THE RELATIONSHIP BETWEEN INFLATION AND STOCK PRICES (A Case of JORDAN)

|

|

|

- Dominick Fox

- 7 years ago

- Views:

Transcription

1 THE RELATIONSHIP BETWEEN INFLATION AND STOCK PRICES (A Case of JORDAN) Shukairi Nori Mousa 1, Waleed Al safi 2, AbdulBaset Hasoneh 3 & Marwan Mohammad Abo-orabi 4 1 Assistant Professor of Financial Management, Al isra University, Jordan 2 Assistant Professor of Financial Management, Jerash University, Jordan 3 Associate professor of Marketing, Al isra University, Jordan 4 Assistant Professor of Financial Management, Petra University, Jordan ABSTRACT Jordan is a lower middle income country with about 5.6 million inhabitants. The inflation phenomenon in the Jordanian economy is enforced by three main reasons; the monetary and fiscal policies, the high openness rate toward the regional and international economics and the weak of structural productive base for the Jordanian economy. The last two reasons make the inflation is a sensitive and serious problem and hard to control or put high burden on the government. This paper aims to explain the impact of inflation on stock prices at the Amman stock exchange by takes a random sample from the companies that listed in the market. So we will use some statistic programmers to analysis the data that The result of the study varies. Not all companies offers a perfect hedge against inflation. The companies such as (JOIN,JOEP,NPSC, ZAR, ACDT, ELZA, and DADI ) are negatively correlated against inflation. Whereas the other selected companies such as (ARBK,CABK, and JOPH ) shows a slightly positive correlation between stock price changes and inflation.will use it in this study. And we obtained the data from the CBJ and Department of Statistics in Jordan. INTRODUCTION: Jordan is a lower middle income country with about 5.6 million inhabitants. The inflation phenomenon in the Jordanian economy is enforced by three main reasons; the monetary and fiscal policies, the high openness rate toward the regional and international economics and the weak of structural productive base for the Jordanian economy. The last two reasons make the inflation is a sensitive and serious problem and hard to control or put high burden on the government. This paper aims to explain the impact of inflation on stock prices at the Amman stock exchange by takes a random sample from the companies that listed in the market. So we will use some statistic programmers to analysis the data that will use it in this study. And we obtained the data from the CBJ and Department of Statistics in Jordan. This paper is organized as follow : in section (1) talk about the inflation concept, then talked about inflation in Jordan, then talk about the role of exchange market and talk about Amman exchange market. And in section (2) explained the inflation relation with stock price for some companies listed in (ASE) by use the (E-views 4) statistics program. and the results are available in the section three. The Study Objectives: This study aims at: 1- know the concept of inflation, and to take a look about the inflation in Jordan. and investigating the inflation process in Jordan. 2- Identify the relationship between inflation and stock prices. Questions of the Study: 1- Are the stocks hedge against inflation? 2- What is the relationship between the stock prices and inflation?, and is the relation constant between all companies? The Methodology of the Study: This paper begins with brief summary and previous studies that have been written in this field of The impact of inflation on stock prices. Then analyze and test these data by using spread sheet (Excel) and the researcher use some statistic programs such as(e-views 4). The researcher used two methods in this paper to collect the data and information: 1- primary data: obtained from several positions, such as Department of Statistics- Jordan and central Bank of Jordan. 46

2 2-Secondary data: from previous studies, references, and International journals. Previous Studies: Chao Wei, (2006),( inflation and stock Prices, no illusion), used VAR results to advocate in inflation illusion as the explanation for the positive association between in inflation and the dividend yield. Contrary to their results, we find that a fully rational dynamic general equilibrium model can generate a positive correlation between the dividend yield and inflation of comparable size to its data counterpart. The model results support a proxy hypothesis, according to which, a third factor, which in our model represents technology shocks, moves both inflation and the dividend yield in the same direction, resulting in a positive correlation between the two. The VAR structure of our model solutions makes it possible to decompose the dividend yield into the long-run expected dividend growth rate and the discount rate components, so that their relative importance can be studied. Al-Rjoub,( The Adjustments of Stock Prices to Information about Inflation: Evidence Form MENA Countries ), This paper extend the empirical evidence by analyzing the reaction of monthly stock returns to the unexpected portion of CPI inflation rate and by capturing the asymmetric shocks to volatility of unexpected inflation in five MENA countries. Both Threshold GARCH and Exponential GARCH are used to catch the news affect that unexpected inflation may have on stock returns. Results document a negative and strongly significant relationship between unexpected inflation and stock returns in MENA countries. Results also indicate that the stock markets of the listed MENA countries does not feel the high up s and down s movements in the markets and as such the volatilities. The asymmetric news effect is absent. Ioannides, Katrakilidis, and Lake, (the relationship between stock market returns and inflation), this study examined whether this holds for Greece, over the period Taking a step further, we re-examine the above relationship taking into account the existence of possible structural breaks over the considered time horizon. The empirical methodology uses ARDL cointegration technique in conjunction with Granger causality tests to detect possible long-run and short-run effects between the involved variables as well as the direction of these effects. The results provide evidence in favour of a negative long-run causal relationship between the considered series after Boucher, (2004),( Stock Prices, Inflation and Stock Returns Predictability), This paper considers a new perspective on the relationship between stock prices and inflation, by estimating the common long-term trend in real stock prices, as reflected in the earning-price ratio, and both expected and realized inflation. He study the role of the transitory deviations from the common trend in the earning-price ratio and realized inflation for predicting stock market fluctuations. In particular, he find that these deviations exhibit substantial in sample and out-of-sample forecasting abilities for both real stock returns and excess returns. Moreover, he find that this variable provides information about future stock returns at short and intermediate horizons that is not captured by other popular forecasting variables. Concept of Inflation: Inflation is defined as a rise in the average level of price for all goods and services. and we can be defined it as a permanent increase in the aggregate price level which implies a diminishing of the purchasing power1 and increase the cost of living. It is important to note from this definition that the movement in the price level needs to be permanent to believe it as inflation. Inflation considered one of the economic phenomena that still polarized attention of both development and developing countries. Also, it is considered a complex economic subject because it represents a tangible phenomenon and not only a macroeconomic variable such as gross domestic product and investment. In addition, there are many different reasons that may cause inflation. Therefore, the economic school of thoughts and many economists tried to study this observable variable in order to analyze, explain and understand its relation with the other macroeconomic variables. The importance of inflation, as a macroeconomic variable, in the literature comes from its ability to reflect the economic stability of a nation, or the ability of the government to control the economy through its monetary and fiscal policies. Moreover, inflation may give an idea about the trade policy of a nation such as the degree of openness. Inflation in Jordan Jordan is a lower middle income country with about 5.6 million inhabitants and annual per capital income at current prices of JD The inflation phenomenon in the Jordanian economy is enforced by three main reasons; the monetary and fiscal policies, the high openness rate toward the regional and international economics and the weak of structural productive base for the Jordanian economy. The last two reasons make the inflation is a sensitive and 47

3 serious problem and hard to control or put high burden on the government. Looking historically to the inflation rate measured by the percentage change in the annual consumer price index (CPI) in Jordan during the period ( ) shows clearly that this rate fluctuates. The average inflation rate during this period is around (2.484%) and this rate considered high if we take into consideration that the average annual inflation rate in Jordan is not indexed to the annual increase of the wages and salaries. Table 1 gives an idea about the fluctuation of the inflation rate during sub periods. And we can show the inflation movements in the graph (1) Table (1) : Inflation rate in Jordan from ( ) Years Inflation Rate Graph (1) : Inflation movements in Jordan 8 6 Inflation rate The Role of a Stock Exchange: The primary role of a stock exchange to provide a market where financial instruments, including shares, can be traded in a regulated environment, without restraint. A stock market is a vital part of any economic system in which ownership can be bought or sold. A stock exchange and it's presence in an economic system can be justified by the some functions as : channel savings into investments, to convert investment into cash, and to evaluate and manage securities. Inflation and Stock Prices: The relationship between stock prices, rates of return and inflation is perhaps best illustrated in the context of the dividend-discount model (DDM). Investors will set the price of a stock at time t, St, to a point where the expected return on the stock is equal to the required rate of return. Consider first a world with no inflation and a company is expected to genera a real cash flow of C per period in perpetuity. Assume that the firm pays out all free cash flow as a dividend. Where is : the current price of a stock (S t ) is calculated by dividing the dividend (D) by the required rate of return (k s ). The formula expressed mathematically is as follows: S t =D/ k s (1) Suppose now that expected inflation increases. This brings about two fundamental changes. First, the cash flows of the company may change as general Inflation acts on both revenues and expenses. Second, the discount rate will change to a nominal rate (k nom ) defined by: k nom =(1+k r )(1+I) (2) where: k is the real required rate of return given that expected inflation (I) is at some positive value. 48

and this rate considered high if we take into consideration that the average annual inflation rate in Jordan is not indexed to the annual increase of the wages and salaries.")

4 The Fisher Effect expresses the nominal rate of interest (r) as the sum of the real rate of interest plus the inflation rate. as follows: 1+r=(1+R)(1+I) r =R+I (3) Where: r is the nominal rate of interest. R is the real rate of interest. I is the real rate of inflation. To test if there is a relationship between stock prices and inflation we used time series data from the CPI as a measure of inflation and the stock prices of selected companies as a measure of stock validation. The time series was between 1998 and We used a regression analysis to determine if there is indeed a negative correlation between inflation and stock prices. If there were a negative correlation then the fundamental teaching hold true and the relationship would be negative. Table 2 indicates the change in CPI and stock prices for the selected companies in the Amman stock exchange. The price change (PC) is measured as follows: PC=(P 2 P 1 )/P 1 (4) Where P 1, and P 2 represents the stock price or CPI index in time one and two respectively. Table 2 : Change in CPI and stock prices for the selected companies in the Amman stock exchange. For the period from ( ) Years ARBK CABK JOIN JOEP NPSC ZAR JOPH ACDT ELZA DADI CPI Figure 2 : Change in CPI and stock prices for the selected companies in the Amman stock exchange. For the period from ( ) CPI ARBK CABK ACDT DADI ELZA JOIN JOEP JOPH NPSC 49

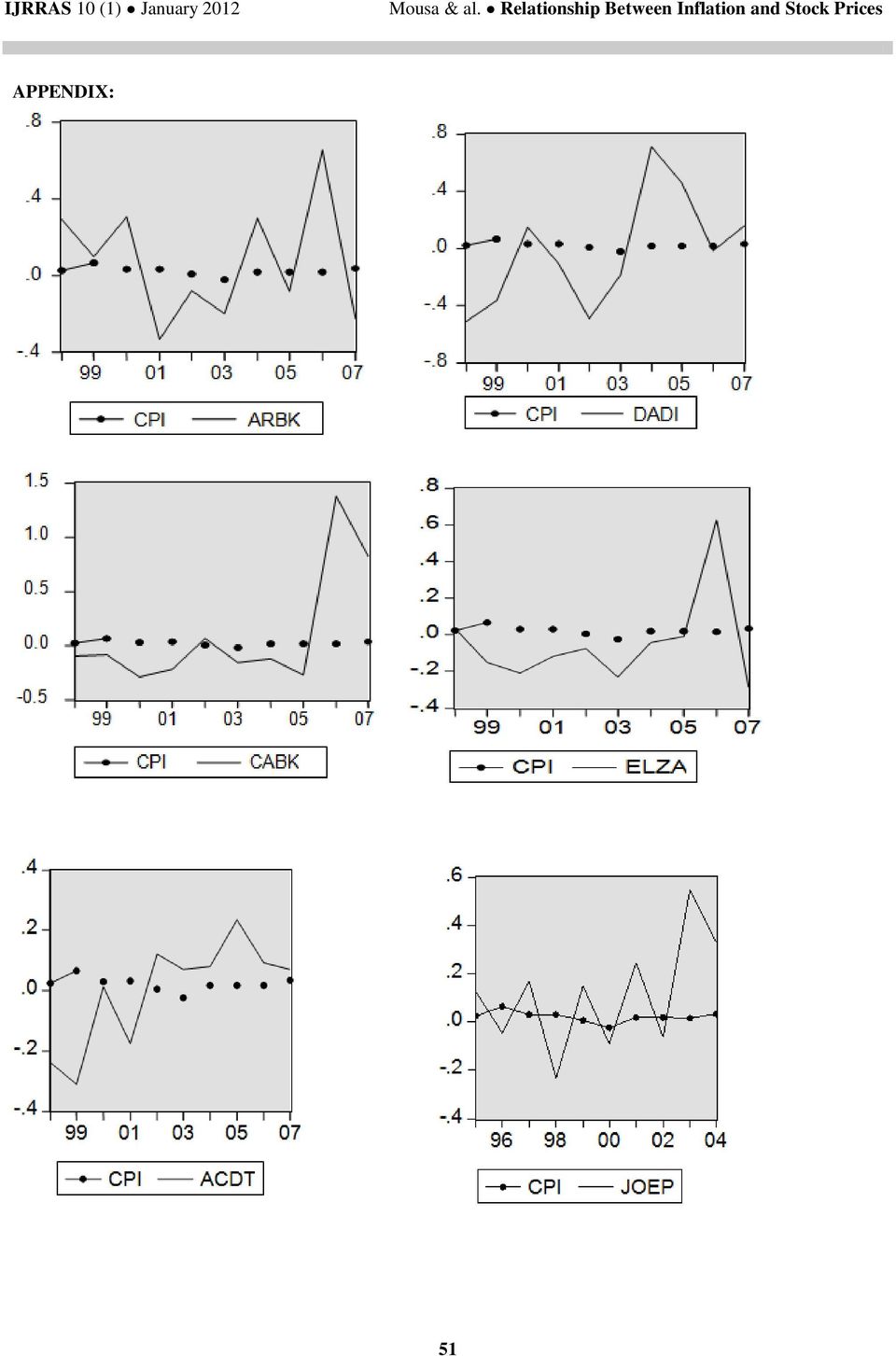

5 Table 3 explained the results of the regression analysis in determining the correlation between stock price movements and CPI movements. Table 3: Correlations between changes CPI and stock prices for the selected companies in the Amman stock exchange. Companies Names Correlations ARBK CABK JOIN JOEP NPSC ZAR JOPH ACDT ELZA DADI CONCLUSION Stocks represent claims to underlying real assets, and as such, should maintain their value in the face of increases in the general price level. The result of the study varies. Not all companies offers a perfect hedge against inflation. The companies such as (JOIN,JOEP,NPSC, ZAR, ACDT, ELZA, and DADI ) are negatively correlated against inflation. Whereas the other selected companies such as (ARBK,CABK, and JOPH ) shows a slightly positive correlation between stock price changes and inflation. Stocks are not a perfect hedge to the degree that corporate cash flows are negatively related to inflation. And sometimes the correlation between the inflation and stock price may be negative or positively. List of Abbreviation: ASE CPI ARBK CABK JOIN JOEP NPSC ZAR JOPH ACDT ELZA DADI Amman Stock Exchange Consumer Price Index Arab Bank Cairo Amman Bank Jordan Insurance Jordanian Electric Power National Portfolio Securities AL-Zarqa for Education & Investment Jordan Phosphate Mines Arab Chemical Detergents Industries EL-Zay Ready Wear Manuf Dar AL Dawa Development & Investment REFERENCES [1]. Rose,S.& Marquis,H Money and Capital Market. 9 th ed. Mcgrawhill. [2]. Madura, Jeff International Corporate Finance. 8 th ed. Thomson. [3]. Bodie,Z. Kane,A.& Marcus,A Invesetments. 6 th ed. Mcgrawhill. [4]. Boucher Stock prices, Inflation and stock returns predicatively. [5]. Giammarino,R. Central Bank Policy, Inflation, and Stock Prices. P [6]. Wei, Ch Ination and Stock Prices: No Illusion. [7]. Al-Rjoub,S. The Adjustments of Stock Prices to Information about Inflation: Evidence Form MENA Countries. [8]. Al-Khazali,O. Empirical Tests of the Proxy Hypothesis: Evidence From Jordan. [9]. Ioannides. Katrakilidis. and Lake. the relationship between stock market returns and inflation. P

6 APPENDIX: 51

7 52

The relationships between stock market capitalization rate and interest rate: Evidence from Jordan

Peer-reviewed & Open access journal ISSN: 1804-1205 www.pieb.cz BEH - Business and Economic Horizons Volume 2 Issue 2 July 2010 pp. 60-66 The relationships between stock market capitalization rate and

Peer-reviewed & Open access journal ISSN: 1804-1205 www.pieb.cz BEH - Business and Economic Horizons Volume 2 Issue 2 July 2010 pp. 60-66 The relationships between stock market capitalization rate and

INFLATION, INTEREST RATE, AND EXCHANGE RATE: WHAT IS THE RELATIONSHIP?

107 INFLATION, INTEREST RATE, AND EXCHANGE RATE: WHAT IS THE RELATIONSHIP? Maurice K. Shalishali, Columbus State University Johnny C. Ho, Columbus State University ABSTRACT A test of IFE (International

107 INFLATION, INTEREST RATE, AND EXCHANGE RATE: WHAT IS THE RELATIONSHIP? Maurice K. Shalishali, Columbus State University Johnny C. Ho, Columbus State University ABSTRACT A test of IFE (International

Problem Set #4: Aggregate Supply and Aggregate Demand Econ 100B: Intermediate Macroeconomics

roblem Set #4: Aggregate Supply and Aggregate Demand Econ 100B: Intermediate Macroeconomics 1) Explain the differences between demand-pull inflation and cost-push inflation. Demand-pull inflation results

roblem Set #4: Aggregate Supply and Aggregate Demand Econ 100B: Intermediate Macroeconomics 1) Explain the differences between demand-pull inflation and cost-push inflation. Demand-pull inflation results

Use the following to answer question 9: Exhibit: Keynesian Cross

1. Leading economic indicators are: A) the most popular economic statistics. B) data that are used to construct the consumer price index and the unemployment rate. C) variables that tend to fluctuate in

1. Leading economic indicators are: A) the most popular economic statistics. B) data that are used to construct the consumer price index and the unemployment rate. C) variables that tend to fluctuate in

ECON 3312 Macroeconomics Exam 3 Fall 2014. Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

ECON 3312 Macroeconomics Exam 3 Fall 2014 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Everything else held constant, an increase in net

ECON 3312 Macroeconomics Exam 3 Fall 2014 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Everything else held constant, an increase in net

The Impact Of Inflation On Stock Prices In Two SADC Countries. Geyser, J.M. & Lowies, G.A.

The Impact Of Inflation On Stock Prices In Two SADC Countries Geyser, J.M. & Lowies, G.A. Working paper: 2001-14 Department of Agricultural Economics, Extension and Rural Development University of Pretoria

The Impact Of Inflation On Stock Prices In Two SADC Countries Geyser, J.M. & Lowies, G.A. Working paper: 2001-14 Department of Agricultural Economics, Extension and Rural Development University of Pretoria

Introduction to Risk, Return and the Historical Record

Introduction to Risk, Return and the Historical Record Rates of return Investors pay attention to the rate at which their fund have grown during the period The holding period returns (HDR) measure the

Introduction to Risk, Return and the Historical Record Rates of return Investors pay attention to the rate at which their fund have grown during the period The holding period returns (HDR) measure the

Dynamic Relationship between Interest Rate and Stock Price: Empirical Evidence from Colombo Stock Exchange

International Journal of Business and Social Science Vol. 6, No. 4; April 2015 Dynamic Relationship between Interest Rate and Stock Price: Empirical Evidence from Colombo Stock Exchange AAMD Amarasinghe

International Journal of Business and Social Science Vol. 6, No. 4; April 2015 Dynamic Relationship between Interest Rate and Stock Price: Empirical Evidence from Colombo Stock Exchange AAMD Amarasinghe

Relationships among Inflation, Interest Rates, and Exchange Rates. J. Gaspar: Adapted from Jeff Madura, International Financial Management

Chapter8 Relationships among Inflation, Interest Rates, and Exchange Rates J. Gaspar: Adapted from Jeff Madura, International Financial Management 8. 1 International Finance Theories (cont) Purchasing

Chapter8 Relationships among Inflation, Interest Rates, and Exchange Rates J. Gaspar: Adapted from Jeff Madura, International Financial Management 8. 1 International Finance Theories (cont) Purchasing

CH 10 - REVIEW QUESTIONS

CH 10 - REVIEW QUESTIONS 1. The short-run aggregate supply curve is horizontal at: A) a level of output determined by aggregate demand. B) the natural level of output. C) the level of output at which the

CH 10 - REVIEW QUESTIONS 1. The short-run aggregate supply curve is horizontal at: A) a level of output determined by aggregate demand. B) the natural level of output. C) the level of output at which the

Causes of Inflation in the Iranian Economy

Causes of Inflation in the Iranian Economy Hamed Armesh* and Abas Alavi Rad** It is clear that in the nearly last four decades inflation is one of the important problems of Iranian economy. In this study,

Causes of Inflation in the Iranian Economy Hamed Armesh* and Abas Alavi Rad** It is clear that in the nearly last four decades inflation is one of the important problems of Iranian economy. In this study,

THE RELATIONSHIP BETWEEN INFLATION AND STOCK MARKET: EVIDENCE FROM MALAYSIA, UNITED STATES AND CHINA.

ISSN: 2162-6359 International Journal of Economics and Management Sciences Vol. 1, No. 2, 2011, pp. 01-16 MANAGEMENT JOURNALS managementjournals.org THE RELATIONSHIP BETWEEN INFLATION AND STOCK MARKET:

ISSN: 2162-6359 International Journal of Economics and Management Sciences Vol. 1, No. 2, 2011, pp. 01-16 MANAGEMENT JOURNALS managementjournals.org THE RELATIONSHIP BETWEEN INFLATION AND STOCK MARKET:

Impact of Economic Factors on the Stock Prices at Amman Stock Market (1992-2010)

") Impact of Economic Factors on the Stock Prices at Amman Stock Market (1992-2010) Dr. Ghazi F. Momani Associate Professor, Department of Financial Sciences he Arab Academy for Banking & Financial Sciences

Impact of Economic Factors on the Stock Prices at Amman Stock Market (1992-2010) Dr. Ghazi F. Momani Associate Professor, Department of Financial Sciences he Arab Academy for Banking & Financial Sciences

Econ 303: Intermediate Macroeconomics I Dr. Sauer Sample Questions for Exam #3

Econ 303: Intermediate Macroeconomics I Dr. Sauer Sample Questions for Exam #3 1. When firms experience unplanned inventory accumulation, they typically: A) build new plants. B) lay off workers and reduce

Econ 303: Intermediate Macroeconomics I Dr. Sauer Sample Questions for Exam #3 1. When firms experience unplanned inventory accumulation, they typically: A) build new plants. B) lay off workers and reduce

Determinants of Stock Market Performance in Pakistan

Determinants of Stock Market Performance in Pakistan Mehwish Zafar Sr. Lecturer Bahria University, Karachi campus Abstract Stock market performance, economic and political condition of a country is interrelated

Determinants of Stock Market Performance in Pakistan Mehwish Zafar Sr. Lecturer Bahria University, Karachi campus Abstract Stock market performance, economic and political condition of a country is interrelated

4 Macroeconomics LESSON 6

4 Macroeconomics LESSON 6 Interest Rates and Monetary Policy in the Short Run and the Long Run Introduction and Description This lesson explores the relationship between the nominal interest rate and the

4 Macroeconomics LESSON 6 Interest Rates and Monetary Policy in the Short Run and the Long Run Introduction and Description This lesson explores the relationship between the nominal interest rate and the

Review for Exam 2. Instructions: Please read carefully

Review for Exam Instructions: Please read carefully The exam will have 1 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation questions.

Review for Exam Instructions: Please read carefully The exam will have 1 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation questions.

ijcrb.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS AUGUST 2014 VOL 6, NO 4

RELATIONSHIP AND CAUSALITY BETWEEN INTEREST RATE AND INFLATION RATE CASE OF JORDAN Dr. Mahmoud A. Jaradat Saleh A. AI-Hhosban Al al-bayt University, Jordan ABSTRACT This study attempts to examine and study

RELATIONSHIP AND CAUSALITY BETWEEN INTEREST RATE AND INFLATION RATE CASE OF JORDAN Dr. Mahmoud A. Jaradat Saleh A. AI-Hhosban Al al-bayt University, Jordan ABSTRACT This study attempts to examine and study

Stock market booms and real economic activity: Is this time different?

International Review of Economics and Finance 9 (2000) 387 415 Stock market booms and real economic activity: Is this time different? Mathias Binswanger* Institute for Economics and the Environment, University

International Review of Economics and Finance 9 (2000) 387 415 Stock market booms and real economic activity: Is this time different? Mathias Binswanger* Institute for Economics and the Environment, University

THE IMPACT OF FUTURE MARKET ON MONEY DEMAND IN IRAN

THE IMPACT OF FUTURE MARKET ON MONEY DEMAND IN IRAN Keikha M. 1 and *Shams Koloukhi A. 2 and Parsian H. 2 and Darini M. 3 1 Department of Economics, Allameh Tabatabaie University, Iran 2 Young Researchers

THE IMPACT OF FUTURE MARKET ON MONEY DEMAND IN IRAN Keikha M. 1 and *Shams Koloukhi A. 2 and Parsian H. 2 and Darini M. 3 1 Department of Economics, Allameh Tabatabaie University, Iran 2 Young Researchers

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Suvey of Macroeconomics, MBA 641 Fall 2006, Final Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Modern macroeconomics emerged from

Suvey of Macroeconomics, MBA 641 Fall 2006, Final Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Modern macroeconomics emerged from

by Maria Heiden, Berenberg Bank

Dynamic hedging of equity price risk with an equity protect overlay: reduce losses and exploit opportunities by Maria Heiden, Berenberg Bank As part of the distortions on the international stock markets

Dynamic hedging of equity price risk with an equity protect overlay: reduce losses and exploit opportunities by Maria Heiden, Berenberg Bank As part of the distortions on the international stock markets

Do Commodity Price Spikes Cause Long-Term Inflation?

No. 11-1 Do Commodity Price Spikes Cause Long-Term Inflation? Geoffrey M.B. Tootell Abstract: This public policy brief examines the relationship between trend inflation and commodity price increases and

No. 11-1 Do Commodity Price Spikes Cause Long-Term Inflation? Geoffrey M.B. Tootell Abstract: This public policy brief examines the relationship between trend inflation and commodity price increases and

Equity Market Risk Premium Research Summary. 12 April 2016

Equity Market Risk Premium Research Summary 12 April 2016 Introduction welcome If you are reading this, it is likely that you are in regular contact with KPMG on the topic of valuations. The goal of this

Equity Market Risk Premium Research Summary 12 April 2016 Introduction welcome If you are reading this, it is likely that you are in regular contact with KPMG on the topic of valuations. The goal of this

10/7/2013. Chapter 9: Introduction to Economic Fluctuations. Facts about the business cycle. Unemployment. Okun s Law Y Y

Facts about the business cycle Chapter 9: GD growth averages 3 3.5 percent per year over the long run with large fluctuations in the short run. Consumption and investment fluctuate with GD, but consumption

Facts about the business cycle Chapter 9: GD growth averages 3 3.5 percent per year over the long run with large fluctuations in the short run. Consumption and investment fluctuate with GD, but consumption

MSc Financial Economics - SH506 (Under Review)

") MSc Financial Economics - SH506 (Under Review) 1. Objectives The objectives of the MSc Financial Economics programme are: To provide advanced postgraduate training in financial economics with emphasis

MSc Financial Economics - SH506 (Under Review) 1. Objectives The objectives of the MSc Financial Economics programme are: To provide advanced postgraduate training in financial economics with emphasis

Measuring the Cost of Living THE CONSUMER PRICE INDEX

6 In this chapter, look for the answers to these questions: What is the Consumer (CPI)? How is it calculated? What s it used for? What are the problems with the CPI? How serious are they? How does the

6 In this chapter, look for the answers to these questions: What is the Consumer (CPI)? How is it calculated? What s it used for? What are the problems with the CPI? How serious are they? How does the

CHAPTER 11. AN OVEVIEW OF THE BANK OF ENGLAND QUARTERLY MODEL OF THE (BEQM)

") 1 CHAPTER 11. AN OVEVIEW OF THE BANK OF ENGLAND QUARTERLY MODEL OF THE (BEQM) This model is the main tool in the suite of models employed by the staff and the Monetary Policy Committee (MPC) in the construction

1 CHAPTER 11. AN OVEVIEW OF THE BANK OF ENGLAND QUARTERLY MODEL OF THE (BEQM) This model is the main tool in the suite of models employed by the staff and the Monetary Policy Committee (MPC) in the construction

Professor Christina Romer. LECTURE 17 MACROECONOMIC VARIABLES AND ISSUES March 17, 2016

Economics 2 Spring 2016 Professor Christina Romer Professor David Romer LECTURE 17 MACROECONOMIC VARIABLES AND ISSUES March 17, 2016 I. MACROECONOMICS VERSUS MICROECONOMICS II. REAL GDP A. Definition B.

Economics 2 Spring 2016 Professor Christina Romer Professor David Romer LECTURE 17 MACROECONOMIC VARIABLES AND ISSUES March 17, 2016 I. MACROECONOMICS VERSUS MICROECONOMICS II. REAL GDP A. Definition B.

Chapter 13. Aggregate Demand and Aggregate Supply Analysis

Chapter 13. Aggregate Demand and Aggregate Supply Analysis Instructor: JINKOOK LEE Department of Economics / Texas A&M University ECON 203 502 Principles of Macroeconomics In the short run, real GDP and

Chapter 13. Aggregate Demand and Aggregate Supply Analysis Instructor: JINKOOK LEE Department of Economics / Texas A&M University ECON 203 502 Principles of Macroeconomics In the short run, real GDP and

Extra Problems #3. ECON 410.502 Macroeconomic Theory Spring 2010 Instructor: Guangyi Ma. Notice:

ECON 410.502 Macroeconomic Theory Spring 2010 Instructor: Guangyi Ma Extra Problems #3 Notice: (1) There are 25 multiple-choice problems covering Chapter 6, 9, 10, 11. These problems are not homework and

ECON 410.502 Macroeconomic Theory Spring 2010 Instructor: Guangyi Ma Extra Problems #3 Notice: (1) There are 25 multiple-choice problems covering Chapter 6, 9, 10, 11. These problems are not homework and

Interpreting Market Responses to Economic Data

Interpreting Market Responses to Economic Data Patrick D Arcy and Emily Poole* This article discusses how bond, equity and foreign exchange markets have responded to the surprise component of Australian

Interpreting Market Responses to Economic Data Patrick D Arcy and Emily Poole* This article discusses how bond, equity and foreign exchange markets have responded to the surprise component of Australian

Theories of Exchange rate determination

Theories of Exchange rate determination INTRODUCTION By definition, the Foreign Exchange Market is a market 1 in which different currencies can be exchanged at a specific rate called the foreign exchange

Theories of Exchange rate determination INTRODUCTION By definition, the Foreign Exchange Market is a market 1 in which different currencies can be exchanged at a specific rate called the foreign exchange

PERPETUITIES NARRATIVE SCRIPT 2004 SOUTH-WESTERN, A THOMSON BUSINESS

NARRATIVE SCRIPT 2004 SOUTH-WESTERN, A THOMSON BUSINESS NARRATIVE SCRIPT: SLIDE 2 A good understanding of the time value of money is crucial for anybody who wants to deal in financial markets. It does

NARRATIVE SCRIPT 2004 SOUTH-WESTERN, A THOMSON BUSINESS NARRATIVE SCRIPT: SLIDE 2 A good understanding of the time value of money is crucial for anybody who wants to deal in financial markets. It does

In this chapter we learn the potential causes of fluctuations in national income. We focus on demand shocks other than supply shocks.

Chapter 11: Applying IS-LM Model In this chapter we learn the potential causes of fluctuations in national income. We focus on demand shocks other than supply shocks. We also learn how the IS-LM model

Chapter 11: Applying IS-LM Model In this chapter we learn the potential causes of fluctuations in national income. We focus on demand shocks other than supply shocks. We also learn how the IS-LM model

APPENDIX 3 TIME VALUE OF MONEY. Time Lines and Notation. The Intuitive Basis for Present Value

1 2 TIME VALUE OF MONEY APPENDIX 3 The simplest tools in finance are often the most powerful. Present value is a concept that is intuitively appealing, simple to compute, and has a wide range of applications.

1 2 TIME VALUE OF MONEY APPENDIX 3 The simplest tools in finance are often the most powerful. Present value is a concept that is intuitively appealing, simple to compute, and has a wide range of applications.

Appropriate discount rates for long term public projects

Appropriate discount rates for long term public projects Kåre P. Hagen, Professor Norwegian School of Economics Norway The 5th Concept Symposium on Project Governance Valuing the Future - Public Investments

Appropriate discount rates for long term public projects Kåre P. Hagen, Professor Norwegian School of Economics Norway The 5th Concept Symposium on Project Governance Valuing the Future - Public Investments

Econ 202 Section 4 Final Exam

Douglas, Fall 2009 December 15, 2009 A: Special Code 00004 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 202 Section 4 Final Exam 1. Oceania buys $40

Douglas, Fall 2009 December 15, 2009 A: Special Code 00004 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 202 Section 4 Final Exam 1. Oceania buys $40

Examiner s report F9 Financial Management June 2011

Examiner s report F9 Financial Management June 2011 General Comments Congratulations to candidates who passed Paper F9 in June 2011! The examination paper looked at many areas of the syllabus and a consideration

Examiner s report F9 Financial Management June 2011 General Comments Congratulations to candidates who passed Paper F9 in June 2011! The examination paper looked at many areas of the syllabus and a consideration

Aggregate Demand and Aggregate Supply Ing. Mansoor Maitah Ph.D. et Ph.D.

Aggregate Demand and Aggregate Supply Ing. Mansoor Maitah Ph.D. et Ph.D. Aggregate Demand and Aggregate Supply Economic fluctuations, also called business cycles, are movements of GDP away from potential

Aggregate Demand and Aggregate Supply Ing. Mansoor Maitah Ph.D. et Ph.D. Aggregate Demand and Aggregate Supply Economic fluctuations, also called business cycles, are movements of GDP away from potential

ECONOMIC QUESTIONS FOR THE MASTER'S EXAM

ECONOMIC QUESTIONS FOR THE MASTER'S EXAM Introduction 1. What is economics? Discuss the purpose and method of work of economists. Consider observation, induction, deduction and scientific criticism. 2.

ECONOMIC QUESTIONS FOR THE MASTER'S EXAM Introduction 1. What is economics? Discuss the purpose and method of work of economists. Consider observation, induction, deduction and scientific criticism. 2.

WITH-PROFIT ANNUITIES

WITH-PROFIT ANNUITIES BONUS DECLARATION 2014 Contents 1. INTRODUCTION 3 2. SUMMARY OF BONUS DECLARATION 3 3. ECONOMIC OVERVIEW 5 4. WITH-PROFIT ANNUITY OVERVIEW 7 5. INVESTMENTS 9 6. EXPECTED LONG-TERM

WITH-PROFIT ANNUITIES BONUS DECLARATION 2014 Contents 1. INTRODUCTION 3 2. SUMMARY OF BONUS DECLARATION 3 3. ECONOMIC OVERVIEW 5 4. WITH-PROFIT ANNUITY OVERVIEW 7 5. INVESTMENTS 9 6. EXPECTED LONG-TERM

The Impact of Interest Rate Shocks on the Performance of the Banking Sector

The Impact of Interest Rate Shocks on the Performance of the Banking Sector by Wensheng Peng, Kitty Lai, Frank Leung and Chang Shu of the Research Department A rise in the Hong Kong dollar risk premium,

The Impact of Interest Rate Shocks on the Performance of the Banking Sector by Wensheng Peng, Kitty Lai, Frank Leung and Chang Shu of the Research Department A rise in the Hong Kong dollar risk premium,

Answer: C Learning Objective: Money supply Level of Learning: Knowledge Type: Word Problem Source: Unique

1.The aggregate demand curve shows the relationship between inflation and: A) the nominal interest rate. D) the exchange rate. B) the real interest rate. E) short-run equilibrium output. C) the unemployment

1.The aggregate demand curve shows the relationship between inflation and: A) the nominal interest rate. D) the exchange rate. B) the real interest rate. E) short-run equilibrium output. C) the unemployment

Part V: Fundamental Analysis

Securities & Investments Analysis Last 2 Weeks: Part IV Bond Portfolio Management Risk Management + Primer on Derivatives Lecture #0: Part V Individual equity valuation Fundamental Analysis Top-Down Analysis

Securities & Investments Analysis Last 2 Weeks: Part IV Bond Portfolio Management Risk Management + Primer on Derivatives Lecture #0: Part V Individual equity valuation Fundamental Analysis Top-Down Analysis

Nature and Purpose of the Valuation of Business and Financial Assets

G. BUSINESS VALUATIONS 1. Nature and Purpose of the Valuation of Business and Financial Assets 2. Models for the Valuation of Shares 3. The Valuation of Debt and Other Financial Assets 4. Efficient Market

G. BUSINESS VALUATIONS 1. Nature and Purpose of the Valuation of Business and Financial Assets 2. Models for the Valuation of Shares 3. The Valuation of Debt and Other Financial Assets 4. Efficient Market

South African Trade-Offs among Depreciation, Inflation, and Unemployment. Alex Diamond Stephanie Manning Jose Vasquez Erin Whitaker

South African Trade-Offs among Depreciation, Inflation, and Unemployment Alex Diamond Stephanie Manning Jose Vasquez Erin Whitaker April 16, 2003 Introduction South Africa has one of the most unique histories

South African Trade-Offs among Depreciation, Inflation, and Unemployment Alex Diamond Stephanie Manning Jose Vasquez Erin Whitaker April 16, 2003 Introduction South Africa has one of the most unique histories

Determinants of the Hungarian forint/ US dollar exchange rate

Theoretical and Applied Economics FFet al Volume XXIII (2016), No. 1(606), Spring, pp. 163-170 Determinants of the Hungarian forint/ US dollar exchange rate Yu HSING Southeastern Louisiana University,

Theoretical and Applied Economics FFet al Volume XXIII (2016), No. 1(606), Spring, pp. 163-170 Determinants of the Hungarian forint/ US dollar exchange rate Yu HSING Southeastern Louisiana University,

A Test of the International Fisher Effect in Selected Asian Countries

A Test of the International Fisher Effect in Selected Asian Countries Maurice K. Shalishali Columbus State University United States of America Abstract In a simplified statistical test of the IFE (International

A Test of the International Fisher Effect in Selected Asian Countries Maurice K. Shalishali Columbus State University United States of America Abstract In a simplified statistical test of the IFE (International

LECTURE NOTES ON MACROECONOMIC PRINCIPLES

LECTURE NOTES ON MACROECONOMIC PRINCIPLES Peter Ireland Department of Economics Boston College peter.ireland@bc.edu http://www2.bc.edu/peter-ireland/ec132.html Copyright (c) 2013 by Peter Ireland. Redistribution

LECTURE NOTES ON MACROECONOMIC PRINCIPLES Peter Ireland Department of Economics Boston College peter.ireland@bc.edu http://www2.bc.edu/peter-ireland/ec132.html Copyright (c) 2013 by Peter Ireland. Redistribution

EC2105, Professor Laury EXAM 2, FORM A (3/13/02)

") EC2105, Professor Laury EXAM 2, FORM A (3/13/02) Print Your Name: ID Number: Multiple Choice (32 questions, 2.5 points each; 80 points total). Clearly indicate (by circling) the ONE BEST response to each

EC2105, Professor Laury EXAM 2, FORM A (3/13/02) Print Your Name: ID Number: Multiple Choice (32 questions, 2.5 points each; 80 points total). Clearly indicate (by circling) the ONE BEST response to each

Inflation. Chapter 8. 8.1 Money Supply and Demand

Chapter 8 Inflation This chapter examines the causes and consequences of inflation. Sections 8.1 and 8.2 relate inflation to money supply and demand. Although the presentation differs somewhat from that

Chapter 8 Inflation This chapter examines the causes and consequences of inflation. Sections 8.1 and 8.2 relate inflation to money supply and demand. Although the presentation differs somewhat from that

Inflation and Unemployment CHAPTER 22 THE SHORT-RUN TRADE-OFF 0

22 The Short-Run Trade-off Between Inflation and Unemployment CHAPTER 22 THE SHORT-RUN TRADE-OFF 0 In this chapter, look for the answers to these questions: How are inflation and unemployment related in

22 The Short-Run Trade-off Between Inflation and Unemployment CHAPTER 22 THE SHORT-RUN TRADE-OFF 0 In this chapter, look for the answers to these questions: How are inflation and unemployment related in

TD is currently among an exclusive group of 77 stocks awarded our highest average score of 10. SAMPLE. Peers BMO 9 RY 9 BNS 9 CM 8

Updated April 16, 2012 TORONTO-DOMINION BANK (THE) (-T) Banking & Investment Svcs. / Banking Services / Banks Description The Average Score combines the quantitative analysis of five widely-used investment

Updated April 16, 2012 TORONTO-DOMINION BANK (THE) (-T) Banking & Investment Svcs. / Banking Services / Banks Description The Average Score combines the quantitative analysis of five widely-used investment

Concepts in Investments Risks and Returns (Relevant to PBE Paper II Management Accounting and Finance)

") Concepts in Investments Risks and Returns (Relevant to PBE Paper II Management Accounting and Finance) Mr. Eric Y.W. Leung, CUHK Business School, The Chinese University of Hong Kong In PBE Paper II, students

Concepts in Investments Risks and Returns (Relevant to PBE Paper II Management Accounting and Finance) Mr. Eric Y.W. Leung, CUHK Business School, The Chinese University of Hong Kong In PBE Paper II, students

The Orthogonal Response of Stock Returns to Dividend Yield and Price-to-Earnings Innovations

The Orthogonal Response of Stock Returns to Dividend Yield and Price-to-Earnings Innovations Vichet Sum School of Business and Technology, University of Maryland, Eastern Shore Kiah Hall, Suite 2117-A

The Orthogonal Response of Stock Returns to Dividend Yield and Price-to-Earnings Innovations Vichet Sum School of Business and Technology, University of Maryland, Eastern Shore Kiah Hall, Suite 2117-A

Chapter 12 Unemployment and Inflation

Chapter 12 Unemployment and Inflation Multiple Choice Questions 1. The origin of the idea of a trade-off between inflation and unemployment was a 1958 article by (a) A.W. Phillips. (b) Edmund Phelps. (c)

Chapter 12 Unemployment and Inflation Multiple Choice Questions 1. The origin of the idea of a trade-off between inflation and unemployment was a 1958 article by (a) A.W. Phillips. (b) Edmund Phelps. (c)

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Econ 111 Summer 2007 Final Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The classical dichotomy allows us to explore economic growth

Econ 111 Summer 2007 Final Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The classical dichotomy allows us to explore economic growth

CIS September 2012 Exam Diet. Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis

CIS September 2012 Exam Diet Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis Corporate Finance (1 13) 1. Assume a firm issues N1 billion in debt

CIS September 2012 Exam Diet Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis Corporate Finance (1 13) 1. Assume a firm issues N1 billion in debt

Ch.6 Aggregate Supply, Wages, Prices, and Unemployment

1 Econ 302 Intermediate Macroeconomics Chul-Woo Kwon Ch.6 Aggregate Supply, Wages, rices, and Unemployment I. Introduction A. The dynamic changes of and the price adjustment B. Link between the price change

1 Econ 302 Intermediate Macroeconomics Chul-Woo Kwon Ch.6 Aggregate Supply, Wages, rices, and Unemployment I. Introduction A. The dynamic changes of and the price adjustment B. Link between the price change

I. Introduction to Aggregate Demand/Aggregate Supply Model

University of California-Davis Economics 1B-Intro to Macro Handout 8 TA: Jason Lee Email: jawlee@ucdavis.edu I. Introduction to Aggregate Demand/Aggregate Supply Model In this chapter we develop a model

University of California-Davis Economics 1B-Intro to Macro Handout 8 TA: Jason Lee Email: jawlee@ucdavis.edu I. Introduction to Aggregate Demand/Aggregate Supply Model In this chapter we develop a model

The Relationship between the ROA, ROE and ROI Ratios with Jordanian Insurance Public Companies Market Share Prices

International Journal of Humanities and Social Science Vol. 2 No. 11; June 2012 The Relationship between the ROA, ROE and ROI Ratios with Jordanian Insurance Public Companies Market Share Prices Dr. Majed

International Journal of Humanities and Social Science Vol. 2 No. 11; June 2012 The Relationship between the ROA, ROE and ROI Ratios with Jordanian Insurance Public Companies Market Share Prices Dr. Majed

Big Concepts. Measuring U.S. GDP. The Expenditure Approach. Economics 202 Principles Of Macroeconomics

Lecture 6 Economics 202 Principles Of Macroeconomics Measuring GDP Professor Yamin Ahmad Real GDP and the Price Level Economic Growth and Welfare Big Concepts Ways to Measure GDP Expenditure Approach Income

Lecture 6 Economics 202 Principles Of Macroeconomics Measuring GDP Professor Yamin Ahmad Real GDP and the Price Level Economic Growth and Welfare Big Concepts Ways to Measure GDP Expenditure Approach Income

Chapter 9. The Valuation of Common Stock. 1.The Expected Return (Copied from Unit02, slide 36)

") Readings Chapters 9 and 10 Chapter 9. The Valuation of Common Stock 1. The investor s expected return 2. Valuation as the Present Value (PV) of dividends and the growth of dividends 3. The investor s required

Readings Chapters 9 and 10 Chapter 9. The Valuation of Common Stock 1. The investor s expected return 2. Valuation as the Present Value (PV) of dividends and the growth of dividends 3. The investor s required

The Effect on Housing Prices of Changes in Mortgage Rates and Taxes

Preliminary. Comments welcome. The Effect on Housing Prices of Changes in Mortgage Rates and Taxes Lars E.O. Svensson SIFR The Institute for Financial Research, Swedish House of Finance, Stockholm School

Preliminary. Comments welcome. The Effect on Housing Prices of Changes in Mortgage Rates and Taxes Lars E.O. Svensson SIFR The Institute for Financial Research, Swedish House of Finance, Stockholm School

1. Currency Exposure. VaR for currency positions. Hedged and unhedged positions

RISK MANAGEMENT [635-0]. Currency Exposure. ar for currency positions. Hedged and unhedged positions Currency Exposure Currency exposure represents the relationship between stated financial goals and exchange

RISK MANAGEMENT [635-0]. Currency Exposure. ar for currency positions. Hedged and unhedged positions Currency Exposure Currency exposure represents the relationship between stated financial goals and exchange

MEASURING A NATION S INCOME

10 MEASURING A NATION S INCOME WHAT S NEW IN THE FIFTH EDITION: There is more clarification on the GDP deflator. The Case Study on Who Wins at the Olympics? is now an FYI box. LEARNING OBJECTIVES: By the

10 MEASURING A NATION S INCOME WHAT S NEW IN THE FIFTH EDITION: There is more clarification on the GDP deflator. The Case Study on Who Wins at the Olympics? is now an FYI box. LEARNING OBJECTIVES: By the

Import Prices and Inflation

Import Prices and Inflation James D. Hamilton Department of Economics, University of California, San Diego Understanding the consequences of international developments for domestic inflation is an extremely

Import Prices and Inflation James D. Hamilton Department of Economics, University of California, San Diego Understanding the consequences of international developments for domestic inflation is an extremely

The Term Structure of Interest Rates, Spot Rates, and Yield to Maturity

Chapter 5 How to Value Bonds and Stocks 5A-1 Appendix 5A The Term Structure of Interest Rates, Spot Rates, and Yield to Maturity In the main body of this chapter, we have assumed that the interest rate

Chapter 5 How to Value Bonds and Stocks 5A-1 Appendix 5A The Term Structure of Interest Rates, Spot Rates, and Yield to Maturity In the main body of this chapter, we have assumed that the interest rate

Accrual Accounting and Valuation: Pricing Earnings

Security, Third Chapter Six LINKS Accrual Accounting and : Pricing Earnings Link to previous chapter Chapter 5 showed how to price book values in the balance sheet and calculate intrinsic price-to-book

Security, Third Chapter Six LINKS Accrual Accounting and : Pricing Earnings Link to previous chapter Chapter 5 showed how to price book values in the balance sheet and calculate intrinsic price-to-book

11.2 Monetary Policy and the Term Structure of Interest Rates

518 Chapter 11 INFLATION AND MONETARY POLICY Thus, the monetary policy that is consistent with a permanent drop in inflation is a sudden upward jump in the money supply, followed by low growth. And, in

518 Chapter 11 INFLATION AND MONETARY POLICY Thus, the monetary policy that is consistent with a permanent drop in inflation is a sudden upward jump in the money supply, followed by low growth. And, in

International Economic Relations

nternational conomic Relations Prof. Murphy Chapter 12 Krugman and Obstfeld 2. quation 2 can be written as CA = (S p ) + (T G). Higher U.S. barriers to imports may have little or no impact upon private

nternational conomic Relations Prof. Murphy Chapter 12 Krugman and Obstfeld 2. quation 2 can be written as CA = (S p ) + (T G). Higher U.S. barriers to imports may have little or no impact upon private

PROVIDENT FUNDS PROVIDENT FUNDS

PROVIDENT FUNDS 1 2 Table of contents 1. Introduction and general review...3 A) Composition of membership in benefit and severance pay provident funds...6 B) High Centralization in banks...6 2. Summary

PROVIDENT FUNDS 1 2 Table of contents 1. Introduction and general review...3 A) Composition of membership in benefit and severance pay provident funds...6 B) High Centralization in banks...6 2. Summary

ON THE RISK ADJUSTED DISCOUNT RATE FOR DETERMINING LIFE OFFICE APPRAISAL VALUES BY M. SHERRIS B.A., M.B.A., F.I.A., F.I.A.A. 1.

ON THE RISK ADJUSTED DISCOUNT RATE FOR DETERMINING LIFE OFFICE APPRAISAL VALUES BY M. SHERRIS B.A., M.B.A., F.I.A., F.I.A.A. 1. INTRODUCTION 1.1 A number of papers have been written in recent years that

ON THE RISK ADJUSTED DISCOUNT RATE FOR DETERMINING LIFE OFFICE APPRAISAL VALUES BY M. SHERRIS B.A., M.B.A., F.I.A., F.I.A.A. 1. INTRODUCTION 1.1 A number of papers have been written in recent years that

1 Define Management. Explain Mintzberg Managerial Roles. 12M

Question Paper Code :GMB11T01 MANAGEMENT AND ORGANIZATIONAL BEHAVI0R 1 Define Management. Explain Mintzberg Managerial Roles. 2 Define Social Responsibility. Explain the Arguments for and against Social

Question Paper Code :GMB11T01 MANAGEMENT AND ORGANIZATIONAL BEHAVI0R 1 Define Management. Explain Mintzberg Managerial Roles. 2 Define Social Responsibility. Explain the Arguments for and against Social

Lina Warrad. Applied Science University, Amman, Jordan

Journal of Modern Accounting and Auditing, March 2015, Vol. 11, No. 3, 168-174 doi: 10.17265/1548-6583/2015.03.006 D DAVID PUBLISHING The Effect of Net Working Capital on Jordanian Industrial and Energy

Journal of Modern Accounting and Auditing, March 2015, Vol. 11, No. 3, 168-174 doi: 10.17265/1548-6583/2015.03.006 D DAVID PUBLISHING The Effect of Net Working Capital on Jordanian Industrial and Energy

Effects of Inflation Unanticipated Inflation in the Labor Market

Effects of Inflation Unanticipated Inflation in the Labor Market Unanticipated inflation has two main consequences in the labor market: Redistribution of income Departure from full employment Effects of

Effects of Inflation Unanticipated Inflation in the Labor Market Unanticipated inflation has two main consequences in the labor market: Redistribution of income Departure from full employment Effects of

Chapter 9. The IS-LM/AD-AS Model: A General Framework for Macroeconomic Analysis. 2008 Pearson Addison-Wesley. All rights reserved

Chapter 9 The IS-LM/AD-AS Model: A General Framework for Macroeconomic Analysis Chapter Outline The FE Line: Equilibrium in the Labor Market The IS Curve: Equilibrium in the Goods Market The LM Curve:

Chapter 9 The IS-LM/AD-AS Model: A General Framework for Macroeconomic Analysis Chapter Outline The FE Line: Equilibrium in the Labor Market The IS Curve: Equilibrium in the Goods Market The LM Curve:

Tracking the Macroeconomy

chapter 7(23) Tracking the Macroeconomy Chapter Objectives Students will learn in this chapter: How economists use aggregate measures to track the performance of the economy. What gross domestic product,

chapter 7(23) Tracking the Macroeconomy Chapter Objectives Students will learn in this chapter: How economists use aggregate measures to track the performance of the economy. What gross domestic product,

University of Lethbridge Department of Economics ECON 1012 Introduction to Microeconomics Instructor: Michael G. Lanyi. Chapter 29 Fiscal Policy

University of Lethbridge Department of Economics ECON 1012 Introduction to Microeconomics Instructor: Michael G. Lanyi Chapter 29 Fiscal Policy 1) If revenues exceed outlays, the government's budget balance

University of Lethbridge Department of Economics ECON 1012 Introduction to Microeconomics Instructor: Michael G. Lanyi Chapter 29 Fiscal Policy 1) If revenues exceed outlays, the government's budget balance

Masters in Money, Banking and Finance

Masters in Money, Banking and Finance Taught Element: Compulsory modules 100 credits: EC5605, EC5608, EC5609, EC5801, EC5901 Optional modules 20 credits from: EC5225, EC5606, EC5610, EC5611, EC5722 MSc:

Masters in Money, Banking and Finance Taught Element: Compulsory modules 100 credits: EC5605, EC5608, EC5609, EC5801, EC5901 Optional modules 20 credits from: EC5225, EC5606, EC5610, EC5611, EC5722 MSc:

Edmonds Community College Macroeconomic Principles ECON 202C - Winter 2011 Online Course Instructor: Andy Williams

Edmonds Community College Macroeconomic Principles ECON 202C - Winter 2011 Online Course Instructor: Andy Williams Textbooks: Economics: Principles, Problems and Policies, 18th Edition, by McConnell, Brue,

Edmonds Community College Macroeconomic Principles ECON 202C - Winter 2011 Online Course Instructor: Andy Williams Textbooks: Economics: Principles, Problems and Policies, 18th Edition, by McConnell, Brue,

Programme Curriculum for Master Programme in Finance

Programme Curriculum for Master Programme in Finance 1. Identification Name of programme Scope of programme Level Programme code Master Programme in Finance 60 ECTS Master level Decision details Board

Programme Curriculum for Master Programme in Finance 1. Identification Name of programme Scope of programme Level Programme code Master Programme in Finance 60 ECTS Master level Decision details Board

Untangling F9 terminology

Untangling F9 terminology Welcome! This is not a textbook and we are certainly not trying to replace yours! However, we do know that some students find some of the terminology used in F9 difficult to understand.

Untangling F9 terminology Welcome! This is not a textbook and we are certainly not trying to replace yours! However, we do know that some students find some of the terminology used in F9 difficult to understand.

EQUITY MARKET RISK PREMIUMS IN THE U.S. AND CANADA

CANADA U.S. BY LAURENCE BOOTH EQUITY MARKET RISK PREMIUMS IN THE U.S. AND CANADA The bond market has recently been almost as risky as the equity markets. In the Spring 1995 issue of Canadian Investment

CANADA U.S. BY LAURENCE BOOTH EQUITY MARKET RISK PREMIUMS IN THE U.S. AND CANADA The bond market has recently been almost as risky as the equity markets. In the Spring 1995 issue of Canadian Investment

Determining the cost of equity

Determining the cost of equity Macroeconomic factors and the discount rate Baring Asset Management Limited 155 Bishopsgate London EC2M 3XY Tel: +44 (0)20 7628 6000 Fax: +44 (0)20 7638 7928 www.barings.com

Determining the cost of equity Macroeconomic factors and the discount rate Baring Asset Management Limited 155 Bishopsgate London EC2M 3XY Tel: +44 (0)20 7628 6000 Fax: +44 (0)20 7638 7928 www.barings.com

The Lee Kong Chian School of Business Academic Year 2015 /16 Term 1

The Lee Kong Chian School of Business Academic Year 2015 /16 Term 1 FNCE101 FINANCE Instructor : Dr Chiraphol New Chiyachantana Tittle : Assistant Professor of Finance (Education) Tel : 6828 0776 Email

The Lee Kong Chian School of Business Academic Year 2015 /16 Term 1 FNCE101 FINANCE Instructor : Dr Chiraphol New Chiyachantana Tittle : Assistant Professor of Finance (Education) Tel : 6828 0776 Email

The Conversion of Cooperatives to Publicly Held Corporations: A Financial Analysis of Limited Evidence

The Conversion of Cooperatives to Publicly Held Corporations: A Financial Analysis of Limited Evidence Robert A. Collins Recent reorganizations of agricultural cooperatives have created concern that the

The Conversion of Cooperatives to Publicly Held Corporations: A Financial Analysis of Limited Evidence Robert A. Collins Recent reorganizations of agricultural cooperatives have created concern that the

Masters in Financial Economics (MFE)

") Masters in Financial Economics (MFE) Admission Requirements Candidates must submit the following to the Office of Admissions and Registration: 1. Official Transcripts of previous academic record 2. Two

Masters in Financial Economics (MFE) Admission Requirements Candidates must submit the following to the Office of Admissions and Registration: 1. Official Transcripts of previous academic record 2. Two

The Master of Science in Finance (English Program) - MSF. Department of Banking and Finance. Chulalongkorn Business School. Chulalongkorn University

- MSF. Department of Banking and Finance. Chulalongkorn Business School. Chulalongkorn University") The Master of Science in Finance (English Program) - MSF Department of Banking and Finance Chulalongkorn Business School Chulalongkorn University Overview of Program Structure Full Time Program: 1 Year

The Master of Science in Finance (English Program) - MSF Department of Banking and Finance Chulalongkorn Business School Chulalongkorn University Overview of Program Structure Full Time Program: 1 Year

Chapter 6 The Tradeoff Between Risk and Return

Chapter 6 The Tradeoff Between Risk and Return MULTIPLE CHOICE 1. Which of the following is an example of systematic risk? a. IBM posts lower than expected earnings. b. Intel announces record earnings.

Chapter 6 The Tradeoff Between Risk and Return MULTIPLE CHOICE 1. Which of the following is an example of systematic risk? a. IBM posts lower than expected earnings. b. Intel announces record earnings.

Paper F9. Financial Management. Friday 6 June 2014. Fundamentals Level Skills Module. The Association of Chartered Certified Accountants.

Fundamentals Level Skills Module Financial Management Friday 6 June 2014 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Fundamentals Level Skills Module Financial Management Friday 6 June 2014 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

CHAPTER 3 THE LOANABLE FUNDS MODEL

CHAPTER 3 THE LOANABLE FUNDS MODEL The next model in our series is called the Loanable Funds Model. This is a model of interest rate determination. It allows us to explore the causes of rising and falling

CHAPTER 3 THE LOANABLE FUNDS MODEL The next model in our series is called the Loanable Funds Model. This is a model of interest rate determination. It allows us to explore the causes of rising and falling

ON THE DEATH OF THE PHILLIPS CURVE William A. Niskanen

ON THE DEATH OF THE PHILLIPS CURVE William A. Niskanen There is no evidence of a Phillips curve showing a tradeoff between unemployment and inflation. The function for estimating the nonaccelerating inflation

ON THE DEATH OF THE PHILLIPS CURVE William A. Niskanen There is no evidence of a Phillips curve showing a tradeoff between unemployment and inflation. The function for estimating the nonaccelerating inflation

I.e., the return per dollar from investing in the shares from time 0 to time 1,

XVII. SECURITY PRICING AND SECURITY ANALYSIS IN AN EFFICIENT MARKET Consider the following somewhat simplified description of a typical analyst-investor's actions in making an investment decision. First,

XVII. SECURITY PRICING AND SECURITY ANALYSIS IN AN EFFICIENT MARKET Consider the following somewhat simplified description of a typical analyst-investor's actions in making an investment decision. First,

7 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Chapter. Key Concepts

Chapter 7 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Key Concepts Aggregate Supply The aggregate production function shows that the quantity of real GDP (Y ) supplied depends on the quantity of labor (L ),

Chapter 7 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Key Concepts Aggregate Supply The aggregate production function shows that the quantity of real GDP (Y ) supplied depends on the quantity of labor (L ),

Pricing Forwards and Futures

Pricing Forwards and Futures Peter Ritchken Peter Ritchken Forwards and Futures Prices 1 You will learn Objectives how to price a forward contract how to price a futures contract the relationship between

Pricing Forwards and Futures Peter Ritchken Peter Ritchken Forwards and Futures Prices 1 You will learn Objectives how to price a forward contract how to price a futures contract the relationship between

THE INFLUENCE OF CASH FLOW ON THE RESEARCH AND DEVELOPMENT INVESTING DECISION

THE INFLUENCE OF CASH FLOW ON THE RESEARCH AND DEVELOPMENT INVESTING DECISION Author: Sabina Raluca Radu Coordinator: Univ. Prof. Dr. Laura Obreja Brasoveanu Abstract This paper attempts to explore the

THE INFLUENCE OF CASH FLOW ON THE RESEARCH AND DEVELOPMENT INVESTING DECISION Author: Sabina Raluca Radu Coordinator: Univ. Prof. Dr. Laura Obreja Brasoveanu Abstract This paper attempts to explore the

On the long run relationship between gold and silver prices A note

Global Finance Journal 12 (2001) 299 303 On the long run relationship between gold and silver prices A note C. Ciner* Northeastern University College of Business Administration, Boston, MA 02115-5000,

Global Finance Journal 12 (2001) 299 303 On the long run relationship between gold and silver prices A note C. Ciner* Northeastern University College of Business Administration, Boston, MA 02115-5000,

Primary Market - Place where the sale of new stock first occurs. Initial Public Offering (IPO) - First offering of stock to the general public.

- First offering of stock to the general public.") Stock Valuation Primary Market - Place where the sale of new stock first occurs. Initial Public Offering (IPO) - First offering of stock to the general public. Seasoned Issue - Sale of new shares by a

Stock Valuation Primary Market - Place where the sale of new stock first occurs. Initial Public Offering (IPO) - First offering of stock to the general public. Seasoned Issue - Sale of new shares by a