Chapter Copyright 2012 Pearson Education, Inc. Publishing as Prentice Hall.

|

|

|

- Alisha Harmon

- 10 years ago

- Views:

Transcription

1 Chapter 14 1

2 Identify the purposes of the statement of cash flows Distinguish among operating, investing, and financing cash flows Prepare the statement of cash flows by the indirect method Identify noncash investing and financing activities 2

3 Analyze cash flows Prepare the statement of cash flows by the direct method (Appendix 14A) Prepare the indirect statement of cash flows using a spreadsheet (Appendix 14B) 3

4 1 Identify the purposes of the statement of cash flows 4

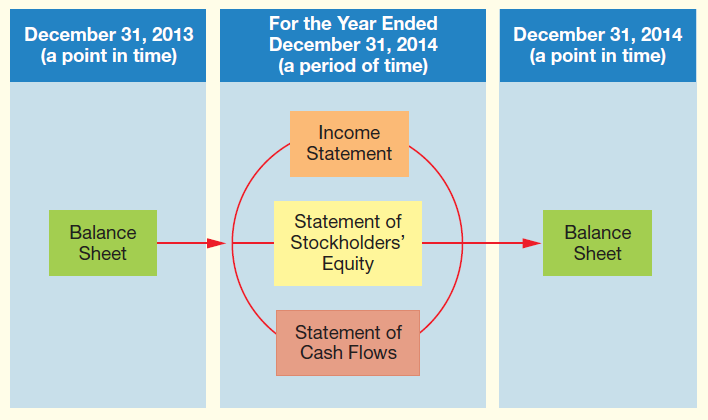

5 The comparative balance sheet reports financial position Shows whether cash increased or decreased Does not show why cash changed Covers a specific moment in time The statement of cash flows reports cash flows Shows where cash came from (receipts) and how cash was spent (payments) Reports why cash increased or decreased during the period Covers a span of time and is dated the same as the income statement The communicating link between income statement 5 and balance sheet

6 6

7 Predict future cash flows Evaluate management decisions Predict ability to pay debts and dividends 7

8 Highly liquid investments Can convert into cash three months or less So close to cash it is considered as equals Examples: Money-market accounts Investments in U.S. government securities 8

9 2 Distinguish among operating, investing, and financing cash flows 9

10 Operating Day-to-day operations Investing Long-term assets Financing Equity & Long-term liabilities 10

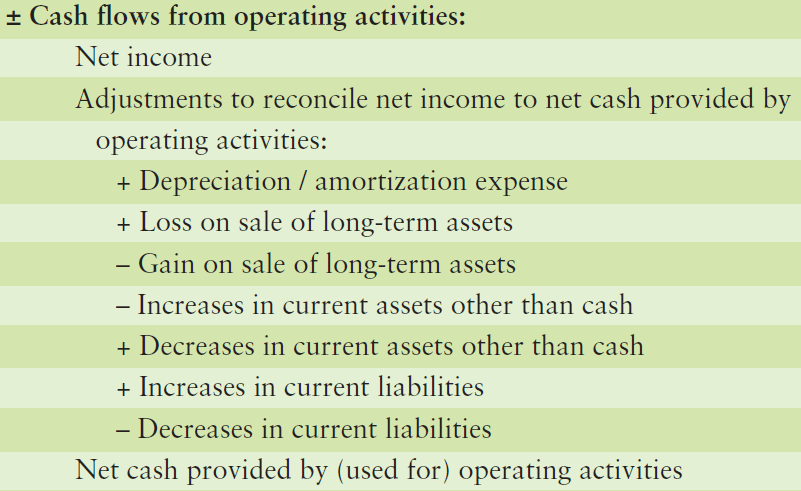

11 Most important category Reflects the day-to-day operations Determines the future of an organization Generate revenues, expenses, gains, and losses Affect net income on the income statement Affect current assets and current liabilities on the balance sheet 11

and collections of those loans Include purchases and sales of long-term")

12 Increase and decrease long-term assets Computers, software, land, buildings, and equipment Include purchases and sales of these assets Include long-term loans receivable from others (non-trade) and collections of those loans Include purchases and sales of long-term investments 12

13 Increase and decrease long-term liabilities and equity Include issuing stock, paying dividends, and buying and selling treasury stock Include borrowing money and paying off loans 13

14 Current assets Long-term assets Current liabilities Long-term liabilities Owners equity 14

15 Indirect method Starts with net income; adjusts it to net cash provided by operating activities Used by most companies Direct method Restates income statement in terms of cash Shows cash receipts and payments from operating activities Use different computations, but same operating cash flows No effect on investing and financial cash flows 15

16 16

17 17

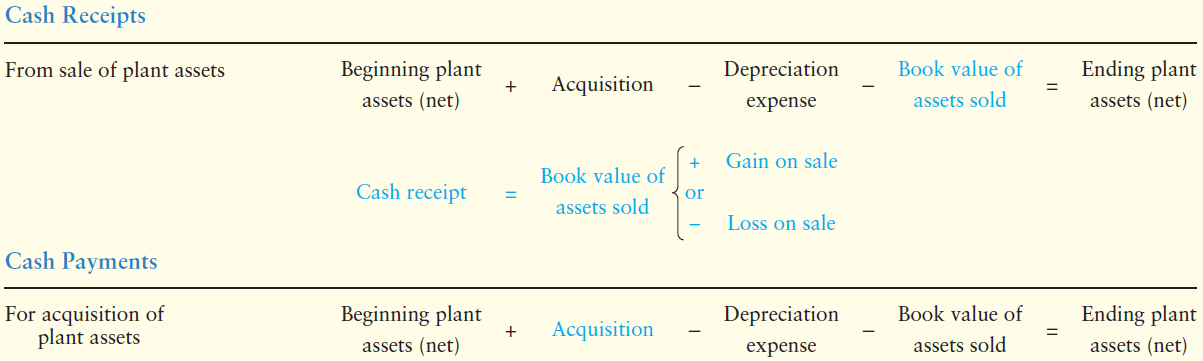

18 Destiny Corporation is preparing its statement of cash flows by the indirect method. Destiny has the following items for you to consider in preparing the statement: O+ F- O- F+ a. Increase in accounts payable f. Loss on sale of land b. Payment of dividends g. Depreciation expense c. Decrease in accrued liabilities h. Increase in inventory d. Issuance of common stock i. Decrease in accounts receivable e. Gain on sale of building I- j. Purchase of equipment Identify each item as a(n): Operating activity addition to net income (O+), or subtraction from net income (O ) Investing activity addition to cash flow (I+), or subtraction from cash flow (I ) Financing activity addition to cash flow (F+), or subtraction from cash flow (F ) Activity that is not used to prepare the indirect cash flow statement (N) O- O+ O+ O- O+ 18

: Operating activity addition to net income (O+), or subtraction from net income (O ) Investing activity addition to cash flow (I+), or subtraction")

19 3 Prepare the statement of cash flows by the indirect method 19

20 Gather the income statement and both the current and prior year s balance sheets. Step 1: Lay out statement format Step 2: Compute the change in cash from the comparative balance sheet Step 3: Take the figures Net Income, depreciation, and any gains or losses from the income statement Step 4: Complete the statement of cash flows 20

21 21

22 Items from the income statement not affecting cash 22

23 23

24 Effect on cash Current assets If an increase If a decrease Current liabilities 24

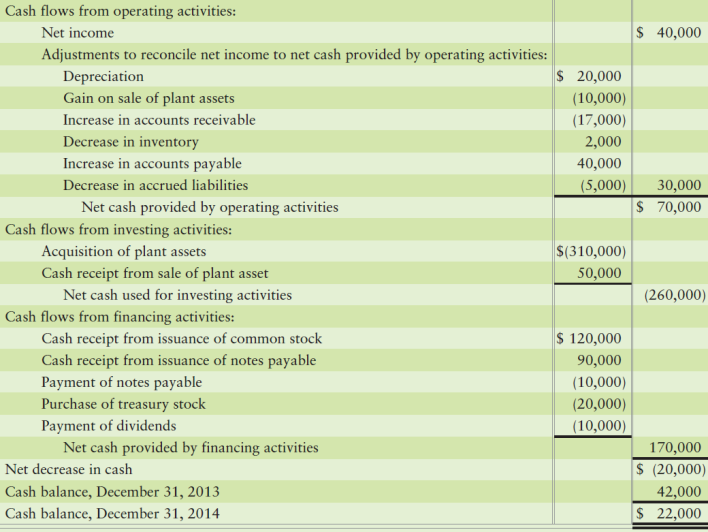

25 Refer to the balance sheet for changes in the accounts Operations provided net cash flow of $70,000. This amount exceeds net income of $40,

26 Sales and acquisitions of long-term assets Plant assets and investments Analyze accounts to determine activity Use of T-account is helpful If gain or loss appears on the income statement, a long-term asset has been sold 26

27 Combine all the plant assets into a single Plant assets account Find the cost of the sold assets The missing value in our net T-account 27

28 Solve cash received using the T-account and journal entry Adding the cost of the sold asset to the gain yields cash received 28

29 29

30 Issuances of and payments on long-term notes payable Issuances of stock and purchases of treasury stock Payments of dividends 30

31 Review balance sheet for differences Note increase in Long-term notes payable If new issuances or payments are known, the other can be calculated If unknown, review account for debits and credits With knowledge of a new note, note payments can be calculated 31

32 Review balance sheet for differences Note change in Common stock of $120,000 If either new issuances or purchases are known, the other can be calculated If unknown, review account for debits and credits 32

33 Review balance sheet for differences Note change in Treasury stock of $20,000 If either new issuances or purchases are known, the other can be calculated If unknown, review account for debits and credits 33

34 Review balance sheet for differences in Retained earnings Note change in Retained earnings Retained earnings is changed by net income, net losses and dividends Net income of $40,000 is indicated on the income statement Cannot have both income and loss 34

35 35

36 One Way Cellular accountants have assembled the following data for the year ended September 30, 2012: Payment of dividends $6,100 Net income $ 55,000 Depreciation expense 20,000 Purchase of equipment 39,000 Cash receipt from sale of land 34,000 Cash receipt from issuance of common stk. 30,000 Decrease in current liabilities 19,000 Increase in current assets other than cash 14,000 Prepare the operating activities section using the indirect method for One Way Cellular s statement of cash flows for the year ended September 30,

37 37 One Way Cellular Statement of Cash Partial Year Ended September 30, 2012 Cash flows from operating activities Net income: $55,000 Adjustments to reconcile net income to net cash provided by operating activities Depreciation $20,000 Increase in current assets other than cash (14,000) Decrease in current liabilities (19,000) (13,000) Net cash provided by operating activities $42,000

38 Use the data in Short Exercise 14-5 to complete this exercise. Prepare One Way Cellular s statement of cash flows using the indirect method for the year ended September 30, Stop after determining the net increase (or decrease) in cash. 38

39 One Way Cellular Statement of Cash Flows Partial Year Ended September 30, 2012 Cash flows from operating activities Net income: $55,000 Adjustments to reconcile net income to net cash provided by operating activities Depreciation $20,000 Increase in current assets other than cash (14,000) Decrease in current liabilities (19,000) (13,000) Net cash provided by operating activities $42,000 39

40 One Way Cellular Statement of Cash Flows Partial Year Ended September 30, 2012 Net cash provided by operating activities $ 42,000 Cash flows from investing activities: Acquisition of equipment $ (39,000) Cash receipt from sale of land 34,000 Net cash used for investing activities (5,000) Cash flows from financing activities: Cash receipt from issuance of common stock $ 30,000 Payments of cash dividends (6,100) Net cash provided by financing activities 23,900 Net increase in cash $ 60,900 40

41 4 Identify noncash investing and financing activities 41

42 Investing and financing activities that do not affect cash Some examples are: Acquired building by issuing stock Acquired land by issuing note payable Paid note payable by issuing common stock Reported in separate schedule or in a note Key Cash not listed in entry to record transaction 42

43 Judy s Makeup Shops earned net income of $22,000, which included depreciation of $14,000. Judy s acquired a $119,000 building by borrowing $119,000 on a long-term note payable. 1. How much did Judy s cash balance increase or decrease during the year? Net income $22,000 Depreciation 14,000 Purchase of building with long-term notes 0 Increase in cash $36,000 43

44 2. Were there any noncash transactions for the company? If so, show how they would be reported in the statement of cash flows. Yes, acquisition of building with long-term note payable reported in non-cash investing and financing activities. 44

45 5 Analyze cash flows 45

46 Cash available from operations after: Paying for planned investments in long-term assets Paying dividends to shareholders Used to manage operations If investment opportunity is available, cash is free to invest 46

47 Cooper Lopez Company expects the following for 2012: Net cash provided by operating activities of $158,000. Net cash provided by financing activities of $60,000. Net cash used for investing activities of $80,000 (no sales of longterm assets). Cash dividends paid to shareholders was $10, How much free cash flow does Lopez expect for 2012? NCOA - Payments for planned - invest. Payments of cash = dividends Free cash flow $158,000 80,000 10,000 = $68,000 47

48 6 Prepare the statement of cash flows by the direct method (Appendix 14A) 48

49 Preferred by FASB Provides clearer information about cash receipts and payments Normally not used by private companies Takes more computations Only operating activities presentation changes Net cash flow from operating activities has the same amount of cash Investing and Financing sections not changed 49

50 Net cash provided is the same as indirect method 50

51 STEP 1: Lay out the operating section by the direct method STEP 2: Use the comparative balance sheet to determine the increase or decrease in cash STEP 3: Use the available data to prepare the statement of cash flows Reports only transactions with cash effects Essentially a cash-basis income statement 51

52 First item on income statement Sales Total of all sales, whether for cash or on account Yields cash collected from customers Formula or Sales revenue Increase in Accounts receivable Cash collections from customers Sales revenue + Decrease in Accounts receivable Cash collections from customers 52

53 Second item on income statement Interest revenue Related account is Interest receivable Receivable account indicates some not received Formula or Interest revenue Increase in Interest receivable Cash collections from interest Interest revenue + Decrease in Interest receivable Cash collections from interest 53

54 Third item on income statement Dividend revenue Related account is Dividend receivable Receivable account indicates some not received Formula or Dividend revenue Increase in Dividend receivable Cash collections from dividends Dividend revenue + Decrease in Dividend receivable Cash collections from dividends 54

55 Payments to suppliers include all payments for inventory and operating expenses Formula Cost of goods sold Decrease in Inventory Increase in Accounts payable = Cash paid for Inventory Cost of goods sold + Increase in Inventory + Decrease in Accounts payable = Cash paid for Inventory 55

56 Payments to suppliers include all payments for inventory and operating expenses Formula Other operating expenses + Decrease in Accrued liabilities = Cash paid for operating expenses Other operating expenses Increase in Accrued liabilities = Cash paid for operating expenses 56

57 Payments to suppliers include all payments for inventory and operating expenses Formula Cash paid for Inventory + Cash paid for operating expenses = Cash paid to suppliers 57

58 Payments to employees includes salaries, wages, other employee compensation Formula Salary expense or Wages expense + Decrease in Accrued salaries = Cash paid to employees Salary expense or Wages expense Increase in Accrued salaries = Cash paid to employees 58

59 Payments for interest include all payments of interest on notes and bonds Formula Interest expense + Decrease in Accrued interest = Cash paid for interest Interest expense Increase in Accrued interest = Cash paid for interest 59

60 Payments for income taxes for all payments of taxes on income Formula Income tax expense + Decrease in Income tax payable = Cash paid for income tax Income tax expense Increase in Income tax payable = Cash paid for income tax 60

61 Add them all together 61

")

62 7 Prepare the indirect statement of cash flows using a spreadsheet (Appendix 14B) 62

63 Companies face complex accounting situations Spreadsheet can help Four column spreadsheet Includes beginning and ending account balances The center left and right columns are for transactional analysis 63

64 a. Net income of $40,000 is the first operating cash inflow b. Next come the adjustments to net income c. Removes the gain on the sale of assets d. Entries D G balance changes in current assets and liabilities h. Long-term asset changes i. Change in Common stock j. Entries J K balance changes in Long-term liabilities l. L M balance changes in Retained earnings and Treasury stock n. Final item is the Net decrease in cash 64

65 Each letter matches an item in the statement of cash flows Change in cash from beginning to end Each letter matches an item in the statement of cash flows Net Income Starting point 65

66 Each letter matches an item in the statement of cash flows 66 Change in cash from beginning to end

67 The statement of cash flows explains why the cash balance does not equal net income (loss) from the income statement. Cash on the statement of cash flows includes cash equivalents. Cash equivalents are assets so close to being cash that they are treated like cash. The statement helps users predict future cash flows, evaluate management decisions, and predict the company s ability to pay debts and dividends. 67

68 Operating activities reflect the day-to-day business operations. Operating activities affect current assets and current liabilities. Investing activities report purchase and sales of long-term assets, such as buildings and longterm (nontrade) loans receivable. Financing activities reflect the capitalization of the business and include increases and decreases in long-term liability and equity accounts, paying dividends, and treasury stock transactions. 68

69 Only the operating activities section is presented differently between the indirect and direct methods. The indirect cash flow statement begins with operating activities. Net income (or net loss) from the income statement is the first item listed. Then, adjustments are made based on changes in current asset and current liability accounts to derive cash provided by (used for) operating activities. 69

70 Then, investing activities are reported, showing cash used to purchase or cash received from selling long-term assets. Finally, financing activities are reported, showing cash used to pay long-term liabilities, to pay cash dividends, or to purchase treasury shares AND cash received from issuing new long-term liabilities or issuing stock. The total of the cash flows from the three activities (operating, investing, and financing) equals the change in the cash balance. 70

71 Companies make investments that do not require cash. They also obtain financing other than cash. Such transactions are called noncash investing and financing activities and appear in a separate part of the cash flow statement. Free cash flow measures the amount of cash available from normal operations after paying for planned investments in long-term assets and after paying cash dividends to shareholders. 71

72 Appendix 14A - The Financial Accounting Standards Board (FASB) prefers the direct method of reporting cash flows from operating activities. The direct method provides clearer information about the sources and uses of cash than does the indirect method. Appendix 14B - The T-account approach works well as a learning device. In practice, however, most companies face complex situations. In these cases, a spreadsheet can help in preparing the statement of cash flows. 72

73 73

74 Copyright All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the publisher. Printed in the United States of America. 74

COMPONENTS OF THE STATEMENT OF CASH FLOWS

ILLUSTRATION 24-1 OPERATING, INVESTING, AND FINANCING ACTIVITIES COMPONENTS OF THE STATEMENT OF CASH FLOWS CASH FLOWS FROM OPERATING ACTIVITIES + Sales and Service Revenue Received Cost of Sales Paid Selling

ILLUSTRATION 24-1 OPERATING, INVESTING, AND FINANCING ACTIVITIES COMPONENTS OF THE STATEMENT OF CASH FLOWS CASH FLOWS FROM OPERATING ACTIVITIES + Sales and Service Revenue Received Cost of Sales Paid Selling

Statement of Cash Flows

THE CONTENT AND VALUE OF THE STATEMENT OF CASH FLOWS The cash flow statement reconciles beginning and ending cash by presenting the cash receipts and cash disbursements of an enterprise for an accounting

THE CONTENT AND VALUE OF THE STATEMENT OF CASH FLOWS The cash flow statement reconciles beginning and ending cash by presenting the cash receipts and cash disbursements of an enterprise for an accounting

ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL)

") Page 1 ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL) Complete these sample exam problems/objective questions and check your answers with the solutions at the end of the review file and identify where

Page 1 ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL) Complete these sample exam problems/objective questions and check your answers with the solutions at the end of the review file and identify where

how to prepare a cash flow statement

business builder 4 how to prepare a cash flow statement zions business resource center zions business resource center 2 how to prepare a cash flow statement A cash flow statement is important to your business

business builder 4 how to prepare a cash flow statement zions business resource center zions business resource center 2 how to prepare a cash flow statement A cash flow statement is important to your business

CH 23 STATEMENT OF CASH FLOWS SELF-STUDY QUESTIONS

C H 2 3, P a g e 1 CH 23 STATEMENT OF CASH FLOWS SELF-STUDY QUESTIONS (note from Dr. N: I have deleted questions for you to omit, but did not renumber the remaining questions) 1. The primary purpose of

C H 2 3, P a g e 1 CH 23 STATEMENT OF CASH FLOWS SELF-STUDY QUESTIONS (note from Dr. N: I have deleted questions for you to omit, but did not renumber the remaining questions) 1. The primary purpose of

Chapter 21 The Statement of Cash Flows Revisited

Chapter 21 The Statement of Cash Flows Revisited AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments,

Chapter 21 The Statement of Cash Flows Revisited AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments,

Statement of Cash Flows

PREPARING THE STATEMENT OF CASH FLOWS: THE INDIRECT METHOD OF REPORTING CASH FLOWS FROM OPERATING ACTIVITIES The work sheet method described in the text book is not the recommended approach. We will provide

PREPARING THE STATEMENT OF CASH FLOWS: THE INDIRECT METHOD OF REPORTING CASH FLOWS FROM OPERATING ACTIVITIES The work sheet method described in the text book is not the recommended approach. We will provide

Reporting and Analyzing Cash Flows QUESTIONS

Chapter 12 Reporting and Analyzing Cash Flows QUESTIONS 1. The purpose of the cash flow statement is to report all major cash receipts (inflows) and cash payments (outflows) during a period. It helps users

Chapter 12 Reporting and Analyzing Cash Flows QUESTIONS 1. The purpose of the cash flow statement is to report all major cash receipts (inflows) and cash payments (outflows) during a period. It helps users

CHAPTER 23. Statement of Cash Flows 1, 2, 7, 8, 12 3, 4, 5, 6, 16, 17, 19 9, 20 4, 5, 9, 10, 11 10, 13, 15, 16. 7. Worksheet adjustments.

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

Cash is King. cash flow is less likely to be affected

Reading 27: Understanding Cash Flow Statements Relevance of Cash Flow The primary purpose of the statement of cash flows (SCF) is to provide: Info about a firm s cash receipts & cash payments during an

Reading 27: Understanding Cash Flow Statements Relevance of Cash Flow The primary purpose of the statement of cash flows (SCF) is to provide: Info about a firm s cash receipts & cash payments during an

The Statement of Cash Flows

CHAPTER The Statement of Cash Flows OBJECTIVES After careful study of this chapter, you will be able to: 1. Define operating, investing, and financing activities. 2. Know the categories of inflows and

CHAPTER The Statement of Cash Flows OBJECTIVES After careful study of this chapter, you will be able to: 1. Define operating, investing, and financing activities. 2. Know the categories of inflows and

Statement of Cash Flow

Management Accounting 337 Statement of Cash Flow Cash is obviously an important asset to all, both individually and in business. A shortage or lack of cash may mean an inability to purchase needed inventory

Management Accounting 337 Statement of Cash Flow Cash is obviously an important asset to all, both individually and in business. A shortage or lack of cash may mean an inability to purchase needed inventory

CASH FLOW STATEMENT. On the statement, cash flows are segregated based on source:

CASH FLOW STATEMENT On the statement, cash flows are segregated based on source: Operating activities: involve the cash effects of transactions that enter into the determination of net income. Investing

CASH FLOW STATEMENT On the statement, cash flows are segregated based on source: Operating activities: involve the cash effects of transactions that enter into the determination of net income. Investing

Chapter 6 Statement of Cash Flows

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

EXERCISES. The cash from operating activities detail is provided as follows for class discussion:

EXERCISES Ex. 14 1 There were net additions, such as depreciation and amortization of intangible assets of $389 million, to the net loss reported on the income statement to convert the net loss from the

EXERCISES Ex. 14 1 There were net additions, such as depreciation and amortization of intangible assets of $389 million, to the net loss reported on the income statement to convert the net loss from the

How to Prepare a Cash Flow Statement

How to Prepare a Cash Flow Statement Peoples Bank Business Resource Center Business Builder 4 peoplesbancorp.com 800.374.6123 Table of Contents What to Expect... 4 What You Should Know Before Getting

How to Prepare a Cash Flow Statement Peoples Bank Business Resource Center Business Builder 4 peoplesbancorp.com 800.374.6123 Table of Contents What to Expect... 4 What You Should Know Before Getting

STATEMENT OF CHANGES IN FINANCIAL POSITION

Home Page - Statement of Changes in Financial Position STATEMENT OF CHANGES IN FINANCIAL POSITION by Dr. J. Herbert Smith/ACOA Chair Technology Management and Entrepreneurship Faculty of Engineering University

Home Page - Statement of Changes in Financial Position STATEMENT OF CHANGES IN FINANCIAL POSITION by Dr. J. Herbert Smith/ACOA Chair Technology Management and Entrepreneurship Faculty of Engineering University

CHAPTER 2 REVIEW OF THE ACCOUNTING PROCESS. Lecture Outline

CHAPTER 2 REVIEW OF THE ACCOUNTING PROCESS Overview Chapter 1 explained that the primary means of conveying financial information to investors, creditors, and other external users is through financial

CHAPTER 2 REVIEW OF THE ACCOUNTING PROCESS Overview Chapter 1 explained that the primary means of conveying financial information to investors, creditors, and other external users is through financial

Section A: Questions On Fill In The Blanks

Section A : 26 FILL IN THE BLANK Section B : 10 TRUE OR FALSE QUESTIONS Section C : 11 Multiple Choice Questions Section A: Questions Fill In The Blanks the right column please insert the items from which

Section A : 26 FILL IN THE BLANK Section B : 10 TRUE OR FALSE QUESTIONS Section C : 11 Multiple Choice Questions Section A: Questions Fill In The Blanks the right column please insert the items from which

T-Account Approach to Preparing a Statement of Cash Flows Indirect Method

266 Part 1 E M Foundations of Financial Accounting With these adjustments to the income statement, we can now present the operating activities section of the statement of cash flows using either the direct

266 Part 1 E M Foundations of Financial Accounting With these adjustments to the income statement, we can now present the operating activities section of the statement of cash flows using either the direct

Understanding A Firm s Financial Statements

CHAPTER OUTLINE Spotlight: J&S Construction Company (http://www.jsconstruction.com) 1 The Lemonade Kids Financial statement (accounting statements) reports of a firm s financial performance and resources,

CHAPTER OUTLINE Spotlight: J&S Construction Company (http://www.jsconstruction.com) 1 The Lemonade Kids Financial statement (accounting statements) reports of a firm s financial performance and resources,

Financial Statements

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

CASH FLOW STATEMENT (AND FINANCIAL STATEMENT)

") CASH FLOW STATEMENT (AND FINANCIAL STATEMENT) - At the most fundamental level, firms do two different things: (i) They generate cash (ii) They spend it. Cash is generated by selling a product, an asset

CASH FLOW STATEMENT (AND FINANCIAL STATEMENT) - At the most fundamental level, firms do two different things: (i) They generate cash (ii) They spend it. Cash is generated by selling a product, an asset

> DO IT! Chapter 13. Classification of Cash Flows. Cash from Operating Activities D-1. Solution. Action Plan

Chapter 13 > DO IT! Classification of Cash Flows Identify the three types of activities used to report all cash inflows and outflows. Report as operating activities the cash effects of transactions that

Chapter 13 > DO IT! Classification of Cash Flows Identify the three types of activities used to report all cash inflows and outflows. Report as operating activities the cash effects of transactions that

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased.

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased. Accounts Receivable are the total amounts customers owe your business for goods or services sold

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased. Accounts Receivable are the total amounts customers owe your business for goods or services sold

STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

Analyzing the Statement of Cash Flows

Analyzing the Statement of Cash Flows Operating Activities NACM Upstate New York Credit Conference 2015 By Ron Sereika, CCE,CEW NACM 1 Objectives of this Educational Session u Show how the statement of

Analyzing the Statement of Cash Flows Operating Activities NACM Upstate New York Credit Conference 2015 By Ron Sereika, CCE,CEW NACM 1 Objectives of this Educational Session u Show how the statement of

RECOGNIZING A MINORITY INTEREST IN CONSOLIDATED FINANCIAL STATEMENTS

RECOGNIZING A MINORITY INTEREST IN CONSOLIDATED FINANCIAL STATEMENTS L E A R N I N G O B J E C T I V E Adapt the consolidation work sheet procedure to recognize a minority interest. Chapter 11 illustrates

RECOGNIZING A MINORITY INTEREST IN CONSOLIDATED FINANCIAL STATEMENTS L E A R N I N G O B J E C T I V E Adapt the consolidation work sheet procedure to recognize a minority interest. Chapter 11 illustrates

The Income Statement and Statement of Cash Flows

THE STATEMENT OF CASH FLOWS Purpose of the Statement of Cash Flows The purpose of the statement of cash flows is to identify the sources and uses of cash and the change in cash from the beginning to the

THE STATEMENT OF CASH FLOWS Purpose of the Statement of Cash Flows The purpose of the statement of cash flows is to identify the sources and uses of cash and the change in cash from the beginning to the

Course pack Accounting 202 Chapter 13: Cash Flow Statement

Course pack Accounting 202 Chapter 13: Cash Flow Statement Value Chapter Included 13 Purpose of Cash Flow Understand Operating, Investing, Financing activities Prepare a Cash Flow Statement indirect only

Course pack Accounting 202 Chapter 13: Cash Flow Statement Value Chapter Included 13 Purpose of Cash Flow Understand Operating, Investing, Financing activities Prepare a Cash Flow Statement indirect only

TRANSACTIONS ANALYSIS EXAMPLE. Maxwell Partners Medical Diagnostic Services report the following information for 2011, their first year of operations:

TRANSACTIONS ANALYSIS EXAMPLE Maxwell Partners Medical Diagnostic Services report the following information for 2011, their first year of operations: 1. Billings to clients for services provided: $350,000

TRANSACTIONS ANALYSIS EXAMPLE Maxwell Partners Medical Diagnostic Services report the following information for 2011, their first year of operations: 1. Billings to clients for services provided: $350,000

Cash Flow Analysis. 15.501/516 Accounting Spring 2004. Professor S. Roychowdhury. Sloan School of Management Massachusetts Institute of Technology

Cash Flow Analysis 15.501/516 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology Mar 1/3, 2004 1 About The Exam March 10 th a week from today.

Cash Flow Analysis 15.501/516 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology Mar 1/3, 2004 1 About The Exam March 10 th a week from today.

THE STATEMENT OF CASH FLOWS

THE STATEMENT OF CASH FLOWS Associate Professor PhD Cernusca Lucian University Aurel Vlaicu of Arad, [email protected] Professor PhD Mates Dorel, West University of Timisoara Abstract: In today

THE STATEMENT OF CASH FLOWS Associate Professor PhD Cernusca Lucian University Aurel Vlaicu of Arad, [email protected] Professor PhD Mates Dorel, West University of Timisoara Abstract: In today

Financial Statements Tutorial

Financial Statement Review: Financial Statements Tutorial There are four major financial statements used to communicate information to external users (creditors, investors, suppliers, etc.) - 1. Balance

Financial Statement Review: Financial Statements Tutorial There are four major financial statements used to communicate information to external users (creditors, investors, suppliers, etc.) - 1. Balance

Authored for ENMU Tutoring Services. By Jessica Huff

By Jessica Huff The standard accounting equation is Assets=Liabilities + Stockholders Equity. Depending on which item someone is looking at will determine what the normal balance is. The normal balance

By Jessica Huff The standard accounting equation is Assets=Liabilities + Stockholders Equity. Depending on which item someone is looking at will determine what the normal balance is. The normal balance

Statement of Change in Working Capital & Inflows/Outflows of Working Capital

HOSP 2110 (Management Acct) Learning Centre Statement of Change in Working Capital & Inflows/Outflows of Working Capital The statement of changes in working capital shows the net change in working capital

HOSP 2110 (Management Acct) Learning Centre Statement of Change in Working Capital & Inflows/Outflows of Working Capital The statement of changes in working capital shows the net change in working capital

CASH FLOW STATEMENT. MODULE - 6A Analysis of Financial Statements. Cash Flow Statement. Notes

MODULE - 6A Cash Flow Statement 30 CASH FLOW STATEMENT In the previous lesson, you have learnt various types of analysis of financial statements and its tools such as comparative statements, common size

MODULE - 6A Cash Flow Statement 30 CASH FLOW STATEMENT In the previous lesson, you have learnt various types of analysis of financial statements and its tools such as comparative statements, common size

Ratio Analysis. A) Liquidity Ratio : - 1) Current ratio = Current asset Current Liability

Liquidity Ratio : - 1) Current ratio = Current asset Current Liability") A) Liquidity Ratio : - Ratio Analysis 1) Current ratio = Current asset Current Liability 2) Quick ratio or Acid Test ratio = Quick Asset Quick liability Quick Asset = Current Asset Stock Quick Liability

A) Liquidity Ratio : - Ratio Analysis 1) Current ratio = Current asset Current Liability 2) Quick ratio or Acid Test ratio = Quick Asset Quick liability Quick Asset = Current Asset Stock Quick Liability

Understanding Cash Flow Statements

Understanding Cash Flow Statements 2014 Level I Financial Reporting and Analysis IFT Notes for the CFA exam Contents 1. Introduction... 3 2. Components and Format of the Cash Flow Statement... 3 3. The

Understanding Cash Flow Statements 2014 Level I Financial Reporting and Analysis IFT Notes for the CFA exam Contents 1. Introduction... 3 2. Components and Format of the Cash Flow Statement... 3 3. The

APPENDIX 1 The Statement of Financial Position

APPENDIX 1 The Statement of Financial Position 1. Assets: the resources of the organization which are used to provide service and generate value 2. Current assets: assets which can be converted to cash

APPENDIX 1 The Statement of Financial Position 1. Assets: the resources of the organization which are used to provide service and generate value 2. Current assets: assets which can be converted to cash

Guide to Financial Statements Study Guide

Guide to Financial Statements Study Guide Overview (Topic 1) Three major financial statements: The Income Statement The Balance Sheet The Cash Flow Statement Objectives: Explain the underlying equation

Guide to Financial Statements Study Guide Overview (Topic 1) Three major financial statements: The Income Statement The Balance Sheet The Cash Flow Statement Objectives: Explain the underlying equation

This week its Accounting and Beyond

This week its Accounting and Beyond Monday Morning Session Introduction/Accounting Cycle Afternoon Session Tuesday The Balance Sheet Wednesday The Income Statement The Cash Flow Statement Thursday Tools

This week its Accounting and Beyond Monday Morning Session Introduction/Accounting Cycle Afternoon Session Tuesday The Balance Sheet Wednesday The Income Statement The Cash Flow Statement Thursday Tools

Basic Accounting Principles

Basic Accounting Principles Basic Accounting Model The basic accounting model represents the relationship between assets (what the company owns), liabilities (what the company owes), and owner s equity

Basic Accounting Principles Basic Accounting Model The basic accounting model represents the relationship between assets (what the company owns), liabilities (what the company owes), and owner s equity

Income Measurement and Profitability Analysis

PROFITABILITY ANALYSIS The following financial statements for Spencer Company will be used to demonstrate the calculation of the various ratios in profitability analysis. Spencer Company Comparative Balance

PROFITABILITY ANALYSIS The following financial statements for Spencer Company will be used to demonstrate the calculation of the various ratios in profitability analysis. Spencer Company Comparative Balance

Statement of Cash Flows

HOSP 2110 (Management Acct) Learning Centre Statement of Cash Flows The Statement of Cash Flows (or cash flow statement) is one of the main financial statements used by investors. It shows the cash generated

HOSP 2110 (Management Acct) Learning Centre Statement of Cash Flows The Statement of Cash Flows (or cash flow statement) is one of the main financial statements used by investors. It shows the cash generated

Technical Note: Understanding the Effects of Cash Flow Category Assignment

Article # 1131 Technical Note: Understanding the Effects of Cash Flow Category Assignment Difficulty Level: Intermediate Level AccountMate User Version(s) Affected: AccountMate 7 for SQL, Express and LAN

Article # 1131 Technical Note: Understanding the Effects of Cash Flow Category Assignment Difficulty Level: Intermediate Level AccountMate User Version(s) Affected: AccountMate 7 for SQL, Express and LAN

Learning Module 3 Journal Entries

Learning Module 3 Journal Entries The Accounting Equation Balance Sheet Income Statement = + + - Assets Liabilities Owners' Equity Revenue Expenses Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Recording journal

Learning Module 3 Journal Entries The Accounting Equation Balance Sheet Income Statement = + + - Assets Liabilities Owners' Equity Revenue Expenses Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Recording journal

Financial Reporting & Analysis Chapter 17 Solutions Statement of Cash Flows Exercises

Financial Reporting & Analysis Chapter 17 Solutions Statement of Cash Flows Exercises Exercises E17-1. Determining cash flows from operations Using the indirect method, cash flow from operations is computed

Financial Reporting & Analysis Chapter 17 Solutions Statement of Cash Flows Exercises Exercises E17-1. Determining cash flows from operations Using the indirect method, cash flow from operations is computed

Cash Flow Statement. Introduction. Introd. Contd. Chapter 4

Cash Flow Statement Chapter 4 Introduction Management and other interested external parties have always recognized the need for a cash flow statement but it was never required until the FASB (Financial

Cash Flow Statement Chapter 4 Introduction Management and other interested external parties have always recognized the need for a cash flow statement but it was never required until the FASB (Financial

Consolidated Balance Sheets

Consolidated Balance Sheets March 31 2015 2014 2015 Assets: Current assets Cash and cash equivalents 726,888 604,571 $ 6,057,400 Marketable securities 19,033 16,635 158,608 Notes and accounts receivable:

Consolidated Balance Sheets March 31 2015 2014 2015 Assets: Current assets Cash and cash equivalents 726,888 604,571 $ 6,057,400 Marketable securities 19,033 16,635 158,608 Notes and accounts receivable:

Fuqua School of Business, Duke University ACCOUNTG 510: Foundations of Financial Accounting

Fuqua School of Business, Duke University ACCOUNTG 510: Foundations of Financial Accounting Lecture Note: Financial Statement Basics, Transaction Recording, and Terminology I. The Financial Reporting Package

Fuqua School of Business, Duke University ACCOUNTG 510: Foundations of Financial Accounting Lecture Note: Financial Statement Basics, Transaction Recording, and Terminology I. The Financial Reporting Package

The Statement of Cash Flows Direct Method

23 The Statement of Cash Flows Direct Method DEMONSTRATION PROBLEM The financial statements of Bolero Corporation follow. Copyright Houghton Mifflin Company. All rights reserved. 1 Bolero Corporation Income

23 The Statement of Cash Flows Direct Method DEMONSTRATION PROBLEM The financial statements of Bolero Corporation follow. Copyright Houghton Mifflin Company. All rights reserved. 1 Bolero Corporation Income

Preparing a Successful Financial Plan

Topic 9 Preparing a Successful Financial Plan LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Describe the overview of accounting methods; 2. Prepare the three major financial statements

Topic 9 Preparing a Successful Financial Plan LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Describe the overview of accounting methods; 2. Prepare the three major financial statements

GENERAL LIGHTING CORPORATION Income Statement For the Year Ended December 31, 2013

Chapter 4 Exercises and Problems Exercise 4 2 Requirement 1 GENERAL LIGHTING CORPORATION Income Statement Revenues and gains: Sales... $2,350,000 Rental revenue... 80,000 Total revenues and gains... 2,430,000

Chapter 4 Exercises and Problems Exercise 4 2 Requirement 1 GENERAL LIGHTING CORPORATION Income Statement Revenues and gains: Sales... $2,350,000 Rental revenue... 80,000 Total revenues and gains... 2,430,000

Learning Objectives: Quick answer key: Question # Multiple Choice True/False. 14.1 Describe the important of accounting and financial information.

0 Learning Objectives: 14.1 Describe the important of accounting and financial information. 14.2 Differentiate between managerial and financial accounting. 14.3 Identify the six steps of the accounting

0 Learning Objectives: 14.1 Describe the important of accounting and financial information. 14.2 Differentiate between managerial and financial accounting. 14.3 Identify the six steps of the accounting

ČEZ, a. s. BALANCE SHEET in accordance with IFRS as of March 31, 2015 in CZK Millions

BALANCE SHEET Assets Property, plant and equipment: 31. 03. 2015 31. 12. 2014 Plant in service 345,012 344,246 Less accumulated provision for depreciation (199,841) (196,333) Net plant in service 145,171

BALANCE SHEET Assets Property, plant and equipment: 31. 03. 2015 31. 12. 2014 Plant in service 345,012 344,246 Less accumulated provision for depreciation (199,841) (196,333) Net plant in service 145,171

Understanding Financial Information for Bankruptcy Lawyers Understanding Financial Statements

Understanding Financial Information for Bankruptcy Lawyers Understanding Financial Statements In the United States, businesses generally present financial information in the form of financial statements

Understanding Financial Information for Bankruptcy Lawyers Understanding Financial Statements In the United States, businesses generally present financial information in the form of financial statements

CASH FLOW STATEMENT & BALANCE SHEET GUIDE

CASH FLOW STATEMENT & BALANCE SHEET GUIDE The Agriculture Development Council requires the submission of a cash flow statement and balance sheet that provide annual financial projections for the business

CASH FLOW STATEMENT & BALANCE SHEET GUIDE The Agriculture Development Council requires the submission of a cash flow statement and balance sheet that provide annual financial projections for the business

The Basic Framework of Budgeting

Master Budgeting 1 The Basic Framework of Budgeting A budget is a detailed quantitative plan for acquiring and using financial and other resources over a specified forthcoming time period. 1. The act of

Master Budgeting 1 The Basic Framework of Budgeting A budget is a detailed quantitative plan for acquiring and using financial and other resources over a specified forthcoming time period. 1. The act of

ČEZ, a. s. BALANCE SHEET in accordance with IFRS as of June 30, 2014 in CZK Millions

BALANCE SHEET Assets Property, plant and equipment: 30. 6. 2014 31. 12. 2013 Plant in service 319 440 319 081 Less accumulated provision for depreciation (188 197) (182 282) Net plant in service 131 243

BALANCE SHEET Assets Property, plant and equipment: 30. 6. 2014 31. 12. 2013 Plant in service 319 440 319 081 Less accumulated provision for depreciation (188 197) (182 282) Net plant in service 131 243

How To Calculate A Trial Balance For A Company

THE BASIC MODEL The accounting information system is designed to collect and organize data into information that is useful for stakeholders. The Accounting Equation The basic accounting equation is what

THE BASIC MODEL The accounting information system is designed to collect and organize data into information that is useful for stakeholders. The Accounting Equation The basic accounting equation is what

Essentials of Financial Statement Analysis

Essentials of Financial Statement Analysis An Introduction to Financial Statement Analysis Gregory Mostyn, CPA Worthy and James Publishing www.worthyjames.com Essentials of Financial Statement Analysis

Essentials of Financial Statement Analysis An Introduction to Financial Statement Analysis Gregory Mostyn, CPA Worthy and James Publishing www.worthyjames.com Essentials of Financial Statement Analysis

! "#$ %&!& "& ' - 3+4 &*!&-.,,5///2!(.//+ & $!- )!* & % +, -).//0)& 7+00///2 *&&.4 &*!&- 7.00///2 )!*.//+ 8 -!% %& "#$ ) &!&.

!* & % +, -).//0)& 7+00///2 *&&.4 &*!&- 7.00///2 )!*.//+ 8 -!% %& #$ ) &!&.") ! "#!""#$%$#$#$"& $'"()*+,$-).,/ 012! "#$ %&!& "& '!(&)!*&%+,-).//0 -#$#3-4' &,'1$1# $!-!(.//0)& +01+///2 *&& - 3+4 &*!&-.,,5///2!(.//+ &!(!-6%(!(.//.$(!(.//0)& 01,///2 //+2% &*!&- 5,0///2 //32%!(.//+

! "#!""#$%$#$#$"& $'"()*+,$-).,/ 012! "#$ %&!& "& '!(&)!*&%+,-).//0 -#$#3-4' &,'1$1# $!-!(.//0)& +01+///2 *&& - 3+4 &*!&-.,,5///2!(.//+ &!(!-6%(!(.//.$(!(.//0)& 01,///2 //+2% &*!&- 5,0///2 //32%!(.//+

Completing the Accounting Cycle

C H A P T E R 4 Completing the Accounting Cycle Financial Accounting 14e Warren Reeve Duchac human/istock/360/getty Images Flow of Accounting Information (slide 1 of 5) End-of-Period Spreadsheet (Work

C H A P T E R 4 Completing the Accounting Cycle Financial Accounting 14e Warren Reeve Duchac human/istock/360/getty Images Flow of Accounting Information (slide 1 of 5) End-of-Period Spreadsheet (Work

Review of Accounting Principles

Appendix A Review of Accounting Principles Appendix A is a review of basic accounting principles and procedures. Standard accounting procedures are based on the double-entry system. This means that each

Appendix A Review of Accounting Principles Appendix A is a review of basic accounting principles and procedures. Standard accounting procedures are based on the double-entry system. This means that each

a. $ 65,000. b. $ 80,000. c. $130,000. d. $145,000.

注 意 1. 本 試 題 卷 共 50 題, 總 分 100 分 第 01-15 題, 每 題 1.75 分, 合 計 26.25 分 ; 第 16-35 題, 每 題 2 分, 合 計 40 分 ; 第 36-50 題, 每 題 2.25 分, 合 計 33.75 答 錯 不 倒 扣 2. 請 將 答 案 按 試 題 題 號, 依 序 填 入 答 案 卡 1.FastForward had cash

注 意 1. 本 試 題 卷 共 50 題, 總 分 100 分 第 01-15 題, 每 題 1.75 分, 合 計 26.25 分 ; 第 16-35 題, 每 題 2 分, 合 計 40 分 ; 第 36-50 題, 每 題 2.25 分, 合 計 33.75 答 錯 不 倒 扣 2. 請 將 答 案 按 試 題 題 號, 依 序 填 入 答 案 卡 1.FastForward had cash

Cash Flow Analysis. 15.511 Corporate Accounting Summer 2004. Professor SP Kothari. Sloan School of Management Massachusetts Institute of Technology

Cash Flow Analysis 15.511 Corporate Accounting Summer 2004 Professor SP Kothari Sloan School of Management Massachusetts Institute of Technology June 16, 2004 1 Statement of Cash Flows Reports operating

Cash Flow Analysis 15.511 Corporate Accounting Summer 2004 Professor SP Kothari Sloan School of Management Massachusetts Institute of Technology June 16, 2004 1 Statement of Cash Flows Reports operating

Midterm Fall 2012 Solution

Midterm Fall 2012 Solution Instructions: 1) Answers for the multiple-choice questions must be recorded on the UW answer card. All other questions must be answered in the space provided on the examination

Midterm Fall 2012 Solution Instructions: 1) Answers for the multiple-choice questions must be recorded on the UW answer card. All other questions must be answered in the space provided on the examination

NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS

NAS 03 NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-3 BENEFITS OF CASH FLOWS INFORMATION 4-5 DEFINITIONS 6-9 Cash and cash equivalents 7-9 PRESENTATION OF A

NAS 03 NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-3 BENEFITS OF CASH FLOWS INFORMATION 4-5 DEFINITIONS 6-9 Cash and cash equivalents 7-9 PRESENTATION OF A

TOPIC LEARNING OBJECTIVE

Topic Mapping 1 Transaction Analysis Understand the effect of various types of transactions on the accounting equation, accounting journal and accounting ledger. Concepts and Skills Accounting Equation

Topic Mapping 1 Transaction Analysis Understand the effect of various types of transactions on the accounting equation, accounting journal and accounting ledger. Concepts and Skills Accounting Equation

1. Operating, Investment and Financial Cash Flows

1. Operating, Investment and Financial Cash Flows Solutions Problem 1 During 2005, Myears Oil Co. had gross sales of $1 000,000, cost of goods sold of $400,000, and general and selling expenses of $300,000.

1. Operating, Investment and Financial Cash Flows Solutions Problem 1 During 2005, Myears Oil Co. had gross sales of $1 000,000, cost of goods sold of $400,000, and general and selling expenses of $300,000.

THEME: CASH FLOW. By John W. Day, MBA

THEME: CASH FLOW By John W. Day, MBA ACCOUNTING TERM: Cash Flow Cash flow is the difference between the cash in and cash out of a business during an accounting period. Stated differently, it is the amount

THEME: CASH FLOW By John W. Day, MBA ACCOUNTING TERM: Cash Flow Cash flow is the difference between the cash in and cash out of a business during an accounting period. Stated differently, it is the amount

CONSOLIDATED STATEMENT OF INCOME

CONSOLIDATED STATEMENT OF INCOME 4 th quarter (a) 3 rd quarter 4 th quarter 2009 Sales 40,157 40,180 36,228 Excise taxes (4,397) (4,952) (4,933) Revenues from sales 35,760 35,228 31,295 Purchases, net

CONSOLIDATED STATEMENT OF INCOME 4 th quarter (a) 3 rd quarter 4 th quarter 2009 Sales 40,157 40,180 36,228 Excise taxes (4,397) (4,952) (4,933) Revenues from sales 35,760 35,228 31,295 Purchases, net

Vol. 1, Chapter 7 The Statement of Cash Flows

Vol. 1, Chapter 7 The Statement of Cash Flows Problem 1: Solution Transaction # Identification 1 Operating 2 Investing 3 Noncash transaction 4 Financing 5 Noncash transaction 6 Operating 7 Investing 8

Vol. 1, Chapter 7 The Statement of Cash Flows Problem 1: Solution Transaction # Identification 1 Operating 2 Investing 3 Noncash transaction 4 Financing 5 Noncash transaction 6 Operating 7 Investing 8

Using Accounts to Interpret Performance

Using s to Interpret Performance ing information is used by stakeholders to judge the performance and efficiency of a business Different stakeholders will look for different things: STAKEHOLDER Shareholders

Using s to Interpret Performance ing information is used by stakeholders to judge the performance and efficiency of a business Different stakeholders will look for different things: STAKEHOLDER Shareholders

THE STATEMENT OF CASH FLOWS USING FINANCIAL STATEMENT EQUATIONS Harold Fletcher, Loyola University Maryland Thomas Ulrich, Loyola University Maryland

BUSINESS EDUCATION & ACCREDITATION Volume 2 Number 1 2010 THE STATEMENT OF CASH FLOWS USING FINANCIAL STATEMENT EQUATIONS Harold Fletcher, Loyola University Maryland Thomas Ulrich, Loyola University Maryland

BUSINESS EDUCATION & ACCREDITATION Volume 2 Number 1 2010 THE STATEMENT OF CASH FLOWS USING FINANCIAL STATEMENT EQUATIONS Harold Fletcher, Loyola University Maryland Thomas Ulrich, Loyola University Maryland

Statement of Cash Flows: Reporting and Analysis

Statement of Cash Flows: Reporting and Analysis Statement of Cash Flows: Reporting and Analysis Copyright 2014 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form

Statement of Cash Flows: Reporting and Analysis Statement of Cash Flows: Reporting and Analysis Copyright 2014 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form

Accounting and Reporting Policy FRS 102. Staff Education Note 1 Cash flow statements

Staff Education Note 1: Cash flow Statements Accounting and Reporting Policy FRS 102 Staff Education Note 1 Cash flow statements Disclaimer This Education Note has been prepared by FRC staff for the convenience

Staff Education Note 1: Cash flow Statements Accounting and Reporting Policy FRS 102 Staff Education Note 1 Cash flow statements Disclaimer This Education Note has been prepared by FRC staff for the convenience

International Financial Accounting (IFA)

") International Financial Accounting (IFA) Preparation and presentation of Financial Statements DEPARTMENT OF BUSINESS AND LAW ROBERTO DI PIETRA SIENA, NOVEMBER 4, 2013 1 INTERNATIONAL FINANCIAL ACCOUNTING

International Financial Accounting (IFA) Preparation and presentation of Financial Statements DEPARTMENT OF BUSINESS AND LAW ROBERTO DI PIETRA SIENA, NOVEMBER 4, 2013 1 INTERNATIONAL FINANCIAL ACCOUNTING

The Nature of Accounting Systems

Basic Accounting & Budgeting February 4, 2009 The Nature of Accounting Systems Accounting is the process of recording, classifying, summarizing, reporting and interpreting information about the economic

Basic Accounting & Budgeting February 4, 2009 The Nature of Accounting Systems Accounting is the process of recording, classifying, summarizing, reporting and interpreting information about the economic

2-8. Identify whether each of the following items increases or decreases cash flow:

Problems 2-8. Identify whether each of the following items increases or decreases cash flow: Increase in accounts receivable Increase in notes payable Depreciation expense Increase in investments Decrease

Problems 2-8. Identify whether each of the following items increases or decreases cash flow: Increase in accounts receivable Increase in notes payable Depreciation expense Increase in investments Decrease

Chapter. Statement of Cash Flows For Single Company

Chapter 4 Statement of Cash Flows For Single Company 4.1 Single company statement of cash flows Statement of cash flows are primary financial statements and are required along side the income statement

Chapter 4 Statement of Cash Flows For Single Company 4.1 Single company statement of cash flows Statement of cash flows are primary financial statements and are required along side the income statement

MIDTERM EXAMINATION. [email protected]. Fall 2009

MIDTERM EXAMINATION [email protected] Fall 2009 FIN621- Financial Statement Analysis Asslam O Alikum FIN621- Financial Statement Analysis (Session 3) solved by Afaaq n Shani Bhai with reference n numerical

MIDTERM EXAMINATION [email protected] Fall 2009 FIN621- Financial Statement Analysis Asslam O Alikum FIN621- Financial Statement Analysis (Session 3) solved by Afaaq n Shani Bhai with reference n numerical

Accounting Self Study Guide for Staff of Micro Finance Institutions

Accounting Self Study Guide for Staff of Micro Finance Institutions LESSON 2 The Balance Sheet OBJECTIVES The purpose of this lesson is to introduce the Balance Sheet and explain its components: Assets,

Accounting Self Study Guide for Staff of Micro Finance Institutions LESSON 2 The Balance Sheet OBJECTIVES The purpose of this lesson is to introduce the Balance Sheet and explain its components: Assets,

SOLUTIONS. Learning Goal 15

Learning Goal 15: Prepare a Classified S1 Learning Goal 15 Multiple Choice 1. b 2. c 3. a 4. b 5. d 6. a 7. c Their importance in paying current liabilities is the main reason current assets are shown

Learning Goal 15: Prepare a Classified S1 Learning Goal 15 Multiple Choice 1. b 2. c 3. a 4. b 5. d 6. a 7. c Their importance in paying current liabilities is the main reason current assets are shown

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods TABLE OF CONTENTS

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods 1.0 FINANCIAL FORECASTING METHODS 1.01 Introduction

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods 1.0 FINANCIAL FORECASTING METHODS 1.01 Introduction

Consolidated balance sheet

83 Consolidated balance sheet December 31 Non-current assets Goodwill 14 675.1 978.4 Other intangible assets 14 317.4 303.8 Property, plant, and equipment 15 530.7 492.0 Investment in associates 16 2.5

83 Consolidated balance sheet December 31 Non-current assets Goodwill 14 675.1 978.4 Other intangible assets 14 317.4 303.8 Property, plant, and equipment 15 530.7 492.0 Investment in associates 16 2.5

Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows

7 Statement of Cash Flows") Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

6. Depreciation is a process of a. asset devaluation. b. cost accumulation. c. cost allocation. d. asset valuation.

1. A company purchased land for $72,000 cash. Real estate brokers' commission was $5,000 and $7,000 was spent for demolishing an old building on the land before construction of a new building could start.

1. A company purchased land for $72,000 cash. Real estate brokers' commission was $5,000 and $7,000 was spent for demolishing an old building on the land before construction of a new building could start.

Chapter 8 Accounting for Receivables

Chapter 8 Accounting for Receivables Accounts Receivable Accounts Receivables are current assets. They are usually expected to be collected within 30 days. Allowance Method and Bad Debt Expense 2 methods:

Chapter 8 Accounting for Receivables Accounts Receivable Accounts Receivables are current assets. They are usually expected to be collected within 30 days. Allowance Method and Bad Debt Expense 2 methods:

In this chapter, we build on the basic knowledge of how businesses

03-Seidman.qxd 5/15/04 11:52 AM Page 41 3 An Introduction to Business Financial Statements In this chapter, we build on the basic knowledge of how businesses are financed by looking at how firms organize

03-Seidman.qxd 5/15/04 11:52 AM Page 41 3 An Introduction to Business Financial Statements In this chapter, we build on the basic knowledge of how businesses are financed by looking at how firms organize

Modeling Readiness Quiz

Modeling Readiness Quiz 1 Dear Students, Modeling Readiness Quiz Prepared by Prof. Dan Gode http://www.dangode.com Modeling is a useful course, but it also a rigorous and demanding elective. In the future,

Modeling Readiness Quiz 1 Dear Students, Modeling Readiness Quiz Prepared by Prof. Dan Gode http://www.dangode.com Modeling is a useful course, but it also a rigorous and demanding elective. In the future,

Chapter 002 Financial Statements, Taxes and Cash Flow

Multiple Choice Questions 1. The financial statement summarizing the value of a firm's equity on a particular date is the: a. income statement. B. balance sheet. c. statement of cash flows. d. cash flow

Multiple Choice Questions 1. The financial statement summarizing the value of a firm's equity on a particular date is the: a. income statement. B. balance sheet. c. statement of cash flows. d. cash flow

ICAP GROUP S.A. FINANCIAL RATIOS EXPLANATION

ICAP GROUP S.A. FINANCIAL RATIOS EXPLANATION OCTOBER 2006 Table of Contents 1. INTRODUCTION... 3 2. FINANCIAL RATIOS FOR COMPANIES (INDUSTRY - COMMERCE - SERVICES) 4 2.1 Profitability Ratios...4 2.2 Viability

ICAP GROUP S.A. FINANCIAL RATIOS EXPLANATION OCTOBER 2006 Table of Contents 1. INTRODUCTION... 3 2. FINANCIAL RATIOS FOR COMPANIES (INDUSTRY - COMMERCE - SERVICES) 4 2.1 Profitability Ratios...4 2.2 Viability

Accounting Cycle. Matching Principle

CHAPTER 3 Accounting Cycle Analyze and record the transactions Post the transactions and prepare trial balance Adjust the accounts and prepare trial balance Prepare the financial statements Close the accounts

CHAPTER 3 Accounting Cycle Analyze and record the transactions Post the transactions and prepare trial balance Adjust the accounts and prepare trial balance Prepare the financial statements Close the accounts

INTRODUCTION TO FARM AND RANCH ACCOUNTING USING QUICKEN

INTRODUCTION TO FARM AND RANCH ACCOUNTING USING QUICKEN Larry K. Bond Extension Economist and Associate Professor Department of Economics Utah State University May 1995 Economic Institute Study Paper ~

INTRODUCTION TO FARM AND RANCH ACCOUNTING USING QUICKEN Larry K. Bond Extension Economist and Associate Professor Department of Economics Utah State University May 1995 Economic Institute Study Paper ~