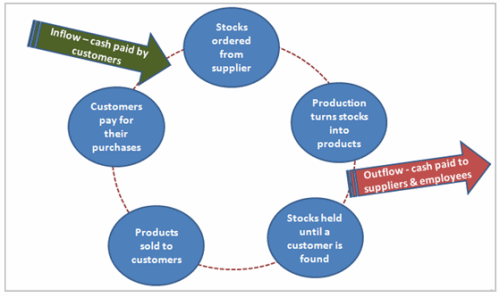

It is concerned with decisions relating to current assets and current liabilities

|

|

|

- Miles Webster

- 9 years ago

- Views:

Transcription

1 It is concerned with decisions relating to current assets and current liabilities

2 Best Buy Co, NA s largest consumer electronics retailer, has performed extremely well over the past decade. Its stock sold for $50 in late 2007 up from $2 ten years earlier. Its excellent performance stemmed from sound financial and operating practices, especially in working capital management. WCM involves finding optimal levels for cash marketable securities, accounts receivable and inventory and then financing that working capital for the least cost. Most of best buy s customers use credit cards, so neither in-store cash nor accounts receivable is significant. Therefore Best buy s working capital focuses on inventories. 2

3 To maintain sales, its stores must be well stocked with the goods customers are seeking at the time they are shopping. This involves determining what new products are hot, determining where they can be obtained at the lowest cost and delivering them to stores in a timely manner. Dramatic improvements in communications and computer technology have transformed the way Best Buy manages its inventories. It now collects real-time data from each store on how each products is selling and its computers place orders automatically to keep the shelves full. Moreover, if sales of an item are slipping, prices are lowered to recue stocks of that item before the situation gets so bad that drastic price cuts are necessary. Working capital needs to be managed to maximize profits and stock prices. 3

4 Inventories Raw materials and components Work-in-progress Trade debtors Loans and advances Bills Receivable Marketable securities Cash and bank balances Sundry creditors Bills payable Outstanding expenses Trade advances Borrowings Provisions 4

5 Gross working capital is the total of all current assets Net working capital = current assets - current liabilities The working capital cycle can often be expressed as a period of time (60 days) Current ratio and Quick ratio Cash budget is an estimate of future cash inflows and outflows Characteristics of current assets Short life span Swift transformation into other asset forms 5

6 6

7 Operating cycle is the time that elapses between the purchase of raw materials and the collection of cash for sales. It is divided into 4 stages: raw materials, WIP, finished goods inventory and debtors collection = Inventory conversion period + accounts receivable period Cash conversion cycle is the time length between the payment for raw material purchases and the collection of cash for sales =Inventory conversion period + accounts receivable period accounts payable period 7

8 Reported as cash and cash equivalents in the balance sheet Marketable securities - Very liquid securities that can be converted into cash quickly at a reasonable price. They tend to have maturities of less than one year. Furthermore, the rate at which these securities can be bought or sold has little effect on their prices. Examples of marketable securities include commercial paper, banker's acceptances, bank certificates, Treasury bills and other money market instruments. Case of Microsoft one time dividend, stock repurchase program, retiring debt, acquiring firms, financing major expansions etc. 8

9 Short term securities that can be bought and sold at short notice Securities are held mostly for precautionary purposes but earn returns Invest in securities when interest rates are high otherwise it is expensive and time consuming to convert them into cash Firm which have high growth rate Firms with volatile cash flow Small new firms which do not have exceptional credit ratings 9

10 Cash discounts on cash payment to suppliers Maintain and improve its credit rating Take advantage of favorable business opportunities Meet emergencies 10

11 An estimate of receipts, disbursements and cash balances for a firm over a specified future period 11

12 Goals of inventory management To ensure that inventories needed to sustain operations are available To hold the costs of ordering and carrying inventories to the lowest possible level Types of costs Ordering & Receiving costs (cost of placing orders, shipping and handling costs) Carrying costs (warehouse rent, interest on capital locked up, insurance, property taxes, spoilage, depreciation and obsolescence, pilferage) Shortage or stockout costs (loss of sales, customer, goodwill, disruption of production schedules) Inventories are supplies, raw materials, work-inprogress and finished goods 12

13 What should be the size of the order? When should the order be placed? Assumptions: The forecast demand for a period is known Orders can be replenished quickly The only costs are ordering and carrying The cost per order does not change with size Cost of carrying is a percentage of inventory value 13

14 It implies that a firm should maintain a minimal level of inventory and rely on suppliers to provide parts and components just in time to meet its assembly requirements It requires a strong and dependable relationship with suppliers who are geographically not very remote from the mfg facility a reliable transportation system an easy physical access in the form of enough doors and conveniently located docks and storage areas to dovetail incoming supplies to the needs of assembly line impeccable quality maintenance of component parts by the supplier Lowers the ordering cost and also the safety stock by forging stronger long term relationship with the suppliers, average inventory level is lower 14

15 A sole trader having $800 capital buys stock for $800. The next day he sells the stock on a 10 day credit for $1000 and takes an overdraft of $800 for stock purchase. Accounts receivable is determined by Volume of credit sales Average time between sales and collection Increase in receivables must be financed in some way Entire amount of receivables need not be financed because of the profit component which does not involve any cash flow 15

16 Credit period: 2 / 10, net 30; lengthening the credit period pushes sales up, lengthens cash conversion cycle, requires larger investment in debtors, leads to higher incidence of bad debts loss Cash discount and trade discount Should attract new customers Will increase cash flow Credit standards: 5 C s of credit are character, capacity, capital, collateral and conditions on which information is received from financial statements, bank references, firm experiences and stock market data Collection policy: procedure that the firm follows to collect accounts receivable Profit potential in granting credit through carrying charges levied on credit sales (nominal and effective interest rates) makes credit sales more profitable than cash sales 16

17 It is unsecured short term pro notes of large firms with high credit rating having an interest rate below the prime rate (a published interest rate charged by commercial banks to large, strong borrowers) Maturity period ranges from 90 to 180 days Generally sold at a discount from its face value and redeemed at its face value, difference constitutes interest. No well developed secondary market The minimum size of commercial paper issue is Rs.2.5 and in denominations of half a million or more Commercial paper is not backed by any form of collateral, so only firms with high-quality debt ratings will easily find buyers without having to offer a substantial discount (higher cost) for the debt issue. The proceeds from this type of financing can only be used on current assets (inventories) and are not allowed to be used on fixed assets, such as a new plant, without SEC involvement. 17

18 A factor is a financial institution which offers services relating to management and financing of debts arising from credit sales, which ensures a definite pattern of cash inflows from credit sales of an organization and eliminates the need for credit and collection department RBI authorized public sector banks that do factoring: SBI, Canbank, PNB, Bank of Allahabad selects the accounts of the client and establishes the credit limits factor assumes responsibility for collecting the debt Advances money against not yet collected / not yet due accounts Factoring is on a recourse basis Besides interest on advances against debt the factor charges a commission which maybe 1 2% of the face value of the debt factored 18

It is concerned with decisions relating to current assets and current liabilities

It is concerned with decisions relating to current assets and current liabilities Best Buy Co, NA s largest consumer electronics retailer, has performed extremely well over the past decade. Its stock sold

It is concerned with decisions relating to current assets and current liabilities Best Buy Co, NA s largest consumer electronics retailer, has performed extremely well over the past decade. Its stock sold

Ratio Analysis. A) Liquidity Ratio : - 1) Current ratio = Current asset Current Liability

Liquidity Ratio : - 1) Current ratio = Current asset Current Liability") A) Liquidity Ratio : - Ratio Analysis 1) Current ratio = Current asset Current Liability 2) Quick ratio or Acid Test ratio = Quick Asset Quick liability Quick Asset = Current Asset Stock Quick Liability

A) Liquidity Ratio : - Ratio Analysis 1) Current ratio = Current asset Current Liability 2) Quick ratio or Acid Test ratio = Quick Asset Quick liability Quick Asset = Current Asset Stock Quick Liability

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle 9.1 Current Assets and 9.1.1 Cash A firm should maintain as little cash as possible, because cash is a nonproductive asset. It earns no

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle 9.1 Current Assets and 9.1.1 Cash A firm should maintain as little cash as possible, because cash is a nonproductive asset. It earns no

WORKING CAPITAL MANAGEMENT

CHAPTER 9 WORKING CAPITAL MANAGEMENT Working capital is the long term fund required to run the day to day operations of the business. The company starts with cash. It buys raw materials, employs staff

CHAPTER 9 WORKING CAPITAL MANAGEMENT Working capital is the long term fund required to run the day to day operations of the business. The company starts with cash. It buys raw materials, employs staff

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions Chapter 6 Working Capital Management Concept Check 6.1 1. What is the meaning of the terms working

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions Chapter 6 Working Capital Management Concept Check 6.1 1. What is the meaning of the terms working

7 Management of Working Capital

7 Management of Working Capital BASIC CONCEPTS AND FORMULAE 1. Working Capital Management Working Capital Management involves managing the balance between firm s shortterm assets and its short-term liabilities.

7 Management of Working Capital BASIC CONCEPTS AND FORMULAE 1. Working Capital Management Working Capital Management involves managing the balance between firm s shortterm assets and its short-term liabilities.

Notes. CIMA Paper P1. Performance Operations

Chapter 5 extract from our ExPress notes for use with the current video. A full set of P1 ExPress notes can be downloaded free of charge at www.. CIMA Paper P1 Performance Operations For exams in 2011

Chapter 5 extract from our ExPress notes for use with the current video. A full set of P1 ExPress notes can be downloaded free of charge at www.. CIMA Paper P1 Performance Operations For exams in 2011

tutor2u Cash Management How and Why Businesses Need to Manage their Cash AS & A2 Business Studies PowerPoint Presentations 2005

Cash Management How and Why Businesses Need to Manage their Cash AS & A2 Business Studies PowerPoint Presentations 2005 Importance of Cash (1) A business can exist for a while without making profits but

Cash Management How and Why Businesses Need to Manage their Cash AS & A2 Business Studies PowerPoint Presentations 2005 Importance of Cash (1) A business can exist for a while without making profits but

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

Working Capital Management Nature & Scope

Working Capital Management Nature & Scope Introduction & Definitions Components of Working Capital Significance of Working Capital Operating Cycle Types of Working Capital Net Vs Gross Working Capital

Working Capital Management Nature & Scope Introduction & Definitions Components of Working Capital Significance of Working Capital Operating Cycle Types of Working Capital Net Vs Gross Working Capital

Planning & Financing of Working Capital

Planning & Financing of Working Capital Objectives of Working Capital Elements of Working Capital Sources of Working Capital Working Capital Control and Banking Policy Tondon Committees Recommendations

Planning & Financing of Working Capital Objectives of Working Capital Elements of Working Capital Sources of Working Capital Working Capital Control and Banking Policy Tondon Committees Recommendations

WORKING CAPITAL MANAGEMENT

WORKING CAPITAL MANAGEMENT What is Working Capital Working capital management is the set of activities that are required to run day to day operations of the business to ensure that cash is adequate to

WORKING CAPITAL MANAGEMENT What is Working Capital Working capital management is the set of activities that are required to run day to day operations of the business to ensure that cash is adequate to

Chapter 019 Short-Term Finance and Planning

Multiple Choice Questions 1. The length of time between the acquisition of inventory and the collection of cash from receivables is called the: a. operating cycle. b. inventory period. c. accounts receivable

Multiple Choice Questions 1. The length of time between the acquisition of inventory and the collection of cash from receivables is called the: a. operating cycle. b. inventory period. c. accounts receivable

Learning Objectives: Quick answer key: Question # Multiple Choice True/False. 14.1 Describe the important of accounting and financial information.

0 Learning Objectives: 14.1 Describe the important of accounting and financial information. 14.2 Differentiate between managerial and financial accounting. 14.3 Identify the six steps of the accounting

0 Learning Objectives: 14.1 Describe the important of accounting and financial information. 14.2 Differentiate between managerial and financial accounting. 14.3 Identify the six steps of the accounting

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased.

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased. Accounts Receivable are the total amounts customers owe your business for goods or services sold

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased. Accounts Receivable are the total amounts customers owe your business for goods or services sold

Working Capital Concept & Animation

Working Capital Concept & Animation Meaning A measure of both a company's efficiency and its short-term financial health. The working capital is calculated as: Working Capital = Current Assets Current

Working Capital Concept & Animation Meaning A measure of both a company's efficiency and its short-term financial health. The working capital is calculated as: Working Capital = Current Assets Current

CHAPTER 16 Current Asset Management and Financing

Copyright 2008 by the Foundation of the American College of Healthcare Executives 6/13/07 Version 16-1 CHAPTER 16 Current Asset Management and Financing Investment and financing policies Cash and marketable

Copyright 2008 by the Foundation of the American College of Healthcare Executives 6/13/07 Version 16-1 CHAPTER 16 Current Asset Management and Financing Investment and financing policies Cash and marketable

WORKING CAPITAL & CASH MANAGEMENT

WORKING CAPITAL & CASH MANAGEMENT STRATEGIES TO PROTECT THE FINANCIAL POSITION OF YOUR BUSINESS PRESENTATION BY HM Nhende 1 Overview of the Presentation Definition of Working Capital Components of Working

WORKING CAPITAL & CASH MANAGEMENT STRATEGIES TO PROTECT THE FINANCIAL POSITION OF YOUR BUSINESS PRESENTATION BY HM Nhende 1 Overview of the Presentation Definition of Working Capital Components of Working

M. Com (1st Semester) Examination, 2013 Paper Code: AS-2368. * (Prepared by: Harish Khandelwal, Assistant Professor, Department of Commerce, GGV)

Examination, 2013 Paper Code: AS-2368. * (Prepared by: Harish Khandelwal, Assistant Professor, Department of Commerce, GGV)") Model Answer/suggested solution Business Finance M. Com (1st Semester) Examination, 2013 Paper Code: AS-2368 * (Prepared by: Harish Khandelwal, Assistant Professor, Department of Commerce, GGV) Note: These

Model Answer/suggested solution Business Finance M. Com (1st Semester) Examination, 2013 Paper Code: AS-2368 * (Prepared by: Harish Khandelwal, Assistant Professor, Department of Commerce, GGV) Note: These

Lecture 13 Working Capital Management and Credit Issues

Lecture 13 - Working Capital Management Gross working capital: Net working capital: BASIC DEFINITIONS Total current assets. Net operating working capital (NOWC): Operating CA Operating CL = Current assets

Lecture 13 - Working Capital Management Gross working capital: Net working capital: BASIC DEFINITIONS Total current assets. Net operating working capital (NOWC): Operating CA Operating CL = Current assets

Short Term Finance and Planning. Sources and Uses of Cash

Short Term Finance and Planning (Text reference: Chapter 27) Topics sources and uses of cash operating cycle and cash cycle short term financial policy cash budgeting short term financial planning AFM

Short Term Finance and Planning (Text reference: Chapter 27) Topics sources and uses of cash operating cycle and cash cycle short term financial policy cash budgeting short term financial planning AFM

Chapter 14. 1 Copyright 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Chapter 14 1 Identify the purposes of the statement of cash flows Distinguish among operating, investing, and financing cash flows Prepare the statement of cash flows by the indirect method Identify noncash

Chapter 14 1 Identify the purposes of the statement of cash flows Distinguish among operating, investing, and financing cash flows Prepare the statement of cash flows by the indirect method Identify noncash

INTERNATIONAL ACCOUNTING STANDARDS. CIE Guidance for teachers of. 7110 Principles of Accounts and. 0452 Accounting

www.xtremepapers.com INTERNATIONAL ACCOUNTING STANDARDS CIE Guidance for teachers of 7110 Principles of Accounts and 0452 Accounting 1 CONTENTS Introduction...3 Use of this document... 3 Users of financial

www.xtremepapers.com INTERNATIONAL ACCOUNTING STANDARDS CIE Guidance for teachers of 7110 Principles of Accounts and 0452 Accounting 1 CONTENTS Introduction...3 Use of this document... 3 Users of financial

Financial. Management FOR A SMALL BUSINESS

Financial Management FOR A SMALL BUSINESS 1 Agenda Welcome, Pre-Test, Agenda, and Learning Objectives Benefits of Financial Management Budgeting Bookkeeping Financial Statements Business Financing Key

Financial Management FOR A SMALL BUSINESS 1 Agenda Welcome, Pre-Test, Agenda, and Learning Objectives Benefits of Financial Management Budgeting Bookkeeping Financial Statements Business Financing Key

Financial Statements

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

CASH FLOW STATEMENT. MODULE - 6A Analysis of Financial Statements. Cash Flow Statement. Notes

MODULE - 6A Cash Flow Statement 30 CASH FLOW STATEMENT In the previous lesson, you have learnt various types of analysis of financial statements and its tools such as comparative statements, common size

MODULE - 6A Cash Flow Statement 30 CASH FLOW STATEMENT In the previous lesson, you have learnt various types of analysis of financial statements and its tools such as comparative statements, common size

The Nature, Elements and Importance of Working Capital

C. WORKING CAPITAL MANAGEMENT 1. The nature, elements and importance of working capital 2. Management of inventories, accounts receivable, accounts payable and cash 3. Determining working capital needs

C. WORKING CAPITAL MANAGEMENT 1. The nature, elements and importance of working capital 2. Management of inventories, accounts receivable, accounts payable and cash 3. Determining working capital needs

Chapter 12 Forecasting and Short- Term Financial Planning

Chapter 12 Forecasting and Short- Term Financial Planning LEARNING OBJECTIVES 1. Understand the sources and uses of cash in building a cash budget. 2. Explain how companies use sales forecasts to predict

Chapter 12 Forecasting and Short- Term Financial Planning LEARNING OBJECTIVES 1. Understand the sources and uses of cash in building a cash budget. 2. Explain how companies use sales forecasts to predict

Having cash on hand is costly since you either have to raise money initially (for example, by borrowing from a bank) or, if you retain cash out of

or, if you retain cash out of") 1 Working capital refers to liquid funds used to purchase materials and pay workers. This is in contrast to long term capital such as buildings and machinery. Part of working capital management is cash

1 Working capital refers to liquid funds used to purchase materials and pay workers. This is in contrast to long term capital such as buildings and machinery. Part of working capital management is cash

1. Operating, Investment and Financial Cash Flows

1. Operating, Investment and Financial Cash Flows Solutions Problem 1 During 2005, Myears Oil Co. had gross sales of $1 000,000, cost of goods sold of $400,000, and general and selling expenses of $300,000.

1. Operating, Investment and Financial Cash Flows Solutions Problem 1 During 2005, Myears Oil Co. had gross sales of $1 000,000, cost of goods sold of $400,000, and general and selling expenses of $300,000.

Course 4: Managing Cash Flow

Excellence in Financial Management Course 4: Managing Cash Flow Prepared by: Matt H. Evans, CPA, CMA, CFM This course provides an introduction to cash flow management. This course is recommended for 2

Excellence in Financial Management Course 4: Managing Cash Flow Prepared by: Matt H. Evans, CPA, CMA, CFM This course provides an introduction to cash flow management. This course is recommended for 2

1. Planning - Establishing organizational goals and deciding how to accomplish them

1 : Understanding the Management Process Basic Management Functions 1. Planning - Establishing organizational goals and deciding how to accomplish them SWOT analysis - The identification and evaluation

1 : Understanding the Management Process Basic Management Functions 1. Planning - Establishing organizational goals and deciding how to accomplish them SWOT analysis - The identification and evaluation

FINANCIAL MANAGEMENT

100 Arbor Drive, Suite 108 Christiansburg, VA 24073 Voice: 540-381-9333 FAX: 540-381-8319 www.becpas.com Providing Professional Business Advisory & Consulting Services Douglas L. Johnston, II [email protected]

100 Arbor Drive, Suite 108 Christiansburg, VA 24073 Voice: 540-381-9333 FAX: 540-381-8319 www.becpas.com Providing Professional Business Advisory & Consulting Services Douglas L. Johnston, II [email protected]

Jackson Masonry loan relationship: A case in commercial bank lending

Jackson Masonry loan relationship: A case in commercial bank lending Steve A. Nenninger Sam Houston State University James B. Bexley Sam Houston State University ABSTRACT This case describes a series of

Jackson Masonry loan relationship: A case in commercial bank lending Steve A. Nenninger Sam Houston State University James B. Bexley Sam Houston State University ABSTRACT This case describes a series of

So You Want to Borrow Money to Start a Business?

So You Want to Borrow Money to Start a Business? M any small business owners cannot understand why a lending institution would refuse to lend them money. Others have no trouble getting money, but they

So You Want to Borrow Money to Start a Business? M any small business owners cannot understand why a lending institution would refuse to lend them money. Others have no trouble getting money, but they

Chapter. Working capital

Chapter 10 Working capital 1 10.1 Working capital Working capital is the capital available for conducting the day-to-day operations of the business and consists of current assets and current liabilities.

Chapter 10 Working capital 1 10.1 Working capital Working capital is the capital available for conducting the day-to-day operations of the business and consists of current assets and current liabilities.

CHAPTER 21. Working Capital Management

CHAPTER 21 Working Capital Management 1 Topics in Chapter Alternative working capital policies Cash, inventory, and A/R management Accounts payable management Short-term financing policies Bank debt and

CHAPTER 21 Working Capital Management 1 Topics in Chapter Alternative working capital policies Cash, inventory, and A/R management Accounts payable management Short-term financing policies Bank debt and

7 Management of Working Capital

7 Management of Working Capital UNIT I : MEANING, CONCEPT AND POLICIES OF WORKING CAPITAL Learning Objectives After studying this chapter you will be able to: Discuss in detail about working capital management,

7 Management of Working Capital UNIT I : MEANING, CONCEPT AND POLICIES OF WORKING CAPITAL Learning Objectives After studying this chapter you will be able to: Discuss in detail about working capital management,

STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL)

") Page 1 ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL) Complete these sample exam problems/objective questions and check your answers with the solutions at the end of the review file and identify where

Page 1 ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL) Complete these sample exam problems/objective questions and check your answers with the solutions at the end of the review file and identify where

Financial Statement Ratio Analysis

Management Accounting 319 Financial Statement Ratio Analysis Financial statements as prepared by the accountant are documents containing much valuable information. Some of the information requires little

Management Accounting 319 Financial Statement Ratio Analysis Financial statements as prepared by the accountant are documents containing much valuable information. Some of the information requires little

Understanding A Firm s Financial Statements

CHAPTER OUTLINE Spotlight: J&S Construction Company (http://www.jsconstruction.com) 1 The Lemonade Kids Financial statement (accounting statements) reports of a firm s financial performance and resources,

CHAPTER OUTLINE Spotlight: J&S Construction Company (http://www.jsconstruction.com) 1 The Lemonade Kids Financial statement (accounting statements) reports of a firm s financial performance and resources,

MARK SCHEME for the October/November 2011 question paper for the guidance of teachers 0452 ACCOUNTING. 0452/23 Paper 2, maximum raw mark 120

www.xtremepapers.com UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS International General Certificate of Secondary Education MARK SCHEME for the October/November question paper for the guidance of

www.xtremepapers.com UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS International General Certificate of Secondary Education MARK SCHEME for the October/November question paper for the guidance of

You have learnt about the financial statements

Analysis of Financial Statements 4 You have learnt about the financial statements (Income Statement and Balance Sheet) of companies. Basically, these are summarised financial reports which provide the

Analysis of Financial Statements 4 You have learnt about the financial statements (Income Statement and Balance Sheet) of companies. Basically, these are summarised financial reports which provide the

WORKING CAPITAL MANAGEMENT (FINANCE) UNIT I

UNIT I") WORKING CAPITAL MANAGEMENT (FINANCE) UNIT I Q. Explain Working Capital. What do you mean by Gross Working Capital and Net Working Capital? Ans. Introduction:- Working capital plays the same role in the

WORKING CAPITAL MANAGEMENT (FINANCE) UNIT I Q. Explain Working Capital. What do you mean by Gross Working Capital and Net Working Capital? Ans. Introduction:- Working capital plays the same role in the

In this chapter, we build on the basic knowledge of how businesses

03-Seidman.qxd 5/15/04 11:52 AM Page 41 3 An Introduction to Business Financial Statements In this chapter, we build on the basic knowledge of how businesses are financed by looking at how firms organize

03-Seidman.qxd 5/15/04 11:52 AM Page 41 3 An Introduction to Business Financial Statements In this chapter, we build on the basic knowledge of how businesses are financed by looking at how firms organize

FINANCIAL MANAGEMENT

STUDY MATERIAL:- FINANCIAL MANAGEMENT VERY SHORT QUESTIONS ( 1 MARK) 1 Define Financial Management. Ans financial management is that specialized activity which is responsible for obtaining and affectively

STUDY MATERIAL:- FINANCIAL MANAGEMENT VERY SHORT QUESTIONS ( 1 MARK) 1 Define Financial Management. Ans financial management is that specialized activity which is responsible for obtaining and affectively

Financial. Management FOR A SMALL BUSINESS

Financial Management FOR A SMALL BUSINESS Welcome 1. Agenda 2. Ground Rules 3. Introductions FINANCIAL MANAGEMENT 2 Objectives Explain the concept of financial management and its importance to a small

Financial Management FOR A SMALL BUSINESS Welcome 1. Agenda 2. Ground Rules 3. Introductions FINANCIAL MANAGEMENT 2 Objectives Explain the concept of financial management and its importance to a small

6. Show all your workings. icpar

CERTIFIED PUBLIC ACCOUNTANT FOUNDATION LEVEL 1 EXAMINATION F1.3: FINANCIAL ACCOUNTING MONDAY: 10 JUNE 2013 INSTRUCTIONS: 1. Time Allowed: 3 hours 15 minutes (15 minutes reading and 3 hours writing). 2.

CERTIFIED PUBLIC ACCOUNTANT FOUNDATION LEVEL 1 EXAMINATION F1.3: FINANCIAL ACCOUNTING MONDAY: 10 JUNE 2013 INSTRUCTIONS: 1. Time Allowed: 3 hours 15 minutes (15 minutes reading and 3 hours writing). 2.

Chapter 6 Statement of Cash Flows

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

For a balance sheet item, an asset increase is a Debit a liability increase is a Credit

1 CASH FLOW ANALYSIS 1.1 Introduction For a further discussion on cash flow, please refer to the guide to financial statements in the Learning Centre. The key to cashflow analysis is recognition of cashflow,

1 CASH FLOW ANALYSIS 1.1 Introduction For a further discussion on cash flow, please refer to the guide to financial statements in the Learning Centre. The key to cashflow analysis is recognition of cashflow,

CH 23 STATEMENT OF CASH FLOWS SELF-STUDY QUESTIONS

C H 2 3, P a g e 1 CH 23 STATEMENT OF CASH FLOWS SELF-STUDY QUESTIONS (note from Dr. N: I have deleted questions for you to omit, but did not renumber the remaining questions) 1. The primary purpose of

C H 2 3, P a g e 1 CH 23 STATEMENT OF CASH FLOWS SELF-STUDY QUESTIONS (note from Dr. N: I have deleted questions for you to omit, but did not renumber the remaining questions) 1. The primary purpose of

THE STATEMENT OF CASH FLOWS

THE STATEMENT OF CASH FLOWS Associate Professor PhD Cernusca Lucian University Aurel Vlaicu of Arad, [email protected] Professor PhD Mates Dorel, West University of Timisoara Abstract: In today

THE STATEMENT OF CASH FLOWS Associate Professor PhD Cernusca Lucian University Aurel Vlaicu of Arad, [email protected] Professor PhD Mates Dorel, West University of Timisoara Abstract: In today

Consolidated balance sheet

Consolidated balance sheet Non current assets 31/12/2009 31/12/2008 (*) 01/01/2008 (*) Property, plant and equipment 1,352 1,350 1,144 Investment property 7 11 11 Fixed assets held under concessions 13,089

Consolidated balance sheet Non current assets 31/12/2009 31/12/2008 (*) 01/01/2008 (*) Property, plant and equipment 1,352 1,350 1,144 Investment property 7 11 11 Fixed assets held under concessions 13,089

The Basic Framework of Budgeting

Master Budgeting 1 The Basic Framework of Budgeting A budget is a detailed quantitative plan for acquiring and using financial and other resources over a specified forthcoming time period. 1. The act of

Master Budgeting 1 The Basic Framework of Budgeting A budget is a detailed quantitative plan for acquiring and using financial and other resources over a specified forthcoming time period. 1. The act of

CASH FLOW STATEMENT. On the statement, cash flows are segregated based on source:

CASH FLOW STATEMENT On the statement, cash flows are segregated based on source: Operating activities: involve the cash effects of transactions that enter into the determination of net income. Investing

CASH FLOW STATEMENT On the statement, cash flows are segregated based on source: Operating activities: involve the cash effects of transactions that enter into the determination of net income. Investing

FINA351, Managerial Finance - Chapter 16 Notes WORKING CAPITAL. Involves current assets and liabilities in the operating cycle

FINA351, Managerial Finance - Chapter 16 Notes WORKING CAPITAL Involves current assets and liabilities in the operating cycle Is important for every business major to understand because: (1) it is where

FINA351, Managerial Finance - Chapter 16 Notes WORKING CAPITAL Involves current assets and liabilities in the operating cycle Is important for every business major to understand because: (1) it is where

Suggested layouts for financial statements in Accounting Courses National 5 and Higher

Suggested layouts for financial statements in Accounting Courses National 5 and Higher The following suggested layouts may be used when presenting financial statements in the Accounting Courses for National

Suggested layouts for financial statements in Accounting Courses National 5 and Higher The following suggested layouts may be used when presenting financial statements in the Accounting Courses for National

tutor2u Working Capital Introduction to the Management of Working Capital AS & A2 Business Studies PowerPoint Presentations 2005

Working Capital Introduction to the Management of Working Capital AS & A2 Business Studies PowerPoint Presentations 2005 Introduction All businesses need cash to survive Cash is needed to: Invest in fixed

Working Capital Introduction to the Management of Working Capital AS & A2 Business Studies PowerPoint Presentations 2005 Introduction All businesses need cash to survive Cash is needed to: Invest in fixed

Working Capital Management & Short Term Financing

CA BUSINESS SCHOOL POSTGRADUATE DIPLOMA IN BUSINESS & FINANCE SEMESTER 3: Financial Strategy Working Capital Management & Short Term Financing M B G Wimalarathna (FCA, FCMA, MCIM, FMAAT, MCPM)(MBA PIM/USJ)

CA BUSINESS SCHOOL POSTGRADUATE DIPLOMA IN BUSINESS & FINANCE SEMESTER 3: Financial Strategy Working Capital Management & Short Term Financing M B G Wimalarathna (FCA, FCMA, MCIM, FMAAT, MCPM)(MBA PIM/USJ)

1. A set of procedures for controlling cash payments by preparing and approving vouchers before payments are made is known as a voucher system.

Accounting II True/False Indicate whether the sentence or statement is true or false. 1. A set of procedures for controlling cash payments by preparing and approving vouchers before payments are made is

Accounting II True/False Indicate whether the sentence or statement is true or false. 1. A set of procedures for controlling cash payments by preparing and approving vouchers before payments are made is

Sri Lanka Accounting Standard-LKAS 7. Statement of Cash Flows

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

Management of Working Capital

7 Management of Working Capital UNIT I : MEANING, CONCEPT AND POLICIES OF WORKING CAPITAL Learning Objectives After studying this chapter you will be able to: Discuss in detail about working capital management,

7 Management of Working Capital UNIT I : MEANING, CONCEPT AND POLICIES OF WORKING CAPITAL Learning Objectives After studying this chapter you will be able to: Discuss in detail about working capital management,

½ a mark for rounding up (6 marks) (b) There are a number of costs to the business associated with holding inventory:

(b) There are a number of costs to the business associated with holding inventory:") EDI LCCI IQ ON DEMAND AWARD IN BUSINESS FINANCE AND BANKING OPERATIONS SAMPLE LEVEL 4 MARKING SCHEME DISTINCTION MARK 75% CREDIT MARK 60% PASS MARK 50% TOTAL 100 MARKS QUESTION 1 (a) Inventory days Receivable

EDI LCCI IQ ON DEMAND AWARD IN BUSINESS FINANCE AND BANKING OPERATIONS SAMPLE LEVEL 4 MARKING SCHEME DISTINCTION MARK 75% CREDIT MARK 60% PASS MARK 50% TOTAL 100 MARKS QUESTION 1 (a) Inventory days Receivable

CHAPTER 4. Final Accounts

CHAPTER 4 Final Accounts Meaning Preparation of final account is the last stage of the accounting cycle. The basic objective of every concern maintaining the book of accounts is to find out the profit

CHAPTER 4 Final Accounts Meaning Preparation of final account is the last stage of the accounting cycle. The basic objective of every concern maintaining the book of accounts is to find out the profit

B Exercises 4-1. (d) Intangible assets. (i) Paid-in capital in excess of par.

Intangible assets. (i) Paid-in capital in excess of par.") B Exercises E4-1B (Balance Sheet Classifications) Presented below are a number of balance sheet accounts of Castillo Inc. (a) Trading Securities. (h) Warehouse in Process of Construction. (b) Work in Process.

B Exercises E4-1B (Balance Sheet Classifications) Presented below are a number of balance sheet accounts of Castillo Inc. (a) Trading Securities. (h) Warehouse in Process of Construction. (b) Work in Process.

B. Division of Costs The purpose of a Manufacturing Account is to ascertain Cost of Production ( ).

.") Manufacturing Accounts ( ) S5 Manufacturing Account/LWL A. Function of a Manufacturing Acccount For those businesses which deal with manufacturing products. It is common in today s business to act both

Manufacturing Accounts ( ) S5 Manufacturing Account/LWL A. Function of a Manufacturing Acccount For those businesses which deal with manufacturing products. It is common in today s business to act both

ICAP GROUP S.A. FINANCIAL RATIOS EXPLANATION

ICAP GROUP S.A. FINANCIAL RATIOS EXPLANATION OCTOBER 2006 Table of Contents 1. INTRODUCTION... 3 2. FINANCIAL RATIOS FOR COMPANIES (INDUSTRY - COMMERCE - SERVICES) 4 2.1 Profitability Ratios...4 2.2 Viability

ICAP GROUP S.A. FINANCIAL RATIOS EXPLANATION OCTOBER 2006 Table of Contents 1. INTRODUCTION... 3 2. FINANCIAL RATIOS FOR COMPANIES (INDUSTRY - COMMERCE - SERVICES) 4 2.1 Profitability Ratios...4 2.2 Viability

Management of Working Capital

International Journal of Computer Science & Management Studies, Vol. 13, Issue 03, May 2013 Management of Working Capital Arti Rani Assistant Professor Kanya Mahavidhyalya, Kharkhoda, Sonepat, Haryana

International Journal of Computer Science & Management Studies, Vol. 13, Issue 03, May 2013 Management of Working Capital Arti Rani Assistant Professor Kanya Mahavidhyalya, Kharkhoda, Sonepat, Haryana

Accounting and Reporting Policy FRS 102. Staff Education Note 1 Cash flow statements

Staff Education Note 1: Cash flow Statements Accounting and Reporting Policy FRS 102 Staff Education Note 1 Cash flow statements Disclaimer This Education Note has been prepared by FRC staff for the convenience

Staff Education Note 1: Cash flow Statements Accounting and Reporting Policy FRS 102 Staff Education Note 1 Cash flow statements Disclaimer This Education Note has been prepared by FRC staff for the convenience

CASH FLOW STATEMENT (AND FINANCIAL STATEMENT)

") CASH FLOW STATEMENT (AND FINANCIAL STATEMENT) - At the most fundamental level, firms do two different things: (i) They generate cash (ii) They spend it. Cash is generated by selling a product, an asset

CASH FLOW STATEMENT (AND FINANCIAL STATEMENT) - At the most fundamental level, firms do two different things: (i) They generate cash (ii) They spend it. Cash is generated by selling a product, an asset

3,000 3,000 2,910 2,910 3,000 3,000 2,940 2,940

1. David Company uses the gross method to record its credit purchases, and it uses the periodic inventory system. On July 21, 20D, the company purchased goods that had an invoice price of $ with terms

1. David Company uses the gross method to record its credit purchases, and it uses the periodic inventory system. On July 21, 20D, the company purchased goods that had an invoice price of $ with terms

This week its Accounting and Beyond

This week its Accounting and Beyond Monday Morning Session Introduction/Accounting Cycle Afternoon Session Tuesday The Balance Sheet Wednesday The Income Statement The Cash Flow Statement Thursday Tools

This week its Accounting and Beyond Monday Morning Session Introduction/Accounting Cycle Afternoon Session Tuesday The Balance Sheet Wednesday The Income Statement The Cash Flow Statement Thursday Tools

Chapter Sources of Short-Term Financing

Chapter Sources of Short-Term Financing Chapter 8 - Outline PPT 8-2 Sources of Short-Term Financing Trade Credit from Suppliers Net Credit Position Chartered Banks in Canada Types of Short-term Loans Interest

Chapter Sources of Short-Term Financing Chapter 8 - Outline PPT 8-2 Sources of Short-Term Financing Trade Credit from Suppliers Net Credit Position Chartered Banks in Canada Types of Short-term Loans Interest

Business Plan. In completing the following proposal provide as much detailed information as possible.

Business Plan A business plan is an integral part of a financing request. It is an introduction to your business, and it provides us with the initial information that we require to start to an application.

Business Plan A business plan is an integral part of a financing request. It is an introduction to your business, and it provides us with the initial information that we require to start to an application.

Management Accounting and Decision-Making

Management Accounting 15 Management Accounting and Decision-Making Management accounting writers tend to present management accounting as a loosely connected set of decision making tools. Although the

Management Accounting 15 Management Accounting and Decision-Making Management accounting writers tend to present management accounting as a loosely connected set of decision making tools. Although the

Analyzing the Statement of Cash Flows

Analyzing the Statement of Cash Flows Operating Activities NACM Upstate New York Credit Conference 2015 By Ron Sereika, CCE,CEW NACM 1 Objectives of this Educational Session u Show how the statement of

Analyzing the Statement of Cash Flows Operating Activities NACM Upstate New York Credit Conference 2015 By Ron Sereika, CCE,CEW NACM 1 Objectives of this Educational Session u Show how the statement of

HOW TO IMPROVE THE WORKING CAPITAL OF A COMPANY

Volume 3, Issue 5 (May, 2014) Online ISSN-2277-1166 Published by: Abhinav Publication Abhinav National Monthly Refereed Journal of Research in HOW TO IMPROVE THE WORKING CAPITAL OF A COMPANY Hemanshu Kapadia

Volume 3, Issue 5 (May, 2014) Online ISSN-2277-1166 Published by: Abhinav Publication Abhinav National Monthly Refereed Journal of Research in HOW TO IMPROVE THE WORKING CAPITAL OF A COMPANY Hemanshu Kapadia

CENTRE FOR CONTINUING EDUCATION BBA (AVIATION OPERATION)

") CENTRE FOR CONTINUING EDUCATION BBA (AVIATION OPERATION) BATCH: SEMESTER: NAME: ROLL NO: ASSIGNMENT 1 & 2 FOR BUSINESS ACCOUNTING BBCF 131 UNIVERSITY OF PETROLEUM & ENERGY STUDIES Assignment-1 Note: All

CENTRE FOR CONTINUING EDUCATION BBA (AVIATION OPERATION) BATCH: SEMESTER: NAME: ROLL NO: ASSIGNMENT 1 & 2 FOR BUSINESS ACCOUNTING BBCF 131 UNIVERSITY OF PETROLEUM & ENERGY STUDIES Assignment-1 Note: All

CHAPTER 26. Working Capital Management. Chapter Synopsis

CHAPTER 26 Working Capital Management Chapter Synopsis 26.1 Overview of Working Capital Any reduction in working capital requirements generates a positive free cash flow that the firm can distribute immediately

CHAPTER 26 Working Capital Management Chapter Synopsis 26.1 Overview of Working Capital Any reduction in working capital requirements generates a positive free cash flow that the firm can distribute immediately

Working Capital. Learning Objectives. By the end of this chapter, you should be able to: List the five objectives of financial management.

Working Capital Learning Objectives By the end of this chapter, you should be able to: List the five objectives of financial management. Explain the operation of the operating cycle. Define the term net

Working Capital Learning Objectives By the end of this chapter, you should be able to: List the five objectives of financial management. Explain the operation of the operating cycle. Define the term net

Financial Ratios and Quality Indicators

Financial Ratios and Quality Indicators From U.S. Small Business Administration Online Women's Business Center If you monitor the ratios on a regular basis you'll gain insight into how effectively you

Financial Ratios and Quality Indicators From U.S. Small Business Administration Online Women's Business Center If you monitor the ratios on a regular basis you'll gain insight into how effectively you

On January 1, 2005, retailing giant Wal-Mart began requiring. Short-Term Financial Planning PART EIGHT SHORT-TERM FINANCIAL MANAGEMENT

SHORT-TERM FINANCIAL MANAGEMENT On January 1, 2005, retailing giant Wal-Mart began requiring its 100 largest suppliers to put radio-frequency identification (RFID) tags on cases and pallets shipped to

SHORT-TERM FINANCIAL MANAGEMENT On January 1, 2005, retailing giant Wal-Mart began requiring its 100 largest suppliers to put radio-frequency identification (RFID) tags on cases and pallets shipped to

CPD Spotlight Quiz September 2012. Working Capital

CPD Spotlight Quiz September 2012 Working Capital 1 What is working capital? This is a topic that has been the subject of debate for many years and will, no doubt, continue to be so. One response to the

CPD Spotlight Quiz September 2012 Working Capital 1 What is working capital? This is a topic that has been the subject of debate for many years and will, no doubt, continue to be so. One response to the

Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows

7 Statement of Cash Flows") Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

Working Capital Management

Working Capital Management Gitman and Hennessey, Chapter 14 Spring 2004 14.1 Net Working Capital Fundamentals In 2002, current assets accounted for 31.7% of non-financial Canadian corporations total assets.

Working Capital Management Gitman and Hennessey, Chapter 14 Spring 2004 14.1 Net Working Capital Fundamentals In 2002, current assets accounted for 31.7% of non-financial Canadian corporations total assets.

Working Capital Management

Working Capital Management Gitman and Hennessey, Chapter 14 Spring 2004 14.1 Net Working Capital Fundamentals In 2002, current assets accounted for 31.7% of non-financial Canadian corporations total assets.

Working Capital Management Gitman and Hennessey, Chapter 14 Spring 2004 14.1 Net Working Capital Fundamentals In 2002, current assets accounted for 31.7% of non-financial Canadian corporations total assets.

Grade 10 Accounting Notes SET 2: Basics Cash Retail Business Cash Transactions. Name: JCansfield Page 1 of 27

Grade 10 Accounting Notes SET 2: Basics Cash Retail Business Cash Transactions Name: JCansfield Page 1 of 27 Accounting Cycle The Accounting cycle takes place over 12 months. We refer to this as the Financial

Grade 10 Accounting Notes SET 2: Basics Cash Retail Business Cash Transactions Name: JCansfield Page 1 of 27 Accounting Cycle The Accounting cycle takes place over 12 months. We refer to this as the Financial

STATE BANK OF INDIA BRANCH. Interview Form For Loans above Rs.25,000/- (To be submitted to the Sanctioning Authority along with the Application Form)

") Annexure-SBF/3 STATE BANK OF INDIA BRANCH SMALL BUSINESS FINANCE Interview Form For Loans above 25,000/- (To be submitted to the Sanctioning Authority along with the Application Form) To be used for :

Annexure-SBF/3 STATE BANK OF INDIA BRANCH SMALL BUSINESS FINANCE Interview Form For Loans above 25,000/- (To be submitted to the Sanctioning Authority along with the Application Form) To be used for :

v. Other things held constant, which of the following will cause an increase in working capital?

Net working capital i. Net working capital may be defined as current assets minus current liabilities. This also defines the current ratio. Motives for holding cash ii. Firms hold cash balances in order

Net working capital i. Net working capital may be defined as current assets minus current liabilities. This also defines the current ratio. Motives for holding cash ii. Firms hold cash balances in order

Accounting 201 Comprehensive Practice Exam 2C Page 1

Accounting 201 Comprehensive Practice Exam 2C Page 1 1. A business organized as a corporation a. is not a separate legal entity in most states. b. requires that stockholders be personally liable for the

Accounting 201 Comprehensive Practice Exam 2C Page 1 1. A business organized as a corporation a. is not a separate legal entity in most states. b. requires that stockholders be personally liable for the

Chapter. Statement of Cash Flows For Single Company

Chapter 4 Statement of Cash Flows For Single Company 4.1 Single company statement of cash flows Statement of cash flows are primary financial statements and are required along side the income statement

Chapter 4 Statement of Cash Flows For Single Company 4.1 Single company statement of cash flows Statement of cash flows are primary financial statements and are required along side the income statement

RENAISSANCE ENTREPRENEURSHIP CENTER First Finance Class (FIN-1)

") Finance 1 (FIN-1) RENAISSANCE ENTREPRENEURSHIP CENTER (FIN-1) Learning Outcomes At the conclusion of this class, you should: Know what will be covered in the six finance class sessions. Have reviewed some

Finance 1 (FIN-1) RENAISSANCE ENTREPRENEURSHIP CENTER (FIN-1) Learning Outcomes At the conclusion of this class, you should: Know what will be covered in the six finance class sessions. Have reviewed some

Summary of Financial Report for the FY ending March 2015 (Non-Consolidated)

") Summary of Financial Report for the FY ending March 2015 (Non-Consolidated) April 30, 2015 Listed Company Name: Japan Tissue Engineering Co., Ltd. Listed Securities Exchange: JQ Stock Code: 7774 URL http://www.jpte.co.jp

Summary of Financial Report for the FY ending March 2015 (Non-Consolidated) April 30, 2015 Listed Company Name: Japan Tissue Engineering Co., Ltd. Listed Securities Exchange: JQ Stock Code: 7774 URL http://www.jpte.co.jp

6. Financial Planning. Break-even. Operating and Financial Leverage.

6. Financial Planning. Break-even. Operating and Financial Leverage. Financial planning primarily involves anticipating the impact of operating, investment and financial decisions on the firm s future

6. Financial Planning. Break-even. Operating and Financial Leverage. Financial planning primarily involves anticipating the impact of operating, investment and financial decisions on the firm s future

MASTER BUDGET - EXAMPLE

MASTER BUDGET - EXAMPLE Sales IN UNITS for the previous two months (of last quarter), as well as the sales forecast for next quarter are as follows: Sales Budget Units May sales (ACTUAL) 20 June sales

MASTER BUDGET - EXAMPLE Sales IN UNITS for the previous two months (of last quarter), as well as the sales forecast for next quarter are as follows: Sales Budget Units May sales (ACTUAL) 20 June sales

Short-term Financial Planning and Management.

Short-term Financial Planning and Management. This topic discusses the fundamentals of short-term nancial management; the analysis of decisions involving cash ows which occur within a year or less. These

Short-term Financial Planning and Management. This topic discusses the fundamentals of short-term nancial management; the analysis of decisions involving cash ows which occur within a year or less. These

Topic 4 Working Capital Management. 1. Concept of Working Capital 2. Measuring Working Capital and Net Working Capital. 4.

Topic 4 Working Capital Management 1. Concept of Working Capital 2. Measuring Working Capital and Net Working Capital 3. Optimization i i of Working Capital 4. Applications 80 Learning objectives This

Topic 4 Working Capital Management 1. Concept of Working Capital 2. Measuring Working Capital and Net Working Capital 3. Optimization i i of Working Capital 4. Applications 80 Learning objectives This