CR-370 CASH RECEIPTS

|

|

|

- Ellen Hope Perry

- 10 years ago

- Views:

Transcription

1 CR-370 CASH RECEIPTS UNIT DEPOSITING PROCEDURES GENERAL INTERNAL POLICIES RELATING TO THE CASHIER TIMELY DEPOSITS COUNTING THE ENTERPRISE UNIT DEPOSIT PREPARING THE BANK DEPOSIT CASHIER S CHANGE FUND POLICY AND PROCEDURES SECURITY OF VAULT AREA & SAFES COMBINATION/KEY(S) FOR SAFE CHECK ACCEPTANCE PROCEDURES RETURNED CHECK PROCESSING COUNTERFEIT CURRENCY SEPARATION OF RESPONSIBILITIES RECORDING TO THE GENERAL LEDGER GIFT PROCESSING & ANNUAL FUND DEPOSITS APPENDICES 370-A Deposit Log 370-B Deposit Transmittal 370-C Cashier s Daily Vault Cash Count Form 370-D Cash Room Authorization List 370-E Deposit Slip 370-F Cash Receipt 370-G Courier Log 370-H Coin Order Form 370-I Change Order Form 1

2 370.1 UNIT DEPOSITING PROCEDURES A. Policy The Foundation CFO has the responsibility for reviewing the procedures for proper accountability of cash receipts. A variation from established procedures requires the prior approval of the CFO. All units must document the deposit of cash and negotiables by obtaining a receipt or copy of the Deposit Transmittal (Appendix 370-B) that indicates the date, amount and initials of the person depositing the cash. Units deposits are to be documented in the cashier s log (Appendix 370-A) by both the depositor and the cashier. Deposits delivered by Dunbar are documented by the copy of the Dunbar record (Appendix 370-G). B. Background The Foundation staff is involved in depositing funds from a variety of operations. Checks should be endorsed immediately upon receipt. In order for the Foundation to deposit these funds, the following procedures are necessary: C. Procedures for Depositing Counted Monies Counted deposits are those that have been counted by the depositing unit prior to being turned in to the Foundation Cashier. These are normally receipts from cash register sales and consist of cash, checks, and credit cards. Fund 4 operations deposit the counted drawer drops. These deposits will be made in the following manner: 1. The Units deposit bags are opened and counted as follows: a. The cash is sorted by denomination. b. The currency, coin and checks are counted and listed on the Deposit Transmittal by denomination. c. When there is enough loose coin to make a full roll it should be wrapped. Checks should be added on a calculator tape by the cashier and scanned through the Desktop Deposit system which submits the checks directly to the bank for payment. Checks are no longer sent to the bank through the Armored car carrier Dunbar for payment. d. The deposit is totaled on the Deposit Transmittal. 2

by both the depositor and the cashier.")

3 2. The over or short amounts are determined as follows: a. Total monies are counted and compared to the Deposit Transmittal. b. In cases where the vault cashier discovers the discrepancy and if the variance is significant ($10.00 or more) the vault cashier will immediately notify the department s unit manager of the discrepancy. c. In cases where the unit discovers the discrepancy and if the variance is ($25.00 or more) the discrepancy should be researched and the unit manager notified. d. Any shortages of cash of ($50.00 or more) must be reported immediately to one of the following: Executive Director or Chief Financial Officer. e. In compliance with Executive Order No. 813 any actual or suspected theft, defalcation, fraud or irregularities, must be reported by the next business day to the following: Executive Director or Chief Financial Officer. 3. The deposit is compiled as follows: a. It should be verified that all remaining items on the Deposit Transmittal have been entered with two signatures, date, name of unit, and amount. b. The cash bag must be sealed when received from the units by the vault cashier. 4. The money is deposited as follows: a. Dunbar picks up cash bags and transports them to the Foundation. b. The deposits transported to the vault by Dunbar are documented by the Dunbar record (Appendix 370-G). Each unit has their own Dunbar record book. Deposits brought down individually will be entered into the logbook and signed by the cashier and depositor. c. Deposits are counted. d. Foundation Accounting will notify the depositing unit of the actual deposit amount by cash receipt. 3

the discrepancy should be researched and the unit manager notified. d. Any shortages of cash of ($50.")

4 e. All Deposit Transmittals and receipts from Accounts Receivable are kept at least 3 full years GENERAL INTERNAL POLICIES RELATING TO THE CASHIER The Cashier s vault change fund will be counted daily before the Cashier leaves at the end of the day. Monies received will be deposited within one working day after receipt by the Cashier TIMELY DEPOSITS The Foundation Vault Cashier may receive deposits in several different ways depending on the type of unit operation. In each case, however, accountability and documentation must be maintained. The appropriate method in which deposits are received and the corresponding Cashier procedures are as follows: A. Dunbar delivers directly from Commercial Units. 1. A completed Deposit Transmittal form must be with the deposits. B. Cashier receives deposit from a non-commercial unit: 1. The depositor presents the deposit slip and funds to the vault cashier. (Appendix 370-E) 2. The cashier verifies the funds and gives the depositor a cash receipt. (Appendix 370-F) C. All departments collecting monies on behalf of the Foundation must deposit the funds in a timely manner, as follows: 1. Projects receiving more than $ per day in cash, check or credit card receipts are required to bring their deposits to the Foundation cashier, the next business day. 2. Projects receiving less than $ per day in cash, check or credit card receipt are required to bring their deposits when they accumulate $100.00, or weekly, whichever comes first, to the Foundation Cashier. 3. Projects are required to deposit all cash, checks and credit card receipt at least weekly, regardless of the amount collected. 4

5 4. If the staff fails to meet any of the above criteria, the Foundation General Accountant will notify the project s manager/staff via with a CC: to the Director of Enterprise Accounting and Project Director. If the delay in depositing funds continues, the Project Director will be notified, with a CC: to the Chief Financial Officer, Executive Director, Director of Enterprise Accounting and Dean (Vice President for Academic Affairs or Administrative Affairs if applicable). If the delay in depositing funds still continues, a meeting will be held with the Project Director(s), Chief Financial Officer, Director of Enterprise Accounting, and Dean (Vice President for Academic Affairs or Administrative Affairs if applicable) to discuss and resolve the issue. 5. A representative making a deposit should always receive a cash receipt from the Foundation Vault Cashier to verify that funds were deposited. 6. Under no circumstances are deposits to be forwarded to the Foundation Vault Cashier s Office through Campus mail COUNTING THE ENTERPRISE UNIT DEPOSIT The counted deposits are normally register sales that have been counted by the depositor and a Deposit Transmittal completed prior to turning it in to the Cashier. A. Procedures for Verifying Pre-counted Commercial Unit Deposits 1. All checks must be endorsed by the cashier. If only one credit card slip is received then a copy needs to be made. 2. The count is verified by denomination and all calculations on the Deposit Transmittal are checked. 3. Any corrections should be noted by a *, with an additional explanation made in the Accounting Use Only block of the Deposit Transmittal. If an over/short or discrepancy is more than $10.00 the Director of Enterprise Accounting should be notified after completion of the deposit and the vault cashier will notify the unit manager. 5

.")

6 370.5 PREPARING THE BANK DEPOSIT A. Campus Center and Bronco Student Center respectively have several bags per unit, which make one deposit each. Other unit s deposits, i.e. Kellogg West, Los Olivos, etc., are treated as individual deposits. An adding machine tape is run on the Deposit Transmittal totals and the cash by denomination. These tapes are attached to the appropriate Deposit Transmittals and forwarded to the Accounting Specialist the same day. B. One set of bank deposit forms is completed for all cash deposits. The Foundation s yellow copy is given to the Accounting Specialist. For checks, an adding machine tape should be run and the total should be entered as the control total in the Desktop Deposit system. Checks are scanned through the system and a deposit confirmation sheet is printed and the total should match the adding machine tape. An adding machine tape of the cash by denomination should be added to the total deposit. The white and pink copies are placed with the deposit money in the deposits bag. The tape of checks and a Deposit Confirmation sheet, and the scanned checks are placed in a separate bag and kept in the safe for 6 months before being destroyed. Loose coin should be put into a coin envelope or small sealed bag. C. The bank deposit bag is sealed. The amount on the bag should always equal the yellow deposit slip total. D. The yellow copies of all the deposit slips should be added together. This amount must agree with the total of the bags. This total should then be logged for the courier pick up. E. When the courier arrives for the daily deposits he signs the log designating the total amount of the day s deposits. (Appendix 370-G) CASHIER S CHANGE FUND POLICY AND PROCEDURES The Cashier s Change Fund is used for providing all necessary cash for authorized register change funds, purchase of coin and necessary cashing of checks. A specific amount is authorized and documented and the Change Fund must always balance to $18,000 in the safe and $30 in the drawer. It is not to be used for any expenditure other than reimbursing other register funds and change. This Change Fund is the only authorized means of providing coin and currency from the cash room without the specific approval of the Director of Enterprise Accounting. It is the Cashier s responsibility to account for all transactions through this fund and maintain the appropriate mix of coin and currency for normal operations. When requesting currency from the bank the coin order limit is $10,000. 6

7 A. Procedure to Order Currency and Coin 1. The Change Fund is inspected daily for checks and any overabundance of certain denominations of coin and currency. The Cashier completes a coin order form (370-H) to order the required denominations of coin and currency. One copy of the Coin Order form is attached to the cashiers daily vault cash count for reconciling the change fund. (Appendix 370-C) 2. The completed Coin Order form is given to the Financial Analyst who will call in the order to the bank by the 10:30 a.m. deadline. B. Receiving Change Order from the Armored Vehicle Courier 1. It must be verified that the correct amount is received immediately while the courier is still in the cash room. C. Preparing Register Banks from Change Fund for Commercial Units 1. The changing of the register bank amount is documented by writing down on the Deposit Transmittal the exact amount (by denomination) going to the Cashier. This amount is for buying back coin and small currency to begin the new register. It is a change fund revolving amount, not part of the deposit. Banks will be made up according to each individual register s specifications. Most units keep their register banks on site in a secured safe. 2. A Change Order form (Appendix 370-I) is completed showing the exact denominations going From Cashier and indicating to whom it goes. The person picking up the register banks must sign the Sign out Log. 3. The Change Order form is placed in the Change Fund as a Cash Out document for later reconciliation. D. Making Change 1. Both sides of a Change Order form are completed, i.e., what monies were given out and what was taken in. 2. The Change Order form is placed with the Change Fund for later reconciliation. E. Personal and Petty Cash Check Cashing Procedure 1. Personal checks of not more than $50.00 will be cashed for currently employed, central office, full-time Foundation employees working in Building #55 by the vault cashier during regular business hours. 7

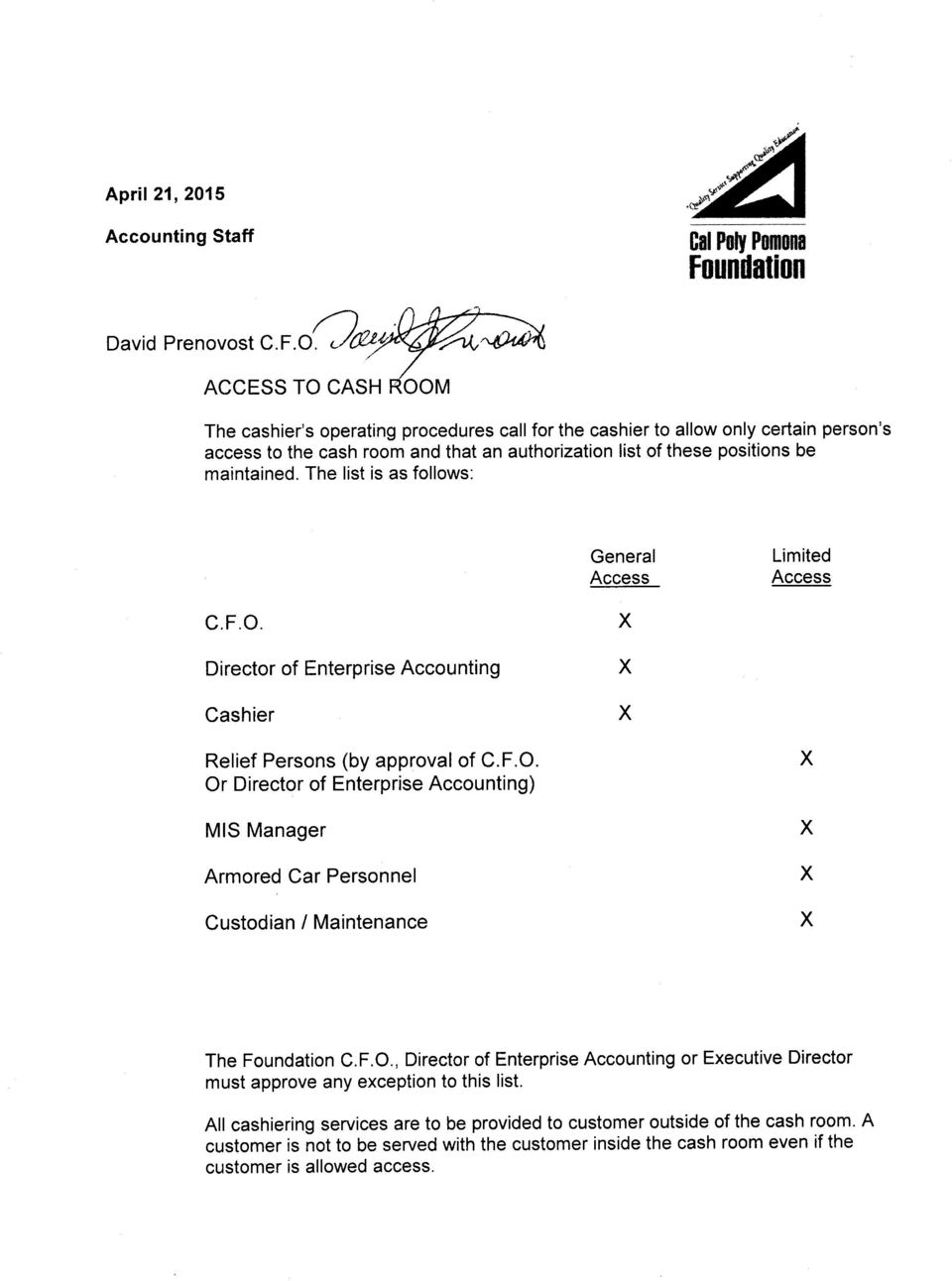

8 2. Foundation issued petty cash reimbursement checks will be cashed by the vault cashier during regular business hours. F. Daily Reconciliation of Vault At the close of business every day, Change Fund monies are counted by the vault cashier and verified by the Director of Enterprise Accounting or his/her designee. Using the Cashier s Daily Cash Count form, the total of cash should equal the Proof total at the bottom of the form: yesterday s cash, plus the coin order received from the bank (Cash In), less cash deposited to pay for today s cash/coin order (Cash Out) SECURITY OF VAULT AREA AND SAFES A. At the close of each business day, the cash vault, Cashier s window, cash room door and all safes must be secured. B. The Director of Enterprise Accounting must be notified if the vault and or safes are left open for any reason. C. All keys and combinations must be continuously safeguarded. D. Only persons on the authorization list are allowed into the cash room (Appendix 370-D). E. The alarm system must be functioning. The red light on the movement sensor should go on when a person passes in front of the beam. The silent alarm button and fire extinguisher should be kept unobstructed at all times COMBINATION/KEY(S) FOR SAFE A. If a vault/safe will be used to hold currency and or checks for a project, the Manager/Director or Authorized Signor or their designee(s) must maintain a record of those individuals with knowledge of the vault/safe combination and/or key(s). In addition, when the combination/key(s) becomes known/available to an excessive number of individuals and/or an individual having knowledge of the combination/key(s) leaves or no longer requires the combination/key(s) in the performance of his or her duties the combination/key(s) must be changed and a record of the date last changed must be kept by the Manager/Director or Authorized Signor or their designee(s). B. An accurate record must be maintained by the Authorized Signor/Project Director, or their designee of when the vault/safe combination and/or key(s) were last changed and the names of persons knowing the present combination or access 8

9 to the key(s) to identify the individuals with this knowledge and the last time the combination/key(s) was changed. C. The vault/safe combination must be changed by the Director of Enterprise Accounting at least once a year CHECK ACCEPTANCE PROCEDURES This section relates to checks presented in payment for goods or services or as a donation to the Foundation. ACCEPTING CHECKS: Subject to limitations or exceptions stated below, checks are accepted by the Foundation in exchange for goods or services provided. A. CONDITIONS FOR ACCEPTANCE: To be accepted, each check presented must: 1. Be payable to the Cal Poly Pomona Foundation Inc. except for a check payable to project with a DBA (Doing Business As) name. 2. Be recently dated - no postdated or stale dated (i.e., dating no earlier than 30 days prior to the day of acceptance), if so the checks will be brought to the attention of the Authorized Signer/Project Director via by the Foundation cashier, see section for further details. 3. Be properly signed or endorsed for deposit only by the presenter. 4. Be in agreement as to numeric and written amounts. 5. Be legibly written in ink or typed. 6. Have Federal Reserve routing codes printed as part of the MICR encoding at the bottom of the check. 7. Not be altered or grossly mutilated. 8. Not have any unreasonable restrictions placed on the face which excessively limit its application. 9. Contain sufficient information to permit tracing the presenter (e.g. address, telephone number, etc.). 9

10 10. Checks and Cash Equivalents bearing the legend Payable/Paid in Full are not to be accepted. Some units may have more restricted policy. B. VERIFYING PRESENTER IDENTIFICATION: IDENTIFICATION REQUIRED -Some form of identification, preferably one having a picture, must be checked to verify the identification of each presenter of a check. NOTE - The Cashier verifying the identification must initial the check. C. RESTRICTIVE ENDORSEMENT AND OTHER INFORMATION REQUIRED: ON ALL CHECKS ACCEPTED -before deposited with the Foundation cashier. All checks must be restrictively endorsed immediately or by the close of each business day. Endorsed check(s) held overnight must be located in a safe or vault in a secure location until deposited with the Foundation. If the total deposit is $100 or more the funds must be deposited in the Foundation the next business day. If the total deposit is less than $100 the funds must be deposited in the Foundation within a week. D. DISCREPANCY BETWEEN NUMERIC AND WRITTEN AMOUNTS: When the numeric and written amounts on a check do not agree, a new check should be requested. If a corrected check cannot be obtained, the check should clear based on the written amount. The written amount is entered above the numeric amount and circled RETURNED CHECK PROCESSING A. Checks may be returned unpaid by the banking system for a number of reasons; the primary causes of returns are non-sufficient funds, account closed and stop payment. Returned checks must be controlled during the process of attempting to collect on the returned amount. B. When the Financial System Department receives a notice of Non-Sufficient Funds (NSF) from the bank, it is forwarded to the Accounts Receivable Specialist in the Accounting Department. With the exception of donations, the Accounts Receivable Specialist will send all NSF checks to the collection agency for collection after 1 year unless otherwise notified by the Authorized Signer/Project Director. The collection agency will send series of letters to request the person/entity to pay the NSF check and all applicable fees to avoid possible actions including credit reporting and legal pursuit of payment. C. NSF checks greater than one year old will be written off with the prior written approval of the Authorized Signer/Project Director and Chief Financial Officer and Executive Director or Associate Director Auxiliary Operations. 10

11 COUNTERFEIT CURRENCY When a counterfeit note is received, the Cashier should: 1. Notify Campus Police by phone to pick up the counterfeit note. 2. Project Director, with a CC: to the Executive Director, Chief Financial Officer, and Director of Enterprise Accounting SEPARATION OF RESPONSIBILITIES A. Separation of duties must be maintained when cash is received. No single person should have complete control over the entire process of receiving, processing applying a payment, preparing the bank deposit and verifying the deposit. B. The Cashier responsible for collecting cash, issuing cash receipts, and preparing the departmental deposit shall be someone other than the person verifying the deposit. Deposit verification is the responsibility of the General Accountant and Director of Enterprise Accounting RECORDING TO THE GENERAL LEDGER A. Bank deposits must be reviewed, approved and recorded to the general ledger in a timely manner. All bank deposits must be accounted for in the general ledger during the appropriate month. B. The Cashier with cash handling responsibilities cannot prepare and post journal entries. The General Accountant is responsible for preparing journal entries. All journal automatic and manual entries must be reviewed, approved, and posted by the Director of Enterprise Accounting or their designee. The preparer and reviewer/approver must be different persons GIFT PROCESSING & ANNUAL FUND DEPOSITS Donations made to the Foundation and the University are processing through the Gift Processing and Annual Fund departments. All donations are recorded in Gift Processing s Viking system. Cash Receipts are produced as follows: 1. Each day donations are made to the Gift Processing department and to the Annual Fund, a deposit transmittal is printed from their system. The cash, checks, and credit card receipts are submitted directly to the Foundation cashier in person. 11

12 2. Each deposit is documented in the cashier s log by both the depositor and the cashier. 3. The cash is sorted by denomination. The currency, coin and checks are counted and listed on the daily cash log. Gift Processing and Annual Fund batches are listed separately so each batch can be verified separately. Checks are already endorsed when deposited. If they are missing endorsement the cashier will stamp them. 4. The amounts of the deposits are verified with the deposit transmittals that are submitted with the deposits by the units. 5. Currency and checks are deposited to the bank as per guidelines specified in section Preparing the Bank Deposit 6. The deposit transmittals are sent to the Accounting Specialist for processing of the cash receipts. 7. The Accounting Specialist will verify cash, check and credit card totals from the deposit transmittal to the cash log and to the credit card batch settlements. 8. Any discrepancies are discussed with the depositing units. 9. The Accounting Specialist processes the batch through the GL and prints the cash receipts. Copies of the receipts are kept by the accounting department and the other set of receipts are sent back to Gift Processing or Annual Fund for their reconciliation. 12

13 13 Last Revised 2/11/2015

14

15

16

17 CAL POLY POMONA FOUNDATION, INC. DEPOSIT SLIP Department: Delivered By: Date: Extension: Prepared By: Authorized Signer Signature: To assist us with our review of this deposit, please provide a detailed description of the revenue, such as purpose, benefit and attach any supporting documents. Please refer to page two of this deposit slip for the types of revenue allowed per Executive Order and the corresponding object codes. Payment Type CA CK CC Project Code Object Code Amount Detailed Description: Total $ * YOU MUST COMPLETE THE ABOVE PRIOR TO DEPOSITING AT THE FOUNDATION'S CASHIER * ** All departments collecting monies on behalf of the Foundation must deposit the funds timely defined as follows: Projects receiving more than $ per day are required to make deposits with the Foundation cashier, the next business day. Projects receiving less than $ per day are required to make deposits when they accumulate $100.00, or weekly, whichever comes first with the Foundation Cashier. Projects are required to deposit all cash and checks at least weekly, regardless of the amount collected. To review foundation cash receipt procedures click this link: Cal Poly Pomona Foundation Inc. CR-370 Revised 2/2011 Page 1 of 2

18

19

20

21 21 Last Revised 2/11/2015

Best Practices for Cash Control

Best Practices for Cash Control The procedures listed below are a list of best practices to accept, store, reconcile and deposit, document, and transport deposits, for cash, checks and payment cards. There

Best Practices for Cash Control The procedures listed below are a list of best practices to accept, store, reconcile and deposit, document, and transport deposits, for cash, checks and payment cards. There

ASSOCIATED STUDENTS, INCORPORATED CALIFORNIA STATE UNIVERSITY, LONG BEACH DATE REVISED: 04/10/2013

Cash Handling BACKGROUND AND PURPOSE...1 POLICY STATEMENT...2 WHO SHOULD KNOW THIS POLICY...2 DEFINITIONS...2 STANDARDS AND PROCEDURES...3 1.0 CONDITIONS FOR EMPLOYMENT IN CASH HANDLING ENVIRONMENT...3

Cash Handling BACKGROUND AND PURPOSE...1 POLICY STATEMENT...2 WHO SHOULD KNOW THIS POLICY...2 DEFINITIONS...2 STANDARDS AND PROCEDURES...3 1.0 CONDITIONS FOR EMPLOYMENT IN CASH HANDLING ENVIRONMENT...3

POLICY & PROCEDURE DOCUMENT NUMBER: 3.3011. DIVISION: Finance & Administration. TITLE: Cash Operations Policy and Procedures. DATE: July 15, 2011

POLICY & PROCEDURE DOCUMENT NUMBER: 3.3011 DIVISION: Finance & Administration TITLE: Cash Operations Policy and Procedures DATE: July 15, 2011 Authorized by: K. Ann Mead, VP for Finance & Administration

POLICY & PROCEDURE DOCUMENT NUMBER: 3.3011 DIVISION: Finance & Administration TITLE: Cash Operations Policy and Procedures DATE: July 15, 2011 Authorized by: K. Ann Mead, VP for Finance & Administration

Bursar s Office Department Cash Receipting Training for Receipt Book, Pre Numbered Tickets and Cash Register Users.

Bursar s Office Department Cash Receipting Training for Receipt Book, Pre Numbered Tickets and Cash Register Users Updated 9/24/15 1 Receipt Book/Pre-numbered Ticket/Cash Register Users Customers of the

Bursar s Office Department Cash Receipting Training for Receipt Book, Pre Numbered Tickets and Cash Register Users Updated 9/24/15 1 Receipt Book/Pre-numbered Ticket/Cash Register Users Customers of the

Ithaca College Accepting Cash and Checks Procedures

Ithaca College Accepting Cash and Checks Procedures I. Procedure Statement To minimize institutional risk, Ithaca College discourages individual departments from accepting cash and checks on its behalf.

Ithaca College Accepting Cash and Checks Procedures I. Procedure Statement To minimize institutional risk, Ithaca College discourages individual departments from accepting cash and checks on its behalf.

UNT Cash Control and Departmental Deposit Handbook

UNT Cash Control and Departmental Deposit Handbook University of North Texas January 2014 Volume 2, Issue 1 STUDENT ACCOUNTING & UNIVERSITY CASHIERING SERVICES Table of Contents General Overview...1 Proper

UNT Cash Control and Departmental Deposit Handbook University of North Texas January 2014 Volume 2, Issue 1 STUDENT ACCOUNTING & UNIVERSITY CASHIERING SERVICES Table of Contents General Overview...1 Proper

Pitt County Schools Individual School Accounting. Internal Controls and Responsibilities Fiscal Year 2009-10

Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Contents Page Principal Statement

Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Contents Page Principal Statement

Vance County Schools Individual School Accounting

Individual School Accounting Internal Controls and Responsibilities Individual School Accounting Internal Controls and Responsibilities Contents Page Principal Statement of Understanding 3 Treasurer Statement

Individual School Accounting Internal Controls and Responsibilities Individual School Accounting Internal Controls and Responsibilities Contents Page Principal Statement of Understanding 3 Treasurer Statement

Department of Sociology Cash Handling Procedures Fiscal Year 2016

Department of Sociology Cash Handling Procedures Fiscal Year 2016 I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving the University, its colleges,

Department of Sociology Cash Handling Procedures Fiscal Year 2016 I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving the University, its colleges,

Draft Version 12 of working document

A. Guarantee that all donations collected by the ushers are delivered intact (as collected) to the count team by supplying pre-numbered tamper resistant bags. The donations are consolidated into one sealed

A. Guarantee that all donations collected by the ushers are delivered intact (as collected) to the count team by supplying pre-numbered tamper resistant bags. The donations are consolidated into one sealed

ABC Division Cash Handling Procedures Fiscal Year 20XX

ABC Division Cash Handling Procedures Fiscal Year 20XX I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving the University, its colleges, or any departments

ABC Division Cash Handling Procedures Fiscal Year 20XX I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving the University, its colleges, or any departments

US Bank Departmental Deposits

US Bank Departmental Deposits Overview: Departments may request approval from the Treasurer s Office to make departmental deposits directly to US Bank. Once approved, the Treasurer s Office will assign

US Bank Departmental Deposits Overview: Departments may request approval from the Treasurer s Office to make departmental deposits directly to US Bank. Once approved, the Treasurer s Office will assign

COUNTY OF TRINITY CASH HANDLING PROCEDURES

COUNTY OF TRINITY CASH HANDLING PROCEDURES Prepared by the Trinity County Auditor/Controller s Office Revised October 1, 2009 TABLE OF CONTENTS I. Introduction--------------------------------------------------------------------1

COUNTY OF TRINITY CASH HANDLING PROCEDURES Prepared by the Trinity County Auditor/Controller s Office Revised October 1, 2009 TABLE OF CONTENTS I. Introduction--------------------------------------------------------------------1

2. Is the mail log prepared by someone who does not participate in any other aspects of the revenue receipts process?

CASH AND CHECK HANDLING SELF ASSESSMENT Because of the relatively high risk associated with transactions involving cash, universities need to have a cash management program to safeguard cash and ensure

CASH AND CHECK HANDLING SELF ASSESSMENT Because of the relatively high risk associated with transactions involving cash, universities need to have a cash management program to safeguard cash and ensure

INSTRUCTIONS FOR PREPARING CASH TRANSMITTALS AND WEB DEPOSITS

INSTRUCTIONS FOR PREPARING CASH TRANSMITTALS AND WEB DEPOSITS It is the responsibility of all individuals receiving money on behalf of the University to be aware of and to comply with the following procedures

INSTRUCTIONS FOR PREPARING CASH TRANSMITTALS AND WEB DEPOSITS It is the responsibility of all individuals receiving money on behalf of the University to be aware of and to comply with the following procedures

TOWN OF CARLYLE POLICY MANUAL

TOWN OF CARLYLE POLICY MANUAL POLICY DESCRIPTION: POLICY NUMBER: IAC 0010 Internal Accounting Controls DATE APPROVED: March 26, 2008 DATE REVISED: October 12, 2011 Purpose of Policy: To promote and protect

TOWN OF CARLYLE POLICY MANUAL POLICY DESCRIPTION: POLICY NUMBER: IAC 0010 Internal Accounting Controls DATE APPROVED: March 26, 2008 DATE REVISED: October 12, 2011 Purpose of Policy: To promote and protect

BUSINESS SERVICES DIVISION PROCEDURES MANUAL REVISED DATE 08/13 CASH HANDLING

BUSINESS SERVICES DIVISION PROCEDURES MANUAL CASH HANDLING REVISED DATE 08/13 When handling money, internal controls ensure resources are guarded against waste, loss, and misuse. Basic principles of internal

BUSINESS SERVICES DIVISION PROCEDURES MANUAL CASH HANDLING REVISED DATE 08/13 When handling money, internal controls ensure resources are guarded against waste, loss, and misuse. Basic principles of internal

Deposit of Cash Receipts

Deposit of Cash Receipts Table of Contents 01. Policy Statement... 2 02. Reason for Policy... 2 03. Who Needs to Know This Policy... 2 04. Bonding Requirements... 2 05. Definitions... 2 06. Lockboxes and

Deposit of Cash Receipts Table of Contents 01. Policy Statement... 2 02. Reason for Policy... 2 03. Who Needs to Know This Policy... 2 04. Bonding Requirements... 2 05. Definitions... 2 06. Lockboxes and

SUMMARY OF CORRECTIVE ACTION FOR SEGREGATION OF DUTIES AUDIT ISSUES

SUMMARY OF CORRECTIVE ACTION FOR SEGREGATION OF DUTIES AUDIT ISSUES CASH MANAGEMENT I. Checks a. All checks are restrictively endorsed, using the endorsement stamp maintained by the building secretary.

SUMMARY OF CORRECTIVE ACTION FOR SEGREGATION OF DUTIES AUDIT ISSUES CASH MANAGEMENT I. Checks a. All checks are restrictively endorsed, using the endorsement stamp maintained by the building secretary.

Cash Operations Manual - Cash Receipts

A. DEFINITION OF CASH Cash Operations Manual - Cash Receipts The term "cash" as used in this manual, refers to U.S. currency and coin, checks drawn on U.S. banks and written in U.S. dollar values (including

A. DEFINITION OF CASH Cash Operations Manual - Cash Receipts The term "cash" as used in this manual, refers to U.S. currency and coin, checks drawn on U.S. banks and written in U.S. dollar values (including

Cash Handling Questionnaire

Cash Handling Questionnaire Internal Control Questionnaire Question Yes No N/A Remarks Because of the relatively high risk associated with transactions involving cash, universities should have a cash management

Cash Handling Questionnaire Internal Control Questionnaire Question Yes No N/A Remarks Because of the relatively high risk associated with transactions involving cash, universities should have a cash management

Chapter 8. Internal Control. Chapter 8-1

8 Internal Control and Cash 8-1 Internal Control and Cash Internal Control Cash Controls Use of a Bank Reporting Cash The Sarbanes- Oxley Act Principles Limitations Control over cash receipts Control over

8 Internal Control and Cash 8-1 Internal Control and Cash Internal Control Cash Controls Use of a Bank Reporting Cash The Sarbanes- Oxley Act Principles Limitations Control over cash receipts Control over

FS-06-SF3 School Funds Receipt Log; FS-04-SF2 Schools Funds Payment Request; FS-04-SF1 School Funds: Advance of Funds

Administrative SCHOOL FUNDS Responsibility: Legal References: Related References: Executive Superintendent of Business Services Nil FS-04-SF4 School Funds: Receipts; FS-06-SF3 School Funds Receipt Log;

Administrative SCHOOL FUNDS Responsibility: Legal References: Related References: Executive Superintendent of Business Services Nil FS-04-SF4 School Funds: Receipts; FS-06-SF3 School Funds Receipt Log;

Cash Handling & Deposit Procedures for Departments

Cash Handling & Deposit Procedures for Departments STUDENT ACCOUNT SERVICES BPSF CA-108 - Finance & Accounting Dated October 2014 Table of Contents Revenue Collection and Deposits Purpose... 1 Introduction...

Cash Handling & Deposit Procedures for Departments STUDENT ACCOUNT SERVICES BPSF CA-108 - Finance & Accounting Dated October 2014 Table of Contents Revenue Collection and Deposits Purpose... 1 Introduction...

TWU CASH RECEIPTS POLICY

TWU CASH RECEIPTS POLICY The TWU Cash Receipts Policy provides procedures and guidelines to all University departments handling cash collections. Procedures have been established to encourage an effective

TWU CASH RECEIPTS POLICY The TWU Cash Receipts Policy provides procedures and guidelines to all University departments handling cash collections. Procedures have been established to encourage an effective

PROCEDURES for CAMPUS CASH MANAGEMENT POLICY ADM-0113 California State University, Sacramento. CASH HANDLING Updated February 2014

PROCEDURES for CAMPUS CASH MANAGEMENT POLICY ADM-0113 California State University, Sacramento CASH HANDLING Updated February 2014 I. ACCEPTING UNIVERSITY FUNDS II. III. IV. CASH CHANGE FUNDS SAFEGUARDING

PROCEDURES for CAMPUS CASH MANAGEMENT POLICY ADM-0113 California State University, Sacramento CASH HANDLING Updated February 2014 I. ACCEPTING UNIVERSITY FUNDS II. III. IV. CASH CHANGE FUNDS SAFEGUARDING

SUBJECT: Cash Handling Policy. Forest Preserve District of Cook County: Employee Handbook Rules of Conduct

POLICY PROCEDURE GUIDELINES POLICY NUMBER: 04.30.00. SUBJECT: Cash Handling Policy PAGE NUMBER: 1 of 7 Adopted: 7/6/2015 Latest Revision: 12/8/2015 Next Review: 04.30.00. POLICY STATEMENT 04.30.01. PURPOSE

POLICY PROCEDURE GUIDELINES POLICY NUMBER: 04.30.00. SUBJECT: Cash Handling Policy PAGE NUMBER: 1 of 7 Adopted: 7/6/2015 Latest Revision: 12/8/2015 Next Review: 04.30.00. POLICY STATEMENT 04.30.01. PURPOSE

Management and Set up for Cash and Credit Card Handling Procedures

Management and Set up for Cash and Credit Card Handling Procedures This presentation is designed to give managers a brief outline of key procedures and controls that should be in place to safeguard cash

Management and Set up for Cash and Credit Card Handling Procedures This presentation is designed to give managers a brief outline of key procedures and controls that should be in place to safeguard cash

Cash Handling Procedures

Introduction Cash Handling Procedures The state of Texas and the University of Houston require that all employees (student employees included) who handle cash for the university complete a cash handling

Introduction Cash Handling Procedures The state of Texas and the University of Houston require that all employees (student employees included) who handle cash for the university complete a cash handling

CASH HANDLING & DEPOSIT GUIDE TEXAS STATE UNIVERSITY STUDENT BUSINESS SERVICES

CASH HANDLING & DEPOSIT GUIDE TEXAS STATE UNIVERSITY STUDENT BUSINESS SERVICES General Overview UPPS 03.01.05 establishes requirements and procedures for the collection and recording of university income,

CASH HANDLING & DEPOSIT GUIDE TEXAS STATE UNIVERSITY STUDENT BUSINESS SERVICES General Overview UPPS 03.01.05 establishes requirements and procedures for the collection and recording of university income,

AAM 50. CASH. AAM 50.010 Treasury Investment (10-09)

") AAM 50. CASH 50.010 Treasury Investment 10/09 50.020 Accountability 10/09 50.030 Control 10/09 50.040 Receipt for Payments 10/09 50.050 Daily Record of Collections 10/09 50.060 Mail Collections 50.070

AAM 50. CASH 50.010 Treasury Investment 10/09 50.020 Accountability 10/09 50.030 Control 10/09 50.040 Receipt for Payments 10/09 50.050 Daily Record of Collections 10/09 50.060 Mail Collections 50.070

Daily Till Reconciliation

1. Remove the till float and print reports 2. Sort the contents of the till drawer Ensure that the till float has been removed from the till Print a Current Report Print a Product Sales Report Commence

1. Remove the till float and print reports 2. Sort the contents of the till drawer Ensure that the till float has been removed from the till Print a Current Report Print a Product Sales Report Commence

CASH HANDLING POLICY

COUNTY OF SAN LUIS OBISPO OFFICE OF THE AUDITOR-CONTROLLER CASH HANDLING POLICY Revised September 22, 2008 COUNTY OF SAN LUIS OBISPO OFFICE OF THE AUDITOR-CONTROLLER CASH HANDLING POLICY FORWARD This manual

COUNTY OF SAN LUIS OBISPO OFFICE OF THE AUDITOR-CONTROLLER CASH HANDLING POLICY Revised September 22, 2008 COUNTY OF SAN LUIS OBISPO OFFICE OF THE AUDITOR-CONTROLLER CASH HANDLING POLICY FORWARD This manual

OFFICIAL CASH HANDLING PROCEDURES FOR DEPARTMENTS, STUDENT FINANCIAL SERVICES, AND ACCOUNTING

Last Updated 7/15/15 OFFICIAL CASH HANDLING PROCEDURES FOR DEPARTMENTS, STUDENT FINANCIAL SERVICES, AND ACCOUNTING To be in compliance with the Cash Handling and Deposits Policy, Departments must also

Last Updated 7/15/15 OFFICIAL CASH HANDLING PROCEDURES FOR DEPARTMENTS, STUDENT FINANCIAL SERVICES, AND ACCOUNTING To be in compliance with the Cash Handling and Deposits Policy, Departments must also

50.P.03: HANDLING CASH, CHECK, CREDIT CARD, AND ACH PAYMENTS

SOP OP: 50.P.03: HANDLING CASH, CHECK, CREDIT CARD, AND ACH PAYMENTS PURPOSE: The purpose of this School of Pharmacy Operating Policy and Procedure (SOP OP) is to establish procedures for handling all

SOP OP: 50.P.03: HANDLING CASH, CHECK, CREDIT CARD, AND ACH PAYMENTS PURPOSE: The purpose of this School of Pharmacy Operating Policy and Procedure (SOP OP) is to establish procedures for handling all

Cash Letter Deposit Service Guide

Cash Letter Deposit Service Guide July 2005 Table of Contents Cash Letter Deposit Service Overview...3 Introduction...3 Cash Letter Pre-Encoded Deposit Workflow...4 Cash Letter Un-Encoded Deposit Workflow...5

Cash Letter Deposit Service Guide July 2005 Table of Contents Cash Letter Deposit Service Overview...3 Introduction...3 Cash Letter Pre-Encoded Deposit Workflow...4 Cash Letter Un-Encoded Deposit Workflow...5

Agenda. Lecture Chapter 9 Quiz Chapter 8 Exercises & Problem Chapter 8. Objective. Cash Receipts. Cash Receipts, Payments, & Banking Procedures

Cash Receipts, Payments, & Banking Procedures Agenda Lecture Chapter 9 Quiz Chapter 8 Exercises & Problem Chapter 8 Cash Receipts, Payments, & Banking Procedures Objective Cash Receipts 1.cash receipts

Cash Receipts, Payments, & Banking Procedures Agenda Lecture Chapter 9 Quiz Chapter 8 Exercises & Problem Chapter 8 Cash Receipts, Payments, & Banking Procedures Objective Cash Receipts 1.cash receipts

1501 BANKING RELATIONSHIPS

1501 BANKING RELATIONSHIPS Effective: December 1986 Revised: May 2013 Responsible Office: Treasurer Approval: Treasurer The Vice President for Finance and Treasurer is responsible for the efficient operations

1501 BANKING RELATIONSHIPS Effective: December 1986 Revised: May 2013 Responsible Office: Treasurer Approval: Treasurer The Vice President for Finance and Treasurer is responsible for the efficient operations

Accounting for Cash. College Accounting. Heintz & Parry CASH INTERNAL CONTROL OPENING A CHECKING ACCOUNT

Heintz & Parry 0 th Edition Chapter 0 th Edition College Accounting Accounting for Cash CASH INTERNAL CONTROL Includes: Currency, coins, and checking accounts Checks received from customers Money orders

Heintz & Parry 0 th Edition Chapter 0 th Edition College Accounting Accounting for Cash CASH INTERNAL CONTROL Includes: Currency, coins, and checking accounts Checks received from customers Money orders

Internal Control and Cash

Accounting Principles, 7 th Edition Weygandt Kieso Kimmel Chapter 8 Internal Control and Cash Prepared by Naomi Karolinski Monroe Community College and Marianne Bradford Bryant College John Wiley & Sons,

Accounting Principles, 7 th Edition Weygandt Kieso Kimmel Chapter 8 Internal Control and Cash Prepared by Naomi Karolinski Monroe Community College and Marianne Bradford Bryant College John Wiley & Sons,

Cash Handling. To successfully complete this course you must score at least 80% on the quiz.

Cash Handling Directions Welcome to the online Cash Handling course for University of Iowa staff members. The content for this online course has been approved by Accounting and Financial Reporting. During

Cash Handling Directions Welcome to the online Cash Handling course for University of Iowa staff members. The content for this online course has been approved by Accounting and Financial Reporting. During

FINANCIAL INFORMATION SYSTEM. Managing Cash Receipts

FINANCIAL INFORMATION SYSTEM Managing Cash Receipts August 2007 Agenda Definition of Cash Receipts Responsibility for Processing Processing Departments Maintaining Cash Security Making Timely Deposit General

FINANCIAL INFORMATION SYSTEM Managing Cash Receipts August 2007 Agenda Definition of Cash Receipts Responsibility for Processing Processing Departments Maintaining Cash Security Making Timely Deposit General

Chapter Five: Cash Receipts

Chapter Five: Cash Receipts A. Policies Overview In order to maintain good controls over accounting, the Central Office is responsible for depositing all cash and checks into the operating account. Cash

Chapter Five: Cash Receipts A. Policies Overview In order to maintain good controls over accounting, the Central Office is responsible for depositing all cash and checks into the operating account. Cash

COUNTY OF MENDOCINO CASH CONTROL AND ACCOUNTING STANDARD PRACTICE MANUAL F O R E W O R D

F O R E W O R D This Manual has been developed to provide basic guidance and to standardize operating procedures for all phases of handling cash. The policies and procedures contained in the Manual are

F O R E W O R D This Manual has been developed to provide basic guidance and to standardize operating procedures for all phases of handling cash. The policies and procedures contained in the Manual are

Cash & Check Handling Policy

Cash & Check Handling Policy Effective Date: October 27, 2006 Revised Date: October 31, 2011 Policy Statement This policy sets requirements for the collection and secure processing of coin, currency, checks,

Cash & Check Handling Policy Effective Date: October 27, 2006 Revised Date: October 31, 2011 Policy Statement This policy sets requirements for the collection and secure processing of coin, currency, checks,

COMMUNITY EDUCATION Department Summary Transactions Summary Internal Controls of Cash Receipts

COMMUNITY EDUCATION Department Summary Community Education provides quality programs and services for more than 25,000 residents of our community and beyond each year. Programs include Adult Education

COMMUNITY EDUCATION Department Summary Community Education provides quality programs and services for more than 25,000 residents of our community and beyond each year. Programs include Adult Education

FINANCIAL CONTROLS POLICIES AND PROCEDURES FOR SMALL NONPROFIT ORGANIZATIONS

By Cindy Cumfer NOTE: These policies and procedures are designed for small nonprofits that do not have an administrator with financial expertise. They are set up to divide the fiscal control roles between

By Cindy Cumfer NOTE: These policies and procedures are designed for small nonprofits that do not have an administrator with financial expertise. They are set up to divide the fiscal control roles between

ADMINISTRATIVE PRACTICE LETTER

ADMINISTRATIVE PRACTICE LETTER SUBJECT: PETTY CASH Section I - E Issue 6 Page 1 of 2 Effective 7/10/07 GENERAL Each petty cash fund is in the sole custody of a business manager who is responsible to the

ADMINISTRATIVE PRACTICE LETTER SUBJECT: PETTY CASH Section I - E Issue 6 Page 1 of 2 Effective 7/10/07 GENERAL Each petty cash fund is in the sole custody of a business manager who is responsible to the

Unit 2 The Basic Accounting Cycle

Unit 2 The Basic Accounting Cycle Chapter 3 Chapter 4 Chapter 5 Chapter 6 Chapter 7 Chapter 8 Chapter 9 Business Transactions and the Accounting Equation Transactions That Affect Assets, Liabilities, and

Unit 2 The Basic Accounting Cycle Chapter 3 Chapter 4 Chapter 5 Chapter 6 Chapter 7 Chapter 8 Chapter 9 Business Transactions and the Accounting Equation Transactions That Affect Assets, Liabilities, and

MINIMUM INTERNAL CONTROLS FOR RACETRACK GAMING OPERATORS

NEW MEXICO GAMING CONTROL BOARD MINIMUM INTERNAL CONTROLS FOR RACETRACK GAMING OPERATORS 4900 Alameda Boulevard, NE Albuquerque, NM 87113 Phone 505.841.9700 Fax 505.841.9720 Effective 02/28/2005 i Table

NEW MEXICO GAMING CONTROL BOARD MINIMUM INTERNAL CONTROLS FOR RACETRACK GAMING OPERATORS 4900 Alameda Boulevard, NE Albuquerque, NM 87113 Phone 505.841.9700 Fax 505.841.9720 Effective 02/28/2005 i Table

Oklahoma State University Policy and Procedures

Oklahoma State University Policy and Procedures COLLECTIONS, DEPOSIT AND CONTROL OF CASH OR CHECKS RECEIVED IN THE NAME OF OKLAHOMA STATE UNIVERSITY 3-0331 ADMINISTRATION & FINANCE May 2008 POLICY AND

Oklahoma State University Policy and Procedures COLLECTIONS, DEPOSIT AND CONTROL OF CASH OR CHECKS RECEIVED IN THE NAME OF OKLAHOMA STATE UNIVERSITY 3-0331 ADMINISTRATION & FINANCE May 2008 POLICY AND

Index #: 302.12 Page 1 of 7

State of Alaska Index #: 302.12 Page 1 of 7 Department of Corrections Effective: 04/6/2011 Reviewed: Policies and Procedures Due for Distribution: Public Rev: 04/2013 Chapter: Fiscal Management and Prisoner

State of Alaska Index #: 302.12 Page 1 of 7 Department of Corrections Effective: 04/6/2011 Reviewed: Policies and Procedures Due for Distribution: Public Rev: 04/2013 Chapter: Fiscal Management and Prisoner

Chapter 7 Fraud, Internal Control, and Cash 高立翰

Chapter 7 Fraud, Internal Control, and Cash 高立翰 Study Objectives 1. Define fraud and internal control. 2. Identify the principles of internal control activities. 3. Explain the applications of internal

Chapter 7 Fraud, Internal Control, and Cash 高立翰 Study Objectives 1. Define fraud and internal control. 2. Identify the principles of internal control activities. 3. Explain the applications of internal

CASH MANAGEMENT AND CASH HANDLING POLICY CONTENTS POLICY STATEMENT

UT System Administration Policy Library -- Policy UTS166 CASH MANAGEMENT AND CASH HANDLING POLICY Responsible Officer: Associate Vice Chancellor for Finance Sponsoring Office: Office of Finance Effective

UT System Administration Policy Library -- Policy UTS166 CASH MANAGEMENT AND CASH HANDLING POLICY Responsible Officer: Associate Vice Chancellor for Finance Sponsoring Office: Office of Finance Effective

Cash Handling Policies & Procedures Revised February 11, 2008

Cash Handling Policies & Procedures Revised February 11, 2008 Table of Contents POLICY - CASH COLLECTION AND DEPOSIT 1 Purpose... 1 Introduction... 1 Cash Handling Units... 2 Required Authorization to

Cash Handling Policies & Procedures Revised February 11, 2008 Table of Contents POLICY - CASH COLLECTION AND DEPOSIT 1 Purpose... 1 Introduction... 1 Cash Handling Units... 2 Required Authorization to

CASH: CASH CONTROLS C-173 ACCOUNTING MANUAL Page 1. Contents. I. Introduction 2. II. General Description of Cash Operations 2

ACCOUNTING MANUAL Page 1 CASH: CASH CONTROLS Contents I. Introduction 2 II. General Description of Cash Operations 2 III. Bank Account Controls 3 A. Regulations Governing Bank Accounts 3 B. Establishment

ACCOUNTING MANUAL Page 1 CASH: CASH CONTROLS Contents I. Introduction 2 II. General Description of Cash Operations 2 III. Bank Account Controls 3 A. Regulations Governing Bank Accounts 3 B. Establishment

Cash, Petty Cash, Change Funds, and Credit Cards

CASH As public servants, it is our responsibility to safeguard taxpayer s dollars while adhering to laws and regulations governing processes over cash handling. Internal controls over cash are necessary

CASH As public servants, it is our responsibility to safeguard taxpayer s dollars while adhering to laws and regulations governing processes over cash handling. Internal controls over cash are necessary

Cash Handling Procedure

1 Purpose This procedure provides a series of cash handling practices for Victoria University of Wellington (the University ) to supplement and support the cash handling material contained within the Treasury

1 Purpose This procedure provides a series of cash handling practices for Victoria University of Wellington (the University ) to supplement and support the cash handling material contained within the Treasury

DIXON MONTESSORI CHARTER SCHOOL FISCAL CONTROL POLICY

DIXON MONTESSORI CHARTER SCHOOL FISCAL CONTROL POLICY 1. Purpose The Dixon Montessori Charter School Board of Directors ( Board ) has reviewed and adopted the following policies and procedures to ensure

DIXON MONTESSORI CHARTER SCHOOL FISCAL CONTROL POLICY 1. Purpose The Dixon Montessori Charter School Board of Directors ( Board ) has reviewed and adopted the following policies and procedures to ensure

Collections, Contributions, and Accounts Receivable Policies

Collections, Contributions, and Accounts Receivable Policies The Office of the Student Financial Services is responsible for monitoring, processing and recording the collection of all funds collected by

Collections, Contributions, and Accounts Receivable Policies The Office of the Student Financial Services is responsible for monitoring, processing and recording the collection of all funds collected by

Cash Equivalents & Cash Handling Guide. Cashier s Office, UCSB 893-2177

Cash Equivalents & Cash Handling Guide Cashier s Office, UCSB 893-2177 Cashiering Responsibilities University employees who receive and handle cash and securities must follow and maintain the appropriate

Cash Equivalents & Cash Handling Guide Cashier s Office, UCSB 893-2177 Cashiering Responsibilities University employees who receive and handle cash and securities must follow and maintain the appropriate

Businesses: Payment by Cheque

Businesses: Payment by Cheque As Canada s digital economy evolves, many Canadian businesses are examining their payment processes, considering the transition from paper to electronic payments. The efficiencies,

Businesses: Payment by Cheque As Canada s digital economy evolves, many Canadian businesses are examining their payment processes, considering the transition from paper to electronic payments. The efficiencies,

Date Adopted: 05-18-11

Page 1 of 9 I. PURPOSE: The Oakland County Parks and Recreation Cash and Payment Card Industry (PCI) outlines procedures for the safe handling of funds managed on behalf of Oakland County as well as PCI

Page 1 of 9 I. PURPOSE: The Oakland County Parks and Recreation Cash and Payment Card Industry (PCI) outlines procedures for the safe handling of funds managed on behalf of Oakland County as well as PCI

Fiscal Procedure Sequence page number

Table of Contents Fiscal Procedure Sequence page number Treasurer Responsibilities Maintenance of General Ledger Financial Statements Financial Signature/Review Policy Insurance Protection Payroll Procedures

Table of Contents Fiscal Procedure Sequence page number Treasurer Responsibilities Maintenance of General Ledger Financial Statements Financial Signature/Review Policy Insurance Protection Payroll Procedures

CASH HANDLING AND REPORTING

CASH HANDLING AND REPORTING A. Purpose The purpose of this policy is to outline procedures for the consistent cash management at The University of Texas Rio Grande Valley (UTRGV). B. Persons Affected This

CASH HANDLING AND REPORTING A. Purpose The purpose of this policy is to outline procedures for the consistent cash management at The University of Texas Rio Grande Valley (UTRGV). B. Persons Affected This

Introduction to Accounting 2 Modul 1 Internal Control and Cash

Introduction to Accounting 2 Modul 1 Internal Control and Cash After studying this chapter, you should be able to: 1. Describe the Sarbanes-Oxley Act of 2002 and its impact on internal controls and financial

Introduction to Accounting 2 Modul 1 Internal Control and Cash After studying this chapter, you should be able to: 1. Describe the Sarbanes-Oxley Act of 2002 and its impact on internal controls and financial

Accounting Policies and Procedures Manual (Sample)

") Accounting Policies and Procedures Manual (Sample) Table of Contents Introduction General Business Office Staff Revenues and Cash Receipts Sources of Revenues Collecting Offerings Posting Revenues Cash

Accounting Policies and Procedures Manual (Sample) Table of Contents Introduction General Business Office Staff Revenues and Cash Receipts Sources of Revenues Collecting Offerings Posting Revenues Cash

UCLA Policy 360: Internal Control Guidelines for Campus Departments

UCLA Policy 360: Internal Control Guidelines for Campus Departments Issuing Officer: Assistant Vice Chancellor, Corporate Financial Services Responsible Dept: Financial Management Programs Effective Date:

UCLA Policy 360: Internal Control Guidelines for Campus Departments Issuing Officer: Assistant Vice Chancellor, Corporate Financial Services Responsible Dept: Financial Management Programs Effective Date:

SKAGIT COUNTY CASH COLLECTION POLICIES

SKAGIT COUNTY CASH COLLECTION POLICIES Administered by the Skagit County Treasurer Revised June 8, 2004 TABLE OF CONTENTS Policy Page I. Mandatory training for Cash Handlers 3 II. Temporary Employees as

SKAGIT COUNTY CASH COLLECTION POLICIES Administered by the Skagit County Treasurer Revised June 8, 2004 TABLE OF CONTENTS Policy Page I. Mandatory training for Cash Handlers 3 II. Temporary Employees as

Internal Control and Cash. Study Objectives. Chapter Outline

Study Objectives Identify the principles of internal control. Explain the applications of internal control to cash receipts. Explain the applications of internal control to cash disbursements. Prepare

Study Objectives Identify the principles of internal control. Explain the applications of internal control to cash receipts. Explain the applications of internal control to cash disbursements. Prepare

Cash Handling Process (Cash and Checks) - Gap Analysis FY 2015

- Gap Analysis FY 2015") Cash Handling Process (Cash and Checks) - Gap Analysis F 2015 **Sample/Mock Gap Analysis** ~~Evidence of completed annual Gap Analysis should be kept on file until the following year~~ Receiving Funds

Cash Handling Process (Cash and Checks) - Gap Analysis F 2015 **Sample/Mock Gap Analysis** ~~Evidence of completed annual Gap Analysis should be kept on file until the following year~~ Receiving Funds

PETTY CASH AND CHANGE FUNDS

PURPOSE To provide procedures and guidance to maintain an adequate system of internal control to protect petty cash and change funds from loss in accordance with ICSUAM Policy and ICSUAM 3103.11. SCOPE

PURPOSE To provide procedures and guidance to maintain an adequate system of internal control to protect petty cash and change funds from loss in accordance with ICSUAM Policy and ICSUAM 3103.11. SCOPE

State of New York Office of the State Comptroller Division of Management Audit and State Financial Services

State of New York Office of the State Comptroller Division of Management Audit and State Financial Services OFFICE OF MENTAL HEALTH KINGSBORO PSYCHIATRIC CENTER CONTROLS OVER PATIENT CASH REPORT 98-S-43

State of New York Office of the State Comptroller Division of Management Audit and State Financial Services OFFICE OF MENTAL HEALTH KINGSBORO PSYCHIATRIC CENTER CONTROLS OVER PATIENT CASH REPORT 98-S-43

Guides for County Office Fiscal Management

Guides for County Office Fiscal Management UNIVERSITY OF GEORGIA CAES March 3, 2014 Authored by: Timothy Gray Table of Contents: Page 1. Bank Reconciliations 2 2. Spot Checking for CECs..3-4 3. Checkout

Guides for County Office Fiscal Management UNIVERSITY OF GEORGIA CAES March 3, 2014 Authored by: Timothy Gray Table of Contents: Page 1. Bank Reconciliations 2 2. Spot Checking for CECs..3-4 3. Checkout

CASH RECONCILIATION & INTERNAL CONTROLS

CASH RECONCILIATION & INTERNAL CONTROLS Montana Clerks, Treasurers & Finance Officers Institute ~ May 2011 Presented by: Brenda Schneider, Superior; Doris Pinkerton, Forsyth & Darla Erickson, Local Government

CASH RECONCILIATION & INTERNAL CONTROLS Montana Clerks, Treasurers & Finance Officers Institute ~ May 2011 Presented by: Brenda Schneider, Superior; Doris Pinkerton, Forsyth & Darla Erickson, Local Government

Cash Receipt and Banking Internal Controls

Chapter 4 Cash Receipt and Banking Internal Controls A major asset of parishes is its cash and cash equivalents, including marketable securities and other highly liquid assets readily convertible into

Chapter 4 Cash Receipt and Banking Internal Controls A major asset of parishes is its cash and cash equivalents, including marketable securities and other highly liquid assets readily convertible into

APPENDIX A DRAFT Policy DIE-1 School Funds: Audit & Financial Monitoring Procedures

APPENDIX A DRAFT Policy DIE-1 School Funds: Audit & Financial Monitoring Procedures Administrative Guidelines Financial Monitoring Procedures The following Administrative Guidelines support the Principal

APPENDIX A DRAFT Policy DIE-1 School Funds: Audit & Financial Monitoring Procedures Administrative Guidelines Financial Monitoring Procedures The following Administrative Guidelines support the Principal

The policy and procedural guidelines contained in this handbook are designed to:

BASIC POLICY STATEMENT The Mikva Challenge is committed to responsible financial management. The entire organization including the board of directors, administrators, and staff will work together to make

BASIC POLICY STATEMENT The Mikva Challenge is committed to responsible financial management. The entire organization including the board of directors, administrators, and staff will work together to make

BEDFORD PUBLIC SCHOOLS BUSINESS OFFICE PROCEDURES MANUAL

BEDFORD PUBLIC SCHOOLS BUSINESS OFFICE PROCEDURES MANUAL Revised 3-27-2014 TABLE OF CONTENTS Section 1: Section 2: Section 3: Section 4: Section 5: Section 6: Section 7: Section 8: Section 9: Cash Management

BEDFORD PUBLIC SCHOOLS BUSINESS OFFICE PROCEDURES MANUAL Revised 3-27-2014 TABLE OF CONTENTS Section 1: Section 2: Section 3: Section 4: Section 5: Section 6: Section 7: Section 8: Section 9: Cash Management

Accounting software & data

Accounting software & data Accounting software and data should reside at church or be webbased where the data base can be accessed by multiple users Multiple people should be trained on software Software

Accounting software & data Accounting software and data should reside at church or be webbased where the data base can be accessed by multiple users Multiple people should be trained on software Software

Cash Receipts, Cash Payments, and Banking Procedures

9-1 McGraw-Hill 2009 The McGraw-Hill Companies, Inc. All rights reserved. Cash Receipts, Cash Payments, and Banking Procedures Section 1: Cash Receipts Section Objectives 1. Record cash receipts in a cash

9-1 McGraw-Hill 2009 The McGraw-Hill Companies, Inc. All rights reserved. Cash Receipts, Cash Payments, and Banking Procedures Section 1: Cash Receipts Section Objectives 1. Record cash receipts in a cash

RECEIVING CASH & CHECKS

SECTION: SUBJECT: APPLIES TO: Treasury Cash Handling Process Cash and Checks Documented Procedures Receiving, depositing and reconciling cash and checks Cash Handling (cash and checks) Overview The objective

SECTION: SUBJECT: APPLIES TO: Treasury Cash Handling Process Cash and Checks Documented Procedures Receiving, depositing and reconciling cash and checks Cash Handling (cash and checks) Overview The objective

Write Checks the Right Way

Write Checks the Right Way Guide G-220 Revised by Fahzy Abdul-Rahman 1 Cooperative Extension Service College of Agricultural, Consumer and Environmental Sciences CHECKS VS. OTHER PAYMENT METHODS Checks

Write Checks the Right Way Guide G-220 Revised by Fahzy Abdul-Rahman 1 Cooperative Extension Service College of Agricultural, Consumer and Environmental Sciences CHECKS VS. OTHER PAYMENT METHODS Checks

Mobile Check Deposit. Frequently Asked Questions

Mobile Check Deposit Frequently Asked Questions Q - What is Mobile Check Deposit? A - Mobile Check Deposit is a service that allows members to electronically transmit an image of their check using an iphone,

Mobile Check Deposit Frequently Asked Questions Q - What is Mobile Check Deposit? A - Mobile Check Deposit is a service that allows members to electronically transmit an image of their check using an iphone,