. The mining sectored continued in red. The electricity generation saw a growth of 6.2%. Within the use based classification Capital goods saw a decline of 2.7%. The biggest drop being in the consumer durables contributed by the drop in motor vehicles segment (-6.2%). Industry Classification May-13 Apr-13 Use Based Classification May-13 Apr-13 Mining Basic Goods (45.7) Manufacturing Capital Goods (8.8) Electricity Intermediate (15.69) IIP Consumer (29.81) of which Durables (8.46) Non Durables 21.35) WPI for June 2013 came lower at 4.86% (May WPI 4.7%) and the core inflation dropped to 2.10% y-o-y. The food inflation increased from the previous month, the mfg inflation dropped on back of low demand) and the fuel inflation remained flat. The June CPI came in at 9.9% vs 9.2% in May The CPI was higher because of the food inflation which was up 10.84% The trade deficit narrowed in June 2013 to $12.2 bn compared to $20.1 bn in May The reduction of trade deficit was on back of lower gold and oil buying. At the aggregate level the exports contracted by 4.5% and imports narrowed by 0.4%. The Gold imports were down to 30 tonnes from 160 tonnes in May Global News: The world Economy is in balance as far as growth is concerned. The developed market has shown growth in the second quarter while the emerging economies, largely China, have show signs of growth slowing down. The US has led the way in terms of the annualized Q2 GDP growth coming in at 1.6% vs the expected 1%. Though the consumer confidence index has not fared well but there is definite drop in the unemployment rate. This would also mean that the anticipated tapering of the QE3 is on course in September. The ECB left its policy rate unchanged at 0.50% and the ECB President has re-assured the market that the monetary policy will remain accommodative till warranted. The Euro-Zone consumer confidence surveys are encouraging. After a long time, since Apr 2011, the unemployment rate fell down in Jul 2013 though in percent terms it remained high at 12.1% 5

-0.4 1.3 Manufacturing -2 2.8 Capital Goods (8.8) -2.7 1 Electricity 6.2 0.8 Intermediate (15.69) 1.5 2.4 IIP -1.6 2 Consumer (29.81) -4 2.8 of which Durables (8.46) -10.4-8.")

6 DEBT OUTLOOK The RBI Governor in his post policy conference stated that India is currently facing the impossible trinity. While we are in midst of falling growth, lower inflation trajectory and we need to reduce rates but the pace of currency depreciation requires immediate attention. The immediate reason for currency depreciation can be attributed to rise in yields in US and expected tapering of US stimulus; however the weakness is likely to prevail due to weak domestic macro factors and high Current account Deficit (CAD). In the past India was able to fund its huge Current account deficit via record FII flows and FDI however with weak global growth and deteriorating macro fundamentals, funding a high CAD on a sustainable basis is becoming increasingly difficult. Due to this dilemma arising from weak growth and benign core inflation on one hand and depreciating currency on other hand the signaling of rate hike has not come through the conventional Repo rate or CRR, but RBI has resorted to keep the cost of liquidity high and thereby caused interest rates to rise indirectly. Given the scenario and the limited options available with the government to bring in more foreign currency in short term, we do not expect RBI to reduce short term rates in hurry. Post the measures announced on 15 th July Rupee has not appreciated and we expect some more measures coming from RBI if the current sets of measures don t bring the desired effect. Having said that both RBI and the finance ministry are also aware of the ill effect of higher rates on already weak growth and hence we expect some measures to bring in foreign currency by way of ECB flows, INR sovereign bond issue etc which will be announced soon. Yield have gone up by 75 basis points in one month and this provides opportunity for investors with longer horizon to invest or stay invested in bond markets to take advantage of current higher yields and participate in capital gains once the rates fall. EQUITY OUTLOOK Sensex showed resilience against bout s of bad news to finally fall during the month. Reserve Bank of India announced a slew of measures to curb rupee volatility. Federal Reserve Chairman Mr. Ben Bernenke announced tapering off for the quantitative easing program that started aftermath the financial crisis. Rupee depreciated sharply. Sensex gave off 0.26% during the month to end at 19,396. It underperformed most of developed market indices like the Dow Jones (up 3.9%) & the FTSE 100 (up 6.5%). There was a clear delinking here. Within the index itself, we see clear difference between stocks that performed and the one that did not. Stocks that withstood the fall in indices are a very few. Government tried its best to defend the fall in rupee. Reserve Bank of India tightened the noose. Overnight rates went up 200 basis. Amount to be borrowed on overnight basis was cut to 0.5% of the Net Demand and Time Liabilities for the banks. Cash reserve ratio maintenance was restricted to daily basis instead of on a reported day. As a result we see inverted yield curve. This would result in increase in cost of borrowing on short term substantially. President cleared the Food Security Bill that gives legal right for 67% of the population for subsidized grains every month. In the process of garnering forex reserves government relaxed the FDI norms for 12 sectors including the telecom and the insurance. 6

.")

7 RBI also took further steps to curb gold imports with CAD in mind, in addition to rupee. It restricted gold imports to entities that would export 1/5th and imports to be made available only for making jewelry. Rupee though fell 1.6% during the month. Data that came out during the month in terms of manufacturing PMI (for the month of June at 50.1%), exports (fall at 4.6% for the month of june on YoY basis), Index of Industrial production (negative 1.6% for the month of May, yoy) and core sector growth (0.1% for the month of june) indicates complete collapse of demand across the sectors. Many institutional houses have downgraded their forecast GDP growth on the back of measures that RBI had taken. Even though the monsoons have been good, we clearly see growth slowing. With increased cost of borrowing and lack of confidence in corporate India to set up new projects that is eminent in loan growth by the banking system, we turn negative on the markets and expect them to correct in the coming month. Results and the forecast / outlook given by managements supports our arguments for being negative. Disclaimer: 1) This newsletter only gives an overview of economy and should not be construed as financial advice 2) SBI Life Insurance Co. Ltd however makes no warranties, representations, promises or statements that information contained herein are correct and accurate. Please consult your Advisor/Consultant before making the investment decision 7

, Index of Industrial production (negative 1.6% for the month of May, yoy) and core sector growth (0.")

Debt Market Outlook - 2015

Debt Market Outlook - 2015 DEBT MARKET PERFORMANCE IN 2014 The Indian bond market saw a sharp rally in H2 of CY 14, inspite of absence of rate cuts. The bond market rallied due to the following factors.

Debt Market Outlook - 2015 DEBT MARKET PERFORMANCE IN 2014 The Indian bond market saw a sharp rally in H2 of CY 14, inspite of absence of rate cuts. The bond market rallied due to the following factors.

MACROECONOMIC OVERVIEW

MACROECONOMIC OVERVIEW MAY 20 Koç Holding CONTENTS Global Economy... 3 Global Financial Markets... 3 Global Economic Growth Forecasts... 3 Turkey Macroeconomic Indicators... Economic Growth... Industrial

MACROECONOMIC OVERVIEW MAY 20 Koç Holding CONTENTS Global Economy... 3 Global Financial Markets... 3 Global Economic Growth Forecasts... 3 Turkey Macroeconomic Indicators... Economic Growth... Industrial

How To Understand The Turkish Economy

BRSA Bank Only Macro Outlook Q1 GDP growth at 3.2%, mostly backed by net exports. Budget deficit was TRY 6.7 billion in H1 12, one third of Latest GDP figure is supportive of the soft landing the government

BRSA Bank Only Macro Outlook Q1 GDP growth at 3.2%, mostly backed by net exports. Budget deficit was TRY 6.7 billion in H1 12, one third of Latest GDP figure is supportive of the soft landing the government

Public Debt Management

Public Debt Management quarterly report Apr-Jun 2010 Government of India Ministry of finance Department of economic affairs September 2010 www.finmin.nic.in CONTENTS Section Page No. Introduction 1 1 Macroeconomic

Public Debt Management quarterly report Apr-Jun 2010 Government of India Ministry of finance Department of economic affairs September 2010 www.finmin.nic.in CONTENTS Section Page No. Introduction 1 1 Macroeconomic

Bond Market Insights October 10, 2014

Bond Market Insights October 10, 2014 by John Simms, CFA and Jerry Wiesner, CFA General Bond Market Treasury yields rose in September as prices fell. Yields in the belly of the curve (5- to 7-year maturities)

Bond Market Insights October 10, 2014 by John Simms, CFA and Jerry Wiesner, CFA General Bond Market Treasury yields rose in September as prices fell. Yields in the belly of the curve (5- to 7-year maturities)

Bond Market Momentum, Valuation and Risks

Bond Market Momentum, Valuation and Risks New Zealand Fixed Income Monthly Commentary August 1 [email protected] + 89 Global bond yields stabilised in July, as markets weighed up two opposing

Bond Market Momentum, Valuation and Risks New Zealand Fixed Income Monthly Commentary August 1 [email protected] + 89 Global bond yields stabilised in July, as markets weighed up two opposing

ISBANK EARNINGS PRESENTATION 2016 Q1

ISBANK EARNINGS PRESENTATION 2016 Q1 2016 Q1 Recent Developments in the Economy Binler Global Outlook Main Indicators of Turkey US EA Moderate expansion in the US economy Solid labor market data Still

ISBANK EARNINGS PRESENTATION 2016 Q1 2016 Q1 Recent Developments in the Economy Binler Global Outlook Main Indicators of Turkey US EA Moderate expansion in the US economy Solid labor market data Still

Taking stock of China s external debt: low indebtedness, but rapid growth is a concern

1991 1993 1995 1997 1999 21 23 25 27 29 211 213 1991 1992 1993 1994 1995 1996 1997 1998 1999 2 21 22 23 24 25 26 27 28 29 21 211 212 213 ECONOMIC ANALYSIS Taking stock of China s external debt: low indebtedness,

1991 1993 1995 1997 1999 21 23 25 27 29 211 213 1991 1992 1993 1994 1995 1996 1997 1998 1999 2 21 22 23 24 25 26 27 28 29 21 211 212 213 ECONOMIC ANALYSIS Taking stock of China s external debt: low indebtedness,

TREASURY MANAGEMENT UPDATE QUARTER 4 2014/15

Committee and Date Cabinet 10 June 2015 12.30 pm Item 9 Public TREASURY MANAGEMENT UPDATE QUARTER 4 2014/15 Responsible Officer James Walton e-mail: [email protected] Tel: (01743) 255011 1.

Committee and Date Cabinet 10 June 2015 12.30 pm Item 9 Public TREASURY MANAGEMENT UPDATE QUARTER 4 2014/15 Responsible Officer James Walton e-mail: [email protected] Tel: (01743) 255011 1.

Crude oil surges & global bond sell off dominate the market

Crude oil surges & global bond sell off dominate the market April witnessed resurgence in crude oil prices, which soared by as much as 13% driven by factors such as fluctuating Libyan oil production and

Crude oil surges & global bond sell off dominate the market April witnessed resurgence in crude oil prices, which soared by as much as 13% driven by factors such as fluctuating Libyan oil production and

A Checklist for a Bond Market Sell-off

A Checklist for a Bond Market Sell-off New Zealand Fixed Income Monthly Commentary February 2013 [email protected] +64 4 460 8309 Just like 2011 and 2012, the start of a new year has again prompted

A Checklist for a Bond Market Sell-off New Zealand Fixed Income Monthly Commentary February 2013 [email protected] +64 4 460 8309 Just like 2011 and 2012, the start of a new year has again prompted

Taurus Ultra Short Term Bond Fund Outlook & Strategy Dec 2015

1 Taurus Ultra Short Term Bond Fund Outlook & Strategy Dec 2015 2 Taurus Ultra Short Term Bond Fund 3 Product Labeling Name Of Scheme Taurus Ultra Short Term Bond Fund An open end debt scheme. This Product

1 Taurus Ultra Short Term Bond Fund Outlook & Strategy Dec 2015 2 Taurus Ultra Short Term Bond Fund 3 Product Labeling Name Of Scheme Taurus Ultra Short Term Bond Fund An open end debt scheme. This Product

Economic Data. November 06, 2015. November 05, 2015

Economic Data November 05, 2015 Country Economic Data Actual Expected Previous JPY BOJ Minutes for Oct. 6-7 Meeting CHF SECO Consumer Confidence Oct -18-19 EUR German Factory Orders M/M Sep -1.70% 1.00%

Economic Data November 05, 2015 Country Economic Data Actual Expected Previous JPY BOJ Minutes for Oct. 6-7 Meeting CHF SECO Consumer Confidence Oct -18-19 EUR German Factory Orders M/M Sep -1.70% 1.00%

Financing government s borrowing requirement

7 Financing government s borrowing requirement In brief Government s net borrowing requirement is expected to be R173.1 billion in 2015/16, decreasing to R155.5 billion in 2017/18. South Africa s deep

7 Financing government s borrowing requirement In brief Government s net borrowing requirement is expected to be R173.1 billion in 2015/16, decreasing to R155.5 billion in 2017/18. South Africa s deep

NORTHERN TRUST ACTIVE FIXED INCOME QUARTERLY UPDATE. Core/Core Plus Investment Strategy

NORTHERN TRUST ACTIVE FIXED INCOME QUARTERLY UPDATE Core/Core Plus Investment Strategy SUMMARY: The Northern Fixed Income Fund (NOFIX)*and Northern Core Bond Fund (NOCBX)** both received four-star overall

NORTHERN TRUST ACTIVE FIXED INCOME QUARTERLY UPDATE Core/Core Plus Investment Strategy SUMMARY: The Northern Fixed Income Fund (NOFIX)*and Northern Core Bond Fund (NOCBX)** both received four-star overall

Understanding Fixed Income

Understanding Fixed Income 2014 AMP Capital Investors Limited ABN 59 001 777 591 AFSL 232497 Understanding Fixed Income About fixed income at AMP Capital Our global presence helps us deliver outstanding

Understanding Fixed Income 2014 AMP Capital Investors Limited ABN 59 001 777 591 AFSL 232497 Understanding Fixed Income About fixed income at AMP Capital Our global presence helps us deliver outstanding

Report to the public on the Bank of Israel s discussions prior to deciding on. the interest rate for January 2015

BANK OF ISRAEL Office of the Spokesperson and Economic Information January 12, 2015 Report to the public on the Bank of Israel s discussions prior to deciding on General the interest rate for January 2015

BANK OF ISRAEL Office of the Spokesperson and Economic Information January 12, 2015 Report to the public on the Bank of Israel s discussions prior to deciding on General the interest rate for January 2015

Monthly Economic Dashboard

RETIREMENT INSTITUTE SM Economic perspective Monthly Economic Dashboard Modest acceleration in economic growth appears in store for 2016 as the inventory-caused soft patch ends, while monetary policy moves

RETIREMENT INSTITUTE SM Economic perspective Monthly Economic Dashboard Modest acceleration in economic growth appears in store for 2016 as the inventory-caused soft patch ends, while monetary policy moves

Nivesh Daily Currency

Nivesh Daily Currency February 3, 2016 Currency Pivot Levels Currency % OI % Prev OI Close Pair Change Change %Change R * Pivot S* USDINR 68.27 0.20 6.75-3.2 68.3550 68.2025 68.1175 EURINR 74.50 0.67 20.16-10.6

Nivesh Daily Currency February 3, 2016 Currency Pivot Levels Currency % OI % Prev OI Close Pair Change Change %Change R * Pivot S* USDINR 68.27 0.20 6.75-3.2 68.3550 68.2025 68.1175 EURINR 74.50 0.67 20.16-10.6

Monetary Policy Matters

Monetary Policy Matters February 26, 2015 by Mark Mobius of Franklin Templeton Investments This year we expect the divergence in monetary policy among the world s central banks to be a key theme and a

Monetary Policy Matters February 26, 2015 by Mark Mobius of Franklin Templeton Investments This year we expect the divergence in monetary policy among the world s central banks to be a key theme and a

P A R A G O N CAPITAL MANAGEMENT

Bond Market Overview July 2013 Bonds declined in value last quarter as interest rates rose by the most in over two years. The increase was a function of economic surprises, Federal Reserve policy confusion,

Bond Market Overview July 2013 Bonds declined in value last quarter as interest rates rose by the most in over two years. The increase was a function of economic surprises, Federal Reserve policy confusion,

The Macroeconomic Situation and Monetary Policy in Russia. Ladies and Gentlemen,

The Money and Banking Conference Monetary Policy under Uncertainty Dr. Sergey Ignatiev Chairman of the Bank of Russia (The 4 th of June 2007, Central Bank of Argentina, Buenos Aires) The Macroeconomic

The Money and Banking Conference Monetary Policy under Uncertainty Dr. Sergey Ignatiev Chairman of the Bank of Russia (The 4 th of June 2007, Central Bank of Argentina, Buenos Aires) The Macroeconomic

Chris Galbraith Vocabulary Terms:

Chris Galbraith Vocabulary Terms: Basis Points (abbreviated bps and the jargon word is pronounced bipps ) 1/100 th of a percent. For example, 1.02% can be expressed as 102 bps. To give a sense, a 5 bps

Chris Galbraith Vocabulary Terms: Basis Points (abbreviated bps and the jargon word is pronounced bipps ) 1/100 th of a percent. For example, 1.02% can be expressed as 102 bps. To give a sense, a 5 bps

High interest rates have contributed to a stronger currency

Financial markets and Central Bank measures: 1 High interest rates have contributed to a stronger currency The króna has appreciated after the extension of the exchange rate band and the Central Bank s

Financial markets and Central Bank measures: 1 High interest rates have contributed to a stronger currency The króna has appreciated after the extension of the exchange rate band and the Central Bank s

EAST AYRSHIRE COUNCIL CABINET 21 OCTOBER 2009 TREASURY MANAGEMENT ANNUAL REPORT FOR 2008/2009 AND UPDATE ON 2009/10 STRATEGY

EAST AYRSHIRE COUNCIL CABINET 21 OCTOBER 2009 TREASURY MANAGEMENT ANNUAL REPORT FOR 2008/2009 AND UPDATE ON 2009/10 STRATEGY Report by Executive Head of Finance and Asset Management 1 PURPOSE OF REPORT

EAST AYRSHIRE COUNCIL CABINET 21 OCTOBER 2009 TREASURY MANAGEMENT ANNUAL REPORT FOR 2008/2009 AND UPDATE ON 2009/10 STRATEGY Report by Executive Head of Finance and Asset Management 1 PURPOSE OF REPORT

MBA Forecast Commentary Joel Kan, [email protected]

Jun 20, 2014 MBA Forecast Commentary Joel Kan, [email protected] Improving Job Market, Weak Housing Market, Lower Mortgage Originations MBA Economic and Mortgage Finance Commentary: June 2014 Key highlights

Jun 20, 2014 MBA Forecast Commentary Joel Kan, [email protected] Improving Job Market, Weak Housing Market, Lower Mortgage Originations MBA Economic and Mortgage Finance Commentary: June 2014 Key highlights

LifePath Index 2060 Fund Q

Release Date: 9-3-215 LifePath Index 26 Fund Q Standard & Poor's 5 Index LifePath Index 26 Custom Target Date 251+... Allocation of Stocks and Bonds 1 8 6 4 2 45 4 35 3 25 2 15 1 5 Years Until Retirement

Release Date: 9-3-215 LifePath Index 26 Fund Q Standard & Poor's 5 Index LifePath Index 26 Custom Target Date 251+... Allocation of Stocks and Bonds 1 8 6 4 2 45 4 35 3 25 2 15 1 5 Years Until Retirement

EIOPA Risk Dashboard March 2015 Q4 2014 data PUBLIC. EIOPA-FS-15/209 Frankfurt, 20th March 2015

EIOPA Risk Dashboard March 2015 Q4 2014 data PUBLIC EIOPA-FS-15/209 Frankfurt, 20th March 2015 Summary The release of this EIOPA Risk Dashboard is based on 2014- Q4 indicators submitted on a best effort

EIOPA Risk Dashboard March 2015 Q4 2014 data PUBLIC EIOPA-FS-15/209 Frankfurt, 20th March 2015 Summary The release of this EIOPA Risk Dashboard is based on 2014- Q4 indicators submitted on a best effort

Euro Zone s Economic Outlook and What it Means for the United States

WELCOME TO THE WEBINAR WEBINAR LINK: HTTP://FRBATL.ADOBECONNECT.COM/ECONOMY/ DIAL-IN NUMBER (MUST USE FOR AUDIO): 855-377-2663 ACCESS CODE: 71032685 Euro Zone s Economic Outlook and What it Means for the

WELCOME TO THE WEBINAR WEBINAR LINK: HTTP://FRBATL.ADOBECONNECT.COM/ECONOMY/ DIAL-IN NUMBER (MUST USE FOR AUDIO): 855-377-2663 ACCESS CODE: 71032685 Euro Zone s Economic Outlook and What it Means for the

Reliance Dual Advantage Fixed Tenure Fund I Plan K (A Close Ended Income Scheme) NFO Opens: 10 th May, 2011 NFO Closes: 24 th May, 2011

NFO Opens: 10 th May, 2011 NFO Closes: 24 th May, 2011") Reliance Dual Advantage Fixed Tenure Fund I Plan K (A Close Ended Income Scheme) NFO Opens: 10 th May, 2011 NFO Closes: 24 th May, 2011 MARKETS & ECONOMY Highlights of the RBI s Monetary Policy Statement

Reliance Dual Advantage Fixed Tenure Fund I Plan K (A Close Ended Income Scheme) NFO Opens: 10 th May, 2011 NFO Closes: 24 th May, 2011 MARKETS & ECONOMY Highlights of the RBI s Monetary Policy Statement

Floating rate Payments 6m Libor. Fixed rate payments 1 300000 337500-37500 2 300000 337500-37500 3 300000 337500-37500 4 300000 325000-25000

Introduction: Interest rate swaps are used to hedge interest rate risks as well as to take on interest rate risks. If a treasurer is of the view that interest rates will be falling in the future, he may

Introduction: Interest rate swaps are used to hedge interest rate risks as well as to take on interest rate risks. If a treasurer is of the view that interest rates will be falling in the future, he may

Fixed Income Liquidity in a Rising Rate Environment

Fixed Income Liquidity in a Rising Rate Environment 2 Executive Summary Ò Fixed income market liquidity has declined, causing greater concern about prospective liquidity in a potential broad market sell-off

Fixed Income Liquidity in a Rising Rate Environment 2 Executive Summary Ò Fixed income market liquidity has declined, causing greater concern about prospective liquidity in a potential broad market sell-off

AVIVA INVESTOR PORTFOLIO RETURNS SINCE INCEPTION FUND PERFORMANCE

AVIVA INVESTOR December,2013 IN ULIP PRODUCTS THE INVESTMENT RISK IN THE INVESTMENT PORTFOLIO SHALL BE BORNE BY THE POLICY HOLDER THE LINKED INSURANCE PRODUCTS DO NOT OFFER ANY LIQUIDITY DURING THE FIRST

AVIVA INVESTOR December,2013 IN ULIP PRODUCTS THE INVESTMENT RISK IN THE INVESTMENT PORTFOLIO SHALL BE BORNE BY THE POLICY HOLDER THE LINKED INSURANCE PRODUCTS DO NOT OFFER ANY LIQUIDITY DURING THE FIRST

PERSONAL RETIREMENT SAVINGS ACCOUNT INVESTMENT REPORT

PENSIONS INVESTMENTS LIFE INSURANCE PERSONAL RETIREMENT SAVINGS ACCOUNT INVESTMENT REPORT FOR PERSONAL RETIREMENT SAVINGS ACCOUNT () PRODUCTS WITH AN ANNUAL FUND MANAGEMENT CHARGE OF 1% - JULY 201 Thank

PENSIONS INVESTMENTS LIFE INSURANCE PERSONAL RETIREMENT SAVINGS ACCOUNT INVESTMENT REPORT FOR PERSONAL RETIREMENT SAVINGS ACCOUNT () PRODUCTS WITH AN ANNUAL FUND MANAGEMENT CHARGE OF 1% - JULY 201 Thank

INR Volatility - Hedging Options & Effective Strategies

INR Volatility - Hedging Options & Effective Strategies The purpose of the article is to draw attention on the recent volatility in Indian Rupee, various hedging options and effective hedging strategies.

INR Volatility - Hedging Options & Effective Strategies The purpose of the article is to draw attention on the recent volatility in Indian Rupee, various hedging options and effective hedging strategies.

Chapter 12. Page 1. Bonds: Analysis and Strategy. Learning Objectives. INVESTMENTS: Analysis and Management Second Canadian Edition

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 12 Bonds: Analysis and Strategy Learning Objectives Explain why investors buy bonds. Discuss major considerations

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 12 Bonds: Analysis and Strategy Learning Objectives Explain why investors buy bonds. Discuss major considerations

Recent Developments and Outlook for the Mexican Economy Credit Suisse, 2016 Macro Conference April 19, 2016

Credit Suisse, Macro Conference April 19, Outline 1 Inflation and Monetary Policy 2 Recent Developments and Outlook for the Mexican Economy 3 Final Remarks 2 In line with its constitutional mandate, the

Credit Suisse, Macro Conference April 19, Outline 1 Inflation and Monetary Policy 2 Recent Developments and Outlook for the Mexican Economy 3 Final Remarks 2 In line with its constitutional mandate, the

Spectrum Insights. Time to float. Why invest in corporate bonds? - Value

Spectrum Insights Damien Wood, Principal JUNE 25, 2015 Time to float Investing in floating rate bonds as opposed to fixed rate bonds helps protect bond investors from price slumps. Spectrum expects that

Spectrum Insights Damien Wood, Principal JUNE 25, 2015 Time to float Investing in floating rate bonds as opposed to fixed rate bonds helps protect bond investors from price slumps. Spectrum expects that

OFFICE OF REGIONAL ECONOMIC INTEGRATION (OREI)

") No. 8 August 213 Policy Brief OFFICE OF REGIONAL ECONOMIC INTEGRATION (OREI) Key Points: The comments from the US Federal Reserve Chairman that quantitative easing could soon be tapering off resulted in

No. 8 August 213 Policy Brief OFFICE OF REGIONAL ECONOMIC INTEGRATION (OREI) Key Points: The comments from the US Federal Reserve Chairman that quantitative easing could soon be tapering off resulted in

CIO Flash Revisions to our 2016 global outlook Jan 25, 2016

CIO Flash Revisions to our global outlook Jan 25, +++ CIO FLASH +++ CIO FLASH +++ CIO FLASH +++ CIO FLASH +++ CIO FLASH +++ CIO FLASH +++ CIO FLASH +++ CIO FLASH +++ CIO FLASH The global macro picture:

CIO Flash Revisions to our global outlook Jan 25, +++ CIO FLASH +++ CIO FLASH +++ CIO FLASH +++ CIO FLASH +++ CIO FLASH +++ CIO FLASH +++ CIO FLASH +++ CIO FLASH +++ CIO FLASH The global macro picture:

BANK OF ISRAEL Office of the Spokesperson and Economic Information. Report to the public on the Bank of Israel s discussions prior to deciding on the

BANK OF ISRAEL Office of the Spokesperson and Economic Information September 7, 2015 Report to the public on the Bank of Israel s discussions prior to deciding on the General interest rate for September

BANK OF ISRAEL Office of the Spokesperson and Economic Information September 7, 2015 Report to the public on the Bank of Israel s discussions prior to deciding on the General interest rate for September

Certification Program on Corporate Treasury Management

Certification Program on Corporate Treasury Management Introduction to corporate treasury management Introduction to corporate treasury management: relevance, scope, approach and issues Understanding treasury

Certification Program on Corporate Treasury Management Introduction to corporate treasury management Introduction to corporate treasury management: relevance, scope, approach and issues Understanding treasury

Investment insight. Fixed income the what, when, where, why and how TABLE 1: DIFFERENT TYPES OF FIXED INCOME SECURITIES. What is fixed income?

Fixed income investments make up a large proportion of the investment universe and can form a significant part of a diversified portfolio but investors are often much less familiar with how fixed income

Fixed income investments make up a large proportion of the investment universe and can form a significant part of a diversified portfolio but investors are often much less familiar with how fixed income

Q4.14 Financial Results. March 23, 2015

Q4.14 Financial Results March 23, 2015 Table of Contents 1 Results overview 2 Liquidity 3 Profitability 4 Asset quality 5 Capital 6 Appendix Results overview 1 4Q14 results: key take-aways Liquidity Group

Q4.14 Financial Results March 23, 2015 Table of Contents 1 Results overview 2 Liquidity 3 Profitability 4 Asset quality 5 Capital 6 Appendix Results overview 1 4Q14 results: key take-aways Liquidity Group

WITH-PROFIT ANNUITIES

WITH-PROFIT ANNUITIES BONUS DECLARATION 2014 Contents 1. INTRODUCTION 3 2. SUMMARY OF BONUS DECLARATION 3 3. ECONOMIC OVERVIEW 5 4. WITH-PROFIT ANNUITY OVERVIEW 7 5. INVESTMENTS 9 6. EXPECTED LONG-TERM

WITH-PROFIT ANNUITIES BONUS DECLARATION 2014 Contents 1. INTRODUCTION 3 2. SUMMARY OF BONUS DECLARATION 3 3. ECONOMIC OVERVIEW 5 4. WITH-PROFIT ANNUITY OVERVIEW 7 5. INVESTMENTS 9 6. EXPECTED LONG-TERM

Kazakhstan Financial Review September 2009. News on Kazkommertsbank: Kazakh banking sector developments:

Official exchange KZT/US$ rate at 1 October 2009 150.95 Summary News on Kazkommertsbank: The inflation rate in was 0.4%, and 4.7% YTD The National Bank s monetary policy in the next five years will aim

Official exchange KZT/US$ rate at 1 October 2009 150.95 Summary News on Kazkommertsbank: The inflation rate in was 0.4%, and 4.7% YTD The National Bank s monetary policy in the next five years will aim

Global high yield: We believe it s still offering value December 2013

Global high yield: We believe it s still offering value December 2013 02 of 08 Global high yield: we believe it s still offering value Patrick Maldari, CFA Senior Portfolio Manager North American Fixed

Global high yield: We believe it s still offering value December 2013 02 of 08 Global high yield: we believe it s still offering value Patrick Maldari, CFA Senior Portfolio Manager North American Fixed

FINANCIAL REPORT - MARCH 2015

FINANCIAL REPORT - MARCH 2015 SUMMARY OF THE MACROECONOMIC INFORMATION The macroeconomic scenario Deflation in Europe, the USA well. The passage of years is very positive for the United States: the positive

FINANCIAL REPORT - MARCH 2015 SUMMARY OF THE MACROECONOMIC INFORMATION The macroeconomic scenario Deflation in Europe, the USA well. The passage of years is very positive for the United States: the positive

Today s bond market is riskier and more volatile than in several generations. As

Fixed Income Approach 2014 Volume 1 Executive Summary Today s bond market is riskier and more volatile than in several generations. As interest rates rise so does the anxiety of fixed income investors

Fixed Income Approach 2014 Volume 1 Executive Summary Today s bond market is riskier and more volatile than in several generations. As interest rates rise so does the anxiety of fixed income investors

8.21 % 85.6 % 70 % 17.8 % 5 MUST-KNOW FACTS ON FTSE100 RUPEE DENOMINATED. world s equity Market-cap. UK s equity Market capitalization

5 MUST-KNOW FACTS ON FTSE100 8.21 % world s equity Market-cap 85.6 % UK s equity Market capitalization 100 largest UK listed blue-chip companies 70 % of FTSE100 represented by MNC s 17.8 % 3 years return

5 MUST-KNOW FACTS ON FTSE100 8.21 % world s equity Market-cap 85.6 % UK s equity Market capitalization 100 largest UK listed blue-chip companies 70 % of FTSE100 represented by MNC s 17.8 % 3 years return

Banking. July 25, 2014

July 25, 2014 Banking BANKING SECTOR PERFORMANCE STUDY FY14 Our study covers 39 banks 26 Public Sector Banks & 13 Private Sector Banks. Foreword The in the Indian economy continued to be moderate in FY14

July 25, 2014 Banking BANKING SECTOR PERFORMANCE STUDY FY14 Our study covers 39 banks 26 Public Sector Banks & 13 Private Sector Banks. Foreword The in the Indian economy continued to be moderate in FY14

Introduction to Government Bond, Corporate Bond and Money Markets

Introduction to Government Bond, Corporate Bond and Money Markets Fixed income market in India can be categorized into five segments, Money Market, Government Bond Market, Corporate Bond Market, Interest

Introduction to Government Bond, Corporate Bond and Money Markets Fixed income market in India can be categorized into five segments, Money Market, Government Bond Market, Corporate Bond Market, Interest

Purpose of Selling Stocks Short JANUARY 2007 NUMBER 5

An Overview of Short Stock Selling An effective short stock selling strategy provides an important hedge to a long portfolio and allows hedge fund managers to reduce sector and portfolio beta. Short selling

An Overview of Short Stock Selling An effective short stock selling strategy provides an important hedge to a long portfolio and allows hedge fund managers to reduce sector and portfolio beta. Short selling

Economic Data. October 30, 2015. October 29, 2015

Economic Data October 29, 2015 Country Economic Data Actual Expected Previous NZD RBNZ Rate Decision 2.75% 2.75% 2.75% JPY Industrial Production M/M Sep 1.00% -0.60% -1.20% AUD Import Price Index Q/Q Q3

Economic Data October 29, 2015 Country Economic Data Actual Expected Previous NZD RBNZ Rate Decision 2.75% 2.75% 2.75% JPY Industrial Production M/M Sep 1.00% -0.60% -1.20% AUD Import Price Index Q/Q Q3

South African Reserve Bank. Statement of the Monetary Policy Committee. Issued by Lesetja Kganyago, Governor of the South African Reserve Bank

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 17 March 2016 Statement of the Monetary Policy Committee Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 17 March 2016 Statement of the Monetary Policy Committee Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous

Blyth Fund: Fixed Income Currencies & Commodities Coverage Group May 27, 2014

Blyth Fund: Fixed Income Currencies & Commodities Coverage Group May 27, 2014 VP: Miraj Rahematpura Associate: John Cherian Analysts: Reinier Eenkema van Dijk, Michael Limandibhratha, Ian Naccarella, David

Blyth Fund: Fixed Income Currencies & Commodities Coverage Group May 27, 2014 VP: Miraj Rahematpura Associate: John Cherian Analysts: Reinier Eenkema van Dijk, Michael Limandibhratha, Ian Naccarella, David

2015Q1 INVESTMENT OUTLOOK

TTG WEALTH MANAGEMENT 2015Q1 INVESTMENT OUTLOOK TABLE OF CONTENTS Contents 2015Q1 Core Asset Allocation Summary 1 2015Q1 Satellite Asset Allocation Summary 2 2014 Year-End Review 3 Investment Outlook for

TTG WEALTH MANAGEMENT 2015Q1 INVESTMENT OUTLOOK TABLE OF CONTENTS Contents 2015Q1 Core Asset Allocation Summary 1 2015Q1 Satellite Asset Allocation Summary 2 2014 Year-End Review 3 Investment Outlook for

Forecasting Chinese Economy for the Years 2013-2014

Forecasting Chinese Economy for the Years 2013-2014 Xuesong Li Professor of Economics Deputy Director of Institute of Quantitative & Technical Economics Chinese Academy of Social Sciences Email: [email protected]

Forecasting Chinese Economy for the Years 2013-2014 Xuesong Li Professor of Economics Deputy Director of Institute of Quantitative & Technical Economics Chinese Academy of Social Sciences Email: [email protected]

Improved US data halts gold while supporting oil

Improved US data halts gold while supporting oil The first week of the last quarter brought a host of important economic data culminating with the US unemployment report which turned out to be better than

Improved US data halts gold while supporting oil The first week of the last quarter brought a host of important economic data culminating with the US unemployment report which turned out to be better than

Commodities not finding much traction despite USD weakness

Commodities not finding much traction despite USD weakness Commodities continued to show weakness into the second week of 2013 despite rising stock markets and a falling US dollar. Investors are generally

Commodities not finding much traction despite USD weakness Commodities continued to show weakness into the second week of 2013 despite rising stock markets and a falling US dollar. Investors are generally

JPMorgan Global Bond Fund. Global investing - A less volatile choice NEW. SFC-authorised global bond fund with RMB-hedged share classes*!

AVAILABLE FOR PUBLIC CIRCULATION NEW JPMorgan Global Bond Fund December 2015 Asset Management Company of the Year 2014 Fundamental Strategies, Asia + Important information 1. The Fund invests primarily

AVAILABLE FOR PUBLIC CIRCULATION NEW JPMorgan Global Bond Fund December 2015 Asset Management Company of the Year 2014 Fundamental Strategies, Asia + Important information 1. The Fund invests primarily

Money market portfolio

1 Money market portfolio April 11 Management of Norges Bank s money market portfolio Report for the fourth quarter 1 Contents 1 Key figures Market value and return 3 3 Market risk and management guidelines

1 Money market portfolio April 11 Management of Norges Bank s money market portfolio Report for the fourth quarter 1 Contents 1 Key figures Market value and return 3 3 Market risk and management guidelines

2015 Mid-Year Market Review

2015 Mid-Year Market Review Cedar Hill Associates, LLC www.cedhill.com 6111 North River Road, Suite 1100, Rosemont, Illinois 60018 Phone: 312/445-2900 An Affiliate of MB Financial Bank 2015 Major Investment

2015 Mid-Year Market Review Cedar Hill Associates, LLC www.cedhill.com 6111 North River Road, Suite 1100, Rosemont, Illinois 60018 Phone: 312/445-2900 An Affiliate of MB Financial Bank 2015 Major Investment

Development of the government bond market and public debt management in Singapore

Development of the government bond market and public debt management in Singapore Monetary Authority of Singapore Abstract This paper describes the growth of the Singapore Government Securities (SGS) market.

Development of the government bond market and public debt management in Singapore Monetary Authority of Singapore Abstract This paper describes the growth of the Singapore Government Securities (SGS) market.

percentage points to the overall CPI outcome. Goods price inflation increased to 4,6

South African Reserve Bank Press Statement Embargo on Delivery 28 January 2016 Statement of the Monetary Policy Committee Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the

South African Reserve Bank Press Statement Embargo on Delivery 28 January 2016 Statement of the Monetary Policy Committee Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the

Recent crude oil price dynamics, PETRONAS and Malaysia

Recent crude oil price dynamics, PETRONAS and Malaysia Lim Kim- Hwa [email protected] Tim Niklas Schoepp [email protected] 23 January 2015 Executive Summary Since PETRONAS contributed

Recent crude oil price dynamics, PETRONAS and Malaysia Lim Kim- Hwa [email protected] Tim Niklas Schoepp [email protected] 23 January 2015 Executive Summary Since PETRONAS contributed

Public Debt Management

Public Debt Management Quarterly report OCTOBER- DECEMBER 2015 Government of India Ministry of finance Budget Division Department of economic affairs MARCH 2016 www.finmin.nic.in CONTENTS Section Page

Public Debt Management Quarterly report OCTOBER- DECEMBER 2015 Government of India Ministry of finance Budget Division Department of economic affairs MARCH 2016 www.finmin.nic.in CONTENTS Section Page

Q1 2016. Qatar Quarterly Monitor

Q1 216 Qatar Quarterly Monitor Asiya Research at a glance 2 Every month, we provide: 1) Macroeconomic outlook. 2) Analysis of all countries in Asia and GCC, and some key industrialized economies. 3) Trading

Q1 216 Qatar Quarterly Monitor Asiya Research at a glance 2 Every month, we provide: 1) Macroeconomic outlook. 2) Analysis of all countries in Asia and GCC, and some key industrialized economies. 3) Trading

Global Markets Update Signature Global Advisors

SIGNATURE GLOBAL ADVISORS MARKETS UPDATE AUGUST 3, 2011 The following comments come from an internal interview with Chief Investment Officer, Eric Bushell. They represent Signature s current market views

SIGNATURE GLOBAL ADVISORS MARKETS UPDATE AUGUST 3, 2011 The following comments come from an internal interview with Chief Investment Officer, Eric Bushell. They represent Signature s current market views

Capital preservation strategy update

Client Education Summit 2012 Capital preservation strategy update Head of Institutional Fixed Income Investments, Americas October 9, 2012 Topics for discussion 1 Capital preservation strategies 2 3 4

Client Education Summit 2012 Capital preservation strategy update Head of Institutional Fixed Income Investments, Americas October 9, 2012 Topics for discussion 1 Capital preservation strategies 2 3 4

An Alternative Way to Diversify an Income Strategy

Senior Secured Loans An Alternative Way to Diversify an Income Strategy Alternative Thinking Series There is no shortage of uncertainty and risk facing today s investor. From high unemployment and depressed

Senior Secured Loans An Alternative Way to Diversify an Income Strategy Alternative Thinking Series There is no shortage of uncertainty and risk facing today s investor. From high unemployment and depressed

First Quarter 2015 Financial Market Commentary April, 2015. Stocks Hit New Highs in a Volatile Quarter

Hit New Highs in a Volatile Quarter Stock investors in the U.S. and around the globe had plenty to cheer about during the first quarter of 2015 as at least 17 world stock indexes set news highs due to

Hit New Highs in a Volatile Quarter Stock investors in the U.S. and around the globe had plenty to cheer about during the first quarter of 2015 as at least 17 world stock indexes set news highs due to

Fixed Income Strategy Quarterly April 2015

Doucet Asset Management Fixed Income Strategy Quarterly April 2015 The first quarter of 2015 was a fairly uneventful one. Across the world, the pullback in yields we witnessed in 2014 continued; however,

Doucet Asset Management Fixed Income Strategy Quarterly April 2015 The first quarter of 2015 was a fairly uneventful one. Across the world, the pullback in yields we witnessed in 2014 continued; however,

New Monetary Policy Challenges

New Monetary Policy Challenges 63 Journal of Central Banking Theory and Practice, 2013, 1, pp. 63-67 Received: 5 December 2012; accepted: 4 January 2013 UDC: 336.74 Alexey V. Ulyukaev * New Monetary Policy

New Monetary Policy Challenges 63 Journal of Central Banking Theory and Practice, 2013, 1, pp. 63-67 Received: 5 December 2012; accepted: 4 January 2013 UDC: 336.74 Alexey V. Ulyukaev * New Monetary Policy

UPDATE ON CURRENT MACRO ENVIRONMENT

1 Oct 213 Macro & Strategy Equity Credit Commodities 13 13 #1 Global Strategy #1 Multi Asset Research #3 Global Economics #2 Equity Quant #2 Index Analysis #3 SRI Research 12 sector teams in the Top 1

1 Oct 213 Macro & Strategy Equity Credit Commodities 13 13 #1 Global Strategy #1 Multi Asset Research #3 Global Economics #2 Equity Quant #2 Index Analysis #3 SRI Research 12 sector teams in the Top 1

THE POTENTIAL MACROECONOMIC EFFECT OF DEBT CEILING BRINKMANSHIP

OCTOBER 2013 THE POTENTIAL MACROECONOMIC EFFECT OF DEBT CEILING BRINKMANSHIP Introduction The United States has never defaulted on its obligations, and the U. S. dollar and Treasury securities are at the

OCTOBER 2013 THE POTENTIAL MACROECONOMIC EFFECT OF DEBT CEILING BRINKMANSHIP Introduction The United States has never defaulted on its obligations, and the U. S. dollar and Treasury securities are at the

Global Financials Update April 13, 2012

Global Financials Update April 13, 2012 Global Market Update After posting a fairly strong and consistent rally over much of the last six months, the global equity markets have changed course over the

Global Financials Update April 13, 2012 Global Market Update After posting a fairly strong and consistent rally over much of the last six months, the global equity markets have changed course over the

2013 global economic outlook: Are promising growth trends sustainable? Timothy Hopper, Ph.D., Chief Economist, TIAA-CREF January 24, 2013

2013 global economic outlook: Are promising growth trends sustainable? Timothy Hopper, Ph.D., Chief Economist, TIAA-CREF January 24, 2013 U.S. stock market performance in 2012 * +12.59% total return +6.35%

2013 global economic outlook: Are promising growth trends sustainable? Timothy Hopper, Ph.D., Chief Economist, TIAA-CREF January 24, 2013 U.S. stock market performance in 2012 * +12.59% total return +6.35%

LIST OF MAJOR LEADING & LAGGING ECONOMIC INDICATORS

APRIL 2014 LIST OF MAJOR LEADING & LAGGING ECONOMIC INDICATORS Most economists talk about where the economy is headed it s what they do. Paying attention to economic indicators can give you an idea of

APRIL 2014 LIST OF MAJOR LEADING & LAGGING ECONOMIC INDICATORS Most economists talk about where the economy is headed it s what they do. Paying attention to economic indicators can give you an idea of

Investment Strategies for Pension Funds. Christopher Nichols Investment Director, Multi Asset Investing Standard Life Investments (UK)

") Investment Strategies for Pension Funds Christopher Nichols Investment Director, Multi Asset Investing Standard Life Investments (UK) Pensions need consistency but markets deliver chaos Discrete Yearly

Investment Strategies for Pension Funds Christopher Nichols Investment Director, Multi Asset Investing Standard Life Investments (UK) Pensions need consistency but markets deliver chaos Discrete Yearly

Finance Ministers Speech NDTV Profit Business Leadership awards 2011

Finance Ministers Speech NDTV Profit Business Leadership awards 2011 Ladies and Gentlemen, I am very happy to be here today among this distinguished gathering of industrialists and business persons on

Finance Ministers Speech NDTV Profit Business Leadership awards 2011 Ladies and Gentlemen, I am very happy to be here today among this distinguished gathering of industrialists and business persons on

Lecture 4: The Aftermath of the Crisis

Lecture 4: The Aftermath of the Crisis 2 The Fed s Efforts to Restore Financial Stability A financial panic in fall 2008 threatened the stability of the global financial system. In its lender-of-last-resort

Lecture 4: The Aftermath of the Crisis 2 The Fed s Efforts to Restore Financial Stability A financial panic in fall 2008 threatened the stability of the global financial system. In its lender-of-last-resort

Mutual Fund Category Analysis Banking Sector Funds

November 18, 2014 Mutual Fund Category Analysis Banking Sector Funds Key Facts: What are they? Banking Sector funds are equity oriented schemes investing predominantly in the banking stocks. Banking Category:

November 18, 2014 Mutual Fund Category Analysis Banking Sector Funds Key Facts: What are they? Banking Sector funds are equity oriented schemes investing predominantly in the banking stocks. Banking Category: