Topic Overview. Strategies and Management E4: Resources Management Sources of Financing

|

|

|

- Peregrine Hall

- 9 years ago

- Views:

Transcription

1 Resources for the TEKLA curriculum at Junior Secondary Topic 7 Sources of Financing Strategies and Management Extension Learning Element Module E4 Resources Management Topic Level Duration Topic Overview Strategies and Management E4: Resources Management Sources of Financing S3 3 lessons (40 minutes per lesson) Learning Objectives: 1. To identify the main forms of financing, 2. To understand the characteristics of different forms of financing, and 3. To understand the benefits and drawbacks of different forms of financing. Overview of Contents: Lesson 1 Lesson 2 Lesson 3 Short-term Finance Long-term Finance (Debts) Capital Finance Resources: Topic Overview and Teaching Plan PowerPoint Presentation Suggested Activities: Class Discussion In-class exercise After-class exercise

Capital Finance Resources: Topic Overview and Teaching Plan PowerPoint Presentation Suggested")

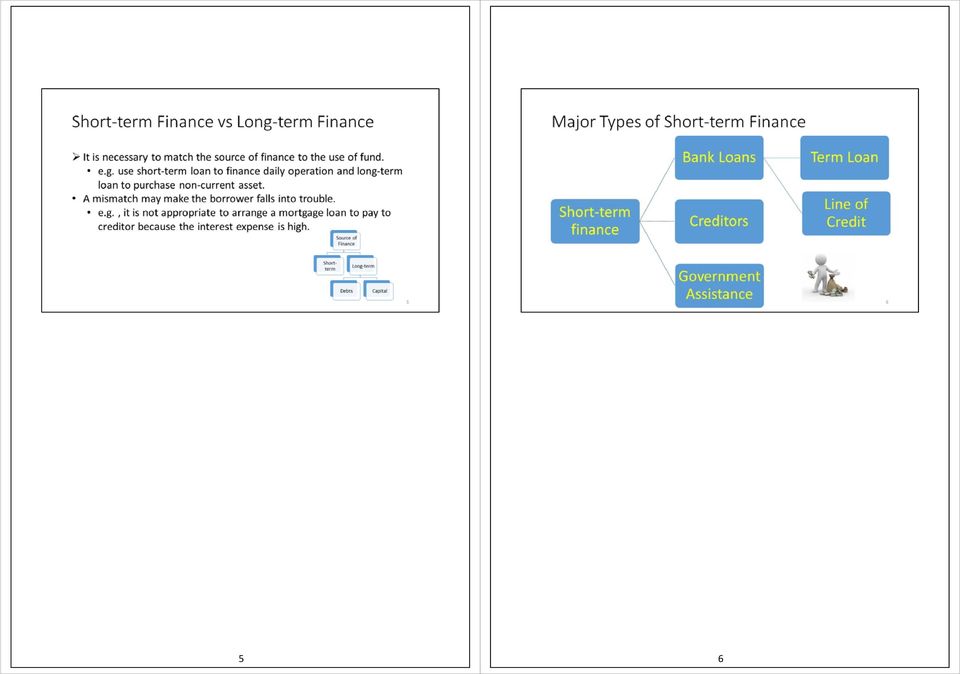

2 Resources for the TEKLA curriculum at Junior Secondary Topic 7 Sources of Financing Strategies and Management Extension Learning Element Module E4 Resources Management Theme Duration Short-term Finance 40 minutes Lesson 1 Expected Learning Outcomes: Upon completion of this lesson, students will be able to: 1. identify the main forms of short-term borrowing, 2. describe the characteristics of term loan, trade credit and government assistance, and 3. describe the benefits and drawbacks of short-term financing. Teaching Sequence and Time Allocation: Activities Part I: Introduction Teacher starts the lesson by a discussion with students of how to obtain funds for business expansion. Teacher explains the concept and definition of short-term and long-term financing. Part II: Content Teacher introduces the major types of short-term financing and their characteristics. Teacher further explains the following types of short-term financing: Banking facilities term loans and loans with line of credit (e.g. overdraft and credit card) trade credit government assistance programme Teacher explains the benefits and drawbacks of short-term financing. Activity 1: After-class exercise Teacher explains the activity to students, asking them to perform a research on different kinds of loan facilities for discussion in the next lesson. Part III: Conclusion Teacher concludes the lesson by reviewing the key points covered. Reference PPT #2 3 PPT #4 5 PPT #6 7 PPT #8 9 PPT #10 PPT #11 PPT #12 13 PPT #14 Time Allocation 8 minutes 6 minutes 5 minutes 10 minutes 6 minutes 3 minutes 2 minutes

3 Resources for the TEKLA curriculum at Junior Secondary Topic 7 Sources of Financing Strategies and Management Extension Learning Element Module E4 Resources Management Theme Duration Long-term Finance (Debts) 40 minutes Lesson 2 Expected Learning Outcomes: Upon completion of this lesson, students will be able to: 1. name the main forms of long-term debts, 2. explain the characteristics of the main types of long-term loans, and 3. select appropriate types of long-term loans in cases. Teaching Sequence and Time Allocation: Activities Part I: Introduction Teacher recaps the purpose and sources of short-term finance and introduces the concept of long-term loan. Part II: Content Teacher describes major types of long-term financing and their characteristics, including: banking facilities term loan and mortgage as well as the concepts of floating and fixed interest rate. leasing including operating and finance lease the characteristics and functions of debenture government assistance programme Teacher explains the benefits and drawbacks of long-term debt. Activity 1: Class discussion Compare the research results of students. Teacher discusses the findings from students and makes conclusion. Part III: Conclusion Teacher concludes the lesson by reviewing the key points covered. Reference PPT #2 3 PPT # 4 6 PPT #7 PPT #8 PPT #9 PPT #10 11 PPT #12 Time Allocation 2 minutes 5 minutes 6 minutes 4 minutes 4 minutes 3 minutes 6 minutes 5 minutes 3 minutes 2 minutes

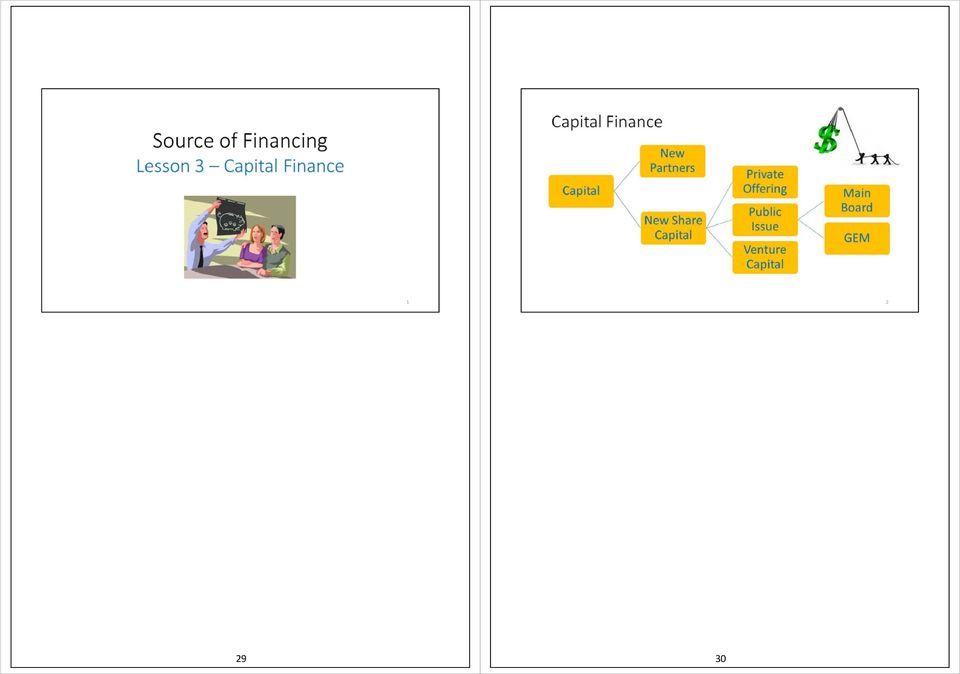

4 Resources for the TEKLA curriculum at Junior Secondary Topic 7 Sources of Financing Strategies and Management Extension Learning Element Module E4 Resources Management Theme Duration Capital Finance 40 minutes Lesson 3 Expected Learning Outcomes: Upon completion of this lesson, students will be able to: 1. explain the common sources of capital finance: introducing new partners and issuing shares, 2. explain the two major forms of share issuing: private offering and public issue (IPO), and 3. describe the difference between Main Board and GEM. Teaching Sequence and Time Allocation: Activities Part I: Introduction Teacher recaps both short-term and long-term loan financing and introduces capital finance Part II: Content Teacher describes major types of capital finance. Teacher explains the advantages and disadvantages of introducing new partners to source fund. Teacher explains the characteristics of two share issuing methods: private offering and public issue. Activity 1: Class discussion Students are required to consider the best solution for financing the expansion of online trading business. Teacher discusses the suggestions provided by students and makes conclusion. (Note: there is no absolute answer but the purpose is to stimulate students thinking and understanding of capital finance.) Part III: Conclusion Teacher concludes the lesson by reviewing the key points covered. Reference PPT #2 PPT #3 5 PPT #6 12 PPT #13 Time Allocation 2 minutes 2 minutes 8 minutes 18 minutes 5 minutes 3 minutes 2 minutes

5 Students are free to suggest any ideas. Teacher encourages them not just simply say borrowing because it is too general. Split the discussion into two parts: the financing of goods for sale and financing of computer server and development of website. 1 2

6 Teacher asks students to apply their suggestions to fit the purpose of purchasing of goods and development of website by completing the table. Discuss with students whether their suggestions are appropriate or not. E.g. if students say using credit card to buy computer hardware, it may not be appropriate because short term loan does not fit for purchase of non current assets. Teacher then discusses the concept of short term finance and long term finance. Teacher highlights the importance of the matching principle of source of finance. For example, it is not appropriate to arrange a mortgage loan to pay to creditor because the interest expense is high. Similarly, if a business uses short term loan to purchase non current assets, it is not easy to have the money back in near future to repay the loan. 3 4

7 5 6

8 7 8

9 9 10

10 11 12

11 Teacher refers students to think about the question in slide 2 and ask them to search for appropriate sources that fit for the purposes as stated in the question

12 15 16

13 17 18

14 19 20

15 Teacher may tell students the current prime rate and HIBOR and explain how it operates in the mortgage loan arrangement. E.g. Compare P 2% with HIBOR + 1% and see which one is good for the borrower and explain the risk of changes of P or HIBOR

16 Students are required to search different kind of loan finance last lesson. Therefore, teacher can introduce another government resource: Youth e start ( start.gov.hk) during the activity session if students cannot find this source

17 Higher interest rate is incurred because long term financing includes a greater span of time for default. A shorter term is less risky to the lender, as it is easier to forecast a borrower s financial status in the short term than long term

18 Teacher discusses the findings from students and make conclusions. There are some suggestions for reference as listed below. For purchase of goods, it is better to finance by short term loan because the goods are held for sale and be able to converted into cash shortly. For example, overdraft or asking for a trade credit. For purchase of computer server, it is better to finance by long term loan because the server is held for use to earn incomes for several years. For example, mortgage loan, government assistance programme such as SME fund and Microfinance Schemes

19 29 30

20 31 32

21 33 34

22 Teacher can give examples of recent IPO and ask students to give examples of listed company to ensure they understand what it is

23 Explain to students: Pt 2: because shareholders can sell part of their holdings to outsiders/new investors. Pt 3: listed company may give a positive image to the public as being large, profitable, powerful etc

24 The removal of record of profitability enables growth enterprises to capitalize on the growth opportunities of the region by raising expansion capital under a well established market and regulatory infrastructure

25 Teacher discusses the suggestions provided by students and makes conclusion. (Note: there is no absolute answers but the purpose of the discussion is to stimulate students to think and understand more about capital finance.) 41 42

26 Resources for the TEKLA curriculum at Junior Secondary Topic 7 Sources of Financing Strategies and Management Extension Learning Element Module E4 Resources Management Section A: Multiple Choice Questions (@1, total 10 marks) 1. Which of the following is not a source of short-term financing? A. Bond. B. Overdraft. C. Credit card. D. Government assistance. Level of difficulty: * 2. Companies selling goods or services to other businesses on credit is called: A. bad debt. B. trade credit. C. overdraft. D. loan. Level of difficulty: * 3. What is the benefit of using short-term bank loan? A. There is no interest charge. B. Borrowers do not require good credit. C. Borrowers can borrow a large amount. D. Borrowers can borrow at an amount at any time so long as the amount borrowed does not exceed the agreed limit. Level of difficulty: ** 4. An interest rate which fluctuates from time to time with the financial market is called: A. bank prime rate. B. fixed interest rate. C. floating interest rate. D. HIBOR. Level of difficulty: * Classwork/Home Assignment P.1

27 Resources for the TEKLA curriculum at Junior Secondary Topic 7 Sources of Financing Strategies and Management Extension Learning Element Module E4 Resources Management 5. A lease that allows lessee to keep the asset after the lease period is called: A. finance lease. B. operating lease. C. mortgage lease. D. instalment. Level of difficulty: ** 6. The payment of interest on debentures is. A. unconditional. B. at discretion of the borrower. C. at discretion of the lender. D. necessary when the borrower makes profit for the year. Level of difficulty: * 7. Which of the following is not a benefit of borrowing long-term debt? A. Stable. B. Flexible. C. Can borrow a larger amount. D. Lenders cannot affect business decisions. Level of difficulty: * 8. What is the benefit of introducing new partners? A. New partners can control the business. B. New partners can provide additional skills. C. Partners has unlimited liabilities regarding the business obligation. D. Shares can be traded in the stock market. Level of difficulty: * Classwork/Home Assignment P.2

28 Resources for the TEKLA curriculum at Junior Secondary Topic 7 Sources of Financing Strategies and Management Extension Learning Element Module E4 Resources Management 9. A company offers its shares to be sold on a stock exchange for the first time is called: A. Private offering. B. Initial public offering. C. Introduction. D. Right issue. Level of difficulty: ** 10. The expected market capitalisation of a new applicant at the time of listing must be at least $ million. A. 20. B. 30. C. 50. D Level of difficulty: * Classwork/Home Assignment P.3

29 Resources for the TEKLA curriculum at Junior Secondary Topic 7 Sources of Financing Strategies and Management Extension Learning Element Module E4 Resources Management Section B: Short Questions (20 marks) * 1. Briefly describe the characteristics of short-term financing. (10 marks) *** 2. As compared with the other sources, what are the benefits and drawbacks of using trade credit as short-term finance? (6 marks) ** 3. What is secured loan? Give one example of secured loan. (4 marks) Classwork/Home Assignment P.4

30 Resources for the TEKLA curriculum at Junior Secondary Topic 7 Sources of Financing Strategies and Management Extension Learning Element Module E4 Resources Management Suggested Solutions Section A: MCQs 1. A 2. B 3. B 4. C 5. A 6. A 7. B 8. B 9. B 10. D Section B: Short Questions. Question 1 (@2, total 10 marks) There is no credit check and assessment and therefore the approval for the loan is quick and easy to obtain. Generally unsecured because the loans are for short periods of time. There is no collateral required against the loan amount. No restriction for the use of fund i.e. it can be used for any purposes. Flexible repayment period e.g. from 1 day to 1 year. Question 2 (@3, total 6 marks) Benefit: There is no cost for the borrower until the due date. Drawback: If the borrower are unable to pay to the supplier, it will affect their relationship and stability of goods supplied. Question 3 (4 marks) A loan is secured when lender has claims against the borrower and against assets of the borrower when the payment of interest or repayment of principal is in default. Mortgage loan is an example of secured loan. Classwork/Home Assignment P.5

Current liabilities - Obligations that are due within one year. Obligations due beyond that period of time are classified as long-term liabilities.

Accounting Fundamentals Lesson 8 8.0 Liabilities Current liabilities - Obligations that are due within one year. Obligations due beyond that period of time are classified as long-term liabilities. Current

Accounting Fundamentals Lesson 8 8.0 Liabilities Current liabilities - Obligations that are due within one year. Obligations due beyond that period of time are classified as long-term liabilities. Current

Long-term sources - those repayable beyond 1 year. No guaranteed return, but potential is unlimited. High risks require a high rate of return.

Sources of Finance Ord Shares Total Finance Long Short Term Term Pref Shares Loans & Debens Bank O/D Leases Debt Factoring Long-term sources - those repayable beyond 1 year. Ordinary Shares The risk capital

Sources of Finance Ord Shares Total Finance Long Short Term Term Pref Shares Loans & Debens Bank O/D Leases Debt Factoring Long-term sources - those repayable beyond 1 year. Ordinary Shares The risk capital

Financial Ratios and Quality Indicators

Financial Ratios and Quality Indicators From U.S. Small Business Administration Online Women's Business Center If you monitor the ratios on a regular basis you'll gain insight into how effectively you

Financial Ratios and Quality Indicators From U.S. Small Business Administration Online Women's Business Center If you monitor the ratios on a regular basis you'll gain insight into how effectively you

Selecting sources of finance for business

Selecting sources of finance for business by Steve Jay 08 Sep 2003 This article considers the practical issues facing a business when selecting appropriate sources of finance. It does not consider the

Selecting sources of finance for business by Steve Jay 08 Sep 2003 This article considers the practical issues facing a business when selecting appropriate sources of finance. It does not consider the

11/11/2013. Lecture 10 Debt capital. Prof. Maged Attia 11/11/2013. Idea or opportunity. Entrepreneur and team. Resources & Financing

Lecture 10 Debt capital Prof. Maged Attia 11/11/2013 1 2 Entrepreneur and team Idea or opportunity Lectures 1,5 Lectures 2, 3,4 Resources & Financing Lectures 6-10 Other topics: - Exit options - Family

Lecture 10 Debt capital Prof. Maged Attia 11/11/2013 1 2 Entrepreneur and team Idea or opportunity Lectures 1,5 Lectures 2, 3,4 Resources & Financing Lectures 6-10 Other topics: - Exit options - Family

RELEVANT TO ACCA QUALIFICATION PAPER F9. Studying Paper F9? Performance objectives 15 and 16 are relevant to this exam

RELEVANT TO ACCA QUALIFICATION PAPER F9 Studying Paper F9? Performance objectives 15 and 16 are relevant to this exam Business finance Section E of the Paper F9, Financial Management syllabus deals with

RELEVANT TO ACCA QUALIFICATION PAPER F9 Studying Paper F9? Performance objectives 15 and 16 are relevant to this exam Business finance Section E of the Paper F9, Financial Management syllabus deals with

Topic 3: Accounts and finance

Topic 3: Accounts and finance 3.1 Sources of Finance LO1: Evaluate advantages & disadvantages of each form of finance. LO2: Evaluate appropriateness of source of finance for given situation. Short, Medium,

Topic 3: Accounts and finance 3.1 Sources of Finance LO1: Evaluate advantages & disadvantages of each form of finance. LO2: Evaluate appropriateness of source of finance for given situation. Short, Medium,

Appraisal A written analysis prepared by a qualified appraiser and estimating the value of a property

REAL ESTATE BASICS Affordability Analysis An analysis of a buyer s ability to afford the purchase of a home, reviews income, liabilities, and available funds, and considers the type of mortgage a buyer

REAL ESTATE BASICS Affordability Analysis An analysis of a buyer s ability to afford the purchase of a home, reviews income, liabilities, and available funds, and considers the type of mortgage a buyer

Major Sources of Financing Solutions to Chapter Review Questions

Chapter 2: Major Sources of Financing Solutions to Chapter Review Questions 1. Debt finance available in Australia: Trade Credit Bank Overdraft Trade Bills Promissory Notes Commercial Bills Inter-Company

Chapter 2: Major Sources of Financing Solutions to Chapter Review Questions 1. Debt finance available in Australia: Trade Credit Bank Overdraft Trade Bills Promissory Notes Commercial Bills Inter-Company

Section A: Introduction

Section A: Introduction A1 Was this business a subsidiary of another business in 2014? Yes No A2 If you are a subsidiary, what is the name of your current parent business? A3 Did your business generate

Section A: Introduction A1 Was this business a subsidiary of another business in 2014? Yes No A2 If you are a subsidiary, what is the name of your current parent business? A3 Did your business generate

Topic Overview BAFS Elective Part Accounting Module Financial Accounting A05: ICT Applications in Accounting S5 / S6 3 lessons (40 minutes per lesson)

") : Topic Overview P.1 Topic Level Duration Topic Overview Accounting Module Financial Accounting A05: S5 / S6 3 lessons (40 minutes per lesson) Learning Objectives: 1. To understand the advantages and disadvantages

: Topic Overview P.1 Topic Level Duration Topic Overview Accounting Module Financial Accounting A05: S5 / S6 3 lessons (40 minutes per lesson) Learning Objectives: 1. To understand the advantages and disadvantages

Financial Statements

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

CIMA F3 Course Notes. Chapter 3. Short term finance

CIMA F3 Course Notes c Chapter 3 Short term finance Personal use only - not licensed for use on courses 31 1. Conservative, Aggressive and Matching strategies There are three over-riding approaches to

CIMA F3 Course Notes c Chapter 3 Short term finance Personal use only - not licensed for use on courses 31 1. Conservative, Aggressive and Matching strategies There are three over-riding approaches to

26Business f inance. Activity 26.1 (page 477)

") 26Business f inance Activity 26.1 (page 477) 1 Using the list of reasons why businesses require finance on page 476, identify: two business situations that are likely to need long-term finance (more than

26Business f inance Activity 26.1 (page 477) 1 Using the list of reasons why businesses require finance on page 476, identify: two business situations that are likely to need long-term finance (more than

Business Studies - Financial Planning and Management Study Notes. Financial Planning and Management Study Notes:

Business Studies - Financial Planning and Management Study Notes Financial Planning and Management Study Notes: The Role of Financial Planning: The strategic role of financial management: Organisational

Business Studies - Financial Planning and Management Study Notes Financial Planning and Management Study Notes: The Role of Financial Planning: The strategic role of financial management: Organisational

Part 10. Small Business Finance and IPOs

Part 10. Small Business Finance and IPOs In the last section, we looked at how large corporations raised money. In this section, we will examine some of the financing issues facing small and start-up businesses.

Part 10. Small Business Finance and IPOs In the last section, we looked at how large corporations raised money. In this section, we will examine some of the financing issues facing small and start-up businesses.

5.3.2015 г. OC = AAI + ACP

D. Dimov Working capital (or short-term financial) management is the management of current assets and current liabilities: Current assets include inventory, accounts receivable, marketable securities,

D. Dimov Working capital (or short-term financial) management is the management of current assets and current liabilities: Current assets include inventory, accounts receivable, marketable securities,

Chapter 6 Interest rates and Bond Valuation. 2012 Pearson Prentice Hall. All rights reserved. 4-1

Chapter 6 Interest rates and Bond Valuation 2012 Pearson Prentice Hall. All rights reserved. 4-1 Interest Rates and Required Returns: Interest Rate Fundamentals The interest rate is usually applied to

Chapter 6 Interest rates and Bond Valuation 2012 Pearson Prentice Hall. All rights reserved. 4-1 Interest Rates and Required Returns: Interest Rate Fundamentals The interest rate is usually applied to

The Trading Profit and Loss Account

The Trading Profit and Loss Account Businesses usually calculate their profit level by creating a Trading Profit and Loss Account (TPL) The TPL is produced because: It is a legal requirement It summarises

The Trading Profit and Loss Account Businesses usually calculate their profit level by creating a Trading Profit and Loss Account (TPL) The TPL is produced because: It is a legal requirement It summarises

Financial Statements and Ratios: Notes

Financial Statements and Ratios: Notes 1. Uses of the income statement for evaluation Investors use the income statement to help judge their return on investment and creditors (lenders) use it to help

Financial Statements and Ratios: Notes 1. Uses of the income statement for evaluation Investors use the income statement to help judge their return on investment and creditors (lenders) use it to help

Chapter Sources of Short-Term Financing

Chapter Sources of Short-Term Financing Chapter 8 - Outline PPT 8-2 Sources of Short-Term Financing Trade Credit from Suppliers Net Credit Position Chartered Banks in Canada Types of Short-term Loans Interest

Chapter Sources of Short-Term Financing Chapter 8 - Outline PPT 8-2 Sources of Short-Term Financing Trade Credit from Suppliers Net Credit Position Chartered Banks in Canada Types of Short-term Loans Interest

HOW DO SMALL BUSINESSES OPERATE

HOW DO SMALL BUSINESSES OPERATE Sources of Finance and Advice N4 BUSINESS IN ACTION N5 UNDERSTANDING BUSINESS LEARNING INTENTIONS AND LEARNING INTENTION: I understand the SUCCESS CRITERIA different sources

HOW DO SMALL BUSINESSES OPERATE Sources of Finance and Advice N4 BUSINESS IN ACTION N5 UNDERSTANDING BUSINESS LEARNING INTENTIONS AND LEARNING INTENTION: I understand the SUCCESS CRITERIA different sources

Current liabilities and payroll

Chapter 12 Current liabilities and payroll Current liabilities are obligations that the business has to discharge within 12 months or its operating cycle if longer than one year. Obligations that are due

Chapter 12 Current liabilities and payroll Current liabilities are obligations that the business has to discharge within 12 months or its operating cycle if longer than one year. Obligations that are due

Financing Business Growth

Name: Class: Date Taken: Total Possible Marks: 30 Financing Business Growth Complete the following questions in the time allowed by your teacher. Identify up to three factors that a business should consider

Name: Class: Date Taken: Total Possible Marks: 30 Financing Business Growth Complete the following questions in the time allowed by your teacher. Identify up to three factors that a business should consider

Use this section to learn more about business loans and specific financial products that might be right for your company.

Types of Financing Use this section to learn more about business loans and specific financial products that might be right for your company. Revolving Line Of Credit Revolving lines of credit are the most

Types of Financing Use this section to learn more about business loans and specific financial products that might be right for your company. Revolving Line Of Credit Revolving lines of credit are the most

2. Financial management:

2. Financial management: Meaning, scope and role, a brief study of functional areas of financial management. Introduction to various FM tools: ratio analysis, fund flow statement, cash flow statement.

2. Financial management: Meaning, scope and role, a brief study of functional areas of financial management. Introduction to various FM tools: ratio analysis, fund flow statement, cash flow statement.

Chapter 18 Working Capital Management

Chapter 18 Working Capital Management Slide Contents Learning Objectives Principles Used in This Chapter 1. Working Capital Management and the Risk-Return Tradeoff 2. Working Capital Policy 3. Operating

Chapter 18 Working Capital Management Slide Contents Learning Objectives Principles Used in This Chapter 1. Working Capital Management and the Risk-Return Tradeoff 2. Working Capital Policy 3. Operating

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

CASH MANAGEMENT & FINANCING CHOICES THE DEBT MARKET

CASH MANAGEMENT & FINANCING CHOICES THE DEBT MARKET Lesson 6&7 Castellanza, 21 st October 4 th November2015 LESSON5: EXAMPLEN 2 Compute the cash source / cash use prospect and the cash flow statement of

CASH MANAGEMENT & FINANCING CHOICES THE DEBT MARKET Lesson 6&7 Castellanza, 21 st October 4 th November2015 LESSON5: EXAMPLEN 2 Compute the cash source / cash use prospect and the cash flow statement of

Dealing With Your Banker &

Dealing With Your Banker & Other Lenders Your financing The success or failure of your business will depend on whether or not you have enough capital to: buy the equipment and inventory you need; pay overhead

Dealing With Your Banker & Other Lenders Your financing The success or failure of your business will depend on whether or not you have enough capital to: buy the equipment and inventory you need; pay overhead

Sri Lanka Accounting Standard-LKAS 7. Statement of Cash Flows

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

CHAPTER 20 LONG TERM FINANCE: SHARES, DEBENTURES AND TERM LOANS

CHAPTER 20 LONG TERM FINANCE: SHARES, DEBENTURES AND TERM LOANS Q.1 What is an ordinary share? How does it differ from a preference share and debenture? Explain its most important features. A.1 Ordinary

CHAPTER 20 LONG TERM FINANCE: SHARES, DEBENTURES AND TERM LOANS Q.1 What is an ordinary share? How does it differ from a preference share and debenture? Explain its most important features. A.1 Ordinary

11.437 Financing Community Economic Development Class 6: Fixed Asset Financing

11.437 Financing Community Economic Development Class 6: Fixed Asset Financing I. Purpose of asset financing Fixed asset financing refers to the financing for real estate and equipment needs of a business.

11.437 Financing Community Economic Development Class 6: Fixed Asset Financing I. Purpose of asset financing Fixed asset financing refers to the financing for real estate and equipment needs of a business.

December 2013 exam. (4CW) SME cash and working capital. Instructions to students. reading time.

SME cash and working capital. Instructions to students. reading time.") 1 December 2013 exam (4CW) SME cash and working capital Instructions to students 1. Time allowed is 3 hours and 10 minutes, which includes 10 minutes reading time. 2. This is a closed book exam. 3. Use

1 December 2013 exam (4CW) SME cash and working capital Instructions to students 1. Time allowed is 3 hours and 10 minutes, which includes 10 minutes reading time. 2. This is a closed book exam. 3. Use

Chapter 16. Debentures: An Introduction. Non-current Liabilities. Horngren, Best, Fraser, Willett: Accounting 6e 2010 Pearson Australia.

PowerPoint to accompany Non-current Liabilities Chapter 16 Learning Objectives 1. Account for debentures payable transactions 2. Measure interest expense by the straight line interest method 3. Account

PowerPoint to accompany Non-current Liabilities Chapter 16 Learning Objectives 1. Account for debentures payable transactions 2. Measure interest expense by the straight line interest method 3. Account

Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows

7 Statement of Cash Flows") Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

Module 1: Corporate Finance and the Role of Venture Capital Financing TABLE OF CONTENTS

1.0 FINANCING PRINCIPLES Module 1: Corporate Finance and the Role of Venture Capital Financing Financing Principles 1.01 Introduction to Financing Principles 1.02 Capitalization of a Business 1.03 Capital

1.0 FINANCING PRINCIPLES Module 1: Corporate Finance and the Role of Venture Capital Financing Financing Principles 1.01 Introduction to Financing Principles 1.02 Capitalization of a Business 1.03 Capital

Margin Trading. A. How Margin Works? B. Why Trading on Margin Can Be Very Risky and Is Not Suitable for Everyone? C. Conclusion

A. How Margin Works? B. Why Trading on Margin Can Be Very Risky and Is Not Suitable for Everyone? C. Conclusion 2 An investor who purchases securities may pay for the securities in full, from his own resources,

A. How Margin Works? B. Why Trading on Margin Can Be Very Risky and Is Not Suitable for Everyone? C. Conclusion 2 An investor who purchases securities may pay for the securities in full, from his own resources,

5 Interesting Facts about the Peer to Peer (P2P) Market

Market") 5 Interesting Facts about the Peer to Peer (P2P) Market 1 P2P is not crowdfunding PEER TO PEER LENDING CROWDFUNDING The practice of unrelated individuals or companies lending money directly to one another

5 Interesting Facts about the Peer to Peer (P2P) Market 1 P2P is not crowdfunding PEER TO PEER LENDING CROWDFUNDING The practice of unrelated individuals or companies lending money directly to one another

Module 1: Corporate Finance and the Role of Venture Capital Financing TABLE OF CONTENTS

1.0 ALTERNATIVE SOURCES OF FINANCE Module 1: Corporate Finance and the Role of Venture Capital Financing Alternative Sources of Finance TABLE OF CONTENTS 1.1 Short-Term Debt (Short-Term Loans, Line of

1.0 ALTERNATIVE SOURCES OF FINANCE Module 1: Corporate Finance and the Role of Venture Capital Financing Alternative Sources of Finance TABLE OF CONTENTS 1.1 Short-Term Debt (Short-Term Loans, Line of

Short-term investments (also known as marketable securities) are easily convertible to cash that a company plans to hold for a year or less.

are easily convertible to cash that a company plans to hold for a year or less.") Accounting Fundamentals Lesson 5 5.0 Receivables & Investments Short-term investments (also known as marketable securities) are easily convertible to cash that a company plans to hold for a year or less.

Accounting Fundamentals Lesson 5 5.0 Receivables & Investments Short-term investments (also known as marketable securities) are easily convertible to cash that a company plans to hold for a year or less.

Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money.

TEACHER GUIDE 7.2 BORROWING MONEY PAGE 1 Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money. It Is In Your Interest Priority Academic Student Skills

TEACHER GUIDE 7.2 BORROWING MONEY PAGE 1 Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money. It Is In Your Interest Priority Academic Student Skills

The Nature, Elements and Importance of Working Capital

C. WORKING CAPITAL MANAGEMENT 1. The nature, elements and importance of working capital 2. Management of inventories, accounts receivable, accounts payable and cash 3. Determining working capital needs

C. WORKING CAPITAL MANAGEMENT 1. The nature, elements and importance of working capital 2. Management of inventories, accounts receivable, accounts payable and cash 3. Determining working capital needs

Accounting Self Study Guide for Staff of Micro Finance Institutions

Accounting Self Study Guide for Staff of Micro Finance Institutions LESSON 2 The Balance Sheet OBJECTIVES The purpose of this lesson is to introduce the Balance Sheet and explain its components: Assets,

Accounting Self Study Guide for Staff of Micro Finance Institutions LESSON 2 The Balance Sheet OBJECTIVES The purpose of this lesson is to introduce the Balance Sheet and explain its components: Assets,

NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS

NAS 03 NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-3 BENEFITS OF CASH FLOWS INFORMATION 4-5 DEFINITIONS 6-9 Cash and cash equivalents 7-9 PRESENTATION OF A

NAS 03 NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-3 BENEFITS OF CASH FLOWS INFORMATION 4-5 DEFINITIONS 6-9 Cash and cash equivalents 7-9 PRESENTATION OF A

Secured loans - A guide

Secured loans - A guide WHAT IS A SECURED LOAN? A secured loan is a loan in which the borrower pledges some asset such as a car or property as collateral for the loan, which then becomes a secured debt

Secured loans - A guide WHAT IS A SECURED LOAN? A secured loan is a loan in which the borrower pledges some asset such as a car or property as collateral for the loan, which then becomes a secured debt

Small Business Finance Thinking Strategically

Small Business Finance Thinking Strategically Copyright 2007 by AbdulJaami, PLLC. All Rights Reserved. This publication is intended as a general guide only. It does not contain a general legal analysis

Small Business Finance Thinking Strategically Copyright 2007 by AbdulJaami, PLLC. All Rights Reserved. This publication is intended as a general guide only. It does not contain a general legal analysis

Chapter 18 Working Capital Management

Chapter 18 Working Capital Management Slide Contents Learning Objectives Principles Used in This Chapter 1. Working Capital Management and the Risk- Return Tradeoff 2. Working Capital Policy 3. Operating

Chapter 18 Working Capital Management Slide Contents Learning Objectives Principles Used in This Chapter 1. Working Capital Management and the Risk- Return Tradeoff 2. Working Capital Policy 3. Operating

tutor2u Cash Management How and Why Businesses Need to Manage their Cash AS & A2 Business Studies PowerPoint Presentations 2005

Cash Management How and Why Businesses Need to Manage their Cash AS & A2 Business Studies PowerPoint Presentations 2005 Importance of Cash (1) A business can exist for a while without making profits but

Cash Management How and Why Businesses Need to Manage their Cash AS & A2 Business Studies PowerPoint Presentations 2005 Importance of Cash (1) A business can exist for a while without making profits but

M. Com (1st Semester) Examination, 2013 Paper Code: AS-2368. * (Prepared by: Harish Khandelwal, Assistant Professor, Department of Commerce, GGV)

Examination, 2013 Paper Code: AS-2368. * (Prepared by: Harish Khandelwal, Assistant Professor, Department of Commerce, GGV)") Model Answer/suggested solution Business Finance M. Com (1st Semester) Examination, 2013 Paper Code: AS-2368 * (Prepared by: Harish Khandelwal, Assistant Professor, Department of Commerce, GGV) Note: These

Model Answer/suggested solution Business Finance M. Com (1st Semester) Examination, 2013 Paper Code: AS-2368 * (Prepared by: Harish Khandelwal, Assistant Professor, Department of Commerce, GGV) Note: These

How To Understand The Financial System

E. BUSINESS FINANCE 1. Sources of, and raising short-term finance 2. Sources of, and raising long-term finance 3. Internal sources of finance and dividend policy 4. Gearing and capital structure considerations

E. BUSINESS FINANCE 1. Sources of, and raising short-term finance 2. Sources of, and raising long-term finance 3. Internal sources of finance and dividend policy 4. Gearing and capital structure considerations

The Kansai Electric Power Company, Incorporated and Subsidiaries

The Kansai Electric Power Company, Incorporated and Subsidiaries Consolidated Financial Statements for the Years Ended March 31, 2003 and 2002 and for the Six Months Ended September 30, 2003 and 2002 The

The Kansai Electric Power Company, Incorporated and Subsidiaries Consolidated Financial Statements for the Years Ended March 31, 2003 and 2002 and for the Six Months Ended September 30, 2003 and 2002 The

Indicative Content. 1.1.1 The main types of corporate form. 1.1.2 The regulatory framework for companies. 1.1.6 Shareholder Value Analysis.

Unit Title: Corporate Finance Unit Reference Number: L/601/3900 Guided Learning Hours: 210 Level: Level 6 Number of Credits: 25 Learning Outcome 1 The learner will: Understand the role of the Corporate

Unit Title: Corporate Finance Unit Reference Number: L/601/3900 Guided Learning Hours: 210 Level: Level 6 Number of Credits: 25 Learning Outcome 1 The learner will: Understand the role of the Corporate

SAMA GENERAL DEPARTMENT OF FINANCE COMPANIES CONTROL. Prudential Returns Handbook (Finance Companies)

") SAMA GENERAL DEPARTMENT OF FINANCE COMPANIES CONTROL Prudential Returns Handbook (Finance Companies) 1. Introduction Submission schedule All licensed finance companies in Saudi Arabia are required to submit

SAMA GENERAL DEPARTMENT OF FINANCE COMPANIES CONTROL Prudential Returns Handbook (Finance Companies) 1. Introduction Submission schedule All licensed finance companies in Saudi Arabia are required to submit

STATEMENT OF CHANGES IN FINANCIAL POSITION

Home Page - Statement of Changes in Financial Position STATEMENT OF CHANGES IN FINANCIAL POSITION by Dr. J. Herbert Smith/ACOA Chair Technology Management and Entrepreneurship Faculty of Engineering University

Home Page - Statement of Changes in Financial Position STATEMENT OF CHANGES IN FINANCIAL POSITION by Dr. J. Herbert Smith/ACOA Chair Technology Management and Entrepreneurship Faculty of Engineering University

Athens University of Economics and Business

Athens University of Economics and Business MSc in International Shipping, Finance and Management Corporate Finance George Leledakis An Overview of Corporate Financing Topics Covered Corporate Structure

Athens University of Economics and Business MSc in International Shipping, Finance and Management Corporate Finance George Leledakis An Overview of Corporate Financing Topics Covered Corporate Structure

LINX EDUCATIONAL INSTRUCTOR S GUIDE

EXTRA CREDIT: UNDERSTANDING THE DO S & DON TS OF USING CREDIT TAKING CHARGE OF CREDIT: 10 TIPS TO CREDIT DISCIPLINE Use the following suggestions as guidelines to self-discipline to keep your credit in

EXTRA CREDIT: UNDERSTANDING THE DO S & DON TS OF USING CREDIT TAKING CHARGE OF CREDIT: 10 TIPS TO CREDIT DISCIPLINE Use the following suggestions as guidelines to self-discipline to keep your credit in

how to prepare a cash flow statement

business builder 4 how to prepare a cash flow statement zions business resource center zions business resource center 2 how to prepare a cash flow statement A cash flow statement is important to your business

business builder 4 how to prepare a cash flow statement zions business resource center zions business resource center 2 how to prepare a cash flow statement A cash flow statement is important to your business

Corporate Credit Analysis. Arnold Ziegel Mountain Mentors Associates

Corporate Credit Analysis Arnold Ziegel Mountain Mentors Associates I. Introduction The Goals and Nature of Credit Analysis II. Capital Structure and the Suppliers of Capital January, 2008 2008 Arnold

Corporate Credit Analysis Arnold Ziegel Mountain Mentors Associates I. Introduction The Goals and Nature of Credit Analysis II. Capital Structure and the Suppliers of Capital January, 2008 2008 Arnold

Calculating financial position and cash flow indicators

Calculating financial position and cash flow indicators Introduction When a business is deciding whether to grant credit to a potential customer, or whether to continue to grant credit terms to an existing

Calculating financial position and cash flow indicators Introduction When a business is deciding whether to grant credit to a potential customer, or whether to continue to grant credit terms to an existing

So You Want to Borrow Money to Start a Business?

So You Want to Borrow Money to Start a Business? M any small business owners cannot understand why a lending institution would refuse to lend them money. Others have no trouble getting money, but they

So You Want to Borrow Money to Start a Business? M any small business owners cannot understand why a lending institution would refuse to lend them money. Others have no trouble getting money, but they

RELEVANT TO ACCA QUALIFICATION PAPER F9

RELEVANT TO ACCA QUALIFICATION PAPER F9 Analysing the suitability of financing alternatives The requirement to analyse suitable financing alternatives for a company has been common in Paper F9 over the

RELEVANT TO ACCA QUALIFICATION PAPER F9 Analysing the suitability of financing alternatives The requirement to analyse suitable financing alternatives for a company has been common in Paper F9 over the

How To Calculate Financial Leverage Ratio

What Do Short-Term Liquidity Ratios Measure? What Is Working Capital? HOCK international - 2004 1 HOCK international - 2004 2 How Is the Current Ratio Calculated? How Is the Quick Ratio Calculated? HOCK

What Do Short-Term Liquidity Ratios Measure? What Is Working Capital? HOCK international - 2004 1 HOCK international - 2004 2 How Is the Current Ratio Calculated? How Is the Quick Ratio Calculated? HOCK

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle 9.1 Current Assets and 9.1.1 Cash A firm should maintain as little cash as possible, because cash is a nonproductive asset. It earns no

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle 9.1 Current Assets and 9.1.1 Cash A firm should maintain as little cash as possible, because cash is a nonproductive asset. It earns no

GUIDE TO BUSINESS FINANCE & BUSINESS FUNDING

GUIDE TO BUSINESS FINANCE & BUSINESS FUNDING M3 Corporate Finance M3 Corporate Finance is an independent corporate finance house focused exclusively on mid-market transactions. M3 offers specialist corporate

GUIDE TO BUSINESS FINANCE & BUSINESS FUNDING M3 Corporate Finance M3 Corporate Finance is an independent corporate finance house focused exclusively on mid-market transactions. M3 offers specialist corporate

Sources of Short-Term Financing C H A P T E R E I G H T

Sources of -Term Financing C H A P T E R E I G H T Figure 8-1 Structure of corporate debt, 1998 PPT 8-1 35% 30% 25% 20% 15% 10% 5% 0% Accounts payable Bank loans Other short term loans term paper Bonds

Sources of -Term Financing C H A P T E R E I G H T Figure 8-1 Structure of corporate debt, 1998 PPT 8-1 35% 30% 25% 20% 15% 10% 5% 0% Accounts payable Bank loans Other short term loans term paper Bonds

Funding Your Business

Funding Your Business Your business idea may be solid, but without adequate funding your chances of success are slim. Starting a viable business takes judicious financial planning. There are several different

Funding Your Business Your business idea may be solid, but without adequate funding your chances of success are slim. Starting a viable business takes judicious financial planning. There are several different

International Financial Accounting (IFA)

") International Financial Accounting (IFA) Preparation and presentation of Financial Statements DEPARTMENT OF BUSINESS AND LAW ROBERTO DI PIETRA SIENA, NOVEMBER 4, 2013 1 INTERNATIONAL FINANCIAL ACCOUNTING

International Financial Accounting (IFA) Preparation and presentation of Financial Statements DEPARTMENT OF BUSINESS AND LAW ROBERTO DI PIETRA SIENA, NOVEMBER 4, 2013 1 INTERNATIONAL FINANCIAL ACCOUNTING

Lecture 18 SOURCES OF FINANCE AND GOVERNMENT POLICIES

Lecture 18 SOURCES OF FINANCE AND GOVERNMENT POLICIES Learning Objectives Sources of finance for small and medium-sized businesses. Types of financial assistance Finance is needed throughout a company

Lecture 18 SOURCES OF FINANCE AND GOVERNMENT POLICIES Learning Objectives Sources of finance for small and medium-sized businesses. Types of financial assistance Finance is needed throughout a company

how to finance the business

A DV I C E B O O K L E T how to finance the business HOW TO FINANCE THE BUSINESS Getting enough of the right funding is one of the more difficult tasks that you will face as a new entrepreneur. Typically,

A DV I C E B O O K L E T how to finance the business HOW TO FINANCE THE BUSINESS Getting enough of the right funding is one of the more difficult tasks that you will face as a new entrepreneur. Typically,

Invoice Factoring, Debtors Discounting and Trade Finance are bridging facilities using your debtors, stock or movable assets to raise cash.

Dear Sir / Madam, Re Bridging Facilities Invoice Factoring, Debtors Discounting and Trade Finance are bridging facilities using your debtors, stock or movable assets to raise cash. A key element is that

Dear Sir / Madam, Re Bridging Facilities Invoice Factoring, Debtors Discounting and Trade Finance are bridging facilities using your debtors, stock or movable assets to raise cash. A key element is that

Ratio Analysis. A) Liquidity Ratio : - 1) Current ratio = Current asset Current Liability

Liquidity Ratio : - 1) Current ratio = Current asset Current Liability") A) Liquidity Ratio : - Ratio Analysis 1) Current ratio = Current asset Current Liability 2) Quick ratio or Acid Test ratio = Quick Asset Quick liability Quick Asset = Current Asset Stock Quick Liability

A) Liquidity Ratio : - Ratio Analysis 1) Current ratio = Current asset Current Liability 2) Quick ratio or Acid Test ratio = Quick Asset Quick liability Quick Asset = Current Asset Stock Quick Liability

Interest is only paid on the amount of the overdraft drawn down.

Overdraft By enabling you to overdraw from your cheque account, an overdraft is particularly useful at times when income is temporarily insufficient to meet payments that are due. Overdrafts do not require

Overdraft By enabling you to overdraw from your cheque account, an overdraft is particularly useful at times when income is temporarily insufficient to meet payments that are due. Overdrafts do not require

Long Term Business Financing Strategy For A Pakistan Business. Byco Petroleum Pakistan Limited

Long Term Business Financing Strategy For A Pakistan Business Byco Petroleum Pakistan Limited Contents Why We Need Financing Strategy 3 How Financing Strategies are driven? 4 Financing Prerequisite for

Long Term Business Financing Strategy For A Pakistan Business Byco Petroleum Pakistan Limited Contents Why We Need Financing Strategy 3 How Financing Strategies are driven? 4 Financing Prerequisite for

Article Accounting Terminology

Article Accounting Terminology Contents Page 1. Accounting Period... 4 2. Accounts Payable (Sundry Creditors)... 4 3. Accounts Receivable (Sundry Debtors)... 4 4. Assets... 4 5. Benchmarks... 4 6. B.O.S.

Article Accounting Terminology Contents Page 1. Accounting Period... 4 2. Accounts Payable (Sundry Creditors)... 4 3. Accounts Receivable (Sundry Debtors)... 4 4. Assets... 4 5. Benchmarks... 4 6. B.O.S.

Paper F9. Financial Management. Fundamentals Pilot Paper Skills module. The Association of Chartered Certified Accountants

Fundamentals Pilot Paper Skills module Financial Management Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Do NOT open this paper

Fundamentals Pilot Paper Skills module Financial Management Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Do NOT open this paper

STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

Current Assets. Current Liabilities. Quick Assets or Liquid Assets. Current Liabilities. 1. Liquidity Ratios 1 Current Ratio Formula.

1. Liquidity Ratios 1 Current Ratio Current Assets Current Liabilities This ratio shows short-term financial soundness of the business. Higher ratio means better capacity to meet its current obligation.

1. Liquidity Ratios 1 Current Ratio Current Assets Current Liabilities This ratio shows short-term financial soundness of the business. Higher ratio means better capacity to meet its current obligation.

Financing the Business

USQ UNIVERSITY OF SOUTHERN QUEENSLAND MBA - ACC5502 Accounting & Financial Management / S1 / 2015 Financing the Business M B G Wimalarathna [FCA, FCMA, MCIM, FMAAT, MCPM, (MBA PIM/USJ)] Financing through

USQ UNIVERSITY OF SOUTHERN QUEENSLAND MBA - ACC5502 Accounting & Financial Management / S1 / 2015 Financing the Business M B G Wimalarathna [FCA, FCMA, MCIM, FMAAT, MCPM, (MBA PIM/USJ)] Financing through

For our curriculum in Grade 12 we are going to use ratios to analyse the information available in the Income statement and the Balance sheet.

SUBJECT: ACCOUNTING GRADE 12 CHAPTER: COMPANIES LESSON: ANALYSIS AND INTERPRETATION-RATIOS LESSON OVERVIEW (KNOWLEDGE AREAS) LESSON 1. Introduction 2. Analysing of financial statements and its purpose

SUBJECT: ACCOUNTING GRADE 12 CHAPTER: COMPANIES LESSON: ANALYSIS AND INTERPRETATION-RATIOS LESSON OVERVIEW (KNOWLEDGE AREAS) LESSON 1. Introduction 2. Analysing of financial statements and its purpose

Statement of Cash Flows

HKAS 7 Revised February November 2014 Hong Kong Accounting Standard 7 Statement of Cash Flows HKAS 7 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

HKAS 7 Revised February November 2014 Hong Kong Accounting Standard 7 Statement of Cash Flows HKAS 7 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

FINANCIAL STATEMENTS ANALYSIS - AN INTRODUCTION

27 FINANCIAL STATEMENTS ANALYSIS - AN INTRODUCTION You have already learnt about the preparation of financial statements i.e. Balance Sheet and Trading and Profit and Loss Account in the module titled

27 FINANCIAL STATEMENTS ANALYSIS - AN INTRODUCTION You have already learnt about the preparation of financial statements i.e. Balance Sheet and Trading and Profit and Loss Account in the module titled

Understanding Leverage in Closed-End Funds

Closed-End Funds Understanding Leverage in Closed-End Funds The concept of leverage seems simple: borrowing money at a low cost and using it to seek higher returns on an investment. Leverage as it applies

Closed-End Funds Understanding Leverage in Closed-End Funds The concept of leverage seems simple: borrowing money at a low cost and using it to seek higher returns on an investment. Leverage as it applies

Focus Question: How do businesses finance their operations?

LES S ON 14: INT RODUCTION T O FINANCE Focus Question: How do businesses finance their operations? Objectives Students will be able to: Compare and contrast short-, intermediate-, and long-term financing.

LES S ON 14: INT RODUCTION T O FINANCE Focus Question: How do businesses finance their operations? Objectives Students will be able to: Compare and contrast short-, intermediate-, and long-term financing.

Plan and Track Your Finances

Chapter 9 Plan and Track Your Finances 9.1 Finance Your Business 9.2 Pro Forma Financial Statements 9.3 Record Keeping for Businesses Ideas in Action Electronic Safekeeping Katelin Shea addressed the unmet

Chapter 9 Plan and Track Your Finances 9.1 Finance Your Business 9.2 Pro Forma Financial Statements 9.3 Record Keeping for Businesses Ideas in Action Electronic Safekeeping Katelin Shea addressed the unmet

It is concerned with decisions relating to current assets and current liabilities

It is concerned with decisions relating to current assets and current liabilities Best Buy Co, NA s largest consumer electronics retailer, has performed extremely well over the past decade. Its stock sold

It is concerned with decisions relating to current assets and current liabilities Best Buy Co, NA s largest consumer electronics retailer, has performed extremely well over the past decade. Its stock sold

asset classes Understanding Equities Property Bonds Cash

NEWSLETTER Understanding asset classes High return Property FIND OUT MORE Equities FIND OUT MORE Bonds FIND OUT MORE Cash FIND OUT MORE Low risk High risk Asset classes are building blocks of any investment.

NEWSLETTER Understanding asset classes High return Property FIND OUT MORE Equities FIND OUT MORE Bonds FIND OUT MORE Cash FIND OUT MORE Low risk High risk Asset classes are building blocks of any investment.

A GUIDE ON FINANCIAL LEASING I. INTRODUCTION

NATIONAL BANK OF SERBIA A GUIDE ON FINANCIAL LEASING I. INTRODUCTION The purpose of this Guide is to provide basic information on financial leasing as a way to finance purchase of equipment and other fixed

NATIONAL BANK OF SERBIA A GUIDE ON FINANCIAL LEASING I. INTRODUCTION The purpose of this Guide is to provide basic information on financial leasing as a way to finance purchase of equipment and other fixed

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased.

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased. Accounts Receivable are the total amounts customers owe your business for goods or services sold

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased. Accounts Receivable are the total amounts customers owe your business for goods or services sold

WHAT IS BUSINESS CREDIT?

1 WHAT IS BUSINESS CREDIT? Why Do I Need Credit? Establishing a good credit rating is an important financial priority for every business. Having good business credit means that owners of businesses can

1 WHAT IS BUSINESS CREDIT? Why Do I Need Credit? Establishing a good credit rating is an important financial priority for every business. Having good business credit means that owners of businesses can

Management of Receivables

Management of Receivables Different costs involved in maintaining the debtors: 1. Interest. 2. Discount. 3. Collection Charges. 4. Bad Debts. Different approaches of calculating Interest: Total Cost approach.(priority)

Management of Receivables Different costs involved in maintaining the debtors: 1. Interest. 2. Discount. 3. Collection Charges. 4. Bad Debts. Different approaches of calculating Interest: Total Cost approach.(priority)

Financial Ratio Analysis A GUIDE TO USEFUL RATIOS FOR UNDERSTANDING YOUR SOCIAL ENTERPRISE S FINANCIAL PERFORMANCE

Financial Ratio Analysis A GUIDE TO USEFUL RATIOS FOR UNDERSTANDING YOUR SOCIAL ENTERPRISE S FINANCIAL PERFORMANCE December 2013 Acknowledgments This guide and supporting tools were developed by Julie

Financial Ratio Analysis A GUIDE TO USEFUL RATIOS FOR UNDERSTANDING YOUR SOCIAL ENTERPRISE S FINANCIAL PERFORMANCE December 2013 Acknowledgments This guide and supporting tools were developed by Julie

STELLENBOSCH MUNICIPALITY

STELLENBOSCH MUNICIPALITY APPENDIX 9 BORROWING POLICY 203/204 TABLE OF CONTENTS. PURPOSE... 3 2. OBJECTIVES... 3 3. DEFINITIONS... 3 4. SCOPE OF THE POLICY... 4 5. LEGISLATIVE FRAMEWORK AND DELEGATION

STELLENBOSCH MUNICIPALITY APPENDIX 9 BORROWING POLICY 203/204 TABLE OF CONTENTS. PURPOSE... 3 2. OBJECTIVES... 3 3. DEFINITIONS... 3 4. SCOPE OF THE POLICY... 4 5. LEGISLATIVE FRAMEWORK AND DELEGATION

CASH FLOW STATEMENT. MODULE - 6A Analysis of Financial Statements. Cash Flow Statement. Notes

MODULE - 6A Cash Flow Statement 30 CASH FLOW STATEMENT In the previous lesson, you have learnt various types of analysis of financial statements and its tools such as comparative statements, common size

MODULE - 6A Cash Flow Statement 30 CASH FLOW STATEMENT In the previous lesson, you have learnt various types of analysis of financial statements and its tools such as comparative statements, common size

Guide to Financial Statements Study Guide

Guide to Financial Statements Study Guide Overview (Topic 1) Three major financial statements: The Income Statement The Balance Sheet The Cash Flow Statement Objectives: Explain the underlying equation

Guide to Financial Statements Study Guide Overview (Topic 1) Three major financial statements: The Income Statement The Balance Sheet The Cash Flow Statement Objectives: Explain the underlying equation

Management & Principles of Accounting Date: 09/11/2015 Introduction to financial accounting Basic concepts and tools

Management & Principles of Accounting Date: 09/11/2015 Introduction to financial accounting Basic concepts and tools Patrizia Tettamanzi Sophie Goodman Source: Kimmel/Weygandt/Kieso Financial Accounting

Management & Principles of Accounting Date: 09/11/2015 Introduction to financial accounting Basic concepts and tools Patrizia Tettamanzi Sophie Goodman Source: Kimmel/Weygandt/Kieso Financial Accounting

Fundamentals Level Skills Module, Paper F9

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2008 Answers 1 (a) Calculation of weighted average cost of capital (WACC) Cost of equity Cost of equity using capital asset

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2008 Answers 1 (a) Calculation of weighted average cost of capital (WACC) Cost of equity Cost of equity using capital asset