Needles in the Haystack: Data Mining for Fraud Detection

|

|

|

- Cynthia Skinner

- 9 years ago

- Views:

Transcription

1 acumen insight Needles in the Haystack: Data Mining for Fraud Detection ideas attention reach Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant expertise depth agility talent

2 Perp Poetry

3 Straw Vendor Invoice Invoice With 40 % Mark-up Print Job Legit Vendor Employee Graphic Designer Client Company

4 REPORT TO THE NATIONS

5 2012 by the Association of Certified Fraud Examiners, Inc.

6 Common Data Mining Areas Employees and Payroll Vendors and Accounts Payable Expense Reimbursement P Cards & Corporate Credit Cards Loans (financial institutions only) Patient accounting (health care only) Sales Inventory

Patient accounting (health care only) Sales")

7 Vendor Trending Analysis Time Series Analysis: Acceleration Vendor: JLM Plumbing Authorized: Janice L. McPhearson Acceleration as confidence builds Getting Greedy Test phase

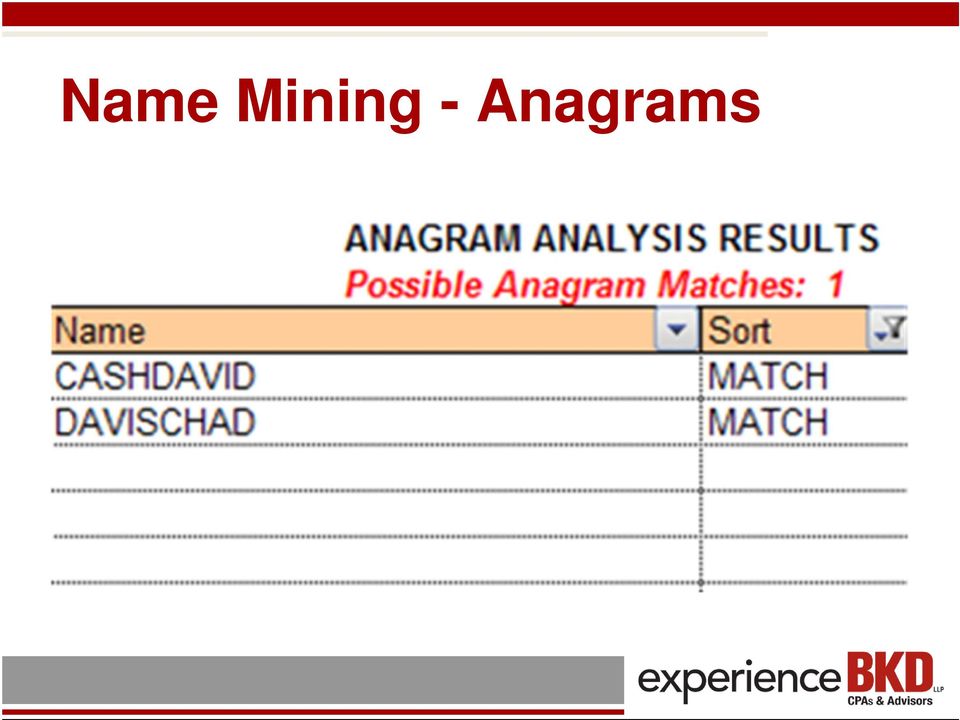

8 Name Mining - Anagrams

9 Geocoding AP Manager Vinny s Salvage Yard

10 Address Mining - Maildrops Fictitious Vendor with UPS Store Address

11 Name and Address Mining Name and ID analysis Direct matching Phonetic matching (Double Metaphone Hybrid) Compare to known name dictionaries Anagram search Duplicate Employee ID / SSN, Invalid SSNs Address analysis Direct matching No address, invalid address, PO/RR address Proximity by latitude/longitude lookup Address is a known mailbox service (FedEx Kinkos, UPS Store, etc.) Visual Map Analysis

12 Address Matching Address Match Example

13 Employee-Vendor Proximity

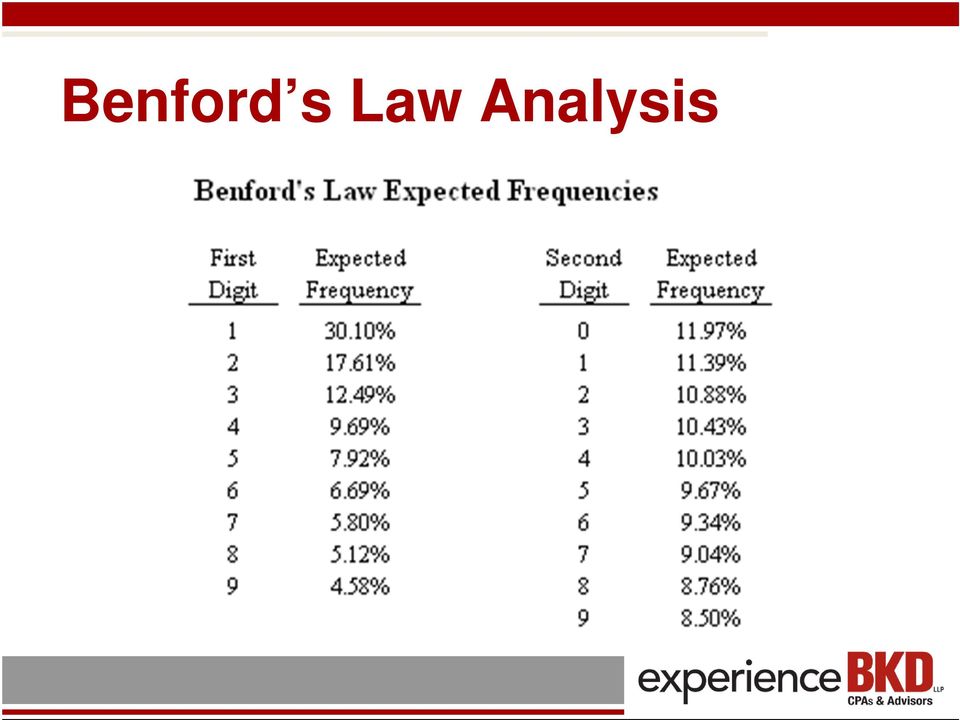

14 Benford s Law Analysis

15 Check Sequence Analysis

16 Split Purchase

17 Accounts Payable Mining AP: Fictitious vendors, duplicate payments, etc. Benford s analysis Acronym search on employee name Acceleration (systematic spending increases) via time series analysis Duplicate invoices Duplicate payments Identify invoices in excess of n% of vendor average Compare PO/invoice amount to check amount Identify transactions ending in 5 or 0 Baseline vendor activity against overall activity Classify transactions by clerk/approver Compare multiple vendor master files over 3 years Identify statistical outliers (Z-score method)

18 Payroll Mining Payroll Detail Employees with no deductions PR activity subsequent to termination Employee vs department baselines ($ and hrs) Department vs company baselines ($ and hrs) Benford's analysis of gross / net payroll Time series analysis Employee with no sick/vacation/time off Computed pay rate vs. Employee master rate Compare actual pay rates to rate schedule Other analysis Duplicate phone number(s) Duplicate direct deposit accounts Short duration of hire/termination

Duplicate direct")

19 acumen insight ideas Fictitious Loans attention reach expertise depth agility talent

20 Loan Master File HOME BUS ORIGINAL CUST_NAME ADDRESS1 city state zip PHONE PHONE TIN_SSN AMT P & Q BUILDERS P O BOX 145 SOMEWHERE ST XX093X64X6 0 X10X23X5 600, TERRY CEO PO BOX 145 SOMEWHERE ST XX093X64X6 0 4X22X68X 352, P & Q BUILDERS P O BOX 145 SOMEWHERE ST XX093X64X6 0 X10X23X5 269, P & Q BUILDERS P O BOX 145 SOMEWHERE ST XX093X64X6 0 X10X23X5 200, TERRY CEO PO BOX 145 SOMEWHERE ST XX093X64X6 0 4X22X68X 100, P & Q DISTRIBUTING INC PO BOX 247 CITY ST XX05X53X66 XX05X52X7 X10X23X5 100, P & Q DISTRIBUTING INC PO BOX 247 CITY ST XX05X53X66 XX05X52X7 X10X23X5 10,000.00

21 acumen insight ideas Manipulation of Portfolio Quality attention reach expertise depth agility talent

22 Loan Maintenance File Interest Rate Manipulations Past Due Manipulations Maintenance by User

23 2012 by the Association of Certified Fraud Examiners, Inc.

24 Resources IIA Guidance - GTAG Series GTAG 3 Continuous Auditing: Implications for Assurance, Monitoring & Risk Assessment GTAG 13 Fraud Prevention and Detection in an Automated World GTAG 16 Data Analysis Technologies Other Resources

25 Contact Information Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant BKD, LLP 910 E. St. Louis Street Springfield, MO Phone: Fax: Blog: Follow me on

26 acumen insight ideas Questions? attention reach expertise depth agility talent

Perp Poetry. Fraud & Embezzlement: Lessons From the Trenches. Presented by. acumen insight. ideas attention reach. expertise depth agility talent

acumen insight Fraud & Embezzlement: Lessons From the Trenches ideas attention reach Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant www.bkdforensics.com expertise depth

acumen insight Fraud & Embezzlement: Lessons From the Trenches ideas attention reach Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant www.bkdforensics.com expertise depth

Leveraging Big Data to Mitigate Health Care Fraud Risk

Leveraging Big Data to Mitigate Health Care Fraud Risk Jeremy Clopton, CPA, CFE, ACDA Senior Managing Consultant BKD, LLP Forensics & Valuation Services Introduction Health Care Is Victimized by Fraud

Leveraging Big Data to Mitigate Health Care Fraud Risk Jeremy Clopton, CPA, CFE, ACDA Senior Managing Consultant BKD, LLP Forensics & Valuation Services Introduction Health Care Is Victimized by Fraud

Introductions, Course Outline, and Other Administration Issues. Ed Ferrara, MSIA, CISSP [email protected]. Copyright 2015 Edward S.

MIS 520 Week 2 Fraud Detection & Prevention Introductions, Course Outline, and Other Administration Issues Ed Ferrara, MSIA, CISSP [email protected] Fraud Awareness & Internal Controls Awareness Internal

MIS 520 Week 2 Fraud Detection & Prevention Introductions, Course Outline, and Other Administration Issues Ed Ferrara, MSIA, CISSP [email protected] Fraud Awareness & Internal Controls Awareness Internal

Advanced Data Analytics, the Fraudsters Worst Enemy

Advanced Data Analytics, the Fraudsters Worst Enemy Introducing Powerful Tools and Techniques to Uncover Fraud Agenda Overview of data analytics in the anti-fraud and fraud investigation context Capability

Advanced Data Analytics, the Fraudsters Worst Enemy Introducing Powerful Tools and Techniques to Uncover Fraud Agenda Overview of data analytics in the anti-fraud and fraud investigation context Capability

Using Technology to Automate Fraud Detection Within Key Business Process Areas

Using Technology to Automate Fraud Detection Within Key Business Process Areas 2013 ACFE Canadian Fraud Conference September 10, 2013 John Verver, CA, CISA, CMA Vice President, Strategy ACL Services Ltd

Using Technology to Automate Fraud Detection Within Key Business Process Areas 2013 ACFE Canadian Fraud Conference September 10, 2013 John Verver, CA, CISA, CMA Vice President, Strategy ACL Services Ltd

Auditing for Value in the Procure to Pay Cycle Dallas IIA Chapter. October 1, 2009

Auditing for Value in the Procure to Pay Cycle Dallas IIA Chapter October 1, 2009 Supply Chain Risk Overview * Today s Focus * Includes Working Capital benefits 1 2009 Protiviti Inc. An Equal Opportunity

Auditing for Value in the Procure to Pay Cycle Dallas IIA Chapter October 1, 2009 Supply Chain Risk Overview * Today s Focus * Includes Working Capital benefits 1 2009 Protiviti Inc. An Equal Opportunity

Microsoft Confidential

Brock Phillips, CPA, CFE, CCEP Forensic Accounting Sr. Manager Financial Integrity Unit Microsoft Audit Group Lou DeCola, CPA, CIA, CFE Forensic Accounting Sr. Manager Financial Integrity Unit Microsoft

Brock Phillips, CPA, CFE, CCEP Forensic Accounting Sr. Manager Financial Integrity Unit Microsoft Audit Group Lou DeCola, CPA, CIA, CFE Forensic Accounting Sr. Manager Financial Integrity Unit Microsoft

An Auditor s Guide to Data Analytics

An Auditor s Guide to Data Analytics Natasha DeKroon, Duke University Health System Brian Karp Services Experis, Risk Advisory May 11, 2013 1 Today s Agenda Data Analytics the Basics Tools of the Trade

An Auditor s Guide to Data Analytics Natasha DeKroon, Duke University Health System Brian Karp Services Experis, Risk Advisory May 11, 2013 1 Today s Agenda Data Analytics the Basics Tools of the Trade

How to set up a people based. accounting system that makes your. small business work for you. Thomas G. Post. Certified Public Accountant 281-351-2688

How to set up a people based accounting system that makes your small business work for you. By Thomas G. Post Certified Public Accountant 281-351-2688 www.texastaxman.com 1 Title How to set up a people

How to set up a people based accounting system that makes your small business work for you. By Thomas G. Post Certified Public Accountant 281-351-2688 www.texastaxman.com 1 Title How to set up a people

Why is Internal Audit so Hard?

Why is Internal Audit so Hard? 2 2014 Why is Internal Audit so Hard? 3 2014 Why is Internal Audit so Hard? Waste Abuse Fraud 4 2014 Waves of Change 1 st Wave Personal Computers Electronic Spreadsheets

Why is Internal Audit so Hard? 2 2014 Why is Internal Audit so Hard? 3 2014 Why is Internal Audit so Hard? Waste Abuse Fraud 4 2014 Waves of Change 1 st Wave Personal Computers Electronic Spreadsheets

Using Data Analytics to Detect Fraud

Using Data Analytics to Detect Fraud Fundamental Data Analysis Techniques 2016 Association of Certified Fraud Examiners, Inc. Discussion Question For each data analysis technique discussed in this section,

Using Data Analytics to Detect Fraud Fundamental Data Analysis Techniques 2016 Association of Certified Fraud Examiners, Inc. Discussion Question For each data analysis technique discussed in this section,

Fraud Workshop Finding the truth in the transactions

Your Trusted Partner for Audit Analytics Fraud Workshop Finding the truth in the transactions Copyright 2011 ACL Services Ltd. Robin Clough, ACDA ACL Certified Trainer Copyright 2011 ACL Services Ltd.

Your Trusted Partner for Audit Analytics Fraud Workshop Finding the truth in the transactions Copyright 2011 ACL Services Ltd. Robin Clough, ACDA ACL Certified Trainer Copyright 2011 ACL Services Ltd.

Procurement Fraud Identification & Role of Data Mining

The paper describes the known boundaries of Procurement Fraud and outlines the scope of data mining within the same. The paper also highlights some of the basic steps to be taken care of before the application

The paper describes the known boundaries of Procurement Fraud and outlines the scope of data mining within the same. The paper also highlights some of the basic steps to be taken care of before the application

Use of Data Extraction & Analysis Software In a Financial Statement Audit

Use of Data Extraction & Analysis Software In a Financial Statement Audit A Message from The Audit Wizard April 2008 Making Auditors Proficient, Inc. Phone: 352-750-9636 www.billallen.com E-mail: [email protected]

Use of Data Extraction & Analysis Software In a Financial Statement Audit A Message from The Audit Wizard April 2008 Making Auditors Proficient, Inc. Phone: 352-750-9636 www.billallen.com E-mail: [email protected]

Auditing Applications. ISACA Seminar: February 10, 2012

Auditing Applications ISACA Seminar: February 10, 2012 Planning Objectives Mapping Controls Functionality Tests Complications Financial Assertions Tools Reporting AGENDA 2 PLANNING Consideration / understanding

Auditing Applications ISACA Seminar: February 10, 2012 Planning Objectives Mapping Controls Functionality Tests Complications Financial Assertions Tools Reporting AGENDA 2 PLANNING Consideration / understanding

VERSION NINE. Be A Better Auditor. You Have The Knowledge. We Have The Tools. PRODUCT PROFILE

VERSION NINE Be A Better Auditor. You Have The Knowledge. We Have The Tools. PRODUCT PROFILE IMPROVE BUSINESS PERFORMANCE DRIVE QUALITYCOMPLIANCE DO MORE WITH LESS ACCOUNTABILITY FIND FRAUDREDUCE RISK

VERSION NINE Be A Better Auditor. You Have The Knowledge. We Have The Tools. PRODUCT PROFILE IMPROVE BUSINESS PERFORMANCE DRIVE QUALITYCOMPLIANCE DO MORE WITH LESS ACCOUNTABILITY FIND FRAUDREDUCE RISK

Data Analytics For the Restaurant Industry

Data Analytics For the Restaurant Industry 2014 Sunera Snapshot SAP ACL Copyright 2013 Sunera LLC. 2 About Our Speaker Matt Osbeck, CPA, CIA, ACDA Matt is a Senior Manager in the Los Angeles office of

Data Analytics For the Restaurant Industry 2014 Sunera Snapshot SAP ACL Copyright 2013 Sunera LLC. 2 About Our Speaker Matt Osbeck, CPA, CIA, ACDA Matt is a Senior Manager in the Los Angeles office of

FRAUD PREVENTION STRATEGIES FOR HEALTH CARE A FORENSIC ACCOUNTANT S PERSPECTIVE

FRAUD PREVENTION STRATEGIES FOR HEALTH CARE A FORENSIC ACCOUNTANT S PERSPECTIVE CPAs & ADVISORS experience reach // S. Todd Burchett, CPA, ABV, ASA, CFF, CFE Partner [email protected] 210.268.1932 AGENDA

FRAUD PREVENTION STRATEGIES FOR HEALTH CARE A FORENSIC ACCOUNTANT S PERSPECTIVE CPAs & ADVISORS experience reach // S. Todd Burchett, CPA, ABV, ASA, CFF, CFE Partner [email protected] 210.268.1932 AGENDA

Accounting Notes. Purchasing Merchandise under the Perpetual Inventory system:

Systems: Perpetual VS Periodic " Keeps running record of all goods " Does not keep a running record bought and sold " is counted once a year " is counted at least once a year " Used for all types of goods

Systems: Perpetual VS Periodic " Keeps running record of all goods " Does not keep a running record bought and sold " is counted once a year " is counted at least once a year " Used for all types of goods

Fraud and Fraud Detection. A Data Analytics Approach + Website. Wiley Corporate F&A

Brochure More information from http://www.researchandmarkets.com/reports/2866056/ Fraud and Fraud Detection. A Data Analytics Approach + Website. Wiley Corporate F&A Description: Detect fraud faster no

Brochure More information from http://www.researchandmarkets.com/reports/2866056/ Fraud and Fraud Detection. A Data Analytics Approach + Website. Wiley Corporate F&A Description: Detect fraud faster no

Contents. xiii xv. Case Studies Preface

Case Studies Preface xiii xv CHAPTER 1 What Is Fraud? 1 Fraud: A Definition 3 Why Fraud Happens 4 Who Is Responsible for Fraud Detection? 7 What Is a Fraud Awareness Program? 11 Screening Job Applicants

Case Studies Preface xiii xv CHAPTER 1 What Is Fraud? 1 Fraud: A Definition 3 Why Fraud Happens 4 Who Is Responsible for Fraud Detection? 7 What Is a Fraud Awareness Program? 11 Screening Job Applicants

ACCOUNTING RECORDS: HOW THEY ARE USED TO CONCEAL FRAUD. ROSANNE TERHART, CFE, CA Senior Manager BDO Canada LLP Vancouver, British Columbia Canada

Once an employee commits fraud, he has limited time to conceal the financial transaction in the accounting records. Learn how employees hide these fraudulent transactions and what to look for when reviewing

Once an employee commits fraud, he has limited time to conceal the financial transaction in the accounting records. Learn how employees hide these fraudulent transactions and what to look for when reviewing

THE ABC S OF DATA ANALYTICS

THE ABC S OF DATA ANALYTICS ANGEL BUTLER MAY 23, 2013 HOUSTON AREA SCHOOL DISTRICT INTERNAL AUDITORS (HASDIA) AGENDA Data Analytics Overview Data Analytics Examples Compliance Purchasing and Accounts Payable

THE ABC S OF DATA ANALYTICS ANGEL BUTLER MAY 23, 2013 HOUSTON AREA SCHOOL DISTRICT INTERNAL AUDITORS (HASDIA) AGENDA Data Analytics Overview Data Analytics Examples Compliance Purchasing and Accounts Payable

Fraud Detection & Data Analytics

September 2008 Fraud Detection & Data Analytics How to Utilize CAATs to detect fraud AN INDEPENDENT MEMBER OF BAKER TILLY INTERNATIONAL 505 AFFILIATE OFFICES WORLDWIDE Course Topics Overview of Data Analytics

September 2008 Fraud Detection & Data Analytics How to Utilize CAATs to detect fraud AN INDEPENDENT MEMBER OF BAKER TILLY INTERNATIONAL 505 AFFILIATE OFFICES WORLDWIDE Course Topics Overview of Data Analytics

OFFICE OF THE CITY AUDITOR

OFFICE OF THE CITY AUDITOR TO: THRU: FROM: DATE: SUBJECT: Mayor and Council Members Margaret Krym, City Auditor Kathy Magaw, Assistant Auditor~ September 27, 2013 Accounts Payable - Search for Duplicate

OFFICE OF THE CITY AUDITOR TO: THRU: FROM: DATE: SUBJECT: Mayor and Council Members Margaret Krym, City Auditor Kathy Magaw, Assistant Auditor~ September 27, 2013 Accounts Payable - Search for Duplicate

Presented by: Donald F. Conway, CPA Mercadien, P.C., Certified Public Accountants. Forensic Accounting, Political Corruption & White Collar Offenses

Presented by: Donald F. Conway, CPA Mercadien, P.C., Certified Public Accountants Forensic Accounting, Political Corruption & White Collar Offenses Defining Fraud The dictionary defines fraud as a deception

Presented by: Donald F. Conway, CPA Mercadien, P.C., Certified Public Accountants Forensic Accounting, Political Corruption & White Collar Offenses Defining Fraud The dictionary defines fraud as a deception

Financial Services Group

Fraud Detection and Prevention Presented by: Carrie Kennedy, CPA, Partner Anthony Porter, CPA, Manager 1 The material appearing in this presentation is for informational purposes only and should not be

Fraud Detection and Prevention Presented by: Carrie Kennedy, CPA, Partner Anthony Porter, CPA, Manager 1 The material appearing in this presentation is for informational purposes only and should not be

Strong Corporate Governance & Internal Controls: Internal Auditing in Higher Education

Strong Corporate Governance & Internal Controls: Internal Auditing in Higher Education Contents Introduction Internal Audit as Trusted Advisor & Business Partner Big Ticket Items: Fraud, Revenue Leakage

Strong Corporate Governance & Internal Controls: Internal Auditing in Higher Education Contents Introduction Internal Audit as Trusted Advisor & Business Partner Big Ticket Items: Fraud, Revenue Leakage

204 Reports Included with Version 7.0!

204 Reports Included with Version 7.0! Accounts Payable Aged A/P summary by name Aged A/P summary by number Detailed A/P activity by name Detailed A/P activity by number Detailed aged A/P by name Detailed

204 Reports Included with Version 7.0! Accounts Payable Aged A/P summary by name Aged A/P summary by number Detailed A/P activity by name Detailed A/P activity by number Detailed aged A/P by name Detailed

Data Mining: Unlocking the Intelligence in Your Data. Marlon B. Williams, CPA, ACDA Partner, IT Advisory Services Weaver

Data Mining: Unlocking the Intelligence in Your Data Marlon B. Williams, CPA, ACDA Partner, IT Advisory Services Weaver 0 Today s Agenda Big Data What is it? Data Mining at a Glance Why the Accounting

Data Mining: Unlocking the Intelligence in Your Data Marlon B. Williams, CPA, ACDA Partner, IT Advisory Services Weaver 0 Today s Agenda Big Data What is it? Data Mining at a Glance Why the Accounting

Accounts Payable. Cash Projections Reports - 3-tiered Pay on Dates show what is due in the next 30/60/90 days.

The Accounts Payable module can process multiple Companies and Locations and is fully integrated to the General Ledger module. With the Reporting and Query capabilities of the AP module, you can increase

The Accounts Payable module can process multiple Companies and Locations and is fully integrated to the General Ledger module. With the Reporting and Query capabilities of the AP module, you can increase

Internal Controls for Small Organizations. Jen Parker, CPA Director of Accounting & Finance US Youth Soccer

Internal Controls for Small Organizations Jen Parker, CPA Director of Accounting & Finance US Youth Soccer Fraud Statistics: The following statistics about fraud and white collar crime are from the Association

Internal Controls for Small Organizations Jen Parker, CPA Director of Accounting & Finance US Youth Soccer Fraud Statistics: The following statistics about fraud and white collar crime are from the Association

February 2, 2012 ACCOUNTS PAYABLE BEST PRACTICES

February 2, 2012 ACCOUNTS PAYABLE BEST PRACTICES IMPORTANCE OF A/P BEST PRACTICES After payroll, the largest disbursement of a firm s funds typically comes from Accounts Payable (A/P) Accounts Payable

February 2, 2012 ACCOUNTS PAYABLE BEST PRACTICES IMPORTANCE OF A/P BEST PRACTICES After payroll, the largest disbursement of a firm s funds typically comes from Accounts Payable (A/P) Accounts Payable

Automating the Audit July 2010

Jamie Williams PwC, Systems & Process Assurance PwC Agenda 1. Technology and PwC State of Internal Audit Survey 2. Technology/Data Analytics 3. Continuous Monitoring 4. Common Software 5. ACL Scripts 6.

Jamie Williams PwC, Systems & Process Assurance PwC Agenda 1. Technology and PwC State of Internal Audit Survey 2. Technology/Data Analytics 3. Continuous Monitoring 4. Common Software 5. ACL Scripts 6.

Integrating Payables and Receivables to Unlock Working Capital

Integrating Payables and Receivables to Unlock Working Capital Approved for 1 CTP / CCM recertification credit by the Association of Financial Professionals May 2009 Introductions David Kunz Treasury Management

Integrating Payables and Receivables to Unlock Working Capital Approved for 1 CTP / CCM recertification credit by the Association of Financial Professionals May 2009 Introductions David Kunz Treasury Management

December 2004 2303 Camino Ramon, Suite 210 San Ramon, CA 94583-1389 Voice: 925.244.5930 Fax: 925.867.1580 Website: www.miscorp.com

December 2004 2303 Camino Ramon, Suite 210 San Ramon, CA 94583-1389 Voice: 925.244.5930 Fax: 925.867.1580 Website: www.miscorp.com Copyright 2004 All rights protected and reserved TABLE OF CONTENTS I.

December 2004 2303 Camino Ramon, Suite 210 San Ramon, CA 94583-1389 Voice: 925.244.5930 Fax: 925.867.1580 Website: www.miscorp.com Copyright 2004 All rights protected and reserved TABLE OF CONTENTS I.

GENERAL PAYROLL CONTROLS Dates in scope:

GENERAL PAYROLL CONTROLS Risk # Risk Expected Control Step # Testing Documents/Info Needed 1 Unauthorized initial pay rate 2 Unauthorized/unsupported deductions (statutory deductions and benefits). Initial

GENERAL PAYROLL CONTROLS Risk # Risk Expected Control Step # Testing Documents/Info Needed 1 Unauthorized initial pay rate 2 Unauthorized/unsupported deductions (statutory deductions and benefits). Initial

How To Understand And Understand Forensic Accounting

Forensic Accounting and Investigations University of Texas at Arlington 14 August 2013 Overview What is Forensic Accounting? Definition and Services The Forensic Accountant History Roles Within Organizations

Forensic Accounting and Investigations University of Texas at Arlington 14 August 2013 Overview What is Forensic Accounting? Definition and Services The Forensic Accountant History Roles Within Organizations

For illustrative purposes only, we will look at the logical flow of the Data Pro Job Cost package as a general contractor might use it.

ACCOUNTING FLOW OF JOB COST / TIME BILLING The Data Pro Job Costing Series has a number of component parts that create both the reporting capability and the accounting flow through the modules. These component

ACCOUNTING FLOW OF JOB COST / TIME BILLING The Data Pro Job Costing Series has a number of component parts that create both the reporting capability and the accounting flow through the modules. These component

FINANCIAL POLICIES INDEX

FINANCIAL POLICIES INDEX Page Accounts Payable 2 Cash Receipts 6 Credit Cards 9 General Ledger Adjustments 10 Fixed Asset 11 Payroll Tax Reporting 13 Travel Reimbursement 14 Handling Mail 15 1 Accounts

FINANCIAL POLICIES INDEX Page Accounts Payable 2 Cash Receipts 6 Credit Cards 9 General Ledger Adjustments 10 Fixed Asset 11 Payroll Tax Reporting 13 Travel Reimbursement 14 Handling Mail 15 1 Accounts

Pace & Hawley, LLC Certified Public Accountants

Pace & Hawley, LLC Certified Public Accountants Form 990 Return of Organization Exempt From Income Tax Robert Pace, CPA, - Nathan Hawley, CPA PO Box 603 - Montpelier, VT 05601 TEL (802) 461-2587 - FAX

Pace & Hawley, LLC Certified Public Accountants Form 990 Return of Organization Exempt From Income Tax Robert Pace, CPA, - Nathan Hawley, CPA PO Box 603 - Montpelier, VT 05601 TEL (802) 461-2587 - FAX

Business Intelligence Inquiry Dashboard Job Aid

Business Intelligence Inquiry Dashboard Job Aid DASHBOARD AND DASHBOARD PAGES: DASHBOARD: Inquiry DATA: The data in the Inquiry dashboard is from the Cardinal Financial System General Ledger, Accounts

Business Intelligence Inquiry Dashboard Job Aid DASHBOARD AND DASHBOARD PAGES: DASHBOARD: Inquiry DATA: The data in the Inquiry dashboard is from the Cardinal Financial System General Ledger, Accounts

Proactive Fraud Detection with Data Mining Fear not the computer You play ball with it and it will play ball with you

3/27/2012 Proactive Fraud Detection with Data Mining Fear not the computer You play ball with it and it will play ball with you Executive Summary The time to test fraud controls is before you have a fraud

3/27/2012 Proactive Fraud Detection with Data Mining Fear not the computer You play ball with it and it will play ball with you Executive Summary The time to test fraud controls is before you have a fraud

Welcome to Metafile. Solving document issues for over 30 years. Matt Akin [email protected] 800-638-2445 x 301

Welcome to Metafile Solving document issues for over 30 years Matt Akin [email protected] 800-638-2445 x 301 Janine Peck [email protected] 800-638-2445 x 303 Metafile helps many companies with their AP,

Welcome to Metafile Solving document issues for over 30 years Matt Akin [email protected] 800-638-2445 x 301 Janine Peck [email protected] 800-638-2445 x 303 Metafile helps many companies with their AP,

ACL WHITEPAPER. Automating Fraud Detection: The Essential Guide. John Verver, CA, CISA, CMC, Vice President, Product Strategy & Alliances

ACL WHITEPAPER Automating Fraud Detection: The Essential Guide John Verver, CA, CISA, CMC, Vice President, Product Strategy & Alliances Contents EXECUTIVE SUMMARY..................................................................3

ACL WHITEPAPER Automating Fraud Detection: The Essential Guide John Verver, CA, CISA, CMC, Vice President, Product Strategy & Alliances Contents EXECUTIVE SUMMARY..................................................................3

WHAT S NEW IN SAGE 100 2015. Colleen A. Gutirrez, Senior Consultant II, BKD Technologies

WHAT S NEW IN SAGE 100 2015 Colleen A. Gutirrez, Senior Consultant II, BKD Technologies WELCOME/INTRODUCTIONS Colleen Gutirrez 19 years of experience in technology consulting Primarily distribution & manufacturing

WHAT S NEW IN SAGE 100 2015 Colleen A. Gutirrez, Senior Consultant II, BKD Technologies WELCOME/INTRODUCTIONS Colleen Gutirrez 19 years of experience in technology consulting Primarily distribution & manufacturing

Finding the Sweet Spot. Using analytics to combine Fraud and AML

www.pwc.com Finding the Sweet Spot Using analytics to combine Fraud and AML October, 2012 Overview Who are we? John Sabatini Partner PwC [email protected] Vikas Agarwal Managing Director PwC [email protected]

www.pwc.com Finding the Sweet Spot Using analytics to combine Fraud and AML October, 2012 Overview Who are we? John Sabatini Partner PwC [email protected] Vikas Agarwal Managing Director PwC [email protected]

PeopleSoft Version 9.2

PeopleSoft Version 9.2 Version 1 September 2015 TABLE OF CONTENTS COURSES FOR ALL AGENCY CAPPS EMPLOYEES... 1 CAPPS FINANCIALS FUNDAMENTALS... 1 CAPPS FINANCIALS TRAINING COURSES... 2 ACCOUNTS PAYABLE

PeopleSoft Version 9.2 Version 1 September 2015 TABLE OF CONTENTS COURSES FOR ALL AGENCY CAPPS EMPLOYEES... 1 CAPPS FINANCIALS FUNDAMENTALS... 1 CAPPS FINANCIALS TRAINING COURSES... 2 ACCOUNTS PAYABLE

Data Mining/Fraud Detection. April 28, 2014 Jonathan Meyer, CPA KPMG, LLP

Data Mining/Fraud Detection April 28, 2014 Jonathan Meyer, CPA KPMG, LLP 1 Agenda Overview of Data Analytics & Fraud Getting Started with Data Analytics Where to Look & Why? What is Possible? 2 D&A Business

Data Mining/Fraud Detection April 28, 2014 Jonathan Meyer, CPA KPMG, LLP 1 Agenda Overview of Data Analytics & Fraud Getting Started with Data Analytics Where to Look & Why? What is Possible? 2 D&A Business

Volume No. 1 Policies & Procedures TOPIC NO. 20319 Function No. 20000 General Accounting TOPIC ELECTRONIC FEDERAL TAX PAYMENTS PROCESSING

Table of Contents Overview... 3 Introduction to EFTPS... 3 Tax Reporting Entity... 3 Policy... 3 To Enroll in EFTPS... 3 Tax Payment Frequency... 4 IRS Penalty... 4 Payment Procedures--Form 941, Employer's

Table of Contents Overview... 3 Introduction to EFTPS... 3 Tax Reporting Entity... 3 Policy... 3 To Enroll in EFTPS... 3 Tax Payment Frequency... 4 IRS Penalty... 4 Payment Procedures--Form 941, Employer's

Fraud Triangle Analytics Anti-Fraud Research and Methodologies

Fraud Triangle Analytics Anti-Fraud Research and Methodologies Risk Management Committee Meeting American Hotel & Lodging Association November 18, 2009 Topics for discussion Why incorporate fraud detection

Fraud Triangle Analytics Anti-Fraud Research and Methodologies Risk Management Committee Meeting American Hotel & Lodging Association November 18, 2009 Topics for discussion Why incorporate fraud detection

Current Uses and Trends in ACL and Data Mining

Current Uses and Trends in ACL and Data Mining Weaver and Tidwell, L.L.P. January 10, 2013 Marlon B Williams, CPA, ACDA Partner, Assurance Reema Parappilly, CISA Senior Manager, IT Advisory Objective Discuss

Current Uses and Trends in ACL and Data Mining Weaver and Tidwell, L.L.P. January 10, 2013 Marlon B Williams, CPA, ACDA Partner, Assurance Reema Parappilly, CISA Senior Manager, IT Advisory Objective Discuss

Armanino LLP Welcomes You To Today s Webinar: GP Tips and Tricks: Using Credit Cards in GP

Armanino LLP Welcomes You To Today s Webinar: GP Tips and Tricks: Using Credit Cards in GP The presentation will begin in a few moments Participants will receive an email within 48 hours with a link to

Armanino LLP Welcomes You To Today s Webinar: GP Tips and Tricks: Using Credit Cards in GP The presentation will begin in a few moments Participants will receive an email within 48 hours with a link to

Microsoft Project Professional

Microsoft Project Professional A 100% practical workshop to master Microsoft Project, training the main features of the application for project management. Objective Insight into the functions required

Microsoft Project Professional A 100% practical workshop to master Microsoft Project, training the main features of the application for project management. Objective Insight into the functions required

MD AOC Project Introduction to PeopleSoft

Insert Pictures that represent Customer on Master slide MD AOC Project Introduction to PeopleSoft PeopleSoft Vendor Management Agenda Introduction Session Objectives PeopleSoft Overview Key Features Business

Insert Pictures that represent Customer on Master slide MD AOC Project Introduction to PeopleSoft PeopleSoft Vendor Management Agenda Introduction Session Objectives PeopleSoft Overview Key Features Business

by: Scott Baranowski, CIA

Community Bank Auditors Group A/P, Procurement and Credit Card Internal Controls June 4, 2014 by: Scott Baranowski, CIA MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2013 Wolf

Community Bank Auditors Group A/P, Procurement and Credit Card Internal Controls June 4, 2014 by: Scott Baranowski, CIA MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2013 Wolf

Workshop: Private Fund Fee and Expense Allocations

Workshop: Private Fund Fee and Expense Allocations November 10, 2015 Presented by Ann Gittleman & Sherif Assef 1. Introduction 2 Potential Risks for Private Funds Investor skepticism has increased as violations

Workshop: Private Fund Fee and Expense Allocations November 10, 2015 Presented by Ann Gittleman & Sherif Assef 1. Introduction 2 Potential Risks for Private Funds Investor skepticism has increased as violations

Generally Accepted Record Retention Guidelines

Document Name /Type Accident reports and claims (settled cases) Accommodation requests Accounts payable ledgers and schedules Accounts receivable ledgers and schedules Ads and Notices of overtime opportunities

Document Name /Type Accident reports and claims (settled cases) Accommodation requests Accounts payable ledgers and schedules Accounts receivable ledgers and schedules Ads and Notices of overtime opportunities

Audits of Automobile Body and Repair Shops

Audits of Automobile Body and Repair Shops If you are in certain retail businesses, industry specific audit procedures may be performed by the IRS in addition to the standard procedures performed during

Audits of Automobile Body and Repair Shops If you are in certain retail businesses, industry specific audit procedures may be performed by the IRS in addition to the standard procedures performed during

Leverage T echnology: Move Your Business Forward

Give me a lever long enough and a fulcrum on which to place it, and I shall move the world - Archimedes Copyright. Fulcrum Information Technology, Inc. Is Oracle ERP in Scope for 2014 Audit Plan? Learn,

Give me a lever long enough and a fulcrum on which to place it, and I shall move the world - Archimedes Copyright. Fulcrum Information Technology, Inc. Is Oracle ERP in Scope for 2014 Audit Plan? Learn,

Accounts Payable Fraud Services

Accounts Payable Fraud Services According to research conducted by the Association of Certified Fraud Examiners (ACFE), U.S. organizations lose an estimated 7 percent of annual revenues to fraud. 1 In

Accounts Payable Fraud Services According to research conducted by the Association of Certified Fraud Examiners (ACFE), U.S. organizations lose an estimated 7 percent of annual revenues to fraud. 1 In

Segregation of Duties

Segregation of Duties Scott Mitchell, Senior Manager (503) 478-2193 John Earl, Manager (503) 478-2188 January 5, 2010 Our Objectives Clarify the role of Segregation of Duties (SOD) Identify alternatives

Segregation of Duties Scott Mitchell, Senior Manager (503) 478-2193 John Earl, Manager (503) 478-2188 January 5, 2010 Our Objectives Clarify the role of Segregation of Duties (SOD) Identify alternatives

BusinessPlus 7.9 Vendor Look Up

BusinessPlus 7.9 Vendor Look Up New to 7.9 is access to view information on PEID (Vendor) files. No access is given to change existing information or to add new information. To look up a vendor, begin

BusinessPlus 7.9 Vendor Look Up New to 7.9 is access to view information on PEID (Vendor) files. No access is given to change existing information or to add new information. To look up a vendor, begin

MOUNTAIN VIEW SCHOOL DISTRICT

MOUNTAIN VIEW SCHOOL DISTRICT COMPUTERIZED ACCOUNTING I Curriculum Content Frameworks 0 Curriculum Content Frameworks COMPUTERIZED ACCOUNTING I Grade Levels: 0,, Course Code: 900 Prerequisite: Tech Prep

MOUNTAIN VIEW SCHOOL DISTRICT COMPUTERIZED ACCOUNTING I Curriculum Content Frameworks 0 Curriculum Content Frameworks COMPUTERIZED ACCOUNTING I Grade Levels: 0,, Course Code: 900 Prerequisite: Tech Prep

Data Analytics Leveraging Data Visualization and Automation in Audit Real World Examples

Data Analytics Leveraging Data Visualization and Automation in Audit Real World Examples June 3, 2015 Cliff Stephens, CISA Agenda Introductions Technological Advances in Analytics Capitalizing on Analytics

Data Analytics Leveraging Data Visualization and Automation in Audit Real World Examples June 3, 2015 Cliff Stephens, CISA Agenda Introductions Technological Advances in Analytics Capitalizing on Analytics

Accounts Payable Reference Guide

Create a New Vendor Vendors supply you with goods or services you need to run your business. Vendor records must be created prior to processing bills or other payable transactions. 1 Before entering in

Create a New Vendor Vendors supply you with goods or services you need to run your business. Vendor records must be created prior to processing bills or other payable transactions. 1 Before entering in

Simplify Your Life. Switch to Central Bank of the Ozarks. Account Application. Email Address

Personal Information Individual Account Holder Joint Account Holder Physical (no P.O. Box) Physical (no P.O. Box) Mailing Mailing Email Email Signer Information Individual Account Holder Joint Account

Personal Information Individual Account Holder Joint Account Holder Physical (no P.O. Box) Physical (no P.O. Box) Mailing Mailing Email Email Signer Information Individual Account Holder Joint Account

Portfolio Based Enterprise Property Management System allows you to manage hundreds of properties from your virtual desktop.

AP Cash GL Portfolio Based Enterprise Property Management System allows you to manage hundreds of properties from your virtual desktop. User friendly interface allows most actions to be completed in one

AP Cash GL Portfolio Based Enterprise Property Management System allows you to manage hundreds of properties from your virtual desktop. User friendly interface allows most actions to be completed in one

Completing an Accounts Payable Audit With ACL (Aired on Feb 15)

") AuditSoftwareVideos.com Video Training Titles (ACL Software Sessions Only) Contents Completing an Accounts Payable Audit With ACL (Aired on Feb 15)... 1 Statistical Analysis in ACL The Analyze Menu (Aired

AuditSoftwareVideos.com Video Training Titles (ACL Software Sessions Only) Contents Completing an Accounts Payable Audit With ACL (Aired on Feb 15)... 1 Statistical Analysis in ACL The Analyze Menu (Aired

Tips to Prevent and Detect Workplace Fraud

40 Tips to Prevent and Detect Workplace Fraud an E-book developed for you by: Table of Contents preventive controls detective controls 1. culture of ethics 2. free of moral hazards 3. risk management policy

40 Tips to Prevent and Detect Workplace Fraud an E-book developed for you by: Table of Contents preventive controls detective controls 1. culture of ethics 2. free of moral hazards 3. risk management policy

Records Retention Guidelines

Records Retention Guidelines There are no hard and fast rules regarding the amount of time taxpayers should keep important legal and financial documents. However, the following list of guidelines aims

Records Retention Guidelines There are no hard and fast rules regarding the amount of time taxpayers should keep important legal and financial documents. However, the following list of guidelines aims

Florida A & M University

Florida A & M University AP PROCEDURES 3-8-2013 TABLE OF CONTENTS 1.0 OVERVIEW... 1 2.0 DEFINITIONS... 1 3.0 RESPONSIBILITIES... 2 4.0 GENERAL PROCEDURES... 3 4.1 DEPARTMENTAL FISCAL REPRESENTATIVES...

Florida A & M University AP PROCEDURES 3-8-2013 TABLE OF CONTENTS 1.0 OVERVIEW... 1 2.0 DEFINITIONS... 1 3.0 RESPONSIBILITIES... 2 4.0 GENERAL PROCEDURES... 3 4.1 DEPARTMENTAL FISCAL REPRESENTATIVES...

SOLUTIONS MICROSOFT DYNAMICS GP 2010. Business Ready Licensing Product Module Guide

SOLUTIONS MICROSOFT DYNAMICS GP 2010 Business Ready Licensing Product Module Guide Business Ready Licensing for Microsoft Dynamics GP 2010 Microsoft Dynamics business management solutions are designed

SOLUTIONS MICROSOFT DYNAMICS GP 2010 Business Ready Licensing Product Module Guide Business Ready Licensing for Microsoft Dynamics GP 2010 Microsoft Dynamics business management solutions are designed

Risk-Based Assessment of User Access Controls and Segregation of Duties for Companies Running Oracle Applications

Risk-Based Assessment of User Access Controls and Segregation of Duties for Companies Running Oracle Applications Presented by: Jeffrey T. Hare, CPA CISA CIA Webinar Logistics Hide and unhide the Webinar

Risk-Based Assessment of User Access Controls and Segregation of Duties for Companies Running Oracle Applications Presented by: Jeffrey T. Hare, CPA CISA CIA Webinar Logistics Hide and unhide the Webinar

Vendors. Procedure To access the Vendors screen: 1. Select Financials. 2. Select Accounts Payable. 3. Select Vendor Processing. 4. Select Vendors.

Vendors Objective The Vendors screen is used to maintain the vendor file used throughout the financial system. If vendors are to be categorized by type, those types must first be defined by using the Accounts

Vendors Objective The Vendors screen is used to maintain the vendor file used throughout the financial system. If vendors are to be categorized by type, those types must first be defined by using the Accounts

10/13/2015 THE SAGA CONTINUES. An Update on Fraud Issues. Angela R. Morelock, CPA, CFE, CFF, ABV Partner [email protected].

THE SAGA CONTINUES An Update on Fraud Issues October 14, 2015 Angela R. Morelock, CPA, CFE, CFF, ABV Partner [email protected] 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they

THE SAGA CONTINUES An Update on Fraud Issues October 14, 2015 Angela R. Morelock, CPA, CFE, CFF, ABV Partner [email protected] 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they