Econometric Research and Special Studies Department. Forecasting at the Central Bank: still à la mode? M.M.G. Fase

|

|

|

- Wilfred Scott

- 7 years ago

- Views:

Transcription

1 Econometric Research and Special Studies Department Forecasting at the Central Bank: still à la mode? M.M.G. Fase Research Memorandum WO&E nr. 600 December 1999 'H1HGHUODQGVFKH%DQN

2

3 FORECASTING AT THE CENTRAL BANK: still à la mode? M.M.G. Fase * * Deputy director of De Nederlandsche Bank NV and professor of monetary economics, University of Amsterdam. I am indebted to Marga Peeters for her help and professor E. Sterken for his comments. Research Memorandum WO&E no. 600/9933 December 1999 De Nederlandsche Bank NV Econometric Research and Special Studies Department P.O. Box AB AMSTERDAM The Netherlands

4

5 ABSTRACT Forecasting at the Central Bank: still à la mode? M.M.G. Fase This paper presents a reflection on and assessment of the practice of forecasting at the Bank. The focus is on macroeconomics, and the currency circulation both domestic and Euro area wide. Key words: JEL codes: C5, E3, M2 SAMENVATTING Voorspellen bij een centrale bank: nog steeds à la mode? M.M.G. Fase Dit rapport biedt een reflectie op de beoordeling van de voorspelpraktijk op de Bank. De aandacht gaat daarbij in het bijzonder uit naar de macroeconomische prognoses en die voor de circulatie van munten en bankbiljetten in zowel Nederland als het Eurogebied. Trefwoorden: JEL codes: C5, E3, M2

6

7 - 1-1 INLEIDING Seven years ago, I gave a lecture at the University of Amsterdam carrying the title Forecasting is an art, also at the central bank 1. In this lecture the question was raised whether models are a necessity or not. Today, I will not deal with this question again, but will start off by saying and emphasizing that I am convinced that econometric models are important tools for the design of economic or business policy. The same is evidently true of forecasting. Econometric techniques are often used to establish stylized facts in order to analyze future developments and to generate forecasts. I am also still convinced, and maybe even more so than before, that forecasting is a kind of art. What I mean to say is that it is often not the econometric model alone that is used to forecast. Forecasts often require further creativity in order to come to an estimate of the future developments to be investigated. Let us call this future development the projection. Projections are made by using the econometric framework for forecasts complemented with judgemental elements. The optimal mix of econometrics and judgement is, unfortunately, hard to determine; in general this will depend on the topic, on the timing, and on many other factors as well. Talking about macroeconomics, I think that, given the current developments in the world and in Europe in particular, macroeconomic forecasting on e.g. economic growth or inflation, has not become easier. This definitely holds for a small open economy like the Netherlands, but also for Euroland as a whole. The Netherlands has always been influenced considerably by developments in neighbouring countries, such as Germany. In Europe we now have a common market. The European Economic and Monetary Union has been established with a single currency, the euro, and a common monetary policy. In addition to this great institutional change, capital flows have substantially increased because of capital liberalisation and deregulation. New technologies like the Internet with electronic payment possibilities and novel communication tools like mobile phones have accelerated this process even further. As uncertainty tends to grow, and economies become more integrated, there is surely more need for forecasts and financial risk-analyses, requiring predictions. On the other hand, fortunately, we have gained more knowledge in the field of econometrics and have improved on data collection. New analytical and statistical techniques enable researchers to use vast and reasonably easily accessible data sets to accomplish their work. These data can be exploited to examine economic phenomena in a far more elaborate manner and shorter time span than in the earlier days of e.g. R. Stone, when he wrote his article the Fortune teller. This article is a 1 M.M.G. Fase, Forecasting is an art, even for the central bank, De Nederlandsche Bank, Quarterly Bulletin, 1991, nr 4,

8 - 2 - review of Collin Clarks s provocative The economics of 1960, published in In this interesting monograph Clark attempted to forecast the future but Stone could not resist the temptation to call Clark s projections fortune or storytelling, reflecting his own scepticism on forecasting. At the Bank forecasting is an essential part of to days research. In monetary policy, questions concerning future economic growth and future inflation in the Netherlands and Euroland surely need to be monitored and therefore forecast on a highly frequent basis. Also, in the payment system the demand for banknotes and other payment instruments are forecast on a regular basis. In this article I will present some forecasting exercises undertaken at the Econometric Research and Special Studies Department of the Bank to illustrate this practice. With these examples I will try to indicate to what extent econometrics and judgement play a role. Furthermore, I will reflect on what we have learned and which new avenues could be considered to improve our work. 2 See Economica, 1943, x, p

9 - 3-2 FOUR FORECASTING EXAMPLES FROM THE BANK S PRACTICE One rather simple, though essential, example is the Bank s profit, which comes under the non-tax revenues of the Treasury, the Bank s sole shareholder since The Bank generates profit because a substantial part of its liabilities consists of banknotes where no interest is paid, while on the major parts of its assets interest is received. The projection of the Bank s profit is based on an accounting framework. This framework bears in mind the development of the Bank s assets and liabilities and their corresponding yields. Important exogenous assumptions which underlie the projection refer to interest rates and exchange rates. The profit projections are made frequently, often for one year ahead. For the Bank itself they are also suitable in order to assess, in a quick and convenient way, the impact of the given interest and exchange rate changes on its profit performance. I have three other examples to show, which will be illustrated in some more detail than the above internal business-like illustration. The first example is the Bank business cycle indicator. With respect to this indicator -as with other indicators- no causal relations are assumed between the factors included. This characteristic evidently does not hold for macroeconometric models, i.e. my second example. In these models, the economic theory about private and public sector behaviour and monetary policy forms the basis, and many causalities are therefore explicitly assumed. In my view, macroeconometric modeling is an important part of our economic research although our research portfolio is diversified. The third example I want to discuss concerns forecasting the circulation of euro notes and coins. This is (most probably) a once-only topic though I envisage challenging research avenues here. The euro will be introduced in January 2002 in all EMU member countries. This implies for all EMU countries that their current currency circulation will completely disappear and be substituted by euro notes and coins. In order to do so for the Netherlands, the Bank had to forecast the demand for euro currency in Example I: Forecasting the business cycle The DNB business cycle indicator forecasts Dutch industrial production. Figure 1 shows this indicator along with the realisations over the time span The realisations are in deviations from trend (this is the dotted line). The DNB indicator (the bold line) is also in deviations from trend and, as you can see, forecasts a couple of months ahead. The main purpose of the indicator is to act as an early warning

10 - 4 - instrument that points out business cycle turning points. Just like projecting the DNB profit, projecting the industrial production has also become an exercise that takes place on a very regular basis 3. The construction of the indicator is as follows 4. Five time series are selected as appropriate leading indicators. The five leading indicators presently used are (1) the IFO-indicator of Germany, (2) the expected economic activity in the Dutch economy, (3) real money demand M1, (4) three-months euroguilder interest rate and (5) the Dutch yield curve. Each indicator is detrended by means of a Hodrick- Prescott filter. The DNB business cycle indicator is composed of these five series, that are each standardized and synchronised according to its business cycle. The lead of each series is at least six months and the correlation with industrial production is at least 0.7. The Bank s forecast of business cycle is a weighted average of the lagged five leading indicators, where weights follow from a principal components analyses. The impact of the indicator can of course always be questioned. The indicator can point out something about the near future that may induce policy makers, bankers, firms and households 3 The DNB business cycle indicator is published monthly in Economische Statistische Berichten. It was developed by M.M.G. Fase and J.A. Bikker, 1985, Maandschrift Economie, further referred to in Grandeur and malheur van de conjunctuurbarometer, M.M.G. Fase and H. van der Wielen, Economische Statistische Berichten, 1989, nr 3701, p and included in M.M.G. Fase, Geld in het fin de siècle, Amsterdam 1999, chapter For detailed information on the new methodology to construct the indicator, see L. de Haan and F.W. Vijselaar, de vernieuwde dnb-conjunctuurindicator, Economische Statistische Berichten, September 1998, 83ste jrg, nr 4165, p

the IFO-indicator of Germany, (2) the expected economic activity in the Dutch economy, (3) real money demand M1, (4) three-months euroguilder")

11 - 5 - to adjust their policy or behaviour. So, although we will never really know the precise impact of such an indicator, the signalling effect of this easy one-dimensional figure, might often influence future developments. Some time ago, our Minister of Finance dropped the remark that the business cycle indicator used by the the Central Planning Bureau (CPB) is better and clearer than the one of the DNB. He was not explicit on the criteria he had in mind for better and clearer, but we at DNB did not understand him for reasons of empirical evidence and economic reasoning. As to the latter one important difference between the two indicators is that the CPB measurement includes not only the industrial production, but also includes construction and services. However, our own investigation on this topic has shown that these two additional sectors do not give a good indication of the business cycle. Furthermore, CPB usually presents two indicators instead of one: one is called short-leading and the other is long-leading. In making policy decisions, more information may sometimes be desirable, but then again, it may also lead to more confusion. Perhaps, this is the case with the two leading indicators of the CPB. Example II: Forecasting by means of large macroeconometric models Since January of this year, we have one common monetary policy within the EMU. For the Bank this means a substantial change. Instead of targeting the German Deutsche Mark, the policy strategy followed during the last few years, the Governing Council of the European Central Bank ( ECB ) decides on monetary policy for the whole EMU area. The president of De Nederlandsche Bank is one of the seventeen members of this Governing Council. In the conduct of European monetary policy many factors are of importance. Price stability is aimed at, but it is price stability in the medium term. Hence, it is important to closely monitor those factors that can influence medium term inflation. In order to do so, the Bank has developed several large and small macroeconometric models which enable the Bank to make forecasts both for individual countries and the EMU as a whole, i.e. the euroarea. The two most important models of the Bank are MORKMON and EUROMON. MORKMON is a quarterly macroeconomic model for the Dutch economy with a well developed monetary block This model is very detailed, i.e. it has many equations and in particular the Dutch monetary sector is quite wellspecified. Many foreign variables, like German GDP and world trade, are highly relevant to the Dutch economy and therefore drive the forecasts with MORKMON. These factors, though, are all exogenous in this model but forecast carefully and in different ways. EUROMON is also a quarterly model for Europe,

12 - 6 - Japan and the US. It is far less detailed than MORKMON, but again includes a well specified monetary sector. Moreover, it is a multi-country model with currently 13 countries modelled explicitly. In the very near future the still missing (small) countries, Ireland, Luxembourg and Portugal, will also be included. Then, all countries of the EMU are represented in EUROMON, along with Japan and the US. International linkages are explicitly modelled through export relationships and currently a big effort is made to include also the output gap and financial wealth to account for inflationary expectations and financial distress. EUROMON differs from MULTIMOD - the multi-country model used by the IMF - and NiGEM - the model developed by the National Institute in London - in several important respects. In contrast to MULTIMOD, EUROMON has equations that are all estimated separately (although some parameters are calibrated). As known, MULTIMOD is a model where many long-term parameter estimates are obtained by pooling techniques. This has the disadvantage that most countries exhibit to similar long-run responses to shocks. If we compare EUROMON with NiGEM, it is worth mentioning that in EUROMON more attention is paid to small countries like the Netherlands and Belgium. This is of course very important for the Bank, as is the detailed simulation exercise to examine the model properties and its forecasting power for EMU. Some years ago, the Bank started to publish annual forecasts, for one to two years ahead. The Bank does this bi-annually with MORKMON, for the Dutch economy, and with EUROMON, for the main European countries. Along with these forecasts, also simulation experiments were published to evaluate, for instance, depreciations or appreciations of the European currencies vis-à-vis the dollar, or macroeconomic responses to movements in stock or housing prices. At the moment the main focus is on policy scenarios in EMU. It is further interesting that these publications have received much public attention and are used in policy discussions at the ECB. Nowadays, as monetary policy-making is in the hands of the Governing Council of the ECB, forecasting exercises are coordinated among the EMU countries. At the ECB meetings take place, where all national central banks of the European System of Central Banks (ESCB) participate in so-called narrow and broad forecasting exercises. In the narrow forecasting exercise only the Harmonised Index of Consumer Prices (HICP) is considered. Each country makes a forecast concerning the HICP of its own economy. In the broad forecasting exercise, much more variables are considered, and here also, each participating national central bank makes a forecast of its own (national) economy. In this process consistency is aimed at, among other things by initially assuming the same exogenous variables. This may seem logical and a good thing to do, but is not trivial at all. EMU-wide forecasts are afterwards constructed from these eleven individual country forecasts.

13 - 7 - At the Bank the narrow forecast, i.e. the HICP forecast, is made by using a VARX model. This is a Vector AutoRegressive model where some variables are exogenous and others are exogenous. Currently, the endogenous variables concern four inflation components, ie. wages, retail sales, producer prices and final product prices. Important exogenous variables are the dollar-euro exchange rate, the short-term interest rate, the long-term interest rate of the Netherlands and the world oil price. The VARX model is monthly and forecasts are made for about 15 months ahead. The main advantage in comparison with indicator models is that causalities are not neglected. In comparison with large macroeconometric models, like MORKMON and EUROMON, the forecast is more tractable and therefore more straightforward to understand. For the broad forecasts, the Bank uses MORKMON and EUROMON. Of course, the main advantage of these exercises is that all important national and international linkages are incorporated. Inevitably, in these forecasting exercises a lot of judgement is involved. This is necessary as, for instance, developments in the Dutch labour market are hard to explain. An example is the considerable decrease in unemployment over the last three to four years whereas at the same time inflation stayed quite low. The explanation is particularly difficult to find along the lines of standard economic theory and, therefore, linear macroeconometric models are of no use either. Also the developments in the stock markets and the convergence of long-term and short-term interest rates, a process in the EMU countries that was set in train following the announced start of the EMU in 1999, are hard to explain in such a standard framework. Nevertheless, macroeconometric models offer a useful framework to discuss new economic developments, to evaluate the impact of one macroeconomic factor on other economic factors, and to come up with a plausible economic story. This may be partly due to the non-linear set up of our models. As known, the CPB has to publish projections for the Dutch economy on a regular basis, among other things on inflation as the Bank does. To illustrate this I show some statistics. To give an idea of the similarities and the differences between DNB and CPB forecasts the average absolute forecast errors (and the root mean squared forecast errors) for the 1990 s and have been calculated. For the CPB these statistics are 0.49 (0.69) and 0.43 (0.51) respectively while for the DNB 0.49 (0.64) and 0.18 (0.22) were obtained, indicating a slightly better forecasting performance of the Bank s model in the recent period. However, the important issue is to which this better outcome is due. Closer examination shows that the source of the discrepancies is twofold. For a large part this is due to different assumptions about the exogenous worldprices and exchange rate assumptions.

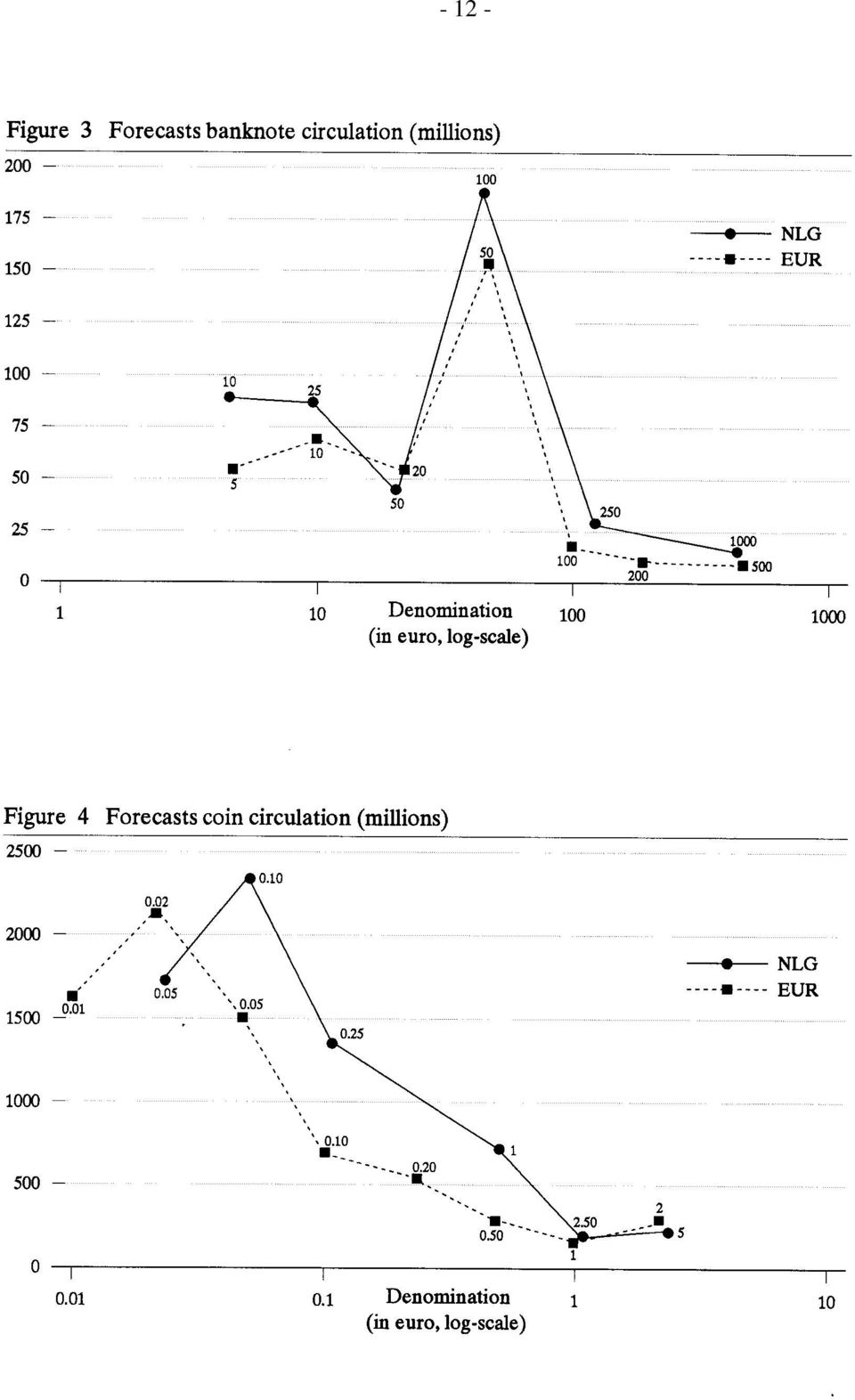

14 - 8 - Quality tests like these, that compare forecast performances, are useful to maintain or gain credibility as an institution. However, they are definitely not univocal and to enhance its practical use perhaps subjective probability statements in the sense of degrees of belief should be attached to the predictions. However what I want to emphasize foremost at this point is that I see the use of large macroeconometric models still as an essential tool for the Bank s policy making. Their forecast performance may fluctuate over time, and the projections are never undisputable, but these projections are nevertheless very essential tools in the decision making, in our case monetary policy process. A similar view is held at the ECB in Frankfurt and its staff. Example III: Forecasting the euro circulation The final example I want to discuss is a more tangible forecast example 5. As said before, in 2002, euro banknotes and euro coins will be put into circulation in the EMU countries. In the Netherlands this implies that the current twelve guilder-denominations -six banknotes and six coins- will be replaced by fifteen euro denominations. Compared with the present situation in the Netherlands one more banknote and two more coins will be introduced. This alteration in composition is a major problem in forecasting the disaggregated demand for euro notes and coins. As production has to start well in advance in order to produce the whole amount of notes and coins, anticipated forecasts per denomination were needed for a considerable period ahead, i.e. more than 3 years 6. To give you an idea of the composition of the circulation, Figure 2 shows the composition in 1998, which was used as the base year in the forecast. The Dutch notes circulation has been studied widely at the Bank. Already two decades ago an econometric model to forecast was developed 7. This model explains the demand for each banknote by looking at personal consumption and short-term interest rates. As personal consumption increases, the demand for notes increases. Moreover, with the increase of nominal consumption, we see a shift towards the higher denominations, due to the pattern of elasticities. Next to this positive effect of consumption on demand for notes, the interest rate has a clear negative effect. Apparently, the demand for notes decreases whenever there is an opportunity cost of interest income. 5 For more details on this issue, see G.E. Hebbink and H.M.M. Peeters, The circulation of euro banknotes and coins in the Netherlands, 1999, De Economist 147, As a matter of fact, production of both notes and coins started at the beginning of this year. 7 See e.g. M.M.G. Fase and M. van Nieuwkerk, 1976, The banknote circulation in the netherlands since 1900; Prospect and Retrospect, De Nederlandsche Bank, Quarterly Statistics, pp

15 - 9 -

16 Empirical research shows, however, that the effects are only significant for the larger denominations. Recently, the point-of-sales terminals (POS terminals, for short 8 ) and other innovations in the payment system have been added. To give you a flavour of these influences, the estimated impact elasticities of main factors involved are shown in Table 1. Table 1 The long-term (semi-)elasticities Denomination Private consumption elasticity Short-term Interest rate Semi-elasticity POS-turnover Elasticity NLG. 1, NLG NLG NLG NLG NLG Long run relationship : CU IT = C T + 2 R T + 3 POS T In contrast to the notes circulation, far less research has been done on the coins circulation 9. For the purpose of forecasting the need for coins in 2002, an unrestricted VARIX(1,1) was therefore estimated 10. Thus, on the basis of assumptions about future developments with respect to consumption, the interest rate and the use POS terminals, forecasts were made. In this way forecasts for each coin denomination in 2002 become available. In order to forecast the euro circulation, however, two important additional assumptions were made. First, an assumption was needed on the conversion from guilders into euro. As we do not have any relevant benchmark or knowledge, this is carried out in a pragmatic way as shown in Table 2. Here, as one can see, the demand for the EUR 200 notes for which we do not have an equivalent in guilders, is assumed to consist of 20% of the notes of NFG 1000 and 80% of notes of NFG 250. A similar assumption is made for the (new) coin of 20 euro cents. The demand for the coin of 1 euro cent is finally assumed to equal 40% of the NFG Second, more factors than only consumption, interest rates 8 Along with the POS terminals, the cash dispensers also play an important role. As yet, no long times series exist on the use of the cash machines. But the effect of the cash dispensers on the demand for notes remains an item on the DNB-agenda for future research. 9 See chapter 10 of M.M.G. Fase, On Money and Credit in Europe, 1998, Edward Elgar, UK. 10 A VARIX(1,1) is a Vector-AutoRegressive process of first order, that is integrated of first order, and has additional exogenous variables.

elasticities Denomination Private consumption elasticity Short-term Interest rate Semi-elasticity POS-turnover Elasticity NLG. 1,000 0.95-0.097 0 NLG. 250 0.92-0.033-0.")

17 Table 2 Assumed conversion ratio from guilders into euros , Vertical axis: guilder-denominations. Horizontal axis: euro-denominations. For example: Fl. 1,000 is assumed to be converted for 80% in 500-euro-notes and for 20% in 200-euro-notes. and POS-turnover will influence the demand for euro notes and coins. One such factor is electronic money. One may suspect that electronic money may have an impact on future circulation by the more and more intensive use of the Internet. Another factor is that not each guilder note and coin currently in circulation, will be offered for exchange in In particular, coins are often lost, kept by tourists as a collector s item. This characteristic will also reduce euro demand. Although these latter factors are extremely hard to measure, they will definitely have an substantial impact. Therefore, the impact is roughly estimated by means of proxies taken from other studies. The final result is that we arrive at projections of all fifteen euro-denominations in notes and coins as shown in Figures 3 and 4. What I would like to illustrate with this forecasting example is again the mixture of econometrics, pragmatics and economic intuition leading to projections or judgemental forecasts that are used as an input in the policy-making process. In this case this policy concerns the payment system, that is still an important task of the Bank according to the Bank Act 1998 (that replaced Bank Act 1948).

18 - 12 -

19 A REFLECTION ON A FUTURE AVENUE At the end of this paper, I want to return to stress once again, referring to the four examples given before, that forecasting at the Bank is still part and surely will remain part of her daily practice. So, the answer to the question raised in the title of this paper is confirmative: forecasting at the central bank is still à la mode 11! Talking about the methodology followed when forecasting, and playing on words like the The Economist tends to do - probably to make economics more attractive - I hasten to add that, in case the distribution of the forecast is asymmetric, my focus is not on the mode but on the median, and that rather than probability I, as indicated above, want to attach à la the young Keynes at forecasts a degree of belief or subjective probability 12. Ten years ago, in a provocative essay, the American new Keynesian scholar N. Gregory Mankiw pointed out a difference in sympathy of large-scale macroeconometric modellers and a majority of those in the academic macroeconomic profession 13. He questioned the behaviour of many academics in their dislike of large-scale macroeconometric models and forecasting. In Mankiw s view - which I share - these rational expectations people neglected the wealth of information included in macromodel use by policy makers. According to Mankiw, this seems to be contrary to rational behaviour seeking to exploit all available information. And macroeconomic forecasters surely generate relevant information for decision making. As to the question what new avenues could be explored in modelling, I think that we should try to incorporate forward looking behaviour à la rational expectations to get, for instance, a better understanding of the capital flows in the world. The fact that we have much more integrated capital markets and that financial crises, as we have recently seen, can occur quite fast and have an enormous economic impact, has triggered new research fields already. Also, to come back in particular to EMU, the impact of the mergers and acquisitions among commercial banks and insurance companies, leads to huge financial conglomerates, requiring a new type of research. Again modelling and forecasting may be usefule although regulatory issues are also quite important. These studies should of course take maximum advantage of the micro data that have become available. 11 A phrase referring to Ken Wallis s comments on inflation forecasting at the Bank of England and the visual aids employed. The Economist, Finance and Economics: Economics Focus, titled A la mode, March 27th 1999, p J.M. Keynes, A treatise on probability. London N.G. Mankiw, Recent developments in macroeconomics: a very quick refresher course, Journal of Money, Credit and Banking 20, (1988),

20 Micro studies, also on firm and consumer levels, could generate much more knowledge about monetary transmission than presently available, taking into account that the strangth of monetary transmission differs across countries and financial arrangements 14. I strongly believe that in this field the research network of national central banks created in the ESCB may be of vital importance. This network also enables researchers to incorporate institutional elements to examine e.g. the monetary transmission processes. On this issue there are still important differences in institutional detail between the UK and continental Europe that count for the transmission process. Therefore, I think that macro- and micromodelling as well as forecasting will remain important analytical and practical tools. 14 M.M.G. Fase and G.A. de Bondt, Institutional environment and monetary transmission in the Euro area, Revue de la Banque, nr (forthcoming).

21 - 15 -

CHAPTER 11. AN OVEVIEW OF THE BANK OF ENGLAND QUARTERLY MODEL OF THE (BEQM)

") 1 CHAPTER 11. AN OVEVIEW OF THE BANK OF ENGLAND QUARTERLY MODEL OF THE (BEQM) This model is the main tool in the suite of models employed by the staff and the Monetary Policy Committee (MPC) in the construction

1 CHAPTER 11. AN OVEVIEW OF THE BANK OF ENGLAND QUARTERLY MODEL OF THE (BEQM) This model is the main tool in the suite of models employed by the staff and the Monetary Policy Committee (MPC) in the construction

The use of projections and forecasts in the ECB s monetary policy

The use of projections and forecasts in the ECB s monetary policy AIECE Conference, Brussels 6 November 2007 Hans-Joachim Klöckers Director Economic Developments ECB The views expressed in this presentation

The use of projections and forecasts in the ECB s monetary policy AIECE Conference, Brussels 6 November 2007 Hans-Joachim Klöckers Director Economic Developments ECB The views expressed in this presentation

The labour market, I: real wages, productivity and unemployment 7.1 INTRODUCTION

7 The labour market, I: real wages, productivity and unemployment 7.1 INTRODUCTION Since the 1970s one of the major issues in macroeconomics has been the extent to which low output and high unemployment

7 The labour market, I: real wages, productivity and unemployment 7.1 INTRODUCTION Since the 1970s one of the major issues in macroeconomics has been the extent to which low output and high unemployment

The Elasticity of Taxable Income: A Non-Technical Summary

The Elasticity of Taxable Income: A Non-Technical Summary John Creedy The University of Melbourne Abstract This paper provides a non-technical summary of the concept of the elasticity of taxable income,

The Elasticity of Taxable Income: A Non-Technical Summary John Creedy The University of Melbourne Abstract This paper provides a non-technical summary of the concept of the elasticity of taxable income,

Understanding Currency

Understanding Currency Overlay July 2010 PREPARED BY Gregory J. Leonberger, FSA Director of Research Abstract As portfolios have expanded to include international investments, investors must be aware of

Understanding Currency Overlay July 2010 PREPARED BY Gregory J. Leonberger, FSA Director of Research Abstract As portfolios have expanded to include international investments, investors must be aware of

5 Comparison with the Previous Convergence Programme and Sensitivity Analysis

5 Comparison with the Previous Convergence Programme and Sensitivity Analysis 5.1 Comparison with the Previous Macroeconomic Scenario The differences between the macroeconomic scenarios of the current

5 Comparison with the Previous Convergence Programme and Sensitivity Analysis 5.1 Comparison with the Previous Macroeconomic Scenario The differences between the macroeconomic scenarios of the current

Lars Heikensten: The krona, Sweden and EMU

Lars Heikensten: The krona, Sweden and EMU Speech by Mr Lars Heikensten, First Deputy Governor of the Sveriges Riksbank, at the Öhman Fondkommission, Stockholm, 13 November 2002. * * * During the past

Lars Heikensten: The krona, Sweden and EMU Speech by Mr Lars Heikensten, First Deputy Governor of the Sveriges Riksbank, at the Öhman Fondkommission, Stockholm, 13 November 2002. * * * During the past

DO WE NEED ALL EURO DENOMINATIONS?

DO WE NEED ALL EURO DENOMINATIONS? Jeanine Kippers De Nederlandsche Bank, Amsterdam and Philip Hans Franses Econometric Institute, Erasmus University Rotterdam November 7, 2003 Econometric Institute Report

DO WE NEED ALL EURO DENOMINATIONS? Jeanine Kippers De Nederlandsche Bank, Amsterdam and Philip Hans Franses Econometric Institute, Erasmus University Rotterdam November 7, 2003 Econometric Institute Report

Fiscal Consolidation During a Depression

NIESR Fiscal Consolidation During a Depression Nitika Bagaria*, Dawn Holland** and John van Reenen* *London School of Economics **National Institute of Economic and Social Research October 2012 Project

NIESR Fiscal Consolidation During a Depression Nitika Bagaria*, Dawn Holland** and John van Reenen* *London School of Economics **National Institute of Economic and Social Research October 2012 Project

The Macroeconomic Effects of Tax Changes: The Romer-Romer Method on the Austrian case

The Macroeconomic Effects of Tax Changes: The Romer-Romer Method on the Austrian case By Atila Kilic (2012) Abstract In 2010, C. Romer and D. Romer developed a cutting-edge method to measure tax multipliers

The Macroeconomic Effects of Tax Changes: The Romer-Romer Method on the Austrian case By Atila Kilic (2012) Abstract In 2010, C. Romer and D. Romer developed a cutting-edge method to measure tax multipliers

Texas Christian University. Department of Economics. Working Paper Series. Modeling Interest Rate Parity: A System Dynamics Approach

Texas Christian University Department of Economics Working Paper Series Modeling Interest Rate Parity: A System Dynamics Approach John T. Harvey Department of Economics Texas Christian University Working

Texas Christian University Department of Economics Working Paper Series Modeling Interest Rate Parity: A System Dynamics Approach John T. Harvey Department of Economics Texas Christian University Working

Commentary: What Do Budget Deficits Do?

Commentary: What Do Budget Deficits Do? Allan H. Meltzer The title of Ball and Mankiw s paper asks: What Do Budget Deficits Do? One answer to that question is a restatement on the pure theory of debt-financed

Commentary: What Do Budget Deficits Do? Allan H. Meltzer The title of Ball and Mankiw s paper asks: What Do Budget Deficits Do? One answer to that question is a restatement on the pure theory of debt-financed

T T Mboweni: Economic growth, inflation and monetary policy in South Africa

T T Mboweni: Economic growth, inflation and monetary policy in South Africa Speech by Mr T T Mboweni, Governor of the South African Reserve Bank, at the business conference of the Bureau for Economic Research,

T T Mboweni: Economic growth, inflation and monetary policy in South Africa Speech by Mr T T Mboweni, Governor of the South African Reserve Bank, at the business conference of the Bureau for Economic Research,

CH 10 - REVIEW QUESTIONS

CH 10 - REVIEW QUESTIONS 1. The short-run aggregate supply curve is horizontal at: A) a level of output determined by aggregate demand. B) the natural level of output. C) the level of output at which the

CH 10 - REVIEW QUESTIONS 1. The short-run aggregate supply curve is horizontal at: A) a level of output determined by aggregate demand. B) the natural level of output. C) the level of output at which the

Lars Nyberg: The Riksbank's monetary policy strategy

Lars Nyberg: The Riksbank's monetary policy strategy Speech by Mr Lars Nyberg, Deputy Governor of the Sveriges Riksbank, at the Foreign Banker s Association, Stockholm, 14 September 2006. Introduction

Lars Nyberg: The Riksbank's monetary policy strategy Speech by Mr Lars Nyberg, Deputy Governor of the Sveriges Riksbank, at the Foreign Banker s Association, Stockholm, 14 September 2006. Introduction

Finance 581: Arbitrage and Purchasing Power Parity Conditions Module 5: Lecture 1 [Speaker: Sheen Liu] [On Screen]

![Finance 581: Arbitrage and Purchasing Power Parity Conditions Module 5: Lecture 1 [Speaker: Sheen Liu] [On Screen]](/thumbs/40/21465294.jpg "Finance 581: Arbitrage and Purchasing Power Parity Conditions Module 5: Lecture 1 [Speaker: Sheen Liu] [On Screen]") Finance 581: Arbitrage and Purchasing Power Parity Conditions Module 5: Lecture 1 [Speaker: Sheen Liu] MODULE 5 Arbitrage and Purchasing Power Parity Conditions [Sheen Liu]: Managers of multinational firms,

Finance 581: Arbitrage and Purchasing Power Parity Conditions Module 5: Lecture 1 [Speaker: Sheen Liu] MODULE 5 Arbitrage and Purchasing Power Parity Conditions [Sheen Liu]: Managers of multinational firms,

85 Quantifying the Impact of Oil Prices on Inflation

85 Quantifying the Impact of Oil Prices on Inflation By Colin Bermingham* Abstract The substantial increase in the volatility of oil prices over the past six or seven years has provoked considerable comment

85 Quantifying the Impact of Oil Prices on Inflation By Colin Bermingham* Abstract The substantial increase in the volatility of oil prices over the past six or seven years has provoked considerable comment

Statistics Netherlands. Macroeconomic Imbalances Factsheet

Macroeconomic Imbalances Factsheet Introduction Since the outbreak of the credit crunch crisis in 2008, and the subsequent European debt crisis, it has become clear that there are large macroeconomic imbalances

Macroeconomic Imbalances Factsheet Introduction Since the outbreak of the credit crunch crisis in 2008, and the subsequent European debt crisis, it has become clear that there are large macroeconomic imbalances

Monetary Policy Bank of Canada

Bank of Canada The objective of monetary policy may be gleaned from to preamble to the Bank of Canada Act of 1935 which says, regulate credit and currency in the best interests of the economic life of

Bank of Canada The objective of monetary policy may be gleaned from to preamble to the Bank of Canada Act of 1935 which says, regulate credit and currency in the best interests of the economic life of

Do Currency Unions Affect Foreign Direct Investment? Evidence from US FDI Flows into the European Union

Economic Issues, Vol. 10, Part 2, 2005 Do Currency Unions Affect Foreign Direct Investment? Evidence from US FDI Flows into the European Union Kyriacos Aristotelous 1 ABSTRACT This paper investigates the

Economic Issues, Vol. 10, Part 2, 2005 Do Currency Unions Affect Foreign Direct Investment? Evidence from US FDI Flows into the European Union Kyriacos Aristotelous 1 ABSTRACT This paper investigates the

The Economic Importance of the Country of Origin Principle in the Proposed Services Directive. Final report

The Economic Importance of the Country of Origin Principle in the Proposed Services Final report Table of Contents Preface... 3 Executive summary... 4 Chapter 1 The economic importance of the Country of

The Economic Importance of the Country of Origin Principle in the Proposed Services Final report Table of Contents Preface... 3 Executive summary... 4 Chapter 1 The economic importance of the Country of

CHAPTER 7: AGGREGATE DEMAND AND AGGREGATE SUPPLY

CHAPTER 7: AGGREGATE DEMAND AND AGGREGATE SUPPLY Learning goals of this chapter: What forces bring persistent and rapid expansion of real GDP? What causes inflation? Why do we have business cycles? How

CHAPTER 7: AGGREGATE DEMAND AND AGGREGATE SUPPLY Learning goals of this chapter: What forces bring persistent and rapid expansion of real GDP? What causes inflation? Why do we have business cycles? How

Main Indicators for the Finnish Economy

BANK OF FINLAND Monetary Policy and Research - Financial Markets and Statistics Main Indicators for the Finnish Economy 1/11 January 1 January 11 Monetary Policy and Research - Financial Markets and Statistics

BANK OF FINLAND Monetary Policy and Research - Financial Markets and Statistics Main Indicators for the Finnish Economy 1/11 January 1 January 11 Monetary Policy and Research - Financial Markets and Statistics

Oxford University Business Economics Programme

The Open Economy Gavin Cameron Tuesday 10 July 2001 Oxford University Business Economics Programme the exchange rate The nominal exchange rate is simply the price of one currency in terms of another pounds

The Open Economy Gavin Cameron Tuesday 10 July 2001 Oxford University Business Economics Programme the exchange rate The nominal exchange rate is simply the price of one currency in terms of another pounds

Main Indicators for the Finnish Economy

BANK OF FINLAND Monetary Policy and Research - Financial Markets and Statistics Main Indicators for the Finnish Economy 3/11 17 March 11 Main Indicators for the Finnish Economy is produced jointly by the

BANK OF FINLAND Monetary Policy and Research - Financial Markets and Statistics Main Indicators for the Finnish Economy 3/11 17 March 11 Main Indicators for the Finnish Economy is produced jointly by the

DEMB Working Paper Series N. 53. What Drives US Inflation and Unemployment in the Long Run? Antonio Ribba* May 2015

DEMB Working Paper Series N. 53 What Drives US Inflation and Unemployment in the Long Run? Antonio Ribba* May 2015 *University of Modena and Reggio Emilia RECent (Center for Economic Research) Address:

DEMB Working Paper Series N. 53 What Drives US Inflation and Unemployment in the Long Run? Antonio Ribba* May 2015 *University of Modena and Reggio Emilia RECent (Center for Economic Research) Address:

Inflation Risk and the Private Investor: Saving is often not the best decision

Inflation Risk and the Private Investor: Saving is often not the best decision February 2013 Inflation Risk and the Private Investor: Saving is often not the best decision Authors: Ronald A.M. Janssen,

Inflation Risk and the Private Investor: Saving is often not the best decision February 2013 Inflation Risk and the Private Investor: Saving is often not the best decision Authors: Ronald A.M. Janssen,

Aggregate Demand and Aggregate Supply Ing. Mansoor Maitah Ph.D. et Ph.D.

Aggregate Demand and Aggregate Supply Ing. Mansoor Maitah Ph.D. et Ph.D. Aggregate Demand and Aggregate Supply Economic fluctuations, also called business cycles, are movements of GDP away from potential

Aggregate Demand and Aggregate Supply Ing. Mansoor Maitah Ph.D. et Ph.D. Aggregate Demand and Aggregate Supply Economic fluctuations, also called business cycles, are movements of GDP away from potential

The Equity Premium in India

The Equity Premium in India Rajnish Mehra University of California, Santa Barbara and National Bureau of Economic Research January 06 Prepared for the Oxford Companion to Economics in India edited by Kaushik

The Equity Premium in India Rajnish Mehra University of California, Santa Barbara and National Bureau of Economic Research January 06 Prepared for the Oxford Companion to Economics in India edited by Kaushik

Main Indicators for the Finnish Economy

BANK OF FINLAND Monetary Policy and Research - Financial Markets and Statistics Main Indicators for the Finnish Economy /1 13 April 1 13 April 1 Monetary Policy and Research - Financial Markets and Statistics

BANK OF FINLAND Monetary Policy and Research - Financial Markets and Statistics Main Indicators for the Finnish Economy /1 13 April 1 13 April 1 Monetary Policy and Research - Financial Markets and Statistics

A. Introduction. 1. Motivation

A. Introduction 1. Motivation One issue for currency areas such as the European Monetary Union (EMU) is that not necessarily one size fits all, i.e. the interest rate setting of the central bank cannot

A. Introduction 1. Motivation One issue for currency areas such as the European Monetary Union (EMU) is that not necessarily one size fits all, i.e. the interest rate setting of the central bank cannot

a) Aggregate Demand (AD) and Aggregate Supply (AS) analysis

Aggregate Demand (AD) and Aggregate Supply (AS) analysis") a) Aggregate Demand (AD) and Aggregate Supply (AS) analysis Determinants of AD: Aggregate demand is the total demand in the economy. It measures spending on goods and services by consumers, firms, the

a) Aggregate Demand (AD) and Aggregate Supply (AS) analysis Determinants of AD: Aggregate demand is the total demand in the economy. It measures spending on goods and services by consumers, firms, the

Consumer Price Indices in the UK. Main Findings

Consumer Price Indices in the UK Main Findings The report Consumer Price Indices in the UK, written by Mark Courtney, assesses the array of official inflation indices in terms of their suitability as an

Consumer Price Indices in the UK Main Findings The report Consumer Price Indices in the UK, written by Mark Courtney, assesses the array of official inflation indices in terms of their suitability as an

Interpreting Market Responses to Economic Data

Interpreting Market Responses to Economic Data Patrick D Arcy and Emily Poole* This article discusses how bond, equity and foreign exchange markets have responded to the surprise component of Australian

Interpreting Market Responses to Economic Data Patrick D Arcy and Emily Poole* This article discusses how bond, equity and foreign exchange markets have responded to the surprise component of Australian

Do Commodity Price Spikes Cause Long-Term Inflation?

No. 11-1 Do Commodity Price Spikes Cause Long-Term Inflation? Geoffrey M.B. Tootell Abstract: This public policy brief examines the relationship between trend inflation and commodity price increases and

No. 11-1 Do Commodity Price Spikes Cause Long-Term Inflation? Geoffrey M.B. Tootell Abstract: This public policy brief examines the relationship between trend inflation and commodity price increases and

The Aggregate Demand- Aggregate Supply (AD-AS) Model

Model") The AD-AS Model The Aggregate Demand- Aggregate Supply (AD-AS) Model Chapter 9 The AD-AS Model addresses two deficiencies of the AE Model: No explicit modeling of aggregate supply. Fixed price level. 2

The AD-AS Model The Aggregate Demand- Aggregate Supply (AD-AS) Model Chapter 9 The AD-AS Model addresses two deficiencies of the AE Model: No explicit modeling of aggregate supply. Fixed price level. 2

ANNEX 1 - MACROECONOMIC IMPLICATIONS FOR ITALY OF ACHIEVING COMPLIANCE WITH THE DEBT RULE UNDER TWO DIFFERENT SCENARIOS

ANNEX 1 - MACROECONOMIC IMPLICATIONS FOR ITALY OF ACHIEVING COMPLIANCE WITH THE DEBT RULE UNDER TWO DIFFERENT SCENARIOS The aim of this note is first to illustrate the impact of a fiscal adjustment aimed

ANNEX 1 - MACROECONOMIC IMPLICATIONS FOR ITALY OF ACHIEVING COMPLIANCE WITH THE DEBT RULE UNDER TWO DIFFERENT SCENARIOS The aim of this note is first to illustrate the impact of a fiscal adjustment aimed

1 Scope and Objectives of Financial Management

1 Scope and Objectives of Financial Management BASIC CONCEPTS 1. Definition of Financial Management Financial management comprises the forecasting, planning, organizing, directing, co-ordinating and controlling

1 Scope and Objectives of Financial Management BASIC CONCEPTS 1. Definition of Financial Management Financial management comprises the forecasting, planning, organizing, directing, co-ordinating and controlling

Government and public sector debt measures

Introduction Government and public sector debt measures 1. One measure of governments performance in managing the public finances is the level of public sector debt. The definition and responsibilities

Introduction Government and public sector debt measures 1. One measure of governments performance in managing the public finances is the level of public sector debt. The definition and responsibilities

How carbon-proof is Kyoto?

How carbon-proof is Kyoto? Carbon leakage and hot air Arjan Lejour and Ton Manders* 1 Abstract Carbon leakage reduces the effectiveness of policies to reduce greenhouse gas emissions as agreed upon by

How carbon-proof is Kyoto? Carbon leakage and hot air Arjan Lejour and Ton Manders* 1 Abstract Carbon leakage reduces the effectiveness of policies to reduce greenhouse gas emissions as agreed upon by

Banking System Stress Testing

Date: 7.5.214 Number: Date: 17.6.214 14-4a Number: 14-55a Case Study www.riskcontrollimited.com Contents Introduction... 3 Generating Consistent Macroeconomic Scenarios... 4 Loan Portfolio Modelling...

Date: 7.5.214 Number: Date: 17.6.214 14-4a Number: 14-55a Case Study www.riskcontrollimited.com Contents Introduction... 3 Generating Consistent Macroeconomic Scenarios... 4 Loan Portfolio Modelling...

EFN REPORT. ECONOMIC OUTLOOK FOR THE EURO AREA IN 2016 and 2017

EFN REPORT ECONOMIC OUTLOOK FOR THE EURO AREA IN 2016 and 2017 Summer 2016 1 About the European ing Network The European ing Network (EFN) is a research group of European institutions, founded in 2001

EFN REPORT ECONOMIC OUTLOOK FOR THE EURO AREA IN 2016 and 2017 Summer 2016 1 About the European ing Network The European ing Network (EFN) is a research group of European institutions, founded in 2001

C A R I B B E A N E X A M I N A T I O N S C O U N C I L REPORT ON CANDIDATES WORK IN THE SECONDARY EDUCATION CERTIFICATE EXAMINATION MAY/JUNE 2011

C A R I B B E A N E X A M I N A T I O N S C O U N C I L REPORT ON CANDIDATES WORK IN THE SECONDARY EDUCATION CERTIFICATE EXAMINATION MAY/JUNE 2011 ECONOMICS GENERAL PROFICIENCY EXAMINATION Copyright 2011

C A R I B B E A N E X A M I N A T I O N S C O U N C I L REPORT ON CANDIDATES WORK IN THE SECONDARY EDUCATION CERTIFICATE EXAMINATION MAY/JUNE 2011 ECONOMICS GENERAL PROFICIENCY EXAMINATION Copyright 2011

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Suvey of Macroeconomics, MBA 641 Fall 2006, Final Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Modern macroeconomics emerged from

Suvey of Macroeconomics, MBA 641 Fall 2006, Final Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Modern macroeconomics emerged from

SHORT-RUN FLUCTUATIONS. David Romer. University of California, Berkeley. First version: August 1999 This revision: January 2012

SHORT-RUN FLUCTUATIONS David Romer University of California, Berkeley First version: August 1999 This revision: January 2012 Copyright 2012 by David Romer CONTENTS Preface vi I The IS-MP Model 1 I-1 Monetary

SHORT-RUN FLUCTUATIONS David Romer University of California, Berkeley First version: August 1999 This revision: January 2012 Copyright 2012 by David Romer CONTENTS Preface vi I The IS-MP Model 1 I-1 Monetary

Capital Markets Memorandum

Capital Markets Memorandum Capital Markets and Asset Allocation insights from Frontier Advisors Frontier s Medium Term Fundamental Currency Model November 014 Alvin Tan is a member of the Capital Markets

Capital Markets Memorandum Capital Markets and Asset Allocation insights from Frontier Advisors Frontier s Medium Term Fundamental Currency Model November 014 Alvin Tan is a member of the Capital Markets

Money market portfolio

1 Money market portfolio April 11 Management of Norges Bank s money market portfolio Report for the fourth quarter 1 Contents 1 Key figures Market value and return 3 3 Market risk and management guidelines

1 Money market portfolio April 11 Management of Norges Bank s money market portfolio Report for the fourth quarter 1 Contents 1 Key figures Market value and return 3 3 Market risk and management guidelines

A layperson s guide to monetary policy

1999/8 17 December 1999 A layperson s guide to Executive Summary Monetary policy refers to those actions by the Reserve Bank which affect interest rates, the exchange rate and the money supply. The objective

1999/8 17 December 1999 A layperson s guide to Executive Summary Monetary policy refers to those actions by the Reserve Bank which affect interest rates, the exchange rate and the money supply. The objective

The Bank of Italy and the euro

Association of the Economic Representatives of the OECD countries in Rome The Bank of Italy and the euro Speech by Antonio Finocchiaro Deputy Director General of the Bank of Italy Rome, 11 October 2001

Association of the Economic Representatives of the OECD countries in Rome The Bank of Italy and the euro Speech by Antonio Finocchiaro Deputy Director General of the Bank of Italy Rome, 11 October 2001

The Impact of Interest Rate Shocks on the Performance of the Banking Sector

The Impact of Interest Rate Shocks on the Performance of the Banking Sector by Wensheng Peng, Kitty Lai, Frank Leung and Chang Shu of the Research Department A rise in the Hong Kong dollar risk premium,

The Impact of Interest Rate Shocks on the Performance of the Banking Sector by Wensheng Peng, Kitty Lai, Frank Leung and Chang Shu of the Research Department A rise in the Hong Kong dollar risk premium,

EMU and the monetary transmission mechanism. EMU study

EMU and the monetary transmission mechanism EMU study EMU and the monetary transmission mechanism EMU study This study has been prepared by HM Treasury to inform the assessment of the five economic tests

EMU and the monetary transmission mechanism EMU study EMU and the monetary transmission mechanism EMU study This study has been prepared by HM Treasury to inform the assessment of the five economic tests

PROJECTION OF THE FISCAL BALANCE AND PUBLIC DEBT (2012 2027) - SUMMARY

- SUMMARY") PROJECTION OF THE FISCAL BALANCE AND PUBLIC DEBT (2012 2027) - SUMMARY PUBLIC FINANCE REVIEW February 2013 SUMMARY Key messages The purpose of our analysis is to highlight the risks that fiscal policy

PROJECTION OF THE FISCAL BALANCE AND PUBLIC DEBT (2012 2027) - SUMMARY PUBLIC FINANCE REVIEW February 2013 SUMMARY Key messages The purpose of our analysis is to highlight the risks that fiscal policy

Adverse macro-financial scenario for the EBA 2016 EU-wide bank stress testing exercise

29 January 2016 Adverse macro-financial scenario for the EBA 2016 EU-wide bank stress testing exercise The European Banking Authority (EBA) 2016 EU-wide stress testing exercise will require banks to use

29 January 2016 Adverse macro-financial scenario for the EBA 2016 EU-wide bank stress testing exercise The European Banking Authority (EBA) 2016 EU-wide stress testing exercise will require banks to use

MONETARY AND FISCAL POLICY IN THE VERY SHORT RUN

C H A P T E R12 MONETARY AND FISCAL POLICY IN THE VERY SHORT RUN LEARNING OBJECTIVES After reading and studying this chapter, you should be able to: Understand that both fiscal and monetary policy can

C H A P T E R12 MONETARY AND FISCAL POLICY IN THE VERY SHORT RUN LEARNING OBJECTIVES After reading and studying this chapter, you should be able to: Understand that both fiscal and monetary policy can

INFLATION, INTEREST RATE, AND EXCHANGE RATE: WHAT IS THE RELATIONSHIP?

107 INFLATION, INTEREST RATE, AND EXCHANGE RATE: WHAT IS THE RELATIONSHIP? Maurice K. Shalishali, Columbus State University Johnny C. Ho, Columbus State University ABSTRACT A test of IFE (International

107 INFLATION, INTEREST RATE, AND EXCHANGE RATE: WHAT IS THE RELATIONSHIP? Maurice K. Shalishali, Columbus State University Johnny C. Ho, Columbus State University ABSTRACT A test of IFE (International

With lectures 1-8 behind us, we now have the tools to support the discussion and implementation of economic policy.

The Digital Economist Lecture 9 -- Economic Policy With lectures 1-8 behind us, we now have the tools to support the discussion and implementation of economic policy. There is still great debate about

The Digital Economist Lecture 9 -- Economic Policy With lectures 1-8 behind us, we now have the tools to support the discussion and implementation of economic policy. There is still great debate about

MSc Finance and Economics detailed module information

MSc Finance and Economics detailed module information Example timetable Please note that information regarding modules is subject to change. TERM 1 TERM 2 TERM 3 INDUCTION WEEK EXAM PERIOD Week 1 EXAM

MSc Finance and Economics detailed module information Example timetable Please note that information regarding modules is subject to change. TERM 1 TERM 2 TERM 3 INDUCTION WEEK EXAM PERIOD Week 1 EXAM

The European Union s Economic and Monetary Union

The European Union s Economic and Monetary Union Lesson Focus Question How do individuals, businesses, and economies benefit from using the Euro? Introduction In this lesson students will examine the benefits

The European Union s Economic and Monetary Union Lesson Focus Question How do individuals, businesses, and economies benefit from using the Euro? Introduction In this lesson students will examine the benefits

7 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Chapter. Key Concepts

Chapter 7 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Key Concepts Aggregate Supply The aggregate production function shows that the quantity of real GDP (Y ) supplied depends on the quantity of labor (L ),

Chapter 7 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Key Concepts Aggregate Supply The aggregate production function shows that the quantity of real GDP (Y ) supplied depends on the quantity of labor (L ),

Session 12. Aggregate Supply: The Phillips curve. Credibility

Session 12. Aggregate Supply: The Phillips curve. Credibility v Potential Output and v Okun s law v The Role of Expectations and the Phillips Curve v Oil Prices and v US Monetary Policy and World Real

Session 12. Aggregate Supply: The Phillips curve. Credibility v Potential Output and v Okun s law v The Role of Expectations and the Phillips Curve v Oil Prices and v US Monetary Policy and World Real

EUROPEAN MONETARY SYSTEM

EUROPEAN MONETARY SYSTEM 1. Bretton Woods 2. Exchange rate determination Fixed v flexible exchange rates 3. Breakdown of Bretton Woods: Werner Report Snake in the tunnel 4. European Monetary System (EMS)

EUROPEAN MONETARY SYSTEM 1. Bretton Woods 2. Exchange rate determination Fixed v flexible exchange rates 3. Breakdown of Bretton Woods: Werner Report Snake in the tunnel 4. European Monetary System (EMS)

Econ 202 H01 Final Exam Spring 2005

Econ202Final Spring 2005 1 Econ 202 H01 Final Exam Spring 2005 1. Which of the following tends to reduce the size of a shift in aggregate demand? a. the multiplier effect b. the crowding-out effect c.

Econ202Final Spring 2005 1 Econ 202 H01 Final Exam Spring 2005 1. Which of the following tends to reduce the size of a shift in aggregate demand? a. the multiplier effect b. the crowding-out effect c.

ON THE DEATH OF THE PHILLIPS CURVE William A. Niskanen

ON THE DEATH OF THE PHILLIPS CURVE William A. Niskanen There is no evidence of a Phillips curve showing a tradeoff between unemployment and inflation. The function for estimating the nonaccelerating inflation

ON THE DEATH OF THE PHILLIPS CURVE William A. Niskanen There is no evidence of a Phillips curve showing a tradeoff between unemployment and inflation. The function for estimating the nonaccelerating inflation

2.5 Monetary policy: Interest rates

2.5 Monetary policy: Interest rates Learning Outcomes Describe the role of central banks as regulators of commercial banks and bankers to governments. Explain that central banks are usually made responsible

2.5 Monetary policy: Interest rates Learning Outcomes Describe the role of central banks as regulators of commercial banks and bankers to governments. Explain that central banks are usually made responsible

Static and dynamic analysis: basic concepts and examples

Static and dynamic analysis: basic concepts and examples Ragnar Nymoen Department of Economics, UiO 18 August 2009 Lecture plan and web pages for this course The lecture plan is at http://folk.uio.no/rnymoen/econ3410_h08_index.html,

Static and dynamic analysis: basic concepts and examples Ragnar Nymoen Department of Economics, UiO 18 August 2009 Lecture plan and web pages for this course The lecture plan is at http://folk.uio.no/rnymoen/econ3410_h08_index.html,

A Review of the Literature of Real Business Cycle theory. By Student E XXXXXXX

A Review of the Literature of Real Business Cycle theory By Student E XXXXXXX Abstract: The following paper reviews five articles concerning Real Business Cycle theory. First, the review compares the various

A Review of the Literature of Real Business Cycle theory By Student E XXXXXXX Abstract: The following paper reviews five articles concerning Real Business Cycle theory. First, the review compares the various

IV. Special feature: Foreign currency deposits of firms and individuals with banks in China

Robert N McCauley (+852) 2878 71 RMcCauley@bis.org.hk YK Mo (+852) 2878 71 IV. Special feature: deposits of firms and individuals with banks in China In principle, an economy with capital controls can

Robert N McCauley (+852) 2878 71 RMcCauley@bis.org.hk YK Mo (+852) 2878 71 IV. Special feature: deposits of firms and individuals with banks in China In principle, an economy with capital controls can

FISCAL POLICY* Chapter. Key Concepts

Chapter 11 FISCAL POLICY* Key Concepts The Federal Budget The federal budget is an annual statement of the government s expenditures and tax revenues. Using the federal budget to achieve macroeconomic

Chapter 11 FISCAL POLICY* Key Concepts The Federal Budget The federal budget is an annual statement of the government s expenditures and tax revenues. Using the federal budget to achieve macroeconomic

Reserve Bank of New Zealand Analytical Notes

Reserve Bank of New Zealand Analytical Notes Why the drivers of migration matter for the labour market AN26/2 Jed Armstrong and Chris McDonald April 26 Reserve Bank of New Zealand Analytical Note Series

Reserve Bank of New Zealand Analytical Notes Why the drivers of migration matter for the labour market AN26/2 Jed Armstrong and Chris McDonald April 26 Reserve Bank of New Zealand Analytical Note Series

How could a shock to growth in China affect growth in the United Kingdom?

4 Quarterly Bulletin 2016 Q1 How could a shock to growth in China affect growth in the United Kingdom? By Ambrogio Cesa-Bianchi and Kate Stratford of the Bank s Global Spillovers and Interconnections Division.

4 Quarterly Bulletin 2016 Q1 How could a shock to growth in China affect growth in the United Kingdom? By Ambrogio Cesa-Bianchi and Kate Stratford of the Bank s Global Spillovers and Interconnections Division.

Renminbi Depreciation and the Hong Kong Economy

Thomas Shik Acting Chief Economist thomasshik@hangseng.com Renminbi Depreciation and the Hong Kong Economy If the recent weakness of the renminbi persists, it is likely to have a positive direct impact

Thomas Shik Acting Chief Economist thomasshik@hangseng.com Renminbi Depreciation and the Hong Kong Economy If the recent weakness of the renminbi persists, it is likely to have a positive direct impact

Assessing the Value of Flexibility in the Dutch Office Sector using Real Option Analysis

Assessing the Value of Flexibility in the Dutch Office Sector using Real Option Analysis Joost P. Poort, Jun Hoo Abstract Flexibility is one of the key aspects of the Zuidas project, a major construction

Assessing the Value of Flexibility in the Dutch Office Sector using Real Option Analysis Joost P. Poort, Jun Hoo Abstract Flexibility is one of the key aspects of the Zuidas project, a major construction

Estimating the Market Risk Premium for Australia using a Benchmark Approach

Appendix B Estimating the Market Risk Premium for Australia using a Benchmark Approach 1 The market risk premium ( MRP ) for Australia in 2005 and going forward is set in an international market. Investment

Appendix B Estimating the Market Risk Premium for Australia using a Benchmark Approach 1 The market risk premium ( MRP ) for Australia in 2005 and going forward is set in an international market. Investment

Chapter 12 Unemployment and Inflation

Chapter 12 Unemployment and Inflation Multiple Choice Questions 1. The origin of the idea of a trade-off between inflation and unemployment was a 1958 article by (a) A.W. Phillips. (b) Edmund Phelps. (c)

Chapter 12 Unemployment and Inflation Multiple Choice Questions 1. The origin of the idea of a trade-off between inflation and unemployment was a 1958 article by (a) A.W. Phillips. (b) Edmund Phelps. (c)

Chapter 13. Aggregate Demand and Aggregate Supply Analysis

Chapter 13. Aggregate Demand and Aggregate Supply Analysis Instructor: JINKOOK LEE Department of Economics / Texas A&M University ECON 203 502 Principles of Macroeconomics In the short run, real GDP and

Chapter 13. Aggregate Demand and Aggregate Supply Analysis Instructor: JINKOOK LEE Department of Economics / Texas A&M University ECON 203 502 Principles of Macroeconomics In the short run, real GDP and

S.Y.B.COM. (SEM-III) ECONOMICS

ECONOMICS") Fill in the Blanks. Module 1 S.Y.B.COM. (SEM-III) ECONOMICS 1. The continuous flow of money and goods and services between firms and households is called the Circular Flow. 2. Saving constitute a leakage

Fill in the Blanks. Module 1 S.Y.B.COM. (SEM-III) ECONOMICS 1. The continuous flow of money and goods and services between firms and households is called the Circular Flow. 2. Saving constitute a leakage

Econ 202 Final Exam. Table 3-1 Labor Hours Needed to Make 1 Pound of: Meat Potatoes Farmer 8 2 Rancher 4 5

Econ 202 Final Exam 1. If inflation expectations rise, the short-run Phillips curve shifts a. right, so that at any inflation rate unemployment is higher. b. left, so that at any inflation rate unemployment

Econ 202 Final Exam 1. If inflation expectations rise, the short-run Phillips curve shifts a. right, so that at any inflation rate unemployment is higher. b. left, so that at any inflation rate unemployment

THE IMPACT OF FUTURE MARKET ON MONEY DEMAND IN IRAN

THE IMPACT OF FUTURE MARKET ON MONEY DEMAND IN IRAN Keikha M. 1 and *Shams Koloukhi A. 2 and Parsian H. 2 and Darini M. 3 1 Department of Economics, Allameh Tabatabaie University, Iran 2 Young Researchers

THE IMPACT OF FUTURE MARKET ON MONEY DEMAND IN IRAN Keikha M. 1 and *Shams Koloukhi A. 2 and Parsian H. 2 and Darini M. 3 1 Department of Economics, Allameh Tabatabaie University, Iran 2 Young Researchers

Econ 336 - Spring 2007 Homework 5

Econ 336 - Spring 2007 Homework 5 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The real exchange rate, q, is defined as A) E times P B)

Econ 336 - Spring 2007 Homework 5 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The real exchange rate, q, is defined as A) E times P B)

Use the following to answer question 9: Exhibit: Keynesian Cross

1. Leading economic indicators are: A) the most popular economic statistics. B) data that are used to construct the consumer price index and the unemployment rate. C) variables that tend to fluctuate in

1. Leading economic indicators are: A) the most popular economic statistics. B) data that are used to construct the consumer price index and the unemployment rate. C) variables that tend to fluctuate in

What is the neutral interest rate level? Is it worthwhile searching for it from a market perspective? Bjørn Roger Wilhelmsen

What is the neutral interest rate level? Is it worthwhile searching for it from a market perspective? Bjørn Roger Wilhelmsen The neutral rate a crucial concept in monetary theory h A benchmark for monetary

What is the neutral interest rate level? Is it worthwhile searching for it from a market perspective? Bjørn Roger Wilhelmsen The neutral rate a crucial concept in monetary theory h A benchmark for monetary

Nigel Jenkinson: Developing a framework for stress testing of financial stability risks

Nigel Jenkinson: Developing a framework for stress testing of financial stability risks Comments by Mr Nigel Jenkinson, Executive Director, Financial Stability, Bank of England, at the ECB High Level Conference

Nigel Jenkinson: Developing a framework for stress testing of financial stability risks Comments by Mr Nigel Jenkinson, Executive Director, Financial Stability, Bank of England, at the ECB High Level Conference

7 AGGREGATE SUPPLY AND AGGREGATE DEMAND* * Chapter Key Ideas. Outline

C h a p t e r 7 AGGREGATE SUPPLY AND AGGREGATE DEMAND* * Chapter Key Ideas Outline Production and Prices A. What forces bring persistent and rapid expansion of real GDP? B. What leads to inflation? C.

C h a p t e r 7 AGGREGATE SUPPLY AND AGGREGATE DEMAND* * Chapter Key Ideas Outline Production and Prices A. What forces bring persistent and rapid expansion of real GDP? B. What leads to inflation? C.

1. Firms react to unplanned inventory investment by increasing output.

Macro Exam 2 Self Test -- T/F questions Dr. McGahagan Fill in your answer (T/F) in the blank in front of the question. If false, provide a brief explanation of why it is false, and state what is true.

Macro Exam 2 Self Test -- T/F questions Dr. McGahagan Fill in your answer (T/F) in the blank in front of the question. If false, provide a brief explanation of why it is false, and state what is true.

Import Prices and Inflation

Import Prices and Inflation James D. Hamilton Department of Economics, University of California, San Diego Understanding the consequences of international developments for domestic inflation is an extremely

Import Prices and Inflation James D. Hamilton Department of Economics, University of California, San Diego Understanding the consequences of international developments for domestic inflation is an extremely

Econ 202 Section 4 Final Exam

Douglas, Fall 2009 December 15, 2009 A: Special Code 00004 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 202 Section 4 Final Exam 1. Oceania buys $40

Douglas, Fall 2009 December 15, 2009 A: Special Code 00004 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 202 Section 4 Final Exam 1. Oceania buys $40

OPINION OF THE EUROPEAN CENTRAL BANK

EN ECB-PUBLIC OPINION OF THE EUROPEAN CENTRAL BANK of 24 January 2012 on a guarantee scheme for the liabilities of Italian banks and on the exchange of lira banknotes (CON/2012/4) Introduction and legal

EN ECB-PUBLIC OPINION OF THE EUROPEAN CENTRAL BANK of 24 January 2012 on a guarantee scheme for the liabilities of Italian banks and on the exchange of lira banknotes (CON/2012/4) Introduction and legal

Econ 303: Intermediate Macroeconomics I Dr. Sauer Sample Questions for Exam #3

Econ 303: Intermediate Macroeconomics I Dr. Sauer Sample Questions for Exam #3 1. When firms experience unplanned inventory accumulation, they typically: A) build new plants. B) lay off workers and reduce

Econ 303: Intermediate Macroeconomics I Dr. Sauer Sample Questions for Exam #3 1. When firms experience unplanned inventory accumulation, they typically: A) build new plants. B) lay off workers and reduce

2 0 0 0 E D I T I O N CLEP O F F I C I A L S T U D Y G U I D E. The College Board. College Level Examination Program

2 0 0 0 E D I T I O N CLEP O F F I C I A L S T U D Y G U I D E College Level Examination Program The College Board Principles of Macroeconomics Description of the Examination The Subject Examination in

2 0 0 0 E D I T I O N CLEP O F F I C I A L S T U D Y G U I D E College Level Examination Program The College Board Principles of Macroeconomics Description of the Examination The Subject Examination in

Macroeconomics, Fall 2007 Exam 3, TTh classes, various versions

Name: _ Days/Times Class Meets: Today s Date: Macroeconomics, Fall 2007 Exam 3, TTh classes, various versions Read these Instructions carefully! You must follow them exactly! I) On your Scantron card you

Name: _ Days/Times Class Meets: Today s Date: Macroeconomics, Fall 2007 Exam 3, TTh classes, various versions Read these Instructions carefully! You must follow them exactly! I) On your Scantron card you

A European Unemployment Insurance Scheme

A European Unemployment Insurance Scheme Necessary? Desirable? Optimal? Grégory Claeys, Research Fellow, Bruegel Zsolt Darvas, Senior Fellow, Bruegel Guntram Wolff, Director, Bruegel July, 2014 Key messages

A European Unemployment Insurance Scheme Necessary? Desirable? Optimal? Grégory Claeys, Research Fellow, Bruegel Zsolt Darvas, Senior Fellow, Bruegel Guntram Wolff, Director, Bruegel July, 2014 Key messages

10 DOWNING STREET LONDON SWtA 2AA A NEW SETTLEMENT FOR THE UNITED KINGDOM IN A REFORMED EUROPEAN UNION

> 10 DOWNING STREET LONDON SWtA 2AA THE PRIME MINISTER 10 November 2015 A NEW SETTLEMENT FOR THE UNITED KINGDOM IN A REFORMED EUROPEAN UNION Thank you for inviting me to write setting out the areas where

> 10 DOWNING STREET LONDON SWtA 2AA THE PRIME MINISTER 10 November 2015 A NEW SETTLEMENT FOR THE UNITED KINGDOM IN A REFORMED EUROPEAN UNION Thank you for inviting me to write setting out the areas where

Working Paper No. 549. Excess Capital and Liquidity Management

Working Paper No. 549 Excess Capital and Liquidity Management by Jan Toporowski Economics Department, School of Oriental and African Studies, University of London and the Research Centre for the History

Working Paper No. 549 Excess Capital and Liquidity Management by Jan Toporowski Economics Department, School of Oriental and African Studies, University of London and the Research Centre for the History

Economics 152 Solution to Sample Midterm 2

Economics 152 Solution to Sample Midterm 2 N. Das PART 1 (84 POINTS): Answer the following 28 multiple choice questions on the scan sheet. Each question is worth 3 points. 1. If Congress passes legislation

Economics 152 Solution to Sample Midterm 2 N. Das PART 1 (84 POINTS): Answer the following 28 multiple choice questions on the scan sheet. Each question is worth 3 points. 1. If Congress passes legislation

Davy Defensive High Yield Fund from New Ireland

Davy Asset Management For Financial Advisors Only Davy Defensive High Yield Fund from New Ireland Davy Asset Management is regulated by the Central Bank of Ireland. Exposure to: equity-market type returns

Davy Asset Management For Financial Advisors Only Davy Defensive High Yield Fund from New Ireland Davy Asset Management is regulated by the Central Bank of Ireland. Exposure to: equity-market type returns

The Norwegian economy

The Norwegian economy Slower speed ahead, but still growth Strong mechanisms support mainland economy Wriggle room to smooth business cycles Rune Bjerke CEO Just how bad is it? Slower speed ahead but still

The Norwegian economy Slower speed ahead, but still growth Strong mechanisms support mainland economy Wriggle room to smooth business cycles Rune Bjerke CEO Just how bad is it? Slower speed ahead but still

Research and Statistics Department, Bank of Japan. E-mail: yoshiko.satou@boj.or.jp

&200(176216(66,21, $66(66,1*38%/,&/,$%,/,7,(6

&200(176216(66,21, $66(66,1*38%/,&/,$%,/,7,(6

The current economic situation in Germany. Deutsche Bundesbank Monthly Report February 2015 5

The current economic situation in Germany Deutsche Bundesbank 5 6 Overview Global economy German economy emerging from sluggish phase faster than expected The global economy looks to have expanded in the

The current economic situation in Germany Deutsche Bundesbank 5 6 Overview Global economy German economy emerging from sluggish phase faster than expected The global economy looks to have expanded in the

12.1 Introduction. 12.2 The MP Curve: Monetary Policy and the Interest Rates 1/24/2013. Monetary Policy and the Phillips Curve

Chapter 12 Monetary Policy and the Phillips Curve By Charles I. Jones Media Slides Created By Dave Brown Penn State University The short-run model summary: Through the MP curve the nominal interest rate

Chapter 12 Monetary Policy and the Phillips Curve By Charles I. Jones Media Slides Created By Dave Brown Penn State University The short-run model summary: Through the MP curve the nominal interest rate

Professor Christina Romer. LECTURE 17 MACROECONOMIC VARIABLES AND ISSUES March 17, 2016

Economics 2 Spring 2016 Professor Christina Romer Professor David Romer LECTURE 17 MACROECONOMIC VARIABLES AND ISSUES March 17, 2016 I. MACROECONOMICS VERSUS MICROECONOMICS II. REAL GDP A. Definition B.

Economics 2 Spring 2016 Professor Christina Romer Professor David Romer LECTURE 17 MACROECONOMIC VARIABLES AND ISSUES March 17, 2016 I. MACROECONOMICS VERSUS MICROECONOMICS II. REAL GDP A. Definition B.