Plan and Track Your Finances

|

|

|

- Randolf Owens

- 10 years ago

- Views:

Transcription

1 Plan and Track Your Finances 9.1 Financing Your Business 9.2 Pro Forma Financial Statements 9.3 Recordkeeping for Businesses

2 Lesson 9.1 Financing Your Business Goals Estimate your startup costs and personal net worth. Identify sources of equity capital for your business. Identify sources of debt capital for your business. Slide 2

3 Assess Your Financial Needs Estimate startup costs. Create a personal financial statement. Prepare pro forma financial statements. Slide 3

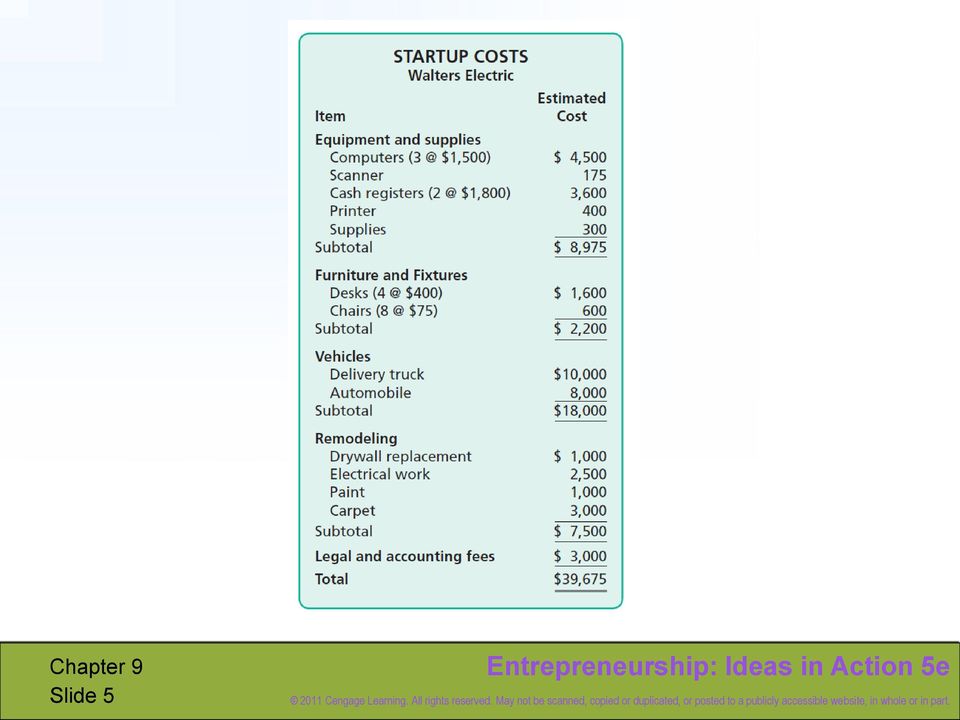

4 Startup Costs Itemize startup costs. equipment and supplies furniture and fixtures vehicles remodeling legal and accounting fees licensing fees Chapter 1 Slide 4

5 Slide 5

6 Personal Financial Statement net worth = assets liabilities personal financial statement = personal assets personal liabilities Slide 6

7 Slide 7

8 Equity Capital debt-to-equity ratio the relation between the dollars you have borrowed and the dollars you have invested in your business total liabilities total equity Lenders prefer low debt-to-equity ratios. Slide 8

9 equity capital money invested in a business in return for a share in the profits of the business Sources of equity include: Personal Contributions Friends and Relatives Venture Capitalists individuals and companies that make a living investing in startup companies Slide 9

10 Using page 249 as an example, create a start up cost statement to include in your business plan. Equipment & supplies Furniture & fixtures Inventory Remodel/Rent/Building Vehicles (if needed) Legal & accounting fees (if needed) Licensing fees The total will be the amount you are asking for in a loan. Chapter 1 Slide 10

Legal & accounting fees (if needed) Licensing fees The")

11 Debt Capital debt capital money loaned to a business with the understanding that the money will be repaid usually with interest Slide 11

12 Borrowing from Friends and Relatives Determine how the loan will affect your relationship. Prepare a formal agreement regarding terms of the loan. Chapter 1 Slide 12

13 Commercial Bank Loans secured loans loans that are backed by collateral collateral property that the borrower forfeits if he or she defaults on the loan Slide 13

14 Types of secured loans include the following: line of credit long-term loan accounts receivable financing inventory financing Slide 14

15 unsecured loans loans that are not guaranteed with collateral only made to creditworthy customers Slide 15

16 Reasons a bank may not lend money include: The business is a startup. A lack of: a solid business plan adequate experience confidence in the borrower adequate personal investment Slide 16

17 Other sources of loans include: Small Business Administration Small Business Investment Companies Minority Enterprise Small Business Investment Companies Department of Housing and Urban Development The Economic Development Administration State Governments Local and Municipal Governments Slide 17

18 SBA loans: Net Bookmark page 254 Chapter 1 Slide 18

19 Lesson 9.2 Pro Forma Financial Statements Goals Prepare a pro forma cash flow statement. Prepare a pro forma income statement. Prepare pro forma balance sheet. Slide 19

20 Cash Flow Statement cash flow statement an accounting report that describes the way cash flows into and out of your business over a period of time Slide 20

21 Prepare the Cash Flow Statement net cash flow = cash receipts cash disbursements Pro forma statements help you anticipate when negative cash flows will occur. You can plan how to handle or avoid them. Slide 21

22 Slide 22

23 Economic Effects on Cash Flow Changes in the economy can dramatically effect the cash flow of businesses. Business owners should make conservative estimates. Slide 23

24 Income Statement income statement shows revenues and expenses incurred over a period of time shows the profit or loss for the time period Slide 24

25 Prepare a Pro Forma Income Statement The long-term growth of your business can be demonstrated by a pro forma income statement prepared for multiple years. Slide 25

26 The pro forma income statement consists of: Revenue Cost of goods sold Gross profit Operating expenses Net income before taxes Taxes Net income/loss after taxes Slide 26

27 Slide 27

28 Balance Sheet balance sheet a financial statement that lists what a business owns what a business owes how much a business is worth at a point in time assets = liabilities + owner s equity Slide 28

29 Prepare a Pro Forma Balance Sheet Types of Assets current assets can be converted to cash easily (inventory, cash) accounts receivable the amounts owed to a business by its credit customers fixed assets cannot be converted into cash easily (equipment, vehicles) Slide 29

30 Types of Liabilities long-term liabilities debts that are payable over a year or longer (loans) current liabilities debts that must be paid in full in less than a year accounts payable amounts owed to vendors for merchandise purchased on credit Slide 30

31 Reductions in Assets allowance for uncollectible accounts the amount a company estimates it will not receive from customers depreciation the lowering of an asset s value to reflect its current worth Slide 31

32 Slide 32

33 Using pages as guides, create a pro forma cash flow statement, a pro forma income statement, and a pro forma balance sheet. Remember: these are made-up numbers, but should be reasonable. Chapter 1 Slide 33

34 Lesson 9.3 Recordkeeping for Businesses Goals Differentiate between alternative methods of accounting. Describe the use of journals and ledgers in a recordkeeping system. Explain the importance of keeping accurate and up-to-date bank, payroll, and tax records. Slide 34

35 Cash or Accrual Accounting Methods The major difference between the cash and accrual accounting methods is the timing of when transactions are recorded. Chapter 1 Slide 35

36 Cash Accounting Method cash method revenue is not recorded until cash (or a check) is actually received expenses are not recorded until they are actually paid The cash flow statement is prepared using the cash method. Chapter 1 Slide 36

37 Accrual Accounting Method accrual method revenue is recorded when the sale occurs expenses are recorded when you receive the goods or services Chapter 1 Slide 37

38 Choosing an Accounting Method Only very small businesses use the cash method. A business must use the accrual method if: annual sales exceed $5 million the company stocks inventory that will be sold to the public and has annual sales of over $1 million Chapter 1 Slide 38

39 Recording Transactions transaction any business activity that changes assets, liabilities or net worth Slide 39

40 Journals journals accounting records of the transactions you make for sales cash payments cash receipts purchases general Chapter 1 Slide 40

41 Ledgers A general ledger is made up of accounts. account an accounting record that provides financial detail for a particular business item Chapter 1 Slide 41

42 subsidiary ledgers used for accounts payable to show in detail the transactions with each vendor from whom merchandise is purchased on account Slide 42

43 Chapter 1 Slide 43

44 aging table a record keeping tool for tracking accounts receivable shows how long it takes customers to pay their bills Slide 44

45 Slide 45

46 Business Records Good recordkeeping can help you make smart business decisions. Incomplete records can cause you to mismanage your business. Chapter 1 Slide 46

47 1.Banking Records A business checking account should be established. check register a booklet where you record information for each check written amount date name of person or business receiving your payment Slide 47

48 Balance Your Account You should balance your account each time a transaction occurs. Reconcile Your Account Each month you should reconcile your bank statement with your check register. Slide 48

49 2. Payroll Records payroll a list of people who receive salary or wage payments from a business Chapter 1 Slide 49

50 3. Tax Records Income tax Businesses that earn a profit must pay income tax. quarterly Payroll Taxes and Deductions deduct taxes from employees paychecks submit taxes to the government unemployment insurance taxes social security and Medicare taxes voluntary deductions Chapter 1 Slide 50

51 Sales Tax Sales taxes are based on a percentage of sales. Each month you deposit sales tax into a government owned account. Slide 51

52 Complete the Finance Section of your Business Plan III. Projected Financial Statements A. Identification of Risk B. Financial Statements 1. Startup Cost 2. Cash Flow Statement 3. Income Statement 4. Balance Sheet C. Funding Request Chapter 1 Slide 52

Plan and Track Your Finances

Chapter 9 Plan and Track Your Finances 9.1 Finance Your Business 9.2 Pro Forma Financial Statements 9.3 Record Keeping for Businesses Ideas in Action Electronic Safekeeping Katelin Shea addressed the unmet

Chapter 9 Plan and Track Your Finances 9.1 Finance Your Business 9.2 Pro Forma Financial Statements 9.3 Record Keeping for Businesses Ideas in Action Electronic Safekeeping Katelin Shea addressed the unmet

PERSONAL FINANCIAL STATEMENT

PERSONAL FINANCIAL STATEMENT As of, 20 BUSINESS PLAN GUIDELINES Name: Residence Phone: Residence Address: City, State, Zip Code: Social Security Number: PERSONAL ASSETS PERSONAL LIABILITIES Cash in Bank

PERSONAL FINANCIAL STATEMENT As of, 20 BUSINESS PLAN GUIDELINES Name: Residence Phone: Residence Address: City, State, Zip Code: Social Security Number: PERSONAL ASSETS PERSONAL LIABILITIES Cash in Bank

Financial. Management FOR A SMALL BUSINESS

Financial Management FOR A SMALL BUSINESS 1 Agenda Welcome, Pre-Test, Agenda, and Learning Objectives Benefits of Financial Management Budgeting Bookkeeping Financial Statements Business Financing Key

Financial Management FOR A SMALL BUSINESS 1 Agenda Welcome, Pre-Test, Agenda, and Learning Objectives Benefits of Financial Management Budgeting Bookkeeping Financial Statements Business Financing Key

Understanding Financial Statements. For Your Business

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

Financial. Management FOR A SMALL BUSINESS

Financial Management FOR A SMALL BUSINESS Welcome 1. Agenda 2. Ground Rules 3. Introductions FINANCIAL MANAGEMENT 2 Objectives Explain the concept of financial management and its importance to a small

Financial Management FOR A SMALL BUSINESS Welcome 1. Agenda 2. Ground Rules 3. Introductions FINANCIAL MANAGEMENT 2 Objectives Explain the concept of financial management and its importance to a small

Financial Plan. A) Estimated One-Time Financial Requirements. Part One

Estimated One-Time Financial Requirements. Part One") Financial Plan The Financial Plan is perhaps one of the most important components of your Business Plan (see Business Plan Handout). Not only is it essential if you are seeking external financing it is

Financial Plan The Financial Plan is perhaps one of the most important components of your Business Plan (see Business Plan Handout). Not only is it essential if you are seeking external financing it is

UNDERSTANDING WHERE YOU STAND. A Simple Guide to Your Company s Financial Statements

UNDERSTANDING WHERE YOU STAND A Simple Guide to Your Company s Financial Statements Contents INTRODUCTION One statement cannot diagnose your company s financial health. Put several statements together

UNDERSTANDING WHERE YOU STAND A Simple Guide to Your Company s Financial Statements Contents INTRODUCTION One statement cannot diagnose your company s financial health. Put several statements together

Study Guide - Final Exam Accounting I

Study Guide - Final Exam Accounting I True/False Indicate whether the sentence or statement is true or false. 1. Entries in a sales journal affect account balances in both the accounts receivable ledger

Study Guide - Final Exam Accounting I True/False Indicate whether the sentence or statement is true or false. 1. Entries in a sales journal affect account balances in both the accounts receivable ledger

BACKGROUND KNOWLEDGE for Teachers and Students

Pathway: Business, Marketing, and Computer Education Lesson: BMM C6 4: Financial Statements and Reports Common Core State Standards for Mathematics: N.Q.2 Domain: Quantities Cluster: Reason quantitatively

Pathway: Business, Marketing, and Computer Education Lesson: BMM C6 4: Financial Statements and Reports Common Core State Standards for Mathematics: N.Q.2 Domain: Quantities Cluster: Reason quantitatively

How to Prepare a Cash Flow Forecast

The Orangeville & Area Small Business Enterprise Centre (SBEC) 87 Broadway, Orangeville ON L9W 1K1 519-941-0440 Ext. 2286 or 2291 [email protected] www.orangevillebusiness.ca Supported by its Partners:

The Orangeville & Area Small Business Enterprise Centre (SBEC) 87 Broadway, Orangeville ON L9W 1K1 519-941-0440 Ext. 2286 or 2291 [email protected] www.orangevillebusiness.ca Supported by its Partners:

Developing Financial Statements

New York StartUP! Business Plan Competition Developing Financial Statements Presented by Paisley Demby, CEO PBN Consulting, LLC www.pbnconsulting.com 1 Invitation to Tweet #2015NYStartUp PaisleyDemby Contents

New York StartUP! Business Plan Competition Developing Financial Statements Presented by Paisley Demby, CEO PBN Consulting, LLC www.pbnconsulting.com 1 Invitation to Tweet #2015NYStartUp PaisleyDemby Contents

FINANCIAL MANAGEMENT

100 Arbor Drive, Suite 108 Christiansburg, VA 24073 Voice: 540-381-9333 FAX: 540-381-8319 www.becpas.com Providing Professional Business Advisory & Consulting Services Douglas L. Johnston, II [email protected]

100 Arbor Drive, Suite 108 Christiansburg, VA 24073 Voice: 540-381-9333 FAX: 540-381-8319 www.becpas.com Providing Professional Business Advisory & Consulting Services Douglas L. Johnston, II [email protected]

Learning Objectives: Quick answer key: Question # Multiple Choice True/False. 14.1 Describe the important of accounting and financial information.

0 Learning Objectives: 14.1 Describe the important of accounting and financial information. 14.2 Differentiate between managerial and financial accounting. 14.3 Identify the six steps of the accounting

0 Learning Objectives: 14.1 Describe the important of accounting and financial information. 14.2 Differentiate between managerial and financial accounting. 14.3 Identify the six steps of the accounting

UNITED STATES BANKRUPTCY COURT NORTHERN & EASTERN DISTRICTS OF TEXAS REGION 6 MONTHLY OPERATING REPORT

ACCRUAL BASIS JUDGE: UNITED STATES BANKRUPTCY COURT NORTHERN & EASTERN DISTRICTS OF TEXAS REGION 6 MONTHLY OPERATING REPORT MONTH ENDING: MONTH YEAR IN ACCORDANCE WITH TITLE 28, SECTION 1746, OF THE UNITED

ACCRUAL BASIS JUDGE: UNITED STATES BANKRUPTCY COURT NORTHERN & EASTERN DISTRICTS OF TEXAS REGION 6 MONTHLY OPERATING REPORT MONTH ENDING: MONTH YEAR IN ACCORDANCE WITH TITLE 28, SECTION 1746, OF THE UNITED

How To Calculate A Trial Balance For A Company

THE BASIC MODEL The accounting information system is designed to collect and organize data into information that is useful for stakeholders. The Accounting Equation The basic accounting equation is what

THE BASIC MODEL The accounting information system is designed to collect and organize data into information that is useful for stakeholders. The Accounting Equation The basic accounting equation is what

Statement of Cash Flows

THE CONTENT AND VALUE OF THE STATEMENT OF CASH FLOWS The cash flow statement reconciles beginning and ending cash by presenting the cash receipts and cash disbursements of an enterprise for an accounting

THE CONTENT AND VALUE OF THE STATEMENT OF CASH FLOWS The cash flow statement reconciles beginning and ending cash by presenting the cash receipts and cash disbursements of an enterprise for an accounting

Basic Accounting Principles

Basic Accounting Principles Basic Accounting Model The basic accounting model represents the relationship between assets (what the company owns), liabilities (what the company owes), and owner s equity

Basic Accounting Principles Basic Accounting Model The basic accounting model represents the relationship between assets (what the company owns), liabilities (what the company owes), and owner s equity

Financial Management for a Small Business

Table of Contents Welcome... 3 What Do You Know? Financial Management for a Small Business... 4 Pre-Test... 5 Benefits of Financial Management... 7 Budgeting... 7 Discussion Point #1: Budgeting... 7 Bookkeeping...

Table of Contents Welcome... 3 What Do You Know? Financial Management for a Small Business... 4 Pre-Test... 5 Benefits of Financial Management... 7 Budgeting... 7 Discussion Point #1: Budgeting... 7 Bookkeeping...

How To Balance Sheet

Page 1 of 6 Balance Sheet Accounts The Chart of Accounts is normally arranged or grouped by the Major Types of Accounts. The Balance Sheet Accounts (Assets, Liabilities, & Equity) are presented first,

Page 1 of 6 Balance Sheet Accounts The Chart of Accounts is normally arranged or grouped by the Major Types of Accounts. The Balance Sheet Accounts (Assets, Liabilities, & Equity) are presented first,

STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

Accounts payable Money which you owe to an individual or business for goods or services that have been received but not yet paid for.

A Account A record of a business transaction. A contract arrangement, written or unwritten, to purchase and take delivery with payment to be made later as arranged. Accounts payable Money which you owe

A Account A record of a business transaction. A contract arrangement, written or unwritten, to purchase and take delivery with payment to be made later as arranged. Accounts payable Money which you owe

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased.

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased. Accounts Receivable are the total amounts customers owe your business for goods or services sold

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased. Accounts Receivable are the total amounts customers owe your business for goods or services sold

Borrowing Money for Your Business

Borrowing Money for Your Business After you have developed a cash flow analysis and determined when your business will make profit, you may decide you need additional funding. Borrowing money is one of

Borrowing Money for Your Business After you have developed a cash flow analysis and determined when your business will make profit, you may decide you need additional funding. Borrowing money is one of

Cash Flow Forecasting & Break-Even Analysis

Cash Flow Forecasting & Break-Even Analysis 1. Cash Flow Cash Flow Projections What is cash flow? Cash flow is an estimate of the timing of when the cash associated with sales will be received and when

Cash Flow Forecasting & Break-Even Analysis 1. Cash Flow Cash Flow Projections What is cash flow? Cash flow is an estimate of the timing of when the cash associated with sales will be received and when

Account Numbering. By separating each account by several numbers, many new accounts can be added between any two while maintaining the logical order.

Chart of Accounts The chart of accounts is a listing of all the accounts in the general ledger, each account accompanied by a reference number. To set up a chart of accounts, one first needs to define

Chart of Accounts The chart of accounts is a listing of all the accounts in the general ledger, each account accompanied by a reference number. To set up a chart of accounts, one first needs to define

Guide to Financial Statements Study Guide

Guide to Financial Statements Study Guide Overview (Topic 1) Three major financial statements: The Income Statement The Balance Sheet The Cash Flow Statement Objectives: Explain the underlying equation

Guide to Financial Statements Study Guide Overview (Topic 1) Three major financial statements: The Income Statement The Balance Sheet The Cash Flow Statement Objectives: Explain the underlying equation

SMALL BUSINESS DEVELOPMENT CENTER RM. 032

SMALL BUSINESS DEVELOPMENT CENTER RM. 032 FINANCING THROUGH COMMERCIAL BANKS Revised January, 2013 Adapted from: National Federation of Independent Business report Steps to Small Business Financing Jeffrey

SMALL BUSINESS DEVELOPMENT CENTER RM. 032 FINANCING THROUGH COMMERCIAL BANKS Revised January, 2013 Adapted from: National Federation of Independent Business report Steps to Small Business Financing Jeffrey

CHAPTER 2 REVIEW OF THE ACCOUNTING PROCESS. Lecture Outline

CHAPTER 2 REVIEW OF THE ACCOUNTING PROCESS Overview Chapter 1 explained that the primary means of conveying financial information to investors, creditors, and other external users is through financial

CHAPTER 2 REVIEW OF THE ACCOUNTING PROCESS Overview Chapter 1 explained that the primary means of conveying financial information to investors, creditors, and other external users is through financial

Chapter 6 Statement of Cash Flows

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Too often business owners do a cash flow in their head. Putting the information down on paper will give you the following:

CASH FLOW A cash flow is a forecast of when you expect to receive cash from your sales and when you expect to pay your bills. It is not and should not be confused with a pro-forma income statement. A cash

CASH FLOW A cash flow is a forecast of when you expect to receive cash from your sales and when you expect to pay your bills. It is not and should not be confused with a pro-forma income statement. A cash

Current liabilities - Obligations that are due within one year. Obligations due beyond that period of time are classified as long-term liabilities.

Accounting Fundamentals Lesson 8 8.0 Liabilities Current liabilities - Obligations that are due within one year. Obligations due beyond that period of time are classified as long-term liabilities. Current

Accounting Fundamentals Lesson 8 8.0 Liabilities Current liabilities - Obligations that are due within one year. Obligations due beyond that period of time are classified as long-term liabilities. Current

What is a business plan?

What is a business plan? A business plan is the presentation of an idea for a new business. When a person (or group) is planning to open a business, there is a great deal of research that must be done

What is a business plan? A business plan is the presentation of an idea for a new business. When a person (or group) is planning to open a business, there is a great deal of research that must be done

In the event of a tie, the score on the last ten questions will be used as a tie-breaker.

NEW YORK STATE ASSOCIATION FUTURE BUSINESS LEADERS OF AMERICA SPRING DISTRICT MEETING ACCOUNTING II 2010 TEST DIRECTIONS 1. Complete the information requested on the answer sheet. PRINT your name on the

NEW YORK STATE ASSOCIATION FUTURE BUSINESS LEADERS OF AMERICA SPRING DISTRICT MEETING ACCOUNTING II 2010 TEST DIRECTIONS 1. Complete the information requested on the answer sheet. PRINT your name on the

Basic Business Plan Outline

Basic Business Plan Outline A business plan needs to be a well thought out, honest, appraisal of the business and opportunity. This outline is meant to be used for your road map. It should be a living

Basic Business Plan Outline A business plan needs to be a well thought out, honest, appraisal of the business and opportunity. This outline is meant to be used for your road map. It should be a living

How to Assess Your Financial Planning and Loan Proposals By BizMove Management Training Institute

How to Assess Your Financial Planning and Loan Proposals By BizMove Management Training Institute Other free books by BizMove that may interest you: Free starting a business books Free management skills

How to Assess Your Financial Planning and Loan Proposals By BizMove Management Training Institute Other free books by BizMove that may interest you: Free starting a business books Free management skills

Financial Statements and Ratios: Notes

Financial Statements and Ratios: Notes 1. Uses of the income statement for evaluation Investors use the income statement to help judge their return on investment and creditors (lenders) use it to help

Financial Statements and Ratios: Notes 1. Uses of the income statement for evaluation Investors use the income statement to help judge their return on investment and creditors (lenders) use it to help

The Basic Framework of Budgeting

Master Budgeting 1 The Basic Framework of Budgeting A budget is a detailed quantitative plan for acquiring and using financial and other resources over a specified forthcoming time period. 1. The act of

Master Budgeting 1 The Basic Framework of Budgeting A budget is a detailed quantitative plan for acquiring and using financial and other resources over a specified forthcoming time period. 1. The act of

SMALL BUSINESS OWNER S HANDBOOK

SMALL BUSINESS OWNER S HANDBOOK PART II: FINANCIAL PLANNING FOR SMALL BUSINESSES Introduction Financial Planning Methods of Financing Your Business Other Types of Funds & Financing How to Approach Lenders

SMALL BUSINESS OWNER S HANDBOOK PART II: FINANCIAL PLANNING FOR SMALL BUSINESSES Introduction Financial Planning Methods of Financing Your Business Other Types of Funds & Financing How to Approach Lenders

GBA 521 Midterm Review Dr. Markelevich

GBA 521 Midterm Review Dr. Markelevich Multiple Choice (3 points for each question) Identify the letter of the choice that best completes the statement or answers the question. Wynn Corp. Wynn Corp. reported

GBA 521 Midterm Review Dr. Markelevich Multiple Choice (3 points for each question) Identify the letter of the choice that best completes the statement or answers the question. Wynn Corp. Wynn Corp. reported

Financing Entrepreneurial Ventures Part 1 Financial Plan & Statements

Financing Entrepreneurial Ventures Part 1 Financial Plan & Statements Barbara Peitsch Program Director, Univ. of Michigan Peter Scott Professor of Entrepreneurship/Consultant August 2015 Economic Empowerment

Financing Entrepreneurial Ventures Part 1 Financial Plan & Statements Barbara Peitsch Program Director, Univ. of Michigan Peter Scott Professor of Entrepreneurship/Consultant August 2015 Economic Empowerment

State of Idaho - Public Works Contractor Licensing MULTI-PURPOSE BALANCE SHEET (For Class D and C Licenses Only)

") State of Idaho - Public Works Contractor Licensing MULTI-PURPOSE SHEET (For Class D and C Licenses Only) Instructions: Complete only the sections that pertain to your company structure. Do not include

State of Idaho - Public Works Contractor Licensing MULTI-PURPOSE SHEET (For Class D and C Licenses Only) Instructions: Complete only the sections that pertain to your company structure. Do not include

! "#$ %&!& "& ' - 3+4 &*!&-.,,5///2!(.//+ & $!- )!* & % +, -).//0)& 7+00///2 *&&.4 &*!&- 7.00///2 )!*.//+ 8 -!% %& "#$ ) &!&.

!* & % +, -).//0)& 7+00///2 *&&.4 &*!&- 7.00///2 )!*.//+ 8 -!% %& #$ ) &!&.") ! "#!""#$%$#$#$"& $'"()*+,$-).,/ 012! "#$ %&!& "& '!(&)!*&%+,-).//0 -#$#3-4' &,'1$1# $!-!(.//0)& +01+///2 *&& - 3+4 &*!&-.,,5///2!(.//+ &!(!-6%(!(.//.$(!(.//0)& 01,///2 //+2% &*!&- 5,0///2 //32%!(.//+

! "#!""#$%$#$#$"& $'"()*+,$-).,/ 012! "#$ %&!& "& '!(&)!*&%+,-).//0 -#$#3-4' &,'1$1# $!-!(.//0)& +01+///2 *&& - 3+4 &*!&-.,,5///2!(.//+ &!(!-6%(!(.//.$(!(.//0)& 01,///2 //+2% &*!&- 5,0///2 //32%!(.//+

Purchasing/Human Resources/Payment Process: Recording and Evaluating Expenditure Process Activities

Chapter 8 Purchasing/Human Resources/Payment Process: Recording and Evaluating Expenditure Process Activities McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. What

Chapter 8 Purchasing/Human Resources/Payment Process: Recording and Evaluating Expenditure Process Activities McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. What

Job Ready Assessment Blueprint. Accounting-Advanced. Test Code: 3900 / Version: 01

Job Ready Assessment Blueprint Accounting-Advanced Test Code: 3900 / Version: 01 Measuring What Matters Specific Competencies and Skills Tested in this Assessment: Journalizing Journalize an opening entry

Job Ready Assessment Blueprint Accounting-Advanced Test Code: 3900 / Version: 01 Measuring What Matters Specific Competencies and Skills Tested in this Assessment: Journalizing Journalize an opening entry

TOPIC LEARNING OBJECTIVE

Topic Mapping 1 Transaction Analysis Understand the effect of various types of transactions on the accounting equation, accounting journal and accounting ledger. Concepts and Skills Accounting Equation

Topic Mapping 1 Transaction Analysis Understand the effect of various types of transactions on the accounting equation, accounting journal and accounting ledger. Concepts and Skills Accounting Equation

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account.

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account. Account fee the amount charged by a financial institution for the

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account. Account fee the amount charged by a financial institution for the

Report Description. Business Counts. Top 10 States (by Business Counts) Page 1 of 16

Page 1 of 16") 5-Year County-Level Financial Profile Industry Report Architectural Services (SIC Code: 8712) in Prince George County, Maryland Sales Range: $500,000 - $999,999 Date: 11/07/08 Report Description This 5-Year

5-Year County-Level Financial Profile Industry Report Architectural Services (SIC Code: 8712) in Prince George County, Maryland Sales Range: $500,000 - $999,999 Date: 11/07/08 Report Description This 5-Year

RENAISSANCE ENTREPRENEURSHIP CENTER First Finance Class (FIN-1)

") Finance 1 (FIN-1) RENAISSANCE ENTREPRENEURSHIP CENTER (FIN-1) Learning Outcomes At the conclusion of this class, you should: Know what will be covered in the six finance class sessions. Have reviewed some

Finance 1 (FIN-1) RENAISSANCE ENTREPRENEURSHIP CENTER (FIN-1) Learning Outcomes At the conclusion of this class, you should: Know what will be covered in the six finance class sessions. Have reviewed some

SETTING UP YOUR BUSINESS ACCOUNTING SYSTEM

100 Arbor Drive, Suite 108 Christiansburg, VA 24073 Voice: 540-381-9333 FAX: 540-381-8319 www.becpas.com Providing Professional Business Advisory & Consulting Services Douglas L. Johnston, II [email protected]

100 Arbor Drive, Suite 108 Christiansburg, VA 24073 Voice: 540-381-9333 FAX: 540-381-8319 www.becpas.com Providing Professional Business Advisory & Consulting Services Douglas L. Johnston, II [email protected]

Business Plan Workbook

Business Plan Workbook Developed by the staff of the Niagara County Community College Small Business Development Center 3111 Saunders Settlement Rd Sanborn, NY 14132 7162102515 www.niagarasbdc.org Call

Business Plan Workbook Developed by the staff of the Niagara County Community College Small Business Development Center 3111 Saunders Settlement Rd Sanborn, NY 14132 7162102515 www.niagarasbdc.org Call

Vol. 1, Chapter 7 The Statement of Cash Flows

Vol. 1, Chapter 7 The Statement of Cash Flows Problem 1: Solution Transaction # Identification 1 Operating 2 Investing 3 Noncash transaction 4 Financing 5 Noncash transaction 6 Operating 7 Investing 8

Vol. 1, Chapter 7 The Statement of Cash Flows Problem 1: Solution Transaction # Identification 1 Operating 2 Investing 3 Noncash transaction 4 Financing 5 Noncash transaction 6 Operating 7 Investing 8

How Do I Qualify for a loan?

How Do I Qualify for a loan? Borrowing money is one of the most common sources of funding for a small business, but obtaining a loan isn't always easy. Before you approach your banker for a loan, it is

How Do I Qualify for a loan? Borrowing money is one of the most common sources of funding for a small business, but obtaining a loan isn't always easy. Before you approach your banker for a loan, it is

Article Accounting Terminology

Article Accounting Terminology Contents Page 1. Accounting Period... 4 2. Accounts Payable (Sundry Creditors)... 4 3. Accounts Receivable (Sundry Debtors)... 4 4. Assets... 4 5. Benchmarks... 4 6. B.O.S.

Article Accounting Terminology Contents Page 1. Accounting Period... 4 2. Accounts Payable (Sundry Creditors)... 4 3. Accounts Receivable (Sundry Debtors)... 4 4. Assets... 4 5. Benchmarks... 4 6. B.O.S.

Chapter 18 Working Capital Management

Chapter 18 Working Capital Management Slide Contents Learning Objectives Principles Used in This Chapter 1. Working Capital Management and the Risk-Return Tradeoff 2. Working Capital Policy 3. Operating

Chapter 18 Working Capital Management Slide Contents Learning Objectives Principles Used in This Chapter 1. Working Capital Management and the Risk-Return Tradeoff 2. Working Capital Policy 3. Operating

Financial Information Statement for Businesses

Financial Information Statement for Businesses How to Complete This Statement Enter the most current data available in all spaces. Write N/A in spaces that don t apply to you. The Taxation and Revenue

Financial Information Statement for Businesses How to Complete This Statement Enter the most current data available in all spaces. Write N/A in spaces that don t apply to you. The Taxation and Revenue

CENTURY 21 ACCOUNTING, 8e General Journal Chapter Objectives

CENTURY 21 ACCOUNTING, 8e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

CENTURY 21 ACCOUNTING, 8e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

Chapter 9 Solutions to Problems

Chapter 9 Solutions to Problems 1. a. Cash and cash equivalents are cash in hand and in banks, plus money market securities with maturities of 90 days or less. Accounts receivable are claims on customers

Chapter 9 Solutions to Problems 1. a. Cash and cash equivalents are cash in hand and in banks, plus money market securities with maturities of 90 days or less. Accounts receivable are claims on customers

Gold Run Snowmobile. Adjusting Entries and Closing Entries For The Quarter Ended December 31. Final Project Evaluation. 5 th Edition.

Gold Run Snowmobile 5 th Edition Adjusting Entries and Closing Entries For The Quarter Ended December 31 and the Final Project Evaluation Page 1 ADJUSTING ENTRIES FOR THE QUARTER Using a copy of the December

Gold Run Snowmobile 5 th Edition Adjusting Entries and Closing Entries For The Quarter Ended December 31 and the Final Project Evaluation Page 1 ADJUSTING ENTRIES FOR THE QUARTER Using a copy of the December

Accounting Self Study Guide for Staff of Micro Finance Institutions

Accounting Self Study Guide for Staff of Micro Finance Institutions LESSON 2 The Balance Sheet OBJECTIVES The purpose of this lesson is to introduce the Balance Sheet and explain its components: Assets,

Accounting Self Study Guide for Staff of Micro Finance Institutions LESSON 2 The Balance Sheet OBJECTIVES The purpose of this lesson is to introduce the Balance Sheet and explain its components: Assets,

Understanding A Firm s Financial Statements

CHAPTER OUTLINE Spotlight: J&S Construction Company (http://www.jsconstruction.com) 1 The Lemonade Kids Financial statement (accounting statements) reports of a firm s financial performance and resources,

CHAPTER OUTLINE Spotlight: J&S Construction Company (http://www.jsconstruction.com) 1 The Lemonade Kids Financial statement (accounting statements) reports of a firm s financial performance and resources,

how to prepare a cash flow statement

business builder 4 how to prepare a cash flow statement zions business resource center zions business resource center 2 how to prepare a cash flow statement A cash flow statement is important to your business

business builder 4 how to prepare a cash flow statement zions business resource center zions business resource center 2 how to prepare a cash flow statement A cash flow statement is important to your business

Century 21 Accounting, 8e General Journal Chapter Outlines

Century 21 Accounting, 8e General Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

Century 21 Accounting, 8e General Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

Accounting 101 you don t have to be an accountant to run MYOB Your Daily Lives Cash vs. Accrual Accounting

MYOB US, Inc. April 2002 Accounting 101 Like all small business owners, you went into business with a dream: to sell your unique product or services and make a living for you, your family, and your employees.

MYOB US, Inc. April 2002 Accounting 101 Like all small business owners, you went into business with a dream: to sell your unique product or services and make a living for you, your family, and your employees.

Information About Financial Statements for Intrastate Household Goods Movers

Instructions for Page 4 of Application (FINANCIAL STATEMENTS) Part of determining whether an applicant is fit to become a household goods mover involves provision of information about financial capability.

Instructions for Page 4 of Application (FINANCIAL STATEMENTS) Part of determining whether an applicant is fit to become a household goods mover involves provision of information about financial capability.

STATE OF FLORIDA DEPARTMENT OF BUSINESS AND PROFESSIONAL REGULATION. BALANCE SHEET As of

STATE OF FLORIDA DEPARTMENT OF BUSINESS AND PROFESSIONAL REGULATION BALANCE SHEET As of ASSETS CURRENT ASSETS Cash and Cash Equivalents Cash - Restricted Accounts Receivable - Trade Accounts Receivable

STATE OF FLORIDA DEPARTMENT OF BUSINESS AND PROFESSIONAL REGULATION BALANCE SHEET As of ASSETS CURRENT ASSETS Cash and Cash Equivalents Cash - Restricted Accounts Receivable - Trade Accounts Receivable

Model is used to calculate Financial Statements on a Quarterly Basis for a One Year period. Model provides the ability to:

ADDITIONAL REFERENCES AND FINANCIAL MODELS: For more information about financial statements and terms refer to e book, How to Read Financial Statements. Advanced financial models providing 5 year projections

ADDITIONAL REFERENCES AND FINANCIAL MODELS: For more information about financial statements and terms refer to e book, How to Read Financial Statements. Advanced financial models providing 5 year projections

Sample Test for entrance into Acct 3110 and Acct 3310

Sample Test for entrance into Acct 3110 and Acct 3310 1. Which of the following financial statements could properly have the following in the date line: For the Year Ended December 31, 2010"? a. Balance

Sample Test for entrance into Acct 3110 and Acct 3310 1. Which of the following financial statements could properly have the following in the date line: For the Year Ended December 31, 2010"? a. Balance

INSTRUCTIONS FOR COMPLETING INSURANCE COMPANY FINANCIAL STATEMENTS

INSTRUCTIONS FOR COMPLETING INSURANCE COMPANY "DRAFT VERSION FOR FIRST REVIEW ONLY" Submitted to: Minstry of Finance and Economy Head of Insurance Department Republic of Armenia Submitted by: BearingPoint

INSTRUCTIONS FOR COMPLETING INSURANCE COMPANY "DRAFT VERSION FOR FIRST REVIEW ONLY" Submitted to: Minstry of Finance and Economy Head of Insurance Department Republic of Armenia Submitted by: BearingPoint

RETAIL LEASING ADVISORS, LLC

Personal Financial Statement Page 1 of 2 Name (I, We) make the following statement of all (my, our) assets and liabilities as of the day of, 20, and give other material information for the purpose of obtaining

Personal Financial Statement Page 1 of 2 Name (I, We) make the following statement of all (my, our) assets and liabilities as of the day of, 20, and give other material information for the purpose of obtaining

COMPONENTS OF THE STATEMENT OF CASH FLOWS

ILLUSTRATION 24-1 OPERATING, INVESTING, AND FINANCING ACTIVITIES COMPONENTS OF THE STATEMENT OF CASH FLOWS CASH FLOWS FROM OPERATING ACTIVITIES + Sales and Service Revenue Received Cost of Sales Paid Selling

ILLUSTRATION 24-1 OPERATING, INVESTING, AND FINANCING ACTIVITIES COMPONENTS OF THE STATEMENT OF CASH FLOWS CASH FLOWS FROM OPERATING ACTIVITIES + Sales and Service Revenue Received Cost of Sales Paid Selling

Self-test Comprehensive Problems II 综 合 自 测 题 II

Self-test Comprehensive Problems II 综 合 自 测 题 II Part One (30%) 1. Give the Chinese/English of the following terms: (5%) subsidiary ledger 统 制 账 户 purchase requisition 现 金 溢 缺 petty cash fund 永 续 盘 存 制

Self-test Comprehensive Problems II 综 合 自 测 题 II Part One (30%) 1. Give the Chinese/English of the following terms: (5%) subsidiary ledger 统 制 账 户 purchase requisition 现 金 溢 缺 petty cash fund 永 续 盘 存 制

Preparing a Successful Financial Plan

Topic 9 Preparing a Successful Financial Plan LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Describe the overview of accounting methods; 2. Prepare the three major financial statements

Topic 9 Preparing a Successful Financial Plan LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Describe the overview of accounting methods; 2. Prepare the three major financial statements

United States Bankruptcy Court - Northern District of Alabama BUSINESS DEBTOR S AFFIRMATIONS

CHAPTER 11 OPERATING ORDER FORM 04/00 BUSINESS BA-01 Operating reports are to be filed monthly, in duplicate, with the Bankruptcy Clerk s Office by the 15 th of each month BUSINESS DEBTOR S AFFIRMATIONS

CHAPTER 11 OPERATING ORDER FORM 04/00 BUSINESS BA-01 Operating reports are to be filed monthly, in duplicate, with the Bankruptcy Clerk s Office by the 15 th of each month BUSINESS DEBTOR S AFFIRMATIONS

BOOKKEEPING FUNDAMENTALS TRAINING

Phone:1300 121 400 Email: [email protected] BOOKKEEPING FUNDAMENTALS TRAINING Generate a group quote today or register now for the next public course date COURSE LENGTH: 1.0 DAYS Developing essential

Phone:1300 121 400 Email: [email protected] BOOKKEEPING FUNDAMENTALS TRAINING Generate a group quote today or register now for the next public course date COURSE LENGTH: 1.0 DAYS Developing essential

1. A set of procedures for controlling cash payments by preparing and approving vouchers before payments are made is known as a voucher system.

Accounting II True/False Indicate whether the sentence or statement is true or false. 1. A set of procedures for controlling cash payments by preparing and approving vouchers before payments are made is

Accounting II True/False Indicate whether the sentence or statement is true or false. 1. A set of procedures for controlling cash payments by preparing and approving vouchers before payments are made is

Financial Statements

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

BUSINESS LOAN APPLICATION

BUSINESS LOAN APPLICATION 1. Applicant Name: Name of Business: Sole Proprietorship: S Corporation: Partnership: C Corporation: LLC/LLP: Mailing Address: Street Address: Business Telephone: Home Telephone:

BUSINESS LOAN APPLICATION 1. Applicant Name: Name of Business: Sole Proprietorship: S Corporation: Partnership: C Corporation: LLC/LLP: Mailing Address: Street Address: Business Telephone: Home Telephone:

Measuring Financial Performance: A Critical Key to Managing Risk

Measuring Financial Performance: A Critical Key to Managing Risk Dr. Laurence M. Crane Director of Education and Training National Crop Insurance Services, Inc. The essence of managing risk is making good

Measuring Financial Performance: A Critical Key to Managing Risk Dr. Laurence M. Crane Director of Education and Training National Crop Insurance Services, Inc. The essence of managing risk is making good

Financial Accounting. (Exam)

") Financial Accounting (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials Take a quick tour by visiting wwwaccountingcoachcom/quicktour Table of Contents (click to

Financial Accounting (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials Take a quick tour by visiting wwwaccountingcoachcom/quicktour Table of Contents (click to

BUSINESS BUILDER 2 HOW TO PREPARE AND ANALYZE A BALANCE SHEET

BUSINESS BUILDER 2 HOW TO PREPARE AND ANALYZE A BALANCE SHEET zions business resource center 2 how to prepare and analyze a balance sheet Examine the concepts of assets, liabilities, and net worth in a

BUSINESS BUILDER 2 HOW TO PREPARE AND ANALYZE A BALANCE SHEET zions business resource center 2 how to prepare and analyze a balance sheet Examine the concepts of assets, liabilities, and net worth in a

RISK ASSESSMENT FOR SMALL BUSINESS. Terry S. Campbell, Community Development Officer Department of Development & Technology

RISK ASSESSMENT FOR SMALL BUSINESS Terry S. Campbell, Community Development Officer Department of Development & Technology Date: March 25, 2004 1 Counseling Tool Outline - Cover Page - Outline - Introduction

RISK ASSESSMENT FOR SMALL BUSINESS Terry S. Campbell, Community Development Officer Department of Development & Technology Date: March 25, 2004 1 Counseling Tool Outline - Cover Page - Outline - Introduction

Funding Your Business

Page 12 County of Bucks Community Services Division Lynn T. Bush, Executive Director and County Chief Clerk Community and Business Development Department Vitor A. Vicente, Director Neshaminy Manor Center

Page 12 County of Bucks Community Services Division Lynn T. Bush, Executive Director and County Chief Clerk Community and Business Development Department Vitor A. Vicente, Director Neshaminy Manor Center

EXERCISES. The cash from operating activities detail is provided as follows for class discussion:

EXERCISES Ex. 14 1 There were net additions, such as depreciation and amortization of intangible assets of $389 million, to the net loss reported on the income statement to convert the net loss from the

EXERCISES Ex. 14 1 There were net additions, such as depreciation and amortization of intangible assets of $389 million, to the net loss reported on the income statement to convert the net loss from the

Definition of Accounting

SOLUTIONS TO EXERCISES Lesson 1: Definition of Accounting 1. What is accounting? What are its main functions? Accounting is the process of financially measuring, recording, summarizing and communicating

SOLUTIONS TO EXERCISES Lesson 1: Definition of Accounting 1. What is accounting? What are its main functions? Accounting is the process of financially measuring, recording, summarizing and communicating

Receipts and Payments Accounts Introductory Notes

Receipts and Payments Accounts Introductory Notes Purpose of pro forma receipts and payments accounts These guidance notes reflect the requirements for accounting periods ending on or after 1 April 2009

Receipts and Payments Accounts Introductory Notes Purpose of pro forma receipts and payments accounts These guidance notes reflect the requirements for accounting periods ending on or after 1 April 2009

Ratio Analysis. A) Liquidity Ratio : - 1) Current ratio = Current asset Current Liability

Liquidity Ratio : - 1) Current ratio = Current asset Current Liability") A) Liquidity Ratio : - Ratio Analysis 1) Current ratio = Current asset Current Liability 2) Quick ratio or Acid Test ratio = Quick Asset Quick liability Quick Asset = Current Asset Stock Quick Liability

A) Liquidity Ratio : - Ratio Analysis 1) Current ratio = Current asset Current Liability 2) Quick ratio or Acid Test ratio = Quick Asset Quick liability Quick Asset = Current Asset Stock Quick Liability

Gross Sales (Gross Revenue): the total amount of money received from customers

: the total amount of money received from customers") Chapter 17 Financial Statements and Ratios 17.1: The Income Statement 17.1.1: Learn the terms used with income statements Income Statement: a financial statement used to summarize all income and expenses

Chapter 17 Financial Statements and Ratios 17.1: The Income Statement 17.1.1: Learn the terms used with income statements Income Statement: a financial statement used to summarize all income and expenses

Understanding Financial Information for Bankruptcy Lawyers Understanding Financial Statements

Understanding Financial Information for Bankruptcy Lawyers Understanding Financial Statements In the United States, businesses generally present financial information in the form of financial statements

Understanding Financial Information for Bankruptcy Lawyers Understanding Financial Statements In the United States, businesses generally present financial information in the form of financial statements

Appraisal A written analysis prepared by a qualified appraiser and estimating the value of a property

REAL ESTATE BASICS Affordability Analysis An analysis of a buyer s ability to afford the purchase of a home, reviews income, liabilities, and available funds, and considers the type of mortgage a buyer

REAL ESTATE BASICS Affordability Analysis An analysis of a buyer s ability to afford the purchase of a home, reviews income, liabilities, and available funds, and considers the type of mortgage a buyer

Vol. 1, Chapter 3 - Accounting Adjustments

Vol. 1, Chapter 3 - Accounting Adjustments Problem 1 1. ($20,000 2,000) 48 = $375 per month 2. Jan. 31 Depreciation Expense $375 Accumulated Depreciation Van $375 To record depreciation expense for January

Vol. 1, Chapter 3 - Accounting Adjustments Problem 1 1. ($20,000 2,000) 48 = $375 per month 2. Jan. 31 Depreciation Expense $375 Accumulated Depreciation Van $375 To record depreciation expense for January

Small-business owners who need

BUSINESS PLANS ARE MORE IMPORTANT NOW THAN EVER Jenni Jeras 1 Small-business owners who need financing are smart to do their homework, and that includes creating a comprehensive business plan. Lenders

BUSINESS PLANS ARE MORE IMPORTANT NOW THAN EVER Jenni Jeras 1 Small-business owners who need financing are smart to do their homework, and that includes creating a comprehensive business plan. Lenders

CHAPTER 16 Current Asset Management and Financing

Copyright 2008 by the Foundation of the American College of Healthcare Executives 6/13/07 Version 16-1 CHAPTER 16 Current Asset Management and Financing Investment and financing policies Cash and marketable

Copyright 2008 by the Foundation of the American College of Healthcare Executives 6/13/07 Version 16-1 CHAPTER 16 Current Asset Management and Financing Investment and financing policies Cash and marketable

Financial Projections. Making sense of the money

Financial Projections Making sense of the money The Burning Questions What are your capital needs? Projections How will you get that capital? Structure: Equity or debt? Ownership structure Up-front or

Financial Projections Making sense of the money The Burning Questions What are your capital needs? Projections How will you get that capital? Structure: Equity or debt? Ownership structure Up-front or

Group Exercise I: Calculating the Revenue Requirement

Group Exercise I: Calculating the Revenue Requirement Ron Davis Principal Economist Colorado Department of Regulatory Agencies Public Utilities Commission 1560 Broadway, Suite 250 Denver, CO 80202 P 303.894.2883

Group Exercise I: Calculating the Revenue Requirement Ron Davis Principal Economist Colorado Department of Regulatory Agencies Public Utilities Commission 1560 Broadway, Suite 250 Denver, CO 80202 P 303.894.2883

Chapter 9 E-Commerce: Digital Markets, Digital Goods

1 Chapter 9 E-Commerce: Digital Markets, Digital Goods LEARNING TRACK #: 2: BUILD BUSINESS PLAN There are lots of different ways to lay out a business plan. The sample

1 Chapter 9 E-Commerce: Digital Markets, Digital Goods LEARNING TRACK #: 2: BUILD BUSINESS PLAN There are lots of different ways to lay out a business plan. The sample

So You Want to Borrow Money to Start a Business?

So You Want to Borrow Money to Start a Business? M any small business owners cannot understand why a lending institution would refuse to lend them money. Others have no trouble getting money, but they

So You Want to Borrow Money to Start a Business? M any small business owners cannot understand why a lending institution would refuse to lend them money. Others have no trouble getting money, but they