Internal Control and Cash

|

|

|

- Beverley Stafford

- 10 years ago

- Views:

Transcription

1 Accounting Principles, 7 th Edition Weygandt Kieso Kimmel Chapter 8 Internal Control and Cash Prepared by Naomi Karolinski Monroe Community College and Marianne Bradford Bryant College John Wiley & Sons, Inc. 2005

2 CHAPTER 8 INTERNAL CONTROL AND CASH After studying this chapter, you should be able to: 1 Define internal control. 2 Identify the principles of internal control. 3 Explain the applications of internal control principles to cash receipts. 4 Explain the applications of internal control principles to cash disbursements. 5 Describe the operation of a petty cash fund. 6 Indicate the control features of a bank account. 7 Prepare a bank reconciliation. 8 Explain the reporting of cash.

3 INTERNAL CONTROL STUDY OBJECTIVE 1 Internal Control 1. Safeguards an organization s assets 2. Enhances the accuracy and reliability of accounting records

4 PRINCIPLES OF INTERNAL CONTROL STUDY OBJECTIVE 2

5 PRINCIPLES OF INTERNAL CONTROL Establishment of responsibility: most effective when only one person is responsible for a given task Segregation of duties: the work of one employee should provide a reliable basis for evaluating the work of another employee Documentation procedures: documents provide evidence that transactions and events have occurred

6 PRINCIPLES OF INTERNAL CONTROL Physical, mechanical, and electronic controls: safeguarding of assets and enhancing accuracy and reliability of the accounting records. Independent internal verification: the review, comparison, and reconciliation of information from two sources. Other controls: bonding of employees who handle cash, rotating employee s duties, and requiring employees to take vacations.

7 PHYSICAL, MECHANICAL, AND ELECTRONIC CONTROLS Locked warehouses and storage cabinets for inventories and records Safes, vaults, and safety deposit boxes for cash and business papers Time clocks for recording time worked Computer facilities with pass key access Alarms to prevent break-ins Television monitors and garment sensors to deter theft

8 PHYSICAL, MECHANICAL, AND ELECTRONIC CONTROLS

9 INDEPENDENT INTERNAL VERIFICATION Maximum benefit Independent internal verification: 1 Made on periodic or surprise basis 2 Should be done by someone who is independent of the employee responsible for the information 3 Report discrepancies and exceptions to a management level that can take appropriate corrective action

10 COMPARISON OF SEGREGATION OF DUTIES PRINCIPLE WITH INDEPENDENT INTERNAL VERIFICATION PRINCIPLE

11 LIMITATIONS OF INTERNAL Costs of establishing control procedures should not exceed their expected benefits The human element is an important factor in every system of internal control. A good system can become ineffective through employee fatigue, carelessness, or indifference. Collusion may result. CONTROL Two or more individuals work together to get around prescribed controls and may significantly impair the effectiveness of a system.

12 CASH Cash Coins, currency, checks, money orders, and money on hand or on deposit at a bank or similar depository Internal control over cash is imperative Safeguards cash and assure the accuracy of the accounting records for cash

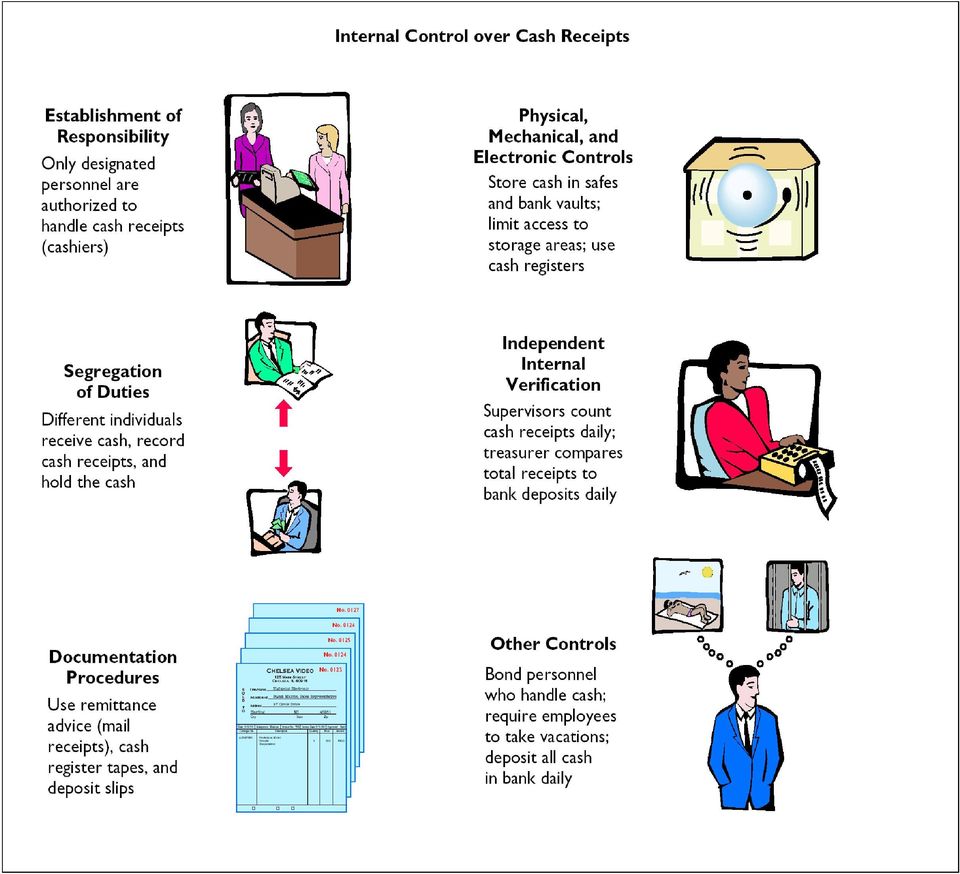

13 CONTROL OVER CASH Only designated personnel should be authorized to handle or have access to cash receipts. Different individuals should: 1 receive cash RECEIPTS STUDY OBJECTIVE 3 2 record cash receipt transactions 3 have custody of cash

14 CONTROL OVER CASH RECEIPTS Documents should include: 1 Remittance advices 2 Cash register tapes 3 Deposit slips Cash should be stored in safes and bank vaults Access to storage areas should be limited to authorized personnel Cash registers should be used in executing over-the-counter receipts

15 Internal control is used in a business to enhance the accuracy and reliability of its accounting records and to: a. safeguard its assets. b. prevent fraud. c. produce correct financial statements. d. deter employee dishonesty.

16 Internal control is used in a business to enhance the accuracy and reliability of its accounting records and to: a. safeguard its assets. b. prevent fraud. c. produce correct financial statements. d. deter employee dishonesty.

17 CONTROL OVER CASH RECEIPTS Daily cash counts and daily comparisons of total receipts. All personnel who handle cash receipts should be bonded and required to take vacations. Control of over-the-counter receipts is centered on cash registers that are visible to customers.

18

19

20 CONTROL OVER CASH DISBURSEMENTS STUDY OBJECTIVE 4 Payments are made by check rather than by cash, except for petty cash transactions. Only specified individuals should be authorized to sign checks. Different departments or individuals should be assigned the duties of approving an item for payment and paying it.

21 What does a check (cheque) look like?

22 CONTROL OVER CASH DISBURSEMENTS Prenumbered checks should be used and each check should be supported by an approved invoice or other document. Blank checks should be stored in a safe. 1 Access should be restricted to authorized personnel. 2 A check writer machine should be used to imprint the amount on the check in indelible ink.

23 CONTROL OVER CASH DISBURSEMENTS Each check should be compared with the approved invoice before it is issued. Following payment, the approved invoice should be stamped PAID.

24

25 VOUCHER SYSTEM The voucher system Is often used to enhance the internal control over cash disbursements. Is an extensive network of approvals by authorized individuals acting independently to ensure that all disbursements by check are proper. A voucher is an authorization form prepared for each expenditure. Vouchers are recorded in a journal called the voucher register.

26 ELECTRONIC FUNDS TRANSFER SYSTEM Checks processing is expensive New methods are being developed to transfer funds among parties without the use of paper Electronic Funds Transfer (EFT) System A disbursement system that uses wire, telephone, telegraph, or computer to transfer cash from one location to another

27 PETTY CASH FUND STUDY OBJECTIVE 5 A petty cash fund is used to pay relatively small amounts Operation of the fund, often called an imprest system, involves: 1 Establishing the fund 2 Making payments from the fund 3 Replenishing the fund Accounting entries are required when: 1 The fund is established 2 The fund is replenished 3 The amount of the fund is changed

28 ESTABLISHING THE FUND Two essential steps in establishing a petty cash fund are: 1 appointing a petty cash custodian who will be responsible for the fund and 2 determining the size of the fund. Ordinarily, the amount is expected to cover anticipated disbursements for a 3 to 4 week period.

29 ESTABLISHING THE FUND GENERALJOURNAL Date Account Titles and Explanation Debit Credit Mar. 1 Petty Cash 100 Cash 100 (To establish a petty cash fund) When the fund is established, a check payable to the petty cash custodian is issued for the stipulated amount.

30 REPLENISHING THE FUND When the money in the petty cash fund reaches a minimum level, the fund is replenished. The request for reimbursement is initiated by the petty cash custodian. The petty cash custodian prepares a schedule of the payments that have been made and sends the schedule, with supporting documentation, to the treasurer s office.

31 REPLENISHING THE FUND GENERAL JOURNAL Date Account Titles and Explanation Debit Credit Mar. 15 Postage Expense 44 Freight-out 38 Miscellaneous Expense 5 Cash 87 (To replenish petty cash fund) On March 15 the petty cash custodian requests a check for $87. The fund contains $13 cash and petty cash receipts for postage, $44, freight-out, $38, and miscellaneous expenses, $5.

32 REPLENISHING THE FUND GENERAL JOURNAL Date Account Titles and Explanation Debit Credit Mar. 15 Postage Expense 44 Freight-out 38 Miscellaneous Expense 5 Cash Over and Short 1 Cash 88 (To replenish petty cash fund) On March 15 the petty cash custodian requests a check for $88. The fund contains $12 cash and petty cash receipts for postage, $44, freight-out, $38, and miscellaneous expenses, $5.

33 USE OF A BANK STUDY OBJECTIVE 6 The use of a bank minimizes the amount of currency that must be kept on hand and contributes significantly to good internal control over cash. A company can safeguard its cash by using a bank as a depository and as a clearing house for checks received and checks written.

34 WRITING CHECKS A check is a written order signed by the depositor directing the bank to pay a specified sum of money to a designated recipient. Three parties to a check are: 1 Maker (drawer) issues the check 2 Bank (payer) on which check is drawn 3 Payee to whom check is payable

35 WRITING CHECKS

36 BANK STATEMENTS A bank statement shows: 1 Checks paid and other debits charged against the account 2 Deposits and other credits made to the account 3 Account balance after each day s transactions

37 MEMORANDA Bank debit memoranda Indicate charges against the depositor s account. Example: ATM service charges Bank credit memoranda Indicate amounts that will increase the depositor s account. Example: interest income on account balance

38 RECONCILING THE BANK ACCOUNT STUDY OBJECTIVE 7 Reconciliation Necessary as the balance per bank and balance per books are seldom in agreement due to time lags and errors. A bank reconciliation Should be prepared by an employee who has no other responsibilities pertaining to cash.

39 RECONCILING THE BANK ACCOUNT Steps in preparing a bank reconciliation: 1 Determine deposits in transit 2 Determine outstanding checks 3 Note any errors discovered 4 Trace bank memoranda to the records Each reconciling item used in determining the adjusted cash balance per books should be recorded by the depositor.

40 BANK RECONCILIATION

41 BANK RECONCILIATION W. A. LAIRD COMPANY Bank Reconciliation April 30, 2005 Cash balance per bank statement $ 15, Add: Deposits in transit The bank statement for 2, the Laird Company 18, Less: Outstanding checks shows a balance per No. 453 bank of $15, on $ 3, No , April 30, No , , Adjusted cash balance per bank $ 12, Cash balance per books $ 11, Add: Collection of $1,000 note receivable plus interest earned $50, less collection fee $15 $ 1, Error in recording check , , On this date the Less: NSF check Bank service charge balance of cash per books is $11, Adjusted cash balance per books $ 12,204.85

42 ENTRIES FROM BANK RECONCILIATION GENERAL JOURNAL Date Account Titles and Explanation Debit Credit Apr. 30 Cash 1035 Miscellaneous Expense 15 Notes Receivable 1000 Interest Revenue 50 (To record collection of notes receivable by bank) Collection of Note Receivable: This entry involves four accounts. Interest of $50 has not been accrued and the collection fee is charged to Miscellaneous Expense.

43 ENTRIES FROM BANK RECONCILIATION GENERAL JOURNAL Date Account Titles and Explanation Debit Credit Apr. 30 Cash Accounts Payable Andrea Company (To correct error in recording check No. 443) Book Error: An examination of the cash disbursements journal shows that check No. 443 was a payment on account to Andrea Company, a supplier. The check, with a correct amount of $1,226.00, was recorded at $1,

44 ENTRIES FROM BANK RECONCILIATION GENERAL JOURNAL Date Account Titles and Explanation Debit Credit Apr. 30 Accounts Receivable J. R. Baron Cash (To record NSF check) NSF Check: An NSF check becomes an accounts receivable to the depositor.

45 ENTRIES FROM BANK RECONCILIATION GENERAL JOURNAL Date Account Titles and Explanation Debit Credit Apr. 30 Miscellaneous Expense 30 Cash (To record charge for printing 30 company checks) Bank Service Charges: Check printing charges (DM) and other bank service charges (SC) are debited to Miscellaneous Expense because they are usually nominal in amount.

46 REPORTING CASH STUDY OBJECTIVE 8 Cash reported on the Balance Sheet includes: 1 Cash on hand 2 Cash in banks 3 Petty cash Cash is listed first in the balance sheet under the title cash and cash equivalents because it is the most liquid asset.

47 CASH EQUIVALENTS Cash equivalents Are highly liquid investments that can be converted into a specific amount of cash Typically have maturities of 3 months or less when purchased Examples: Money market funds, bank certificates of deposit, and U.S. Treasury bills and notes

48 The statement that correctly describes the reporting of cash is: a. Cash cannot be combined with cash equivelants b. Restricted cash funds may be combined with Cash. c. Cash is listed first in the current assets. d. Restricted cash funds cannot be reported as a current asset.

49 The statement that correctly describes the reporting of cash is: a. Cash cannot be combined with cash equivelants. b. Restricted cash funds may be combined with Cash. c. Cash is listed first in the current assets. d. Restricted cash funds cannot be reported as a current asset.

50 COPYRIGHT Copyright 2005 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written consent of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein.

Introduction to Accounting 2 Modul 1 Internal Control and Cash

Introduction to Accounting 2 Modul 1 Internal Control and Cash After studying this chapter, you should be able to: 1. Describe the Sarbanes-Oxley Act of 2002 and its impact on internal controls and financial

Introduction to Accounting 2 Modul 1 Internal Control and Cash After studying this chapter, you should be able to: 1. Describe the Sarbanes-Oxley Act of 2002 and its impact on internal controls and financial

Chapter 8. Internal Control. Chapter 8-1

8 Internal Control and Cash 8-1 Internal Control and Cash Internal Control Cash Controls Use of a Bank Reporting Cash The Sarbanes- Oxley Act Principles Limitations Control over cash receipts Control over

8 Internal Control and Cash 8-1 Internal Control and Cash Internal Control Cash Controls Use of a Bank Reporting Cash The Sarbanes- Oxley Act Principles Limitations Control over cash receipts Control over

Chapter 7 Fraud, Internal Control, and Cash 高立翰

Chapter 7 Fraud, Internal Control, and Cash 高立翰 Study Objectives 1. Define fraud and internal control. 2. Identify the principles of internal control activities. 3. Explain the applications of internal

Chapter 7 Fraud, Internal Control, and Cash 高立翰 Study Objectives 1. Define fraud and internal control. 2. Identify the principles of internal control activities. 3. Explain the applications of internal

Internal Control and Cash. Study Objectives. Chapter Outline

Study Objectives Identify the principles of internal control. Explain the applications of internal control to cash receipts. Explain the applications of internal control to cash disbursements. Prepare

Study Objectives Identify the principles of internal control. Explain the applications of internal control to cash receipts. Explain the applications of internal control to cash disbursements. Prepare

Fraud, Internal Control, and Cash

Chapter 7 Fraud, Internal Control, and Cash 7-1 Learning Objectives After studying this chapter, you should be able to: 1. Define fraud ( 欺 騙 ) and internal control ( 內 部 控 制 ). 2. Identify the principles

Chapter 7 Fraud, Internal Control, and Cash 7-1 Learning Objectives After studying this chapter, you should be able to: 1. Define fraud ( 欺 騙 ) and internal control ( 內 部 控 制 ). 2. Identify the principles

CHAPTER 7. Fraud, Internal Control, and Cash 5, 6, 7, 8, 9, 10, 11 6, 13, 14, 15 16, 17, 18, 19 11, 12 13, 14

CHAPTER 7 Fraud, Internal Control, and Cash ASSIGNMENT CLASSIFICATION TABLE Learning Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Define fraud and internal control. 1,

CHAPTER 7 Fraud, Internal Control, and Cash ASSIGNMENT CLASSIFICATION TABLE Learning Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Define fraud and internal control. 1,

Caused By 1. Time. 2. Errors. lags $ XXX. but not by bank (e.g., deposits. Add: Deposits recorded by business. Cash balance per bank statement

ILLUSTRATION 8-5 BANK RECONCILIATION FORMAT Balances Should Agree Bank Reconciliation (Date) balance per bank statement Add: Deposits recorded by business but not by bank (e.g., deposits in transit) Less:Charges

ILLUSTRATION 8-5 BANK RECONCILIATION FORMAT Balances Should Agree Bank Reconciliation (Date) balance per bank statement Add: Deposits recorded by business but not by bank (e.g., deposits in transit) Less:Charges

8-1. Prepared by Coby Harmon University of California, Santa Barbara Westmont College

8-1 Prepared by Coby Harmon University of California, Santa Barbara Westmont College 8 Fraud, Internal Control, and Cash Learning Objectives After studying this chapter, you should be able to: [1] Define

8-1 Prepared by Coby Harmon University of California, Santa Barbara Westmont College 8 Fraud, Internal Control, and Cash Learning Objectives After studying this chapter, you should be able to: [1] Define

Fraud, Internal Control, and Cash

Prepared by Coby Harmon University of California, Santa Barbara Westmont College 8-1 8 Fraud, Internal Control, and Cash Learning Objectives After studying this chapter, you should be able to: [1] Define

Prepared by Coby Harmon University of California, Santa Barbara Westmont College 8-1 8 Fraud, Internal Control, and Cash Learning Objectives After studying this chapter, you should be able to: [1] Define

COUNTY OF TRINITY CASH HANDLING PROCEDURES

COUNTY OF TRINITY CASH HANDLING PROCEDURES Prepared by the Trinity County Auditor/Controller s Office Revised October 1, 2009 TABLE OF CONTENTS I. Introduction--------------------------------------------------------------------1

COUNTY OF TRINITY CASH HANDLING PROCEDURES Prepared by the Trinity County Auditor/Controller s Office Revised October 1, 2009 TABLE OF CONTENTS I. Introduction--------------------------------------------------------------------1

TOWN OF CARLYLE POLICY MANUAL

TOWN OF CARLYLE POLICY MANUAL POLICY DESCRIPTION: POLICY NUMBER: IAC 0010 Internal Accounting Controls DATE APPROVED: March 26, 2008 DATE REVISED: October 12, 2011 Purpose of Policy: To promote and protect

TOWN OF CARLYLE POLICY MANUAL POLICY DESCRIPTION: POLICY NUMBER: IAC 0010 Internal Accounting Controls DATE APPROVED: March 26, 2008 DATE REVISED: October 12, 2011 Purpose of Policy: To promote and protect

FS-06-SF3 School Funds Receipt Log; FS-04-SF2 Schools Funds Payment Request; FS-04-SF1 School Funds: Advance of Funds

Administrative SCHOOL FUNDS Responsibility: Legal References: Related References: Executive Superintendent of Business Services Nil FS-04-SF4 School Funds: Receipts; FS-06-SF3 School Funds Receipt Log;

Administrative SCHOOL FUNDS Responsibility: Legal References: Related References: Executive Superintendent of Business Services Nil FS-04-SF4 School Funds: Receipts; FS-06-SF3 School Funds Receipt Log;

Cash, Petty Cash, Change Funds, and Credit Cards

CASH As public servants, it is our responsibility to safeguard taxpayer s dollars while adhering to laws and regulations governing processes over cash handling. Internal controls over cash are necessary

CASH As public servants, it is our responsibility to safeguard taxpayer s dollars while adhering to laws and regulations governing processes over cash handling. Internal controls over cash are necessary

Chapter 7 Internal Control, Managing Cash, and Making Ethical Judgments 503

Chapter 7 Internal Control, Managing Cash, and Making Ethical Judgments 7 Questions 1. Safeguarding assets is the most fundamental internal control feature because the entity must safeguard its assets

Chapter 7 Internal Control, Managing Cash, and Making Ethical Judgments 7 Questions 1. Safeguarding assets is the most fundamental internal control feature because the entity must safeguard its assets

Pitt County Schools Individual School Accounting. Internal Controls and Responsibilities Fiscal Year 2009-10

Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Contents Page Principal Statement

Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Contents Page Principal Statement

Financial Accounting. John J. Wild. Sixth Edition. McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 06 Reporting and Analyzing Cash and Internal Controls Conceptual

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 06 Reporting and Analyzing Cash and Internal Controls Conceptual

Monitoring of controls Information System Control procedures

Chapter 7 Define internal control Organizational plan and all the related measures to: Congress passed SOX after the Enron and WorldCom scandals 3 4 6 Monitoring of controls Information System Control

Chapter 7 Define internal control Organizational plan and all the related measures to: Congress passed SOX after the Enron and WorldCom scandals 3 4 6 Monitoring of controls Information System Control

Controlling and Reporting Cash

Controlling and Reporting Cash Essential Principles for Safeguarding Cash and Reporting It On Financial Statements Gregory Mostyn, CPA Worthy and James Publishing www.worthyjames.com Controlling and Reporting

Controlling and Reporting Cash Essential Principles for Safeguarding Cash and Reporting It On Financial Statements Gregory Mostyn, CPA Worthy and James Publishing www.worthyjames.com Controlling and Reporting

CHAPTER 9 CASH. Chapter 9. Copyright 2012 The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 9 CASH Chapter Opener: Thinking Critically Office expenditures may include petty cash disbursements for office supplies and postage. Cash expenditures might also include payments for rent and utilities.

CHAPTER 9 CASH Chapter Opener: Thinking Critically Office expenditures may include petty cash disbursements for office supplies and postage. Cash expenditures might also include payments for rent and utilities.

ASSOCIATED STUDENTS, INCORPORATED CALIFORNIA STATE UNIVERSITY, LONG BEACH DATE REVISED: 04/10/2013

Cash Handling BACKGROUND AND PURPOSE...1 POLICY STATEMENT...2 WHO SHOULD KNOW THIS POLICY...2 DEFINITIONS...2 STANDARDS AND PROCEDURES...3 1.0 CONDITIONS FOR EMPLOYMENT IN CASH HANDLING ENVIRONMENT...3

Cash Handling BACKGROUND AND PURPOSE...1 POLICY STATEMENT...2 WHO SHOULD KNOW THIS POLICY...2 DEFINITIONS...2 STANDARDS AND PROCEDURES...3 1.0 CONDITIONS FOR EMPLOYMENT IN CASH HANDLING ENVIRONMENT...3

AAM 50. CASH. AAM 50.010 Treasury Investment (10-09)

") AAM 50. CASH 50.010 Treasury Investment 10/09 50.020 Accountability 10/09 50.030 Control 10/09 50.040 Receipt for Payments 10/09 50.050 Daily Record of Collections 10/09 50.060 Mail Collections 50.070

AAM 50. CASH 50.010 Treasury Investment 10/09 50.020 Accountability 10/09 50.030 Control 10/09 50.040 Receipt for Payments 10/09 50.050 Daily Record of Collections 10/09 50.060 Mail Collections 50.070

Fundamentals of Financial Accounting

Fundamentals of Financial Accounting CHAPTER I Accounting in action. What is accounting? Accounting is the recording of financial transactions plus storing, sorting, retrieving, summarizing, and presenting

Fundamentals of Financial Accounting CHAPTER I Accounting in action. What is accounting? Accounting is the recording of financial transactions plus storing, sorting, retrieving, summarizing, and presenting

Chapter 9. Learning Objectives. Define internal control. Objective 1. Internal Control and Cash

PowerPoint to accompany Chapter 9 Internal Control and Cash Learning Objectives 1. Define internal control 2. Describe good internal control procedures 3. Prepare a bank reconciliation and the related

PowerPoint to accompany Chapter 9 Internal Control and Cash Learning Objectives 1. Define internal control 2. Describe good internal control procedures 3. Prepare a bank reconciliation and the related

FINANCE COMMITTEE PROCEDURES. Audit Process. Cash Handling

1 FINANCE COMMITTEE PROCEDURES Audit Process 1. Internal audits are conducted once a year. 2. The bookkeeper will provide the following information: bank statements, prior year vouchers, and access to

1 FINANCE COMMITTEE PROCEDURES Audit Process 1. Internal audits are conducted once a year. 2. The bookkeeper will provide the following information: bank statements, prior year vouchers, and access to

Accounting for Cash. College Accounting. Heintz & Parry CASH INTERNAL CONTROL OPENING A CHECKING ACCOUNT

Heintz & Parry 0 th Edition Chapter 0 th Edition College Accounting Accounting for Cash CASH INTERNAL CONTROL Includes: Currency, coins, and checking accounts Checks received from customers Money orders

Heintz & Parry 0 th Edition Chapter 0 th Edition College Accounting Accounting for Cash CASH INTERNAL CONTROL Includes: Currency, coins, and checking accounts Checks received from customers Money orders

The policy and procedural guidelines contained in this handbook are designed to:

BASIC POLICY STATEMENT The Mikva Challenge is committed to responsible financial management. The entire organization including the board of directors, administrators, and staff will work together to make

BASIC POLICY STATEMENT The Mikva Challenge is committed to responsible financial management. The entire organization including the board of directors, administrators, and staff will work together to make

Controlling and Reporting Cash

Controlling and Reporting Cash Essential Principles for Safeguarding Cash and Reporting It On Financial Statements Gregory Mostyn, CPA Worthy and James Publishing www.worthyjames.com Controlling and Reporting

Controlling and Reporting Cash Essential Principles for Safeguarding Cash and Reporting It On Financial Statements Gregory Mostyn, CPA Worthy and James Publishing www.worthyjames.com Controlling and Reporting

Vance County Schools Individual School Accounting

Individual School Accounting Internal Controls and Responsibilities Individual School Accounting Internal Controls and Responsibilities Contents Page Principal Statement of Understanding 3 Treasurer Statement

Individual School Accounting Internal Controls and Responsibilities Individual School Accounting Internal Controls and Responsibilities Contents Page Principal Statement of Understanding 3 Treasurer Statement

Income Statements. Accounting for Merchandising Operations

Accounting Principles, 7 th Edition Weygandt Kieso Kimmel Income Statements Accounting for Merchandising Operations Prepared by Naomi Karolinski Monroe Community College and Marianne Bradford Bryant College

Accounting Principles, 7 th Edition Weygandt Kieso Kimmel Income Statements Accounting for Merchandising Operations Prepared by Naomi Karolinski Monroe Community College and Marianne Bradford Bryant College

1501 BANKING RELATIONSHIPS

1501 BANKING RELATIONSHIPS Effective: December 1986 Revised: May 2013 Responsible Office: Treasurer Approval: Treasurer The Vice President for Finance and Treasurer is responsible for the efficient operations

1501 BANKING RELATIONSHIPS Effective: December 1986 Revised: May 2013 Responsible Office: Treasurer Approval: Treasurer The Vice President for Finance and Treasurer is responsible for the efficient operations

LOCAL TRAINING INITIATIVE

Training Standards System LOCAL TRAINING INITIATIVE BOOKS OF ACCOUNT AND RECORD KEEPING Best Practice Guidelines Page 1 of 13 The LTI must comply with public procurement guidelines when purchasing goods

Training Standards System LOCAL TRAINING INITIATIVE BOOKS OF ACCOUNT AND RECORD KEEPING Best Practice Guidelines Page 1 of 13 The LTI must comply with public procurement guidelines when purchasing goods

Department of Sociology Cash Handling Procedures Fiscal Year 2016

Department of Sociology Cash Handling Procedures Fiscal Year 2016 I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving the University, its colleges,

Department of Sociology Cash Handling Procedures Fiscal Year 2016 I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving the University, its colleges,

Appendix. Time Value of Money. Financial Accounting, IFRS Edition Weygandt Kimmel Kieso. Appendix C- 1

C Time Value of Money C- 1 Financial Accounting, IFRS Edition Weygandt Kimmel Kieso C- 2 Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount.

C Time Value of Money C- 1 Financial Accounting, IFRS Edition Weygandt Kimmel Kieso C- 2 Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount.

BUSINESS SERVICES DIVISION PROCEDURES MANUAL REVISED DATE 08/13 CASH HANDLING

BUSINESS SERVICES DIVISION PROCEDURES MANUAL CASH HANDLING REVISED DATE 08/13 When handling money, internal controls ensure resources are guarded against waste, loss, and misuse. Basic principles of internal

BUSINESS SERVICES DIVISION PROCEDURES MANUAL CASH HANDLING REVISED DATE 08/13 When handling money, internal controls ensure resources are guarded against waste, loss, and misuse. Basic principles of internal

CEBU CPAR CENTER M a n d a u e C I t y

1 of 11 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF CASH AND CASH EQUIVALENTS PROBLEM NO. 1 You were able to gather the following from the December 31, 2005 trial balance of Peso

1 of 11 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF CASH AND CASH EQUIVALENTS PROBLEM NO. 1 You were able to gather the following from the December 31, 2005 trial balance of Peso

Unit 2 The Basic Accounting Cycle

Unit 2 The Basic Accounting Cycle Chapter 3 Chapter 4 Chapter 5 Chapter 6 Chapter 7 Chapter 8 Chapter 9 Business Transactions and the Accounting Equation Transactions That Affect Assets, Liabilities, and

Unit 2 The Basic Accounting Cycle Chapter 3 Chapter 4 Chapter 5 Chapter 6 Chapter 7 Chapter 8 Chapter 9 Business Transactions and the Accounting Equation Transactions That Affect Assets, Liabilities, and

CHAPTER 7 - SARBANES-OXLEY, INTERNAL CONTROL, CASH. Material Copyright- Protected: Janice Stoudemire and Barbara wagers

CHAPTER 7 - SARBANES-OXLEY, INTERNAL CONTROL, CASH Material Copyright- Protected: Janice Stoudemire and Barbara wagers Chapter 7 SARBANES-OXLEY, INTERNAL CONTROL, CASH Learning Objectives 1. Sarbanes-Oxley

CHAPTER 7 - SARBANES-OXLEY, INTERNAL CONTROL, CASH Material Copyright- Protected: Janice Stoudemire and Barbara wagers Chapter 7 SARBANES-OXLEY, INTERNAL CONTROL, CASH Learning Objectives 1. Sarbanes-Oxley

POLICY & PROCEDURE DOCUMENT NUMBER: 3.3011. DIVISION: Finance & Administration. TITLE: Cash Operations Policy and Procedures. DATE: July 15, 2011

POLICY & PROCEDURE DOCUMENT NUMBER: 3.3011 DIVISION: Finance & Administration TITLE: Cash Operations Policy and Procedures DATE: July 15, 2011 Authorized by: K. Ann Mead, VP for Finance & Administration

POLICY & PROCEDURE DOCUMENT NUMBER: 3.3011 DIVISION: Finance & Administration TITLE: Cash Operations Policy and Procedures DATE: July 15, 2011 Authorized by: K. Ann Mead, VP for Finance & Administration

Ithaca College Accepting Cash and Checks Procedures

Ithaca College Accepting Cash and Checks Procedures I. Procedure Statement To minimize institutional risk, Ithaca College discourages individual departments from accepting cash and checks on its behalf.

Ithaca College Accepting Cash and Checks Procedures I. Procedure Statement To minimize institutional risk, Ithaca College discourages individual departments from accepting cash and checks on its behalf.

UCLA Policy 360: Internal Control Guidelines for Campus Departments

UCLA Policy 360: Internal Control Guidelines for Campus Departments Issuing Officer: Assistant Vice Chancellor, Corporate Financial Services Responsible Dept: Financial Management Programs Effective Date:

UCLA Policy 360: Internal Control Guidelines for Campus Departments Issuing Officer: Assistant Vice Chancellor, Corporate Financial Services Responsible Dept: Financial Management Programs Effective Date:

ABC Division Cash Handling Procedures Fiscal Year 20XX

ABC Division Cash Handling Procedures Fiscal Year 20XX I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving the University, its colleges, or any departments

ABC Division Cash Handling Procedures Fiscal Year 20XX I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving the University, its colleges, or any departments

ACCOUNTING 105 CONCEPTS REVIEW

ACCOUNTING 105 CONCEPTS REVIEW A note from the tutors: This handout is designed to help you review important information as you study for your cumulative final exam. While it does cover many important

ACCOUNTING 105 CONCEPTS REVIEW A note from the tutors: This handout is designed to help you review important information as you study for your cumulative final exam. While it does cover many important

FINANCIAL CONTROLS POLICIES AND PROCEDURES FOR SMALL NONPROFIT ORGANIZATIONS

By Cindy Cumfer NOTE: These policies and procedures are designed for small nonprofits that do not have an administrator with financial expertise. They are set up to divide the fiscal control roles between

By Cindy Cumfer NOTE: These policies and procedures are designed for small nonprofits that do not have an administrator with financial expertise. They are set up to divide the fiscal control roles between

Agenda. Lecture Chapter 9 Quiz Chapter 8 Exercises & Problem Chapter 8. Objective. Cash Receipts. Cash Receipts, Payments, & Banking Procedures

Cash Receipts, Payments, & Banking Procedures Agenda Lecture Chapter 9 Quiz Chapter 8 Exercises & Problem Chapter 8 Cash Receipts, Payments, & Banking Procedures Objective Cash Receipts 1.cash receipts

Cash Receipts, Payments, & Banking Procedures Agenda Lecture Chapter 9 Quiz Chapter 8 Exercises & Problem Chapter 8 Cash Receipts, Payments, & Banking Procedures Objective Cash Receipts 1.cash receipts

APPENDIX A DRAFT Policy DIE-1 School Funds: Audit & Financial Monitoring Procedures

APPENDIX A DRAFT Policy DIE-1 School Funds: Audit & Financial Monitoring Procedures Administrative Guidelines Financial Monitoring Procedures The following Administrative Guidelines support the Principal

APPENDIX A DRAFT Policy DIE-1 School Funds: Audit & Financial Monitoring Procedures Administrative Guidelines Financial Monitoring Procedures The following Administrative Guidelines support the Principal

Cash Receipt and Banking Internal Controls

Chapter 4 Cash Receipt and Banking Internal Controls A major asset of parishes is its cash and cash equivalents, including marketable securities and other highly liquid assets readily convertible into

Chapter 4 Cash Receipt and Banking Internal Controls A major asset of parishes is its cash and cash equivalents, including marketable securities and other highly liquid assets readily convertible into

Chapter Five: Cash Receipts

Chapter Five: Cash Receipts A. Policies Overview In order to maintain good controls over accounting, the Central Office is responsible for depositing all cash and checks into the operating account. Cash

Chapter Five: Cash Receipts A. Policies Overview In order to maintain good controls over accounting, the Central Office is responsible for depositing all cash and checks into the operating account. Cash

CASH RECONCILIATION & INTERNAL CONTROLS

CASH RECONCILIATION & INTERNAL CONTROLS Montana Clerks, Treasurers & Finance Officers Institute ~ May 2011 Presented by: Brenda Schneider, Superior; Doris Pinkerton, Forsyth & Darla Erickson, Local Government

CASH RECONCILIATION & INTERNAL CONTROLS Montana Clerks, Treasurers & Finance Officers Institute ~ May 2011 Presented by: Brenda Schneider, Superior; Doris Pinkerton, Forsyth & Darla Erickson, Local Government

Cash Receipts, Cash Payments, and Banking Procedures

9-1 McGraw-Hill 2009 The McGraw-Hill Companies, Inc. All rights reserved. Cash Receipts, Cash Payments, and Banking Procedures Section 1: Cash Receipts Section Objectives 1. Record cash receipts in a cash

9-1 McGraw-Hill 2009 The McGraw-Hill Companies, Inc. All rights reserved. Cash Receipts, Cash Payments, and Banking Procedures Section 1: Cash Receipts Section Objectives 1. Record cash receipts in a cash

INTERNAL CONTROL QUESTIONNAIRE OFFICE OF INTERNAL AUDIT UNIVERSITY OF THE VIRGIN ISLANDS

Cabinet Member or Representative responsible for completing this form: INSTRUCTIONS FOR COMPLETING THIS FORM: Answer each question by placing an X in the either the Yes, No,, or Applicable () column. Provide

Cabinet Member or Representative responsible for completing this form: INSTRUCTIONS FOR COMPLETING THIS FORM: Answer each question by placing an X in the either the Yes, No,, or Applicable () column. Provide

Equity The remainder is the shareholders claim on the assets-equity. It is often referred to as residual equity.

ACT 1600 Fundamental of Financial Accounting Chapter 1 The Basic Accounting Equation Asset = Liabilities + Equity Asset Assets are resources a business owns. The common characteristic possessed by all

ACT 1600 Fundamental of Financial Accounting Chapter 1 The Basic Accounting Equation Asset = Liabilities + Equity Asset Assets are resources a business owns. The common characteristic possessed by all

Cash Handling Questionnaire

Cash Handling Questionnaire Internal Control Questionnaire Question Yes No N/A Remarks Because of the relatively high risk associated with transactions involving cash, universities should have a cash management

Cash Handling Questionnaire Internal Control Questionnaire Question Yes No N/A Remarks Because of the relatively high risk associated with transactions involving cash, universities should have a cash management

CR-370 CASH RECEIPTS

CR-370 CASH RECEIPTS 370.1 UNIT DEPOSITING PROCEDURES 370.2 GENERAL INTERNAL POLICIES RELATING TO THE CASHIER 370.3 TIMELY DEPOSITS 370.4 COUNTING THE ENTERPRISE UNIT DEPOSIT 370.5 PREPARING THE BANK DEPOSIT

CR-370 CASH RECEIPTS 370.1 UNIT DEPOSITING PROCEDURES 370.2 GENERAL INTERNAL POLICIES RELATING TO THE CASHIER 370.3 TIMELY DEPOSITS 370.4 COUNTING THE ENTERPRISE UNIT DEPOSIT 370.5 PREPARING THE BANK DEPOSIT

Standard Procedures and Controls for the Title Industry. Prepared by the ALTA Internal Auditing Committee ALTA

Standard Procedures and Controls for the Title Industry Prepared by the ALTA Internal Auditing Committee ALTA The American Land Title Association, founded in 1907, is the national trade association and

Standard Procedures and Controls for the Title Industry Prepared by the ALTA Internal Auditing Committee ALTA The American Land Title Association, founded in 1907, is the national trade association and

BEDFORD PUBLIC SCHOOLS BUSINESS OFFICE PROCEDURES MANUAL

BEDFORD PUBLIC SCHOOLS BUSINESS OFFICE PROCEDURES MANUAL Revised 3-27-2014 TABLE OF CONTENTS Section 1: Section 2: Section 3: Section 4: Section 5: Section 6: Section 7: Section 8: Section 9: Cash Management

BEDFORD PUBLIC SCHOOLS BUSINESS OFFICE PROCEDURES MANUAL Revised 3-27-2014 TABLE OF CONTENTS Section 1: Section 2: Section 3: Section 4: Section 5: Section 6: Section 7: Section 8: Section 9: Cash Management

Accounting Manual for School Activity Funds 2011 V 1.0 Edition

Accounting Manual for School Activity Funds 2011 V 1.0 Edition Office of the Chief Financial Officer 200 East North Avenue, Room 403B Baltimore, MD 21202 Foreward The purpose of this manual is to communicate

Accounting Manual for School Activity Funds 2011 V 1.0 Edition Office of the Chief Financial Officer 200 East North Avenue, Room 403B Baltimore, MD 21202 Foreward The purpose of this manual is to communicate

ADMINISTRATIVE PRACTICE LETTER

ADMINISTRATIVE PRACTICE LETTER SUBJECT: PETTY CASH Section I - E Issue 6 Page 1 of 2 Effective 7/10/07 GENERAL Each petty cash fund is in the sole custody of a business manager who is responsible to the

ADMINISTRATIVE PRACTICE LETTER SUBJECT: PETTY CASH Section I - E Issue 6 Page 1 of 2 Effective 7/10/07 GENERAL Each petty cash fund is in the sole custody of a business manager who is responsible to the

COUNTY OF MENDOCINO CASH CONTROL AND ACCOUNTING STANDARD PRACTICE MANUAL F O R E W O R D

F O R E W O R D This Manual has been developed to provide basic guidance and to standardize operating procedures for all phases of handling cash. The policies and procedures contained in the Manual are

F O R E W O R D This Manual has been developed to provide basic guidance and to standardize operating procedures for all phases of handling cash. The policies and procedures contained in the Manual are

CASH: PETTY CASH DISBURSEMENTS C-173-61 ACCOUNTING MANUAL Page 1 CASH: PETTY CASH DISBURSEMENTS. Contents. II. Establishment of Petty Cash Funds 2

ACCOUNTING MANUAL Page 1 CASH: PETTY CASH DISBURSEMENTS Contents Page I. Introduction 2 II. Establishment of Petty Cash Funds 2 III. Operating Procedures 2 A. Designation of Custodian 2 B. Petty Cash Disbursements

ACCOUNTING MANUAL Page 1 CASH: PETTY CASH DISBURSEMENTS Contents Page I. Introduction 2 II. Establishment of Petty Cash Funds 2 III. Operating Procedures 2 A. Designation of Custodian 2 B. Petty Cash Disbursements

Cash & Check Handling Policy

Cash & Check Handling Policy Effective Date: October 27, 2006 Revised Date: October 31, 2011 Policy Statement This policy sets requirements for the collection and secure processing of coin, currency, checks,

Cash & Check Handling Policy Effective Date: October 27, 2006 Revised Date: October 31, 2011 Policy Statement This policy sets requirements for the collection and secure processing of coin, currency, checks,

ACCOUNTING FOR REVENUE

CHAPTER 4 ACCOUNTING FOR REVENUE SCOPE This chapter provides information on the laws, approved forms, reports, and procedures used in the accounting for revenue received by state agencies. Specific instructions

CHAPTER 4 ACCOUNTING FOR REVENUE SCOPE This chapter provides information on the laws, approved forms, reports, and procedures used in the accounting for revenue received by state agencies. Specific instructions

Deposit of Cash Receipts

Deposit of Cash Receipts Table of Contents 01. Policy Statement... 2 02. Reason for Policy... 2 03. Who Needs to Know This Policy... 2 04. Bonding Requirements... 2 05. Definitions... 2 06. Lockboxes and

Deposit of Cash Receipts Table of Contents 01. Policy Statement... 2 02. Reason for Policy... 2 03. Who Needs to Know This Policy... 2 04. Bonding Requirements... 2 05. Definitions... 2 06. Lockboxes and

INTERNAL ACCOUNTING CONTROLS CHECKLIST FOR NTMA CHAPTERS

P R E C I S I O N INTERNAL ACCOUNTING CONTROLS CHECKLIST FOR NTMA CHAPTERS Presented at NTMA 2004 Annual Convention Palm Springs, CA February 2004 National Tooling & Machining Association 9300 Livingston

P R E C I S I O N INTERNAL ACCOUNTING CONTROLS CHECKLIST FOR NTMA CHAPTERS Presented at NTMA 2004 Annual Convention Palm Springs, CA February 2004 National Tooling & Machining Association 9300 Livingston

CHAPTER 9 Information Unique to Each Fund

CHAPTER 9 Information Unique to Each Fund Table of Contents Section - Page INTRODUCTION 1 1 THE GENERAL FUND 2 1 ASSOCIATED STUDENT BODY FUND (ASB) 3 1 Introduction...1 Accounting Methods and Procedures...2

CHAPTER 9 Information Unique to Each Fund Table of Contents Section - Page INTRODUCTION 1 1 THE GENERAL FUND 2 1 ASSOCIATED STUDENT BODY FUND (ASB) 3 1 Introduction...1 Accounting Methods and Procedures...2

THE CITY OF NEW YORK OFFICE OF THE COMPTROLLER INTERNAL CONTROL AND ACCOUNTABILITY DIRECTIVES

THE CITY OF NEW YORK OFFICE OF THE COMPTROLLER INTERNAL CONTROL AND ACCOUNTABILITY DIRECTIVES DIRECTIVE 11 - CASH ACCOUNTABILITY AND CONTROL INTRODUCTION AND SUMMARY The purpose of this Directive is to

THE CITY OF NEW YORK OFFICE OF THE COMPTROLLER INTERNAL CONTROL AND ACCOUNTABILITY DIRECTIVES DIRECTIVE 11 - CASH ACCOUNTABILITY AND CONTROL INTRODUCTION AND SUMMARY The purpose of this Directive is to

CONCEPTS FOR REVIEW INTERNAL CONTROL AND CASH

INTERNAL CONTROL AND CASH THE NAVIGATOR Understand Concepts for Review Read Feature Story Scan Study Objectives Read Preview Read text and answer Before You Go On p. 296 p. 301 p. 309 Work Demonstration

INTERNAL CONTROL AND CASH THE NAVIGATOR Understand Concepts for Review Read Feature Story Scan Study Objectives Read Preview Read text and answer Before You Go On p. 296 p. 301 p. 309 Work Demonstration

Accounting software & data

Accounting software & data Accounting software and data should reside at church or be webbased where the data base can be accessed by multiple users Multiple people should be trained on software Software

Accounting software & data Accounting software and data should reside at church or be webbased where the data base can be accessed by multiple users Multiple people should be trained on software Software

Appendix C- 1. Time Value of Money. Appendix C- 2. Financial Accounting, Fifth Edition

C- 1 Time Value of Money C- 2 Financial Accounting, Fifth Edition Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount. 3. Solve for future

C- 1 Time Value of Money C- 2 Financial Accounting, Fifth Edition Study Objectives 1. Distinguish between simple and compound interest. 2. Solve for future value of a single amount. 3. Solve for future

WALLA WALLA PUBLIC SCHOOLS ACCOUNTING GUIDELINES

Walla Walla Walla Public Schools Business Office 364 South Park Street Walla Walla WA 99362-3249 FAX (509) 529-7713 (509) 527-3000 WALLA WALLA PUBLIC SCHOOLS ACCOUNTING GUIDELINES Table of Contents I.

Walla Walla Walla Public Schools Business Office 364 South Park Street Walla Walla WA 99362-3249 FAX (509) 529-7713 (509) 527-3000 WALLA WALLA PUBLIC SCHOOLS ACCOUNTING GUIDELINES Table of Contents I.

Audit Guidelines. The Annual Church Audit. by Dan Busby. Key Concepts. Idea! Use this document as a checklist for your annual audit.

The Annual Church Audit by Dan Busby Audit Guidelines Church board members have a long list of responsibilities. Among these is the responsibility for the money that flows through the church. Included

The Annual Church Audit by Dan Busby Audit Guidelines Church board members have a long list of responsibilities. Among these is the responsibility for the money that flows through the church. Included

SECTION 2.05 IMPREST CHECKING ACCOUNTS Contact: Accounting @ Extension 4170

SECTION 2.05 IMPREST CHECKING ACCOUNTS Contact: Accounting @ Extension 4170 A. Overview Imprest checking accounts are District-owned bank accounts operated by schools and departments. These accounts are

SECTION 2.05 IMPREST CHECKING ACCOUNTS Contact: Accounting @ Extension 4170 A. Overview Imprest checking accounts are District-owned bank accounts operated by schools and departments. These accounts are

1. SEGREGATION OF DUTIES IS ESSENTIAL

The way a church handles money can present a positive or negative witness. Churches need to be diligent in handling money to encourage integrity and positive Biblical stewardship. Every step should be

The way a church handles money can present a positive or negative witness. Churches need to be diligent in handling money to encourage integrity and positive Biblical stewardship. Every step should be

TABLE OF CONTENTS CHAPTER 9

TABLE OF CONTENTS CHAPTER 9 Purpose...1 Balance Sheet Accounts...1 Assets...1 Cash...1 Accounts Receivable...2 Accounts Receivable Allowances...4 Loans and Notes Receivable...4 Loans and Notes Allowances...5

TABLE OF CONTENTS CHAPTER 9 Purpose...1 Balance Sheet Accounts...1 Assets...1 Cash...1 Accounts Receivable...2 Accounts Receivable Allowances...4 Loans and Notes Receivable...4 Loans and Notes Allowances...5

State of New York Office of the State Comptroller Division of Management Audit and State Financial Services

State of New York Office of the State Comptroller Division of Management Audit and State Financial Services OFFICE OF MENTAL HEALTH KINGSBORO PSYCHIATRIC CENTER CONTROLS OVER PATIENT CASH REPORT 98-S-43

State of New York Office of the State Comptroller Division of Management Audit and State Financial Services OFFICE OF MENTAL HEALTH KINGSBORO PSYCHIATRIC CENTER CONTROLS OVER PATIENT CASH REPORT 98-S-43

ACCOUNTING POLICIES AND PROCEDURES SAMPLE MANUAL

(Name of Organization & logo) ACCOUNTING POLICIES AND PROCEDURES SAMPLE MANUAL (Date) Note: this sample manual is designed for nonprofit organizations with the following staff involved with accounting

(Name of Organization & logo) ACCOUNTING POLICIES AND PROCEDURES SAMPLE MANUAL (Date) Note: this sample manual is designed for nonprofit organizations with the following staff involved with accounting

5:31-7 Appendix B LOCAL AUTHORITIES - ACCOUNTING AND AUDITING IF ANY ARE NOT APPLICABLE, INSERT N/A AS YOUR ANSWER. FIRE DISTRICT YEAR UNDER AUDIT

5:31-7 Appendix B LOCAL AUTHORITIES - ACCOUNTING AND AUDITING AUDIT QUESTIONNAIRE FOR FIRE DISTRICT AUDITS EACH QUESTION MUST BE ANSWERED. PLEASE CIRCLE YES OR NO. IF ANY ARE NOT APPLICABLE, INSERT N/A

5:31-7 Appendix B LOCAL AUTHORITIES - ACCOUNTING AND AUDITING AUDIT QUESTIONNAIRE FOR FIRE DISTRICT AUDITS EACH QUESTION MUST BE ANSWERED. PLEASE CIRCLE YES OR NO. IF ANY ARE NOT APPLICABLE, INSERT N/A

Cash in bank checking account $22,500 U.S. treasury bills 5,000 Cash on hand 1,350 Undeposited customer checks 1,840 Total $30,690 Requirement 2

Chapter 7 Solutions EXERCISES Exercise 7 2 Cash and cash equivalents includes: Cash in bank checking account $22,500 U.S. treasury bills 5,000 Cash on hand 1,350 Undeposited customer checks 1,840 Total

Chapter 7 Solutions EXERCISES Exercise 7 2 Cash and cash equivalents includes: Cash in bank checking account $22,500 U.S. treasury bills 5,000 Cash on hand 1,350 Undeposited customer checks 1,840 Total

To the Rector, Wardens and Vestry of (Church Name; Church Address; City and Zip)

") Section B. Sample Audit Committee Certificate Date To the Rector, Wardens and Vestry of (Church Name; Church Address; City and Zip) Subject: (Audit Year) Audit of (Church Name) We have inspected the statement

Section B. Sample Audit Committee Certificate Date To the Rector, Wardens and Vestry of (Church Name; Church Address; City and Zip) Subject: (Audit Year) Audit of (Church Name) We have inspected the statement

Cj Debit Bank Sen!~ Charge Ei<pense $60 and ct edit Cesh $60. Cj Debit cash $100 and Cfedit Note Receivable $100.

The bank reconciliation of XYZ Co. is provided below. Demonstrate the entries needed to update the cash account in the general Jedger by selecting the correct answers belo\v XYZCo. Bank Reconciliation

The bank reconciliation of XYZ Co. is provided below. Demonstrate the entries needed to update the cash account in the general Jedger by selecting the correct answers belo\v XYZCo. Bank Reconciliation

Accounting and Administrative Manual Section 100: Accounting and Finance

No.: G-03 Page: 1 of 6 General: The application of good financial management requires the prompt reconciliation of accounts. Since departmental revenue and expenditure accounts are scrutinized monthly

No.: G-03 Page: 1 of 6 General: The application of good financial management requires the prompt reconciliation of accounts. Since departmental revenue and expenditure accounts are scrutinized monthly

06-06 08-06. 4-H Club Officer Handbook. Treasurer

06-06 08-06 4-H Club Officer Handbook Treasurer Treasurer Congratulations! Your fellow club members have selected you to lead them through a successful 4-H year as Treasurer. In case you may have some

06-06 08-06 4-H Club Officer Handbook Treasurer Treasurer Congratulations! Your fellow club members have selected you to lead them through a successful 4-H year as Treasurer. In case you may have some

CASH HANDLING & DEPOSIT GUIDE TEXAS STATE UNIVERSITY STUDENT BUSINESS SERVICES

CASH HANDLING & DEPOSIT GUIDE TEXAS STATE UNIVERSITY STUDENT BUSINESS SERVICES General Overview UPPS 03.01.05 establishes requirements and procedures for the collection and recording of university income,

CASH HANDLING & DEPOSIT GUIDE TEXAS STATE UNIVERSITY STUDENT BUSINESS SERVICES General Overview UPPS 03.01.05 establishes requirements and procedures for the collection and recording of university income,

INTERNATIONAL BANKING AND CASH MANAGEMENT TULANE INTERNATIONAL

INTERNATIONAL BANKING AND CASH MANAGEMENT TULANE INTERNATIONAL RESPONSIBLE TULANE INTERNATIONAL OFFICIAL: Treasurer 1 RESPONSIBLE OFFICE: Tulane International Financial Office COORDINATING DEPARTMENTS:

INTERNATIONAL BANKING AND CASH MANAGEMENT TULANE INTERNATIONAL RESPONSIBLE TULANE INTERNATIONAL OFFICIAL: Treasurer 1 RESPONSIBLE OFFICE: Tulane International Financial Office COORDINATING DEPARTMENTS:

UNT Cash Control and Departmental Deposit Handbook

UNT Cash Control and Departmental Deposit Handbook University of North Texas January 2014 Volume 2, Issue 1 STUDENT ACCOUNTING & UNIVERSITY CASHIERING SERVICES Table of Contents General Overview...1 Proper

UNT Cash Control and Departmental Deposit Handbook University of North Texas January 2014 Volume 2, Issue 1 STUDENT ACCOUNTING & UNIVERSITY CASHIERING SERVICES Table of Contents General Overview...1 Proper

TOPIC NO. 20330 TOPIC PETTY CASH December 2008 Table of Contents

Table of Contents Overview... 3 Introduction... 3 Policy... 3 Non-Routine Purchasing... 3 Routine Purchasing... 3 Small Purchases Charge Card... 3 Use of EDI for Repayment... 3 Definitions... 4 Change

Table of Contents Overview... 3 Introduction... 3 Policy... 3 Non-Routine Purchasing... 3 Routine Purchasing... 3 Small Purchases Charge Card... 3 Use of EDI for Repayment... 3 Definitions... 4 Change

GRAP Implementation Guide for Municipalities

GRAP Implementation Guide for Municipalities TOPIC 2.3: BANK ACCOUNTS AND CASH This section of the manual sets out the FSOP s that need to be executed by the municipality regarding Bank Balances and Cash.

GRAP Implementation Guide for Municipalities TOPIC 2.3: BANK ACCOUNTS AND CASH This section of the manual sets out the FSOP s that need to be executed by the municipality regarding Bank Balances and Cash.

Best Practices for Cash Control

Best Practices for Cash Control The procedures listed below are a list of best practices to accept, store, reconcile and deposit, document, and transport deposits, for cash, checks and payment cards. There

Best Practices for Cash Control The procedures listed below are a list of best practices to accept, store, reconcile and deposit, document, and transport deposits, for cash, checks and payment cards. There

MS 760 Overseas Imprest Management

MS 760 Overseas Imprest Management Effective Date: January 7, 2013 Responsible Office: Office of Chief Financial Officer Supersedes: 5/15/84 V.2; MS 731 Issuance Memo Issuance Memo 01/07/2013 Table of

MS 760 Overseas Imprest Management Effective Date: January 7, 2013 Responsible Office: Office of Chief Financial Officer Supersedes: 5/15/84 V.2; MS 731 Issuance Memo Issuance Memo 01/07/2013 Table of

4. $4,319 Accounts Receivable account in the General Ledger (5 min.) S 8-8

S 8-8") Inventory... 151 Accounts Payable... 201 Jan Marks, Capital... 301 Jan Marks, Drawings... 311 Service Revenue... 411 Depreciation Expense... 531 (5 min.) S 8-4 (5 min.) S 8-7 1. $1,718 Inventory account

Inventory... 151 Accounts Payable... 201 Jan Marks, Capital... 301 Jan Marks, Drawings... 311 Service Revenue... 411 Depreciation Expense... 531 (5 min.) S 8-4 (5 min.) S 8-7 1. $1,718 Inventory account

Cash Operations Manual - Cash Receipts

A. DEFINITION OF CASH Cash Operations Manual - Cash Receipts The term "cash" as used in this manual, refers to U.S. currency and coin, checks drawn on U.S. banks and written in U.S. dollar values (including

A. DEFINITION OF CASH Cash Operations Manual - Cash Receipts The term "cash" as used in this manual, refers to U.S. currency and coin, checks drawn on U.S. banks and written in U.S. dollar values (including

Financial Management Policy

Financial Management Policy POLICY STATEMENT: Hastings Early Intervention Program Inc. is required by the Associations Incorporation Act 2009 to keep proper financial records, ensure financial probity

Financial Management Policy POLICY STATEMENT: Hastings Early Intervention Program Inc. is required by the Associations Incorporation Act 2009 to keep proper financial records, ensure financial probity

Accounting 201 Comprehensive Practice Exam 2C Page 1

Accounting 201 Comprehensive Practice Exam 2C Page 1 1. A business organized as a corporation a. is not a separate legal entity in most states. b. requires that stockholders be personally liable for the

Accounting 201 Comprehensive Practice Exam 2C Page 1 1. A business organized as a corporation a. is not a separate legal entity in most states. b. requires that stockholders be personally liable for the

CANI Financial Policy and Procedures

CANI Financial Policy and Procedures Policy CANI Council is conscious of the need to ensure that all funds received by the organisation are used in accordance with the aims and objectives of CANI; that

CANI Financial Policy and Procedures Policy CANI Council is conscious of the need to ensure that all funds received by the organisation are used in accordance with the aims and objectives of CANI; that

MEMORANDUM INTERNAL CONTROL REQUIREMENTS FOR NON-PROFITS

DIVISION OF CHILD CARE AND EARLY CHILDHOOD EDUCATION HEALTH AND NUTRITION UNIT P O BOX 1437, SLOT S 155 501-320-8982 FAX: 501-682-2334 TDD: 501-682-1550 TO: NON-PROFIT INSTITUTIONS FROM: HEALTH AND NUTRITION

DIVISION OF CHILD CARE AND EARLY CHILDHOOD EDUCATION HEALTH AND NUTRITION UNIT P O BOX 1437, SLOT S 155 501-320-8982 FAX: 501-682-2334 TDD: 501-682-1550 TO: NON-PROFIT INSTITUTIONS FROM: HEALTH AND NUTRITION

ACCT 652 Accounting. Review of last week. Should you always take discounts? 5/17/15. ACCT652 Week 4 1

ACCT 652 Accounting Week 4 Special Journals, Cash, and Internal Controls Some slides Times Mirror Higher Education Division, Inc. Used by permission Michael D. Kinsman, Ph.D. Review of last week Some highlights

ACCT 652 Accounting Week 4 Special Journals, Cash, and Internal Controls Some slides Times Mirror Higher Education Division, Inc. Used by permission Michael D. Kinsman, Ph.D. Review of last week Some highlights

Manual of Accounting Policies and Procedures Bridgewater State College Foundation Bridgewater Alumni Association

Manual of Accounting Policies and Procedures Bridgewater State College Foundation Bridgewater Alumni Association Table of Contents MANUAL OF 1 ACCOUNTING 1 POLICIES AND PROCEDURES 1 BRIDGEWATER STATE COLLEGE

Manual of Accounting Policies and Procedures Bridgewater State College Foundation Bridgewater Alumni Association Table of Contents MANUAL OF 1 ACCOUNTING 1 POLICIES AND PROCEDURES 1 BRIDGEWATER STATE COLLEGE

CASH HANDLING POLICY

COUNTY OF SAN LUIS OBISPO OFFICE OF THE AUDITOR-CONTROLLER CASH HANDLING POLICY Revised September 22, 2008 COUNTY OF SAN LUIS OBISPO OFFICE OF THE AUDITOR-CONTROLLER CASH HANDLING POLICY FORWARD This manual

COUNTY OF SAN LUIS OBISPO OFFICE OF THE AUDITOR-CONTROLLER CASH HANDLING POLICY Revised September 22, 2008 COUNTY OF SAN LUIS OBISPO OFFICE OF THE AUDITOR-CONTROLLER CASH HANDLING POLICY FORWARD This manual