Introduction to Predictive Modeling Using GLMs

|

|

|

- Letitia Barnett

- 10 years ago

- Views:

Transcription

1 Introduction to Predictive Modeling Using GLMs Dan Tevet, FCAS, MAAA, Liberty Mutual Insurance Group Anand Khare, FCAS, MAAA, CPCU, Milliman 1

2 Antitrust Notice The Casualty Actuarial Society is committed to adhering strictly to the letter and spirit of the antitrust laws. Seminars conducted under the auspices of the CAS are designed solely to provide a forum for the expression of various points of view on topics described in the programs or agendas for such meetings. Under no circumstances shall CAS seminars be used as a means for competing companies or firms to reach any understanding expressed or implied that restricts competition or in any way impairs the ability of members to exercise independent business judgment regarding matters affecting competition. It is the responsibility of all seminar participants to be aware of antitrust regulations, to prevent any written or verbal discussions that appear to violate these laws, and to adhere in every respect to the CAS antitrust compliance policy. 2

3 A New England vacation The weather The car insurance

4 A few words about overfitting - The more data we have The more models we have The more sophisticated models become The potential for overfitting data never goes away! That s one big reason to validate models.

5 Prediction error In a nutshell Training data Test data Model Complexity

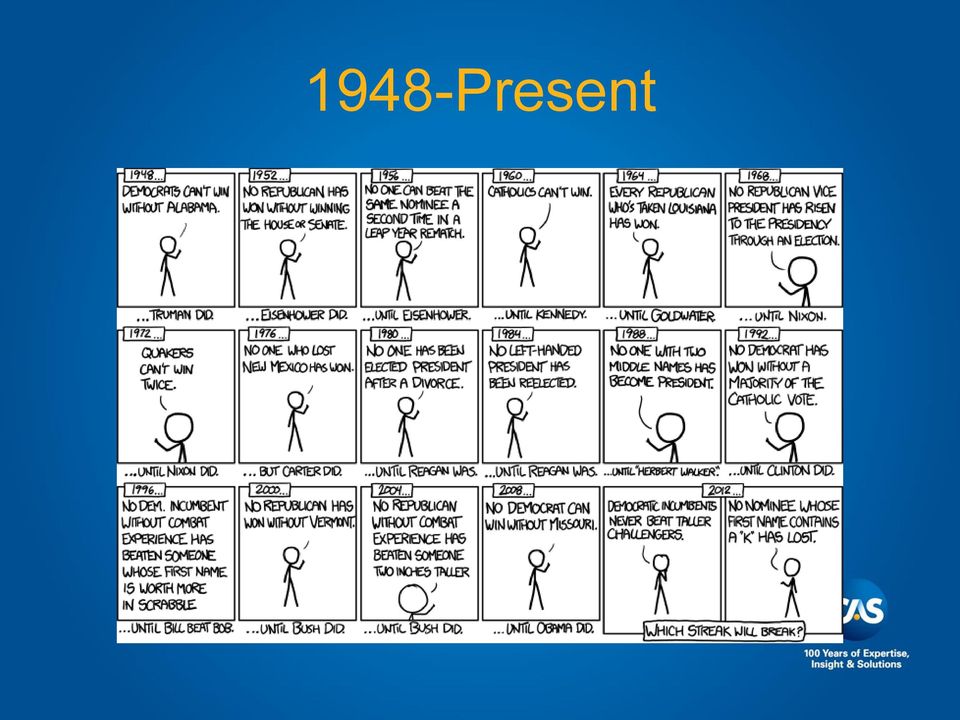

6 Overfitting U.S. Elections (courtesy of Randall Munroe, writer of xkcd and What If)

7

8 1948-Present

9 Outline Overview of predictive modeling Predictive modeling in the actuarial world Simple linear models vs generalized linear models (GLMs) Specification of GLMs Interpretation of GLM output Frequency/severity vs pure premium modeling Model validation Modeling process and important considerations The next 100 years 9

10 What is Predictive Modeling Model an abstraction of reality, generally with a random or probabilistic component Simplification of a real world phenomenon Model types include: Linear models predict target variable using linear combination of predictor variables Trees split dataset, one variable at a time, into subgroups that behave similarly Neural networks self-learning algorithms that adapt to best predict a quantity of interest 10

11 How Do Actuaries Use Modeling? Rating plans model insurance loss data to build plans that charge actuarially fair rates Underwriting plans knowing relative riskiness of policyholder can inform underwriting decisions Enterprise risk management model correlations between lines of business or probability of ruin Product analytics customer retention, conversion, lifetime value 11

12 Simple Linear Model Y = β 0 + β 1 *X 1 + β 2 *X ε Y is the target or response variable it is what we are trying to predict (e.g. pure premium) X 1, X 2, etc are the explanatory (e.g. age of driver, type of vehicle) variables we use them to predict Y ε is the error or noise term it is the portion of Y that is unexplained by X μ = E(Y) = β 0 + β 1 *X 1 + β 2 *X β n *X n In general, we are modeling the mean of Y 12

X 1, X 2, etc are the explanatory (e.g.")

13 Simple Linear Model Assumptions Assumptions of simple linear models Target variable Y does not depend on the value of Y for any other record, only the predictors Y is normally distributed Mean of Y depends on the predictors, but all records have same variance Y is related to predictors through simple linear function Unfortunately, these assumptions are often unrealistic Target variables of interest, such as pure premium, frequency, and severity, are not normally distributed and have non-constant variance 13

14 Generalized Linear Models Generalized linear model: g( ) = β 0 + β 1 *X 1 + β 2 *X β n *X n Assumptions of generalized linear models Target variable Y does not depend on the value of Y for any other record, only the predictors Distribution of Y is a member of the exponential family of distributions Variance of Y is a function of the mean of Y g( ) is linearly related to the predictors. The function g is called the link function The exponential family of distributions include the following: Normal, Poisson, Gamma, Binomial, Negative Binomial, Inverse Gaussian, Tweedie 14

15 GLM Variance Function Var(Y) = φ*v(μ)/w φ is the dispersion coefficient, which is estimated by the GLM w is the weight assigned to each record GLMs calculate the coefficients that maximize likelihood, and w is the weight that each record gets in that calculation V(μ) is the GLM Variance Function, and is determined by the distribution Normal: V(μ) = 1 Poisson: V(μ) = μ Gamma: V(μ) = μ 2 15

= 1 Poisson: V(μ) = μ")

16 GLM Link Function g(μ) = β 0 + β 1 *X 1 + β 2 *X 2 + Common choices for link function Identity: g(μ) = μ Log: g(μ) = ln(μ) Logit: g(μ) = ln(μ/(1- μ)) Log link commonly used to model rating plans because it produces multiplicative relativities ln(μ) = β 0 + β 1 *X 1 + β 2 *X 2 μ = exp(β 0 + β 1 *X 1 + β 2 *X 2 ) μ = exp(β 0 )*exp(β 1 *X 1 ) *exp(β 2 *X 2 ) Logit link used to model probability of an event occurring 16

μ = exp(β 0 )*exp(β 1 *X 1 ) *exp(β 2 *X 2 ) Logit link used to model probability of an event")

17 Offsets An effect in a model that is fixed by the modeler Variable offsets fix the effect of variables that are not being modeled Example: Constructing a rating plan and not modeling base territory rates Solution: Offset for current territory rates Volume offsets reflect fact that different records have different volumes of data and thus have different expected values Example: Modeling claim counts. Some records have a single exposure, other have many exposures Solution: Offset for exposure volume of each observation 17

18 Interpreting GLM Coefficients w/ Log Link Discrete variables: exponentiate GLM coefficient Example: coefficient for youth drivers is 0.52 Rating factor = exp(0.52) = 1.68 Youth drivers have 68% surcharge relative to base level of adult drivers (who, by definition, have rating factor of 1.00) Continuous variables with no transformation Example: modeling pure premium, and annual miles driven is a continuous variable As miles driven increases by 1 unit, expected pure premium is scaled by a factor of exp(β), regardless of whether mileage goes from 1,000 to 2,000 or 20,000 to 21,000 Continuous variables with log transformation Pure premium ~ (annual mileage)^β If β < 1, then as mileage increases, pure premium increases at decreasing rate 18

, regardless of whether mileage goes from 1,000 to 2,000 or 20,000 to 21,000 Continuous variables with log transformation Pure premium ~ (annual")

19 Uncertainty in Parameter Estimates GLMs allow us to quantify uncertainty in parameter estimates Wald 95% confidence interval for mean of parameter estimate = Mean +/- 1.96*(Standard Error) Test for the significance of an individual parameter Wald Chi Square = (Parameter Estimate/Standard Error)^2 Approximately follows a Chi Squared distribution with 1 degree of freedom P-value is probability of obtaining a Chi Square statistic of given magnitude by pure chance Lower p-value more significant 19

^2 Approximately follows a Chi Squared distribution with 1 degree of freedom P-value is probability of obtaining a Chi")

20 Two Modeling Approaches Pure Premium Approach: Build a single model for pure premium Generally straightforward to implement Frequency-Severity Approach: Build one model for claim frequency and another for claims severity Additional work for additional insight 20

21 Pure Premium Approach Advantages: Only a single model needs to be built No need to split variable offsets Results often very similar to frequency-severity approach Disadvantages: Yields less insight than frequency-severity Tweedie distribution is only good choice Relatively new and mathematically complex Includes implicit assumptions that may not hold 21

22 Frequency-Severity Approach Advantages: May yield meaningful insights about data Can choose from several well-known and wellunderstood distributions Disadvantages: Two models to build, run, and validate Requires splitting variable offsets Often produces limited additional benefit 22

23 Tweedie Distribution Mixed Poisson-Gamma process number of claims follow a Poisson distribution, and the size of each claim follows a Gamma distribution The Tweedie is a 3-parameter distribution: Mean (μ), equal to the product of the means of the underlying Poisson and Gamma distributions Power (p), which depends on the coefficient of variation of the underlying Gamma distribution Dispersion (φ), a measure of variance 23

24 Frequency Distribution Options Poisson The Coca Cola of claim count distributions Overdispersed frequency distributions Overdispersed Poisson Zero-Inflated Poisson Negative Binomial Zero-Inflated Negative Binomial 24

25 Severity Distribution Options Several reasonable distributions Criteria Member of exponential family p 2, where V(µ)=µ p In order of increasing variance: Gamma (p=2) Tweedie (2<p<3) Inverse Gaussian (p=3) Tweedie (p>3) 25

26 Three Pillars of Model Validation Tests of Fit Tests of Lift Tests of Stability 26

27 Fit Statistics Traditional: Absolute/Squared Error Alternatives: Likelihood, Deviance, Pearson s Chi-Squared Penalized: AIC, BIC Per Observation: Residuals, Leverage 27

28 Absolute/Squared Error Only appropriate if data is normally distributed Inappropriate to use on disaggregate claim frequency, severity, or pure premium data Useful to assess model fit within buckets Bucket data into percentiles, or similar quantiles, and calculate squared difference between actual and predicted for each bucket 28

29 Better Alternatives to Squared Error Likelihood: chance of observation, given model Always increases as parameters are added to model Deviance: twice the difference in loglikelihoods between the saturated and fitted models GLMs are fit so as to minimize deviance Accounts for the shape of the distribution Pearson s chi-squared: squared error divided by the variance function of the distribution Accounts for the skew of the distribution 29

30 Penalized Measures Akaike Information Criterion (AIC): Penalizes loglikelihood for additional model parameters Bayesian Information Criterion (BIC): Penalizes loglikelihood for additional model parameters, and this penalty increases as the number of records in the dataset increases Can be too restrictive Used primarily for variable selection 30

31 Per Observation Traditional residual: actual minus predicted Deviance residual: square root of weighted deviance times sign of actual minus predicted Reflects the shape of the distribution Plotting deviance residual against weight or any predictor should yield an uninformative cloud Should be approximately normally distributed Leverage: used to identify extreme outliers Does not necessarily measure impact 31

32 Model Lift Lift is meant to approximate economic value Fit has no relationship with economic value Economic value is produced by comparative advantage in avoidance of adverse selection Lift is a comparative measure, i.e. the lift of one model over another, or the lift of a model over status quo Lift should always be measured on holdout data 32

33 Lift Measures Simple Quantile Plot Double Lift Chart Loss Ratio Chart Gini Index 33

34 Model Lift Simple Quantile Plots 34

35 Double Lift Chart 35

36 Loss Ratio Chart 36

37 Economic Gini Index 37

38 Gini Index of Rating Plan Model should differentiate lowest and highest loss cost policyholders Creation of Gini index: Order policyholders by model prediction, from best to worst X-axis is cumulative percent of exposures Y-axis is cumulative percent of losses Had model produced Gini index in prior slide, would have identified 60% of exposures that contribute only 20% of losses 38

39 Methods for Testing Model Stability Cross-validation Split data into subsets (e.g. by time period) Refit model on each subset Compare model parameter estimates Bootstrapping Refit model on many bootstrapped samples Calculate variability of parameter estimates Deletion of influential records 39

40 Measures of Influence Cook s Distance: Statistical measure of the impact each record has on the overall model Excellent tool for identifying errors or anomalies Deletion of records with high Cook s Distance may significantly change model results, and so this procedure can be used to test stability DFBETA: Influence on a certain parameter Influence is not to be confused with leverage 40

41 Predictive Modeling Process Collect Data Exploratory Data Analysis Examine univariate distributions Examine relationship of each variable to target Specify Model Evaluate Output Validate Model Productize Model Maintain Model Rebuild Model 41

42 Some important considerations What are you trying to predict? Which explanatory variables to use? Legal concerns Reputation risk Explainability Data integrity Cost What components of the product are not included in the model? Does the model need regulatory approval? What do you expect to find? 42

43 Some important considerations Who will work on the model, and how will you set clearly defined roles for each member of the team? Does the model significantly outperform the existing one? How will you sell the results to each of the key stakeholders? 43

44 Predictive modeling the next 100 years! As GLMs become ingrained in actuarial work, what will be the next development in actuarial predictive modeling? What challenges will we face in adopting new modeling frameworks? 1. Gaining acceptance from key stakeholders 2. Regulatory approval 3. Conforming to actuarial standards 4. Finding/developing the necessary talent 44

45 The future of actuarial predictive modeling Extended linear models Generalized Linear Mixed Models (GLMMs): include both fixed and random effects Generalized Additive Models (GAMs): linear predictor depends on smooth function of predictor variables Bayesian statistics Parameters of the distribution are random and have an a priori distribution Data is sampled to create posterior distribution Produces better estimates of uncertainty than traditional statistics Potential to be heavily used in reserving 45

46 The black box Black box methods (e.g. machine learning) are gaining popularity among many statisticians Little to no knowledge of the underlying data is required Use of such methods in actuarial work raises several questions: 1. Can we accept an accurate but unexplainable answer? 2. Do actuaries need to be involved in the construction of such models? 46

47 For Further Reference Anderson, Duncan, et. al., A Practitioner s Guide to Generalized Linear Models, CAS Discussion Paper Program,

48 For Further Reference McCullagh, Peter and Nelder, John A., Generalized Linear Models, 2nd Ed., Chapman & Hall,

49 For Further Reference De Jong, Piet and Heller, Gillian, Generalized Linear Models for Insurance Data, Cambridge University Press,

50 For Further Reference Ohlsson, Esbjörn and Johansson, Björn, Non-Life Pricing with Generalized Linear Models, Springer,

51 Questions?

GLM I An Introduction to Generalized Linear Models

GLM I An Introduction to Generalized Linear Models CAS Ratemaking and Product Management Seminar March 2009 Presented by: Tanya D. Havlicek, Actuarial Assistant 0 ANTITRUST Notice The Casualty Actuarial

GLM I An Introduction to Generalized Linear Models CAS Ratemaking and Product Management Seminar March 2009 Presented by: Tanya D. Havlicek, Actuarial Assistant 0 ANTITRUST Notice The Casualty Actuarial

STATISTICA Formula Guide: Logistic Regression. Table of Contents

: Table of Contents... 1 Overview of Model... 1 Dispersion... 2 Parameterization... 3 Sigma-Restricted Model... 3 Overparameterized Model... 4 Reference Coding... 4 Model Summary (Summary Tab)... 5 Summary

: Table of Contents... 1 Overview of Model... 1 Dispersion... 2 Parameterization... 3 Sigma-Restricted Model... 3 Overparameterized Model... 4 Reference Coding... 4 Model Summary (Summary Tab)... 5 Summary

Anti-Trust Notice. Agenda. Three-Level Pricing Architect. Personal Lines Pricing. Commercial Lines Pricing. Conclusions Q&A

Achieving Optimal Insurance Pricing through Class Plan Rating and Underwriting Driven Pricing 2011 CAS Spring Annual Meeting Palm Beach, Florida by Beth Sweeney, FCAS, MAAA American Family Insurance Group

Achieving Optimal Insurance Pricing through Class Plan Rating and Underwriting Driven Pricing 2011 CAS Spring Annual Meeting Palm Beach, Florida by Beth Sweeney, FCAS, MAAA American Family Insurance Group

SAS Software to Fit the Generalized Linear Model

SAS Software to Fit the Generalized Linear Model Gordon Johnston, SAS Institute Inc., Cary, NC Abstract In recent years, the class of generalized linear models has gained popularity as a statistical modeling

SAS Software to Fit the Generalized Linear Model Gordon Johnston, SAS Institute Inc., Cary, NC Abstract In recent years, the class of generalized linear models has gained popularity as a statistical modeling

Predictive Modeling for Life Insurers

Predictive Modeling for Life Insurers Application of Predictive Modeling Techniques in Measuring Policyholder Behavior in Variable Annuity Contracts April 30, 2010 Guillaume Briere-Giroux, FSA, MAAA, CFA

Predictive Modeling for Life Insurers Application of Predictive Modeling Techniques in Measuring Policyholder Behavior in Variable Annuity Contracts April 30, 2010 Guillaume Briere-Giroux, FSA, MAAA, CFA

GENERALIZED LINEAR MODELS IN VEHICLE INSURANCE

ACTA UNIVERSITATIS AGRICULTURAE ET SILVICULTURAE MENDELIANAE BRUNENSIS Volume 62 41 Number 2, 2014 http://dx.doi.org/10.11118/actaun201462020383 GENERALIZED LINEAR MODELS IN VEHICLE INSURANCE Silvie Kafková

ACTA UNIVERSITATIS AGRICULTURAE ET SILVICULTURAE MENDELIANAE BRUNENSIS Volume 62 41 Number 2, 2014 http://dx.doi.org/10.11118/actaun201462020383 GENERALIZED LINEAR MODELS IN VEHICLE INSURANCE Silvie Kafková

How To Build A Predictive Model In Insurance

The Do s & Don ts of Building A Predictive Model in Insurance University of Minnesota November 9 th, 2012 Nathan Hubbell, FCAS Katy Micek, Ph.D. Agenda Travelers Broad Overview Actuarial & Analytics Career

The Do s & Don ts of Building A Predictive Model in Insurance University of Minnesota November 9 th, 2012 Nathan Hubbell, FCAS Katy Micek, Ph.D. Agenda Travelers Broad Overview Actuarial & Analytics Career

Revising the ISO Commercial Auto Classification Plan. Anand Khare, FCAS, MAAA, CPCU

Revising the ISO Commercial Auto Classification Plan Anand Khare, FCAS, MAAA, CPCU 1 THE EXISTING PLAN 2 Context ISO Personal Lines Commercial Lines Property Homeowners, Dwelling Commercial Property, BOP,

Revising the ISO Commercial Auto Classification Plan Anand Khare, FCAS, MAAA, CPCU 1 THE EXISTING PLAN 2 Context ISO Personal Lines Commercial Lines Property Homeowners, Dwelling Commercial Property, BOP,

A Deeper Look Inside Generalized Linear Models

A Deeper Look Inside Generalized Linear Models University of Minnesota February 3 rd, 2012 Nathan Hubbell, FCAS Agenda Property & Casualty (P&C Insurance) in one slide The Actuarial Profession Travelers

A Deeper Look Inside Generalized Linear Models University of Minnesota February 3 rd, 2012 Nathan Hubbell, FCAS Agenda Property & Casualty (P&C Insurance) in one slide The Actuarial Profession Travelers

Combining Linear and Non-Linear Modeling Techniques: EMB America. Getting the Best of Two Worlds

Combining Linear and Non-Linear Modeling Techniques: Getting the Best of Two Worlds Outline Who is EMB? Insurance industry predictive modeling applications EMBLEM our GLM tool How we have used CART with

Combining Linear and Non-Linear Modeling Techniques: Getting the Best of Two Worlds Outline Who is EMB? Insurance industry predictive modeling applications EMBLEM our GLM tool How we have used CART with

Underwriting risk control in non-life insurance via generalized linear models and stochastic programming

Underwriting risk control in non-life insurance via generalized linear models and stochastic programming 1 Introduction Martin Branda 1 Abstract. We focus on rating of non-life insurance contracts. We

Underwriting risk control in non-life insurance via generalized linear models and stochastic programming 1 Introduction Martin Branda 1 Abstract. We focus on rating of non-life insurance contracts. We

Logistic Regression (a type of Generalized Linear Model)

") Logistic Regression (a type of Generalized Linear Model) 1/36 Today Review of GLMs Logistic Regression 2/36 How do we find patterns in data? We begin with a model of how the world works We use our knowledge

Logistic Regression (a type of Generalized Linear Model) 1/36 Today Review of GLMs Logistic Regression 2/36 How do we find patterns in data? We begin with a model of how the world works We use our knowledge

Model Validation Techniques

Model Validation Techniques Kevin Mahoney, FCAS kmahoney@ travelers.com CAS RPM Seminar March 17, 2010 Uses of Statistical Models in P/C Insurance Examples of Applications Determine expected loss cost

Model Validation Techniques Kevin Mahoney, FCAS kmahoney@ travelers.com CAS RPM Seminar March 17, 2010 Uses of Statistical Models in P/C Insurance Examples of Applications Determine expected loss cost

UBI-5: Usage-Based Insurance from a Regulatory Perspective

UBI-5: Usage-Based Insurance from a Regulatory Perspective Carl Sornson, FCAS Managing Actuary Property/Casualty NJ Dept of Banking & Insurance 2015 CAS RPM Seminar March 10, 2015 Antitrust Notice The

UBI-5: Usage-Based Insurance from a Regulatory Perspective Carl Sornson, FCAS Managing Actuary Property/Casualty NJ Dept of Banking & Insurance 2015 CAS RPM Seminar March 10, 2015 Antitrust Notice The

BOOSTED REGRESSION TREES: A MODERN WAY TO ENHANCE ACTUARIAL MODELLING

BOOSTED REGRESSION TREES: A MODERN WAY TO ENHANCE ACTUARIAL MODELLING Xavier Conort [email protected] Session Number: TBR14 Insurance has always been a data business The industry has successfully

BOOSTED REGRESSION TREES: A MODERN WAY TO ENHANCE ACTUARIAL MODELLING Xavier Conort [email protected] Session Number: TBR14 Insurance has always been a data business The industry has successfully

Nonnested model comparison of GLM and GAM count regression models for life insurance data

Nonnested model comparison of GLM and GAM count regression models for life insurance data Claudia Czado, Julia Pfettner, Susanne Gschlößl, Frank Schiller December 8, 2009 Abstract Pricing and product development

Nonnested model comparison of GLM and GAM count regression models for life insurance data Claudia Czado, Julia Pfettner, Susanne Gschlößl, Frank Schiller December 8, 2009 Abstract Pricing and product development

Stochastic programming approaches to pricing in non-life insurance

Stochastic programming approaches to pricing in non-life insurance Martin Branda Charles University in Prague Department of Probability and Mathematical Statistics 11th International Conference on COMPUTATIONAL

Stochastic programming approaches to pricing in non-life insurance Martin Branda Charles University in Prague Department of Probability and Mathematical Statistics 11th International Conference on COMPUTATIONAL

Predictive Modeling in Workers Compensation 2008 CAS Ratemaking Seminar

Predictive Modeling in Workers Compensation 2008 CAS Ratemaking Seminar Prepared by Louise Francis, FCAS, MAAA Francis Analytics and Actuarial Data Mining, Inc. www.data-mines.com [email protected]

Predictive Modeling in Workers Compensation 2008 CAS Ratemaking Seminar Prepared by Louise Francis, FCAS, MAAA Francis Analytics and Actuarial Data Mining, Inc. www.data-mines.com [email protected]

Munich Re INSURANCE AND REINSURANCE. May 6 & 7, 2010 Dave Clark Munich Reinsurance America, Inc 4/26/2010 1

Antitrust Notice The Casualty Actuarial Society is committed to adhering strictly to the letter and spirit of the antitrust laws. Seminars conducted under the auspices of the CAS are designed solely to

Antitrust Notice The Casualty Actuarial Society is committed to adhering strictly to the letter and spirit of the antitrust laws. Seminars conducted under the auspices of the CAS are designed solely to

New Work Item for ISO 3534-5 Predictive Analytics (Initial Notes and Thoughts) Introduction

Introduction") Introduction New Work Item for ISO 3534-5 Predictive Analytics (Initial Notes and Thoughts) Predictive analytics encompasses the body of statistical knowledge supporting the analysis of massive data sets.

Introduction New Work Item for ISO 3534-5 Predictive Analytics (Initial Notes and Thoughts) Predictive analytics encompasses the body of statistical knowledge supporting the analysis of massive data sets.

Insurance Analytics - analýza dat a prediktivní modelování v pojišťovnictví. Pavel Kříž. Seminář z aktuárských věd MFF 4.

Insurance Analytics - analýza dat a prediktivní modelování v pojišťovnictví Pavel Kříž Seminář z aktuárských věd MFF 4. dubna 2014 Summary 1. Application areas of Insurance Analytics 2. Insurance Analytics

Insurance Analytics - analýza dat a prediktivní modelování v pojišťovnictví Pavel Kříž Seminář z aktuárských věd MFF 4. dubna 2014 Summary 1. Application areas of Insurance Analytics 2. Insurance Analytics

Predictive Modeling Techniques in Insurance

Predictive Modeling Techniques in Insurance Tuesday May 5, 2015 JF. Breton Application Engineer 2014 The MathWorks, Inc. 1 Opening Presenter: JF. Breton: 13 years of experience in predictive analytics

Predictive Modeling Techniques in Insurance Tuesday May 5, 2015 JF. Breton Application Engineer 2014 The MathWorks, Inc. 1 Opening Presenter: JF. Breton: 13 years of experience in predictive analytics

Location matters. 3 techniques to incorporate geo-spatial effects in one's predictive model

Location matters. 3 techniques to incorporate geo-spatial effects in one's predictive model Xavier Conort [email protected] Motivation Location matters! Observed value at one location is

Location matters. 3 techniques to incorporate geo-spatial effects in one's predictive model Xavier Conort [email protected] Motivation Location matters! Observed value at one location is

Reserving for loyalty rewards programs Part I

Reserving for loyalty rewards programs Part I Rachel C. Dolsky, FCAS, MAAA Casualty loss reserving seminar Disclaimer The views expressed by the presenter are not necessarily those of EY or its member

Reserving for loyalty rewards programs Part I Rachel C. Dolsky, FCAS, MAAA Casualty loss reserving seminar Disclaimer The views expressed by the presenter are not necessarily those of EY or its member

Predictive modelling around the world 28.11.13

Predictive modelling around the world 28.11.13 Agenda Why this presentation is really interesting Introduction to predictive modelling Case studies Conclusions Why this presentation is really interesting

Predictive modelling around the world 28.11.13 Agenda Why this presentation is really interesting Introduction to predictive modelling Case studies Conclusions Why this presentation is really interesting

Penalized regression: Introduction

Penalized regression: Introduction Patrick Breheny August 30 Patrick Breheny BST 764: Applied Statistical Modeling 1/19 Maximum likelihood Much of 20th-century statistics dealt with maximum likelihood

Penalized regression: Introduction Patrick Breheny August 30 Patrick Breheny BST 764: Applied Statistical Modeling 1/19 Maximum likelihood Much of 20th-century statistics dealt with maximum likelihood

Institute of Actuaries of India Subject CT3 Probability and Mathematical Statistics

Institute of Actuaries of India Subject CT3 Probability and Mathematical Statistics For 2015 Examinations Aim The aim of the Probability and Mathematical Statistics subject is to provide a grounding in

Institute of Actuaries of India Subject CT3 Probability and Mathematical Statistics For 2015 Examinations Aim The aim of the Probability and Mathematical Statistics subject is to provide a grounding in

Offset Techniques for Predictive Modeling for Insurance

Offset Techniques for Predictive Modeling for Insurance Matthew Flynn, Ph.D, ISO Innovative Analytics, W. Hartford CT Jun Yan, Ph.D, Deloitte & Touche LLP, Hartford CT ABSTRACT This paper presents the

Offset Techniques for Predictive Modeling for Insurance Matthew Flynn, Ph.D, ISO Innovative Analytics, W. Hartford CT Jun Yan, Ph.D, Deloitte & Touche LLP, Hartford CT ABSTRACT This paper presents the

More Flexible GLMs Zero-Inflated Models and Hybrid Models

More Flexible GLMs Zero-Inflated Models and Hybrid Models Mathew Flynn, Ph.D. Louise A. Francis FCAS, MAAA Motivation: GLMs are widely used in insurance modeling applications. Claim or frequency models

More Flexible GLMs Zero-Inflated Models and Hybrid Models Mathew Flynn, Ph.D. Louise A. Francis FCAS, MAAA Motivation: GLMs are widely used in insurance modeling applications. Claim or frequency models

Non-life insurance mathematics. Nils F. Haavardsson, University of Oslo and DNB Skadeforsikring

Non-life insurance mathematics Nils F. Haavardsson, University of Oslo and DNB Skadeforsikring Overview Important issues Models treated Curriculum Duration (in lectures) What is driving the result of a

Non-life insurance mathematics Nils F. Haavardsson, University of Oslo and DNB Skadeforsikring Overview Important issues Models treated Curriculum Duration (in lectures) What is driving the result of a

Regulatory Process for Reviewing Hurricane Models and use in Florida Rate Filings

Regulatory Process for Reviewing Hurricane Models and use in Florida Rate Filings Robert Lee, FCAS Florida Office of Insurance Regulation CAS IN FOCUS TAMING CATS OCTOBER 2012 1 Antitrust Notice The Casualty

Regulatory Process for Reviewing Hurricane Models and use in Florida Rate Filings Robert Lee, FCAS Florida Office of Insurance Regulation CAS IN FOCUS TAMING CATS OCTOBER 2012 1 Antitrust Notice The Casualty

R-3: What Makes a Good Rate Filing?

R-3: What Makes a Good Rate Filing? Carl Sornson, FCAS Managing Actuary Property/Casualty NJ Dept of Banking & Insurance 2012 CAS Ratemaking and Product Management Seminar March 19-21, 2012 Antitrust Notice

R-3: What Makes a Good Rate Filing? Carl Sornson, FCAS Managing Actuary Property/Casualty NJ Dept of Banking & Insurance 2012 CAS Ratemaking and Product Management Seminar March 19-21, 2012 Antitrust Notice

11. Analysis of Case-control Studies Logistic Regression

Research methods II 113 11. Analysis of Case-control Studies Logistic Regression This chapter builds upon and further develops the concepts and strategies described in Ch.6 of Mother and Child Health:

Research methods II 113 11. Analysis of Case-control Studies Logistic Regression This chapter builds upon and further develops the concepts and strategies described in Ch.6 of Mother and Child Health:

GENERALIZED LINEAR MODELS FOR INSURANCE RATING Mark Goldburd, FCAS, MAAA Anand Khare, FCAS, MAAA, CPCU Dan Tevet, FCAS, MAAA

CAS MONOGRAPH SERIES NUMBER 5 GENERALIZED LINEAR MODELS FOR INSURANCE RATING Mark Goldburd, FCAS, MAAA Anand Khare, FCAS, MAAA, CPCU Dan Tevet, FCAS, MAAA CASUALTY ACTUARIAL SOCIETY Casualty Actuarial

CAS MONOGRAPH SERIES NUMBER 5 GENERALIZED LINEAR MODELS FOR INSURANCE RATING Mark Goldburd, FCAS, MAAA Anand Khare, FCAS, MAAA, CPCU Dan Tevet, FCAS, MAAA CASUALTY ACTUARIAL SOCIETY Casualty Actuarial

PREDICTIVE LOSS RATIO

PREDICTIVE LOSS RATIO MODELING WITH CREDIT SCORES, FOR INSURANCE PURPOSES Major Qualifying Project submitted to the faculty of Worcester Polytechnic Institute in partial fulfillment of the requirements

PREDICTIVE LOSS RATIO MODELING WITH CREDIT SCORES, FOR INSURANCE PURPOSES Major Qualifying Project submitted to the faculty of Worcester Polytechnic Institute in partial fulfillment of the requirements

Fairfield Public Schools

Mathematics Fairfield Public Schools AP Statistics AP Statistics BOE Approved 04/08/2014 1 AP STATISTICS Critical Areas of Focus AP Statistics is a rigorous course that offers advanced students an opportunity

Mathematics Fairfield Public Schools AP Statistics AP Statistics BOE Approved 04/08/2014 1 AP STATISTICS Critical Areas of Focus AP Statistics is a rigorous course that offers advanced students an opportunity

Chapter 7: Simple linear regression Learning Objectives

Chapter 7: Simple linear regression Learning Objectives Reading: Section 7.1 of OpenIntro Statistics Video: Correlation vs. causation, YouTube (2:19) Video: Intro to Linear Regression, YouTube (5:18) -

Chapter 7: Simple linear regression Learning Objectives Reading: Section 7.1 of OpenIntro Statistics Video: Correlation vs. causation, YouTube (2:19) Video: Intro to Linear Regression, YouTube (5:18) -

Travelers Analytics: U of M Stats 8053 Insurance Modeling Problem

Travelers Analytics: U of M Stats 8053 Insurance Modeling Problem October 30 th, 2013 Nathan Hubbell, FCAS Shengde Liang, Ph.D. Agenda Travelers: Who Are We & How Do We Use Data? Insurance 101 Basic business

Travelers Analytics: U of M Stats 8053 Insurance Modeling Problem October 30 th, 2013 Nathan Hubbell, FCAS Shengde Liang, Ph.D. Agenda Travelers: Who Are We & How Do We Use Data? Insurance 101 Basic business

Reserving for loyalty rewards programs Part III

Reserving for loyalty rewards programs Part III Tim A. Gault, FCAS, MAAA, ARM Casualty Loss Reserving Seminar 15 16 September 2014 Disclaimer The views expressed by the presenter are not necessarily those

Reserving for loyalty rewards programs Part III Tim A. Gault, FCAS, MAAA, ARM Casualty Loss Reserving Seminar 15 16 September 2014 Disclaimer The views expressed by the presenter are not necessarily those

Automated Biosurveillance Data from England and Wales, 1991 2011

Article DOI: http://dx.doi.org/10.3201/eid1901.120493 Automated Biosurveillance Data from England and Wales, 1991 2011 Technical Appendix This online appendix provides technical details of statistical

Article DOI: http://dx.doi.org/10.3201/eid1901.120493 Automated Biosurveillance Data from England and Wales, 1991 2011 Technical Appendix This online appendix provides technical details of statistical

Business Statistics. Successful completion of Introductory and/or Intermediate Algebra courses is recommended before taking Business Statistics.

Business Course Text Bowerman, Bruce L., Richard T. O'Connell, J. B. Orris, and Dawn C. Porter. Essentials of Business, 2nd edition, McGraw-Hill/Irwin, 2008, ISBN: 978-0-07-331988-9. Required Computing

Business Course Text Bowerman, Bruce L., Richard T. O'Connell, J. B. Orris, and Dawn C. Porter. Essentials of Business, 2nd edition, McGraw-Hill/Irwin, 2008, ISBN: 978-0-07-331988-9. Required Computing

The zero-adjusted Inverse Gaussian distribution as a model for insurance claims

The zero-adjusted Inverse Gaussian distribution as a model for insurance claims Gillian Heller 1, Mikis Stasinopoulos 2 and Bob Rigby 2 1 Dept of Statistics, Macquarie University, Sydney, Australia. email:

The zero-adjusted Inverse Gaussian distribution as a model for insurance claims Gillian Heller 1, Mikis Stasinopoulos 2 and Bob Rigby 2 1 Dept of Statistics, Macquarie University, Sydney, Australia. email:

Generalized Linear Models

Generalized Linear Models We have previously worked with regression models where the response variable is quantitative and normally distributed. Now we turn our attention to two types of models where the

Generalized Linear Models We have previously worked with regression models where the response variable is quantitative and normally distributed. Now we turn our attention to two types of models where the

Innovations and Value Creation in Predictive Modeling. David Cummings Vice President - Research

Innovations and Value Creation in Predictive Modeling David Cummings Vice President - Research ISO Innovative Analytics 1 Innovations and Value Creation in Predictive Modeling A look back at the past decade

Innovations and Value Creation in Predictive Modeling David Cummings Vice President - Research ISO Innovative Analytics 1 Innovations and Value Creation in Predictive Modeling A look back at the past decade

The Probit Link Function in Generalized Linear Models for Data Mining Applications

Journal of Modern Applied Statistical Methods Copyright 2013 JMASM, Inc. May 2013, Vol. 12, No. 1, 164-169 1538 9472/13/$95.00 The Probit Link Function in Generalized Linear Models for Data Mining Applications

Journal of Modern Applied Statistical Methods Copyright 2013 JMASM, Inc. May 2013, Vol. 12, No. 1, 164-169 1538 9472/13/$95.00 The Probit Link Function in Generalized Linear Models for Data Mining Applications

240ST014 - Data Analysis of Transport and Logistics

Coordinating unit: Teaching unit: Academic year: Degree: ECTS credits: 2015 240 - ETSEIB - Barcelona School of Industrial Engineering 715 - EIO - Department of Statistics and Operations Research MASTER'S

Coordinating unit: Teaching unit: Academic year: Degree: ECTS credits: 2015 240 - ETSEIB - Barcelona School of Industrial Engineering 715 - EIO - Department of Statistics and Operations Research MASTER'S

5. Multiple regression

5. Multiple regression QBUS6840 Predictive Analytics https://www.otexts.org/fpp/5 QBUS6840 Predictive Analytics 5. Multiple regression 2/39 Outline Introduction to multiple linear regression Some useful

5. Multiple regression QBUS6840 Predictive Analytics https://www.otexts.org/fpp/5 QBUS6840 Predictive Analytics 5. Multiple regression 2/39 Outline Introduction to multiple linear regression Some useful

Measuring per-mile risk for pay-as-youdrive automobile insurance. Eric Minikel CAS Ratemaking & Product Management Seminar March 20, 2012

Measuring per-mile risk for pay-as-youdrive automobile insurance Eric Minikel CAS Ratemaking & Product Management Seminar March 20, 2012 Professor Joseph Ferreira, Jr. and Eric Minikel Measuring per-mile

Measuring per-mile risk for pay-as-youdrive automobile insurance Eric Minikel CAS Ratemaking & Product Management Seminar March 20, 2012 Professor Joseph Ferreira, Jr. and Eric Minikel Measuring per-mile

Why Taking This Course? Course Introduction, Descriptive Statistics and Data Visualization. Learning Goals. GENOME 560, Spring 2012

Why Taking This Course? Course Introduction, Descriptive Statistics and Data Visualization GENOME 560, Spring 2012 Data are interesting because they help us understand the world Genomics: Massive Amounts

Why Taking This Course? Course Introduction, Descriptive Statistics and Data Visualization GENOME 560, Spring 2012 Data are interesting because they help us understand the world Genomics: Massive Amounts

Personal Auto Predictive Modeling Update: What s Next? Roosevelt Mosley, FCAS, MAAA CAS Predictive Modeling Seminar October 6 7, 2008 San Diego, CA

Personal Auto Predictive Modeling Update: What s Next? Roosevelt Mosley, FCAS, MAAA CAS Predictive Modeling Seminar October 6 7, 2008 San Diego, CA You ve Heard Where predictive modeling for auto has been

Personal Auto Predictive Modeling Update: What s Next? Roosevelt Mosley, FCAS, MAAA CAS Predictive Modeling Seminar October 6 7, 2008 San Diego, CA You ve Heard Where predictive modeling for auto has been

Logistic Regression. http://faculty.chass.ncsu.edu/garson/pa765/logistic.htm#sigtests

Logistic Regression http://faculty.chass.ncsu.edu/garson/pa765/logistic.htm#sigtests Overview Binary (or binomial) logistic regression is a form of regression which is used when the dependent is a dichotomy

Logistic Regression http://faculty.chass.ncsu.edu/garson/pa765/logistic.htm#sigtests Overview Binary (or binomial) logistic regression is a form of regression which is used when the dependent is a dichotomy

Probabilistic concepts of risk classification in insurance

Probabilistic concepts of risk classification in insurance Emiliano A. Valdez Michigan State University East Lansing, Michigan, USA joint work with Katrien Antonio* * K.U. Leuven 7th International Workshop

Probabilistic concepts of risk classification in insurance Emiliano A. Valdez Michigan State University East Lansing, Michigan, USA joint work with Katrien Antonio* * K.U. Leuven 7th International Workshop

Computer exercise 4 Poisson Regression

Chalmers-University of Gothenburg Department of Mathematical Sciences Probability, Statistics and Risk MVE300 Computer exercise 4 Poisson Regression When dealing with two or more variables, the functional

Chalmers-University of Gothenburg Department of Mathematical Sciences Probability, Statistics and Risk MVE300 Computer exercise 4 Poisson Regression When dealing with two or more variables, the functional

Model Selection and Claim Frequency for Workers Compensation Insurance

Model Selection and Claim Frequency for Workers Compensation Insurance Jisheng Cui, David Pitt and Guoqi Qian Abstract We consider a set of workers compensation insurance claim data where the aggregate

Model Selection and Claim Frequency for Workers Compensation Insurance Jisheng Cui, David Pitt and Guoqi Qian Abstract We consider a set of workers compensation insurance claim data where the aggregate

Overview Classes. 12-3 Logistic regression (5) 19-3 Building and applying logistic regression (6) 26-3 Generalizations of logistic regression (7)

19-3 Building and applying logistic regression (6) 26-3 Generalizations of logistic regression (7)") Overview Classes 12-3 Logistic regression (5) 19-3 Building and applying logistic regression (6) 26-3 Generalizations of logistic regression (7) 2-4 Loglinear models (8) 5-4 15-17 hrs; 5B02 Building and

Overview Classes 12-3 Logistic regression (5) 19-3 Building and applying logistic regression (6) 26-3 Generalizations of logistic regression (7) 2-4 Loglinear models (8) 5-4 15-17 hrs; 5B02 Building and

Gerry Hobbs, Department of Statistics, West Virginia University

Decision Trees as a Predictive Modeling Method Gerry Hobbs, Department of Statistics, West Virginia University Abstract Predictive modeling has become an important area of interest in tasks such as credit

Decision Trees as a Predictive Modeling Method Gerry Hobbs, Department of Statistics, West Virginia University Abstract Predictive modeling has become an important area of interest in tasks such as credit

Studying Auto Insurance Data

Studying Auto Insurance Data Ashutosh Nandeshwar February 23, 2010 1 Introduction To study auto insurance data using traditional and non-traditional tools, I downloaded a well-studied data from http://www.statsci.org/data/general/motorins.

Studying Auto Insurance Data Ashutosh Nandeshwar February 23, 2010 1 Introduction To study auto insurance data using traditional and non-traditional tools, I downloaded a well-studied data from http://www.statsci.org/data/general/motorins.

business statistics using Excel OXFORD UNIVERSITY PRESS Glyn Davis & Branko Pecar

business statistics using Excel Glyn Davis & Branko Pecar OXFORD UNIVERSITY PRESS Detailed contents Introduction to Microsoft Excel 2003 Overview Learning Objectives 1.1 Introduction to Microsoft Excel

business statistics using Excel Glyn Davis & Branko Pecar OXFORD UNIVERSITY PRESS Detailed contents Introduction to Microsoft Excel 2003 Overview Learning Objectives 1.1 Introduction to Microsoft Excel

Improving Demand Forecasting

Improving Demand Forecasting 2 nd July 2013 John Tansley - CACI Overview The ideal forecasting process: Efficiency, transparency, accuracy Managing and understanding uncertainty: Limits to forecast accuracy,

Improving Demand Forecasting 2 nd July 2013 John Tansley - CACI Overview The ideal forecasting process: Efficiency, transparency, accuracy Managing and understanding uncertainty: Limits to forecast accuracy,

Chapter 29 The GENMOD Procedure. Chapter Table of Contents

Chapter 29 The GENMOD Procedure Chapter Table of Contents OVERVIEW...1365 WhatisaGeneralizedLinearModel?...1366 ExamplesofGeneralizedLinearModels...1367 TheGENMODProcedure...1368 GETTING STARTED...1370

Chapter 29 The GENMOD Procedure Chapter Table of Contents OVERVIEW...1365 WhatisaGeneralizedLinearModel?...1366 ExamplesofGeneralizedLinearModels...1367 TheGENMODProcedure...1368 GETTING STARTED...1370

Stochastic Analysis of Long-Term Multiple-Decrement Contracts

Stochastic Analysis of Long-Term Multiple-Decrement Contracts Matthew Clark, FSA, MAAA, and Chad Runchey, FSA, MAAA Ernst & Young LLP Published in the July 2008 issue of the Actuarial Practice Forum Copyright

Stochastic Analysis of Long-Term Multiple-Decrement Contracts Matthew Clark, FSA, MAAA, and Chad Runchey, FSA, MAAA Ernst & Young LLP Published in the July 2008 issue of the Actuarial Practice Forum Copyright

Simple Linear Regression Inference

Simple Linear Regression Inference 1 Inference requirements The Normality assumption of the stochastic term e is needed for inference even if it is not a OLS requirement. Therefore we have: Interpretation

Simple Linear Regression Inference 1 Inference requirements The Normality assumption of the stochastic term e is needed for inference even if it is not a OLS requirement. Therefore we have: Interpretation

Data Visualization Techniques and Practices Introduction to GIS Technology

Data Visualization Techniques and Practices Introduction to GIS Technology Michael Greene Advanced Analytics & Modeling, Deloitte Consulting LLP March 16 th, 2010 Antitrust Notice The Casualty Actuarial

Data Visualization Techniques and Practices Introduction to GIS Technology Michael Greene Advanced Analytics & Modeling, Deloitte Consulting LLP March 16 th, 2010 Antitrust Notice The Casualty Actuarial

Course Text. Required Computing Software. Course Description. Course Objectives. StraighterLine. Business Statistics

Course Text Business Statistics Lind, Douglas A., Marchal, William A. and Samuel A. Wathen. Basic Statistics for Business and Economics, 7th edition, McGraw-Hill/Irwin, 2010, ISBN: 9780077384470 [This

Course Text Business Statistics Lind, Douglas A., Marchal, William A. and Samuel A. Wathen. Basic Statistics for Business and Economics, 7th edition, McGraw-Hill/Irwin, 2010, ISBN: 9780077384470 [This

II. DISTRIBUTIONS distribution normal distribution. standard scores

Appendix D Basic Measurement And Statistics The following information was developed by Steven Rothke, PhD, Department of Psychology, Rehabilitation Institute of Chicago (RIC) and expanded by Mary F. Schmidt,

Appendix D Basic Measurement And Statistics The following information was developed by Steven Rothke, PhD, Department of Psychology, Rehabilitation Institute of Chicago (RIC) and expanded by Mary F. Schmidt,

Cross Validation techniques in R: A brief overview of some methods, packages, and functions for assessing prediction models.

Cross Validation techniques in R: A brief overview of some methods, packages, and functions for assessing prediction models. Dr. Jon Starkweather, Research and Statistical Support consultant This month

Cross Validation techniques in R: A brief overview of some methods, packages, and functions for assessing prediction models. Dr. Jon Starkweather, Research and Statistical Support consultant This month

Lecture 8: Gamma regression

Lecture 8: Gamma regression Claudia Czado TU München c (Claudia Czado, TU Munich) ZFS/IMS Göttingen 2004 0 Overview Models with constant coefficient of variation Gamma regression: estimation and testing

Lecture 8: Gamma regression Claudia Czado TU München c (Claudia Czado, TU Munich) ZFS/IMS Göttingen 2004 0 Overview Models with constant coefficient of variation Gamma regression: estimation and testing

NCSS Statistical Software Principal Components Regression. In ordinary least squares, the regression coefficients are estimated using the formula ( )

") Chapter 340 Principal Components Regression Introduction is a technique for analyzing multiple regression data that suffer from multicollinearity. When multicollinearity occurs, least squares estimates

Chapter 340 Principal Components Regression Introduction is a technique for analyzing multiple regression data that suffer from multicollinearity. When multicollinearity occurs, least squares estimates

Predictive Modeling in Long-Term Care Insurance

Predictive Modeling in Long-Term Care Insurance Nathan R. Lally and Brian M. Hartman May 3, 2015 Abstract The accurate prediction of long-term care insurance (LTCI) mortality, lapse, and claim rates is

Predictive Modeling in Long-Term Care Insurance Nathan R. Lally and Brian M. Hartman May 3, 2015 Abstract The accurate prediction of long-term care insurance (LTCI) mortality, lapse, and claim rates is

CHAPTER 3 EXAMPLES: REGRESSION AND PATH ANALYSIS

Examples: Regression And Path Analysis CHAPTER 3 EXAMPLES: REGRESSION AND PATH ANALYSIS Regression analysis with univariate or multivariate dependent variables is a standard procedure for modeling relationships

Examples: Regression And Path Analysis CHAPTER 3 EXAMPLES: REGRESSION AND PATH ANALYSIS Regression analysis with univariate or multivariate dependent variables is a standard procedure for modeling relationships

Advanced Statistical Analysis of Mortality. Rhodes, Thomas E. and Freitas, Stephen A. MIB, Inc. 160 University Avenue. Westwood, MA 02090

Advanced Statistical Analysis of Mortality Rhodes, Thomas E. and Freitas, Stephen A. MIB, Inc 160 University Avenue Westwood, MA 02090 001-(781)-751-6356 fax 001-(781)-329-3379 [email protected] Abstract

Advanced Statistical Analysis of Mortality Rhodes, Thomas E. and Freitas, Stephen A. MIB, Inc 160 University Avenue Westwood, MA 02090 001-(781)-751-6356 fax 001-(781)-329-3379 [email protected] Abstract

Curriculum Map Statistics and Probability Honors (348) Saugus High School Saugus Public Schools 2009-2010

Saugus High School Saugus Public Schools 2009-2010") Curriculum Map Statistics and Probability Honors (348) Saugus High School Saugus Public Schools 2009-2010 Week 1 Week 2 14.0 Students organize and describe distributions of data by using a number of different

Curriculum Map Statistics and Probability Honors (348) Saugus High School Saugus Public Schools 2009-2010 Week 1 Week 2 14.0 Students organize and describe distributions of data by using a number of different

Credibility and Pooling Applications to Group Life and Group Disability Insurance

Credibility and Pooling Applications to Group Life and Group Disability Insurance Presented by Paul L. Correia Consulting Actuary [email protected] (207) 771-1204 May 20, 2014 What I plan to cover

Credibility and Pooling Applications to Group Life and Group Disability Insurance Presented by Paul L. Correia Consulting Actuary [email protected] (207) 771-1204 May 20, 2014 What I plan to cover

Reserving for Loyalty Rewards Programs

Albert Zhou, FCAS, MAAA CAS Casualty Loss Reserve Seminar September 15-17, 2014 Chesney House, 96 Pitts Bay Road Pembroke HM08, Bermuda www.thirdpointre.bm Antitrust Notice The Casualty Actuarial Society

Albert Zhou, FCAS, MAAA CAS Casualty Loss Reserve Seminar September 15-17, 2014 Chesney House, 96 Pitts Bay Road Pembroke HM08, Bermuda www.thirdpointre.bm Antitrust Notice The Casualty Actuarial Society

A Property & Casualty Insurance Predictive Modeling Process in SAS

Paper AA-02-2015 A Property & Casualty Insurance Predictive Modeling Process in SAS 1.0 ABSTRACT Mei Najim, Sedgwick Claim Management Services, Chicago, Illinois Predictive analytics has been developing

Paper AA-02-2015 A Property & Casualty Insurance Predictive Modeling Process in SAS 1.0 ABSTRACT Mei Najim, Sedgwick Claim Management Services, Chicago, Illinois Predictive analytics has been developing

Motor and Household Insurance: Pricing to Maximise Profit in a Competitive Market

Motor and Household Insurance: Pricing to Maximise Profit in a Competitive Market by Tom Wright, Partner, English Wright & Brockman 1. Introduction This paper describes one way in which statistical modelling

Motor and Household Insurance: Pricing to Maximise Profit in a Competitive Market by Tom Wright, Partner, English Wright & Brockman 1. Introduction This paper describes one way in which statistical modelling

Large Account Pricing

Workshop 5: Large Account Pricing Large Account Pricing Presenter: Joshua Taub, FCAS CAS Ratemaking and Product Management Seminar March 30, 2014 Washington, D.C. 1 / 34 CAS Antitrust Notice The Casualty

Workshop 5: Large Account Pricing Large Account Pricing Presenter: Joshua Taub, FCAS CAS Ratemaking and Product Management Seminar March 30, 2014 Washington, D.C. 1 / 34 CAS Antitrust Notice The Casualty

Risk pricing for Australian Motor Insurance

Risk pricing for Australian Motor Insurance Dr Richard Brookes November 2012 Contents 1. Background Scope How many models? 2. Approach Data Variable filtering GLM Interactions Credibility overlay 3. Model

Risk pricing for Australian Motor Insurance Dr Richard Brookes November 2012 Contents 1. Background Scope How many models? 2. Approach Data Variable filtering GLM Interactions Credibility overlay 3. Model

Time Series Analysis

Time Series Analysis [email protected] Informatics and Mathematical Modelling Technical University of Denmark DK-2800 Kgs. Lyngby 1 Outline of the lecture Identification of univariate time series models, cont.:

Time Series Analysis [email protected] Informatics and Mathematical Modelling Technical University of Denmark DK-2800 Kgs. Lyngby 1 Outline of the lecture Identification of univariate time series models, cont.:

Data Mining Techniques Chapter 6: Decision Trees

Data Mining Techniques Chapter 6: Decision Trees What is a classification decision tree?.......................................... 2 Visualizing decision trees...................................................

Data Mining Techniques Chapter 6: Decision Trees What is a classification decision tree?.......................................... 2 Visualizing decision trees...................................................

SOA 2013 Life & Annuity Symposium May 6-7, 2013. Session 30 PD, Predictive Modeling Applications for Life and Annuity Pricing and Underwriting

SOA 2013 Life & Annuity Symposium May 6-7, 2013 Session 30 PD, Predictive Modeling Applications for Life and Annuity Pricing and Underwriting Moderator: Barry D. Senensky, FSA, FCIA, MAAA Presenters: Jonathan

SOA 2013 Life & Annuity Symposium May 6-7, 2013 Session 30 PD, Predictive Modeling Applications for Life and Annuity Pricing and Underwriting Moderator: Barry D. Senensky, FSA, FCIA, MAAA Presenters: Jonathan

15.1 The Structure of Generalized Linear Models

15 Generalized Linear Models Due originally to Nelder and Wedderburn (1972), generalized linear models are a remarkable synthesis and extension of familiar regression models such as the linear models described

15 Generalized Linear Models Due originally to Nelder and Wedderburn (1972), generalized linear models are a remarkable synthesis and extension of familiar regression models such as the linear models described

A Comparison of Variable Selection Techniques for Credit Scoring

1 A Comparison of Variable Selection Techniques for Credit Scoring K. Leung and F. Cheong and C. Cheong School of Business Information Technology, RMIT University, Melbourne, Victoria, Australia E-mail:

1 A Comparison of Variable Selection Techniques for Credit Scoring K. Leung and F. Cheong and C. Cheong School of Business Information Technology, RMIT University, Melbourne, Victoria, Australia E-mail:

Poisson Models for Count Data

Chapter 4 Poisson Models for Count Data In this chapter we study log-linear models for count data under the assumption of a Poisson error structure. These models have many applications, not only to the

Chapter 4 Poisson Models for Count Data In this chapter we study log-linear models for count data under the assumption of a Poisson error structure. These models have many applications, not only to the

Why do statisticians "hate" us?

Why do statisticians "hate" us? David Hand, Heikki Mannila, Padhraic Smyth "Data mining is the analysis of (often large) observational data sets to find unsuspected relationships and to summarize the data

Why do statisticians "hate" us? David Hand, Heikki Mannila, Padhraic Smyth "Data mining is the analysis of (often large) observational data sets to find unsuspected relationships and to summarize the data

Principle Component Analysis and Partial Least Squares: Two Dimension Reduction Techniques for Regression

Principle Component Analysis and Partial Least Squares: Two Dimension Reduction Techniques for Regression Saikat Maitra and Jun Yan Abstract: Dimension reduction is one of the major tasks for multivariate

Principle Component Analysis and Partial Least Squares: Two Dimension Reduction Techniques for Regression Saikat Maitra and Jun Yan Abstract: Dimension reduction is one of the major tasks for multivariate

Accurately and Efficiently Measuring Individual Account Credit Risk On Existing Portfolios

Accurately and Efficiently Measuring Individual Account Credit Risk On Existing Portfolios By: Michael Banasiak & By: Daniel Tantum, Ph.D. What Are Statistical Based Behavior Scoring Models And How Are

Accurately and Efficiently Measuring Individual Account Credit Risk On Existing Portfolios By: Michael Banasiak & By: Daniel Tantum, Ph.D. What Are Statistical Based Behavior Scoring Models And How Are

Simple Linear Regression

STAT 101 Dr. Kari Lock Morgan Simple Linear Regression SECTIONS 9.3 Confidence and prediction intervals (9.3) Conditions for inference (9.1) Want More Stats??? If you have enjoyed learning how to analyze

STAT 101 Dr. Kari Lock Morgan Simple Linear Regression SECTIONS 9.3 Confidence and prediction intervals (9.3) Conditions for inference (9.1) Want More Stats??? If you have enjoyed learning how to analyze

Aspects of Risk Adjustment in Healthcare

Aspects of Risk Adjustment in Healthcare 1. Exploring the relationship between demographic and clinical risk adjustment Matthew Myers, Barry Childs 2. Application of various statistical measures to hospital

Aspects of Risk Adjustment in Healthcare 1. Exploring the relationship between demographic and clinical risk adjustment Matthew Myers, Barry Childs 2. Application of various statistical measures to hospital

Section 6: Model Selection, Logistic Regression and more...

Section 6: Model Selection, Logistic Regression and more... Carlos M. Carvalho The University of Texas McCombs School of Business http://faculty.mccombs.utexas.edu/carlos.carvalho/teaching/ 1 Model Building

Section 6: Model Selection, Logistic Regression and more... Carlos M. Carvalho The University of Texas McCombs School of Business http://faculty.mccombs.utexas.edu/carlos.carvalho/teaching/ 1 Model Building

The IRS Is Knocking Are You Ready?

The IRS Is Knocking Are You Ready? Casualty Loss Reserve Seminar Denver, Colorado September 5-7, 2012 Presented by: Travis J Grulkowski, FCAS, MAAA Principal & Consulting Actuary Milliman, Inc. 262-796-3319

The IRS Is Knocking Are You Ready? Casualty Loss Reserve Seminar Denver, Colorado September 5-7, 2012 Presented by: Travis J Grulkowski, FCAS, MAAA Principal & Consulting Actuary Milliman, Inc. 262-796-3319

13. Poisson Regression Analysis

136 Poisson Regression Analysis 13. Poisson Regression Analysis We have so far considered situations where the outcome variable is numeric and Normally distributed, or binary. In clinical work one often

136 Poisson Regression Analysis 13. Poisson Regression Analysis We have so far considered situations where the outcome variable is numeric and Normally distributed, or binary. In clinical work one often

BNG 202 Biomechanics Lab. Descriptive statistics and probability distributions I

BNG 202 Biomechanics Lab Descriptive statistics and probability distributions I Overview The overall goal of this short course in statistics is to provide an introduction to descriptive and inferential

BNG 202 Biomechanics Lab Descriptive statistics and probability distributions I Overview The overall goal of this short course in statistics is to provide an introduction to descriptive and inferential