The Basic Framework of Budgeting

|

|

|

- Annabelle Mills

- 10 years ago

- Views:

Transcription

1 Master Budgeting 1

2 The Basic Framework of Budgeting A budget is a detailed quantitative plan for acquiring and using financial and other resources over a specified forthcoming time period. 1. The act of preparing a budget is called budgeting. 2. The use of budgets to control an organization s activity is known as budgetary control. 2

3 Planning and Control Planning Control involves developing involves the steps objectives and taken by preparing various management that budgets to achieve attempt to ensure these objectives. the objectives are attained. 3

4 Advantages of Budgeting Define goal and objectives Communicate Think about and plans plan for the future Coordinate activities Advantages Uncover potential bottlenecks Means of allocating resources 4

5 Choosing the Budget Period Operating Budget The annual operating budget may be divided into quarterly or monthly budgets. A continuous budget is a 12-month budget that rolls forward one month (or quarter) as the current month (or quarter) is completed. 5

6 The Master Budget: An Overview Ending Finished Goods Budget Sales Budget Production Budget Selling and Administrative Budget Direct Materials Budget Direct Labor Budget Manufacturing Overhead Budget Cash Budget Budgeted Financial Statements 6

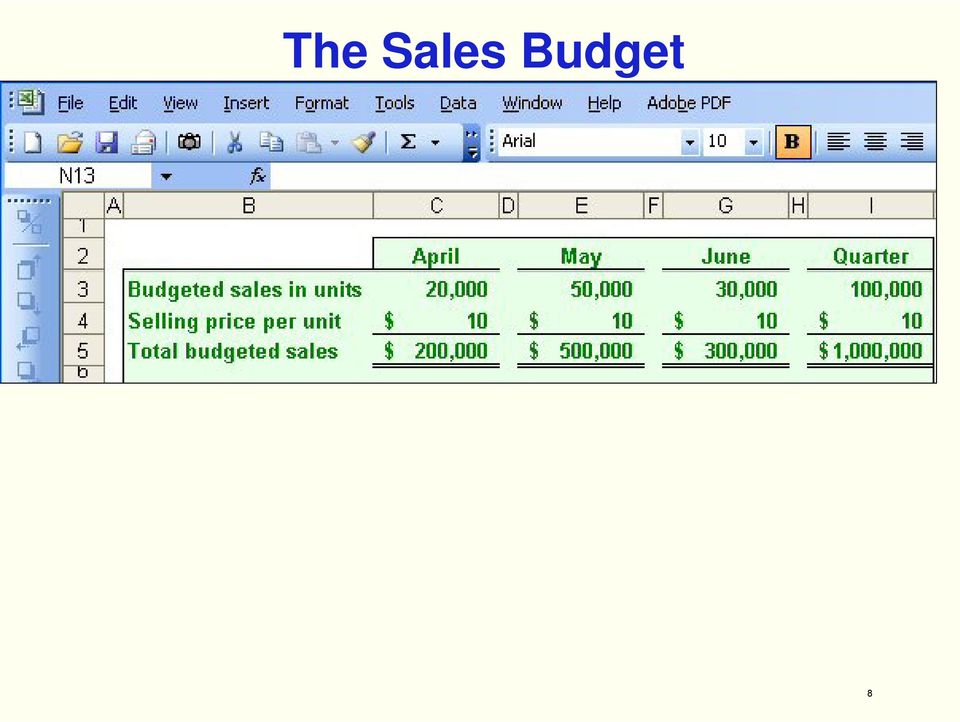

7 Budgeting Example Royal l Company is preparing budgets for the quarter ending June 30. Budgeted sales for the next five months are: April May June July August 20,000 units 50,000 units 30,000 units 25,000 units 15,000 units. The selling price is $10 per unit. 7

8 The Sales Budget 8

9 Expected Cash Collections All sales are on account. Royal s collection pattern is: 70% collected in the month of sale, 25% collected in the month following sale, 5% uncollectible. The March 31 accounts receivable balance of $30,000 will be collected in full. 9

10 Expected Cash Collections From the Sales Budget for May. 10

11 The Production Budget Sales Budget and Expected Cash Collections Production Budget Production must be adequate to meet budgeted sales and provide for sufficient ending inventory. 11

12 The Production Budget The management at Royal Company wants ending inventory to be equal to 20% of the following month s budgeted d sales in units. On March 31, 4,000 units were on hand. Let s prepare the production budget. 12

13 The Production Budget Assumed ending inventory. 13

14 The Production Budget 14

15 The Direct Materials Budget At Royal Company, five pounds of material are required per unit of product. Management wants materials on hand at the end of each month equal to 10% of the following month s production. On March 31, 13,000 pounds of material are on hand. Material cost is $0.40 per pound. Let s prepare p the direct materials budget. 15

16 The Direct Materials Budget Assumed ending inventory 16

17 The Direct Materials Budget 17

18 Expected Cash Disbursement for Materials Royal pays $0.40 per pound for its materials. One-half of a month s purchases is paid for in the month of purchase; the other half is paid in the following month. The March 31 accounts payable balance is $12,000. Let s calculate expected cash disbursements. 18

19 Expected Cash Disbursement for Materials Compute the expected cash disbursements for materials for the quarter. 140,000 lbs. $.40/lb. = $56,000 19

20 The Direct Labor Budget At Royal, each unit of product requires 005hours 0.05 (3 minutes) of direct labor. The Company has a no layoff policy so all employees will be paid for 40 hours of work each week. In exchange for the no layoff policy, workers agree to a wage rate of $10 per hour regardless of the hours worked (no overtime pay). For the next three months, the direct labor workforce will be paid for a minimum i of 1,500 hours per month. Let s prepare the direct labor budget. 20

.")

21 The Direct Labor Budget 21

22 Manufacturing Overhead Budget At Royal, manufacturing overhead is applied to units of product on the basis of direct labor hours. The variable manufacturing overhead rate is $20 per direct labor hour. Fixed manufacturing overhead is $50,000 per month and includes $20,000 of noncash costs (primarily depreciation of plant assets). Let s prepare the manufacturing overhead budget. 22

23 Manufacturing Overhead Budget 23

24 Manufacturing Overhead Budget Depreciation is a noncash charge. 24

25 Ending Finished Goods Inventory Budget Production costs per unit Quantity Cost Total Direct materials 5.00 lbs. $ 0.40 $ 2.00 Direct labor 0.05 hrs. $ Manufacturing overhead 0.05 hrs. $ $ 4.99 Budgeted finished goods inventory Ending inventory in units 5,000 Unit product cost $ 4.99 Ending finished goods inventory $ 24,950 Production Budget. 25

26 Selling and Administrative Expense Budget At Royal, the selling and administrative expenses budget is divided id d into variable and fixed components. The variable selling and administrative expenses are $0.50 per unit sold. Fixed selling and administrative expenses are $70,000 per month. The fixed selling and administrative expenses include $10, in costs primarily depreciation that are not cash outflows of the current month. Let s prepare the company s selling and administrative expense budget. 26

27 Selling and Administrative Expense Budget 27

28 Selling and Administrative Expense Budget Calculate the selling and administrative cash expenses for the quarter. 28

29 The Cash Budget Royal: Maintains a 16% open line of credit for $75,000 Maintains a minimum cash balance of $30,000 Borrows on the first day of the month and repays loans on the last day of the quarter. Pays a cash dividend of $49,000 in April Purchases $143,700 of equipment in May and $48,300 in June (both purchases paid in cash) Has an April 1 cash balance of $40,

30 The Cash Budget $50, % 3/12 = $2,000 Borrowings on April 1 and repayment on June

31 The Budgeted Income Statement Cash Budget Budgeted Income Statement After we complete the cash budget, we can prepare the budgeted income statement for Royal. 31

32 The Budgeted Income Statement Royal Company Budgeted Income Statement For the Three Months Ended June 30 Sales (100,000 $10) $ 1,000,000 Cost of goods sold (100,000 $4.99) 499,000 Gross margin 501,000 Selling and administrative expenses 260,000 Operating income 241,000 Interest expense 2,000 Net income $ 239,000 Sales Budget. Ending Finished Goods Inventory. Selling and Administrative Expense Budget. Cash Budget. 32

33 The Budgeted Balance Sheet Royal reported the following account balances prior to preparing its budgeted financial statements: Land - $50, Common stock - $200,000 Retained earnings - $146, Equipment - $175,000 33

34 Royal Company Budgeted Balance Sheet June 30 Current assets Cash $ 43,000 Accounts receivable 75,000 Raw materials inventory 4,600 Finished goods inventory 24,950 Total current assets 147,550 Property and equipment Land 50,000 Equipment 367,000 Total property and equipment 417,000 Total assets $ 564,550 Accounts payable $ 28,400 Common stock 200,000 Retained earnings 336,150 Total liabilities and equities $ 564,550 25% of June sales of $300, ,500 lbs. at $0.40/lb. 5,000 units at $4.99 each. 50% of June purchases of $56,

35 Royal Company Budgeted Balance Sheet June 30 Current assets Cash $ 43,000 Accounts receivable 75,000 Raw materials inventory 4,600 Finished goods inventory 24,950 Total current assets 147,550 Property and equipment Land 50,000 Equipment 367,000 Total property and equipment 417,000 Total assets $ 564,550 Beginning balance $ 146,150 Add: net income 239,000 Deduct: dividends (49,000) Ending balance $ 336,150 Accounts payable $ 28,400 Common stock 200,000 Retained earnings 336,150 Total liabilities and equities $ 564,550 35

MASTER BUDGET - EXAMPLE

MASTER BUDGET - EXAMPLE Sales IN UNITS for the previous two months (of last quarter), as well as the sales forecast for next quarter are as follows: Sales Budget Units May sales (ACTUAL) 20 June sales

MASTER BUDGET - EXAMPLE Sales IN UNITS for the previous two months (of last quarter), as well as the sales forecast for next quarter are as follows: Sales Budget Units May sales (ACTUAL) 20 June sales

Dutchess Community College ACC 204 Managerial Accounting Quiz Prep Chapter 9

Dutchess Community College ACC 204 Managerial Accounting Quiz Prep Chapter 9 Budgetary Planning Peter Rivera March 2011 Disclaimer This Quiz Prep is provided as an outline of the key concepts from the

Dutchess Community College ACC 204 Managerial Accounting Quiz Prep Chapter 9 Budgetary Planning Peter Rivera March 2011 Disclaimer This Quiz Prep is provided as an outline of the key concepts from the

COMPONENTS OF THE STATEMENT OF CASH FLOWS

ILLUSTRATION 24-1 OPERATING, INVESTING, AND FINANCING ACTIVITIES COMPONENTS OF THE STATEMENT OF CASH FLOWS CASH FLOWS FROM OPERATING ACTIVITIES + Sales and Service Revenue Received Cost of Sales Paid Selling

ILLUSTRATION 24-1 OPERATING, INVESTING, AND FINANCING ACTIVITIES COMPONENTS OF THE STATEMENT OF CASH FLOWS CASH FLOWS FROM OPERATING ACTIVITIES + Sales and Service Revenue Received Cost of Sales Paid Selling

Chapter 6 Statement of Cash Flows

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

2-8. Identify whether each of the following items increases or decreases cash flow:

Problems 2-8. Identify whether each of the following items increases or decreases cash flow: Increase in accounts receivable Increase in notes payable Depreciation expense Increase in investments Decrease

Problems 2-8. Identify whether each of the following items increases or decreases cash flow: Increase in accounts receivable Increase in notes payable Depreciation expense Increase in investments Decrease

CH 23 STATEMENT OF CASH FLOWS SELF-STUDY QUESTIONS

C H 2 3, P a g e 1 CH 23 STATEMENT OF CASH FLOWS SELF-STUDY QUESTIONS (note from Dr. N: I have deleted questions for you to omit, but did not renumber the remaining questions) 1. The primary purpose of

C H 2 3, P a g e 1 CH 23 STATEMENT OF CASH FLOWS SELF-STUDY QUESTIONS (note from Dr. N: I have deleted questions for you to omit, but did not renumber the remaining questions) 1. The primary purpose of

Ratio Analysis. A) Liquidity Ratio : - 1) Current ratio = Current asset Current Liability

Liquidity Ratio : - 1) Current ratio = Current asset Current Liability") A) Liquidity Ratio : - Ratio Analysis 1) Current ratio = Current asset Current Liability 2) Quick ratio or Acid Test ratio = Quick Asset Quick liability Quick Asset = Current Asset Stock Quick Liability

A) Liquidity Ratio : - Ratio Analysis 1) Current ratio = Current asset Current Liability 2) Quick ratio or Acid Test ratio = Quick Asset Quick liability Quick Asset = Current Asset Stock Quick Liability

Model is used to calculate Financial Statements on a Quarterly Basis for a One Year period. Model provides the ability to:

ADDITIONAL REFERENCES AND FINANCIAL MODELS: For more information about financial statements and terms refer to e book, How to Read Financial Statements. Advanced financial models providing 5 year projections

ADDITIONAL REFERENCES AND FINANCIAL MODELS: For more information about financial statements and terms refer to e book, How to Read Financial Statements. Advanced financial models providing 5 year projections

CASH FLOW STATEMENT (AND FINANCIAL STATEMENT)

") CASH FLOW STATEMENT (AND FINANCIAL STATEMENT) - At the most fundamental level, firms do two different things: (i) They generate cash (ii) They spend it. Cash is generated by selling a product, an asset

CASH FLOW STATEMENT (AND FINANCIAL STATEMENT) - At the most fundamental level, firms do two different things: (i) They generate cash (ii) They spend it. Cash is generated by selling a product, an asset

ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL)

") Page 1 ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL) Complete these sample exam problems/objective questions and check your answers with the solutions at the end of the review file and identify where

Page 1 ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL) Complete these sample exam problems/objective questions and check your answers with the solutions at the end of the review file and identify where

Statement of Cash Flows

THE CONTENT AND VALUE OF THE STATEMENT OF CASH FLOWS The cash flow statement reconciles beginning and ending cash by presenting the cash receipts and cash disbursements of an enterprise for an accounting

THE CONTENT AND VALUE OF THE STATEMENT OF CASH FLOWS The cash flow statement reconciles beginning and ending cash by presenting the cash receipts and cash disbursements of an enterprise for an accounting

Financial Statements

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

EXERCISES. The cash from operating activities detail is provided as follows for class discussion:

EXERCISES Ex. 14 1 There were net additions, such as depreciation and amortization of intangible assets of $389 million, to the net loss reported on the income statement to convert the net loss from the

EXERCISES Ex. 14 1 There were net additions, such as depreciation and amortization of intangible assets of $389 million, to the net loss reported on the income statement to convert the net loss from the

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods TABLE OF CONTENTS

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods 1.0 FINANCIAL FORECASTING METHODS 1.01 Introduction

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods 1.0 FINANCIAL FORECASTING METHODS 1.01 Introduction

Understanding A Firm s Financial Statements

CHAPTER OUTLINE Spotlight: J&S Construction Company (http://www.jsconstruction.com) 1 The Lemonade Kids Financial statement (accounting statements) reports of a firm s financial performance and resources,

CHAPTER OUTLINE Spotlight: J&S Construction Company (http://www.jsconstruction.com) 1 The Lemonade Kids Financial statement (accounting statements) reports of a firm s financial performance and resources,

Income Measurement and Profitability Analysis

PROFITABILITY ANALYSIS The following financial statements for Spencer Company will be used to demonstrate the calculation of the various ratios in profitability analysis. Spencer Company Comparative Balance

PROFITABILITY ANALYSIS The following financial statements for Spencer Company will be used to demonstrate the calculation of the various ratios in profitability analysis. Spencer Company Comparative Balance

1. Operating, Investment and Financial Cash Flows

1. Operating, Investment and Financial Cash Flows Solutions Problem 1 During 2005, Myears Oil Co. had gross sales of $1 000,000, cost of goods sold of $400,000, and general and selling expenses of $300,000.

1. Operating, Investment and Financial Cash Flows Solutions Problem 1 During 2005, Myears Oil Co. had gross sales of $1 000,000, cost of goods sold of $400,000, and general and selling expenses of $300,000.

TOPIC LEARNING OBJECTIVE

Topic Mapping 1 Transaction Analysis Understand the effect of various types of transactions on the accounting equation, accounting journal and accounting ledger. Concepts and Skills Accounting Equation

Topic Mapping 1 Transaction Analysis Understand the effect of various types of transactions on the accounting equation, accounting journal and accounting ledger. Concepts and Skills Accounting Equation

Receivables from August sales: $400,000 x 20% = $ 80,000 Receivables from September sales: $180,000 x (50% + 20%) = 126,000 Total $ 206,000

= 126,000 Total $ 206,000") EXERCISE 8-3 (15 minutes) 1. Schedule of Budgeted Collections Third Quarter, Year 5 Quarter July August September Total May sales x 20% $38,000 $38,000 June sales x 50%,20% 105,000 $42,000 147,000 July

EXERCISE 8-3 (15 minutes) 1. Schedule of Budgeted Collections Third Quarter, Year 5 Quarter July August September Total May sales x 20% $38,000 $38,000 June sales x 50%,20% 105,000 $42,000 147,000 July

BACKGROUND KNOWLEDGE for Teachers and Students

Pathway: Business, Marketing, and Computer Education Lesson: BMM C6 4: Financial Statements and Reports Common Core State Standards for Mathematics: N.Q.2 Domain: Quantities Cluster: Reason quantitatively

Pathway: Business, Marketing, and Computer Education Lesson: BMM C6 4: Financial Statements and Reports Common Core State Standards for Mathematics: N.Q.2 Domain: Quantities Cluster: Reason quantitatively

Vol. 1, Chapter 7 The Statement of Cash Flows

Vol. 1, Chapter 7 The Statement of Cash Flows Problem 1: Solution Transaction # Identification 1 Operating 2 Investing 3 Noncash transaction 4 Financing 5 Noncash transaction 6 Operating 7 Investing 8

Vol. 1, Chapter 7 The Statement of Cash Flows Problem 1: Solution Transaction # Identification 1 Operating 2 Investing 3 Noncash transaction 4 Financing 5 Noncash transaction 6 Operating 7 Investing 8

STATEMENT ON FINANCIAL POSITION

STATEMENT ON FINANCIAL POSITION DESCRIPTION NOTE DAY 30.06.2013 31.12.2012 Fixed assets 218 532 221 493 214 682 Intangibles 3 583 3 057 3 033 Tangible fixed assets 2 69 812 69 272 63 027 Investment properties

STATEMENT ON FINANCIAL POSITION DESCRIPTION NOTE DAY 30.06.2013 31.12.2012 Fixed assets 218 532 221 493 214 682 Intangibles 3 583 3 057 3 033 Tangible fixed assets 2 69 812 69 272 63 027 Investment properties

Guide to Financial Statements Study Guide

Guide to Financial Statements Study Guide Overview (Topic 1) Three major financial statements: The Income Statement The Balance Sheet The Cash Flow Statement Objectives: Explain the underlying equation

Guide to Financial Statements Study Guide Overview (Topic 1) Three major financial statements: The Income Statement The Balance Sheet The Cash Flow Statement Objectives: Explain the underlying equation

Exercise 17-1 (15 minutes)

") Exercise 17-1 (15 minutes) 1. 2002 2001 Sales... 100.0% 100.0 % Less cost of goods sold... 63.2 60.0 Gross margin... 36.8 40.0 Selling expenses... 18.0 17.5 Administrative expenses... 13.6 14.6 Total expenses...

Exercise 17-1 (15 minutes) 1. 2002 2001 Sales... 100.0% 100.0 % Less cost of goods sold... 63.2 60.0 Gross margin... 36.8 40.0 Selling expenses... 18.0 17.5 Administrative expenses... 13.6 14.6 Total expenses...

APPENDIX 1 The Statement of Financial Position

APPENDIX 1 The Statement of Financial Position 1. Assets: the resources of the organization which are used to provide service and generate value 2. Current assets: assets which can be converted to cash

APPENDIX 1 The Statement of Financial Position 1. Assets: the resources of the organization which are used to provide service and generate value 2. Current assets: assets which can be converted to cash

Working Capital Concept & Animation

Working Capital Concept & Animation Meaning A measure of both a company's efficiency and its short-term financial health. The working capital is calculated as: Working Capital = Current Assets Current

Working Capital Concept & Animation Meaning A measure of both a company's efficiency and its short-term financial health. The working capital is calculated as: Working Capital = Current Assets Current

CASH FLOW STATEMENT. MODULE - 6A Analysis of Financial Statements. Cash Flow Statement. Notes

MODULE - 6A Cash Flow Statement 30 CASH FLOW STATEMENT In the previous lesson, you have learnt various types of analysis of financial statements and its tools such as comparative statements, common size

MODULE - 6A Cash Flow Statement 30 CASH FLOW STATEMENT In the previous lesson, you have learnt various types of analysis of financial statements and its tools such as comparative statements, common size

Section A: Questions On Fill In The Blanks

Section A : 26 FILL IN THE BLANK Section B : 10 TRUE OR FALSE QUESTIONS Section C : 11 Multiple Choice Questions Section A: Questions Fill In The Blanks the right column please insert the items from which

Section A : 26 FILL IN THE BLANK Section B : 10 TRUE OR FALSE QUESTIONS Section C : 11 Multiple Choice Questions Section A: Questions Fill In The Blanks the right column please insert the items from which

Statement of Change in Working Capital & Inflows/Outflows of Working Capital

HOSP 2110 (Management Acct) Learning Centre Statement of Change in Working Capital & Inflows/Outflows of Working Capital The statement of changes in working capital shows the net change in working capital

HOSP 2110 (Management Acct) Learning Centre Statement of Change in Working Capital & Inflows/Outflows of Working Capital The statement of changes in working capital shows the net change in working capital

The estimated total cash collections during April from sales and accounts receivables would be: A) $155,900. B) $167,000. C) $171,666. D) $173,400.

$155,900. B) $167,000. C) $171,666. D) $173,400.") 1. Orion Corporation is preparing a cash budget for the six months beginning January 1. Shown below are the company's expected collection pattern and the budgeted sales for the period. Expected collection

1. Orion Corporation is preparing a cash budget for the six months beginning January 1. Shown below are the company's expected collection pattern and the budgeted sales for the period. Expected collection

Financial. Management FOR A SMALL BUSINESS

Financial Management FOR A SMALL BUSINESS 1 Agenda Welcome, Pre-Test, Agenda, and Learning Objectives Benefits of Financial Management Budgeting Bookkeeping Financial Statements Business Financing Key

Financial Management FOR A SMALL BUSINESS 1 Agenda Welcome, Pre-Test, Agenda, and Learning Objectives Benefits of Financial Management Budgeting Bookkeeping Financial Statements Business Financing Key

Using Accounts to Interpret Performance

Using s to Interpret Performance ing information is used by stakeholders to judge the performance and efficiency of a business Different stakeholders will look for different things: STAKEHOLDER Shareholders

Using s to Interpret Performance ing information is used by stakeholders to judge the performance and efficiency of a business Different stakeholders will look for different things: STAKEHOLDER Shareholders

1. A set of procedures for controlling cash payments by preparing and approving vouchers before payments are made is known as a voucher system.

Accounting II True/False Indicate whether the sentence or statement is true or false. 1. A set of procedures for controlling cash payments by preparing and approving vouchers before payments are made is

Accounting II True/False Indicate whether the sentence or statement is true or false. 1. A set of procedures for controlling cash payments by preparing and approving vouchers before payments are made is

The Statement of Cash Flows Direct Method

23 The Statement of Cash Flows Direct Method DEMONSTRATION PROBLEM The financial statements of Bolero Corporation follow. Copyright Houghton Mifflin Company. All rights reserved. 1 Bolero Corporation Income

23 The Statement of Cash Flows Direct Method DEMONSTRATION PROBLEM The financial statements of Bolero Corporation follow. Copyright Houghton Mifflin Company. All rights reserved. 1 Bolero Corporation Income

Management Accounting and Decision-Making

Management Accounting 15 Management Accounting and Decision-Making Management accounting writers tend to present management accounting as a loosely connected set of decision making tools. Although the

Management Accounting 15 Management Accounting and Decision-Making Management accounting writers tend to present management accounting as a loosely connected set of decision making tools. Although the

Total shares at the end of ten years is 100*(1+5%) 10 =162.9.

10 =162.9.") FCS5510 Sample Homework Problems Unit04 CHAPTER 8 STOCK PROBLEMS 1. An investor buys 100 shares if a $40 stock that pays a annual cash dividend of $2 a share (a 5% dividend yield) and signs up for the

FCS5510 Sample Homework Problems Unit04 CHAPTER 8 STOCK PROBLEMS 1. An investor buys 100 shares if a $40 stock that pays a annual cash dividend of $2 a share (a 5% dividend yield) and signs up for the

LEBANESE ASSOCIATION OF CERTIFIED PUBLIC ACCOUNTANTS MANAGERIAL ACCOUNTING

LEBANESE ASSOCIATION OF CERTIFIED PUBLIC ACCOUNTANTS MANAGERIAL ACCOUNTING JULY 2015 MULTIPLE CHOICE QUESTIONS (37.5%) Choose the correct answer 1. All of the following statements concerning standard costs

LEBANESE ASSOCIATION OF CERTIFIED PUBLIC ACCOUNTANTS MANAGERIAL ACCOUNTING JULY 2015 MULTIPLE CHOICE QUESTIONS (37.5%) Choose the correct answer 1. All of the following statements concerning standard costs

Cash is King. cash flow is less likely to be affected

Reading 27: Understanding Cash Flow Statements Relevance of Cash Flow The primary purpose of the statement of cash flows (SCF) is to provide: Info about a firm s cash receipts & cash payments during an

Reading 27: Understanding Cash Flow Statements Relevance of Cash Flow The primary purpose of the statement of cash flows (SCF) is to provide: Info about a firm s cash receipts & cash payments during an

Plan and Track Your Finances

Chapter 9 Plan and Track Your Finances 9.1 Finance Your Business 9.2 Pro Forma Financial Statements 9.3 Record Keeping for Businesses Ideas in Action Electronic Safekeeping Katelin Shea addressed the unmet

Chapter 9 Plan and Track Your Finances 9.1 Finance Your Business 9.2 Pro Forma Financial Statements 9.3 Record Keeping for Businesses Ideas in Action Electronic Safekeeping Katelin Shea addressed the unmet

Chapter 14. 1 Copyright 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Chapter 14 1 Identify the purposes of the statement of cash flows Distinguish among operating, investing, and financing cash flows Prepare the statement of cash flows by the indirect method Identify noncash

Chapter 14 1 Identify the purposes of the statement of cash flows Distinguish among operating, investing, and financing cash flows Prepare the statement of cash flows by the indirect method Identify noncash

> DO IT! Chapter 13. Classification of Cash Flows. Cash from Operating Activities D-1. Solution. Action Plan

Chapter 13 > DO IT! Classification of Cash Flows Identify the three types of activities used to report all cash inflows and outflows. Report as operating activities the cash effects of transactions that

Chapter 13 > DO IT! Classification of Cash Flows Identify the three types of activities used to report all cash inflows and outflows. Report as operating activities the cash effects of transactions that

Chapter 9 Profit Planning

Chapter 9 Profit Planning Solutions to Questions 9-1 A budget is a detailed quantitative plan for the acquisition and use of financial and other resources over a given time period. Budgetary control involves

Chapter 9 Profit Planning Solutions to Questions 9-1 A budget is a detailed quantitative plan for the acquisition and use of financial and other resources over a given time period. Budgetary control involves

Summary of Financial Report for the FY ending March 2015 (Non-Consolidated)

") Summary of Financial Report for the FY ending March 2015 (Non-Consolidated) April 30, 2015 Listed Company Name: Japan Tissue Engineering Co., Ltd. Listed Securities Exchange: JQ Stock Code: 7774 URL http://www.jpte.co.jp

Summary of Financial Report for the FY ending March 2015 (Non-Consolidated) April 30, 2015 Listed Company Name: Japan Tissue Engineering Co., Ltd. Listed Securities Exchange: JQ Stock Code: 7774 URL http://www.jpte.co.jp

FINANCIAL MANAGEMENT

100 Arbor Drive, Suite 108 Christiansburg, VA 24073 Voice: 540-381-9333 FAX: 540-381-8319 www.becpas.com Providing Professional Business Advisory & Consulting Services Douglas L. Johnston, II [email protected]

100 Arbor Drive, Suite 108 Christiansburg, VA 24073 Voice: 540-381-9333 FAX: 540-381-8319 www.becpas.com Providing Professional Business Advisory & Consulting Services Douglas L. Johnston, II [email protected]

Teaching the Budgeting Process Using a Spreadsheet Template

Teaching the Budgeting Process Using a Spreadsheet Template Benoît N. Boyer, Professor of Accounting and Chair of the Accounting and Information Systems Department, Sacred Heart University, Fairfield,

Teaching the Budgeting Process Using a Spreadsheet Template Benoît N. Boyer, Professor of Accounting and Chair of the Accounting and Information Systems Department, Sacred Heart University, Fairfield,

In this chapter, we build on the basic knowledge of how businesses

03-Seidman.qxd 5/15/04 11:52 AM Page 41 3 An Introduction to Business Financial Statements In this chapter, we build on the basic knowledge of how businesses are financed by looking at how firms organize

03-Seidman.qxd 5/15/04 11:52 AM Page 41 3 An Introduction to Business Financial Statements In this chapter, we build on the basic knowledge of how businesses are financed by looking at how firms organize

Preparing a Successful Financial Plan

Topic 9 Preparing a Successful Financial Plan LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Describe the overview of accounting methods; 2. Prepare the three major financial statements

Topic 9 Preparing a Successful Financial Plan LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Describe the overview of accounting methods; 2. Prepare the three major financial statements

Consolidated Statement of Profit or Loss (in million Euro)

") Consolidated Statement of Profit or Loss (in million Euro) Q3 2013 Q3 2014 % change 9m 2013 9m 2014 % change Revenue 689 636-7.7% 2,126 1,909-10.2% Cost of sales (497) (440) -11.5% (1,520) (1,324) -12.9%

Consolidated Statement of Profit or Loss (in million Euro) Q3 2013 Q3 2014 % change 9m 2013 9m 2014 % change Revenue 689 636-7.7% 2,126 1,909-10.2% Cost of sales (497) (440) -11.5% (1,520) (1,324) -12.9%

GVEP Workshop Finance 101

GVEP Workshop Finance 101 Nairobi, January 2013 Agenda Introducing business finance Understanding financial statements Understanding cash flow LUNCH Reading and interpreting financial statements Evaluating

GVEP Workshop Finance 101 Nairobi, January 2013 Agenda Introducing business finance Understanding financial statements Understanding cash flow LUNCH Reading and interpreting financial statements Evaluating

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased.

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased. Accounts Receivable are the total amounts customers owe your business for goods or services sold

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased. Accounts Receivable are the total amounts customers owe your business for goods or services sold

Business Plan. In completing the following proposal provide as much detailed information as possible.

Business Plan A business plan is an integral part of a financing request. It is an introduction to your business, and it provides us with the initial information that we require to start to an application.

Business Plan A business plan is an integral part of a financing request. It is an introduction to your business, and it provides us with the initial information that we require to start to an application.

Chapter Financial Forecasting

Chapter Financial Forecasting PPT 4-2 Chapter 4 - Outline What is Financial Forecasting? 3 Financial Statements for Forecasting Constructing Pro Forma Statements Basis for Sales Projections Steps in a

Chapter Financial Forecasting PPT 4-2 Chapter 4 - Outline What is Financial Forecasting? 3 Financial Statements for Forecasting Constructing Pro Forma Statements Basis for Sales Projections Steps in a

EMERSON AND SUBSIDIARIES CONSOLIDATED OPERATING RESULTS (AMOUNTS IN MILLIONS EXCEPT PER SHARE, UNAUDITED)

") CONSOLIDATED OPERATING RESULTS (AMOUNTS IN MILLIONS EXCEPT PER SHARE, UNAUDITED) TABLE 1 Quarter Ended March 31, Percent Change Net Sales $ 5,854 $ 5,919 1% Costs and expenses: Cost of sales 3,548 3,583

CONSOLIDATED OPERATING RESULTS (AMOUNTS IN MILLIONS EXCEPT PER SHARE, UNAUDITED) TABLE 1 Quarter Ended March 31, Percent Change Net Sales $ 5,854 $ 5,919 1% Costs and expenses: Cost of sales 3,548 3,583

Analyzing the Statement of Cash Flows

Analyzing the Statement of Cash Flows Operating Activities NACM Upstate New York Credit Conference 2015 By Ron Sereika, CCE,CEW NACM 1 Objectives of this Educational Session u Show how the statement of

Analyzing the Statement of Cash Flows Operating Activities NACM Upstate New York Credit Conference 2015 By Ron Sereika, CCE,CEW NACM 1 Objectives of this Educational Session u Show how the statement of

Budgetary Planning. Managerial Accounting Fifth Edition Weygandt Kimmel Kieso. Page 9-2

9-1 Budgetary Planning Managerial Accounting Fifth Edition Weygandt Kimmel Kieso 9-2 study objectives 1. Indicate the benefits of budgeting. 2. State the essentials of effective budgeting. 3. Identify

9-1 Budgetary Planning Managerial Accounting Fifth Edition Weygandt Kimmel Kieso 9-2 study objectives 1. Indicate the benefits of budgeting. 2. State the essentials of effective budgeting. 3. Identify

Consolidated balance sheet

83 Consolidated balance sheet December 31 Non-current assets Goodwill 14 675.1 978.4 Other intangible assets 14 317.4 303.8 Property, plant, and equipment 15 530.7 492.0 Investment in associates 16 2.5

83 Consolidated balance sheet December 31 Non-current assets Goodwill 14 675.1 978.4 Other intangible assets 14 317.4 303.8 Property, plant, and equipment 15 530.7 492.0 Investment in associates 16 2.5

Consolidated Statement of Profit or Loss (in million Euro)

") Consolidated Statement of Profit or Loss (in million Euro) Q3 2014 Q3 2015 % change 9m 2014 9m 2015 % change Revenue 636 661 3.9% 1,909 1,974 3.4% Cost of sales (440) (453) 3.0% (1,324) (1,340) 1.2% Gross

Consolidated Statement of Profit or Loss (in million Euro) Q3 2014 Q3 2015 % change 9m 2014 9m 2015 % change Revenue 636 661 3.9% 1,909 1,974 3.4% Cost of sales (440) (453) 3.0% (1,324) (1,340) 1.2% Gross

Statement of Cash Flows

HOSP 2110 (Management Acct) Learning Centre Statement of Cash Flows The Statement of Cash Flows (or cash flow statement) is one of the main financial statements used by investors. It shows the cash generated

HOSP 2110 (Management Acct) Learning Centre Statement of Cash Flows The Statement of Cash Flows (or cash flow statement) is one of the main financial statements used by investors. It shows the cash generated

Consolidated balance sheet

Consolidated balance sheet Non current assets 31/12/2009 31/12/2008 (*) 01/01/2008 (*) Property, plant and equipment 1,352 1,350 1,144 Investment property 7 11 11 Fixed assets held under concessions 13,089

Consolidated balance sheet Non current assets 31/12/2009 31/12/2008 (*) 01/01/2008 (*) Property, plant and equipment 1,352 1,350 1,144 Investment property 7 11 11 Fixed assets held under concessions 13,089

A Simple Model. Introduction to Financial Statements

Introduction to Financial Statements NOTES TO ACCOMPANY VIDEOS These notes are intended to supplement the videos on ASimpleModel.com. They are not to be used as stand alone study aids, and are not written

Introduction to Financial Statements NOTES TO ACCOMPANY VIDEOS These notes are intended to supplement the videos on ASimpleModel.com. They are not to be used as stand alone study aids, and are not written

Financial Statements for Manufacturing Businesses

Management Accounting 31 Financial Statements for Manufacturing Businesses Importance of Financial Statements Accounting plays a critical role in decision-making. Accounting provides the financial framework

Management Accounting 31 Financial Statements for Manufacturing Businesses Importance of Financial Statements Accounting plays a critical role in decision-making. Accounting provides the financial framework

Budget types. CH 6: Budgets HOW DO YOU COME UP WITH THE NUMBERS? Budget Periods WHY BUDGET?

CH 6: s WHY? PLANNING COMMUNICATION CONTROL:PERFORMANCE EVALUATION MOTIVATING types Master» Operating Sales, Production [purchases], Operating Expense. ProForma Income Statement» Financial Cash, Capital,

CH 6: s WHY? PLANNING COMMUNICATION CONTROL:PERFORMANCE EVALUATION MOTIVATING types Master» Operating Sales, Production [purchases], Operating Expense. ProForma Income Statement» Financial Cash, Capital,

Instructions for E-PLAN Financial Planning Template

Instructions for E-PLAN Financial Planning Template The EPLAN template will assist you in preparing financial projections for your existing business. The template uses Microsoft Excel to prepare your projected

Instructions for E-PLAN Financial Planning Template The EPLAN template will assist you in preparing financial projections for your existing business. The template uses Microsoft Excel to prepare your projected

PRODUCTION BUDGET Budgeted sales + desired ending inventory beginning inventory = required production

PARTS 3 and 4: Master Budget Formulas SALES BUDGET Forecasted units sold x selling price = total sales PRODUCTION BUDGET Budgeted sales + desired ending inventory beginning inventory = required production

PARTS 3 and 4: Master Budget Formulas SALES BUDGET Forecasted units sold x selling price = total sales PRODUCTION BUDGET Budgeted sales + desired ending inventory beginning inventory = required production

UNITED STATES BANKRUPTCY COURT NORTHERN & EASTERN DISTRICTS OF TEXAS REGION 6 MONTHLY OPERATING REPORT

ACCRUAL BASIS JUDGE: UNITED STATES BANKRUPTCY COURT NORTHERN & EASTERN DISTRICTS OF TEXAS REGION 6 MONTHLY OPERATING REPORT MONTH ENDING: MONTH YEAR IN ACCORDANCE WITH TITLE 28, SECTION 1746, OF THE UNITED

ACCRUAL BASIS JUDGE: UNITED STATES BANKRUPTCY COURT NORTHERN & EASTERN DISTRICTS OF TEXAS REGION 6 MONTHLY OPERATING REPORT MONTH ENDING: MONTH YEAR IN ACCORDANCE WITH TITLE 28, SECTION 1746, OF THE UNITED

Plan and Track Your Finances

Plan and Track Your Finances 9.1 Financing Your Business 9.2 Pro Forma Financial Statements 9.3 Recordkeeping for Businesses Lesson 9.1 Financing Your Business Goals Estimate your startup costs and personal

Plan and Track Your Finances 9.1 Financing Your Business 9.2 Pro Forma Financial Statements 9.3 Recordkeeping for Businesses Lesson 9.1 Financing Your Business Goals Estimate your startup costs and personal

Short Term Finance and Planning. Sources and Uses of Cash

Short Term Finance and Planning (Text reference: Chapter 27) Topics sources and uses of cash operating cycle and cash cycle short term financial policy cash budgeting short term financial planning AFM

Short Term Finance and Planning (Text reference: Chapter 27) Topics sources and uses of cash operating cycle and cash cycle short term financial policy cash budgeting short term financial planning AFM

BUSINESS ACCOUNTS. sample documents. sourced from www.osbornebooks.co.uk

BUSINESS ACCOUNTS sample documents sourced from www.osbornebooks.co.uk Sample documents document page invoice 3 statement 4 double-entry accounts 5 cash book 6 petty cash book 7 extended trial balance

BUSINESS ACCOUNTS sample documents sourced from www.osbornebooks.co.uk Sample documents document page invoice 3 statement 4 double-entry accounts 5 cash book 6 petty cash book 7 extended trial balance

Suggested layouts for financial statements in Accounting Courses National 5 and Higher

Suggested layouts for financial statements in Accounting Courses National 5 and Higher The following suggested layouts may be used when presenting financial statements in the Accounting Courses for National

Suggested layouts for financial statements in Accounting Courses National 5 and Higher The following suggested layouts may be used when presenting financial statements in the Accounting Courses for National

Discussion Board Articles Ratio Analysis

Excellence in Financial Management Discussion Board Articles Ratio Analysis Written by: Matt H. Evans, CPA, CMA, CFM All articles can be viewed on the internet at www.exinfm.com/board Ratio Analysis Cash

Excellence in Financial Management Discussion Board Articles Ratio Analysis Written by: Matt H. Evans, CPA, CMA, CFM All articles can be viewed on the internet at www.exinfm.com/board Ratio Analysis Cash

Comprehensive Business Budgeting

Management Accounting 137 Comprehensive Business Budgeting Goals and Objectives Profit planning, commonly called master budgeting or comprehensive business budgeting, is one of the more important techniques

Management Accounting 137 Comprehensive Business Budgeting Goals and Objectives Profit planning, commonly called master budgeting or comprehensive business budgeting, is one of the more important techniques

how to prepare a cash flow statement

business builder 4 how to prepare a cash flow statement zions business resource center zions business resource center 2 how to prepare a cash flow statement A cash flow statement is important to your business

business builder 4 how to prepare a cash flow statement zions business resource center zions business resource center 2 how to prepare a cash flow statement A cash flow statement is important to your business

Course pack Accounting 202 Chapter 13: Cash Flow Statement

Course pack Accounting 202 Chapter 13: Cash Flow Statement Value Chapter Included 13 Purpose of Cash Flow Understand Operating, Investing, Financing activities Prepare a Cash Flow Statement indirect only

Course pack Accounting 202 Chapter 13: Cash Flow Statement Value Chapter Included 13 Purpose of Cash Flow Understand Operating, Investing, Financing activities Prepare a Cash Flow Statement indirect only

RAPID REVIEW Chapter Content

RAPID REVIEW BASIC ACCOUNTING EQUATION (Chapter 2) INVENTORY (Chapters 5 and 6) Basic Equation Assets Owner s Equity Expanded Owner s Owner s Assets Equation = Liabilities Capital Drawing Revenues Debit

RAPID REVIEW BASIC ACCOUNTING EQUATION (Chapter 2) INVENTORY (Chapters 5 and 6) Basic Equation Assets Owner s Equity Expanded Owner s Owner s Assets Equation = Liabilities Capital Drawing Revenues Debit

Learning Module 3 Journal Entries

Learning Module 3 Journal Entries The Accounting Equation Balance Sheet Income Statement = + + - Assets Liabilities Owners' Equity Revenue Expenses Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Recording journal

Learning Module 3 Journal Entries The Accounting Equation Balance Sheet Income Statement = + + - Assets Liabilities Owners' Equity Revenue Expenses Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Recording journal

This is How Are Operating Budgets Created?, chapter 9 from the book Accounting for Managers (index.html) (v. 1.0).

(v. 1.0).") This is How Are Operating Budgets Created?, chapter 9 from the book Accounting for Managers (index.html) (v. 1.0). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/

This is How Are Operating Budgets Created?, chapter 9 from the book Accounting for Managers (index.html) (v. 1.0). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/

JOHN WILEY & SONS, INC. UNAUDITED SUMMARY OF OPERATIONS FOR THE FIRST QUARTER ENDED JULY 31, 2011 AND 2010 (in thousands, except per share amounts)

") UNAUDITED SUMMARY OF OPERATIONS FOR THE FIRST QUARTER ENDED JULY 31, 2011 AND 2010 (in thousands, except per share amounts) US GAAP First Quarter Ended Revenue $ 430,069 407,938 5% Costs and Expenses Cost

UNAUDITED SUMMARY OF OPERATIONS FOR THE FIRST QUARTER ENDED JULY 31, 2011 AND 2010 (in thousands, except per share amounts) US GAAP First Quarter Ended Revenue $ 430,069 407,938 5% Costs and Expenses Cost

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle 9.1 Current Assets and 9.1.1 Cash A firm should maintain as little cash as possible, because cash is a nonproductive asset. It earns no

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle 9.1 Current Assets and 9.1.1 Cash A firm should maintain as little cash as possible, because cash is a nonproductive asset. It earns no

CONSOLIDATED STATEMENT OF INCOME

CONSOLIDATED STATEMENT OF INCOME 4 th quarter (a) 3 rd quarter 4 th quarter 2009 Sales 40,157 40,180 36,228 Excise taxes (4,397) (4,952) (4,933) Revenues from sales 35,760 35,228 31,295 Purchases, net

CONSOLIDATED STATEMENT OF INCOME 4 th quarter (a) 3 rd quarter 4 th quarter 2009 Sales 40,157 40,180 36,228 Excise taxes (4,397) (4,952) (4,933) Revenues from sales 35,760 35,228 31,295 Purchases, net

Learning Objectives: Quick answer key: Question # Multiple Choice True/False. 14.1 Describe the important of accounting and financial information.

0 Learning Objectives: 14.1 Describe the important of accounting and financial information. 14.2 Differentiate between managerial and financial accounting. 14.3 Identify the six steps of the accounting

0 Learning Objectives: 14.1 Describe the important of accounting and financial information. 14.2 Differentiate between managerial and financial accounting. 14.3 Identify the six steps of the accounting

Reporting and Analyzing Cash Flows QUESTIONS

Chapter 12 Reporting and Analyzing Cash Flows QUESTIONS 1. The purpose of the cash flow statement is to report all major cash receipts (inflows) and cash payments (outflows) during a period. It helps users

Chapter 12 Reporting and Analyzing Cash Flows QUESTIONS 1. The purpose of the cash flow statement is to report all major cash receipts (inflows) and cash payments (outflows) during a period. It helps users

Multiple Choice Questions (45%)

") Multiple Choice Questions (45%) Choose the Correct Answer 1. The following information was taken from XYZ Company s accounting records for the year ended December 31, 2014: Increase in raw materials inventory

Multiple Choice Questions (45%) Choose the Correct Answer 1. The following information was taken from XYZ Company s accounting records for the year ended December 31, 2014: Increase in raw materials inventory

CASH FLOW STATEMENT. On the statement, cash flows are segregated based on source:

CASH FLOW STATEMENT On the statement, cash flows are segregated based on source: Operating activities: involve the cash effects of transactions that enter into the determination of net income. Investing

CASH FLOW STATEMENT On the statement, cash flows are segregated based on source: Operating activities: involve the cash effects of transactions that enter into the determination of net income. Investing

GBA 521 Midterm Review Dr. Markelevich

GBA 521 Midterm Review Dr. Markelevich Multiple Choice (3 points for each question) Identify the letter of the choice that best completes the statement or answers the question. Wynn Corp. Wynn Corp. reported

GBA 521 Midterm Review Dr. Markelevich Multiple Choice (3 points for each question) Identify the letter of the choice that best completes the statement or answers the question. Wynn Corp. Wynn Corp. reported

Financial Projections. Making sense of the money

Financial Projections Making sense of the money The Burning Questions What are your capital needs? Projections How will you get that capital? Structure: Equity or debt? Ownership structure Up-front or

Financial Projections Making sense of the money The Burning Questions What are your capital needs? Projections How will you get that capital? Structure: Equity or debt? Ownership structure Up-front or

PROFITCENTS ANALYTICAL PROCEDURES EXPECTED VALUE METHODOLOGY

PROFITCENTS ANALYTICAL PROCEDURES EXPECTED VALUE METHODOLOGY INTRODUCTION This document includes an analysis of the projection methodology used in ProfitCents Analytical Procedures in calculating expectations

PROFITCENTS ANALYTICAL PROCEDURES EXPECTED VALUE METHODOLOGY INTRODUCTION This document includes an analysis of the projection methodology used in ProfitCents Analytical Procedures in calculating expectations

Consolidated Financial Results for Fiscal Year 2013 (April 1, 2013 March 31, 2014)

") Consolidated Financial Results for Fiscal Year 2013 (April 1, 2013 March 31, 2014) 28/4/2014 Name of registrant: ShinMaywa Industries, Ltd. Stock Exchange Listed: Tokyo Code number: 7224 (URL: http://www.shinmaywa.co.jp

Consolidated Financial Results for Fiscal Year 2013 (April 1, 2013 March 31, 2014) 28/4/2014 Name of registrant: ShinMaywa Industries, Ltd. Stock Exchange Listed: Tokyo Code number: 7224 (URL: http://www.shinmaywa.co.jp

Brief Report on Closing of Accounts (connection) for the Term Ended March 31, 2007

for the Term Ended March 31, 2007") MARUHAN Co., Ltd. Brief Report on Closing of (connection) for the Term Ended March 31, 2007 (Amounts less than 1 million yen omitted) 1.Business Results for the term ended on March, 2007 (From April 1,

MARUHAN Co., Ltd. Brief Report on Closing of (connection) for the Term Ended March 31, 2007 (Amounts less than 1 million yen omitted) 1.Business Results for the term ended on March, 2007 (From April 1,

This week its Accounting and Beyond

This week its Accounting and Beyond Monday Morning Session Introduction/Accounting Cycle Afternoon Session Tuesday The Balance Sheet Wednesday The Income Statement The Cash Flow Statement Thursday Tools

This week its Accounting and Beyond Monday Morning Session Introduction/Accounting Cycle Afternoon Session Tuesday The Balance Sheet Wednesday The Income Statement The Cash Flow Statement Thursday Tools

02.Murray Company debited Prepaid Insurance for $960 on July 1, 1998 for a one-year

八 十 八 學 年 度 會 計 學 考 古 題 題 目 難 易 的 順 序 ( 難 易 ) 為 : I III II I Multiple Choice (74%) 01.The purchase of office equipment for $15,000 cash a. is a cash outflow from financing activities. b. is a cash outflow

八 十 八 學 年 度 會 計 學 考 古 題 題 目 難 易 的 順 序 ( 難 易 ) 為 : I III II I Multiple Choice (74%) 01.The purchase of office equipment for $15,000 cash a. is a cash outflow from financing activities. b. is a cash outflow

JOHNSON GRADUATE SCHOOL OF MANAGEMENT Cornell University

JOHNSON GRADUATE SCHOOL OF MANAGEMENT Cornell University Sample Accounting Exemption Exam Questions 1. On July 1, 20D, Allen Company signed a $50,000, one-year, 10 percent note payable. At due date, June

JOHNSON GRADUATE SCHOOL OF MANAGEMENT Cornell University Sample Accounting Exemption Exam Questions 1. On July 1, 20D, Allen Company signed a $50,000, one-year, 10 percent note payable. At due date, June

What is a business plan?

What is a business plan? A business plan is the presentation of an idea for a new business. When a person (or group) is planning to open a business, there is a great deal of research that must be done

What is a business plan? A business plan is the presentation of an idea for a new business. When a person (or group) is planning to open a business, there is a great deal of research that must be done

STATEMENT OF CHANGES IN FINANCIAL POSITION

Home Page - Statement of Changes in Financial Position STATEMENT OF CHANGES IN FINANCIAL POSITION by Dr. J. Herbert Smith/ACOA Chair Technology Management and Entrepreneurship Faculty of Engineering University

Home Page - Statement of Changes in Financial Position STATEMENT OF CHANGES IN FINANCIAL POSITION by Dr. J. Herbert Smith/ACOA Chair Technology Management and Entrepreneurship Faculty of Engineering University

Construction Economics & Finance. Module 6. Lecture-1

Construction Economics & Finance Module 6 Lecture-1 Financial management: Financial management involves planning, allocation and control of financial resources of a company. Financial management is essential

Construction Economics & Finance Module 6 Lecture-1 Financial management: Financial management involves planning, allocation and control of financial resources of a company. Financial management is essential

Consolidated Financial Statements (For the fiscal year ended March 31, 2013)

") Consolidated Financial Statements (For the fiscal year ended ) Consolidated Balance Sheets Current assets: Cash and deposits Other Assets Notes receivable, accounts receivable from completed construction

Consolidated Financial Statements (For the fiscal year ended ) Consolidated Balance Sheets Current assets: Cash and deposits Other Assets Notes receivable, accounts receivable from completed construction

STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

Chapter 4. Systems Design: Process Costing. Types of Costing Systems Used to Determine Product Costs

4-1 Types of Systems Used to Determine Product Costs Chapter 4 Process Job-order Systems Design: Many units of a single, homogeneous product flow evenly through a continuous production process. One unit

4-1 Types of Systems Used to Determine Product Costs Chapter 4 Process Job-order Systems Design: Many units of a single, homogeneous product flow evenly through a continuous production process. One unit

Financial Ratios and Quality Indicators

Financial Ratios and Quality Indicators From U.S. Small Business Administration Online Women's Business Center If you monitor the ratios on a regular basis you'll gain insight into how effectively you

Financial Ratios and Quality Indicators From U.S. Small Business Administration Online Women's Business Center If you monitor the ratios on a regular basis you'll gain insight into how effectively you