Corporate Taxes and Securitization

|

|

|

- Arleen Fletcher

- 7 years ago

- Views:

Transcription

1 Corporate Taxes and Securitization The Journal of Finance by JoongHo Han KDI School of Public Policy and Management Kwangwoo Park Korea Advanced Institute of Science and Technology (KAIST) George Pennacchi University of Illinois 1

George Pennacchi University of")

2 Introduction Until its recent crash, securitization grew tremendously over the last few decades. Securitization has risk management benefits: banks may transfer interest rate and credit risks to investors willing to bear them. But securitization has harmful side effects. Transferring credit risk reduces a bank s incentive to screen the credit of loan applicants and monitor borrowers (Pennacchi, 1988). The current paper emphasizes that securitization may be excessive because it is also motivated by a desire to avoid corporate taxes. Most banks must pay corporate income taxes but special purpose corporations that hold securitized loans do not. 2

.")

3 Contribution of Paper A model is developed to examine the relationship between a bank s loan and deposit market power, its corporate income tax rate, and its incentive to securitize. The model shows that if a bank has profitable lending opportunities but limited deposit market power, then its incentive to securitize increases as its corporate income tax rate rises. Data from Home Mortgage Disclosure Act (HMDA) filings of commercial banks mortgage originations and sales during 2001 to 2008 are used to test the model s predictions. Variation in state corporate income tax rates and MSA demographics allows us to analyze the interaction of taxes, loan and retail deposit opportunities, and loan selling. 3

4 Outline I. A Model of Bank Loan Sales II. Empirical Evidence III. Conclusion 4

5 I. A Model of Bank Loan Sales I.A Assumptions (A1) Each period a bank faces multiple lending opportunities. A one unit loan made to borrower i returns the cash flow of x i (s,a i ) at the end of the period, where s S is the end-of-period state of nature and a i is the bank s initial credit screening/monitoring. (A2) x i (s,a i ) is a weakly increasing and concave function of a i. The bank s screening/monitoring is not verifiable and contractible by outsiders (loan buyers) and its (end-of-period) cost equals c a i. (A3) The bank is subject to a corporate income tax at rateτ and must meet a regulatory minimum equity (E) to deposits (D) ratio. This leverage constraint is given by κd E. 5

and its (end-of-period) cost equals c a i.")

6 Assumptions (continued) (A4) p e (s) and p d (s) are initial prices of unit end-of-period payments in state s for securities (personally) taxed as equity and debt. Certainty-equivalent competitive returns to equity and debt are r e and r d, where 1/(1+r i ) S p i (s) for i = e, d. p e (s)/p d (s) is constant across states, equal to (1+r d )/(1+r e ). Also, r d (1-τ) < r e. (A5) The bank can invest in securities that have state-contingent returns and a certainty-equivalent rate of return of r d. (A6) The bank has deposit market power and pays a certaintyequivalent deposit interest rate of r D = r D (D), where r D / D 0. (A7) The bank maximizes the after-tax return to shareholders equity. Deposits are fully insured with the bank paying an insurance premium that fairly reflects its default risk. 6

The bank has deposit market power and pays a certaintyequivalent deposit interest rate of r D = r D (D), where r D / D 0. (A7) The bank maximizes the after-tax return to shareholders equity.")

7 I.B The Bank s Optimization Problem Denote N h (N m ) to be the number of loans that the bank holds (sells or markets) and let B be its investment in securities. h { } N, N, a, B, D, E { m e h N d m ( ) ( ) ( ) ( ) ( ) max h N 1 + r, 1,0 1 m 1 e p s x i S i s ai ds ca i + p s x i 1 S i s ds = = i }( 1 τ ) + rb rd re subject to d D e ( ) ( ) N m h N d m + B D + E + p s x s, 0 i= 1 S i ds 1 financing κ D E capital Let λ f and λ k be the Lagrange multipliers on the financing and capital constraints, respectively. 7

+ rb rd re subject to d D e ( ) ( ) N m h N d m + B D + E + p s x s, 0 i= 1 S i ds 1 financing κ D E capital Let λ")

8 I.C Equilibria With No Loan Sales Market (N m =0) I.C.1 Equilibrium with Excess Capital With λ k = 0, the tax-adjusted cost of financing equals λ f rd re = rd + D = 1 τ D 1 τ In this Loan rich, deposit poor equilibrium the bank has many profitable loans which are funded at the margin with excess equity. ( 1 r ) p e( s ) x h ( s, a ) ds 1 ca r /( 1 τ ) h h h + e = S N N N e Deposits are issued up to the point where their marginal cost equals the tax-adjusted cost of equity. It is unprofitable for the bank to hold securities since r d < r e /(1-τ). 8

p e( s ) x h ( s, a ) ds 1 ca r /( 1 τ ) h h h + e = S N N N e Deposits are issued up to the point where their marginal cost")

9 I.C.2 Equilibrium with Binding Capital and Security Investments With λ k > 0, the tax-adjusted cost of financing equals λ f 1 rd κ re = rd + D + 1 τ 1+ κ D 1+ κ 1 τ If it is optimal for the bank to invest in securities, it must have limited lending opportunities but substantial deposit market power. In this Loan poor, deposit rich equilibrium, λ f /(1-τ) = r d and the marginal loan satisfies e h ( ) ( ) ( ) e 1 + r p s x s h, a ds h 1 ca r h = N N N S d 9

= r d and the marginal loan satisfies e h ( ) ( ) ( ) e 1")

10 I.C.3 Equilibrium with Binding Capital and without Security Investments Another equilibrium with λ k > 0 but where the bank holds no securities can be described as Loan and deposit compatibility. In this equilibrium, the marginal cost of financing satisfies λ f re rd 1 τ 1 τ ( ) A special case is a bank that has access to a perfectly elastic supply of competitively-priced brokered or wholesale deposits: λ f 1 κ re = rd + 1 τ 1+ κ 1+ κ 1 τ 10

11 Summary: Equilibria Without Loan Sales Market There are three types of equilibria: 1. There is a Loan rich, deposit poor equilibrium where: Many profitable loans are funded at the margin with excess equity. Deposits are issued to the point where their marginal cost equals the taxadjusted cost of equity. It is unprofitable to invest in securities. 2. There is a Loan and deposit compatibility equilibrium where: Loans are funded at the margin with equity and moderate cost deposits. Capital constraints bind; it is unprofitable to invest in securities. 3. There is a Loan poor, deposit rich equilibrium where: Few profitable loans are originated. Equity and low cost deposits are invested at the margin in securities. Capital constraints bind. 11

12 I.D Equilibria with a Loan Sales Market If loan i is retained on the balance sheet, then a * i satisfies h ( * x ) i s, a e i ( 1+ re ) p ( s) ds = c S * a and the present value of the profit from holding the loan is S * ca 1 / 1 d * i λf p s x s a ds h ( ) (, ) i i i 1+ r d ( τ) + + If, instead, the loan is sold, the present value of profit is m ( ) ( ) p d s x s i,0 ds 1 S 12

+ + If, instead, the loan is sold, the present value of profit is m ( ) ( ) p d s x s i,0")

13 Excess Profit of Holding versus Selling The excess profit from retaining versus selling the loan is S λ /1 * * f i i i i ( ) (, ) (,0) ( τ) d p s x s a ca x s ds 1+ r The first term (integral) is unambiguously positive. If the bank s equilibrium is Loan poor, deposit rich, so that it invests in securities and λ f /(1-τ) = r d, then the second term equals zero and there is never an incentive to securitize. d r d In this case, a marginal increase in the corporate tax rateτ has no effect on the incentive to sell loans. 13

14 A Potential Loan Selling Equilibrium If the bank s equilibrium is Loan rich, deposit poor, so that it holds no securities and λ f /(1-τ) = r e /(1-τ), then the excess profit of retaining versus selling is d ( ) ( * ( ) ) * re /1 τ r d p s xi s, ai cai xi( s,0) ds S 1+ r Since r e /(1-τ) > r d, the second term is negative, so there could be a net advantage to selling the loan. Importantly, the net advantage to loan selling is an increasing function of the corporate tax rateτ. Similarly, an advantage to loan selling can exist for the Loan and deposit compatibility equilibrium if r d < λ f /(1-τ) r e /(1-τ). d 14

15 Summary: Equilibria With Loan Sales Proposition 1: A Loan poor, deposit rich bank will invest in securities, and a marginal increase in its corporate tax rate has no effect on leverage or its incentive to sell loans. A marginally higher tax rate or equity capital requirement decreases its securities purchased but not the quantity of loans held on its balance sheet. Proposition 2: A Loan rich, deposit poor or Loan and deposit compatibility bank chooses not to invest in securities, and a marginal increase in its corporate tax rate increases its incentive to sell loans and can raise its leverage. A marginal increase in the bank s equity capital requirement also raises its incentive to sell loans. 15

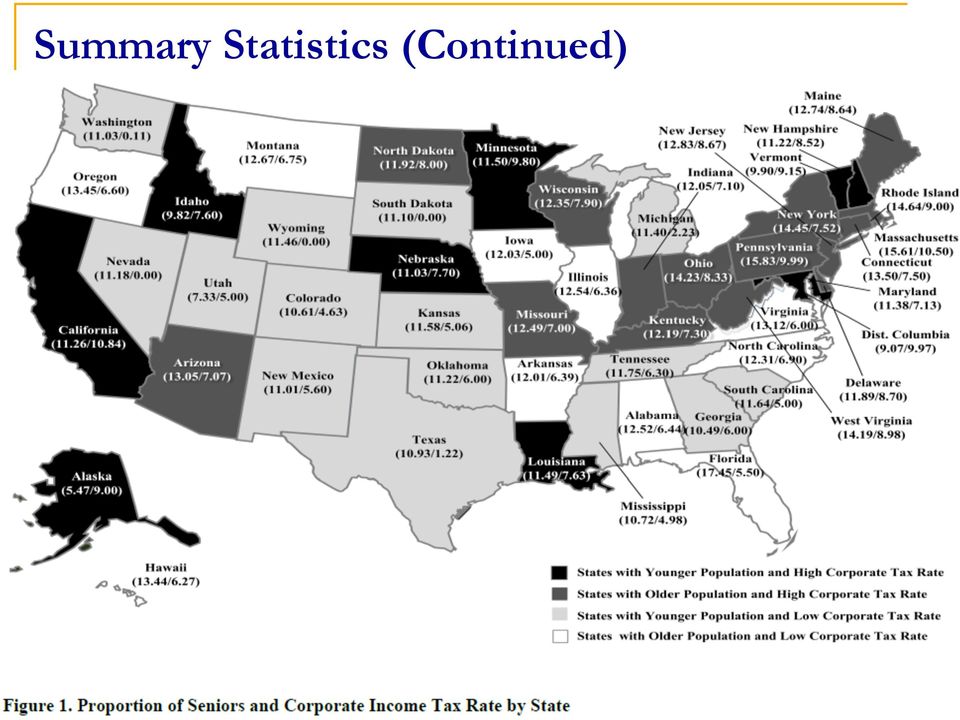

16 II. Empirical Evidence II.A Data The data covers the period and includes: 1. Individual bank s HMDA filings on mortgages originated and sold during each calendar year. 2. Call Report and Summary of Deposits data on C-Corp banks that have at least 90% of their deposits in a single state and a single MSA. 3. State corporate income tax rates for each year from the Tax Foundation 4. Census Bureau projections on each MSA s proportion of seniors (aged 65) for each year. Following Becker JFE 2007, this proxies for an MSA s extent of being loan poor, deposit rich. 5. Other MSA-level data on housing supply elasticity (Saiz (2010)), population growth, personal income growth, and unemployment. The final sample has 12,175 bank-year observations. 16

for each year.")

17 Mortgage Sales Ratio Our main variable of interest is the Mortgage Sales Ratio, MSR: MSR = Value of mortgages that were originated and sold during the year Value of mortgages that were originated during the year We also differentiate between non-jumbo mortgages and jumbo mortgages, since the former may be easier to sell (to GSEs). 17

18 II.B Summary Statistics 18

19 Summary Statistics (Continued) 19

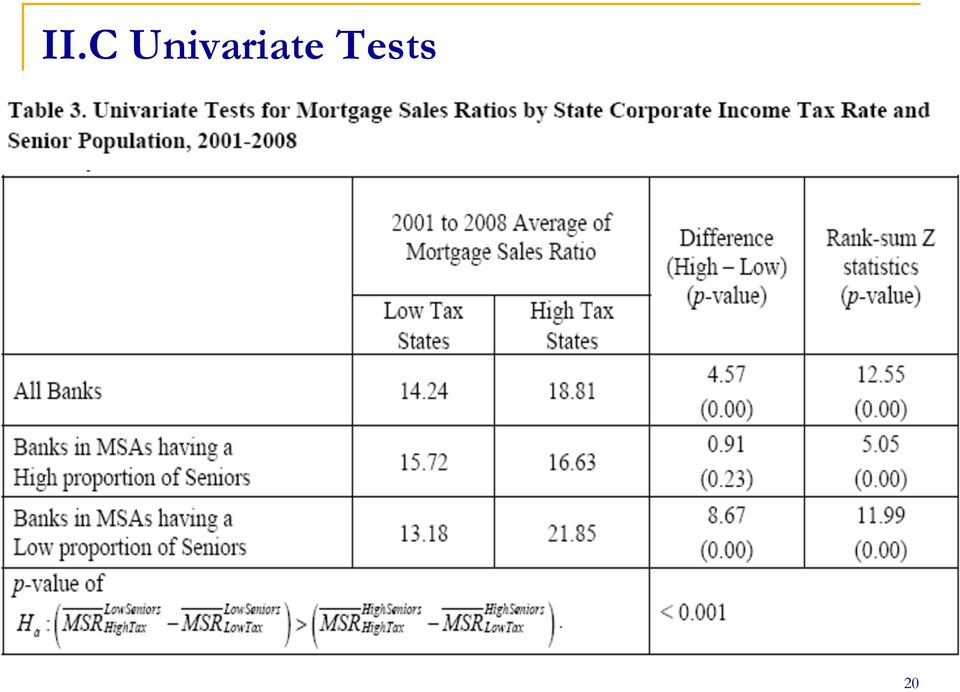

20 II.C Univariate Tests 20

21 II.D Multivariate Tests To test the proposition that higher corporate taxes lead to loan sales at low security banks, we run the following Tobit regression: MSR = a TaxRate + a I TaxRate + a I 1 2 Seniors< Median 3 Seniors< Median + Bank Controls + MSA Controls + Time Effects I Seniors< Median where is an indicator variable that equals 1 if the bank s MSA population has a proportion of seniors (aged 65) below the median. Our model predicts that the sum of the coefficients a 1 and a 2 should be positive. 21

22 Tobit Analysis of Mortgage Sales Ratio 22

23 Analysis of Mortgage Sales Ratio: Robustness 23

24 Tobit Analysis: Senior Population Subsamples 24

25 Fama-MacBeth Regressions: Low Senior Sample 25

26 Regressions of Annual Changes, ΔMSR 26

27 Interpreting the Results The results imply: Higher corporate tax rates have little effect on mortgage sales for banks in high senior loan poor, deposit rich MSAs. A one standard deviation increase in the corporate tax rate (1.88%) increases the mortgage sales of banks in low senior loan rich, deposit poor MSAs by 24.6%. Mortgage sales increase with a bank s size. Non-jumbo mortgages are more likely to be sold and their sales are more sensitive to corporate taxes than are jumbo mortgages. 27

28 III. Conclusions and Policy Implications Corporate taxes lead to greater (excessive?) loan selling for banks with substantial lending, but limited retail deposit, opportunities. This implication most likely extends to larger, multistate banks and non-bank lenders (e.g., finance companies). Reforms to strengthen capital standards and/or deposit insurance may increase the tax incentive to securitize, leading to less credit screening and monitoring by banks. * Similarly, recent proposals to levy new taxes on banks may be counter-productive due to the asymmetric tax treatment of banks versus special purpose corporations. * Higher capital requirements are claimed to cause French banks to begin securitizing. 28 See French Banks Try an Import from U.S. Wall Street Journal Nov. 6, 2012.

Corporate Taxes and Securitization

Corporate Taxes and Securitization JOONGHO HAN, KWANGWOO PARK, and GEORGE PENNACCHI ABSTRACT Most banks pay corporate income taxes, but securitization vehicles do not. Our model shows that when a bank

Corporate Taxes and Securitization JOONGHO HAN, KWANGWOO PARK, and GEORGE PENNACCHI ABSTRACT Most banks pay corporate income taxes, but securitization vehicles do not. Our model shows that when a bank

Online Appendix. Banks Liability Structure and Mortgage Lending. During the Financial Crisis

Online Appendix Banks Liability Structure and Mortgage Lending During the Financial Crisis Jihad Dagher Kazim Kazimov Outline This online appendix is split into three sections. Section 1 provides further

Online Appendix Banks Liability Structure and Mortgage Lending During the Financial Crisis Jihad Dagher Kazim Kazimov Outline This online appendix is split into three sections. Section 1 provides further

An Empirical Analysis of Insider Rates vs. Outsider Rates in Bank Lending

An Empirical Analysis of Insider Rates vs. Outsider Rates in Bank Lending Lamont Black* Indiana University Federal Reserve Board of Governors November 2006 ABSTRACT: This paper analyzes empirically the

An Empirical Analysis of Insider Rates vs. Outsider Rates in Bank Lending Lamont Black* Indiana University Federal Reserve Board of Governors November 2006 ABSTRACT: This paper analyzes empirically the

Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.)

") Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.) The primary focus of the next two chapters will be to examine the debt/equity choice by firms. In particular,

Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.) The primary focus of the next two chapters will be to examine the debt/equity choice by firms. In particular,

Federal Reserve Bank of Dallas A Banker s Quick Reference Guide to CRA

Federal Reserve Bank of Dallas A Banker s Quick Reference Guide to CRA This publication is a guide to the CRA regulation and examination procedures. It is intended for bank CEOs, presidents, and CRA and

Federal Reserve Bank of Dallas A Banker s Quick Reference Guide to CRA This publication is a guide to the CRA regulation and examination procedures. It is intended for bank CEOs, presidents, and CRA and

6. Budget Deficits and Fiscal Policy

Prof. Dr. Thomas Steger Advanced Macroeconomics II Lecture SS 2012 6. Budget Deficits and Fiscal Policy Introduction Ricardian equivalence Distorting taxes Debt crises Introduction (1) Ricardian equivalence

Prof. Dr. Thomas Steger Advanced Macroeconomics II Lecture SS 2012 6. Budget Deficits and Fiscal Policy Introduction Ricardian equivalence Distorting taxes Debt crises Introduction (1) Ricardian equivalence

6/18/2015. Sources of Funds for Residential Mortgages

Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 11-3 11-4 Formerly backbone of home mortgage finance Dominated mortgage

Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 11-3 11-4 Formerly backbone of home mortgage finance Dominated mortgage

A Banker s Quick Reference Guide to CRA

Federal Reserve Bank of Dallas A Banker s Quick Reference Guide to CRA As amended effective September 1, 2005 This publication is a guide to the CRA regulation and examination procedures. It is intended

Federal Reserve Bank of Dallas A Banker s Quick Reference Guide to CRA As amended effective September 1, 2005 This publication is a guide to the CRA regulation and examination procedures. It is intended

Financial Development and Macroeconomic Stability

Financial Development and Macroeconomic Stability Vincenzo Quadrini University of Southern California Urban Jermann Wharton School of the University of Pennsylvania January 31, 2005 VERY PRELIMINARY AND

Financial Development and Macroeconomic Stability Vincenzo Quadrini University of Southern California Urban Jermann Wharton School of the University of Pennsylvania January 31, 2005 VERY PRELIMINARY AND

Mortgage Finance Under Basel III Raymond Natter July, 2012

Mortgage Finance Under Basel III Raymond Natter July, 2012 The Basel Committee The Basel Committee on Banking Supervision is an informal organization consisting of the chief banking regulatory authorities

Mortgage Finance Under Basel III Raymond Natter July, 2012 The Basel Committee The Basel Committee on Banking Supervision is an informal organization consisting of the chief banking regulatory authorities

2013 Financial Institutions Forum. www.padgett-cpa.com

2013 Financial Institutions Forum www.padgett-cpa.com Community Banking in the Dodd - Frank Era John Heasley Texas Bankers Association August 28, 2013 Financial Institutions Forum The Subprime Crisis Causes:

2013 Financial Institutions Forum www.padgett-cpa.com Community Banking in the Dodd - Frank Era John Heasley Texas Bankers Association August 28, 2013 Financial Institutions Forum The Subprime Crisis Causes:

ICAP GROUP S.A. FINANCIAL RATIOS EXPLANATION

ICAP GROUP S.A. FINANCIAL RATIOS EXPLANATION OCTOBER 2006 Table of Contents 1. INTRODUCTION... 3 2. FINANCIAL RATIOS FOR COMPANIES (INDUSTRY - COMMERCE - SERVICES) 4 2.1 Profitability Ratios...4 2.2 Viability

ICAP GROUP S.A. FINANCIAL RATIOS EXPLANATION OCTOBER 2006 Table of Contents 1. INTRODUCTION... 3 2. FINANCIAL RATIOS FOR COMPANIES (INDUSTRY - COMMERCE - SERVICES) 4 2.1 Profitability Ratios...4 2.2 Viability

Capital Structure II

Capital Structure II Introduction In the previous lecture we introduced the subject of capital gearing. Gearing occurs when a company is financed partly through fixed return finance (e.g. loans, loan stock

Capital Structure II Introduction In the previous lecture we introduced the subject of capital gearing. Gearing occurs when a company is financed partly through fixed return finance (e.g. loans, loan stock

The Tangent or Efficient Portfolio

The Tangent or Efficient Portfolio 1 2 Identifying the Tangent Portfolio Sharpe Ratio: Measures the ratio of reward-to-volatility provided by a portfolio Sharpe Ratio Portfolio Excess Return E[ RP ] r

The Tangent or Efficient Portfolio 1 2 Identifying the Tangent Portfolio Sharpe Ratio: Measures the ratio of reward-to-volatility provided by a portfolio Sharpe Ratio Portfolio Excess Return E[ RP ] r

Should Banks Trade Equity Derivatives to Manage Credit Risk? Kevin Davis 9/4/1991

Should Banks Trade Equity Derivatives to Manage Credit Risk? Kevin Davis 9/4/1991 Banks incur a variety of risks and utilise different techniques to manage the exposures so created. Some of those techniques

Should Banks Trade Equity Derivatives to Manage Credit Risk? Kevin Davis 9/4/1991 Banks incur a variety of risks and utilise different techniques to manage the exposures so created. Some of those techniques

Chapter 10 6/16/2010. Mortgage Types and Borrower Decisions: Overview Role of the secondary market. Mortgage types:

Mortgage Types and Borrower Decisions: Overview Role of the secondary market Chapter 10 Residential Mortgage Types and Borrower Decisions Mortgage types: Conventional mortgages FHA mortgages VA mortgages

Mortgage Types and Borrower Decisions: Overview Role of the secondary market Chapter 10 Residential Mortgage Types and Borrower Decisions Mortgage types: Conventional mortgages FHA mortgages VA mortgages

t = 1 2 3 1. Calculate the implied interest rates and graph the term structure of interest rates. t = 1 2 3 X t = 100 100 100 t = 1 2 3

MØA 155 PROBLEM SET: Summarizing Exercise 1. Present Value [3] You are given the following prices P t today for receiving risk free payments t periods from now. t = 1 2 3 P t = 0.95 0.9 0.85 1. Calculate

MØA 155 PROBLEM SET: Summarizing Exercise 1. Present Value [3] You are given the following prices P t today for receiving risk free payments t periods from now. t = 1 2 3 P t = 0.95 0.9 0.85 1. Calculate

The Cost of Financial Frictions for Life Insurers

The Cost of Financial Frictions for Life Insurers Ralph S. J. Koijen Motohiro Yogo University of Chicago and NBER Federal Reserve Bank of Minneapolis 1 1 The views expressed herein are not necessarily

The Cost of Financial Frictions for Life Insurers Ralph S. J. Koijen Motohiro Yogo University of Chicago and NBER Federal Reserve Bank of Minneapolis 1 1 The views expressed herein are not necessarily

Paper F9. Financial Management. Fundamentals Pilot Paper Skills module. The Association of Chartered Certified Accountants

Fundamentals Pilot Paper Skills module Financial Management Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Do NOT open this paper

Fundamentals Pilot Paper Skills module Financial Management Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Do NOT open this paper

How To Buy Stock On Margin

LESSON 8 BUYING ON MARGIN AND SELLING SHORT ACTIVITY 8.1 A MARGINAL PLAY Stockbroker Luke, Katie, and Jeremy are sitting around a desk near a sign labeled Brokerage Office. The Moderator is standing in

LESSON 8 BUYING ON MARGIN AND SELLING SHORT ACTIVITY 8.1 A MARGINAL PLAY Stockbroker Luke, Katie, and Jeremy are sitting around a desk near a sign labeled Brokerage Office. The Moderator is standing in

Executive Summary. In the Tenth Federal Reserve District September 2014. Survey Demographics

In the Tenth Federal Reserve District September 2014 Executive Summary Surveys were emailed to community depository institutions (including banks, credit unions, and savings and loans) with assets less

In the Tenth Federal Reserve District September 2014 Executive Summary Surveys were emailed to community depository institutions (including banks, credit unions, and savings and loans) with assets less

Long-Run Average Cost. Econ 410: Micro Theory. Long-Run Average Cost. Long-Run Average Cost. Economies of Scale & Scope Minimizing Cost Mathematically

Slide 1 Slide 3 Econ 410: Micro Theory & Scope Minimizing Cost Mathematically Friday, November 9 th, 2007 Cost But, at some point, average costs for a firm will tend to increase. Why? Factory space and

Slide 1 Slide 3 Econ 410: Micro Theory & Scope Minimizing Cost Mathematically Friday, November 9 th, 2007 Cost But, at some point, average costs for a firm will tend to increase. Why? Factory space and

HMDA DATA ON DEMAND FREQUENTLY ASKED QUESTIONS

HMDA DATA ON DEMAND FREQUENTLY ASKED QUESTIONS About the Home Mortgage Disclosure Act (HMDA) One of the most comprehensive sources of publically available application-level information on the single-family

HMDA DATA ON DEMAND FREQUENTLY ASKED QUESTIONS About the Home Mortgage Disclosure Act (HMDA) One of the most comprehensive sources of publically available application-level information on the single-family

Liquidity and the Development of Robust Corporate Bond Markets

Liquidity and the Development of Robust Corporate Bond Markets Marti G. Subrahmanyam Stern School of Business New York University For presentation at the CAMRI Executive Roundtable Luncheon Talk National

Liquidity and the Development of Robust Corporate Bond Markets Marti G. Subrahmanyam Stern School of Business New York University For presentation at the CAMRI Executive Roundtable Luncheon Talk National

Leverage. FINANCE 350 Global Financial Management. Professor Alon Brav Fuqua School of Business Duke University. Overview

Leverage FINANCE 35 Global Financial Management Professor Alon Brav Fuqua School of Business Duke University Overview Capital Structure does not matter! Modigliani & Miller propositions Implications for

Leverage FINANCE 35 Global Financial Management Professor Alon Brav Fuqua School of Business Duke University Overview Capital Structure does not matter! Modigliani & Miller propositions Implications for

Market Structure, Credit Expansion and Mortgage Default Risk

Market Structure, Credit Expansion and Mortgage Default Risk By Liu, Shilling, and Sing Discussion by David Ling Primary Research Questions 1. Is concentration in the banking industry within a state associated

Market Structure, Credit Expansion and Mortgage Default Risk By Liu, Shilling, and Sing Discussion by David Ling Primary Research Questions 1. Is concentration in the banking industry within a state associated

Module 1: Corporate Finance and the Role of Venture Capital Financing TABLE OF CONTENTS

1.0 ALTERNATIVE SOURCES OF FINANCE Module 1: Corporate Finance and the Role of Venture Capital Financing Alternative Sources of Finance TABLE OF CONTENTS 1.1 Short-Term Debt (Short-Term Loans, Line of

1.0 ALTERNATIVE SOURCES OF FINANCE Module 1: Corporate Finance and the Role of Venture Capital Financing Alternative Sources of Finance TABLE OF CONTENTS 1.1 Short-Term Debt (Short-Term Loans, Line of

What s on a bank s balance sheet?

The Capital Markets Initiative January 2014 TO: Interested Parties FROM: David Hollingsworth and Lauren Oppenheimer RE: Capital Requirements and Bank Balance Sheets: Reviewing the Basics What s on a bank

The Capital Markets Initiative January 2014 TO: Interested Parties FROM: David Hollingsworth and Lauren Oppenheimer RE: Capital Requirements and Bank Balance Sheets: Reviewing the Basics What s on a bank

Are banks too large and complex?

Are banks too large and complex? Luc Laeven with Lindsay Mollineaux, Lev Ratnovski, Yangfan Sun, and Hui Tong (IMF Research Department) t) The views expressed here are our own and do not reflect those

Are banks too large and complex? Luc Laeven with Lindsay Mollineaux, Lev Ratnovski, Yangfan Sun, and Hui Tong (IMF Research Department) t) The views expressed here are our own and do not reflect those

Capital Structure. Itay Goldstein. Wharton School, University of Pennsylvania

Capital Structure Itay Goldstein Wharton School, University of Pennsylvania 1 Debt and Equity There are two main types of financing: debt and equity. Consider a two-period world with dates 0 and 1. At

Capital Structure Itay Goldstein Wharton School, University of Pennsylvania 1 Debt and Equity There are two main types of financing: debt and equity. Consider a two-period world with dates 0 and 1. At

Online Appendix for Demand for Crash Insurance, Intermediary Constraints, and Risk Premia in Financial Markets

Online Appendix for Demand for Crash Insurance, Intermediary Constraints, and Risk Premia in Financial Markets Hui Chen Scott Joslin Sophie Ni August 3, 2015 1 An Extension of the Dynamic Model Our model

Online Appendix for Demand for Crash Insurance, Intermediary Constraints, and Risk Premia in Financial Markets Hui Chen Scott Joslin Sophie Ni August 3, 2015 1 An Extension of the Dynamic Model Our model

COMMUNITY REINVESTMENT ACT

COMMUNITY REINVESTMENT ACT EXAMINATION PROCEDURES FOR LARGE INSTITUTIONS Examination Scope For institutions (interstate and intrastate) with more than one assessment area, identify assessment areas for

COMMUNITY REINVESTMENT ACT EXAMINATION PROCEDURES FOR LARGE INSTITUTIONS Examination Scope For institutions (interstate and intrastate) with more than one assessment area, identify assessment areas for

TECHNICAL NOTE 2 EQUITY & LEVERAGE IN INDIAN MFIS

TECHNICAL NOTE 2 EQUITY & LEVERAGE IN INDIAN MFIS Micro-Credit Ratings International Limited, Gurgaon, India September 2005 The purpose of this technical note is to provide a practical understanding of

TECHNICAL NOTE 2 EQUITY & LEVERAGE IN INDIAN MFIS Micro-Credit Ratings International Limited, Gurgaon, India September 2005 The purpose of this technical note is to provide a practical understanding of

Estimating Beta. Aswath Damodaran

Estimating Beta The standard procedure for estimating betas is to regress stock returns (R j ) against market returns (R m ) - R j = a + b R m where a is the intercept and b is the slope of the regression.

Estimating Beta The standard procedure for estimating betas is to regress stock returns (R j ) against market returns (R m ) - R j = a + b R m where a is the intercept and b is the slope of the regression.

SUMMARY: Section 1076 of the Dodd-Frank Wall Street Reform and Consumer Protection Act

This document is scheduled to be published in the Federal Register on 07/02/2012 and available online at http://federalregister.gov/a/2012-16078, and on FDsys.gov Billing Code: 4810-AM-P BUREAU OF CONSUMER

This document is scheduled to be published in the Federal Register on 07/02/2012 and available online at http://federalregister.gov/a/2012-16078, and on FDsys.gov Billing Code: 4810-AM-P BUREAU OF CONSUMER

Empirical Applying Of Mutual Funds

Internet Appendix for A Model of hadow Banking * At t = 0, a generic intermediary j solves the optimization problem: max ( D, I H, I L, H, L, TH, TL ) [R (I H + T H H ) + p H ( H T H )] + [E ω (π ω ) A

Internet Appendix for A Model of hadow Banking * At t = 0, a generic intermediary j solves the optimization problem: max ( D, I H, I L, H, L, TH, TL ) [R (I H + T H H ) + p H ( H T H )] + [E ω (π ω ) A

Part A, Section 1: 1-4 Family Residential Lending: Home Purchase and Refinance Mortgage Loans

Part A, Section 1: 1-4 Family Residential Lending: Home Purchase and Refinance Mortgage Loans General Instructions: What type of lending is reported in this section? This section of Part A of the survey

Part A, Section 1: 1-4 Family Residential Lending: Home Purchase and Refinance Mortgage Loans General Instructions: What type of lending is reported in this section? This section of Part A of the survey

The Effects of Funding Costs and Risk on Banks Lending Rates

The Effects of Funding Costs and Risk on Banks Lending Rates Daniel Fabbro and Mark Hack* After falling for over a decade, the major banks net interest margins appear to have stabilised in a relatively

The Effects of Funding Costs and Risk on Banks Lending Rates Daniel Fabbro and Mark Hack* After falling for over a decade, the major banks net interest margins appear to have stabilised in a relatively

Opening Doors For Muslim Families In America

Fe r d de i M a c We Open Doors Opening Doors For Muslim Families In America Saber Salam Vice President, Freddie Mac April 2002 Introduction The dream of homeownership is at the core of American society.

Fe r d de i M a c We Open Doors Opening Doors For Muslim Families In America Saber Salam Vice President, Freddie Mac April 2002 Introduction The dream of homeownership is at the core of American society.

Chapter 07 - Accounts and Notes Receivable. Chapter Outline

Chapter 07 - Accounts and Receivable I. Accounts Receivable A receivable is an amount due from another party. Accounts Receivable are amounts due from customers for credit sales. A. Recognizing Accounts

Chapter 07 - Accounts and Receivable I. Accounts Receivable A receivable is an amount due from another party. Accounts Receivable are amounts due from customers for credit sales. A. Recognizing Accounts

Ethiopian Institute of Financial Studies (EIFS) PROJECT FINANCE

PROJECT FINANCE") PROJECT FINANCE With the growth in the economy and the revival in the industrial sector coupled with the increasing role of private players in the field of infrastructure, more and more Ethiopian banks

PROJECT FINANCE With the growth in the economy and the revival in the industrial sector coupled with the increasing role of private players in the field of infrastructure, more and more Ethiopian banks

Macroeconomic Effects of Financial Shocks Online Appendix

Macroeconomic Effects of Financial Shocks Online Appendix By Urban Jermann and Vincenzo Quadrini Data sources Financial data is from the Flow of Funds Accounts of the Federal Reserve Board. We report the

Macroeconomic Effects of Financial Shocks Online Appendix By Urban Jermann and Vincenzo Quadrini Data sources Financial data is from the Flow of Funds Accounts of the Federal Reserve Board. We report the

Discussion. Credit Boom and Lending Standard: Evidence from Subprime Mortgage Lending. Satyajit Chatterjee

Credit Boom and Lending Standard: Evidence from Subprime Mortgage Lending Research Department Federal Reserve Bank of Philadelphia September 2008 OBJECTIVES AND FINDINGS Consensus that the source of the

Credit Boom and Lending Standard: Evidence from Subprime Mortgage Lending Research Department Federal Reserve Bank of Philadelphia September 2008 OBJECTIVES AND FINDINGS Consensus that the source of the

The Effect of Housing on Portfolio Choice. July 2009

The Effect of Housing on Portfolio Choice Raj Chetty Harvard Univ. Adam Szeidl UC-Berkeley July 2009 Introduction How does homeownership affect financial portfolios? Linkages between housing and financial

The Effect of Housing on Portfolio Choice Raj Chetty Harvard Univ. Adam Szeidl UC-Berkeley July 2009 Introduction How does homeownership affect financial portfolios? Linkages between housing and financial

Return on Equity has three ratio components. The three ratios that make up Return on Equity are:

Evaluating Financial Performance Chapter 1 Return on Equity Why Use Ratios? It has been said that you must measure what you expect to manage and accomplish. Without measurement, you have no reference to

Evaluating Financial Performance Chapter 1 Return on Equity Why Use Ratios? It has been said that you must measure what you expect to manage and accomplish. Without measurement, you have no reference to

Stapled Finance. Paul Povel and Raj Singh. Bauer College of Business, Univ. of Houston Carlson School of Management, Univ.

Paul Povel and Raj Singh Bauer College of Business, Univ. of Houston Carlson School of Management, Univ. of Minnesota What Is? What is? From the Business Press Explanations Acquisition financing, pre-arranged

Paul Povel and Raj Singh Bauer College of Business, Univ. of Houston Carlson School of Management, Univ. of Minnesota What Is? What is? From the Business Press Explanations Acquisition financing, pre-arranged

Box D Self-managed Superannuation Funds

Box D Self-managed Superannuation Funds 1 8 6 4 2 Self-managed superannuation funds (SMSFs) are the fastest-growing segment of the Australian superannuation industry. In June 213, SMSFs held around $5

Box D Self-managed Superannuation Funds 1 8 6 4 2 Self-managed superannuation funds (SMSFs) are the fastest-growing segment of the Australian superannuation industry. In June 213, SMSFs held around $5

FI3300 Corporation Finance

Learning Objectives FI3300 Corporation Finance Spring Semester 2010 Dr. Isabel Tkatch Assistant Professor of Finance Explain the objectives of financial statement analysis and its benefits for creditors,

Learning Objectives FI3300 Corporation Finance Spring Semester 2010 Dr. Isabel Tkatch Assistant Professor of Finance Explain the objectives of financial statement analysis and its benefits for creditors,

Securitization Perspectives: Final U.S. Liquidity Coverage Ratio. September 10, 2014

Securitization Perspectives: Final U.S. Liquidity Coverage Ratio September 10, 2014 Introduction! On September 3rd, the Agencies adopted regulations implementing a liquidity coverage ratio (LCR) requirement

Securitization Perspectives: Final U.S. Liquidity Coverage Ratio September 10, 2014 Introduction! On September 3rd, the Agencies adopted regulations implementing a liquidity coverage ratio (LCR) requirement

Sierra Lending Group LLC Document Check List

Sierra Lending Group LLC Document Check List The following documents will be needed for full credit approval: Application 1. Fully completed and signed initial 1003. Please make sure to provide all assets

Sierra Lending Group LLC Document Check List The following documents will be needed for full credit approval: Application 1. Fully completed and signed initial 1003. Please make sure to provide all assets

BANK INTEREST RATE MARGINS

Reserve Bank of Australia Bulletin May BANK INTEREST RATE MARGINS Bank interest rate margins the difference between what interest rates banks borrow at and what they lend at have been the subject of much

Reserve Bank of Australia Bulletin May BANK INTEREST RATE MARGINS Bank interest rate margins the difference between what interest rates banks borrow at and what they lend at have been the subject of much

Have the GSE Affordable Housing Goals Increased. the Supply of Mortgage Credit?

Have the GSE Affordable Housing Goals Increased the Supply of Mortgage Credit? Brent W. Ambrose * Professor of Finance and Director Center for Real Estate Studies Gatton College of Business and Economics

Have the GSE Affordable Housing Goals Increased the Supply of Mortgage Credit? Brent W. Ambrose * Professor of Finance and Director Center for Real Estate Studies Gatton College of Business and Economics

Ch. 18: Taxes + Bankruptcy cost

Ch. 18: Taxes + Bankruptcy cost If MM1 holds, then Financial Management has little (if any) impact on value of the firm: If markets are perfect, transaction cost (TAC) and bankruptcy cost are zero, no

Ch. 18: Taxes + Bankruptcy cost If MM1 holds, then Financial Management has little (if any) impact on value of the firm: If markets are perfect, transaction cost (TAC) and bankruptcy cost are zero, no

Online Appendix: Bank Competition, Risk Taking and Their Consequences

Online Appendix: Bank Competition, Risk Taking and Their Consequences Xiaochen (Alan) Feng Princeton University - Not for Pulication- This version: Novemer 2014 (Link to the most updated version) OA1.

Online Appendix: Bank Competition, Risk Taking and Their Consequences Xiaochen (Alan) Feng Princeton University - Not for Pulication- This version: Novemer 2014 (Link to the most updated version) OA1.

How Bankers Think. Build a sound financial base to support your company for future growth

How Bankers Think Build a sound financial base to support your company for future growth Presented by: Lisa Chapman Business Planning, Social Media Marketing & SEO 615-477-8412 Questions to Consider First

How Bankers Think Build a sound financial base to support your company for future growth Presented by: Lisa Chapman Business Planning, Social Media Marketing & SEO 615-477-8412 Questions to Consider First

Analyzing the Statement of Cash Flows

Analyzing the Statement of Cash Flows Operating Activities NACM Upstate New York Credit Conference 2015 By Ron Sereika, CCE,CEW NACM 1 Objectives of this Educational Session u Show how the statement of

Analyzing the Statement of Cash Flows Operating Activities NACM Upstate New York Credit Conference 2015 By Ron Sereika, CCE,CEW NACM 1 Objectives of this Educational Session u Show how the statement of

EXAMINATION PROCEDURES FOR LARGE INSTITUTIONS... 2 EXAMINATION SCOPE... 2 PERFORMANCE CONTEXT... 3 ASSESSMENT AREA... 4

TABLE OF CONTENTS EXAMINATION PROCEDURES FOR LARGE INSTITUTIONS... 2 EXAMINATION SCOPE... 2 PERFORMANCE CONTEXT... 3 ASSESSMENT AREA... 4 LENDING, INVESTMENT, AND SERVICE TESTS FOR LARGE RETAIL INSTITUTIONS...

TABLE OF CONTENTS EXAMINATION PROCEDURES FOR LARGE INSTITUTIONS... 2 EXAMINATION SCOPE... 2 PERFORMANCE CONTEXT... 3 ASSESSMENT AREA... 4 LENDING, INVESTMENT, AND SERVICE TESTS FOR LARGE RETAIL INSTITUTIONS...

October 21, 2015 MEDIA & INVESTOR CONTACT Heather Worley, 214.932.6646 heather.worley@texascapitalbank.com

October 21, 2015 MEDIA & INVESTOR CONTACT Heather Worley, 214.932.6646 heather.worley@texascapitalbank.com TEXAS CAPITAL BANCSHARES, INC. ANNOUNCES OPERATING RESULTS FOR Q3 2015 DALLAS - October 21, 2015

October 21, 2015 MEDIA & INVESTOR CONTACT Heather Worley, 214.932.6646 heather.worley@texascapitalbank.com TEXAS CAPITAL BANCSHARES, INC. ANNOUNCES OPERATING RESULTS FOR Q3 2015 DALLAS - October 21, 2015

PUBLIC DISCLOSURE COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION

SMALL BANK Comptroller the Currency Administrator National Banks Washington, DC 20219 PUBLIC DISCLOSURE March 24, 2008 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Charter National Bank And Trust

SMALL BANK Comptroller the Currency Administrator National Banks Washington, DC 20219 PUBLIC DISCLOSURE March 24, 2008 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Charter National Bank And Trust

Part A, Section 3: Small Business Lending General Instructions:

Part A, Section 3: Small Business Lending General Instructions: What type of lending is reported in this section? This section of Part A of the survey focuses on small business lending. For purposes of

Part A, Section 3: Small Business Lending General Instructions: What type of lending is reported in this section? This section of Part A of the survey focuses on small business lending. For purposes of

Residential Mortgage Finance and Housing Markets in Russia February 9, 2004. Britt Gwinner The World Bank

Residential Mortgage Finance and Housing Markets in Russia February 9, 2004 Britt Gwinner The World Bank 1 Overview of Presentation Two Sections: 1. Residential Mortgage Finance Internationally 2. Mortgage

Residential Mortgage Finance and Housing Markets in Russia February 9, 2004 Britt Gwinner The World Bank 1 Overview of Presentation Two Sections: 1. Residential Mortgage Finance Internationally 2. Mortgage

How To Calculate Financial Leverage Ratio

What Do Short-Term Liquidity Ratios Measure? What Is Working Capital? HOCK international - 2004 1 HOCK international - 2004 2 How Is the Current Ratio Calculated? How Is the Quick Ratio Calculated? HOCK

What Do Short-Term Liquidity Ratios Measure? What Is Working Capital? HOCK international - 2004 1 HOCK international - 2004 2 How Is the Current Ratio Calculated? How Is the Quick Ratio Calculated? HOCK

Comments on Collateral Valuation

Comments on Collateral Valuation Lawrence J. White Stern School of Business New York University Lwhite@stern.nyu.edu Presentation at FTC, November 16, 2012 1 Overview The problem/issue What they did What

Comments on Collateral Valuation Lawrence J. White Stern School of Business New York University Lwhite@stern.nyu.edu Presentation at FTC, November 16, 2012 1 Overview The problem/issue What they did What

Module 1: Corporate Finance and the Role of Venture Capital Financing TABLE OF CONTENTS

1.0 FINANCING PRINCIPLES Module 1: Corporate Finance and the Role of Venture Capital Financing Financing Principles 1.01 Introduction to Financing Principles 1.02 Capitalization of a Business 1.03 Capital

1.0 FINANCING PRINCIPLES Module 1: Corporate Finance and the Role of Venture Capital Financing Financing Principles 1.01 Introduction to Financing Principles 1.02 Capitalization of a Business 1.03 Capital

J.P. Morgan FinTech and Specialty Finance Forum December 2015

J.P. Morgan FinTech and Specialty Finance Forum December 2015 Forward-Looking Statements This presentation contains forward-looking statements within the meaning of Section 21E of the Securities Exchange

J.P. Morgan FinTech and Specialty Finance Forum December 2015 Forward-Looking Statements This presentation contains forward-looking statements within the meaning of Section 21E of the Securities Exchange

Policy Guidance on Supervisory and Enforcement Considerations Relevant to Mortgage

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION Policy Guidance on Supervisory and Enforcement Considerations Relevant to Mortgage Brokers Transitioning to Mini-Correspondent Lenders AGENCY:

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION Policy Guidance on Supervisory and Enforcement Considerations Relevant to Mortgage Brokers Transitioning to Mini-Correspondent Lenders AGENCY:

Game Theory: Supermodular Games 1

Game Theory: Supermodular Games 1 Christoph Schottmüller 1 License: CC Attribution ShareAlike 4.0 1 / 22 Outline 1 Introduction 2 Model 3 Revision questions and exercises 2 / 22 Motivation I several solution

Game Theory: Supermodular Games 1 Christoph Schottmüller 1 License: CC Attribution ShareAlike 4.0 1 / 22 Outline 1 Introduction 2 Model 3 Revision questions and exercises 2 / 22 Motivation I several solution

Chapter 2. Practice Problems. MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chapter 2 Practice Problems MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Assume that you borrow $2000 at 10% annual interest to finance a new

Chapter 2 Practice Problems MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Assume that you borrow $2000 at 10% annual interest to finance a new

A Test Of The M&M Capital Structure Theories Richard H. Fosberg, William Paterson University, USA

A Test Of The M&M Capital Structure Theories Richard H. Fosberg, William Paterson University, USA ABSTRACT Modigliani and Miller (1958, 1963) predict two very specific relationships between firm value

A Test Of The M&M Capital Structure Theories Richard H. Fosberg, William Paterson University, USA ABSTRACT Modigliani and Miller (1958, 1963) predict two very specific relationships between firm value

Mortgage Revenue Bond Program Analysis: Origination Practices and Borrower Outcomes Ohio, Indiana & Florida 1. SUMMARY REPORT April, 2009

Mortgage Revenue Bond Program Analysis: Origination Practices and Borrower Outcomes Ohio, Indiana & Florida 1 SUMMARY REPORT April, 2009 Prepared By: Stephanie Moulton Principal Researcher, Mortgage Revenue

Mortgage Revenue Bond Program Analysis: Origination Practices and Borrower Outcomes Ohio, Indiana & Florida 1 SUMMARY REPORT April, 2009 Prepared By: Stephanie Moulton Principal Researcher, Mortgage Revenue

Small Business Borrowing and the Owner Manager Agency Costs: Evidence on Finnish Data. Jyrki Niskanen Mervi Niskanen 10.11.2005

Small Business Borrowing and the Owner Manager Agency Costs: Evidence on Finnish Data Jyrki Niskanen Mervi Niskanen 10.11.2005 Abstract. This study investigates the impact that managerial ownership has

Small Business Borrowing and the Owner Manager Agency Costs: Evidence on Finnish Data Jyrki Niskanen Mervi Niskanen 10.11.2005 Abstract. This study investigates the impact that managerial ownership has

Determinants of short-term debt financing

ABSTRACT Determinants of short-term debt financing Richard H. Fosberg William Paterson University In this study, it is shown that both theories put forward to explain the amount of shortterm debt financing

ABSTRACT Determinants of short-term debt financing Richard H. Fosberg William Paterson University In this study, it is shown that both theories put forward to explain the amount of shortterm debt financing

Financial Statements and Ratios: Notes

Financial Statements and Ratios: Notes 1. Uses of the income statement for evaluation Investors use the income statement to help judge their return on investment and creditors (lenders) use it to help

Financial Statements and Ratios: Notes 1. Uses of the income statement for evaluation Investors use the income statement to help judge their return on investment and creditors (lenders) use it to help

NIKE Case Study Solutions

NIKE Case Study Solutions Professor Corwin This case study includes several problems related to the valuation of Nike. We will work through these problems throughout the course to demonstrate some of the

NIKE Case Study Solutions Professor Corwin This case study includes several problems related to the valuation of Nike. We will work through these problems throughout the course to demonstrate some of the

Economics of Insurance

Economics of Insurance In this last lecture, we cover most topics of Economics of Information within a single application. Through this, you will see how the differential informational assumptions allow

Economics of Insurance In this last lecture, we cover most topics of Economics of Information within a single application. Through this, you will see how the differential informational assumptions allow

Alternative Asset Classes for Pension Funds

International Finance Corporation and National Pension Commission of Nigeria Alternative Asset Classes for Pension Funds Impediments to Corporate Bond Development in Nigeria Patricia M c Kean & David White

International Finance Corporation and National Pension Commission of Nigeria Alternative Asset Classes for Pension Funds Impediments to Corporate Bond Development in Nigeria Patricia M c Kean & David White

Chapter 5. Conditional CAPM. 5.1 Conditional CAPM: Theory. 5.1.1 Risk According to the CAPM. The CAPM is not a perfect model of expected returns.

Chapter 5 Conditional CAPM 5.1 Conditional CAPM: Theory 5.1.1 Risk According to the CAPM The CAPM is not a perfect model of expected returns. In the 40+ years of its history, many systematic deviations

Chapter 5 Conditional CAPM 5.1 Conditional CAPM: Theory 5.1.1 Risk According to the CAPM The CAPM is not a perfect model of expected returns. In the 40+ years of its history, many systematic deviations

A systemic approach to home loans: Continuous workouts vs. fixed rate contracts (Shiller et al., 2014)

") A systemic approach to home loans: Continuous workouts vs. fixed rate contracts (Shiller et al., 2014) Discussion Cristian Badarinza EFA Meeting, Lugano, August 2014 Summary 1. Unexpected house price declines

A systemic approach to home loans: Continuous workouts vs. fixed rate contracts (Shiller et al., 2014) Discussion Cristian Badarinza EFA Meeting, Lugano, August 2014 Summary 1. Unexpected house price declines

2. Information Economics

2. Information Economics In General Equilibrium Theory all agents had full information regarding any variable of interest (prices, commodities, state of nature, cost function, preferences, etc.) In many

2. Information Economics In General Equilibrium Theory all agents had full information regarding any variable of interest (prices, commodities, state of nature, cost function, preferences, etc.) In many

Dimitri Vayanos and Pierre-Olivier Weill: A Search-Based Theory of the On-the-Run Phenomenon

Dimitri Vayanos and Pierre-Olivier Weill: A Search-Based Theory of the On-the-Run Phenomenon Presented by: András Kiss Economics Department CEU The on-the-run phenomenon Bonds with almost identical cash-flows

Dimitri Vayanos and Pierre-Olivier Weill: A Search-Based Theory of the On-the-Run Phenomenon Presented by: András Kiss Economics Department CEU The on-the-run phenomenon Bonds with almost identical cash-flows

Models of Risk and Return

Models of Risk and Return Aswath Damodaran Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for

Models of Risk and Return Aswath Damodaran Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for

Securitizing Accounts Receivable

Review of Quantitative Finance and Accounting, 22: 29 38, 24 c 24 Kluwer Academic Publishers. Manufactured in The Netherlands. Securitizing Accounts Receivable DARIUS PAIA AND BEN J. SOPRANZETTI Rutgers

Review of Quantitative Finance and Accounting, 22: 29 38, 24 c 24 Kluwer Academic Publishers. Manufactured in The Netherlands. Securitizing Accounts Receivable DARIUS PAIA AND BEN J. SOPRANZETTI Rutgers

FNCE 301, Financial Management H Guy Williams, 2006

Stock Valuation Stock characteristics Stocks are the other major traded security (stocks & bonds). Options are another traded security but not as big as these two. - Ownership Stockholders are the owner

Stock Valuation Stock characteristics Stocks are the other major traded security (stocks & bonds). Options are another traded security but not as big as these two. - Ownership Stockholders are the owner

Bank Loans, Trade Credits, and Borrower Characteristics: Theory and Empirical Analysis. Byung-Uk Chong*, Ha-Chin Yi** March, 2010 ABSTRACT

Bank Loans, Trade Credits, and Borrower Characteristics: Theory and Empirical Analysis Byung-Uk Chong*, Ha-Chin Yi** March, 2010 ABSTRACT Trade credit is a non-bank financing offered by a supplier to finance

Bank Loans, Trade Credits, and Borrower Characteristics: Theory and Empirical Analysis Byung-Uk Chong*, Ha-Chin Yi** March, 2010 ABSTRACT Trade credit is a non-bank financing offered by a supplier to finance

Econ 202 Section 4 Final Exam

Douglas, Fall 2009 December 15, 2009 A: Special Code 00004 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 202 Section 4 Final Exam 1. Oceania buys $40

Douglas, Fall 2009 December 15, 2009 A: Special Code 00004 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 202 Section 4 Final Exam 1. Oceania buys $40

Organizational Structure and Insurers Risk Taking: Evidence from the Life Insurance Industry in Japan

Organizational Structure and Insurers Risk Taking: Evidence from the Life Insurance Industry in Japan Noriyoshi Yanase, Ph.D (Tokyo Keizai University, Japan) 2013 ARIA Annual Meeting 1 1. Introduction

Organizational Structure and Insurers Risk Taking: Evidence from the Life Insurance Industry in Japan Noriyoshi Yanase, Ph.D (Tokyo Keizai University, Japan) 2013 ARIA Annual Meeting 1 1. Introduction

A Presentation On the State of the Real Estate Crisis 1/30/2009

A Presentation On the State of the Real Estate Crisis 1/30/2009 Presented by Mike Anderson, CRMS President, Essential Mortgage, a Latter & Blum Realtors Company Immediate past president/legislative Chair

A Presentation On the State of the Real Estate Crisis 1/30/2009 Presented by Mike Anderson, CRMS President, Essential Mortgage, a Latter & Blum Realtors Company Immediate past president/legislative Chair

Also in 2013 MIP Will No Longer Expire Currently MIP Expires in five years and when loan to value drops to 78%

FHA MORTGAGE INSURANCE PREMIMUM (MIP & UFMIP) FHA charges Two Mortgage Insurance fees on each loan; Up Front Mortgage Insurance Premium (UFMIP) typically financed in the loan and Annual mortgage Insurance

FHA MORTGAGE INSURANCE PREMIMUM (MIP & UFMIP) FHA charges Two Mortgage Insurance fees on each loan; Up Front Mortgage Insurance Premium (UFMIP) typically financed in the loan and Annual mortgage Insurance

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods TABLE OF CONTENTS

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods 1.0 FINANCIAL FORECASTING METHODS 1.01 Introduction

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods 1.0 FINANCIAL FORECASTING METHODS 1.01 Introduction

Commercial Mortgage Types and Decisions

Commercial Mortgage Types and Decisions Commercial mortgages & notes for existing properties not as standardized as home loans Documents are longer & more complex Often no personal liability: Legal borrower

Commercial Mortgage Types and Decisions Commercial mortgages & notes for existing properties not as standardized as home loans Documents are longer & more complex Often no personal liability: Legal borrower

Understanding Credit and the Types of Interest Rates that Affect Your Loans

Understanding Credit and the Types of Interest Rates that Affect Your Loans Presented By: Barbara Hume, Senior Assistant General Manager, NCB Retail Banking Division Why Borrow? To increase your capacity

Understanding Credit and the Types of Interest Rates that Affect Your Loans Presented By: Barbara Hume, Senior Assistant General Manager, NCB Retail Banking Division Why Borrow? To increase your capacity

Step-by-Step Home Mortgage Steps

1 Applicants with a good credit report will be in a stronger position to negotiate best rate and terms Your credit report is used by banks and other lending institutions to determine your creditworthiness.

1 Applicants with a good credit report will be in a stronger position to negotiate best rate and terms Your credit report is used by banks and other lending institutions to determine your creditworthiness.

Financing Your Dreams

Financing Your Dreams Working together for your benefit Your personal balance sheet comprises assets what you own and liabilities what you owe. When or whether you eventually reach your long-term financial

Financing Your Dreams Working together for your benefit Your personal balance sheet comprises assets what you own and liabilities what you owe. When or whether you eventually reach your long-term financial

ARION BANK S 2014 FINANCIAL RESULTS

Press release, 24 February 2015 ARION BANK S 2014 FINANCIAL RESULTS Arion Bank reported net earnings of ISK 28.7 billion for the year 2014, compared with ISK 12.7 billion for the year 2013. Return on equity

Press release, 24 February 2015 ARION BANK S 2014 FINANCIAL RESULTS Arion Bank reported net earnings of ISK 28.7 billion for the year 2014, compared with ISK 12.7 billion for the year 2013. Return on equity

Incentive Compensation for Risk Managers when Effort is Unobservable

Incentive Compensation for Risk Managers when Effort is Unobservable by Paul Kupiec 1 This Draft: October 2013 Abstract In a stylized model of a financial intermediary, risk managers can expend effort

Incentive Compensation for Risk Managers when Effort is Unobservable by Paul Kupiec 1 This Draft: October 2013 Abstract In a stylized model of a financial intermediary, risk managers can expend effort

The Impact of Interest Rate Shocks on the Performance of the Banking Sector

The Impact of Interest Rate Shocks on the Performance of the Banking Sector by Wensheng Peng, Kitty Lai, Frank Leung and Chang Shu of the Research Department A rise in the Hong Kong dollar risk premium,

The Impact of Interest Rate Shocks on the Performance of the Banking Sector by Wensheng Peng, Kitty Lai, Frank Leung and Chang Shu of the Research Department A rise in the Hong Kong dollar risk premium,

SMALL BUSINESS DEVELOPMENT CENTER RM. 032

SMALL BUSINESS DEVELOPMENT CENTER RM. 032 FINANCING THROUGH COMMERCIAL BANKS Revised January, 2013 Adapted from: National Federation of Independent Business report Steps to Small Business Financing Jeffrey

SMALL BUSINESS DEVELOPMENT CENTER RM. 032 FINANCING THROUGH COMMERCIAL BANKS Revised January, 2013 Adapted from: National Federation of Independent Business report Steps to Small Business Financing Jeffrey

1. Supply and demand are the most important concepts in economics.

Page 1 1. Supply and demand are the most important concepts in economics. 2. Markets and Competition a. Market is a group of buyers and sellers of a particular good or service. P. 66. b. These individuals

Page 1 1. Supply and demand are the most important concepts in economics. 2. Markets and Competition a. Market is a group of buyers and sellers of a particular good or service. P. 66. b. These individuals

US LOAN SERVICES APRIL 2016 NICK OLDFIELD / TOBY WELLS

US LOAN SERVICES APRIL 2016 NICK OLDFIELD / TOBY WELLS US Mortgage Servicing Market $10 trillion in New mortgage Business debt outstanding, with more than $1 trillion in new originations each year Corporate

US LOAN SERVICES APRIL 2016 NICK OLDFIELD / TOBY WELLS US Mortgage Servicing Market $10 trillion in New mortgage Business debt outstanding, with more than $1 trillion in new originations each year Corporate

FINANCIAL ANALYSIS GUIDE

MAN 4720 POLICY ANALYSIS AND FORMULATION FINANCIAL ANALYSIS GUIDE Revised -August 22, 2010 FINANCIAL ANALYSIS USING STRATEGIC PROFIT MODEL RATIOS Introduction Your policy course integrates information

MAN 4720 POLICY ANALYSIS AND FORMULATION FINANCIAL ANALYSIS GUIDE Revised -August 22, 2010 FINANCIAL ANALYSIS USING STRATEGIC PROFIT MODEL RATIOS Introduction Your policy course integrates information