Asset Revaluation or Impairment?

|

|

|

- Mervin Edwards

- 9 years ago

- Views:

Transcription

1 Asset Revaluation or Impairment? Session ID#: TBD Understanding the Accounting for Fixed Assets in Release 12 Prepared by: Brian Lewis, CPA Corporate Controller eprentise, REMINDER Check in on the COLLABORATE mobile app

2 : Transformation Software for E-Business Suite Company Overview: Incorporated 2007 Helene Abrams, CEO eprentise Can Consolidate Multiple EBS Instances Change Underlying Structures and Configurations Chart of Accounts, Other Flexfields Inventory Organizations Operating Groups, Legal Entities, Ledgers Calendars Costing Methods Resolve Duplicates, Change Sequences, IDs Separate Data So Our Customers Can: Reduce Operating Costs and Increase Efficiencies Shared Services Data Centers Adapt to Change Align with New Business Initiatives Mergers, Acquisitions, Divestitures Pattern-Based Strategies Make ERP an Adaptive Technology Avoid a Reimplementation Reduce Complexity and Control Risk Improve Business Continuity, Service Quality and Compliance Establish Data Quality Standards and a Single Source of Truth

3 Learning Objectives Objective 1: Understand how IFRS requirements compare to U.S. GAAP requirements. Objective 2: Explain fixed asset functionality in Oracle E- Business Suite Release 12. Objective 3: Identify how cost and revaluation model assets are adjusted during an acquisition or divestiture.

4 Agenda Introduction IFRS and U.S. GAAP Reporting in Oracle E-Business Suite Accounting for Fixed Assets Under IFRS and U.S. GAAP Revaluation of Fixed Assets Depreciation After Revaluation Decline in Value After a Revaluation Impairment EBS Considerations for the Revaluation Model Revaluing Assets in a Merger/Acquisition Conclusion Questions

5 IFRS and U.S. GAAP Reporting in Oracle E-Business Suite (EBS) Update on IFRS: Why it is important for fixed asset reporting even if you are solely U.S. GAAP? Dual-reporting requirements IFRS-U.S. GAAP convergence Numerous features in both 11i and R12 to accommodate extensive differences in the reporting frameworks Focus will be on fixed assets accounting

6 Overview of New Fixed Assets Functionality in R12 Full SLA integration Enhanced mass additions Mass additions auto-prepare XML reporting Automatic depreciation rollback Enhanced energy industry enhancements Retirements and revaluation enhancements

7 Accounting for Fixed Assets Under IFRS and U.S. GAAP Two general models for accounting for fixed assets: U.S. GAAP IFRS: Cost (similar to U.S. GAAP) Revaluation model Impairment (common to both models)

8 Comparing IFRS and U.S. GAAP for Fixed Asset Accounting U.S. GAAP IFRS Depreciation Same Same Revaluation Depreciation after Revaluation Impairment Prohibited N/A Direct Write Down Allowed/Create Revaluation Surplus Allowed Write Down to Revaluation Surplus First, then Direct Write Down

9 Why Both Models are Correct U.S. GAAP is a conservative rule-based accounting standard that focuses on P & L (profit and loss) financials for use of owners of the entity (shareholders) IFRS is more of a principle-based accounting standard that focuses on the balance sheet primarily for creditors of the entity

10 Revaluation of Fixed Assets Revaluation of a company's assets takes into account inflation or changes in fair value since the assets were purchased or acquired. There must be persuasive evidence to revalue.

11 Revaluation for a Single or a Few Asset(s) Typically real property that has appreciated in value.

12 Example of a Single Asset Revaluation Consider the example of Acme Ltd. used in the cost model. Assume that on December 31, 2010, the company intends to switch to a revaluation model and carries out a revaluation exercise which estimates the fair value of the building to be $190,000 (again, at December 31, 2010). The carrying amount at the date is $170,000 and revalued amount is $190,000, so an upward adjustment of $20,000 is required for the building account.

13 Revaluation Event Building Rises Significantly in Value In the case of Acme Ltd: Will switch to a revaluation model on December 31, 2010 The carrying amount at the date is $170,000 The revalued amount is $190,000 An upward adjustment of $20,000 is required for the building account: Building 20,000 Revaluation Surplus 20,000

14 Accounting Effect of Revaluation Upward revaluation is not considered a normal gain and is not recorded on the income statement Rather, it is directly credited to an equity account called revaluation surplus Revaluation surplus holds all the upward revaluations of a company's assets until those assets are disposed

15 Depreciation after Revaluation The depreciation in periods after revaluation is based on the revalued amount. In the case of Acme Ltd: Will switch to a revaluation model on December 31, 2010 The carrying amount at the date is $170,000 The revalued amount is $190,000 An upward adjustment of $20,000 is required for the building account Depreciation for 2011 was the new carrying amount divided by the remaining useful life, or $190,000/17 which equals $11,176

16 Decline in Value Suppose on December 31, 2012, Acme Ltd. revalues the building again to find out that the fair value should be $160,000 The carrying amount as of December 31, 2012, is $190,000 minus two years depreciation of $22,352, which amounts to $167,648 The carrying amount exceeds the fair value by $7,648, so the account balance should be reduced by that amount We already have a balance of $20,000 in the revaluation surplus account related to the same building, so no impairment loss will go to the income statement

17 Journal Entry for a Decline in Value with a Prior Revaluation Surplus In the case of Acme Ltd.: Revalues the building again on December 31, fair value should be $160,000 The carrying amount is $190,000 minus two years depreciation of $22,352, which amounts to $167,648 The carrying amount exceeds the fair value by $7,648 Already has a balance of $20,000 in the revaluation surplus, so no impairment loss will go to the income statement Revaluation Surplus 7,648 Building Account 7,648

18 Impairment When the Value Declines More than the Revaluation Surplus Had the fair value been $140,000, the excess of the carrying amount over fair value would have been $27,648 In that situation, the following journal entry would have been required: Revaluation Surplus 20,000 Impairment Losses 7,648 Building 20,000 Accumulated Impairment Losses 7,648 Gain in Value of Building 300,000 Revaluation Surplus 20,000 Note: Under U.S. GAAP, assets are not revalued except in business combinations (mergers).

.")

19 Revaluation in EBS In EBS, you can revalue all categories in a fixed asset book (mass revaluation) all assets in a category, or just individual assets.

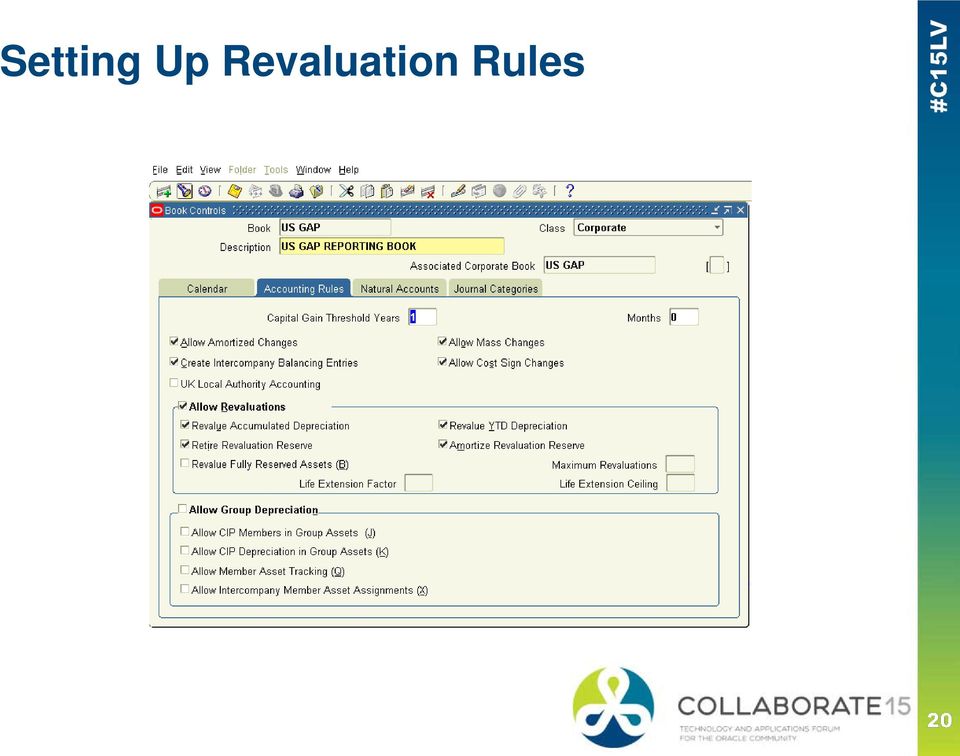

20 Setting Up Revaluation Rules

21 The Mass Revaluation Process Includes the Following Steps: Create Mass Revaluation Definition Preview Revaluation Run Revaluation Optionally Review Revaluation

22 Mass Revaluations Screen

23 To Revalue All Assets in a Category Navigate to the Mass Revaluations window Enter the book for which you want to revalue assets Enter a description for the revaluation definition Important: Note the mass transaction number Specify revaluation rule Enter the category you want to revalue Enter the revaluation percentage rate to revalue your assets Enter either a positive or negative number

24 To Revalue All Assets in a Category Override default revaluation rules if necessary Choose Preview Note: You must preview before EBS will let you proceed If, after previewing, you need to make changes, edit the revaluation rule or percentage Find the revaluation definition using the Mass Transaction Number Choose Run Oracle Assets begins a concurrent process to perform the revaluation Review the log file after the request completes

25 To Revalue an Individual Asset Enter the asset number you wish to revalue instead of a category.

26 Revaluing Assets in a Merger/Acquisition Under Financial Accounting Standard 141(R) and IFRS 3, Business Combinations, acquired companies are required to revalue their assets to fair value at date of acquisition.

27 Oracle Mass Revaluation (OMR) OMR functionality will not work for these types of revaluations for the following reasons: The date placed in-service must be changed to date of the business combination OMR does not support this OMR mass and category revaluation will not accommodate netting accumulated depreciation or loading multiple, nonpercentage driven fair value restatements Individual asset revaluation is impractical for large numbers of assets and also does not accommodate netting accumulated depreciation or resetting the date placed in service

28 Conclusion Addressing fixed assets in both the U.S. GAAP and IFRS accounting models has become easier in R12 The flexibility of the accounting rule setup allows requirements in different legislative, geographic or industry contexts within a single instance The mass additions and automatic preparation processes can be used to convert data from legacy systems following an acquisition or consolidation Reporting is flexible with prepopulated or customizable templates

29 Questions? Comments?

30 THANK YOU Brian Lewis, CPA eprentise Accelerating the time for change in Oracle E-Business Suite Visit eprentise at booth 1225! 30

31 Please complete the session evaluation We appreciate your feedback and insight You may complete the session evaluation either on paper or online via the mobile app

Subledger Accounting Reconciliation in R12

Subledger Accounting Reconciliation in R12 Karen Kerames Accenture 2013 eprentise. All rights reserved. Webinar Mechanics Open and close your panel. View, select, and test your audio. Submit text questions.

Subledger Accounting Reconciliation in R12 Karen Kerames Accenture 2013 eprentise. All rights reserved. Webinar Mechanics Open and close your panel. View, select, and test your audio. Submit text questions.

To Cross-Validate or Not? Best Practices to Enforce Valid GL Combinations. Helene Abrams CEO eprentise [email protected]

To Cross-Validate or Not? Best Practices to Enforce Valid GL Combinations Helene Abrams CEO eprentise [email protected] Webinar Mechanics Open and close your panel. View, select, and test your audio.

To Cross-Validate or Not? Best Practices to Enforce Valid GL Combinations Helene Abrams CEO eprentise [email protected] Webinar Mechanics Open and close your panel. View, select, and test your audio.

Losing Control: Controls, Risks, Governance, and Stewardship of Enterprise Data

Losing Control: Controls, Risks, Governance, and Stewardship of Enterprise Data an eprentise white paper tel: 407.290.6952 toll-free: 1.888.943.5363 web: www.eprentise.com Author: Helene Abrams Published:

Losing Control: Controls, Risks, Governance, and Stewardship of Enterprise Data an eprentise white paper tel: 407.290.6952 toll-free: 1.888.943.5363 web: www.eprentise.com Author: Helene Abrams Published:

How to Reduce: 10 Benefits of Instance Consolidation in Oracle E-Business Suite

How to Reduce: 10 Benefits of Instance Consolidation in Oracle E-Business Suite Monday, September 20, 2010 2:00 PM Moscone West L2, Room 2018 Session ID: S316469 Helene Abrams Founder and CEO eprentise,

How to Reduce: 10 Benefits of Instance Consolidation in Oracle E-Business Suite Monday, September 20, 2010 2:00 PM Moscone West L2, Room 2018 Session ID: S316469 Helene Abrams Founder and CEO eprentise,

Getting to One: Consolidating Multiple Charts of Accounts During an Oracle E-Business Suite Upgrade

Getting to One: Consolidating Multiple Charts of Accounts During an Oracle E-Business Suite Upgrade Bob Von Der Ahe Experian Paul Phillips CARQUEST Helene Abrams eprentise Introduction A single global

Getting to One: Consolidating Multiple Charts of Accounts During an Oracle E-Business Suite Upgrade Bob Von Der Ahe Experian Paul Phillips CARQUEST Helene Abrams eprentise Introduction A single global

PEOPLESOFT ENTERPRISE ASSET MANAGEMENT

PEOPLESOFT ENTERPRISE ASSET MANAGEMENT Oracle s PeopleSoft Enterprise Asset Management is a critical component of the Plan-to-Retire business process that provides enterprise-wide integration across the

PEOPLESOFT ENTERPRISE ASSET MANAGEMENT Oracle s PeopleSoft Enterprise Asset Management is a critical component of the Plan-to-Retire business process that provides enterprise-wide integration across the

Overview of Oracle Asset Management

Overview of Oracle Asset Management Overview Effective mm/dd/yy Page 1 of 48 Rev 1 System References None Distribution Oracle Assets Job Title * Ownership The Job Title [[email protected]?subject=eduxxxxx]

Overview of Oracle Asset Management Overview Effective mm/dd/yy Page 1 of 48 Rev 1 System References None Distribution Oracle Assets Job Title * Ownership The Job Title [[email protected]?subject=eduxxxxx]

PeopleSoft v9.1 Asset Management

PeopleSoft v9.1 Asset Management Training Manual Contact Information: SpearMC Consulting, Inc. 1-866-SPEARMC [email protected] www.spearmc.com TABLE OF CONTENTS... ERROR! BOOKMARK NOT DEFINED. PURPOSE...

PeopleSoft v9.1 Asset Management Training Manual Contact Information: SpearMC Consulting, Inc. 1-866-SPEARMC [email protected] www.spearmc.com TABLE OF CONTENTS... ERROR! BOOKMARK NOT DEFINED. PURPOSE...

Oracle E-Business Suite - Release 12 Oracle General Ledger Technology Course Material April-2009

Oracle E-Business Suite - Release 12 Oracle General Ledger Technology Course Material April-2009 1 Contents 1. Introduction 2. Accounting Manager Setup 3. General Ledger -Key Setups 4. Journal Entry 5.

Oracle E-Business Suite - Release 12 Oracle General Ledger Technology Course Material April-2009 1 Contents 1. Introduction 2. Accounting Manager Setup 3. General Ledger -Key Setups 4. Journal Entry 5.

Mergers and Acquisitions: How do you Increase the Value of Two Companies Joined Together?

Mergers and Acquisitions: How do you Increase the Value of Two Companies Joined Together? Helene Abrams eprentise Introduction There are few things that generate excitement and speculation like the announcement

Mergers and Acquisitions: How do you Increase the Value of Two Companies Joined Together? Helene Abrams eprentise Introduction There are few things that generate excitement and speculation like the announcement

Chapter 6. Revaluations and impairment testing of non-current assets. Objectives of this lecture. Objectives (cont.)

") Chapter 6 Revaluations and impairment testing of non-current assets PPTs to accompany Deegan, Australian Financial Accounting 7e 6-1 Objectives of this lecture Understand the meaning of fair value Understand

Chapter 6 Revaluations and impairment testing of non-current assets PPTs to accompany Deegan, Australian Financial Accounting 7e 6-1 Objectives of this lecture Understand the meaning of fair value Understand

Essentials of financial consolidation applications

Essentials of financial A white paper prepared by Software 2012 Table of contents Executive summary...3 Overview of financial...3 What is the purpose of financial?...4 Assessing financial solutions...5

Essentials of financial A white paper prepared by Software 2012 Table of contents Executive summary...3 Overview of financial...3 What is the purpose of financial?...4 Assessing financial solutions...5

Financial Statement Presentation. Introduction. Staff draft of an exposure draft

Financial Statement Presentation Staff draft of an exposure draft Introduction The project on financial statement presentation is a joint project of the International Accounting Standards Board (IASB)

Financial Statement Presentation Staff draft of an exposure draft Introduction The project on financial statement presentation is a joint project of the International Accounting Standards Board (IASB)

Norming Asset Management. To make asset management easy and automatic with Sage Accpac ERP

Norming Asset Management To make asset management easy and automatic with Sage Accpac ERP Modules Asset Accounting Asset Maintenance Asset Leasing Asset Tracking Highlights Integrates with Sage Accpac

Norming Asset Management To make asset management easy and automatic with Sage Accpac ERP Modules Asset Accounting Asset Maintenance Asset Leasing Asset Tracking Highlights Integrates with Sage Accpac

Supporting IFRS Compliance with SAP Enterprise Resource Planning System

IBM Global Business Services White Paper Financial Management Supporting IFRS Compliance with SAP Enterprise Resource Planning System IBM Global Business Services 3 IFRS An Overview What is IFRS? International

IBM Global Business Services White Paper Financial Management Supporting IFRS Compliance with SAP Enterprise Resource Planning System IBM Global Business Services 3 IFRS An Overview What is IFRS? International

A Single Version of the Truth Top 10 Benefits of a Global Consolidation

A Single Version of the Truth Top 10 Benefits of a Global Consolidation Paul Phillips CARQUEST Bob Von Der Ahe Experian Helene Abrams eprentise Introduction Two global companies, CARQUEST and Experian,

A Single Version of the Truth Top 10 Benefits of a Global Consolidation Paul Phillips CARQUEST Bob Von Der Ahe Experian Helene Abrams eprentise Introduction Two global companies, CARQUEST and Experian,

Overview of Business Results for the 2nd Quarter of Fiscal Year Ending March 31, 2012 (2Q FY2011)

") November 8, 2011 Overview of Business Results for the 2nd Quarter of Fiscal Year Ending March 31, 2012 () Name of the company: Iwatani Corporation Share traded: TSE, OSE, and NSE first sections Company

November 8, 2011 Overview of Business Results for the 2nd Quarter of Fiscal Year Ending March 31, 2012 () Name of the company: Iwatani Corporation Share traded: TSE, OSE, and NSE first sections Company

Oracle ERP Cloud Period Close Procedures O R A C L E W H I T E P A P E R J U N E 2 0 1 5

Oracle ERP Cloud Period Close Procedures O R A C L E W H I T E P A P E R J U N E 2 0 1 5 Table of Contents Introduction 7 Chapter 1 Period Close Dependencies 8 Chapter 2 Subledger Accounting Overview 9

Oracle ERP Cloud Period Close Procedures O R A C L E W H I T E P A P E R J U N E 2 0 1 5 Table of Contents Introduction 7 Chapter 1 Period Close Dependencies 8 Chapter 2 Subledger Accounting Overview 9

Welcome to the fixed assets topic. 6-2-1

Welcome to the fixed assets topic. 6-2-1 After completing this topic, you will be able to: Explain the process of managing fixed asset items. Recognize key terms in the Fixed Assets solution. Identify

Welcome to the fixed assets topic. 6-2-1 After completing this topic, you will be able to: Explain the process of managing fixed asset items. Recognize key terms in the Fixed Assets solution. Identify

Microsoft Business Contact Manager 2010 - Complete

Microsoft Business Contact Manager 2010 - Complete Introduction Prerequisites Section 1: Getting Started with Business Contact Manager Lesson 1.1: Setting up Business Contact Manager What is Business Contact

Microsoft Business Contact Manager 2010 - Complete Introduction Prerequisites Section 1: Getting Started with Business Contact Manager Lesson 1.1: Setting up Business Contact Manager What is Business Contact

CIP Asset Additions. www.focusthread.com. Overview. Effective mm/dd/yy Page 1 of 27 Rev 1. Copyright Oracle, 2007. All rights reserved.

Overview Effective mm/dd/yy Page 1 of 27 Rev 1 System References None Distribution Oracle Assets Job Title * Ownership The Job Title [[email protected]?subject=eduxxxxx] is responsible for ensuring

Overview Effective mm/dd/yy Page 1 of 27 Rev 1 System References None Distribution Oracle Assets Job Title * Ownership The Job Title [[email protected]?subject=eduxxxxx] is responsible for ensuring

INTANGIBLE ASSETS IAS 38

INTANGIBLE ASSETS IAS 38 Road Map on IAS 38 1. Definition of intangible asset 2. Recognition and measurement 3. Recognition of expense 4. Measurement after recognition 5. Useful life 6. Intangible assets

INTANGIBLE ASSETS IAS 38 Road Map on IAS 38 1. Definition of intangible asset 2. Recognition and measurement 3. Recognition of expense 4. Measurement after recognition 5. Useful life 6. Intangible assets

Fixed Assets setup Fixed Assets posting group Depreciation books Depreciation tables Fixed Assets journals

MODULE 1: FIXED ASSETS SETUP Module Overview Microsoft Dynamics NAV 2013 provides a fully integrated fixed asset management functionality which helps a company manage its assets effectively and efficiently.

MODULE 1: FIXED ASSETS SETUP Module Overview Microsoft Dynamics NAV 2013 provides a fully integrated fixed asset management functionality which helps a company manage its assets effectively and efficiently.

ORACLE FINANCIALS ACCOUNTING HUB

ORACLE FINANCIALS ACCOUNTING HUB KEY FEATURES: A FINANCE TRANSFORMATION SOLUTION Integrated accounting rules repository Create accounting rules for every GAAP Accounting engine Multiple accounting representations

ORACLE FINANCIALS ACCOUNTING HUB KEY FEATURES: A FINANCE TRANSFORMATION SOLUTION Integrated accounting rules repository Create accounting rules for every GAAP Accounting engine Multiple accounting representations

ACCT 265 Chapter 10 Review

ACCT 265 Chapter 10 Review This chapter deals with the accounting for Property Plant & Equipment (PPE) or Capital Assets. When recording cost of PPE, the price of the asset is not the only cost recorded

ACCT 265 Chapter 10 Review This chapter deals with the accounting for Property Plant & Equipment (PPE) or Capital Assets. When recording cost of PPE, the price of the asset is not the only cost recorded

Glossary of Accounting Terms

Glossary of Accounting Terms Account - Something to which transactions are assigned. Accounts in MYOB are in one of eight categories: Asset Liability Equity Income Cost of sales Expense Other income Other

Glossary of Accounting Terms Account - Something to which transactions are assigned. Accounts in MYOB are in one of eight categories: Asset Liability Equity Income Cost of sales Expense Other income Other

Essentials of Financial Consolidation Applications. A white paper prepared by PROPHIX Software October 2010

A white paper prepared by PROPHIX Software October 2010 Table of Contents Executive Summary... 3 Overview of Financial Consolidation... 3 What is the purpose of Financial Consolidation?...4 Assessing Financial

A white paper prepared by PROPHIX Software October 2010 Table of Contents Executive Summary... 3 Overview of Financial Consolidation... 3 What is the purpose of Financial Consolidation?...4 Assessing Financial

Sumitomo Mitsui Trust Holdings, Inc.(SMTH) Financial Results for the Nine Months ended December 31, 2012 [Japanese GAAP] (Consolidated)

![Sumitomo Mitsui Trust Holdings, Inc.(SMTH) Financial Results for the Nine Months ended December 31, 2012 [Japanese GAAP] (Consolidated)](/thumbs/39/19509428.jpg "Sumitomo Mitsui Trust Holdings, Inc.(SMTH) Financial Results for the Nine Months ended December 31, 2012 [Japanese GAAP] (Consolidated)") Sumitomo Mitsui Trust Holdings, Inc.(SMTH) Financial Results for the Nine Months ended December 31, 2012 [Japanese GAAP] (Consolidated) January 31, 2013 Stock exchange listings : Tokyo, Osaka and Nagoya

Sumitomo Mitsui Trust Holdings, Inc.(SMTH) Financial Results for the Nine Months ended December 31, 2012 [Japanese GAAP] (Consolidated) January 31, 2013 Stock exchange listings : Tokyo, Osaka and Nagoya

The statements are presented in pounds sterling and have been prepared under IFRS using the historical cost convention.

Note 1 to the financial information Basis of accounting ITE Group Plc is a UK listed company and together with its subsidiary operations is hereafter referred to as the Company. The Company is required

Note 1 to the financial information Basis of accounting ITE Group Plc is a UK listed company and together with its subsidiary operations is hereafter referred to as the Company. The Company is required

CONVERTING TO THE INTERNATIONAL FINANCIAL REPORTING STANDARDS FREQUENTLY ASKED QUESTIONS REGARDING IFRS AND SAP

Frequently Asked Questions SAP ERP Financials CONVERTING TO THE INTERNATIONAL FINANCIAL REPORTING STANDARDS FREQUENTLY ASKED QUESTIONS REGARDING IFRS AND SAP CONTENT 4 Introduction 4 Terms Used in This

Frequently Asked Questions SAP ERP Financials CONVERTING TO THE INTERNATIONAL FINANCIAL REPORTING STANDARDS FREQUENTLY ASKED QUESTIONS REGARDING IFRS AND SAP CONTENT 4 Introduction 4 Terms Used in This

IASB. Request for Views. Effective Dates and Transition Methods. International Accounting Standards Board

IASB International Accounting Standards Board Request for Views on Effective Dates and Transition Methods Respondents are asked to send their comments electronically to the IASB website (www.ifrs.org),

IASB International Accounting Standards Board Request for Views on Effective Dates and Transition Methods Respondents are asked to send their comments electronically to the IASB website (www.ifrs.org),

Fixed Scope Offering Fusion Financial Implementation

Fixed Scope Offering Fusion Financial Implementation Mindtree limited 2015 Agenda Introduction Business Objectives Product Overview Key Implementation Features Implementation Packages & Timelines Cloud

Fixed Scope Offering Fusion Financial Implementation Mindtree limited 2015 Agenda Introduction Business Objectives Product Overview Key Implementation Features Implementation Packages & Timelines Cloud

Tips and Techniques to Manage Asset Accounting Activities to Stay in Compliance with IFRS. Eric Barlow Managing Partner Serio Consulting

1 Tips and Techniques to Manage Asset Accounting Activities to Stay in Compliance with IFRS Eric Barlow Managing Partner Serio Consulting In This Session Asset Accounting (FI-AA) is one of the areas most

1 Tips and Techniques to Manage Asset Accounting Activities to Stay in Compliance with IFRS Eric Barlow Managing Partner Serio Consulting In This Session Asset Accounting (FI-AA) is one of the areas most

Demystifying Oracle Cloud ERP Financials

Demystifying Oracle Cloud ERP Financials Thank You! Samantha German Based in Fort Worth, TX Over 16 years of Oracle Applications experience Enterprise Architect at CSS CSS Based in Charleston, SC Exclusively

Demystifying Oracle Cloud ERP Financials Thank You! Samantha German Based in Fort Worth, TX Over 16 years of Oracle Applications experience Enterprise Architect at CSS CSS Based in Charleston, SC Exclusively

Fixed Assets Functional Implementation ...

... FA Setups...2 FA Basics...4 Asset Accounting...11 Reconciliation in FA...15 Setting up Depreciation...18 Categories...21 Manual Asset Addition...24 Journal Entries for Manual Asset addition...29 Asset

... FA Setups...2 FA Basics...4 Asset Accounting...11 Reconciliation in FA...15 Setting up Depreciation...18 Categories...21 Manual Asset Addition...24 Journal Entries for Manual Asset addition...29 Asset

Financial Statements

Financial Statements Years ended March 31,2002 and 2003 Contents Consolidated Financial Statements...1 Report of Independent Auditors on Consolidated Financial Statements...2 Consolidated Balance Sheets...3

Financial Statements Years ended March 31,2002 and 2003 Contents Consolidated Financial Statements...1 Report of Independent Auditors on Consolidated Financial Statements...2 Consolidated Balance Sheets...3

Consolidated Statements of Profit or Loss Ricoh Company, Ltd. and Consolidated Subsidiaries For the Years Ended March 31, 2014 and 2015

Consolidated Statements of Profit or Loss Sales: Products 1,041,794 1,071,446 8,928,717 Post sales and rentals 1,064,555 1,068,678 8,905,650 Other revenue 89,347 91,818 765,150 Total sales 2,195,696 2,231,942

Consolidated Statements of Profit or Loss Sales: Products 1,041,794 1,071,446 8,928,717 Post sales and rentals 1,064,555 1,068,678 8,905,650 Other revenue 89,347 91,818 765,150 Total sales 2,195,696 2,231,942

deferred tax RELEVANT TO acca qualification papers f7 and p2

deferred tax RELEVANT TO acca qualification papers f7 and p2 Deferred tax is a topic that is consistently tested in Paper F7, Financial Reporting and is often tested in further detail in Paper P2, Corporate

deferred tax RELEVANT TO acca qualification papers f7 and p2 Deferred tax is a topic that is consistently tested in Paper F7, Financial Reporting and is often tested in further detail in Paper P2, Corporate

Consolidated Financial Results for Six Months Ended September 30, 2007

Consolidated Financial Results for Six Months Ended September 30, 2007 SOHGO SECURITY SERVICES CO., LTD (URL http://ir.alsok.co.jp/english) (Code No.:2331, TSE 1 st Sec.) Representative: Atsushi Murai,

Consolidated Financial Results for Six Months Ended September 30, 2007 SOHGO SECURITY SERVICES CO., LTD (URL http://ir.alsok.co.jp/english) (Code No.:2331, TSE 1 st Sec.) Representative: Atsushi Murai,

The Effects of Changes in Foreign Exchange Rates

Indian Accounting Standard (Ind AS) 21 The Effects of Changes in Foreign Exchange Rates (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority.

Indian Accounting Standard (Ind AS) 21 The Effects of Changes in Foreign Exchange Rates (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority.

Diploma in International Financial Reporting Standards (IFRSs)

") Chartered Accountants Ireland Diploma in International Financial Reporting Standards (IFRSs) Objective This Diploma is designed to provide qualified Chartered Accountants with the opportunity to enhance

Chartered Accountants Ireland Diploma in International Financial Reporting Standards (IFRSs) Objective This Diploma is designed to provide qualified Chartered Accountants with the opportunity to enhance

Reconciliations between IFRS and UK GAAP

Reconciliations between IFRS and UK GAAP The following reconciliations provide a quantification of the effect of the transition to IFRS. The following seven reconciliations provide details of the impact

Reconciliations between IFRS and UK GAAP The following reconciliations provide a quantification of the effect of the transition to IFRS. The following seven reconciliations provide details of the impact

Customer Case Studies on MDM Driving Real Business Value

Customer Case Studies on MDM Driving Real Business Value Dan Gage Oracle Master Data Management Master Data has Domain Specific Requirements CDI (Customer, Supplier, Vendor) PIM (Product, Service) Financial

Customer Case Studies on MDM Driving Real Business Value Dan Gage Oracle Master Data Management Master Data has Domain Specific Requirements CDI (Customer, Supplier, Vendor) PIM (Product, Service) Financial

POLICY ASSET MANAGEMENT - INVESTMENT PROPERTY FINANCE

Document #:5968866 POLICY CP ID: OS Date adopted: 18/09/2012 File no: 416945-1 Minute number: 274/2012 Policy title: Stream: Branch: ASSET MANAGEMENT - INVESTMENT PROPERTY ORGANISATIONAL SERVICES FINANCE

Document #:5968866 POLICY CP ID: OS Date adopted: 18/09/2012 File no: 416945-1 Minute number: 274/2012 Policy title: Stream: Branch: ASSET MANAGEMENT - INVESTMENT PROPERTY ORGANISATIONAL SERVICES FINANCE

GUIDE TO FRS 102 DISCLOSURE

GUIDE TO FRS 102 DISCLOSURE in Relate Accounts +353 1 4597800 +44 871 284 3446 [email protected] www.relate-software.com ROI R005 CONTENTS Relate Accounts Introduction...4 Background...4 The Future

GUIDE TO FRS 102 DISCLOSURE in Relate Accounts +353 1 4597800 +44 871 284 3446 [email protected] www.relate-software.com ROI R005 CONTENTS Relate Accounts Introduction...4 Background...4 The Future

Consolidated Statement of Profit or Loss

Consolidated Statement of Profit or Loss Sales: Products 864,699 1,041,794 $ 10,114,505 Post sales and rentals 941,610 1,064,555 10,335,485 Other revenue 79,686 89,347 867,447 Total sales 1,885,995 2,195,696

Consolidated Statement of Profit or Loss Sales: Products 864,699 1,041,794 $ 10,114,505 Post sales and rentals 941,610 1,064,555 10,335,485 Other revenue 79,686 89,347 867,447 Total sales 1,885,995 2,195,696

ED 4 DISPOSAL OF NON-CURRENT ASSETS AND PRESENTATION OF DISCONTINUED OPERATIONS

Exposure Draft ED 4 DISPOSAL OF NON-CURRENT ASSETS AND PRESENTATION OF DISCONTINUED OPERATIONS Comments to be received by 24 October 2003 ED 4 DISPOSAL OF NON-CURRENT ASSETS AND PRESENTATION OF DISCONTINUED

Exposure Draft ED 4 DISPOSAL OF NON-CURRENT ASSETS AND PRESENTATION OF DISCONTINUED OPERATIONS Comments to be received by 24 October 2003 ED 4 DISPOSAL OF NON-CURRENT ASSETS AND PRESENTATION OF DISCONTINUED

Reminder Mate Instructions

Reminder Mate Instructions Reminder Mate is a Practice Mate add-on Service which will make automated phone calls to remind patients of upcoming scheduled appointments, reduce missed appointments and receive

Reminder Mate Instructions Reminder Mate is a Practice Mate add-on Service which will make automated phone calls to remind patients of upcoming scheduled appointments, reduce missed appointments and receive

Oracle General Ledger Advanced Journal Entries Consolidations Process [ ] Describe, create and [ ] Explain Consolidations

![Oracle General Ledger Advanced Journal Entries Consolidations Process [ ] Describe, create and [ ] Explain Consolidations](/thumbs/27/10234968.jpg "Oracle General Ledger Advanced Journal Entries Consolidations Process [ ] Describe, create and [ ] Explain Consolidations") ERP Solutions Oracle Applications Whether you are implementing Oracle Financials for the first time or you are a veteran user of the Oracle E-Business Suite, Coriolis Business Systems can help reduce the

ERP Solutions Oracle Applications Whether you are implementing Oracle Financials for the first time or you are a veteran user of the Oracle E-Business Suite, Coriolis Business Systems can help reduce the

FINANCIAL REPORTING FLASH REPORT

FINANCIAL REPORTING FLASH REPORT First Quarter Changes Driven by International Convergence and Transparency March 21, 2006 Recent headlines reported 2005 to be another record breaking year for financial

FINANCIAL REPORTING FLASH REPORT First Quarter Changes Driven by International Convergence and Transparency March 21, 2006 Recent headlines reported 2005 to be another record breaking year for financial

How Do I Get Financial Reports from the Cloud

How Do I Get Financial Reports from the Cloud Session ID#: 10435 Prepared by: Lee Briggs Director, Oracle Financials Management BizTech @BTLeeBriggs REMINDER Check in on the COLLABORATE mobile app Please

How Do I Get Financial Reports from the Cloud Session ID#: 10435 Prepared by: Lee Briggs Director, Oracle Financials Management BizTech @BTLeeBriggs REMINDER Check in on the COLLABORATE mobile app Please

Fixed Asset in SAP Business One 9.0

Fixed Asset in SAP Business One 9.0 Hilko Mueller, Solution Management,SAP AG May 2013 2013 SAP AG. All rights reserved. 1 Agenda Fixed Asset Overview Fixed Asset Setup Fixed Asset Application Product

Fixed Asset in SAP Business One 9.0 Hilko Mueller, Solution Management,SAP AG May 2013 2013 SAP AG. All rights reserved. 1 Agenda Fixed Asset Overview Fixed Asset Setup Fixed Asset Application Product

Enterprise Financial Management: ERP for Small and Mid-market Companies

Delivering Oracle Success Enterprise Financial Management: ERP for Small and Mid-market Companies Deb Morton December 7, 2011 Agenda Business Case Representative Company Profile Legacy Issues Evaluate

Delivering Oracle Success Enterprise Financial Management: ERP for Small and Mid-market Companies Deb Morton December 7, 2011 Agenda Business Case Representative Company Profile Legacy Issues Evaluate

International Accounting Standard 16 (IAS 16), Property, Plant and Equipment

, Property, Plant and Equipment") International Accounting Standard 16 (IAS 16), Property, Plant and Equipment By BRIAN FRIEDRICH, MEd, CGA, FCCA(UK), CertIFR and LAURA FRIEDRICH, MSc, CGA, FCCA(UK), CertIFR Updated By STEPHEN SPECTOR,

International Accounting Standard 16 (IAS 16), Property, Plant and Equipment By BRIAN FRIEDRICH, MEd, CGA, FCCA(UK), CertIFR and LAURA FRIEDRICH, MSc, CGA, FCCA(UK), CertIFR Updated By STEPHEN SPECTOR,

International Financial Reporting Standards (IFRS)

") FACT SHEET September 2011 IAS 12 Income Taxes (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial

FACT SHEET September 2011 IAS 12 Income Taxes (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial

Year ended 31 Dec 2009

PACE PLC CHANGE OF FUNCTIONAL AND PRESENTATIONAL CURRENCY AND COMPARATIVES RE-PRESENTED IN US DOLLARS Introduction Pace announced at the time of its preliminary results announcement that the Board had

PACE PLC CHANGE OF FUNCTIONAL AND PRESENTATIONAL CURRENCY AND COMPARATIVES RE-PRESENTED IN US DOLLARS Introduction Pace announced at the time of its preliminary results announcement that the Board had

HansaWorld Enterprise

HansaWorld Enterprise Integrated Accounting, CRM and ERP System for Macintosh, Windows, Linux, PocketPC 2002 and AIX Assets Program version: 4.2 2005-03-04 2004 HansaWorld Ireland Limited, Dublin, Ireland

HansaWorld Enterprise Integrated Accounting, CRM and ERP System for Macintosh, Windows, Linux, PocketPC 2002 and AIX Assets Program version: 4.2 2005-03-04 2004 HansaWorld Ireland Limited, Dublin, Ireland

Diploma in Business Competence. Learning outcomes for the Diploma in Business Competence (EBCL)

") Diploma in Business Competence Learning outcomes for the Diploma in Business Competence (EBCL) Section 1: Understanding Business Accounts Overall Learning Objectives Upon completing this section you will

Diploma in Business Competence Learning outcomes for the Diploma in Business Competence (EBCL) Section 1: Understanding Business Accounts Overall Learning Objectives Upon completing this section you will

Paper F7. Financial Reporting. March/June 2016 Sample Questions. Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Fundamentals Level Skills Module Financial Reporting March/June 2016 Sample Questions Time allowed Reading and planning: 15 minutes Writing: 3 hours This question paper is divided into two sections: Section

Fundamentals Level Skills Module Financial Reporting March/June 2016 Sample Questions Time allowed Reading and planning: 15 minutes Writing: 3 hours This question paper is divided into two sections: Section

WESTERN DIGITAL CORPORATION CONDENSED CONSOLIDATED BALANCE SHEETS. (in millions; unaudited) ASSETS

ASSETS") CONDENSED CONSOLIDATED BALANCE SHEETS (in millions; unaudited) ASSETS Apr. 1, July 3, 2016 2015 Current assets: Cash and cash equivalents $ 5,887 $ 5,024 Short-term investments 146 262 Accounts receivable,

CONDENSED CONSOLIDATED BALANCE SHEETS (in millions; unaudited) ASSETS Apr. 1, July 3, 2016 2015 Current assets: Cash and cash equivalents $ 5,887 $ 5,024 Short-term investments 146 262 Accounts receivable,

Cash is King. cash flow is less likely to be affected

Reading 27: Understanding Cash Flow Statements Relevance of Cash Flow The primary purpose of the statement of cash flows (SCF) is to provide: Info about a firm s cash receipts & cash payments during an

Reading 27: Understanding Cash Flow Statements Relevance of Cash Flow The primary purpose of the statement of cash flows (SCF) is to provide: Info about a firm s cash receipts & cash payments during an

Oracle Fusion Applications Asset Lifecycle Management, Assets Guide. 11g Release 1 (11.1.3) Part Number E22894-03

Part Number E22894-03") Oracle Fusion Applications Asset Lifecycle Management, Assets Guide 11g Release 1 (11.1.3) Part Number E22894-03 December 2011 Oracle Fusion Applications Asset Lifecycle Management, Assets Guide Part Number

Oracle Fusion Applications Asset Lifecycle Management, Assets Guide 11g Release 1 (11.1.3) Part Number E22894-03 December 2011 Oracle Fusion Applications Asset Lifecycle Management, Assets Guide Part Number

Meeting the Needs of Private Equity in the Finance Organization

Meeting the Needs of Private Equity in the Finance Organization When there is a change in a company s ownership, significant changes are generally required in its finance organization. This is especially

Meeting the Needs of Private Equity in the Finance Organization When there is a change in a company s ownership, significant changes are generally required in its finance organization. This is especially

CIMA Managerial Level Paper F2 FINANCIAL MANAGEMENT (REVISION SUMMARIES)

") CIMA Managerial Level Paper F2 FINANCIAL MANAGEMENT (REVISION SUMMARIES) Chapter Title Page number 1 The regulatory framework 3 2 What is a group 9 3 Group accounts the statement of financial position

CIMA Managerial Level Paper F2 FINANCIAL MANAGEMENT (REVISION SUMMARIES) Chapter Title Page number 1 The regulatory framework 3 2 What is a group 9 3 Group accounts the statement of financial position

Top 3 steps to a successful ERP implementation for M&A in manufacturing - a project management point of view

VIEW POINT Top 3 steps to a successful ERP implementation for M&A in manufacturing - a project management point of view Abstract The benefits of a merger and acquisition (M&A) can be great in various ways

VIEW POINT Top 3 steps to a successful ERP implementation for M&A in manufacturing - a project management point of view Abstract The benefits of a merger and acquisition (M&A) can be great in various ways

Consolidated Statement of Profit or Loss (in million Euro)

") Consolidated Statement of Profit or Loss (in million Euro) Q2 2012 Q2 2013 % H1 2012 H1 2013 % Restated * change Restated * change Revenue 779 732-6.0% 1,513 1,437-5.0% Cost of sales (553) (521) -5.8%

Consolidated Statement of Profit or Loss (in million Euro) Q2 2012 Q2 2013 % H1 2012 H1 2013 % Restated * change Restated * change Revenue 779 732-6.0% 1,513 1,437-5.0% Cost of sales (553) (521) -5.8%

JGAAP-IFRS comparison. English version 3.0 [equivalent of Japanese version 4.0]

![JGAAP-IFRS comparison. English version 3.0 [equivalent of Japanese version 4.0]](/thumbs/24/3831703.jpg "JGAAP-IFRS comparison. English version 3.0 [equivalent of Japanese version 4.0]") - comparison English version 3.0 [equivalent of Japanese version 4.0] Contents Contents... 2 Introduction... 3 Presentation of Financial Statements, Accounting Policies, Changes in Accounting Estimates

- comparison English version 3.0 [equivalent of Japanese version 4.0] Contents Contents... 2 Introduction... 3 Presentation of Financial Statements, Accounting Policies, Changes in Accounting Estimates

Benefits. Feature Overview. Architecture. 1 AP Invoice Wizard Fact Sheet

AP Invoice Wizard AP Invoice Wizard enables you to create your Oracle Payable invoices using Excel. Forget about manual data entry when you can now download or copy invoice information into Excel, make

AP Invoice Wizard AP Invoice Wizard enables you to create your Oracle Payable invoices using Excel. Forget about manual data entry when you can now download or copy invoice information into Excel, make

Paper F7 (INT) Financial Reporting (International) Wednesday 5 June 2013. Fundamentals Level Skills Module

Financial Reporting (International) Wednesday 5 June 2013. Fundamentals Level Skills Module") Fundamentals Level Skills Module Financial Reporting (International) Wednesday 5 June 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted.

Fundamentals Level Skills Module Financial Reporting (International) Wednesday 5 June 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted.

What Do I See on Cash Flow Statements?

Cash Flow Statements» What Do I See on Cash Flow Statements» Learning Objectives and Key Take-aways www.navigatingaccounting.com What Do I See on Cash Flow Statements? L E A R N I N G O B J E C T I V E

Cash Flow Statements» What Do I See on Cash Flow Statements» Learning Objectives and Key Take-aways www.navigatingaccounting.com What Do I See on Cash Flow Statements? L E A R N I N G O B J E C T I V E

SOLUTION ADVANCED FINANCIAL REPORTING MAY 2010

(a) WORKINGS CONSOLIDATION SCHEDULE Silver Ltd: Ordinary share capital (60:10) Preference shares (40:60) Capital surplus: At acquisition (60:40) Post acquisition (60:40) (1,070,000 900,000) Fair value

(a) WORKINGS CONSOLIDATION SCHEDULE Silver Ltd: Ordinary share capital (60:10) Preference shares (40:60) Capital surplus: At acquisition (60:40) Post acquisition (60:40) (1,070,000 900,000) Fair value

Understanding Cash Flow Statements

Understanding Cash Flow Statements 2014 Level I Financial Reporting and Analysis IFT Notes for the CFA exam Contents 1. Introduction... 3 2. Components and Format of the Cash Flow Statement... 3 3. The

Understanding Cash Flow Statements 2014 Level I Financial Reporting and Analysis IFT Notes for the CFA exam Contents 1. Introduction... 3 2. Components and Format of the Cash Flow Statement... 3 3. The

MD348 Umoja Asset, Inventory and Equipment Master Data Maintenance. Umoja Asset, Inventory and Equipment Master Data Maintenance Version 5 1

MD348 Umoja Asset, Inventory and Equipment Master Data Maintenance Umoja Asset, Inventory and Equipment Master Data Maintenance Version 5 Copyright Last Modified: United Nations 17-August-13 1 Agenda Course

MD348 Umoja Asset, Inventory and Equipment Master Data Maintenance Umoja Asset, Inventory and Equipment Master Data Maintenance Version 5 Copyright Last Modified: United Nations 17-August-13 1 Agenda Course

Consolidated balance sheet

Consolidated balance sheet Non current assets 31/12/2009 31/12/2008 (*) 01/01/2008 (*) Property, plant and equipment 1,352 1,350 1,144 Investment property 7 11 11 Fixed assets held under concessions 13,089

Consolidated balance sheet Non current assets 31/12/2009 31/12/2008 (*) 01/01/2008 (*) Property, plant and equipment 1,352 1,350 1,144 Investment property 7 11 11 Fixed assets held under concessions 13,089

for Sage 100 ERP General Ledger Overview Document

for Sage 100 ERP General Ledger Document 2012 Sage Software, Inc. All rights reserved. Sage Software, Sage Software logos, and the Sage Software product and service names mentioned herein are registered

for Sage 100 ERP General Ledger Document 2012 Sage Software, Inc. All rights reserved. Sage Software, Sage Software logos, and the Sage Software product and service names mentioned herein are registered

Inform Upgrade Version 20.0.77.77. New Features Improved Google Calendar Synchronization

**The latest Inform upgrade includes features and fixes from all previous upgrades. Please review the upgrade notes for any additional versions that fall between your current version and this upgrade.**

**The latest Inform upgrade includes features and fixes from all previous upgrades. Please review the upgrade notes for any additional versions that fall between your current version and this upgrade.**

Article by Martin Kelly, BSc (Econ) Hons, DIP. Acc, FCA, MBA, MCMI. Examiner in Professional 2 Advanced Corporate Reporting

Hons, DIP. Acc, FCA, MBA, MCMI. Examiner in Professional 2 Advanced Corporate Reporting") IMPAIRMENT - IAS 36 Article by Martin Kelly, BSc (Econ) Hons, DIP. Acc, FCA, MBA, MCMI. Examiner in Professional 2 Advanced Corporate Reporting Introduction Intangible assets, particularly goodwill, have

IMPAIRMENT - IAS 36 Article by Martin Kelly, BSc (Econ) Hons, DIP. Acc, FCA, MBA, MCMI. Examiner in Professional 2 Advanced Corporate Reporting Introduction Intangible assets, particularly goodwill, have

Forecast Financial Statements. Crown Law Office. JUSTICE SECTOR - INFORMATION SUPPORTING THE ESTIMATES 2008/09 B.5A Vol.7 211

Forecast Financial Statements Crown Law Office JUSTICE SECTOR - INFORMATION SUPPORTING THE ESTIMATES B.5A Vol.7 211 Statement of Forecast Financial Performance for the year ending 30 June 2009 Note Income

Forecast Financial Statements Crown Law Office JUSTICE SECTOR - INFORMATION SUPPORTING THE ESTIMATES B.5A Vol.7 211 Statement of Forecast Financial Performance for the year ending 30 June 2009 Note Income

KOREAN AIR LINES CO., LTD. AND SUBSIDIARIES. Consolidated Financial Statements

Consolidated Financial Statements December 31, 2015 (With Independent Auditors Report Thereon) Contents Page Independent Auditors Report 1 Consolidated Statements of Financial Position 3 Consolidated Statements

Consolidated Financial Statements December 31, 2015 (With Independent Auditors Report Thereon) Contents Page Independent Auditors Report 1 Consolidated Statements of Financial Position 3 Consolidated Statements

Accounting Changes and Error Corrections

ACCOUNTING CHANGES Types of Accounting Changes 1. Change in accounting principle-change from one generally accepted accounting principle to another. 2. Change in accounting estimate-revision of an estimate

ACCOUNTING CHANGES Types of Accounting Changes 1. Change in accounting principle-change from one generally accepted accounting principle to another. 2. Change in accounting estimate-revision of an estimate

A change of classification in presentation in financial statements is a change of accounting policy (CAP) under IAS 8.

under IAS 8.") Answers Fundamentals Level Skills Module, Paper F7 Financial Reporting December 2014 Answers Section A 1 A A change of classification in presentation in financial statements is a change of accounting policy

Answers Fundamentals Level Skills Module, Paper F7 Financial Reporting December 2014 Answers Section A 1 A A change of classification in presentation in financial statements is a change of accounting policy

Accounting & Finance. Guidebook

Accounting & Finance Guidebook January 2012 TABLE OF CONTENTS Table of Contents... 2 Preface... 6 Getting Started... 8 Accounting... 10 Accounting Welcome... 10 Sales Quotes... 11 New Sales Quote... 11

Accounting & Finance Guidebook January 2012 TABLE OF CONTENTS Table of Contents... 2 Preface... 6 Getting Started... 8 Accounting... 10 Accounting Welcome... 10 Sales Quotes... 11 New Sales Quote... 11

MYOB EXO FIXED ASSETS

MYOB EXO FIXED ASSETS User Guide 2015.5 Important Notices This material is copyright. It is intended only for MYOB Enterprise Solutions Business Partners and their customers. No part of it may be reproduced

MYOB EXO FIXED ASSETS User Guide 2015.5 Important Notices This material is copyright. It is intended only for MYOB Enterprise Solutions Business Partners and their customers. No part of it may be reproduced

Staples, Inc. Announces First Quarter 2016 Performance

Media Contact: Mark Cautela 508-253-3832 Investor Contact: Chris Powers/Scott Tilghman 508-253-4632/1487 Staples, Inc. Announces First Quarter 2016 Performance FRAMINGHAM, Mass., May 18, 2016 Staples,

Media Contact: Mark Cautela 508-253-3832 Investor Contact: Chris Powers/Scott Tilghman 508-253-4632/1487 Staples, Inc. Announces First Quarter 2016 Performance FRAMINGHAM, Mass., May 18, 2016 Staples,

Asset Management User Guide

Asset Management User Guide Version 9.0 May 2006 Document Number AMUG-90UW-02 Lawson Enterprise Financial Management Legal Notices Lawson does not warrant the content of this document or the results of

Asset Management User Guide Version 9.0 May 2006 Document Number AMUG-90UW-02 Lawson Enterprise Financial Management Legal Notices Lawson does not warrant the content of this document or the results of

ACCOUNTING POLICY 1.1 FINANCIAL REPORTING. Policy Statement. Definitions. Area covered. This Policy is University-wide.

POLICY Area covered ACCOUNTING POLICY This Policy is University-wide Approval date 5 May 2016 Policy Statement Intent Scope Effective date 5 May 2016 Next review date 5 May 2019 To establish decisions,

POLICY Area covered ACCOUNTING POLICY This Policy is University-wide Approval date 5 May 2016 Policy Statement Intent Scope Effective date 5 May 2016 Next review date 5 May 2019 To establish decisions,

Examinable Documents September 2016 to June 2017

Examinable Documents September 2016 to June 2017 FINANCIAL REPORTING The examinable documents below are applicable to the International and UK papers as indicated at the start of each table. Knowledge

Examinable Documents September 2016 to June 2017 FINANCIAL REPORTING The examinable documents below are applicable to the International and UK papers as indicated at the start of each table. Knowledge

CORNING INCORPORATED AND SUBSIDIARY COMPANIES CONSOLIDATED STATEMENTS OF OPERATIONS (Unaudited; in millions, except per share amounts)

") CONSOLIDATED STATEMENTS OF OPERATIONS (Unaudited; in millions, except per share amounts) Three months ended March 31, 2006 2005 As Restated Net sales $ 1,262 $ 1,050 Cost of sales 689 621 Gross margin

CONSOLIDATED STATEMENTS OF OPERATIONS (Unaudited; in millions, except per share amounts) Three months ended March 31, 2006 2005 As Restated Net sales $ 1,262 $ 1,050 Cost of sales 689 621 Gross margin

Consolidated Financial Highlights for the Third Quarter Ended December 31, 2015 [under Japanese GAAP] SMC Corporation

![Consolidated Financial Highlights for the Third Quarter Ended December 31, 2015 [under Japanese GAAP] SMC Corporation](/thumbs/31/15020134.jpg "Consolidated Financial Highlights for the Third Quarter Ended December 31, 2015 [under Japanese GAAP] SMC Corporation") February 9, 2016 Consolidated Financial Highlights for the Third Quarter Ended December 31, [under Japanese GAAP] SMC Corporation Company name : Stock exchange listing : Tokyo Stock Exchange first section

February 9, 2016 Consolidated Financial Highlights for the Third Quarter Ended December 31, [under Japanese GAAP] SMC Corporation Company name : Stock exchange listing : Tokyo Stock Exchange first section

CHAPTER 3 UNDERSTANDING FINANCIAL STATEMENTS

1 CHAPTER 3 UNDERSTANDING FINANCIAL STATEMENTS Financial statements provide the fundamental information that we use to analyze and answer valuation questions. It is important, therefore, that we understand

1 CHAPTER 3 UNDERSTANDING FINANCIAL STATEMENTS Financial statements provide the fundamental information that we use to analyze and answer valuation questions. It is important, therefore, that we understand

Examinable Documents 2013 and June 2014

Examinable Documents 2013 and June 2014 FINANCIAL REPORTING The examinable documents below are applicable to the International and UK papers as indicated at the start of each table Knowledge of new examinable

Examinable Documents 2013 and June 2014 FINANCIAL REPORTING The examinable documents below are applicable to the International and UK papers as indicated at the start of each table Knowledge of new examinable

Finance Effectiveness Efficiency

Business Unit Finance Effectiveness Efficiency An overview Agenda Page 1 Efficiency - An overview 1 2 Our services 7 3 Case study 14 Section 1 Efficiency - An overview 1 Section 1 Efficiency - An overview

Business Unit Finance Effectiveness Efficiency An overview Agenda Page 1 Efficiency - An overview 1 2 Our services 7 3 Case study 14 Section 1 Efficiency - An overview 1 Section 1 Efficiency - An overview

Oracle Assets Special Interest Group (SIG)

") Oracle Assets Special Interest Group (SIG) CONGRATULATIONS! 2010 OAUG Certificate of Distinction Award Meeting Agenda Housekeeping Board Introductions Board/Volunteer Openings SIG Direction / Vision SIG

Oracle Assets Special Interest Group (SIG) CONGRATULATIONS! 2010 OAUG Certificate of Distinction Award Meeting Agenda Housekeeping Board Introductions Board/Volunteer Openings SIG Direction / Vision SIG