Guide to Financial Statements Study Guide

|

|

|

- Shannon Phelps

- 10 years ago

- Views:

Transcription

1 Guide to Financial Statements Study Guide Overview (Topic 1) Three major financial statements: The Income Statement The Balance Sheet The Cash Flow Statement Objectives: Explain the underlying equation of each statement. Understand the structure and purpose of each statement. Why are they important? (Topic 2) (Slide 1) Financial statements provide information about a company s financial health. Managers use them to strategize and identify areas that require their intervention. Shareholders use them to ensure their capital is well managed Outside investors use them to identify opportunities. Lenders and suppliers use them to assess the creditworthiness of businesses they plan to deal with. The government uses them for tax-collection and regulation purposes. (Slide 2) Understanding financial statements is important when Making sound investment decisions Dealing with companies Managing a department Starting your own business Managing your personal finances Taking a job with a company 1

2 (Slide 3) Financial statements are commonly provided together, as part of a company s annual report. You will often need to look at all three statements to fully answer a question or make a decision. Income Statement (Topic 4) (Slide 1) The Income Statement: Specifies the financial results of a business over a defined period of time - usually a month, a quarter, or a fiscal year. States whether a business is making a profit or not. (Slide 2) Underlying equation: Revenues - Expenses = Profit/Loss (Net Income) (Slide 3) (SAMPLE INCOME STATEMENT: Page 15) Sales/Revenue: Includes money generated by the company by selling its products or services to customers Sometimes referred to as sales Only includes revenue associated with the company s main operations (Slide 4) Expense Categories: 1. Cost of Goods Sold 2. Operating Expenses (including depreciation) 3. Interest Expense 4. Income Tax 2

Underlying equation: Revenues - Expenses = Profit/Loss (Net Income) (Slide 3) (SAMPLE INCOME STATEMENT: Page 15) Sales/Revenue: Includes money generated by the company by selling its")

3 (Slide 5) The income statement in addition to the balance sheet follows the accrual accounting system. Accrual Accounting: Revenues are recorded when earned and expenses are recorded when incurred. Therefore, earned revenues may include sales on credit for which the company has yet to receive cash and expenses may include bills the company has not yet paid. (Slide 7) Cost of Goods Sold: Includes all expenses directly related to making and storing a company's goods Examples: raw materials, warehousing, direct labor costs Service companies do not have this section on their income statements, since they don t produce products. By deducting cost of goods sold from sales/revenue you arrive at gross profit. (Slide 8) Operating Expenses: Include all costs incurred in operating the business that are not directly related to the production and storage of a company's goods. Examples: administrative salaries, research and development expenses, marketing costs (Slide 9) Cost of Goods Sold vs. Operating Expenses: If an expense can be eliminated without affecting the production and storage of the company s products, then it's an operating expense and not part of the cost of goods sold. 3

4 (Slides 11-13) Depreciation: Listed with operating expenses on the income statement. Instead of including the full price of a fixed (longterm) asset under operating expenses, its cost is spread over the years it will be used and listed under depreciation. The reason: The asset will benefit the company for several years not just during the year it was purchased. Without depreciation, a company would be overstating its first-year expenses and understating its expenses over the following years during which the asset is used. (Slide 14) By subtracting operating expenses and depreciation from gross profit, you arrive at operating earnings. These earnings are also called earnings before interest and taxes, or EBIT for short. (Slide 15) Many companies and investors look at the ratio of EBIT to revenues as a measurement of profitability. EBIT Sales X 100 = % Revenue that is Operating Earnings Companies use this number to compare changes in their profitability over time and to compare their profitability to other companies in their industry. If the percentage is smaller than a competitor, it means the company is less profitable; if it is bigger, then the company is more profitable. (Slide 16) Interest Expense interest paid by the company for loans it incurred Income Tax tax levied by the government for income 4

5 REVENUE EXPENSES = NET INCOME Net Profit: Revenue/Sales > Expenses Net Loss: Revenue/Sales < Expenses (Slide 17) OVERVIEW: Sales/Revenue Cost of Goods Sold = Gross Profit Operating Expenses Depreciation = Operating Earnings (EBIT) Interest Expense Interest Expense = NET INCOME (Slide 19) Income Statement: Equation: Revenues - Expenses = Profit/Loss Summarizes the financial results of a business over a fixed period of time. Tells whether a company is making a profit or not Can help spot trends and turnarounds when compared to previous periods 5

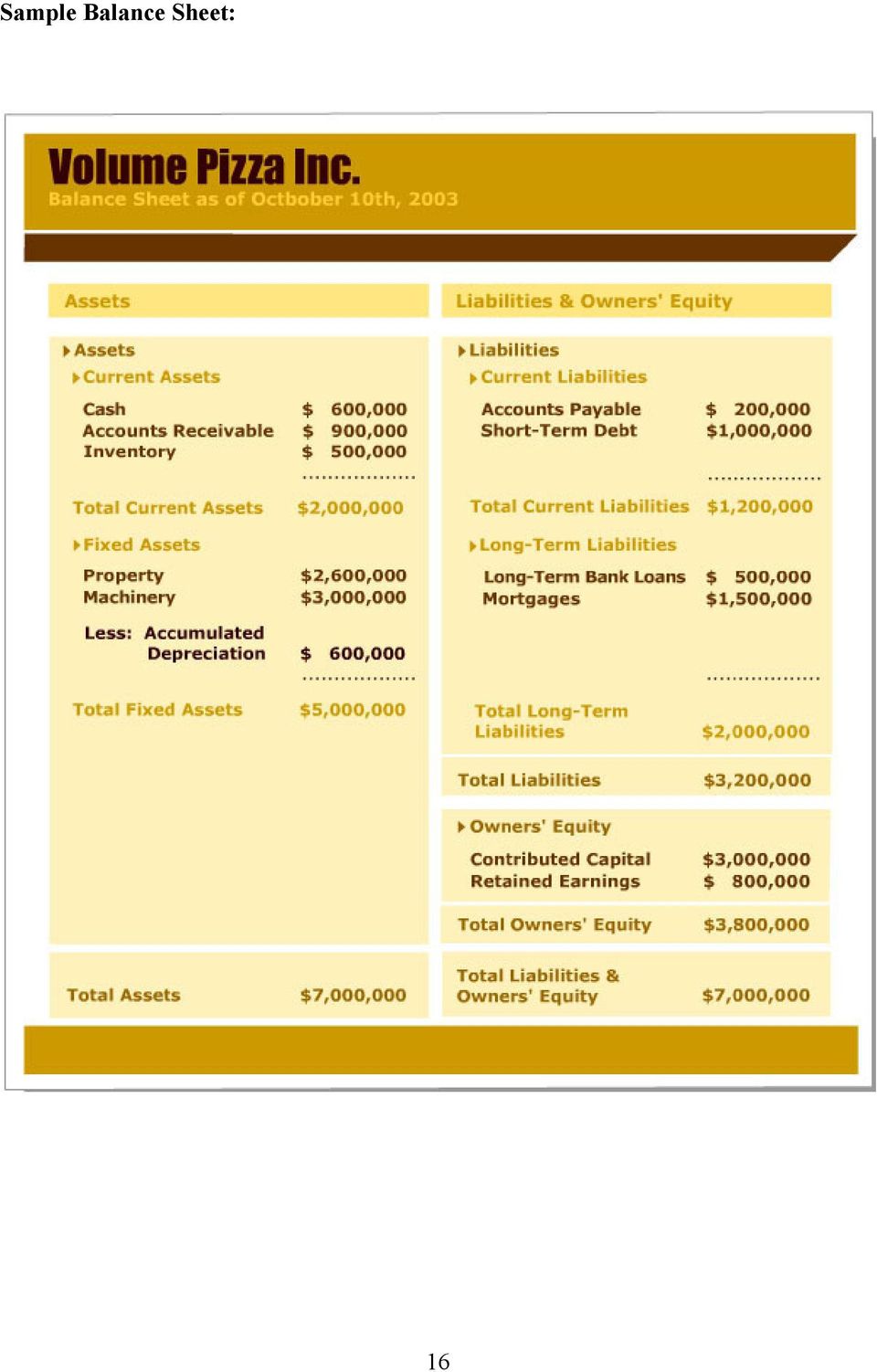

6 Balance Sheet (Topic 6) (Slide 1) The Balance Sheet: Gives a snapshot of a company's financial situation at a particular point in time Is usually prepared at the end of a month, quarter, or fiscal year. Lists the company's different assets and how they have been funded - with the capital of creditors (liabilities), with the capital of the owners (equity), or with both. (Slide 2) Underlying equation: Assets = Liabilities + Owners' Equity (Slide 3) Assets include the value of everything a company uses to conduct business, such as cash, equipment, land, inventories, office equipment, and money owed to the company by customers and clients. Liabilities include existing debts a company owes to its creditors and lenders. Owners' Equity equals assets minus liabilities and represents the part of the company owned by its owners or shareholders. (if a company has $4 million in assets and $3 million in liabilities, it has $1 million in owners' equity.) (Slide 4) Example of the balance between assets and liabilities/owners equity: If a company buys $2 million worth of inventory with payment due in 60 days, assets increases by $2 million and liabilities also increase by $2 million. Once the company pays for the inventory, assets (cash) and current liabilities will, then, both be reduced by $2 million. (Slide 6) (SAMPLE INCOME STATEMENT: Page 16) 6

7 Assets are listed on the left side of the balance sheet and are generally organized into two categories: Current Assets: Assets the company plans to convert to cash, sell, or use during the coming year Examples: cash, accounts receivable, inventory on hand Fixed Assets Assets that the company does not plan to turn into cash within one year or that would take longer than one year to convert Examples: property, plants, machinery, patents (Slide 7) Again, like in the income statement, the company must account for the depreciating value of its assets. Accumulated depreciation is deducted from fixed assets. (Slide 9) Liabilities and owners' equity are listed on the right side of the balance sheet. Liabilities are generally organized into two categories: Current Liabilities: Money the company expected to pay within one year Examples: accounts payable and short-term borrowings Long-term Liabilities Money the company needed to pay back in one or more years Examples: long-term bank loans, mortgages, bonds (Slide 11) Owners' Equity (all assets minus all liabilities) represents the part of the company owned by its shareholders and is generally organized into two categories: Contributed Capital capital invested by a company's owners/shareholders Retained Earnings earnings reinvested in the business after all dividends were paid 7

Liabilities and owners' equity are listed on the right side of the balance sheet.")

8 (Slide 14) OVERVIEW: Balance Sheet: Equation: Assets = Liabilities + Owners' Equity Provides a snapshot of a company's balance between its assets, liabilities and owners' equity at a specific point in time. Cash Flow Statement (Topic 12) (Slide 1) The Cash Flow Statement: Records a company s cash inflows and cash outflows over a defined period of time Usually derived from the income statement and balance sheet. Shows where the company s cash originated, how the company used its cash, and if the company has enough cash to return its loans and continue to operate. (Slide 2) Important Difference from Other Two Statements: The income statement and balance sheet follow the accrual basis of accounting, where revenues are recorded when earned (whether or not cash was received) and expenses are recorded when incurred (whether or not they have been paid). The cash flow statement follows the cash basis of accounting where only actual cash inflows and outflows are recorded. (Slide 4) (SAMPLE CASH FLOW STATEMENT: Page17) Three sections of cash flow statement: 1. Operating Cash Flow 2. Investing Cash Flow 3. Financing Cash Flow 8

9 Underlying equation: Net cash provided or used by operating activities + Net cash provided or used by investing activities + Net cash provided or used by financing activities = Total net increase or decrease in cash + Beginning cash balance = Ending cash balance (Slide 5) Operating Cash Flow: Includes cash generated by and required for the daily operations of a business Inflow Example: cash received from the sale of products or services Outflow Example: payments to suppliers, salaries to employees, rents, taxes Operating cash inflows minus operating cash outflows equal net operating cash flow. Methods for calculating net operating cash flow: (1) The Indirect Method (most widely used) (2) The Direct Method (Slide 6) Indirect Method adding and subtracting non-cash revenues and expenses from net income Net income must be adjusted for the cash flow statement because, on the income statement, it was calculated under the accrual basis of accounting and, thus, non-cash items such accounts receivable were included in calculating it. Non-cash items requiring adjustment under the indirect method usually fall into three categories: 1. Depreciation, depletion, and amortization 2. Gains and losses on the sale of fixed assets, such as equipment 3. Changes in current non-cash assets liabilities, such as accounts receivable and accounts payable 9

10 (Slide 7) Depreciation, depletion, and amortization Example: Depreciation Depreciation is a non-cash expense deducted to arrive at net income. Therefore, we must add depreciation back to net income to arrive at net operating cash flow. (Slide 8) Gains and losses on the sale of fixed assets, such as equipment Example: Non-cash gain from the sale of equipment When a company sells a fixed asset, it records the gain or loss from the sale on the income statement under a special category called other revenues/expenses. If the sale was non-cash (e.g. on credit), then we must now deduct this amount to adjust net income to a cash basis system. (Slide 10) Changes in current non-cash assets liabilities Example 1: Accounts Receivable (A/R) A/R represents uncollected revenues that are included as revenue on the income statement. Any increase in A/R over the period needs to be deducted from net income on the cash flow statement. Any decrease in A/R over the period needs to be added back to net income on the cash flow statement. (Slide 12) Example 2: Accounts Payable (A/P) A/P represents expenses not yet paid that are included as expenses on the income statement. Any increase in A/P over the period needs to be added back to net income on the cash flow statement. Any decrease in A/P needs to be deducted from net income on the cash flow statement. (Slide 14) 10

, then we must now deduct this amount to adjust net income to a cash basis system.")

11 (Slide 16) Direct Method adjusting each item on the income statement from an accrual basis to a cash basis. (Slide 17) Investing Cash Flow: Includes cash used for investing in long-term assets and cash received from the sale of such investments Inflow Examples: sale of property, debt, or equity Outflow Examples: purchase of property/equipment, loans made to other entities (Slide 18) Financing Cash Flow: Includes cash paid to or received from external sources such as lenders, investors, and shareholders Inflow Examples: include issuance of bonds, issuance of stock, bank loans Outflow Examples: dividends paid, payment of loans (Slide 19) Net operating cash flow + Net investing cash flow + Net financing cash flow = Net Cash Flow Net cash flow should equal the difference between the amounts of cash listed on the balance sheets from the beginning and the ending the period. (Slide 20) Net Cash Flow + Beginning cash balance = Ending cash balance (Slide 22) OVERVIEW: Cash Flow Statement: Tells you how much cash the company has generated and spent over a specific period of time 11

Net operating cash flow + Net investing cash flow")

12 Finding Financial Statements (Topic 12) (Slide 1) All publicly traded companies in the U.S. are required by the SEC to distribute their annual reports to their investors and make them available to the public. (Slide 2) Resources for finding financial statements: 1. The SEC website allows you to search and view the annual reports of all U.S. publicly traded companies through its EDGAR database. To search for a company s annual report: 1. Go to the SEC home page and click on Search for Company Filings. 2. Choose Companies & Other Filers. 3. Type the name of the company in which you are interested. 4. Click Find Companies. 5. (Type 10-K to view the most recent annual report.) (Slide 3) 2. The Company s Website most publicly traded companies make their reports available online under the Investor Relations section of their website. (Slide 4) 3. Thomson Research - as a student at Baruch you have access to Thomson Research through the library s website. This database is unique because: It includes historical SEC filings not included in EDGAR. It allows you to view only the parts of the report in which you are interested. It allows you to download the filing as a word document, PDF file, or Excel spreadsheet. 12

(Slide 3) 2.")

13 To search this database: 1. Type the name of the company in which you are interested. 2. Choose the type of report you want to view. Ethics in Accounting (Topic 13) (Slide 1) It is the responsibility of corporations to ensure that financial integrity and investor trust are upheld. (Slide 2) Enron is an example of what can happen when a company does not meet this responsibility. One of the world's leading energy, commodities, and services companies America's 7th largest company, employing 21,000 staff in more than 40 countries Admitted to overstating company value in financial statements by $1.2 billion Accused of concealing debts and not listing them on the company's financial statements (Slide 3) Investors and creditors withdrew from the company. The company declared bankruptcy. Thousands of employees lost their jobs and retirement accounts. Enron stockholders lost billions of dollars. New government regulations, such as the Sarbanes- Oxley Act, were passed by the U.S. government. (Slide 4) Professional accounting organizations such as AICPA require members to follow a code of conduct to maintain the public s confidence in the accounting industry. (Slide 5) Through the Robert Zicklin Center for Corporate Integrity, Baruch College is committed to introducing students to the important issue of ethics in financial reporting. 13

14 Conclusion (Topic 14) (Slide 1) The income statement tells you the bottom line over a specific period of time. Is the company turning out a profit or a loss? The balance sheet gives you a snapshot of a company's financial situation (its assets, liabilities, and owners' equity) at a particular point in time. The cash flow statement tells you how much cash the company possesses and its sources and uses of cash. 14

at a particular point in time.")

15 Sample Income Statement: 15

16 Sample Balance Sheet: 16

17 Sample Cash Flow Statement: 17

CH 23 STATEMENT OF CASH FLOWS SELF-STUDY QUESTIONS

C H 2 3, P a g e 1 CH 23 STATEMENT OF CASH FLOWS SELF-STUDY QUESTIONS (note from Dr. N: I have deleted questions for you to omit, but did not renumber the remaining questions) 1. The primary purpose of

C H 2 3, P a g e 1 CH 23 STATEMENT OF CASH FLOWS SELF-STUDY QUESTIONS (note from Dr. N: I have deleted questions for you to omit, but did not renumber the remaining questions) 1. The primary purpose of

Chapter 6 Statement of Cash Flows

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Understanding A Firm s Financial Statements

CHAPTER OUTLINE Spotlight: J&S Construction Company (http://www.jsconstruction.com) 1 The Lemonade Kids Financial statement (accounting statements) reports of a firm s financial performance and resources,

CHAPTER OUTLINE Spotlight: J&S Construction Company (http://www.jsconstruction.com) 1 The Lemonade Kids Financial statement (accounting statements) reports of a firm s financial performance and resources,

In this chapter, we build on the basic knowledge of how businesses

03-Seidman.qxd 5/15/04 11:52 AM Page 41 3 An Introduction to Business Financial Statements In this chapter, we build on the basic knowledge of how businesses are financed by looking at how firms organize

03-Seidman.qxd 5/15/04 11:52 AM Page 41 3 An Introduction to Business Financial Statements In this chapter, we build on the basic knowledge of how businesses are financed by looking at how firms organize

COMPONENTS OF THE STATEMENT OF CASH FLOWS

ILLUSTRATION 24-1 OPERATING, INVESTING, AND FINANCING ACTIVITIES COMPONENTS OF THE STATEMENT OF CASH FLOWS CASH FLOWS FROM OPERATING ACTIVITIES + Sales and Service Revenue Received Cost of Sales Paid Selling

ILLUSTRATION 24-1 OPERATING, INVESTING, AND FINANCING ACTIVITIES COMPONENTS OF THE STATEMENT OF CASH FLOWS CASH FLOWS FROM OPERATING ACTIVITIES + Sales and Service Revenue Received Cost of Sales Paid Selling

Cash is King. cash flow is less likely to be affected

Reading 27: Understanding Cash Flow Statements Relevance of Cash Flow The primary purpose of the statement of cash flows (SCF) is to provide: Info about a firm s cash receipts & cash payments during an

Reading 27: Understanding Cash Flow Statements Relevance of Cash Flow The primary purpose of the statement of cash flows (SCF) is to provide: Info about a firm s cash receipts & cash payments during an

STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

Financial Statements Tutorial

Financial Statement Review: Financial Statements Tutorial There are four major financial statements used to communicate information to external users (creditors, investors, suppliers, etc.) - 1. Balance

Financial Statement Review: Financial Statements Tutorial There are four major financial statements used to communicate information to external users (creditors, investors, suppliers, etc.) - 1. Balance

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased.

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased. Accounts Receivable are the total amounts customers owe your business for goods or services sold

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased. Accounts Receivable are the total amounts customers owe your business for goods or services sold

CASH FLOW STATEMENT (AND FINANCIAL STATEMENT)

") CASH FLOW STATEMENT (AND FINANCIAL STATEMENT) - At the most fundamental level, firms do two different things: (i) They generate cash (ii) They spend it. Cash is generated by selling a product, an asset

CASH FLOW STATEMENT (AND FINANCIAL STATEMENT) - At the most fundamental level, firms do two different things: (i) They generate cash (ii) They spend it. Cash is generated by selling a product, an asset

Financial Statements

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods TABLE OF CONTENTS

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods 1.0 FINANCIAL FORECASTING METHODS 1.01 Introduction

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods 1.0 FINANCIAL FORECASTING METHODS 1.01 Introduction

Reporting and Analyzing Cash Flows QUESTIONS

Chapter 12 Reporting and Analyzing Cash Flows QUESTIONS 1. The purpose of the cash flow statement is to report all major cash receipts (inflows) and cash payments (outflows) during a period. It helps users

Chapter 12 Reporting and Analyzing Cash Flows QUESTIONS 1. The purpose of the cash flow statement is to report all major cash receipts (inflows) and cash payments (outflows) during a period. It helps users

how to prepare a cash flow statement

business builder 4 how to prepare a cash flow statement zions business resource center zions business resource center 2 how to prepare a cash flow statement A cash flow statement is important to your business

business builder 4 how to prepare a cash flow statement zions business resource center zions business resource center 2 how to prepare a cash flow statement A cash flow statement is important to your business

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

Course pack Accounting 202 Chapter 13: Cash Flow Statement

Course pack Accounting 202 Chapter 13: Cash Flow Statement Value Chapter Included 13 Purpose of Cash Flow Understand Operating, Investing, Financing activities Prepare a Cash Flow Statement indirect only

Course pack Accounting 202 Chapter 13: Cash Flow Statement Value Chapter Included 13 Purpose of Cash Flow Understand Operating, Investing, Financing activities Prepare a Cash Flow Statement indirect only

Oklahoma State University Spears School of Business. Financial Statements

Oklahoma State University Spears School of Business Financial Statements Slide 2 Sources of Information Annual reports (10K) & Quarterly reports (10Q) SEC EDGAR Major databases COMPUSTAT(access through

Oklahoma State University Spears School of Business Financial Statements Slide 2 Sources of Information Annual reports (10K) & Quarterly reports (10Q) SEC EDGAR Major databases COMPUSTAT(access through

A Simple Model. Introduction to Financial Statements

Introduction to Financial Statements NOTES TO ACCOMPANY VIDEOS These notes are intended to supplement the videos on ASimpleModel.com. They are not to be used as stand alone study aids, and are not written

Introduction to Financial Statements NOTES TO ACCOMPANY VIDEOS These notes are intended to supplement the videos on ASimpleModel.com. They are not to be used as stand alone study aids, and are not written

ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL)

") Page 1 ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL) Complete these sample exam problems/objective questions and check your answers with the solutions at the end of the review file and identify where

Page 1 ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL) Complete these sample exam problems/objective questions and check your answers with the solutions at the end of the review file and identify where

Statement of Cash Flows

THE CONTENT AND VALUE OF THE STATEMENT OF CASH FLOWS The cash flow statement reconciles beginning and ending cash by presenting the cash receipts and cash disbursements of an enterprise for an accounting

THE CONTENT AND VALUE OF THE STATEMENT OF CASH FLOWS The cash flow statement reconciles beginning and ending cash by presenting the cash receipts and cash disbursements of an enterprise for an accounting

EXERCISES. The cash from operating activities detail is provided as follows for class discussion:

EXERCISES Ex. 14 1 There were net additions, such as depreciation and amortization of intangible assets of $389 million, to the net loss reported on the income statement to convert the net loss from the

EXERCISES Ex. 14 1 There were net additions, such as depreciation and amortization of intangible assets of $389 million, to the net loss reported on the income statement to convert the net loss from the

CHAPTER 23. Statement of Cash Flows 1, 2, 7, 8, 12 3, 4, 5, 6, 16, 17, 19 9, 20 4, 5, 9, 10, 11 10, 13, 15, 16. 7. Worksheet adjustments.

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

What is a business plan?

What is a business plan? A business plan is the presentation of an idea for a new business. When a person (or group) is planning to open a business, there is a great deal of research that must be done

What is a business plan? A business plan is the presentation of an idea for a new business. When a person (or group) is planning to open a business, there is a great deal of research that must be done

Chapter 002 Financial Statements, Taxes and Cash Flow

Multiple Choice Questions 1. The financial statement summarizing the value of a firm's equity on a particular date is the: a. income statement. B. balance sheet. c. statement of cash flows. d. cash flow

Multiple Choice Questions 1. The financial statement summarizing the value of a firm's equity on a particular date is the: a. income statement. B. balance sheet. c. statement of cash flows. d. cash flow

Statement of Cash Flows

HOSP 2110 (Management Acct) Learning Centre Statement of Cash Flows The Statement of Cash Flows (or cash flow statement) is one of the main financial statements used by investors. It shows the cash generated

HOSP 2110 (Management Acct) Learning Centre Statement of Cash Flows The Statement of Cash Flows (or cash flow statement) is one of the main financial statements used by investors. It shows the cash generated

CASH FLOW STATEMENT. On the statement, cash flows are segregated based on source:

CASH FLOW STATEMENT On the statement, cash flows are segregated based on source: Operating activities: involve the cash effects of transactions that enter into the determination of net income. Investing

CASH FLOW STATEMENT On the statement, cash flows are segregated based on source: Operating activities: involve the cash effects of transactions that enter into the determination of net income. Investing

2-8. Identify whether each of the following items increases or decreases cash flow:

Problems 2-8. Identify whether each of the following items increases or decreases cash flow: Increase in accounts receivable Increase in notes payable Depreciation expense Increase in investments Decrease

Problems 2-8. Identify whether each of the following items increases or decreases cash flow: Increase in accounts receivable Increase in notes payable Depreciation expense Increase in investments Decrease

Financial Statement and Cash Flow Analysis

Chapter 2 Financial Statement and Cash Flow Analysis Answers to Concept Review Questions 1. What role do the FASB and SEC play with regard to GAAP? The FASB is a nongovernmental, professional standards

Chapter 2 Financial Statement and Cash Flow Analysis Answers to Concept Review Questions 1. What role do the FASB and SEC play with regard to GAAP? The FASB is a nongovernmental, professional standards

Statement of Cash Flow

Management Accounting 337 Statement of Cash Flow Cash is obviously an important asset to all, both individually and in business. A shortage or lack of cash may mean an inability to purchase needed inventory

Management Accounting 337 Statement of Cash Flow Cash is obviously an important asset to all, both individually and in business. A shortage or lack of cash may mean an inability to purchase needed inventory

GVEP Workshop Finance 101

GVEP Workshop Finance 101 Nairobi, January 2013 Agenda Introducing business finance Understanding financial statements Understanding cash flow LUNCH Reading and interpreting financial statements Evaluating

GVEP Workshop Finance 101 Nairobi, January 2013 Agenda Introducing business finance Understanding financial statements Understanding cash flow LUNCH Reading and interpreting financial statements Evaluating

Preparing a Successful Financial Plan

Topic 9 Preparing a Successful Financial Plan LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Describe the overview of accounting methods; 2. Prepare the three major financial statements

Topic 9 Preparing a Successful Financial Plan LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Describe the overview of accounting methods; 2. Prepare the three major financial statements

CHAPTER 4. FINANCIAL STATEMENTS

CHAPTER 4. FINANCIAL STATEMENTS Accounting standards require statements that show the financial position, earnings, cash flows, and investment (distribution) by (to) owners. These measurements are reported,

CHAPTER 4. FINANCIAL STATEMENTS Accounting standards require statements that show the financial position, earnings, cash flows, and investment (distribution) by (to) owners. These measurements are reported,

E2-2: Identifying Financing, Investing and Operating Transactions?

E2-2: Identifying Financing, Investing and Operating Transactions? Listed below are eight transactions. In each case, identify whether the transaction is an example of financing, investing or operating

E2-2: Identifying Financing, Investing and Operating Transactions? Listed below are eight transactions. In each case, identify whether the transaction is an example of financing, investing or operating

> DO IT! Chapter 13. Classification of Cash Flows. Cash from Operating Activities D-1. Solution. Action Plan

Chapter 13 > DO IT! Classification of Cash Flows Identify the three types of activities used to report all cash inflows and outflows. Report as operating activities the cash effects of transactions that

Chapter 13 > DO IT! Classification of Cash Flows Identify the three types of activities used to report all cash inflows and outflows. Report as operating activities the cash effects of transactions that

CASH FLOW STATEMENT. MODULE - 6A Analysis of Financial Statements. Cash Flow Statement. Notes

MODULE - 6A Cash Flow Statement 30 CASH FLOW STATEMENT In the previous lesson, you have learnt various types of analysis of financial statements and its tools such as comparative statements, common size

MODULE - 6A Cash Flow Statement 30 CASH FLOW STATEMENT In the previous lesson, you have learnt various types of analysis of financial statements and its tools such as comparative statements, common size

Chapter 21 The Statement of Cash Flows Revisited

Chapter 21 The Statement of Cash Flows Revisited AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments,

Chapter 21 The Statement of Cash Flows Revisited AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments,

Understanding Financial Information for Bankruptcy Lawyers Understanding Financial Statements

Understanding Financial Information for Bankruptcy Lawyers Understanding Financial Statements In the United States, businesses generally present financial information in the form of financial statements

Understanding Financial Information for Bankruptcy Lawyers Understanding Financial Statements In the United States, businesses generally present financial information in the form of financial statements

Understanding Cash Flow Statements

Understanding Cash Flow Statements 2014 Level I Financial Reporting and Analysis IFT Notes for the CFA exam Contents 1. Introduction... 3 2. Components and Format of the Cash Flow Statement... 3 3. The

Understanding Cash Flow Statements 2014 Level I Financial Reporting and Analysis IFT Notes for the CFA exam Contents 1. Introduction... 3 2. Components and Format of the Cash Flow Statement... 3 3. The

The Trading Profit and Loss Account

The Trading Profit and Loss Account Businesses usually calculate their profit level by creating a Trading Profit and Loss Account (TPL) The TPL is produced because: It is a legal requirement It summarises

The Trading Profit and Loss Account Businesses usually calculate their profit level by creating a Trading Profit and Loss Account (TPL) The TPL is produced because: It is a legal requirement It summarises

Preparing Agricultural Financial Statements

Preparing Agricultural Financial Statements Thoroughly understanding your business financial performance is critical for success in today s increasingly competitive agricultural environment. Accurate records

Preparing Agricultural Financial Statements Thoroughly understanding your business financial performance is critical for success in today s increasingly competitive agricultural environment. Accurate records

Chapter 14. 1 Copyright 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Chapter 14 1 Identify the purposes of the statement of cash flows Distinguish among operating, investing, and financing cash flows Prepare the statement of cash flows by the indirect method Identify noncash

Chapter 14 1 Identify the purposes of the statement of cash flows Distinguish among operating, investing, and financing cash flows Prepare the statement of cash flows by the indirect method Identify noncash

ACCOUNTING COMPETENCY EXAM SAMPLE EXAM. 2. The financial statement or statements that pertain to a stated period of time is (are) the:

the:") ACCOUNTING COMPETENCY EXAM SAMPLE EXAM 1. The accounting process does not include: a. interpreting d. observing b. reporting e. classifying c. purchasing 2. The financial statement or statements that pertain

ACCOUNTING COMPETENCY EXAM SAMPLE EXAM 1. The accounting process does not include: a. interpreting d. observing b. reporting e. classifying c. purchasing 2. The financial statement or statements that pertain

Statement of Cash Flows

PREPARING THE STATEMENT OF CASH FLOWS: THE INDIRECT METHOD OF REPORTING CASH FLOWS FROM OPERATING ACTIVITIES The work sheet method described in the text book is not the recommended approach. We will provide

PREPARING THE STATEMENT OF CASH FLOWS: THE INDIRECT METHOD OF REPORTING CASH FLOWS FROM OPERATING ACTIVITIES The work sheet method described in the text book is not the recommended approach. We will provide

Report Description. Business Counts. Top 10 States (by Business Counts) Page 1 of 16

Page 1 of 16") 5-Year County-Level Financial Profile Industry Report Architectural Services (SIC Code: 8712) in Prince George County, Maryland Sales Range: $500,000 - $999,999 Date: 11/07/08 Report Description This 5-Year

5-Year County-Level Financial Profile Industry Report Architectural Services (SIC Code: 8712) in Prince George County, Maryland Sales Range: $500,000 - $999,999 Date: 11/07/08 Report Description This 5-Year

Analyzing the Statement of Cash Flows

Analyzing the Statement of Cash Flows Operating Activities NACM Upstate New York Credit Conference 2015 By Ron Sereika, CCE,CEW NACM 1 Objectives of this Educational Session u Show how the statement of

Analyzing the Statement of Cash Flows Operating Activities NACM Upstate New York Credit Conference 2015 By Ron Sereika, CCE,CEW NACM 1 Objectives of this Educational Session u Show how the statement of

Accounting Self Study Guide for Staff of Micro Finance Institutions

Accounting Self Study Guide for Staff of Micro Finance Institutions LESSON 2 The Balance Sheet OBJECTIVES The purpose of this lesson is to introduce the Balance Sheet and explain its components: Assets,

Accounting Self Study Guide for Staff of Micro Finance Institutions LESSON 2 The Balance Sheet OBJECTIVES The purpose of this lesson is to introduce the Balance Sheet and explain its components: Assets,

Chapter 1. Introduction to Accounting and Business

1 Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature of Business and Accounting A business

1 Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature of Business and Accounting A business

The Basic Framework of Budgeting

Master Budgeting 1 The Basic Framework of Budgeting A budget is a detailed quantitative plan for acquiring and using financial and other resources over a specified forthcoming time period. 1. The act of

Master Budgeting 1 The Basic Framework of Budgeting A budget is a detailed quantitative plan for acquiring and using financial and other resources over a specified forthcoming time period. 1. The act of

The Statement of Cash Flows

CHAPTER The Statement of Cash Flows OBJECTIVES After careful study of this chapter, you will be able to: 1. Define operating, investing, and financing activities. 2. Know the categories of inflows and

CHAPTER The Statement of Cash Flows OBJECTIVES After careful study of this chapter, you will be able to: 1. Define operating, investing, and financing activities. 2. Know the categories of inflows and

BRIEF EXERCISES. CHAPTER 11 Statement of Cash Flows. Determine proper classification (LO1) Determine proper classification (LO1)

Determine proper classification (LO1)") BRIEF EXERCISES BE11 1 Classify each of the following items as an operating, investing, or financing activity. 1. Dividends paid. 2. Repayment of notes payable. 3. Payment for inventory. 4. Purchase of

BRIEF EXERCISES BE11 1 Classify each of the following items as an operating, investing, or financing activity. 1. Dividends paid. 2. Repayment of notes payable. 3. Payment for inventory. 4. Purchase of

Authored for ENMU Tutoring Services. By Jessica Huff

By Jessica Huff The standard accounting equation is Assets=Liabilities + Stockholders Equity. Depending on which item someone is looking at will determine what the normal balance is. The normal balance

By Jessica Huff The standard accounting equation is Assets=Liabilities + Stockholders Equity. Depending on which item someone is looking at will determine what the normal balance is. The normal balance

Understanding Financial Statements. For Your Business

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

The Nature of Accounting Systems

Basic Accounting & Budgeting February 4, 2009 The Nature of Accounting Systems Accounting is the process of recording, classifying, summarizing, reporting and interpreting information about the economic

Basic Accounting & Budgeting February 4, 2009 The Nature of Accounting Systems Accounting is the process of recording, classifying, summarizing, reporting and interpreting information about the economic

This week its Accounting and Beyond

This week its Accounting and Beyond Monday Morning Session Introduction/Accounting Cycle Afternoon Session Tuesday The Balance Sheet Wednesday The Income Statement The Cash Flow Statement Thursday Tools

This week its Accounting and Beyond Monday Morning Session Introduction/Accounting Cycle Afternoon Session Tuesday The Balance Sheet Wednesday The Income Statement The Cash Flow Statement Thursday Tools

UNIVERSITY OF WATERLOO School of Accounting and Finance

UNIVERSITY OF WATERLOO School of Accounting and Finance AFM 101 Professor Shari Mann Professor Donna Psutka Professor Mindy Wolfe Mid-Term Examination Fall 2010 Date and Time: October 21, 2010, 6:30 8:00pm

UNIVERSITY OF WATERLOO School of Accounting and Finance AFM 101 Professor Shari Mann Professor Donna Psutka Professor Mindy Wolfe Mid-Term Examination Fall 2010 Date and Time: October 21, 2010, 6:30 8:00pm

Cash Flow Analysis. 15.501/516 Accounting Spring 2004. Professor S. Roychowdhury. Sloan School of Management Massachusetts Institute of Technology

Cash Flow Analysis 15.501/516 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology Mar 1/3, 2004 1 About The Exam March 10 th a week from today.

Cash Flow Analysis 15.501/516 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology Mar 1/3, 2004 1 About The Exam March 10 th a week from today.

Midterm Fall 2012 Solution

Midterm Fall 2012 Solution Instructions: 1) Answers for the multiple-choice questions must be recorded on the UW answer card. All other questions must be answered in the space provided on the examination

Midterm Fall 2012 Solution Instructions: 1) Answers for the multiple-choice questions must be recorded on the UW answer card. All other questions must be answered in the space provided on the examination

Preparing Financial Statements

Preparing Financial Statements Understanding financial statements is essential to the success of a small business. They can be used as a roadmap to steer you in the right direction and help you avoid costly

Preparing Financial Statements Understanding financial statements is essential to the success of a small business. They can be used as a roadmap to steer you in the right direction and help you avoid costly

TOPIC LEARNING OBJECTIVE

Topic Mapping 1 Transaction Analysis Understand the effect of various types of transactions on the accounting equation, accounting journal and accounting ledger. Concepts and Skills Accounting Equation

Topic Mapping 1 Transaction Analysis Understand the effect of various types of transactions on the accounting equation, accounting journal and accounting ledger. Concepts and Skills Accounting Equation

T-Account Approach to Preparing a Statement of Cash Flows Indirect Method

266 Part 1 E M Foundations of Financial Accounting With these adjustments to the income statement, we can now present the operating activities section of the statement of cash flows using either the direct

266 Part 1 E M Foundations of Financial Accounting With these adjustments to the income statement, we can now present the operating activities section of the statement of cash flows using either the direct

Financial Reporting & Analysis Chapter 17 Solutions Statement of Cash Flows Exercises

Financial Reporting & Analysis Chapter 17 Solutions Statement of Cash Flows Exercises Exercises E17-1. Determining cash flows from operations Using the indirect method, cash flow from operations is computed

Financial Reporting & Analysis Chapter 17 Solutions Statement of Cash Flows Exercises Exercises E17-1. Determining cash flows from operations Using the indirect method, cash flow from operations is computed

Return on Equity has three ratio components. The three ratios that make up Return on Equity are:

Evaluating Financial Performance Chapter 1 Return on Equity Why Use Ratios? It has been said that you must measure what you expect to manage and accomplish. Without measurement, you have no reference to

Evaluating Financial Performance Chapter 1 Return on Equity Why Use Ratios? It has been said that you must measure what you expect to manage and accomplish. Without measurement, you have no reference to

FINANCIAL MANAGEMENT

100 Arbor Drive, Suite 108 Christiansburg, VA 24073 Voice: 540-381-9333 FAX: 540-381-8319 www.becpas.com Providing Professional Business Advisory & Consulting Services Douglas L. Johnston, II [email protected]

100 Arbor Drive, Suite 108 Christiansburg, VA 24073 Voice: 540-381-9333 FAX: 540-381-8319 www.becpas.com Providing Professional Business Advisory & Consulting Services Douglas L. Johnston, II [email protected]

6. Depreciation is a process of a. asset devaluation. b. cost accumulation. c. cost allocation. d. asset valuation.

1. A company purchased land for $72,000 cash. Real estate brokers' commission was $5,000 and $7,000 was spent for demolishing an old building on the land before construction of a new building could start.

1. A company purchased land for $72,000 cash. Real estate brokers' commission was $5,000 and $7,000 was spent for demolishing an old building on the land before construction of a new building could start.

A Simple Model. Cash Flow Statement

An introduction to the cash flow statement in the context of building a financial model. This series introduces the financial statements in the context of a financial model. Cash Flow Statement NOTES TO

An introduction to the cash flow statement in the context of building a financial model. This series introduces the financial statements in the context of a financial model. Cash Flow Statement NOTES TO

UNDERSTANDING WHERE YOU STAND. A Simple Guide to Your Company s Financial Statements

UNDERSTANDING WHERE YOU STAND A Simple Guide to Your Company s Financial Statements Contents INTRODUCTION One statement cannot diagnose your company s financial health. Put several statements together

UNDERSTANDING WHERE YOU STAND A Simple Guide to Your Company s Financial Statements Contents INTRODUCTION One statement cannot diagnose your company s financial health. Put several statements together

Income Measurement and Profitability Analysis

PROFITABILITY ANALYSIS The following financial statements for Spencer Company will be used to demonstrate the calculation of the various ratios in profitability analysis. Spencer Company Comparative Balance

PROFITABILITY ANALYSIS The following financial statements for Spencer Company will be used to demonstrate the calculation of the various ratios in profitability analysis. Spencer Company Comparative Balance

The Basics of Accounting ACCT 201

The Basics of Accounting ACCT 201 Content Accounting definition Accounting equation Accounting elements Asset, Liabilities, & Equity Transactions Accounts Receivable vs Accounts Payable Retained Earnings

The Basics of Accounting ACCT 201 Content Accounting definition Accounting equation Accounting elements Asset, Liabilities, & Equity Transactions Accounts Receivable vs Accounts Payable Retained Earnings

1. Operating, Investment and Financial Cash Flows

1. Operating, Investment and Financial Cash Flows Solutions Problem 1 During 2005, Myears Oil Co. had gross sales of $1 000,000, cost of goods sold of $400,000, and general and selling expenses of $300,000.

1. Operating, Investment and Financial Cash Flows Solutions Problem 1 During 2005, Myears Oil Co. had gross sales of $1 000,000, cost of goods sold of $400,000, and general and selling expenses of $300,000.

STATEMENT OF CHANGES IN FINANCIAL POSITION

Home Page - Statement of Changes in Financial Position STATEMENT OF CHANGES IN FINANCIAL POSITION by Dr. J. Herbert Smith/ACOA Chair Technology Management and Entrepreneurship Faculty of Engineering University

Home Page - Statement of Changes in Financial Position STATEMENT OF CHANGES IN FINANCIAL POSITION by Dr. J. Herbert Smith/ACOA Chair Technology Management and Entrepreneurship Faculty of Engineering University

3,000 3,000 2,910 2,910 3,000 3,000 2,940 2,940

1. David Company uses the gross method to record its credit purchases, and it uses the periodic inventory system. On July 21, 20D, the company purchased goods that had an invoice price of $ with terms

1. David Company uses the gross method to record its credit purchases, and it uses the periodic inventory system. On July 21, 20D, the company purchased goods that had an invoice price of $ with terms

Components of a Business Model Core Strategy 1-5 Strategic 1-5 Partnership 1-5 Customer 1-5 Resources Network Interface

ENGI 8607: Business Planning and Strategy in an Entrepreneurial Environment ZipCar Dr. Amy Hsiao Lecture 5 Memorial University of Newfoundland ZipCar Components of a Business Model How It Works http://www.zipcar.com/cambridge/findcars?zipfleet_id=94396

ENGI 8607: Business Planning and Strategy in an Entrepreneurial Environment ZipCar Dr. Amy Hsiao Lecture 5 Memorial University of Newfoundland ZipCar Components of a Business Model How It Works http://www.zipcar.com/cambridge/findcars?zipfleet_id=94396

Learning Objectives: Quick answer key: Question # Multiple Choice True/False. 14.1 Describe the important of accounting and financial information.

0 Learning Objectives: 14.1 Describe the important of accounting and financial information. 14.2 Differentiate between managerial and financial accounting. 14.3 Identify the six steps of the accounting

0 Learning Objectives: 14.1 Describe the important of accounting and financial information. 14.2 Differentiate between managerial and financial accounting. 14.3 Identify the six steps of the accounting

CHAPTER 2 ACCOUNTING STATEMENTS, TAXES, AND CASH FLOW

CHAPTER 2 ACCOUNTING STATEMENTS, TAXES, AND CASH FLOW Answers to Concepts Review and Critical Thinking Questions 1. True. Every asset can be converted to cash at some price. However, when we are referring

CHAPTER 2 ACCOUNTING STATEMENTS, TAXES, AND CASH FLOW Answers to Concepts Review and Critical Thinking Questions 1. True. Every asset can be converted to cash at some price. However, when we are referring

Statement of Cash Flows: Reporting and Analysis

Statement of Cash Flows: Reporting and Analysis Statement of Cash Flows: Reporting and Analysis Copyright 2014 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form

Statement of Cash Flows: Reporting and Analysis Statement of Cash Flows: Reporting and Analysis Copyright 2014 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form

Construction Economics & Finance. Module 6. Lecture-1

Construction Economics & Finance Module 6 Lecture-1 Financial management: Financial management involves planning, allocation and control of financial resources of a company. Financial management is essential

Construction Economics & Finance Module 6 Lecture-1 Financial management: Financial management involves planning, allocation and control of financial resources of a company. Financial management is essential

Plan and Track Your Finances

Plan and Track Your Finances 9.1 Financing Your Business 9.2 Pro Forma Financial Statements 9.3 Recordkeeping for Businesses Lesson 9.1 Financing Your Business Goals Estimate your startup costs and personal

Plan and Track Your Finances 9.1 Financing Your Business 9.2 Pro Forma Financial Statements 9.3 Recordkeeping for Businesses Lesson 9.1 Financing Your Business Goals Estimate your startup costs and personal

Financial Statement Analysis: An Introduction

Financial Statement Analysis: An Introduction 2014 Level I Financial Reporting and Analysis IFT Notes for the CFA exam Contents 1. Introduction... 3 2. Scope of Financial Statement Analysis... 3 3. Major

Financial Statement Analysis: An Introduction 2014 Level I Financial Reporting and Analysis IFT Notes for the CFA exam Contents 1. Introduction... 3 2. Scope of Financial Statement Analysis... 3 3. Major

Guide to Financial Ratios Analysis A Step by Step Guide to Balance Sheet and Profit and Loss Statement Analysis

Guide to Financial Ratios Analysis A Step by Step Guide to Balance Sheet and Profit and Loss Statement Analysis By BizMove Management Training Institute Other free books by BizMove that may interest you:

Guide to Financial Ratios Analysis A Step by Step Guide to Balance Sheet and Profit and Loss Statement Analysis By BizMove Management Training Institute Other free books by BizMove that may interest you:

ACCOUNTING III Cash Flow Statement & Linking the 3 Financial Statements. Fall 2015 Comp Week 5

ACCOUNTING III Cash Flow Statement & Linking the 3 Financial Statements Fall 2015 Comp Week 5 CODE: CA$H Administrative Stuff Send an email to [email protected] if you have not been added

ACCOUNTING III Cash Flow Statement & Linking the 3 Financial Statements Fall 2015 Comp Week 5 CODE: CA$H Administrative Stuff Send an email to [email protected] if you have not been added

Ratio Analysis. A) Liquidity Ratio : - 1) Current ratio = Current asset Current Liability

Liquidity Ratio : - 1) Current ratio = Current asset Current Liability") A) Liquidity Ratio : - Ratio Analysis 1) Current ratio = Current asset Current Liability 2) Quick ratio or Acid Test ratio = Quick Asset Quick liability Quick Asset = Current Asset Stock Quick Liability

A) Liquidity Ratio : - Ratio Analysis 1) Current ratio = Current asset Current Liability 2) Quick ratio or Acid Test ratio = Quick Asset Quick liability Quick Asset = Current Asset Stock Quick Liability

BACKGROUND KNOWLEDGE for Teachers and Students

Pathway: Business, Marketing, and Computer Education Lesson: BMM C6 4: Financial Statements and Reports Common Core State Standards for Mathematics: N.Q.2 Domain: Quantities Cluster: Reason quantitatively

Pathway: Business, Marketing, and Computer Education Lesson: BMM C6 4: Financial Statements and Reports Common Core State Standards for Mathematics: N.Q.2 Domain: Quantities Cluster: Reason quantitatively

MASTER BUDGET - EXAMPLE

MASTER BUDGET - EXAMPLE Sales IN UNITS for the previous two months (of last quarter), as well as the sales forecast for next quarter are as follows: Sales Budget Units May sales (ACTUAL) 20 June sales

MASTER BUDGET - EXAMPLE Sales IN UNITS for the previous two months (of last quarter), as well as the sales forecast for next quarter are as follows: Sales Budget Units May sales (ACTUAL) 20 June sales

Statement of Cash Flows. Study Objectives

Statement of Cash Flows Study Objectives Indicate the primary purpose of the statement of cash flows. Distinguish among operating, investing, and financing activities. Explain the impact of the product

Statement of Cash Flows Study Objectives Indicate the primary purpose of the statement of cash flows. Distinguish among operating, investing, and financing activities. Explain the impact of the product

Financial Terms & Calculations

Financial Terms & Calculations So much about business and its management requires knowledge and information as to financial measurements. Unfortunately these key terms and ratios are often misunderstood

Financial Terms & Calculations So much about business and its management requires knowledge and information as to financial measurements. Unfortunately these key terms and ratios are often misunderstood

14. Calculating Total Cash Flows.

14. Calculating Total Cash Flows. Greene Co. shows the following information on its 2008 income statement: Sales = $138,000 Costs = $71,500 Other expenses = $4,100 Depreciation expense = $10,100 Interest

14. Calculating Total Cash Flows. Greene Co. shows the following information on its 2008 income statement: Sales = $138,000 Costs = $71,500 Other expenses = $4,100 Depreciation expense = $10,100 Interest

CHAPTER 11 ANALYZING FINANCIAL STATEMENTS: A MANAGERIAL PERSPECTIVE

CHAPTER 11 ANALYZING FINANCIAL STATEMENTS: A MANAGERIAL PERSPECTIVE Bill Reston is the chief operating officer of Valley Home Loans, a residential mortgage lender located in Philadelphia, Pennsylvania.

CHAPTER 11 ANALYZING FINANCIAL STATEMENTS: A MANAGERIAL PERSPECTIVE Bill Reston is the chief operating officer of Valley Home Loans, a residential mortgage lender located in Philadelphia, Pennsylvania.

The BASICS of FINANCIAL STATEMENTS For Agricultural Producers

The BASICS of FINANCIAL STATEMENTS For Agricultural Producers Authors: James McGrann Francisco Abelló Doug Richardson Christy Waggoner Department of Agricultural Economics Texas Cooperative Extension Texas

The BASICS of FINANCIAL STATEMENTS For Agricultural Producers Authors: James McGrann Francisco Abelló Doug Richardson Christy Waggoner Department of Agricultural Economics Texas Cooperative Extension Texas

Chapter 10 Statement of Cash Flows

Chapter 10 Statement of Cash Flows TO THE NET 1. a. Item 1 Business History Northrop Grumman Corporation ( Northrop Grumman or the company ) is an integrated enterprise consisting of businesses that cover

Chapter 10 Statement of Cash Flows TO THE NET 1. a. Item 1 Business History Northrop Grumman Corporation ( Northrop Grumman or the company ) is an integrated enterprise consisting of businesses that cover

Cash Flow Analysis. 15.511 Corporate Accounting Summer 2004. Professor SP Kothari. Sloan School of Management Massachusetts Institute of Technology

Cash Flow Analysis 15.511 Corporate Accounting Summer 2004 Professor SP Kothari Sloan School of Management Massachusetts Institute of Technology June 16, 2004 1 Statement of Cash Flows Reports operating

Cash Flow Analysis 15.511 Corporate Accounting Summer 2004 Professor SP Kothari Sloan School of Management Massachusetts Institute of Technology June 16, 2004 1 Statement of Cash Flows Reports operating

National Black Law Journal UCLA

National Black Law Journal UCLA Peer Reviewed Title: An Introduction to Financial Statements for the Practicing Lawyer Journal Issue: National Black Law Journal, 4(1) Author: Edmonds, Thom Publication

National Black Law Journal UCLA Peer Reviewed Title: An Introduction to Financial Statements for the Practicing Lawyer Journal Issue: National Black Law Journal, 4(1) Author: Edmonds, Thom Publication

Essentials of Financial Statement Analysis

Essentials of Financial Statement Analysis An Introduction to Financial Statement Analysis Gregory Mostyn, CPA Worthy and James Publishing www.worthyjames.com Essentials of Financial Statement Analysis

Essentials of Financial Statement Analysis An Introduction to Financial Statement Analysis Gregory Mostyn, CPA Worthy and James Publishing www.worthyjames.com Essentials of Financial Statement Analysis

a. $ 65,000. b. $ 80,000. c. $130,000. d. $145,000.

注 意 1. 本 試 題 卷 共 50 題, 總 分 100 分 第 01-15 題, 每 題 1.75 分, 合 計 26.25 分 ; 第 16-35 題, 每 題 2 分, 合 計 40 分 ; 第 36-50 題, 每 題 2.25 分, 合 計 33.75 答 錯 不 倒 扣 2. 請 將 答 案 按 試 題 題 號, 依 序 填 入 答 案 卡 1.FastForward had cash

注 意 1. 本 試 題 卷 共 50 題, 總 分 100 分 第 01-15 題, 每 題 1.75 分, 合 計 26.25 分 ; 第 16-35 題, 每 題 2 分, 合 計 40 分 ; 第 36-50 題, 每 題 2.25 分, 合 計 33.75 答 錯 不 倒 扣 2. 請 將 答 案 按 試 題 題 號, 依 序 填 入 答 案 卡 1.FastForward had cash

Chapter 1 Financial Statement and Cash Flow Analysis

Chapter 1 Financial Statement and Cash Flow Analysis MULTIPLE CHOICE 1. Which of the following items can be found on an income statement? a. Accounts receivable b. Long-term debt c. Sales d. Inventory

Chapter 1 Financial Statement and Cash Flow Analysis MULTIPLE CHOICE 1. Which of the following items can be found on an income statement? a. Accounts receivable b. Long-term debt c. Sales d. Inventory

Course 1: Evaluating Financial Performance

Excellence in Financial Management Course 1: Evaluating Financial Performance Prepared by: Matt H. Evans, CPA, CMA, CFM This course provides a basic understanding of how to use ratio analysis for evaluating

Excellence in Financial Management Course 1: Evaluating Financial Performance Prepared by: Matt H. Evans, CPA, CMA, CFM This course provides a basic understanding of how to use ratio analysis for evaluating

APPENDIX 1 The Statement of Financial Position

APPENDIX 1 The Statement of Financial Position 1. Assets: the resources of the organization which are used to provide service and generate value 2. Current assets: assets which can be converted to cash

APPENDIX 1 The Statement of Financial Position 1. Assets: the resources of the organization which are used to provide service and generate value 2. Current assets: assets which can be converted to cash

13:11. Statement of Cash Flows. Chapter. Illustration. Statement of Cash Flows- summary. Overview

Overview Statement of Cash Flows Chapter 23 BECAUSE of the SCF, users of the financial statements get the best of both worlds! SCF bridges the gap created by paper income resulting from applying an accrual

Overview Statement of Cash Flows Chapter 23 BECAUSE of the SCF, users of the financial statements get the best of both worlds! SCF bridges the gap created by paper income resulting from applying an accrual