Two-State Model of Option Pricing

|

|

|

- Jennifer Carr

- 9 years ago

- Views:

Transcription

1 Rendleman and Bartter [1] put forward a simple two-state model of option pricing. As in the Black-Scholes model, to buy the stock and to sell the call in the hedge ratio obtains a risk-free portfolio. To avoid an opportunity for arbitrage profit, this portfolio must yield the risk-free rate of return, which sets the call price. We analyze an example. 1

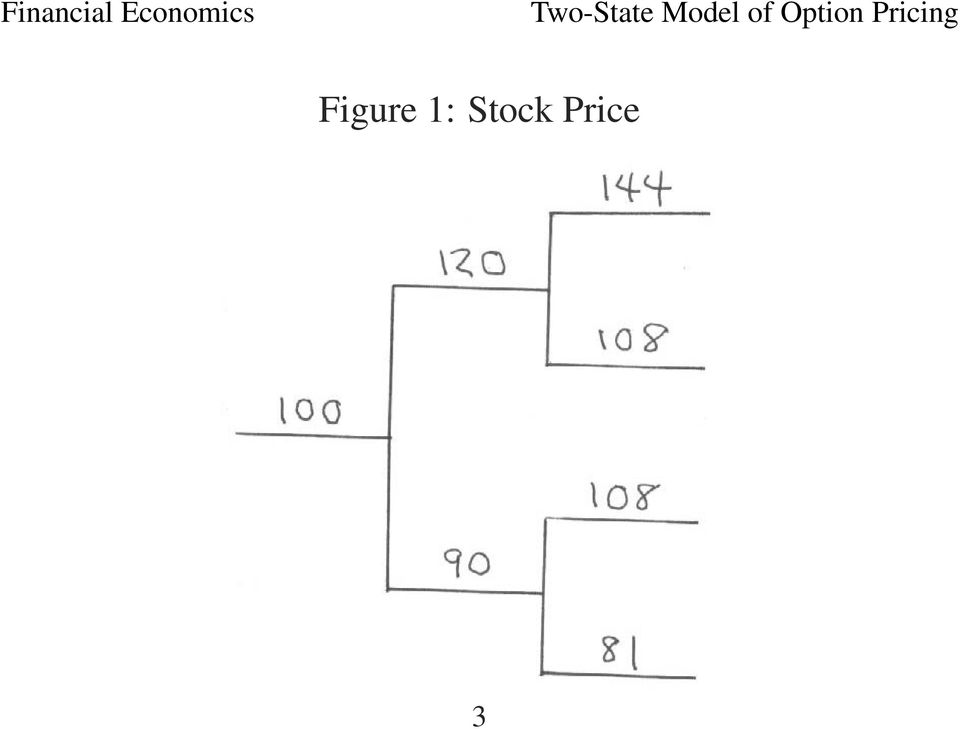

2 Stock Consider a stock such that each period either the price rises by 20% or the price falls by 10%. Let S denote the stock price. Suppose that the initial price in period zero is S = 100. The tree diagram in figure (1) shows the possibilities over two periods. 2

3 Figure 1: Stock Price 3

4 Risk-Free Asset We assume that there exists a risk-free asset exists, with rate-of-return R. For simplicity in the calculations below, assume R = 0: a one-dollar investment is worth just one dollar in the next period. 4

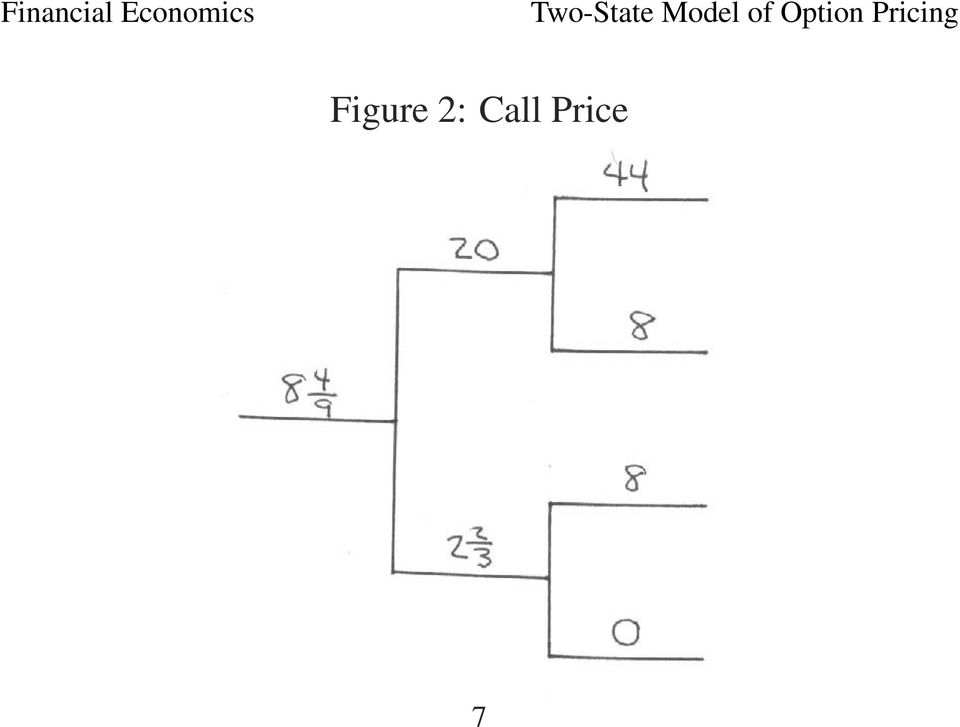

5 Call Consider a call expiring in period two with exercise price 100. Let C denote the call price. The stock price in period two determines the value of the call in period two. If the stock price in period two is 144, then the call price is C = = 44. If the stock price is 108, then the value of the call is C = = 8. If the stock price is 81, then it is not profitable to exercise the call, so its value is zero. 5

6 No Opportunity for Profitable Arbitrage By working backwards in time, we can find the value of the call in the earlier periods. First one finds the two possible call prices in period one. Given these two values, one then finds the call price in period zero. The key to the argument is that from the stock and the call one can create a risk-free portfolio. This portfolio must earn the risk-free rate of return, as otherwise there would be an opportunity for profitable arbitrage. From this condition, one can solve uniquely for the call price. Figure (2) summarizes the results of the calculations explained below. 6

7 Figure 2: Call Price 7

8 Hedge Ratio Suppose that the stock price in period one is 108, and compare the two possibilities in period two. The stock price is either 144 or 108, so the difference is S = = 36. The call price is either 44 or 8, so the difference is C = 44 8 = 36. The hedge ratio is therefore C S = = 1. 8

9 Risk-Free Portfolio Since the hedge ratio is one, to buy one share of the stock and to sell one call obtains a risk-free portfolio. If C is the price of the call in period one, then the cost of the portfolio is 120 C. Let us verify that this portfolio is risk-free. If the stock price in period two is 144, the call price is 44, so the value of the portfolio is = 100. If the stock price in period two is 108, the call price is 8, so the value of the portfolio is =

10 No Arbitrage No opportunity for profitable arbitrage requires that this portfolio yield the risk-free rate of return: (120 C)(1 + R)=100 is the no-arbitrage condition. Since R = 0, therefore C = 20. Any other call price would allow profitable arbitrage. 10

11 Second Possibility in Period One For a stock price of 90 in period one, we work out in the same way the call price in period one. Compare the two possibilities in period two. If the stock price is 108, then the call value is = 8. If the stock price is 81, then it is not profitable to exercise the call, so the call value is zero. 11

12 Hedge Ratio As the stock price is either 108 or 81, the difference is S = = 27. As the call price is either 8 or 0, the difference is C = 8 0 = 8. The hedge ratio is therefore C S =

13 Risk-Free Portfolio Hence to buy stock and to sell calls in the ratio of 8 to 27 obtains a risk-free portfolio. Suppose that one buys one share of stock and sells 27/8 calls. If C is the price of the call in period one, then the cost of the portfolio is 90 (27/8)C. This portfolio is indeed risk-free. If the stock price in period two is 108, the value of the portfolio is 108 (27/8)8 = 81. If the stock price in period two is 81, the value of the portfolio is 81 (27/8)0 =

14 No Arbitrage No opportunity for profitable arbitrage requires that this portfolio yield the risk-free rate of return. Hence [90 (27/8)C](1 + R)=81 is the no-arbitrage condition. Since R = 0, therefore C = Any other call price would allow profitable arbitrage. 14

=81 is the no-arbitrage condition.](/docs-images/48/19193934/images/page_14.jpg "Since R = 0, therefore C = 2 2 3.")

15 Call Price in Period Zero Working backwards, we work out in the same way the call price in period zero, when the stock price is 100. In period one the stock price is either 120 or 90, so the difference is S = = 30. As the call price is either 20 or 2 2 3, the difference is C = = The hedge ratio is therefore C S = =

16 Risk-Free Portfolio Hence to buy stock and to sell calls in the ratio of 26 to 45 obtains a risk-free portfolio. Suppose that one buys one share of stock and sells 45/26 calls. If C is the price of the call in period zero, then the cost of the portfolio is 100 (45/26)C. This portfolio is indeed risk-free. If the stock price in period two is 120, the value of the portfolio is 120 (45/26) 20 = 1110/ If the stock price in period two is 90, the value of the portfolio is 90 (45/26) ( 2 2 3) = 1110/

17 No Arbitrage No opportunity for profitable arbitrage requires that this portfolio yield the risk-free rate of return. Hence [100 (45/26)C](1 + R)= 1110/13 is the no-arbitrage condition. Since R = 0, therefore C = Any other call price would allow profitable arbitrage. 17

= 1110/13 is the no-arbitrage condition.](/docs-images/48/19193934/images/page_17.jpg "Since R = 0, therefore C = 8 4 9.")

18 Changing Hedge Ratio The hedge ratio changes as time passes. 18

19 Comparison with Black-Scholes Note that the probability of each state is irrelevant to the calculations. This property corresponds to how in the Black-Scholes model the expected rate of return on the stock has no effect on the call price. It is possible to obtain the Black-Scholes partial differential equation as the limit of the two-state model, by making the length of the time period shrink to zero. 19

20 References [1] Richard J. Rendleman, Jr. and Brit J. Bartter. Two-state option pricing. Journal of Finance, XXXIV(5): , December HG1J6. 20

:1093")

Two-State Option Pricing

Rendleman and Bartter [1] present a simple two-state model of option pricing. The states of the world evolve like the branches of a tree. Given the current state, there are two possible states next period.

Rendleman and Bartter [1] present a simple two-state model of option pricing. The states of the world evolve like the branches of a tree. Given the current state, there are two possible states next period.

BINOMIAL OPTION PRICING

Darden Graduate School of Business Administration University of Virginia BINOMIAL OPTION PRICING Binomial option pricing is a simple but powerful technique that can be used to solve many complex option-pricing

Darden Graduate School of Business Administration University of Virginia BINOMIAL OPTION PRICING Binomial option pricing is a simple but powerful technique that can be used to solve many complex option-pricing

Call Price as a Function of the Stock Price

Call Price as a Function of the Stock Price Intuitively, the call price should be an increasing function of the stock price. This relationship allows one to develop a theory of option pricing, derived

Call Price as a Function of the Stock Price Intuitively, the call price should be an increasing function of the stock price. This relationship allows one to develop a theory of option pricing, derived

Option Valuation. Chapter 21

Option Valuation Chapter 21 Intrinsic and Time Value intrinsic value of in-the-money options = the payoff that could be obtained from the immediate exercise of the option for a call option: stock price

Option Valuation Chapter 21 Intrinsic and Time Value intrinsic value of in-the-money options = the payoff that could be obtained from the immediate exercise of the option for a call option: stock price

Introduction to Binomial Trees

11 C H A P T E R Introduction to Binomial Trees A useful and very popular technique for pricing an option involves constructing a binomial tree. This is a diagram that represents di erent possible paths

11 C H A P T E R Introduction to Binomial Trees A useful and very popular technique for pricing an option involves constructing a binomial tree. This is a diagram that represents di erent possible paths

Institutional Finance 08: Dynamic Arbitrage to Replicate Non-linear Payoffs. Binomial Option Pricing: Basics (Chapter 10 of McDonald)

") Copyright 2003 Pearson Education, Inc. Slide 08-1 Institutional Finance 08: Dynamic Arbitrage to Replicate Non-linear Payoffs Binomial Option Pricing: Basics (Chapter 10 of McDonald) Originally prepared

Copyright 2003 Pearson Education, Inc. Slide 08-1 Institutional Finance 08: Dynamic Arbitrage to Replicate Non-linear Payoffs Binomial Option Pricing: Basics (Chapter 10 of McDonald) Originally prepared

Options Pricing. This is sometimes referred to as the intrinsic value of the option.

Options Pricing We will use the example of a call option in discussing the pricing issue. Later, we will turn our attention to the Put-Call Parity Relationship. I. Preliminary Material Recall the payoff

Options Pricing We will use the example of a call option in discussing the pricing issue. Later, we will turn our attention to the Put-Call Parity Relationship. I. Preliminary Material Recall the payoff

Part A: The put call parity relation is: call + present value of exercise price = put + stock price.

Corporate Finance Mod 20: Options, put call parity relation, Practice Problem s ** Exercise 20.1: Put Call Parity Relation! One year European put and call options trade on a stock with strike prices of

Corporate Finance Mod 20: Options, put call parity relation, Practice Problem s ** Exercise 20.1: Put Call Parity Relation! One year European put and call options trade on a stock with strike prices of

BUS 316 NOTES AND ANSWERS BINOMIAL OPTION PRICING

BUS 316 NOTES AND ANSWERS BINOMIAL OPTION PRICING 3. Suppose there are only two possible future states of the world. In state 1 the stock price rises by 50%. In state 2, the stock price drops by 25%. The

BUS 316 NOTES AND ANSWERS BINOMIAL OPTION PRICING 3. Suppose there are only two possible future states of the world. In state 1 the stock price rises by 50%. In state 2, the stock price drops by 25%. The

10 Binomial Trees. 10.1 One-step model. 1. Model structure. ECG590I Asset Pricing. Lecture 10: Binomial Trees 1

ECG590I Asset Pricing. Lecture 10: Binomial Trees 1 10 Binomial Trees 10.1 One-step model 1. Model structure ECG590I Asset Pricing. Lecture 10: Binomial Trees 2 There is only one time interval (t 0, t

ECG590I Asset Pricing. Lecture 10: Binomial Trees 1 10 Binomial Trees 10.1 One-step model 1. Model structure ECG590I Asset Pricing. Lecture 10: Binomial Trees 2 There is only one time interval (t 0, t

Overview. Option Basics. Options and Derivatives. Professor Lasse H. Pedersen. Option basics and option strategies

Options and Derivatives Professor Lasse H. Pedersen Prof. Lasse H. Pedersen 1 Overview Option basics and option strategies No-arbitrage bounds on option prices Binomial option pricing Black-Scholes-Merton

Options and Derivatives Professor Lasse H. Pedersen Prof. Lasse H. Pedersen 1 Overview Option basics and option strategies No-arbitrage bounds on option prices Binomial option pricing Black-Scholes-Merton

a. What is the portfolio of the stock and the bond that replicates the option?

Practice problems for Lecture 2. Answers. 1. A Simple Option Pricing Problem in One Period Riskless bond (interest rate is 5%): 1 15 Stock: 5 125 5 Derivative security (call option with a strike of 8):?

Practice problems for Lecture 2. Answers. 1. A Simple Option Pricing Problem in One Period Riskless bond (interest rate is 5%): 1 15 Stock: 5 125 5 Derivative security (call option with a strike of 8):?

One Period Binomial Model

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 One Period Binomial Model These notes consider the one period binomial model to exactly price an option. We will consider three different methods of pricing

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 One Period Binomial Model These notes consider the one period binomial model to exactly price an option. We will consider three different methods of pricing

Chapter 11 Options. Main Issues. Introduction to Options. Use of Options. Properties of Option Prices. Valuation Models of Options.

Chapter 11 Options Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. Part C Determination of risk-adjusted discount rate. Part D Introduction to derivatives. Forwards

Chapter 11 Options Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. Part C Determination of risk-adjusted discount rate. Part D Introduction to derivatives. Forwards

Lecture 12: The Black-Scholes Model Steven Skiena. http://www.cs.sunysb.edu/ skiena

Lecture 12: The Black-Scholes Model Steven Skiena Department of Computer Science State University of New York Stony Brook, NY 11794 4400 http://www.cs.sunysb.edu/ skiena The Black-Scholes-Merton Model

Lecture 12: The Black-Scholes Model Steven Skiena Department of Computer Science State University of New York Stony Brook, NY 11794 4400 http://www.cs.sunysb.edu/ skiena The Black-Scholes-Merton Model

Option Values. Determinants of Call Option Values. CHAPTER 16 Option Valuation. Figure 16.1 Call Option Value Before Expiration

CHAPTER 16 Option Valuation 16.1 OPTION VALUATION: INTRODUCTION Option Values Intrinsic value - profit that could be made if the option was immediately exercised Call: stock price - exercise price Put:

CHAPTER 16 Option Valuation 16.1 OPTION VALUATION: INTRODUCTION Option Values Intrinsic value - profit that could be made if the option was immediately exercised Call: stock price - exercise price Put:

Lecture 6: Option Pricing Using a One-step Binomial Tree. Friday, September 14, 12

Lecture 6: Option Pricing Using a One-step Binomial Tree An over-simplified model with surprisingly general extensions a single time step from 0 to T two types of traded securities: stock S and a bond

Lecture 6: Option Pricing Using a One-step Binomial Tree An over-simplified model with surprisingly general extensions a single time step from 0 to T two types of traded securities: stock S and a bond

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 Options These notes consider the way put and call options and the underlying can be combined to create hedges, spreads and combinations. We will consider the

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 Options These notes consider the way put and call options and the underlying can be combined to create hedges, spreads and combinations. We will consider the

Option pricing. Vinod Kothari

Option pricing Vinod Kothari Notation we use this Chapter will be as follows: S o : Price of the share at time 0 S T : Price of the share at time T T : time to maturity of the option r : risk free rate

Option pricing Vinod Kothari Notation we use this Chapter will be as follows: S o : Price of the share at time 0 S T : Price of the share at time T T : time to maturity of the option r : risk free rate

Lecture 17/18/19 Options II

1 Lecture 17/18/19 Options II Alexander K. Koch Department of Economics, Royal Holloway, University of London February 25, February 29, and March 10 2008 In addition to learning the material covered in

1 Lecture 17/18/19 Options II Alexander K. Koch Department of Economics, Royal Holloway, University of London February 25, February 29, and March 10 2008 In addition to learning the material covered in

On Black-Scholes Equation, Black- Scholes Formula and Binary Option Price

On Black-Scholes Equation, Black- Scholes Formula and Binary Option Price Abstract: Chi Gao 12/15/2013 I. Black-Scholes Equation is derived using two methods: (1) risk-neutral measure; (2) - hedge. II.

On Black-Scholes Equation, Black- Scholes Formula and Binary Option Price Abstract: Chi Gao 12/15/2013 I. Black-Scholes Equation is derived using two methods: (1) risk-neutral measure; (2) - hedge. II.

Determination of Forward and Futures Prices. Chapter 5

Determination of Forward and Futures Prices Chapter 5 Fundamentals of Futures and Options Markets, 8th Ed, Ch 5, Copyright John C. Hull 2013 1 Consumption vs Investment Assets Investment assets are assets

Determination of Forward and Futures Prices Chapter 5 Fundamentals of Futures and Options Markets, 8th Ed, Ch 5, Copyright John C. Hull 2013 1 Consumption vs Investment Assets Investment assets are assets

CHAPTER 11: ARBITRAGE PRICING THEORY

CHAPTER 11: ARBITRAGE PRICING THEORY 1. The revised estimate of the expected rate of return on the stock would be the old estimate plus the sum of the products of the unexpected change in each factor times

CHAPTER 11: ARBITRAGE PRICING THEORY 1. The revised estimate of the expected rate of return on the stock would be the old estimate plus the sum of the products of the unexpected change in each factor times

Call and Put. Options. American and European Options. Option Terminology. Payoffs of European Options. Different Types of Options

Call and Put Options A call option gives its holder the right to purchase an asset for a specified price, called the strike price, on or before some specified expiration date. A put option gives its holder

Call and Put Options A call option gives its holder the right to purchase an asset for a specified price, called the strike price, on or before some specified expiration date. A put option gives its holder

Lecture 7: Bounds on Options Prices Steven Skiena. http://www.cs.sunysb.edu/ skiena

Lecture 7: Bounds on Options Prices Steven Skiena Department of Computer Science State University of New York Stony Brook, NY 11794 4400 http://www.cs.sunysb.edu/ skiena Option Price Quotes Reading the

Lecture 7: Bounds on Options Prices Steven Skiena Department of Computer Science State University of New York Stony Brook, NY 11794 4400 http://www.cs.sunysb.edu/ skiena Option Price Quotes Reading the

Computational Finance Options

1 Options 1 1 Options Computational Finance Options An option gives the holder of the option the right, but not the obligation to do something. Conversely, if you sell an option, you may be obliged to

1 Options 1 1 Options Computational Finance Options An option gives the holder of the option the right, but not the obligation to do something. Conversely, if you sell an option, you may be obliged to

Options. + Concepts and Buzzwords. Readings. Put-Call Parity Volatility Effects

+ Options + Concepts and Buzzwords Put-Call Parity Volatility Effects Call, put, European, American, underlying asset, strike price, expiration date Readings Tuckman, Chapter 19 Veronesi, Chapter 6 Options

+ Options + Concepts and Buzzwords Put-Call Parity Volatility Effects Call, put, European, American, underlying asset, strike price, expiration date Readings Tuckman, Chapter 19 Veronesi, Chapter 6 Options

CHAPTER 7: PROPERTIES OF STOCK OPTION PRICES

CHAPER 7: PROPERIES OF SOCK OPION PRICES 7.1 Factors Affecting Option Prices able 7.1 Summary of the Effect on the Price of a Stock Option of Increasing One Variable While Keeping All Other Fixed Variable

CHAPER 7: PROPERIES OF SOCK OPION PRICES 7.1 Factors Affecting Option Prices able 7.1 Summary of the Effect on the Price of a Stock Option of Increasing One Variable While Keeping All Other Fixed Variable

Two-State Options. John Norstad. [email protected] http://www.norstad.org. January 12, 1999 Updated: November 3, 2011.

Two-State Options John Norstad [email protected] http://www.norstad.org January 12, 1999 Updated: November 3, 2011 Abstract How options are priced when the underlying asset has only two possible

Two-State Options John Norstad [email protected] http://www.norstad.org January 12, 1999 Updated: November 3, 2011 Abstract How options are priced when the underlying asset has only two possible

Example 1. Consider the following two portfolios: 2. Buy one c(s(t), 20, τ, r) and sell one c(s(t), 10, τ, r).

, 20, τ, r) and sell one c(s(t), 10, τ, r).") Chapter 4 Put-Call Parity 1 Bull and Bear Financial analysts use words such as bull and bear to describe the trend in stock markets. Generally speaking, a bull market is characterized by rising prices.

Chapter 4 Put-Call Parity 1 Bull and Bear Financial analysts use words such as bull and bear to describe the trend in stock markets. Generally speaking, a bull market is characterized by rising prices.

Figure S9.1 Profit from long position in Problem 9.9

Problem 9.9 Suppose that a European call option to buy a share for $100.00 costs $5.00 and is held until maturity. Under what circumstances will the holder of the option make a profit? Under what circumstances

Problem 9.9 Suppose that a European call option to buy a share for $100.00 costs $5.00 and is held until maturity. Under what circumstances will the holder of the option make a profit? Under what circumstances

1 Introduction to Option Pricing

ESTM 60202: Financial Mathematics Alex Himonas 03 Lecture Notes 1 October 7, 2009 1 Introduction to Option Pricing We begin by defining the needed finance terms. Stock is a certificate of ownership of

ESTM 60202: Financial Mathematics Alex Himonas 03 Lecture Notes 1 October 7, 2009 1 Introduction to Option Pricing We begin by defining the needed finance terms. Stock is a certificate of ownership of

CHAPTER 21: OPTION VALUATION

CHAPTER 21: OPTION VALUATION 1. Put values also must increase as the volatility of the underlying stock increases. We see this from the parity relation as follows: P = C + PV(X) S 0 + PV(Dividends). Given

CHAPTER 21: OPTION VALUATION 1. Put values also must increase as the volatility of the underlying stock increases. We see this from the parity relation as follows: P = C + PV(X) S 0 + PV(Dividends). Given

Chapter 5 Financial Forwards and Futures

Chapter 5 Financial Forwards and Futures Question 5.1. Four different ways to sell a share of stock that has a price S(0) at time 0. Question 5.2. Description Get Paid at Lose Ownership of Receive Payment

Chapter 5 Financial Forwards and Futures Question 5.1. Four different ways to sell a share of stock that has a price S(0) at time 0. Question 5.2. Description Get Paid at Lose Ownership of Receive Payment

Use the option quote information shown below to answer the following questions. The underlying stock is currently selling for $83.

Problems on the Basics of Options used in Finance 2. Understanding Option Quotes Use the option quote information shown below to answer the following questions. The underlying stock is currently selling

Problems on the Basics of Options used in Finance 2. Understanding Option Quotes Use the option quote information shown below to answer the following questions. The underlying stock is currently selling

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008. Options

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 Options These notes describe the payoffs to European and American put and call options the so-called plain vanilla options. We consider the payoffs to these

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 Options These notes describe the payoffs to European and American put and call options the so-called plain vanilla options. We consider the payoffs to these

Pricing Forwards and Swaps

Chapter 7 Pricing Forwards and Swaps 7. Forwards Throughout this chapter, we will repeatedly use the following property of no-arbitrage: P 0 (αx T +βy T ) = αp 0 (x T )+βp 0 (y T ). Here, P 0 (w T ) is

Chapter 7 Pricing Forwards and Swaps 7. Forwards Throughout this chapter, we will repeatedly use the following property of no-arbitrage: P 0 (αx T +βy T ) = αp 0 (x T )+βp 0 (y T ). Here, P 0 (w T ) is

Exam MFE Spring 2007 FINAL ANSWER KEY 1 B 2 A 3 C 4 E 5 D 6 C 7 E 8 C 9 A 10 B 11 D 12 A 13 E 14 E 15 C 16 D 17 B 18 A 19 D

Exam MFE Spring 2007 FINAL ANSWER KEY Question # Answer 1 B 2 A 3 C 4 E 5 D 6 C 7 E 8 C 9 A 10 B 11 D 12 A 13 E 14 E 15 C 16 D 17 B 18 A 19 D **BEGINNING OF EXAMINATION** ACTUARIAL MODELS FINANCIAL ECONOMICS

Exam MFE Spring 2007 FINAL ANSWER KEY Question # Answer 1 B 2 A 3 C 4 E 5 D 6 C 7 E 8 C 9 A 10 B 11 D 12 A 13 E 14 E 15 C 16 D 17 B 18 A 19 D **BEGINNING OF EXAMINATION** ACTUARIAL MODELS FINANCIAL ECONOMICS

SOLUTION1. exercise 1

exercise 1 Stock BBB has a spot price equal to 80$ and a dividend equal to 10$ will be paid in 5 months. The on year interest rate is equal to 8% (c.c). 1. Calculate the 6 month forward price? 2. Calculate

exercise 1 Stock BBB has a spot price equal to 80$ and a dividend equal to 10$ will be paid in 5 months. The on year interest rate is equal to 8% (c.c). 1. Calculate the 6 month forward price? 2. Calculate

TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II + III

SOLUTIONS RE-EXAMS 2014 II + III") TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II III Instructions 1. Only one problem should be treated on each sheet of paper and only one side of the sheet should be used. 2. The solutions folder

TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II III Instructions 1. Only one problem should be treated on each sheet of paper and only one side of the sheet should be used. 2. The solutions folder

On Market-Making and Delta-Hedging

On Market-Making and Delta-Hedging 1 Market Makers 2 Market-Making and Bond-Pricing On Market-Making and Delta-Hedging 1 Market Makers 2 Market-Making and Bond-Pricing What to market makers do? Provide

On Market-Making and Delta-Hedging 1 Market Makers 2 Market-Making and Bond-Pricing On Market-Making and Delta-Hedging 1 Market Makers 2 Market-Making and Bond-Pricing What to market makers do? Provide

How To Price A Call Option

Now by Itô s formula But Mu f and u g in Ū. Hence τ θ u(x) =E( Mu(X) ds + u(x(τ θ))) 0 τ θ u(x) E( f(x) ds + g(x(τ θ))) = J x (θ). 0 But since u(x) =J x (θ ), we consequently have u(x) =J x (θ ) = min

Now by Itô s formula But Mu f and u g in Ū. Hence τ θ u(x) =E( Mu(X) ds + u(x(τ θ))) 0 τ θ u(x) E( f(x) ds + g(x(τ θ))) = J x (θ). 0 But since u(x) =J x (θ ), we consequently have u(x) =J x (θ ) = min

Trading Strategies Involving Options. Chapter 11

Trading Strategies Involving Options Chapter 11 1 Strategies to be Considered A risk-free bond and an option to create a principal-protected note A stock and an option Two or more options of the same type

Trading Strategies Involving Options Chapter 11 1 Strategies to be Considered A risk-free bond and an option to create a principal-protected note A stock and an option Two or more options of the same type

Does Black-Scholes framework for Option Pricing use Constant Volatilities and Interest Rates? New Solution for a New Problem

Does Black-Scholes framework for Option Pricing use Constant Volatilities and Interest Rates? New Solution for a New Problem Gagan Deep Singh Assistant Vice President Genpact Smart Decision Services Financial

Does Black-Scholes framework for Option Pricing use Constant Volatilities and Interest Rates? New Solution for a New Problem Gagan Deep Singh Assistant Vice President Genpact Smart Decision Services Financial

Session X: Lecturer: Dr. Jose Olmo. Module: Economics of Financial Markets. MSc. Financial Economics. Department of Economics, City University, London

Session X: Options: Hedging, Insurance and Trading Strategies Lecturer: Dr. Jose Olmo Module: Economics of Financial Markets MSc. Financial Economics Department of Economics, City University, London Option

Session X: Options: Hedging, Insurance and Trading Strategies Lecturer: Dr. Jose Olmo Module: Economics of Financial Markets MSc. Financial Economics Department of Economics, City University, London Option

The Behavior of Bonds and Interest Rates. An Impossible Bond Pricing Model. 780 w Interest Rate Models

780 w Interest Rate Models The Behavior of Bonds and Interest Rates Before discussing how a bond market-maker would delta-hedge, we first need to specify how bonds behave. Suppose we try to model a zero-coupon

780 w Interest Rate Models The Behavior of Bonds and Interest Rates Before discussing how a bond market-maker would delta-hedge, we first need to specify how bonds behave. Suppose we try to model a zero-coupon

Factors Affecting Option Prices

Factors Affecting Option Prices 1. The current stock price S 0. 2. The option strike price K. 3. The time to expiration T. 4. The volatility of the stock price σ. 5. The risk-free interest rate r. 6. The

Factors Affecting Option Prices 1. The current stock price S 0. 2. The option strike price K. 3. The time to expiration T. 4. The volatility of the stock price σ. 5. The risk-free interest rate r. 6. The

Lecture 5: Put - Call Parity

Lecture 5: Put - Call Parity Reading: J.C.Hull, Chapter 9 Reminder: basic assumptions 1. There are no arbitrage opportunities, i.e. no party can get a riskless profit. 2. Borrowing and lending are possible

Lecture 5: Put - Call Parity Reading: J.C.Hull, Chapter 9 Reminder: basic assumptions 1. There are no arbitrage opportunities, i.e. no party can get a riskless profit. 2. Borrowing and lending are possible

Lecture 11. Sergei Fedotov. 20912 - Introduction to Financial Mathematics. Sergei Fedotov (University of Manchester) 20912 2010 1 / 7

20912 2010 1 / 7") Lecture 11 Sergei Fedotov 20912 - Introduction to Financial Mathematics Sergei Fedotov (University of Manchester) 20912 2010 1 / 7 Lecture 11 1 American Put Option Pricing on Binomial Tree 2 Replicating

Lecture 11 Sergei Fedotov 20912 - Introduction to Financial Mathematics Sergei Fedotov (University of Manchester) 20912 2010 1 / 7 Lecture 11 1 American Put Option Pricing on Binomial Tree 2 Replicating

Caput Derivatives: October 30, 2003

Caput Derivatives: October 30, 2003 Exam + Answers Total time: 2 hours and 30 minutes. Note 1: You are allowed to use books, course notes, and a calculator. Question 1. [20 points] Consider an investor

Caput Derivatives: October 30, 2003 Exam + Answers Total time: 2 hours and 30 minutes. Note 1: You are allowed to use books, course notes, and a calculator. Question 1. [20 points] Consider an investor

Finance 436 Futures and Options Review Notes for Final Exam. Chapter 9

Finance 436 Futures and Options Review Notes for Final Exam Chapter 9 1. Options: call options vs. put options, American options vs. European options 2. Characteristics: option premium, option type, underlying

Finance 436 Futures and Options Review Notes for Final Exam Chapter 9 1. Options: call options vs. put options, American options vs. European options 2. Characteristics: option premium, option type, underlying

Bond Options, Caps and the Black Model

Bond Options, Caps and the Black Model Black formula Recall the Black formula for pricing options on futures: C(F, K, σ, r, T, r) = Fe rt N(d 1 ) Ke rt N(d 2 ) where d 1 = 1 [ σ ln( F T K ) + 1 ] 2 σ2

Bond Options, Caps and the Black Model Black formula Recall the Black formula for pricing options on futures: C(F, K, σ, r, T, r) = Fe rt N(d 1 ) Ke rt N(d 2 ) where d 1 = 1 [ σ ln( F T K ) + 1 ] 2 σ2

CHAPTER 22: FUTURES MARKETS

CHAPTER 22: FUTURES MARKETS PROBLEM SETS 1. There is little hedging or speculative demand for cement futures, since cement prices are fairly stable and predictable. The trading activity necessary to support

CHAPTER 22: FUTURES MARKETS PROBLEM SETS 1. There is little hedging or speculative demand for cement futures, since cement prices are fairly stable and predictable. The trading activity necessary to support

2. How is a fund manager motivated to behave with this type of renumeration package?

MØA 155 PROBLEM SET: Options Exercise 1. Arbitrage [2] In the discussions of some of the models in this course, we relied on the following type of argument: If two investment strategies have the same payoff

MØA 155 PROBLEM SET: Options Exercise 1. Arbitrage [2] In the discussions of some of the models in this course, we relied on the following type of argument: If two investment strategies have the same payoff

Chapter 21 Valuing Options

Chapter 21 Valuing Options Multiple Choice Questions 1. Relative to the underlying stock, a call option always has: A) A higher beta and a higher standard deviation of return B) A lower beta and a higher

Chapter 21 Valuing Options Multiple Choice Questions 1. Relative to the underlying stock, a call option always has: A) A higher beta and a higher standard deviation of return B) A lower beta and a higher

CS 522 Computational Tools and Methods in Finance Robert Jarrow Lecture 1: Equity Options

CS 5 Computational Tools and Methods in Finance Robert Jarrow Lecture 1: Equity Options 1. Definitions Equity. The common stock of a corporation. Traded on organized exchanges (NYSE, AMEX, NASDAQ). A common

CS 5 Computational Tools and Methods in Finance Robert Jarrow Lecture 1: Equity Options 1. Definitions Equity. The common stock of a corporation. Traded on organized exchanges (NYSE, AMEX, NASDAQ). A common

CHAPTER 21: OPTION VALUATION

CHAPTER 21: OPTION VALUATION PROBLEM SETS 1. The value of a put option also increases with the volatility of the stock. We see this from the put-call parity theorem as follows: P = C S + PV(X) + PV(Dividends)

CHAPTER 21: OPTION VALUATION PROBLEM SETS 1. The value of a put option also increases with the volatility of the stock. We see this from the put-call parity theorem as follows: P = C S + PV(X) + PV(Dividends)

Practice Set #4 and Solutions.

FIN-469 Investments Analysis Professor Michel A. Robe Practice Set #4 and Solutions. What to do with this practice set? To help students prepare for the assignment and the exams, practice sets with solutions

FIN-469 Investments Analysis Professor Michel A. Robe Practice Set #4 and Solutions. What to do with this practice set? To help students prepare for the assignment and the exams, practice sets with solutions

Hedging. An Undergraduate Introduction to Financial Mathematics. J. Robert Buchanan. J. Robert Buchanan Hedging

Hedging An Undergraduate Introduction to Financial Mathematics J. Robert Buchanan 2010 Introduction Definition Hedging is the practice of making a portfolio of investments less sensitive to changes in

Hedging An Undergraduate Introduction to Financial Mathematics J. Robert Buchanan 2010 Introduction Definition Hedging is the practice of making a portfolio of investments less sensitive to changes in

Investments, Chapter 4

Investments, Chapter 4 Answers to Selected Problems 2. An open-end fund has a net asset value of $10.70 per share. It is sold with a front-end load of 6 percent. What is the offering price? Answer: When

Investments, Chapter 4 Answers to Selected Problems 2. An open-end fund has a net asset value of $10.70 per share. It is sold with a front-end load of 6 percent. What is the offering price? Answer: When

2. Exercising the option - buying or selling asset by using option. 3. Strike (or exercise) price - price at which asset may be bought or sold

price - price at which asset may be bought or sold") Chapter 21 : Options-1 CHAPTER 21. OPTIONS Contents I. INTRODUCTION BASIC TERMS II. VALUATION OF OPTIONS A. Minimum Values of Options B. Maximum Values of Options C. Determinants of Call Value D. Black-Scholes

Chapter 21 : Options-1 CHAPTER 21. OPTIONS Contents I. INTRODUCTION BASIC TERMS II. VALUATION OF OPTIONS A. Minimum Values of Options B. Maximum Values of Options C. Determinants of Call Value D. Black-Scholes

Options: Valuation and (No) Arbitrage

Arbitrage") Prof. Alex Shapiro Lecture Notes 15 Options: Valuation and (No) Arbitrage I. Readings and Suggested Practice Problems II. Introduction: Objectives and Notation III. No Arbitrage Pricing Bound IV. The Binomial

Prof. Alex Shapiro Lecture Notes 15 Options: Valuation and (No) Arbitrage I. Readings and Suggested Practice Problems II. Introduction: Objectives and Notation III. No Arbitrage Pricing Bound IV. The Binomial

The Black-Scholes Formula

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 The Black-Scholes Formula These notes examine the Black-Scholes formula for European options. The Black-Scholes formula are complex as they are based on the

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 The Black-Scholes Formula These notes examine the Black-Scholes formula for European options. The Black-Scholes formula are complex as they are based on the

第 9 讲 : 股 票 期 权 定 价 : B-S 模 型 Valuing Stock Options: The Black-Scholes Model

1 第 9 讲 : 股 票 期 权 定 价 : B-S 模 型 Valuing Stock Options: The Black-Scholes Model Outline 有 关 股 价 的 假 设 The B-S Model 隐 性 波 动 性 Implied Volatility 红 利 与 期 权 定 价 Dividends and Option Pricing 美 式 期 权 定 价 American

1 第 9 讲 : 股 票 期 权 定 价 : B-S 模 型 Valuing Stock Options: The Black-Scholes Model Outline 有 关 股 价 的 假 设 The B-S Model 隐 性 波 动 性 Implied Volatility 红 利 与 期 权 定 价 Dividends and Option Pricing 美 式 期 权 定 价 American

EXP 481 -- Capital Markets Option Pricing. Options: Definitions. Arbitrage Restrictions on Call Prices. Arbitrage Restrictions on Call Prices 1) C > 0

C > 0") EXP 481 -- Capital Markets Option Pricing imple arbitrage relations Payoffs to call options Black-choles model Put-Call Parity Implied Volatility Options: Definitions A call option gives the buyer the

EXP 481 -- Capital Markets Option Pricing imple arbitrage relations Payoffs to call options Black-choles model Put-Call Parity Implied Volatility Options: Definitions A call option gives the buyer the

General Forex Glossary

General Forex Glossary A ADR American Depository Receipt Arbitrage The simultaneous buying and selling of a security at two different prices in two different markets, with the aim of creating profits without

General Forex Glossary A ADR American Depository Receipt Arbitrage The simultaneous buying and selling of a security at two different prices in two different markets, with the aim of creating profits without

Moreover, under the risk neutral measure, it must be the case that (5) r t = µ t.

r t = µ t.") LECTURE 7: BLACK SCHOLES THEORY 1. Introduction: The Black Scholes Model In 1973 Fisher Black and Myron Scholes ushered in the modern era of derivative securities with a seminal paper 1 on the pricing

LECTURE 7: BLACK SCHOLES THEORY 1. Introduction: The Black Scholes Model In 1973 Fisher Black and Myron Scholes ushered in the modern era of derivative securities with a seminal paper 1 on the pricing

Part V: Option Pricing Basics

erivatives & Risk Management First Week: Part A: Option Fundamentals payoffs market microstructure Next 2 Weeks: Part B: Option Pricing fundamentals: intrinsic vs. time value, put-call parity introduction

erivatives & Risk Management First Week: Part A: Option Fundamentals payoffs market microstructure Next 2 Weeks: Part B: Option Pricing fundamentals: intrinsic vs. time value, put-call parity introduction

University of Texas at Austin. HW Assignment 7. Butterfly spreads. Convexity. Collars. Ratio spreads.

HW: 7 Course: M339D/M389D - Intro to Financial Math Page: 1 of 5 University of Texas at Austin HW Assignment 7 Butterfly spreads. Convexity. Collars. Ratio spreads. 7.1. Butterfly spreads and convexity.

HW: 7 Course: M339D/M389D - Intro to Financial Math Page: 1 of 5 University of Texas at Austin HW Assignment 7 Butterfly spreads. Convexity. Collars. Ratio spreads. 7.1. Butterfly spreads and convexity.

CHAPTER 23: FUTURES, SWAPS, AND RISK MANAGEMENT

CHAPTER 23: FUTURES, SWAPS, AND RISK MANAGEMENT PROBLEM SETS 1. In formulating a hedge position, a stock s beta and a bond s duration are used similarly to determine the expected percentage gain or loss

CHAPTER 23: FUTURES, SWAPS, AND RISK MANAGEMENT PROBLEM SETS 1. In formulating a hedge position, a stock s beta and a bond s duration are used similarly to determine the expected percentage gain or loss

The Valuation of Currency Options

The Valuation of Currency Options Nahum Biger and John Hull Both Nahum Biger and John Hull are Associate Professors of Finance in the Faculty of Administrative Studies, York University, Canada. Introduction

The Valuation of Currency Options Nahum Biger and John Hull Both Nahum Biger and John Hull are Associate Professors of Finance in the Faculty of Administrative Studies, York University, Canada. Introduction

Numerical Methods for Option Pricing

Chapter 9 Numerical Methods for Option Pricing Equation (8.26) provides a way to evaluate option prices. For some simple options, such as the European call and put options, one can integrate (8.26) directly

Chapter 9 Numerical Methods for Option Pricing Equation (8.26) provides a way to evaluate option prices. For some simple options, such as the European call and put options, one can integrate (8.26) directly

Finance 400 A. Penati - G. Pennacchi. Option Pricing

Finance 400 A. Penati - G. Pennacchi Option Pricing Earlier we derived general pricing relationships for contingent claims in terms of an equilibrium stochastic discount factor or in terms of elementary

Finance 400 A. Penati - G. Pennacchi Option Pricing Earlier we derived general pricing relationships for contingent claims in terms of an equilibrium stochastic discount factor or in terms of elementary

Four Derivations of the Black Scholes PDE by Fabrice Douglas Rouah www.frouah.com www.volopta.com

Four Derivations of the Black Scholes PDE by Fabrice Douglas Rouah www.frouah.com www.volopta.com In this Note we derive the Black Scholes PDE for an option V, given by @t + 1 + rs @S2 @S We derive the

Four Derivations of the Black Scholes PDE by Fabrice Douglas Rouah www.frouah.com www.volopta.com In this Note we derive the Black Scholes PDE for an option V, given by @t + 1 + rs @S2 @S We derive the

1.1 Some General Relations (for the no dividend case)

") 1 American Options Most traded stock options and futures options are of American-type while most index options are of European-type. The central issue is when to exercise? From the holder point of view,

1 American Options Most traded stock options and futures options are of American-type while most index options are of European-type. The central issue is when to exercise? From the holder point of view,

7: The CRR Market Model

Ben Goldys and Marek Rutkowski School of Mathematics and Statistics University of Sydney MATH3075/3975 Financial Mathematics Semester 2, 2015 Outline We will examine the following issues: 1 The Cox-Ross-Rubinstein

Ben Goldys and Marek Rutkowski School of Mathematics and Statistics University of Sydney MATH3075/3975 Financial Mathematics Semester 2, 2015 Outline We will examine the following issues: 1 The Cox-Ross-Rubinstein

FIN 411 -- Investments Option Pricing. Options: Definitions. Arbitrage Restrictions on Call Prices. Arbitrage Restrictions on Call Prices

FIN 411 -- Investments Option Pricing imple arbitrage relations s to call options Black-choles model Put-Call Parity Implied Volatility Options: Definitions A call option gives the buyer the right, but

FIN 411 -- Investments Option Pricing imple arbitrage relations s to call options Black-choles model Put-Call Parity Implied Volatility Options: Definitions A call option gives the buyer the right, but

Futures Price d,f $ 0.65 = (1.05) (1.04)

(1.04)") 24 e. Currency Futures In a currency futures contract, you enter into a contract to buy a foreign currency at a price fixed today. To see how spot and futures currency prices are related, note that holding

24 e. Currency Futures In a currency futures contract, you enter into a contract to buy a foreign currency at a price fixed today. To see how spot and futures currency prices are related, note that holding

Chapter 1: Financial Markets and Financial Derivatives

Chapter 1: Financial Markets and Financial Derivatives 1.1 Financial Markets Financial markets are markets for financial instruments, in which buyers and sellers find each other and create or exchange

Chapter 1: Financial Markets and Financial Derivatives 1.1 Financial Markets Financial markets are markets for financial instruments, in which buyers and sellers find each other and create or exchange

Lecture 4: Properties of stock options

Lecture 4: Properties of stock options Reading: J.C.Hull, Chapter 9 An European call option is an agreement between two parties giving the holder the right to buy a certain asset (e.g. one stock unit)

Lecture 4: Properties of stock options Reading: J.C.Hull, Chapter 9 An European call option is an agreement between two parties giving the holder the right to buy a certain asset (e.g. one stock unit)

ECMC49F Options Practice Questions Suggested Solution Date: Nov 14, 2005

ECMC49F Options Practice Questions Suggested Solution Date: Nov 14, 2005 Options: General [1] Define the following terms associated with options: a. Option An option is a contract which gives the holder

ECMC49F Options Practice Questions Suggested Solution Date: Nov 14, 2005 Options: General [1] Define the following terms associated with options: a. Option An option is a contract which gives the holder

11 Option. Payoffs and Option Strategies. Answers to Questions and Problems

11 Option Payoffs and Option Strategies Answers to Questions and Problems 1. Consider a call option with an exercise price of $80 and a cost of $5. Graph the profits and losses at expiration for various

11 Option Payoffs and Option Strategies Answers to Questions and Problems 1. Consider a call option with an exercise price of $80 and a cost of $5. Graph the profits and losses at expiration for various

Hedging Strategies Using Futures. Chapter 3

Hedging Strategies Using Futures Chapter 3 Fundamentals of Futures and Options Markets, 8th Ed, Ch3, Copyright John C. Hull 2013 1 The Nature of Derivatives A derivative is an instrument whose value depends

Hedging Strategies Using Futures Chapter 3 Fundamentals of Futures and Options Markets, 8th Ed, Ch3, Copyright John C. Hull 2013 1 The Nature of Derivatives A derivative is an instrument whose value depends

Forward Contracts and Forward Rates

Forward Contracts and Forward Rates Outline and Readings Outline Forward Contracts Forward Prices Forward Rates Information in Forward Rates Reading Veronesi, Chapters 5 and 7 Tuckman, Chapters 2 and 16

Forward Contracts and Forward Rates Outline and Readings Outline Forward Contracts Forward Prices Forward Rates Information in Forward Rates Reading Veronesi, Chapters 5 and 7 Tuckman, Chapters 2 and 16

UCLA Anderson School of Management Daniel Andrei, Derivative Markets 237D, Winter 2014. MFE Midterm. February 2014. Date:

UCLA Anderson School of Management Daniel Andrei, Derivative Markets 237D, Winter 2014 MFE Midterm February 2014 Date: Your Name: Your Equiz.me email address: Your Signature: 1 This exam is open book,

UCLA Anderson School of Management Daniel Andrei, Derivative Markets 237D, Winter 2014 MFE Midterm February 2014 Date: Your Name: Your Equiz.me email address: Your Signature: 1 This exam is open book,

The Black-Scholes pricing formulas

The Black-Scholes pricing formulas Moty Katzman September 19, 2014 The Black-Scholes differential equation Aim: Find a formula for the price of European options on stock. Lemma 6.1: Assume that a stock

The Black-Scholes pricing formulas Moty Katzman September 19, 2014 The Black-Scholes differential equation Aim: Find a formula for the price of European options on stock. Lemma 6.1: Assume that a stock

Chapter 3: Commodity Forwards and Futures

Chapter 3: Commodity Forwards and Futures In the previous chapter we study financial forward and futures contracts and we concluded that are all alike. Each commodity forward, however, has some unique

Chapter 3: Commodity Forwards and Futures In the previous chapter we study financial forward and futures contracts and we concluded that are all alike. Each commodity forward, however, has some unique

Options pricing in discrete systems

UNIVERZA V LJUBLJANI, FAKULTETA ZA MATEMATIKO IN FIZIKO Options pricing in discrete systems Seminar II Mentor: prof. Dr. Mihael Perman Author: Gorazd Gotovac //2008 Abstract This paper is a basic introduction

UNIVERZA V LJUBLJANI, FAKULTETA ZA MATEMATIKO IN FIZIKO Options pricing in discrete systems Seminar II Mentor: prof. Dr. Mihael Perman Author: Gorazd Gotovac //2008 Abstract This paper is a basic introduction

CHAPTER 20. Financial Options. Chapter Synopsis

CHAPTER 20 Financial Options Chapter Synopsis 20.1 Option Basics A financial option gives its owner the right, but not the obligation, to buy or sell a financial asset at a fixed price on or until a specified

CHAPTER 20 Financial Options Chapter Synopsis 20.1 Option Basics A financial option gives its owner the right, but not the obligation, to buy or sell a financial asset at a fixed price on or until a specified

CHAPTER 22: FUTURES MARKETS

CHAPTER 22: FUTURES MARKETS 1. a. The closing price for the spot index was 1329.78. The dollar value of stocks is thus $250 1329.78 = $332,445. The closing futures price for the March contract was 1364.00,

CHAPTER 22: FUTURES MARKETS 1. a. The closing price for the spot index was 1329.78. The dollar value of stocks is thus $250 1329.78 = $332,445. The closing futures price for the March contract was 1364.00,

Lecture 9. Sergei Fedotov. 20912 - Introduction to Financial Mathematics. Sergei Fedotov (University of Manchester) 20912 2010 1 / 8

20912 2010 1 / 8") Lecture 9 Sergei Fedotov 20912 - Introduction to Financial Mathematics Sergei Fedotov (University of Manchester) 20912 2010 1 / 8 Lecture 9 1 Risk-Neutral Valuation 2 Risk-Neutral World 3 Two-Steps Binomial

Lecture 9 Sergei Fedotov 20912 - Introduction to Financial Mathematics Sergei Fedotov (University of Manchester) 20912 2010 1 / 8 Lecture 9 1 Risk-Neutral Valuation 2 Risk-Neutral World 3 Two-Steps Binomial

Lecture 11: The Greeks and Risk Management

Lecture 11: The Greeks and Risk Management This lecture studies market risk management from the perspective of an options trader. First, we show how to describe the risk characteristics of derivatives.

Lecture 11: The Greeks and Risk Management This lecture studies market risk management from the perspective of an options trader. First, we show how to describe the risk characteristics of derivatives.

Currency Options (2): Hedging and Valuation

: Hedging and Valuation") Overview Chapter 9 (2): Hedging and Overview Overview The Replication Approach The Hedging Approach The Risk-adjusted Probabilities Notation Discussion Binomial Option Pricing Backward Pricing, Dynamic

Overview Chapter 9 (2): Hedging and Overview Overview The Replication Approach The Hedging Approach The Risk-adjusted Probabilities Notation Discussion Binomial Option Pricing Backward Pricing, Dynamic

Coupon Bonds and Zeroes

Coupon Bonds and Zeroes Concepts and Buzzwords Coupon bonds Zero-coupon bonds Bond replication No-arbitrage price relationships Zero rates Zeroes STRIPS Dedication Implied zeroes Semi-annual compounding

Coupon Bonds and Zeroes Concepts and Buzzwords Coupon bonds Zero-coupon bonds Bond replication No-arbitrage price relationships Zero rates Zeroes STRIPS Dedication Implied zeroes Semi-annual compounding

Lecture. S t = S t δ[s t ].

![Lecture. S t = S t δ[s t ].](/thumbs/28/12512709.jpg "Lecture. S t = S t δ[s t ].") Lecture In real life the vast majority of all traded options are written on stocks having at least one dividend left before the date of expiration of the option. Thus the study of dividends is important

Lecture In real life the vast majority of all traded options are written on stocks having at least one dividend left before the date of expiration of the option. Thus the study of dividends is important

The Binomial Option Pricing Model André Farber

1 Solvay Business School Université Libre de Bruxelles The Binomial Option Pricing Model André Farber January 2002 Consider a non-dividend paying stock whose price is initially S 0. Divide time into small

1 Solvay Business School Université Libre de Bruxelles The Binomial Option Pricing Model André Farber January 2002 Consider a non-dividend paying stock whose price is initially S 0. Divide time into small

Binomial lattice model for stock prices

Copyright c 2007 by Karl Sigman Binomial lattice model for stock prices Here we model the price of a stock in discrete time by a Markov chain of the recursive form S n+ S n Y n+, n 0, where the {Y i }

Copyright c 2007 by Karl Sigman Binomial lattice model for stock prices Here we model the price of a stock in discrete time by a Markov chain of the recursive form S n+ S n Y n+, n 0, where the {Y i }

Dynamic Trading Strategies

Dynamic Trading Strategies Concepts and Buzzwords Multi-Period Bond Model Replication and Pricing Using Dynamic Trading Strategies Pricing Using Risk- eutral Probabilities One-factor model, no-arbitrage

Dynamic Trading Strategies Concepts and Buzzwords Multi-Period Bond Model Replication and Pricing Using Dynamic Trading Strategies Pricing Using Risk- eutral Probabilities One-factor model, no-arbitrage

Name: 1 (5) a b c d e TRUE/FALSE 1 (2) TRUE FALSE. 2 (5) a b c d e. 3 (5) a b c d e 2 (2) TRUE FALSE. 4 (5) a b c d e.

a b c d e TRUE/FALSE 1 (2) TRUE FALSE. 2 (5) a b c d e. 3 (5) a b c d e 2 (2) TRUE FALSE. 4 (5) a b c d e.") Name: Thursday, February 28 th M375T=M396C Introduction to Actuarial Financial Mathematics Spring 2013, The University of Texas at Austin In-Term Exam I Instructor: Milica Čudina Notes: This is a closed

Name: Thursday, February 28 th M375T=M396C Introduction to Actuarial Financial Mathematics Spring 2013, The University of Texas at Austin In-Term Exam I Instructor: Milica Čudina Notes: This is a closed