ECO 610: Lecture 7. Perfectly Competitive Markets

|

|

|

- Nancy Payne

- 7 years ago

- Views:

Transcription

1 ECO 610: Lecture 7 Perfectly Competitive Markets

2 Perfectly Competitive Markets: Outline Goal: understanding firm and market supply in competitive markets Characteristics of perfectly competitive industries Short-run production decision of a perfectly competitive firm Short-run market supply and equilibrium in a perfectly competitive market Long-run adjustments and equilibrium in a perfectly competitive market

3 A taxonomy of market structures

4 Characteristics of a perfectly competitive market Large number of small, independent sellers Large number of small, independent buyers Homogeneous product Insignificant barriers to entry and exit Perfect information available to buyers and sellers Examples? Alligator farming?

5 Can you really farm these things?

6 Short-run production decision of a perfectly competitive firm Imagine that you are a commodity market analyst for a major fashion house: id=11836 The CEO comes to you and asks where you think alligator skin prices are going, because she wants to add a line of alligator handbags, luggage, and cowboy boots. You say let me do some research and get back to you on that. What analytical framework do you use to figure out what is going on now in the alligator market and where things are headed?

7 The usefulness of abstract models

8 Modeling the firm s supply decision To understand how price and output get determined in both the short run and long run in a competitive industry, let s ask and answer a series of questions: How is the price of alligators determined? What does the demand curve facing each individual alligator farmer look like? What output will maximize profit for the farmer in the short run? What happens to the farmer s optimal output as market price changes? What does the farmer s short-run supply curve look like? What does the short-run market supply curve for alligators look like, given information on individual farmers supply curves?

9 How is the price of alligators determined? Market demand and supply. Market demand represents the collective decisions of all alligator buyers. We are building towards understanding how market supply is determined. What is P* in 1987 in the market for alligators? du/login?url= search.proquest.co m/docview/ ?accountid=11836

10 What does the demand curve facing each individual alligator farmer look like? If each producer is small relative to the market, what impact will any one producer s output decision have on market price? What is the relevant range of output for an individual alligator farmer? What is industry output? What happens to market price if an individual alligator farmer withholds all his gators from the market in a given year? What happens to market price if that farmer produces and sells as many as he can in a given year? We say that a firm in a perfectly competitive industry is a Price Taker, because the firm s demand curve is perfectly elastic at the market price.

11 Demand Curve of a Perfectly Competitive Firm Price $ per 4-foot gator Firm Price $ per 4-foot gator Market S $180 d $180 D q: Output (4-foot alligators) ,000 Q: Output (4-foot alligators) 11

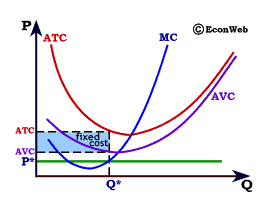

12 What output will maximize profit for the firm in the short run? The shutdown rule First decision: produce q = 0 or produce q > 0 in the short run? What does producing q = 0 in the short run [i.e. shut down] look like? What does producing q = 0 in the long run [i.e. go out of business] look like? How to decide whether to shut down or produce a positive output? π = TR TC = TR TVC TFC If q = 0, then TR = 0 and TVC = 0, so π = - TFC; i.e. your losses equal your fixed costs If q > 0, then π = TR TVC TFC So, if [TR TVC] > 0, you are better off producing q > 0. If TR < TVC, you are better off shutting down in the short run. Alternatively, if TR/q < TVC/q, i.e. if P < AVC, then shut down in the short run.

13

14 What output will maximize profit for the firm in the short run? Producing a positive rate of output If P Mkt > min AVC such that producing a q > 0 is optimal, what q will maximize profit for the firm in the short run? Expand output as long as producing and selling another unit adds more to total revenue than it does to total cost. In other words, expand output up to point where MR = MC. [Refer to diagram drawn on board for typical alligator farmer, with AVC and MC diagrams included.] What is marginal revenue for a perfectly competitive firm? MR = ΔTR/Δq. As the firm expands output, does it have to lower price to sell more output? No, hence MR = P = d.

15 What does the firm s short-run supply curve look like? As market price varies from zero to $200 per four-foot gator, what output will maximize profits (minimize losses) at each possible price? [Refer to diagram drawn on board for derivation of competitive firm s short-run supply curve] If P Mkt < min AVC, then q* = 0, where q* is the firm s profit-maximizing output. If P Mkt > min AVC, then producing q* where P Mkt = MC will maximize shortrun profits (minimize short-run losses) for the firm. Does the firm s short-run supply curve obey the Law of Supply? What is the logic of the economic behavior suggested by the firm s shortrun supply curve that we have just derived?

16 A Firm s Short-Run Supply Curve Price ($ per unit) P 2 P 1 S = MC above AVC MC ATC AVC P = AVC Shut-down q 1 q 2 Output 16

17 What does the market supply curve look like? Suppose we have information on the supply behavior of all the producers currently in the market, i.e. we know the individual firms supply curves. How do we derive the market supply curve? The market supply curve is the aggregation of the supply curves of all firms in the market. Thus we sum the quantities supplied by all firms at each possible price to get the market supply curve, i.e. we sum the firm supply curves horizontally (since we are aggregating quantities). [Refer to diagram drawn on board.] Does the short-run market supply curve for a perfectly competitive industry obey the Law of Supply? Why?

18

19 Short-run equilibrium in a perfectly competitive market A competitive market is in equilibrium in the short run when: Market price, P*, clears the market, i.e. market quantity demanded equals quantity supplied, i.e. Q D = Q S. Each firm maximizes profit, producing q i where P* = mc i. Market quantity supplied equals the aggregation of each firm s profit maximization decision: Q S = σ n i=1 q i Do firms make positive, negative, or zero economic profit? Depends on market price. [refer to diagrams on board]

20

21 Predicting the future: 1987 Suppose it is 1987 and the market price of a 4-foot alligator is $180. Alligator farmers are doing great, earning significant economic profits. ountid=11836 [refer to diagrams on board]. What do you think will happen as time passes? What does it mean that firms in the industry are earning positive economic profits? As entry occurs, what will happen to the market supply curve? What will happen to market price? After enough time passes for all adjustments to occur, what do you predict market price will be? How long will that take?

22 Predicting the future: 1997 Suppose it is 1997 and the market price of a 4-foot alligator is $100. Alligator farmers are struggling, suffering significant economic losses. ountid=11836 [refer to diagrams on board]. What do you think will happen as time passes? What does it mean that firms in the industry are earning negative economic profits? As exit occurs, what will happen to the market supply curve? What will happen to market price? After enough time passes for all adjustments to occur, what do you predict market price will be? How long will that take?

23 Long-run equilibrium in a perfectly competitive market A competitive market is in long-run equilibrium when: Market price P* clears the market, i.e. market quantity demanded equals quantity supplied, i.e. Q D = Q S. Each firm maximizes profit, producing q i where P* = mc i. Market quantity supplied equals the aggregation of each firm s profit maximization decision: Q S = σ n i=1 q i At P* firms earn a normal economic return, i.e. zero economic profit. P* = min LRAC, i.e. firms produce the product as cheaply as is possible, given input prices and technology.

24 Working with the perfectly competitive model Market is in long-run equilibrium. Demand increases. What happens in the short run? What happens in the long run? Market is in long-run equilibrium. Demand decreases. What happens in the short run? What happens in the long run? Market is in long-run equilibrium. Technology improves, such that LRAC shifts downward. What happens in the short run? What happens in the long run? Market is in long-run equilibrium. The price of a key input increases, such that LRAC shifts upward. What happens in the short run? What happens in the long run?

25

26 Choosing Output in the Long Run Price ($ per unit of output) $40 D Question: Where are long-run profits zero? A SMC SAC E LMC LAC P = MR C G $30 B F q 1 q 2 q 3 Output 26

27 Long-Run Competitive Equilibrium $ per unit of output Firm Profit attracts firms Supply increases until profit = 0 $ per unit of output Industry S 1 LMC $40 LAC P 1 S 2 $30 P 2 D q 2 Output Q 1 Q 2 Output 27

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron.

Principles of Microeconomics, Quiz #5 Fall 2007 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron. 1) Perfect competition

Principles of Microeconomics, Quiz #5 Fall 2007 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron. 1) Perfect competition

Chapter 6 Competitive Markets

Chapter 6 Competitive Markets After reading Chapter 6, COMPETITIVE MARKETS, you should be able to: List and explain the characteristics of Perfect Competition and Monopolistic Competition Explain why a

Chapter 6 Competitive Markets After reading Chapter 6, COMPETITIVE MARKETS, you should be able to: List and explain the characteristics of Perfect Competition and Monopolistic Competition Explain why a

Learning Objectives. After reading Chapter 11 and working the problems for Chapter 11 in the textbook and in this Workbook, you should be able to:

Learning Objectives After reading Chapter 11 and working the problems for Chapter 11 in the textbook and in this Workbook, you should be able to: Discuss three characteristics of perfectly competitive

Learning Objectives After reading Chapter 11 and working the problems for Chapter 11 in the textbook and in this Workbook, you should be able to: Discuss three characteristics of perfectly competitive

Managerial Economics & Business Strategy Chapter 8. Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets

Managerial Economics & Business Strategy Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets I. Perfect Competition Overview Characteristics and profit outlook. Effect

Managerial Economics & Business Strategy Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets I. Perfect Competition Overview Characteristics and profit outlook. Effect

Profit Maximization. 2. product homogeneity

Perfectly Competitive Markets It is essentially a market in which there is enough competition that it doesn t make sense to identify your rivals. There are so many competitors that you cannot single out

Perfectly Competitive Markets It is essentially a market in which there is enough competition that it doesn t make sense to identify your rivals. There are so many competitors that you cannot single out

Pre-Test Chapter 21 ed17

Pre-Test Chapter 21 ed17 Multiple Choice Questions 1. Which of the following is not a basic characteristic of pure competition? A. considerable nonprice competition B. no barriers to the entry or exodus

Pre-Test Chapter 21 ed17 Multiple Choice Questions 1. Which of the following is not a basic characteristic of pure competition? A. considerable nonprice competition B. no barriers to the entry or exodus

Chapter 9: Perfect Competition

Chapter 9: Perfect Competition Perfect Competition Law of One Price Short-Run Equilibrium Long-Run Equilibrium Maximize Profit Market Equilibrium Constant- Cost Industry Increasing- Cost Industry Decreasing-

Chapter 9: Perfect Competition Perfect Competition Law of One Price Short-Run Equilibrium Long-Run Equilibrium Maximize Profit Market Equilibrium Constant- Cost Industry Increasing- Cost Industry Decreasing-

Practice Questions Week 8 Day 1

Practice Questions Week 8 Day 1 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The characteristics of a market that influence the behavior of market participants

Practice Questions Week 8 Day 1 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The characteristics of a market that influence the behavior of market participants

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Practice for Perfect Competition Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Which of the following is a defining characteristic of a

Practice for Perfect Competition Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Which of the following is a defining characteristic of a

Chapter 8. Competitive Firms and Markets

Chapter 8. Competitive Firms and Markets We have learned the production function and cost function, the question now is: how much to produce such that firm can maximize his profit? To solve this question,

Chapter 8. Competitive Firms and Markets We have learned the production function and cost function, the question now is: how much to produce such that firm can maximize his profit? To solve this question,

Chapter. Perfect Competition CHAPTER IN PERSPECTIVE

Perfect Competition Chapter 10 CHAPTER IN PERSPECTIVE In Chapter 10 we study perfect competition, the market that arises when the demand for a product is large relative to the output of a single producer.

Perfect Competition Chapter 10 CHAPTER IN PERSPECTIVE In Chapter 10 we study perfect competition, the market that arises when the demand for a product is large relative to the output of a single producer.

Market Structure: Perfect Competition and Monopoly

WSG8 7/7/03 4:34 PM Page 113 8 Market Structure: Perfect Competition and Monopoly OVERVIEW One of the most important decisions made by a manager is how to price the firm s product. If the firm is a profit

WSG8 7/7/03 4:34 PM Page 113 8 Market Structure: Perfect Competition and Monopoly OVERVIEW One of the most important decisions made by a manager is how to price the firm s product. If the firm is a profit

D) Marginal revenue is the rate at which total revenue changes with respect to changes in output.

Marginal revenue is the rate at which total revenue changes with respect to changes in output.") Ch. 9 1. Which of the following is not an assumption of a perfectly competitive market? A) Fragmented industry B) Differentiated product C) Perfect information D) Equal access to resources 2. Which of

Ch. 9 1. Which of the following is not an assumption of a perfectly competitive market? A) Fragmented industry B) Differentiated product C) Perfect information D) Equal access to resources 2. Which of

c. Given your answer in part (b), what do you anticipate will happen in this market in the long-run?

, what do you anticipate will happen in this market in the long-run?") Perfect Competition Questions Question 1 Suppose there is a perfectly competitive industry where all the firms are identical with identical cost curves. Furthermore, suppose that a representative firm

Perfect Competition Questions Question 1 Suppose there is a perfectly competitive industry where all the firms are identical with identical cost curves. Furthermore, suppose that a representative firm

CEVAPLAR. Solution: a. Given the competitive nature of the industry, Conigan should equate P to MC.

1 I S L 8 0 5 U Y G U L A M A L I İ K T İ S A T _ U Y G U L A M A ( 4 ) _ 9 K a s ı m 2 0 1 2 CEVAPLAR 1. Conigan Box Company produces cardboard boxes that are sold in bundles of 1000 boxes. The market

1 I S L 8 0 5 U Y G U L A M A L I İ K T İ S A T _ U Y G U L A M A ( 4 ) _ 9 K a s ı m 2 0 1 2 CEVAPLAR 1. Conigan Box Company produces cardboard boxes that are sold in bundles of 1000 boxes. The market

Pricing and Output Decisions: i Perfect. Managerial Economics: Economic Tools for Today s Decision Makers, 4/e By Paul Keat and Philip Young

Chapter 9 Pricing and Output Decisions: i Perfect Competition and Monopoly M i l E i E i Managerial Economics: Economic Tools for Today s Decision Makers, 4/e By Paul Keat and Philip Young Pricing and

Chapter 9 Pricing and Output Decisions: i Perfect Competition and Monopoly M i l E i E i Managerial Economics: Economic Tools for Today s Decision Makers, 4/e By Paul Keat and Philip Young Pricing and

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chapter 11 Perfect Competition - Sample Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Perfect competition is an industry with A) a

Chapter 11 Perfect Competition - Sample Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Perfect competition is an industry with A) a

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

MBA 640 Survey of Microeconomics Fall 2006, Quiz 6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly is best defined as a firm that

MBA 640 Survey of Microeconomics Fall 2006, Quiz 6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly is best defined as a firm that

Learning Objectives. Chapter 6. Market Structures. Market Structures (cont.) The Two Extremes: Perfect Competition and Pure Monopoly

The Two Extremes: Perfect Competition and Pure Monopoly") Chapter 6 The Two Extremes: Perfect Competition and Pure Monopoly Learning Objectives List the four characteristics of a perfectly competitive market. Describe how a perfect competitor makes the decision

Chapter 6 The Two Extremes: Perfect Competition and Pure Monopoly Learning Objectives List the four characteristics of a perfectly competitive market. Describe how a perfect competitor makes the decision

Experiment 8: Entry and Equilibrium Dynamics

Experiment 8: Entry and Equilibrium Dynamics Everyone is a demander of a meal. There are approximately equal numbers of values at 24, 18, 12 and 8. These will change, due to a random development, after

Experiment 8: Entry and Equilibrium Dynamics Everyone is a demander of a meal. There are approximately equal numbers of values at 24, 18, 12 and 8. These will change, due to a random development, after

Price Theory Lecture 6: Market Structure Perfect Competition

Price Theory Lecture 6: Market tructure Perfect Competition I. Concepts of Competition Whether a firm can be regarded as competitive depends on several factors, the most important of which are: The number

Price Theory Lecture 6: Market tructure Perfect Competition I. Concepts of Competition Whether a firm can be regarded as competitive depends on several factors, the most important of which are: The number

Lab 12: Perfectly Competitive Market

Lab 12: Perfectly Competitive Market 1. Perfectly competitive market 1) three conditions that make a market perfectly competitive: a. many buyers and sellers, all of whom are small relative to market b.

Lab 12: Perfectly Competitive Market 1. Perfectly competitive market 1) three conditions that make a market perfectly competitive: a. many buyers and sellers, all of whom are small relative to market b.

chapter Perfect Competition and the >> Supply Curve Section 3: The Industry Supply Curve

chapter 9 The industry supply curve shows the relationship between the price of a good and the total output of the industry as a whole. Perfect Competition and the >> Supply Curve Section 3: The Industry

chapter 9 The industry supply curve shows the relationship between the price of a good and the total output of the industry as a whole. Perfect Competition and the >> Supply Curve Section 3: The Industry

Long Run Supply and the Analysis of Competitive Markets. 1 Long Run Competitive Equilibrium

Long Run Competitive Equilibrium. rinciples of Microeconomics, Fall 7 Chia-Hui Chen October 9, 7 Lecture 6 Long Run Supply and the Analysis of Competitive Markets Outline. Chap 8: Long Run Equilibrium.

Long Run Competitive Equilibrium. rinciples of Microeconomics, Fall 7 Chia-Hui Chen October 9, 7 Lecture 6 Long Run Supply and the Analysis of Competitive Markets Outline. Chap 8: Long Run Equilibrium.

11 PERFECT COMPETITION. Chapter. Competition

Chapter 11 PERFECT COMPETITION Competition Topic: Perfect Competition 1) Perfect competition is an industry with A) a few firms producing identical goods B) a few firms producing goods that differ somewhat

Chapter 11 PERFECT COMPETITION Competition Topic: Perfect Competition 1) Perfect competition is an industry with A) a few firms producing identical goods B) a few firms producing goods that differ somewhat

We will study the extreme case of perfect competition, where firms are price takers.

Perfectly Competitive Markets A firm s decision about how much to produce or what price to charge depends on how competitive the market structure is. If the Cincinnati Bengals raise their ticket prices

Perfectly Competitive Markets A firm s decision about how much to produce or what price to charge depends on how competitive the market structure is. If the Cincinnati Bengals raise their ticket prices

MPP 801 Monopoly Kevin Wainwright Study Questions

MPP 801 Monopoly Kevin Wainwright Study Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The marginal revenue facing a monopolist A) is

MPP 801 Monopoly Kevin Wainwright Study Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The marginal revenue facing a monopolist A) is

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chapter 11 Monopoly practice Davidson spring2007 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly industry is characterized by 1) A)

Chapter 11 Monopoly practice Davidson spring2007 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly industry is characterized by 1) A)

AP Microeconomics Review

AP Microeconomics Review 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry 3. Natural Monopoly with Fair-Return

AP Microeconomics Review 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry 3. Natural Monopoly with Fair-Return

Understanding Economics 2nd edition by Mark Lovewell and Khoa Nguyen

Understanding Economics 2nd edition by Mark Lovewell and Khoa Nguyen Chapter 5 Perfect Competition Chapter Objectives! In this chapter you will: " Consider the four market structures, and the main differences

Understanding Economics 2nd edition by Mark Lovewell and Khoa Nguyen Chapter 5 Perfect Competition Chapter Objectives! In this chapter you will: " Consider the four market structures, and the main differences

Equilibrium of a firm under perfect competition in the short-run. A firm is under equilibrium at that point where it maximizes its profits.

Equilibrium of a firm under perfect competition in the short-run. A firm is under equilibrium at that point where it maximizes its profits. Profit depends upon two factors Revenue Structure Cost Structure

Equilibrium of a firm under perfect competition in the short-run. A firm is under equilibrium at that point where it maximizes its profits. Profit depends upon two factors Revenue Structure Cost Structure

CHAPTER 8 PROFIT MAXIMIZATION AND COMPETITIVE SUPPLY

CHAPTER 8 PROFIT MAXIMIZATION AND COMPETITIVE SUPPLY TEACHING NOTES This chapter begins by explaining what we mean by a competitive market and why it makes sense to assume that firms try to maximize profit.

CHAPTER 8 PROFIT MAXIMIZATION AND COMPETITIVE SUPPLY TEACHING NOTES This chapter begins by explaining what we mean by a competitive market and why it makes sense to assume that firms try to maximize profit.

CHAPTER 9: PURE COMPETITION

CHAPTER 9: PURE COMPETITION Introduction In Chapters 9-11, we reach the heart of microeconomics, the concepts which comprise more than a quarter of the AP microeconomics exam. With a fuller understanding

CHAPTER 9: PURE COMPETITION Introduction In Chapters 9-11, we reach the heart of microeconomics, the concepts which comprise more than a quarter of the AP microeconomics exam. With a fuller understanding

Microeconomics Topic 7: Contrast market outcomes under monopoly and competition.

Microeconomics Topic 7: Contrast market outcomes under monopoly and competition. Reference: N. Gregory Mankiw s rinciples of Microeconomics, 2 nd edition, Chapter 14 (p. 291-314) and Chapter 15 (p. 315-347).

Microeconomics Topic 7: Contrast market outcomes under monopoly and competition. Reference: N. Gregory Mankiw s rinciples of Microeconomics, 2 nd edition, Chapter 14 (p. 291-314) and Chapter 15 (p. 315-347).

ANSWERS TO END-OF-CHAPTER QUESTIONS

ANSWERS TO END-OF-CHAPTER QUESTIONS 23-1 Briefly indicate the basic characteristics of pure competition, pure monopoly, monopolistic competition, and oligopoly. Under which of these market classifications

ANSWERS TO END-OF-CHAPTER QUESTIONS 23-1 Briefly indicate the basic characteristics of pure competition, pure monopoly, monopolistic competition, and oligopoly. Under which of these market classifications

Chapter 7 Monopoly, Oligopoly and Strategy

Chapter 7 Monopoly, Oligopoly and Strategy After reading Chapter 7, MONOPOLY, OLIGOPOLY AND STRATEGY, you should be able to: Define the characteristics of Monopoly and Oligopoly, and explain why the are

Chapter 7 Monopoly, Oligopoly and Strategy After reading Chapter 7, MONOPOLY, OLIGOPOLY AND STRATEGY, you should be able to: Define the characteristics of Monopoly and Oligopoly, and explain why the are

Economics 10: Problem Set 3 (With Answers)

") Economics 1: Problem Set 3 (With Answers) 1. Assume you own a bookstore that has the following cost and revenue information for last year: - gross revenue from sales $1, - cost of inventory 4, - wages

Economics 1: Problem Set 3 (With Answers) 1. Assume you own a bookstore that has the following cost and revenue information for last year: - gross revenue from sales $1, - cost of inventory 4, - wages

21 : Theory of Cost 1

21 : Theory of Cost 1 Recap from last Session Production cost Types of Cost: Accounting/Economic Analysis Cost Output Relationship Short run cost Analysis Session Outline The Long-Run Cost-Output Relations

21 : Theory of Cost 1 Recap from last Session Production cost Types of Cost: Accounting/Economic Analysis Cost Output Relationship Short run cost Analysis Session Outline The Long-Run Cost-Output Relations

UNIVERSITY OF CALICUT MICRO ECONOMICS - II

UNIVERSITY OF CALICUT SCHOOL OF DISTANCE EDUCATION BA ECONOMICS III SEMESTER CORE COURSE (2011 Admission onwards) MICRO ECONOMICS - II QUESTION BANK 1. Which of the following industry is most closely approximates

UNIVERSITY OF CALICUT SCHOOL OF DISTANCE EDUCATION BA ECONOMICS III SEMESTER CORE COURSE (2011 Admission onwards) MICRO ECONOMICS - II QUESTION BANK 1. Which of the following industry is most closely approximates

Theory of Perfectly Competitive Markets

Economics 147 John F. Stewart Theory of Perfectly Competitive Markets University of North Carolina Chapel Hill Theory: The Structure of an Economic Model Economic theory is based on deductive logic, if

Economics 147 John F. Stewart Theory of Perfectly Competitive Markets University of North Carolina Chapel Hill Theory: The Structure of an Economic Model Economic theory is based on deductive logic, if

EXAM TWO REVIEW: A. Explicit Cost vs. Implicit Cost and Accounting Costs vs. Economic Costs:

EXAM TWO REVIEW: A. Explicit Cost vs. Implicit Cost and Accounting Costs vs. Economic Costs: Economic Cost: the monetary value of all inputs used in a particular activity or enterprise over a given period.

EXAM TWO REVIEW: A. Explicit Cost vs. Implicit Cost and Accounting Costs vs. Economic Costs: Economic Cost: the monetary value of all inputs used in a particular activity or enterprise over a given period.

An increase in the number of students attending college. shifts to the left. An increase in the wage rate of refinery workers.

1. Which of the following would shift the demand curve for new textbooks to the right? a. A fall in the price of paper used in publishing texts. b. A fall in the price of equivalent used text books. c.

1. Which of the following would shift the demand curve for new textbooks to the right? a. A fall in the price of paper used in publishing texts. b. A fall in the price of equivalent used text books. c.

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron.

Principles of Microeconomics Fall 2007, Quiz #6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron. 1) A monopoly is

Principles of Microeconomics Fall 2007, Quiz #6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron. 1) A monopoly is

Unit 2.3 - Theory of the Firm Unit Overview

Unit 2.3.1 - Introduction to Market Structures and Cost Theory Intro to Market Structures Pure competition Monopolistic competition Oligopoly Monopoly Cost theory Types of costs: fixed costs, variable

Unit 2.3.1 - Introduction to Market Structures and Cost Theory Intro to Market Structures Pure competition Monopolistic competition Oligopoly Monopoly Cost theory Types of costs: fixed costs, variable

CHAPTER 11 PRICE AND OUTPUT IN MONOPOLY, MONOPOLISTIC COMPETITION, AND PERFECT COMPETITION

CHAPTER 11 PRICE AND OUTPUT IN MONOPOLY, MONOPOLISTIC COMPETITION, AND PERFECT COMPETITION Chapter in a Nutshell Now that we understand the characteristics of different market structures, we ask the question

CHAPTER 11 PRICE AND OUTPUT IN MONOPOLY, MONOPOLISTIC COMPETITION, AND PERFECT COMPETITION Chapter in a Nutshell Now that we understand the characteristics of different market structures, we ask the question

ECON 103, 2008-2 ANSWERS TO HOME WORK ASSIGNMENTS

ECON 103, 2008-2 ANSWERS TO HOME WORK ASSIGNMENTS Due the Week of June 23 Chapter 8 WRITE [4] Use the demand schedule that follows to calculate total revenue and marginal revenue at each quantity. Plot

ECON 103, 2008-2 ANSWERS TO HOME WORK ASSIGNMENTS Due the Week of June 23 Chapter 8 WRITE [4] Use the demand schedule that follows to calculate total revenue and marginal revenue at each quantity. Plot

Final Exam (Version 1) Answers

Answers") Final Exam Economics 101 Fall 2003 Wallace Final Exam (Version 1) Answers 1. The marginal revenue product equals A) total revenue divided by total product (output). B) marginal revenue divided by marginal

Final Exam Economics 101 Fall 2003 Wallace Final Exam (Version 1) Answers 1. The marginal revenue product equals A) total revenue divided by total product (output). B) marginal revenue divided by marginal

CHAPTER 10 MARKET POWER: MONOPOLY AND MONOPSONY

CHAPTER 10 MARKET POWER: MONOPOLY AND MONOPSONY EXERCISES 3. A monopolist firm faces a demand with constant elasticity of -.0. It has a constant marginal cost of $0 per unit and sets a price to maximize

CHAPTER 10 MARKET POWER: MONOPOLY AND MONOPSONY EXERCISES 3. A monopolist firm faces a demand with constant elasticity of -.0. It has a constant marginal cost of $0 per unit and sets a price to maximize

CHAPTER 6 MARKET STRUCTURE

CHAPTER 6 MARKET STRUCTURE CHAPTER SUMMARY This chapter presents an economic analysis of market structure. It starts with perfect competition as a benchmark. Potential barriers to entry, that might limit

CHAPTER 6 MARKET STRUCTURE CHAPTER SUMMARY This chapter presents an economic analysis of market structure. It starts with perfect competition as a benchmark. Potential barriers to entry, that might limit

Chapter 15: Monopoly WHY MONOPOLIES ARISE HOW MONOPOLIES MAKE PRODUCTION AND PRICING DECISIONS

Chapter 15: While a competitive firm is a taker, a monopoly firm is a maker. A firm is considered a monopoly if... it is the sole seller of its product. its product does not have close substitutes. The

Chapter 15: While a competitive firm is a taker, a monopoly firm is a maker. A firm is considered a monopoly if... it is the sole seller of its product. its product does not have close substitutes. The

Econ 201 Final Exam. Douglas, Fall 2007 Version A Special Codes 00000. PLEDGE: I have neither given nor received unauthorized help on this exam.

, Fall 2007 Version A Special Codes 00000 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 201 Final Exam 1. For a profit-maximizing monopolist, a. MR

, Fall 2007 Version A Special Codes 00000 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 201 Final Exam 1. For a profit-maximizing monopolist, a. MR

Midterm Exam #1 - Answers

Page 1 of 9 Midterm Exam #1 Answers Instructions: Answer all questions directly on these sheets. Points for each part of each question are indicated, and there are 1 points total. Budget your time. 1.

Page 1 of 9 Midterm Exam #1 Answers Instructions: Answer all questions directly on these sheets. Points for each part of each question are indicated, and there are 1 points total. Budget your time. 1.

Chapter 7: The Costs of Production QUESTIONS FOR REVIEW

HW #7: Solutions QUESTIONS FOR REVIEW 8. Assume the marginal cost of production is greater than the average variable cost. Can you determine whether the average variable cost is increasing or decreasing?

HW #7: Solutions QUESTIONS FOR REVIEW 8. Assume the marginal cost of production is greater than the average variable cost. Can you determine whether the average variable cost is increasing or decreasing?

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chap 13 Monopolistic Competition and Oligopoly These questions may include topics that were not covered in class and may not be on the exam. MULTIPLE CHOICE. Choose the one alternative that best completes

Chap 13 Monopolistic Competition and Oligopoly These questions may include topics that were not covered in class and may not be on the exam. MULTIPLE CHOICE. Choose the one alternative that best completes

12 PERFECT COMPETITION. Chapter. Answers to the Review Quizzes. Page 275. Page 279

Chapter 12 PERFECT COMPETITION Answers to the Review Quizzes Page 275 1. Why is a firm in perfect competition a price taker? One firm s output is a perfect substitute for another firm s output and each

Chapter 12 PERFECT COMPETITION Answers to the Review Quizzes Page 275 1. Why is a firm in perfect competition a price taker? One firm s output is a perfect substitute for another firm s output and each

PART A: For each worker, determine that worker's marginal product of labor.

ECON 3310 Homework #4 - Solutions 1: Suppose the following indicates how many units of output y you can produce per hour with different levels of labor input (given your current factory capacity): PART

ECON 3310 Homework #4 - Solutions 1: Suppose the following indicates how many units of output y you can produce per hour with different levels of labor input (given your current factory capacity): PART

Chapter 8 Production Technology and Costs 8.1 Economic Costs and Economic Profit

Chapter 8 Production Technology and Costs 8.1 Economic Costs and Economic Profit 1) Accountants include costs as part of a firm's costs, while economists include costs. A) explicit; no explicit B) implicit;

Chapter 8 Production Technology and Costs 8.1 Economic Costs and Economic Profit 1) Accountants include costs as part of a firm's costs, while economists include costs. A) explicit; no explicit B) implicit;

COST THEORY. I What costs matter? A Opportunity Costs

COST THEORY Cost theory is related to production theory, they are often used together. However, the question is how much to produce, as opposed to which inputs to use. That is, assume that we use production

COST THEORY Cost theory is related to production theory, they are often used together. However, the question is how much to produce, as opposed to which inputs to use. That is, assume that we use production

A. a change in demand. B. a change in quantity demanded. C. a change in quantity supplied. D. unit elasticity. E. a change in average variable cost.

1. The supply of gasoline changes, causing the price of gasoline to change. The resulting movement from one point to another along the demand curve for gasoline is called A. a change in demand. B. a change

1. The supply of gasoline changes, causing the price of gasoline to change. The resulting movement from one point to another along the demand curve for gasoline is called A. a change in demand. B. a change

Practice Multiple Choice Questions Answers are bolded. Explanations to come soon!!

Practice Multiple Choice Questions Answers are bolded. Explanations to come soon!! For more, please visit: http://courses.missouristate.edu/reedolsen/courses/eco165/qeq.htm Market Equilibrium and Applications

Practice Multiple Choice Questions Answers are bolded. Explanations to come soon!! For more, please visit: http://courses.missouristate.edu/reedolsen/courses/eco165/qeq.htm Market Equilibrium and Applications

Chapter 22 The Cost of Production Extra Multiple Choice Questions for Review

Chapter 22 The Cost of Production Extra Multiple Choice Questions for Review 1. Implicit costs are: A) equal to total fixed costs. B) comprised entirely of variable costs. C) "payments" for self-employed

Chapter 22 The Cost of Production Extra Multiple Choice Questions for Review 1. Implicit costs are: A) equal to total fixed costs. B) comprised entirely of variable costs. C) "payments" for self-employed

N. Gregory Mankiw Principles of Economics. Chapter 14. FIRMS IN COMPETITIVE MARKETS

N. Gregory Mankiw Principles of Economics Chapter 14. FIRMS IN COMPETITIVE MARKETS Solutions to Problems and Applications 1. A competitive market is one in which: (1) there are many buyers and many sellers

N. Gregory Mankiw Principles of Economics Chapter 14. FIRMS IN COMPETITIVE MARKETS Solutions to Problems and Applications 1. A competitive market is one in which: (1) there are many buyers and many sellers

Market for cream: P 1 P 2 D 1 D 2 Q 2 Q 1. Individual firm: W Market for labor: W, S MRP w 1 w 2 D 1 D 1 D 2 D 2

Factor Markets Problem 1 (APT 93, P2) Two goods, coffee and cream, are complements. Due to a natural disaster in Brazil that drastically reduces the supply of coffee in the world market the price of coffee

Factor Markets Problem 1 (APT 93, P2) Two goods, coffee and cream, are complements. Due to a natural disaster in Brazil that drastically reduces the supply of coffee in the world market the price of coffee

Econ 101: Principles of Microeconomics

Econ 101: Principles of Microeconomics Chapter 16 - Monopolistic Competition and Product Differentiation Fall 2010 Herriges (ISU) Ch. 16 Monopolistic Competition Fall 2010 1 / 18 Outline 1 What is Monopolistic

Econ 101: Principles of Microeconomics Chapter 16 - Monopolistic Competition and Product Differentiation Fall 2010 Herriges (ISU) Ch. 16 Monopolistic Competition Fall 2010 1 / 18 Outline 1 What is Monopolistic

Figure: Computing Monopoly Profit

Name: Date: 1. Most electric, gas, and water companies are examples of: A) unregulated monopolies. B) natural monopolies. C) restricted-input monopolies. D) sunk-cost monopolies. Use the following to answer

Name: Date: 1. Most electric, gas, and water companies are examples of: A) unregulated monopolies. B) natural monopolies. C) restricted-input monopolies. D) sunk-cost monopolies. Use the following to answer

22 COMPETITIVE MARKETS IN THE LONG-RUN

22 COMPETITIVE MARKETS IN THE LONG-RUN Purpose: To illustrate price determination in the long-run in a competitive market. Computer file: lrmkt198.xls Instructions and background information: You are a

22 COMPETITIVE MARKETS IN THE LONG-RUN Purpose: To illustrate price determination in the long-run in a competitive market. Computer file: lrmkt198.xls Instructions and background information: You are a

Market Supply in the Short Run

Equilibrium in Perfectly Competitive Markets (Assume for simplicity that all firms have access to the same technology and input markets, so they all have the same cost curves.) Market Supply in the Short

Equilibrium in Perfectly Competitive Markets (Assume for simplicity that all firms have access to the same technology and input markets, so they all have the same cost curves.) Market Supply in the Short

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The four-firm concentration ratio equals the percentage of the value of accounted for by the four

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The four-firm concentration ratio equals the percentage of the value of accounted for by the four

Monopoly WHY MONOPOLIES ARISE

In this chapter, look for the answers to these questions: Why do monopolies arise? Why is MR < P for a monopolist? How do monopolies choose their P and Q? How do monopolies affect society s well-being?

In this chapter, look for the answers to these questions: Why do monopolies arise? Why is MR < P for a monopolist? How do monopolies choose their P and Q? How do monopolies affect society s well-being?

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Economics 103 Spring 2012: Multiple choice review questions for final exam. Exam will cover chapters on perfect competition, monopoly, monopolistic competition and oligopoly up to the Nash equilibrium

Economics 103 Spring 2012: Multiple choice review questions for final exam. Exam will cover chapters on perfect competition, monopoly, monopolistic competition and oligopoly up to the Nash equilibrium

Pre-Test Chapter 18 ed17

Pre-Test Chapter 18 ed17 Multiple Choice Questions 1. (Consider This) Elastic demand is analogous to a and inelastic demand to a. A. normal wrench; socket wrench B. Ace bandage; firm rubber tie-down C.

Pre-Test Chapter 18 ed17 Multiple Choice Questions 1. (Consider This) Elastic demand is analogous to a and inelastic demand to a. A. normal wrench; socket wrench B. Ace bandage; firm rubber tie-down C.

Pure Competition urely competitive markets are used as the benchmark to evaluate market

R. Larry Reynolds Pure Competition urely competitive markets are used as the benchmark to evaluate market P performance. It is generally believed that market structure influences the behavior and performance

R. Larry Reynolds Pure Competition urely competitive markets are used as the benchmark to evaluate market P performance. It is generally believed that market structure influences the behavior and performance

Econ 101: Principles of Microeconomics

Econ 101: Principles of Microeconomics Chapter 12 - Behind the Supply Curve - Inputs and Costs Fall 2010 Herriges (ISU) Ch. 12 Behind the Supply Curve Fall 2010 1 / 30 Outline 1 The Production Function

Econ 101: Principles of Microeconomics Chapter 12 - Behind the Supply Curve - Inputs and Costs Fall 2010 Herriges (ISU) Ch. 12 Behind the Supply Curve Fall 2010 1 / 30 Outline 1 The Production Function

4. Market Structures. Learning Objectives 4-63. Market Structures

1. Supply and Demand: Introduction 3 2. Supply and Demand: Consumer Demand 33 3. Supply and Demand: Company Analysis 43 4. Market Structures 63 5. Key Formulas 81 2014 Allen Resources, Inc. All rights

1. Supply and Demand: Introduction 3 2. Supply and Demand: Consumer Demand 33 3. Supply and Demand: Company Analysis 43 4. Market Structures 63 5. Key Formulas 81 2014 Allen Resources, Inc. All rights

Practice Questions Week 6 Day 1

Practice Questions Week 6 Day 1 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Economists assume that the goal of the firm is to a. maximize total revenue

Practice Questions Week 6 Day 1 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Economists assume that the goal of the firm is to a. maximize total revenue

Chapter 14 Monopoly. 14.1 Monopoly and How It Arises

Chapter 14 Monopoly 14.1 Monopoly and How It Arises 1) One of the requirements for a monopoly is that A) products are high priced. B) there are several close substitutes for the product. C) there is a

Chapter 14 Monopoly 14.1 Monopoly and How It Arises 1) One of the requirements for a monopoly is that A) products are high priced. B) there are several close substitutes for the product. C) there is a

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Firms that survive in the long run are usually those that A) remain small. B) strive for the largest

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Firms that survive in the long run are usually those that A) remain small. B) strive for the largest

INTRODUCTORY MICROECONOMICS

INTRODUCTORY MICROECONOMICS UNIT-I PRODUCTION POSSIBILITIES CURVE The production possibilities (PP) curve is a graphical medium of highlighting the central problem of 'what to produce'. To decide what

INTRODUCTORY MICROECONOMICS UNIT-I PRODUCTION POSSIBILITIES CURVE The production possibilities (PP) curve is a graphical medium of highlighting the central problem of 'what to produce'. To decide what

Principles of Economics: Micro: Exam #2: Chapters 1-10 Page 1 of 9

Principles of Economics: Micro: Exam #2: Chapters 1-10 Page 1 of 9 print name on the line above as your signature INSTRUCTIONS: 1. This Exam #2 must be completed within the allocated time (i.e., between

Principles of Economics: Micro: Exam #2: Chapters 1-10 Page 1 of 9 print name on the line above as your signature INSTRUCTIONS: 1. This Exam #2 must be completed within the allocated time (i.e., between

Oligopoly: How do firms behave when there are only a few competitors? These firms produce all or most of their industry s output.

Topic 8 Chapter 13 Oligopoly and Monopolistic Competition Econ 203 Topic 8 page 1 Oligopoly: How do firms behave when there are only a few competitors? These firms produce all or most of their industry

Topic 8 Chapter 13 Oligopoly and Monopolistic Competition Econ 203 Topic 8 page 1 Oligopoly: How do firms behave when there are only a few competitors? These firms produce all or most of their industry

How To Calculate Profit Maximization In A Competitive Dairy Firm

Microeconomic FRQ s 2005 1. Bestmilk, a typical profit-maximizing dairy firm, is operating in a constant-cost, perfectly competitive industry that is in long-run equilibrium. a. Draw correctly-labeled

Microeconomic FRQ s 2005 1. Bestmilk, a typical profit-maximizing dairy firm, is operating in a constant-cost, perfectly competitive industry that is in long-run equilibrium. a. Draw correctly-labeled

Revenue Structure, Objectives of a Firm and. Break-Even Analysis.

Revenue :The income receipt by way of sale proceeds is the revenue of the firm. As with costs, we need to study concepts of total, average and marginal revenues. Each unit of output sold in the market

Revenue :The income receipt by way of sale proceeds is the revenue of the firm. As with costs, we need to study concepts of total, average and marginal revenues. Each unit of output sold in the market

CE2451 Engineering Economics & Cost Analysis. Objectives of this course

CE2451 Engineering Economics & Cost Analysis Dr. M. Selvakumar Associate Professor Department of Civil Engineering Sri Venkateswara College of Engineering Objectives of this course The main objective of

CE2451 Engineering Economics & Cost Analysis Dr. M. Selvakumar Associate Professor Department of Civil Engineering Sri Venkateswara College of Engineering Objectives of this course The main objective of

LIST OF MEMBERS WHO PREPARED QUESTION BANK FOR ECONOMICS FOR CLASS XII TEAM MEMBERS. Sl. No. Name Designation

LIST OF MEMBERS WHO PREPARED QUESTION BANK FOR ECONOMICS FOR CLASS XII TEAM MEMBERS Sl. No. Name Designation 1. Mrs. Neelam Vinayak V. Principal (Team Leader) G.G.S.S. Deputy Ganj, Sadar Bazar Delhi-110006

LIST OF MEMBERS WHO PREPARED QUESTION BANK FOR ECONOMICS FOR CLASS XII TEAM MEMBERS Sl. No. Name Designation 1. Mrs. Neelam Vinayak V. Principal (Team Leader) G.G.S.S. Deputy Ganj, Sadar Bazar Delhi-110006

Chapter 05 Perfect Competition, Monopoly, and Economic

Chapter 05 Perfect Competition, Monopoly, and Economic Multiple Choice Questions Use Figure 5.1 to answer questions 1-2: Figure 5.1 1. In Figure 5.1 above, what output would a perfect competitor produce?

Chapter 05 Perfect Competition, Monopoly, and Economic Multiple Choice Questions Use Figure 5.1 to answer questions 1-2: Figure 5.1 1. In Figure 5.1 above, what output would a perfect competitor produce?

Cost OVERVIEW. WSG6 7/7/03 4:36 PM Page 79. Copyright 2003 by Academic Press. All rights of reproduction in any form reserved.

WSG6 7/7/03 4:36 PM Page 79 6 Cost OVERVIEW The previous chapter reviewed the theoretical implications of the technological process whereby factors of production are efficiently transformed into goods

WSG6 7/7/03 4:36 PM Page 79 6 Cost OVERVIEW The previous chapter reviewed the theoretical implications of the technological process whereby factors of production are efficiently transformed into goods

Microeconomics and mathematics (with answers) 5 Cost, revenue and profit

5 Cost, revenue and profit") Microeconomics and mathematics (with answers) 5 Cost, revenue and profit Remarks: = uantity Costs TC = Total cost (= AC * ) AC = Average cost (= TC ) MC = Marginal cost [= (TC)'] FC = Fixed cost VC = (Total)

Microeconomics and mathematics (with answers) 5 Cost, revenue and profit Remarks: = uantity Costs TC = Total cost (= AC * ) AC = Average cost (= TC ) MC = Marginal cost [= (TC)'] FC = Fixed cost VC = (Total)

SAMPLE PAPER II ECONOMICS Class - XII BLUE PRINT

SAMPLE PAPER II ECONOMICS Class - XII Maximum Marks 100 Time : 3 hrs. BLUE PRINT Sl. No. Form of Very Short Short Answer Long Answer Total Questions (1 Mark) (3, 4 Marks) (6 Marks) Content Unit 1 Unit

SAMPLE PAPER II ECONOMICS Class - XII Maximum Marks 100 Time : 3 hrs. BLUE PRINT Sl. No. Form of Very Short Short Answer Long Answer Total Questions (1 Mark) (3, 4 Marks) (6 Marks) Content Unit 1 Unit

Pre-Test Chapter 23 ed17

Pre-Test Chapter 23 ed17 Multiple Choice Questions 1. The kinked-demand curve model of oligopoly: A. assumes a firm's rivals will ignore a price cut but match a price increase. B. embodies the possibility

Pre-Test Chapter 23 ed17 Multiple Choice Questions 1. The kinked-demand curve model of oligopoly: A. assumes a firm's rivals will ignore a price cut but match a price increase. B. embodies the possibility

Final Exam 15 December 2006

Eco 301 Name Final Exam 15 December 2006 120 points. Please write all answers in ink. You may use pencil and a straight edge to draw graphs. Allocate your time efficiently. Part 1 (10 points each) 1. As

Eco 301 Name Final Exam 15 December 2006 120 points. Please write all answers in ink. You may use pencil and a straight edge to draw graphs. Allocate your time efficiently. Part 1 (10 points each) 1. As

Perfect Competition. Chapter CHAPTER OUTLINE. What s New in this Edition? CHAPTER ROADMAP

Perfect Competition Chapter CHAPTER OUTLINE 1. Explain a perfectly competitive firm s profit-maximizing choices and derive its supply curve. A. Perfect Competition B. Other Market Types C. Price Taker

Perfect Competition Chapter CHAPTER OUTLINE 1. Explain a perfectly competitive firm s profit-maximizing choices and derive its supply curve. A. Perfect Competition B. Other Market Types C. Price Taker

Profit maximization in different market structures

Profit maximization in different market structures In the cappuccino problem as well in your team project, demand is clearly downward sloping if the store wants to sell more drink, it has to lower the

Profit maximization in different market structures In the cappuccino problem as well in your team project, demand is clearly downward sloping if the store wants to sell more drink, it has to lower the

Market Structure: Oligopoly (Imperfect Competition)

") Market Structure: Oligopoly (Imperfect Competition) I. Characteristics of Imperfectly Competitive Industries A. Monopolistic Competition large number of potential buyers and sellers differentiated product

Market Structure: Oligopoly (Imperfect Competition) I. Characteristics of Imperfectly Competitive Industries A. Monopolistic Competition large number of potential buyers and sellers differentiated product

A2 Micro Business Economics Diagrams

A2 Micro Business Economics Diagrams Advice on drawing diagrams in the exam The right size for a diagram is ½ of a side of A4 don t make them too small if needed, move onto a new side of paper rather than

A2 Micro Business Economics Diagrams Advice on drawing diagrams in the exam The right size for a diagram is ½ of a side of A4 don t make them too small if needed, move onto a new side of paper rather than

BEE2017 Intermediate Microeconomics 2

BEE2017 Intermediate Microeconomics 2 Dieter Balkenborg Sotiris Karkalakos Yiannis Vailakis Organisation Lectures Mon 14:00-15:00, STC/C Wed 12:00-13:00, STC/D Tutorials Mon 15:00-16:00, STC/106 (will

BEE2017 Intermediate Microeconomics 2 Dieter Balkenborg Sotiris Karkalakos Yiannis Vailakis Organisation Lectures Mon 14:00-15:00, STC/C Wed 12:00-13:00, STC/D Tutorials Mon 15:00-16:00, STC/106 (will

Microeconomics Topic 6: Be able to explain and calculate average and marginal cost to make production decisions.

Microeconomics Topic 6: Be able to explain and calculate average and marginal cost to make production decisions. Reference: Gregory Mankiw s Principles of Microeconomics, 2 nd edition, Chapter 13. Long-Run

Microeconomics Topic 6: Be able to explain and calculate average and marginal cost to make production decisions. Reference: Gregory Mankiw s Principles of Microeconomics, 2 nd edition, Chapter 13. Long-Run

Chapter 5 The Production Process and Costs

Managerial Economics & Business Strategy Chapter 5 The Production Process and Costs McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. Overview I. Production Analysis

Managerial Economics & Business Strategy Chapter 5 The Production Process and Costs McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. Overview I. Production Analysis

Pre-Test Chapter 20 ed17

Pre-Test Chapter 20 ed17 Multiple Choice Questions 1. In the above diagram it is assumed that: A. some costs are fixed and other costs are variable. B. all costs are variable. C. the law of diminishing

Pre-Test Chapter 20 ed17 Multiple Choice Questions 1. In the above diagram it is assumed that: A. some costs are fixed and other costs are variable. B. all costs are variable. C. the law of diminishing

CHAPTER 12 MARKETS WITH MARKET POWER Microeconomics in Context (Goodwin, et al.), 2 nd Edition

, 2 nd Edition") CHAPTER 12 MARKETS WITH MARKET POWER Microeconomics in Context (Goodwin, et al.), 2 nd Edition Chapter Summary Now that you understand the model of a perfectly competitive market, this chapter complicates

CHAPTER 12 MARKETS WITH MARKET POWER Microeconomics in Context (Goodwin, et al.), 2 nd Edition Chapter Summary Now that you understand the model of a perfectly competitive market, this chapter complicates

Demand, Supply and Elasticity

Demand, Supply and Elasticity CHAPTER 2 OUTLINE 2.1 Demand and Supply Definitions, Determinants and Disturbances 2.2 The Market Mechanism 2.3 Changes in Market Equilibrium 2.4 Elasticities of Supply and

Demand, Supply and Elasticity CHAPTER 2 OUTLINE 2.1 Demand and Supply Definitions, Determinants and Disturbances 2.2 The Market Mechanism 2.3 Changes in Market Equilibrium 2.4 Elasticities of Supply and