Indicators for shock resilience and pro cyclicality at the Central Bank of Hungary Gergely Fabian

|

|

|

- Vivien Flowers

- 7 years ago

- Views:

Transcription

1 Indicators for shock resilience and pro cyclicality at the Central Bank of Hungary Gergely Fabian Workshop for heads of financial stability, Bank of England February 2016

2 Table of content Motivation Credit cycle Stress tests Portfólió-tisztítási gyakorlat Magyar Nemzeti Bank 2

3 Table of content Motivation Credit cycle Stress tests Portfólió-tisztítási gyakorlat Magyar Nemzeti Bank 3

4 Motivation November 2012 Need for visualization Need for comparability May 2013 Create time series from stress test results Understanding the cyclical position of credit and the banking sector behaviour Procyclicality itself Taking into account the specialties of the local credit market May 2013 November 2012 Shock-absorbing capacity Magyar Nemzeti Bank 4

5 Table of content Motivation Pro-cyclicality Stress tests Portfólió-tisztítási gyakorlat Magyar Nemzeti Bank 5

6 Stress tests Liquidity stress 30 day forward looking test of liquidity position for simultaneous occurrence of severe but plausible liquidity shocks Solvency stress 2 year forward looking test of capital position for severe but plausible macroeconomic shock Magyar Nemzeti Bank 6

7 Transforming the individual liquidity needs to an index Calculate the stressed liquidity surplus as a percentage of balance sheet total, then transform: surplus under 0 percent: illiquidity (value 1) surplus above 10 percent: enough liquidity (value 0) surplus between 0 10 percent: linear interpolation Weighted aggregates Red alert : the index is above percent of the banking sector is illiquid each bank is below the regulatory minimum by 3 percentage points Magyar Nemzeti Bank 7

8 The Liquidity Stress Index Magyar Nemzeti Bank 8

9 Transformation of solvency stresses We use the structure and methodology of last stress test We estimate the parameters based on knowledge of today and not the reference time This approach implies full revision of the time series in case of major change in methodology In a normal stress test we report many variables: capital needs and buffers in billion HUF to 8% and 9%, mean and distribution of CAR We need to compress so much information as we can in one index We examine stressed CAR between 6% and 8% and transform to [0,1] for each bank We take the weighted average, by the regulatory capital requirements Red alert : 0.3 again Magyar Nemzeti Bank 9

10 The Solvency Stress Index Magyar Nemzeti Bank 10

11 Table of content Motivation Credit cycle Stress tests Magyar Nemzeti Bank 11

12 Credit cycle Financial condition index (FCI) The impact of the financial factors on GDP growth Multivariate Hodrick Prescott filter Based on Hosszú, Zs. Körmendi, Gy. Mérő, B. (2015): Univariate and multivariate filters to measure the credit gap, MNB Ocassional Papers. They regress the cyclical component and the trend component of the time series and add the sum of errors of these regressions as two additional terms to the original objective function of the HP filter. Magyar Nemzeti Bank 12

13 Explanatory variables used for the household sector Regression of the cyclical component weighted interest rate of outstanding loans ( ) BUBOR ( ) nominal house price index (+) leverage ratio of the banking sector (+) loan deposit ratio (+) Regression of the trend component log of real GDP (+) log of real GDP s trend using Kalman filter (+) 13

log of real GDP s trend using")

14 Explanatory variables used for the corporate sector Regression of the cyclical component interest rate of new loan disbursements( ) BUBOR ( ) leverage ratio of the banking sector (+) loan deposit ratio (+) Regression of the trend component log of real GDP (+) log of real GDP s trend using Kalman filter (+) 14

log of real GDP s trend using Kalman")

15 Multivariate HP filter robustness 15

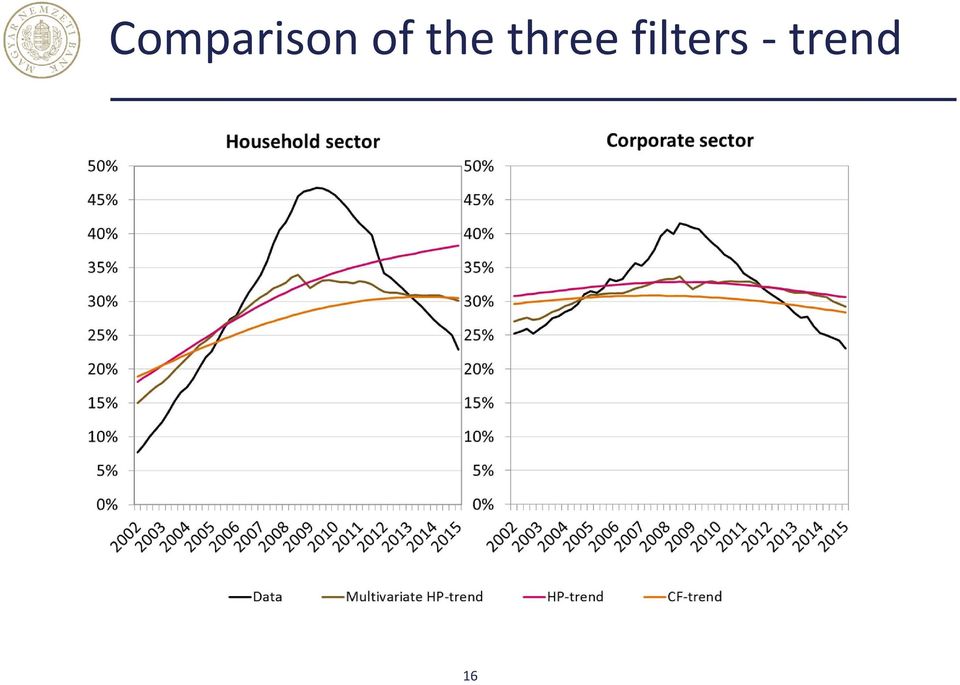

16 Comparison of the three filters trend 16

17 Comparison of the three filters Total credit to GDP 17

18 Measuring procyclicality: first generation financial conditions index (FCI) First generation FCI: based on a bayesian SVAR estimation (Tamási Világi [2011]) Weighted average of various financial time series (EUR/HUF, 3 month interest rate (BUBOR), credit, credit spreads) on the basis of their impact on GDP growth Interpretation: if the value of the FCI is 1, the banking sector accounts for one percentage point in the annual GDP growth Issues: High revisions It contains also the effect of the monetary policy (not just the banking system) Endogeneity: just little information about the credit supply Magyar Nemzeti Bank 18

Endogeneity: just little information about the credit supply Magyar Nemzeti")

19 The new second generation FCI New FCI: based on a time varying parameter FAVAR (Koop and Koroblilis [2014]) Financial factors estimated on a panel database: indicators related to banks liquidity and solvency positions as well as risk appetite Interpretation: if the value of the FCI is 1, the banking sector s lending activity accounts for one percentage point in the annual GDP growth Advantage of the new estimation: Wide set of information is used Factors concentrate on the supply side of the credit market Time varying parameters: the estimation is more robust for structural changes (for example: new macroprudential regulations) Magyar Nemzeti Bank 19

Magyar")

20 FCIs and GDP growth Magyar Nemzeti Bank 20

21 Thank you for the attention! Magyar Nemzeti Bank 21

Ádám Banai, Zsuzsanna Hosszú, Gyöngyi Körmendi and Bence Mérő: Impact of base rate cuts on bank profitability*

Ádám Banai, Zsuzsanna Hosszú, Gyöngyi Körmendi and Bence Mérő: Impact of base rate cuts on bank profitability* The adequate long-term earnings potential of the financial intermediary system is essential

Ádám Banai, Zsuzsanna Hosszú, Gyöngyi Körmendi and Bence Mérő: Impact of base rate cuts on bank profitability* The adequate long-term earnings potential of the financial intermediary system is essential

Dániel Holló: Risk developments on the retail mortgage loan market*

Dániel Holló: Risk developments on the retail mortgage loan market* In this study, using three commercial banks retail mortgage loan portfolios (consisting of approximately 200,000 clients with housing

Dániel Holló: Risk developments on the retail mortgage loan market* In this study, using three commercial banks retail mortgage loan portfolios (consisting of approximately 200,000 clients with housing

Early Warning Systems

Dániel Holló: Identifying imbalances in the Hungarian banking system ( early warning system)* The new Hungarian Central Bank Act passed at the end of 2011 delegated macroprudential regulatory powers to

Dániel Holló: Identifying imbalances in the Hungarian banking system ( early warning system)* The new Hungarian Central Bank Act passed at the end of 2011 delegated macroprudential regulatory powers to

econstor Make Your Publication Visible

econstor Make Your Publication Visible A Service of Wirtschaft Centre zbwleibniz-informationszentrum Economics Hosszú, Zsuzsanna; Körmendi, Gyöngyi; Mérő, Bence Working Paper Univariate and multivariate

econstor Make Your Publication Visible A Service of Wirtschaft Centre zbwleibniz-informationszentrum Economics Hosszú, Zsuzsanna; Körmendi, Gyöngyi; Mérő, Bence Working Paper Univariate and multivariate

Charts to the Press Release on the aggregated balance sheet of credit institutions, March 2011

29 January 21 January 211 29 January 21 January 211 Charts to the Press Release on the aggregated balance sheet of credit institutions, 211 Chart 1 Real growth of households outstanding borrowing 1 2 2

29 January 21 January 211 29 January 21 January 211 Charts to the Press Release on the aggregated balance sheet of credit institutions, 211 Chart 1 Real growth of households outstanding borrowing 1 2 2

NPL resolution in progress: the Hungarian experience Gergely Fábián

NPL resolution in progress: the Hungarian experience Gergely Fábián Vienna Initiative 2: NPL Resolution in emerging Europe: Taking Stock and Next Steps 26 June 215 29Q1 21Q1 211Q1 212Q1 213Q1 214Q1 215Q1

NPL resolution in progress: the Hungarian experience Gergely Fábián Vienna Initiative 2: NPL Resolution in emerging Europe: Taking Stock and Next Steps 26 June 215 29Q1 21Q1 211Q1 212Q1 213Q1 214Q1 215Q1

Pro-cyclicality, current trends, issues and priorities for insurance mutuals.

1 Pro-cyclicality, current trends, issues and priorities for insurance mutuals. Giles Fairhead Head 2 Agenda Pro-cyclicality of insurers PRA perspective on Current Trends and Issues Regulatory Priorities

1 Pro-cyclicality, current trends, issues and priorities for insurance mutuals. Giles Fairhead Head 2 Agenda Pro-cyclicality of insurers PRA perspective on Current Trends and Issues Regulatory Priorities

Stress-testing testing in the early warning system of financial crises: application to stability analysis of Russian banking sector

CENTER FOR MACROECONOMIC ANALYSIS AND SHORT-TERM TERM FORESACTING Tel.: (499)129-17-22, fax: (499)129-09-22, e-mail: mail@forecast.ru, http://www.forecast.ru Stress-testing testing in the early warning

CENTER FOR MACROECONOMIC ANALYSIS AND SHORT-TERM TERM FORESACTING Tel.: (499)129-17-22, fax: (499)129-09-22, e-mail: mail@forecast.ru, http://www.forecast.ru Stress-testing testing in the early warning

Trends in lending. August 2015

Trends in lending August 15 Trends in lending August 15 Trends in lending (August 15) Analysis prepared by Máté Bálint, Zita Fellner, Zsolt Oláh (Directorate Financial System Analysis) This publication

Trends in lending August 15 Trends in lending August 15 Trends in lending (August 15) Analysis prepared by Máté Bálint, Zita Fellner, Zsolt Oláh (Directorate Financial System Analysis) This publication

In the case of CIRS transactions, the MNB does not apply any FX-rate reset. Detailed terms and conditions

NOTICE ON THE TERMS AND CONDITIONS OF CROSS-CURRENCY INTEREST RATE SWAP TENDERS COMBINED WITH SPOT TRANSACTIONS RELATED TO THE MEASURES NECESSARY IN ORDER TO TERMINATE THE SHIFTING OF RISKS ARISING FROM

NOTICE ON THE TERMS AND CONDITIONS OF CROSS-CURRENCY INTEREST RATE SWAP TENDERS COMBINED WITH SPOT TRANSACTIONS RELATED TO THE MEASURES NECESSARY IN ORDER TO TERMINATE THE SHIFTING OF RISKS ARISING FROM

FINANCIAL STABILITY ISSUES FOR SMALL STATES. Mirko Mallia Assistant Executive Financial Stability Surveillance, Assessment and Data

FINANCIAL STABILITY ISSUES FOR SMALL STATES Mirko Mallia Assistant Executive Financial Stability Surveillance, Assessment and Data Disclaimer: Any views expressed are only the author s s own and do not

FINANCIAL STABILITY ISSUES FOR SMALL STATES Mirko Mallia Assistant Executive Financial Stability Surveillance, Assessment and Data Disclaimer: Any views expressed are only the author s s own and do not

Guidance Note: Stress Testing Class 2 Credit Unions. November, 2013. Ce document est également disponible en français

Guidance Note: Stress Testing Class 2 Credit Unions November, 2013 Ce document est également disponible en français This Guidance Note is for use by all Class 2 credit unions with assets in excess of $1

Guidance Note: Stress Testing Class 2 Credit Unions November, 2013 Ce document est également disponible en français This Guidance Note is for use by all Class 2 credit unions with assets in excess of $1

Financial Stability Report 2015/2016

Financial Stability Report 2015/2016 Press Conference Presentation Miroslav Singer Governor Prague, 14 June 2016 Structure of presentation I. Overall assessment of risks and setting of countercyclical

Financial Stability Report 2015/2016 Press Conference Presentation Miroslav Singer Governor Prague, 14 June 2016 Structure of presentation I. Overall assessment of risks and setting of countercyclical

Monetary Policy in the Post Crisis Period: The Turkish Perspective

Monetary Policy in the Post Crisis Period: The Turkish Perspective Hakan Kara Economic Research Forum Conference İstanbul April 19, 2013 Outline 1. Motivation of the New Policy Framework 2. New Instruments

Monetary Policy in the Post Crisis Period: The Turkish Perspective Hakan Kara Economic Research Forum Conference İstanbul April 19, 2013 Outline 1. Motivation of the New Policy Framework 2. New Instruments

Comments of Magyar Nemzeti Bank, the central bank of Hungary on Countercyclical Capital Buffer Proposal (BIS Consultative Document)

") Comments of Magyar Nemzeti Bank, the central bank of Hungary on Countercyclical Capital Buffer Proposal (BIS Consultative Document) Calibration The implementation of the proposed countercyclical capital

Comments of Magyar Nemzeti Bank, the central bank of Hungary on Countercyclical Capital Buffer Proposal (BIS Consultative Document) Calibration The implementation of the proposed countercyclical capital

THE EARLY WARNING SYSTEM PRESENTATION DEFINITION

THE EARLY WARNING SYSTEM PRESENTED BY: PETER GATERE MANGER, BANK SUPERVISION CENTRAL BANK OF KENYA 1 PRESENTATION Definition Background Objectives of an early warning system Role of qualitative information

THE EARLY WARNING SYSTEM PRESENTED BY: PETER GATERE MANGER, BANK SUPERVISION CENTRAL BANK OF KENYA 1 PRESENTATION Definition Background Objectives of an early warning system Role of qualitative information

uncertainty. Credit flows are especially pro cyclical

Dilemma not Trilemma: The Global Financial Cycle and Monetary Policy Independence Hélène Rey London Business School, CEPR and NBER Jackson Hole Symposium 2013 Global financial cycle: capital flows Strong

Dilemma not Trilemma: The Global Financial Cycle and Monetary Policy Independence Hélène Rey London Business School, CEPR and NBER Jackson Hole Symposium 2013 Global financial cycle: capital flows Strong

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Study Questions 5 (Money) MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The functions of money are 1) A) medium of exchange, unit of account,

Study Questions 5 (Money) MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The functions of money are 1) A) medium of exchange, unit of account,

PROJECTION OF THE FISCAL BALANCE AND PUBLIC DEBT (2012 2027) - SUMMARY

- SUMMARY") PROJECTION OF THE FISCAL BALANCE AND PUBLIC DEBT (2012 2027) - SUMMARY PUBLIC FINANCE REVIEW February 2013 SUMMARY Key messages The purpose of our analysis is to highlight the risks that fiscal policy

PROJECTION OF THE FISCAL BALANCE AND PUBLIC DEBT (2012 2027) - SUMMARY PUBLIC FINANCE REVIEW February 2013 SUMMARY Key messages The purpose of our analysis is to highlight the risks that fiscal policy

(Part.1) FOUNDATIONS OF RISK MANAGEMENT

FOUNDATIONS OF RISK MANAGEMENT") (Part.1) FOUNDATIONS OF RISK MANAGEMENT 1 : Risk Taking: A Corporate Governance Perspective Delineating Efficient Portfolios 2: The Standard Capital Asset Pricing Model 1 : Risk : A Helicopter View 2:

(Part.1) FOUNDATIONS OF RISK MANAGEMENT 1 : Risk Taking: A Corporate Governance Perspective Delineating Efficient Portfolios 2: The Standard Capital Asset Pricing Model 1 : Risk : A Helicopter View 2:

Charts to the Press Release on the aggregated balance sheet of credit institutions, April 2013

Charts to the Press Release on the aggregated balance sheet of credit institutions, 213 Chart 1 Real growth of households outstanding borrowing 1, 2 1 1 - - -1-1 -1-1 -2-2 -2-2 -3-3 -3-3 211 January 212

Charts to the Press Release on the aggregated balance sheet of credit institutions, 213 Chart 1 Real growth of households outstanding borrowing 1, 2 1 1 - - -1-1 -1-1 -2-2 -2-2 -3-3 -3-3 211 January 212

International competition will change mortgage lending

Pentti Hakkarainen Deputy Governor, Bank of Finland International competition will change mortgage lending Nordic Mortgage Council Helsinki, 28 August 2015 28.8.2015 Unrestricted 1 Financial stability

Pentti Hakkarainen Deputy Governor, Bank of Finland International competition will change mortgage lending Nordic Mortgage Council Helsinki, 28 August 2015 28.8.2015 Unrestricted 1 Financial stability

Corporate Defaults and Large Macroeconomic Shocks

Corporate Defaults and Large Macroeconomic Shocks Mathias Drehmann Bank of England Andrew Patton London School of Economics and Bank of England Steffen Sorensen Bank of England The presentation expresses

Corporate Defaults and Large Macroeconomic Shocks Mathias Drehmann Bank of England Andrew Patton London School of Economics and Bank of England Steffen Sorensen Bank of England The presentation expresses

Network Analysis Workshop for Heads of Financial Stability CCBS, Bank of England, London February 22-23, 2016

Network Analysis Workshop for Heads of Financial Stability CCBS, Bank of England, London February 22-23, 2016 Dr. S. Rajagopal Chief General Manager Financial Stability Unit Reserve Bank of India Outline

Network Analysis Workshop for Heads of Financial Stability CCBS, Bank of England, London February 22-23, 2016 Dr. S. Rajagopal Chief General Manager Financial Stability Unit Reserve Bank of India Outline

18 ECB STYLISED FACTS OF MONEY AND CREDIT OVER THE BUSINESS CYCLE

Box 1 STYLISED FACTS OF MONEY AND CREDIT OVER THE BUSINESS CYCLE Over the past three decades, the growth rates of MFI loans to the private sector and the narrow monetary aggregate M1 have displayed relatively

Box 1 STYLISED FACTS OF MONEY AND CREDIT OVER THE BUSINESS CYCLE Over the past three decades, the growth rates of MFI loans to the private sector and the narrow monetary aggregate M1 have displayed relatively

Chart 9.1 Non-performing loans ratio and structure of non-performing loans (right) 25% 80 06/08 03/11 03/09 12/07 12/08 06/09 09/09 12/09 09/08 06/11

25% 80 06/08 03/11 03/09 12/07 12/08 06/09 09/09 12/09 09/08 06/11") Financial Stability Report 21 H1 9. MONITORING BANKING SECTOR RISKS 9.1 CREDIT RISK (88) Loan portfolio quality improved and banks were more active in writingoff the loss loans from their balance sheets.

Financial Stability Report 21 H1 9. MONITORING BANKING SECTOR RISKS 9.1 CREDIT RISK (88) Loan portfolio quality improved and banks were more active in writingoff the loss loans from their balance sheets.

Kiwi drivers the New Zealand dollar experience AN 2012/ 02

Kiwi drivers the New Zealand dollar experience AN 2012/ 02 Chris McDonald May 2012 Reserve Bank of New Zealand Analytical Note series ISSN 2230-5505 Reserve Bank of New Zealand PO Box 2498 Wellington NEW

Kiwi drivers the New Zealand dollar experience AN 2012/ 02 Chris McDonald May 2012 Reserve Bank of New Zealand Analytical Note series ISSN 2230-5505 Reserve Bank of New Zealand PO Box 2498 Wellington NEW

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Survey of Macroeconomics, MBA 641 Fall 2006, Quiz 4 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The central bank for the United States

Survey of Macroeconomics, MBA 641 Fall 2006, Quiz 4 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The central bank for the United States

The Impact of Surplus Liquidity

The Impact of Surplus Liquidity Garreth Rule CCBS PFTAC Course on Monetary Transmission Channels, Liquidity Conditions, and Determinants of Inflation Central Bank of Solomon Islands 18 23 July 2012 The

The Impact of Surplus Liquidity Garreth Rule CCBS PFTAC Course on Monetary Transmission Channels, Liquidity Conditions, and Determinants of Inflation Central Bank of Solomon Islands 18 23 July 2012 The

How To Convert Foreign Exchange Loans Into Forint

EN ECB-PUBLIC OPINION OF THE EUROPEAN CENTRAL BANK of 16 December 2014 on the conversion of foreign exchange loans (CON/2014/87) Introduction and legal basis On 17 November 2014, the European Central Bank

EN ECB-PUBLIC OPINION OF THE EUROPEAN CENTRAL BANK of 16 December 2014 on the conversion of foreign exchange loans (CON/2014/87) Introduction and legal basis On 17 November 2014, the European Central Bank

THE IMPACT OF MACROECONOMIC FACTORS ON NON-PERFORMING LOANS IN THE REPUBLIC OF MOLDOVA

Abstract THE IMPACT OF MACROECONOMIC FACTORS ON NON-PERFORMING LOANS IN THE REPUBLIC OF MOLDOVA Dorina CLICHICI 44 Tatiana COLESNICOVA 45 The purpose of this research is to estimate the impact of several

Abstract THE IMPACT OF MACROECONOMIC FACTORS ON NON-PERFORMING LOANS IN THE REPUBLIC OF MOLDOVA Dorina CLICHICI 44 Tatiana COLESNICOVA 45 The purpose of this research is to estimate the impact of several

Stress testing at the Magyar Nemzeti Bank

Ádám Banai, Zsuzsanna Hosszú, Gyöngyi Körmendi, Sándor Sóvágó, Róbert Szegedi Stress testing at the Magyar Nemzeti Bank MNB Occasional Papers 109 2014 Ádám Banai, Zsuzsanna Hosszú, Gyöngyi Körmendi, Sándor

Ádám Banai, Zsuzsanna Hosszú, Gyöngyi Körmendi, Sándor Sóvágó, Róbert Szegedi Stress testing at the Magyar Nemzeti Bank MNB Occasional Papers 109 2014 Ádám Banai, Zsuzsanna Hosszú, Gyöngyi Körmendi, Sándor

State Farm Bank, F.S.B.

State Farm Bank, F.S.B. 2015 Annual Stress Test Disclosure Dodd-Frank Act Company Run Stress Test Results Supervisory Severely Adverse Scenario June 25, 2015 1 Regulatory Requirement The 2015 Annual Stress

State Farm Bank, F.S.B. 2015 Annual Stress Test Disclosure Dodd-Frank Act Company Run Stress Test Results Supervisory Severely Adverse Scenario June 25, 2015 1 Regulatory Requirement The 2015 Annual Stress

Chart I.1. Difference between Primary Surplus (PS) and Bond Yield Spreads in Selected EU 1 Countries

and Bond Yield Spreads in Selected EU 1 Countries") LIST OF CHARTS Chart I.1. Difference between Primary Surplus (PS) and Bond Yield Spreads in Selected EU 1 Countries Chart I.2. Gross Debt Stock and Budget Deficits of Selected Countries as of 2010 1 Chart

LIST OF CHARTS Chart I.1. Difference between Primary Surplus (PS) and Bond Yield Spreads in Selected EU 1 Countries Chart I.2. Gross Debt Stock and Budget Deficits of Selected Countries as of 2010 1 Chart

52 ARTICLE The relationship between the repo rate and interest rates for households and companies

ARTICLE The relationship between the repo rate and interest rates for households and companies Figure A. Rates for new mortgage agreements for households and the repo rate 8 9 Average mortgage rate Short

ARTICLE The relationship between the repo rate and interest rates for households and companies Figure A. Rates for new mortgage agreements for households and the repo rate 8 9 Average mortgage rate Short

René Garcia Professor of finance

Liquidity Risk: What is it? How to Measure it? René Garcia Professor of finance EDHEC Business School, CIRANO Cirano, Montreal, January 7, 2009 The financial and economic environment We are living through

Liquidity Risk: What is it? How to Measure it? René Garcia Professor of finance EDHEC Business School, CIRANO Cirano, Montreal, January 7, 2009 The financial and economic environment We are living through

Financial stability, systemic risk & macroprudential supervision: an actuarial perspective

Financial stability, systemic risk & macroprudential supervision: an actuarial perspective Paul Thornton International Actuarial Association Presentation to OECD Insurance and Pensions Committee June 2010

Financial stability, systemic risk & macroprudential supervision: an actuarial perspective Paul Thornton International Actuarial Association Presentation to OECD Insurance and Pensions Committee June 2010

MACROECONOMIC IMPLICATIONS OF FINANCIAL FRICTIONS IN THE EURO ZONE: LESSONS FROM CANADA

MACROECONOMIC IMPLICATIONS OF FINANCIAL FRICTIONS IN THE EURO ZONE: LESSONS FROM CANADA Pierre L. Siklos WLU and Viessmann European Research Centre JUNE 2014 Prepared for the 20 th Dubrovnik Economic Conference,

MACROECONOMIC IMPLICATIONS OF FINANCIAL FRICTIONS IN THE EURO ZONE: LESSONS FROM CANADA Pierre L. Siklos WLU and Viessmann European Research Centre JUNE 2014 Prepared for the 20 th Dubrovnik Economic Conference,

Monetary policy in Russia: Recent challenges and changes

Monetary policy in Russia: Recent challenges and changes Central Bank of the Russian Federation (Bank of Russia) Abstract Increasing trade and financial flows between the world s countries has been a double-edged

Monetary policy in Russia: Recent challenges and changes Central Bank of the Russian Federation (Bank of Russia) Abstract Increasing trade and financial flows between the world s countries has been a double-edged

NPL resolution: a macro view

NPL resolution: a macro view Gergely Fábián MNB-EBRD workshop on debt Restructuring and NPL Resolution in Hungary 3 March 215 29Q1 21Q1 211Q1 212Q1 213Q1 214Q1 High corporate NPL has been a problem for

NPL resolution: a macro view Gergely Fábián MNB-EBRD workshop on debt Restructuring and NPL Resolution in Hungary 3 March 215 29Q1 21Q1 211Q1 212Q1 213Q1 214Q1 High corporate NPL has been a problem for

LENDING SURVEY Senior loan officer opinion survey on bank lending practices. Aggregated results of the first three surveys

LENDING SURVEY Senior loan officer opinion survey on bank lending practices Aggregated results of the first three surveys by András Bethlendi Financial Stability Department Magyar Nemzeti Bank To gain

LENDING SURVEY Senior loan officer opinion survey on bank lending practices Aggregated results of the first three surveys by András Bethlendi Financial Stability Department Magyar Nemzeti Bank To gain

Directors Review. Domestic Economy

Directors Review On behalf of the Board of Directors, I am pleased to present the condensed interim unconsolidated financial statements for the half year ended June 30, 2015. Domestic Economy Pakistan

Directors Review On behalf of the Board of Directors, I am pleased to present the condensed interim unconsolidated financial statements for the half year ended June 30, 2015. Domestic Economy Pakistan

Economic Commentaries

n Economic Commentaries In its Financial Stability Report 214:1, the Riksbank recommended that a requirement for the Liquidity Coverage Ratio (LCR) in Swedish kronor be introduced. The background to this

n Economic Commentaries In its Financial Stability Report 214:1, the Riksbank recommended that a requirement for the Liquidity Coverage Ratio (LCR) in Swedish kronor be introduced. The background to this

Household debt and spending in the United Kingdom

Household debt and spending in the United Kingdom Phil Bunn and May Rostom Bank of England Norges Bank Workshop: 24 March 2015 1 Outline Motivation Literature/theory Data/methodology Econometric results

Household debt and spending in the United Kingdom Phil Bunn and May Rostom Bank of England Norges Bank Workshop: 24 March 2015 1 Outline Motivation Literature/theory Data/methodology Econometric results

KLP BOLIGKREDITT AS Interim report Q4 2014

KLP BOLIGKREDITT AS Interim report Q4 2014 INCOME STATEMENT BALANCE SHEET NOTES Contents Interim Financial Statements 4/2014 3 Income Statement 4 Balance Sheet 5 Statement of owners' equity 6 Statement

KLP BOLIGKREDITT AS Interim report Q4 2014 INCOME STATEMENT BALANCE SHEET NOTES Contents Interim Financial Statements 4/2014 3 Income Statement 4 Balance Sheet 5 Statement of owners' equity 6 Statement

Net Stable Funding Ratio

Net Stable Funding Ratio Aims to establish a minimum acceptable amount of stable funding based on the liquidity characteristics of an institution s assets and activities over a one year horizon. The amount

Net Stable Funding Ratio Aims to establish a minimum acceptable amount of stable funding based on the liquidity characteristics of an institution s assets and activities over a one year horizon. The amount

DNB The Norwegian bank

DNB The Norwegian bank New York, Deutsche Bank 22 May 2012 CFO Bjørn Erik Næss Agenda DNB - Q1 results DNB drivers for successful banking 2 Agenda Q1 results DNB drivers for successful banking 3 Profit

DNB The Norwegian bank New York, Deutsche Bank 22 May 2012 CFO Bjørn Erik Næss Agenda DNB - Q1 results DNB drivers for successful banking 2 Agenda Q1 results DNB drivers for successful banking 3 Profit

CHILE FINANCIAL SECTOR ASSESSMENT PROGRAM

FINANCIAL SECTOR ASSESSMENT PROGRAM CHILE TECHNICAL NOTE: THE BANKING SECTOR RISK EXPOSURES AND INDUSTRY PRACTICES CONDUCIVE TO EFFECTIVE RISK BASED SUPERVISION NOVEMBER 2004 INTERNATIONAL MONETARY FUND

FINANCIAL SECTOR ASSESSMENT PROGRAM CHILE TECHNICAL NOTE: THE BANKING SECTOR RISK EXPOSURES AND INDUSTRY PRACTICES CONDUCIVE TO EFFECTIVE RISK BASED SUPERVISION NOVEMBER 2004 INTERNATIONAL MONETARY FUND

HAS FINANCE BECOME TOO EXPENSIVE? AN ESTIMATION OF THE UNIT COST OF FINANCIAL INTERMEDIATION IN EUROPE 1951-2007

HAS FINANCE BECOME TOO EXPENSIVE? AN ESTIMATION OF THE UNIT COST OF FINANCIAL INTERMEDIATION IN EUROPE 1951-2007 IPP Policy Briefs n 10 June 2014 Guillaume Bazot www.ipp.eu Summary Finance played an increasing

HAS FINANCE BECOME TOO EXPENSIVE? AN ESTIMATION OF THE UNIT COST OF FINANCIAL INTERMEDIATION IN EUROPE 1951-2007 IPP Policy Briefs n 10 June 2014 Guillaume Bazot www.ipp.eu Summary Finance played an increasing

FINANCIAL DOMINANCE MARKUS K. BRUNNERMEIER & YULIY SANNIKOV

Based on: The I Theory of Money - Redistributive Monetary Policy CFS Symposium: Banking, Liquidity, and Monetary Policy 26 September 2013, Frankfurt am Main 2013 FINANCIAL DOMINANCE MARKUS K. BRUNNERMEIER

Based on: The I Theory of Money - Redistributive Monetary Policy CFS Symposium: Banking, Liquidity, and Monetary Policy 26 September 2013, Frankfurt am Main 2013 FINANCIAL DOMINANCE MARKUS K. BRUNNERMEIER

NOTICE ON THE TERMS AND CONDITIONS OF SPOT SWISS FRANC SALE TENDERS RELATED TO FORINT CONVERSION OF FOREIGN CURRENCY NON-MORTGAGE CONSUMER LOANS

Unofficial translation only! The official version is the Hungarian one! NOTICE ON THE TERMS AND CONDITIONS OF SPOT SWISS FRANC SALE TENDERS RELATED TO FORINT CONVERSION OF FOREIGN CURRENCY NON-MORTGAGE

Unofficial translation only! The official version is the Hungarian one! NOTICE ON THE TERMS AND CONDITIONS OF SPOT SWISS FRANC SALE TENDERS RELATED TO FORINT CONVERSION OF FOREIGN CURRENCY NON-MORTGAGE

EIOPA Risk Dashboard. March 2013 EIOPAFS13022

EIOPA Risk Dashboard March 2013 EIOPAFS13022 Systemic risks and vulnerabilities On the basis of observed market conditions, data gathered from undertakings, and expert judgment, EIOPA assesses the main

EIOPA Risk Dashboard March 2013 EIOPAFS13022 Systemic risks and vulnerabilities On the basis of observed market conditions, data gathered from undertakings, and expert judgment, EIOPA assesses the main

HOW DID THE FINANCIAL CRISIS AFFECT SMALL-BUSINESS LENDING IN THE U.S.?

HOW DID THE FINANCIAL CRISIS AFFECT SMALL-BUSINESS LENDING IN THE U.S.? Rebel A. Cole Driehaus College of Business DePaul University Email: rcole@depaul.edu Presentation for the 2013 AIDEA Bicentenniel

HOW DID THE FINANCIAL CRISIS AFFECT SMALL-BUSINESS LENDING IN THE U.S.? Rebel A. Cole Driehaus College of Business DePaul University Email: rcole@depaul.edu Presentation for the 2013 AIDEA Bicentenniel

Forecasting Retail Credit Market Conditions

Forecasting Retail Credit Market Conditions Eric McVittie Experian Experian and the marks used herein are service marks or registered trademarks of Experian Limited. Other products and company names mentioned

Forecasting Retail Credit Market Conditions Eric McVittie Experian Experian and the marks used herein are service marks or registered trademarks of Experian Limited. Other products and company names mentioned

The package of measures to avoid artificial volatility and pro-cyclicality

The package of measures to avoid artificial volatility and pro-cyclicality Explanation of the measures and the need to include them in the Solvency II framework Contents 1. Key messages 2. Why the package

The package of measures to avoid artificial volatility and pro-cyclicality Explanation of the measures and the need to include them in the Solvency II framework Contents 1. Key messages 2. Why the package

IW Monetary Outlook December 2015

IW policy paper 37/2015 Contributions to the political debate by the Cologne Institute for Economic Research IW Monetary Outlook December 2015 Weak Credit Growth Hinders Eurozone Inflation to Increase

IW policy paper 37/2015 Contributions to the political debate by the Cologne Institute for Economic Research IW Monetary Outlook December 2015 Weak Credit Growth Hinders Eurozone Inflation to Increase

Basel 3: A new perspective on portfolio risk management. Tamar JOULIA-PARIS October 2011

Basel 3: A new perspective on portfolio risk management Tamar JOULIA-PARIS October 2011 1 Content 1. Basel 3 A complex regulatory framework With possible unintended consequences 2. Consequences on Main

Basel 3: A new perspective on portfolio risk management Tamar JOULIA-PARIS October 2011 1 Content 1. Basel 3 A complex regulatory framework With possible unintended consequences 2. Consequences on Main

List of legislative acts

List of legislative acts BRRd : d irective 2014/59/EU of the European Parliament and of the Council of 15 May 2014 establishing a framework for the recovery and resolution of credit institutions and investment

List of legislative acts BRRd : d irective 2014/59/EU of the European Parliament and of the Council of 15 May 2014 establishing a framework for the recovery and resolution of credit institutions and investment

How Risky are Residential Mortgages in Switzerland?

How Risky are Residential Mortgages in Switzerland? Martin Brown* & Benjamin Guin* 6 December 2013 * Swiss Institute of Banking and Finance, University of St. Gallen, Rosenbergstrasse 52, CH-9000 St. Gallen.

How Risky are Residential Mortgages in Switzerland? Martin Brown* & Benjamin Guin* 6 December 2013 * Swiss Institute of Banking and Finance, University of St. Gallen, Rosenbergstrasse 52, CH-9000 St. Gallen.

CONSULTATION PAPER P016-2006 October 2006. Proposed Regulatory Framework on Mortgage Insurance Business

CONSULTATION PAPER P016-2006 October 2006 Proposed Regulatory Framework on Mortgage Insurance Business PREFACE 1 Mortgage insurance protects residential mortgage lenders against losses on mortgage loans

CONSULTATION PAPER P016-2006 October 2006 Proposed Regulatory Framework on Mortgage Insurance Business PREFACE 1 Mortgage insurance protects residential mortgage lenders against losses on mortgage loans

Government Spending Multipliers in Developing Countries: Evidence from Lending by Official Creditors

Government Spending Multipliers in Developing Countries: Evidence from Lending by Official Creditors Aart Kraay The World Bank International Growth Center Workshop on Fiscal and Monetary Policy in Low-Income

Government Spending Multipliers in Developing Countries: Evidence from Lending by Official Creditors Aart Kraay The World Bank International Growth Center Workshop on Fiscal and Monetary Policy in Low-Income

Macroeconomics, Fall 2007 Exam 3, TTh classes, various versions

Name: _ Days/Times Class Meets: Today s Date: Macroeconomics, Fall 2007 Exam 3, TTh classes, various versions Read these Instructions carefully! You must follow them exactly! I) On your Scantron card you

Name: _ Days/Times Class Meets: Today s Date: Macroeconomics, Fall 2007 Exam 3, TTh classes, various versions Read these Instructions carefully! You must follow them exactly! I) On your Scantron card you

Internet Appendix to Stock Market Liquidity and the Business Cycle

Internet Appendix to Stock Market Liquidity and the Business Cycle Randi Næs, Johannes A. Skjeltorp and Bernt Arne Ødegaard This Internet appendix contains additional material to the paper Stock Market

Internet Appendix to Stock Market Liquidity and the Business Cycle Randi Næs, Johannes A. Skjeltorp and Bernt Arne Ødegaard This Internet appendix contains additional material to the paper Stock Market

STRESS TESTING GUIDELINE

STRESS TESTING GUIDELINE JUIN 2012 Table of Contents Preamble... 2 Introduction... 3 Scope... 5 Coming into effect and updating... 6 1. Stress testing... 7 A. Concept... 7 B. Approaches underlying stress

STRESS TESTING GUIDELINE JUIN 2012 Table of Contents Preamble... 2 Introduction... 3 Scope... 5 Coming into effect and updating... 6 1. Stress testing... 7 A. Concept... 7 B. Approaches underlying stress

A- RULES AFFECTING THE ABILITY OF THE ECONOMY TO FINANCE ITSELF AND GROW

High-level overview of Bank of England Response to the European Commission Call for Evidence on the EU Regulatory Framework for Financial Services, January 2016 Structure A- Rules affecting the ability

High-level overview of Bank of England Response to the European Commission Call for Evidence on the EU Regulatory Framework for Financial Services, January 2016 Structure A- Rules affecting the ability

Understanding the macroeconomic effects of working capital in the United Kingdom

Understanding the macroeconomic effects of working capital in the United Kingdom Emilio Fernandez-Corugedo 1, Michael McMahon 2, Stephen Millard 3, and Lukasz Rachel 1 1 Bank of England 2 University of

Understanding the macroeconomic effects of working capital in the United Kingdom Emilio Fernandez-Corugedo 1, Michael McMahon 2, Stephen Millard 3, and Lukasz Rachel 1 1 Bank of England 2 University of

Deposit Insurance Pricing. Luc Laeven World Bank Global Dialogue 2002

Deposit Insurance Pricing Luc Laeven World Bank Global Dialogue 2002 1 Introduction Explicit deposit insurance should not be adopted in countries with a weak institutional environment Political economy

Deposit Insurance Pricing Luc Laeven World Bank Global Dialogue 2002 1 Introduction Explicit deposit insurance should not be adopted in countries with a weak institutional environment Political economy

Correlation between Growth Rate and Non Performing Retail Loans in the Republic of Macedonia

Vol. 3, No.3, July 2013, pp. 133 138 ISSN: 2225-8329 2013 HRMARS www.hrmars.com Correlation between Growth Rate and Non Performing Retail Loans in the Republic of Macedonia Sedat MAHMUDI Faculty of Business

Vol. 3, No.3, July 2013, pp. 133 138 ISSN: 2225-8329 2013 HRMARS www.hrmars.com Correlation between Growth Rate and Non Performing Retail Loans in the Republic of Macedonia Sedat MAHMUDI Faculty of Business

Financial and Economic Review Vol. 14 No. 1, March 2015, pp. 236 240.

Financial and Economic Review Vol. 14 No. 1, March 2015, pp. 236 240. What lies ahead for insurance companies?* Review of the V. International Insurance Conference of the Association of Hungarian Insurance

Financial and Economic Review Vol. 14 No. 1, March 2015, pp. 236 240. What lies ahead for insurance companies?* Review of the V. International Insurance Conference of the Association of Hungarian Insurance

A macroeconomic credit risk model for stress testing the Romanian corporate credit portfolio

Academy of Economic Studies Bucharest Doctoral School of Finance and Banking A macroeconomic credit risk model for stress testing the Romanian corporate credit portfolio Supervisor Professor PhD. Moisă

Academy of Economic Studies Bucharest Doctoral School of Finance and Banking A macroeconomic credit risk model for stress testing the Romanian corporate credit portfolio Supervisor Professor PhD. Moisă

PRACTICE- Unit 6 AP Economics

PRACTICE- Unit 6 AP Economics Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The term liquid asset means: A. that the asset is used in a barter exchange.

PRACTICE- Unit 6 AP Economics Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The term liquid asset means: A. that the asset is used in a barter exchange.

OneWest Bank N. A. Dodd-Frank Act Stress Test Disclosure

OneWest Bank N. A. Dodd-Frank Act Stress Test Disclosure Capital Stress Testing Results Covering the Time Period October 1, through December 31, for OneWest Bank N.A. under a Hypothetical Severely Adverse

OneWest Bank N. A. Dodd-Frank Act Stress Test Disclosure Capital Stress Testing Results Covering the Time Period October 1, through December 31, for OneWest Bank N.A. under a Hypothetical Severely Adverse

GHANA S IMF PROGRAM - THE RISK OF FISCAL CONSOLIDATION WITHOUT STRONG FISCAL POLICY RULES. Commentary

GHANA S IMF PROGRAM - THE RISK OF FISCAL CONSOLIDATION WITHOUT STRONG FISCAL POLICY RULES Introduction Commentary Mohammed Amin Adam, PhD Africa Centre for Energy Policy Following macroeconomic challenges

GHANA S IMF PROGRAM - THE RISK OF FISCAL CONSOLIDATION WITHOUT STRONG FISCAL POLICY RULES Introduction Commentary Mohammed Amin Adam, PhD Africa Centre for Energy Policy Following macroeconomic challenges

ESRB Recommendation for Retail Loans Secured by Residential Property

OFFICIAL INFORMATION OF THE CZECH NATIONAL BANK of 16 June 2015 Recommendation on the management of risks associated with the provision of retail loans secured by residential property I. Purpose of the

OFFICIAL INFORMATION OF THE CZECH NATIONAL BANK of 16 June 2015 Recommendation on the management of risks associated with the provision of retail loans secured by residential property I. Purpose of the

Endogenous Money and Monetary Policy

Endogenous Money and Monetary Policy Koppány Krisztián, assistant lecturer, Széchenyi István University, Győr HU ISSN 1418-7108: HEJ Manuscript no.: ECO-040630-A Abstract Orthodox macroeconomic models

Endogenous Money and Monetary Policy Koppány Krisztián, assistant lecturer, Széchenyi István University, Győr HU ISSN 1418-7108: HEJ Manuscript no.: ECO-040630-A Abstract Orthodox macroeconomic models

28.10.2013. The recovery of the Spanish economy XVI Congreso Nacional de la Empresa Familiar/Instituto de la Empresa Familiar Luis M.

28.10.2013 The recovery of the Spanish economy XVI Congreso Nacional de la Empresa Familiar/Instituto de la Empresa Familiar Luis M. Linde Governor Let me begin by thanking you for inviting me to take

28.10.2013 The recovery of the Spanish economy XVI Congreso Nacional de la Empresa Familiar/Instituto de la Empresa Familiar Luis M. Linde Governor Let me begin by thanking you for inviting me to take

Financial Stability Oversight Council. Staff Guidance. Methodologies Relating to Stage 1 Thresholds. June 8, 2015

Financial Stability Oversight Council Staff Guidance Methodologies Relating to Stage 1 Thresholds June 8, 2015 Stage 1 Overview Section 113 of the Dodd-Frank Wall Street Reform and Consumer Protection

Financial Stability Oversight Council Staff Guidance Methodologies Relating to Stage 1 Thresholds June 8, 2015 Stage 1 Overview Section 113 of the Dodd-Frank Wall Street Reform and Consumer Protection

Discussion of Current Account Imabalances in the Southern Euro Area: Causes, Consequences, and Remedies. Massimiliano Pisani (Bank of Italy)

") Discussion of Current Account Imabalances in the Southern Euro Area: Causes, Consequences, and Remedies Massimiliano Pisani (Bank of Italy) Italy s External Competitiveness Ministry of Economy and Finance,

Discussion of Current Account Imabalances in the Southern Euro Area: Causes, Consequences, and Remedies Massimiliano Pisani (Bank of Italy) Italy s External Competitiveness Ministry of Economy and Finance,

Valuation of debt instruments

Valuation of debt instruments Csaba Ilyés 1 and László Lakatos 2 Last decade in Hungary the securities market developed very rapidly. During this period the amount of securities increased by more than

Valuation of debt instruments Csaba Ilyés 1 and László Lakatos 2 Last decade in Hungary the securities market developed very rapidly. During this period the amount of securities increased by more than

Financial vulnerability of mortgage-indebted households in New Zealand evidence from the Household Economic Survey

ARTICLES Financial vulnerability of mortgage-indebted in New Zealand evidence from the Household Economic Survey Mizuho Kida Aggregate household debt more than doubled between 1 and 8, alongside similarly

ARTICLES Financial vulnerability of mortgage-indebted in New Zealand evidence from the Household Economic Survey Mizuho Kida Aggregate household debt more than doubled between 1 and 8, alongside similarly

BIS database for debt service ratios for the private nonfinancial

BIS database for debt service ratios for the private nonfinancial sector Data documentation The debt service ratio (DSR) is defined as the ratio of interest payments plus amortisations to income. As such,

BIS database for debt service ratios for the private nonfinancial sector Data documentation The debt service ratio (DSR) is defined as the ratio of interest payments plus amortisations to income. As such,

Assessing the Supplementary Leverage Ratio. September 20, 2013

Assessing the Supplementary Leverage Ratio September 20, 2013 Executive summary We have supplementary leverage and capital data as of 2Q 2013 covering 100% of US G-SIB assets, and ~93% of total US domiciled

Assessing the Supplementary Leverage Ratio September 20, 2013 Executive summary We have supplementary leverage and capital data as of 2Q 2013 covering 100% of US G-SIB assets, and ~93% of total US domiciled

Basel III and project finance

July 2011 Basel III and project finance In this article, published by Project Finance International (Issue 460), Edward Chan and Matthew Worth go through what Basel III means and the impact on projects

July 2011 Basel III and project finance In this article, published by Project Finance International (Issue 460), Edward Chan and Matthew Worth go through what Basel III means and the impact on projects

Application of micro-data for systemic risk assessment and policy formulation

Application of micro-data for systemic risk assessment and policy formulation Karen Lee Fong Ling 1 1. Introduction In general, macro trends are useful as it indicates collective behaviours and can be

Application of micro-data for systemic risk assessment and policy formulation Karen Lee Fong Ling 1 1. Introduction In general, macro trends are useful as it indicates collective behaviours and can be

Household debt and consumption in the UK. Evidence from UK microdata. 10 March 2015

Household debt and consumption in the UK Evidence from UK microdata 10 March 2015 Disclaimer This presentation does not necessarily represent the views of the Bank of England or members of the Monetary

Household debt and consumption in the UK Evidence from UK microdata 10 March 2015 Disclaimer This presentation does not necessarily represent the views of the Bank of England or members of the Monetary

Czech National Bank Information regarding changes in recommended LTV limits 15 June 2016

Czech National Bank Information regarding changes in recommended LTV limits 15 June 2016 The Czech National Bank published on 14 June 2016 the amendment of its Recommendation on the management of risks

Czech National Bank Information regarding changes in recommended LTV limits 15 June 2016 The Czech National Bank published on 14 June 2016 the amendment of its Recommendation on the management of risks

Discussion of Capital Injection, Monetary Policy, and Financial Accelerators

Discussion of Capital Injection, Monetary Policy, and Financial Accelerators Karl Walentin Sveriges Riksbank 1. Background This paper is part of the large literature that takes as its starting point the

Discussion of Capital Injection, Monetary Policy, and Financial Accelerators Karl Walentin Sveriges Riksbank 1. Background This paper is part of the large literature that takes as its starting point the

REMARKS ON THE BASEL CAPITAL FRAMEWORK AND TRADE FINANCE, 27 FEBRUARY 2014 SESSION 4. Mr. Andrew CORNFORD Research Fellow Financial Markets Center

REMARKS ON THE BASEL CAPITAL FRAMEWORK AND TRADE FINANCE, 27 FEBRUARY 2014 SESSION 4 Mr. Andrew CORNFORD Research Fellow Financial Markets Center 1 Webster2014.B3&TF Remarks on the Basel Capital Framework

REMARKS ON THE BASEL CAPITAL FRAMEWORK AND TRADE FINANCE, 27 FEBRUARY 2014 SESSION 4 Mr. Andrew CORNFORD Research Fellow Financial Markets Center 1 Webster2014.B3&TF Remarks on the Basel Capital Framework

Key matters in examining Liquidity Risk Management at Large Complex Financial Groups

Key matters in examining Liquidity Risk Management at Large Complex Financial Groups (1) Governance of liquidity risk management Senior management of a large complex financial group (hereinafter referred

Key matters in examining Liquidity Risk Management at Large Complex Financial Groups (1) Governance of liquidity risk management Senior management of a large complex financial group (hereinafter referred

Supplement to the December 2015 Financial Stability Report: The framework of capital requirements for UK banks

Supplement to the December 2015 Financial Stability Report: The framework of capital requirements for UK banks 1 The framework of capital requirements for UK banks December 2015 The framework of capital

Supplement to the December 2015 Financial Stability Report: The framework of capital requirements for UK banks 1 The framework of capital requirements for UK banks December 2015 The framework of capital

The Banking System and the Money Supply. 2003 South-Western/Thomson Learning

The Banking System and the Money Supply 2003 South-Western/Thomson Learning What Counts as Money MONEY Anything that is widely accepted as a means of payment What Counts as Money MONEY Anything that is

The Banking System and the Money Supply 2003 South-Western/Thomson Learning What Counts as Money MONEY Anything that is widely accepted as a means of payment What Counts as Money MONEY Anything that is

EcOS (Economic Outlook Suite)

") EcOS (Economic Outlook Suite) Customer profile The International Monetary Fund (IMF) is an international organization working to promote international monetary cooperation and exchange stability; to foster

EcOS (Economic Outlook Suite) Customer profile The International Monetary Fund (IMF) is an international organization working to promote international monetary cooperation and exchange stability; to foster

EIOPA Stress Test 2011. Press Briefing Frankfurt am Main, 4 July 2011

EIOPA Stress Test 2011 Press Briefing Frankfurt am Main, 4 July 2011 Topics 1. Objectives 2. Initial remarks 3. Framework 4. Participation 5. Results 6. Summary 7. Follow up 2 Objectives Overall objective

EIOPA Stress Test 2011 Press Briefing Frankfurt am Main, 4 July 2011 Topics 1. Objectives 2. Initial remarks 3. Framework 4. Participation 5. Results 6. Summary 7. Follow up 2 Objectives Overall objective

Monetary and Financial Trends First Quarter 2011. Table of Contents

Financial Stability Directorate Monetary and Financial Trends First Quarter 2011 Table of Contents Highlights... 1 1. Monetary Aggregates... 3 2. Credit Developments... 4 3. Interest Rates... 7 4. Domestic

Financial Stability Directorate Monetary and Financial Trends First Quarter 2011 Table of Contents Highlights... 1 1. Monetary Aggregates... 3 2. Credit Developments... 4 3. Interest Rates... 7 4. Domestic

Regulation of Foreign Currency Mortgage Loans. - the case of transition countries in Central and Eastern Europe

Regulation of Foreign Currency Mortgage Loans - the case of transition countries in Central and Eastern Europe 4 th World Bank conference on Housing Finance in Emerging Markets Washington, D.C., May 26-27,

Regulation of Foreign Currency Mortgage Loans - the case of transition countries in Central and Eastern Europe 4 th World Bank conference on Housing Finance in Emerging Markets Washington, D.C., May 26-27,

Figure C Supervisory risk assessment for insurance and pension funds expected future development

5. Risk assessment This chapter aims to asses those risks which were identified in the first chapter and further elaborated in the next parts on insurance, reinsurance and occupational pensions. 5.1. Qualitative

5. Risk assessment This chapter aims to asses those risks which were identified in the first chapter and further elaborated in the next parts on insurance, reinsurance and occupational pensions. 5.1. Qualitative

Credit Risk Models. August 24 26, 2010

Credit Risk Models August 24 26, 2010 AGENDA 1 st Case Study : Credit Rating Model Borrowers and Factoring (Accounts Receivable Financing) pages 3 10 2 nd Case Study : Credit Scoring Model Automobile Leasing

Credit Risk Models August 24 26, 2010 AGENDA 1 st Case Study : Credit Rating Model Borrowers and Factoring (Accounts Receivable Financing) pages 3 10 2 nd Case Study : Credit Scoring Model Automobile Leasing

Exam 1 Review. 3. A severe recession is called a(n): A) depression. B) deflation. C) exogenous event. D) market-clearing assumption.

: A) depression. B) deflation. C) exogenous event. D) market-clearing assumption.") Exam 1 Review 1. Macroeconomics does not try to answer the question of: A) why do some countries experience rapid growth. B) what is the rate of return on education. C) why do some countries have high

Exam 1 Review 1. Macroeconomics does not try to answer the question of: A) why do some countries experience rapid growth. B) what is the rate of return on education. C) why do some countries have high

Lecture 4: The Aftermath of the Crisis

Lecture 4: The Aftermath of the Crisis 2 The Fed s Efforts to Restore Financial Stability A financial panic in fall 2008 threatened the stability of the global financial system. In its lender-of-last-resort

Lecture 4: The Aftermath of the Crisis 2 The Fed s Efforts to Restore Financial Stability A financial panic in fall 2008 threatened the stability of the global financial system. In its lender-of-last-resort

Econ 202 Section 4 Final Exam

Douglas, Fall 2009 December 15, 2009 A: Special Code 00004 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 202 Section 4 Final Exam 1. Oceania buys $40

Douglas, Fall 2009 December 15, 2009 A: Special Code 00004 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 202 Section 4 Final Exam 1. Oceania buys $40