Optimal order placement in a limit order book. Adrien de Larrard and Xin Guo. Laboratoire de Probabilités, Univ Paris VI & UC Berkeley

|

|

|

- Marianna Barton

- 8 years ago

- Views:

Transcription

1 Optimal order placement in a limit order book Laboratoire de Probabilités, Univ Paris VI & UC Berkeley

2 Outline 1 Background: Algorithm trading in different time scales 2 Some note on optimal execution in daily trading 3 Optimal execution with key statistics of the limit order book Basics of LOB Model without price impact Model with linear price impact 4 Optimal strategy with full information of the limit order book

3 Optimal execution (on daily) time scale What is algorithm trading In an electronic order-driven market, orders arrive to the exchange and wait in the LOB (Limit Order Book) to be executed LOB contains detailed information of each order: size, buy and sell type (market order or limit order) Algorithm trading: automatic and rapid trading of large quantities based on LOB information, orders are specified and implemented by computer algorithm

4 Optimal execution (on daily) time scale Order flow: traffic is heavy... Citigroup 4469 General Electric 2356 General Motors 1275 Table: Average number of orders in a 10 second interval (June 26th, 2008) Citigroup General Electric 7862 General Motors 9016 Table: Number of changes in the price on June 26th, 2008.

5 Optimal execution (on daily) time scale On main issue in algorithm trading Selling/buying a (large) number of shares Trading strategy has impact on stock price Too quick selling will cause price to drop too fast Too slow selling will loss appropriate appreciation Transaction cost

6 Optimal execution (on daily) time scale Algorithm trading in three time scales Regime Time scale Issues Ultra-high frequency (UHF) Tick ( s) Microstructure, Latency High Frequency (HF) s Optimal placement (**) Daily s Trading, Option hedging (*) Table: A hierarchy of time scales.

Table: A hierarchy of time")

7 Optimal execution (on daily) time scale Optimal execution in algorithmic trading On a daily (weekly) time scale, give the optimal rate of trading: On a 1/5 minute time scale, optimally place the orders in the limit order book in order to get the best price and minimize trading costs

8 Optimal execution (on daily) time scale Optimal execution (on daily) time scale Brownian motion/random walk based models Two types of price impact: temporary vs permanent Finite time horizon, with 0 discount rate Static/deterministic trading is optimal VWAP, POV, Bertimas and Lo (98), Almgren-Chriss (99,01,03), Huberman and Stanzl (00), Obizhaeva and Wang (05), Schied and Schoneborn (07,08), Almgren and Lorenz (07), Gatheral (2010)

, Obizhaeva and Wang (05), Schied and Schoneborn (07,08), Almgren and Lorenz (07), Gatheral")

9 Optimal execution (on daily) time scale Why deterministic is optimal Because of the martingale property, minimize the price impact is equivalent to minimizing the cost Because of the martingale property, minimizing the price impact is equivalent to a deterministic optimization problem No known explicit solution for other existing models with price impact Gatheral (2010), Predoiu, Shaiket, and Shreve (2010)

, Predoiu, Shaiket, and")

10 Optimal execution (on daily) time scale A simple example for which optimal strategy is not static (Guo and Zervos (2010)) Y t (ω): the number of shares held at time t, Y 0 = y ξ t (ω): the total number of shares sold up to time t, is a non-decreasing process, so that Y t = y ξ t, dy t = dξ t S t (ω): the stock price at time t with S t = e Xt dx t = µdt λdξ t + σdw t for some constant µ, λ, σ, with x = X 0 = ln S 0

11 Optimal execution (on daily) time scale Optimization problem with T V (x, y) = sup E[ e δt (e Xt C) dξ t ] ξ 0 C the transaction cost of selling each share δ the impatience index Non-linear price impact in the performance critrion ξt (e Xt C) dξ t = e Xt dξt c + e X t λu du Cdξ t 0

dξ t = e Xt dξt c + e X t λu du")

12 Optimal execution (on daily) time scale Explicit solution for T = The value function is finite iff µ < δ, If C = 0 and µ < δ, sell off everything immediately is optimal In general, when C > 0 and µ < δ The state space {(x, y), y > 0} is divided into Continuation Region C and Action Region A, and the free boundary is x = F (y). In A, e x C λw x(x, y) W y (x, y) = 0 In C, 1 2 σ2 W xx(x, y) + µw x(x, y) δw (x, y) = 0

.")

13 Optimal execution (on daily) time scale Derivation of solution Standard Verification Theorem Approach In C, smooth-fit principle solves explicitly F (y) = ln nc n 1 with n > 1 satisfying 1 2 σ2 n 2 + µn δ = 0 In A, two possible actions Sell off everything immediately Jump to the boundary and continue afterwards Value function is C 2.

14 Optimal execution (on daily) time scale y A 1 ln(cn/(n-1))+ y A 2 C ln (cn/(n-1)) x

)+ y A 2")

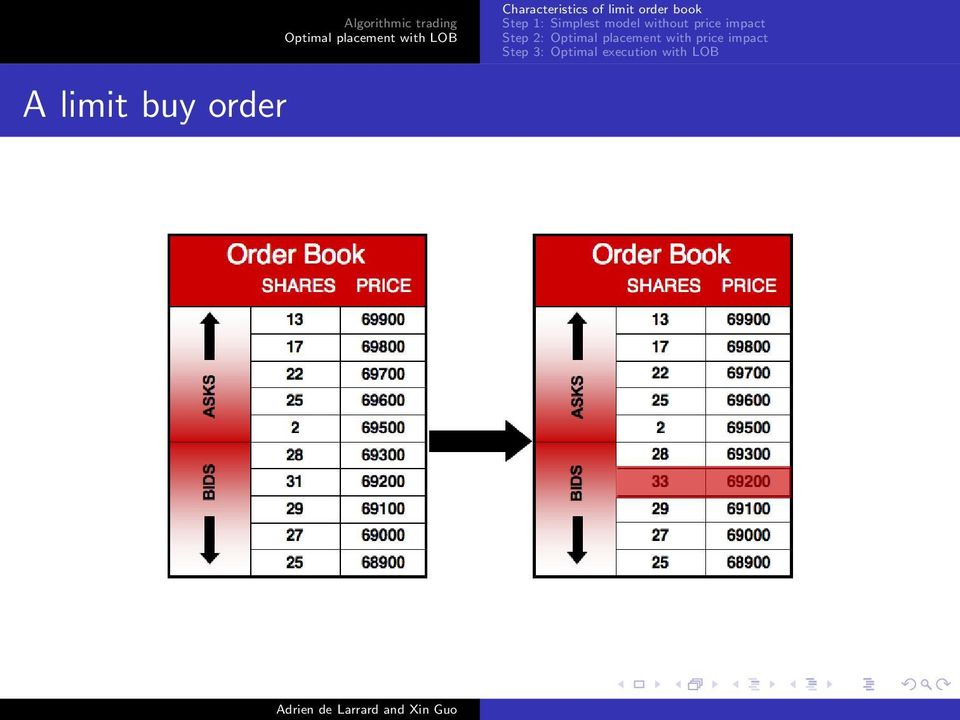

15 A limit buy order Algorithmic trading

16 A limit buy order Algorithmic trading

17 A market sell order Algorithmic trading

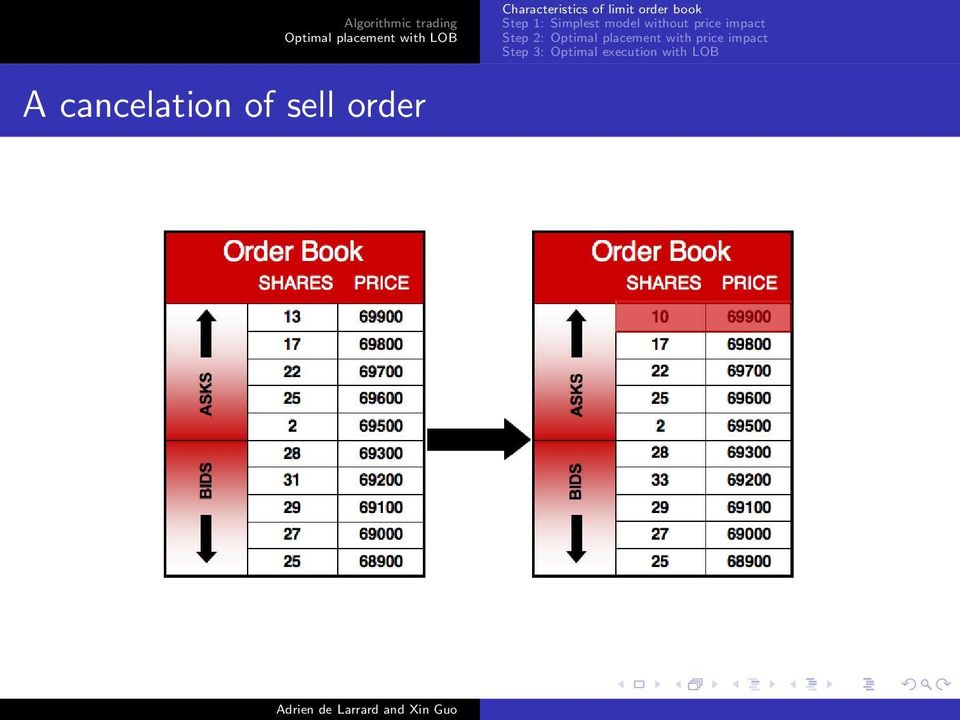

18 A cancelation of sell order

19 What is a LOB LOB contains detailed information of buy and sell types (market order or limit order) and their sizes Limit buy/sell order: an order to buy/sell a certain quantity at a given price Market buy/sell order: an order to buy/sell a certain quantity at the best available price in LOB (Best) ask price: lowest price in limit sell order (Best) bid price: the highest price in limit buy order

ask price: lowest price in limit sell order (Best) bid price: the highest price in limit buy")

20 Main characteristics of LOB Ask/bid prices in high frequency trading are believed by practitioners to be mean-reverting Probability of a limit order being executed depends on the queue length, its position in the LOB, frequency of price changes, cancelation of orders... Traders face trade-off between limit orders and market orders: pay the spread and fees vs execution/inventory risk

21 Our work (de larrard and Guo (2010)) Address the following questions: should one use market orders or limit orders? At which levels should one place orders and how? Provide optimal order execution strategy with the incorporation of 1 key statistics of the limit order book 2 statistics and realistic assumptions on the order flow (arrival rates of market, limit orders and cancelation)

22 A simple mean-reverting model Fix a time horizon [0, T ]. The spread between the bid price (B t, t 0) and the ask price (A t, t 0) is constant, say equal to one tick The (ask) price (A t, t 0) follows a continuous time, piecewise constant process Increments of the ask are +1 or 1 tick The probability of execution if spent time t as the first limit is F (t). The price moves at time 0 T 1 < T 2 < T n T and the distribution of the number of price moves before time T is given by a distribution G T.

23 Given G T = n, A T = n i=1 X i where where p c is a constant P(X 1 = 1) = P(X 1 = 1) = 1 2, P(X i = X i 1 X i 1 ) = p c, Note: when p c = 1 2, the price is a time-changed random walk; when p c < 1 2, the price mean-reverts.

24 Objective Buy N orders before time T > 0 (T 1/5 minutes) Split the N orders in (N 0, N 1,...) where N 0 is the number of orders at market orders, N 1 the number of orders at the bid... If the N orders are not executed at time T, have to buy the non-executed orders at the market price When one limit order is executed, the market gives a rebate of r > 0 When the trader submits a market order, there is a fee of f > 0 Given (N 0, N 1,..., N k ), find the optimal strategy for min (N 0,..,N k..), k=0 N k =N E[C(N 0,..., N k,...)]

25 Two key quantities for the model P( n X i = k) = u(n, k), i=1 φ(k, T ) = P[ min A(t) = k]. 0 t T

26 Theorem Given n price changes, u(n + k, n k) = 2k i=1 ( (1 p c) i 2 p k+n i 1 c g(n, k, i) where g(n, k, i) = 2C n 1 (i 1)/2 C k 1 (i 1)/2, n is odd g(n, k, i) = C n 1 [(i 1)/2] C k 1 [(i+1)/2] + C n 1 [(i+1)/2] C k 1 [(i 1)/2] n is even

27 Key: Algorithmic trading calculating u(n + k, n k) amounts to calculating the probability of a sequence of 1 and -1 of length n+k, with n 1 s and k -1 s and i switches, with i = 1,, 2k.

28 For the second quantity, note that P[min s T A r = k G T = n] can be calculated using the idea of the reflection principle of a random walk.

29 Derivation of optimal strategy: two steps Consider C i (γ, T ) the average cost of 1 share put at i-th limit from the ask, then E[C(N 0, N 1,..., N k )] = C i (γ, T )N i Key lemma For all i 1, there is a function (f i (γ, T ), 0 γ, ) such that C i (γ, T ) = C i (0, T ) + f i (γ, T )(C i (, T ) C i (0, T )). Moreover if k 0, φ(k, T ) = P[min 0 t T A(t) = k], k=0 C i (0, T ) = f (r + f ) φ( k, T ), k=i and C i (, T ) = f (r + f + 1) φ( k, T ) k=i 1

30 Corollary For all 0 γ and for all T > 0, C 0 (γ, T ) >... > C k (γ, T ) > C k 1 (γ, T ) >... > C 1 (γ, T )

31 Optimal dynamic strategy Using the Dynamic Programming Principle, we have Theorem The optimal strategy is to peg the price. That is, follow the price at the bid.

32 Estimating G T from LOB Two possible candidates for G T Empirical studies suggest that G T might be exponentially distributed Modeling the dynamics of order book (q a, q b ) by a correlated Brownian motion as in Cont and Larrard (2011), so that the distribution of next price change can be explicitly computed by Iryengar (1985).

33 A model with linear price impact Fix time [0, T ] and 0 = t 0 < t 1 < t n = T, t k t k 1 constant Buy N orders by time T. Orders are placed only at 0 = t 0 < t 1 < t n = T A t is the mean-reverting random walk as before, if no order placed N m t, N l t the number of shares to be placed on market order and limit order at time t respectively Linear price impact: additional price increase by α(nt m market order and (best) limit order placed + N l t) with Probability of limit order being executed by the next time step is a constant p(t k t k 1 )

34 Remark on linear price impact Recently an empirical study by Cont, Kubanov and Stoikov (2010) shows that on the trade level all trades have linear price impact

35 Objective Algorithmic trading The objective is to minimize T E[ g(a t, Nt m, Nt, l r, f )] t=1 overall all sequences {(N1 m, Nl 1 ), (Nm 2, Nl 2 ),, (Nm T, Nl T )}. Here g(x t, Nt m, Nt, l r, f ) is the cost at time t associated with placing orders Nt m, Nt, l with fee f and spread for each marker order and rebate r for each limit order. In particular, one is to minimize the expected price.

36 Optimal dynamic strategy Theorem There exists an optimal sequence of {(N m t, N l t), t = 0,, T } which is solved explicitly and recursively through a quadratic programming with linear constraint. Depending on the parameters, there are three cases Put everything on market order at time 0 or time T Put everything on limit order in a VWAP sense Put everything on limit order, but not in VWAP sense. Note: Because the underlying price is not martingale, minimize the cost is in general not equivalent to minimizing the price impact

37 Key idea for the underlying model Focus on the (best) bid and ask and their queue length The queue length is renewed according to some distributions after a price increase/decrease Quantities q b q a δ Price s b s a

38 Price dynamics Algorithmic trading Quantities f(,. ) f(., ) δ Price s b s a Figure: Joint density of bid and ask queues after a price move.

39 Optimal placement with full inclusion of LOB dynamics Take the ask and bid dynamics as a queuing system suggested in Cont and de Larrard (2011) Impulse control formulation of order placement (on both market order and limit orders) Associated HJB equation is with non-standard boundary conditions Work in Progress

40 Related references Xin Guo and Mihail Zervos (2010) Optimal Selling With Liquidation Constraint and Transaction Cost (2011) Optimal order placement in a limit order book, Working paper.

41 THANK YOU

FE570 Financial Markets and Trading. Stevens Institute of Technology

FE570 Financial Markets and Trading Lecture 13. Execution Strategies (Ref. Anatoly Schmidt CHAPTER 13 Execution Strategies) Steve Yang Stevens Institute of Technology 11/27/2012 Outline 1 Execution Strategies

FE570 Financial Markets and Trading Lecture 13. Execution Strategies (Ref. Anatoly Schmidt CHAPTER 13 Execution Strategies) Steve Yang Stevens Institute of Technology 11/27/2012 Outline 1 Execution Strategies

Adaptive Arrival Price

Adaptive Arrival Price Julian Lorenz (ETH Zurich, Switzerland) Robert Almgren (Adjunct Professor, New York University) Algorithmic Trading 2008, London 07. 04. 2008 Outline Evolution of algorithmic trading

Adaptive Arrival Price Julian Lorenz (ETH Zurich, Switzerland) Robert Almgren (Adjunct Professor, New York University) Algorithmic Trading 2008, London 07. 04. 2008 Outline Evolution of algorithmic trading

Semi-Markov model for market microstructure and HF trading

Semi-Markov model for market microstructure and HF trading LPMA, University Paris Diderot and JVN Institute, VNU, Ho-Chi-Minh City NUS-UTokyo Workshop on Quantitative Finance Singapore, 26-27 september

Semi-Markov model for market microstructure and HF trading LPMA, University Paris Diderot and JVN Institute, VNU, Ho-Chi-Minh City NUS-UTokyo Workshop on Quantitative Finance Singapore, 26-27 september

FE670 Algorithmic Trading Strategies. Stevens Institute of Technology

FE670 Algorithmic Trading Strategies Lecture 10. Investment Management and Algorithmic Trading Steve Yang Stevens Institute of Technology 11/14/2013 Outline 1 Algorithmic Trading Strategies 2 Optimal Execution

FE670 Algorithmic Trading Strategies Lecture 10. Investment Management and Algorithmic Trading Steve Yang Stevens Institute of Technology 11/14/2013 Outline 1 Algorithmic Trading Strategies 2 Optimal Execution

Chapter 2: Binomial Methods and the Black-Scholes Formula

Chapter 2: Binomial Methods and the Black-Scholes Formula 2.1 Binomial Trees We consider a financial market consisting of a bond B t = B(t), a stock S t = S(t), and a call-option C t = C(t), where the

Chapter 2: Binomial Methods and the Black-Scholes Formula 2.1 Binomial Trees We consider a financial market consisting of a bond B t = B(t), a stock S t = S(t), and a call-option C t = C(t), where the

OPTIMAL TIMING FOR SHORT COVERING OF AN ILLIQUID SECURITY

Journal of the Operations Research Society of Japan Vol. 58, No. 2, April 2015, pp. 165 183 c The Operations Research Society of Japan OPTIMAL TIMING FOR SHORT COVERING OF AN ILLIQUID SECURITY Tsz-Kin

Journal of the Operations Research Society of Japan Vol. 58, No. 2, April 2015, pp. 165 183 c The Operations Research Society of Japan OPTIMAL TIMING FOR SHORT COVERING OF AN ILLIQUID SECURITY Tsz-Kin

Two Topics in Parametric Integration Applied to Stochastic Simulation in Industrial Engineering

Two Topics in Parametric Integration Applied to Stochastic Simulation in Industrial Engineering Department of Industrial Engineering and Management Sciences Northwestern University September 15th, 2014

Two Topics in Parametric Integration Applied to Stochastic Simulation in Industrial Engineering Department of Industrial Engineering and Management Sciences Northwestern University September 15th, 2014

Supplement to Call Centers with Delay Information: Models and Insights

Supplement to Call Centers with Delay Information: Models and Insights Oualid Jouini 1 Zeynep Akşin 2 Yves Dallery 1 1 Laboratoire Genie Industriel, Ecole Centrale Paris, Grande Voie des Vignes, 92290

Supplement to Call Centers with Delay Information: Models and Insights Oualid Jouini 1 Zeynep Akşin 2 Yves Dallery 1 1 Laboratoire Genie Industriel, Ecole Centrale Paris, Grande Voie des Vignes, 92290

Hedging market risk in optimal liquidation

Hedging market risk in optimal liquidation Phillip Monin The Office of Financial Research Washington, DC Conference on Stochastic Asymptotics & Applications, Joint with 6th Western Conference on Mathematical

Hedging market risk in optimal liquidation Phillip Monin The Office of Financial Research Washington, DC Conference on Stochastic Asymptotics & Applications, Joint with 6th Western Conference on Mathematical

Bayesian Adaptive Trading with a Daily Cycle

Bayesian Adaptive Trading with a Daily Cycle Robert Almgren and Julian Lorenz July 28, 26 Abstract Standard models of algorithmic trading neglect the presence of a daily cycle. We construct a model in

Bayesian Adaptive Trading with a Daily Cycle Robert Almgren and Julian Lorenz July 28, 26 Abstract Standard models of algorithmic trading neglect the presence of a daily cycle. We construct a model in

CS 522 Computational Tools and Methods in Finance Robert Jarrow Lecture 1: Equity Options

CS 5 Computational Tools and Methods in Finance Robert Jarrow Lecture 1: Equity Options 1. Definitions Equity. The common stock of a corporation. Traded on organized exchanges (NYSE, AMEX, NASDAQ). A common

CS 5 Computational Tools and Methods in Finance Robert Jarrow Lecture 1: Equity Options 1. Definitions Equity. The common stock of a corporation. Traded on organized exchanges (NYSE, AMEX, NASDAQ). A common

High-frequency trading in a limit order book

High-frequency trading in a limit order book Marco Avellaneda & Sasha Stoikov October 5, 006 Abstract We study a stock dealer s strategy for submitting bid and ask quotes in a limit order book. The agent

High-frequency trading in a limit order book Marco Avellaneda & Sasha Stoikov October 5, 006 Abstract We study a stock dealer s strategy for submitting bid and ask quotes in a limit order book. The agent

The Exponential Distribution

21 The Exponential Distribution From Discrete-Time to Continuous-Time: In Chapter 6 of the text we will be considering Markov processes in continuous time. In a sense, we already have a very good understanding

21 The Exponential Distribution From Discrete-Time to Continuous-Time: In Chapter 6 of the text we will be considering Markov processes in continuous time. In a sense, we already have a very good understanding

arxiv:1210.1625v4 [q-fin.tr] 23 Nov 2014

![arxiv:1210.1625v4 [q-fin.tr] 23 Nov 2014](/thumbs/40/21841398.jpg "arxiv:1210.1625v4 [q-fin.tr] 23 Nov 2014") Optimal order placement in limit order markets Rama Cont and Arseniy Kukanov Imperial College London & AQR Capital Management arxiv:1210.1625v4 [q-fin.tr] 23 Nov 2014 To execute a trade, participants in

Optimal order placement in limit order markets Rama Cont and Arseniy Kukanov Imperial College London & AQR Capital Management arxiv:1210.1625v4 [q-fin.tr] 23 Nov 2014 To execute a trade, participants in

A Log-Robust Optimization Approach to Portfolio Management

A Log-Robust Optimization Approach to Portfolio Management Dr. Aurélie Thiele Lehigh University Joint work with Ban Kawas Research partially supported by the National Science Foundation Grant CMMI-0757983

A Log-Robust Optimization Approach to Portfolio Management Dr. Aurélie Thiele Lehigh University Joint work with Ban Kawas Research partially supported by the National Science Foundation Grant CMMI-0757983

Hedging Options In The Incomplete Market With Stochastic Volatility. Rituparna Sen Sunday, Nov 15

Hedging Options In The Incomplete Market With Stochastic Volatility Rituparna Sen Sunday, Nov 15 1. Motivation This is a pure jump model and hence avoids the theoretical drawbacks of continuous path models.

Hedging Options In The Incomplete Market With Stochastic Volatility Rituparna Sen Sunday, Nov 15 1. Motivation This is a pure jump model and hence avoids the theoretical drawbacks of continuous path models.

Lectures on Stochastic Processes. William G. Faris

Lectures on Stochastic Processes William G. Faris November 8, 2001 2 Contents 1 Random walk 7 1.1 Symmetric simple random walk................... 7 1.2 Simple random walk......................... 9 1.3

Lectures on Stochastic Processes William G. Faris November 8, 2001 2 Contents 1 Random walk 7 1.1 Symmetric simple random walk................... 7 1.2 Simple random walk......................... 9 1.3

Algorithmic Trading: Model of Execution Probability and Order Placement Strategy

Algorithmic Trading: Model of Execution Probability and Order Placement Strategy Chaiyakorn Yingsaeree A dissertation submitted in partial fulfillment of the requirements for the degree of Doctor of Philosophy

Algorithmic Trading: Model of Execution Probability and Order Placement Strategy Chaiyakorn Yingsaeree A dissertation submitted in partial fulfillment of the requirements for the degree of Doctor of Philosophy

Order Book Simulator and Optimal Liquidation Strategies

Stanford University MS&E 444 Investment Practice Course Project Order Book Simulator and Optimal Liquidation Strategies Su Chen *, Chen Hu, Yijia Zhou June 2010 Abstract Our project analyzes the statistics

Stanford University MS&E 444 Investment Practice Course Project Order Book Simulator and Optimal Liquidation Strategies Su Chen *, Chen Hu, Yijia Zhou June 2010 Abstract Our project analyzes the statistics

OPTIMAL TIMING OF THE ANNUITY PURCHASES: A

OPTIMAL TIMING OF THE ANNUITY PURCHASES: A COMBINED STOCHASTIC CONTROL AND OPTIMAL STOPPING PROBLEM Gabriele Stabile 1 1 Dipartimento di Matematica per le Dec. Econ. Finanz. e Assic., Facoltà di Economia

OPTIMAL TIMING OF THE ANNUITY PURCHASES: A COMBINED STOCHASTIC CONTROL AND OPTIMAL STOPPING PROBLEM Gabriele Stabile 1 1 Dipartimento di Matematica per le Dec. Econ. Finanz. e Assic., Facoltà di Economia

Optimal Insurance Coverage of a Durable Consumption Good with a Premium Loading in a Continuous Time Economy

Optimal Insurance Coverage of a Durable Consumption Good with a Premium Loading in a Continuous Time Economy Masaaki Kijima 1 Teruyoshi Suzuki 2 1 Tokyo Metropolitan University and Daiwa Securities Group

Optimal Insurance Coverage of a Durable Consumption Good with a Premium Loading in a Continuous Time Economy Masaaki Kijima 1 Teruyoshi Suzuki 2 1 Tokyo Metropolitan University and Daiwa Securities Group

Optimal proportional reinsurance and dividend pay-out for insurance companies with switching reserves

Optimal proportional reinsurance and dividend pay-out for insurance companies with switching reserves Abstract: This paper presents a model for an insurance company that controls its risk and dividend

Optimal proportional reinsurance and dividend pay-out for insurance companies with switching reserves Abstract: This paper presents a model for an insurance company that controls its risk and dividend

Christfried Webers. Canberra February June 2015

c Statistical Group and College of Engineering and Computer Science Canberra February June (Many figures from C. M. Bishop, "Pattern Recognition and ") 1of 829 c Part VIII Linear Classification 2 Logistic

c Statistical Group and College of Engineering and Computer Science Canberra February June (Many figures from C. M. Bishop, "Pattern Recognition and ") 1of 829 c Part VIII Linear Classification 2 Logistic

Online Appendix. Supplemental Material for Insider Trading, Stochastic Liquidity and. Equilibrium Prices. by Pierre Collin-Dufresne and Vyacheslav Fos

Online Appendix Supplemental Material for Insider Trading, Stochastic Liquidity and Equilibrium Prices by Pierre Collin-Dufresne and Vyacheslav Fos 1. Deterministic growth rate of noise trader volatility

Online Appendix Supplemental Material for Insider Trading, Stochastic Liquidity and Equilibrium Prices by Pierre Collin-Dufresne and Vyacheslav Fos 1. Deterministic growth rate of noise trader volatility

Financial Market Microstructure Theory

The Microstructure of Financial Markets, de Jong and Rindi (2009) Financial Market Microstructure Theory Based on de Jong and Rindi, Chapters 2 5 Frank de Jong Tilburg University 1 Determinants of the

The Microstructure of Financial Markets, de Jong and Rindi (2009) Financial Market Microstructure Theory Based on de Jong and Rindi, Chapters 2 5 Frank de Jong Tilburg University 1 Determinants of the

Brownian Motion and Stochastic Flow Systems. J.M Harrison

Brownian Motion and Stochastic Flow Systems 1 J.M Harrison Report written by Siva K. Gorantla I. INTRODUCTION Brownian motion is the seemingly random movement of particles suspended in a fluid or a mathematical

Brownian Motion and Stochastic Flow Systems 1 J.M Harrison Report written by Siva K. Gorantla I. INTRODUCTION Brownian motion is the seemingly random movement of particles suspended in a fluid or a mathematical

Stochastic Models for Inventory Management at Service Facilities

Stochastic Models for Inventory Management at Service Facilities O. Berman, E. Kim Presented by F. Zoghalchi University of Toronto Rotman School of Management Dec, 2012 Agenda 1 Problem description Deterministic

Stochastic Models for Inventory Management at Service Facilities O. Berman, E. Kim Presented by F. Zoghalchi University of Toronto Rotman School of Management Dec, 2012 Agenda 1 Problem description Deterministic

Mathematical Finance

Mathematical Finance Option Pricing under the Risk-Neutral Measure Cory Barnes Department of Mathematics University of Washington June 11, 2013 Outline 1 Probability Background 2 Black Scholes for European

Mathematical Finance Option Pricing under the Risk-Neutral Measure Cory Barnes Department of Mathematics University of Washington June 11, 2013 Outline 1 Probability Background 2 Black Scholes for European

The London School of Economics and Political Science. Stochastic Models for the Limit Order Book. Filippo Riccardi

The London School of Economics and Political Science Stochastic Models for the Limit Order Book Filippo Riccardi A thesis submitted to the Department of Statistics of the London School of Economics for

The London School of Economics and Political Science Stochastic Models for the Limit Order Book Filippo Riccardi A thesis submitted to the Department of Statistics of the London School of Economics for

Martingale Pricing Applied to Options, Forwards and Futures

IEOR E4706: Financial Engineering: Discrete-Time Asset Pricing Fall 2005 c 2005 by Martin Haugh Martingale Pricing Applied to Options, Forwards and Futures We now apply martingale pricing theory to the

IEOR E4706: Financial Engineering: Discrete-Time Asset Pricing Fall 2005 c 2005 by Martin Haugh Martingale Pricing Applied to Options, Forwards and Futures We now apply martingale pricing theory to the

A Uniform Asymptotic Estimate for Discounted Aggregate Claims with Subexponential Tails

12th International Congress on Insurance: Mathematics and Economics July 16-18, 2008 A Uniform Asymptotic Estimate for Discounted Aggregate Claims with Subexponential Tails XUEMIAO HAO (Based on a joint

12th International Congress on Insurance: Mathematics and Economics July 16-18, 2008 A Uniform Asymptotic Estimate for Discounted Aggregate Claims with Subexponential Tails XUEMIAO HAO (Based on a joint

Trade arrival dynamics and quote imbalance in a limit order book

Trade arrival dynamics and quote imbalance in a limit order book arxiv:1312.0514v1 [q-fin.tr] 2 Dec 2013 Alexander Lipton, Umberto Pesavento and Michael G Sotiropoulos 2 December 2013 Abstract We examine

Trade arrival dynamics and quote imbalance in a limit order book arxiv:1312.0514v1 [q-fin.tr] 2 Dec 2013 Alexander Lipton, Umberto Pesavento and Michael G Sotiropoulos 2 December 2013 Abstract We examine

Numerical methods for American options

Lecture 9 Numerical methods for American options Lecture Notes by Andrzej Palczewski Computational Finance p. 1 American options The holder of an American option has the right to exercise it at any moment

Lecture 9 Numerical methods for American options Lecture Notes by Andrzej Palczewski Computational Finance p. 1 American options The holder of an American option has the right to exercise it at any moment

Some stability results of parameter identification in a jump diffusion model

Some stability results of parameter identification in a jump diffusion model D. Düvelmeyer Technische Universität Chemnitz, Fakultät für Mathematik, 09107 Chemnitz, Germany Abstract In this paper we discuss

Some stability results of parameter identification in a jump diffusion model D. Düvelmeyer Technische Universität Chemnitz, Fakultät für Mathematik, 09107 Chemnitz, Germany Abstract In this paper we discuss

e.g. arrival of a customer to a service station or breakdown of a component in some system.

Poisson process Events occur at random instants of time at an average rate of λ events per second. e.g. arrival of a customer to a service station or breakdown of a component in some system. Let N(t) be

Poisson process Events occur at random instants of time at an average rate of λ events per second. e.g. arrival of a customer to a service station or breakdown of a component in some system. Let N(t) be

14 Greeks Letters and Hedging

ECG590I Asset Pricing. Lecture 14: Greeks Letters and Hedging 1 14 Greeks Letters and Hedging 14.1 Illustration We consider the following example through out this section. A financial institution sold

ECG590I Asset Pricing. Lecture 14: Greeks Letters and Hedging 1 14 Greeks Letters and Hedging 14.1 Illustration We consider the following example through out this section. A financial institution sold

The execution puzzle: How and when to trade to minimize cost

The execution puzzle: How and when to trade to minimize cost Jim Gatheral 5th International Financial and Capital Markets Conference Campos de Jordão, Brazil, August 27th, 2011 Overview of this talk What

The execution puzzle: How and when to trade to minimize cost Jim Gatheral 5th International Financial and Capital Markets Conference Campos de Jordão, Brazil, August 27th, 2011 Overview of this talk What

Sensitivity analysis of utility based prices and risk-tolerance wealth processes

Sensitivity analysis of utility based prices and risk-tolerance wealth processes Dmitry Kramkov, Carnegie Mellon University Based on a paper with Mihai Sirbu from Columbia University Math Finance Seminar,

Sensitivity analysis of utility based prices and risk-tolerance wealth processes Dmitry Kramkov, Carnegie Mellon University Based on a paper with Mihai Sirbu from Columbia University Math Finance Seminar,

Market Micro Structure knowledge needed to control an intra-day trading process

Market Micro Structure knowledge needed to control an intra-day trading process Gobal Head of Quantitative Research Crédit Agricole Chevreux Based on joint works with B. Bouchard and M. Dang (Impulse control);

Market Micro Structure knowledge needed to control an intra-day trading process Gobal Head of Quantitative Research Crédit Agricole Chevreux Based on joint works with B. Bouchard and M. Dang (Impulse control);

ALGORITHMIC TRADING WITH MARKOV CHAINS

June 16, 2010 ALGORITHMIC TRADING WITH MARKOV CHAINS HENRIK HULT AND JONAS KIESSLING Abstract. An order book consists of a list of all buy and sell offers, represented by price and quantity, available

June 16, 2010 ALGORITHMIC TRADING WITH MARKOV CHAINS HENRIK HULT AND JONAS KIESSLING Abstract. An order book consists of a list of all buy and sell offers, represented by price and quantity, available

Supervised Learning of Market Making Strategy

Supervised Learning of Market Making Strategy Ori Gil Gal Zahavi April 2, 2012 Abstract Many economic markets, including most major stock exchanges, employ market-makers to aid in the transactions and

Supervised Learning of Market Making Strategy Ori Gil Gal Zahavi April 2, 2012 Abstract Many economic markets, including most major stock exchanges, employ market-makers to aid in the transactions and

Generating Random Numbers Variance Reduction Quasi-Monte Carlo. Simulation Methods. Leonid Kogan. MIT, Sloan. 15.450, Fall 2010

Simulation Methods Leonid Kogan MIT, Sloan 15.450, Fall 2010 c Leonid Kogan ( MIT, Sloan ) Simulation Methods 15.450, Fall 2010 1 / 35 Outline 1 Generating Random Numbers 2 Variance Reduction 3 Quasi-Monte

Simulation Methods Leonid Kogan MIT, Sloan 15.450, Fall 2010 c Leonid Kogan ( MIT, Sloan ) Simulation Methods 15.450, Fall 2010 1 / 35 Outline 1 Generating Random Numbers 2 Variance Reduction 3 Quasi-Monte

A joint chance-constrained programming approach for call center workforce scheduling under uncertain call arrival forecasts

*Manuscript Click here to view linked References A joint chance-constrained programming approach for call center workforce scheduling under uncertain call arrival forecasts Abstract We consider a workforce

*Manuscript Click here to view linked References A joint chance-constrained programming approach for call center workforce scheduling under uncertain call arrival forecasts Abstract We consider a workforce

Private Equity Fund Valuation and Systematic Risk

An Equilibrium Approach and Empirical Evidence Axel Buchner 1, Christoph Kaserer 2, Niklas Wagner 3 Santa Clara University, March 3th 29 1 Munich University of Technology 2 Munich University of Technology

An Equilibrium Approach and Empirical Evidence Axel Buchner 1, Christoph Kaserer 2, Niklas Wagner 3 Santa Clara University, March 3th 29 1 Munich University of Technology 2 Munich University of Technology

UNIT 2 QUEUING THEORY

UNIT 2 QUEUING THEORY LESSON 24 Learning Objective: Apply formulae to find solution that will predict the behaviour of the single server model II. Apply formulae to find solution that will predict the

UNIT 2 QUEUING THEORY LESSON 24 Learning Objective: Apply formulae to find solution that will predict the behaviour of the single server model II. Apply formulae to find solution that will predict the

Exponential Distribution

Exponential Distribution Definition: Exponential distribution with parameter λ: { λe λx x 0 f(x) = 0 x < 0 The cdf: F(x) = x Mean E(X) = 1/λ. f(x)dx = Moment generating function: φ(t) = E[e tx ] = { 1

Exponential Distribution Definition: Exponential distribution with parameter λ: { λe λx x 0 f(x) = 0 x < 0 The cdf: F(x) = x Mean E(X) = 1/λ. f(x)dx = Moment generating function: φ(t) = E[e tx ] = { 1

A new model of a market maker

A new model of a market maker M.C. Cheung 28786 Master s thesis Economics and Informatics Specialisation in Computational Economics and Finance Erasmus University Rotterdam, the Netherlands January 6,

A new model of a market maker M.C. Cheung 28786 Master s thesis Economics and Informatics Specialisation in Computational Economics and Finance Erasmus University Rotterdam, the Netherlands January 6,

An introduction to asymmetric information and financial market microstructure (Tutorial)

") An introduction to asymmetric information and financial market microstructure (Tutorial) Fabrizio Lillo Scuola Normale Superiore di Pisa, University of Palermo (Italy) and Santa Fe Institute (USA) Pisa

An introduction to asymmetric information and financial market microstructure (Tutorial) Fabrizio Lillo Scuola Normale Superiore di Pisa, University of Palermo (Italy) and Santa Fe Institute (USA) Pisa

Hydrodynamic Limits of Randomized Load Balancing Networks

Hydrodynamic Limits of Randomized Load Balancing Networks Kavita Ramanan and Mohammadreza Aghajani Brown University Stochastic Networks and Stochastic Geometry a conference in honour of François Baccelli

Hydrodynamic Limits of Randomized Load Balancing Networks Kavita Ramanan and Mohammadreza Aghajani Brown University Stochastic Networks and Stochastic Geometry a conference in honour of François Baccelli

QUANTIZED INTEREST RATE AT THE MONEY FOR AMERICAN OPTIONS

QUANTIZED INTEREST RATE AT THE MONEY FOR AMERICAN OPTIONS L. M. Dieng ( Department of Physics, CUNY/BCC, New York, New York) Abstract: In this work, we expand the idea of Samuelson[3] and Shepp[,5,6] for

QUANTIZED INTEREST RATE AT THE MONEY FOR AMERICAN OPTIONS L. M. Dieng ( Department of Physics, CUNY/BCC, New York, New York) Abstract: In this work, we expand the idea of Samuelson[3] and Shepp[,5,6] for

Pricing of an Exotic Forward Contract

Pricing of an Exotic Forward Contract Jirô Akahori, Yuji Hishida and Maho Nishida Dept. of Mathematical Sciences, Ritsumeikan University 1-1-1 Nojihigashi, Kusatsu, Shiga 525-8577, Japan E-mail: {akahori,

Pricing of an Exotic Forward Contract Jirô Akahori, Yuji Hishida and Maho Nishida Dept. of Mathematical Sciences, Ritsumeikan University 1-1-1 Nojihigashi, Kusatsu, Shiga 525-8577, Japan E-mail: {akahori,

Optimal Consumption and Investment with Asymmetric Long-term/Short-term Capital Gains Taxes

Optimal Consumption and Investment with Asymmetric Long-term/Short-term Capital Gains Taxes Min Dai Hong Liu Yifei Zhong This revision: November 28, 2012 Abstract We propose an optimal consumption and

Optimal Consumption and Investment with Asymmetric Long-term/Short-term Capital Gains Taxes Min Dai Hong Liu Yifei Zhong This revision: November 28, 2012 Abstract We propose an optimal consumption and

CHAPTER IV - BROWNIAN MOTION

CHAPTER IV - BROWNIAN MOTION JOSEPH G. CONLON 1. Construction of Brownian Motion There are two ways in which the idea of a Markov chain on a discrete state space can be generalized: (1) The discrete time

CHAPTER IV - BROWNIAN MOTION JOSEPH G. CONLON 1. Construction of Brownian Motion There are two ways in which the idea of a Markov chain on a discrete state space can be generalized: (1) The discrete time

Lecture 24: Market Microstructure Steven Skiena. http://www.cs.sunysb.edu/ skiena

Lecture 24: Market Microstructure Steven Skiena Department of Computer Science State University of New York Stony Brook, NY 11794 4400 http://www.cs.sunysb.edu/ skiena Types of Buy/Sell Orders Brokers

Lecture 24: Market Microstructure Steven Skiena Department of Computer Science State University of New York Stony Brook, NY 11794 4400 http://www.cs.sunysb.edu/ skiena Types of Buy/Sell Orders Brokers

Valuation and Optimal Decision for Perpetual American Employee Stock Options under a Constrained Viscosity Solution Framework

Valuation and Optimal Decision for Perpetual American Employee Stock Options under a Constrained Viscosity Solution Framework Quan Yuan Joint work with Shuntai Hu, Baojun Bian Email: candy5191@163.com

Valuation and Optimal Decision for Perpetual American Employee Stock Options under a Constrained Viscosity Solution Framework Quan Yuan Joint work with Shuntai Hu, Baojun Bian Email: candy5191@163.com

Lecture 13: Martingales

Lecture 13: Martingales 1. Definition of a Martingale 1.1 Filtrations 1.2 Definition of a martingale and its basic properties 1.3 Sums of independent random variables and related models 1.4 Products of

Lecture 13: Martingales 1. Definition of a Martingale 1.1 Filtrations 1.2 Definition of a martingale and its basic properties 1.3 Sums of independent random variables and related models 1.4 Products of

Detection of changes in variance using binary segmentation and optimal partitioning

Detection of changes in variance using binary segmentation and optimal partitioning Christian Rohrbeck Abstract This work explores the performance of binary segmentation and optimal partitioning in the

Detection of changes in variance using binary segmentation and optimal partitioning Christian Rohrbeck Abstract This work explores the performance of binary segmentation and optimal partitioning in the

A Tutorial Introduction to Financial Engineering

A Tutorial Introduction to Financial Engineering M. Vidyasagar Tata Consultancy Services Ltd. No. 1, Software Units Layout, Madhapur Hyderabad 500081, INDIA sagar@atc.tcs.com Abstract In this paper we

A Tutorial Introduction to Financial Engineering M. Vidyasagar Tata Consultancy Services Ltd. No. 1, Software Units Layout, Madhapur Hyderabad 500081, INDIA sagar@atc.tcs.com Abstract In this paper we

Functional Optimization Models for Active Queue Management

Functional Optimization Models for Active Queue Management Yixin Chen Department of Computer Science and Engineering Washington University in St Louis 1 Brookings Drive St Louis, MO 63130, USA chen@cse.wustl.edu

Functional Optimization Models for Active Queue Management Yixin Chen Department of Computer Science and Engineering Washington University in St Louis 1 Brookings Drive St Louis, MO 63130, USA chen@cse.wustl.edu

Applied Stochastic Control in High Frequency and Algorithmic Trading. Jason Ricci

Applied Stochastic Control in High Frequency and Algorithmic Trading by Jason Ricci A thesis submitted in conformity with the requirements for the degree of Doctor of Philosophy Graduate Department of

Applied Stochastic Control in High Frequency and Algorithmic Trading by Jason Ricci A thesis submitted in conformity with the requirements for the degree of Doctor of Philosophy Graduate Department of

ST 371 (IV): Discrete Random Variables

: Discrete Random Variables") ST 371 (IV): Discrete Random Variables 1 Random Variables A random variable (rv) is a function that is defined on the sample space of the experiment and that assigns a numerical variable to each possible

ST 371 (IV): Discrete Random Variables 1 Random Variables A random variable (rv) is a function that is defined on the sample space of the experiment and that assigns a numerical variable to each possible

Buy Low Sell High: a High Frequency Trading Perspective

Buy Low Sell High: a High Frequency Trading Perspective Álvaro Cartea a, Sebastian Jaimungal b, Jason Ricci b a Department of Mathematics, University College London, UK b Department of Statistics, University

Buy Low Sell High: a High Frequency Trading Perspective Álvaro Cartea a, Sebastian Jaimungal b, Jason Ricci b a Department of Mathematics, University College London, UK b Department of Statistics, University

Energy Management and Profit Maximization of Green Data Centers

Energy Management and Profit Maximization of Green Data Centers Seyed Mahdi Ghamkhari, B.S. A Thesis Submitted to Graduate Faculty of Texas Tech University in Partial Fulfilment of the Requirements for

Energy Management and Profit Maximization of Green Data Centers Seyed Mahdi Ghamkhari, B.S. A Thesis Submitted to Graduate Faculty of Texas Tech University in Partial Fulfilment of the Requirements for

RANDOM INTERVAL HOMEOMORPHISMS. MICHA L MISIUREWICZ Indiana University Purdue University Indianapolis

RANDOM INTERVAL HOMEOMORPHISMS MICHA L MISIUREWICZ Indiana University Purdue University Indianapolis This is a joint work with Lluís Alsedà Motivation: A talk by Yulij Ilyashenko. Two interval maps, applied

RANDOM INTERVAL HOMEOMORPHISMS MICHA L MISIUREWICZ Indiana University Purdue University Indianapolis This is a joint work with Lluís Alsedà Motivation: A talk by Yulij Ilyashenko. Two interval maps, applied

Black-Scholes Equation for Option Pricing

Black-Scholes Equation for Option Pricing By Ivan Karmazin, Jiacong Li 1. Introduction In early 1970s, Black, Scholes and Merton achieved a major breakthrough in pricing of European stock options and there

Black-Scholes Equation for Option Pricing By Ivan Karmazin, Jiacong Li 1. Introduction In early 1970s, Black, Scholes and Merton achieved a major breakthrough in pricing of European stock options and there

Optimal Trade Execution: A Mean Quadratic-Variation Approach

1 2 3 Optimal Trade Execution: A Mean Quadratic-Variation Approach P.A. Forsyth J.S. Kennedy S. T. Tse H. Windcliff September 25, 211 4 5 6 7 8 9 1 11 12 13 14 Abstract We propose the use of a mean quadratic-variation

1 2 3 Optimal Trade Execution: A Mean Quadratic-Variation Approach P.A. Forsyth J.S. Kennedy S. T. Tse H. Windcliff September 25, 211 4 5 6 7 8 9 1 11 12 13 14 Abstract We propose the use of a mean quadratic-variation

Development and Usage of Short Term Signals in Order Execution

Development and Usage of Short Term Signals in Order Execution Michael G Sotiropoulos Algorithmic Trading Quantitative Research Cornell Financial Engineering Seminar New York, 10-Oct-2012 M.G.Sotiropoulos,

Development and Usage of Short Term Signals in Order Execution Michael G Sotiropoulos Algorithmic Trading Quantitative Research Cornell Financial Engineering Seminar New York, 10-Oct-2012 M.G.Sotiropoulos,

Pacific Journal of Mathematics

Pacific Journal of Mathematics GLOBAL EXISTENCE AND DECREASING PROPERTY OF BOUNDARY VALUES OF SOLUTIONS TO PARABOLIC EQUATIONS WITH NONLOCAL BOUNDARY CONDITIONS Sangwon Seo Volume 193 No. 1 March 2000

Pacific Journal of Mathematics GLOBAL EXISTENCE AND DECREASING PROPERTY OF BOUNDARY VALUES OF SOLUTIONS TO PARABOLIC EQUATIONS WITH NONLOCAL BOUNDARY CONDITIONS Sangwon Seo Volume 193 No. 1 March 2000

Quantitative Challenges in Algorithmic Execution

Quantitative Challenges in Algorithmic Execution Robert Almgren Quantitative Brokers and NYU Feb 2009 Sell-side (broker) viewpoint "Flow" business no pricing computations use for standardized exchange-traded

Quantitative Challenges in Algorithmic Execution Robert Almgren Quantitative Brokers and NYU Feb 2009 Sell-side (broker) viewpoint "Flow" business no pricing computations use for standardized exchange-traded

Modeling the Implied Volatility Surface. Jim Gatheral Stanford Financial Mathematics Seminar February 28, 2003

Modeling the Implied Volatility Surface Jim Gatheral Stanford Financial Mathematics Seminar February 28, 2003 This presentation represents only the personal opinions of the author and not those of Merrill

Modeling the Implied Volatility Surface Jim Gatheral Stanford Financial Mathematics Seminar February 28, 2003 This presentation represents only the personal opinions of the author and not those of Merrill

Hedging. An Undergraduate Introduction to Financial Mathematics. J. Robert Buchanan. J. Robert Buchanan Hedging

Hedging An Undergraduate Introduction to Financial Mathematics J. Robert Buchanan 2010 Introduction Definition Hedging is the practice of making a portfolio of investments less sensitive to changes in

Hedging An Undergraduate Introduction to Financial Mathematics J. Robert Buchanan 2010 Introduction Definition Hedging is the practice of making a portfolio of investments less sensitive to changes in

Financial Mathematics and Simulation MATH 6740 1 Spring 2011 Homework 2

Financial Mathematics and Simulation MATH 6740 1 Spring 2011 Homework 2 Due Date: Friday, March 11 at 5:00 PM This homework has 170 points plus 20 bonus points available but, as always, homeworks are graded

Financial Mathematics and Simulation MATH 6740 1 Spring 2011 Homework 2 Due Date: Friday, March 11 at 5:00 PM This homework has 170 points plus 20 bonus points available but, as always, homeworks are graded

Probability Generating Functions

page 39 Chapter 3 Probability Generating Functions 3 Preamble: Generating Functions Generating functions are widely used in mathematics, and play an important role in probability theory Consider a sequence

page 39 Chapter 3 Probability Generating Functions 3 Preamble: Generating Functions Generating functions are widely used in mathematics, and play an important role in probability theory Consider a sequence

EXAM 3, FALL 003 Please note: On a one-time basis, the CAS is releasing annotated solutions to Fall 003 Examination 3 as a study aid to candidates. It is anticipated that for future sittings, only the

EXAM 3, FALL 003 Please note: On a one-time basis, the CAS is releasing annotated solutions to Fall 003 Examination 3 as a study aid to candidates. It is anticipated that for future sittings, only the

A Martingale System Theorem for Stock Investments

A Martingale System Theorem for Stock Investments Robert J. Vanderbei April 26, 1999 DIMACS New Market Models Workshop 1 Beginning Middle End Controversial Remarks Outline DIMACS New Market Models Workshop

A Martingale System Theorem for Stock Investments Robert J. Vanderbei April 26, 1999 DIMACS New Market Models Workshop 1 Beginning Middle End Controversial Remarks Outline DIMACS New Market Models Workshop

The continuous and discrete Fourier transforms

FYSA21 Mathematical Tools in Science The continuous and discrete Fourier transforms Lennart Lindegren Lund Observatory (Department of Astronomy, Lund University) 1 The continuous Fourier transform 1.1

FYSA21 Mathematical Tools in Science The continuous and discrete Fourier transforms Lennart Lindegren Lund Observatory (Department of Astronomy, Lund University) 1 The continuous Fourier transform 1.1

Practice Problems for Homework #6. Normal distribution and Central Limit Theorem.

Practice Problems for Homework #6. Normal distribution and Central Limit Theorem. 1. Read Section 3.4.6 about the Normal distribution and Section 4.7 about the Central Limit Theorem. 2. Solve the practice

Practice Problems for Homework #6. Normal distribution and Central Limit Theorem. 1. Read Section 3.4.6 about the Normal distribution and Section 4.7 about the Central Limit Theorem. 2. Solve the practice

A note on the distribution of the aggregate claim amount at ruin

A note on the distribution of the aggregate claim amount at ruin Jingchao Li, David C M Dickson, Shuanming Li Centre for Actuarial Studies, Department of Economics, University of Melbourne, VIC 31, Australia

A note on the distribution of the aggregate claim amount at ruin Jingchao Li, David C M Dickson, Shuanming Li Centre for Actuarial Studies, Department of Economics, University of Melbourne, VIC 31, Australia

VALUATION IN DERIVATIVES MARKETS

VALUATION IN DERIVATIVES MARKETS September 2005 Rawle Parris ABN AMRO Property Derivatives What is a Derivative? A contract that specifies the rights and obligations between two parties to receive or deliver

VALUATION IN DERIVATIVES MARKETS September 2005 Rawle Parris ABN AMRO Property Derivatives What is a Derivative? A contract that specifies the rights and obligations between two parties to receive or deliver

1 = (a 0 + b 0 α) 2 + + (a m 1 + b m 1 α) 2. for certain elements a 0,..., a m 1, b 0,..., b m 1 of F. Multiplying out, we obtain

2 + + (a m 1 + b m 1 α) 2. for certain elements a 0,..., a m 1, b 0,..., b m 1 of F. Multiplying out, we obtain") Notes on real-closed fields These notes develop the algebraic background needed to understand the model theory of real-closed fields. To understand these notes, a standard graduate course in algebra is

Notes on real-closed fields These notes develop the algebraic background needed to understand the model theory of real-closed fields. To understand these notes, a standard graduate course in algebra is

Exploratory Data Analysis

Exploratory Data Analysis Johannes Schauer johannes.schauer@tugraz.at Institute of Statistics Graz University of Technology Steyrergasse 17/IV, 8010 Graz www.statistics.tugraz.at February 12, 2008 Introduction

Exploratory Data Analysis Johannes Schauer johannes.schauer@tugraz.at Institute of Statistics Graz University of Technology Steyrergasse 17/IV, 8010 Graz www.statistics.tugraz.at February 12, 2008 Introduction

Notes from Week 1: Algorithms for sequential prediction

CS 683 Learning, Games, and Electronic Markets Spring 2007 Notes from Week 1: Algorithms for sequential prediction Instructor: Robert Kleinberg 22-26 Jan 2007 1 Introduction In this course we will be looking

CS 683 Learning, Games, and Electronic Markets Spring 2007 Notes from Week 1: Algorithms for sequential prediction Instructor: Robert Kleinberg 22-26 Jan 2007 1 Introduction In this course we will be looking

Optimal shift scheduling with a global service level constraint

Optimal shift scheduling with a global service level constraint Ger Koole & Erik van der Sluis Vrije Universiteit Division of Mathematics and Computer Science De Boelelaan 1081a, 1081 HV Amsterdam The

Optimal shift scheduling with a global service level constraint Ger Koole & Erik van der Sluis Vrije Universiteit Division of Mathematics and Computer Science De Boelelaan 1081a, 1081 HV Amsterdam The

Multiple Kernel Learning on the Limit Order Book

JMLR: Workshop and Conference Proceedings 11 (2010) 167 174 Workshop on Applications of Pattern Analysis Multiple Kernel Learning on the Limit Order Book Tristan Fletcher Zakria Hussain John Shawe-Taylor

JMLR: Workshop and Conference Proceedings 11 (2010) 167 174 Workshop on Applications of Pattern Analysis Multiple Kernel Learning on the Limit Order Book Tristan Fletcher Zakria Hussain John Shawe-Taylor

Polarization codes and the rate of polarization

Polarization codes and the rate of polarization Erdal Arıkan, Emre Telatar Bilkent U., EPFL Sept 10, 2008 Channel Polarization Given a binary input DMC W, i.i.d. uniformly distributed inputs (X 1,...,

Polarization codes and the rate of polarization Erdal Arıkan, Emre Telatar Bilkent U., EPFL Sept 10, 2008 Channel Polarization Given a binary input DMC W, i.i.d. uniformly distributed inputs (X 1,...,

An Incomplete Market Approach to Employee Stock Option Valuation

An Incomplete Market Approach to Employee Stock Option Valuation Kamil Kladívko Department of Statistics, University of Economics, Prague Department of Finance, Norwegian School of Economics, Bergen Mihail

An Incomplete Market Approach to Employee Stock Option Valuation Kamil Kladívko Department of Statistics, University of Economics, Prague Department of Finance, Norwegian School of Economics, Bergen Mihail

COMPLETE MARKETS DO NOT ALLOW FREE CASH FLOW STREAMS

COMPLETE MARKETS DO NOT ALLOW FREE CASH FLOW STREAMS NICOLE BÄUERLE AND STEFANIE GRETHER Abstract. In this short note we prove a conjecture posed in Cui et al. 2012): Dynamic mean-variance problems in

COMPLETE MARKETS DO NOT ALLOW FREE CASH FLOW STREAMS NICOLE BÄUERLE AND STEFANIE GRETHER Abstract. In this short note we prove a conjecture posed in Cui et al. 2012): Dynamic mean-variance problems in

Optimal trading? In what sense?

Optimal trading? In what sense? Market Microstructure in Practice 3/3 Charles-Albert Lehalle Senior Research Advisor, Capital Fund Management, Paris April 2015, Printed the April 13, 2015 CA Lehalle 1

Optimal trading? In what sense? Market Microstructure in Practice 3/3 Charles-Albert Lehalle Senior Research Advisor, Capital Fund Management, Paris April 2015, Printed the April 13, 2015 CA Lehalle 1

Algorithms for VWAP and Limit Order Trading

Algorithms for VWAP and Limit Order Trading Sham Kakade TTI (Toyota Technology Institute) Collaborators: Michael Kearns, Yishay Mansour, Luis Ortiz Technological Revolutions in Financial Markets Competition

Algorithms for VWAP and Limit Order Trading Sham Kakade TTI (Toyota Technology Institute) Collaborators: Michael Kearns, Yishay Mansour, Luis Ortiz Technological Revolutions in Financial Markets Competition

Execution Costs. Post-trade reporting. December 17, 2008 Robert Almgren / Encyclopedia of Quantitative Finance Execution Costs 1

December 17, 2008 Robert Almgren / Encyclopedia of Quantitative Finance Execution Costs 1 Execution Costs Execution costs are the difference in value between an ideal trade and what was actually done.

December 17, 2008 Robert Almgren / Encyclopedia of Quantitative Finance Execution Costs 1 Execution Costs Execution costs are the difference in value between an ideal trade and what was actually done.

Math 526: Brownian Motion Notes

Math 526: Brownian Motion Notes Definition. Mike Ludkovski, 27, all rights reserved. A stochastic process (X t ) is called Brownian motion if:. The map t X t (ω) is continuous for every ω. 2. (X t X t

Math 526: Brownian Motion Notes Definition. Mike Ludkovski, 27, all rights reserved. A stochastic process (X t ) is called Brownian motion if:. The map t X t (ω) is continuous for every ω. 2. (X t X t

Does Black-Scholes framework for Option Pricing use Constant Volatilities and Interest Rates? New Solution for a New Problem

Does Black-Scholes framework for Option Pricing use Constant Volatilities and Interest Rates? New Solution for a New Problem Gagan Deep Singh Assistant Vice President Genpact Smart Decision Services Financial

Does Black-Scholes framework for Option Pricing use Constant Volatilities and Interest Rates? New Solution for a New Problem Gagan Deep Singh Assistant Vice President Genpact Smart Decision Services Financial

Safety margins for unsystematic biometric risk in life and health insurance

Safety margins for unsystematic biometric risk in life and health insurance Marcus C. Christiansen June 1, 2012 7th Conference in Actuarial Science & Finance on Samos Seite 2 Safety margins for unsystematic

Safety margins for unsystematic biometric risk in life and health insurance Marcus C. Christiansen June 1, 2012 7th Conference in Actuarial Science & Finance on Samos Seite 2 Safety margins for unsystematic

Behind Stock Price Movement: Supply and Demand in Market Microstructure and Market Influence SUMMER 2015 V O LUME10NUMBER3 WWW.IIJOT.

WWW.IIJOT.COM OT SUMMER 2015 V O LUME10NUMBER3 The Voices of Influence iijournals.com Behind Stock Price Movement: Supply and Demand in Market Microstructure and Market Influence JINGLE LIU AND SANGHYUN

WWW.IIJOT.COM OT SUMMER 2015 V O LUME10NUMBER3 The Voices of Influence iijournals.com Behind Stock Price Movement: Supply and Demand in Market Microstructure and Market Influence JINGLE LIU AND SANGHYUN

Pricing of Limit Orders in the Electronic Security Trading System Xetra

Pricing of Limit Orders in the Electronic Security Trading System Xetra Li Xihao Bielefeld Graduate School of Economics and Management Bielefeld University, P.O. Box 100 131 D-33501 Bielefeld, Germany

Pricing of Limit Orders in the Electronic Security Trading System Xetra Li Xihao Bielefeld Graduate School of Economics and Management Bielefeld University, P.O. Box 100 131 D-33501 Bielefeld, Germany

arxiv:1112.0829v1 [math.pr] 5 Dec 2011

![arxiv:1112.0829v1 [math.pr] 5 Dec 2011](/thumbs/39/18839218.jpg "arxiv:1112.0829v1 [math.pr] 5 Dec 2011") How Not to Win a Million Dollars: A Counterexample to a Conjecture of L. Breiman Thomas P. Hayes arxiv:1112.0829v1 [math.pr] 5 Dec 2011 Abstract Consider a gambling game in which we are allowed to repeatedly

How Not to Win a Million Dollars: A Counterexample to a Conjecture of L. Breiman Thomas P. Hayes arxiv:1112.0829v1 [math.pr] 5 Dec 2011 Abstract Consider a gambling game in which we are allowed to repeatedly

A Simple Model for Intra-day Trading

A Simple Model for Intra-day Trading Anton Golub 1 1 Marie Curie Fellow, Manchester Business School April 15, 2011 Abstract Since currency market is an OTC market, there is no information about orders,

A Simple Model for Intra-day Trading Anton Golub 1 1 Marie Curie Fellow, Manchester Business School April 15, 2011 Abstract Since currency market is an OTC market, there is no information about orders,

15 Kuhn -Tucker conditions

5 Kuhn -Tucker conditions Consider a version of the consumer problem in which quasilinear utility x 2 + 4 x 2 is maximised subject to x +x 2 =. Mechanically applying the Lagrange multiplier/common slopes

5 Kuhn -Tucker conditions Consider a version of the consumer problem in which quasilinear utility x 2 + 4 x 2 is maximised subject to x +x 2 =. Mechanically applying the Lagrange multiplier/common slopes