GENERAL EQUILIBRIUM WITH BANKS AND THE FACTOR-INTENSITY CONDITION

|

|

|

- Horace Spencer

- 8 years ago

- Views:

Transcription

1 GENERAL EQUILIBRIUM WITH BANKS AND THE FACTOR-INTENSITY CONDITION Emanuel R. Leão Pedro R. Leão Junho 2008 WP nº 2008/63 DOCUMENTO DE TRABALHO WORKING PAPER

2 General Equilibrium with Banks and the Factor-Intensity Condition Emanuel R. Leão 1 Pedro R. Leão 2 WP nº 2008/63 Junho de 2008 Abstract 1. INTRODUCTION 3 2. THE MODEL 3 3. THE FACTOR-INTENSITY CONDITION 7 4. REVERSING THE FACTOR-INTENSITY CONDITION 8 5. WHY ARE THE RESPONSES OF SECTORAL OUTPUTS NOT DEPENDENT UPON THE FACTOR-INTENSITY CONDITION? CONCLUSION 13 REFERENCES 14 ANNEXES 1 Departament of Economics, Instituto Superior de Ciências do Trabalho e da Empresa and Dinâmia Centro de Estudos sobre a Mudança Socioeconómica, Avenida das Forcas Armadas, Lisboa, Portugal, Phone: , Fax: emanuel.leao@iscte.pt 2 Department of Economics, Instituto Superior de Economia e Gestão, Technical University of Lisbon and UECE, Rua Miguel Lupi, Nº 20, 1200 Lisboa, Portugal pleao@iseg.utl.pt ISCTE INSTITUTO SUPERIOR DE CIÊNCIAS DO TRABALHO E DA EMPRESA Av. das Forças Armadas, Lisboa, PORTUGAL Tel Fax dinamia@iscte.pt Internet:

3 General Equilibrium with Banks and the Factor-Intensity Condition General Equilibrium with Banks and the Factor-Intensity Condition* Abstract This paper looks at the role played by the factor-intensity condition in the model developed by Leao (2003). To do this, we examine how the model reacts when the factor-intensity condition is reversed so that the banking industry ceases to be the capital intensive sector and becomes the labour intensive sector. Simulation results show that, in general, the qualitative nature of the results does not change. However, there two cases where the qualitative results are affected: the response of the real wage and of the labour supply to a shock in the banks technological parameter. We present an interpretation for these results based in part on the framework devised by Heckscher and Ohlin. We conclude that the factor-intensity condition does play a significant role in the model of Leao (2003). Keywords: general equilibrium, banking industry, factor-intensity condition, Heckscher-Ohlin framework, sectoral shocks, allocation of capital and work hours between sectors. JEL classification: E17, E22, E24, E32. * We have received helpful comments from Mário Olivares. They are in no way responsible for our interpretations or any errors that the paper may contain. ISCTE INSTITUTO SUPERIOR DE CIÊNCIAS DO TRABALHO E DA EMPRESA Av. das Forças Armadas, Lisboa, PORTUGAL Tel Fax dinamia@iscte.pt Internet:

4 1 Introduction Leao (2003) develops a model with two sectors - output sector and banking sector - and two factors of production in each sector (physical capital and labour effort). With the parameters used in his work, the banking sector is the capital intensive sector. In the present paper, we examine the role of the factor-intensity condition in his model: we change the parameters of the model so that the output sector becomes the capital intensive sector and we then make simulation experiments to see if this implies any significant modification to the results. We conclude that, in general, the qualitative results do not change when the banking industry ceases to be the capital intensive industry and becomes the labour intensive industry. There is, however, one interesting qualitative change: the response of the real wage and of the labour supply to a technological improvement in banks. After showing the simulation results and pointing out the difference, we present an interpretation based on the framework devised by Heckscher and Ohlin. 2 The Model In the model of Leao (2003), there are households, firms and banks. The typical household s utility function is denoted u(c t, 1 n s t), wherec t is consumption and n s t typical firm s production function is written y t = A t F (k t,n d t ), wherey t is labour supply. The is real output, A t is a technological parameter, k t is the capital stock and n d t is labour demand. The typical bank s production function is given by b s t = D t (kt b ) 1 γ (n b t) γ,whereb s t is the bank s supply of credit in real terms, D t is a technological parameter, kt b is the stock of capital of the bank and n b t is the number of work hours hired by the bank. Page: 3

5 Households borrow from banks and then use the money thus obtained to buy goods from firms. There are five markets: goods market, labour market, bank loans market, firm shares market and bank shares market. As can be seen on page 157 of his paper, the competitive equilibrium is given by the following set of equations: u 1 (c t, 1 n s t)=λ t (1) u 2 (c t, 1 n s t)=βe t [λ t+1 ] w t 1+E t [ p t+1 ] (2) λ t = βe t [λ t+1 ] 1+R t 1+E t [ p t+1 ] (3) b t+1 1+R t = c t (4) A t F 2 (k t, n d t )=w t (5) E t [A t+1 ] F 1 kt+1,e t n d t+1 +(1 δ) = 1+E t [R t+1 ] 1+E t [ p t+1 ] (6) Page: 4

=βe t [λ t+1 ] w t 1+E t [ p t+1 ] (2) λ t = βe t [λ t+1 ] 1+R t 1+E t [ p t+1 ] (3) b t+1 1+R t = c t (4) A t F 2 (k t, n d t )=w t")

6 ³ R t D t γ k b n b γ 1 t 1 γ t = wt (7) ³ E t [R t+1 ] E t [D t+1 ](1 γ) k b Et t+1 γ n b γ t+1 +(1 δb )= = 1+E t [R t+1 ] 1+E t [ p t+1 ] (8) c t + i k t+1 (1 δ)k t + hk b t+1 (1 δ B )k b t = A t F (k t, n d t ) (9) n s t = n d t + n b t (10) b ³ t+1 = D t k b n b γ t 1 γ 1+R t (11) t z f t+1 = 1 H (12) Page: 5

b ³ t+1 = D t k b n b γ t 1 γ 1+R t (11) t z f t+1 = 1 H (12)")

7 z bank,l t+1 = 1 H (13) for t =0, 1, 2, 3,... where λ t is a Lagrangean multiplier, w t is the real wage, p t+1 istherateofinflation between period t and period (t+1), R t is the interest rate on bank loans, b t+1 is borrowing per household in real terms, z f t+1 is the share of firm f owned by each household, and zbank,l t+1 is the share of bank l owned by each household. H is the number of households. β is a discount factor (0 <β<1) that reflects a preference for current over future consumption-leisure bundles. δ B is the rate of depreciation of the banks capital stock and δ is the rate of depreciation of the firms capital stock. The operator E t [.] yields the mathematical expectation of the indicated argument. u 1 (, ) denotes the partial derivative of u(c t, 1 n s t) with respect to its first variable. Variables with a bar on top are per household variables. Equations (1)-(4) have their origin in the typical household s first order conditions. Equations (5) and (6) have their origin in the typical firm s first-order conditions. Equations (7) and (8) have their origin in the typical bank s first-order conditions. Equations (9)-(13) are the market clearing conditions. There are two exogenous variables (A t and D t ) and thirteen endogenous variables. The firm s production function and household s utility function used were A t F (k t,n d t )= A t (k t ) 1 α n d α t and u(ct, t )=lnc t + φ ln(1 n s t). To look at the response of the model (1)-(13) to shocks in the exogenous variables (A t and D t ), we log-linearize each of the equations around the steady-state value of its variables and then use the method of King, Plosser and Rebelo (1988) which is based on Blanchard and Khan (1980). Page: 6

that reflects a preference for current over future consumption-leisure bundles.")

8 3 The Factor-Intensity Condition Since there are two sectors that both use capital and labour, there is a (capital / labour) ratio for each sector: (k t /n d t ) in the case of the output sector; and (k b t/n b t) inthecaseofthebankingsector. The ratio between these two ratios is known as the factor-intensity condition. In our study of the dynamic properties of this type of models, we always start from the steadystate of the model. On the other hand, because of the linearization, our analysis is only valid around the steady-state. Hence, we are specially interested in knowing the value of the factor-intensity condition in the steady-state. Using the equations that correspond to the first-order conditions of the firms problem and first order conditions of the banks problem [equations (5), (6), (7) and (8)], it is possible to show that, in the steady-state, the factor-intensity condition is given by (k/n d ) (k b /n b ) = 1 α α γ 1 γ r + δ B r + δ where k is the firms capital stock, n d is work hours in firms, k b is the banks capital stock, n b is work hours in banks, α is the firms Cobb-Douglas parameter, γ is the banks Cobb-Douglas parameter, r is the real interest rate, δ B is the rate of depreciation of the banks capital stock and δ is the rate of depreciation of the firms capital stock. Using the values of α, γ, δ B, δ and r that were obtained by calibrating the model with U.S. data - see section 8 of Leao (2003) - we conclude that, in the steady-state, the value of the factor-intensity condition is (k/n d ) (k b /n b =0.19 (14) ) which means that in Leao (2003) the banking sector is the capital intensive sector. Small deviations from the steady-state are not strong enough to cause a reversal of this value of the factor-intensity condition. Page: 7

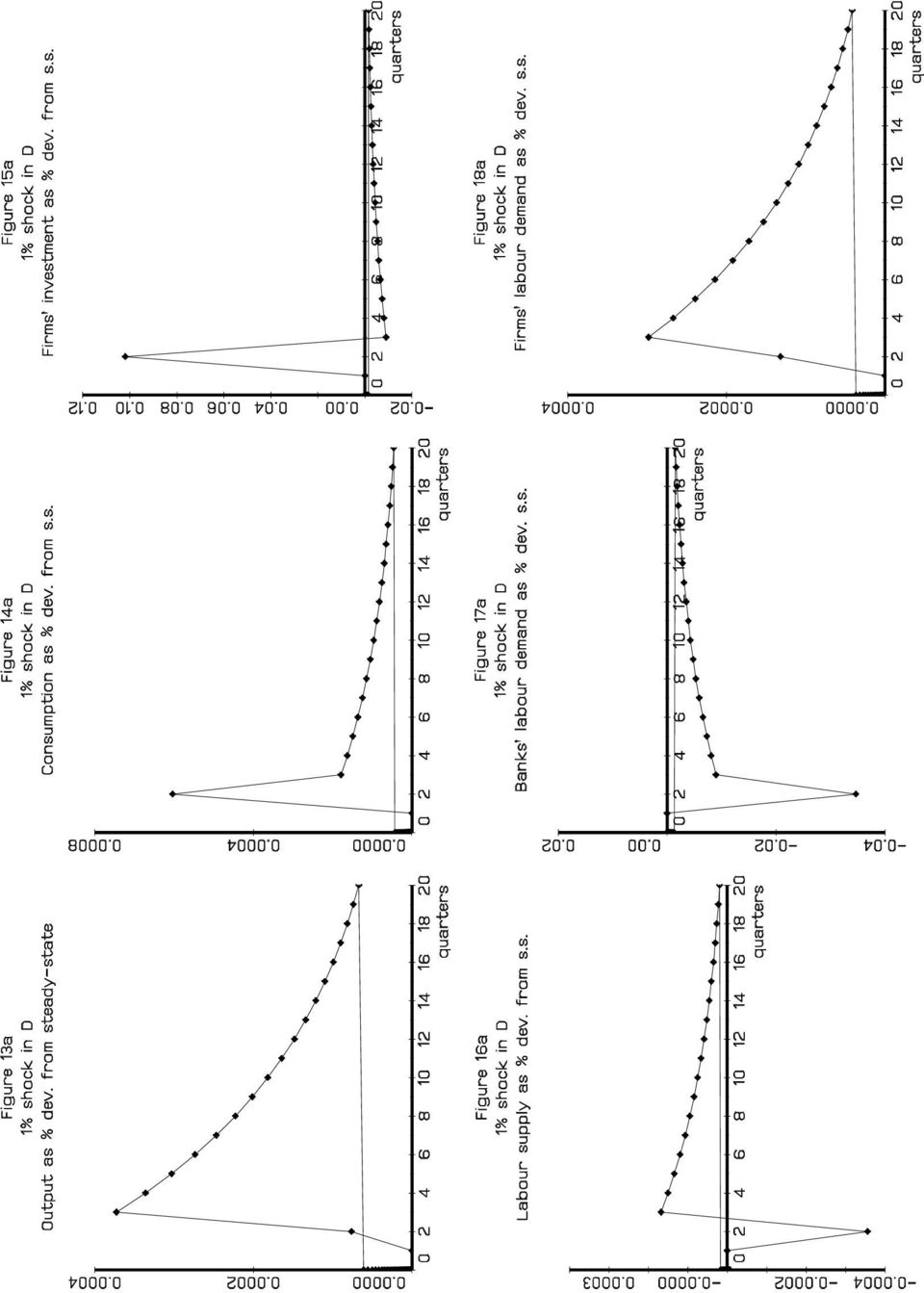

9 Leao (2003) performs two types of impulse response experiments: a shock in the firms technological parameter (A t ) and a shock in the banks technological parameter (D t ). The results of the impulse response exercises - obtained with the factor-intensity condition (14) - are shown in figures 1 to 24 of Leao (2003) and are reproduced for convenience at the end of the present paper with the numbering (1a) to (24a). Note, in particular, that when a technological improvement occurs in banks, some capital and labour are transferred from banks to firms (figures 17a, 18a, 23a and 24a). The reason why this happens is as follows: when a technological improvement occurs in banks, the amount of credit that the banks can supply with their existing resources increases automatically (through the banks production functions). However, bank credit in itself does not give utility to households. Bank credit only becomes useful if used to finance consumption. Therefore, some capital and labour are transferred from banks to firms to allow an increase in output that will permit consumption to rise along with bank credit (the more powerful technology in banks enables them to supply more credit even with fewer resources). 4 Reversing the Factor-Intensity Condition The main goal of the present paper is to examine the role of the factor-intensity condition in the model of Leao (2003). To do this, we reverse the factor-intensity condition so that the banking industry ceases to be the capital intensive industry and becomes the labour intensive industry. We can change the factor-intensity condition by changing the values used for α, γ, δ B, δ and/or r. We did several experiments and the main conclusions can be illustrated using the following example. If we use γ =0.78 and take into account the implied change in the calibrated δ B, then the factor-intensity condition becomes The impulse response results obtained with this Page: 8

.")

10 factor-intensity condition are shown in figures (1b) to (24b). We can see that in general - when compared to figures (1a) to (24a), which are the results of Leao (2003) - the results do not change qualitatively although they change quantitatively. In particular, the results we obtain with a 1% technological shock in firms (1% shock in A) are approximately the same as before. The variables more affected are the variables directly related to the banking system. On the other hand, the results we obtain with a 1% technological shock in banks (1% shock in D) show the same pattern as before but change in quantitative way (the response is, in general, less pronounced). We conclude that, in general, the qualitative results do not change when the banking industry ceases to be the capital intensive industry and becomes the labour intensive industry. There is, however, one interesting qualitative change: the response of the real wage and of the labour supply to a technological improvement in banks. If we ignore period 2 (which is the period where the shock occurs and hence is different from the following periods because capital cannot adjust), we can see that the effect on those two variables of a technological innovation in banks is the opposite of the results we have in Leao (2003): the real wage falls and the labour supply also falls (compare figure 16a to figure 16b and figure 21a to figure 21b). Let us try to explain why this happens. We have seen that when a technological improvement occurs in banks there is a transfer of capital and labour from banks to firms. When the banking sector is the labour intensive sector, it will release relatively more labour than capital (when compared with the case where the banking sector is the capital intensive sector). This stronger release of work hours will exert downward pressure on the real wage and this will make the labour supply fall. The conclusion to be drawn is that the factor-intensity condition does play a role in the model. Page: 9

11 5 Why are the responses of sectoral outputs not dependent upon the factor-intensity condition? The interpretation we have just provided is typical of Heckscher-Ohlin models. There is however one notable difference between our results and the typical H-O results. In the H-O framework, the changes of sectoral outputs often depend upon the factor-intensity condition. By contrast, in the two-sector and two-factor model we are looking at, the qualitative nature of results regarding the changes in real output and in bank credit do not depend on the factor-intensity condition (when a technological innovation occurs in one sector, output always rises in both sectors). Let us try to explain why. 5.1 The Heckscher-Ohlin framework In the Hecksher-Ohlin framework, the response of the sectoral outputs to exogenous shocks may depend on the factor-intensity condition, even in a closed economy. For example, an increase in the endowment of capital may lead to an increase in the output of the capital intensive sector and to a reduction in the output of the labour intensive sector. In fact, an increase in the endowment of capital leads to a reduction in the price of capital relative to the price of labour. As a result, there is a reduction in the relative marginal cost and therefore in the relative price of the capital intensive good. This raises the demand for this good at the expense of the demand for the labour intensive good. The price effect of an increase in the endowment of capital is thus an increase in the output of the capital intensive sector at the expense of the output of the labour intensive sector. Of course, the increase in the capital endowment also increases the wealth of the economy, and this positive wealth effect increases the demand and output in both sectors. Hence, an increase Page: 10

. Let us try to explain why. 5.")

12 in the endowment of capital leads to a reduction in the output of the labour intensive sector only if its negative price effect on this sector is greater than its positive wealth effect 1. In an analogous way, in the Hecksher-Ohlin framework a neutral technological improvement in (for example) the capital intensive sector may lead to an increase in the output of this sector and a reduction in the output of the labour intensive sector. In fact, a technological improvement in the capital intensive sector reduces the relative marginal cost and therefore the relative price of the capital intensive good. This raises the demand and output of this good at the expense of the demand and output of the labour intensive good. Obviously, the technological improvement also increases the wealth of the economy, and this wealth effect increases the demand and output in both sectors. Therefore, a technological improvement in the capital intensive sector leads to a reduction in the output of the labour intensive sector only if its negative price effect on this sector is greater than its positive wealth effect. The same results are obtained, mutatis mutandis, fortheeffectofanincreaseintheen- dowment of labour and for a neutral technological improvement in the labour intensive sector. 5.2 The model of Leao (2003) In the model of Leao (2003), the response of sectoral outputs to exogenous shocks does not depend on the factor intensity condition. We can see in figures 1a, 2a, 13a, 14a, 1b, 2b, 13b and 14b that whenever a technological improvement occurs in one sector, output rises in both sectors (note that the output of the banking sector is bank credit in real terms which, in this model, corresponds to consumption in real terms). The reason for these results is as follows. 1 In a small open economy, a stronger assertion is true. According to the Rybczinsky Theorem, an increase in the endowment of capital always leads to an increase in the output of the capital intensive sector and to a reduction in the output of the labour intensive sector. Page: 11

13 When a technological improvement occurs in nonbank firms, output increases automatically (through the firms production functions). More output will translate into higher utility levels by an increase in consumption. However, this increase in desired consumption can only materialize if there is an increase in the supply of bank credit that allows households to buy more consumption goods (the increase in bank credit is obtained by an increase in work hours in the banking industry). Note that the qualitative nature of the changes of sectoral outputs implied by this shock in the nonbank firms technology is the same (increase in output and increase in bank credit) irrespective of which sector is capital intensive. On the other hand, as already mentioned, when a technological improvement occurs in banks, the amount of credit that the banks can supply with their existing resources increases automatically (through the banks production functions). However, bank credit in itself does not give utility to households. Therefore, some capital and labour are transferred from banks to firms to allow an increase in output that will permit consumption to rise along with bank credit (the more powerful technology in banks enables them to supply more credit even with fewer resources). Note that the qualitative nature of these changes of sectoral outputs (increase in output and increase in bank credit) does not depend on which sector is capital intensive. 5.3 Rationalization We may rationalize as follows. Although the model of Leao (2003) has the basic Heckscher-Ohlin features - two sectors and two factors of production -, there is one important difference between his model and the standard Heckscher-Ohlin framework. In Leao (2003), the output of the banking sector is bank credit and bank credit in itself does not give utility to households. The only use of bank credit is to finance consumption (which in his model corresponds to over 80% of total Page: 12

.")

14 output). On the other hand, if they wish to increase consumption, households must borrow from the banks; and so the banking sector can be seen as an intermediate sector that produces an input - credit -which is necessary for the other sector to be able to sell its output. This means that the production of the two sectors is not independent in Leao (2003): it is not possible to increase consumption without raising the supply of bank credit; and it does not make sense in economic terms to increase the supply of bank credit without an increase in consumption. In the Heckscher-Ohlin framework, we have two goods which directly affect the households utility and there is no complementarity whatsoever between the two sectors. Therefore, it is perfectly possible for the output of one sector to rise while the output of the other sector falls. 6 Conclusion Leao (2003) builds a model with two sectors: output sector and banking sector. We have looked at how the impulse response results from his model are affected by reversing the factor-intensity condition. Wehaveconcludedthat,with two exceptions, thequalitative nature of the results is not affected. In particular, when a technological shock occurs in one sector, output rises in both sectors. The only cases where the impulse response results are reversed are the response of the real wage and of the labour supply to a shock in the banks technological parameter. We have provided an interpretation based on the framework devised by Heckscher and Ohlin. The results we obtained confirm that the factor-intensity condition plays an important role in the model of Leao (2003). This role is however less important than it is in the Heckscher-Ohlin framework. Page: 13

: it is not possible to increase consumption without raising the supply of bank credit; and it does not make sense")

15 References [1] Blanchard, O. and Khan, C. (1980). The solution of linear difference models under rational expectations. Econometrica 48: [2] Hansen, G Indivisible labor and the business cycle. Journal of Monetary Economics 56: [3] King, R., Plosser, C. and Rebelo, S. (1988). Production, growth and business cycles: I. The basic neoclassical model. Journal of Monetary Economics 21: [4] Kydland, F. and Prescott, E. (1982). Time to build and aggregate fluctuations. Econometrica 50: [5] Leao, E. (2003). A dynamic general equilibrium model with technological innovations in the banking sector. Journal of Economics (Zeitschrift für Nationalökonomie) 79: [6] Long, J. and Plosser, C. (1983). Real Business Cycles. Journal of Political Economy 91: [7] Rybczynski, T. (1955). Factor endowment and relative commodity prices. Economica 22: Page: 14

![The basic neoclassical model. Journal of Monetary Economics 21: 195-232. [4] Kydland, F. and Prescott, E. (1982). Time to build and aggregate fluctuations. Econometrica 50: 1345-1370. [5] Leao, E.](/docs-images/57/6958385/images/page_15.jpg "(2003). A dynamic general equilibrium model with technological innovations in the banking sector. Journal of Economics (Zeitschrift für Nationalökonomie) 79: 145-185. [6] Long, J. and Plosser, C.")

16

17

18

19

20

21

22

23

VI. Real Business Cycles Models

VI. Real Business Cycles Models Introduction Business cycle research studies the causes and consequences of the recurrent expansions and contractions in aggregate economic activity that occur in most industrialized

VI. Real Business Cycles Models Introduction Business cycle research studies the causes and consequences of the recurrent expansions and contractions in aggregate economic activity that occur in most industrialized

2. Real Business Cycle Theory (June 25, 2013)

") Prof. Dr. Thomas Steger Advanced Macroeconomics II Lecture SS 13 2. Real Business Cycle Theory (June 25, 2013) Introduction Simplistic RBC Model Simple stochastic growth model Baseline RBC model Introduction

Prof. Dr. Thomas Steger Advanced Macroeconomics II Lecture SS 13 2. Real Business Cycle Theory (June 25, 2013) Introduction Simplistic RBC Model Simple stochastic growth model Baseline RBC model Introduction

The Specific-Factors Model: HO Model in the Short Run

The Specific-Factors Model: HO Model in the Short Run Rahul Giri Contact Address: Centro de Investigacion Economica, Instituto Tecnologico Autonomo de Mexico (ITAM). E-mail: rahul.giri@itam.mx In this

The Specific-Factors Model: HO Model in the Short Run Rahul Giri Contact Address: Centro de Investigacion Economica, Instituto Tecnologico Autonomo de Mexico (ITAM). E-mail: rahul.giri@itam.mx In this

The RBC methodology also comes down to two principles:

Chapter 5 Real business cycles 5.1 Real business cycles The most well known paper in the Real Business Cycles (RBC) literature is Kydland and Prescott (1982). That paper introduces both a specific theory

Chapter 5 Real business cycles 5.1 Real business cycles The most well known paper in the Real Business Cycles (RBC) literature is Kydland and Prescott (1982). That paper introduces both a specific theory

UNIVERSITY OF OSLO DEPARTMENT OF ECONOMICS

UNIVERSITY OF OSLO DEPARTMENT OF ECONOMICS Exam: ECON4310 Intertemporal macroeconomics Date of exam: Thursday, November 27, 2008 Grades are given: December 19, 2008 Time for exam: 09:00 a.m. 12:00 noon

UNIVERSITY OF OSLO DEPARTMENT OF ECONOMICS Exam: ECON4310 Intertemporal macroeconomics Date of exam: Thursday, November 27, 2008 Grades are given: December 19, 2008 Time for exam: 09:00 a.m. 12:00 noon

ECON20310 LECTURE SYNOPSIS REAL BUSINESS CYCLE

ECON20310 LECTURE SYNOPSIS REAL BUSINESS CYCLE YUAN TIAN This synopsis is designed merely for keep a record of the materials covered in lectures. Please refer to your own lecture notes for all proofs.

ECON20310 LECTURE SYNOPSIS REAL BUSINESS CYCLE YUAN TIAN This synopsis is designed merely for keep a record of the materials covered in lectures. Please refer to your own lecture notes for all proofs.

Real Business Cycles. Federal Reserve Bank of Minneapolis Research Department Staff Report 370. February 2006. Ellen R. McGrattan

Federal Reserve Bank of Minneapolis Research Department Staff Report 370 February 2006 Real Business Cycles Ellen R. McGrattan Federal Reserve Bank of Minneapolis and University of Minnesota Abstract:

Federal Reserve Bank of Minneapolis Research Department Staff Report 370 February 2006 Real Business Cycles Ellen R. McGrattan Federal Reserve Bank of Minneapolis and University of Minnesota Abstract:

Graduate Macro Theory II: The Real Business Cycle Model

Graduate Macro Theory II: The Real Business Cycle Model Eric Sims University of Notre Dame Spring 2011 1 Introduction This note describes the canonical real business cycle model. A couple of classic references

Graduate Macro Theory II: The Real Business Cycle Model Eric Sims University of Notre Dame Spring 2011 1 Introduction This note describes the canonical real business cycle model. A couple of classic references

Cash in advance model

Chapter 4 Cash in advance model 4.1 Motivation In this lecture we will look at ways of introducing money into a neoclassical model and how these methods can be developed in an effort to try and explain

Chapter 4 Cash in advance model 4.1 Motivation In this lecture we will look at ways of introducing money into a neoclassical model and how these methods can be developed in an effort to try and explain

Advanced Macroeconomics (2)

") Advanced Macroeconomics (2) Real-Business-Cycle Theory Alessio Moneta Institute of Economics Scuola Superiore Sant Anna, Pisa amoneta@sssup.it March-April 2015 LM in Economics Scuola Superiore Sant Anna

Advanced Macroeconomics (2) Real-Business-Cycle Theory Alessio Moneta Institute of Economics Scuola Superiore Sant Anna, Pisa amoneta@sssup.it March-April 2015 LM in Economics Scuola Superiore Sant Anna

The Real Business Cycle Model

The Real Business Cycle Model Ester Faia Goethe University Frankfurt Nov 2015 Ester Faia (Goethe University Frankfurt) RBC Nov 2015 1 / 27 Introduction The RBC model explains the co-movements in the uctuations

The Real Business Cycle Model Ester Faia Goethe University Frankfurt Nov 2015 Ester Faia (Goethe University Frankfurt) RBC Nov 2015 1 / 27 Introduction The RBC model explains the co-movements in the uctuations

Universidad de Montevideo Macroeconomia II. The Ramsey-Cass-Koopmans Model

Universidad de Montevideo Macroeconomia II Danilo R. Trupkin Class Notes (very preliminar) The Ramsey-Cass-Koopmans Model 1 Introduction One shortcoming of the Solow model is that the saving rate is exogenous

Universidad de Montevideo Macroeconomia II Danilo R. Trupkin Class Notes (very preliminar) The Ramsey-Cass-Koopmans Model 1 Introduction One shortcoming of the Solow model is that the saving rate is exogenous

The Real Business Cycle model

The Real Business Cycle model Spring 2013 1 Historical introduction Modern business cycle theory really got started with Great Depression Keynes: The General Theory of Employment, Interest and Money Keynesian

The Real Business Cycle model Spring 2013 1 Historical introduction Modern business cycle theory really got started with Great Depression Keynes: The General Theory of Employment, Interest and Money Keynesian

A Review of the Literature of Real Business Cycle theory. By Student E XXXXXXX

A Review of the Literature of Real Business Cycle theory By Student E XXXXXXX Abstract: The following paper reviews five articles concerning Real Business Cycle theory. First, the review compares the various

A Review of the Literature of Real Business Cycle theory By Student E XXXXXXX Abstract: The following paper reviews five articles concerning Real Business Cycle theory. First, the review compares the various

Why Does Consumption Lead the Business Cycle?

Why Does Consumption Lead the Business Cycle? Yi Wen Department of Economics Cornell University, Ithaca, N.Y. yw57@cornell.edu Abstract Consumption in the US leads output at the business cycle frequency.

Why Does Consumption Lead the Business Cycle? Yi Wen Department of Economics Cornell University, Ithaca, N.Y. yw57@cornell.edu Abstract Consumption in the US leads output at the business cycle frequency.

Calibration of Normalised CES Production Functions in Dynamic Models

Discussion Paper No. 06-078 Calibration of Normalised CES Production Functions in Dynamic Models Rainer Klump and Marianne Saam Discussion Paper No. 06-078 Calibration of Normalised CES Production Functions

Discussion Paper No. 06-078 Calibration of Normalised CES Production Functions in Dynamic Models Rainer Klump and Marianne Saam Discussion Paper No. 06-078 Calibration of Normalised CES Production Functions

MA Advanced Macroeconomics: 7. The Real Business Cycle Model

MA Advanced Macroeconomics: 7. The Real Business Cycle Model Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) Real Business Cycles Spring 2015 1 / 38 Working Through A DSGE Model We have

MA Advanced Macroeconomics: 7. The Real Business Cycle Model Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) Real Business Cycles Spring 2015 1 / 38 Working Through A DSGE Model We have

This paper is not to be removed from the Examination Halls

This paper is not to be removed from the Examination Halls UNIVERSITY OF LONDON EC2065 ZA BSc degrees and Diplomas for Graduates in Economics, Management, Finance and the Social Sciences, the Diplomas

This paper is not to be removed from the Examination Halls UNIVERSITY OF LONDON EC2065 ZA BSc degrees and Diplomas for Graduates in Economics, Management, Finance and the Social Sciences, the Diplomas

Lecture 1: The intertemporal approach to the current account

Lecture 1: The intertemporal approach to the current account Open economy macroeconomics, Fall 2006 Ida Wolden Bache August 22, 2006 Intertemporal trade and the current account What determines when countries

Lecture 1: The intertemporal approach to the current account Open economy macroeconomics, Fall 2006 Ida Wolden Bache August 22, 2006 Intertemporal trade and the current account What determines when countries

Real Business Cycle Theory

Real Business Cycle Theory Guido Ascari University of Pavia () Real Business Cycle Theory 1 / 50 Outline Introduction: Lucas methodological proposal The application to the analysis of business cycle uctuations:

Real Business Cycle Theory Guido Ascari University of Pavia () Real Business Cycle Theory 1 / 50 Outline Introduction: Lucas methodological proposal The application to the analysis of business cycle uctuations:

1 National Income and Product Accounts

Espen Henriksen econ249 UCSB 1 National Income and Product Accounts 11 Gross Domestic Product (GDP) Can be measured in three different but equivalent ways: 1 Production Approach 2 Expenditure Approach

Espen Henriksen econ249 UCSB 1 National Income and Product Accounts 11 Gross Domestic Product (GDP) Can be measured in three different but equivalent ways: 1 Production Approach 2 Expenditure Approach

Real Business Cycle Models

Phd Macro, 2007 (Karl Whelan) 1 Real Business Cycle Models The Real Business Cycle (RBC) model introduced in a famous 1982 paper by Finn Kydland and Edward Prescott is the original DSGE model. 1 The early

Phd Macro, 2007 (Karl Whelan) 1 Real Business Cycle Models The Real Business Cycle (RBC) model introduced in a famous 1982 paper by Finn Kydland and Edward Prescott is the original DSGE model. 1 The early

Government Consumption Expenditures and the Current Account

FEDERAL RESERVE BANK OF SAN FRANCISCO WORKING PAPER SERIES Government Consumption Expenditures and the Current Account Michele Cavallo Federal Reserve Bank of San Francisco February 25 Working Paper 25-3

FEDERAL RESERVE BANK OF SAN FRANCISCO WORKING PAPER SERIES Government Consumption Expenditures and the Current Account Michele Cavallo Federal Reserve Bank of San Francisco February 25 Working Paper 25-3

CHAPTER 11. AN OVEVIEW OF THE BANK OF ENGLAND QUARTERLY MODEL OF THE (BEQM)

") 1 CHAPTER 11. AN OVEVIEW OF THE BANK OF ENGLAND QUARTERLY MODEL OF THE (BEQM) This model is the main tool in the suite of models employed by the staff and the Monetary Policy Committee (MPC) in the construction

1 CHAPTER 11. AN OVEVIEW OF THE BANK OF ENGLAND QUARTERLY MODEL OF THE (BEQM) This model is the main tool in the suite of models employed by the staff and the Monetary Policy Committee (MPC) in the construction

The real business cycle theory

Chapter 29 The real business cycle theory Since the middle of the 1970s two quite different approaches to the explanation of business cycle fluctuations have been pursued. We may broadly classify them

Chapter 29 The real business cycle theory Since the middle of the 1970s two quite different approaches to the explanation of business cycle fluctuations have been pursued. We may broadly classify them

Inflation. Chapter 8. 8.1 Money Supply and Demand

Chapter 8 Inflation This chapter examines the causes and consequences of inflation. Sections 8.1 and 8.2 relate inflation to money supply and demand. Although the presentation differs somewhat from that

Chapter 8 Inflation This chapter examines the causes and consequences of inflation. Sections 8.1 and 8.2 relate inflation to money supply and demand. Although the presentation differs somewhat from that

Real Business Cycle Theory

Real Business Cycle Theory Barbara Annicchiarico Università degli Studi di Roma "Tor Vergata" April 202 General Features I Theory of uctuations (persistence, output does not show a strong tendency to return

Real Business Cycle Theory Barbara Annicchiarico Università degli Studi di Roma "Tor Vergata" April 202 General Features I Theory of uctuations (persistence, output does not show a strong tendency to return

Increasing for all. Convex for all. ( ) Increasing for all (remember that the log function is only defined for ). ( ) Concave for all.

Increasing for all (remember that the log function is only defined for ). ( ) Concave for all.") 1. Differentiation The first derivative of a function measures by how much changes in reaction to an infinitesimal shift in its argument. The largest the derivative (in absolute value), the faster is evolving.

1. Differentiation The first derivative of a function measures by how much changes in reaction to an infinitesimal shift in its argument. The largest the derivative (in absolute value), the faster is evolving.

Chapter 13 Real Business Cycle Theory

Chapter 13 Real Business Cycle Theory Real Business Cycle (RBC) Theory is the other dominant strand of thought in modern macroeconomics. For the most part, RBC theory has held much less sway amongst policy-makers

Chapter 13 Real Business Cycle Theory Real Business Cycle (RBC) Theory is the other dominant strand of thought in modern macroeconomics. For the most part, RBC theory has held much less sway amongst policy-makers

Real Business Cycle Theory. Marco Di Pietro Advanced () Monetary Economics and Policy 1 / 35

Monetary Economics and Policy 1 / 35") Real Business Cycle Theory Marco Di Pietro Advanced () Monetary Economics and Policy 1 / 35 Introduction to DSGE models Dynamic Stochastic General Equilibrium (DSGE) models have become the main tool for

Real Business Cycle Theory Marco Di Pietro Advanced () Monetary Economics and Policy 1 / 35 Introduction to DSGE models Dynamic Stochastic General Equilibrium (DSGE) models have become the main tool for

Chapter 11. Market-Clearing Models of the Business Cycle

Chapter 11 Market-Clearing Models of the Business Cycle Goal of This Chapter In this chapter, we study three models of business cycle, which were each developed as explicit equilibrium (market-clearing)

Chapter 11 Market-Clearing Models of the Business Cycle Goal of This Chapter In this chapter, we study three models of business cycle, which were each developed as explicit equilibrium (market-clearing)

Chapter 9. The IS-LM/AD-AS Model: A General Framework for Macroeconomic Analysis. 2008 Pearson Addison-Wesley. All rights reserved

Chapter 9 The IS-LM/AD-AS Model: A General Framework for Macroeconomic Analysis Chapter Outline The FE Line: Equilibrium in the Labor Market The IS Curve: Equilibrium in the Goods Market The LM Curve:

Chapter 9 The IS-LM/AD-AS Model: A General Framework for Macroeconomic Analysis Chapter Outline The FE Line: Equilibrium in the Labor Market The IS Curve: Equilibrium in the Goods Market The LM Curve:

Current Accounts in Open Economies Obstfeld and Rogoff, Chapter 2

Current Accounts in Open Economies Obstfeld and Rogoff, Chapter 2 1 Consumption with many periods 1.1 Finite horizon of T Optimization problem maximize U t = u (c t ) + β (c t+1 ) + β 2 u (c t+2 ) +...

Current Accounts in Open Economies Obstfeld and Rogoff, Chapter 2 1 Consumption with many periods 1.1 Finite horizon of T Optimization problem maximize U t = u (c t ) + β (c t+1 ) + β 2 u (c t+2 ) +...

A Progress Report on Business Cycle Models

Federal Reserve Bank of Minneapolis Quarterly Review Vol. 18, No. 4, Fall 1994 A Progress Report on Business Cycle Models Ellen R. McGrattan* Economist Research Department Federal Reserve Bank of Minneapolis

Federal Reserve Bank of Minneapolis Quarterly Review Vol. 18, No. 4, Fall 1994 A Progress Report on Business Cycle Models Ellen R. McGrattan* Economist Research Department Federal Reserve Bank of Minneapolis

Intermediate Macroeconomics: The Real Business Cycle Model

Intermediate Macroeconomics: The Real Business Cycle Model Eric Sims University of Notre Dame Fall 2012 1 Introduction Having developed an operational model of the economy, we want to ask ourselves the

Intermediate Macroeconomics: The Real Business Cycle Model Eric Sims University of Notre Dame Fall 2012 1 Introduction Having developed an operational model of the economy, we want to ask ourselves the

A Simple Model of Price Dispersion *

Federal Reserve Bank of Dallas Globalization and Monetary Policy Institute Working Paper No. 112 http://www.dallasfed.org/assets/documents/institute/wpapers/2012/0112.pdf A Simple Model of Price Dispersion

Federal Reserve Bank of Dallas Globalization and Monetary Policy Institute Working Paper No. 112 http://www.dallasfed.org/assets/documents/institute/wpapers/2012/0112.pdf A Simple Model of Price Dispersion

A Classical Monetary Model - Money in the Utility Function

A Classical Monetary Model - Money in the Utility Function Jarek Hurnik Department of Economics Lecture III Jarek Hurnik (Department of Economics) Monetary Economics 2012 1 / 24 Basic Facts So far, the

A Classical Monetary Model - Money in the Utility Function Jarek Hurnik Department of Economics Lecture III Jarek Hurnik (Department of Economics) Monetary Economics 2012 1 / 24 Basic Facts So far, the

Health Insurance Reform: The impact of a Medicare Buy-In

/ 41 Health Insurance Reform: The impact of a Medicare Buy-In Gary Hansen Minchung Hsu Junsang Lee 2011. 07. 13 GRIPS 2/ 41 Motivation Life-Cycle Model Calibration Quantitative Analysis Motivation Universal

/ 41 Health Insurance Reform: The impact of a Medicare Buy-In Gary Hansen Minchung Hsu Junsang Lee 2011. 07. 13 GRIPS 2/ 41 Motivation Life-Cycle Model Calibration Quantitative Analysis Motivation Universal

REAL BUSINESS CYCLE THEORY METHODOLOGY AND TOOLS

Jakub Gazda 42 Jakub Gazda, Real Business Cycle Theory Methodology and Tools, Economics & Sociology, Vol. 3, No 1, 2010, pp. 42-48. Jakub Gazda Department of Microeconomics Poznan University of Economics

Jakub Gazda 42 Jakub Gazda, Real Business Cycle Theory Methodology and Tools, Economics & Sociology, Vol. 3, No 1, 2010, pp. 42-48. Jakub Gazda Department of Microeconomics Poznan University of Economics

Name: Date: 3. Variables that a model tries to explain are called: A. endogenous. B. exogenous. C. market clearing. D. fixed.

Name: Date: 1 A measure of how fast prices are rising is called the: A growth rate of real GDP B inflation rate C unemployment rate D market-clearing rate 2 Compared with a recession, real GDP during a

Name: Date: 1 A measure of how fast prices are rising is called the: A growth rate of real GDP B inflation rate C unemployment rate D market-clearing rate 2 Compared with a recession, real GDP during a

A Simple Dynamic Applied General Equilibrium Model of a Small Open Economy: Transitional Dynamics and Trade Policy

Volume 23, Number 1, June 1998 A Simple Dynamic Applied General Equilibrium Model of a Small Open Economy: Transitional Dynamics and Trade Policy Xinshen Diao, Erinc Yeldan and Terry L. Roe ** 2 A dynamic

Volume 23, Number 1, June 1998 A Simple Dynamic Applied General Equilibrium Model of a Small Open Economy: Transitional Dynamics and Trade Policy Xinshen Diao, Erinc Yeldan and Terry L. Roe ** 2 A dynamic

The Budget Deficit, Public Debt and Endogenous Growth

The Budget Deficit, Public Debt and Endogenous Growth Michael Bräuninger October 2002 Abstract This paper analyzes the effects of public debt on endogenous growth in an overlapping generations model. The

The Budget Deficit, Public Debt and Endogenous Growth Michael Bräuninger October 2002 Abstract This paper analyzes the effects of public debt on endogenous growth in an overlapping generations model. The

Towards a Structuralist Interpretation of Saving, Investment and Current Account in Turkey

Towards a Structuralist Interpretation of Saving, Investment and Current Account in Turkey MURAT ÜNGÖR Central Bank of the Republic of Turkey http://www.muratungor.com/ April 2012 We live in the age of

Towards a Structuralist Interpretation of Saving, Investment and Current Account in Turkey MURAT ÜNGÖR Central Bank of the Republic of Turkey http://www.muratungor.com/ April 2012 We live in the age of

Lecture 14 More on Real Business Cycles. Noah Williams

Lecture 14 More on Real Business Cycles Noah Williams University of Wisconsin - Madison Economics 312 Optimality Conditions Euler equation under uncertainty: u C (C t, 1 N t) = βe t [u C (C t+1, 1 N t+1)

Lecture 14 More on Real Business Cycles Noah Williams University of Wisconsin - Madison Economics 312 Optimality Conditions Euler equation under uncertainty: u C (C t, 1 N t) = βe t [u C (C t+1, 1 N t+1)

Seminar on. Publishing Doctoral Research

Seminar on Publishing Doctoral Research In collaboration with: ADRM Advances in Doctoral Research in Management World Scientific Lisbon, June 22, 2007 DESCRIPTION ORGANIZATION PROGRAM APPLICATIONS VENUE

Seminar on Publishing Doctoral Research In collaboration with: ADRM Advances in Doctoral Research in Management World Scientific Lisbon, June 22, 2007 DESCRIPTION ORGANIZATION PROGRAM APPLICATIONS VENUE

DECONSTRUCTING THE SUCCESS OF REAL BUSINESS CYCLES

DECONSTRUCTING THE SUCCESS OF REAL BUSINESS CYCLES EMI NAKAMURA* The empirical success of Real Business Cycle (RBC) models is often judged by their ability to explain the behavior of a multitude of real

DECONSTRUCTING THE SUCCESS OF REAL BUSINESS CYCLES EMI NAKAMURA* The empirical success of Real Business Cycle (RBC) models is often judged by their ability to explain the behavior of a multitude of real

Margin Calls, Trading Costs and Asset Prices in Emerging Markets: The Financial Mechanics of the Sudden Stop Phenomenon

Discussion of Margin Calls, Trading Costs and Asset Prices in Emerging Markets: The Financial Mechanics of the Sudden Stop Phenomenon by Enrique Mendoza and Katherine Smith Fabrizio Perri NYUStern,NBERandCEPR

Discussion of Margin Calls, Trading Costs and Asset Prices in Emerging Markets: The Financial Mechanics of the Sudden Stop Phenomenon by Enrique Mendoza and Katherine Smith Fabrizio Perri NYUStern,NBERandCEPR

13. If Y = AK 0.5 L 0.5 and A, K, and L are all 100, the marginal product of capital is: A) 50. B) 100. C) 200. D) 1,000.

50. B) 100. C) 200. D) 1,000.") Name: Date: 1. In the long run, the level of national income in an economy is determined by its: A) factors of production and production function. B) real and nominal interest rate. C) government budget

Name: Date: 1. In the long run, the level of national income in an economy is determined by its: A) factors of production and production function. B) real and nominal interest rate. C) government budget

Macroeconomic Effects of Financial Shocks Online Appendix

Macroeconomic Effects of Financial Shocks Online Appendix By Urban Jermann and Vincenzo Quadrini Data sources Financial data is from the Flow of Funds Accounts of the Federal Reserve Board. We report the

Macroeconomic Effects of Financial Shocks Online Appendix By Urban Jermann and Vincenzo Quadrini Data sources Financial data is from the Flow of Funds Accounts of the Federal Reserve Board. We report the

In ation Tax and In ation Subsidies: Working Capital in a Cash-in-advance model

In ation Tax and In ation Subsidies: Working Capital in a Cash-in-advance model George T. McCandless March 3, 006 Abstract This paper studies the nature of monetary policy with nancial intermediaries that

In ation Tax and In ation Subsidies: Working Capital in a Cash-in-advance model George T. McCandless March 3, 006 Abstract This paper studies the nature of monetary policy with nancial intermediaries that

Working Capital Requirement and the Unemployment Volatility Puzzle

Working Capital Requirement and the Unemployment Volatility Puzzle Tsu-ting Tim Lin Gettysburg College July, 3 Abstract Shimer (5) argues that a search-and-matching model of the labor market in which wage

Working Capital Requirement and the Unemployment Volatility Puzzle Tsu-ting Tim Lin Gettysburg College July, 3 Abstract Shimer (5) argues that a search-and-matching model of the labor market in which wage

Real Business Cycle Models

Real Business Cycle Models Lecture 2 Nicola Viegi April 2015 Basic RBC Model Claim: Stochastic General Equlibrium Model Is Enough to Explain The Business cycle Behaviour of the Economy Money is of little

Real Business Cycle Models Lecture 2 Nicola Viegi April 2015 Basic RBC Model Claim: Stochastic General Equlibrium Model Is Enough to Explain The Business cycle Behaviour of the Economy Money is of little

GROWTH, INCOME TAXES AND CONSUMPTION ASPIRATIONS

GROWTH, INCOME TAXES AND CONSUMPTION ASPIRATIONS Gustavo A. Marrero Alfonso Novales y July 13, 2011 ABSTRACT: In a Barro-type economy with exogenous consumption aspirations, raising income taxes favors

GROWTH, INCOME TAXES AND CONSUMPTION ASPIRATIONS Gustavo A. Marrero Alfonso Novales y July 13, 2011 ABSTRACT: In a Barro-type economy with exogenous consumption aspirations, raising income taxes favors

Business Cycle Models - A Review of the Published Works Paper, Part 1

DEPARTMENT OF ECONOMICS WORKING PAPER SERIES 2008-02 McMASTER UNIVERSITY Department of Economics Kenneth Taylor Hall 426 1280 Main Street West Hamilton, Ontario, Canada L8S 4M4 http://www.mcmaster.ca/economics/

DEPARTMENT OF ECONOMICS WORKING PAPER SERIES 2008-02 McMASTER UNIVERSITY Department of Economics Kenneth Taylor Hall 426 1280 Main Street West Hamilton, Ontario, Canada L8S 4M4 http://www.mcmaster.ca/economics/

Gains from Trade: The Role of Composition

Gains from Trade: The Role of Composition Wyatt Brooks University of Notre Dame Pau Pujolas McMaster University February, 2015 Abstract In this paper we use production and trade data to measure gains from

Gains from Trade: The Role of Composition Wyatt Brooks University of Notre Dame Pau Pujolas McMaster University February, 2015 Abstract In this paper we use production and trade data to measure gains from

MASTER FINANCIAL AND MONETARY ECONOMICS MASTER FINAL WORK DISSERTATION ON THE WELFARE EFFECTS OF FINANCIAL DEVELOPMENT DIOGO MARTINHO DA SILVA

MASTER FINANCIAL AND MONETARY ECONOMICS MASTER FINAL WORK DISSERTATION ON THE WELFARE EFFECTS OF FINANCIAL DEVELOPMENT DIOGO MARTINHO DA SILVA JANUARY-2013 1 MASTER MONETARY AND FINANCIAL ECONOMICS MASTER

MASTER FINANCIAL AND MONETARY ECONOMICS MASTER FINAL WORK DISSERTATION ON THE WELFARE EFFECTS OF FINANCIAL DEVELOPMENT DIOGO MARTINHO DA SILVA JANUARY-2013 1 MASTER MONETARY AND FINANCIAL ECONOMICS MASTER

How To Model The Relationship Between Production And Consumption In A Two Sector Economy

A Gains from Trade Perspective on Macroeconomic Fluctuations Paul Beaudry and Franck Portier This version: October 2011 Abstract Business cycles reflect changes over time in the amount of trade between

A Gains from Trade Perspective on Macroeconomic Fluctuations Paul Beaudry and Franck Portier This version: October 2011 Abstract Business cycles reflect changes over time in the amount of trade between

Trade and Resources: The Heckscher-Ohlin Model. Professor Ralph Ossa 33501 International Commercial Policy

Trade and Resources: The Heckscher-Ohlin Model Professor Ralph Ossa 33501 International Commercial Policy Introduction Remember that countries trade either because they are different from one another or

Trade and Resources: The Heckscher-Ohlin Model Professor Ralph Ossa 33501 International Commercial Policy Introduction Remember that countries trade either because they are different from one another or

3 The Standard Real Business Cycle (RBC) Model. Optimal growth model + Labor decisions

Model. Optimal growth model + Labor decisions") Franck Portier TSE Macro II 29-21 Chapter 3 Real Business Cycles 36 3 The Standard Real Business Cycle (RBC) Model Perfectly competitive economy Optimal growth model + Labor decisions 2 types of agents

Franck Portier TSE Macro II 29-21 Chapter 3 Real Business Cycles 36 3 The Standard Real Business Cycle (RBC) Model Perfectly competitive economy Optimal growth model + Labor decisions 2 types of agents

6. Budget Deficits and Fiscal Policy

Prof. Dr. Thomas Steger Advanced Macroeconomics II Lecture SS 2012 6. Budget Deficits and Fiscal Policy Introduction Ricardian equivalence Distorting taxes Debt crises Introduction (1) Ricardian equivalence

Prof. Dr. Thomas Steger Advanced Macroeconomics II Lecture SS 2012 6. Budget Deficits and Fiscal Policy Introduction Ricardian equivalence Distorting taxes Debt crises Introduction (1) Ricardian equivalence

Ifo Institute for Economic Research at the University of Munich. 6. The New Keynesian Model

6. The New Keynesian Model 1 6.1 The Baseline Model 2 Basic Concepts of the New Keynesian Model Markets are imperfect: Price and wage adjustments: contract duration, adjustment costs, imperfect expectations

6. The New Keynesian Model 1 6.1 The Baseline Model 2 Basic Concepts of the New Keynesian Model Markets are imperfect: Price and wage adjustments: contract duration, adjustment costs, imperfect expectations

The Solow Model. Savings and Leakages from Per Capita Capital. (n+d)k. sk^alpha. k*: steady state 0 1 2.22 3 4. Per Capita Capital, k

k. sk^alpha. k*: steady state 0 1 2.22 3 4. Per Capita Capital, k") Savings and Leakages from Per Capita Capital 0.1.2.3.4.5 The Solow Model (n+d)k sk^alpha k*: steady state 0 1 2.22 3 4 Per Capita Capital, k Pop. growth and depreciation Savings In the diagram... sy =

Savings and Leakages from Per Capita Capital 0.1.2.3.4.5 The Solow Model (n+d)k sk^alpha k*: steady state 0 1 2.22 3 4 Per Capita Capital, k Pop. growth and depreciation Savings In the diagram... sy =

Noah Williams Economics 312. University of Wisconsin Spring 2013. Midterm Examination Solutions

Noah Williams Economics 31 Department of Economics Macroeconomics University of Wisconsin Spring 013 Midterm Examination Solutions Instructions: This is a 75 minute examination worth 100 total points.

Noah Williams Economics 31 Department of Economics Macroeconomics University of Wisconsin Spring 013 Midterm Examination Solutions Instructions: This is a 75 minute examination worth 100 total points.

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Econ 111 Summer 2007 Final Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The classical dichotomy allows us to explore economic growth

Econ 111 Summer 2007 Final Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The classical dichotomy allows us to explore economic growth

Nº 252 Diciembre 2003

Nº 252 Diciembre 2003 Documento de Trabajo ISSN (edición impresa) 0716-7334 ISSN (edición electrónica) 0717-7593 Social Security Financial Crises Rodrigo Cerda www.economia.puc.cl Versión impresa ISSN:

Nº 252 Diciembre 2003 Documento de Trabajo ISSN (edición impresa) 0716-7334 ISSN (edición electrónica) 0717-7593 Social Security Financial Crises Rodrigo Cerda www.economia.puc.cl Versión impresa ISSN:

The Cost of Capital and Optimal Financing Policy in a. Dynamic Setting

The Cost of Capital and Optimal Financing Policy in a Dynamic Setting February 18, 2014 Abstract This paper revisits the Modigliani-Miller propositions on the optimal financing policy and cost of capital

The Cost of Capital and Optimal Financing Policy in a Dynamic Setting February 18, 2014 Abstract This paper revisits the Modigliani-Miller propositions on the optimal financing policy and cost of capital

Foundations of Modern Macroeconomics Second Edition

Foundations of Modern Macroeconomics Second Edition Chapter 15: Real business cycles Ben J. Heijdra Department of Economics & Econometrics University of Groningen 1 September 29 Foundations of Modern Macroeconomics

Foundations of Modern Macroeconomics Second Edition Chapter 15: Real business cycles Ben J. Heijdra Department of Economics & Econometrics University of Groningen 1 September 29 Foundations of Modern Macroeconomics

. In this case the leakage effect of tax increases is mitigated because some of the reduction in disposable income would have otherwise been saved.

Chapter 4 Review Questions. Explain how an increase in government spending and an equal increase in lump sum taxes can generate an increase in equilibrium output. Under what conditions will a balanced

Chapter 4 Review Questions. Explain how an increase in government spending and an equal increase in lump sum taxes can generate an increase in equilibrium output. Under what conditions will a balanced

Fundamental Economic Factors

Classical Model Real business cycle theory seeks to explain business cycles via the classical model. There is general equilibrium: demand equals supply in every market. An ideological conviction underlies

Classical Model Real business cycle theory seeks to explain business cycles via the classical model. There is general equilibrium: demand equals supply in every market. An ideological conviction underlies

Real Business Cycle Theory

Chapter 4 Real Business Cycle Theory This section of the textbook focuses on explaining the behavior of the business cycle. The terms business cycle, short-run macroeconomics, and economic fluctuations

Chapter 4 Real Business Cycle Theory This section of the textbook focuses on explaining the behavior of the business cycle. The terms business cycle, short-run macroeconomics, and economic fluctuations

Introduction to Economics, ECON 100:11 & 13 Multiplier Model

Introduction to Economics, ECON 1:11 & 13 We will now rationalize the shape of the aggregate demand curve, based on the identity we have used previously, AE=C+I+G+(X-IM). We will in the process develop

Introduction to Economics, ECON 1:11 & 13 We will now rationalize the shape of the aggregate demand curve, based on the identity we have used previously, AE=C+I+G+(X-IM). We will in the process develop

Working Paper Series

RGEA Universidade de Vigo http://webs.uvigo.es/rgea Working Paper Series A Market Game Approach to Differential Information Economies Guadalupe Fugarolas, Carlos Hervés-Beloso, Emma Moreno- García and

RGEA Universidade de Vigo http://webs.uvigo.es/rgea Working Paper Series A Market Game Approach to Differential Information Economies Guadalupe Fugarolas, Carlos Hervés-Beloso, Emma Moreno- García and

Graduate Macro Theory II: Notes on Investment

Graduate Macro Theory II: Notes on Investment Eric Sims University of Notre Dame Spring 2011 1 Introduction These notes introduce and discuss modern theories of firm investment. While much of this is done

Graduate Macro Theory II: Notes on Investment Eric Sims University of Notre Dame Spring 2011 1 Introduction These notes introduce and discuss modern theories of firm investment. While much of this is done

Female labor supply as insurance against idiosyncratic risk

Female labor supply as insurance against idiosyncratic risk Orazio Attanasio, University College London and IFS Hamish Low, University of Cambridge and IFS Virginia Sánchez-Marcos, Universidad de Cantabria

Female labor supply as insurance against idiosyncratic risk Orazio Attanasio, University College London and IFS Hamish Low, University of Cambridge and IFS Virginia Sánchez-Marcos, Universidad de Cantabria

Lumpy Investment and Corporate Tax Policy

Lumpy Investment and Corporate Tax Policy Jianjun Miao Pengfei Wang November 9 Abstract This paper studies the impact of corporate tax policy on the economy in the presence of both convex and nonconvex

Lumpy Investment and Corporate Tax Policy Jianjun Miao Pengfei Wang November 9 Abstract This paper studies the impact of corporate tax policy on the economy in the presence of both convex and nonconvex

Discrete Dynamic Optimization: Six Examples

Discrete Dynamic Optimization: Six Examples Dr. Tai-kuang Ho Associate Professor. Department of Quantitative Finance, National Tsing Hua University, No. 101, Section 2, Kuang-Fu Road, Hsinchu, Taiwan 30013,

Discrete Dynamic Optimization: Six Examples Dr. Tai-kuang Ho Associate Professor. Department of Quantitative Finance, National Tsing Hua University, No. 101, Section 2, Kuang-Fu Road, Hsinchu, Taiwan 30013,

ECONOMIC GROWTH* Chapter. Key Concepts

Chapter 5 MEASURING GDP AND ECONOMIC GROWTH* Key Concepts Gross Domestic Product Gross domestic product, GDP, is the market value of all the final goods and services produced within in a country in a given

Chapter 5 MEASURING GDP AND ECONOMIC GROWTH* Key Concepts Gross Domestic Product Gross domestic product, GDP, is the market value of all the final goods and services produced within in a country in a given

Employment Protection and Business Cycles in Emerging Economies

Employment Protection and Business Cycles in Emerging Economies Ruy Lama IMF Carlos Urrutia ITAM August, 2011 Lama and Urrutia () Employment Protection August, 2011 1 / 38 Motivation Business cycles in

Employment Protection and Business Cycles in Emerging Economies Ruy Lama IMF Carlos Urrutia ITAM August, 2011 Lama and Urrutia () Employment Protection August, 2011 1 / 38 Motivation Business cycles in

Annuity market imperfection, retirement and economic growth

Annuity market imperfection, retirement and economic growth Ben J. Heijdra 1 Jochen O. Mierau 2 1 University of Groningen; Institute for Advanced Studies (Vienna); Netspar; CESifo (Munich) 2 University

Annuity market imperfection, retirement and economic growth Ben J. Heijdra 1 Jochen O. Mierau 2 1 University of Groningen; Institute for Advanced Studies (Vienna); Netspar; CESifo (Munich) 2 University

Preparation course MSc Business&Econonomics: Economic Growth

Preparation course MSc Business&Econonomics: Economic Growth Tom-Reiel Heggedal Economics Department 2014 TRH (Institute) Solow model 2014 1 / 27 Theory and models Objective of this lecture: learn Solow

Preparation course MSc Business&Econonomics: Economic Growth Tom-Reiel Heggedal Economics Department 2014 TRH (Institute) Solow model 2014 1 / 27 Theory and models Objective of this lecture: learn Solow

Should Central Banks Respond to Movements in Asset Prices? By Ben S. Bernanke and Mark Gertler *

Should Central Banks Respond to Movements in Asset Prices? By Ben S. Bernanke and Mark Gertler * In recent decades, asset booms and busts have been important factors in macroeconomic fluctuations in both

Should Central Banks Respond to Movements in Asset Prices? By Ben S. Bernanke and Mark Gertler * In recent decades, asset booms and busts have been important factors in macroeconomic fluctuations in both

Europass-Curriculum Vitae

The image cannot be displayed. Your computer may not have enough memory to open the image, or the image may have been corrupted. Restart your computer, and then open the file again. If the red x still

The image cannot be displayed. Your computer may not have enough memory to open the image, or the image may have been corrupted. Restart your computer, and then open the file again. If the red x still

Teaching modern general equilibrium macroeconomics to undergraduates: using the same t. advanced research. Gillman (Cardi Business School)

") Teaching modern general equilibrium macroeconomics to undergraduates: using the same theory required for advanced research Max Gillman Cardi Business School pments in Economics Education (DEE) Conference

Teaching modern general equilibrium macroeconomics to undergraduates: using the same theory required for advanced research Max Gillman Cardi Business School pments in Economics Education (DEE) Conference

The Baby Boom and World War II: A Macroeconomic Analysis

The Baby Boom and World War II: A Macroeconomic Analysis Matthias Doepke, Moshe Hazan, and Yishay Maoz The baby boom started right after World War II. Is there a relation between the two? The Total Fertility

The Baby Boom and World War II: A Macroeconomic Analysis Matthias Doepke, Moshe Hazan, and Yishay Maoz The baby boom started right after World War II. Is there a relation between the two? The Total Fertility

The Real Business Cycle School

Major Currents in Contemporary Economics The Real Business Cycle School Mariusz Próchniak Department of Economics II Warsaw School of Economics 1 Background During 1972-82,the dominant new classical theory

Major Currents in Contemporary Economics The Real Business Cycle School Mariusz Próchniak Department of Economics II Warsaw School of Economics 1 Background During 1972-82,the dominant new classical theory

Monetary Business Cycle Accounting

Monetary Business Cycle Accounting Roman Šustek Bank of England March 3, 2009 Abstract This paper investigates the quantitative importance of various types of frictions for inflation and nominal interest

Monetary Business Cycle Accounting Roman Šustek Bank of England March 3, 2009 Abstract This paper investigates the quantitative importance of various types of frictions for inflation and nominal interest

Overview of Model CREDIT CHAINS Many small firms owned and run by entrepreneurs. Nobuhiro Kiyotaki Entrepreneurs unable to raise outside finance. John Moore January 1997 But an entrepreneur can borrow

Overview of Model CREDIT CHAINS Many small firms owned and run by entrepreneurs. Nobuhiro Kiyotaki Entrepreneurs unable to raise outside finance. John Moore January 1997 But an entrepreneur can borrow

Introduction to Macroeconomics TOPIC 2: The Goods Market

TOPIC 2: The Goods Market Annaïg Morin CBS - Department of Economics August 2013 Goods market Road map: 1. Demand for goods 1.1. Components 1.1.1. Consumption 1.1.2. Investment 1.1.3. Government spending

TOPIC 2: The Goods Market Annaïg Morin CBS - Department of Economics August 2013 Goods market Road map: 1. Demand for goods 1.1. Components 1.1.1. Consumption 1.1.2. Investment 1.1.3. Government spending

Total Factor Productivity

Total Factor Productivity Diego Comin NewYorkUniversityandNBER August 2006 Abstract Total Factor Productivity (TFP) is the portion of output not explained by the amount of inputs used in production. The

Total Factor Productivity Diego Comin NewYorkUniversityandNBER August 2006 Abstract Total Factor Productivity (TFP) is the portion of output not explained by the amount of inputs used in production. The

Dynamics of Small Open Economies

Dynamics of Small Open Economies Lecture 2, ECON 4330 Tord Krogh January 22, 2013 Tord Krogh () ECON 4330 January 22, 2013 1 / 68 Last lecture The models we have looked at so far are characterized by:

Dynamics of Small Open Economies Lecture 2, ECON 4330 Tord Krogh January 22, 2013 Tord Krogh () ECON 4330 January 22, 2013 1 / 68 Last lecture The models we have looked at so far are characterized by:

Uninsured Entrepreneurial Risk and Public Debt Policies

Uninsured Entrepreneurial Risk and Public Debt Policies Sumudu Kankanamge a 1 a Paris School of Economics, CNRS, France Abstract This paper builds a stylized economy with both entrepreneurial and non entrepreneurial

Uninsured Entrepreneurial Risk and Public Debt Policies Sumudu Kankanamge a 1 a Paris School of Economics, CNRS, France Abstract This paper builds a stylized economy with both entrepreneurial and non entrepreneurial

0 100 200 300 Real income (Y)

") Lecture 11-1 6.1 The open economy, the multiplier, and the IS curve Assume that the economy is either closed (no foreign trade) or open. Assume that the exchange rates are either fixed or flexible. Assume

Lecture 11-1 6.1 The open economy, the multiplier, and the IS curve Assume that the economy is either closed (no foreign trade) or open. Assume that the exchange rates are either fixed or flexible. Assume

KIER DISCUSSION PAPER SERIES

KIER DISCUSSION PAPER SERIES KYOTO INSTITUTE OF ECONOMIC RESEARCH Discussion Paper No.880 Time Preference and Income Convergence in a Dynamic Heckscher-Ohlin Model Taketo Kawagishi and Kazuo Mino November

KIER DISCUSSION PAPER SERIES KYOTO INSTITUTE OF ECONOMIC RESEARCH Discussion Paper No.880 Time Preference and Income Convergence in a Dynamic Heckscher-Ohlin Model Taketo Kawagishi and Kazuo Mino November

LECTURE NOTES ON MACROECONOMIC PRINCIPLES

LECTURE NOTES ON MACROECONOMIC PRINCIPLES Peter Ireland Department of Economics Boston College peter.ireland@bc.edu http://www2.bc.edu/peter-ireland/ec132.html Copyright (c) 2013 by Peter Ireland. Redistribution

LECTURE NOTES ON MACROECONOMIC PRINCIPLES Peter Ireland Department of Economics Boston College peter.ireland@bc.edu http://www2.bc.edu/peter-ireland/ec132.html Copyright (c) 2013 by Peter Ireland. Redistribution

The Basic New Keynesian Model

The Basic New Keynesian Model January 11 th 2012 Lecture notes by Drago Bergholt, Norwegian Business School Drago.Bergholt@bi.no I Contents 1. Introduction... 1 1.1 Prologue... 1 1.2 The New Keynesian

The Basic New Keynesian Model January 11 th 2012 Lecture notes by Drago Bergholt, Norwegian Business School Drago.Bergholt@bi.no I Contents 1. Introduction... 1 1.1 Prologue... 1 1.2 The New Keynesian

Heterogeneous firms and dynamic gains from trade

Heterogeneous firms and dynamic gains from trade Julian Emami Namini Department of Economics, University of Duisburg-Essen, Campus Essen, Germany Email: emami@vwl.uni-essen.de 14th March 2005 Abstract

Heterogeneous firms and dynamic gains from trade Julian Emami Namini Department of Economics, University of Duisburg-Essen, Campus Essen, Germany Email: emami@vwl.uni-essen.de 14th March 2005 Abstract

Section 4: Adding Government and Money

Section 4: Adding and Money Ec 123 April 2009 Outline This Section Fiscal Policy Money Next Keynesian Economics Recessions Problem Set 1 due Tuesday in class Fiscal Policy Fiscal Policy is the use of the

Section 4: Adding and Money Ec 123 April 2009 Outline This Section Fiscal Policy Money Next Keynesian Economics Recessions Problem Set 1 due Tuesday in class Fiscal Policy Fiscal Policy is the use of the

Home-Bias in Consumption and Equities: Can Trade Costs Jointly Explain Both?

Home-Bias in Consumption and Equities: Can Trade Costs Jointly Explain Both? Håkon Tretvoll New York University This version: May, 2008 Abstract This paper studies whether including trade costs to explain

Home-Bias in Consumption and Equities: Can Trade Costs Jointly Explain Both? Håkon Tretvoll New York University This version: May, 2008 Abstract This paper studies whether including trade costs to explain

Economic Growth. Chapter 11

Chapter 11 Economic Growth This chapter examines the determinants of economic growth. A startling fact about economic growth is the large variation in the growth experience of different countries in recent

Chapter 11 Economic Growth This chapter examines the determinants of economic growth. A startling fact about economic growth is the large variation in the growth experience of different countries in recent

Debt and the U.S. Economy

Debt and the U.S. Economy Kaiji Chen Ayşe İmrohoroğlu This Version: April 2012 Abstract Publicly held debt to GDP ratio in the U.S. has reached 68% in 2011 and is expected to continue rising. Many proposals

Debt and the U.S. Economy Kaiji Chen Ayşe İmrohoroğlu This Version: April 2012 Abstract Publicly held debt to GDP ratio in the U.S. has reached 68% in 2011 and is expected to continue rising. Many proposals