Introductions, Course Outline, and Other Administration Issues. Ed Ferrara, MSIA, CISSP Copyright 2015 Edward S.

|

|

|

- Justin Rogers

- 8 years ago

- Views:

Transcription

1 MIS 520 Week 2 Fraud Detection & Prevention Introductions, Course Outline, and Other Administration Issues Ed Ferrara, MSIA, CISSP eferrara@forrester.com

2 Fraud Awareness & Internal Controls Awareness Internal Controls Understand Fraud Symptoms Behaviors Data sources Alert Fraudulent behaviors Operational & Control Environment Separation of Duties Account treatments Cybersecurity controls Assess Risk & Exposures Fraud Detection Identify Potential Data Sources for Fraud Detection

3 Risk Factors For Fraud Employee Relationships Attractive Assets Competitive Business Environment Internal Controls Management Environment Fraud Integration of duties

4 Fraud Exposure Fraud Risk Assessment Risk assessment is a sometimes and controversial issue We will have an entire section on risk assessment Examine the risks and exposures to identify process and system weakness Develop Categories of Risk External environment Legal Regulatory Governance Strategy Operational Information Human resources Financial Technology Determining Fraud Exposure Sources of risk Review existing risk assessments Review risk assessment process Business Impact Analysts Types and sources of fraud External environment Governance Legal Regulatory Operational Strategy

5 Risk Factors for Fraud Management Environment Unrealistic Financial Targets Unrealistic Performance Standards Corporate Culture Emphasizing Win At All Costs Evaluate: Company production figures for reasonableness, financial targets, and management s position on same. Competitive & Business Environment Misstatement of Inventory Positions Fraudulent Orders Off Balance Sheet Transactions Evaluate: Recalculate the value of of inventory ensuring it is correctly valued. Employee Relationships Nepotism Insider Trading Collusion Evaluate: Look for nepotism, matching employee and vendor addresses. Attractive Assets Intellectual Property Theft Insider Abuse of Privilege Customer Contact Center Fraud Evaluate: Monetize both physical and information assets for financially based risk assessment. Internal Controls Inadequate internal controls Inventory markdowns Trading Practices Evaluate: Computer systems have necessary corresponding controls, privileged user abuse protection, etc. Separation of Duties Related to Above Reduced Staff Fraud Opportunity Evaluate: Ensure necessary policies, procedures, guidelines and standards are in place.

6 Fraud Schemes A Data Driven Approach Control Weaknesses Approach Examine key controls Determine vulnerabilities System Process Key Fields Focus on data entry Which data can be changed? What is the impact?

7 Control Weakness Internal / External parties Example: Received quantity less than ordered quantity but payment made for full amount Key Fields Data manipulation Privileged user abuse Example: Create fictitious vendors, changing address and bank account.

8 Case Study - Sunbeam

9 Fraud Exposure Identification Control Weakness Perpetrator Data Fields Data Analysis (Tests) Control Weakness Data of Interest

Control Weakness Data")

10 Key Data Vendor Name, Address, Bank Information Who Why Controls Test Clerks & Vendor Duplicate Payments, Fictitious Vendors & Payments Vendor creation, modification, Evaluate: Look for blanks in key fields, look for duplicates in vendor table. Unit Prices Clerk Direct Payments Vendor modification; system log files Evaluate: Look for disparities in unit price and contracted price. Quantities Contracting Officer, Vendor Kickbacks Invoice matching, on order quantity Evaluate: Look for disparities between ordered and delivered quantities. Transaction Amounts Clerk, vendor Overpayment to obtain funds or kickbacks, overcharges Invoice matching, contract amounts Evaluate: Look for disparities between contract and invoice amounts. Dates Clerk, vendor Backdate payment, due dates, backdate to obtain earlier payment Invoice matching, invoice and goods received date Evaluate: Look for transactions where invoice date is less than good receipt.

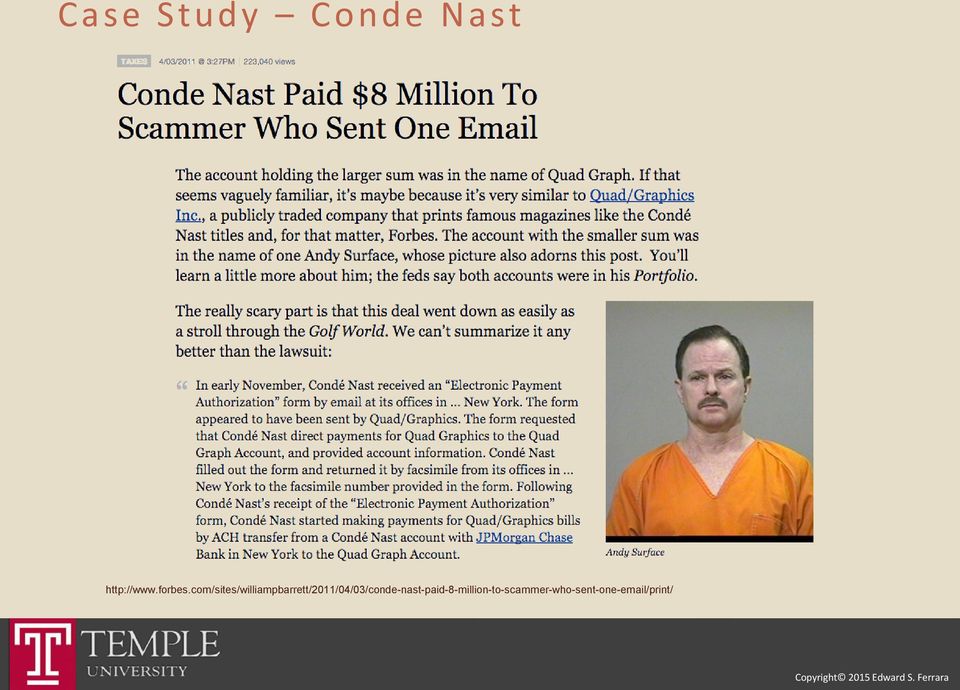

11 Case Study Conde Nast

12 Fraud Standards

13 Investigating Fraud Responsibilities & Limitations SAS 53 SAS 82

14 Investigating Fraud Which of these is true? An audit will: Detect all material errors and irregularities in the financial statements Discover all illegal acts committed by the client Ensure the financial health of the entity

15 Auditors Responsibilities Errors - Unintentional misstatements Mistakes in gathering or processing accounting data Incorrect accounting estimates Mistakes in the application of accounting principles Irregularities - Intentional misstatements, manipulation, falsification, or alteration of accounting records & supporting documents Misrepresentation or intentional omission of events, transactions, or other significant information Intentional misapplication of accounting principles

16 Software Accounting Standards SAS 1 and 22 Plan and perform the audit to provide reasonable assurance that financial statements are free of material misstatements caused by error or fraud. SAS 47 Audit risk, materiality and misstatements in financial statements SAS 54 Detection of illegal acts (AU Section 317) Section 301 of the Private Securities Litigation Reform Act Private Securities Litigation Reform Act of 1995 Section 10(a) of the Exchange Act Requires the inclusion of certain procedures in accordance with generally accepted accounting standards (GAAS). Audit procedures provide reasonable assurance of detecting illegal acts Audit procedures will identify related party transactions material to financial statements Evaluate of there is substantial doubt about the ability of the can stay in business. SAS 82 Auditor s responsibility related to fraud in a financial statement Provides guidance on what auditors should do to meet these responsibilities Describes: Fraudulent Financial Reporting Misappropriation of Assets

17 SAS 82 Requirements Consider the presence of fraud risk factors. - SAS No. 82 provides examples (detailed below) of risk factors an auditor may consider for fraud related to a) fraudulent financial reporting, and b) misappropriation of assets misstatements. An auditor should become familiar with these risk factors and be alert for their presence at the client s. Assess the risk of material misstatement of the financial statements due to fraud. SAS No. 82 requires an assessment as to the risk of material misstatement due to fraud. This assessment is separate from but may be performed in conjunction with other risk assessments (for example, control or inherent risk) made during the audit. SAS No. 82 also requires reevaluation of assessments if other conditions are identified during fieldwork. Develop a response. Based on assessments of risk, SAS No. 82 requires development of appropriate audit response. In some circumstances, an auditor s response may be that existing audit procedures are sufficient to obtain reasonable assurance that the financial statements are free of material misstatement due to fraud. In other circumstances, auditors may decide to extend planned audit procedures. Document certain items in work papers. SAS No. 82 requires auditors to document evidence of the performance of their assessment of risk of material misstatement due to fraud. Documentation should include risk factors identified as being present as well as the auditor s response to these risk factors. Communicate to management. If it is determined that there is evidence that a fraud may exist, an auditor should apprise the appropriate level of management, even if the matter may be considered inconsequential. SAS No. 82 also requires an auditor to communicate directly with the audit committee (or equivalent) if the matter involves fraud that would materially misstate the financial statements or fraud committed by senior management

18 Fraud Investigation

19 Fraud Types Billing - Cash Larceny Cash on Hand Check Tampering Corruption Financial Statement Fraud Non-Cash Payroll Register Disbursements Skimming

20 Fraud Analysis: Useful Information Issues Conflicts of interest Unknown relationships Abnormal patterns of activity Errors in key processes Control weaknesses Hindsight, insight, foresight Business Operations and Expense Areas Accounts payable Claims Damaged Goods Healthcare Insurance Loss Expense reimbursement General Ledger Travel and Entertainment

21 Vendor Attribute Capture Total number of vendors Vendors without: Addresses TAX ID Are they receiving payment? Electronic transfers Paper checks

22 Vendor Activity Assessment Number of Vendors Frequency of Use Number of Active Users Compared Against Total Vendors Unused Vendors can be source of internal abuse Vendor Identity Abuse

23 Name Mining Looking for Fictitious Vendors Fictitious Names Use their initials in the name of a vendor Anagrams Others Substitution Insertion and Omission Transposition Number Substitution

24 Employee Vendor Relationships Employee and Vendor Name are Different Common Addresses Addresses that are different but are at the same geographic location: 201 College Avenue 669 West Chestnut Street Phone Number TAX ID Zip Codes

25 Proximity Analysis Mailbox Services Anonymous These mail drop have the appearance of a physical address Proximity location of vendor to actual employees Employee Addresses Vendor Addresses Proximity Analysis

26 Vendor Trending Analysis Accounts Payable Claims Payable Fraud Payment Acceleration Small initial amounts of fraud Amounts and frequency increases Test Phase Confidence Phase Greed Phase Trend Payments to Vendors Valley and Spike Payment Patterns Long periods of inactivity between periods of very high activity Unusually high periods of activity

27 Payment Trend Analysis Calendar By Day of Week By Day of Month By Month Checks created on weekends (Saturdays and Sundays) Date created Date posted Benford s Law The first digit should be a 1

28 Benford s Law McGinty, J. C. (2014). Accountants Increasingly Use Data Analysis to Catch Fraud - Auditors Wield Mathematical Weapons to Detect Cheating. The Wall Street Journal. (Web Site)

29 Check Sequence Analysis G/L Cash Receipts Identify Gaps in Check Sequences

30 Expense, Payroll, and Vacation Controls Analysis of Overtime Hours Reasonableness Consistent with role Holiday Hours Reasonableness Consistent with role Purchasing Cards Spending over approval limits Split transactions to avoid limit Collusion between subordinate and supervisor to avoid approval scrutiny Vacation Hours Reasonableness Consistent with role Large amounts of vacation outside of guidelines

31 Other Analysis Areas System Access Logs Maintenance Files Social Media The Price is Right Fraud Physical Investigations Surveillance

32 Continuous Auditing Programmatic Auditing System Based Source: Cser, A. (2010).Market Overview: Fraud Management Solutions - Seven Tenets Of Effectively Combating Fraud Costs. Forrester Research.

33 Thank you.

Accounts Payable Best Practices

Accounts Payable Best Practices Presented by: Eddy Castaneda, CPA, MBA Accounts Payable Best Practices Top Practices AP Top Practices Document your current AP procedures Can identify overlapping work Can

Accounts Payable Best Practices Presented by: Eddy Castaneda, CPA, MBA Accounts Payable Best Practices Top Practices AP Top Practices Document your current AP procedures Can identify overlapping work Can

Fraud Awareness Training

UT System Administration General Compliance Training Fall 2014 This training will take approximately 20 minutes to complete Objectives What is occupational fraud Common myths about fraud Conditions for

UT System Administration General Compliance Training Fall 2014 This training will take approximately 20 minutes to complete Objectives What is occupational fraud Common myths about fraud Conditions for

Leveraging Big Data to Mitigate Health Care Fraud Risk

Leveraging Big Data to Mitigate Health Care Fraud Risk Jeremy Clopton, CPA, CFE, ACDA Senior Managing Consultant BKD, LLP Forensics & Valuation Services Introduction Health Care Is Victimized by Fraud

Leveraging Big Data to Mitigate Health Care Fraud Risk Jeremy Clopton, CPA, CFE, ACDA Senior Managing Consultant BKD, LLP Forensics & Valuation Services Introduction Health Care Is Victimized by Fraud

Internal Controls for Small Organizations. Jen Parker, CPA Director of Accounting & Finance US Youth Soccer

Internal Controls for Small Organizations Jen Parker, CPA Director of Accounting & Finance US Youth Soccer Fraud Statistics: The following statistics about fraud and white collar crime are from the Association

Internal Controls for Small Organizations Jen Parker, CPA Director of Accounting & Finance US Youth Soccer Fraud Statistics: The following statistics about fraud and white collar crime are from the Association

INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS CONTENTS

240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS CONTENTS") INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS CONTENTS Paragraphs Introduction... 1-3 Characteristics of Fraud...

INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS CONTENTS Paragraphs Introduction... 1-3 Characteristics of Fraud...

INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 240 THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS

240 THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS") INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 240 Introduction THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS (Effective for audits of financial statements for

INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 240 Introduction THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS (Effective for audits of financial statements for

FRAUD RISK ASSESSMENT

FRAUD RISK ASSESSMENT All agencies are subject to fraud risks and need to complete a fraud risk assessment for their agency at least every biennium. A detailed fraud assessment needs to be performed by

FRAUD RISK ASSESSMENT All agencies are subject to fraud risks and need to complete a fraud risk assessment for their agency at least every biennium. A detailed fraud assessment needs to be performed by

Fundamentals of Computer and Internet Fraud WORLD HEADQUARTERS THE GREGOR BUILDING 716 WEST AVE AUSTIN, TX 78701-2727 USA

Fundamentals of Computer and Internet Fraud WORLD HEADQUARTERS THE GREGOR BUILDING 716 WEST AVE AUSTIN, TX 78701-2727 USA II. THE USE OF COMPUTERS IN OCCUPATIONAL FRAUD Occupational fraud refers to the

Fundamentals of Computer and Internet Fraud WORLD HEADQUARTERS THE GREGOR BUILDING 716 WEST AVE AUSTIN, TX 78701-2727 USA II. THE USE OF COMPUTERS IN OCCUPATIONAL FRAUD Occupational fraud refers to the

Fraud and Fraud Detection. A Data Analytics Approach + Website. Wiley Corporate F&A

Brochure More information from http://www.researchandmarkets.com/reports/2866056/ Fraud and Fraud Detection. A Data Analytics Approach + Website. Wiley Corporate F&A Description: Detect fraud faster no

Brochure More information from http://www.researchandmarkets.com/reports/2866056/ Fraud and Fraud Detection. A Data Analytics Approach + Website. Wiley Corporate F&A Description: Detect fraud faster no

Contents. xiii xv. Case Studies Preface

Case Studies Preface xiii xv CHAPTER 1 What Is Fraud? 1 Fraud: A Definition 3 Why Fraud Happens 4 Who Is Responsible for Fraud Detection? 7 What Is a Fraud Awareness Program? 11 Screening Job Applicants

Case Studies Preface xiii xv CHAPTER 1 What Is Fraud? 1 Fraud: A Definition 3 Why Fraud Happens 4 Who Is Responsible for Fraud Detection? 7 What Is a Fraud Awareness Program? 11 Screening Job Applicants

Using Technology to Automate Fraud Detection Within Key Business Process Areas

Using Technology to Automate Fraud Detection Within Key Business Process Areas 2013 ACFE Canadian Fraud Conference September 10, 2013 John Verver, CA, CISA, CMA Vice President, Strategy ACL Services Ltd

Using Technology to Automate Fraud Detection Within Key Business Process Areas 2013 ACFE Canadian Fraud Conference September 10, 2013 John Verver, CA, CISA, CMA Vice President, Strategy ACL Services Ltd

Advanced Data Analytics, the Fraudsters Worst Enemy

Advanced Data Analytics, the Fraudsters Worst Enemy Introducing Powerful Tools and Techniques to Uncover Fraud Agenda Overview of data analytics in the anti-fraud and fraud investigation context Capability

Advanced Data Analytics, the Fraudsters Worst Enemy Introducing Powerful Tools and Techniques to Uncover Fraud Agenda Overview of data analytics in the anti-fraud and fraud investigation context Capability

Fraud Awareness and Prevention Program Report

Internal Audit Department Fraud Awareness and Prevention Program Report Project 2009-263 A Review of Fraud Awareness, Prevention, Detection and Risk Mitigation Practices in Landfill Operations, Central

Internal Audit Department Fraud Awareness and Prevention Program Report Project 2009-263 A Review of Fraud Awareness, Prevention, Detection and Risk Mitigation Practices in Landfill Operations, Central

The Auditor s Responsibilities Relating to Fraud in an Audit of Financial Statements

ISA 240 February 2008 International Standard on Auditing The Auditor s Responsibilities Relating to Fraud in an Audit of Financial Statements INTERNATIONAL STANDARD ON AUDITING 240 The Auditor s Responsibilities

ISA 240 February 2008 International Standard on Auditing The Auditor s Responsibilities Relating to Fraud in an Audit of Financial Statements INTERNATIONAL STANDARD ON AUDITING 240 The Auditor s Responsibilities

Presented by: Donald F. Conway, CPA Mercadien, P.C., Certified Public Accountants. Forensic Accounting, Political Corruption & White Collar Offenses

Presented by: Donald F. Conway, CPA Mercadien, P.C., Certified Public Accountants Forensic Accounting, Political Corruption & White Collar Offenses Defining Fraud The dictionary defines fraud as a deception

Presented by: Donald F. Conway, CPA Mercadien, P.C., Certified Public Accountants Forensic Accounting, Political Corruption & White Collar Offenses Defining Fraud The dictionary defines fraud as a deception

Fraud Prevention: The Prevention and Detection of Fraud Begins with You

Fraud Prevention: The Prevention and Detection of Fraud Begins with You Takeaways What is fraud? Definition Facts Four factors Fraud risk assessment Four evaluation criteria Common fraud schemes Case studies

Fraud Prevention: The Prevention and Detection of Fraud Begins with You Takeaways What is fraud? Definition Facts Four factors Fraud risk assessment Four evaluation criteria Common fraud schemes Case studies

Chapter 15 Auditing the Expenditure Cycle

Chapter 15 Auditing the Expenditure Cycle Expenditure cycle consists of activities related to the acquisition of and payment for plant assets and goods and services. Two major transaction classes: 1 purchases

Chapter 15 Auditing the Expenditure Cycle Expenditure cycle consists of activities related to the acquisition of and payment for plant assets and goods and services. Two major transaction classes: 1 purchases

How To Handle A Fraud At Psc

FRAUD POLICY Purpose and Background PSC is committed to the highest standards of moral and ethical behavior. The purpose of PSC s Fraud Policy is to foster an environment that promotes awareness to fraudulent

FRAUD POLICY Purpose and Background PSC is committed to the highest standards of moral and ethical behavior. The purpose of PSC s Fraud Policy is to foster an environment that promotes awareness to fraudulent

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS CONTENTS

INTERNATIONAL STANDARD ON 240 THE AUDITOR S RESPONSIBILITIES RELATING TO (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph Introduction

INTERNATIONAL STANDARD ON 240 THE AUDITOR S RESPONSIBILITIES RELATING TO (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph Introduction

716 West Ave Austin, TX 78701-2727 USA

Fundamentals of Computer and Internet Fraud GLOBAL Headquarters the gregor building 716 West Ave Austin, TX 78701-2727 USA II. THE USE OF COMPUTERS IN OCCUPATIONAL FRAUD Occupational fraud refers to the

Fundamentals of Computer and Internet Fraud GLOBAL Headquarters the gregor building 716 West Ave Austin, TX 78701-2727 USA II. THE USE OF COMPUTERS IN OCCUPATIONAL FRAUD Occupational fraud refers to the

Is There Anyway to Prevent Fraud? Bill Gady, CGA CPA Partner

Is There Anyway to Prevent Fraud? Bill Gady, CGA CPA Partner Learning Objectives: Understand how fraud can occur Learn procedures you can implement to prevent fraud Learn how to detect fraud Common Situations

Is There Anyway to Prevent Fraud? Bill Gady, CGA CPA Partner Learning Objectives: Understand how fraud can occur Learn procedures you can implement to prevent fraud Learn how to detect fraud Common Situations

INTRODUCTION TO FRAUD EXAMINATION

INTRODUCTION TO FRAUD EXAMINATION GLOBAL HEADQUARTERS THE GREGOR BUILDING 716 WEST AVE AUSTIN, TX 78701-2727 USA VII. FRAUDULENT FINANCIAL TRANSACTIONS: FRAUD SCHEMES Introduction Fraud can be committed

INTRODUCTION TO FRAUD EXAMINATION GLOBAL HEADQUARTERS THE GREGOR BUILDING 716 WEST AVE AUSTIN, TX 78701-2727 USA VII. FRAUDULENT FINANCIAL TRANSACTIONS: FRAUD SCHEMES Introduction Fraud can be committed

TITLE: Fraud Prevention and Detection Program IDENTIFIER: S-FW-LD-1008 APPROVED: Executive Cabinet (Pending)

") PAGE 1 of 5 TITLE: Fraud Prevention and Detection Program IDENTIFIER: S-FW-LD-1008 APPROVED: Executive Cabinet (Pending) ORIGINAL: 11/03 REVISED: 10/07, 09/10, 04/13 REVIEWED: EFFECTIVE DATE Acute Care

PAGE 1 of 5 TITLE: Fraud Prevention and Detection Program IDENTIFIER: S-FW-LD-1008 APPROVED: Executive Cabinet (Pending) ORIGINAL: 11/03 REVISED: 10/07, 09/10, 04/13 REVIEWED: EFFECTIVE DATE Acute Care

Procurement Fraud Identification & Role of Data Mining

The paper describes the known boundaries of Procurement Fraud and outlines the scope of data mining within the same. The paper also highlights some of the basic steps to be taken care of before the application

The paper describes the known boundaries of Procurement Fraud and outlines the scope of data mining within the same. The paper also highlights some of the basic steps to be taken care of before the application

Perp Poetry. Fraud & Embezzlement: Lessons From the Trenches. Presented by. acumen insight. ideas attention reach. expertise depth agility talent

acumen insight Fraud & Embezzlement: Lessons From the Trenches ideas attention reach Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant www.bkdforensics.com expertise depth

acumen insight Fraud & Embezzlement: Lessons From the Trenches ideas attention reach Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant www.bkdforensics.com expertise depth

5 Important Controls to Mitigate Employee Fraud

5 Important Controls to Mitigate Employee Fraud LMCIT WEBINAR : FEBRUARY 10, 2015 IN PARTNERSHIP WITH EIDE BAILLY Presenter: Jason Olson, MBA, CPA/CFF, CFE, CFI Presentation Disclaimer These seminar materials

5 Important Controls to Mitigate Employee Fraud LMCIT WEBINAR : FEBRUARY 10, 2015 IN PARTNERSHIP WITH EIDE BAILLY Presenter: Jason Olson, MBA, CPA/CFF, CFE, CFI Presentation Disclaimer These seminar materials

Financial Policies Training: Financial Fraud Prevention (1.3.1) Effective: May 1, 2009

Effective: May 1, 2009") Financial Policies Training: Financial Fraud Prevention (1.3.1) Effective: May 1, 2009 These PowerPoint slides are intended for training purposes. In the event of any discrepancy or interpretation difference

Financial Policies Training: Financial Fraud Prevention (1.3.1) Effective: May 1, 2009 These PowerPoint slides are intended for training purposes. In the event of any discrepancy or interpretation difference

Consideration of Fraud in a Financial Statement Audit

Consideration of Fraud in a Financial Statement Audit 1719 AU Section 316 Consideration of Fraud in a Financial Statement Audit (Supersedes SAS No. 82.) Source: SAS No. 99; SAS No. 113. Effective for audits

Consideration of Fraud in a Financial Statement Audit 1719 AU Section 316 Consideration of Fraud in a Financial Statement Audit (Supersedes SAS No. 82.) Source: SAS No. 99; SAS No. 113. Effective for audits

NONPROFIT FINANCIAL MANAGEMENT SELF ASSESSMENT TOOL

NONPROFIT FINANCIAL MANAGEMENT SELF ASSESSMENT TOOL I. Financial Planning/Budget Systems 1. Organization has a comprehensive annual budget which includes all sources and uses of funds for all aspects of

NONPROFIT FINANCIAL MANAGEMENT SELF ASSESSMENT TOOL I. Financial Planning/Budget Systems 1. Organization has a comprehensive annual budget which includes all sources and uses of funds for all aspects of

Consideration of Fraud in a Financial Statement Audit

Consideration of Fraud in a Financial Statement Audit 151 AU-C Section 240 Consideration of Fraud in a Financial Statement Audit Source: SAS No. 122; SAS No. 128. Effective for audits of financial statements

Consideration of Fraud in a Financial Statement Audit 151 AU-C Section 240 Consideration of Fraud in a Financial Statement Audit Source: SAS No. 122; SAS No. 128. Effective for audits of financial statements

Auditing Standard ASA 240 The Auditor's Responsibilities Relating to Fraud in an Audit of a Financial Report

Compiled Auditing Standard ASA 240 (November 2013) Auditing Standard ASA 240 The Auditor's Responsibilities Relating to Fraud in an Audit of a Financial Report This compilation was prepared on 11 November

Compiled Auditing Standard ASA 240 (November 2013) Auditing Standard ASA 240 The Auditor's Responsibilities Relating to Fraud in an Audit of a Financial Report This compilation was prepared on 11 November

Performing Audit Procedures in Response to Assessed Risks and Evaluating the Audit Evidence Obtained

Performing Audit Procedures in Response to Assessed Risks 1781 AU Section 318 Performing Audit Procedures in Response to Assessed Risks and Evaluating the Audit Evidence Obtained (Supersedes SAS No. 55.)

Performing Audit Procedures in Response to Assessed Risks 1781 AU Section 318 Performing Audit Procedures in Response to Assessed Risks and Evaluating the Audit Evidence Obtained (Supersedes SAS No. 55.)

Payment Procedures. Corruption Prevention Department

Payment Procedures Corruption Prevention Department best practices 貪 CONTENTS Pages Introduction 1 Procedural Guidelines 1 Payment Methods 2 Autopay 2 Cheques 3 Petty Cash 3 Payment Records 4 Control and

Payment Procedures Corruption Prevention Department best practices 貪 CONTENTS Pages Introduction 1 Procedural Guidelines 1 Payment Methods 2 Autopay 2 Cheques 3 Petty Cash 3 Payment Records 4 Control and

Introduction to Fraud Examination. World Headquarters the gregor building 716 West Ave Austin, TX 78701-2727 USA

Introduction to Fraud Examination World Headquarters the gregor building 716 West Ave Austin, TX 78701-2727 USA VII. FRAUDULENT FINANCIAL TRANSACTIONS: FRAUD SCHEMES Introduction Fraud can be committed

Introduction to Fraud Examination World Headquarters the gregor building 716 West Ave Austin, TX 78701-2727 USA VII. FRAUDULENT FINANCIAL TRANSACTIONS: FRAUD SCHEMES Introduction Fraud can be committed

Centre for Corporate Governance. Sample listing of fraud schemes

Centre for Corporate Governance Sample listing of fraud schemes Sample listing of fraud schemes The following listing of possible fraud schemes can be utilized by management and auditors to assist in identifying

Centre for Corporate Governance Sample listing of fraud schemes Sample listing of fraud schemes The following listing of possible fraud schemes can be utilized by management and auditors to assist in identifying

Office of the Inspector General

Office of the Inspector General Commonwealth of Massachusetts Gregory W. Sullivan Inspector General Guide to Developing and Implementing Fraud Prevention Programs April 2005 Dear Public Officials: April

Office of the Inspector General Commonwealth of Massachusetts Gregory W. Sullivan Inspector General Guide to Developing and Implementing Fraud Prevention Programs April 2005 Dear Public Officials: April

Fraud Detection & Data Analytics

September 2008 Fraud Detection & Data Analytics How to Utilize CAATs to detect fraud AN INDEPENDENT MEMBER OF BAKER TILLY INTERNATIONAL 505 AFFILIATE OFFICES WORLDWIDE Course Topics Overview of Data Analytics

September 2008 Fraud Detection & Data Analytics How to Utilize CAATs to detect fraud AN INDEPENDENT MEMBER OF BAKER TILLY INTERNATIONAL 505 AFFILIATE OFFICES WORLDWIDE Course Topics Overview of Data Analytics

Webster County Procurement Procedures and County Clerk

Thomas A. Schweich Missouri State Auditor FOLLOW-UP REPORT ON AUDIT FINDINGS Webster County Procurement Procedures and County Clerk November 2014 http://auditor.mo.gov Report No. 2014-118 Follow-Up Report

Thomas A. Schweich Missouri State Auditor FOLLOW-UP REPORT ON AUDIT FINDINGS Webster County Procurement Procedures and County Clerk November 2014 http://auditor.mo.gov Report No. 2014-118 Follow-Up Report

Fraud and internal controls, Part 3: Internal fraud schemes

Fraud and internal controls, Part 3: Internal fraud schemes By EVERETT COLBY, CFE, FCGA This is the third and final article in a series by Mr. Colby on Fraud and internal controls to be carried on PD Net.

Fraud and internal controls, Part 3: Internal fraud schemes By EVERETT COLBY, CFE, FCGA This is the third and final article in a series by Mr. Colby on Fraud and internal controls to be carried on PD Net.

COMPLIANCE POLICY MANUAL

COMPLIANCE POLICY MANUAL FOREIGN CORRUPT PRACTICES ACT 07/24/2012 Policy Number 16-100 SUBJECT: FOREIGN CORRUPT PRACTICES ACT Application: Worldwide Strategic Business Units and Subsidiaries. It is the

COMPLIANCE POLICY MANUAL FOREIGN CORRUPT PRACTICES ACT 07/24/2012 Policy Number 16-100 SUBJECT: FOREIGN CORRUPT PRACTICES ACT Application: Worldwide Strategic Business Units and Subsidiaries. It is the

Before beginning the study of how to conduct an audit, it is necessary to understand

Before beginning the study of how to conduct an audit, it is necessary to understand the overall objectives of the audit, the auditor s responsibilities in conducting the audit, and the specific objectives

Before beginning the study of how to conduct an audit, it is necessary to understand the overall objectives of the audit, the auditor s responsibilities in conducting the audit, and the specific objectives

Financial Transactions and Fraud Schemes

Financial Transactions and Fraud Schemes Asset Misappropriation: Fraudulent Disbursements Fraudulent Disbursement Schemes Register disbursement schemes Check tampering schemes Payroll schemes Billing schemes

Financial Transactions and Fraud Schemes Asset Misappropriation: Fraudulent Disbursements Fraudulent Disbursement Schemes Register disbursement schemes Check tampering schemes Payroll schemes Billing schemes

Fraud: Real Stories, Real People, Real Impact

Fraud: Real Stories, Real People, Real Impact Chris Harper, CPA, MBA Senior Manager Types of Fraud Asset misappropriation Fraudulent financial reporting Identity theft Detection Skills The Fraud Triangle

Fraud: Real Stories, Real People, Real Impact Chris Harper, CPA, MBA Senior Manager Types of Fraud Asset misappropriation Fraudulent financial reporting Identity theft Detection Skills The Fraud Triangle

INTERNAL ACCOUNTING CONTROLS CHECKLIST FOR NTMA CHAPTERS

P R E C I S I O N INTERNAL ACCOUNTING CONTROLS CHECKLIST FOR NTMA CHAPTERS Presented at NTMA 2004 Annual Convention Palm Springs, CA February 2004 National Tooling & Machining Association 9300 Livingston

P R E C I S I O N INTERNAL ACCOUNTING CONTROLS CHECKLIST FOR NTMA CHAPTERS Presented at NTMA 2004 Annual Convention Palm Springs, CA February 2004 National Tooling & Machining Association 9300 Livingston

Accounts Payable Fraud Services

Accounts Payable Fraud Services According to research conducted by the Association of Certified Fraud Examiners (ACFE), U.S. organizations lose an estimated 7 percent of annual revenues to fraud. 1 In

Accounts Payable Fraud Services According to research conducted by the Association of Certified Fraud Examiners (ACFE), U.S. organizations lose an estimated 7 percent of annual revenues to fraud. 1 In

GLOBAL PORTS INVESTMENTS PLC

Adopted by the Directors of GLOBAL PORTS INVESTMENTS PLC Resolution of 14 July 2008 GLOBAL PORTS INVESTMENTS PLC (previously GLOBAL PORTS INVESTMENTS LTD) ANTI-FRAUD POLICY TABLE OF CONTENTS 1. INTRODUCTION.....

Adopted by the Directors of GLOBAL PORTS INVESTMENTS PLC Resolution of 14 July 2008 GLOBAL PORTS INVESTMENTS PLC (previously GLOBAL PORTS INVESTMENTS LTD) ANTI-FRAUD POLICY TABLE OF CONTENTS 1. INTRODUCTION.....

Using Forensic Accounting to Detect Fraud in Public Service Organizations. Kevin M. Bronner, Ph.D. 1

Using Forensic Accounting to Detect Fraud in Public Service Organizations By Kevin M. Bronner, Ph.D. 1 Forensic accounting is a useful technique to detect fraud in public service organizations. This paper

Using Forensic Accounting to Detect Fraud in Public Service Organizations By Kevin M. Bronner, Ph.D. 1 Forensic accounting is a useful technique to detect fraud in public service organizations. This paper

AGA Kansas City Chapter Data Analytics & Continuous Monitoring

AGA Kansas City Chapter Data Analytics & Continuous Monitoring Agenda Market Overview & Drivers for Change Key challenges that organizations face Data Analytics What is data analytics and how can it help

AGA Kansas City Chapter Data Analytics & Continuous Monitoring Agenda Market Overview & Drivers for Change Key challenges that organizations face Data Analytics What is data analytics and how can it help

by: Scott Baranowski, CIA

Community Bank Auditors Group A/P, Procurement and Credit Card Internal Controls June 4, 2014 by: Scott Baranowski, CIA MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2013 Wolf

Community Bank Auditors Group A/P, Procurement and Credit Card Internal Controls June 4, 2014 by: Scott Baranowski, CIA MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2013 Wolf

ACL EBOOK. Detecting and Preventing Fraud with Data Analytics

ACL EBOOK Detecting and Preventing Fraud with Data Analytics Contents Why use data analysis for fraud?... 4 Internal control systems, while good, are not good enough... 5 Purpose-built data analytics is

ACL EBOOK Detecting and Preventing Fraud with Data Analytics Contents Why use data analysis for fraud?... 4 Internal control systems, while good, are not good enough... 5 Purpose-built data analytics is

Fraud Issues in Local Government

Fraud Issues in Local Government CMTA Annual Conference April 24, 2009 Justin Williams, CPA, CVA Fraud Triangle In normal circumstances, all three factors must be present Pressures Opportunity Rationalization

Fraud Issues in Local Government CMTA Annual Conference April 24, 2009 Justin Williams, CPA, CVA Fraud Triangle In normal circumstances, all three factors must be present Pressures Opportunity Rationalization

Audit Risk and Materiality in Conducting an Audit

Audit Risk and Materiality in Conducting an Audit 1647 AU Section 312 Audit Risk and Materiality in Conducting an Audit (Supersedes SAS No. 47.) Source: SAS No. 107. See section 9312 for interpretations

Audit Risk and Materiality in Conducting an Audit 1647 AU Section 312 Audit Risk and Materiality in Conducting an Audit (Supersedes SAS No. 47.) Source: SAS No. 107. See section 9312 for interpretations

Internal Controls and Fraud Detection & Prevention. Harold Monk and Jennifer Christensen

Internal Controls and Fraud Detection & Prevention Harold Monk and Jennifer Christensen 1 Common Fraud Statements Everyone in government has an honest and charitable heart. It may happen other places,

Internal Controls and Fraud Detection & Prevention Harold Monk and Jennifer Christensen 1 Common Fraud Statements Everyone in government has an honest and charitable heart. It may happen other places,

The Confirmation Process

The Confirmation Process 1897 AU Section 330 The Confirmation Process (Supersedes section 331.03.08.) Source: SAS No. 67. Effective for audits of fiscal periods ending after June 15, 1992, unless otherwise

The Confirmation Process 1897 AU Section 330 The Confirmation Process (Supersedes section 331.03.08.) Source: SAS No. 67. Effective for audits of fiscal periods ending after June 15, 1992, unless otherwise

A DOZEN IDEAS FOR SMALL BUSINESS FRAUD PREVENTION

A DOZEN IDEAS FOR SMALL BUSINESS FRAUD PREVENTION Any discussion of fraud can be a difficult one because most individuals value being a trusted member of any organization and, in most cases, key employees

A DOZEN IDEAS FOR SMALL BUSINESS FRAUD PREVENTION Any discussion of fraud can be a difficult one because most individuals value being a trusted member of any organization and, in most cases, key employees

Sharon Kurek, CPA, CFE Director of Internal Audit

Sharon Kurek, CPA, CFE Director of Internal Audit What You Will Take Aware With You Definition of Internal Auditing Scope of Audit Activities Risk and Control Process Common Audit Topics Fraud Awareness

Sharon Kurek, CPA, CFE Director of Internal Audit What You Will Take Aware With You Definition of Internal Auditing Scope of Audit Activities Risk and Control Process Common Audit Topics Fraud Awareness

Red Flags for Fraud. Thomas P. DiNapoli. Steven J. Hancox Deputy Comptroller Division of Local Government and School Accountability

Thomas P. DiNapoli State of New York Office of the State Comptroller Red Flags for Fraud Steven J. Hancox Deputy Comptroller Division of Local Government and School Accountability Introduction Why didn

Thomas P. DiNapoli State of New York Office of the State Comptroller Red Flags for Fraud Steven J. Hancox Deputy Comptroller Division of Local Government and School Accountability Introduction Why didn

Fraud Prevention, Detection and Response. Dean Bunch, Ernst & Young Fraud Investigation & Dispute Services

Fraud Prevention, Detection and Response. Dean Bunch, Ernst & Young Fraud Investigation & Dispute Services Agenda Fraud Overview Fraud Prevention Fraud Detection Fraud Response Questions Page 2 Fraud Overview

Fraud Prevention, Detection and Response. Dean Bunch, Ernst & Young Fraud Investigation & Dispute Services Agenda Fraud Overview Fraud Prevention Fraud Detection Fraud Response Questions Page 2 Fraud Overview

Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement

Understanding the Entity and Its Environment 1667 AU Section 314 Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement (Supersedes SAS No. 55.) Source: SAS No. 109.

Understanding the Entity and Its Environment 1667 AU Section 314 Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement (Supersedes SAS No. 55.) Source: SAS No. 109.

Internal Control Requirements December 11, 2002

1 Internal Control Requirements December 11, 2002 Internal controls are mechanisms, policies, and procedures used to minimize and monitor operational risks. In order to deter employees and/or members from

1 Internal Control Requirements December 11, 2002 Internal controls are mechanisms, policies, and procedures used to minimize and monitor operational risks. In order to deter employees and/or members from

The auditors responsibility to consider fraud in an audit of financial statements

The auditors responsibility to consider fraud in an audit of financial statements Audit in a nutshell Reality Picture (= financial statements) Balance sheet Assets Liabilities Equity Process Detection

The auditors responsibility to consider fraud in an audit of financial statements Audit in a nutshell Reality Picture (= financial statements) Balance sheet Assets Liabilities Equity Process Detection

ACCOUNTING AND FINANCIAL REPORTING REGULATION MANUAL

ACCOUNTING AND FINANCIAL REPORTING REGULATION MANUAL STATE BOARD OF ACCOUNTS 302 West Washington Street Room E418 Indianapolis, Indiana 46204-2769 Issued January 2011 Revised April 2012 TABLE OF CONTENTS

ACCOUNTING AND FINANCIAL REPORTING REGULATION MANUAL STATE BOARD OF ACCOUNTS 302 West Washington Street Room E418 Indianapolis, Indiana 46204-2769 Issued January 2011 Revised April 2012 TABLE OF CONTENTS

Internal Control Systems

D. INTERNAL CONTROL 1. Internal Control Systems 2. The Use of Internal Control Systems by Auditors 3. Transaction Cycles 4. Tests of Control 5. The Evaluation of Internal Control Component 6. Communication

D. INTERNAL CONTROL 1. Internal Control Systems 2. The Use of Internal Control Systems by Auditors 3. Transaction Cycles 4. Tests of Control 5. The Evaluation of Internal Control Component 6. Communication

SAMPLE FRAMEWORK FOR A FRAUD CONTROL POLICY

SAMPLE FRAMEWORK FOR A FRAUD CONTROL POLICY NOTE: This appendix is a sample from another entity. As such, no adjustment has been made to this material. The information may or may not agree with all the

SAMPLE FRAMEWORK FOR A FRAUD CONTROL POLICY NOTE: This appendix is a sample from another entity. As such, no adjustment has been made to this material. The information may or may not agree with all the

September 28, 2011. Audit s Role in Governance, Risk Management and Internal Control

September 28, 2011 Internal Audit Overview Audit s Role in Governance, Risk Management and Internal Control Mission Provide independent, objective assurance and advisory services designed to add value

September 28, 2011 Internal Audit Overview Audit s Role in Governance, Risk Management and Internal Control Mission Provide independent, objective assurance and advisory services designed to add value

Fraud Prevention and Detection in a Manufacturing Environment

Fraud Prevention and Detection in a Manufacturing Environment Introduction The Association of Certified Fraud Examiners (ACFE) estimated in its 2008 Report to the Nation on Occupational Fraud and Abuse

Fraud Prevention and Detection in a Manufacturing Environment Introduction The Association of Certified Fraud Examiners (ACFE) estimated in its 2008 Report to the Nation on Occupational Fraud and Abuse

Internal Controls, Fraud Detection and ERP

Internal Controls, Fraud Detection and ERP Recently the SEC adopted Section 404 of the Sarbanes Oxley Act. This law requires each annual report of a company to contain 1. A statement of management's responsibility

Internal Controls, Fraud Detection and ERP Recently the SEC adopted Section 404 of the Sarbanes Oxley Act. This law requires each annual report of a company to contain 1. A statement of management's responsibility

Internal Control Guidelines

Internal Control Guidelines The four basic functions of management are usually described as planning, organizing, directing, and controlling. Internal control is what we mean when we discuss the fourth

Internal Control Guidelines The four basic functions of management are usually described as planning, organizing, directing, and controlling. Internal control is what we mean when we discuss the fourth

Audit Guide for Audit Committees of Small Nonprofit Organizations

Audit Guide for Audit Committees of Small Nonprofit Organizations A free resource provided by the Virginia Society of Certified Public Accountants Audit Guide for Small Nonprofit Organizations A free resource

Audit Guide for Audit Committees of Small Nonprofit Organizations A free resource provided by the Virginia Society of Certified Public Accountants Audit Guide for Small Nonprofit Organizations A free resource

FRAUD RISK IN PUBLIC PROCUREMENT NATIONAL PUBLIC ENTITIES RISK MANAGEMENT FORUM

FRAUD RISK IN PUBLIC PROCUREMENT NATIONAL PUBLIC ENTITIES RISK MANAGEMENT FORUM Presenter: Zamani Nxumalo SAS, National Treasury 30 March 2011 CONTENTS Key Terms & Definitions Process & Challenges Fraud

FRAUD RISK IN PUBLIC PROCUREMENT NATIONAL PUBLIC ENTITIES RISK MANAGEMENT FORUM Presenter: Zamani Nxumalo SAS, National Treasury 30 March 2011 CONTENTS Key Terms & Definitions Process & Challenges Fraud

STATEMENT OF AUDITING STANDARDS 110 THE AUDITORS' RESPONSIBILITY TO CONSIDER FRAUD AND ERROR IN AN AUDIT OF FINANCIAL STATEMENTS

SAS 110 (October 04) SAS 110 (February 02) STATEMENT OF AUDITING STANDARDS 110 THE AUDITORS' RESPONSIBILITY TO CONSIDER FRAUD AND ERROR IN AN AUDIT OF FINANCIAL STATEMENTS (Effective for audits of financial

SAS 110 (October 04) SAS 110 (February 02) STATEMENT OF AUDITING STANDARDS 110 THE AUDITORS' RESPONSIBILITY TO CONSIDER FRAUD AND ERROR IN AN AUDIT OF FINANCIAL STATEMENTS (Effective for audits of financial

GENERAL PAYROLL CONTROLS Dates in scope:

GENERAL PAYROLL CONTROLS Risk # Risk Expected Control Step # Testing Documents/Info Needed 1 Unauthorized initial pay rate 2 Unauthorized/unsupported deductions (statutory deductions and benefits). Initial

GENERAL PAYROLL CONTROLS Risk # Risk Expected Control Step # Testing Documents/Info Needed 1 Unauthorized initial pay rate 2 Unauthorized/unsupported deductions (statutory deductions and benefits). Initial

Technical Professionals

THE ARC TRAINING GROUP A Division of The ARC Consulting Group, Inc. A Profit Enhancement Firm Providing Educational and Consultative Services to the International Business Community SEMINAR FACT SHEET

THE ARC TRAINING GROUP A Division of The ARC Consulting Group, Inc. A Profit Enhancement Firm Providing Educational and Consultative Services to the International Business Community SEMINAR FACT SHEET

ACCOUNTS PAYABLE AUDIT RECOVERING LOST DOLLARS AT NO COST

ACCOUNTS PAYABLE AUDIT RECOVERING LOST DOLLARS AT NO COST 1 Our Objective To assist organizations in finding lost thousands of dollars in profits through duplicate payments, duplicate billings, overpayments,

ACCOUNTS PAYABLE AUDIT RECOVERING LOST DOLLARS AT NO COST 1 Our Objective To assist organizations in finding lost thousands of dollars in profits through duplicate payments, duplicate billings, overpayments,

Secrets, Conspiracies and Hidden Patterns: Fraud and Advanced Data Mining

Secrets, Conspiracies and Hidden Patterns: Fraud and Advanced Data Mining Shauna Woody-Coussens Director, Forensic & Valuation Services Jeremy Clopton Manager, Forensic & Valuation Services Agenda Fraud

Secrets, Conspiracies and Hidden Patterns: Fraud and Advanced Data Mining Shauna Woody-Coussens Director, Forensic & Valuation Services Jeremy Clopton Manager, Forensic & Valuation Services Agenda Fraud

WEEK 6. Objective 1: Sales Transaction Cycle Risks

WEEK 6 CSA ch4 & GS ch10: pp457-488 Objective 1: Sales Transaction Cycle Risks The major assertions of interest to the auditor in ST of balances for account receivable are existence and valuation and allocation.

WEEK 6 CSA ch4 & GS ch10: pp457-488 Objective 1: Sales Transaction Cycle Risks The major assertions of interest to the auditor in ST of balances for account receivable are existence and valuation and allocation.

Conversion. Concealment methods. Example #1: Skimming. Example #2: Skimming. 2015 GASBO Conference. Thomas Buckhoff, Ph.D.

Top Five Employee Fraud Schemes Forensic Solutions, LLC Forensic accounting and litigation support services Presented by: Thomas Buckhoff, Ph.D., CPA/CFF, CFE Fraudsters love cash! Cash is the asset most

Top Five Employee Fraud Schemes Forensic Solutions, LLC Forensic accounting and litigation support services Presented by: Thomas Buckhoff, Ph.D., CPA/CFF, CFE Fraudsters love cash! Cash is the asset most

B Resource Guide: Implementing Financial Controls

What s in this Guide: I. Definition: What are Financial Controls? II. Why Do You Need Financial Controls? III. Best Practices: Financial Controls to Consider I. Definition: What are Financial Controls?

What s in this Guide: I. Definition: What are Financial Controls? II. Why Do You Need Financial Controls? III. Best Practices: Financial Controls to Consider I. Definition: What are Financial Controls?

DLI CODE OF BUSINESS CONDUCT & ETHICS

DLI CODE OF BUSINESS CONDUCT & ETHICS All DLI employees, regardless of where they are located, must conduct their affairs with uncompromising honesty and integrity. Business ethics are no different from

DLI CODE OF BUSINESS CONDUCT & ETHICS All DLI employees, regardless of where they are located, must conduct their affairs with uncompromising honesty and integrity. Business ethics are no different from

Chapter 18 Auditing Investments and Cash Balances

Chapter 18 Auditing Investments and Cash Balances General Considerations Cash balances include undeposited receipts on hand, cash in bank in unrestricted accounts, and imprest accounts such as petty cash

Chapter 18 Auditing Investments and Cash Balances General Considerations Cash balances include undeposited receipts on hand, cash in bank in unrestricted accounts, and imprest accounts such as petty cash

ACL WHITEPAPER. Automating Fraud Detection: The Essential Guide. John Verver, CA, CISA, CMC, Vice President, Product Strategy & Alliances

ACL WHITEPAPER Automating Fraud Detection: The Essential Guide John Verver, CA, CISA, CMC, Vice President, Product Strategy & Alliances Contents EXECUTIVE SUMMARY..................................................................3

ACL WHITEPAPER Automating Fraud Detection: The Essential Guide John Verver, CA, CISA, CMC, Vice President, Product Strategy & Alliances Contents EXECUTIVE SUMMARY..................................................................3

Numerous missing invoices, receipts, and purchase justifications.

Purchase Cards 1 Shell Company A Department of Defense agency requested an audit of its purchase card program when a quarterly review of cardholder transactions showed an increase of one hundred transactions,

Purchase Cards 1 Shell Company A Department of Defense agency requested an audit of its purchase card program when a quarterly review of cardholder transactions showed an increase of one hundred transactions,

Chapter 15: Accounts Payable and Purchases

Accounting Research Manager - Audit Private Accounting Research Manager Miller Interpretations and Other Resources Knowledge-Based Audit Procedures Chapter 15: Accounts Payable and Purchases Chapter 15:

Accounting Research Manager - Audit Private Accounting Research Manager Miller Interpretations and Other Resources Knowledge-Based Audit Procedures Chapter 15: Accounts Payable and Purchases Chapter 15:

AUDIT PROCEDURES RECEIVABLE AND SALES

184 AUDIT PROCEDURES RECEIVABLE AND SALES Ștefan Zuca Abstract The overall objective of the audit of accounts receivable and sales is to determine if they are fairly presented in the context of the financial

184 AUDIT PROCEDURES RECEIVABLE AND SALES Ștefan Zuca Abstract The overall objective of the audit of accounts receivable and sales is to determine if they are fairly presented in the context of the financial

A Publication of the Center for Audit Quality

Practice Aid for Testing Journal Entries and Other Adjustments Pursuant to AU Section 316 A Publication of the Center for Audit Quality December 8, 2008 1 Practice Aid for Testing Journal Entries and Other

Practice Aid for Testing Journal Entries and Other Adjustments Pursuant to AU Section 316 A Publication of the Center for Audit Quality December 8, 2008 1 Practice Aid for Testing Journal Entries and Other

Table of Contents. Data Analysis Then & Now 1. Changing of the Guard 2. New Generation 4. Core Data Analysis Tasks 6

Table of Contents Data Analysis Then & Now 1 Changing of the Guard 2 New Generation 4 Core Data Analysis Tasks 6 Data Analysis Then & Now Spreadsheets remain one of the most popular applications for auditing

Table of Contents Data Analysis Then & Now 1 Changing of the Guard 2 New Generation 4 Core Data Analysis Tasks 6 Data Analysis Then & Now Spreadsheets remain one of the most popular applications for auditing

Invoice Number Vendor Number Amount 129304 A543891 $1,035.71 129304 A543891 $1,035.71

Fraud Detection: Using Data Analysis Techniques A new approach being used for fraud prevention and detection involves the examination of patterns in the actual data. The rationale is that unexpected patterns

Fraud Detection: Using Data Analysis Techniques A new approach being used for fraud prevention and detection involves the examination of patterns in the actual data. The rationale is that unexpected patterns

Cash Flow Management: The Life of Your Business

Cash Flow Management: The Life of Your Business Brian S. Gottschalk CPA Partner GellerRagans Certified Public Accountants Advisors Cash Flow- defined Movement of money received and spent: the pattern of

Cash Flow Management: The Life of Your Business Brian S. Gottschalk CPA Partner GellerRagans Certified Public Accountants Advisors Cash Flow- defined Movement of money received and spent: the pattern of

U S I N G D A T A A N A L Y S I S T O M E E T T H E R E Q U I R E M E N T S O F R I S K B A S E D A U D I T I N G S T A N D A R D S

U S I N G D A T A A N A L Y S I S T O M E E T T H E R E Q U I R E M E N T S O F R I S K B A S E D A U D I T I N G S T A N D A R D S A C a s e W a r e I D E A R e s e a r c h R e p o r t CaseWare IDEA Inc.

U S I N G D A T A A N A L Y S I S T O M E E T T H E R E Q U I R E M E N T S O F R I S K B A S E D A U D I T I N G S T A N D A R D S A C a s e W a r e I D E A R e s e a r c h R e p o r t CaseWare IDEA Inc.

How To Prevent Fraud On A Credit Card

Fraud Detection and Prevention Financial Management Advisory Council August 28, 2014 Sarah Mahugh, CPA, MBA Financial Audit Audit Manager Overview Fraud trends Fraud Risks and internal controls Case Studies

Fraud Detection and Prevention Financial Management Advisory Council August 28, 2014 Sarah Mahugh, CPA, MBA Financial Audit Audit Manager Overview Fraud trends Fraud Risks and internal controls Case Studies

PREPARING AUDITORS IN THEIR USAGE OF DATA ANALYTICS TOOL IN FRAUD PREVENTION PROGRAM

IN THEIR USAGE OF DATA ANALYTICS TOOL IN FRAUD PREVENTION PROGRAM Auditors need to understand that while audit findings are common, they are not necessarily fraud and due care is needed in building evidence.

IN THEIR USAGE OF DATA ANALYTICS TOOL IN FRAUD PREVENTION PROGRAM Auditors need to understand that while audit findings are common, they are not necessarily fraud and due care is needed in building evidence.

BRIBERY AND CORRUPTION

FRAUD SCHEMES Fraud An intentional act by one or more individuals among management, those charged with governance, employees, or third parties, involving the use of deception to obtain an unjust or illegal

FRAUD SCHEMES Fraud An intentional act by one or more individuals among management, those charged with governance, employees, or third parties, involving the use of deception to obtain an unjust or illegal

IPPF Practice Guide. Internal Auditing and Fraud

IPPF Practice Guide Internal Auditing and Fraud December 2009 IPPF Practice Guide Table of Contents Introduction... 1 Executive Summary... 2 Definition of Fraud... 4 Fraud Awareness... 5 A. Reasons for

IPPF Practice Guide Internal Auditing and Fraud December 2009 IPPF Practice Guide Table of Contents Introduction... 1 Executive Summary... 2 Definition of Fraud... 4 Fraud Awareness... 5 A. Reasons for

The Basics of Internal Controls

The Basics of Internal Controls Presented to: The Institute of Internal Auditors (IIA) Topeka Chapter April 7, 2009 Today s Objectives Provide Insight into Internal Controls! Risk and Fraud the basis for

The Basics of Internal Controls Presented to: The Institute of Internal Auditors (IIA) Topeka Chapter April 7, 2009 Today s Objectives Provide Insight into Internal Controls! Risk and Fraud the basis for

Ethics, Fraud, and Internal Control

Ethics, Fraud, and Internal Control SUPRIYO BHATTACHARJEE AGM & MOF CAB,RBI,PUNE 17/9/07 Objectives Broad issues pertaining to business ethics Ethics in accounting information systems Ethical issues in

Ethics, Fraud, and Internal Control SUPRIYO BHATTACHARJEE AGM & MOF CAB,RBI,PUNE 17/9/07 Objectives Broad issues pertaining to business ethics Ethics in accounting information systems Ethical issues in

Use of Data Extraction & Analysis Software In a Financial Statement Audit

Use of Data Extraction & Analysis Software In a Financial Statement Audit A Message from The Audit Wizard April 2008 Making Auditors Proficient, Inc. Phone: 352-750-9636 www.billallen.com E-mail: ballen@billallen.com

Use of Data Extraction & Analysis Software In a Financial Statement Audit A Message from The Audit Wizard April 2008 Making Auditors Proficient, Inc. Phone: 352-750-9636 www.billallen.com E-mail: ballen@billallen.com

THE ABC S OF DATA ANALYTICS

THE ABC S OF DATA ANALYTICS ANGEL BUTLER MAY 23, 2013 HOUSTON AREA SCHOOL DISTRICT INTERNAL AUDITORS (HASDIA) AGENDA Data Analytics Overview Data Analytics Examples Compliance Purchasing and Accounts Payable

THE ABC S OF DATA ANALYTICS ANGEL BUTLER MAY 23, 2013 HOUSTON AREA SCHOOL DISTRICT INTERNAL AUDITORS (HASDIA) AGENDA Data Analytics Overview Data Analytics Examples Compliance Purchasing and Accounts Payable

USF System & Preventing Identity Fraud

POLICY USF System USF USFSP USFSM Number: 0-109 Subject: Identity Theft Program Procedures and Protocol Responsible Office: Business and Finance Date of Origin: 1-11-11 Date Last Amended: Date Last Reviewed:

POLICY USF System USF USFSP USFSM Number: 0-109 Subject: Identity Theft Program Procedures and Protocol Responsible Office: Business and Finance Date of Origin: 1-11-11 Date Last Amended: Date Last Reviewed:

Accounts Payable. Best Practices: Existing Control: Control Gap: Controls Evaluation and Gap Analysis. Purchasing

Accounts Payable Gap Analysis: POS identifies the following Best Practices as efficient and effective control processes for the above risk. Listed for comparison are the controls currently in place, if

Accounts Payable Gap Analysis: POS identifies the following Best Practices as efficient and effective control processes for the above risk. Listed for comparison are the controls currently in place, if