CASH: PETTY CASH DISBURSEMENTS C ACCOUNTING MANUAL Page 1 CASH: PETTY CASH DISBURSEMENTS. Contents. II. Establishment of Petty Cash Funds 2

|

|

|

- Dorothy Melton

- 7 years ago

- Views:

Transcription

1 ACCOUNTING MANUAL Page 1 CASH: PETTY CASH DISBURSEMENTS Contents Page I. Introduction 2 II. Establishment of Petty Cash Funds 2 III. Operating Procedures 2 A. Designation of Custodian 2 B. Petty Cash Disbursements 3 C. Reimbursement of Funds 3 D. Physical Security 3 E. Change in Custody of Fund 4 IV. Internal Control Procedures 4 V. Responsibilities 5 VI. References 5 Exhibit A: Petty Cash Verification Form 6 Exhibit B: Petty Cash Change of Custodian Form 7 TL 79 12/30/98

2 PAGE 2 ACCOUNTING MANUAL CASH: PETTY CASH DISBURSEMENTS I. INTRODUCTION A petty cash fund may be established in a department when there is evidence that a continuing cash advance should be kept on hand to permit the purchase of low-value supplies and services that cannot be purchased under the Low-Value Purchase Authorization procedures. In the absence of such evidence, procurement cards, blanket purchase orders, and miscellaneous blanket authorizations are used to purchase low-value supplies through the Storehouse, Central Duplicating, Central Garage, and other University service departments. Each campus places its own restrictions on the petty cash funds established on its campus, including the amount of cash in the fund and a dollar limit per expenditure. Each fund must be used strictly in accordance with the purpose for which it was authorized. II. ESTABLISHMENT OF PETTY CASH FUNDS The Vice Chancellor - Administration designates the office responsible for authorizing the establishment of petty cash funds, the specified amount of each fund, and the dollar limit per expenditure. III. OPERATING PROCEDURES When a petty cash fund has been authorized for a department, the following operating procedures must be followed: A. DESIGNATION OF CUSTODIAN A custodian of the fund, who is directly responsible for the safekeeping and disbursement of the cash, must be appointed by the department head. The original check written to establish the fund, and checks written to replenish it, are made payable to the custodian of the fund. Written instructions detailing the procedures that must be followed in using petty cash funds should be provided to the custodian. *Change

3 ACCOUNTING MANUAL Page 3 B. PETTY CASH DISBURSEMENTS Expenses paid from a petty cash fund can only be made for the purpose(s) for which the fund was authorized and must be supported by receipts, which should contain the following information: Date of purchase or payment; Name of vendor or other payee; Positive evidence that a payment was made, i.e., a cash register receipt or a handwritten receipt on which the word "Paid" appears; Amount paid; Description of the goods purchased (entered by the vendor if a handwritten receipt is obtained, or by the purchaser if a cash register tape is issued), or of the services provided; and Signature indicating receipt of purchases or services. The total receipts plus the cash on hand must equal the specified amount of the petty cash fund at all times. C. REIMBURSEMENT OF FUNDS Reimbursements made to a fund custodian for petty cash expenditures are based on a Check Request (Non-Payroll), Form U5, which must be supported by purchase receipts. Such requests must be approved for payment by someone with signature authority who is neither the petty cash fund custodian nor an employee who reports to the fund custodian. Reimbursement should be requested as needed, but the fund should always be reimbursed by the end of the fiscal year.

4 ACCOUNTING MANUAL Page 4 III. OPERATING PROCEDURES (Cont.) D. PHYSICAL SECURITY When not in use, the fund's currency must be placed in a safe or a locked receptacle, which is kept in a properly secured area. In the event of a theft, the loss must be reported to the campus police. E. CHANGE IN CUSTODY OF FUND When custody of a petty cash fund is transferred to another custodian, the existing fund should be turned in to the designated officer, and a new check requested for payment to the new custodian. ** As an alternative, if campus procedures do not require that a new check be issued, a Petty Cash Change of Custodian Form (see sample form in Exhibit B) should be completed at the department level and sent to the campus general accounting office. The purpose of this form is to document that the department head has approved the change of custodian, that the total of the cash and the receipts equal the specified amount of the fund, and that the new custodian is aware of his or her specific responsibilities related to custody of the fund. If the fund consists of cash and unreimbursed receipts, a reimbursement check should be requested as outlined in subsection III.C, above, so that the full amount may be turned in to the officer. The department head must notify the accounting officer in writing that the petty cash fund custodian has been changed. IV. INTERNAL CONTROL PROCEDURES A surprise cash count of each petty cash fund, including a review of the documents on hand, must be performed annually, or more frequently if the accounting officer or the head of another campus department determines that this is necessary. The following procedures must be followed: An employee from the accounting office or another campus department must perform the count.

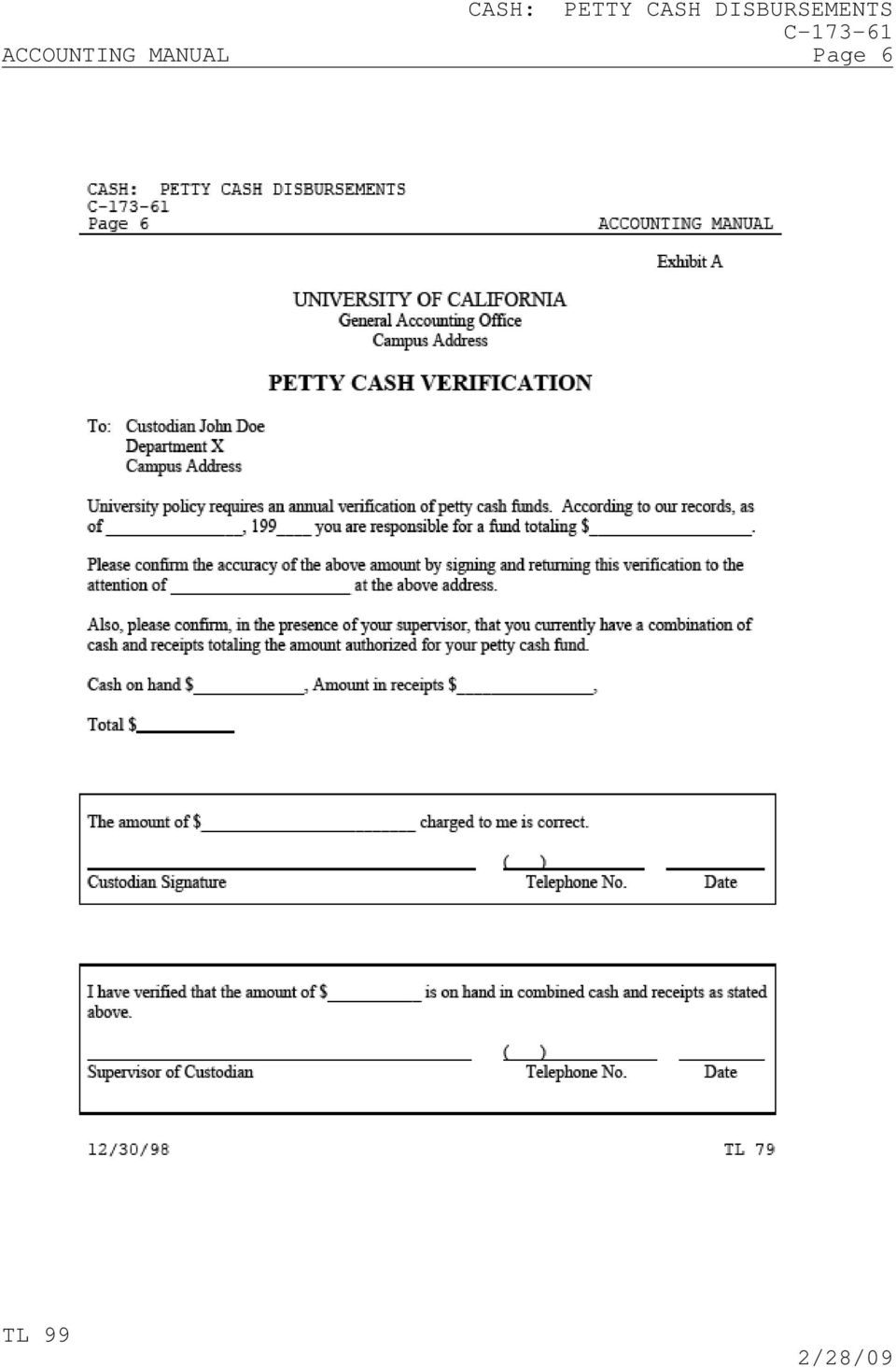

5 ACCOUNTING MANUAL Page 5 The employee should be selected to perform a specified cash count only for this one instance, i.e., the designation should terminate upon completion of the assignment. An employee who is the custodian of other cash, or who reports to, or whose work functions directly relate to, those of the custodian whose cash is to be counted, should not be selected to perform this count. If the cash count is performed by a non-accounting office employee, the results must be reported to the accounting office. Any major discrepancies disclosed by the cash count should be reported to Internal Audit. A petty cash verification letter should be sent to departments when the accounting office is unable to perform a surprise cash count (a sample letter is included as an Exhibit to this chapter). V. RESPONSIBILITIES The accounting office is responsible for reviewing receipt documents provided in support of requests for reimbursement of petty cash expenditures, and for reimbursing the fund custodian. VI. REFERENCES Accounting Manual chapters: D Delegation of Authority--Signature Authorizations Original Accounting Manual chapter first published 6/15/85. Revised 3/31/98, 12/30/98 and ; analyst--john Barrett

6 ACCOUNTING MANUAL Page 6

7 ACCOUNTING MANUAL Page 7

CASH: CASH CONTROLS C-173 ACCOUNTING MANUAL Page 1. Contents. I. Introduction 2. II. General Description of Cash Operations 2

ACCOUNTING MANUAL Page 1 CASH: CASH CONTROLS Contents I. Introduction 2 II. General Description of Cash Operations 2 III. Bank Account Controls 3 A. Regulations Governing Bank Accounts 3 B. Establishment

ACCOUNTING MANUAL Page 1 CASH: CASH CONTROLS Contents I. Introduction 2 II. General Description of Cash Operations 2 III. Bank Account Controls 3 A. Regulations Governing Bank Accounts 3 B. Establishment

DISBURSEMENTS: INVOICE PROCESSING IN RESPONSE TO PURCHASE AUTHORIZATIONS D-371-36 ACCOUNTING MANUAL Page 1

ACCOUNTING MANUAL Page 1 DISBURSEMENTS: INVOICE PROCESSING IN RESPONSE Contents Page I. Introduction 2 II. Definitions 2 III. Sales and Use Taxes 3 IV. Payment of Vendor Invoices -- Special Method 3 V.

ACCOUNTING MANUAL Page 1 DISBURSEMENTS: INVOICE PROCESSING IN RESPONSE Contents Page I. Introduction 2 II. Definitions 2 III. Sales and Use Taxes 3 IV. Payment of Vendor Invoices -- Special Method 3 V.

SECTION 2.05 IMPREST CHECKING ACCOUNTS Contact: Accounting @ Extension 4170

SECTION 2.05 IMPREST CHECKING ACCOUNTS Contact: Accounting @ Extension 4170 A. Overview Imprest checking accounts are District-owned bank accounts operated by schools and departments. These accounts are

SECTION 2.05 IMPREST CHECKING ACCOUNTS Contact: Accounting @ Extension 4170 A. Overview Imprest checking accounts are District-owned bank accounts operated by schools and departments. These accounts are

UCLA Policy 360: Internal Control Guidelines for Campus Departments

UCLA Policy 360: Internal Control Guidelines for Campus Departments Issuing Officer: Assistant Vice Chancellor, Corporate Financial Services Responsible Dept: Financial Management Programs Effective Date:

UCLA Policy 360: Internal Control Guidelines for Campus Departments Issuing Officer: Assistant Vice Chancellor, Corporate Financial Services Responsible Dept: Financial Management Programs Effective Date:

PETTY CASH AND CHANGE FUNDS

PURPOSE To provide procedures and guidance to maintain an adequate system of internal control to protect petty cash and change funds from loss in accordance with ICSUAM Policy and ICSUAM 3103.11. SCOPE

PURPOSE To provide procedures and guidance to maintain an adequate system of internal control to protect petty cash and change funds from loss in accordance with ICSUAM Policy and ICSUAM 3103.11. SCOPE

CASH: DISBURSEMENTS PROCESSING C-173-15.2 ACCOUNTING MANUAL Page 1 CASH: DISBURSEMENTS PROCESSING. Contents

CASH: DISBURSEMENTS PROCESSING ACCOUNTING MANUAL Page 1 CASH: DISBURSEMENTS PROCESSING Contents I. Introduction 2 II. Disbursements Processing 2 Page A. Vendor Payments 2 1. Vendor Checks 2 2. Roles in

CASH: DISBURSEMENTS PROCESSING ACCOUNTING MANUAL Page 1 CASH: DISBURSEMENTS PROCESSING Contents I. Introduction 2 II. Disbursements Processing 2 Page A. Vendor Payments 2 1. Vendor Checks 2 2. Roles in

INTERNATIONAL BANKING AND CASH MANAGEMENT TULANE INTERNATIONAL

INTERNATIONAL BANKING AND CASH MANAGEMENT TULANE INTERNATIONAL RESPONSIBLE TULANE INTERNATIONAL OFFICIAL: Treasurer 1 RESPONSIBLE OFFICE: Tulane International Financial Office COORDINATING DEPARTMENTS:

INTERNATIONAL BANKING AND CASH MANAGEMENT TULANE INTERNATIONAL RESPONSIBLE TULANE INTERNATIONAL OFFICIAL: Treasurer 1 RESPONSIBLE OFFICE: Tulane International Financial Office COORDINATING DEPARTMENTS:

INTERNAL CONTROL QUESTIONNAIRE OFFICE OF INTERNAL AUDIT UNIVERSITY OF THE VIRGIN ISLANDS

Cabinet Member or Representative responsible for completing this form: INSTRUCTIONS FOR COMPLETING THIS FORM: Answer each question by placing an X in the either the Yes, No,, or Applicable () column. Provide

Cabinet Member or Representative responsible for completing this form: INSTRUCTIONS FOR COMPLETING THIS FORM: Answer each question by placing an X in the either the Yes, No,, or Applicable () column. Provide

CASH: CHECK CONTROLS C-173-15 ACCOUNTING MANUAL Page 1 CASH: CHECK CONTROLS. Contents. I. Introduction 2

ACCOUNTING MANUAL Page 1 CASH: CHECK CONTROLS Contents Page I. Introduction 2 II. Procedures for Blank Checks 2 A. Procurement 2 B. Storage 3 C. Blank Check Control Record 4 D. Control of Issuance and

ACCOUNTING MANUAL Page 1 CASH: CHECK CONTROLS Contents Page I. Introduction 2 II. Procedures for Blank Checks 2 A. Procurement 2 B. Storage 3 C. Blank Check Control Record 4 D. Control of Issuance and

FINANCE COMMITTEE PROCEDURES. Audit Process. Cash Handling

1 FINANCE COMMITTEE PROCEDURES Audit Process 1. Internal audits are conducted once a year. 2. The bookkeeper will provide the following information: bank statements, prior year vouchers, and access to

1 FINANCE COMMITTEE PROCEDURES Audit Process 1. Internal audits are conducted once a year. 2. The bookkeeper will provide the following information: bank statements, prior year vouchers, and access to

The policy and procedural guidelines contained in this handbook are designed to:

BASIC POLICY STATEMENT The Mikva Challenge is committed to responsible financial management. The entire organization including the board of directors, administrators, and staff will work together to make

BASIC POLICY STATEMENT The Mikva Challenge is committed to responsible financial management. The entire organization including the board of directors, administrators, and staff will work together to make

Petty Cash Procedure No.: 2007 PR1

Petty Cash No.: 2007 PR1 Policy Reference: N/A Category: Finance and Supply Management Department Responsible: Financial Services Current Approved Date: 2011 Nov 30 Objectives Departments operate petty

Petty Cash No.: 2007 PR1 Policy Reference: N/A Category: Finance and Supply Management Department Responsible: Financial Services Current Approved Date: 2011 Nov 30 Objectives Departments operate petty

Internal Control and Cash

Accounting Principles, 7 th Edition Weygandt Kieso Kimmel Chapter 8 Internal Control and Cash Prepared by Naomi Karolinski Monroe Community College and Marianne Bradford Bryant College John Wiley & Sons,

Accounting Principles, 7 th Edition Weygandt Kieso Kimmel Chapter 8 Internal Control and Cash Prepared by Naomi Karolinski Monroe Community College and Marianne Bradford Bryant College John Wiley & Sons,

Department of Sociology Cash Handling Procedures Fiscal Year 2016

Department of Sociology Cash Handling Procedures Fiscal Year 2016 I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving the University, its colleges,

Department of Sociology Cash Handling Procedures Fiscal Year 2016 I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving the University, its colleges,

Pitt County Schools Individual School Accounting. Internal Controls and Responsibilities Fiscal Year 2009-10

Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Contents Page Principal Statement

Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Contents Page Principal Statement

ABC Division Cash Handling Procedures Fiscal Year 20XX

ABC Division Cash Handling Procedures Fiscal Year 20XX I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving the University, its colleges, or any departments

ABC Division Cash Handling Procedures Fiscal Year 20XX I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving the University, its colleges, or any departments

Caused By 1. Time. 2. Errors. lags $ XXX. but not by bank (e.g., deposits. Add: Deposits recorded by business. Cash balance per bank statement

ILLUSTRATION 8-5 BANK RECONCILIATION FORMAT Balances Should Agree Bank Reconciliation (Date) balance per bank statement Add: Deposits recorded by business but not by bank (e.g., deposits in transit) Less:Charges

ILLUSTRATION 8-5 BANK RECONCILIATION FORMAT Balances Should Agree Bank Reconciliation (Date) balance per bank statement Add: Deposits recorded by business but not by bank (e.g., deposits in transit) Less:Charges

ASSOCIATED STUDENTS, INCORPORATED CALIFORNIA STATE UNIVERSITY, LONG BEACH DATE REVISED: 04/10/2013

Cash Handling BACKGROUND AND PURPOSE...1 POLICY STATEMENT...2 WHO SHOULD KNOW THIS POLICY...2 DEFINITIONS...2 STANDARDS AND PROCEDURES...3 1.0 CONDITIONS FOR EMPLOYMENT IN CASH HANDLING ENVIRONMENT...3

Cash Handling BACKGROUND AND PURPOSE...1 POLICY STATEMENT...2 WHO SHOULD KNOW THIS POLICY...2 DEFINITIONS...2 STANDARDS AND PROCEDURES...3 1.0 CONDITIONS FOR EMPLOYMENT IN CASH HANDLING ENVIRONMENT...3

Office Hours. Telephone Numbers Main: 334 727-8612 Fax: 334 724-4539

GENERAL INFORMATION AP maintains a current listing of University non-payroll obligations (open invoices, pending reimbursements, cash advances, petty cash, and student refunds). AP must also maintain accurate

GENERAL INFORMATION AP maintains a current listing of University non-payroll obligations (open invoices, pending reimbursements, cash advances, petty cash, and student refunds). AP must also maintain accurate

This policy applies to all employees who hold or use petty cash funds, including the security, disbursement, reimbursement and use of these funds.

Policy Number: CS-1001-2013 Policy Title: Petty Cash Fund Policy Policy Owner: Chief Financial Officer Effective Date: April 17, 2013 1. PURPOSE The purpose of Mohawk College s Petty Cash Fund Policy (

Policy Number: CS-1001-2013 Policy Title: Petty Cash Fund Policy Policy Owner: Chief Financial Officer Effective Date: April 17, 2013 1. PURPOSE The purpose of Mohawk College s Petty Cash Fund Policy (

APPENDIX A DRAFT Policy DIE-1 School Funds: Audit & Financial Monitoring Procedures

APPENDIX A DRAFT Policy DIE-1 School Funds: Audit & Financial Monitoring Procedures Administrative Guidelines Financial Monitoring Procedures The following Administrative Guidelines support the Principal

APPENDIX A DRAFT Policy DIE-1 School Funds: Audit & Financial Monitoring Procedures Administrative Guidelines Financial Monitoring Procedures The following Administrative Guidelines support the Principal

AUDIT OF CASH REGISTER, IMPREST FUNDS, AND PETTY CASH TRANSACTIONS JULY 01, 2004 THROUGH JUNE 30, 2005 TABLE OF CONTENTS

AUDIT OF CASH REGISTER, IMPREST FUNDS, AND PETTY CASH TRANSACTIONS JULY 01, 2004 THROUGH JUNE 30, 2005 TABLE OF CONTENTS INTRODUCTION... 1 SCOPE AND OBJECTIVES... 2 METHODOLOGY... 3 SUMMARY OF AUDIT FINDINGS...

AUDIT OF CASH REGISTER, IMPREST FUNDS, AND PETTY CASH TRANSACTIONS JULY 01, 2004 THROUGH JUNE 30, 2005 TABLE OF CONTENTS INTRODUCTION... 1 SCOPE AND OBJECTIVES... 2 METHODOLOGY... 3 SUMMARY OF AUDIT FINDINGS...

Introduction to Accounting 2 Modul 1 Internal Control and Cash

Introduction to Accounting 2 Modul 1 Internal Control and Cash After studying this chapter, you should be able to: 1. Describe the Sarbanes-Oxley Act of 2002 and its impact on internal controls and financial

Introduction to Accounting 2 Modul 1 Internal Control and Cash After studying this chapter, you should be able to: 1. Describe the Sarbanes-Oxley Act of 2002 and its impact on internal controls and financial

COUNTY OF TRINITY CASH HANDLING PROCEDURES

COUNTY OF TRINITY CASH HANDLING PROCEDURES Prepared by the Trinity County Auditor/Controller s Office Revised October 1, 2009 TABLE OF CONTENTS I. Introduction--------------------------------------------------------------------1

COUNTY OF TRINITY CASH HANDLING PROCEDURES Prepared by the Trinity County Auditor/Controller s Office Revised October 1, 2009 TABLE OF CONTENTS I. Introduction--------------------------------------------------------------------1

Purchasing Card Program

Purchasing Card Program User Guidelines University of North Alabama Procurement Department Created: March 2008 / Updated 7/16/2015 University of North Alabama Purchasing Card Program 1 Table of Contents

Purchasing Card Program User Guidelines University of North Alabama Procurement Department Created: March 2008 / Updated 7/16/2015 University of North Alabama Purchasing Card Program 1 Table of Contents

INTERNAL CONTROLS IC INTERNAL SELF-ASSESSMENT IMPREST CHECKING (BANK) ACCOUNTS INTERNAL CONTROLS SELF- ASSESSMENT FOR IMPREST CHECKING (BANK) ACCOUNTS

ACCOUNTS INTERNAL CONTROLS SELF- ASSESSMENT FOR IMPREST CHECKING (BANK) ACCOUNTS") ASSESSMENT TO BE COMPLETED INTERNAL CONTROLS IC INTERNAL CONTROLS SELF-ASSESSMENT The for Imprest Checking (Bank) Accounts was developed as a multipurpose tool to assess a unit s compliance with internal

ASSESSMENT TO BE COMPLETED INTERNAL CONTROLS IC INTERNAL CONTROLS SELF-ASSESSMENT The for Imprest Checking (Bank) Accounts was developed as a multipurpose tool to assess a unit s compliance with internal

Accounting software & data

Accounting software & data Accounting software and data should reside at church or be webbased where the data base can be accessed by multiple users Multiple people should be trained on software Software

Accounting software & data Accounting software and data should reside at church or be webbased where the data base can be accessed by multiple users Multiple people should be trained on software Software

Department of Human Services Client Trust Fund 7290 Trust Accounting System Procedures

Human Services Client Trust Fund 7290 Trust Accounting System Procedures 03.004.00 Effective Date: September 12, 1997 Revised: December 28, 2015 Department of Human Services Client Trust Fund 7290 Trust

Human Services Client Trust Fund 7290 Trust Accounting System Procedures 03.004.00 Effective Date: September 12, 1997 Revised: December 28, 2015 Department of Human Services Client Trust Fund 7290 Trust

MS 760 Overseas Imprest Management

MS 760 Overseas Imprest Management Effective Date: January 7, 2013 Responsible Office: Office of Chief Financial Officer Supersedes: 5/15/84 V.2; MS 731 Issuance Memo Issuance Memo 01/07/2013 Table of

MS 760 Overseas Imprest Management Effective Date: January 7, 2013 Responsible Office: Office of Chief Financial Officer Supersedes: 5/15/84 V.2; MS 731 Issuance Memo Issuance Memo 01/07/2013 Table of

1501 BANKING RELATIONSHIPS

1501 BANKING RELATIONSHIPS Effective: December 1986 Revised: May 2013 Responsible Office: Treasurer Approval: Treasurer The Vice President for Finance and Treasurer is responsible for the efficient operations

1501 BANKING RELATIONSHIPS Effective: December 1986 Revised: May 2013 Responsible Office: Treasurer Approval: Treasurer The Vice President for Finance and Treasurer is responsible for the efficient operations

Ithaca College Accepting Cash and Checks Procedures

Ithaca College Accepting Cash and Checks Procedures I. Procedure Statement To minimize institutional risk, Ithaca College discourages individual departments from accepting cash and checks on its behalf.

Ithaca College Accepting Cash and Checks Procedures I. Procedure Statement To minimize institutional risk, Ithaca College discourages individual departments from accepting cash and checks on its behalf.

ADMINISTRATIVE PRACTICE LETTER

ADMINISTRATIVE PRACTICE LETTER SUBJECT: PETTY CASH Section I - E Issue 6 Page 1 of 2 Effective 7/10/07 GENERAL Each petty cash fund is in the sole custody of a business manager who is responsible to the

ADMINISTRATIVE PRACTICE LETTER SUBJECT: PETTY CASH Section I - E Issue 6 Page 1 of 2 Effective 7/10/07 GENERAL Each petty cash fund is in the sole custody of a business manager who is responsible to the

Imprest Fund Management

Imprest Fund Management 512-471-8802 askus@austin.utexas.edu www.utexas.edu/business/accounting I. Introduction II. III. TABLE OF CONTENTS A. Types of Petty Cash Funds... 1 B. Requesting an Imprest Fund...

Imprest Fund Management 512-471-8802 askus@austin.utexas.edu www.utexas.edu/business/accounting I. Introduction II. III. TABLE OF CONTENTS A. Types of Petty Cash Funds... 1 B. Requesting an Imprest Fund...

Chapter 8. Internal Control. Chapter 8-1

8 Internal Control and Cash 8-1 Internal Control and Cash Internal Control Cash Controls Use of a Bank Reporting Cash The Sarbanes- Oxley Act Principles Limitations Control over cash receipts Control over

8 Internal Control and Cash 8-1 Internal Control and Cash Internal Control Cash Controls Use of a Bank Reporting Cash The Sarbanes- Oxley Act Principles Limitations Control over cash receipts Control over

[Company Name] Accounting Policies and Procedures Manual

![[Company Name] Accounting Policies and Procedures Manual](/thumbs/40/20839575.jpg "[Company Name] Accounting Policies and Procedures Manual") [Company Name] Accounting Policies and Procedures Manual [Company Name] Accounting Policies and Procedures Manual Table of Contents Introduction 1 Division of Duties 2 Cash Receipts Procedures 4 Cash Disbursements

[Company Name] Accounting Policies and Procedures Manual [Company Name] Accounting Policies and Procedures Manual Table of Contents Introduction 1 Division of Duties 2 Cash Receipts Procedures 4 Cash Disbursements

Chapter 7 Fraud, Internal Control, and Cash 高立翰

Chapter 7 Fraud, Internal Control, and Cash 高立翰 Study Objectives 1. Define fraud and internal control. 2. Identify the principles of internal control activities. 3. Explain the applications of internal

Chapter 7 Fraud, Internal Control, and Cash 高立翰 Study Objectives 1. Define fraud and internal control. 2. Identify the principles of internal control activities. 3. Explain the applications of internal

BUSINESS SERVICES DIVISION PROCEDURES MANUAL REVISED DATE 08/13 CASH HANDLING

BUSINESS SERVICES DIVISION PROCEDURES MANUAL CASH HANDLING REVISED DATE 08/13 When handling money, internal controls ensure resources are guarded against waste, loss, and misuse. Basic principles of internal

BUSINESS SERVICES DIVISION PROCEDURES MANUAL CASH HANDLING REVISED DATE 08/13 When handling money, internal controls ensure resources are guarded against waste, loss, and misuse. Basic principles of internal

Vouchers for Reproductive Health Services Project

Vouchers for Reproductive Health Services Project Vouchers for Reproductive Health Services Project ( VMA ) Address: PO Box 585 # 40 F, Corner Street 167 & 426, Sangkat Toul Tom Poung II, Khan Chamkar

Vouchers for Reproductive Health Services Project Vouchers for Reproductive Health Services Project ( VMA ) Address: PO Box 585 # 40 F, Corner Street 167 & 426, Sangkat Toul Tom Poung II, Khan Chamkar

Manual of Accounting Policies and Procedures Bridgewater State College Foundation Bridgewater Alumni Association

Manual of Accounting Policies and Procedures Bridgewater State College Foundation Bridgewater Alumni Association Table of Contents MANUAL OF 1 ACCOUNTING 1 POLICIES AND PROCEDURES 1 BRIDGEWATER STATE COLLEGE

Manual of Accounting Policies and Procedures Bridgewater State College Foundation Bridgewater Alumni Association Table of Contents MANUAL OF 1 ACCOUNTING 1 POLICIES AND PROCEDURES 1 BRIDGEWATER STATE COLLEGE

CASH MANAGEMENT AND CASH HANDLING POLICY CONTENTS POLICY STATEMENT

UT System Administration Policy Library -- Policy UTS166 CASH MANAGEMENT AND CASH HANDLING POLICY Responsible Officer: Associate Vice Chancellor for Finance Sponsoring Office: Office of Finance Effective

UT System Administration Policy Library -- Policy UTS166 CASH MANAGEMENT AND CASH HANDLING POLICY Responsible Officer: Associate Vice Chancellor for Finance Sponsoring Office: Office of Finance Effective

Xx Primary School. Finance Policy

Xx Primary School Finance Policy 1. AIMS 1.1 This document has been adopted by the Governing Body, as the basis for the administration and management of finances. The aim of the policy is to create a framework

Xx Primary School Finance Policy 1. AIMS 1.1 This document has been adopted by the Governing Body, as the basis for the administration and management of finances. The aim of the policy is to create a framework

Cash, Petty Cash, Change Funds, and Credit Cards

CASH As public servants, it is our responsibility to safeguard taxpayer s dollars while adhering to laws and regulations governing processes over cash handling. Internal controls over cash are necessary

CASH As public servants, it is our responsibility to safeguard taxpayer s dollars while adhering to laws and regulations governing processes over cash handling. Internal controls over cash are necessary

DIXON MONTESSORI CHARTER SCHOOL FISCAL CONTROL POLICY

DIXON MONTESSORI CHARTER SCHOOL FISCAL CONTROL POLICY 1. Purpose The Dixon Montessori Charter School Board of Directors ( Board ) has reviewed and adopted the following policies and procedures to ensure

DIXON MONTESSORI CHARTER SCHOOL FISCAL CONTROL POLICY 1. Purpose The Dixon Montessori Charter School Board of Directors ( Board ) has reviewed and adopted the following policies and procedures to ensure

2. The provisions of this chapter do not apply to payroll cheques, which shall be processed as outlined in Chapter 20.

ACCOUNTS PAYABLE AND DISBURSEMENTS INTRODUCTION 1. This chapter contains the policy and procedures relating to accounting and control for Accounts Payable and Disbursements. For ABACIS procedures, see

ACCOUNTS PAYABLE AND DISBURSEMENTS INTRODUCTION 1. This chapter contains the policy and procedures relating to accounting and control for Accounts Payable and Disbursements. For ABACIS procedures, see

Arizona State Real Estate Department

A REPORT TO THE ARIZONA LEGISLATURE Financial Audit Division Procedural Review Arizona State Real Estate Department As of May 16, 2006 Debra K. Davenport Auditor General The Auditor General is appointed

A REPORT TO THE ARIZONA LEGISLATURE Financial Audit Division Procedural Review Arizona State Real Estate Department As of May 16, 2006 Debra K. Davenport Auditor General The Auditor General is appointed

OUR KIDS OF MIAMI-DADE/MONROE, INC. OK Operating NO. 1000-10-007 Revised Date: January 24, 2011 Revised Date: August 25, 2009

OUR KIDS OF MIAMI-DADE/MONROE, INC. OK Operating NO. 1000-10-007 Revised Date: January 24, 2011 Revised Date: August 25, 2009 Our Kids Finance Department Merchant Gift Cards 1. Purpose: This document describes

OUR KIDS OF MIAMI-DADE/MONROE, INC. OK Operating NO. 1000-10-007 Revised Date: January 24, 2011 Revised Date: August 25, 2009 Our Kids Finance Department Merchant Gift Cards 1. Purpose: This document describes

SAMPLE NPO Fiscal Policies & Procedures

SAMPLE NPO NOTE: The most important part of developing policies and procedures is that they are discussed and agreed upon within the organization. This template is designed to be used in conjunction with

SAMPLE NPO NOTE: The most important part of developing policies and procedures is that they are discussed and agreed upon within the organization. This template is designed to be used in conjunction with

Index #: 302.12 Page 1 of 7

State of Alaska Index #: 302.12 Page 1 of 7 Department of Corrections Effective: 04/6/2011 Reviewed: Policies and Procedures Due for Distribution: Public Rev: 04/2013 Chapter: Fiscal Management and Prisoner

State of Alaska Index #: 302.12 Page 1 of 7 Department of Corrections Effective: 04/6/2011 Reviewed: Policies and Procedures Due for Distribution: Public Rev: 04/2013 Chapter: Fiscal Management and Prisoner

PROCEDURES for CAMPUS CASH MANAGEMENT POLICY ADM-0113 California State University, Sacramento. CASH HANDLING Updated February 2014

PROCEDURES for CAMPUS CASH MANAGEMENT POLICY ADM-0113 California State University, Sacramento CASH HANDLING Updated February 2014 I. ACCEPTING UNIVERSITY FUNDS II. III. IV. CASH CHANGE FUNDS SAFEGUARDING

PROCEDURES for CAMPUS CASH MANAGEMENT POLICY ADM-0113 California State University, Sacramento CASH HANDLING Updated February 2014 I. ACCEPTING UNIVERSITY FUNDS II. III. IV. CASH CHANGE FUNDS SAFEGUARDING

FINANCIAL MANAGEMENT POLICIES AND PROCEDURES

FINANCIAL MANAGEMENT POLICIES AND PROCEDURES SAMPLE 1. GENERAL PURPOSE The purpose of these policies is to establish guidelines for developing financial goals and objectives, making financial decisions,

FINANCIAL MANAGEMENT POLICIES AND PROCEDURES SAMPLE 1. GENERAL PURPOSE The purpose of these policies is to establish guidelines for developing financial goals and objectives, making financial decisions,

MANUAL OF PROCEDURE. Miami Dade College Purchasing Card Program. VI-2 Bidding for Commodities and Services VI-3A Minority Business Enterprises

MANUAL OF PROCEDURE PROCEDURE NUMBER: 6520 PAGE 1 of 12 PROCEDURE TITLE: Miami Dade College Purchasing Card Program STATUTORY REFERENCE: FLORIDA STATUTES 1001.65(1) AND 1010.04(2) BASED ON POLICY: VI-2

MANUAL OF PROCEDURE PROCEDURE NUMBER: 6520 PAGE 1 of 12 PROCEDURE TITLE: Miami Dade College Purchasing Card Program STATUTORY REFERENCE: FLORIDA STATUTES 1001.65(1) AND 1010.04(2) BASED ON POLICY: VI-2

THE EVERGREEN STATE COLLEGE

The Evergreen State College Procurement Card Guide JP Morgan Chase VISA THE EVERGREEN STATE COLLEGE PROCUREMENT CARD HANDBOOK For Cardholders & Authorized Users Card Custodians Approving Officials Rev

The Evergreen State College Procurement Card Guide JP Morgan Chase VISA THE EVERGREEN STATE COLLEGE PROCUREMENT CARD HANDBOOK For Cardholders & Authorized Users Card Custodians Approving Officials Rev

Purchasing Card Handbook

Purchasing Card Handbook Contents Purchasing Card Program Overview... 2 Purchasing Card Usage... 2 Purchasing Card contacts... 3 Applying for a PCard... 3 Responsibilities... 3 Cardholder... 3 Cardholder

Purchasing Card Handbook Contents Purchasing Card Program Overview... 2 Purchasing Card Usage... 2 Purchasing Card contacts... 3 Applying for a PCard... 3 Responsibilities... 3 Cardholder... 3 Cardholder

FREQUENTLY ASKED QUESTIONS ABOUT ACCOUNTS PAYABLE WHEN DOES THE STATE OF MARYLAND PAY MY VENDORS?

FREQUENTLY ASKED QUESTIONS ABOUT ACCOUNTS PAYABLE WHEN DOES THE STATE OF MARYLAND PAY MY VENDORS? The state attempts to pay all vendors within 30 days of the Service Date. This is defined as the later

FREQUENTLY ASKED QUESTIONS ABOUT ACCOUNTS PAYABLE WHEN DOES THE STATE OF MARYLAND PAY MY VENDORS? The state attempts to pay all vendors within 30 days of the Service Date. This is defined as the later

INTER-OFFICE CORRESPONDENCE Los Angeles Unified School District Accounting and Disbursements Division

INTER-OFFICE CORRESPONDENCE Los Angeles Unified School District Accounting and Disbursements Division DATE: September 15, 2015 TO: FROM: American Express Business Cardholders District Provided V. Luis

INTER-OFFICE CORRESPONDENCE Los Angeles Unified School District Accounting and Disbursements Division DATE: September 15, 2015 TO: FROM: American Express Business Cardholders District Provided V. Luis

MANUAL OF PROCEDURE. Methodology for the Procurement of Goods and Services Used by the College CHAPTER 6A-14.0262(11), STATE BOARD OF EDUCATION RULES

, STATE BOARD OF EDUCATION RULES") MANUAL OF PROCEDURE PROCEDURE NUMBER: 6000 PAGE 1 of 6 PROCEDURE TITLE: Methodology for the Procurement of Goods and Services Used by the College STATUTORY REFERENCE: FLORIDA STATUTES 1001.65(1) AND 1010.04(2)

MANUAL OF PROCEDURE PROCEDURE NUMBER: 6000 PAGE 1 of 6 PROCEDURE TITLE: Methodology for the Procurement of Goods and Services Used by the College STATUTORY REFERENCE: FLORIDA STATUTES 1001.65(1) AND 1010.04(2)

Fiscal Procedure Sequence page number

Table of Contents Fiscal Procedure Sequence page number Treasurer Responsibilities Maintenance of General Ledger Financial Statements Financial Signature/Review Policy Insurance Protection Payroll Procedures

Table of Contents Fiscal Procedure Sequence page number Treasurer Responsibilities Maintenance of General Ledger Financial Statements Financial Signature/Review Policy Insurance Protection Payroll Procedures

TABLE OF CONTENTS CHAPTER 9

TABLE OF CONTENTS CHAPTER 9 Purpose...1 Balance Sheet Accounts...1 Assets...1 Cash...1 Accounts Receivable...2 Accounts Receivable Allowances...4 Loans and Notes Receivable...4 Loans and Notes Allowances...5

TABLE OF CONTENTS CHAPTER 9 Purpose...1 Balance Sheet Accounts...1 Assets...1 Cash...1 Accounts Receivable...2 Accounts Receivable Allowances...4 Loans and Notes Receivable...4 Loans and Notes Allowances...5

POLICY AND ADMINISTRATIVE PROCEDURE Manual of Policies and Procedures

State of Indiana 1 of POLICY AND ADMINISTRATIVE PROCEDURE Legal References (includes but is not limited to) IC 4-10-11-2 IC 4-13-1-4(7) IC 4-13-2-20 IC 11--2-5(a)() IC 11--2-5(a)(9) 42 IAC 1-5-1 Related

State of Indiana 1 of POLICY AND ADMINISTRATIVE PROCEDURE Legal References (includes but is not limited to) IC 4-10-11-2 IC 4-13-1-4(7) IC 4-13-2-20 IC 11--2-5(a)() IC 11--2-5(a)(9) 42 IAC 1-5-1 Related

Implementation Date: Revised: 4/2005 TABLE OF CONTENTS INTRODUCTION 2 ESTABLISHING CASH COLLECTION DEPARTMENT APPROVAL 3

TABLE OF CONTENTS INTRODUCTION 2 ESTABLISHING CASH COLLECTION DEPARTMENT APPROVAL 3 RECEIPT AND COLLECTION OF CASH 5 Cash Handling Requirements Check Acceptance Methods of Recording Cash Receipts Reconciliation

TABLE OF CONTENTS INTRODUCTION 2 ESTABLISHING CASH COLLECTION DEPARTMENT APPROVAL 3 RECEIPT AND COLLECTION OF CASH 5 Cash Handling Requirements Check Acceptance Methods of Recording Cash Receipts Reconciliation

PAYROLL, PAYABLES AND EXPENDITURES DIVISION EXPENDITURE CONTROL DEPARTMENT

PAYROLL, PAYABLES AND EXPENDITURES DIVISION Summary of Major Accomplishments The Expenditure Control Department consists of two functional areas, the Payroll Section and the Encumbrance and Disbursement

PAYROLL, PAYABLES AND EXPENDITURES DIVISION Summary of Major Accomplishments The Expenditure Control Department consists of two functional areas, the Payroll Section and the Encumbrance and Disbursement

Vance County Schools Individual School Accounting

Individual School Accounting Internal Controls and Responsibilities Individual School Accounting Internal Controls and Responsibilities Contents Page Principal Statement of Understanding 3 Treasurer Statement

Individual School Accounting Internal Controls and Responsibilities Individual School Accounting Internal Controls and Responsibilities Contents Page Principal Statement of Understanding 3 Treasurer Statement

Welcome to Student Organization Banking!

Welcome to Student Organization Banking! Associated Students, Inc. (ASI) Provides banking services to student organizations Invoicing on behalf of student organizations Offers ASI Leadership Funding opportunities

Welcome to Student Organization Banking! Associated Students, Inc. (ASI) Provides banking services to student organizations Invoicing on behalf of student organizations Offers ASI Leadership Funding opportunities

c. Name of Accounts. All accounts of the Association, shall be in the Association s name.

Approved 09/09/13 Financial Policies & Procedures It is the purpose of these financial policies and procedures to provide guidance for all financial activities of Connecticut Junior Soccer Association

Approved 09/09/13 Financial Policies & Procedures It is the purpose of these financial policies and procedures to provide guidance for all financial activities of Connecticut Junior Soccer Association

State of New York Office of the State Comptroller Division of Management Audit and State Financial Services

State of New York Office of the State Comptroller Division of Management Audit and State Financial Services OFFICE OF MENTAL HEALTH KINGSBORO PSYCHIATRIC CENTER CONTROLS OVER PATIENT CASH REPORT 98-S-43

State of New York Office of the State Comptroller Division of Management Audit and State Financial Services OFFICE OF MENTAL HEALTH KINGSBORO PSYCHIATRIC CENTER CONTROLS OVER PATIENT CASH REPORT 98-S-43

PROCEDURE. Accounts Payable

THE RICHARD STOCKTON COLLEGE OF NEW JERSEY PROCEDURE Accounts Payable Procedure Administrator: Associate Vice President for Administration and Finance Authority: N.J.S.A. 18A:64-6 Effective Date: January

THE RICHARD STOCKTON COLLEGE OF NEW JERSEY PROCEDURE Accounts Payable Procedure Administrator: Associate Vice President for Administration and Finance Authority: N.J.S.A. 18A:64-6 Effective Date: January

Accounting Policies and Procedures Manual (Sample)

") Accounting Policies and Procedures Manual (Sample) Table of Contents Introduction General Business Office Staff Revenues and Cash Receipts Sources of Revenues Collecting Offerings Posting Revenues Cash

Accounting Policies and Procedures Manual (Sample) Table of Contents Introduction General Business Office Staff Revenues and Cash Receipts Sources of Revenues Collecting Offerings Posting Revenues Cash

Clare College Financial Policies and Procedures Cash & Banking Procedures

Financial Policies and Procedures Cash & Banking Procedures M:\Bursary\Audit Committee\Financial Procedures -.doc- 1 - Contents 1. Banking Procedures 1.1 Receipt of cash and cheques within a department

Financial Policies and Procedures Cash & Banking Procedures M:\Bursary\Audit Committee\Financial Procedures -.doc- 1 - Contents 1. Banking Procedures 1.1 Receipt of cash and cheques within a department

MEMORANDUM. Municipal Officials. From: Karen Horn, Director, Public Policy and Advocacy; and Abby Friedman, Director, Municipal Assistance Center

MEMORANDUM To: Municipal Officials From: Karen Horn, Director, Public Policy and Advocacy; and Abby Friedman, Director, Municipal Assistance Center 89 Main Street, Suite 4 Montpelier, Vermont 05602-2948

MEMORANDUM To: Municipal Officials From: Karen Horn, Director, Public Policy and Advocacy; and Abby Friedman, Director, Municipal Assistance Center 89 Main Street, Suite 4 Montpelier, Vermont 05602-2948

Deposit of Cash Receipts

Deposit of Cash Receipts Table of Contents 01. Policy Statement... 2 02. Reason for Policy... 2 03. Who Needs to Know This Policy... 2 04. Bonding Requirements... 2 05. Definitions... 2 06. Lockboxes and

Deposit of Cash Receipts Table of Contents 01. Policy Statement... 2 02. Reason for Policy... 2 03. Who Needs to Know This Policy... 2 04. Bonding Requirements... 2 05. Definitions... 2 06. Lockboxes and

CEBU CPAR CENTER M a n d a u e C I t y

1 of 11 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF CASH AND CASH EQUIVALENTS PROBLEM NO. 1 You were able to gather the following from the December 31, 2005 trial balance of Peso

1 of 11 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF CASH AND CASH EQUIVALENTS PROBLEM NO. 1 You were able to gather the following from the December 31, 2005 trial balance of Peso

Or download and view an electronic copy by visiting: www.sarasotagov.com

You can obtain copies of this report by contacting us at: Office of the City Auditor and Clerk 1565 1 st Street Sarasota, FL 34236 (941) 954-4135 Or download and view an electronic copy by visiting: www.sarasotagov.com

You can obtain copies of this report by contacting us at: Office of the City Auditor and Clerk 1565 1 st Street Sarasota, FL 34236 (941) 954-4135 Or download and view an electronic copy by visiting: www.sarasotagov.com

PAYMENT FOR WORKS, GOODS AND SERVICES FINANCIAL PROCEDURE 11

CHIEF FINANCE OFFICER PAYMENT FOR WORKS, GOODS AND SERVICES FINANCIAL PROCEDURE 11 OWNER: HEAD OF FINANCIAL CONTROL Version 2.0 September 2014 FINANCIAL PROCEDURE PAYING FOR WORKS, GOODS AND SERVICES CONTENTS

CHIEF FINANCE OFFICER PAYMENT FOR WORKS, GOODS AND SERVICES FINANCIAL PROCEDURE 11 OWNER: HEAD OF FINANCIAL CONTROL Version 2.0 September 2014 FINANCIAL PROCEDURE PAYING FOR WORKS, GOODS AND SERVICES CONTENTS

Liberty County School District Purchasing Card Procedures

PURCHASING CARD POLICY All purchases made using the Purchasing Card must be for official school business and in accordance with the District procurement code. The card must not be used for personal expenditures

PURCHASING CARD POLICY All purchases made using the Purchasing Card must be for official school business and in accordance with the District procurement code. The card must not be used for personal expenditures

CASH HANDLING & DEPOSIT GUIDE TEXAS STATE UNIVERSITY STUDENT BUSINESS SERVICES

CASH HANDLING & DEPOSIT GUIDE TEXAS STATE UNIVERSITY STUDENT BUSINESS SERVICES General Overview UPPS 03.01.05 establishes requirements and procedures for the collection and recording of university income,

CASH HANDLING & DEPOSIT GUIDE TEXAS STATE UNIVERSITY STUDENT BUSINESS SERVICES General Overview UPPS 03.01.05 establishes requirements and procedures for the collection and recording of university income,

Archdiocese of Chicago Parish Self-Assessment Checklist

Self-Assessment Questions 1. Are written Parish Finance Council guidelines and norms defined, documented, and available to all Parish Finance Council members? 2. Are Archdiocesan best practices communicated

Self-Assessment Questions 1. Are written Parish Finance Council guidelines and norms defined, documented, and available to all Parish Finance Council members? 2. Are Archdiocesan best practices communicated

AAM 50. CASH. AAM 50.010 Treasury Investment (10-09)

") AAM 50. CASH 50.010 Treasury Investment 10/09 50.020 Accountability 10/09 50.030 Control 10/09 50.040 Receipt for Payments 10/09 50.050 Daily Record of Collections 10/09 50.060 Mail Collections 50.070

AAM 50. CASH 50.010 Treasury Investment 10/09 50.020 Accountability 10/09 50.030 Control 10/09 50.040 Receipt for Payments 10/09 50.050 Daily Record of Collections 10/09 50.060 Mail Collections 50.070

FAYETTEVILLE STATE UNIVERSITY ACCOUNTS PAYABLE AND TRAVEL POLICY

FAYETTEVILLE STATE UNIVERSITY ACCOUNTS PAYABLE AND TRAVEL POLICY Authority: Category: Issued by the Chancellor. Changes or exceptions to administrative policies issued by the Chancellor may only be made

FAYETTEVILLE STATE UNIVERSITY ACCOUNTS PAYABLE AND TRAVEL POLICY Authority: Category: Issued by the Chancellor. Changes or exceptions to administrative policies issued by the Chancellor may only be made

Accounts Payable Policies & Guidelines

Accounts Payable Policies & Guidelines Updated July 2014 The following outlines all of the policies and guidelines for the Accounts Payable function at Mount Saint Joseph University. The policies dictate

Accounts Payable Policies & Guidelines Updated July 2014 The following outlines all of the policies and guidelines for the Accounts Payable function at Mount Saint Joseph University. The policies dictate

SAMPLE FINANCIAL PROCEDURES MANUAL

SAMPLE FINANCIAL PROCEDURES MANUAL Approved by (organization s) Board of Directors on (date) I. GENERAL 1. The Board of Directors formulates financial policies, delegates administration of the financial

SAMPLE FINANCIAL PROCEDURES MANUAL Approved by (organization s) Board of Directors on (date) I. GENERAL 1. The Board of Directors formulates financial policies, delegates administration of the financial

FINANCIAL CONTROLS POLICIES AND PROCEDURES FOR SMALL NONPROFIT ORGANIZATIONS

By Cindy Cumfer NOTE: These policies and procedures are designed for small nonprofits that do not have an administrator with financial expertise. They are set up to divide the fiscal control roles between

By Cindy Cumfer NOTE: These policies and procedures are designed for small nonprofits that do not have an administrator with financial expertise. They are set up to divide the fiscal control roles between

Senior Vice President for Administration and Finance and Chief Financial Officer - University Controller s Office (Finance Department).

.") 1 APPROVED BY: Payments to Research Subjects for Incentives/Participation I. Date of Initiation/Revision DATE: May 1, 2009 PAGE: 1 of 5 Initiated: June 1, 2008; Revised: May 1, 2009 II. Policy Classification

1 APPROVED BY: Payments to Research Subjects for Incentives/Participation I. Date of Initiation/Revision DATE: May 1, 2009 PAGE: 1 of 5 Initiated: June 1, 2008; Revised: May 1, 2009 II. Policy Classification

CASH: UNCLAIMED AND UNCASHED CHECKS C-173-78 ACCOUNTING MANUAL Page 1 CASH: UNCLAIMED AND UNCASHED CHECKS I. INTRODUCTION 2 II.

ACCOUNTING MANUAL Page 1 CASH: UNCLAIMED AND UNCASHED CHECKS Contents Page I. INTRODUCTION 2 II. DEFINITIONS 2 III. FOLLOW-UP ACTION 3 IV. TRANSFER OF CHECKS TO OUTSTANDING CHECK ACCOUNTS 5 V. ACCOUNTS

ACCOUNTING MANUAL Page 1 CASH: UNCLAIMED AND UNCASHED CHECKS Contents Page I. INTRODUCTION 2 II. DEFINITIONS 2 III. FOLLOW-UP ACTION 3 IV. TRANSFER OF CHECKS TO OUTSTANDING CHECK ACCOUNTS 5 V. ACCOUNTS

INTERNAL ACCOUNTING CONTROL RECOMMENDATIONS

INTERNAL ACCOUNTING CONTROL RECOMMENDATIONS All moneys collected should be substantiated by pre-numbered receipts, cash register receipts which show cumulative readings, pre-numbered tickets, or other

INTERNAL ACCOUNTING CONTROL RECOMMENDATIONS All moneys collected should be substantiated by pre-numbered receipts, cash register receipts which show cumulative readings, pre-numbered tickets, or other

Fiscal Policies and Procedures Handbook. Crown Preparatory Academy

Fiscal Policies and Procedures Handbook Crown Preparatory Academy TABLE OF CONTENTS Cover Page...i Table of Contents.ii Overview... 1 Annual Financial Audit... 1 Purchasing... 2 Petty Cash... 2 Contracts...

Fiscal Policies and Procedures Handbook Crown Preparatory Academy TABLE OF CONTENTS Cover Page...i Table of Contents.ii Overview... 1 Annual Financial Audit... 1 Purchasing... 2 Petty Cash... 2 Contracts...

Florida A & M University Bank Reconciliation Procedures

TABLE OF CONTENTS 1.0 OVERVIEW...2 2.0 DEFINITIONS...2 3.0 RESPONSIBILITIES..2 4.0 GENERAL PROCEDURES...2 4.1 BANK RECONCILIATIONS.2 4.2 RECORDS 6 1.0 Overview The University currently maintains four bank

TABLE OF CONTENTS 1.0 OVERVIEW...2 2.0 DEFINITIONS...2 3.0 RESPONSIBILITIES..2 4.0 GENERAL PROCEDURES...2 4.1 BANK RECONCILIATIONS.2 4.2 RECORDS 6 1.0 Overview The University currently maintains four bank

THE SCHOOL ADMINISTRATOR

ISSUED BY STATE BOARD OF ACCOUNTS Volume 173 March 2006 ITEMS TO REMEMBER MARCH March 1: March 20: Prove the Fund Ledger and Ledger of Receipts for the month of February to the control of all funds and

ISSUED BY STATE BOARD OF ACCOUNTS Volume 173 March 2006 ITEMS TO REMEMBER MARCH March 1: March 20: Prove the Fund Ledger and Ledger of Receipts for the month of February to the control of all funds and

FIVE MANAGEMENT SYSTEM Policies and Procedures Checklist

FIVE MANAGEMENT SYSTEM Procedures Checklist Provided by: Navajo Nation Office of the Auditor General TABLE OF CONTENTS Introduction.........................................1 General Administrative Procedures...............................1

FIVE MANAGEMENT SYSTEM Procedures Checklist Provided by: Navajo Nation Office of the Auditor General TABLE OF CONTENTS Introduction.........................................1 General Administrative Procedures...............................1

EAST GEORGIA STATE COLLEGE

Approved by President s Cabinet 9-23-14 EAST GEORGIA STATE COLLEGE BUSINESS AFFAIRS POLICIES AND PROCEDURES MANUAL Revised September 16, 2014 Table of Contents Agency Funds 4 General Guidelines 4 Cash

Approved by President s Cabinet 9-23-14 EAST GEORGIA STATE COLLEGE BUSINESS AFFAIRS POLICIES AND PROCEDURES MANUAL Revised September 16, 2014 Table of Contents Agency Funds 4 General Guidelines 4 Cash

PERALTA COMMUNITY COLLEGE DISTRICT CAL CARD VISA PROGRAM ADMINISTRATIVE GUIDELINES

PERALTA COMMUNITY COLLEGE DISTRICT CAL CARD VISA PROGRAM ADMINISTRATIVE GUIDELINES WHAT IS CAL CARD? The Department of General Services, Procurement Division (DGS PD) entered into a Participating Addendum

PERALTA COMMUNITY COLLEGE DISTRICT CAL CARD VISA PROGRAM ADMINISTRATIVE GUIDELINES WHAT IS CAL CARD? The Department of General Services, Procurement Division (DGS PD) entered into a Participating Addendum

REVOLVING FUND CHECKING ACCOUNTS. Revolving fund checking accounts are authorized with payments not to exceed $75.00 per purchase.

BUSINESS SERVICES DIVISION PROCEDURES MANUAL REVOLVING FUND CHECKING ACCOUNTS REVISED DATE 8/03 INTRODUCTION Revolving fund checking accounts are authorized with payments not to exceed $75.00 per purchase.

BUSINESS SERVICES DIVISION PROCEDURES MANUAL REVOLVING FUND CHECKING ACCOUNTS REVISED DATE 8/03 INTRODUCTION Revolving fund checking accounts are authorized with payments not to exceed $75.00 per purchase.

Earlham College - JPMorgan Chase MasterCard Policies and Procedures

1. Program Objective 2. Using the Card 3. Roles & Responsibilities 4. Spending Limits 5. Card Security 6. Lost or Stolen Cards 7. Travel Policy Statement 8. Purchase Ordering Procedures 9. Documentation

1. Program Objective 2. Using the Card 3. Roles & Responsibilities 4. Spending Limits 5. Card Security 6. Lost or Stolen Cards 7. Travel Policy Statement 8. Purchase Ordering Procedures 9. Documentation

Accounting for Cash. College Accounting. Heintz & Parry CASH INTERNAL CONTROL OPENING A CHECKING ACCOUNT

Heintz & Parry 0 th Edition Chapter 0 th Edition College Accounting Accounting for Cash CASH INTERNAL CONTROL Includes: Currency, coins, and checking accounts Checks received from customers Money orders

Heintz & Parry 0 th Edition Chapter 0 th Edition College Accounting Accounting for Cash CASH INTERNAL CONTROL Includes: Currency, coins, and checking accounts Checks received from customers Money orders

Managing Research Subject Payments Draft

UNIVERSITY OF OREGON Managing Research Subject Payments Draft Rob Freytag, Brett Giles, Dan Patten, Martha Schumacher, Teri Rowe, Lynette Schenkel, Beverly Morehouse, Olivia Pierce, Marisa Zuskar THIS

UNIVERSITY OF OREGON Managing Research Subject Payments Draft Rob Freytag, Brett Giles, Dan Patten, Martha Schumacher, Teri Rowe, Lynette Schenkel, Beverly Morehouse, Olivia Pierce, Marisa Zuskar THIS

Ithaca College Purchasing Card Policy

Ithaca College Purchasing Card Policy I. Policy Statement Ithaca College maintains a purchasing card program that allows authorized individuals to make specific, business-related purchases of non-travel

Ithaca College Purchasing Card Policy I. Policy Statement Ithaca College maintains a purchasing card program that allows authorized individuals to make specific, business-related purchases of non-travel

Case Western Reserve University. Payment and Reimbursement Policy. Updated March 26, 2013 Established: March, 1 2008

Case Western Reserve University Payment and Reimbursement Policy Updated March 26, 2013 Established: March, 1 2008 Case Western Reserve University Payment and Reimbursement Policy Full Revision TABLE OF

Case Western Reserve University Payment and Reimbursement Policy Updated March 26, 2013 Established: March, 1 2008 Case Western Reserve University Payment and Reimbursement Policy Full Revision TABLE OF

AP 571 PURCHASING CARD COMMERCIAL CREDIT CARD PROGRAM

AP 571 PURCHASING CARD COMMERCIAL CREDIT CARD PROGRAM BACKGROUND This procedure is for the use and control of purchasing cards (a commercial credit card) for the purpose of obtaining goods and services

AP 571 PURCHASING CARD COMMERCIAL CREDIT CARD PROGRAM BACKGROUND This procedure is for the use and control of purchasing cards (a commercial credit card) for the purpose of obtaining goods and services

New Jersey Commerce and Economic Growth Commission

New Jersey State Legislature Office of Legislative Services Office of the State Auditor New Jersey Commerce and Economic Growth Commission Fiscal Year 2004 Richard L. Fair State Auditor LEGISLATIVE SERVICES

New Jersey State Legislature Office of Legislative Services Office of the State Auditor New Jersey Commerce and Economic Growth Commission Fiscal Year 2004 Richard L. Fair State Auditor LEGISLATIVE SERVICES

Internal Controls and Political Committees

Internal Controls and Political Committees Under the Federal Election Campaign Act (FECA) and the Commission s regulations all political committees are required to file accurate and complete disclosure

Internal Controls and Political Committees Under the Federal Election Campaign Act (FECA) and the Commission s regulations all political committees are required to file accurate and complete disclosure

CASH HANDLING AND REPORTING

CASH HANDLING AND REPORTING A. Purpose The purpose of this policy is to outline procedures for the consistent cash management at The University of Texas Rio Grande Valley (UTRGV). B. Persons Affected This

CASH HANDLING AND REPORTING A. Purpose The purpose of this policy is to outline procedures for the consistent cash management at The University of Texas Rio Grande Valley (UTRGV). B. Persons Affected This