Statistical Tests for Multiple Forecast Comparison

|

|

|

- Eustacia Hicks

- 9 years ago

- Views:

Transcription

1 Statistical Tests for Multiple Forecast Comparison Roberto S. Mariano (Singapore Management University & University of Pennsylvania) Daniel Preve (Uppsala University) June 6-7, 2008 T.W. Anderson Conference, Stanford University

Daniel Preve (Uppsala University) June")

2 Why Test for Predictive Ability?

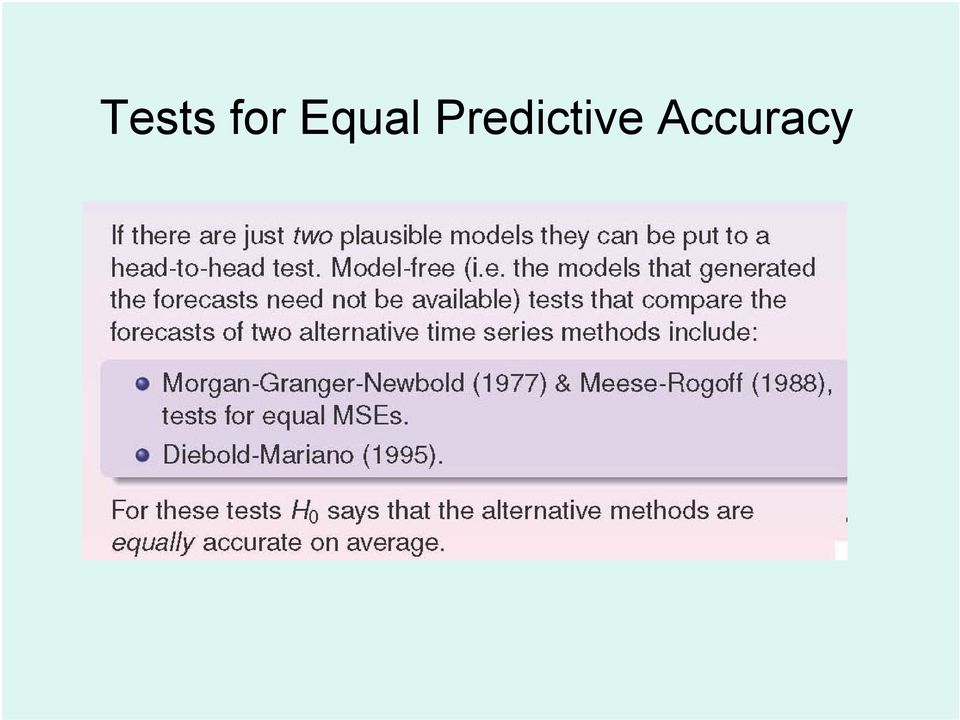

3 Tests for Equal Predictive Accuracy

4 The Diebold-Mariano (DM) Test

5 Introductory Remarks Obvious desirability of formal testing procedures But earlier efforts at assessing forecast accuracy revolved around calculation of summary error statistics-mainly due to complexities in dealing with sampling uncertainties and correlations present in forecast errors

6 Introductory Remarks... continue Formal testing approaches started with loss functions that are quadratic in forecast errors; & forecast errors are assumed to be Gaussian and serially uncorrelated More recent efforts much more relaxed conditions Loss functions may be nonquadratic and asymmetric Forecast errors need not be Gaussian Generally based on large-sample asymtotic analysis With limited experimental studies on small-sample properties

7 Significance Tests of Forecast Accuracy Model-based tests Assumes an econometric model, typically parametric Model is estimated from a given data sample Data and model are both available for testing forecast accuracy Applied in large macroeconometric models, using deterministic and stochastic simulations of the estimated model

8 Significance Tests of Forecast Accuracy... continue Model-free tests Limited information set: set of forecasts and actual values of the predictand

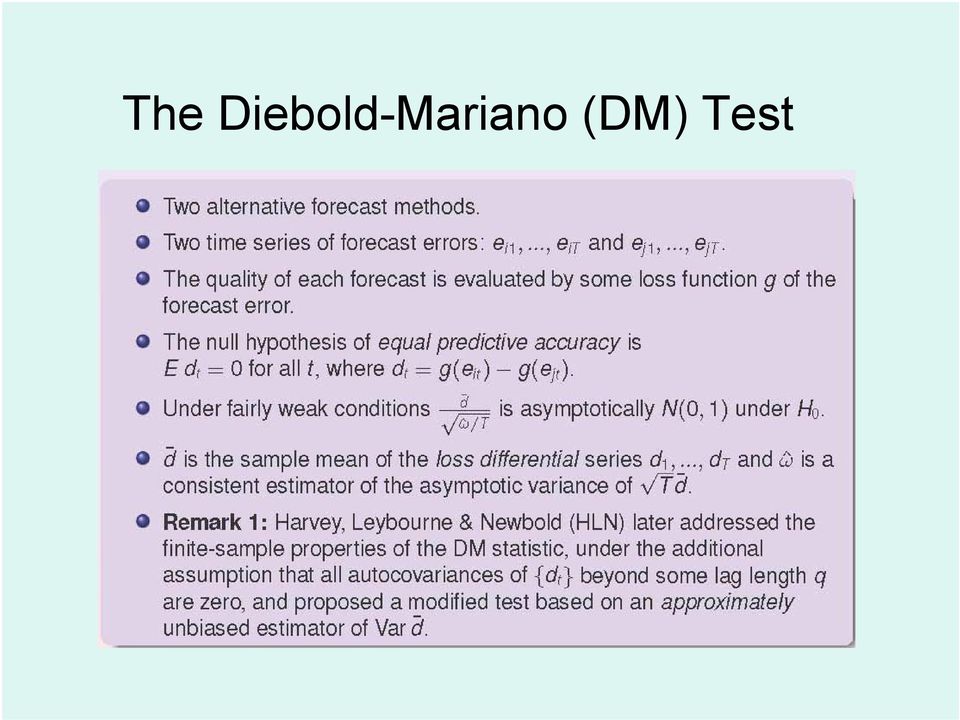

9 Preliminaries (1) Available information: t=1,2,3, T Actual values y t Forecast i: ŷ it, i=1,2 Forecast errors: e it = ŷ it -y t Loss depends on forecast and actual values only through the forecast error: g(y t, ŷ it ) = g(ŷ it -y t ) = g(e it ) Loss differential between the two forecasts d(t) = g(e 1t ) g(e 2t )

Loss differential between the two forecasts d(t) = g(e 1t ) g(e 2t )")

10 Preliminaries (2) Two forecasts have equal accuracy if and only if the loss differential has zero expectation for all t Hence, test H 0 : E(d t ) = 0 for all t versus the alternative hypothesis H 1 : E(d t ) = μ, different from zero

= μ, different")

11 Morgan-Granger-Newbold (MGN) Test (1977) Assume A(1) Loss is quadratic A(2) Forecast errors are (a) zero mean, (b) Gaussian, ( c ) serially uncorrelated Let x t = e 1t + e 2t z t = e 1t e 2t Here, H 0 is equivalent to equality of the two forecast error variances, or, equivalently, zero correlation between x t and z t

12 Variations of MGN Test Harvey, Leybourne and Newbold (1997) regression set up x t = β z t + ε t The MGN test statistic is exactly the same as that for testing the null hypothesis that β = 0 in this regression.

13 Variations of MGN Test... continue When the forecast errors come from a heavytailed distribution, HLN argue that the estimate of the variance of b is biased and suggest utilizing a White-correction for heteroskedasticity to estimate the variance of b. Another HLN variation: Spearman s rank test for zero correlation between x and z

14 Variations of MGN Test... continue Real drawback of all these tests: limitation of applicability to one-step predictions and to squared error loss

15 Meese-Rogoff (MR) Test (1988) Now, forecast errors can be serially and contemporaneously correlated Still maintain assumptions A1, A2a, and A2b and assume squared error loss The MR test is based on the sample covariance between x t and z t

16 Diebold-Mariano (DM) Test (1995) Applicable to nonquadratic loss functions, multi-period forecasts, and forecast errors that are non-gaussian, nonzero-mean, serially correlated, and contemporaneously correlated. Basis of the test: sample mean of the observed loss differential series {d t : t=1, 2, }

17 DM Test (2) Assuming covariance stationarity and other regularity conditions on the process {d t }, then T 1/2 ( d μ) converges in distribution to N(0, 2 π f d (0)), f d (.) is the spectral density of {d t } d is the sample mean loss differential

is the spectral density of {d t } d is the sample mean loss")

18 DM Test Statistic DM = d /[2 π fˆ (0)/ T] d 1/2 ˆ (0) where f d is a consistent estimate of f d (0).

19 Small-Sample Modification of DM Test HLN (1997) :use an approximately unbiased estimate of the variance of the mean loss differential Forecast accuracy is measured in terms of mean squared prediction error

20 Small-Sample Modification of DM Test... continue H-step ahead forecast errors are assumed to have zero autocorrelations at order h and beyond Small-sample modification DM* = DM/{[T+1-2h+h(h-1)/T]/T} 1/2 t-distribution with T-1 df..

/T]/T}")

21 Applications Predictability of nominal exchange rates (Mark 1995) Comparing predictive ability of flexiblespecification, fixed-specification, linear and nonlinear econometric models of macroeconomic variables (Swanson & White 1997)

22 Applications Predictive ability with cointegrated variables (Corradi, Swanson & Olivetti 2001) Predictive ability in the presence of structural breaks (Clark & McCracken 2003) Forecast comparison of volatility models versus GARCH (1,1) (Hansen & Lunde 2005)

23 Applications Forecast comparison of volatility models versus GARCH (1,1) (Hansen & Lunde 2005)

24 A Multivariate Test

25 Invariance and Bias

26 Two Modified Tests

27 Monte Carlo Setup

28

29 Multivariate Case Monte Carlo Results The proposed test can be oversized in moderate samples The test benefits noticeably from the finitesample correction, even in moderately large samples However, the finite-sample correction provides only a partial adjustment

30 Multivariate Case Follow-up Work Consider alternative types of weak stationarity Extensions to Panel data (Pesaran) High frequency data Qualitative and limited dependent variable Semiparametric approaches Compare with White / Hansen's data snooping reality test Relation to Ken West s test for predictive ability Semiparametric approaches to multivariate tests of forecasting performance Power considerations

31 The End

Lesson19: Comparing Predictive Accuracy of two Forecasts: Th. Diebold-Mariano Test

Lesson19: Comparing Predictive Accuracy of two Forecasts: The Diebold-Mariano Test Dipartimento di Ingegneria e Scienze dell Informazione e Matematica Università dell Aquila, [email protected]

Lesson19: Comparing Predictive Accuracy of two Forecasts: The Diebold-Mariano Test Dipartimento di Ingegneria e Scienze dell Informazione e Matematica Università dell Aquila, [email protected]

Department of Economics

Department of Economics On Testing for Diagonality of Large Dimensional Covariance Matrices George Kapetanios Working Paper No. 526 October 2004 ISSN 1473-0278 On Testing for Diagonality of Large Dimensional

Department of Economics On Testing for Diagonality of Large Dimensional Covariance Matrices George Kapetanios Working Paper No. 526 October 2004 ISSN 1473-0278 On Testing for Diagonality of Large Dimensional

Comparing Predictive Accuracy

Diebold, F.X. and Mariano, R. (1995), Comparing Predictive Accuracy, Journal of Business and Economic Statistics, 13, 253-265. Comparing Predictive Accuracy Francis X. Diebold and Roberto S. Mariano Department

Diebold, F.X. and Mariano, R. (1995), Comparing Predictive Accuracy, Journal of Business and Economic Statistics, 13, 253-265. Comparing Predictive Accuracy Francis X. Diebold and Roberto S. Mariano Department

Forecasting Chilean Industrial Production and Sales with Automated Procedures 1

Forecasting Chilean Industrial Production and Sales with Automated Procedures 1 Rómulo A. Chumacero 2 February 2004 1 I thank Ernesto Pastén, Klaus Schmidt-Hebbel, and Rodrigo Valdés for helpful comments

Forecasting Chilean Industrial Production and Sales with Automated Procedures 1 Rómulo A. Chumacero 2 February 2004 1 I thank Ernesto Pastén, Klaus Schmidt-Hebbel, and Rodrigo Valdés for helpful comments

Is the Forward Exchange Rate a Useful Indicator of the Future Exchange Rate?

Is the Forward Exchange Rate a Useful Indicator of the Future Exchange Rate? Emily Polito, Trinity College In the past two decades, there have been many empirical studies both in support of and opposing

Is the Forward Exchange Rate a Useful Indicator of the Future Exchange Rate? Emily Polito, Trinity College In the past two decades, there have been many empirical studies both in support of and opposing

Approximately normal tests for equal predictive accuracy in nested models

Journal of Econometrics 138 (2007) 291 311 www.elsevier.com/locate/jeconom Approximately normal tests for equal predictive accuracy in nested models Todd E. Clark a,, Kenneth D. West b a Economic Research

Journal of Econometrics 138 (2007) 291 311 www.elsevier.com/locate/jeconom Approximately normal tests for equal predictive accuracy in nested models Todd E. Clark a,, Kenneth D. West b a Economic Research

How To Understand The Theory Of Probability

Graduate Programs in Statistics Course Titles STAT 100 CALCULUS AND MATR IX ALGEBRA FOR STATISTICS. Differential and integral calculus; infinite series; matrix algebra STAT 195 INTRODUCTION TO MATHEMATICAL

Graduate Programs in Statistics Course Titles STAT 100 CALCULUS AND MATR IX ALGEBRA FOR STATISTICS. Differential and integral calculus; infinite series; matrix algebra STAT 195 INTRODUCTION TO MATHEMATICAL

FULLY MODIFIED OLS FOR HETEROGENEOUS COINTEGRATED PANELS

FULLY MODIFIED OLS FOR HEEROGENEOUS COINEGRAED PANELS Peter Pedroni ABSRAC his chapter uses fully modified OLS principles to develop new methods for estimating and testing hypotheses for cointegrating

FULLY MODIFIED OLS FOR HEEROGENEOUS COINEGRAED PANELS Peter Pedroni ABSRAC his chapter uses fully modified OLS principles to develop new methods for estimating and testing hypotheses for cointegrating

IAPRI Quantitative Analysis Capacity Building Series. Multiple regression analysis & interpreting results

IAPRI Quantitative Analysis Capacity Building Series Multiple regression analysis & interpreting results How important is R-squared? R-squared Published in Agricultural Economics 0.45 Best article of the

IAPRI Quantitative Analysis Capacity Building Series Multiple regression analysis & interpreting results How important is R-squared? R-squared Published in Agricultural Economics 0.45 Best article of the

MISSING DATA TECHNIQUES WITH SAS. IDRE Statistical Consulting Group

MISSING DATA TECHNIQUES WITH SAS IDRE Statistical Consulting Group ROAD MAP FOR TODAY To discuss: 1. Commonly used techniques for handling missing data, focusing on multiple imputation 2. Issues that could

MISSING DATA TECHNIQUES WITH SAS IDRE Statistical Consulting Group ROAD MAP FOR TODAY To discuss: 1. Commonly used techniques for handling missing data, focusing on multiple imputation 2. Issues that could

Note 2 to Computer class: Standard mis-specification tests

Note 2 to Computer class: Standard mis-specification tests Ragnar Nymoen September 2, 2013 1 Why mis-specification testing of econometric models? As econometricians we must relate to the fact that the

Note 2 to Computer class: Standard mis-specification tests Ragnar Nymoen September 2, 2013 1 Why mis-specification testing of econometric models? As econometricians we must relate to the fact that the

Overview of Violations of the Basic Assumptions in the Classical Normal Linear Regression Model

Overview of Violations of the Basic Assumptions in the Classical Normal Linear Regression Model 1 September 004 A. Introduction and assumptions The classical normal linear regression model can be written

Overview of Violations of the Basic Assumptions in the Classical Normal Linear Regression Model 1 September 004 A. Introduction and assumptions The classical normal linear regression model can be written

Financial Risk Management Exam Sample Questions/Answers

Financial Risk Management Exam Sample Questions/Answers Prepared by Daniel HERLEMONT 1 2 3 4 5 6 Chapter 3 Fundamentals of Statistics FRM-99, Question 4 Random walk assumes that returns from one time period

Financial Risk Management Exam Sample Questions/Answers Prepared by Daniel HERLEMONT 1 2 3 4 5 6 Chapter 3 Fundamentals of Statistics FRM-99, Question 4 Random walk assumes that returns from one time period

Financial Risk Management Exam Sample Questions

Financial Risk Management Exam Sample Questions Prepared by Daniel HERLEMONT 1 PART I - QUANTITATIVE ANALYSIS 3 Chapter 1 - Bunds Fundamentals 3 Chapter 2 - Fundamentals of Probability 7 Chapter 3 Fundamentals

Financial Risk Management Exam Sample Questions Prepared by Daniel HERLEMONT 1 PART I - QUANTITATIVE ANALYSIS 3 Chapter 1 - Bunds Fundamentals 3 Chapter 2 - Fundamentals of Probability 7 Chapter 3 Fundamentals

1 Teaching notes on GMM 1.

Bent E. Sørensen January 23, 2007 1 Teaching notes on GMM 1. Generalized Method of Moment (GMM) estimation is one of two developments in econometrics in the 80ies that revolutionized empirical work in

Bent E. Sørensen January 23, 2007 1 Teaching notes on GMM 1. Generalized Method of Moment (GMM) estimation is one of two developments in econometrics in the 80ies that revolutionized empirical work in

Sales forecasting # 2

Sales forecasting # 2 Arthur Charpentier [email protected] 1 Agenda Qualitative and quantitative methods, a very general introduction Series decomposition Short versus long term forecasting

Sales forecasting # 2 Arthur Charpentier [email protected] 1 Agenda Qualitative and quantitative methods, a very general introduction Series decomposition Short versus long term forecasting

Additional sources Compilation of sources: http://lrs.ed.uiuc.edu/tseportal/datacollectionmethodologies/jin-tselink/tselink.htm

Mgt 540 Research Methods Data Analysis 1 Additional sources Compilation of sources: http://lrs.ed.uiuc.edu/tseportal/datacollectionmethodologies/jin-tselink/tselink.htm http://web.utk.edu/~dap/random/order/start.htm

Mgt 540 Research Methods Data Analysis 1 Additional sources Compilation of sources: http://lrs.ed.uiuc.edu/tseportal/datacollectionmethodologies/jin-tselink/tselink.htm http://web.utk.edu/~dap/random/order/start.htm

Multivariate normal distribution and testing for means (see MKB Ch 3)

") Multivariate normal distribution and testing for means (see MKB Ch 3) Where are we going? 2 One-sample t-test (univariate).................................................. 3 Two-sample t-test (univariate).................................................

Multivariate normal distribution and testing for means (see MKB Ch 3) Where are we going? 2 One-sample t-test (univariate).................................................. 3 Two-sample t-test (univariate).................................................

Practical. I conometrics. data collection, analysis, and application. Christiana E. Hilmer. Michael J. Hilmer San Diego State University

Practical I conometrics data collection, analysis, and application Christiana E. Hilmer Michael J. Hilmer San Diego State University Mi Table of Contents PART ONE THE BASICS 1 Chapter 1 An Introduction

Practical I conometrics data collection, analysis, and application Christiana E. Hilmer Michael J. Hilmer San Diego State University Mi Table of Contents PART ONE THE BASICS 1 Chapter 1 An Introduction

EE 570: Location and Navigation

EE 570: Location and Navigation On-Line Bayesian Tracking Aly El-Osery 1 Stephen Bruder 2 1 Electrical Engineering Department, New Mexico Tech Socorro, New Mexico, USA 2 Electrical and Computer Engineering

EE 570: Location and Navigation On-Line Bayesian Tracking Aly El-Osery 1 Stephen Bruder 2 1 Electrical Engineering Department, New Mexico Tech Socorro, New Mexico, USA 2 Electrical and Computer Engineering

Introduction to Regression and Data Analysis

Statlab Workshop Introduction to Regression and Data Analysis with Dan Campbell and Sherlock Campbell October 28, 2008 I. The basics A. Types of variables Your variables may take several forms, and it

Statlab Workshop Introduction to Regression and Data Analysis with Dan Campbell and Sherlock Campbell October 28, 2008 I. The basics A. Types of variables Your variables may take several forms, and it

Introduction to General and Generalized Linear Models

Introduction to General and Generalized Linear Models General Linear Models - part I Henrik Madsen Poul Thyregod Informatics and Mathematical Modelling Technical University of Denmark DK-2800 Kgs. Lyngby

Introduction to General and Generalized Linear Models General Linear Models - part I Henrik Madsen Poul Thyregod Informatics and Mathematical Modelling Technical University of Denmark DK-2800 Kgs. Lyngby

Masters in Financial Economics (MFE)

") Masters in Financial Economics (MFE) Admission Requirements Candidates must submit the following to the Office of Admissions and Registration: 1. Official Transcripts of previous academic record 2. Two

Masters in Financial Economics (MFE) Admission Requirements Candidates must submit the following to the Office of Admissions and Registration: 1. Official Transcripts of previous academic record 2. Two

Simple Linear Regression Inference

Simple Linear Regression Inference 1 Inference requirements The Normality assumption of the stochastic term e is needed for inference even if it is not a OLS requirement. Therefore we have: Interpretation

Simple Linear Regression Inference 1 Inference requirements The Normality assumption of the stochastic term e is needed for inference even if it is not a OLS requirement. Therefore we have: Interpretation

Auxiliary Variables in Mixture Modeling: 3-Step Approaches Using Mplus

Auxiliary Variables in Mixture Modeling: 3-Step Approaches Using Mplus Tihomir Asparouhov and Bengt Muthén Mplus Web Notes: No. 15 Version 8, August 5, 2014 1 Abstract This paper discusses alternatives

Auxiliary Variables in Mixture Modeling: 3-Step Approaches Using Mplus Tihomir Asparouhov and Bengt Muthén Mplus Web Notes: No. 15 Version 8, August 5, 2014 1 Abstract This paper discusses alternatives

The VAR models discussed so fare are appropriate for modeling I(0) data, like asset returns or growth rates of macroeconomic time series.

data, like asset returns or growth rates of macroeconomic time series.") Cointegration The VAR models discussed so fare are appropriate for modeling I(0) data, like asset returns or growth rates of macroeconomic time series. Economic theory, however, often implies equilibrium

Cointegration The VAR models discussed so fare are appropriate for modeling I(0) data, like asset returns or growth rates of macroeconomic time series. Economic theory, however, often implies equilibrium

Service courses for graduate students in degree programs other than the MS or PhD programs in Biostatistics.

Course Catalog In order to be assured that all prerequisites are met, students must acquire a permission number from the education coordinator prior to enrolling in any Biostatistics course. Courses are

Course Catalog In order to be assured that all prerequisites are met, students must acquire a permission number from the education coordinator prior to enrolling in any Biostatistics course. Courses are

MULTIPLE REGRESSION AND ISSUES IN REGRESSION ANALYSIS

MULTIPLE REGRESSION AND ISSUES IN REGRESSION ANALYSIS MSR = Mean Regression Sum of Squares MSE = Mean Squared Error RSS = Regression Sum of Squares SSE = Sum of Squared Errors/Residuals α = Level of Significance

MULTIPLE REGRESSION AND ISSUES IN REGRESSION ANALYSIS MSR = Mean Regression Sum of Squares MSE = Mean Squared Error RSS = Regression Sum of Squares SSE = Sum of Squared Errors/Residuals α = Level of Significance

The Power of the KPSS Test for Cointegration when Residuals are Fractionally Integrated

The Power of the KPSS Test for Cointegration when Residuals are Fractionally Integrated Philipp Sibbertsen 1 Walter Krämer 2 Diskussionspapier 318 ISNN 0949-9962 Abstract: We show that the power of the

The Power of the KPSS Test for Cointegration when Residuals are Fractionally Integrated Philipp Sibbertsen 1 Walter Krämer 2 Diskussionspapier 318 ISNN 0949-9962 Abstract: We show that the power of the

Cost implications of no-fault automobile insurance. By: Joseph E. Johnson, George B. Flanigan, and Daniel T. Winkler

Cost implications of no-fault automobile insurance By: Joseph E. Johnson, George B. Flanigan, and Daniel T. Winkler Johnson, J. E., G. B. Flanigan, and D. T. Winkler. "Cost Implications of No-Fault Automobile

Cost implications of no-fault automobile insurance By: Joseph E. Johnson, George B. Flanigan, and Daniel T. Winkler Johnson, J. E., G. B. Flanigan, and D. T. Winkler. "Cost Implications of No-Fault Automobile

Optimization of technical trading strategies and the profitability in security markets

Economics Letters 59 (1998) 249 254 Optimization of technical trading strategies and the profitability in security markets Ramazan Gençay 1, * University of Windsor, Department of Economics, 401 Sunset,

Economics Letters 59 (1998) 249 254 Optimization of technical trading strategies and the profitability in security markets Ramazan Gençay 1, * University of Windsor, Department of Economics, 401 Sunset,

Wooldridge, Introductory Econometrics, 3d ed. Chapter 12: Serial correlation and heteroskedasticity in time series regressions

Wooldridge, Introductory Econometrics, 3d ed. Chapter 12: Serial correlation and heteroskedasticity in time series regressions What will happen if we violate the assumption that the errors are not serially

Wooldridge, Introductory Econometrics, 3d ed. Chapter 12: Serial correlation and heteroskedasticity in time series regressions What will happen if we violate the assumption that the errors are not serially

Total Credits: 32 credits are required for master s program graduates and 53 credits for undergraduate program.

Middle East Technical University Graduate School of Social Sciences Doctor of Philosophy in Business Administration In the Field of Quantitative Methods Aim of the PhD Program: Quantitative Methods is

Middle East Technical University Graduate School of Social Sciences Doctor of Philosophy in Business Administration In the Field of Quantitative Methods Aim of the PhD Program: Quantitative Methods is

What s New in Econometrics? Lecture 8 Cluster and Stratified Sampling

What s New in Econometrics? Lecture 8 Cluster and Stratified Sampling Jeff Wooldridge NBER Summer Institute, 2007 1. The Linear Model with Cluster Effects 2. Estimation with a Small Number of Groups and

What s New in Econometrics? Lecture 8 Cluster and Stratified Sampling Jeff Wooldridge NBER Summer Institute, 2007 1. The Linear Model with Cluster Effects 2. Estimation with a Small Number of Groups and

Testing for Granger causality between stock prices and economic growth

MPRA Munich Personal RePEc Archive Testing for Granger causality between stock prices and economic growth Pasquale Foresti 2006 Online at http://mpra.ub.uni-muenchen.de/2962/ MPRA Paper No. 2962, posted

MPRA Munich Personal RePEc Archive Testing for Granger causality between stock prices and economic growth Pasquale Foresti 2006 Online at http://mpra.ub.uni-muenchen.de/2962/ MPRA Paper No. 2962, posted

Least Squares Estimation

Least Squares Estimation SARA A VAN DE GEER Volume 2, pp 1041 1045 in Encyclopedia of Statistics in Behavioral Science ISBN-13: 978-0-470-86080-9 ISBN-10: 0-470-86080-4 Editors Brian S Everitt & David

Least Squares Estimation SARA A VAN DE GEER Volume 2, pp 1041 1045 in Encyclopedia of Statistics in Behavioral Science ISBN-13: 978-0-470-86080-9 ISBN-10: 0-470-86080-4 Editors Brian S Everitt & David

A Subset-Continuous-Updating Transformation on GMM Estimators for Dynamic Panel Data Models

Article A Subset-Continuous-Updating Transformation on GMM Estimators for Dynamic Panel Data Models Richard A. Ashley 1, and Xiaojin Sun 2,, 1 Department of Economics, Virginia Tech, Blacksburg, VA 24060;

Article A Subset-Continuous-Updating Transformation on GMM Estimators for Dynamic Panel Data Models Richard A. Ashley 1, and Xiaojin Sun 2,, 1 Department of Economics, Virginia Tech, Blacksburg, VA 24060;

WORKING PAPER NO. 11-31 OUT-OF-SAMPLE FORECAST TESTS ROBUST TO THE CHOICE OF WINDOW SIZE

WORKING PAPER NO. 11-31 OUT-OF-SAMPLE FORECAST TESTS ROBUST TO THE CHOICE OF WINDOW SIZE Barbara Rossi Duke University and Visiting Scholar, Federal Reserve Bank of Philadelphia Atsushi Inoue North Carolina

WORKING PAPER NO. 11-31 OUT-OF-SAMPLE FORECAST TESTS ROBUST TO THE CHOICE OF WINDOW SIZE Barbara Rossi Duke University and Visiting Scholar, Federal Reserve Bank of Philadelphia Atsushi Inoue North Carolina

Power and sample size in multilevel modeling

Snijders, Tom A.B. Power and Sample Size in Multilevel Linear Models. In: B.S. Everitt and D.C. Howell (eds.), Encyclopedia of Statistics in Behavioral Science. Volume 3, 1570 1573. Chicester (etc.): Wiley,

Snijders, Tom A.B. Power and Sample Size in Multilevel Linear Models. In: B.S. Everitt and D.C. Howell (eds.), Encyclopedia of Statistics in Behavioral Science. Volume 3, 1570 1573. Chicester (etc.): Wiley,

Master programme in Statistics

Master programme in Statistics Björn Holmquist 1 1 Department of Statistics Lund University Cramérsällskapets årskonferens, 2010-03-25 Master programme Vad är ett Master programme? Breddmaster vs Djupmaster

Master programme in Statistics Björn Holmquist 1 1 Department of Statistics Lund University Cramérsällskapets årskonferens, 2010-03-25 Master programme Vad är ett Master programme? Breddmaster vs Djupmaster

Univariate and Multivariate Methods PEARSON. Addison Wesley

Time Series Analysis Univariate and Multivariate Methods SECOND EDITION William W. S. Wei Department of Statistics The Fox School of Business and Management Temple University PEARSON Addison Wesley Boston

Time Series Analysis Univariate and Multivariate Methods SECOND EDITION William W. S. Wei Department of Statistics The Fox School of Business and Management Temple University PEARSON Addison Wesley Boston

Integrated Resource Plan

Integrated Resource Plan March 19, 2004 PREPARED FOR KAUA I ISLAND UTILITY COOPERATIVE LCG Consulting 4962 El Camino Real, Suite 112 Los Altos, CA 94022 650-962-9670 1 IRP 1 ELECTRIC LOAD FORECASTING 1.1

Integrated Resource Plan March 19, 2004 PREPARED FOR KAUA I ISLAND UTILITY COOPERATIVE LCG Consulting 4962 El Camino Real, Suite 112 Los Altos, CA 94022 650-962-9670 1 IRP 1 ELECTRIC LOAD FORECASTING 1.1

16 : Demand Forecasting

16 : Demand Forecasting 1 Session Outline Demand Forecasting Subjective methods can be used only when past data is not available. When past data is available, it is advisable that firms should use statistical

16 : Demand Forecasting 1 Session Outline Demand Forecasting Subjective methods can be used only when past data is not available. When past data is available, it is advisable that firms should use statistical

Non-Stationary Time Series andunitroottests

Econometrics 2 Fall 2005 Non-Stationary Time Series andunitroottests Heino Bohn Nielsen 1of25 Introduction Many economic time series are trending. Important to distinguish between two important cases:

Econometrics 2 Fall 2005 Non-Stationary Time Series andunitroottests Heino Bohn Nielsen 1of25 Introduction Many economic time series are trending. Important to distinguish between two important cases:

171:290 Model Selection Lecture II: The Akaike Information Criterion

171:290 Model Selection Lecture II: The Akaike Information Criterion Department of Biostatistics Department of Statistics and Actuarial Science August 28, 2012 Introduction AIC, the Akaike Information

171:290 Model Selection Lecture II: The Akaike Information Criterion Department of Biostatistics Department of Statistics and Actuarial Science August 28, 2012 Introduction AIC, the Akaike Information

Out-of-Sample Forecast Tests Robust to the Choice of Window Size

Out-of-Sample Forecast Tests Robust to the Choice of Window Size Barbara Rossi and Atsushi Inoue (ICREA,UPF,CREI,BGSE,Duke) (NC State) April 1, 2012 Abstract This paper proposes new methodologies for evaluating

Out-of-Sample Forecast Tests Robust to the Choice of Window Size Barbara Rossi and Atsushi Inoue (ICREA,UPF,CREI,BGSE,Duke) (NC State) April 1, 2012 Abstract This paper proposes new methodologies for evaluating

SYSTEMS OF REGRESSION EQUATIONS

SYSTEMS OF REGRESSION EQUATIONS 1. MULTIPLE EQUATIONS y nt = x nt n + u nt, n = 1,...,N, t = 1,...,T, x nt is 1 k, and n is k 1. This is a version of the standard regression model where the observations

SYSTEMS OF REGRESSION EQUATIONS 1. MULTIPLE EQUATIONS y nt = x nt n + u nt, n = 1,...,N, t = 1,...,T, x nt is 1 k, and n is k 1. This is a version of the standard regression model where the observations

ADVANCED FORECASTING MODELS USING SAS SOFTWARE

ADVANCED FORECASTING MODELS USING SAS SOFTWARE Girish Kumar Jha IARI, Pusa, New Delhi 110 012 [email protected] 1. Transfer Function Model Univariate ARIMA models are useful for analysis and forecasting

ADVANCED FORECASTING MODELS USING SAS SOFTWARE Girish Kumar Jha IARI, Pusa, New Delhi 110 012 [email protected] 1. Transfer Function Model Univariate ARIMA models are useful for analysis and forecasting

Examining the Relationship between ETFS and Their Underlying Assets in Indian Capital Market

2012 2nd International Conference on Computer and Software Modeling (ICCSM 2012) IPCSIT vol. 54 (2012) (2012) IACSIT Press, Singapore DOI: 10.7763/IPCSIT.2012.V54.20 Examining the Relationship between

2012 2nd International Conference on Computer and Software Modeling (ICCSM 2012) IPCSIT vol. 54 (2012) (2012) IACSIT Press, Singapore DOI: 10.7763/IPCSIT.2012.V54.20 Examining the Relationship between

Analysis of Financial Time Series

Analysis of Financial Time Series Analysis of Financial Time Series Financial Econometrics RUEY S. TSAY University of Chicago A Wiley-Interscience Publication JOHN WILEY & SONS, INC. This book is printed

Analysis of Financial Time Series Analysis of Financial Time Series Financial Econometrics RUEY S. TSAY University of Chicago A Wiley-Interscience Publication JOHN WILEY & SONS, INC. This book is printed

2. Linear regression with multiple regressors

2. Linear regression with multiple regressors Aim of this section: Introduction of the multiple regression model OLS estimation in multiple regression Measures-of-fit in multiple regression Assumptions

2. Linear regression with multiple regressors Aim of this section: Introduction of the multiple regression model OLS estimation in multiple regression Measures-of-fit in multiple regression Assumptions

Fixed Effects Bias in Panel Data Estimators

DISCUSSION PAPER SERIES IZA DP No. 3487 Fixed Effects Bias in Panel Data Estimators Hielke Buddelmeyer Paul H. Jensen Umut Oguzoglu Elizabeth Webster May 2008 Forschungsinstitut zur Zukunft der Arbeit

DISCUSSION PAPER SERIES IZA DP No. 3487 Fixed Effects Bias in Panel Data Estimators Hielke Buddelmeyer Paul H. Jensen Umut Oguzoglu Elizabeth Webster May 2008 Forschungsinstitut zur Zukunft der Arbeit

FORECASTING DEPOSIT GROWTH: Forecasting BIF and SAIF Assessable and Insured Deposits

Technical Paper Series Congressional Budget Office Washington, DC FORECASTING DEPOSIT GROWTH: Forecasting BIF and SAIF Assessable and Insured Deposits Albert D. Metz Microeconomic and Financial Studies

Technical Paper Series Congressional Budget Office Washington, DC FORECASTING DEPOSIT GROWTH: Forecasting BIF and SAIF Assessable and Insured Deposits Albert D. Metz Microeconomic and Financial Studies

Vector Time Series Model Representations and Analysis with XploRe

0-1 Vector Time Series Model Representations and Analysis with plore Julius Mungo CASE - Center for Applied Statistics and Economics Humboldt-Universität zu Berlin [email protected] plore MulTi Motivation

0-1 Vector Time Series Model Representations and Analysis with plore Julius Mungo CASE - Center for Applied Statistics and Economics Humboldt-Universität zu Berlin [email protected] plore MulTi Motivation

SIMULATION STUDIES IN STATISTICS WHAT IS A SIMULATION STUDY, AND WHY DO ONE? What is a (Monte Carlo) simulation study, and why do one?

simulation study, and why do one?") SIMULATION STUDIES IN STATISTICS WHAT IS A SIMULATION STUDY, AND WHY DO ONE? What is a (Monte Carlo) simulation study, and why do one? Simulations for properties of estimators Simulations for properties

SIMULATION STUDIES IN STATISTICS WHAT IS A SIMULATION STUDY, AND WHY DO ONE? What is a (Monte Carlo) simulation study, and why do one? Simulations for properties of estimators Simulations for properties

From the help desk: Bootstrapped standard errors

The Stata Journal (2003) 3, Number 1, pp. 71 80 From the help desk: Bootstrapped standard errors Weihua Guan Stata Corporation Abstract. Bootstrapping is a nonparametric approach for evaluating the distribution

The Stata Journal (2003) 3, Number 1, pp. 71 80 From the help desk: Bootstrapped standard errors Weihua Guan Stata Corporation Abstract. Bootstrapping is a nonparametric approach for evaluating the distribution

Econometrics Simple Linear Regression

Econometrics Simple Linear Regression Burcu Eke UC3M Linear equations with one variable Recall what a linear equation is: y = b 0 + b 1 x is a linear equation with one variable, or equivalently, a straight

Econometrics Simple Linear Regression Burcu Eke UC3M Linear equations with one variable Recall what a linear equation is: y = b 0 + b 1 x is a linear equation with one variable, or equivalently, a straight

A Fuel Cost Comparison of Electric and Gas-Powered Vehicles

$ / gl $ / kwh A Fuel Cost Comparison of Electric and Gas-Powered Vehicles Lawrence V. Fulton, McCoy College of Business Administration, Texas State University, [email protected] Nathaniel D. Bastian, University

$ / gl $ / kwh A Fuel Cost Comparison of Electric and Gas-Powered Vehicles Lawrence V. Fulton, McCoy College of Business Administration, Texas State University, [email protected] Nathaniel D. Bastian, University

Implied volatility transmissions between Thai and selected advanced stock markets

MPRA Munich Personal RePEc Archive Implied volatility transmissions between Thai and selected advanced stock markets Supachok Thakolsri and Yuthana Sethapramote and Komain Jiranyakul Public Enterprise

MPRA Munich Personal RePEc Archive Implied volatility transmissions between Thai and selected advanced stock markets Supachok Thakolsri and Yuthana Sethapramote and Komain Jiranyakul Public Enterprise

Statistics Graduate Courses

Statistics Graduate Courses STAT 7002--Topics in Statistics-Biological/Physical/Mathematics (cr.arr.).organized study of selected topics. Subjects and earnable credit may vary from semester to semester.

Statistics Graduate Courses STAT 7002--Topics in Statistics-Biological/Physical/Mathematics (cr.arr.).organized study of selected topics. Subjects and earnable credit may vary from semester to semester.

Examples. David Ruppert. April 25, 2009. Cornell University. Statistics for Financial Engineering: Some R. Examples. David Ruppert.

Cornell University April 25, 2009 Outline 1 2 3 4 A little about myself BA and MA in mathematics PhD in statistics in 1977 taught in the statistics department at North Carolina for 10 years have been in

Cornell University April 25, 2009 Outline 1 2 3 4 A little about myself BA and MA in mathematics PhD in statistics in 1977 taught in the statistics department at North Carolina for 10 years have been in

Advanced Forecasting Techniques and Models: ARIMA

Advanced Forecasting Techniques and Models: ARIMA Short Examples Series using Risk Simulator For more information please visit: www.realoptionsvaluation.com or contact us at: [email protected]

Advanced Forecasting Techniques and Models: ARIMA Short Examples Series using Risk Simulator For more information please visit: www.realoptionsvaluation.com or contact us at: [email protected]

11. Time series and dynamic linear models

11. Time series and dynamic linear models Objective To introduce the Bayesian approach to the modeling and forecasting of time series. Recommended reading West, M. and Harrison, J. (1997). models, (2 nd

11. Time series and dynamic linear models Objective To introduce the Bayesian approach to the modeling and forecasting of time series. Recommended reading West, M. and Harrison, J. (1997). models, (2 nd

Permutation Tests for Comparing Two Populations

Permutation Tests for Comparing Two Populations Ferry Butar Butar, Ph.D. Jae-Wan Park Abstract Permutation tests for comparing two populations could be widely used in practice because of flexibility of

Permutation Tests for Comparing Two Populations Ferry Butar Butar, Ph.D. Jae-Wan Park Abstract Permutation tests for comparing two populations could be widely used in practice because of flexibility of

Chapter 3: The Multiple Linear Regression Model

Chapter 3: The Multiple Linear Regression Model Advanced Econometrics - HEC Lausanne Christophe Hurlin University of Orléans November 23, 2013 Christophe Hurlin (University of Orléans) Advanced Econometrics

Chapter 3: The Multiple Linear Regression Model Advanced Econometrics - HEC Lausanne Christophe Hurlin University of Orléans November 23, 2013 Christophe Hurlin (University of Orléans) Advanced Econometrics

Module 5: Multiple Regression Analysis

Using Statistical Data Using to Make Statistical Decisions: Data Multiple to Make Regression Decisions Analysis Page 1 Module 5: Multiple Regression Analysis Tom Ilvento, University of Delaware, College

Using Statistical Data Using to Make Statistical Decisions: Data Multiple to Make Regression Decisions Analysis Page 1 Module 5: Multiple Regression Analysis Tom Ilvento, University of Delaware, College

The comovement of US and German bond markets

The comovement of US and German bond markets Tom Engsted and Carsten Tanggaard The Aarhus School of Business, Fuglesangs alle 4, DK-8210 Aarhus V. E-mails: [email protected] (Engsted); [email protected] (Tanggaard).

The comovement of US and German bond markets Tom Engsted and Carsten Tanggaard The Aarhus School of Business, Fuglesangs alle 4, DK-8210 Aarhus V. E-mails: [email protected] (Engsted); [email protected] (Tanggaard).

Econometric Forecasting Models

Econometric Forecasting Models presented at THE MIDDLE ATLANTIC ACTUARIAL CLUB, INC. 2006 Annual Meeting, September 12, 2006 Four Points by Sheraton BWI Airport Frederick L. Joutz, Professor Research Program

Econometric Forecasting Models presented at THE MIDDLE ATLANTIC ACTUARIAL CLUB, INC. 2006 Annual Meeting, September 12, 2006 Four Points by Sheraton BWI Airport Frederick L. Joutz, Professor Research Program

Solución del Examen Tipo: 1

Solución del Examen Tipo: 1 Universidad Carlos III de Madrid ECONOMETRICS Academic year 2009/10 FINAL EXAM May 17, 2010 DURATION: 2 HOURS 1. Assume that model (III) verifies the assumptions of the classical

Solución del Examen Tipo: 1 Universidad Carlos III de Madrid ECONOMETRICS Academic year 2009/10 FINAL EXAM May 17, 2010 DURATION: 2 HOURS 1. Assume that model (III) verifies the assumptions of the classical

Chapter 1 Introduction. 1.1 Introduction

Chapter 1 Introduction 1.1 Introduction 1 1.2 What Is a Monte Carlo Study? 2 1.2.1 Simulating the Rolling of Two Dice 2 1.3 Why Is Monte Carlo Simulation Often Necessary? 4 1.4 What Are Some Typical Situations

Chapter 1 Introduction 1.1 Introduction 1 1.2 What Is a Monte Carlo Study? 2 1.2.1 Simulating the Rolling of Two Dice 2 1.3 Why Is Monte Carlo Simulation Often Necessary? 4 1.4 What Are Some Typical Situations

Regression III: Advanced Methods

Lecture 16: Generalized Additive Models Regression III: Advanced Methods Bill Jacoby Michigan State University http://polisci.msu.edu/jacoby/icpsr/regress3 Goals of the Lecture Introduce Additive Models

Lecture 16: Generalized Additive Models Regression III: Advanced Methods Bill Jacoby Michigan State University http://polisci.msu.edu/jacoby/icpsr/regress3 Goals of the Lecture Introduce Additive Models

Dynamic Relationship between Interest Rate and Stock Price: Empirical Evidence from Colombo Stock Exchange

International Journal of Business and Social Science Vol. 6, No. 4; April 2015 Dynamic Relationship between Interest Rate and Stock Price: Empirical Evidence from Colombo Stock Exchange AAMD Amarasinghe

International Journal of Business and Social Science Vol. 6, No. 4; April 2015 Dynamic Relationship between Interest Rate and Stock Price: Empirical Evidence from Colombo Stock Exchange AAMD Amarasinghe

Please follow the directions once you locate the Stata software in your computer. Room 114 (Business Lab) has computers with Stata software

has computers with Stata software") STATA Tutorial Professor Erdinç Please follow the directions once you locate the Stata software in your computer. Room 114 (Business Lab) has computers with Stata software 1.Wald Test Wald Test is used

STATA Tutorial Professor Erdinç Please follow the directions once you locate the Stata software in your computer. Room 114 (Business Lab) has computers with Stata software 1.Wald Test Wald Test is used

Web-based Supplementary Materials for Bayesian Effect Estimation. Accounting for Adjustment Uncertainty by Chi Wang, Giovanni

1 Web-based Supplementary Materials for Bayesian Effect Estimation Accounting for Adjustment Uncertainty by Chi Wang, Giovanni Parmigiani, and Francesca Dominici In Web Appendix A, we provide detailed

1 Web-based Supplementary Materials for Bayesian Effect Estimation Accounting for Adjustment Uncertainty by Chi Wang, Giovanni Parmigiani, and Francesca Dominici In Web Appendix A, we provide detailed

Non Linear Dependence Structures: a Copula Opinion Approach in Portfolio Optimization

Non Linear Dependence Structures: a Copula Opinion Approach in Portfolio Optimization Jean- Damien Villiers ESSEC Business School Master of Sciences in Management Grande Ecole September 2013 1 Non Linear

Non Linear Dependence Structures: a Copula Opinion Approach in Portfolio Optimization Jean- Damien Villiers ESSEC Business School Master of Sciences in Management Grande Ecole September 2013 1 Non Linear

Maximum likelihood estimation of mean reverting processes

Maximum likelihood estimation of mean reverting processes José Carlos García Franco Onward, Inc. [email protected] Abstract Mean reverting processes are frequently used models in real options. For

Maximum likelihood estimation of mean reverting processes José Carlos García Franco Onward, Inc. [email protected] Abstract Mean reverting processes are frequently used models in real options. For

A Trading Strategy Based on the Lead-Lag Relationship of Spot and Futures Prices of the S&P 500

A Trading Strategy Based on the Lead-Lag Relationship of Spot and Futures Prices of the S&P 500 FE8827 Quantitative Trading Strategies 2010/11 Mini-Term 5 Nanyang Technological University Submitted By:

A Trading Strategy Based on the Lead-Lag Relationship of Spot and Futures Prices of the S&P 500 FE8827 Quantitative Trading Strategies 2010/11 Mini-Term 5 Nanyang Technological University Submitted By:

Nonparametric Tests for Randomness

ECE 461 PROJECT REPORT, MAY 2003 1 Nonparametric Tests for Randomness Ying Wang ECE 461 PROJECT REPORT, MAY 2003 2 Abstract To decide whether a given sequence is truely random, or independent and identically

ECE 461 PROJECT REPORT, MAY 2003 1 Nonparametric Tests for Randomness Ying Wang ECE 461 PROJECT REPORT, MAY 2003 2 Abstract To decide whether a given sequence is truely random, or independent and identically

Chapter 10 Introduction to Time Series Analysis

Chapter 1 Introduction to Time Series Analysis A time series is a collection of observations made sequentially in time. Examples are daily mortality counts, particulate air pollution measurements, and

Chapter 1 Introduction to Time Series Analysis A time series is a collection of observations made sequentially in time. Examples are daily mortality counts, particulate air pollution measurements, and

Chapter 3 RANDOM VARIATE GENERATION

Chapter 3 RANDOM VARIATE GENERATION In order to do a Monte Carlo simulation either by hand or by computer, techniques must be developed for generating values of random variables having known distributions.

Chapter 3 RANDOM VARIATE GENERATION In order to do a Monte Carlo simulation either by hand or by computer, techniques must be developed for generating values of random variables having known distributions.

STA 4273H: Statistical Machine Learning

STA 4273H: Statistical Machine Learning Russ Salakhutdinov Department of Statistics! [email protected]! http://www.cs.toronto.edu/~rsalakhu/ Lecture 6 Three Approaches to Classification Construct

STA 4273H: Statistical Machine Learning Russ Salakhutdinov Department of Statistics! [email protected]! http://www.cs.toronto.edu/~rsalakhu/ Lecture 6 Three Approaches to Classification Construct

1.5 Oneway Analysis of Variance

Statistics: Rosie Cornish. 200. 1.5 Oneway Analysis of Variance 1 Introduction Oneway analysis of variance (ANOVA) is used to compare several means. This method is often used in scientific or medical experiments

Statistics: Rosie Cornish. 200. 1.5 Oneway Analysis of Variance 1 Introduction Oneway analysis of variance (ANOVA) is used to compare several means. This method is often used in scientific or medical experiments

TEMPORAL CAUSAL RELATIONSHIP BETWEEN STOCK MARKET CAPITALIZATION, TRADE OPENNESS AND REAL GDP: EVIDENCE FROM THAILAND

I J A B E R, Vol. 13, No. 4, (2015): 1525-1534 TEMPORAL CAUSAL RELATIONSHIP BETWEEN STOCK MARKET CAPITALIZATION, TRADE OPENNESS AND REAL GDP: EVIDENCE FROM THAILAND Komain Jiranyakul * Abstract: This study

I J A B E R, Vol. 13, No. 4, (2015): 1525-1534 TEMPORAL CAUSAL RELATIONSHIP BETWEEN STOCK MARKET CAPITALIZATION, TRADE OPENNESS AND REAL GDP: EVIDENCE FROM THAILAND Komain Jiranyakul * Abstract: This study

Multiple Regression: What Is It?

Multiple Regression Multiple Regression: What Is It? Multiple regression is a collection of techniques in which there are multiple predictors of varying kinds and a single outcome We are interested in

Multiple Regression Multiple Regression: What Is It? Multiple regression is a collection of techniques in which there are multiple predictors of varying kinds and a single outcome We are interested in

Introduction to Fixed Effects Methods

Introduction to Fixed Effects Methods 1 1.1 The Promise of Fixed Effects for Nonexperimental Research... 1 1.2 The Paired-Comparisons t-test as a Fixed Effects Method... 2 1.3 Costs and Benefits of Fixed

Introduction to Fixed Effects Methods 1 1.1 The Promise of Fixed Effects for Nonexperimental Research... 1 1.2 The Paired-Comparisons t-test as a Fixed Effects Method... 2 1.3 Costs and Benefits of Fixed

Statistical Machine Learning

Statistical Machine Learning UoC Stats 37700, Winter quarter Lecture 4: classical linear and quadratic discriminants. 1 / 25 Linear separation For two classes in R d : simple idea: separate the classes

Statistical Machine Learning UoC Stats 37700, Winter quarter Lecture 4: classical linear and quadratic discriminants. 1 / 25 Linear separation For two classes in R d : simple idea: separate the classes

ECON 142 SKETCH OF SOLUTIONS FOR APPLIED EXERCISE #2

University of California, Berkeley Prof. Ken Chay Department of Economics Fall Semester, 005 ECON 14 SKETCH OF SOLUTIONS FOR APPLIED EXERCISE # Question 1: a. Below are the scatter plots of hourly wages

University of California, Berkeley Prof. Ken Chay Department of Economics Fall Semester, 005 ECON 14 SKETCH OF SOLUTIONS FOR APPLIED EXERCISE # Question 1: a. Below are the scatter plots of hourly wages

Part 2: Analysis of Relationship Between Two Variables

Part 2: Analysis of Relationship Between Two Variables Linear Regression Linear correlation Significance Tests Multiple regression Linear Regression Y = a X + b Dependent Variable Independent Variable

Part 2: Analysis of Relationship Between Two Variables Linear Regression Linear correlation Significance Tests Multiple regression Linear Regression Y = a X + b Dependent Variable Independent Variable