FIN Chapter 9. Debt Valuation and Interest Rates. Liuren Wu

|

|

|

- Laura Leonard

- 7 years ago

- Views:

Transcription

1 FIN 3000 Chapter 9 Debt Valuation and Interest Rates Liuren Wu

2 Overview 1. Overview of Corporate Debt Identify the key features of bonds and describe the difference between private and public debt markets. 2. Valuing Corporate Debt Calculate the value of a bond and relate it to the yield to maturity on the bond. 3. Bond Valuation: Four Key Relationships Describe the four key bond valuation relationships. 4. Types of Bonds: Identify the major types of corporate bonds. 5. Determinants of Interest Rates Explain the effects of inflation on interest rates. 2

3 9.1 Corporate Debt There are two main sources of borrowing for a corporation: 1. Loan from a financial institution (known as private debt) 2. Bonds (known as public debt since they can be traded in public financial markets) Smaller firms choose to raise money from banks in the form of loans because of the high costs associated with issuing bonds. Larger firms generally raise money from banks for shortterm needs and depend on the bond market for long-term financing needs. 3

4 Borrowing Money in the Private Financial Market In the private financial market, loans are typically floating rate loans i.e. the interest rate is periodically adjusted based on a specific benchmark rate. The most popular benchmark rate is the London Interbank Offered Rate (LIBOR), which is the daily interest rate that is based on the interest rates at which banks offer to lend in the London wholesale or interbank market. Interbank market is the market where banks loan each other money. 4

5 Borrowing Money in the Private Financial Market A typical floating rate loan will specify the following: The spread or margin between the loan rate and the benchmark rate expressed as basis points. A maximum and a minimum annual rate, to which the rate can adjust, called the ceiling and floor. A maturity date Collateral For example, a corporation may get a 1-year loan with a rate of 300 basis points (or 3%) over LIBOR with a ceiling of 11% and a floor of 4%. 5

6 6

7 Borrowing Money in the Public Financial Market Firms also raise money by selling debt securities to individual investors and financial institutions such as mutual funds. In order to sell debt securities to the public, the issuing firm must meet the legal requirements as specified by the securities laws. Corporate bond is a debt security issued by corporation that has promised future payments and a maturity date. If the firm fails to pay the promised future payments of interest and principal, the bond trustee can classify the firm as insolvent and force the firm into bankruptcy. 7

8 Basic Bond Features The basic features of a bond include the following: Bond Indenture Claims on Assets and Income Par or Face Value Coupon Interest Rate Maturity and Repayment of Principal Call Provision and Conversion Features 8

9 9

10 Bond Ratings and Default Risk Bond ratings indicate the default risk, i.e., the probability that the firm will fail to make the promised payments. Bond ratings affect the rate of return that lenders require of the firm and the firm s cost of borrowing. The lower the bond rating, the higher the risk of default and higher the rate of return demanded in the capital market. Bond ratings are provided by three rating agencies Moody s, Standard & Poor s, and Fitch Investor Services 10

11 11

12 9.2 Valuing Corporate Debt The value of corporate debt is equal to the present value of the contractually promised principal and interest payments (the cash flows) discounted back to the present using the market s required yield. 12

13 Step-by-Step: Valuing Bonds by Discounting Future Cash Flows Step 1: Determine the amount and timing of bondholder cash flows. The total cash flows equal the promised interest payments and principal payment. Annual Interest = Par value coupon rate Example 9.1: The annual interest for a bond with coupon interest rate of 7% and a par value of $1,000 is equal to $70, (.07 $1,000 = $70). Some bonds have semi-annual payments. 13

14 Step-by-Step: Valuing Bonds by Discounting Future Cash Flows Step 2: Estimate the appropriate discount rate on a similar risk bond. Discount rate is the return the bond will yield if it is held to maturity and all bond payments are made. Discount rate can be either calculated or obtained from various sources (such as Yahoo! Finance). Step 3: Calculate the present value of the bond s interest and principal payments from Step 1 using the discount rate estimated in step 2. 14

15 Yield to Maturity (YTM) We can think of YTM as the discount rate that makes the present value of the bond s promised interest and principal equal to the bond s observed market price. You can compute YTM using excel or a financial calculator. 15

16 Using Market Yield to Maturity Data Market yield to maturity is regularly reported by a number of investor services and is quoted in terms of credit spreads or spreads to Treasury bonds. Table 9-4 contains some examples of yield spreads. The spread values in table 9-4 represent basis points over a US Treasury security of the same maturity as the corporate bond. For example, a 30-year Ba1/BB+ corporate bond has a spread of 275 basis points over a similar 30-year US Treasury bond. Thus, this corporate bond should earn 2.75% over the 4.56% earned on treasury yield or 7.31%. 16

17 17

18 Checkpoint 9.3 Valuing a Bond Issue Consider a $1,000 par value bond issued by AT&T (T) with a maturity date of 2026 and a stated coupon rate of 8.5%. On January 1, 2007, the bond had 20 years left to maturity, and the market s required yield to maturity for similar rated debt was 7.5%. If the market s required yield to maturity on a comparable risk bond is 7.5%, what is the value of the bond? 18

19 Checkpoint 9.3 A $1000 par bond with 8.5% coupon rate pays 1000x8.5%=$85 each year as a coupon payment. If the coupon is paid annually, this payment will last for 20 years as an annuity. At the end of the 20 year, we also get the $1,000 principal payment. The bond value is the present value of the 20 coupon payments and the principal. PV = 85*(( )/0.075) / = =

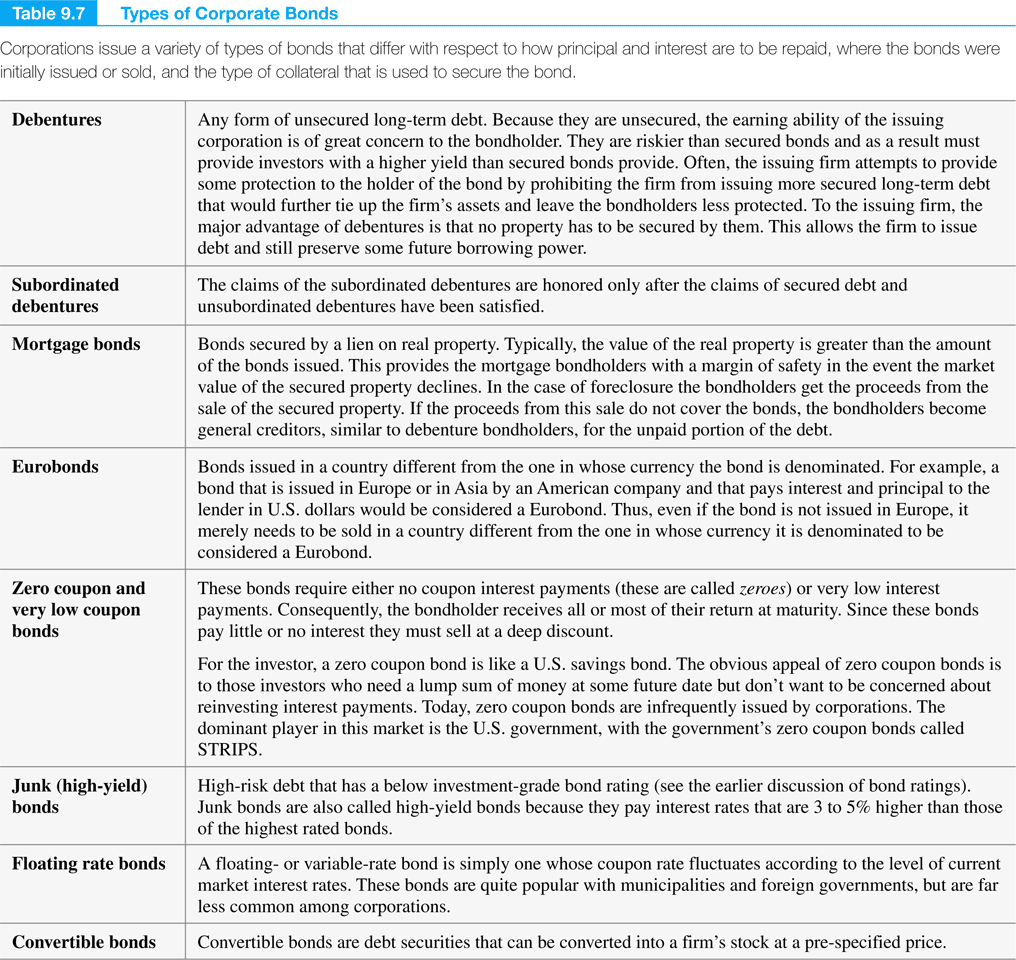

20 Checkpoint 9.3: Check Yourself Calculate the present value of the AT&T bond should the yield to maturity for comparable risk bonds rise to 9% (holding all other things equal). PV = 85*(( )/0.09) / = = The value of AT&T bond falls to $ when the yield to maturity for comparable risk bond rises to 9%. The bonds are now trading at a discount as the coupon rate on AT&T bonds is lower than the market yield. 20

21 Semiannual Interest Payments Corporate bonds typically pay interest to bondholders semiannually. We can adapt Equation (9-2a) from annual to semiannual payments as follows: If the AT&T bond has semi-annual coupon payment, each payment would be 85/2=$42.5 for 40 payments. PV= 42.5*(( )/0.0375) / = PV=42.5*(( )/0.045) / = The values are very close to the annual compounding case. 21

22 9.3 Bond Valuation: Four Key Relationships First Relationship The value of bond is inversely related to changes in the yield to maturity. YTM = 12% YTM rises to 15% Par value $1,000 $1,000 Coupon rate 12% 12% Maturity date 5 years 5 years Bond Value $1,000 $ Bond Value Drops 22

23 The value of bond is inversely related to the yield to maturity. 23

24 Bond Valuation: Four Key Relationships Second Relationship: The market value of a bond will be less than its par value if the yield to maturity is above the coupon interest rate and will be valued above par value if the yield to maturity is below the coupon interest rate. When a bond can be bought for less than its par value, it is called discount bond. For example, buying a $1,000 par value bond for $950. When a bond can be bought for more than its par value, it is called premium bond. For example, buying a $1,000 par value bond for $1,

25 Bond Valuation: Four Key Relationships Third Relationship As the maturity date approaches, the market value of a bond approaches its par value. Regardless of whether the bond was trading at a discount or at a premium, the price of bond will converge towards par value as the maturity date approaches. Fourth Relationship Long term bonds have greater interest rate risk than short-term bonds. While all bonds are affected by a change in interest rates, longterm bonds are exposed to greater volatility as interest rates change. 25

26 26

27 9.4 Types of Bonds Table 9-7 contains a listing of major types of long-term debt securities that are sold in the public financial market. The differences among the various types of bond are based on the following bond attributes: 1. Secured versus Unsecured, 2. Priority of claim, 3. Initial offering market, 4. Abnormal risk, 5. Coupon level, 6. Amortizing or non-amortizing, and 7. Convertibility. 27

28 Types of Bonds 1 2 Secured versus Unsecured Secured bonds have specific assets pledged to support repayment of the bond. Unsecured bond are referred to as debentures. Bonds secured by lien on real property is called a mortgage bond. Priority of Claim The priority of claim refers to the order of repayment when the firm s assets are distributed, as in the case of liquidation. Secured bonds are paid first followed by debentures; Among debentures, subordinated debentures have lower priority than secured debt and unsubordinated debentures. 28

29 Types of Bonds 3 4 Initial Offering Market Bonds are classified by where they were originally issued (in the domestic bond market or not). For example, Eurobonds are issued in a foreign country but are denominated in domestic currency. For example, a US corporation issuing bonds in Germany in US dollars. Abnormal Risk Junk, or high-yield, bonds have a below-investment grade bond rating. These bonds have a high risk of default as the firms that issued these bonds are facing severe financial problems. 29

30 Types of Bonds Coupon Level Bonds with a zero or very low coupon are called zero coupon bonds. Par bond: coupon level is close to ytm so that the bond can be sold at par. Amortizing or Non-Amortizing The payments from amortizing bonds, like a home mortgage, include both the interest and principal. The payments from a non-amortizing bonds include only interest. At maturity, the bonds repay the par value of bond. Convertibility Convertible bonds are debt securities that can be converted into a firm s stock at a pre-specified price. 30

31 31

32 9.5 Determinants of Interest Rates Bond prices vary inversely with interest rates. To understand bond pricing we need to know the determinants of interest rates. Quotes of interest rates in the financial press are commonly referred to as the nominal (or quoted) interest rates. Real rate of interest adjusts the nominal rate for the expected effects of inflation. 32

33 Fisher Effect The relationship between the nominal rate of interest, r nominal, the anticipated rate of inflation, r inflation, and the real rate of interest is known as the Fisher effect. 1+ r nominal = (1+ r real )(1+ r inflation ) We can approximate the relation as r nominal» r real + r inflation 33

34 Fisher Effect: Example Example 9.3 What will be the real rate of interest if the nominal rate of interest is 10% and the anticipated rate of inflation is 3%? (1+nominal)=(1+real)(1+inflation) Hence, 1+real Real = =0.068=6.8% = (1+nominal)/(1+inflation) = (1+.1)/(1+.03)=1.1/1.03= Or approximately, real=nominal-inflation= 10%-3% =7%. 34

35 Checkpoint 9.5 Solving for the Real Rate of Interest You have managed to build up your savings over the three years following your graduation from college to a respectable $10,000 and are wondering how to invest it. Your banker says they could pay you 5% on your account for the next year. However, you recently saw on the news that the expected rate of inflation for next year is 3.5%. If you are earning a 5% annual rate of return but the prices of goods and services are rising at a rate of 3.5%, just how much additional buying power would you gain each year? Stated somewhat differently, what real rate of interest would you earn if you made the investment? 35

36 Checkpoint 9.5: Check Yourself Answer: Real =(1+nominal)/(1+infation)-1= 1.05/ =1.45% Assume now that you expect that inflation will be 5% over the coming year and want to analyze how much better off you will be if you place your savings in an account that also earns just 5%. What is the real rate of return in this circumstance? 36

37 Checkpoint 9.6 Solving for the Nominal Rate of Interest After considering a number of investment opportunities, you have decided that you should be able to earn a real return of 2% on your $10,000 in savings over the coming year. If the expected rate of inflation is expected to be 3.5% over the coming year, what nominal rate of return must you anticipate in order to earn the 2% real rate of return? 37

38 Checkpoint 9.6: Check Yourself Answer: Nominal = (1+real)(1+inflation)-1 = 1.02* =0.0557=5.57% If you anticipate that the rate of inflation will now be 4% next year, holding all else the same, what rate of return will you need to earn on your savings in order to achieve a 2% increase in purchasing power? Nominal=6.08% 38

39 Determinants of corporate interest rates We can decompose a nominal interest rate into four components: Real rate, in terms of actual purchasing power you can call this the time value of real money (real purchasing power). Inflation premium: Higher anticipated inflation leads to higher nominal rate, holding purchasing power constant. Default premium: If a bond has default risk, the interest rate will increase to compensate for this risk. The higher the default risk, the higher the default premium. Maturity premium: Long-term rates on average are higher than short-term rates. 39

Chapter 9 Bonds and Their Valuation ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS

Chapter 9 Bonds and Their Valuation ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 9-1 a. A bond is a promissory note issued by a business or a governmental unit. Treasury bonds, sometimes referred to as

Chapter 9 Bonds and Their Valuation ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 9-1 a. A bond is a promissory note issued by a business or a governmental unit. Treasury bonds, sometimes referred to as

How To Value Bonds

Chapter 6 Interest Rates And Bond Valuation Learning Goals 1. Describe interest rate fundamentals, the term structure of interest rates, and risk premiums. 2. Review the legal aspects of bond financing

Chapter 6 Interest Rates And Bond Valuation Learning Goals 1. Describe interest rate fundamentals, the term structure of interest rates, and risk premiums. 2. Review the legal aspects of bond financing

Chapter 6 Interest rates and Bond Valuation. 2012 Pearson Prentice Hall. All rights reserved. 4-1

Chapter 6 Interest rates and Bond Valuation 2012 Pearson Prentice Hall. All rights reserved. 4-1 Interest Rates and Required Returns: Interest Rate Fundamentals The interest rate is usually applied to

Chapter 6 Interest rates and Bond Valuation 2012 Pearson Prentice Hall. All rights reserved. 4-1 Interest Rates and Required Returns: Interest Rate Fundamentals The interest rate is usually applied to

Click Here to Buy the Tutorial

FIN 534 Week 4 Quiz 3 (Str) Click Here to Buy the Tutorial http://www.tutorialoutlet.com/fin-534/fin-534-week-4-quiz-3- str/ For more course tutorials visit www.tutorialoutlet.com Which of the following

FIN 534 Week 4 Quiz 3 (Str) Click Here to Buy the Tutorial http://www.tutorialoutlet.com/fin-534/fin-534-week-4-quiz-3- str/ For more course tutorials visit www.tutorialoutlet.com Which of the following

ANALYSIS OF FIXED INCOME SECURITIES

ANALYSIS OF FIXED INCOME SECURITIES Valuation of Fixed Income Securities Page 1 VALUATION Valuation is the process of determining the fair value of a financial asset. The fair value of an asset is its

ANALYSIS OF FIXED INCOME SECURITIES Valuation of Fixed Income Securities Page 1 VALUATION Valuation is the process of determining the fair value of a financial asset. The fair value of an asset is its

Chapter 5: Valuing Bonds

FIN 302 Class Notes Chapter 5: Valuing Bonds What is a bond? A long-term debt instrument A contract where a borrower agrees to make interest and principal payments on specific dates Corporate Bond Quotations

FIN 302 Class Notes Chapter 5: Valuing Bonds What is a bond? A long-term debt instrument A contract where a borrower agrees to make interest and principal payments on specific dates Corporate Bond Quotations

Interest Rates and Bond Valuation

Interest Rates and Bond Valuation Chapter 6 Key Concepts and Skills Know the important bond features and bond types Understand bond values and why they fluctuate Understand bond ratings and what they mean

Interest Rates and Bond Valuation Chapter 6 Key Concepts and Skills Know the important bond features and bond types Understand bond values and why they fluctuate Understand bond ratings and what they mean

Bonds and Yield to Maturity

Bonds and Yield to Maturity Bonds A bond is a debt instrument requiring the issuer to repay to the lender/investor the amount borrowed (par or face value) plus interest over a specified period of time.

Bonds and Yield to Maturity Bonds A bond is a debt instrument requiring the issuer to repay to the lender/investor the amount borrowed (par or face value) plus interest over a specified period of time.

Chapter 4 Bonds and Their Valuation ANSWERS TO END-OF-CHAPTER QUESTIONS

Chapter 4 Bonds and Their Valuation ANSWERS TO END-OF-CHAPTER QUESTIONS 4-1 a. A bond is a promissory note issued by a business or a governmental unit. Treasury bonds, sometimes referred to as government

Chapter 4 Bonds and Their Valuation ANSWERS TO END-OF-CHAPTER QUESTIONS 4-1 a. A bond is a promissory note issued by a business or a governmental unit. Treasury bonds, sometimes referred to as government

Money Market and Debt Instruments

Prof. Alex Shapiro Lecture Notes 3 Money Market and Debt Instruments I. Readings and Suggested Practice Problems II. Bid and Ask III. Money Market IV. Long Term Credit Markets V. Additional Readings Buzz

Prof. Alex Shapiro Lecture Notes 3 Money Market and Debt Instruments I. Readings and Suggested Practice Problems II. Bid and Ask III. Money Market IV. Long Term Credit Markets V. Additional Readings Buzz

Fin 3312 Sample Exam 1 Questions

Fin 3312 Sample Exam 1 Questions Here are some representative type questions. This review is intended to give you an idea of the types of questions that may appear on the exam, and how the questions might

Fin 3312 Sample Exam 1 Questions Here are some representative type questions. This review is intended to give you an idea of the types of questions that may appear on the exam, and how the questions might

Topics in Chapter. Key features of bonds Bond valuation Measuring yield Assessing risk

Bond Valuation 1 Topics in Chapter Key features of bonds Bond valuation Measuring yield Assessing risk 2 Determinants of Intrinsic Value: The Cost of Debt Net operating profit after taxes Free cash flow

Bond Valuation 1 Topics in Chapter Key features of bonds Bond valuation Measuring yield Assessing risk 2 Determinants of Intrinsic Value: The Cost of Debt Net operating profit after taxes Free cash flow

FNCE 301, Financial Management H Guy Williams, 2006

REVIEW We ve used the DCF method to find present value. We also know shortcut methods to solve these problems such as perpetuity present value = C/r. These tools allow us to value any cash flow including

REVIEW We ve used the DCF method to find present value. We also know shortcut methods to solve these problems such as perpetuity present value = C/r. These tools allow us to value any cash flow including

Module 1: Corporate Finance and the Role of Venture Capital Financing TABLE OF CONTENTS

1.0 ALTERNATIVE SOURCES OF FINANCE Module 1: Corporate Finance and the Role of Venture Capital Financing Alternative Sources of Finance TABLE OF CONTENTS 1.1 Short-Term Debt (Short-Term Loans, Line of

1.0 ALTERNATIVE SOURCES OF FINANCE Module 1: Corporate Finance and the Role of Venture Capital Financing Alternative Sources of Finance TABLE OF CONTENTS 1.1 Short-Term Debt (Short-Term Loans, Line of

Interest Rates and Bond Valuation

and Bond Valuation 1 Bonds Debt Instrument Bondholders are lending the corporation money for some stated period of time. Liquid Asset Corporate Bonds can be traded in the secondary market. Price at which

and Bond Valuation 1 Bonds Debt Instrument Bondholders are lending the corporation money for some stated period of time. Liquid Asset Corporate Bonds can be traded in the secondary market. Price at which

CHAPTER 9 DEBT SECURITIES. by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA

CHAPTER 9 DEBT SECURITIES by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA LEARNING OUTCOMES After completing this chapter, you should be able to do the following: a Identify issuers of debt securities;

CHAPTER 9 DEBT SECURITIES by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA LEARNING OUTCOMES After completing this chapter, you should be able to do the following: a Identify issuers of debt securities;

Answers to Review Questions

Answers to Review Questions 1. The real rate of interest is the rate that creates an equilibrium between the supply of savings and demand for investment funds. The nominal rate of interest is the actual

Answers to Review Questions 1. The real rate of interest is the rate that creates an equilibrium between the supply of savings and demand for investment funds. The nominal rate of interest is the actual

Chapter 8. Step 2: Find prices of the bonds today: n i PV FV PMT Result Coupon = 4% 29.5 5? 100 4 84.74 Zero coupon 29.5 5? 100 0 23.

Chapter 8 Bond Valuation with a Flat Term Structure 1. Suppose you want to know the price of a 10-year 7% coupon Treasury bond that pays interest annually. a. You have been told that the yield to maturity

Chapter 8 Bond Valuation with a Flat Term Structure 1. Suppose you want to know the price of a 10-year 7% coupon Treasury bond that pays interest annually. a. You have been told that the yield to maturity

Chapter 10. Fixed Income Markets. Fixed-Income Securities

Chapter 10 Fixed-Income Securities Bond: Tradable security that promises to make a pre-specified series of payments over time. Straight bond makes fixed coupon and principal payment. Bonds are traded mainly

Chapter 10 Fixed-Income Securities Bond: Tradable security that promises to make a pre-specified series of payments over time. Straight bond makes fixed coupon and principal payment. Bonds are traded mainly

CHAPTER 14: BOND PRICES AND YIELDS

CHAPTER 14: BOND PRICES AND YIELDS PROBLEM SETS 1. The bond callable at 105 should sell at a lower price because the call provision is more valuable to the firm. Therefore, its yield to maturity should

CHAPTER 14: BOND PRICES AND YIELDS PROBLEM SETS 1. The bond callable at 105 should sell at a lower price because the call provision is more valuable to the firm. Therefore, its yield to maturity should

Bond Valuation. Chapter 7. Example (coupon rate = r d ) Bonds, Bond Valuation, and Interest Rates. Valuing the cash flows

Bonds, Bond Valuation, and Interest Rates. Valuing the cash flows") Bond Valuation Chapter 7 Bonds, Bond Valuation, and Interest Rates Valuing the cash flows (1) coupon payment (interest payment) = (coupon rate * principal) usually paid every 6 months (2) maturity value

Bond Valuation Chapter 7 Bonds, Bond Valuation, and Interest Rates Valuing the cash flows (1) coupon payment (interest payment) = (coupon rate * principal) usually paid every 6 months (2) maturity value

20. Investments 4: Bond Basics

20. Investments 4: Bond Basics Introduction The purpose of an investment portfolio is to help individuals and families meet their financial goals. These goals differ from person to person and change over

20. Investments 4: Bond Basics Introduction The purpose of an investment portfolio is to help individuals and families meet their financial goals. These goals differ from person to person and change over

2. Determine the appropriate discount rate based on the risk of the security

Fixed Income Instruments III Intro to the Valuation of Debt Securities LOS 64.a Explain the steps in the bond valuation process 1. Estimate the cash flows coupons and return of principal 2. Determine the

Fixed Income Instruments III Intro to the Valuation of Debt Securities LOS 64.a Explain the steps in the bond valuation process 1. Estimate the cash flows coupons and return of principal 2. Determine the

Understanding Fixed Income

Understanding Fixed Income 2014 AMP Capital Investors Limited ABN 59 001 777 591 AFSL 232497 Understanding Fixed Income About fixed income at AMP Capital Our global presence helps us deliver outstanding

Understanding Fixed Income 2014 AMP Capital Investors Limited ABN 59 001 777 591 AFSL 232497 Understanding Fixed Income About fixed income at AMP Capital Our global presence helps us deliver outstanding

Financial Instruments. Chapter 2

Financial Instruments Chapter 2 Major Types of Securities debt money market instruments bonds common stock preferred stock derivative securities 1-2 Markets and Instruments Money Market debt instruments

Financial Instruments Chapter 2 Major Types of Securities debt money market instruments bonds common stock preferred stock derivative securities 1-2 Markets and Instruments Money Market debt instruments

Answers to Concepts in Review

Answers to Concepts in Review 1. Bonds are appealing to investors because they provide a generous amount of current income and they can often generate large capital gains. These two sources of income together

Answers to Concepts in Review 1. Bonds are appealing to investors because they provide a generous amount of current income and they can often generate large capital gains. These two sources of income together

CITIZENS PROPERTY INSURANCE CORPORATION. INVESTMENT POLICY for. Liquidity Fund (Taxable)

") CITIZENS PROPERTY INSURANCE CORPORATION INVESTMENT POLICY for Liquidity Fund (Taxable) INTRODUCTION Citizens is a government entity whose purpose is to provide property and casualty insurance for those

CITIZENS PROPERTY INSURANCE CORPORATION INVESTMENT POLICY for Liquidity Fund (Taxable) INTRODUCTION Citizens is a government entity whose purpose is to provide property and casualty insurance for those

You just paid $350,000 for a policy that will pay you and your heirs $12,000 a year forever. What rate of return are you earning on this policy?

1 You estimate that you will have $24,500 in student loans by the time you graduate. The interest rate is 6.5%. If you want to have this debt paid in full within five years, how much must you pay each

1 You estimate that you will have $24,500 in student loans by the time you graduate. The interest rate is 6.5%. If you want to have this debt paid in full within five years, how much must you pay each

Chapter 4 Valuing Bonds

Chapter 4 Valuing Bonds MULTIPLE CHOICE 1. A 15 year, 8%, $1000 face value bond is currently trading at $958. The yield to maturity of this bond must be a. less than 8%. b. equal to 8%. c. greater than

Chapter 4 Valuing Bonds MULTIPLE CHOICE 1. A 15 year, 8%, $1000 face value bond is currently trading at $958. The yield to maturity of this bond must be a. less than 8%. b. equal to 8%. c. greater than

CHAPTER 8 INTEREST RATES AND BOND VALUATION

CHAPTER 8 INTEREST RATES AND BOND VALUATION Answers to Concept Questions 1. No. As interest rates fluctuate, the value of a Treasury security will fluctuate. Long-term Treasury securities have substantial

CHAPTER 8 INTEREST RATES AND BOND VALUATION Answers to Concept Questions 1. No. As interest rates fluctuate, the value of a Treasury security will fluctuate. Long-term Treasury securities have substantial

Investors Chronicle Roadshow 2011. Trading Bonds on the London Stock Exchange

Investors Chronicle Roadshow 2011 Trading Bonds on the London Stock Exchange Agenda How do bonds work? Risks associated with bonds Order book for Retail Bonds London Stock Exchange Website Tools 2 How

Investors Chronicle Roadshow 2011 Trading Bonds on the London Stock Exchange Agenda How do bonds work? Risks associated with bonds Order book for Retail Bonds London Stock Exchange Website Tools 2 How

Goals. Bonds: Fixed Income Securities. Two Parts. Bond Returns

Goals Bonds: Fixed Income Securities History Features and structure Bond ratings Economics 71a: Spring 2007 Mayo chapter 12 Lecture notes 4.3 Bond Returns Two Parts Interest and capital gains Stock comparison:

Goals Bonds: Fixed Income Securities History Features and structure Bond ratings Economics 71a: Spring 2007 Mayo chapter 12 Lecture notes 4.3 Bond Returns Two Parts Interest and capital gains Stock comparison:

CHAPTER 14: BOND PRICES AND YIELDS

CHAPTER 14: BOND PRICES AND YIELDS 1. a. Effective annual rate on 3-month T-bill: ( 100,000 97,645 )4 1 = 1.02412 4 1 =.10 or 10% b. Effective annual interest rate on coupon bond paying 5% semiannually:

CHAPTER 14: BOND PRICES AND YIELDS 1. a. Effective annual rate on 3-month T-bill: ( 100,000 97,645 )4 1 = 1.02412 4 1 =.10 or 10% b. Effective annual interest rate on coupon bond paying 5% semiannually:

MONEY MARKET FUND GLOSSARY

MONEY MARKET FUND GLOSSARY 1-day SEC yield: The calculation is similar to the 7-day Yield, only covering a one day time frame. To calculate the 1-day yield, take the net interest income earned by the fund

MONEY MARKET FUND GLOSSARY 1-day SEC yield: The calculation is similar to the 7-day Yield, only covering a one day time frame. To calculate the 1-day yield, take the net interest income earned by the fund

Duration and convexity

Duration and convexity Prepared by Pamela Peterson Drake, Ph.D., CFA Contents 1. Overview... 1 A. Calculating the yield on a bond... 4 B. The yield curve... 6 C. Option-like features... 8 D. Bond ratings...

Duration and convexity Prepared by Pamela Peterson Drake, Ph.D., CFA Contents 1. Overview... 1 A. Calculating the yield on a bond... 4 B. The yield curve... 6 C. Option-like features... 8 D. Bond ratings...

- Short term notes (bonds) Maturities of 1-4 years - Medium-term notes/bonds Maturities of 5-10 years - Long-term bonds Maturities of 10-30 years

Maturities of 1-4 years - Medium-term notes/bonds Maturities of 5-10 years - Long-term bonds Maturities of 10-30 years") Contents 1. What Is A Bond? 2. Who Issues Bonds? Government Bonds Corporate Bonds 3. Basic Terms of Bonds Maturity Types of Coupon (Fixed, Floating, Zero Coupon) Redemption Seniority Price Yield The Relation

Contents 1. What Is A Bond? 2. Who Issues Bonds? Government Bonds Corporate Bonds 3. Basic Terms of Bonds Maturity Types of Coupon (Fixed, Floating, Zero Coupon) Redemption Seniority Price Yield The Relation

Bond Market Overview and Bond Pricing

Bond Market Overview and Bond Pricing. Overview of Bond Market 2. Basics of Bond Pricing 3. Complications 4. Pricing Floater and Inverse Floater 5. Pricing Quotes and Accrued Interest What is A Bond? Bond:

Bond Market Overview and Bond Pricing. Overview of Bond Market 2. Basics of Bond Pricing 3. Complications 4. Pricing Floater and Inverse Floater 5. Pricing Quotes and Accrued Interest What is A Bond? Bond:

Bond valuation. Present value of a bond = present value of interest payments + present value of maturity value

Bond valuation A reading prepared by Pamela Peterson Drake O U T L I N E 1. Valuation of long-term debt securities 2. Issues 3. Summary 1. Valuation of long-term debt securities Debt securities are obligations

Bond valuation A reading prepared by Pamela Peterson Drake O U T L I N E 1. Valuation of long-term debt securities 2. Issues 3. Summary 1. Valuation of long-term debt securities Debt securities are obligations

VALUATION OF FIXED INCOME SECURITIES. Presented By Sade Odunaiya Partner, Risk Management Alliance Consulting

VALUATION OF FIXED INCOME SECURITIES Presented By Sade Odunaiya Partner, Risk Management Alliance Consulting OUTLINE Introduction Valuation Principles Day Count Conventions Duration Covexity Exercises

VALUATION OF FIXED INCOME SECURITIES Presented By Sade Odunaiya Partner, Risk Management Alliance Consulting OUTLINE Introduction Valuation Principles Day Count Conventions Duration Covexity Exercises

CHAPTER 6: FIXED-INCOME SECURITIES: FEATURES AND TYPES

CHAPTER 6: FIXED-INCOME SECURITIES: FEATURES AND TYPES Topic One: The Fixed-Income Marketplace 1. Overview. A. Investing in a fixed-income security is like holding an IOU. An investor (lender) loans a

CHAPTER 6: FIXED-INCOME SECURITIES: FEATURES AND TYPES Topic One: The Fixed-Income Marketplace 1. Overview. A. Investing in a fixed-income security is like holding an IOU. An investor (lender) loans a

Chapter 3 - Selecting Investments in a Global Market

Chapter 3 - Selecting Investments in a Global Market Questions to be answered: Why should investors have a global perspective regarding their investments? What has happened to the relative size of U.S.

Chapter 3 - Selecting Investments in a Global Market Questions to be answered: Why should investors have a global perspective regarding their investments? What has happened to the relative size of U.S.

Important Information about Investing in Bonds

Robert W. Baird & Co. Incorporated Important Information about Investing in Bonds Baird has prepared this document to help you understand the characteristics and risks associated with bonds and other fixed

Robert W. Baird & Co. Incorporated Important Information about Investing in Bonds Baird has prepared this document to help you understand the characteristics and risks associated with bonds and other fixed

January 2008. Bonds. An introduction to bond basics

January 2008 Bonds An introduction to bond basics The information contained in this publication is for general information purposes only and is not intended by the Investment Industry Association of Canada

January 2008 Bonds An introduction to bond basics The information contained in this publication is for general information purposes only and is not intended by the Investment Industry Association of Canada

CHAPTER 2. Asset Classes. the Money Market. Money market instruments. Capital market instruments. Asset Classes and Financial Instruments

2-2 Asset Classes Money market instruments CHAPTER 2 Capital market instruments Asset Classes and Financial Instruments Bonds Equity Securities Derivative Securities The Money Market 2-3 Table 2.1 Major

2-2 Asset Classes Money market instruments CHAPTER 2 Capital market instruments Asset Classes and Financial Instruments Bonds Equity Securities Derivative Securities The Money Market 2-3 Table 2.1 Major

American Options and Callable Bonds

American Options and Callable Bonds American Options Valuing an American Call on a Coupon Bond Valuing a Callable Bond Concepts and Buzzwords Interest Rate Sensitivity of a Callable Bond exercise policy

American Options and Callable Bonds American Options Valuing an American Call on a Coupon Bond Valuing a Callable Bond Concepts and Buzzwords Interest Rate Sensitivity of a Callable Bond exercise policy

Chapter 5 Bonds, Bond Valuation, and Interest Rates ANSWERS TO END-OF-CHAPTER QUESTIONS

Chapter 5 Bonds, Bond Valuation, and Interest Rates ANSWERS TO END-OF-CHAPTER QUESTIONS 5-1 a. A bond is a promissory note issued by a business or a governmental unit. Treasury bonds, sometimes referred

Chapter 5 Bonds, Bond Valuation, and Interest Rates ANSWERS TO END-OF-CHAPTER QUESTIONS 5-1 a. A bond is a promissory note issued by a business or a governmental unit. Treasury bonds, sometimes referred

Introduction to Fixed Income (IFI) Course Syllabus

Course Syllabus") Introduction to Fixed Income (IFI) Course Syllabus 1. Fixed income markets 1.1 Understand the function of fixed income markets 1.2 Know the main fixed income market products: Loans Bonds Money market instruments

Introduction to Fixed Income (IFI) Course Syllabus 1. Fixed income markets 1.1 Understand the function of fixed income markets 1.2 Know the main fixed income market products: Loans Bonds Money market instruments

Chapter 4: Common Stocks. Chapter 5: Forwards and Futures

15.401 Part B Valuation Chapter 3: Fixed Income Securities Chapter 4: Common Stocks Chapter 5: Forwards and Futures Chapter 6: Options Lecture Notes Introduction 15.401 Part B Valuation We have learned

15.401 Part B Valuation Chapter 3: Fixed Income Securities Chapter 4: Common Stocks Chapter 5: Forwards and Futures Chapter 6: Options Lecture Notes Introduction 15.401 Part B Valuation We have learned

BOND - Security that obligates the issuer to make specified payments to the bondholder.

Bond Valuation BOND - Security that obligates the issuer to make specified payments to the bondholder. COUPON - The interest payments paid to the bondholder. FACE VALUE - Payment at the maturity of the

Bond Valuation BOND - Security that obligates the issuer to make specified payments to the bondholder. COUPON - The interest payments paid to the bondholder. FACE VALUE - Payment at the maturity of the

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

ECON 4110: Sample Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Economists define risk as A) the difference between the return on common

ECON 4110: Sample Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Economists define risk as A) the difference between the return on common

Chapter. Interest Rates. McGraw-Hill/Irwin. Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Interest Rates McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Interest Rates Our goal in this chapter is to discuss the many different interest rates that

Chapter Interest Rates McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Interest Rates Our goal in this chapter is to discuss the many different interest rates that

Chapter. Investing in Bonds. 13.1 Evaluating Bonds 13.2 Buying and Selling Bonds. 2010 South-Western, Cengage Learning

Chapter 13 Investing in Bonds 13.1 Evaluating Bonds 13.2 Buying and Selling Bonds 2010 South-Western, Cengage Learning Standards Standard 4.0 Investigate opportunities available for saving and investing.

Chapter 13 Investing in Bonds 13.1 Evaluating Bonds 13.2 Buying and Selling Bonds 2010 South-Western, Cengage Learning Standards Standard 4.0 Investigate opportunities available for saving and investing.

Bond Valuation. FINANCE 350 Global Financial Management. Professor Alon Brav Fuqua School of Business Duke University. Bond Valuation: An Overview

Bond Valuation FINANCE 350 Global Financial Management Professor Alon Brav Fuqua School of Business Duke University 1 Bond Valuation: An Overview Bond Markets What are they? How big? How important? Valuation

Bond Valuation FINANCE 350 Global Financial Management Professor Alon Brav Fuqua School of Business Duke University 1 Bond Valuation: An Overview Bond Markets What are they? How big? How important? Valuation

Using Derivatives in the Fixed Income Markets

Using Derivatives in the Fixed Income Markets A White Paper by Manning & Napier www.manning-napier.com Unless otherwise noted, all figures are based in USD. 1 Introduction While derivatives may have a

Using Derivatives in the Fixed Income Markets A White Paper by Manning & Napier www.manning-napier.com Unless otherwise noted, all figures are based in USD. 1 Introduction While derivatives may have a

CHAPTER 7: FIXED-INCOME SECURITIES: PRICING AND TRADING

CHAPTER 7: FIXED-INCOME SECURITIES: PRICING AND TRADING Topic One: Bond Pricing Principles 1. Present Value. A. The present-value calculation is used to estimate how much an investor should pay for a bond;

CHAPTER 7: FIXED-INCOME SECURITIES: PRICING AND TRADING Topic One: Bond Pricing Principles 1. Present Value. A. The present-value calculation is used to estimate how much an investor should pay for a bond;

How To Invest In Stocks And Bonds

Review for Exam 1 Instructions: Please read carefully The exam will have 21 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation

Review for Exam 1 Instructions: Please read carefully The exam will have 21 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation

Chapter 11. Bond Pricing - 1. Bond Valuation: Part I. Several Assumptions: To simplify the analysis, we make the following assumptions.

Bond Pricing - 1 Chapter 11 Several Assumptions: To simplify the analysis, we make the following assumptions. 1. The coupon payments are made every six months. 2. The next coupon payment for the bond is

Bond Pricing - 1 Chapter 11 Several Assumptions: To simplify the analysis, we make the following assumptions. 1. The coupon payments are made every six months. 2. The next coupon payment for the bond is

NATIONAL STOCK EXCHANGE OF INDIA LIMITED

NATIONAL STOCK EXCHANGE OF INDIA LIMITED Capital Market FAQ on Corporate Bond Date : September 29, 2011 1. What are securities? Securities are financial instruments that represent a creditor relationship

NATIONAL STOCK EXCHANGE OF INDIA LIMITED Capital Market FAQ on Corporate Bond Date : September 29, 2011 1. What are securities? Securities are financial instruments that represent a creditor relationship

TIME VALUE OF MONEY #6: TREASURY BOND. Professor Peter Harris Mathematics by Dr. Sharon Petrushka. Introduction

TIME VALUE OF MONEY #6: TREASURY BOND Professor Peter Harris Mathematics by Dr. Sharon Petrushka Introduction This problem assumes that you have mastered problems 1-5, which are prerequisites. In this

TIME VALUE OF MONEY #6: TREASURY BOND Professor Peter Harris Mathematics by Dr. Sharon Petrushka Introduction This problem assumes that you have mastered problems 1-5, which are prerequisites. In this

Lecture 11 Fixed-Income Securities: An Overview

1 Lecture 11 Fixed-Income Securities: An Overview Alexander K. Koch Department of Economics, Royal Holloway, University of London January 11, 2008 In addition to learning the material covered in the reading

1 Lecture 11 Fixed-Income Securities: An Overview Alexander K. Koch Department of Economics, Royal Holloway, University of London January 11, 2008 In addition to learning the material covered in the reading

Bond Valuation. Capital Budgeting and Corporate Objectives

Bond Valuation Capital Budgeting and Corporate Objectives Professor Ron Kaniel Simon School of Business University of Rochester 1 Bond Valuation An Overview Introduction to bonds and bond markets» What

Bond Valuation Capital Budgeting and Corporate Objectives Professor Ron Kaniel Simon School of Business University of Rochester 1 Bond Valuation An Overview Introduction to bonds and bond markets» What

Chapter 3 Fixed Income Securities

Chapter 3 Fixed Income Securities Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. Fixed-income securities. Stocks. Real assets (capital budgeting). Part C Determination

Chapter 3 Fixed Income Securities Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. Fixed-income securities. Stocks. Real assets (capital budgeting). Part C Determination

CHAPTER 5. Interest Rates. Chapter Synopsis

CHAPTER 5 Interest Rates Chapter Synopsis 5.1 Interest Rate Quotes and Adjustments Interest rates can compound more than once per year, such as monthly or semiannually. An annual percentage rate (APR)

CHAPTER 5 Interest Rates Chapter Synopsis 5.1 Interest Rate Quotes and Adjustments Interest rates can compound more than once per year, such as monthly or semiannually. An annual percentage rate (APR)

Investing in Bonds - An Introduction

Investing in Bonds - An Introduction By: Scott A. Bishop, CPA, CFP, and Director of Financial Planning What are bonds? Bonds, sometimes called debt instruments or fixed-income securities, are essentially

Investing in Bonds - An Introduction By: Scott A. Bishop, CPA, CFP, and Director of Financial Planning What are bonds? Bonds, sometimes called debt instruments or fixed-income securities, are essentially

Exam 1 Morning Session

91. A high yield bond fund states that through active management, the fund s return has outperformed an index of Treasury securities by 4% on average over the past five years. As a performance benchmark

91. A high yield bond fund states that through active management, the fund s return has outperformed an index of Treasury securities by 4% on average over the past five years. As a performance benchmark

Chapter 2. Practice Problems. MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chapter 2 Practice Problems MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Assume that you borrow $2000 at 10% annual interest to finance a new

Chapter 2 Practice Problems MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Assume that you borrow $2000 at 10% annual interest to finance a new

CHAPTER 8 INTEREST RATES AND BOND VALUATION

CHAPTER 8 INTEREST RATES AND BOND VALUATION Solutions to Questions and Problems 1. The price of a pure discount (zero coupon) bond is the present value of the par value. Remember, even though there are

CHAPTER 8 INTEREST RATES AND BOND VALUATION Solutions to Questions and Problems 1. The price of a pure discount (zero coupon) bond is the present value of the par value. Remember, even though there are

Bonds, in the most generic sense, are issued with three essential components.

Page 1 of 5 Bond Basics Often considered to be one of the most conservative of all investments, bonds actually provide benefits to both conservative and more aggressive investors alike. The variety of

Page 1 of 5 Bond Basics Often considered to be one of the most conservative of all investments, bonds actually provide benefits to both conservative and more aggressive investors alike. The variety of

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES 1. Expectations hypothesis. The yields on long-term bonds are geometric averages of present and expected future short rates. An upward sloping curve is

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES 1. Expectations hypothesis. The yields on long-term bonds are geometric averages of present and expected future short rates. An upward sloping curve is

Bonds. Describe Bonds. Define Key Words. Created 2007 By Michael Worthington Elizabeth City State University

Bonds OBJECTIVES Describe bonds Define key words Explain why bond prices fluctuate Compute interest payments Calculate the price of bonds Created 2007 By Michael Worthington Elizabeth City State University

Bonds OBJECTIVES Describe bonds Define key words Explain why bond prices fluctuate Compute interest payments Calculate the price of bonds Created 2007 By Michael Worthington Elizabeth City State University

Interest Rates and Bond Valuation

Chapter 6 Interest Rates and Bond Valuation LG2 LG2 LG3 LG4 LG5 LG6 LEARNING GOALS Describe interest rate fundamentals, the term structure of interest rates, and risk premiums. Review the legal aspects

Chapter 6 Interest Rates and Bond Valuation LG2 LG2 LG3 LG4 LG5 LG6 LEARNING GOALS Describe interest rate fundamentals, the term structure of interest rates, and risk premiums. Review the legal aspects

Glossary. Accrued Interest. Amortizing Bond. ASK Price (Offer Price) Automatic Order Matching (AOM)

Automatic Order Matching (AOM)") Glossary Accrued Interest Amortizing Bond ASK Price (Offer Price) Automatic Order Matching (AOM) Average Yield BEX The amount of interest accumulated but not yet paid between the last payment and the settlement

Glossary Accrued Interest Amortizing Bond ASK Price (Offer Price) Automatic Order Matching (AOM) Average Yield BEX The amount of interest accumulated but not yet paid between the last payment and the settlement

Financial Market Instruments

appendix to chapter 2 Financial Market Instruments Here we examine the securities (instruments) traded in financial markets. We first focus on the instruments traded in the money market and then turn to

appendix to chapter 2 Financial Market Instruments Here we examine the securities (instruments) traded in financial markets. We first focus on the instruments traded in the money market and then turn to

INTEREST RATE SWAPS September 1999

INTEREST RATE SWAPS September 1999 INTEREST RATE SWAPS Definition: Transfer of interest rate streams without transferring underlying debt. 2 FIXED FOR FLOATING SWAP Some Definitions Notational Principal:

INTEREST RATE SWAPS September 1999 INTEREST RATE SWAPS Definition: Transfer of interest rate streams without transferring underlying debt. 2 FIXED FOR FLOATING SWAP Some Definitions Notational Principal:

Review for Exam 1. Instructions: Please read carefully

Review for Exam 1 Instructions: Please read carefully The exam will have 20 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation

Review for Exam 1 Instructions: Please read carefully The exam will have 20 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation

Shares Mutual funds Structured bonds Bonds Cash money, deposits

FINANCIAL INSTRUMENTS AND RELATED RISKS This description of investment risks is intended for you. The professionals of AB bank Finasta have strived to understandably introduce you the main financial instruments

FINANCIAL INSTRUMENTS AND RELATED RISKS This description of investment risks is intended for you. The professionals of AB bank Finasta have strived to understandably introduce you the main financial instruments

Maturity The date where the issuer must return the principal or the face value to the investor.

PRODUCT INFORMATION SHEET - BONDS 1. WHAT ARE BONDS? A bond is a debt instrument issued by a borrowing entity (issuer) to investors (lenders) in return for lending their money to the issuer. The issuer

PRODUCT INFORMATION SHEET - BONDS 1. WHAT ARE BONDS? A bond is a debt instrument issued by a borrowing entity (issuer) to investors (lenders) in return for lending their money to the issuer. The issuer

LOS 56.a: Explain steps in the bond valuation process.

The following is a review of the Analysis of Fixed Income Investments principles designed to address the learning outcome statements set forth by CFA Institute. This topic is also covered in: Introduction

The following is a review of the Analysis of Fixed Income Investments principles designed to address the learning outcome statements set forth by CFA Institute. This topic is also covered in: Introduction

A guide to investing in high-yield bonds

A guide to investing in high-yield bonds What you should know before you buy Are high-yield bonds suitable for you? High-yield bonds are designed for investors who: Can accept additional risks of investing

A guide to investing in high-yield bonds What you should know before you buy Are high-yield bonds suitable for you? High-yield bonds are designed for investors who: Can accept additional risks of investing

TVM Applications Chapter

Chapter 6 Time of Money UPS, Walgreens, Costco, American Air, Dreamworks Intel (note 10 page 28) TVM Applications Accounting issue Chapter Notes receivable (long-term receivables) 7 Long-term assets 10

Chapter 6 Time of Money UPS, Walgreens, Costco, American Air, Dreamworks Intel (note 10 page 28) TVM Applications Accounting issue Chapter Notes receivable (long-term receivables) 7 Long-term assets 10

Econ 330 Exam 1 Name ID Section Number

Econ 330 Exam 1 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If during the past decade the average rate of monetary growth

Econ 330 Exam 1 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If during the past decade the average rate of monetary growth

YIELD CURVE GENERATION

1 YIELD CURVE GENERATION Dr Philip Symes Agenda 2 I. INTRODUCTION II. YIELD CURVES III. TYPES OF YIELD CURVES IV. USES OF YIELD CURVES V. YIELD TO MATURITY VI. BOND PRICING & VALUATION Introduction 3 A

1 YIELD CURVE GENERATION Dr Philip Symes Agenda 2 I. INTRODUCTION II. YIELD CURVES III. TYPES OF YIELD CURVES IV. USES OF YIELD CURVES V. YIELD TO MATURITY VI. BOND PRICING & VALUATION Introduction 3 A

AMP Capital Understanding Fixed Income a glossary

AMP Capital Understanding Fixed Income a glossary Welcome to our educational series Understanding Fixed Income a glossary About fixed income at AMP Capital As one of the largest and most experienced fixed

AMP Capital Understanding Fixed Income a glossary Welcome to our educational series Understanding Fixed Income a glossary About fixed income at AMP Capital As one of the largest and most experienced fixed

Bank of America AAA 10.00% T-Bill +.30% Hypothetical Resources BBB 11.90% T-Bill +.80% Basis point difference 190 50

Swap Agreements INTEREST RATE SWAP AGREEMENTS An interest rate swap is an agreement to exchange interest rate payments on a notional principal amount over a specific period of time. Generally a swap exchanges

Swap Agreements INTEREST RATE SWAP AGREEMENTS An interest rate swap is an agreement to exchange interest rate payments on a notional principal amount over a specific period of time. Generally a swap exchanges

CITIZENS PROPERTY INSURANCE CORPORATION. INVESTMENT POLICY for. Claims Paying Fund (Taxable)

") CITIZENS PROPERTY INSURANCE CORPORATION INVESTMENT POLICY for Claims Paying Fund (Taxable) INTRODUCTION Citizens is a government entity whose purpose is to provide property and casualty insurance for those

CITIZENS PROPERTY INSURANCE CORPORATION INVESTMENT POLICY for Claims Paying Fund (Taxable) INTRODUCTION Citizens is a government entity whose purpose is to provide property and casualty insurance for those

CHAPTER 10 BOND PRICES AND YIELDS

CHAPTER 10 BOND PRICES AND YIELDS 1. a. Catastrophe bond. Typically issued by an insurance company. They are similar to an insurance policy in that the investor receives coupons and par value, but takes

CHAPTER 10 BOND PRICES AND YIELDS 1. a. Catastrophe bond. Typically issued by an insurance company. They are similar to an insurance policy in that the investor receives coupons and par value, but takes

Advanced forms of currency swaps

Advanced forms of currency swaps Basis swaps Basis swaps involve swapping one floating index rate for another. Banks may need to use basis swaps to arrange a currency swap for the customers. Example A

Advanced forms of currency swaps Basis swaps Basis swaps involve swapping one floating index rate for another. Banks may need to use basis swaps to arrange a currency swap for the customers. Example A

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle 9.1 Current Assets and 9.1.1 Cash A firm should maintain as little cash as possible, because cash is a nonproductive asset. It earns no

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle 9.1 Current Assets and 9.1.1 Cash A firm should maintain as little cash as possible, because cash is a nonproductive asset. It earns no

Bonds and preferred stock. Basic definitions. Preferred(?) stock. Investing in fixed income securities

stock. Investing in fixed income securities") Bonds and preferred stock Investing in fixed income securities Basic definitions Stock: share of ownership Stockholders are the owners of the firm Two types of stock: preferred and common Preferred stock:

Bonds and preferred stock Investing in fixed income securities Basic definitions Stock: share of ownership Stockholders are the owners of the firm Two types of stock: preferred and common Preferred stock:

Commercial paper collateralized by a pool of loans, leases, receivables, or structured credit products. Asset-backed commercial paper (ABCP)

") GLOSSARY Asset-backed commercial paper (ABCP) Asset-backed security (ABS) Asset-backed securities index (ABX) Basel II Call (put) option Carry trade Collateralized debt obligation (CDO) Collateralized

GLOSSARY Asset-backed commercial paper (ABCP) Asset-backed security (ABS) Asset-backed securities index (ABX) Basel II Call (put) option Carry trade Collateralized debt obligation (CDO) Collateralized

Review for Exam 1. Instructions: Please read carefully

Review for Exam 1 Instructions: Please read carefully The exam will have 25 multiple choice questions and 5 work problems covering chapter 1, 2, 3, 4, 14, 16. Questions in the multiple choice section will

Review for Exam 1 Instructions: Please read carefully The exam will have 25 multiple choice questions and 5 work problems covering chapter 1, 2, 3, 4, 14, 16. Questions in the multiple choice section will

Centrale Bank van Curaçao en Sint Maarten. Manual Coordinated Portfolio Investment Survey CPIS. Prepared by: Project group CPIS

Centrale Bank van Curaçao en Sint Maarten Manual Coordinated Portfolio Investment Survey CPIS Prepared by: Project group CPIS Augustus 1, 2015 Contents Introduction 3 General reporting and instruction

Centrale Bank van Curaçao en Sint Maarten Manual Coordinated Portfolio Investment Survey CPIS Prepared by: Project group CPIS Augustus 1, 2015 Contents Introduction 3 General reporting and instruction

Chapter 6 Valuing Bonds. (1) coupon payment - interest payment (coupon rate * principal) - usually paid every 6 months.

coupon payment - interest payment (coupon rate * principal) - usually paid every 6 months.") Chapter 6 Valuing Bonds Bond Valuation - value the cash flows (1) coupon payment - interest payment (coupon rate * principal) - usually paid every 6 months. (2) maturity value = principal or par value

Chapter 6 Valuing Bonds Bond Valuation - value the cash flows (1) coupon payment - interest payment (coupon rate * principal) - usually paid every 6 months. (2) maturity value = principal or par value

NOTE ON LOAN CAPITAL MARKETS

The structure and use of loan products Most businesses use one or more loan products. A company may have a syndicated loan, backstop, line of credit, standby letter of credit, bridge loan, mortgage, or

The structure and use of loan products Most businesses use one or more loan products. A company may have a syndicated loan, backstop, line of credit, standby letter of credit, bridge loan, mortgage, or

A guide to investing in high-yield bonds

A guide to investing in high-yield bonds What you should know before you buy Are high-yield bonds suitable for you? High-yield bonds are designed for investors who: Can accept additional risks of investing

A guide to investing in high-yield bonds What you should know before you buy Are high-yield bonds suitable for you? High-yield bonds are designed for investors who: Can accept additional risks of investing

Prepared by: Dalia A. Marafi Version 2.0

Kuwait University College of Business Administration Department of Finance and Financial Institutions Using )Casio FC-200V( for Fundamentals of Financial Management (220) Prepared by: Dalia A. Marafi Version

Kuwait University College of Business Administration Department of Finance and Financial Institutions Using )Casio FC-200V( for Fundamentals of Financial Management (220) Prepared by: Dalia A. Marafi Version

Current liabilities - Obligations that are due within one year. Obligations due beyond that period of time are classified as long-term liabilities.

Accounting Fundamentals Lesson 8 8.0 Liabilities Current liabilities - Obligations that are due within one year. Obligations due beyond that period of time are classified as long-term liabilities. Current

Accounting Fundamentals Lesson 8 8.0 Liabilities Current liabilities - Obligations that are due within one year. Obligations due beyond that period of time are classified as long-term liabilities. Current

Long-Term Debt. Objectives: simple present value calculations. Understand the terminology of long-term debt Par value Discount vs.

Objectives: Long-Term Debt! Extend our understanding of valuation methods beyond simple present value calculations. Understand the terminology of long-term debt Par value Discount vs. Premium Mortgages!

Objectives: Long-Term Debt! Extend our understanding of valuation methods beyond simple present value calculations. Understand the terminology of long-term debt Par value Discount vs. Premium Mortgages!

LOCKING IN TREASURY RATES WITH TREASURY LOCKS

LOCKING IN TREASURY RATES WITH TREASURY LOCKS Interest-rate sensitive financial decisions often involve a waiting period before they can be implemen-ted. This delay exposes institutions to the risk that

LOCKING IN TREASURY RATES WITH TREASURY LOCKS Interest-rate sensitive financial decisions often involve a waiting period before they can be implemen-ted. This delay exposes institutions to the risk that