How to Establish an SBIR Accounting System that Can Withstand a Government Audit

|

|

|

- Abigail Morton

- 10 years ago

- Views:

Transcription

1 In cooperation with Connecticut Innovations 2/27/14 How to Establish an SBIR Accounting System that Can Withstand a Government Audit Edward G. Jameson, CPA Managing Partner Jameson & Company, CPAs

2 HOW TO SPEAK GREEK (THE FEDERAL ACQUISITION REGS.) 1. REPS AND CERTS SBA RULES ON NEW 5107 POOLS 2. $1.5M COST FOR NOT UNDERSTANDING THE FAR AT PHASE II 3. TWO KEY CONCEPTS TO AN ACCEPTABLE ACCOUNTING SYSTEM? A. ALLOWABLE, REASONABLE, ALLOCABLE B. DIRECT VS. INDIRECT VS. UNALLOWABLE COSTS 4. SOME REQUIRED WRITTEN POLICIES & PRACTICES 5. AUDITS - DOD VS. NIH 6. THE COST OF NON-COMPLIANCE

3 SBIR Program Eligibility You Must Certify SBA - CERTIFY SIZE, OWNERSHIP & CONTROL, OR UNDER 5107 AUTHORITY Only United States small businesses are eligible to participate in the SBIR program. An SBIR awardee must meet the following criteria at the time of Phase I and II awards: 1. Organized for profit, with a place of business located in the United States; 2. More than 50 percent owned and controlled by one or more individuals who are citizens of, or permanent resident aliens in, the United States, or by another for-profit business concern that is more than 50% owned and controlled by one or more individuals who are citizens of, or permanent resident aliens in, the United States; and 3. No more than 500 employees, including affiliates For awards from agencies using the authority under 15 U.S.C. 638(dd)(1), an awardee may be owned and controlled by more than one VC, hedge fund, or private equity firm so long as no one such firm owns a majority of the stock. Phase I awardees with multiple prior awards must meet the benchmark requirements for progress toward commercialization. January 2013 Guide to SBIR/STTR Program Small Business Admin. website

4 WHAT AUDITORS LOOK FOR PRIOR TO YOUR PHASE II DCAA or DFAS 1. Acceptable accounting system 2. Reasonable cost proposal (believable indirect rates)

5 SBIR PHASE II = FAR Phase I = FFP Phase II = CPFF Award and ongoing compliance hinges on maintaining an Acceptable accounting system A contractor is responsible for accounting for costs appropriately and for maintaining records, including supporting documentation, adequate to demonstrate that costs claimed have been incurred, are allocable to the contract, and comply with applicable cost principles in this subpart and agency supplements. The contracting officer may disallow all or part of a claimed cost that is inadequately supported.

6 NIH GRANTS? SECTION III TERMS AND CONDITIONS Standard Language in a Phase II This award is based on the application submitted to, and as approved by, NIH on the above-titled project and is subject to the terms and conditions incorporated either directly or by reference in the following: a. The grant program legislation and program regulation cited in this Notice of Award. b. Conditions on activities and expenditure of funds in other statutory requirements, such as those included in appropriations acts. c. 45 CFR Part 74 or 45 CFR Part 92 as applicable. d. The NIH Grants Policy Statement, including addenda in effect as of the beginning date of the budget period. e. This award notice, INCLUDING THE TERMS AND CONDITIONS CITED BELOW. (See NIH Home Page at for certain references cited above.).lets take a poll

7 POLLING QS DIRECT, INDIRECT OR UNALLOWABLE? Patent costs. (a) The following patent costs are allowable to the extent that they are incurred as requirements of a Government contract (but see ): (1) Costs of preparing invention disclosures, reports, and other documents. (2) Costs for searching the art to the extent necessary to make the invention disclosures. (3) Other costs in connection with the filing and prosecution of a United States patent application where title or royalty-free license is to be conveyed to the Government. (b) General counseling services relating to patent matters, such as advice on patent laws, regulations, clauses, and employee agreements, are allowable (but see ). (c) Other than those for general counseling services, patent costs not required by the contract are unallowable. (See also )

Other costs in connection with the filing and prosecution of a United States patent application where title or royalty-free license is to be conveyed to the Government.")

8 AN ACCEPTABLE ACCOUNTING SYSTEM 1. Does your General ledger segregate: Direct costs Indirect costs Unallowable costs Lab jackets polling question Written accounting policies and procedures The Jameson Pass/Fail quiz: A. Can you produce monthly job cost reports at billing/target rates B. Can you tell me what your indirect rates running now?

9 SOME POLICIES AND PROCEDURES YOU MUST HAVE A. Timesheets 1. Filled out in ink daily 2. Must record all time, signed by the employee 3. Signed by the supervisor 4. Changes must be crossed out (not erased) and initialed B. Accounting for uncompensated overtime 1. $60,000/2,000 = $30/hour 2. Bill the government at $30/hr. 3. Actually works 2,500 hours 4. Actual hourly rate is $24/hr. Surprise floorcheck - The MIT Professor and his wife

10 7 DCAA audits problems surface 1. Pre-award audit Review of the adequacy of your accounting system. You will not receive an award unless you pass. 2. Indirect rate projection audit A review of the underlying projections used in establishing your provisional billing (and bidding) rates. Your invoices will be rejected until you proactively have your indirect rates approved by DCAA. 3. Progress payment audit The DCAA judgmentally selects an invoice that you submit and traces all direct costs back to their originating source documents (timesheets, vendor invoices, expense reports, etc.). 4. Surprise floor check DCAA will visit your facility and randomly (?) select your employees for audit to ensure that they are following the government s strict timekeeping rules. Employees must be ready to properly answer questions on timekeeping procedures and must be able to demonstrate that their timesheets reflect those procedures. 5. Financial capacity audit 6. Annual Incurred Cost Audit With a Phase 2 SBIR, your contract contains Federal Acquisition Regulation (FAR) clause The Allowable Cost Clause. This clause requires you to submit an annual true up report known as an Incurred Cost Submission 180 days after your fiscal year end. This submission has a 100% chance of being audited by DCAA and is their main event! This audit is when you discover if your accountants knew what they were doing, or not years after the fact. 7. Contract close out

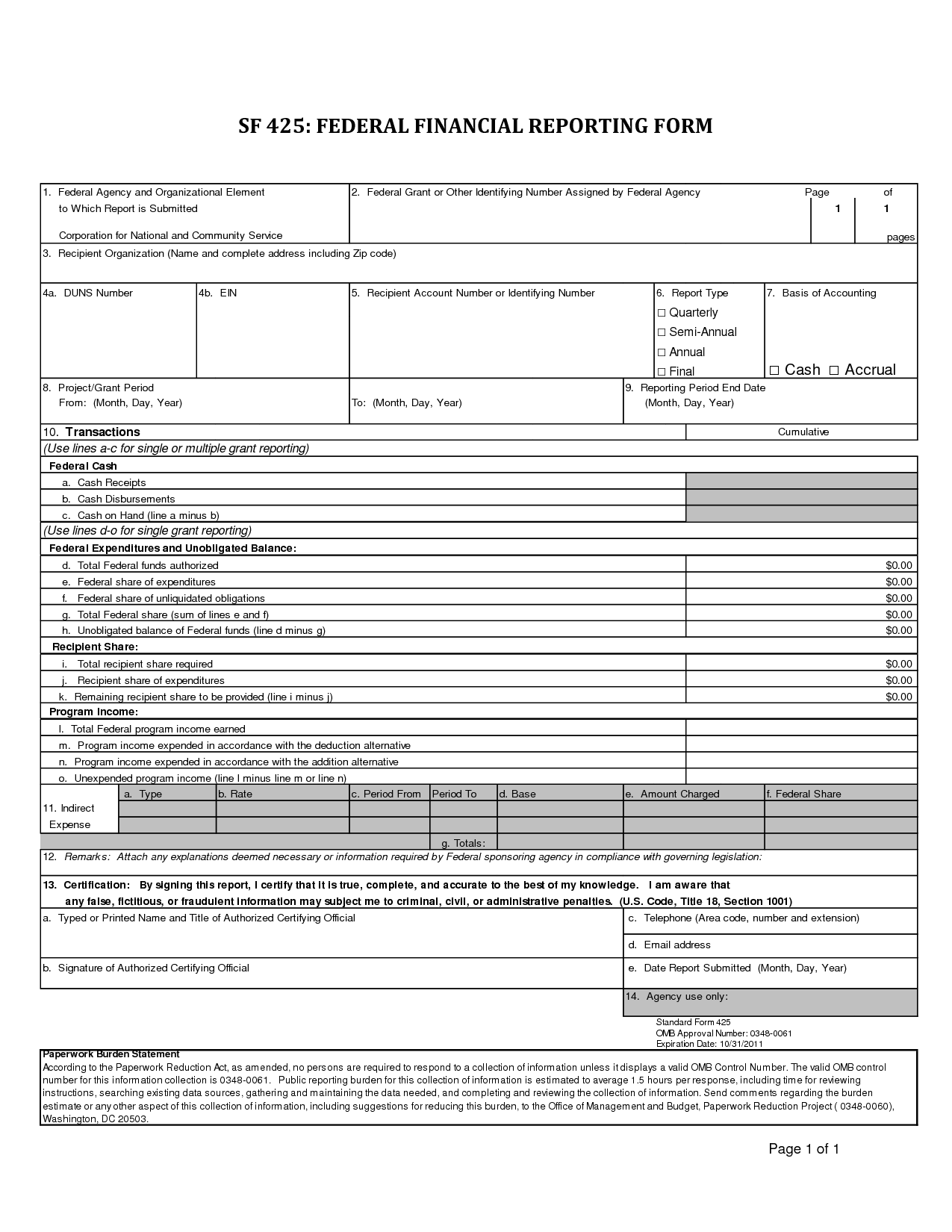

11 NIH Grantee checkpoints 1. Pre-award almost no resistance (J.I.T.) 2. Annual indirect rate negotiation with DFAS if F&A rate > 40% 3. SF425 Reconcile the money drawn from the Payment Management System with what you ve earned (in accordance with the federal acquisition regulations). 4. OMB A133 (Revenue earned > $500,000)

. 4.")

12

13 NORTHWESTERN PAYS $3MM FOR FRAUD According to the Wall Street Journal, Northwestern University agreed to pay nearly $3 million to settle claims that a former cancer researcher fraudulently used federal grant money for personal expenses, including food, hotels and airfare for family trips between 2003 and The whistleblower, Melissa Theis, worked as a purchasing coordinator, processing invoices when she 'noticed some red flags,' according to her attorney. The federal False Claims Act allows private citizens who allege government programs are being defrauded to file actions on behalf of the government and receive a portion, usually 15% to 30%, of any recovered damages. Ms. Theis will get $498,100 in settlement proceeds, according to the agreement.

14 Defense Contractor MPRI Settles $3.2 Million Lawsuit Brought by Whistleblower PR Newswire ATLANTA, Feb. 13, 2014

15 COMPLIANCE SUMMARY SBIR/STTR phase II, R01 & BAA contracts and grants almost always contain Federal Acquisition Regulations (FAR) clause Allowable Costs This FAR clause requires you to follow the Cost Accounting Standards and the Federal Acquisition Regulations Prior to award, you need to have an acceptable accounting system. Your accounting records can be audited at any time and need to be always audit ready. There is an annual Incurred Cost Submission that must be prepared and has a 100% chance of being audited.

16 COST OF NOT BEING COMPLIANT? False sense of security - DCAA hopes to be caught up through 2009 by the end of this year $xxx,000 in disallowances (typically years later) Don t charge the government for things you are entitled to ($xxx,000) Unacceptable accounting system loss of award, employees, investors game over!

Unacceptable")

17 NEXT STEPS Our $495 Phase 1A Analysis: 1. Accounting system adequacy our analysis will include a review of specific areas of your company s accounting system, including job costing, time reporting, and underlying documentation. 2. Unallowable cost assessment 3. Program management TOM PISTONE X2110 [email protected]

How to Establish an SBIR Accounting System that Can Withstand a Government Audit

In cooperation with Connecticut Innovations 4/16/14 How to Establish an SBIR Accounting System that Can Withstand a Government Audit Edward G. Jameson, CPA Managing Partner Jameson & Company, CPAs www.jamesoncpa.com

In cooperation with Connecticut Innovations 4/16/14 How to Establish an SBIR Accounting System that Can Withstand a Government Audit Edward G. Jameson, CPA Managing Partner Jameson & Company, CPAs www.jamesoncpa.com

How to Develop an Indirect Rate for Your SBIR Proposal

Connecticut Innovations June 3, 2014 How to Develop an Indirect Rate for Your SBIR Proposal Edward G. Jameson, CPA Managing Partner Jameson & Company, CPAs www.jamesoncpa.com HOW TO SPEAK GREEK INDIRECT

Connecticut Innovations June 3, 2014 How to Develop an Indirect Rate for Your SBIR Proposal Edward G. Jameson, CPA Managing Partner Jameson & Company, CPAs www.jamesoncpa.com HOW TO SPEAK GREEK INDIRECT

Accounting System Requirements

Accounting System Requirements Further information is available in the Information for Contractors Manual under Enclosure 2 The views expressed in this presentation are DCAA's views and not necessarily

Accounting System Requirements Further information is available in the Information for Contractors Manual under Enclosure 2 The views expressed in this presentation are DCAA's views and not necessarily

Pre-Award Accounting Systems

Pre-Award Accounting Systems 2013 National SBIR Conference Christopher Andrezze, CPA Special Assistant to the Deputy Director May 16, 2013 The views expressed in this presentation are DCAA's views and

Pre-Award Accounting Systems 2013 National SBIR Conference Christopher Andrezze, CPA Special Assistant to the Deputy Director May 16, 2013 The views expressed in this presentation are DCAA's views and

Government Contract Accounting Are You DCAA Compliant? Procurement Technical Assistance Program (PTAP)

") Government Contract Accounting Are You DCAA Compliant? Procurement Technical Assistance Program (PTAP) NH Presentation October 20, 2010 Presented by: Fred Kline, MBA, CPA Tom Martin MBA, CPA Malcolm Young,

Government Contract Accounting Are You DCAA Compliant? Procurement Technical Assistance Program (PTAP) NH Presentation October 20, 2010 Presented by: Fred Kline, MBA, CPA Tom Martin MBA, CPA Malcolm Young,

DEFENSE CONTRACT AUDIT AGENCY

DEFENSE CONTRACT AUDIT AGENCY Fundamental Building Blocks for an Acceptable Accounting System Presented by Sue Reynaga DCAA Branch Manager San Diego Branch Office August 24, 2011 Report Documentation Page

DEFENSE CONTRACT AUDIT AGENCY Fundamental Building Blocks for an Acceptable Accounting System Presented by Sue Reynaga DCAA Branch Manager San Diego Branch Office August 24, 2011 Report Documentation Page

Presenting the Numbers: Accounting Systems for Government Contractors

Presenting the Numbers: Accounting Systems for Government Contractors William D. Craven, CPA Senior Cost/Price Analyst CH2M HILL Plateau Remediation Company William D. Craven, CPA, CMA, CIA Cost/Price

Presenting the Numbers: Accounting Systems for Government Contractors William D. Craven, CPA Senior Cost/Price Analyst CH2M HILL Plateau Remediation Company William D. Craven, CPA, CMA, CIA Cost/Price

Basic Financial Requirements for Government Contracting

Basic Financial Requirements for Government Contracting 2014 National SBIR/STTR Conference The views expressed in this presentation are DCAA's views and not necessarily the views of other DoD organizations

Basic Financial Requirements for Government Contracting 2014 National SBIR/STTR Conference The views expressed in this presentation are DCAA's views and not necessarily the views of other DoD organizations

How to Survive a DCAA Audit

How to Survive a DCAA Audit www.paulgunn.com 1 How to Survive a DCAA Audit - Overview Areas of interest and expectations of a typical audit: 1. Introduction o 2. The DCAA and Types of audits 3. Preparing

How to Survive a DCAA Audit www.paulgunn.com 1 How to Survive a DCAA Audit - Overview Areas of interest and expectations of a typical audit: 1. Introduction o 2. The DCAA and Types of audits 3. Preparing

You've successfully subscribed to this feed! Updated content can be viewed in Internet Explorer and other programs that use the Common Feed List.

Page 1 of 5 You've successfully subscribed to this feed! Updated content can be viewed in Internet Explorer and other programs that use the Common Feed List. View my feeds DCAA News Thursday, May 28, 2009,

Page 1 of 5 You've successfully subscribed to this feed! Updated content can be viewed in Internet Explorer and other programs that use the Common Feed List. View my feeds DCAA News Thursday, May 28, 2009,

Accounting System Requirements

Basic Financial Requirements for Government Contracting The views expressed in this presentation are DCAA's views and not necessarily the views of other DoD organizations Accounting System Requirements

Basic Financial Requirements for Government Contracting The views expressed in this presentation are DCAA's views and not necessarily the views of other DoD organizations Accounting System Requirements

DCAA Guidelines. How the SBIR firm can work effectively with the Defense Contract Audit Agency

DCAA Guidelines How the SBIR firm can work effectively with the Defense Contract Audit Agency Today s Presenters OUTLINE Presenter Introduction DCAA & DCMA DCAA Overview Types of DCAA Audits What it takes

DCAA Guidelines How the SBIR firm can work effectively with the Defense Contract Audit Agency Today s Presenters OUTLINE Presenter Introduction DCAA & DCMA DCAA Overview Types of DCAA Audits What it takes

WHAT MAKES AN ACCOUNTING SYSTEM COMPLIANT

WHAT MAKES AN ACCOUNTING SYSTEM COMPLIANT Presented by: Laura Davis OVERVIEW Why Do I Need a Compliant Accounting System Auditor s Judgment Definitions Key Components Audits How to be prepared for an audit

WHAT MAKES AN ACCOUNTING SYSTEM COMPLIANT Presented by: Laura Davis OVERVIEW Why Do I Need a Compliant Accounting System Auditor s Judgment Definitions Key Components Audits How to be prepared for an audit

DCAA and the Small Business Innovative Research (SBIR) Program

Program") Defense Contract Audit Agency (DCAA) DCAA and the Small Business Innovative Research (SBIR) Program Judice Smith and Chang Ford DCAA/Financial Liaison Advisors NAVAIR 2010 Small Business Aviation Technology

Defense Contract Audit Agency (DCAA) DCAA and the Small Business Innovative Research (SBIR) Program Judice Smith and Chang Ford DCAA/Financial Liaison Advisors NAVAIR 2010 Small Business Aviation Technology

What Exactly is an Acceptable Accounting System?

What Exactly is an Acceptable Accounting System? Kristen Soles, CPA Member Stephanie Widzinski, CPA Senior Manager September 27, 2012 Agenda Review DFARS Business System Rule What Agency is Responsible

What Exactly is an Acceptable Accounting System? Kristen Soles, CPA Member Stephanie Widzinski, CPA Senior Manager September 27, 2012 Agenda Review DFARS Business System Rule What Agency is Responsible

Uncompensated Overtime

Uncompensated Overtime 1 Table of Contents Risk Assessment Research and Planning Risk Assessment Labor System Entrance Conference Preliminary Analytical Procedures Audit Team Brainstorming for Fraud Risk

Uncompensated Overtime 1 Table of Contents Risk Assessment Research and Planning Risk Assessment Labor System Entrance Conference Preliminary Analytical Procedures Audit Team Brainstorming for Fraud Risk

Are you in Compliance with the Financial Rules for 8(a) Companies?

Companies?") Are you in Compliance with the Financial Rules for 8(a) Companies? Sales Less than $1M Withdrawals exceeding $250,000 are considered excessive. Compiled financial statements are required within 90 days

Are you in Compliance with the Financial Rules for 8(a) Companies? Sales Less than $1M Withdrawals exceeding $250,000 are considered excessive. Compiled financial statements are required within 90 days

WELCOME. Accounting Systems for DOD Contracts

WELCOME Accounting Systems for DOD Contracts Moderator: Layli Pietri, Small Business Manager, Balfour Beatty Construction Speaker: Kay Papin, Government Compliance Manager, McCarthy Group Inc. Accounting

WELCOME Accounting Systems for DOD Contracts Moderator: Layli Pietri, Small Business Manager, Balfour Beatty Construction Speaker: Kay Papin, Government Compliance Manager, McCarthy Group Inc. Accounting

Post Award Accounting System Audit at Nonmajor Contractors

Activity Code 17740 B-1 Planning Considerations Post Award Accounting System Audit at Nonmajor Contractors To provide general guidance for the audit of the adequacy and suitability of nonmajor contractor

Activity Code 17740 B-1 Planning Considerations Post Award Accounting System Audit at Nonmajor Contractors To provide general guidance for the audit of the adequacy and suitability of nonmajor contractor

Audit Expectations for Small Businesses

Audit Expectations for Small Businesses DEFENSE CONTRACT CONSULTING Joseph A. Dalton, CGFM/CFE/CAP Over 31 Years -Supervisory/Auditor Service- DCAA Retired Captain, U. S. Naval Reserve 1996 BUSINESS NO.

Audit Expectations for Small Businesses DEFENSE CONTRACT CONSULTING Joseph A. Dalton, CGFM/CFE/CAP Over 31 Years -Supervisory/Auditor Service- DCAA Retired Captain, U. S. Naval Reserve 1996 BUSINESS NO.

Post Award Accounting System Audit at Nonmajor Contractors

Activity Code 17741 Version 3.1, dated November 2015 B-01 Planning Considerations Post Award Accounting System Audit at Nonmajor Contractors Audit Specific Independence Determination Members of the audit

Activity Code 17741 Version 3.1, dated November 2015 B-01 Planning Considerations Post Award Accounting System Audit at Nonmajor Contractors Audit Specific Independence Determination Members of the audit

Accounting Systems: Complying with FAR Requirements. John S. Sroka, CPA Acquisition Cost/Price Analyst

Accounting Systems: Complying with FAR Requirements John S. Sroka, CPA Acquisition Cost/Price Analyst Background Information FAR Requirements FAR Part 9: Contractor Qualifications FAR Part 16: Cost-reimbursement

Accounting Systems: Complying with FAR Requirements John S. Sroka, CPA Acquisition Cost/Price Analyst Background Information FAR Requirements FAR Part 9: Contractor Qualifications FAR Part 16: Cost-reimbursement

Preaward and Post Award Accounting System Audits. November 17, 2011 Pikes Peak NCMA Roland Wick

Preaward and Post Award Accounting System Audits November 17, 2011 Pikes Peak NCMA Roland Wick OVERVIEW This presentation will provide: 1. The basic criteria for the Preaward and Post Award accounting

Preaward and Post Award Accounting System Audits November 17, 2011 Pikes Peak NCMA Roland Wick OVERVIEW This presentation will provide: 1. The basic criteria for the Preaward and Post Award accounting

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AT 2 CFR 200

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AT 2 CFR 200 November 11, 2014 WHAT S CHANGING AND WHEN? Grants Reform Office of Management and Budget Circulars

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AT 2 CFR 200 November 11, 2014 WHAT S CHANGING AND WHEN? Grants Reform Office of Management and Budget Circulars

Government Accounting, Estimating, and Billing Systems: Pitfalls and Answers

Curtis Matthews, Managing Partner Government Accounting, Estimating, and Billing Systems: Pitfalls and Answers Findley Gillespie, Senior Manager May 18, 2011 1 The material appearing in this presentation

Curtis Matthews, Managing Partner Government Accounting, Estimating, and Billing Systems: Pitfalls and Answers Findley Gillespie, Senior Manager May 18, 2011 1 The material appearing in this presentation

Preaward Survey of Prospective Contractor Accounting System

Activity Code 17740 B-1 Planning Considerations Preaward Survey of Prospective Contractor Accounting System Purpose and Scope The major objectives of this audit are to obtain an understanding of the accounting

Activity Code 17740 B-1 Planning Considerations Preaward Survey of Prospective Contractor Accounting System Purpose and Scope The major objectives of this audit are to obtain an understanding of the accounting

DEPARTMENT OF TRANSPORTATION AUDITS & INVESTIGATIONS. Overview of A&E Related Audit Issues

DEPARTMENT OF TRANSPORTATION AUDITS & INVESTIGATIONS Overview of A&E Related Audit Issues 1 INTRODUCTION Overview of Audit Related Issues At the conclusion of this session, you will understand: - Basic

DEPARTMENT OF TRANSPORTATION AUDITS & INVESTIGATIONS Overview of A&E Related Audit Issues 1 INTRODUCTION Overview of Audit Related Issues At the conclusion of this session, you will understand: - Basic

CHAPTER 2. 2-000 Preaward Surveys of Prospective Contractor Accounting Systems

CHAPTER 2 2-000 Preaward Surveys of Prospective Contractor Accounting Systems 2-101 Preaward Survey Overview A preaward survey is an evaluation, usually made by the cognizant contract administration office,

CHAPTER 2 2-000 Preaward Surveys of Prospective Contractor Accounting Systems 2-101 Preaward Survey Overview A preaward survey is an evaluation, usually made by the cognizant contract administration office,

How To Audit A Government Contractor

Activity Code 17740 Version 6.11, dated November 2015 B-1 Planning Considerations Preaward Survey of Prospective Contractor Accounting System Audit Specific Independence Determination Members of the audit

Activity Code 17740 Version 6.11, dated November 2015 B-1 Planning Considerations Preaward Survey of Prospective Contractor Accounting System Audit Specific Independence Determination Members of the audit

MDA Small Business Industry Day

MDA Small Business Industry Day SBIR Proposal Preparation By: John Swan Contracting Officer Missile Defense Agency August 14, 2015 Agenda Introduction - John Swan Accounting System Audits - John Swan Cost

MDA Small Business Industry Day SBIR Proposal Preparation By: John Swan Contracting Officer Missile Defense Agency August 14, 2015 Agenda Introduction - John Swan Accounting System Audits - John Swan Cost

ACCOUNTING & AUDIT GUIDELINES FOR CONTRACTS WITH CALTRANS

ACCOUNTING & AUDIT GUIDELINES FOR CONTRACTS WITH CALTRANS Mendocino County Page 1 of 5 INTRODUCTION The purpose of this brochure is to outline for you, a potential contractor with the California State

ACCOUNTING & AUDIT GUIDELINES FOR CONTRACTS WITH CALTRANS Mendocino County Page 1 of 5 INTRODUCTION The purpose of this brochure is to outline for you, a potential contractor with the California State

Master Document Audit Program. Version 1.5, dated September 2015 B-01 Planning Considerations

Activity Code 11070 Version 1.5, dated September 2015 B-01 Planning Considerations Accounting System Audit Audit Specific Independence Determination Members of the audit team and internal specialists consulting

Activity Code 11070 Version 1.5, dated September 2015 B-01 Planning Considerations Accounting System Audit Audit Specific Independence Determination Members of the audit team and internal specialists consulting

THE DCAA AUDIT BECOMING DCAA COMPLIANT

THE DCAA AUDIT Created to oversee government spending on behalf of the American tax-payer, the Defense Contract Audit Agency (DCAA) is responsible for supervising all Department of Defense (DoD) contracts.

THE DCAA AUDIT Created to oversee government spending on behalf of the American tax-payer, the Defense Contract Audit Agency (DCAA) is responsible for supervising all Department of Defense (DoD) contracts.

Enprise Job Costing and DCAA Compliance

April 2014 Author: Document Version: Product: Product Version: SAP Version: Localization: Enprise Solutions 1.5.0 Enprise Job Costing All versions All current versions North America 2014 Enprise Solutions

April 2014 Author: Document Version: Product: Product Version: SAP Version: Localization: Enprise Solutions 1.5.0 Enprise Job Costing All versions All current versions North America 2014 Enprise Solutions

Slide 1. Slide 2. Slide 3 Standard Form 1408 ACCOUNTING SYSTEM ESSENTIALS

Slide 1 Slide 2 ACCOUNTING SYSTEM ESSENTIALS P r e p a r e d f o r Alliance Northwest 2014 By T e r r y S. N u z z o, C P A, C G M A P a c i f i c N o r t h w e s t C o n s u l t a n t s, L L C Slide 3

Slide 1 Slide 2 ACCOUNTING SYSTEM ESSENTIALS P r e p a r e d f o r Alliance Northwest 2014 By T e r r y S. N u z z o, C P A, C G M A P a c i f i c N o r t h w e s t C o n s u l t a n t s, L L C Slide 3

Preaward Survey of Prospective Contractor Accounting System Checklist

PRE-AWARD SURVEY (SF 1408) OF PROSPECTIVE CONTRACTOR ACCOUNTING SYSTEM Date: XX/XX/201X Company Name, Contract Number, and Full Address: Commercial and Government Agency (CAGE) Code Number: (found at http://www.dlis.dla.mil/cage_welcome.asp)

PRE-AWARD SURVEY (SF 1408) OF PROSPECTIVE CONTRACTOR ACCOUNTING SYSTEM Date: XX/XX/201X Company Name, Contract Number, and Full Address: Commercial and Government Agency (CAGE) Code Number: (found at http://www.dlis.dla.mil/cage_welcome.asp)

As the Defense Contract Audit Agency slowly

Reprinted from Government Contract Costs, Pricing & Accounting Report, with permission of Thomson Reuters. Further use without the permission of West is prohibited. For further information about this publication

Reprinted from Government Contract Costs, Pricing & Accounting Report, with permission of Thomson Reuters. Further use without the permission of West is prohibited. For further information about this publication

Labor Costs Interpretive Guidance Labor Costs: Timekeeping, Direct Labor Base, Labor Transfers & Direct to Indirect Labor Ratio

Labor Costs Interpretive Guidance Labor Costs: Timekeeping, Direct Labor Base, Labor Transfers & Direct to Indirect Labor Ratio External Audits Architectural and Engineering (A&E) Contracts This Document

Labor Costs Interpretive Guidance Labor Costs: Timekeeping, Direct Labor Base, Labor Transfers & Direct to Indirect Labor Ratio External Audits Architectural and Engineering (A&E) Contracts This Document

NSF Grants Conference March 2013. William J. Kilgallin Senior Advisor, Investigations Office of Inspector General National Science Foundation

NSF Grants Conference March 2013 William J. Kilgallin Senior Advisor, Investigations Office of Inspector General National Science Foundation Assistant Inspector General for Audit Inspector General (IG)

NSF Grants Conference March 2013 William J. Kilgallin Senior Advisor, Investigations Office of Inspector General National Science Foundation Assistant Inspector General for Audit Inspector General (IG)

DCAA Audit R 4 Rights to Records, Requirements & Remedies

San Diego Chapters Present DCAA Audit R 4 Rights to Records, Requirements & Remedies A Seminar with Panel Discussion and Audience Participation February 18, 2009 This Morning s Agenda 8:30 Introduction

San Diego Chapters Present DCAA Audit R 4 Rights to Records, Requirements & Remedies A Seminar with Panel Discussion and Audience Participation February 18, 2009 This Morning s Agenda 8:30 Introduction

Presented by Albert D. Goldwasser, CPA Government Contractor Consultant

Presented by Albert D. Goldwasser, CPA Government Contractor Consultant Agenda DCAA s Objectives Accounting 101 Indirect Cost Allocations SF 1408 Passing the DCAA Audit References What does the DCAA want?

Presented by Albert D. Goldwasser, CPA Government Contractor Consultant Agenda DCAA s Objectives Accounting 101 Indirect Cost Allocations SF 1408 Passing the DCAA Audit References What does the DCAA want?

Sage TimeSheet. Defending the Contractor Ensuring DCAA Compliance With Time and Expense Software

Sage TimeSheet Defending the Contractor Ensuring DCAA Compliance With Time and Expense Software Contents Introduction: Executive Summary.............................. 3 History and Mission of the DCAA..............................

Sage TimeSheet Defending the Contractor Ensuring DCAA Compliance With Time and Expense Software Contents Introduction: Executive Summary.............................. 3 History and Mission of the DCAA..............................

FAR UPDATE 52.216-7, Allowable Cost and Payment (Jun 2013)

") FAR UPDATE 52.216-7, Allowable Cost and Payment (Jun 2013) "It's never too early to prepare for your incurred cost submission (A webinar sponsored by Pleasant Valley Business Solutions) 1 Objective Know

FAR UPDATE 52.216-7, Allowable Cost and Payment (Jun 2013) "It's never too early to prepare for your incurred cost submission (A webinar sponsored by Pleasant Valley Business Solutions) 1 Objective Know

DOD's Business Systems Rule: The Challenge Measuring Government Contractor Compliance Against Subjective Criteria and Perceived Risks

DOD's Business Systems Rule: The Challenge Measuring Government Contractor Compliance Against Subjective Criteria and Perceived Risks Breakout Session #: B04 Presented by: Michael E. Steen, CPA Date: July

DOD's Business Systems Rule: The Challenge Measuring Government Contractor Compliance Against Subjective Criteria and Perceived Risks Breakout Session #: B04 Presented by: Michael E. Steen, CPA Date: July

DCAA Our Role. Laura Cloyd-Hall, CPA, MBA John D. Mollohan II, CPA, CFE. Page 1. DCAA 1965-2015: Celebrating 50 Years of Excellence

DCAA Our Role Laura Cloyd-Hall, CPA, MBA John D. Mollohan II, CPA, CFE DCAA 1965-2015: Celebrating 50 Years of Excellence Page 1 Topics About DCAA Typical DCAA Audits for Small Businesses Basic Roles of

DCAA Our Role Laura Cloyd-Hall, CPA, MBA John D. Mollohan II, CPA, CFE DCAA 1965-2015: Celebrating 50 Years of Excellence Page 1 Topics About DCAA Typical DCAA Audits for Small Businesses Basic Roles of

Defending the Contractor: Ensuring DCAA Compliance with Time and Expense Software

Defending the Contractor: Ensuring DCAA Compliance with Time and Expense Software The Premier Sage Software Business Solutions Provider National Presence, Local Touch 1.800.425.9843 www.blytheco.com TABLE

Defending the Contractor: Ensuring DCAA Compliance with Time and Expense Software The Premier Sage Software Business Solutions Provider National Presence, Local Touch 1.800.425.9843 www.blytheco.com TABLE

Defense Contract Audit Agency NAVAIR Small Business Aviation Technology Conference

Defense Contract Audit Agency NAVAIR Small Business Aviation Technology Conference November 29-30, 2006 t Defense Contract Audit Agency Established in 1965 Separate Agency of the Department of Defense

Defense Contract Audit Agency NAVAIR Small Business Aviation Technology Conference November 29-30, 2006 t Defense Contract Audit Agency Established in 1965 Separate Agency of the Department of Defense

Small Business Investment Company Financing Eligibility Statement for Usage of Energy Saving Debenture

OMB Control No. 3245-0379 Small Business Investment Company Financing Eligibility Statement for Usage of Energy Saving Debenture INSTRUCTIONS: Only Small Business Investment Companies ( SBICs ) requesting

OMB Control No. 3245-0379 Small Business Investment Company Financing Eligibility Statement for Usage of Energy Saving Debenture INSTRUCTIONS: Only Small Business Investment Companies ( SBICs ) requesting

Air Force Research Laboratory Grants Terms and Conditions September 2009 Awards to International Educational Institutions and Non-Profit Organizations

Air Force Research Laboratory Grants Terms and Conditions September 2009 Awards to International Educational Institutions and Non-Profit Organizations PART I. Article 1. Administrative Information and

Air Force Research Laboratory Grants Terms and Conditions September 2009 Awards to International Educational Institutions and Non-Profit Organizations PART I. Article 1. Administrative Information and

1 1 1 2 2 2 2 3 3 3 3 3 4 4 4 4 5 back

Introduction Bid Protest Business Systems Design, Evalution and Validation Contractor Accounting & Compliance Risk Assessments Contractor Purchasing System Review (CPSR) Cost Accounting Standards (CAS)

Introduction Bid Protest Business Systems Design, Evalution and Validation Contractor Accounting & Compliance Risk Assessments Contractor Purchasing System Review (CPSR) Cost Accounting Standards (CAS)

SBIR/STTR Post Award Frequently Asked Questions

SBIR/STTR Post Award Frequently Asked Questions FedConnect 1. We have not received notification that our company s grant has been awarded. If our grant has been awarded, how do we access our assistance

SBIR/STTR Post Award Frequently Asked Questions FedConnect 1. We have not received notification that our company s grant has been awarded. If our grant has been awarded, how do we access our assistance

WORKING WITH THE U.S. GOVERNMENT YOUR GUIDE TO THE DCAA

WORKING WITH THE U.S. GOVERNMENT YOUR GUIDE TO THE DCAA The DCAA Audit Created to oversee government spending on behalf of the American tax-payer, the Defense Contract Audit Agency (DCAA) is responsible

WORKING WITH THE U.S. GOVERNMENT YOUR GUIDE TO THE DCAA The DCAA Audit Created to oversee government spending on behalf of the American tax-payer, the Defense Contract Audit Agency (DCAA) is responsible

Government Contractor Business Systems and Overview of System Assessments

Government Contractor Business Systems and Overview of System Assessments Agenda Overview of business systems rules and environment today 3 rd party assessments Practical solutions Contractor perspective

Government Contractor Business Systems and Overview of System Assessments Agenda Overview of business systems rules and environment today 3 rd party assessments Practical solutions Contractor perspective

OFFICE OF THE UNDER SECRETARY OF DEFENSE 3000 DEFENSE PENTAGON WASHINGTON, DC 20301-3000

ACQUISITION. TECHNOLOGY AND LOGISTICS OFFICE OF THE UNDER SECRETARY OF DEFENSE 3000 DEFENSE PENTAGON WASHINGTON, DC 20301-3000 MEMORANDUM FOR ASSISTANT SECRETARY OF THE ARMY (ACQUISITION, LOGISTICS AND

ACQUISITION. TECHNOLOGY AND LOGISTICS OFFICE OF THE UNDER SECRETARY OF DEFENSE 3000 DEFENSE PENTAGON WASHINGTON, DC 20301-3000 MEMORANDUM FOR ASSISTANT SECRETARY OF THE ARMY (ACQUISITION, LOGISTICS AND

Incurred Cost Submissions. John S. Sroka, CPA Acquisition Cost/Price Analyst

Incurred Cost Submissions John S. Sroka, CPA Acquisition Cost/Price Analyst Incurred Cost Proposals Allowable cost and payment clause requires the submission (FAR 52.216-7) Requires a signed certification

Incurred Cost Submissions John S. Sroka, CPA Acquisition Cost/Price Analyst Incurred Cost Proposals Allowable cost and payment clause requires the submission (FAR 52.216-7) Requires a signed certification

What Documents are required at Pre-award Audit of an agreement or sub-agreement. How to Avoid Common Proposal Mistakes

January 29, 2015 What Documents are required at Pre-award Audit of an agreement or sub-agreement How to Avoid Common Proposal Mistakes How to Avoid Common Invoice Mistakes Pre-Award Review New Agreement/Sub-agreement:

January 29, 2015 What Documents are required at Pre-award Audit of an agreement or sub-agreement How to Avoid Common Proposal Mistakes How to Avoid Common Invoice Mistakes Pre-Award Review New Agreement/Sub-agreement:

Peckar & Abramson. A Professional Corporation Attorneys & Counselors at Law

A Professional Corporation Attorneys & Counselors at Law EXPANSION OF FEDERAL GOVERNMENT AUDIT POWERS AND PROGRAMS: WHAT TO DO WHEN THE AUDITORS ARRIVE Our earlier s described initiatives by the federal

A Professional Corporation Attorneys & Counselors at Law EXPANSION OF FEDERAL GOVERNMENT AUDIT POWERS AND PROGRAMS: WHAT TO DO WHEN THE AUDITORS ARRIVE Our earlier s described initiatives by the federal

SUBCHAPTER G CONTRACT MANAGEMENT PART 842 CONTRACT ADMINISTRATION AND AUDIT SERVICES

SUBCHAPTER G CONTRACT MANAGEMENT PART 842 CONTRACT ADMINISTRATION AND AUDIT SERVICES Sec. 842.000 Scope of part. 842.070 Definitions. Subpart 842.1 Contract Audit Services 842.101 Contract audit responsibilities.

SUBCHAPTER G CONTRACT MANAGEMENT PART 842 CONTRACT ADMINISTRATION AND AUDIT SERVICES Sec. 842.000 Scope of part. 842.070 Definitions. Subpart 842.1 Contract Audit Services 842.101 Contract audit responsibilities.

Frequently Asked Questions (FAQ s)

") Questions about Cognizance: Frequently Asked Questions (FAQ s) 1. How can I determine who is my cognizant agency responsible to establish my indirect cost rate(s)? For commercial, for-profit companies

Questions about Cognizance: Frequently Asked Questions (FAQ s) 1. How can I determine who is my cognizant agency responsible to establish my indirect cost rate(s)? For commercial, for-profit companies

NOT ALL COMMUNITY SERVICES BLOCK GRANT RECOVERY ACT COSTS CLAIMED

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL NOT ALL COMMUNITY SERVICES BLOCK GRANT RECOVERY ACT COSTS CLAIMED ON BEHALF OF THE COMMUNITY ACTION PARTNERSHIP OF NATRONA COUNTY FOR

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL NOT ALL COMMUNITY SERVICES BLOCK GRANT RECOVERY ACT COSTS CLAIMED ON BEHALF OF THE COMMUNITY ACTION PARTNERSHIP OF NATRONA COUNTY FOR

Are You Looking to Sell Your Products & Services to the US Government? Overview

Are You Looking to Sell Your Products & Services to the US Government? What You Need to Know About Accounting, Compliance, and Reporting! 1 FICPA Overview The US Government is the largest consumer of goods

Are You Looking to Sell Your Products & Services to the US Government? What You Need to Know About Accounting, Compliance, and Reporting! 1 FICPA Overview The US Government is the largest consumer of goods

Time s Up: DCAA s Renewed Focus on Incurred Cost Submissions

Time s Up: DCAA s Renewed Focus on Incurred Cost Submissions Nicole Mitchell, CPA Donna Dominguez Aronson LLC May 1, 2013 2013 All Rights Reserved 805 King Farm Boulevard Suite 300 Rockville, Maryland

Time s Up: DCAA s Renewed Focus on Incurred Cost Submissions Nicole Mitchell, CPA Donna Dominguez Aronson LLC May 1, 2013 2013 All Rights Reserved 805 King Farm Boulevard Suite 300 Rockville, Maryland

The Environmental Careers Organization Reported Outlays for Five EPA Cooperative Agreements

OFFICE OF INSPECTOR GENERAL Attestation Report Catalyst for Improving the Environment The Environmental Careers Organization Reported Outlays for Five EPA Cooperative Agreements Report No. 2007-4-00065

OFFICE OF INSPECTOR GENERAL Attestation Report Catalyst for Improving the Environment The Environmental Careers Organization Reported Outlays for Five EPA Cooperative Agreements Report No. 2007-4-00065

CAS. Combined Air Support Cost Accounting Standards. Cost Impact Statements

CAS Combined Air Support Cost Accounting Standards Cost Impact Statements Cost Impact Statements Presenter: Anthony J. Nicolella References 48 CFR 9903 CON 252 Fundamentals of CAS FAR Parts 30, 31 and

CAS Combined Air Support Cost Accounting Standards Cost Impact Statements Cost Impact Statements Presenter: Anthony J. Nicolella References 48 CFR 9903 CON 252 Fundamentals of CAS FAR Parts 30, 31 and

ACCOUNTING AND AUDITING GUIDELINES. Table of Contents 11.1 MDT POLICIES AND PROCEDURES...11-1

Table of Contents Section Page 11.1 MDT POLICIES AND PROCEDURES...11-1 11.1.1 General...11-1 11.1.2 Cognizant Indirect Cost Rate Review...11-1 11.1.3 Contract Compliance Audit...11-3 11.1.3.1 Objective...11-3

Table of Contents Section Page 11.1 MDT POLICIES AND PROCEDURES...11-1 11.1.1 General...11-1 11.1.2 Cognizant Indirect Cost Rate Review...11-1 11.1.3 Contract Compliance Audit...11-3 11.1.3.1 Objective...11-3

FLORIDA ATLANTIC UNIVERSITY COST-REIMBURSABLE SUBAWARD AGREEMENT #

FLORIDA ATLANTIC UNIVERSITY COST-REIMBURSABLE SUBAWARD AGREEMENT # This Cost Reimbursable Subaward Agreement is entered into in order to specify the terms and conditions under which Florida Atlantic University,

FLORIDA ATLANTIC UNIVERSITY COST-REIMBURSABLE SUBAWARD AGREEMENT # This Cost Reimbursable Subaward Agreement is entered into in order to specify the terms and conditions under which Florida Atlantic University,

Managing Cost Type Contracts

Managing Cost Type Contracts October 9, 2013 By: Tom Marcinko Donna Dominguez 2013 All Rights Reserved 805 King Farm Boulevard Suite 300 Rockville, Maryland 20850 301.231.6200 P 301.231.7630 F www.aronsonllc.com

Managing Cost Type Contracts October 9, 2013 By: Tom Marcinko Donna Dominguez 2013 All Rights Reserved 805 King Farm Boulevard Suite 300 Rockville, Maryland 20850 301.231.6200 P 301.231.7630 F www.aronsonllc.com

AUDIT OF NASA GRANTS AWARDED TO THE PHILADELPHIA COLLEGE OPPORTUNITY RESOURCES FOR EDUCATION

JULY 26, 2012 AUDIT REPORT OFFICE OF AUDITS AUDIT OF NASA GRANTS AWARDED TO THE PHILADELPHIA COLLEGE OPPORTUNITY RESOURCES FOR EDUCATION OFFICE OF INSPECTOR GENERAL National Aeronautics and Space Administration

JULY 26, 2012 AUDIT REPORT OFFICE OF AUDITS AUDIT OF NASA GRANTS AWARDED TO THE PHILADELPHIA COLLEGE OPPORTUNITY RESOURCES FOR EDUCATION OFFICE OF INSPECTOR GENERAL National Aeronautics and Space Administration

DCAA New Tactics in Obtaining Contractor Internal audit reports

DCAA New Tactics in Obtaining Contractor Internal audit reports By Todd Bishop and David Eck, CPA In August 2012, the Defense Contract Audit Agency (DCAA) issued updates to its policy guidance and the

DCAA New Tactics in Obtaining Contractor Internal audit reports By Todd Bishop and David Eck, CPA In August 2012, the Defense Contract Audit Agency (DCAA) issued updates to its policy guidance and the

Is Your Accounting System Making the Grade? Attributes of an Acceptable Accounting System April 26, 2012

Is Your Accounting System Making the Grade? Attributes of an Acceptable Accounting System April 26, 2012 2012 All Rights Reserved 805 King Farm Boulevard Suite 300 Rockville, Maryland 20850 301.231.6200

Is Your Accounting System Making the Grade? Attributes of an Acceptable Accounting System April 26, 2012 2012 All Rights Reserved 805 King Farm Boulevard Suite 300 Rockville, Maryland 20850 301.231.6200

DCAA Perspective: Key Subcontracting Practices for Maintaining Approved Business Systems Accounting System and Estimating System

DCAA Perspective: Key Subcontracting Practices for Maintaining Approved Business Systems Accounting System and Estimating System Breakout Session A Alfred J. Massey, Western Region, Special Programs Manager,

DCAA Perspective: Key Subcontracting Practices for Maintaining Approved Business Systems Accounting System and Estimating System Breakout Session A Alfred J. Massey, Western Region, Special Programs Manager,

How to Survive a DCAA Pre-Award Audit

How to Survive a DCAA Pre-Award Audit February 27, 13 Presented by: Paul H. Calabrese Senior Manager 301-214-4137 [email protected] Bio http://www.rubino.com/company/staff/11- paul_h_calabrese/view LinkedIn

How to Survive a DCAA Pre-Award Audit February 27, 13 Presented by: Paul H. Calabrese Senior Manager 301-214-4137 [email protected] Bio http://www.rubino.com/company/staff/11- paul_h_calabrese/view LinkedIn

Attachment II FLOW-DOWN CLAUSES APPLICABLE TO PURCHASE ORDERS INVOLVING FUNDS FROM A FEDERAL GOVERNMENT CONTRACT OR GRANT

Attachment II FLOW-DOWN CLAUSES APPLICABLE TO PURCHASE ORDERS INVOLVING FUNDS FROM A FEDERAL GOVERNMENT CONTRACT OR GRANT If the Order involves funds from a Federal government contract or funds from a

Attachment II FLOW-DOWN CLAUSES APPLICABLE TO PURCHASE ORDERS INVOLVING FUNDS FROM A FEDERAL GOVERNMENT CONTRACT OR GRANT If the Order involves funds from a Federal government contract or funds from a

C O N F I D E N T I A L A N D P R O P R I E T A R Y. Page 1 of 7 Title: FRAUD, WASTE, AND ABUSE POLICY

Page 1 of 7 1. Purpose As a Company that does business with U.S. state and federal government health care programs (such as Medicare and Medicaid), Hill-Rom is required to maintain a system of policies

Page 1 of 7 1. Purpose As a Company that does business with U.S. state and federal government health care programs (such as Medicare and Medicaid), Hill-Rom is required to maintain a system of policies

Material Transfers and Material Management and Accounting System (MMAS)

") Material Transfers and Material Management and Accounting System (MMAS) The Scenario Risk Assessment-Research and Planning: The auditor was assigned an audit of major contractor MIL s Material Management

Material Transfers and Material Management and Accounting System (MMAS) The Scenario Risk Assessment-Research and Planning: The auditor was assigned an audit of major contractor MIL s Material Management

DCAA Compliant Accounting Systems

DCAA Compliant Accounting Systems State Designated as Florida s Principal Provider of Business Assistance [ 288.001, Fla. Stat.] Helping Businesses Grow & Succeed About Your Presenter Jenny W. Clark With

DCAA Compliant Accounting Systems State Designated as Florida s Principal Provider of Business Assistance [ 288.001, Fla. Stat.] Helping Businesses Grow & Succeed About Your Presenter Jenny W. Clark With

Chapter 6 Labor-Charging Systems and Other Considerations

6 Chapter 6 Labor-Charging Systems and Other Considerations The purpose of this chapter is to provide interpretive guidance only. This chapter is not intended to be authoritative or to supersede the FAR.

6 Chapter 6 Labor-Charging Systems and Other Considerations The purpose of this chapter is to provide interpretive guidance only. This chapter is not intended to be authoritative or to supersede the FAR.

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission National Archives www.archives.gov/nhprc June 17, 2015 Table of Contents USE OF THE

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission National Archives www.archives.gov/nhprc June 17, 2015 Table of Contents USE OF THE

How to Deal with DCAA Auditors

How to Deal with DCAA Auditors Breakfast Seminar March 13, 2014 Copyright 2014 Rubino & Company, Chartered Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137

How to Deal with DCAA Auditors Breakfast Seminar March 13, 2014 Copyright 2014 Rubino & Company, Chartered Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137

Certificate of Accounting, Billing and Property System Adequacy

Certificate of Accounting, Billing and Property System Adequacy This certifies that, to the best of my knowledge and belief, Contractor s Accounting, Billing and/or Property System and related internal

Certificate of Accounting, Billing and Property System Adequacy This certifies that, to the best of my knowledge and belief, Contractor s Accounting, Billing and/or Property System and related internal

Guide to SBIR/STTR Program Eligibility

Guide to SBIR/STTR Program Eligibility Updated: January 2013 U.S. Small Business Administration This document is published by the U.S. Small Business Administration as the official compliance guide for

Guide to SBIR/STTR Program Eligibility Updated: January 2013 U.S. Small Business Administration This document is published by the U.S. Small Business Administration as the official compliance guide for

DEFENSE CONTRACT AUDIT AGENCY GUIDE FOR DETERMINING ADEQUACY OF CONTRACTOR INCURRED COST PROPOSAL

Instructions: This form should be completed for each proposal submission and maintained in the permanent file. Adequacy reviews of contractor incurred cost proposals include verification for completeness

Instructions: This form should be completed for each proposal submission and maintained in the permanent file. Adequacy reviews of contractor incurred cost proposals include verification for completeness

Flexible Circuits Inc. Purchase Order Standard Terms and Conditions

Flexible Circuits Inc. Purchase Order Standard Terms and Conditions 1. Acceptance- This writing, together with any attachments incorporated herein, constitutes the final, complete, and exclusive contract

Flexible Circuits Inc. Purchase Order Standard Terms and Conditions 1. Acceptance- This writing, together with any attachments incorporated herein, constitutes the final, complete, and exclusive contract

U.S. Department of Justice Office of the Inspector General Audit Division

AUDIT OF THE OFFICE OF JUSTICE PROGRAMS NATIONAL INSTITUTE OF JUSTICE COOPERATIVE AGREEMENTS WITH AKELA, INCORPORATED SANTA BARBARA, CALIFORNIA U.S. Department of Justice Office of the Inspector General

AUDIT OF THE OFFICE OF JUSTICE PROGRAMS NATIONAL INSTITUTE OF JUSTICE COOPERATIVE AGREEMENTS WITH AKELA, INCORPORATED SANTA BARBARA, CALIFORNIA U.S. Department of Justice Office of the Inspector General