Ministry of Finance & Tax Policy Department. Nina Bjerkedal Director General

|

|

|

- Pearl Robertson

- 7 years ago

- Views:

Transcription

1 & Tax Policy Department Nina Bjerkedal Director General

2 The Ministry

3 Areas of responsibilities Planning and implementing economic policy Coordinating the preparation of the budget Ensuring state revenues by maintaining and developing the system of taxes Monitoring financial markets and drawing up regulations Managing the state s financial assets

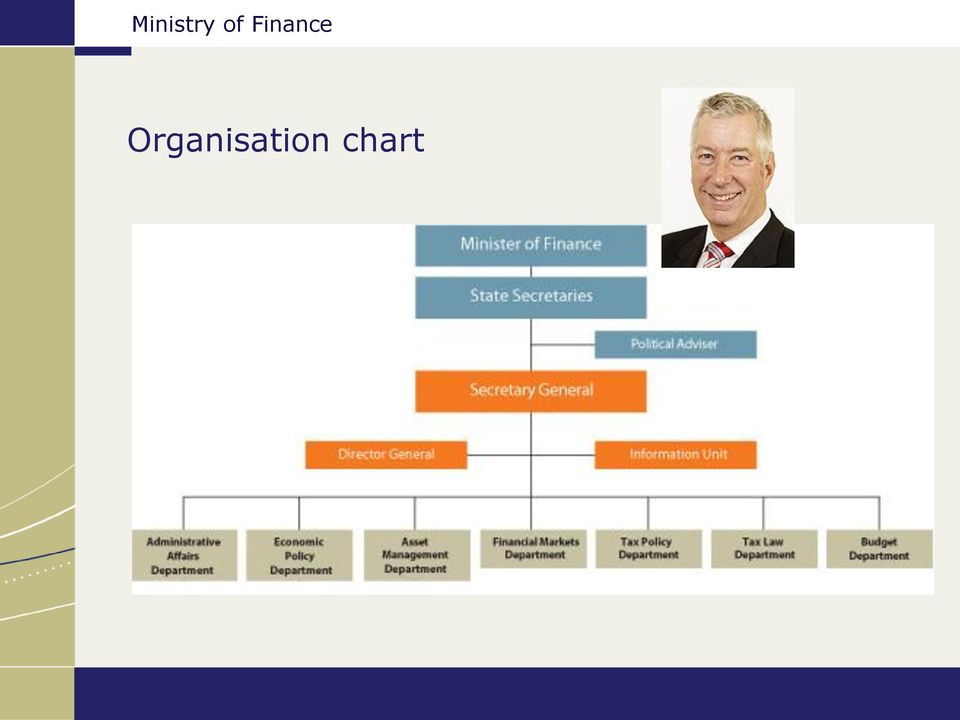

4 Organisation chart

5 The Tax Policy Department Evaluate economic aspects of the tax system: Initiate reforms to improve the design of the tax system Review how tax legislation affects revenue saving, consumption, investments, labour supply etc. the income distribution Responsible for the presentation of tax proposals in the annual budgets Responsible for the Ministry's work related to the petroleum and hydro power sector and to well functioning product markets International Climate Negotiations

6 Main objectives of the tax system Finance the public sector Redistribute income Correct market failures Stabilise the economy

7 Basic principles Broad tax bases reflecting economic realities Relatively low tax rates Redistribution by progressive taxation of wages and pensions Neutrality in capital and corporate taxation

8 Tax Policy Department Direct Taxes Indirect Taxes Structural Policy and Petroleum Petter Solbu: Wealth tax Lovise Bauger: Environmental taxes Torgeir Johnsen: Taxes on resource rent

9 The Ministry of Finance on internet: The National Budget Web Portal: The Recruitment Web Portal:

10 Wealth tax Student introduction 27 th of April 2012 Petter T. Solbu

11 Taxing wealth main topics Current Norwegian rules International trends Basic economic arguments Changes in the Norwegian wealth tax

12 Current wealth tax in Norway 1,1 pct. of net taxable wealth (individuals) Local government 0,7 pct. Central government 0,4 pct. Basic allowance NOK The business sector does not pay wealth tax (a few exceptions) Estimated tax revenue from the wealth tax: Over 14 billion NOK in ,4 pct. of mainland taxes (petroleum taxes excluded) Main weakness: Uneven valuation of different assets property is heavily favoured

13 International trends In the OECD only Norway, France and Switzerland levy a traditional net wealth tax (gross wealth minus debt) Several countries have abolished the wealth tax in recent years among others Spain and Sweden But Norway has a very low property taxation In Norway, the combined tax on property and wealth is 2.9 pct. The OECD average is 5.5 pct In the US, UK, Japan and in Canada the share is above 10 pct.

14 Basic economic arguments Why wealth tax? 14 bn NOK in tax revenue each year -> fills a fiscal need Wealthy individuals more able to pay taxes than individuals that are not wealthy Wealth is unevenly distributed and correlated with income for high income earners the tax is therefore very redistributive No lock-in effects Negative effects of the wealth tax Decreases the return from saving for Norwegians Uneven valuation of different assets distort the investment mix Motivates the tax payer to relocate to another country without a wealth tax The reduced saving can affect investment level in Norway if investors are credit constrained or have incomplete access to the international capital market Tax not dependent on actual cash-flow, which could lead to political demand for exceptions (e.g. pensioners in large villas)

15 Redistribution Increases the progressivity of the income tax Ensures that all tax payers, also the most well off, pay taxes at the personal level Tax as a share of gross income in 2009 (pct.) Wealth tax Income tax Gross income in 1000 NOK 3000 and above 0 16

40 40 Wealth tax Income tax 30 30 20 20 10 10 0 0-300 300-500 500-750 750-1000")

16 The effective tax rate on saving Contributes to very high effective tax rates on saving Example: Bank deposit with 5% return and 2,5% inflation Invested amount 100 Return 5 Inflation 2.5 Real return before tax 2.5 Income tax (28 pct.) 1.4 Wealth tax (1,1 pct.) 1.1 Total tax 2.5 Real return after tax = 0 Effective tax rate (2.5 0)/2.5 = 100 % OECD is concerned about the wealth tax because of its impact on effective tax rates on saving

/2.")

17 Wealth tax changes since 2005 All shares valued at 100 pct. of their market values (up from 65 pct.) since 2008 The tax-assessed values of commercial property based on rental income and capitalization rates since 2009 The tax-assessed values of dwellings based on market values since 2010 But still valued at only 25 pct. (primary) or 40 pct. (secondary) of assessed market value Considerably increased basic allowance (fivefold) Removed 80 percent rule in 2009

or 40 pct.")

18 New valuation system for dwelllings examples of old tax-assessed values Apartment in Frogner, Oslo Sq m: 157 m² Agent s estimate: 19 mill. NOK Tax-assessed value 2009: NOK Share 2009: 1% Apartment in Mortensrud, Oslo Sq m: 102 m² Agent s estimate: 3 mill. NOK Tax-assessed value 2009: NOK Share 2009: 30 %

19 New valuation system for dwelllings examples of new tax-assessed values Apartment in Frogner, Oslo Sq m: 157 m² Agent s estimate: 19 mill. NOK Tax-assessed value 2010: 1.5 mill. NOK Share 2010: 8% Apartment in Mortensrud, Oslo Sq m: 102 m² Agent s estimate: 3 mill. NOK Tax-assessed value 2010: NOK Share 2010: 23 %

20 Summary Very few OECD countries levy a wealth tax But many countries have higher property taxes Wealth tax is primarily a tool for redistribution Some negative effects: Distorts investment mix, reduces incentives to save, motivates relocation and may affect inland investments The government has broadened the tax base in recent years There is still room for improvement in the Norwegian system Property still valued considerably lower than other assets OECD: Effective tax rates on saving very high

21 The Ministry of Finance homepage: The National Budget Web Portal: The Recruitment Web Portal:

22 Environmental taxes Lovise Bauger 27th April 2012 Tax Policy Department, Ministry of Finance, Norway 26

23 Environmental taxes Pricing of negative externalities Corrects market failure Pigou taxes (tax at optimal level) / Cost effective taxes Polluters pay principle Enhance technological progress Decentralized solution and low information requirements Gives income that can be used to reduce other distorting taxes or finance welfare objects 27

24 Environmentally related taxes in Norway Environmental taxes: Revenue: 25 bill. NOK Tax on road usage (petrol, diesel incl. biodiesel) Tax on climate gases (CO2, HFC and PFC) Tax on sulfur and NOx Tax on chemicals TRI and PER Tax on pesticides Tax on lubrication oil Tax on waste at landfills Tax on beverage containers Energy taxes: Revenue 9 bill. NOK. Tax on mineral oil and electricity Vehicle and boat motor taxes : Revenue 30 bill. NOK 28

25 Road usage tax Tax covers petrol and diesel (incl. biodiesel) Object: price external cost by road usage External costs: accidents, congestion, road tear and wear, noise and local emissions CO2-emissions taxed by CO2-tax 29

26 NOK per litre Ministry of Finance Road usage tax -petrol External marginal costs and road usage tax for diesel driven vehicles road wear and tear local emissions noise 2 congestion 1 0 tax petrol petrol cars accidents 30

27 NOK per litre Ministry of Finance Road usage tax - diesel External marginal costs and road usage tax for diesel driven vehicles road wear and tear local emissions noise congestion accidents 0 tax diesel diesel cars heavy vehicles heavy vehicles (3,5-7,5 tonn) (16-23 tonn) 31

28 Road usage tax Road usage tax per kwh fuel 2012 NOK/kWh 0,90 0,80 0,70 0,60 0,50 0,40 0,30 0,20 0,10 0,00 ethanol in petrol blends petrol fossil diesel biodiesel other fuels 32

29 1. Climate instruments by source Agriculture 9 % Other 1 % Landbased industry 16 % Landbased industry(ets) 13 % Fishing& hunting 2 % Offshore 24 % Tax on landfills 3 % HFC/PFC-tax 1 % Heating 2 % Shipping and air transport 7 % Road transport 22 % ETS ETS and tax TAX Few measures 33

30 The CO 2 tax Introduced in Norway in 1991 Levied on mineral oil products and on CO 2 emissions from petroleum activities Objective: cost effective reduction of CO 2 Some extensions and adjustments to emission trading system Covers about 55 per cent of total Norwegian greenhouse gas emissions The current tax rates varies across energy products and users 34

31 CO2-tax versus emission allowances Both economic instrument that put a price on emissions and give a cost effective solution Tax: price on emission will be known, emission level will be unknown Emission trading system: level of emissions will be known, price of emissions will be unknown In principle emission trading and emission tax can give the same results under some assumptions In practice: high degree of free allocation of allowances in the EU ETS and allocation partly adjustable for increased emissions 35

32 Marginal cost of climate gass emissions 2011 NOK Process indusry, agriculture, fishery HFK Landbased industry Mineral oil and gas Offshore petroleum aviation petrol Emissions of CO2-equivalents in mill. tonnes NOK

33 The emission trading system in Norway : Not linked to the European Union emission trading system (EU ETS) Same coverage as EU, but emission with CO2-tax was excluded from the ETS : Part of EU-ETS. Same coverage as EU, but emissions from the offshore sector and inland aviation are also covered by the CO2-tax Adaptation: no restrictions on auctioning Total share of free allowances: 30% of estimated emissions : Part of EU-ETS. Negotiation on EFTA-States participation is ongoing. 37

34 2.d The CO 2 tax - Norwegian experiences Carbon intensities in different Cost effective measure to reduce emissions countries 800 Most significant effects of the CO 2 tax on emissions in the offshore industry USA More moderate effects on 600 emissions in other sectors UK Euro area Better to use the tax 400 system to correct negative externalities like Japan CO 2 emissions than using distorting taxes (i.e. 200 Norway labor) Sweden Tax revenue to the government Low administrative costs Tonnes CO2-eqvivalentes relative to GDP, per million US dollar prices. Source: OECD

35 Useful references- environmental taxes Prop. 1 LS ( ) Skatter, avgifter og toll 2012 NOU 1996:9 Grønne skatter- en politikk for bedre miljø og høy sysselsetting (Green tax Commission) NOU 2007:8 En vurdering av særavgiftene

36 The Ministry of Finance Homepage: The National Budget Web Portal: The Recruitment Web Portal:

37 The Resource Rent and Taxation Torgeir Johnsen, Tax Policy Department Norwegian Ministry of Finance 27 April

38 Taxing Natural Resources - Key Aspects Extraordinary profits Immobile resources A good tax base! Profit based tax rules Stability Predictability Simplicity Efficient tax administration 42

39 Resource rent industries Substantial petroleum resources on the Norwegian shelf Petroleum resources owned by the society Separate tax district with separate government take system Hydropower production Natural resource with cost advantage Tax income to local and regional governments Fisheries and forestry Super-profit in efficient parts of the industry Regional policy important 43

40 Resource rent Super-profit : Potential for increased tax take Extra allowance for ordinary returns Should not distort investment incentives Ordinary income: 28% on net income as in other industries Neutrality between industries Tax on ordinary returns and super-profit 44

41 Million Sm3 oil equivalents Million barrels o.e. per day Ministry of Finance Petroleum Production on the NCS Gas Oil

42 Billion NOK 2010 Value USD 2010 Value Ministry of Finance Total Government Take from the Petroleum Sector Taxes Environmental taxes SDFI Royalty and area fee StatoilHydro dividend Oil Price 46

43 Petroleum tax system on company basis ring fenced against mainland Sales income (norm prices) - Operating costs - Capital depreciation (16,7 pct. over 6 years) - Financial costs (thin capitalisation) - (Deficits from previous years) = Ordinary tax base liable to 28 pct. tax - Uplift (investment based extra depreciation, 7,5 pct. 4 years) - (Excess uplift from previous years) = Tax base liable to 50 pct. tax Companies without taxable income Carry forward with interest - (risk free + 0,5%)*(1-0,28) Tax refund (pay out) of exploration costs Final losses can be sold or tax reimbursed from the state 47

44 State Direct Financial Interest (SDFI) The SDFI is an arrangement where the state keeps an interest in a number of oil and gas fields. Each interest is decided when licenses are awarded, and the size of state interest varies between fields. The state pays its share of investments and costs and receives a corresponding share of the gross income from the license. When Statoil was listed and partially privatised in 2001, the administration of the SDFI portfolio was transferred to a new state-owned trust company, Petoro. Petoro is funded over the state budget and does not receive any of the income from the SDFI. 48

45 Hydro Power Taxation Production from about 1900 Resource rent tax introduced 1997 RRT tax rate 30 %, total marginal tax rate 58% The RRT is neutral with regard to investments Property tax 0,7 % (municipalities) License fee and entitlement to buy max 10 % of power generated (state, county and municipalities) 49

46 Tax basis Hydropower Sales income (market prices) - Operating costs - Concession fees - Property tax - Depreciation (linear: installations 1,5% equipment 2,5%) - Uplift (tax values * risk free rate) = Tax base liable to 30 pct. tax Negative resource rent will be entitled to a tax refund (pay out) 50

47 Mill. NOK Ministry of Finance Hydro Power - Resource Rent Tax Year 51

48 The Ministry of Finance Homepage: The National Budget Web Portal: The Recruitment Web Portal:

CO 2 taxes and emission trading in Norway. Nordic seminar Tokyo 18. juni 2010 Frode Finsås Ministry of Finance, Norway

CO 2 taxes and emission trading in Norway Nordic seminar Tokyo 18. juni 2010 Frode Finsås Ministry of Finance, Norway 1 Outline of the presentation 1. Climate instruments by source 2. The CO2-tax 3. The

CO 2 taxes and emission trading in Norway Nordic seminar Tokyo 18. juni 2010 Frode Finsås Ministry of Finance, Norway 1 Outline of the presentation 1. Climate instruments by source 2. The CO2-tax 3. The

The Norwegian tax system - main features and developments. Chapter 2 of the budget proposal on taxes 2015 Oslo, 8 October 2014

The Norwegian tax system - Chapter 2 of the budget proposal on taxes 215 Oslo, 8 October 214 The Norwegian tax system 2 The Norwegian tax system 2.1 Introduction The tax system funds public welfare and

The Norwegian tax system - Chapter 2 of the budget proposal on taxes 215 Oslo, 8 October 214 The Norwegian tax system 2 The Norwegian tax system 2.1 Introduction The tax system funds public welfare and

Background. When the Government Is the Landlord. 1 Norway's oil and gas reserves are all offshore.

Regional Details: Norway In this appendix, we describe the methods the government uses to obtain revenues from oil and gas production in Norway. We present quantitative estimates of revenues as well as

Regional Details: Norway In this appendix, we describe the methods the government uses to obtain revenues from oil and gas production in Norway. We present quantitative estimates of revenues as well as

// BRIEF STATISTICS 2014

// BRIEF STATISTICS 2014 // TAXATION IN FINLAND Finland s taxation is subject to decisions by the Finnish Parliament, the European Union and the municipalities of Finland. It is governed by tax legislation,

// BRIEF STATISTICS 2014 // TAXATION IN FINLAND Finland s taxation is subject to decisions by the Finnish Parliament, the European Union and the municipalities of Finland. It is governed by tax legislation,

The Norwegian Model: Evolution, performance and benefits

The Norwegian Model: Evolution, performance and benefits Ola Borten Moe Minister of Petroleum and Energy Olje- og energidepartementet regjeringen.no/oed Our largest industry Norwegian Oil and Gas Activities

The Norwegian Model: Evolution, performance and benefits Ola Borten Moe Minister of Petroleum and Energy Olje- og energidepartementet regjeringen.no/oed Our largest industry Norwegian Oil and Gas Activities

How To Tax In Norway

1 Main features of the tax programme for 2015 1.1 The tax policy of the Government The main tax policy objective of the Government is to fund public goods and services in the most efficient manner. Tax

1 Main features of the tax programme for 2015 1.1 The tax policy of the Government The main tax policy objective of the Government is to fund public goods and services in the most efficient manner. Tax

Framework of the energy taxation: the situation in OECD countries!

Framework of the energy taxation: the situation in OECD countries! Presentation at the seminar JORNADA SOBRE LA FISCALIDAD AMBIENTAL EN LA ENERGÍA Y SU APLICACIÓN EN ESPAÑA Hosted by the Institute for

Framework of the energy taxation: the situation in OECD countries! Presentation at the seminar JORNADA SOBRE LA FISCALIDAD AMBIENTAL EN LA ENERGÍA Y SU APLICACIÓN EN ESPAÑA Hosted by the Institute for

Budget 2015. Key figures for the Norwegian economy Main figures of the Fiscal Budget Direct and indirect tax rates

Budget 215 Key figures for the Norwegian economy Main figures of the Fiscal Budget Direct and indirect tax rates 1 Main figures of the Fiscal Budget and the Pension Fund excluding borrowing and lending

Budget 215 Key figures for the Norwegian economy Main figures of the Fiscal Budget Direct and indirect tax rates 1 Main figures of the Fiscal Budget and the Pension Fund excluding borrowing and lending

The Norwegian Government Pension Fund Global

The Norwegian Government Pension Fund Global l Tore Eriksen Paris 1 June 2012 1 Part I The Role of oil & gas in the Norwegian economy 2 Discovery of oil on December 23. 1969; the Ekofisk oil field Foto:

The Norwegian Government Pension Fund Global l Tore Eriksen Paris 1 June 2012 1 Part I The Role of oil & gas in the Norwegian economy 2 Discovery of oil on December 23. 1969; the Ekofisk oil field Foto:

1 Main features of the tax programme for 2014 1.1 Main features of the tax programme

1 Main features of the tax programme for 2014 1.1 Main features of the tax programme The main tax policy objectives of the Government are raising public revenues in an efficient manner, helping to bring

1 Main features of the tax programme for 2014 1.1 Main features of the tax programme The main tax policy objectives of the Government are raising public revenues in an efficient manner, helping to bring

EU study on company car taxation: presentation of the main results

European Commission EU study on company car taxation: presentation of the main results Presentation in the OECD workshop on estimating support to fossil fuels, Paris 18-19 November 2010 Katri Kosonen European

European Commission EU study on company car taxation: presentation of the main results Presentation in the OECD workshop on estimating support to fossil fuels, Paris 18-19 November 2010 Katri Kosonen European

The Norwegian economy

The Norwegian economy Slower speed ahead, but still growth Strong mechanisms support mainland economy Wriggle room to smooth business cycles Rune Bjerke CEO Just how bad is it? Slower speed ahead but still

The Norwegian economy Slower speed ahead, but still growth Strong mechanisms support mainland economy Wriggle room to smooth business cycles Rune Bjerke CEO Just how bad is it? Slower speed ahead but still

Company Income Tax and Other Taxes

Company Income Tax and Other Taxes Company Taxation Arrangements The company tax rate (also known as the corporate) is 30%. The treatment of business expenditure for the mining and petroleum industries

Company Income Tax and Other Taxes Company Taxation Arrangements The company tax rate (also known as the corporate) is 30%. The treatment of business expenditure for the mining and petroleum industries

OIL AND THE NORWEGIAN ECONOMY GOVERNOR ØYSTEIN OLSEN NTNU, 29 SEPTEMBER 2015

OIL AND THE NORWEGIAN ECONOMY GOVERNOR ØYSTEIN OLSEN NTNU, 9 SEPTEMBER 15 GDP per capita relative to OECD Index. OECD = 1. Purchasing power adjusted 15 Norway Mainland Norway 15 1 1 5 197 1975 198 1985

OIL AND THE NORWEGIAN ECONOMY GOVERNOR ØYSTEIN OLSEN NTNU, 9 SEPTEMBER 15 GDP per capita relative to OECD Index. OECD = 1. Purchasing power adjusted 15 Norway Mainland Norway 15 1 1 5 197 1975 198 1985

ECONOMIC COMMENTARIES

ECONOMIC COMMENTARIES The petroleum fund mechanism and associated foreign exchange transactions by Norges Bank NO. 2 2014 AUTHOR: ELLEN AAMODT The views expressed are those of the author and do not necessarily

ECONOMIC COMMENTARIES The petroleum fund mechanism and associated foreign exchange transactions by Norges Bank NO. 2 2014 AUTHOR: ELLEN AAMODT The views expressed are those of the author and do not necessarily

Monetary policy and the economic outlook Governor Svein Gjedrem SR-banken, Stavanger 19 March 2004

Monetary policy and the economic outlook Governor Svein Gjedrem SR-banken, Stavanger 9 March SG SR-banken Stavanger, 9 March Monetary policy regulation. Monetary policy shall be aimed at stability in the

Monetary policy and the economic outlook Governor Svein Gjedrem SR-banken, Stavanger 9 March SG SR-banken Stavanger, 9 March Monetary policy regulation. Monetary policy shall be aimed at stability in the

The economic outlook and monetary policy

The economic outlook and monetary policy Governor Svein Gjedrem SR-Bank, Stavanger March 5 Interest rates and inflation Per cent Market rate Real interest rate Neutral real interest rate Inflation SR-Bank

The economic outlook and monetary policy Governor Svein Gjedrem SR-Bank, Stavanger March 5 Interest rates and inflation Per cent Market rate Real interest rate Neutral real interest rate Inflation SR-Bank

Norway Country Profile

Norway Country Profile Produced by Oslo Revisjon AS P.O. Box 123 Skoyen, N - 0212 Oslo, Norway Phone: +47 22 50 24 50 Fax : +47 22 50 36 80 Email: firmapost@oslorevisjon.no The intention of this profile

Norway Country Profile Produced by Oslo Revisjon AS P.O. Box 123 Skoyen, N - 0212 Oslo, Norway Phone: +47 22 50 24 50 Fax : +47 22 50 36 80 Email: firmapost@oslorevisjon.no The intention of this profile

Biogas in Public Transport

Biogas in Public Transport Cooperation, the key to success Brussel, 19th of June 2012 Baltic Biogas Bus project, aims, objectives & results Lennart Hallgren Stockholm Public Transport www.balticbiogasbus.eu

Biogas in Public Transport Cooperation, the key to success Brussel, 19th of June 2012 Baltic Biogas Bus project, aims, objectives & results Lennart Hallgren Stockholm Public Transport www.balticbiogasbus.eu

Overview of the Norwegian Asset Accounts for Oil and Gas, 1991-2002.

London Group Meeting, 2004 22-24 September, Copenhagen, Denmark Overview of the Norwegian Asset Accounts for Oil and Gas, 1991-2002. Kristine Erlandsen, Statistics Norway Table of contents: 1 INTRODUCTION...

London Group Meeting, 2004 22-24 September, Copenhagen, Denmark Overview of the Norwegian Asset Accounts for Oil and Gas, 1991-2002. Kristine Erlandsen, Statistics Norway Table of contents: 1 INTRODUCTION...

English summary. Chapter I: Energy and Climate Policy

The present report from the Chairmen of the Danish Council of Environmental Economics contains the following three chapters: - Energy and Climate Policy, chapter I - Car taxation, accidents and environment,

The present report from the Chairmen of the Danish Council of Environmental Economics contains the following three chapters: - Energy and Climate Policy, chapter I - Car taxation, accidents and environment,

Value added tax on financial services 1

Value added tax on financial services 1 1. Background Financial services are exempted from value added tax. Proposition No. 1 (2012 2013) to the Storting; Bill and Draft Resolution on Taxes, discussed

Value added tax on financial services 1 1. Background Financial services are exempted from value added tax. Proposition No. 1 (2012 2013) to the Storting; Bill and Draft Resolution on Taxes, discussed

Scotland s Balance Sheet. April 2013

Scotland s Balance Sheet April 2013 Contents Executive Summary... 1 Introduction and Overview... 2 Public Spending... 5 Scottish Tax Revenue... 12 Overall Fiscal Position and Public Sector Debt... 18 Conclusion...

Scotland s Balance Sheet April 2013 Contents Executive Summary... 1 Introduction and Overview... 2 Public Spending... 5 Scottish Tax Revenue... 12 Overall Fiscal Position and Public Sector Debt... 18 Conclusion...

Main trends in industry in 2014 and thoughts on future developments. (April 2015)

") Main trends in industry in 2014 and thoughts on future developments (April 2015) Development of the industrial sector in 2014 After two years of recession, industrial production returned to growth in 2014.

Main trends in industry in 2014 and thoughts on future developments (April 2015) Development of the industrial sector in 2014 After two years of recession, industrial production returned to growth in 2014.

The norwegian economy A short story about equality, trust and natural resources

1 The norwegian economy A short story about equality, trust and natural resources Joakim Prestmo Economist reseacher Reseach department, Statistics Norway 7. March 2011 1 Outline Where do we stand to day?

1 The norwegian economy A short story about equality, trust and natural resources Joakim Prestmo Economist reseacher Reseach department, Statistics Norway 7. March 2011 1 Outline Where do we stand to day?

Topic 2: Fossil Fuel Supply and Demand: Effect of Subsidies and Taxation. () Global Energy Issues, Industries and Markets 1 / 53

Global Energy Issues, Industries and Markets 1 / 53") Topic 2: Fossil Fuel Supply and Demand: Effect of Subsidies and Taxation () Global Energy Issues, Industries and Markets 1 / 53 Introduction This topic follows strategy I plan in using in this course A

Topic 2: Fossil Fuel Supply and Demand: Effect of Subsidies and Taxation () Global Energy Issues, Industries and Markets 1 / 53 Introduction This topic follows strategy I plan in using in this course A

Oil and gas taxation in Norway

Oil and gas taxation in Norway Contents 1.0 Summary 1 2.0 Corporate income tax 1 2.1 Rates 2 2.2 Taxable income 2 2.3 Revenue 2 2.4 Deductions and allowances 2 2.5 Losses 4 2.6 Foreign entity taxation

Oil and gas taxation in Norway Contents 1.0 Summary 1 2.0 Corporate income tax 1 2.1 Rates 2 2.2 Taxable income 2 2.3 Revenue 2 2.4 Deductions and allowances 2 2.5 Losses 4 2.6 Foreign entity taxation

User Fees and the Interest Tax

Problems of Equity in Modern Income Taxation Ole Gjems-Onstad Revenue Driven Taxation The proposition in this article is that the Norwegian tax system is basically revenue driven. Much inequity is accepted

Problems of Equity in Modern Income Taxation Ole Gjems-Onstad Revenue Driven Taxation The proposition in this article is that the Norwegian tax system is basically revenue driven. Much inequity is accepted

PRESSURES ON EU TAX SYSTEMS AND OPTIONS FOR REFORM

PRESSURES ON EU TAX SYSTEMS AND OPTIONS FOR REFORM Professor Peter Birch Sörensen University of Copenhagen Presentation at the conference Wanted: The Tax System of the Future hosted by the German Ministry

PRESSURES ON EU TAX SYSTEMS AND OPTIONS FOR REFORM Professor Peter Birch Sörensen University of Copenhagen Presentation at the conference Wanted: The Tax System of the Future hosted by the German Ministry

Energy Taxation in Europe, Japan and The United States

Energy Taxation in Europe, Japan and The United States ENERGY TAXATION IN EUROPE, JAPAN AND THE UNITED STATES Summary of the energy taxation survey of electricity, fuels, district heat and transport in

Energy Taxation in Europe, Japan and The United States ENERGY TAXATION IN EUROPE, JAPAN AND THE UNITED STATES Summary of the energy taxation survey of electricity, fuels, district heat and transport in

ECON4620 Public Economics I Second lecture by DL

ECON4620 Public Economics I Second lecture by DL Diderik Lund Department of Economics University of Oslo 9 April 2015 Diderik Lund, Dept. of Econ., UiO ECON4620 Lecture DL2 9 April 2015 1 / 13 Outline

ECON4620 Public Economics I Second lecture by DL Diderik Lund Department of Economics University of Oslo 9 April 2015 Diderik Lund, Dept. of Econ., UiO ECON4620 Lecture DL2 9 April 2015 1 / 13 Outline

Summary: Biofuels for a Better Climate How does the tax relief work? RiR 2011:10

Summary: Biofuels for a Better Climate How does the tax relief work? RiR 2011:10 THE SWEDISH NATIONAL AUDIT OFFICE RiR 2011:10 Biofuels for a Better Climate How does the tax relief work? Summary The Swedish

Summary: Biofuels for a Better Climate How does the tax relief work? RiR 2011:10 THE SWEDISH NATIONAL AUDIT OFFICE RiR 2011:10 Biofuels for a Better Climate How does the tax relief work? Summary The Swedish

Key Solutions CO₂ assessment

GE Capital Key Solutions CO₂ assessment CO₂ emissions from company car fleets across Europe s major markets between 2008 and 2010 www.gecapital.eu/fleet Contents Introduction and key findings Reduction

GE Capital Key Solutions CO₂ assessment CO₂ emissions from company car fleets across Europe s major markets between 2008 and 2010 www.gecapital.eu/fleet Contents Introduction and key findings Reduction

Mål og virkemidler i de nordiske landenes handlingsplaner for Fornybar Energi

Mål og virkemidler i de nordiske landenes handlingsplaner for Fornybar Energi Bjarne Juul-Kristensen Energistyrelsen, Nordiske Arbejdsgruppe for Fornybar Energi Content Targets and measures in RES-Directive

Mål og virkemidler i de nordiske landenes handlingsplaner for Fornybar Energi Bjarne Juul-Kristensen Energistyrelsen, Nordiske Arbejdsgruppe for Fornybar Energi Content Targets and measures in RES-Directive

Norsk gass og det skandinaviske energimarked. Thor Otto Lohne, Direktør, Gassco

Norsk gass og det skandinaviske energimarked Thor Otto Lohne, Direktør, Gassco Fyn, 19. november 2009 Gassco A neutral and independent operator for the integrated gas transport system from the Norwegian

Norsk gass og det skandinaviske energimarked Thor Otto Lohne, Direktør, Gassco Fyn, 19. november 2009 Gassco A neutral and independent operator for the integrated gas transport system from the Norwegian

Comprehensive emissions per capita for industrialised countries

THE AUSTRALIA INSTITUTE Comprehensive emissions per capita for industrialised countries Hal Turton and Clive Hamilton The Australia Institute September 2001 the Parties included in Annex I shall implement

THE AUSTRALIA INSTITUTE Comprehensive emissions per capita for industrialised countries Hal Turton and Clive Hamilton The Australia Institute September 2001 the Parties included in Annex I shall implement

Chapter 12: Gross Domestic Product and Growth Section 1

Chapter 12: Gross Domestic Product and Growth Section 1 Key Terms national income accounting: a system economists use to collect and organize macroeconomic statistics on production, income, investment,

Chapter 12: Gross Domestic Product and Growth Section 1 Key Terms national income accounting: a system economists use to collect and organize macroeconomic statistics on production, income, investment,

Monetary policy, inflation and the outlook for the Norwegian economy

Monetary policy, inflation and the outlook for the Norwegian economy DnB, Haugesund Svein Gjedrem, Governor of Norges Bank, April Effective exchange rates January 99= GBP NOK 9 8 NZD 9 8 7 SEK 7 99 99

Monetary policy, inflation and the outlook for the Norwegian economy DnB, Haugesund Svein Gjedrem, Governor of Norges Bank, April Effective exchange rates January 99= GBP NOK 9 8 NZD 9 8 7 SEK 7 99 99

The facts on biodiesel and bioethanol

Renewable biofuels for transport The facts on biodiesel and bioethanol BABFO BRITISH ASSOCIATION FOR BIO FUELS AND OILS RECYCLING CARBON Sustainable development is a key priority for Defra, by which we

Renewable biofuels for transport The facts on biodiesel and bioethanol BABFO BRITISH ASSOCIATION FOR BIO FUELS AND OILS RECYCLING CARBON Sustainable development is a key priority for Defra, by which we

25*$1,6$7,21)25(&2120,&&223(5$7,21$1''(9(/230(17

25(&2120,&&223(5$7,21$1''(9(/230(17") 25*$1,6$7,21)25(&2120,&&223(5$7,21$1''(9(/230(17 7D[3ROLF\5HIRUPVLQ,WDO\ &(175()257$;32/,&

25*$1,6$7,21)25(&2120,&&223(5$7,21$1''(9(/230(17 7D[3ROLF\5HIRUPVLQ,WDO\ &(175()257$;32/,&

9: Indirect taxes. Overview. 9.1: Indirect taxes

9: Indirect taxes Overview This chapter provides an overview of indirect taxes levied on specific goods and services, including fuel taxes, alcohol taxes, tobacco tax, the Luxury Car Tax, agricultural

9: Indirect taxes Overview This chapter provides an overview of indirect taxes levied on specific goods and services, including fuel taxes, alcohol taxes, tobacco tax, the Luxury Car Tax, agricultural

A fuel efficient vehicle fleet for Victoria WHAT THE VICTORIAN GOVERNMENT CAN DO

A fuel efficient vehicle fleet for Victoria WHAT THE VICTORIAN GOVERNMENT CAN DO 2 I A FUEL EFFICIENT VEHICLE FLEET FOR VICTORIA I WHAT THE VICTORIAN GOVERNMENT CAN DO Executive Summary Key Points The

A fuel efficient vehicle fleet for Victoria WHAT THE VICTORIAN GOVERNMENT CAN DO 2 I A FUEL EFFICIENT VEHICLE FLEET FOR VICTORIA I WHAT THE VICTORIAN GOVERNMENT CAN DO Executive Summary Key Points The

BP NORGE AS. Annual Accounts 2010

BP NORGE AS Annual Accounts 2010 BP NORGE AS INCOME STATEMENT NOK 1 000 Notes 2010 2009 Operating income Petroleum income 2 7 423 582 5 622 751 Other income 3 128 843 42 330 Total operating income 7 552

BP NORGE AS Annual Accounts 2010 BP NORGE AS INCOME STATEMENT NOK 1 000 Notes 2010 2009 Operating income Petroleum income 2 7 423 582 5 622 751 Other income 3 128 843 42 330 Total operating income 7 552

From Carbon Subsidy to Carbon Tax: India s Green Actions 1

From Carbon Subsidy to Carbon Tax: India s Green Actions 1 09 CHAPTER 9.1 INTRODUCTION The recent steep decline in international oil prices is seen by many as an opportunity to rationalize the energy prices

From Carbon Subsidy to Carbon Tax: India s Green Actions 1 09 CHAPTER 9.1 INTRODUCTION The recent steep decline in international oil prices is seen by many as an opportunity to rationalize the energy prices

Co-ordinated versus uncoordinated European carbon tax solutions analysed with GEM-E3 1 linking the EU-12 countries

Co-ordinated versus uncoordinated European carbon tax solutions analysed with GEM-E3 1 linking the EU-12 countries by P. Capros, P. Georgakopoulos, S. Zografakis (NTUniversity Athens) D. Van Regemorter,

Co-ordinated versus uncoordinated European carbon tax solutions analysed with GEM-E3 1 linking the EU-12 countries by P. Capros, P. Georgakopoulos, S. Zografakis (NTUniversity Athens) D. Van Regemorter,

Addressing Competitiveness in introducing ETR United Kingdom s climate change levy

Low Carbon Green Growth Roadmap for Asia and the Pacific CASE STUDY Addressing Competitiveness in introducing ETR United Kingdom s climate change levy Key point The UK Government introduced an energy tax

Low Carbon Green Growth Roadmap for Asia and the Pacific CASE STUDY Addressing Competitiveness in introducing ETR United Kingdom s climate change levy Key point The UK Government introduced an energy tax

What does an early ETS mean for businesses?

What does an early ETS mean for businesses? An early transition to an emissions trading scheme from 1 July 2014 will benefit businesses through a reduction in electricity and gas bills. Small businesses

What does an early ETS mean for businesses? An early transition to an emissions trading scheme from 1 July 2014 will benefit businesses through a reduction in electricity and gas bills. Small businesses

Details on the Carbon Tax (Tax for Climate Change Mitigation)

") Details on the Carbon Tax (Tax for Climate Change Mitigation) Introduction of Carbon Tax Contents 1. Background and Purpose of Carbon Tax 2. Mechanism of Carbon Tax 3. Household Burden due to Carbon Tax

Details on the Carbon Tax (Tax for Climate Change Mitigation) Introduction of Carbon Tax Contents 1. Background and Purpose of Carbon Tax 2. Mechanism of Carbon Tax 3. Household Burden due to Carbon Tax

Hungary. 1. Economic situation

2. COUNTRY NOTES: HUNGARY 125 1. Economic situation has faced considerable challenges to regain fiscal credibility. After almost a decade of persistent, high fiscal deficits and the building up of external

2. COUNTRY NOTES: HUNGARY 125 1. Economic situation has faced considerable challenges to regain fiscal credibility. After almost a decade of persistent, high fiscal deficits and the building up of external

The National Budget 2011

Summary The National Budget 211 Summary National Budget 211 Page 1 Contents: page 1. Introduction...2 2. Economic outlook...2 3. Economic policy...5 3.1 The fiscal policy guidelines...5 3.2 Budgetary policy

Summary The National Budget 211 Summary National Budget 211 Page 1 Contents: page 1. Introduction...2 2. Economic outlook...2 3. Economic policy...5 3.1 The fiscal policy guidelines...5 3.2 Budgetary policy

The National Budget 2015

The National Budget 215 214-215 The National Budget 215 1 Contents: page 1. Introduction... 2 2. The Norwegian economy... 3 3. Economic policy... 8 3.1 Fiscal policy... 8 3.2 Tax policy... 17 3.3 Monetary

The National Budget 215 214-215 The National Budget 215 1 Contents: page 1. Introduction... 2 2. The Norwegian economy... 3 3. Economic policy... 8 3.1 Fiscal policy... 8 3.2 Tax policy... 17 3.3 Monetary

How To Tax Company Cars In The Uk

Taxation of Company Cars Workshop An evaluation of the UK s shift to CO 2 based Company Car Taxation Stephen Potter Professor of Transport Strategy and member of the UK Green Fiscal Commission Context

Taxation of Company Cars Workshop An evaluation of the UK s shift to CO 2 based Company Car Taxation Stephen Potter Professor of Transport Strategy and member of the UK Green Fiscal Commission Context

Strategy Document 1/03

Strategy Document / Monetary policy in the period 5 March to 5 June Discussed by the Executive Board at its meeting of 5 February. Approved by the Executive Board at its meeting of 5 March Background Norges

Strategy Document / Monetary policy in the period 5 March to 5 June Discussed by the Executive Board at its meeting of 5 February. Approved by the Executive Board at its meeting of 5 March Background Norges

Did you know...? Facts on Road Transport and Oil

Facts on Road Transport and Oil The International Road Transport Union (IRU) is the international organisation which upholds the interest of the road transport industry worldwide. Via its network of national

Facts on Road Transport and Oil The International Road Transport Union (IRU) is the international organisation which upholds the interest of the road transport industry worldwide. Via its network of national

THE PETROL TAX DEBATE

THE PETROL TAX DEBATE Zoë Smith THE INSTITUTE FOR FISCAL STUDIES Briefing Note No. 8 Published by The Institute for Fiscal Studies 7 Ridgmount Street London WC1E 7AE Tel 2 7291 48 Fax 2 7323 478 mailbox@ifs.org.uk

THE PETROL TAX DEBATE Zoë Smith THE INSTITUTE FOR FISCAL STUDIES Briefing Note No. 8 Published by The Institute for Fiscal Studies 7 Ridgmount Street London WC1E 7AE Tel 2 7291 48 Fax 2 7323 478 mailbox@ifs.org.uk

Renewable energy in public transport

More on Tram From Trikkeprogram Med ny logo Renewable energy in public transport RERC 2014 Pernille Aga, Project Manager Ruter AS Increasing market share for public transport Index: 2007 = 100 Kilde: Ruters

More on Tram From Trikkeprogram Med ny logo Renewable energy in public transport RERC 2014 Pernille Aga, Project Manager Ruter AS Increasing market share for public transport Index: 2007 = 100 Kilde: Ruters

Roadmap for moving to a competitive low carbon economy in 2050

Roadmap for moving to a competitive low carbon economy in 2050 COUNTRY CAPITAL XXX, 9 March 2011 NAME XXX DG Climate Action European Commission 1 Limiting climate change a global challenge Keeping average

Roadmap for moving to a competitive low carbon economy in 2050 COUNTRY CAPITAL XXX, 9 March 2011 NAME XXX DG Climate Action European Commission 1 Limiting climate change a global challenge Keeping average

CONTENTS LEVY. (Prepared by Ian G. Heggie, revised March 1999) 1. Weight-Distance Charges...2. 2. Exempting Non-Road Users...3

1. Weight-Distance Charges...2. 2. Exempting Non-Road Users...3") CONTENTS EXEMPTING NON-ROAD USERS FROM PAYING THE DIESEL LEVY (Prepared by Ian G. Heggie, revised March 1999) 1. Weight-Distance Charges...2 2. Exempting Non-Road Users...3 3. Coloring Un-Taxed Diesel...3

CONTENTS EXEMPTING NON-ROAD USERS FROM PAYING THE DIESEL LEVY (Prepared by Ian G. Heggie, revised March 1999) 1. Weight-Distance Charges...2 2. Exempting Non-Road Users...3 3. Coloring Un-Taxed Diesel...3

Promotion of energy efficiency and renewable energy experiences from Norway

Business planning of Renewable Energy and Energy Efficiency Projects in Ukraine and Eastern Europe Kiev 28. April 2011 Promotion of energy efficiency and renewable energy experiences from Norway Hans Borchsenius

Business planning of Renewable Energy and Energy Efficiency Projects in Ukraine and Eastern Europe Kiev 28. April 2011 Promotion of energy efficiency and renewable energy experiences from Norway Hans Borchsenius

Chapter 3 Demand and production

Chapter 3 Demand and production 3.1 Goods consumption index 1995=1. Seasonally adjusted volume 4 2 22 4 2 21 118 2 118 11 11 114 114 1 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Source: Statistics

Chapter 3 Demand and production 3.1 Goods consumption index 1995=1. Seasonally adjusted volume 4 2 22 4 2 21 118 2 118 11 11 114 114 1 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Source: Statistics

The norwegian economy Lecture in Norwegian Life and Society

1 The norwegian economy Lecture in Norwegian Life and Society Joakim Prestmo Economist reseacher Reseach department, Statistics Norway 1 Outline of today's lecture a. Where do we stand to day? b. How did

1 The norwegian economy Lecture in Norwegian Life and Society Joakim Prestmo Economist reseacher Reseach department, Statistics Norway 1 Outline of today's lecture a. Where do we stand to day? b. How did

Economic Instruments in Practice 1: Carbon Tax in Sweden

Economic Instruments in Practice 1: Carbon Tax in Sweden Bengt Johansson, Swedish Environmental Protection Agency 1) Abstract-In 1991 a carbon tax was introduced in Sweden as a complement to the existing

Economic Instruments in Practice 1: Carbon Tax in Sweden Bengt Johansson, Swedish Environmental Protection Agency 1) Abstract-In 1991 a carbon tax was introduced in Sweden as a complement to the existing

Annex 5A Trends in international carbon dioxide emissions

Annex 5A Trends in international carbon dioxide emissions 5A.1 A global effort will be needed to reduce greenhouse gas emissions and to arrest climate change. The Intergovernmental Panel on Climate Change

Annex 5A Trends in international carbon dioxide emissions 5A.1 A global effort will be needed to reduce greenhouse gas emissions and to arrest climate change. The Intergovernmental Panel on Climate Change

Svein Gjedrem: Prospects for the Norwegian economy

Svein Gjedrem: Prospects for the Norwegian economy Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at Sparebank 1 SR-Bank Stavanger, Stavanger, 26 March 2010. The text below

Svein Gjedrem: Prospects for the Norwegian economy Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at Sparebank 1 SR-Bank Stavanger, Stavanger, 26 March 2010. The text below

The Economic Impacts of Reducing. Natural Gas and Electricity Use in Ontario

The Economic Impacts of Reducing Natural Gas and Electricity Use in Ontario Prepared for Blue Green Canada July 2013 Table of Contents Executive Summary... i Key Findings... i Introduction...1 Secondary

The Economic Impacts of Reducing Natural Gas and Electricity Use in Ontario Prepared for Blue Green Canada July 2013 Table of Contents Executive Summary... i Key Findings... i Introduction...1 Secondary

Eliminating Double Taxation through Corporate Integration

FISCAL FACT Feb. 2015 No. 453 Eliminating Double Taxation through Corporate Integration By Kyle Pomerleau Economist Key Findings The United States tax code places a double-tax on corporate income with

FISCAL FACT Feb. 2015 No. 453 Eliminating Double Taxation through Corporate Integration By Kyle Pomerleau Economist Key Findings The United States tax code places a double-tax on corporate income with

Mainland GDP in Norway Annual growth. Per cent

The outlook for the Norwegian economy and the business sector in southwestern Norway Governor Svein Gjedrem Vats, October Mainland GDP in Norway Annual growth. Per cent 99 99 99 99 99 Sources: Statistics

The outlook for the Norwegian economy and the business sector in southwestern Norway Governor Svein Gjedrem Vats, October Mainland GDP in Norway Annual growth. Per cent 99 99 99 99 99 Sources: Statistics

CRG CONSERVE RESOURCES GROUP ECO ENVIRONMENTAL ENGINEERING TECHNOLOGIES. NEW State of the Art. Advanced OIL REFINERY TECHNOLOGY & PROCESSES

NEW State of the Art Advanced OIL REFINERY TECHNOLOGY & PROCESSES TABLE OF CONTENTS Introduction ( Part 1 ) Comparison Advantages Information Appendix Result of Fraction Refinery Economic indicator + Supporting

NEW State of the Art Advanced OIL REFINERY TECHNOLOGY & PROCESSES TABLE OF CONTENTS Introduction ( Part 1 ) Comparison Advantages Information Appendix Result of Fraction Refinery Economic indicator + Supporting

Financial Scrutiny Unit Briefing What is GDP?

The Scottish Parliament and Scottish Parliament Infor mation C entre l ogos. Financial Scrutiny Unit Briefing What is GDP? Richard Marsh 27 August 2013 13/48 This factsheet provides a short guide to Gross

The Scottish Parliament and Scottish Parliament Infor mation C entre l ogos. Financial Scrutiny Unit Briefing What is GDP? Richard Marsh 27 August 2013 13/48 This factsheet provides a short guide to Gross

ENVIRONMENT. Aviation. Property. Marine Services. Trading & Industrial. Beverages

ENVIRONMENT Our ultimate goal, which we first articulated in 2010, is for our operating companies to achieve zero net impact on the environment. We call this goal Net Zero. In, we developed a preliminary

ENVIRONMENT Our ultimate goal, which we first articulated in 2010, is for our operating companies to achieve zero net impact on the environment. We call this goal Net Zero. In, we developed a preliminary

Renewable Choice Energy

Catawba College Table of Contents About Renewable Choice The Problem: Electricity Production Today The Solutions: Renewable Energy Sources Renewable Energy Credits (RECs) Who can participate in Renewable

Catawba College Table of Contents About Renewable Choice The Problem: Electricity Production Today The Solutions: Renewable Energy Sources Renewable Energy Credits (RECs) Who can participate in Renewable

THE UK CLIMATE CHANGE PROGRAMME AND EXAMPLES OF BEST PRACTICE. Gabrielle Edwards United Kingdom

Workshop on Best Practices in Policies and Measures, 11 13 April 2000, Copenhagen THE UK CLIMATE CHANGE PROGRAMME AND EXAMPLES OF BEST PRACTICE Gabrielle Edwards United Kingdom Abstract: The UK published

Workshop on Best Practices in Policies and Measures, 11 13 April 2000, Copenhagen THE UK CLIMATE CHANGE PROGRAMME AND EXAMPLES OF BEST PRACTICE Gabrielle Edwards United Kingdom Abstract: The UK published

SPANISH EXPERIENCE IN RENEWABLE ENERGY AND ENERGY EFFICIENCY. Anton Garcia Diaz Economic Bureau of the Prime Minister

SPANISH EXPERIENCE IN RENEWABLE ENERGY AND ENERGY EFFICIENCY Anton Garcia Diaz Economic Bureau of the Prime Minister «Symposium on Strengthening Sino-Spain cooperation in multiple Fields» New Energy Cooperation

SPANISH EXPERIENCE IN RENEWABLE ENERGY AND ENERGY EFFICIENCY Anton Garcia Diaz Economic Bureau of the Prime Minister «Symposium on Strengthening Sino-Spain cooperation in multiple Fields» New Energy Cooperation

The oil fields in the NCS are located in the North Sea, Norwegian Sea, and Barents Sea.

A.2 Norway Volumes of Associated Gas Flared on Norwegian Continental Shelf Norway is a major oil producer, and its oil fields are located offshore in the Norwegian Continental Shelf (NCS). 81 In 2002,

A.2 Norway Volumes of Associated Gas Flared on Norwegian Continental Shelf Norway is a major oil producer, and its oil fields are located offshore in the Norwegian Continental Shelf (NCS). 81 In 2002,

Summary of the Impact assessment for a 2030 climate and energy policy framework

Summary of the Impact assessment for a 2030 climate and energy policy framework Contents Overview a. Drivers of electricity prices b. Jobs and growth c. Trade d. Energy dependence A. Impact assessment

Summary of the Impact assessment for a 2030 climate and energy policy framework Contents Overview a. Drivers of electricity prices b. Jobs and growth c. Trade d. Energy dependence A. Impact assessment

6 Quality of Public Finances Revenues and Expenditures

6 Quality of Public Finances Revenues and Expenditures 6.1 The Government s Strategy In 2003, the Czech government launched a public finance reform focusing on fiscal consolidation and elimination of the

6 Quality of Public Finances Revenues and Expenditures 6.1 The Government s Strategy In 2003, the Czech government launched a public finance reform focusing on fiscal consolidation and elimination of the

NEWS FROM DANMARKS NATIONALBANK

1ST QUARTER 2015 N0 1 NEWS FROM DANMARKS NATIONALBANK PROSPECT OF HIGHER GROWTH IN DENMARK Danmarks Nationalbank adjusts its forecast of growth in the Danish economy this year and next year upwards. GDP

1ST QUARTER 2015 N0 1 NEWS FROM DANMARKS NATIONALBANK PROSPECT OF HIGHER GROWTH IN DENMARK Danmarks Nationalbank adjusts its forecast of growth in the Danish economy this year and next year upwards. GDP

Norwegian Energy Production and Consumption

Norwegian Energy Production and Consumption Peter Føllesdal Brown Assistant Director General Energy and Water Resources Department, MPE Oslo, 13 May 2015 Norway and EU Commissioner Miguel Arias Cañete

Norwegian Energy Production and Consumption Peter Føllesdal Brown Assistant Director General Energy and Water Resources Department, MPE Oslo, 13 May 2015 Norway and EU Commissioner Miguel Arias Cañete

Energy and Environment issues in road transport. Prof. Stef Proost KULeuven (B)

") Energy and Environment issues in road transport Prof. Stef Proost KULeuven (B) Long term trends? 2050 World Share OECD Road use cars x 2.5 From 50% now to 20% in 2050 Road use trucks x 5 Air transport

Energy and Environment issues in road transport Prof. Stef Proost KULeuven (B) Long term trends? 2050 World Share OECD Road use cars x 2.5 From 50% now to 20% in 2050 Road use trucks x 5 Air transport

Scope 1 describes direct greenhouse gas emissions from sources that are owned by or under the direct control of the reporting entity;

9 Greenhouse Gas Assessment 9.1 Introduction This chapter presents an assessment of the potential greenhouse gas emissions associated with the Simandou Railway and evaluates the significance of these in

9 Greenhouse Gas Assessment 9.1 Introduction This chapter presents an assessment of the potential greenhouse gas emissions associated with the Simandou Railway and evaluates the significance of these in

Economic Outcomes of a U.S. Carbon Tax. Executive Summary

Economic Outcomes of a U.S. Carbon Tax Executive Summary [ Overview [ During the ongoing debate on how to address our nation s fiscal challenges, some have suggested that imposing a carbon tax would improve

Economic Outcomes of a U.S. Carbon Tax Executive Summary [ Overview [ During the ongoing debate on how to address our nation s fiscal challenges, some have suggested that imposing a carbon tax would improve

An Evaluation of the Possible

An Evaluation of the Possible Macroeconomic Impact of the Income Tax Reduction in Malta Article published in the Quarterly Review 2015:2, pp. 41-47 BOX 4: AN EVALUATION OF THE POSSIBLE MACROECONOMIC IMPACT

An Evaluation of the Possible Macroeconomic Impact of the Income Tax Reduction in Malta Article published in the Quarterly Review 2015:2, pp. 41-47 BOX 4: AN EVALUATION OF THE POSSIBLE MACROECONOMIC IMPACT

Baseline Paper turned in June 2011 Revised DATE

Table of contents Analysis of energy context Sweden... 3 1 Energy infrastructure... 3 2 Organisations and markets... 6 3 Built environment... 9 4 Government... 9 5 Governance instruments... 9 6 Economic,

Table of contents Analysis of energy context Sweden... 3 1 Energy infrastructure... 3 2 Organisations and markets... 6 3 Built environment... 9 4 Government... 9 5 Governance instruments... 9 6 Economic,

The European Renewable Energy Directive and international Trade. Laurent Javaudin Delegation of the European Commission to the U.S.

The European Renewable Energy Directive and international Trade Laurent Javaudin Delegation of the European Commission to the U.S. The European Union 27 Member States 490 million people 2 Outline The Present:

The European Renewable Energy Directive and international Trade Laurent Javaudin Delegation of the European Commission to the U.S. The European Union 27 Member States 490 million people 2 Outline The Present:

The outlook for the Norwegian economy with particular focus on the business sector in Vesterålen

The outlook for the Norwegian economy with particular focus on the business sector in Vesterålen Governor Svein Gjedrem Sortland, October Mainland GDP in Norway Annual growth. Per cent 99 99 99 99 99 Sources:

The outlook for the Norwegian economy with particular focus on the business sector in Vesterålen Governor Svein Gjedrem Sortland, October Mainland GDP in Norway Annual growth. Per cent 99 99 99 99 99 Sources:

Climate Change, driving force for biofuels Regional Seminar Tartu 23-24 of March 2011 Lennart Hallgren Project Manager. www.balticbiogasbus.

Climate Change, driving force for biofuels Regional Seminar Tartu 23-24 of March 2011 Lennart Hallgren Project Manager 1 Climate Change Peak Oil Energy security Diesel shortage Air Quality Congestion Increase

Climate Change, driving force for biofuels Regional Seminar Tartu 23-24 of March 2011 Lennart Hallgren Project Manager 1 Climate Change Peak Oil Energy security Diesel shortage Air Quality Congestion Increase

A JOINT RESOLUTION OF THE SENATE AND THE HOUSE OF REPRESENTATIVES OF THE STATE OF MONTANA REVISING THE OFFICIAL

SJ00.0 SENATE JOINT RESOLUTION NO. INTRODUCED BY B. TUTVEDT A JOINT RESOLUTION OF THE SENATE AND THE HOUSE OF REPRESENTATIVES OF THE STATE OF MONTANA REVISING THE OFFICIAL ESTIMATE OF THE STATE'S GENERAL

SJ00.0 SENATE JOINT RESOLUTION NO. INTRODUCED BY B. TUTVEDT A JOINT RESOLUTION OF THE SENATE AND THE HOUSE OF REPRESENTATIVES OF THE STATE OF MONTANA REVISING THE OFFICIAL ESTIMATE OF THE STATE'S GENERAL

UK Energy Statistics

PRESS NOTICE Reference: 2014/016 STATISTICAL PRESS RELEASE Date: 27 March 2014 UK Energy Statistics Energy Trends and Quarterly Energy Prices publications are published today 27 March 2014 by the Department

PRESS NOTICE Reference: 2014/016 STATISTICAL PRESS RELEASE Date: 27 March 2014 UK Energy Statistics Energy Trends and Quarterly Energy Prices publications are published today 27 March 2014 by the Department

2015 -- S 0417 S T A T E O F R H O D E I S L A N D

LC001 01 -- S 01 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 01 A N A C T RELATING TO TAXATION -- CARBON PRICING AND ECONOMIC DEVELOPMENT INVESTMENT ACT OF 01 Introduced

LC001 01 -- S 01 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 01 A N A C T RELATING TO TAXATION -- CARBON PRICING AND ECONOMIC DEVELOPMENT INVESTMENT ACT OF 01 Introduced

Guide to Calculating your Income Tax Liability for 2001 - Additional Notes -

Guide to Calculating your Income Tax Liability for 2001 - Additional Notes - The purpose of these additional notes is to help you compute some of the more difficult calculations that you will need to do

Guide to Calculating your Income Tax Liability for 2001 - Additional Notes - The purpose of these additional notes is to help you compute some of the more difficult calculations that you will need to do

Sweden Energy efficiency report

Sweden Energy efficiency report Objectives: o 41 TWh of end use energy savings in 216 o 2 reduction in total energy intensity by 22 Overview - (%/year) Primary intensity (EU=1)¹ 124 - -1.8% + CO 2 intensity

Sweden Energy efficiency report Objectives: o 41 TWh of end use energy savings in 216 o 2 reduction in total energy intensity by 22 Overview - (%/year) Primary intensity (EU=1)¹ 124 - -1.8% + CO 2 intensity

From separation to cooperation: Emissions trading systems in the EU and Switzerland

Federal Department of the Environment, Transport, Energy and Communications DETEC Federal Office for the Environment FOEN From separation to cooperation: Emissions trading systems in the EU and Switzerland

Federal Department of the Environment, Transport, Energy and Communications DETEC Federal Office for the Environment FOEN From separation to cooperation: Emissions trading systems in the EU and Switzerland

THE CODE. On Taxes and Other Obligatory Payments

THE CODE of the Republic of Kazakhstan On Taxes and Other Obligatory Payments TO THE BUDGET (THE TAX CODE) Effective January 1, 2015 Developed by ITIC in cooperation with the Information Bulletin of the

THE CODE of the Republic of Kazakhstan On Taxes and Other Obligatory Payments TO THE BUDGET (THE TAX CODE) Effective January 1, 2015 Developed by ITIC in cooperation with the Information Bulletin of the

Prudential plc. Basis of Reporting: GHG emissions data and other environmental metrics.

Prudential plc. Basis of Reporting: GHG emissions data and other environmental metrics. This Basis of Reporting document supports the preparation and reporting of GHG emissions data and other environmental

Prudential plc. Basis of Reporting: GHG emissions data and other environmental metrics. This Basis of Reporting document supports the preparation and reporting of GHG emissions data and other environmental

Svein Gjedrem: The economic situation in Norway

Svein Gjedrem: The economic situation in Norway Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to invited foreign embassy representatives, Norges Bank, 21 March 2002. Please

Svein Gjedrem: The economic situation in Norway Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to invited foreign embassy representatives, Norges Bank, 21 March 2002. Please

CO 2 emissions on quarterly basis

Statistics Netherlands, The Hague 2010 National Accounts Department PO box 24500 2490 HA Den Haag, Netherlands CO 2 emissions on quarterly basis Project and report commissioned by the European Community

Statistics Netherlands, The Hague 2010 National Accounts Department PO box 24500 2490 HA Den Haag, Netherlands CO 2 emissions on quarterly basis Project and report commissioned by the European Community

16 Business Performance

DCC ANNUAL REPORT AND ACCOUNTS 16 Business Performance Operating Review DCC Energy DCC Energy is the leading oil and liquefied petroleum gas (LPG) sales, marketing and distribution business in Europe.

DCC ANNUAL REPORT AND ACCOUNTS 16 Business Performance Operating Review DCC Energy DCC Energy is the leading oil and liquefied petroleum gas (LPG) sales, marketing and distribution business in Europe.

Causes & Inflation. Causes of inflation 01/11/2010. A2 Economics, November 2010

Causes & Effects of Inflation A2 Economics, November 2010 Causes of inflation Inflation is a sustained increase in the general level of prices There are many possible causes of price inflation in an economy

Causes & Effects of Inflation A2 Economics, November 2010 Causes of inflation Inflation is a sustained increase in the general level of prices There are many possible causes of price inflation in an economy

German Tax Facts. The Expatriate Financial Guide to Germany

The Expatriate Financial Guide to Germany German Tax Facts Introduction Tax Year Assessment Basis Income Tax Taxation in Germany occurs at a national and municipal level. The Ministry of Finance controls

The Expatriate Financial Guide to Germany German Tax Facts Introduction Tax Year Assessment Basis Income Tax Taxation in Germany occurs at a national and municipal level. The Ministry of Finance controls

Road Transport Charging ~ Road Pricing. Jani Saarinen Financial Director, Finnish Road Administration

1 Road Transport Charging ~ Road Pricing Jani Saarinen Financial Director, Finnish Road Administration General taxes Earmarked road transport taxes Loans, bonds etc. Funding sources 2 State tax revenue

1 Road Transport Charging ~ Road Pricing Jani Saarinen Financial Director, Finnish Road Administration General taxes Earmarked road transport taxes Loans, bonds etc. Funding sources 2 State tax revenue