Economics I. Decision-making Firm in Imperfect Competition

|

|

|

- Raymond Lucas

- 10 years ago

- Views:

Transcription

1 Economics I Decision-making Firm in Imperfect Competition

2 The aim of the first lecture is to explain and analyze the markets in imperfect competition and firm behavior in imperfectly competitive environment. Explain the causes of imperfect competition, clarify monopoly, monopoly equilibrium, the implications of monopoly, oligopoly - oligopoly with a dominant firm and contract oligopoly.

3 The second lecture is going to explain and analyze the market of monopolistic competition and firm behavior in this type of imperfectly competitive environment. Explain the causes of imperfect competition. In the next part of this lecture is attention given to companies that are coming to market with other purpose than profit maximization. Alternative objectives of the company will be defined as well as characterized and explained managerial and behaviorist models.

4 Content: Introduction 1. Characteristics of imperfect competition. The main causes of imperfect competition 2. Equilibrium firms in imperfect competition 3. Monopoly 4. Oligopoly 4.1 Contracting oligopoly 4.2 Oligopoly with dominant company 5. Monopolistic competition

5 6. Types of companies 6.1 Joint Stock Company 6.2 The behavior of large firms 7. Alternate company objectives 7.1 Alternative Theories Managerial theory of the firm Behaviorist models of the company Staff model of the firm Non-profit firms Conclusion

6 References and further reading: 1. MACÁKOVÁ, L. aj. Mikroekonomie základní kurs. 10. vyd. Praha: Melandrium Slaný, ISBN s SIRŮČEK, P., NEČADOVÁ, M. Mikroekonomická teorie 1 cvičebnice. 1. vyd. Praha: Melandrium Slaný, ISBN s BRADLEY, R. SCHILLER. Mikroekonomie. Brno: Computer Press, ISBN HOLMAN, R. Mikroekonomie středně pokročilý kurz. 1. vyd. Praha: C. H. Beck, ISBN HOLMAN, R. Ekonomie. 3. vyd. Praha: C. H. Beck, ISBN TULEJA, P., NEZVAL, P., MAJEROVÁ, I. Základy mikroekonomie (Učebnice pro ekonomické a obchodně podnikatelské fakulty). 1. vyd. Brno: Nakladatelství CP Books, a. s., ISBN

. 1. vyd. Brno: Nakladatelství CP Books, a. s., 2005.")

7 1. DESCRIPTION OF IMPERFECT COMPETITION. MAIN CAUSES OF OMPERFECT COMPETITION.

8 differentiated product, existence of at least one seller who can influence the price price maker decreasing demand curve for companies production, company decides on the optimal level of production volume as well as price, company size.

9 Graph of the individual demand P perfect competition konkurenci P inperfect competition d d Q Q

10 Forms of imperfect competition: monopoly (pure monopoly, natural monopoly, monopsony) oligopoly (contractual oligopoly, oligopoly with a dominant firm) monopolistic competition

")

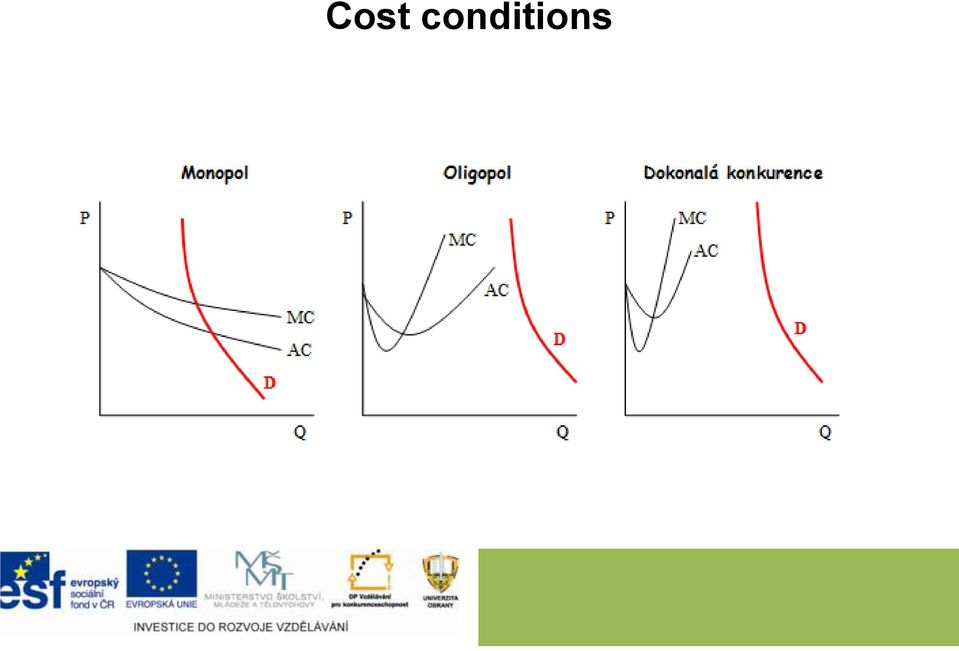

11 The main causes of imperfect competition: cost conditions (increasing returns to scale): barriers to competition

: barriers")

12 cost conditions (increasing returns to scale): - Company whose MC and AC are constantly decreasing. With the growth of the output volume are AC declining - therefore economies of scale are realized. It pays to increase the volume until the intersection with the sector demand curve - the whole demand provided by monopolist.

13 - Economies of scale have been exhausted and the growth of production volume represents an increase of AC. The demand curve does not provide enough large market, for the existence of a large number of firms, but only for a few firms - demand provided by oligopolistic competition.

14 - Companies unit costs are growing quite soon. Market demand curve is very far from efficient production of a single producer. That provides a space for a large number of firms - perfect competition.

15 Cost conditions

16 2. COMPANIES BALANCE IN IMPERFECT COMPETITION

17 To determinate the optimum firm production volume in conditions of perfect competition we come out the conclusions: profit is the difference between total revenue and total costs, profit is maximized at such a volume of production, where is the biggest difference between total revenues and total costs, company is in balance, producing the volume of production, in which maximizes its profits. The equilibrium production volume is derived from the relationship MR = MC.

18 Total revenue in imperfect competition total volume of production is obtained from the relation TR = P.Q, total income may rise or fall (depending on the elasticity of companies production demand). - Demand is elastic - a percentage increase in the volume of the sold production is greater than the percentage decrease in price, so even though the decreases price, the total income is growing. - Demand is inelastic - percentage growth in the volume of the sold production is less than the percentage decrease in price, so if the company lowers the price, its total revenue is decreasing.

19 Marginal revenue in imperfect competition As in the case of imperfect competition is demand curve decreasing, marginal revenue (MR) decreases with the increase of production and must be lower than the price at which is sold the last unit (MR <P) MR like TR is affected by the elasticity of demand: - MR> 0 - demand is elastic, - MR = 0 - demand is unitary elastic, - MR <0 - demand is inelastic.

20 Marginal and average income in imperfect competition definition of unit revenue: - MR = TR / Q -AR = TR / Q = P two basic differences from perfect competition: - AR and MR curves have a negative slope, which is the result of a negative slope of individual demand curve, - MR curve is identical with the curve of the AR, but decreases rapidly.

21 Profit difference between TR and TC z = TR TC MR = MC determine equilibrium quantity of the production MR = ΔTR/ΔQ AR = TR/Q

22 Relationship between TR and demand price elasticity TR e PD > 1 TR grows MR > 0 Max. TR, MR = 0, e PD = 1 e PD < 1 TR decreases MR < 0 TR P e PD > 1 e PD = 1 e PD < 1 q e q max. obrat Q Q

23 3. MONOPOLY

24 Characteristics of monopoly monopoly is a form of competition, the counterpart of perfect competition, existence of a single subject on the supply side, insurmountable barriers to entry, monopoly firm is called "Price maker" close substitutes to the production offered by the monopoly, individual demand = market demand curve, its production is the production of the entire sector, existence of a monopoly is closely associated with geographic definition of the market.

25 Causes of monopoly: amount of the average cost - NATURAL (NETWORK) MONOPOLY (distribution networks of water, electricity, gas, railways, highways, etc.) control of natural resources (single firm controls the natural resources needed to manufacture the product) - NATURAL MONOPOLY, State intervention (State grants the exclusive right to manufacture the product to a particular firm) - Artificially created monopoly (CNB, Czech Post) Legal restrictions - patents and copyrights - Artificially created monopoly (the rights of film companies, etc.).

26 Monopoly production price depends on the willingness of consumers to pay it, thus on the market demand, is intended above MC (P> MC). The difference between price and marginal cost is influenced by the price elasticity of demand, with increasing elasticity of demand decreases. Monopoly supply curve is impossible to be constructed, can not be identified with the MC curve monopoly.

27 Monopoly equilibrium P Kč/Q PROFIT AR>AC profit Output is not usually produced with the min. AC: min. of AC is on the right from Q* P* MR MC AC Q* < Q minac P > MC (DWL Dead Weight Loss) D = AR Q* - MR = MC Q* Q minac Q

28 Monopoly power The price at which the monopoly sells its products contains the monopoly profit since P> MC. The higher the excess of price over marginal cost is, the higher is the monopoly power. Monopoly power is measured by the Lerner index, which has the following form: L = P - MC / P For a perfectly competitive market, applies L = 0, since P = MC. Values greater than zero indicate monopoly power.

29 Efficiency of the monoply and perfect competition Perfect competition Monopoly Kč/Q Consumer surplus Kč/Q Consumer surplus S MC B(P>MC) P M P DK P=MC P DK E Producesr surplus D C Producer surplus D=d Q DK Q Q M Q DK Q MR

30 Monopoly regulation Monopolist sets up the price above marginal cost, what leads to a loss of efficiency. For these reason is the government trying to reduce the costs of monopoly with the following tools: Increasing taxes Price regulation State ownership Antitrust policy Economic regulation

31 Price regulation Price regulation of the monopoly Kč/Q MC P M P R M R I AC P I D=AR=d Q M Q R MR Q I Q

32 Monopsony is the opposite of monopoly, represents a market in which there is only one buyer, monopsony power is the ability of the buyer to affect price in its favor, allows the buyer to purchase goods at a lower price than in perfect competition. For example: the state is the only buyer of a military production

33 4. OLIGOPOLY

34 Represents a few sellers on the market. Companies have a great economic power and the ability to interact. It is a market with a small number of firms in the industry (oligo a few duopoly - two firms in the sector), with a high degree of dependency of decision. The product is similar or identical, each company is so strong that it can affect the price and there are barriers to entry to the sector. Companies can cooperate on the basis of agreements on cooperation or possible individual competition.

35 Oligopoly types According to the type of offered product: pure oligopoly, differentiated oligopoly. Depending the side of the market it operates: supply oligopoly, demand oligopoly - oligopsony. Depending on the number of firms and their market share duopoly contractual oligopoly, oligopoly with a dominant firm.

36 4.1 Contracting oligopoly

37 Cartel - a group of companies in the market, acting in agreement (OPEC): Better for them is to increase the joint profits by increasing prices or market splitting, conclude a secret agreement and set up of monopoly prices for individual firms or production quotas - each firm in an oligopoly then acts as a monopoly. Dual oligopoly or duopoly The market has only two firms. Both companies are very well readable to each other. They adapt their behavior.

38 Contracting oligopoly Kč/Q G MC AC P O F E d 1 Q O MR Q

39 4.2 Oligopoly with dominant company

40 Frequently sector consists of one large and dominant company which is surrounded by a number of smaller rivals. It therefore has two components: Dominant firm - one firm acts as a monopolist, but respects competing hem. Competitive hem a number of small firms that act as perfect competition, ie. accept the price set by the dominant firm.

41 The market situation in which one strong (dominant) firm is called the price leader, and several weaker, smaller firms (competitive hem) operate on the market. Small firms are unable significantly influence the market. competitive hem takes the price from the dominant firm, maximizing profit for the dominant firm MR = MC, maximizing profit for competitive hem P = MC.

42 Oligopoly with a dominant firm and competitive hem P ΣMC ~ S of the comtetitive hem P 1 P 2 P d E d MC d D d D t MR d q E Q d+kl Q 42

43 5. Monopolistic competition

44 Basic assumptions of monopolistic competition: large number of companies in sector, goods are heterogeneous with a small differentiations - location of the company, - packaging, related services, sales conditions, - price. absence of barriers to entry of firms into the industry, existence of a well-informed, there are no market risk.

45 In the long run there is similar situation to the perfect competition. Equilibrium occurs when the intersection of the AR is the same amount as the intersection MR (Profit = 0). In a short run monopolistic firms can realize economic profit, while in the long run due to the input of companies into sector and the subsequent decline in prices is realized zero economic profit.

46 Output in the SR SMC = MR CZK/Q SMC P* SAC AR = d profit MR Q* Q

47 Output in the LR LMC = MR CZK/Q LMC LAC SAC profit P* SR P* LR AR 1 = d 1 AR 2 = d 2 Q* LR Q* SR MR 1 MR 2 Q

48 Monopolistic competition short run long run Kč/Q Kč/Q SMC LMC P SR AC ZISK SAC AR=d P LR P DK LAC AR=d Q SR MR Q Q LR Q DK MR Q

49 6. TYPES OF COMPANIES

50 Division of companies in terms of ownership: Companies owned individually - on his account go all gains and losses and the company is liable for the obligations of its property, Commercial companies - capital association of two or more people = increase the possibility of financial development at the cost of increased legal complexity, Joint Stock Company - wider possibilities of obtaining funds through the issue of shares.

51 6.1 Joint Stock Company

52 Shares - valuable paper that gives its holder the right to co-decide on the fundamentals of firms business (General Meeting). Number of votes depends on the number of shares. Dividend - profit that is for each company owners (shareholders). Joint stock company profit: undistributed profit for the company's development, profits distributed to shareholders as dividends.

53 Control activities carried out by professional managers - a contradiction in the interests of managers and shareholders. The control package is a number of shares sufficient to gain control of the company (51%, but 20% or even 5%). Bonds - a kind of promissory note, the owner is creditor of the company. Bonds bring contractually agreed interest (the amount of shares depends on the results of the company).

54 6.2 The behavior of a large firm conditions of equilibrium profit-maximizing firms: marginal cost (MC) = marginal revenue (MR) Reality is more complex - in fact of impossibility to construct a curve D and curve MC for a large number of different goods P = AC (average cost) + premium (profit) Main limiting factor in determining premiums is demand Profit remains the goal of the company and a major impetus to the business The firm maximizes its profit when maximizing the difference between TR (total revenue) and TC (total cost).

55 Can be divided into two components: - Reducing the cost of production - Revenue maximizing - increase the volume - Price competition - the voluntary renunciation of profits - Non-price competition - increases business costs, but increase the production volume without a price drop.

56 7. ALTERNATIVE COMPANY OBJECTIVES

57 The most common alternative goals of the company: maximize turnover increase market share achieve a satisfactory level of profit survival growth and expansion ensuring solvency increasing independence achieving a certain level of economic power

58 Managerial theory of the firm: Simple management model Baumol model Behaviorist theory of the firm. Model of the employee company.

59 Managerial theory of the firm firmly influenced by neoclassical economics and institutionalism, emphasize the separation of ownership and management, focus on the behavior of large companies, which are managed by professional managers (managers goals may be different from the objectives owners).

60 Simple managerial model: Goal to maximize the benefit of managers Base management model adopted in joint stock companies benefit is given to a manager by the position in the company, Model where the utility function is profit and ancillary benefits and revenue managers.

61 The objectives of managers: Efforts to increase their own salaries, Efforts to increase the number of employees, New development investments, Efforts to obtain additional benefits: - Car for private purposes, - Laptop, - Business mobile phone, - Free training opportunities, - Corporate apartment for free, - Pension insurance, - Health extras, - Premium rewards - Severance pay, and others.

62 assumption - Imperfect competition, Baumol model: - The existence of entry barriers. The goal of managers is to maximize the company's turnover - TR = P. Q maximizing turnover company always produces more volume at a lower price than the profit-maximizing firm and MR <MC.

63 Baumol model P MC P 1 P 2 d = AR Q 1 Q 2 MR Q

64 Behaviorist theory of the firm: goal of the company is the result of clashes of interests and goals of individuals and groups within the company, The company is seen as a coalition of various interest groups, with the goal of a firm can vary with changes in the objectives of individual groups and changes their power within the company, target function is not to maximize a certain variable (profit, turnover), but achieving its "satisfactory" level, thus achieving an acceptable outcome for all groups.

65 Non-profit companies: group of companies whose aim is not profit maximization, their goal is not to achieve a profit, but certain needs of the society, are usually funded by the state (state budget), there are also non-market actors that contribute to meeting the needs of society as a whole - schools, hospitals, churches, some may operate on a commercial basis (private schools,...).

66 Questions? Thank you for your attention

Course: Economics I. Author: Ing. Martin Pop

Course: Economics I Author: Ing. Martin Pop Contents Introduction 1. Characteristics of imperfect competition. The main causes of imperfect competition 2. Equilibrium firms in imperfect competition 3.

Course: Economics I Author: Ing. Martin Pop Contents Introduction 1. Characteristics of imperfect competition. The main causes of imperfect competition 2. Equilibrium firms in imperfect competition 3.

Chapter 15: Monopoly WHY MONOPOLIES ARISE HOW MONOPOLIES MAKE PRODUCTION AND PRICING DECISIONS

Chapter 15: While a competitive firm is a taker, a monopoly firm is a maker. A firm is considered a monopoly if... it is the sole seller of its product. its product does not have close substitutes. The

Chapter 15: While a competitive firm is a taker, a monopoly firm is a maker. A firm is considered a monopoly if... it is the sole seller of its product. its product does not have close substitutes. The

UNIVERSITY OF CALICUT MICRO ECONOMICS - II

UNIVERSITY OF CALICUT SCHOOL OF DISTANCE EDUCATION BA ECONOMICS III SEMESTER CORE COURSE (2011 Admission onwards) MICRO ECONOMICS - II QUESTION BANK 1. Which of the following industry is most closely approximates

UNIVERSITY OF CALICUT SCHOOL OF DISTANCE EDUCATION BA ECONOMICS III SEMESTER CORE COURSE (2011 Admission onwards) MICRO ECONOMICS - II QUESTION BANK 1. Which of the following industry is most closely approximates

Pricing and Output Decisions: i Perfect. Managerial Economics: Economic Tools for Today s Decision Makers, 4/e By Paul Keat and Philip Young

Chapter 9 Pricing and Output Decisions: i Perfect Competition and Monopoly M i l E i E i Managerial Economics: Economic Tools for Today s Decision Makers, 4/e By Paul Keat and Philip Young Pricing and

Chapter 9 Pricing and Output Decisions: i Perfect Competition and Monopoly M i l E i E i Managerial Economics: Economic Tools for Today s Decision Makers, 4/e By Paul Keat and Philip Young Pricing and

1 Monopoly Why Monopolies Arise? Monopoly is a rm that is the sole seller of a product without close substitutes. The fundamental cause of monopoly is barriers to entry: A monopoly remains the only seller

1 Monopoly Why Monopolies Arise? Monopoly is a rm that is the sole seller of a product without close substitutes. The fundamental cause of monopoly is barriers to entry: A monopoly remains the only seller

Oligopoly: How do firms behave when there are only a few competitors? These firms produce all or most of their industry s output.

Topic 8 Chapter 13 Oligopoly and Monopolistic Competition Econ 203 Topic 8 page 1 Oligopoly: How do firms behave when there are only a few competitors? These firms produce all or most of their industry

Topic 8 Chapter 13 Oligopoly and Monopolistic Competition Econ 203 Topic 8 page 1 Oligopoly: How do firms behave when there are only a few competitors? These firms produce all or most of their industry

Learning Objectives. Chapter 6. Market Structures. Market Structures (cont.) The Two Extremes: Perfect Competition and Pure Monopoly

The Two Extremes: Perfect Competition and Pure Monopoly") Chapter 6 The Two Extremes: Perfect Competition and Pure Monopoly Learning Objectives List the four characteristics of a perfectly competitive market. Describe how a perfect competitor makes the decision

Chapter 6 The Two Extremes: Perfect Competition and Pure Monopoly Learning Objectives List the four characteristics of a perfectly competitive market. Describe how a perfect competitor makes the decision

This hand-out gives an overview of the main market structures including perfect competition, monopoly, monopolistic competition, and oligopoly.

Market Structures This hand-out gives an overview of the main market structures including perfect competition, monopoly, monopolistic competition, and oligopoly. Summary Chart Perfect Competition Monopoly

Market Structures This hand-out gives an overview of the main market structures including perfect competition, monopoly, monopolistic competition, and oligopoly. Summary Chart Perfect Competition Monopoly

Managerial Economics & Business Strategy Chapter 9. Basic Oligopoly Models

Managerial Economics & Business Strategy Chapter 9 Basic Oligopoly Models Overview I. Conditions for Oligopoly? II. Role of Strategic Interdependence III. Profit Maximization in Four Oligopoly Settings

Managerial Economics & Business Strategy Chapter 9 Basic Oligopoly Models Overview I. Conditions for Oligopoly? II. Role of Strategic Interdependence III. Profit Maximization in Four Oligopoly Settings

Chapter 9 Basic Oligopoly Models

Managerial Economics & Business Strategy Chapter 9 Basic Oligopoly Models McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. Overview I. Conditions for Oligopoly?

Managerial Economics & Business Strategy Chapter 9 Basic Oligopoly Models McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. Overview I. Conditions for Oligopoly?

Monopoly WHY MONOPOLIES ARISE

In this chapter, look for the answers to these questions: Why do monopolies arise? Why is MR < P for a monopolist? How do monopolies choose their P and Q? How do monopolies affect society s well-being?

In this chapter, look for the answers to these questions: Why do monopolies arise? Why is MR < P for a monopolist? How do monopolies choose their P and Q? How do monopolies affect society s well-being?

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

MBA 640 Survey of Microeconomics Fall 2006, Quiz 6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly is best defined as a firm that

MBA 640 Survey of Microeconomics Fall 2006, Quiz 6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly is best defined as a firm that

Models of Imperfect Competition

Models of Imperfect Competition Monopolistic Competition Oligopoly Models of Imperfect Competition So far, we have discussed two forms of market competition that are difficult to observe in practice Perfect

Models of Imperfect Competition Monopolistic Competition Oligopoly Models of Imperfect Competition So far, we have discussed two forms of market competition that are difficult to observe in practice Perfect

Managerial Economics & Business Strategy Chapter 8. Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets

Managerial Economics & Business Strategy Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets I. Perfect Competition Overview Characteristics and profit outlook. Effect

Managerial Economics & Business Strategy Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets I. Perfect Competition Overview Characteristics and profit outlook. Effect

All these models were characterized by constant returns to scale technologies and perfectly competitive markets.

Economies of scale and international trade In the models discussed so far, differences in prices across countries (the source of gains from trade) were attributed to differences in resources/technology.

Economies of scale and international trade In the models discussed so far, differences in prices across countries (the source of gains from trade) were attributed to differences in resources/technology.

Pre-Test Chapter 23 ed17

Pre-Test Chapter 23 ed17 Multiple Choice Questions 1. The kinked-demand curve model of oligopoly: A. assumes a firm's rivals will ignore a price cut but match a price increase. B. embodies the possibility

Pre-Test Chapter 23 ed17 Multiple Choice Questions 1. The kinked-demand curve model of oligopoly: A. assumes a firm's rivals will ignore a price cut but match a price increase. B. embodies the possibility

MPP 801 Monopoly Kevin Wainwright Study Questions

MPP 801 Monopoly Kevin Wainwright Study Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The marginal revenue facing a monopolist A) is

MPP 801 Monopoly Kevin Wainwright Study Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The marginal revenue facing a monopolist A) is

Figure: Computing Monopoly Profit

Name: Date: 1. Most electric, gas, and water companies are examples of: A) unregulated monopolies. B) natural monopolies. C) restricted-input monopolies. D) sunk-cost monopolies. Use the following to answer

Name: Date: 1. Most electric, gas, and water companies are examples of: A) unregulated monopolies. B) natural monopolies. C) restricted-input monopolies. D) sunk-cost monopolies. Use the following to answer

CHAPTER 18 MARKETS WITH MARKET POWER Principles of Economics in Context (Goodwin et al.)

") CHAPTER 18 MARKETS WITH MARKET POWER Principles of Economics in Context (Goodwin et al.) Chapter Summary Now that you understand the model of a perfectly competitive market, this chapter complicates the

CHAPTER 18 MARKETS WITH MARKET POWER Principles of Economics in Context (Goodwin et al.) Chapter Summary Now that you understand the model of a perfectly competitive market, this chapter complicates the

Common in European countries government runs telephone, water, electric companies.

Public ownership Common in European countries government runs telephone, water, electric companies. US: Postal service. Because delivery of mail seems to be natural monopoly. Private ownership incentive

Public ownership Common in European countries government runs telephone, water, electric companies. US: Postal service. Because delivery of mail seems to be natural monopoly. Private ownership incentive

Chapter 7: Market Structures Section 3

Chapter 7: Market Structures Section 3 Objectives 1. Describe characteristics and give examples of monopolistic competition. 2. Explain how firms compete without lowering prices. 3. Understand how firms

Chapter 7: Market Structures Section 3 Objectives 1. Describe characteristics and give examples of monopolistic competition. 2. Explain how firms compete without lowering prices. 3. Understand how firms

Chapter 11: Price-Searcher Markets with High Entry Barriers

Chapter 11: Price-Searcher Markets with High Entry Barriers I. Why are entry barriers sometimes high? A. Economies of Scale in some markets average total costs fall over the full range of output. Therefore

Chapter 11: Price-Searcher Markets with High Entry Barriers I. Why are entry barriers sometimes high? A. Economies of Scale in some markets average total costs fall over the full range of output. Therefore

Revenue Structure, Objectives of a Firm and. Break-Even Analysis.

Revenue :The income receipt by way of sale proceeds is the revenue of the firm. As with costs, we need to study concepts of total, average and marginal revenues. Each unit of output sold in the market

Revenue :The income receipt by way of sale proceeds is the revenue of the firm. As with costs, we need to study concepts of total, average and marginal revenues. Each unit of output sold in the market

Market Structure: Duopoly and Oligopoly

WSG10 7/7/03 4:24 PM Page 145 10 Market Structure: Duopoly and Oligopoly OVERVIEW An oligopoly is an industry comprising a few firms. A duopoly, which is a special case of oligopoly, is an industry consisting

WSG10 7/7/03 4:24 PM Page 145 10 Market Structure: Duopoly and Oligopoly OVERVIEW An oligopoly is an industry comprising a few firms. A duopoly, which is a special case of oligopoly, is an industry consisting

Profit maximization in different market structures

Profit maximization in different market structures In the cappuccino problem as well in your team project, demand is clearly downward sloping if the store wants to sell more drink, it has to lower the

Profit maximization in different market structures In the cappuccino problem as well in your team project, demand is clearly downward sloping if the store wants to sell more drink, it has to lower the

Marginal cost. Average cost. Marginal revenue 10 20 40

Economics 101 Fall 2011 Homework #6 Due: 12/13/2010 in lecture Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on top of the homework

Economics 101 Fall 2011 Homework #6 Due: 12/13/2010 in lecture Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on top of the homework

CHAPTER 10 MARKET POWER: MONOPOLY AND MONOPSONY

CHAPTER 10 MARKET POWER: MONOPOLY AND MONOPSONY EXERCISES 3. A monopolist firm faces a demand with constant elasticity of -.0. It has a constant marginal cost of $0 per unit and sets a price to maximize

CHAPTER 10 MARKET POWER: MONOPOLY AND MONOPSONY EXERCISES 3. A monopolist firm faces a demand with constant elasticity of -.0. It has a constant marginal cost of $0 per unit and sets a price to maximize

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chapter 11 Monopoly practice Davidson spring2007 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly industry is characterized by 1) A)

Chapter 11 Monopoly practice Davidson spring2007 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly industry is characterized by 1) A)

Understanding Economics 2nd edition by Mark Lovewell and Khoa Nguyen

Understanding Economics 2nd edition by Mark Lovewell and Khoa Nguyen Chapter 5 Perfect Competition Chapter Objectives! In this chapter you will: " Consider the four market structures, and the main differences

Understanding Economics 2nd edition by Mark Lovewell and Khoa Nguyen Chapter 5 Perfect Competition Chapter Objectives! In this chapter you will: " Consider the four market structures, and the main differences

Market Structure: Perfect Competition and Monopoly

WSG8 7/7/03 4:34 PM Page 113 8 Market Structure: Perfect Competition and Monopoly OVERVIEW One of the most important decisions made by a manager is how to price the firm s product. If the firm is a profit

WSG8 7/7/03 4:34 PM Page 113 8 Market Structure: Perfect Competition and Monopoly OVERVIEW One of the most important decisions made by a manager is how to price the firm s product. If the firm is a profit

A2 Micro Business Economics Diagrams

A2 Micro Business Economics Diagrams Advice on drawing diagrams in the exam The right size for a diagram is ½ of a side of A4 don t make them too small if needed, move onto a new side of paper rather than

A2 Micro Business Economics Diagrams Advice on drawing diagrams in the exam The right size for a diagram is ½ of a side of A4 don t make them too small if needed, move onto a new side of paper rather than

Market is a network of dealings between buyers and sellers.

Market is a network of dealings between buyers and sellers. Market is the characteristic phenomenon of economic life and the constitution of markets and market prices is the central problem of Economics.

Market is a network of dealings between buyers and sellers. Market is the characteristic phenomenon of economic life and the constitution of markets and market prices is the central problem of Economics.

MODULE 64: INTRODUCTION TO OLIGOPOLY Schmidty School of Economics. Wednesday, December 4, 2013 9:20:15 PM Central Standard Time

MODULE 64: INTRODUCTION TO OLIGOPOLY Schmidty School of Economics Learning Targets I Can Understand why oligopolists have an incentive to act in ways that reduce their combined profit. Explain why oligopolies

MODULE 64: INTRODUCTION TO OLIGOPOLY Schmidty School of Economics Learning Targets I Can Understand why oligopolists have an incentive to act in ways that reduce their combined profit. Explain why oligopolies

CHAPTER 12 MARKETS WITH MARKET POWER Microeconomics in Context (Goodwin, et al.), 2 nd Edition

, 2 nd Edition") CHAPTER 12 MARKETS WITH MARKET POWER Microeconomics in Context (Goodwin, et al.), 2 nd Edition Chapter Summary Now that you understand the model of a perfectly competitive market, this chapter complicates

CHAPTER 12 MARKETS WITH MARKET POWER Microeconomics in Context (Goodwin, et al.), 2 nd Edition Chapter Summary Now that you understand the model of a perfectly competitive market, this chapter complicates

5. Suppose demand is perfectly elastic, and the supply of the good in question

ECON 1620 Basic Economics Principles 2010 2011 2 nd Semester Mid term test (1) : 40 multiple choice questions Time allowed : 60 minutes 1. When demand is inelastic the price elasticity of demand is (A)

ECON 1620 Basic Economics Principles 2010 2011 2 nd Semester Mid term test (1) : 40 multiple choice questions Time allowed : 60 minutes 1. When demand is inelastic the price elasticity of demand is (A)

Chapter. Perfect Competition CHAPTER IN PERSPECTIVE

Perfect Competition Chapter 10 CHAPTER IN PERSPECTIVE In Chapter 10 we study perfect competition, the market that arises when the demand for a product is large relative to the output of a single producer.

Perfect Competition Chapter 10 CHAPTER IN PERSPECTIVE In Chapter 10 we study perfect competition, the market that arises when the demand for a product is large relative to the output of a single producer.

Equilibrium of a firm under perfect competition in the short-run. A firm is under equilibrium at that point where it maximizes its profits.

Equilibrium of a firm under perfect competition in the short-run. A firm is under equilibrium at that point where it maximizes its profits. Profit depends upon two factors Revenue Structure Cost Structure

Equilibrium of a firm under perfect competition in the short-run. A firm is under equilibrium at that point where it maximizes its profits. Profit depends upon two factors Revenue Structure Cost Structure

Chapter 12 Monopolistic Competition and Oligopoly

Chapter Monopolistic Competition and Oligopoly Review Questions. What are the characteristics of a monopolistically competitive market? What happens to the equilibrium price and quantity in such a market

Chapter Monopolistic Competition and Oligopoly Review Questions. What are the characteristics of a monopolistically competitive market? What happens to the equilibrium price and quantity in such a market

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Economics 103 Spring 2012: Multiple choice review questions for final exam. Exam will cover chapters on perfect competition, monopoly, monopolistic competition and oligopoly up to the Nash equilibrium

Economics 103 Spring 2012: Multiple choice review questions for final exam. Exam will cover chapters on perfect competition, monopoly, monopolistic competition and oligopoly up to the Nash equilibrium

Chapter 16 Monopolistic Competition and Oligopoly

Chapter 16 Monopolistic Competition and Oligopoly Market Structure Market structure refers to the physical characteristics of the market within which firms interact It is determined by the number of firms

Chapter 16 Monopolistic Competition and Oligopoly Market Structure Market structure refers to the physical characteristics of the market within which firms interact It is determined by the number of firms

4. Market Structures. Learning Objectives 4-63. Market Structures

1. Supply and Demand: Introduction 3 2. Supply and Demand: Consumer Demand 33 3. Supply and Demand: Company Analysis 43 4. Market Structures 63 5. Key Formulas 81 2014 Allen Resources, Inc. All rights

1. Supply and Demand: Introduction 3 2. Supply and Demand: Consumer Demand 33 3. Supply and Demand: Company Analysis 43 4. Market Structures 63 5. Key Formulas 81 2014 Allen Resources, Inc. All rights

Practice Questions Week 8 Day 1

Practice Questions Week 8 Day 1 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The characteristics of a market that influence the behavior of market participants

Practice Questions Week 8 Day 1 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The characteristics of a market that influence the behavior of market participants

Chapter 13 Oligopoly 1

Chapter 13 Oligopoly 1 4. Oligopoly A market structure with a small number of firms (usually big) Oligopolists know each other: Strategic interaction: actions of one firm will trigger re-actions of others

Chapter 13 Oligopoly 1 4. Oligopoly A market structure with a small number of firms (usually big) Oligopolists know each other: Strategic interaction: actions of one firm will trigger re-actions of others

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chap 13 Monopolistic Competition and Oligopoly These questions may include topics that were not covered in class and may not be on the exam. MULTIPLE CHOICE. Choose the one alternative that best completes

Chap 13 Monopolistic Competition and Oligopoly These questions may include topics that were not covered in class and may not be on the exam. MULTIPLE CHOICE. Choose the one alternative that best completes

Final Exam 15 December 2006

Eco 301 Name Final Exam 15 December 2006 120 points. Please write all answers in ink. You may use pencil and a straight edge to draw graphs. Allocate your time efficiently. Part 1 (10 points each) 1. As

Eco 301 Name Final Exam 15 December 2006 120 points. Please write all answers in ink. You may use pencil and a straight edge to draw graphs. Allocate your time efficiently. Part 1 (10 points each) 1. As

Figure 1, A Monopolistically Competitive Firm

The Digital Economist Lecture 9 Pricing Power and Price Discrimination Many firms have the ability to charge prices for their products consistent with their best interests even thought they may not be

The Digital Economist Lecture 9 Pricing Power and Price Discrimination Many firms have the ability to charge prices for their products consistent with their best interests even thought they may not be

CHAPTER 6 MARKET STRUCTURE

CHAPTER 6 MARKET STRUCTURE CHAPTER SUMMARY This chapter presents an economic analysis of market structure. It starts with perfect competition as a benchmark. Potential barriers to entry, that might limit

CHAPTER 6 MARKET STRUCTURE CHAPTER SUMMARY This chapter presents an economic analysis of market structure. It starts with perfect competition as a benchmark. Potential barriers to entry, that might limit

CHAPTER 8 PROFIT MAXIMIZATION AND COMPETITIVE SUPPLY

CHAPTER 8 PROFIT MAXIMIZATION AND COMPETITIVE SUPPLY TEACHING NOTES This chapter begins by explaining what we mean by a competitive market and why it makes sense to assume that firms try to maximize profit.

CHAPTER 8 PROFIT MAXIMIZATION AND COMPETITIVE SUPPLY TEACHING NOTES This chapter begins by explaining what we mean by a competitive market and why it makes sense to assume that firms try to maximize profit.

Oligopoly. Unit 4: Imperfect Competition. Unit 4: Imperfect Competition 4-4. Oligopolies FOUR MARKET MODELS

1 Unit 4: Imperfect Competition FOUR MARKET MODELS Perfect Competition Monopolistic Competition Pure Characteristics of Oligopolies: A Few Large Producers (Less than 10) Identical or Differentiated Products

1 Unit 4: Imperfect Competition FOUR MARKET MODELS Perfect Competition Monopolistic Competition Pure Characteristics of Oligopolies: A Few Large Producers (Less than 10) Identical or Differentiated Products

Variable Cost. Marginal Cost. Average Variable Cost 0 $50 $50 $0 -- -- -- -- 1 $150 A B C D E F 2 G H I $120 J K L 3 M N O P Q $120 R

Class: Date: ID: A Principles Fall 2013 Midterm 3 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Trevor s Tire Company produced and sold 500 tires. The

Class: Date: ID: A Principles Fall 2013 Midterm 3 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Trevor s Tire Company produced and sold 500 tires. The

Chapter 7: Market Structures Section 1

Chapter 7: Market Structures Section 1 Key Terms perfect competition: a market structure in which a large number of firms all produce the same product and no single seller controls supply or prices commodity:

Chapter 7: Market Structures Section 1 Key Terms perfect competition: a market structure in which a large number of firms all produce the same product and no single seller controls supply or prices commodity:

Business Ethics Concepts & Cases

Business Ethics Concepts & Cases Manuel G. Velasquez Chapter Four Ethics in the Marketplace Definition of Market A forum in which people come together to exchange ownership of goods; a place where goods

Business Ethics Concepts & Cases Manuel G. Velasquez Chapter Four Ethics in the Marketplace Definition of Market A forum in which people come together to exchange ownership of goods; a place where goods

Oligopoly. Models of Oligopoly Behavior No single general model of oligopoly behavior exists. Oligopoly. Interdependence.

Oligopoly Chapter 16-2 Models of Oligopoly Behavior No single general model of oligopoly behavior exists. Oligopoly An oligopoly is a market structure characterized by: Few firms Either standardized or

Oligopoly Chapter 16-2 Models of Oligopoly Behavior No single general model of oligopoly behavior exists. Oligopoly An oligopoly is a market structure characterized by: Few firms Either standardized or

Extreme cases. In between cases

CHAPTER 16 OLIGOPOLY FOUR TYPES OF MARKET STRUCTURE Extreme cases PERFECTLY COMPETITION Many firms No barriers to entry Identical products MONOPOLY One firm Huge barriers to entry Unique product In between

CHAPTER 16 OLIGOPOLY FOUR TYPES OF MARKET STRUCTURE Extreme cases PERFECTLY COMPETITION Many firms No barriers to entry Identical products MONOPOLY One firm Huge barriers to entry Unique product In between

Microeconomics. Lecture Outline. Claudia Vogel. Winter Term 2009/2010. Part III Market Structure and Competitive Strategy

Microeconomics Claudia Vogel EUV Winter Term 2009/2010 Claudia Vogel (EUV) Microeconomics Winter Term 2009/2010 1 / 25 Lecture Outline Part III Market Structure and Competitive Strategy 12 Monopolistic

Microeconomics Claudia Vogel EUV Winter Term 2009/2010 Claudia Vogel (EUV) Microeconomics Winter Term 2009/2010 1 / 25 Lecture Outline Part III Market Structure and Competitive Strategy 12 Monopolistic

ECON101 STUDY GUIDE 7 CHAPTER 14

ECON101 STUDY GUIDE 7 CHAPTER 14 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) An oligopoly firm is similar to a monopolistically competitive

ECON101 STUDY GUIDE 7 CHAPTER 14 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) An oligopoly firm is similar to a monopolistically competitive

Chapter 8 Production Technology and Costs 8.1 Economic Costs and Economic Profit

Chapter 8 Production Technology and Costs 8.1 Economic Costs and Economic Profit 1) Accountants include costs as part of a firm's costs, while economists include costs. A) explicit; no explicit B) implicit;

Chapter 8 Production Technology and Costs 8.1 Economic Costs and Economic Profit 1) Accountants include costs as part of a firm's costs, while economists include costs. A) explicit; no explicit B) implicit;

Econ 201 Lecture 17. The marginal benefit of expanding output by one unit is the market price. Marginal cost of producing corn

Econ 201 Lecture 17 The Perfectly Competitive Firm Is a Taker (Recap) The perfectly competitive firm has no influence over the market price. It can sell as many units as it wishes at that price. Typically,

Econ 201 Lecture 17 The Perfectly Competitive Firm Is a Taker (Recap) The perfectly competitive firm has no influence over the market price. It can sell as many units as it wishes at that price. Typically,

Thus MR(Q) = P (Q) Q P (Q 1) (Q 1) < P (Q) Q P (Q) (Q 1) = P (Q), since P (Q 1) > P (Q).

= P (Q) Q P (Q 1) (Q 1) < P (Q) Q P (Q) (Q 1) = P (Q), since P (Q 1) > P (Q).") A monopolist s marginal revenue is always less than or equal to the price of the good. Marginal revenue is the amount of revenue the firm receives for each additional unit of output. It is the difference

A monopolist s marginal revenue is always less than or equal to the price of the good. Marginal revenue is the amount of revenue the firm receives for each additional unit of output. It is the difference

Chapter 7: Market Structure in Government and Nonprofit Industries. Soft Drinks. What is a Market? Do NFPs Compete? Some NFPs Compete Directly

Chapter 7: Market Structure in Government and Nonprofit Industries Soft Drinks HTTP:/www.economics.emory.edu/Working_Pa pers/wp/2008wp/frisvold_08_08_paper.pdf What is a Market? A market is a process in

Chapter 7: Market Structure in Government and Nonprofit Industries Soft Drinks HTTP:/www.economics.emory.edu/Working_Pa pers/wp/2008wp/frisvold_08_08_paper.pdf What is a Market? A market is a process in

AP Microeconomics Chapter 12 Outline

I. Learning Objectives In this chapter students will learn: A. The significance of resource pricing. B. How the marginal revenue productivity of a resource relates to a firm s demand for that resource.

I. Learning Objectives In this chapter students will learn: A. The significance of resource pricing. B. How the marginal revenue productivity of a resource relates to a firm s demand for that resource.

Mikroekonomia B by Mikolaj Czajkowski. MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Mikroekonomia B by Mikolaj Czajkowski Test 12 - Oligopoly Name Group MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The market structure in which

Mikroekonomia B by Mikolaj Czajkowski Test 12 - Oligopoly Name Group MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The market structure in which

Price competition with homogenous products: The Bertrand duopoly model [Simultaneous move price setting duopoly]

![Price competition with homogenous products: The Bertrand duopoly model [Simultaneous move price setting duopoly]](/thumbs/24/4353364.jpg "Price competition with homogenous products: The Bertrand duopoly model [Simultaneous move price setting duopoly]") ECON9 (Spring 0) & 350 (Tutorial ) Chapter Monopolistic Competition and Oligopoly (Part ) Price competition with homogenous products: The Bertrand duopoly model [Simultaneous move price setting duopoly]

ECON9 (Spring 0) & 350 (Tutorial ) Chapter Monopolistic Competition and Oligopoly (Part ) Price competition with homogenous products: The Bertrand duopoly model [Simultaneous move price setting duopoly]

ECON 103, 2008-2 ANSWERS TO HOME WORK ASSIGNMENTS

ECON 103, 2008-2 ANSWERS TO HOME WORK ASSIGNMENTS Due the Week of June 23 Chapter 8 WRITE [4] Use the demand schedule that follows to calculate total revenue and marginal revenue at each quantity. Plot

ECON 103, 2008-2 ANSWERS TO HOME WORK ASSIGNMENTS Due the Week of June 23 Chapter 8 WRITE [4] Use the demand schedule that follows to calculate total revenue and marginal revenue at each quantity. Plot

11 PERFECT COMPETITION. Chapter. Competition

Chapter 11 PERFECT COMPETITION Competition Topic: Perfect Competition 1) Perfect competition is an industry with A) a few firms producing identical goods B) a few firms producing goods that differ somewhat

Chapter 11 PERFECT COMPETITION Competition Topic: Perfect Competition 1) Perfect competition is an industry with A) a few firms producing identical goods B) a few firms producing goods that differ somewhat

Oligopoly and Strategic Pricing

R.E.Marks 1998 Oligopoly 1 R.E.Marks 1998 Oligopoly Oligopoly and Strategic Pricing In this section we consider how firms compete when there are few sellers an oligopolistic market (from the Greek). Small

R.E.Marks 1998 Oligopoly 1 R.E.Marks 1998 Oligopoly Oligopoly and Strategic Pricing In this section we consider how firms compete when there are few sellers an oligopolistic market (from the Greek). Small

Chapter 7 Monopoly, Oligopoly and Strategy

Chapter 7 Monopoly, Oligopoly and Strategy After reading Chapter 7, MONOPOLY, OLIGOPOLY AND STRATEGY, you should be able to: Define the characteristics of Monopoly and Oligopoly, and explain why the are

Chapter 7 Monopoly, Oligopoly and Strategy After reading Chapter 7, MONOPOLY, OLIGOPOLY AND STRATEGY, you should be able to: Define the characteristics of Monopoly and Oligopoly, and explain why the are

Economics 431 Fall 2003 1st midterm Answer Key

Economics 431 Fall 003 1st midterm Answer Key 1) (7 points) Consider an industry that consists of a large number of identical firms. In the long run competitive equilibrium, a firm s marginal cost must

Economics 431 Fall 003 1st midterm Answer Key 1) (7 points) Consider an industry that consists of a large number of identical firms. In the long run competitive equilibrium, a firm s marginal cost must

OLIGOPOLY. Nature of Oligopoly. What Causes Oligopoly?

CH 11: OLIGOPOLY 1 OLIGOPOLY When a few big firms dominate the market, the situation is called oligopoly. Any action of one firm will affect the performance of other firms. If one of the firms reduces

CH 11: OLIGOPOLY 1 OLIGOPOLY When a few big firms dominate the market, the situation is called oligopoly. Any action of one firm will affect the performance of other firms. If one of the firms reduces

chapter: Oligopoly Krugman/Wells Economics 2009 Worth Publishers 1 of 35

chapter: 15 >> Oligopoly Krugman/Wells Economics 2009 Worth Publishers 1 of 35 WHAT YOU WILL LEARN IN THIS CHAPTER The meaning of oligopoly, and why it occurs Why oligopolists have an incentive to act

chapter: 15 >> Oligopoly Krugman/Wells Economics 2009 Worth Publishers 1 of 35 WHAT YOU WILL LEARN IN THIS CHAPTER The meaning of oligopoly, and why it occurs Why oligopolists have an incentive to act

CHAPTER 13 MARKETS FOR LABOR Microeconomics in Context (Goodwin, et al.), 2 nd Edition

, 2 nd Edition") CHAPTER 13 MARKETS FOR LABOR Microeconomics in Context (Goodwin, et al.), 2 nd Edition Chapter Summary This chapter deals with supply and demand for labor. You will learn about why the supply curve for

CHAPTER 13 MARKETS FOR LABOR Microeconomics in Context (Goodwin, et al.), 2 nd Edition Chapter Summary This chapter deals with supply and demand for labor. You will learn about why the supply curve for

Oligopoly Mr Traynor. Economics Note 11 Leaving Cert 5 th Year. St. Michaels College, Ailesbury Rd

Oligopoly Mr Traynor Economics Note 11 Leaving Cert 5 th Year, Ailesbury Rd Oligopoly Before, when we looked at Perfect and Imperfect CompeLLon, we nolced that firms in these markets acted independently

Oligopoly Mr Traynor Economics Note 11 Leaving Cert 5 th Year, Ailesbury Rd Oligopoly Before, when we looked at Perfect and Imperfect CompeLLon, we nolced that firms in these markets acted independently

BEE2017 Intermediate Microeconomics 2

BEE2017 Intermediate Microeconomics 2 Dieter Balkenborg Sotiris Karkalakos Yiannis Vailakis Organisation Lectures Mon 14:00-15:00, STC/C Wed 12:00-13:00, STC/D Tutorials Mon 15:00-16:00, STC/106 (will

BEE2017 Intermediate Microeconomics 2 Dieter Balkenborg Sotiris Karkalakos Yiannis Vailakis Organisation Lectures Mon 14:00-15:00, STC/C Wed 12:00-13:00, STC/D Tutorials Mon 15:00-16:00, STC/106 (will

AP Microeconomics Review

AP Microeconomics Review 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry 3. Natural Monopoly with Fair-Return

AP Microeconomics Review 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry 3. Natural Monopoly with Fair-Return

EXAM TWO REVIEW: A. Explicit Cost vs. Implicit Cost and Accounting Costs vs. Economic Costs:

EXAM TWO REVIEW: A. Explicit Cost vs. Implicit Cost and Accounting Costs vs. Economic Costs: Economic Cost: the monetary value of all inputs used in a particular activity or enterprise over a given period.

EXAM TWO REVIEW: A. Explicit Cost vs. Implicit Cost and Accounting Costs vs. Economic Costs: Economic Cost: the monetary value of all inputs used in a particular activity or enterprise over a given period.

Chapter 9: Perfect Competition

Chapter 9: Perfect Competition Perfect Competition Law of One Price Short-Run Equilibrium Long-Run Equilibrium Maximize Profit Market Equilibrium Constant- Cost Industry Increasing- Cost Industry Decreasing-

Chapter 9: Perfect Competition Perfect Competition Law of One Price Short-Run Equilibrium Long-Run Equilibrium Maximize Profit Market Equilibrium Constant- Cost Industry Increasing- Cost Industry Decreasing-

12 Monopolistic Competition and Oligopoly

12 Monopolistic Competition and Oligopoly Read Pindyck and Rubinfeld (2012), Chapter 12 09/04/2015 CHAPTER 12 OUTLINE 12.1 Monopolistic Competition 12.2 Oligopoly 12.3 Price Competition 12.4 Competition

12 Monopolistic Competition and Oligopoly Read Pindyck and Rubinfeld (2012), Chapter 12 09/04/2015 CHAPTER 12 OUTLINE 12.1 Monopolistic Competition 12.2 Oligopoly 12.3 Price Competition 12.4 Competition

Monopolistic Competition

Monopolistic Chapter 17 Copyright 2001 by Harcourt, Inc. All rights reserved. Requests for permission to make copies of any part of the work should be mailed to: Permissions Department, Harcourt College

Monopolistic Chapter 17 Copyright 2001 by Harcourt, Inc. All rights reserved. Requests for permission to make copies of any part of the work should be mailed to: Permissions Department, Harcourt College

A Detailed Price Discrimination Example

A Detailed Price Discrimination Example Suppose that there are two different types of customers for a monopolist s product. Customers of type 1 have demand curves as follows. These demand curves include

A Detailed Price Discrimination Example Suppose that there are two different types of customers for a monopolist s product. Customers of type 1 have demand curves as follows. These demand curves include

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Practice for Perfect Competition Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Which of the following is a defining characteristic of a

Practice for Perfect Competition Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Which of the following is a defining characteristic of a

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chapter 11 Perfect Competition - Sample Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Perfect competition is an industry with A) a

Chapter 11 Perfect Competition - Sample Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Perfect competition is an industry with A) a

Economics 100 Exam 2

Name: 1. During the long run: Economics 100 Exam 2 A. Output is limited because of the law of diminishing returns B. The scale of operations cannot be changed C. The firm must decide how to use the current

Name: 1. During the long run: Economics 100 Exam 2 A. Output is limited because of the law of diminishing returns B. The scale of operations cannot be changed C. The firm must decide how to use the current

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron.

Principles of Microeconomics Fall 2007, Quiz #6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron. 1) A monopoly is

Principles of Microeconomics Fall 2007, Quiz #6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron. 1) A monopoly is

Final Exam (Version 1) Answers

Answers") Final Exam Economics 101 Fall 2003 Wallace Final Exam (Version 1) Answers 1. The marginal revenue product equals A) total revenue divided by total product (output). B) marginal revenue divided by marginal

Final Exam Economics 101 Fall 2003 Wallace Final Exam (Version 1) Answers 1. The marginal revenue product equals A) total revenue divided by total product (output). B) marginal revenue divided by marginal

Chapter 05 Perfect Competition, Monopoly, and Economic

Chapter 05 Perfect Competition, Monopoly, and Economic Multiple Choice Questions Use Figure 5.1 to answer questions 1-2: Figure 5.1 1. In Figure 5.1 above, what output would a perfect competitor produce?

Chapter 05 Perfect Competition, Monopoly, and Economic Multiple Choice Questions Use Figure 5.1 to answer questions 1-2: Figure 5.1 1. In Figure 5.1 above, what output would a perfect competitor produce?

Economics Chapter 7 Review

Name: Class: Date: ID: A Economics Chapter 7 Review Matching a. perfect competition e. imperfect competition b. efficiency f. price and output c. start-up costs g. technological barrier d. commodity h.

Name: Class: Date: ID: A Economics Chapter 7 Review Matching a. perfect competition e. imperfect competition b. efficiency f. price and output c. start-up costs g. technological barrier d. commodity h.

The Analysis of the Article Microsoft's Aggressive New Pricing Strategy Using. Microeconomic Theory

2 The Analysis of the Article Microsoft's Aggressive New Pricing Strategy Using Microeconomic Theory I. Introduction: monopolistic power as a means of getting high profits II. The review of the article

2 The Analysis of the Article Microsoft's Aggressive New Pricing Strategy Using Microeconomic Theory I. Introduction: monopolistic power as a means of getting high profits II. The review of the article

Comparisons of Industry Market Structures. Imperfect Competition Market Structure Models (11/10/09)

") Imperfect Market Structure Models (11/10/09) Today: and Monopsony/Oligopsony Thursday: Market Structure, Conduct and erformance Model Exam III 24 th Characteristics Comparisons of Industry Market Structures

Imperfect Market Structure Models (11/10/09) Today: and Monopsony/Oligopsony Thursday: Market Structure, Conduct and erformance Model Exam III 24 th Characteristics Comparisons of Industry Market Structures

Northern University Bangladesh

Northern University Bangladesh Managerial Economics ( MBA 5208) Session # 09 Oligopoly & Monopolistic Competition Prof. Mahmudul Alam (PMA) 23 September, 2011 (Friday) 1 1. Monopolistic Competition & Oligopoly

Northern University Bangladesh Managerial Economics ( MBA 5208) Session # 09 Oligopoly & Monopolistic Competition Prof. Mahmudul Alam (PMA) 23 September, 2011 (Friday) 1 1. Monopolistic Competition & Oligopoly

QE1: Economics Notes 1

QE1: Economics Notes 1 Box 1: The Household and Consumer Welfare The final basket of goods that is chosen are determined by three factors: a. Income b. Price c. Preferences Substitution Effect: change

QE1: Economics Notes 1 Box 1: The Household and Consumer Welfare The final basket of goods that is chosen are determined by three factors: a. Income b. Price c. Preferences Substitution Effect: change

Pure Competition urely competitive markets are used as the benchmark to evaluate market

R. Larry Reynolds Pure Competition urely competitive markets are used as the benchmark to evaluate market P performance. It is generally believed that market structure influences the behavior and performance

R. Larry Reynolds Pure Competition urely competitive markets are used as the benchmark to evaluate market P performance. It is generally believed that market structure influences the behavior and performance

Economics II: Micro Fall 2009 Exercise session 5. Market with a sole supplier is Monopolistic.

Economics II: Micro Fall 009 Exercise session 5 VŠE 1 Review Optimal production: Independent of the level of market concentration, optimal level of production is where MR = MC. Monopoly: Market with a

Economics II: Micro Fall 009 Exercise session 5 VŠE 1 Review Optimal production: Independent of the level of market concentration, optimal level of production is where MR = MC. Monopoly: Market with a

Chapter 14 Monopoly. 14.1 Monopoly and How It Arises

Chapter 14 Monopoly 14.1 Monopoly and How It Arises 1) One of the requirements for a monopoly is that A) products are high priced. B) there are several close substitutes for the product. C) there is a

Chapter 14 Monopoly 14.1 Monopoly and How It Arises 1) One of the requirements for a monopoly is that A) products are high priced. B) there are several close substitutes for the product. C) there is a

Principle of Microeconomics Econ 202-506 chapter 13

Principle of Microeconomics Econ 202-506 chapter 13 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The WaveHouse on Mission Beach in San Diego

Principle of Microeconomics Econ 202-506 chapter 13 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The WaveHouse on Mission Beach in San Diego

Principles of Economics: Micro: Exam #2: Chapters 1-10 Page 1 of 9

Principles of Economics: Micro: Exam #2: Chapters 1-10 Page 1 of 9 print name on the line above as your signature INSTRUCTIONS: 1. This Exam #2 must be completed within the allocated time (i.e., between

Principles of Economics: Micro: Exam #2: Chapters 1-10 Page 1 of 9 print name on the line above as your signature INSTRUCTIONS: 1. This Exam #2 must be completed within the allocated time (i.e., between

Chapter 6 Competitive Markets

Chapter 6 Competitive Markets After reading Chapter 6, COMPETITIVE MARKETS, you should be able to: List and explain the characteristics of Perfect Competition and Monopolistic Competition Explain why a

Chapter 6 Competitive Markets After reading Chapter 6, COMPETITIVE MARKETS, you should be able to: List and explain the characteristics of Perfect Competition and Monopolistic Competition Explain why a

Cooleconomics.com Monopolistic Competition and Oligopoly. Contents:

Cooleconomics.com Monopolistic Competition and Oligopoly Contents: Monopolistic Competition Attributes Short Run performance Long run performance Excess capacity Importance of Advertising Socialist Critique

Cooleconomics.com Monopolistic Competition and Oligopoly Contents: Monopolistic Competition Attributes Short Run performance Long run performance Excess capacity Importance of Advertising Socialist Critique

Managerial Economics. 1 is the application of Economic theory to managerial practice.

Managerial Economics 1 is the application of Economic theory to managerial practice. 1. Economic Management 2. Managerial Economics 3. Economic Practice 4. Managerial Theory 2 Managerial Economics relates

Managerial Economics 1 is the application of Economic theory to managerial practice. 1. Economic Management 2. Managerial Economics 3. Economic Practice 4. Managerial Theory 2 Managerial Economics relates