Outlook for U.S. Agricultural Trade

|

|

|

- Leon Page

- 8 years ago

- Views:

Transcription

1 Electronic Outlook Report from USDA s Economic Research Service and Foreign Agricultural Service United States Department of Agriculture AES-85 February 19, 2015 Outlook for U.S. Agricultural Trade FY 2015 Exports Forecast Down $11 Billion From Record; Imports at a Record $119 Billion Contents Economic Outlook Export Products Regional Exports Import Products Regional Imports Contact Information Tables Macro Trends Commodity Exports Regional Exports Commodity Imports Regional Imports Reliability Tables Web Sites U.S. Trade Data Fiscal 2015 agricultural exports are forecast at $141.5 billion, down $2.0 billion from the November forecast and $11.0 billion from fiscal Most of the decline from the last forecast is a result of lower exports of high-value products (non-bulk), especially livestock, poultry and dairy, as well as horticultural products. The forecast for livestock, poultry and dairy is down $1.9 billion on lower expected exports of pork, poultry, dairy and hides and skins. Exports of horticultural products are lowered $1.0 billion primarily due to smaller-than-expected shipments of tree nuts and fresh fruits and vegetables. Cotton exports are unchanged this month. Oilseed exports are raised $1.2 billion due to very strong sales and shipments of soybeans and soybean meal. The grain and feed export forecast is unchanged, as higher coarse grain exports offset lower wheat and rice exports. U.S. agricultural imports are forecast at a record $119.0 billion, up $3.0 billion from November, and $10.0 billion higher than in fiscal The U.S. agricultural trade surplus is forecast at $22.5 billion, down from $43.3 billion in fiscal 2014, and the smallest surplus since fiscal FAQ & Summary Data Articles on U.S. Trade The next release is May 28, 2015 Approved by the World Agricultural Outlook Board.

2 Economic Economic Outlook Outlook Dollar Up Sharply, Oil Prices Down, World Growth Up in 2015 World economic growth is expected to accelerate from 2.6.percent in 2014 to 3.1 percent in 2015, driven by faster economic growth in North America and continued solid growth in Developing Asia. The JP Morgan real effective dollar index averaged 99 in January 2015 a level last exceeded in April The real dollar in 2015 is expected to rise by more than 6 percent over 2014 the fastest appreciation since Since August, the dollar has appreciated significantly in the largest U.S. agricultural export markets. For example, it has appreciated almost 13 percent against the euro and 15 percent against the yen. The dollar has also strengthened relative to other competitors, by 15 percent against the Brazilian real and 12 percent against the Canadian dollar. Notably, the dollar s value is expected to fall 3.4 percent in real terms relative to the Argentine peso in 2015, based on recent trends. The dollar s appreciation of recent months reflects the relatively strong and stable U.S. economy and expected central bank policies over the next year. Political instability along with economic weakness and uncertainty due to geopolitical events in Europe, Japan, China and Latin America makes the United States a relatively attractive destination for investors around the world, increasing the value of the dollar. Recent interest rate cuts in many countries add to the attractiveness of the United States as a destination for financial and business investment. These trends are expected to continue, and along with increases in U.S. interest rates expected in late 2015, support our forecast of continued dollar strength through The dollar s strength is expected to be a significant damper on U.S. export growth into Movements in exchange rates are a leading driver of movements in U.S. exports, since they are a key determinant of the relative price of U.S. agricultural products in global markets. ERS research has demonstrated that, while long-term growth in agricultural exports is largely driven by growth in foreign income, changes in exchange rates are the primary factors determining year-to-year variation in exports. While the dollar value is high relative to recent history, it remains well below the highs of the early 2000 s. After a period of relatively consistent strengthening beginning in the early 1990 s, the agricultural trade-weighted dollar depreciated more than 20 percent between 2002 and 2011, supporting record agricultural export growth between 2010 and However, lower energy prices and stronger world growth will mitigate the impact of a strengthening dollar on U.S. agriculture. Higher North American and Iraqi supplies are principally responsible for the downward pressure on oil prices in The expansion in North American oil supply leading to the recent sharp drop in crude oil prices is likely to continue at a slower pace into Due to bottlenecks in the U.S. energy refining and transport system, U.S. prices for crude oil and natural gas are expected to continue to be below world levels in The U.S. energy infrastructure situation and stronger dollar is expected to provide U.S. oil refiners, farmers, manufacturers, fertilizer producers, and farm product exporters a lower cost environment in Due to improved world growth and low energy and commodity prices overall, global trade volume is forecasted to grow about 4 percent in Low U.S. energy costs, expanding international trade, and improved world growth are expected to mute the 2 Economic Research Service, U.S.DA

3 overall domestic economic impact of falling U.S. agricultural exports in Brent crude oil peaked in June at $112 per barrel falling to $63 in December. The futures market for Brent crude implies that the 2015 average crude price will be lowest since Gross domestic product (GDP) in Asia and Oceania minus Japan is expected to grow over 5 percent in Japan and Europe are expected to avoid recession and deflation as easing credit conditions support domestic demand and export expansion. China s structural reforms to enhance long-term growth such as those underway in banking will slow growth to 6.5 percent in Loosening credit, low oil prices, and a weak yuan will slow the effective pace of reform but support 2015 GDP growth. India will likely get a large boost from low oil prices enabling them to surpass China s growth rate in late For both economies, the reforms to reorient industrial production and services to serve domestic consumers will have no net impact on 2015 s GDP. Growth in the rest of South and Southeast Asia is expected to also be strong in 2015 despite widespread potential medium term problems with debt and inflation. Overall, economic growth in North America is projected to improve through In the United States, strong labor market indicators in late 2014 and early 2015 point to more jobs and rising wages through 2015, lifting consumer spending. As a result, both housing and business investment will respond favorably. Business and consumer credit conditions are expected to continue to ease, even as short-term interest rates are likely to rise modestly in late A stronger U.S. economy in 2015 boosts the growth environment for Canadian and Mexican exports. Lower oil and commodity prices in 2015 should moderate the gains in these economies from higher export volumes as oil and gas revenues fall in The recessions in Argentina, Brazil and Venezuela will slow growth in South America in Europe is expected to grow faster in 2015 as consumer and business spending modestly recovers. However, the expected 1.7-percent growth in 2015 is still a drag on world growth. Expected strong U.S. growth and the associated rising imports and falling oil prices provide insurance against a world recession in Nevertheless, a debt default by Greece or a spillover of current geopolitical events to neighboring countries could trigger a world growth slowdown and a sharp rise in the dollar, hurting U.S. farm exports. A large emerging economy such as Venezuela defaulting on its debt would likely cause significant capital outflows out of other countries. Global growth would slow due to effects on world trade and financial markets and a flight to the safety of the dollar. 3 Economic Research Service, U.S.DA

4 4 Economic Research Service, U.S.DA

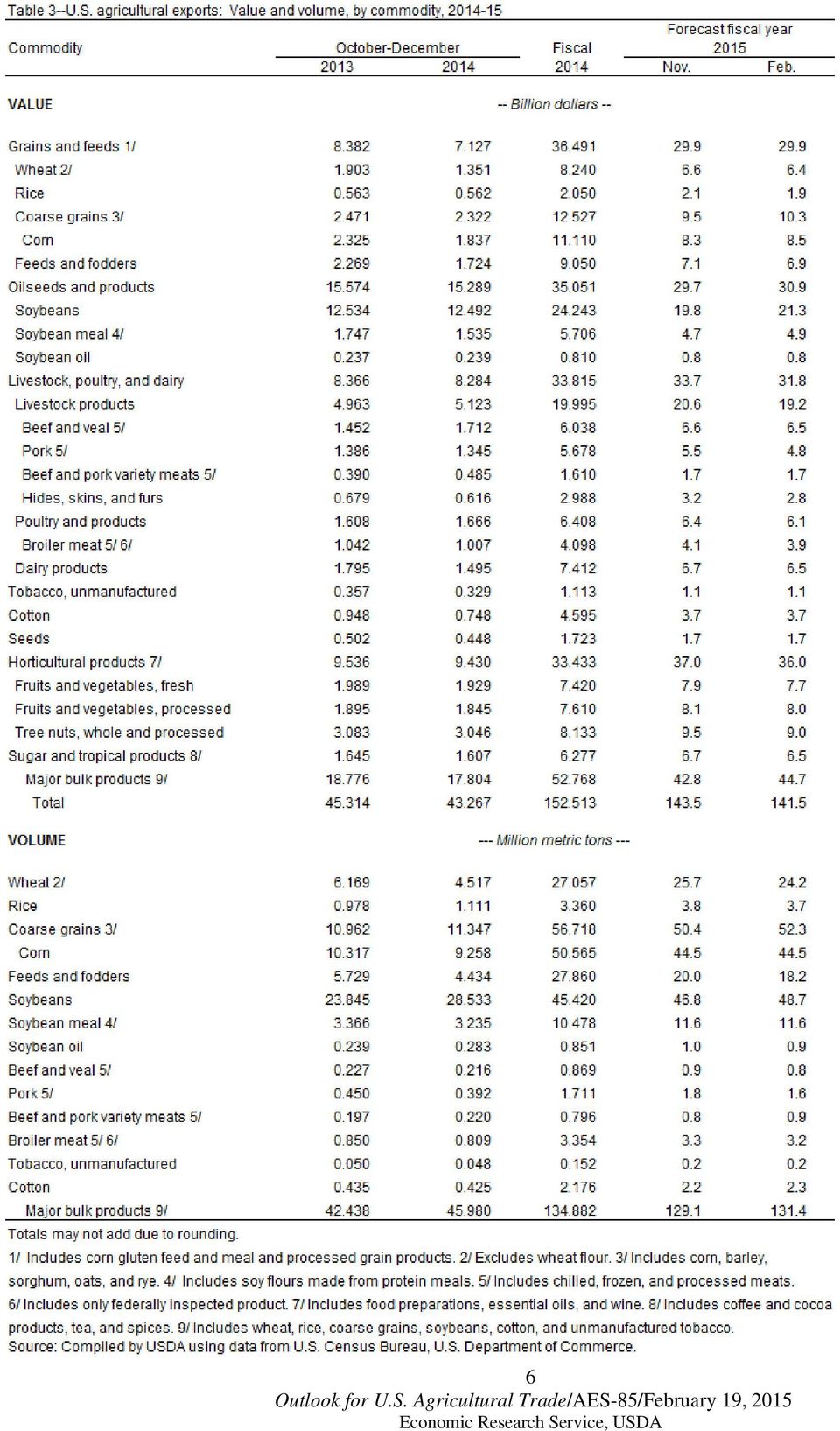

5 Export Products Fiscal year 2015 grain and feed exports are forecast at $29.9 billion. This is unchanged from the November estimate and occurs despite changes in most categories. Coarse grain exports are forecast at $10.3 billion, up $800 million, led mostly by higher sorghum volumes and values. Sorghum shipments are forecast at 7.5 million tons, the highest in nearly 25 years, resulting from continued strong purchases by China. Corn volume is unchanged at 44.5 million tons, but the unit value is raised slightly reflecting firmer prices with tighter supplies. Feeds and fodders are down $200 million as higher unit values for distiller s dried grains with solubles (DDGS) and other products are more than offset by slightly lower volumes. Wheat is forecast at $6.4 billion, down $200 million on lower volume, which more than offsets slightly higher unit values. Abundant competitor supplies continue to constrain export opportunities. Expectations for large global production in 2015/16 limit prospects for early season exports. Rice exports are forecast at $1.9 billion, down $200 million from November. Large global supplies continue to weigh on prices lowering unit values, while volumes are reduced due to greater competition in Africa and the Middle East from Asian exporters. Oilseed and product exports are forecast at $30.9 billion, up $1.2 billion from the November forecast. Soybeans and soybean meal continue to ship at a record pace, buoyed by strong demand and minimal competition from South America. This has kept unit values stronger than expected. Partially offsetting these gains are reductions in soybean oil and other oilseeds where reduced export volumes and weaker unit values prevail, in part due to falling petroleum prices. Fiscal 2015 cotton exports are forecast at $3.7 billion, unchanged from the November estimate. Export volume is forecast up 100,000 tons to 2.3 million, despite a smaller crop than previously expected as U.S. exports capture a rising share of world trade. Unit values are reduced due to expected lower world consumption pushing world prices down. Fiscal 2015 livestock, poultry, and dairy exports are reduced $1.9 billion to $31.8 billion as fewer shipments are expected for beef, pork, poultry, and dairy. Beef is lowered $100 million to $6.5 billion on weaker demand due to higher U.S. prices and a stronger dollar. Pork is forecast down $700 million to $4.8 billion as a strong dollar reduces competitiveness, more than offsetting the impact of a moderation in prices. Poultry and products are cut $300 million to $6.1 billion due to weaker prices and demand. Dairy is reduced $200 million to $6.5 billion as global prices remain weak and the strong U.S. dollar makes exports less competitive. Fiscal 2015 horticultural product exports are forecast at $36.0 billion, down $1.0 billion from the November forecast. Fresh fruit and vegetable exports are forecast at $7.7 billion, down $200 million from November on lower fruit shipments to Canada, Japan and Hong Kong as well as reduced vegetable exports to Mexico. Processed fruit and vegetable exports are forecast at $8.0 billion, down $100 million from November due to reduced dried fruit exports to Europe. Whole and processed tree nuts are forecast at $9.0 billion, down $500 million from November as demand in Europe and China slows. 5

6 6

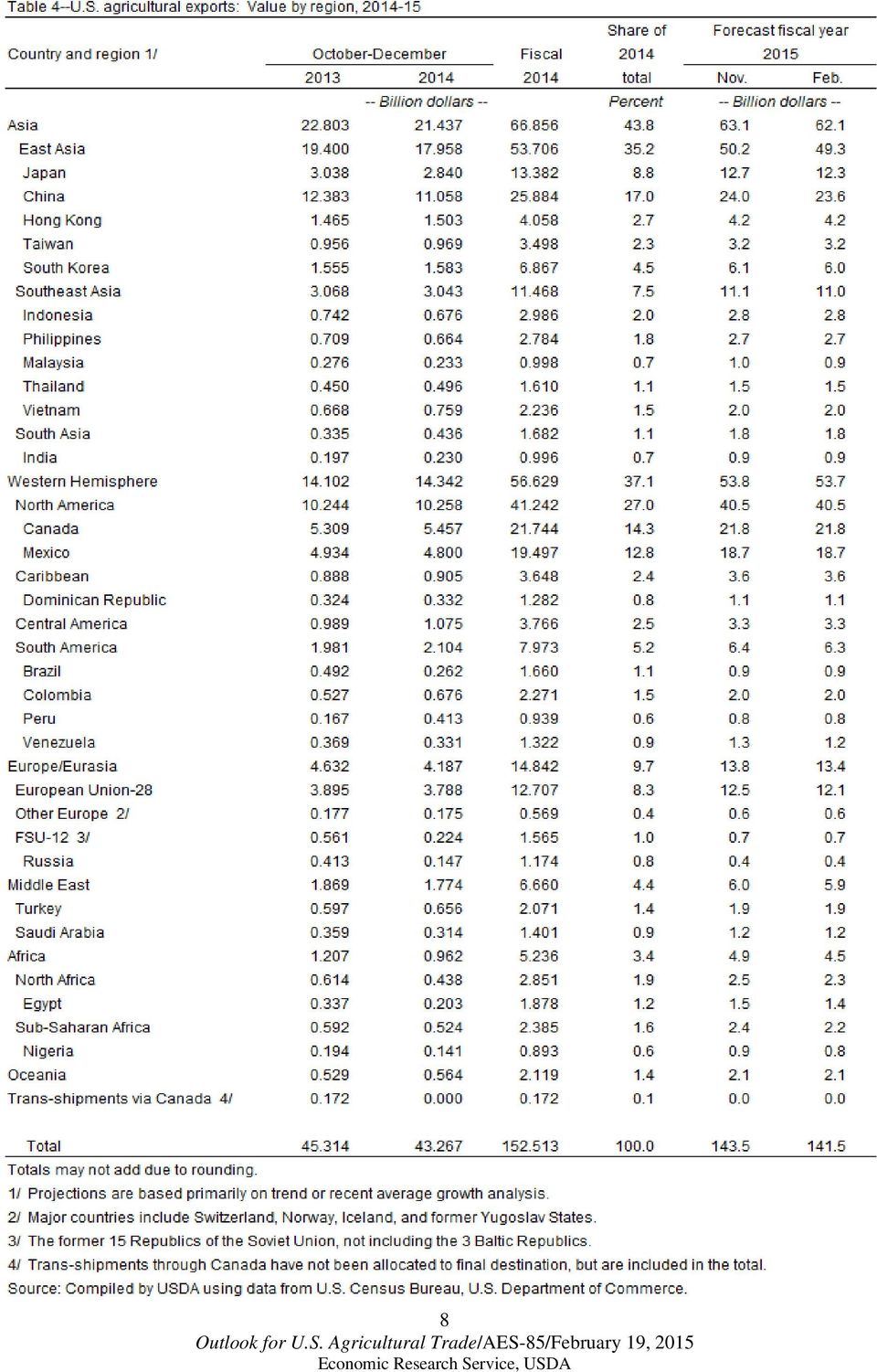

7 Regional Exports Agricultural exports in fiscal 2015 are forecast at $141.5 billion, which is $2.0 billion below the November forecast and $11 billion below the record fiscal 2014 exports. The forecast is down primarily due to Japan, China and the European Union, and is also impacted by the stronger dollar. Asia Exports to China are forecast down $400 million to $23.6 billion. This decline is primarily a result of weaker U.S. exports of hides and skins (of which China accounts for half of all U.S. shipments), as well as softening Chinese demand for U.S. pork, poultry and dairy products. U.S. exports of most horticultural products (especially tree nuts) to China have also slowed. However, exports and sales of soybeans to China have continued to be very strong, as well as a very large increase in sales of sorghum. U.S. agricultural exports to China in the first quarter of fiscal year 2015 (October-December) were down $1.3 billion compared to the same period last year. China is still forecast to remain the largest global export market for U.S. agricultural products. Japan is down $400 million to $12.3 billion as a result of expected lower U.S. shipments of pork and beef (Japan is the largest U.S. market for both of these products). Exports to South Korea are down $100 million to $6.0 billion on weaker demand for U.S. pork and poultry. Malaysia is also down $100 million to $900 million. Western Hemisphere Canada is unchanged as stronger sales of soybeans and corn are expected to offset expected weaker export values of livestock products. Europe, Africa, and the Middle East Exports to the European Union are down $400 million to $12.1 billion as demand, especially for U.S. horticultural products, is expected to weaken due to the stronger dollar. Exports to North Africa are down $200 million to $2.3 billion (including Egypt, which is down $100 million to $1.4 billion) because of a sluggish early-season pace of U.S. exports, especially of dairy in light of increased competition from the European Union. Exports to Sub-Saharan Africa are also down $200 million to $2.2 billion and exports to the Middle East are down $100 million to $5.9 billion. 7

to China have also slowed.")

8 8

9 Import Products Import unit values in the first quarter of fiscal year 2015 were up 10 percent on average, boosting U.S. agricultural import value by 10 percent with volume growth of only 0.3 percent from The stronger domestic economy, which is reflected in the average 2.9-percent growth in real disposable personal income during the last half of 2014 and 3.1 percent for the whole of 2014, is expected to boost import demand for food and other farm products. The last U.S. agricultural import projection of $116 billion for 2015 is raised $3 billion to $119 billion, representing 9 percent more imports than in Prices for imported commodities are expected to stabilize based partly on the dollar s strength, lower fuel prices, and because of relatively slower economic growth in the rest of the world. The volatility of tropical commodity prices from 2012 to 2014, including vegetable oil prices, makes it difficult to estimate the value of U.S. tropical imports (except horticulture crops), which comprise about a quarter of total U.S. import value. Higher prices for coffee beans, cocoa beans, and coconut oil in 2014 contrast with lower prices for sugar (compared to 2012), palm oil, and rubber. Since most of these traded commodities are priced in dollars, the dollar s appreciation reduces their prices in terms of foreign currencies and limits their price volatility. While these commodities source supply conditions influence their export price fluctuations, generally weaker import demand in major global markets dampens any sharp price swings. Imports of sugar and tropical products are projected to climb to $26.6 billion in 2015 from $23.2 billion in 2014, a 15-percent expansion. Led by coffee beans, cocoa beans, and sugar products, these tropical imports growth accounts for 34 percent of the projected $9.8 billion additional total U.S. agricultural import value from More stable prices for tropical oils, which account for 35 percent of U.S. vegetable oil imports, will keep total vegetable oil import value at around $5.4 billion, the same level as in 2014 despite higher prices for imported olive oil. However, imported oilseeds and other oilseed products, estimated at $4.3 billion in 2015, will be lower than in 2014 because of their lower average prices. Prices for horticultural crops and products are not as volatile as tropical commodity prices and their annual import growth rates have been more consistent. Part of the reason for this contrast is the dominant role of NAFTA partners Mexico and Canada as well as the European Union as principal sources of U.S. horticulture imports, together accounting for 61 percent of total import value. More advanced agricultural infrastructure and less weather-related disruptions in these countries contribute to highly reliable supply conditions. For tropical imports such as coffee beans, cocoa beans, sugar, rubber, and spices, supply from Mexico, Canada, and the EU account for only a third of total value, and the rest of suppliers are distributed widely around the world. These tropical crops are more vulnerable to changes in weather and yield which lead to sharp price swings. The combined $7.8 billion import increase of these two groups in 2015 account for 80 percent of the total $9.8 billion projected increase in U.S. agricultural imports. US imports of fresh fruits are projected to exceed $10 billion for the first time. This amount exceeds imports of oilseeds and products, and is just under the import value for grains and feeds. Led by bananas, avocados, and grapes, demand for these fresh fruits is driven by higher consumer incomes and healthier diets. The value of 9 Economic Research Service, U.S.DA

10 imported fresh vegetables is also expected to reach a record high of $7.5 billion in Led by tomatoes and bell peppers, a good portion of these vegetables are grown in greenhouses, enhancing their quality and reducing price volatility. In contrast, imported coffee beans, which are projected to also exceed $7 billion in 2015, are grown in open fields in various countries where yields can vary widely between years and between suppliers, making prices less predictable. Cattle and calve imports in 2015 are projected to increase by $440 million from $2.2 billion in 2014 to $2.6 billion in Demand for cattle is expected to remain strong as domestic herd recovery continues. However, smaller inventories in Canada and Mexico will limit import growth. Beef imports are raised on strong demand for processing-type beef. Greater pork production and lower domestic prices will also limit pork imports in 2015 as well as swine imports. Despite lower expected dairy product prices, a strong dollar will support demand for dairy products. Although bulk grain imports are projected to be lower in 2015 because of ample domestic supply, imported grain products and feeds have higher initial-year volumes than in 2014 since import unit values are lower. The import estimate for processed grain products in 2015 is $6.9 billion, up $400 million from For feeds and fodder, imports are anticipated to climb $200 million to $1.8 billion in The situation for oilseeds and products is not unlike that of grains and feeds where large domestic supplies will reduce import volumes for oilseeds and oilmeal. For vegetable oils, however, diminished beginning stocks in 2015, larger export shipments, and lower import unit values for rapeseed, palm, and olive oils together encourage a bigger import quantity in Economic Research Service, U.S.DA

11 11

12 Regional Imports During the first quarter of fiscal 2015, the imports that registered the largest gains include livestock and meat products led by beef, pork, and cattle. Beef and veal are mostly shipped from Australia, Canada, New Zealand, and Mexico. Top pork sources include Canada, Denmark, Italy, and Poland. Cattle are shipped mainly from Canada and Mexico, attributed to lower transport costs. Horticulture products also posted large import gains led by Mexico, the European Union, Canada, China, and Chile. Vegetables and fruits are shipped from Mexico; wine, beer, and essential oils come from Europe; vegetables from Canada and China; and fruits from Chile, China, and Canada. The dollar s higher exchange rate will foster competition among these suppliers based more on prices. Among the top 20 sources of U.S. agricultural imports that have rising market shares are Vietnam, Peru, and the Philippines with $1.8, $1.6, and $1.1 billion in import values, respectively in Vietnam s top shipments include tree nuts, largely cashews, coffee beans, and spices. From Peru are vegetables, fruits, and coffee. The Philippines shipped coconut oil, fruits, and other coconut products. In recent years, these countries have grabbed US market share from Malaysia, Costa Rica, and Colombia. While commodity price fluctuations influence these relative market shares, the long-term trend in capturing a larger share of the US market favors developing countries at the expense of developed countries over the past decade. 12

13 13

14 Reliability Tables 14

15 15

16 16

17 17

18 Contact Information Forecast Coordinators (area code 202) Exports: Levin Flake/FAS, , Imports: Andy Jerardo/ERS, , Commodity Specialist Contacts (area code 202) Grains and Feeds: Coarse Grains: Edward W. Allen/ERS, Richard O Meara/FAS, Wheat: Olga Liefert/ERS, Teresa McKeivier/FAS, Rice: Nathan Childs/ERS, Yoonhee Macke /FAS, Oilseeds: Mark Ash/ERS, Bill George/FAS, Cotton: James Johnson/FAS, Leslie Meyer/ERS, Livestock, Poultry & Dairy Products: Beef & Cattle: Lindsay Kuberka /FAS, Pork & Hogs: Claire Mezoughem /FAS, Poultry: Dave Harvey/ERS, Joanna Hitchner/FAS, Dairy Products: Paul Kiendl/FAS, Horticultural & Tropical Products: Deciduous Fresh Fruit: Elaine Protzman/FAS, Fresh Citrus: Reed Blauer/FAS, Vegetables & Preparations: Tony Halstead/FAS, Tree Nuts: Tony Halstead/FAS, Sugar and Tropical Products: Reed Blauer/FAS, Sugar: Ron Lord/FAS, Macroeconomics Contact (area code 202) Davide Torgerson/ERS, , dtorg@ers.usda.gov Kari Heerman/ERS, , keheerman@ers.usda.gov Publication Coordinator (area code 202) Stephen MacDonald/ERS, , stephenm@ers.usda.gov Bryce Cooke/ERS, , bryce.cooke@ers.usda.gov Related Websites Outlook for U.S. Agricultural Trade Foreign Agricultural Service homepage: Economic Research Service homepage: U.S.Trade Data: FAQ & Summary Data: The U.S. Department of Agriculture (USDA) prohibits discrimination in all its programs and activities on the basis of race, color, national origin, age, disability, and, where applicable, sex, marital status, familial status, parental status, religion, sexual orientation, genetic information, political beliefs, reprisal, or because all or a part of an individual s income is derived from any public assistance program. (Not all prohibited bases apply to all programs.) Persons with disabilities who require alternative means for communication of program information (Braille, large print, audiotape, etc.) should contact USDA s TARGET Center at (202) (voice and TDD). To file a complaint of discrimination write to USDA, Director, Office of Civil Rights, 1400 Independence Avenue, S.W., Washington, D.C or call (800) (voice) or (202) (TDD). USDA is an equal opportunity provider and employer. Notification Readers of ERS outlook reports have two ways they can receive an e- mail notice about release of reports and associated data. Receive timely notification (soon after the report is posted on the web) via USDA s Economics, Statistics and Market Information System (which is housed at Cornell University s Mann Library). Go to ll.edu/mannusda/aboute mailservice.do and follow the instructions to receive notices about ERS, Agricultural Marketing Service, National Agricultural Statistics Service, and World Agricultural Outlook Board products. Receive weekly notification (on Friday afternoon) via the ERS website. Go to Updates/ and follow the instructions to receive notices about ERS Outlook reports, Amber Waves magazine, and other reports and data products on specific topics. ERS also offers RSS (really simple syndication) feeds for all ERS products. Go to rss/ to get started. 18

U.S. Agriculture and International Trade

Curriculum Guide I. Goals and Objectives A. Understand the importance of exports and imports to agriculture and how risk management is affected. B. Understand factors causing exports to change. C. Understand

Curriculum Guide I. Goals and Objectives A. Understand the importance of exports and imports to agriculture and how risk management is affected. B. Understand factors causing exports to change. C. Understand

USDA Agricultural Projections to 2025

United States Department of Agriculture Office of the Chief Economist World Agricultural Outlook Board Long-term Projections Report OCE-2016-1 February 2016 USDA Agricultural Projections to 2025 Interagency

United States Department of Agriculture Office of the Chief Economist World Agricultural Outlook Board Long-term Projections Report OCE-2016-1 February 2016 USDA Agricultural Projections to 2025 Interagency

Outlook for the 2013 U.S. Farm Economy

Outlook for the 213 U.S. Farm Economy Kevin Patrick Farm and Rural Business Branch Resource and Rural Economics Division Highlights Net farm income in 213 forecast: $128.2 billion Net cash income in 213

Outlook for the 213 U.S. Farm Economy Kevin Patrick Farm and Rural Business Branch Resource and Rural Economics Division Highlights Net farm income in 213 forecast: $128.2 billion Net cash income in 213

OILSEEDS AND OILSEED PRODUCTS

3. COMMODITY SNAPSHOTS OILSEEDS AND OILSEED PRODUCTS Market situation Global oilseeds production in the 214 marketing year (see glossary for a definition of marketing year) reached record levels for the

3. COMMODITY SNAPSHOTS OILSEEDS AND OILSEED PRODUCTS Market situation Global oilseeds production in the 214 marketing year (see glossary for a definition of marketing year) reached record levels for the

Canadian Agricultural Outlook

2015 Canadian Agricultural Outlook Information contained in this report is current as of February 11, 2015. Her Majesty the Queen in Right of Canada, represented by the Minister of Agriculture and Agri-Food,

2015 Canadian Agricultural Outlook Information contained in this report is current as of February 11, 2015. Her Majesty the Queen in Right of Canada, represented by the Minister of Agriculture and Agri-Food,

Short-Term Fertilizer Outlook 2014 2015

A/14/140b November 2014 IFA Strategic Forum Marrakech (Morocco), 19-20 November 2014 Short-Term Fertilizer Outlook 2014 2015 Patrick Heffer and Michel Prud homme International Fertilizer Industry Association

A/14/140b November 2014 IFA Strategic Forum Marrakech (Morocco), 19-20 November 2014 Short-Term Fertilizer Outlook 2014 2015 Patrick Heffer and Michel Prud homme International Fertilizer Industry Association

Wheat Transportation Profile

Wheat Transportation Profile Agricultural Marketing Service / Transportation and Marketing Programs November 2014 Marina R. Denicoff Marvin E. Prater Pierre Bahizi Executive Summary America s farmers depend

Wheat Transportation Profile Agricultural Marketing Service / Transportation and Marketing Programs November 2014 Marina R. Denicoff Marvin E. Prater Pierre Bahizi Executive Summary America s farmers depend

U.S. Trade Overview, 2013

U.S. Trade Overview, 213 Stephanie Han & Natalie Soroka Trade and Economic Analysis Industry and Analysis Department of Commerce International Trade Administration October 214 Trade: A Vital Part of the

U.S. Trade Overview, 213 Stephanie Han & Natalie Soroka Trade and Economic Analysis Industry and Analysis Department of Commerce International Trade Administration October 214 Trade: A Vital Part of the

X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/

1/ X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/ 10.1 Overview of World Economy Latest indicators are increasingly suggesting that the significant contraction in economic activity has come to an end, notably

1/ X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/ 10.1 Overview of World Economy Latest indicators are increasingly suggesting that the significant contraction in economic activity has come to an end, notably

First Quarter 2015 Earnings Conference Call. 20 February 2015

First Quarter 2015 Earnings Conference Call 20 February 2015 Safe Harbor Statement & Disclosures The earnings call and accompanying material include forward-looking comments and information concerning

First Quarter 2015 Earnings Conference Call 20 February 2015 Safe Harbor Statement & Disclosures The earnings call and accompanying material include forward-looking comments and information concerning

Key global markets and suppliers impacting U.S. grain exports BRICs

Key global markets and suppliers impacting U.S. grain exports BRICs Levin Flake Senior Agricultural Economist, Global Policy Analysis Division, OGA/FAS/USDA TEGMA Annual Meeting January 23 rd, 2015 U.S.

Key global markets and suppliers impacting U.S. grain exports BRICs Levin Flake Senior Agricultural Economist, Global Policy Analysis Division, OGA/FAS/USDA TEGMA Annual Meeting January 23 rd, 2015 U.S.

Third Quarter 2014 Earnings Conference Call. 13 August 2014

Third Quarter 2014 Earnings Conference Call 13 August 2014 Safe Harbor Statement & Disclosures The earnings call and accompanying material include forward-looking comments and information concerning the

Third Quarter 2014 Earnings Conference Call 13 August 2014 Safe Harbor Statement & Disclosures The earnings call and accompanying material include forward-looking comments and information concerning the

Third Quarter 2015 Earnings Conference Call. 21 August 2015

Third Quarter 2015 Earnings Conference Call 21 August 2015 Safe Harbor Statement & Disclosures The earnings call and accompanying material include forward-looking comments and information concerning the

Third Quarter 2015 Earnings Conference Call 21 August 2015 Safe Harbor Statement & Disclosures The earnings call and accompanying material include forward-looking comments and information concerning the

Grains and Oilseeds Outlook

United States Department of Agriculture Grains and Oilseeds Outlook Friday, February 20, 2015 www.usda.gov/oce/forum Agricultural Outlook Forum 2015 Released: Friday, February 20, 2015 GRAINS AND OILSEEDS

United States Department of Agriculture Grains and Oilseeds Outlook Friday, February 20, 2015 www.usda.gov/oce/forum Agricultural Outlook Forum 2015 Released: Friday, February 20, 2015 GRAINS AND OILSEEDS

BANK OF ISRAEL Office of the Spokesperson and Economic Information. Report to the public on the Bank of Israel s discussions prior to deciding on the

BANK OF ISRAEL Office of the Spokesperson and Economic Information September 7, 2015 Report to the public on the Bank of Israel s discussions prior to deciding on the General interest rate for September

BANK OF ISRAEL Office of the Spokesperson and Economic Information September 7, 2015 Report to the public on the Bank of Israel s discussions prior to deciding on the General interest rate for September

Insurance Market Outlook

Munich Re Economic Research May 2014 Premium growth is again slowly gathering momentum After a rather restrained 2013 (according to partly preliminary data), we expect growth in global primary insurance

Munich Re Economic Research May 2014 Premium growth is again slowly gathering momentum After a rather restrained 2013 (according to partly preliminary data), we expect growth in global primary insurance

Consumer Credit Worldwide at year end 2012

Consumer Credit Worldwide at year end 2012 Introduction For the fifth consecutive year, Crédit Agricole Consumer Finance has published the Consumer Credit Overview, its yearly report on the international

Consumer Credit Worldwide at year end 2012 Introduction For the fifth consecutive year, Crédit Agricole Consumer Finance has published the Consumer Credit Overview, its yearly report on the international

Commodity Market Monthly

Commodity Market Monthly 1 Research Department, Commodities Team* February 11, 215 www.imf.org/commodities Commodity prices fell by 12. percent in January, mainly the result of a sharp decline in oil prices.

Commodity Market Monthly 1 Research Department, Commodities Team* February 11, 215 www.imf.org/commodities Commodity prices fell by 12. percent in January, mainly the result of a sharp decline in oil prices.

Macroeconomic Influences on U.S. Agricultural Trade

Macroeconomic Influences on U.S. Agricultural Trade In addition to the influence of shifting patterns of growth in foreign populations and per capita income, cyclical macroeconomic factors associated with

Macroeconomic Influences on U.S. Agricultural Trade In addition to the influence of shifting patterns of growth in foreign populations and per capita income, cyclical macroeconomic factors associated with

Wheat Import Projections Towards 2050. Chad Weigand Market Analyst

Wheat Import Projections Towards 2050 Chad Weigand Market Analyst January 2011 Wheat Import Projections Towards 2050 Analysis Prepared by Chad Weigand, Market Analyst January 2011 Purpose The United Nations

Wheat Import Projections Towards 2050 Chad Weigand Market Analyst January 2011 Wheat Import Projections Towards 2050 Analysis Prepared by Chad Weigand, Market Analyst January 2011 Purpose The United Nations

Global outlook: Healthcare

Global outlook: Healthcare March 2014 healthcare 1 Today s presenters Ana Nicholls Managing Editor, Industry Briefing Economist Intelligence Unit Lauren Brayshaw Marketing executive Economist Intelligence

Global outlook: Healthcare March 2014 healthcare 1 Today s presenters Ana Nicholls Managing Editor, Industry Briefing Economist Intelligence Unit Lauren Brayshaw Marketing executive Economist Intelligence

Naturally, these difficult external conditions have affected the Mexican economy. I would stress in particular three developments in this regard:

REMARKS BY MR. JAVIER GUZMÁN CALAFELL, DEPUTY GOVERNOR AT THE BANCO DE MÉXICO, ON THE MEXICAN ECONOMY IN AN ADVERSE EXTERNAL ENVIRONMENT: CHALLENGES AND POLICY RESPONSE, SANTANDER MEXICO DAY 2016, Mexico

REMARKS BY MR. JAVIER GUZMÁN CALAFELL, DEPUTY GOVERNOR AT THE BANCO DE MÉXICO, ON THE MEXICAN ECONOMY IN AN ADVERSE EXTERNAL ENVIRONMENT: CHALLENGES AND POLICY RESPONSE, SANTANDER MEXICO DAY 2016, Mexico

Summary. Economic Update 1 / 7 May 2016

Economic Update Economic Update 1 / 7 Summary 2 Global World GDP is forecast to grow only 2.4% in 2016, weighed down by emerging market weakness and increasing uncertainty. 3 Eurozone The modest eurozone

Economic Update Economic Update 1 / 7 Summary 2 Global World GDP is forecast to grow only 2.4% in 2016, weighed down by emerging market weakness and increasing uncertainty. 3 Eurozone The modest eurozone

LEE BUSI N ESS SCHOOL UNITED STATES QUARTERLY ECONOMIC FORECAST. U.S. Economic Growth to Accelerate. Chart 1. Growth Rate of U.S.

CENTER FOR BUSINESS & ECONOMIC RESEARCH LEE BUSI N ESS SCHOOL UNITED STATES QUARTERLY ECONOMIC FORECAST O U.S. Economic Growth to Accelerate ver the past few years, U.S. economic activity has remained

CENTER FOR BUSINESS & ECONOMIC RESEARCH LEE BUSI N ESS SCHOOL UNITED STATES QUARTERLY ECONOMIC FORECAST O U.S. Economic Growth to Accelerate ver the past few years, U.S. economic activity has remained

Forecasting Chinese Economy for the Years 2013-2014

Forecasting Chinese Economy for the Years 2013-2014 Xuesong Li Professor of Economics Deputy Director of Institute of Quantitative & Technical Economics Chinese Academy of Social Sciences Email: xsli@cass.org.cn

Forecasting Chinese Economy for the Years 2013-2014 Xuesong Li Professor of Economics Deputy Director of Institute of Quantitative & Technical Economics Chinese Academy of Social Sciences Email: xsli@cass.org.cn

Statement by. Janet L. Yellen. Chair. Board of Governors of the Federal Reserve System. before the. Committee on Financial Services

For release at 8:30 a.m. EST February 10, 2016 Statement by Janet L. Yellen Chair Board of Governors of the Federal Reserve System before the Committee on Financial Services U.S. House of Representatives

For release at 8:30 a.m. EST February 10, 2016 Statement by Janet L. Yellen Chair Board of Governors of the Federal Reserve System before the Committee on Financial Services U.S. House of Representatives

RECENT TRENDS AND CRITICAL ISSUES IN INTERNATIONAL TRADE LIBERALIZATION

RECENT TRENDS AND CRITICAL ISSUES IN INTERNATIONAL TRADE LIBERALIZATION Parr Rosson Professor and Extension Economist Department of Agricultural Economics Texas A&M University U.S. agriculture has undergone

RECENT TRENDS AND CRITICAL ISSUES IN INTERNATIONAL TRADE LIBERALIZATION Parr Rosson Professor and Extension Economist Department of Agricultural Economics Texas A&M University U.S. agriculture has undergone

Market Monitor Number 3 November 2012

Market Monitor Number 3 November 2012 AMIS Crops: World Supply-Demand Balances in 2012/13 World supply and demand situation continues to tighten for wheat and maize but rice and soybeans have eased. In

Market Monitor Number 3 November 2012 AMIS Crops: World Supply-Demand Balances in 2012/13 World supply and demand situation continues to tighten for wheat and maize but rice and soybeans have eased. In

RECENT TRADE DEVELOPMENTS AND SELECTED TRENDS IN TRADE

I A RECENT TRADE DEVELOPMENTS AND SELECTED TRENDS IN TRADE RECENT TRENDS IN INTERNATIONAL TRADE 1. INTRODUCTION: THESTATEOFTHEWORLDECONOMYANDTRADE IN 2006 The year 2006 witnessed robust growth in the world

I A RECENT TRADE DEVELOPMENTS AND SELECTED TRENDS IN TRADE RECENT TRENDS IN INTERNATIONAL TRADE 1. INTRODUCTION: THESTATEOFTHEWORLDECONOMYANDTRADE IN 2006 The year 2006 witnessed robust growth in the world

The Impact of Exchange Rate Movements on Vegetable Imports

The Impact of Exchange Rate Movements on Vegetable Imports This paper examines whether movement in the exchange rate of the Australia dollar is the major explanatory factor for changes in the level of

The Impact of Exchange Rate Movements on Vegetable Imports This paper examines whether movement in the exchange rate of the Australia dollar is the major explanatory factor for changes in the level of

The Global Economic Impacts of Oil Price Shocks

The Global Economic Impacts of Oil Price Shocks Presented to: Project LINK, United Nations New York, NY November 22, 2004 Presented by: Sara Johnson Managing Director, Global Macroeconomics Group 781-301-9115

The Global Economic Impacts of Oil Price Shocks Presented to: Project LINK, United Nations New York, NY November 22, 2004 Presented by: Sara Johnson Managing Director, Global Macroeconomics Group 781-301-9115

Corn Transportation Profile

Corn Transportation Profile AMS Transportation and Marketing Programs August 2014 Marina R. Denicoff Marvin E. Prater Pierre Bahizi Executive Summary America s farmers depend on transportation as the critical

Corn Transportation Profile AMS Transportation and Marketing Programs August 2014 Marina R. Denicoff Marvin E. Prater Pierre Bahizi Executive Summary America s farmers depend on transportation as the critical

How much financing will your farm business

Twelve Steps to Ag Decision Maker Cash Flow Budgeting File C3-15 How much financing will your farm business require this year? When will money be needed and from where will it come? A little advance planning

Twelve Steps to Ag Decision Maker Cash Flow Budgeting File C3-15 How much financing will your farm business require this year? When will money be needed and from where will it come? A little advance planning

Soybean Supply and Demand Forecast

Soybean Supply and Demand Forecast U.S. soybean planted acreage is expected to increase 11.5 million acres over the forecast period. U.S. soybean yields are expected to increase 7 bushels per acre or an

Soybean Supply and Demand Forecast U.S. soybean planted acreage is expected to increase 11.5 million acres over the forecast period. U.S. soybean yields are expected to increase 7 bushels per acre or an

Meat and Meat products: price and trade update Issue 1 May 2014. Meat and Meat products. Price and Trade Update: April 2014 1

Issue 1 May 2014 Weekly Newsletter Meat and Meat products Price and Trade Update April export prices stable Meat and Meat products Price and Trade Update: April 2014 1 The FAO Meat Price Index averaged

Issue 1 May 2014 Weekly Newsletter Meat and Meat products Price and Trade Update April export prices stable Meat and Meat products Price and Trade Update: April 2014 1 The FAO Meat Price Index averaged

Cotton and Wool Outlook

Economic Research Service Situation and Outlook CWS-14h Release Date August 14, 2014 Cotton and Wool Outlook Leslie Meyer lmeyer@ers.usda.gov Stephen MacDonald stephenm@ers.usda.gov Global Cotton Stocks

Economic Research Service Situation and Outlook CWS-14h Release Date August 14, 2014 Cotton and Wool Outlook Leslie Meyer lmeyer@ers.usda.gov Stephen MacDonald stephenm@ers.usda.gov Global Cotton Stocks

The impact of the falling yen on U.S. import prices

APRIL 2014 VOLUME 3 / NUMBER 7 GLOBAL ECONOMY The impact of the falling yen on U.S. import prices By David Mead and Sharon Royales In the fall of 2012, Japan set forth economic policies aimed at turning

APRIL 2014 VOLUME 3 / NUMBER 7 GLOBAL ECONOMY The impact of the falling yen on U.S. import prices By David Mead and Sharon Royales In the fall of 2012, Japan set forth economic policies aimed at turning

Monetary Policy Outlook in a Negative Rates Environment Mr. Javier Guzmán Calafell, Deputy Governor, Banco de México J.P. Morgan Investor Seminar

Mr. Javier Guzmán Calafell, Deputy Governor, Banco de México J.P. Morgan Investor Seminar Washington, DC, 15 April 2016 Outline 1 External Conditions 2 Macroeconomic Policy in Mexico 3 Evolution and Outlook

Mr. Javier Guzmán Calafell, Deputy Governor, Banco de México J.P. Morgan Investor Seminar Washington, DC, 15 April 2016 Outline 1 External Conditions 2 Macroeconomic Policy in Mexico 3 Evolution and Outlook

Introduction B.2 & B.3 111

Risks and Scenarios Introduction The forecasts presented in the Economic and Tax Outlook chapter incorporate a number of judgements about how both the New Zealand and the world economies evolve. Some judgements

Risks and Scenarios Introduction The forecasts presented in the Economic and Tax Outlook chapter incorporate a number of judgements about how both the New Zealand and the world economies evolve. Some judgements

WORLDWIDE RETAIL ECOMMERCE SALES: EMARKETER S UPDATED ESTIMATES AND FORECAST THROUGH 2019

WORLDWIDE RETAIL ECOMMERCE SALES: EMARKETER S UPDATED ESTIMATES AND FORECAST THROUGH 2019 Worldwide retail sales including in-store and internet purchases will surpass $22 trillion in 2015, up 5.6% from

WORLDWIDE RETAIL ECOMMERCE SALES: EMARKETER S UPDATED ESTIMATES AND FORECAST THROUGH 2019 Worldwide retail sales including in-store and internet purchases will surpass $22 trillion in 2015, up 5.6% from

Washington State Industry Outlook and Freight Transportation Forecast:

Washington State Industry Outlook and Freight Transportation Forecast: Apple Industry Prepared for the Washington State Department of Transportation Freight Systems Division By Selmin Creamer Research

Washington State Industry Outlook and Freight Transportation Forecast: Apple Industry Prepared for the Washington State Department of Transportation Freight Systems Division By Selmin Creamer Research

ANALYSIS OF LEBANON S FOOD MARKET

ANALYSIS OF LEBANON S FOOD MARKET Table of Contents World Food Market 3 Lebanon s Food Production 8 Lebanon s Food Imports and Exports 11 Evolution of Food Imports 11 Food Imports by Type 12 Food Imports

ANALYSIS OF LEBANON S FOOD MARKET Table of Contents World Food Market 3 Lebanon s Food Production 8 Lebanon s Food Imports and Exports 11 Evolution of Food Imports 11 Food Imports by Type 12 Food Imports

2013 2014e 2015f. www.economics.gov.nl.ca. Real GDP Growth (%)

") The global economy recorded modest growth in 2014. Real GDP rose by 3.4%, however, economic performance varied by country and region (see table). Several regions turned in a lackluster performance. The

The global economy recorded modest growth in 2014. Real GDP rose by 3.4%, however, economic performance varied by country and region (see table). Several regions turned in a lackluster performance. The

Falling Oil Prices and US Economic Activity: Implications for the Future

Date Issue Brief # I S S U E B R I E F Falling Oil Prices and US Economic Activity: Implications for the Future Stephen P.A. Brown December 2014 Issue Brief 14-06 Resources for the Future Resources for

Date Issue Brief # I S S U E B R I E F Falling Oil Prices and US Economic Activity: Implications for the Future Stephen P.A. Brown December 2014 Issue Brief 14-06 Resources for the Future Resources for

Internet address: http://www.bls.gov/fls USDL: 04-2343

Internet address: http://www.bls.gov/fls USDL: 04-2343 Technical information: (202) 691-5654 For Release: 10:00 A.M. EST Media contact: (202) 691-5902 Thursday, November 18, 2004 INTERNATIONAL COMPARISONS

Internet address: http://www.bls.gov/fls USDL: 04-2343 Technical information: (202) 691-5654 For Release: 10:00 A.M. EST Media contact: (202) 691-5902 Thursday, November 18, 2004 INTERNATIONAL COMPARISONS

Ethanol Usage Projections & Corn Balance Sheet (mil. bu.)

") Ethanol Usage Projections & Corn Balance Sheet (mil. bu.) Updated 12/21/215 Historic Est. Prelim. Proj. 216-17 Year: (production/marketing) 1/ 211-12 212-13 213-14 214-15 215-16 Low Med. 4 High Yield (bu.

Ethanol Usage Projections & Corn Balance Sheet (mil. bu.) Updated 12/21/215 Historic Est. Prelim. Proj. 216-17 Year: (production/marketing) 1/ 211-12 212-13 213-14 214-15 215-16 Low Med. 4 High Yield (bu.

AGRICULTURAL SCIENCES Vol. II - Crop Production Capacity In North America - G.K. Pompelli CROP PRODUCTION CAPACITY IN NORTH AMERICA

CROP PRODUCTION CAPACITY IN NORTH AMERICA G.K. Pompelli Economic Research Service, U. S. Department of Agriculture, USA Keywords: Supply, policy, yields. Contents 1. Introduction 2. Past Trends in Demand

CROP PRODUCTION CAPACITY IN NORTH AMERICA G.K. Pompelli Economic Research Service, U. S. Department of Agriculture, USA Keywords: Supply, policy, yields. Contents 1. Introduction 2. Past Trends in Demand

World Manufacturing Production

Quarterly Report World Manufacturing Production Statistics for Quarter III, 2013 Statistics Unit www.unido.org/statistics Report on world manufacturing production, Quarter III, 2013 UNIDO Statistics presents

Quarterly Report World Manufacturing Production Statistics for Quarter III, 2013 Statistics Unit www.unido.org/statistics Report on world manufacturing production, Quarter III, 2013 UNIDO Statistics presents

Grain Transportation Quarterly Updates

Grain Transportation Quarterly Updates Truck Advisory Transportation and Marketing Programs Transportation Services Division www.ams.usda.gov/agtransportation Table 1: U.S. Grain Truck Market, 3 rd Quarter

Grain Transportation Quarterly Updates Truck Advisory Transportation and Marketing Programs Transportation Services Division www.ams.usda.gov/agtransportation Table 1: U.S. Grain Truck Market, 3 rd Quarter

The 2024 prospects for EU agricultural markets: drivers and uncertainties. Tassos Haniotis

1. Introduction The 2024 prospects for EU agricultural markets: drivers and uncertainties Tassos Haniotis Director of Economic Analysis, Perspectives and Evaluations; Communication DG Agriculture and Rural

1. Introduction The 2024 prospects for EU agricultural markets: drivers and uncertainties Tassos Haniotis Director of Economic Analysis, Perspectives and Evaluations; Communication DG Agriculture and Rural

82 nd IFA Annual Conference Sydney (Australia), 26-28 May 2014

, 26-28 May 2014") A/14/65b June 2014 Final Version 82 nd IFA Annual Conference Sydney (Australia), 26-28 May 2014 Fertilizer Outlook 2014-2018 Patrick Heffer and Michel Prud homme International Fertilizer Industry Association

A/14/65b June 2014 Final Version 82 nd IFA Annual Conference Sydney (Australia), 26-28 May 2014 Fertilizer Outlook 2014-2018 Patrick Heffer and Michel Prud homme International Fertilizer Industry Association

percentage points to the overall CPI outcome. Goods price inflation increased to 4,6

South African Reserve Bank Press Statement Embargo on Delivery 28 January 2016 Statement of the Monetary Policy Committee Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the

South African Reserve Bank Press Statement Embargo on Delivery 28 January 2016 Statement of the Monetary Policy Committee Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the

Supply & demand outlook for the canola industry

Supply & demand outlook for the canola industry J.P. Gervais Chief Ag Economist March 2015 @jpgervais Canola Canola is one component of the environment for oil producing crops Growth in demand has supported

Supply & demand outlook for the canola industry J.P. Gervais Chief Ag Economist March 2015 @jpgervais Canola Canola is one component of the environment for oil producing crops Growth in demand has supported

FCC Ag Economics: Farm Sector Health Drives Farm Equipment Sales

FCC Ag Economics: Farm Sector Health Drives Farm Equipment Sales Fall 2015 FCC Ag Economics: Farm Sector Health Drives Farm Equipment Sales 1 Introduction Agriculture is always evolving. Average farm sizes

FCC Ag Economics: Farm Sector Health Drives Farm Equipment Sales Fall 2015 FCC Ag Economics: Farm Sector Health Drives Farm Equipment Sales 1 Introduction Agriculture is always evolving. Average farm sizes

Report to the public on the Bank of Israel s discussions prior to deciding on. the interest rate for January 2015

BANK OF ISRAEL Office of the Spokesperson and Economic Information January 12, 2015 Report to the public on the Bank of Israel s discussions prior to deciding on General the interest rate for January 2015

BANK OF ISRAEL Office of the Spokesperson and Economic Information January 12, 2015 Report to the public on the Bank of Israel s discussions prior to deciding on General the interest rate for January 2015

EUROSYSTEM STAFF MACROECONOMIC PROJECTIONS FOR THE EURO AREA

EUROSYSTEM STAFF MACROECONOMIC PROJECTIONS FOR THE EURO AREA On the basis of the information available up to 22 May 2009, Eurosystem staff have prepared projections for macroeconomic developments in the

EUROSYSTEM STAFF MACROECONOMIC PROJECTIONS FOR THE EURO AREA On the basis of the information available up to 22 May 2009, Eurosystem staff have prepared projections for macroeconomic developments in the

Outlook for Economic Activity and Prices

Not to be released until : p.m. Japan Standard Time on Saturday, January 3, 16. January 3, 16 Bank of Japan Outlook for Economic Activity and Prices January 16 (English translation prepared by the Bank's

Not to be released until : p.m. Japan Standard Time on Saturday, January 3, 16. January 3, 16 Bank of Japan Outlook for Economic Activity and Prices January 16 (English translation prepared by the Bank's

Overview on milk prices and production costs world wide

Overview on milk prices and production costs world wide This article summarises the key findings of the IFCN work in 2013 and the recently published IFCN Dairy Report 2013 Authors: Torsten Hemme and dairy

Overview on milk prices and production costs world wide This article summarises the key findings of the IFCN work in 2013 and the recently published IFCN Dairy Report 2013 Authors: Torsten Hemme and dairy

The Economic Impact of a U.S. Slowdown on the Americas

Issue Brief March 2008 Center for Economic and Policy Research 1611 Connecticut Ave, NW Suite 400 Washington, DC 20009 tel: 202-293-5380 fax:: 202-588-1356 www.cepr.net The Economic Impact of a U.S. Slowdown

Issue Brief March 2008 Center for Economic and Policy Research 1611 Connecticut Ave, NW Suite 400 Washington, DC 20009 tel: 202-293-5380 fax:: 202-588-1356 www.cepr.net The Economic Impact of a U.S. Slowdown

A Business Newsletter for Agriculture. Vol. 12, No. 1 www.extension.iastate.edu/agdm. Energy agriculture - where s the nitrogen?

A Business Newsletter for Agriculture Vol. 12, No. 1 www.extension.iastate.edu/agdm November 2007 Energy agriculture - where s the nitrogen? by Don Hofstrand, value-added agriculture specialist, co-director

A Business Newsletter for Agriculture Vol. 12, No. 1 www.extension.iastate.edu/agdm November 2007 Energy agriculture - where s the nitrogen? by Don Hofstrand, value-added agriculture specialist, co-director

Manpower Employment Outlook Survey Singapore Q3 2014. A Manpower Research Report

Manpower Employment Outlook Survey Singapore Q3 14 A Manpower Research Report Contents Q3/14 Singapore Employment Outlook 2 Sector Comparisons Global Employment Outlook 6 International Comparisons - Asia

Manpower Employment Outlook Survey Singapore Q3 14 A Manpower Research Report Contents Q3/14 Singapore Employment Outlook 2 Sector Comparisons Global Employment Outlook 6 International Comparisons - Asia

TRADE AGREEMENTS AND U.S. AGRICULTURE

TRADE AGREEMENTS AND U.S. AGRICULTURE Overview International trade promotes competition, economic growth, and international market stability key components to expanding consumer income and promoting consumption

TRADE AGREEMENTS AND U.S. AGRICULTURE Overview International trade promotes competition, economic growth, and international market stability key components to expanding consumer income and promoting consumption

Grain Futures Markets & National Cash Indices Review & Observations thru July 27, 2012 PHI Market Analysis Manager Virg Robinson

Grain Futures Markets & National Cash Indices Review & Observations thru July 27, 2012 PHI Market Analysis Manager Virg Robinson S&P 500 FUTURES NEAR BULLISH BREAKOUT The S&P 500 futures monthly continuation

Grain Futures Markets & National Cash Indices Review & Observations thru July 27, 2012 PHI Market Analysis Manager Virg Robinson S&P 500 FUTURES NEAR BULLISH BREAKOUT The S&P 500 futures monthly continuation

Research Commodities El Niño returns grains and soft commodities at risk

Investment Research General Market Conditions 20 May 2015 Research Commodities El Niño returns grains and soft commodities at risk Meteorologists now agree that El Niño has arrived and project that it

Investment Research General Market Conditions 20 May 2015 Research Commodities El Niño returns grains and soft commodities at risk Meteorologists now agree that El Niño has arrived and project that it

2012 Japan Broiler Market Situation Update and 2013 Outlook

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: GAIN Report

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: GAIN Report

EU Milk Margin Estimate up to 2014

Ref. Ares(215)2882499-9/7/215 EU Agricultural and Farm Economics Briefs No 7 June 215 EU Milk Margin Estimate up to 214 An overview of estimates of of production and gross margins of milk production in

Ref. Ares(215)2882499-9/7/215 EU Agricultural and Farm Economics Briefs No 7 June 215 EU Milk Margin Estimate up to 214 An overview of estimates of of production and gross margins of milk production in

Financial Information

Financial Information Solid results with in all key financial metrics of 23.6 bn, up 0.4% like-for like Adjusted EBITA margin up 0.3 pt on organic basis Net profit up +4% to 1.9 bn Record Free Cash Flow

Financial Information Solid results with in all key financial metrics of 23.6 bn, up 0.4% like-for like Adjusted EBITA margin up 0.3 pt on organic basis Net profit up +4% to 1.9 bn Record Free Cash Flow

3.3 Real Returns Above Variable Costs

3.3 Real Returns Above Variable Costs Several factors can impact the returns above variable costs for crop producers. Over a long period of time, sustained increases in the growth rate for purchased inputs

3.3 Real Returns Above Variable Costs Several factors can impact the returns above variable costs for crop producers. Over a long period of time, sustained increases in the growth rate for purchased inputs

Have Recent Increases in International Cereal Prices Been Transmitted to Domestic Economies? The experience in seven large Asian countries

Have Recent Increases in International Cereal Prices Been Transmitted to Domestic Economies? The experience in seven large Asian countries David Dawe ESA Working Paper No. 08-03 April 2008 Agricultural

Have Recent Increases in International Cereal Prices Been Transmitted to Domestic Economies? The experience in seven large Asian countries David Dawe ESA Working Paper No. 08-03 April 2008 Agricultural

World Manufacturing Production

Quarterly Report World Manufacturing Production Statistics for Quarter IV, 2013 Statistics Unit www.unido.org/statistics Report on world manufacturing production, Quarter IV, 2013 UNIDO Statistics presents

Quarterly Report World Manufacturing Production Statistics for Quarter IV, 2013 Statistics Unit www.unido.org/statistics Report on world manufacturing production, Quarter IV, 2013 UNIDO Statistics presents

AGRI- BUSINESS IN ARGENTINA A SEMINAR ON INVESTMENT OPPORTUNITIES

AGRI- BUSINESS IN ARGENTINA A SEMINAR ON INVESTMENT OPPORTUNITIES Maximiliano Moreno Director of Multilateral Negotiations Ministry of Agriculture, Livestock and Fisheries Argentina NEW INTERNATIONAL ENVIRONMENT

AGRI- BUSINESS IN ARGENTINA A SEMINAR ON INVESTMENT OPPORTUNITIES Maximiliano Moreno Director of Multilateral Negotiations Ministry of Agriculture, Livestock and Fisheries Argentina NEW INTERNATIONAL ENVIRONMENT

March 2016 ECB staff macroeconomic projections for the euro area 1

March 2016 ECB staff macroeconomic projections for the euro area 1 1 Euro area outlook: overview and key features The economic recovery in the euro area is expected to continue, albeit with less momentum

March 2016 ECB staff macroeconomic projections for the euro area 1 1 Euro area outlook: overview and key features The economic recovery in the euro area is expected to continue, albeit with less momentum

ENGINEERING LABOUR MARKET

ENGINEERING LABOUR MARKET in Canada Projections to 2025 JUNE 2015 ENGINEERING LABOUR MARKET in Canada Projections to 2025 Prepared by: MESSAGE FROM THE CHIEF EXECUTIVE OFFICER Dear colleagues: Engineers

ENGINEERING LABOUR MARKET in Canada Projections to 2025 JUNE 2015 ENGINEERING LABOUR MARKET in Canada Projections to 2025 Prepared by: MESSAGE FROM THE CHIEF EXECUTIVE OFFICER Dear colleagues: Engineers

Opportunities and Challenges in Global Pork and Beef Markets

Opportunities and Challenges in Global Pork and Beef Markets Derrell S. Peel Breedlove Professor of Agribusiness Department of Agricultural Economics Oklahoma State University Growing Global Demand for

Opportunities and Challenges in Global Pork and Beef Markets Derrell S. Peel Breedlove Professor of Agribusiness Department of Agricultural Economics Oklahoma State University Growing Global Demand for

The global economy Banco de Portugal Lisbon, 24 September 2013 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist

The global economy Banco de Portugal Lisbon, 24 September 213 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist Summary of presentation Global economy slowly exiting recession but

The global economy Banco de Portugal Lisbon, 24 September 213 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist Summary of presentation Global economy slowly exiting recession but

Meeting with Analysts

CNB s New Forecast (Inflation Report II/2015) Meeting with Analysts Petr Král Prague, 11 May, 2015 1 Outline Assumptions of the forecast The new macroeconomic forecast Comparison with the previous forecast

CNB s New Forecast (Inflation Report II/2015) Meeting with Analysts Petr Král Prague, 11 May, 2015 1 Outline Assumptions of the forecast The new macroeconomic forecast Comparison with the previous forecast

A Primer on Exchange Rates and Exporting WASHINGTON STATE UNIVERSITY EXTENSION EM041E

A Primer on Exchange Rates and Exporting WASHINGTON STATE UNIVERSITY EXTENSION EM041E A Primer on Exchange Rates and Exporting By Andrew J. Cassey and Pavan Dhanireddy Abstract Opportunities to begin exporting

A Primer on Exchange Rates and Exporting WASHINGTON STATE UNIVERSITY EXTENSION EM041E A Primer on Exchange Rates and Exporting By Andrew J. Cassey and Pavan Dhanireddy Abstract Opportunities to begin exporting

Explanation beyond exchange rates: trends in UK trade since 2007

Explanation beyond exchange rates: trends in UK trade since 2007 Author Name(s): Michael Hardie, Andrew Jowett, Tim Marshall & Philip Wales, Office for National Statistics Abstract The UK s trade performance

Explanation beyond exchange rates: trends in UK trade since 2007 Author Name(s): Michael Hardie, Andrew Jowett, Tim Marshall & Philip Wales, Office for National Statistics Abstract The UK s trade performance

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S.

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Voluntary - Public Date: 1/29/2013 GAIN Report Number:

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Voluntary - Public Date: 1/29/2013 GAIN Report Number:

ADAMA DELIVERS ROBUST VOLUME GROWTH DESPITE DIFFICULT MARKET AND CURRENCY CONDITIONS

ADAMA DELIVERS ROBUST VOLUME GROWTH DESPITE DIFFICULT MARKET AND CURRENCY CONDITIONS Revenues in constant currencies up estimated 9.5% in the third quarter and 6% year-to-date Strong volume growth in all

ADAMA DELIVERS ROBUST VOLUME GROWTH DESPITE DIFFICULT MARKET AND CURRENCY CONDITIONS Revenues in constant currencies up estimated 9.5% in the third quarter and 6% year-to-date Strong volume growth in all

BTMU Focus Latin America Mexico: Export performance in 2014

BTMU Focus Latin America Mexico: Export performance in 2014 MUFG UNION BANK Economic Research (New York) Hongrui Zhang Latin America Economist hozhang@us.mufg.jp +1(212)782-5708 June 15, 2015 Contents

BTMU Focus Latin America Mexico: Export performance in 2014 MUFG UNION BANK Economic Research (New York) Hongrui Zhang Latin America Economist hozhang@us.mufg.jp +1(212)782-5708 June 15, 2015 Contents

2013 global economic outlook: Are promising growth trends sustainable? Timothy Hopper, Ph.D., Chief Economist, TIAA-CREF January 24, 2013

2013 global economic outlook: Are promising growth trends sustainable? Timothy Hopper, Ph.D., Chief Economist, TIAA-CREF January 24, 2013 U.S. stock market performance in 2012 * +12.59% total return +6.35%

2013 global economic outlook: Are promising growth trends sustainable? Timothy Hopper, Ph.D., Chief Economist, TIAA-CREF January 24, 2013 U.S. stock market performance in 2012 * +12.59% total return +6.35%

What drives crude oil prices?

What drives crude oil prices? An analysis of 7 factors that influence oil markets, with chart data updated monthly and quarterly Washington, DC U.S. Energy Information Administration Independent Statistics

What drives crude oil prices? An analysis of 7 factors that influence oil markets, with chart data updated monthly and quarterly Washington, DC U.S. Energy Information Administration Independent Statistics

MBA Forecast Commentary Joel Kan, jkan@mba.org

MBA Forecast Commentary Joel Kan, jkan@mba.org Weak First Quarter, But Growth Expected to Recover MBA Economic and Mortgage Finance Commentary: May 2015 Broad economic growth in the US got off to a slow

MBA Forecast Commentary Joel Kan, jkan@mba.org Weak First Quarter, But Growth Expected to Recover MBA Economic and Mortgage Finance Commentary: May 2015 Broad economic growth in the US got off to a slow

Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation

August 2014 Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated to reflect the current economic outlook for factors that typically impact

August 2014 Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated to reflect the current economic outlook for factors that typically impact

Euro Zone s Economic Outlook and What it Means for the United States

WELCOME TO THE WEBINAR WEBINAR LINK: HTTP://FRBATL.ADOBECONNECT.COM/ECONOMY/ DIAL-IN NUMBER (MUST USE FOR AUDIO): 855-377-2663 ACCESS CODE: 71032685 Euro Zone s Economic Outlook and What it Means for the

WELCOME TO THE WEBINAR WEBINAR LINK: HTTP://FRBATL.ADOBECONNECT.COM/ECONOMY/ DIAL-IN NUMBER (MUST USE FOR AUDIO): 855-377-2663 ACCESS CODE: 71032685 Euro Zone s Economic Outlook and What it Means for the

Further Developments of Hong Kong s Offshore RMB Market: Opportunities and Challenges

Further Developments of Hong Kong s Offshore RMB Market: Opportunities and Challenges Zhang Ying, Senior Economist In recent years, as the internationalization of the RMB has been steadily carrying out,

Further Developments of Hong Kong s Offshore RMB Market: Opportunities and Challenges Zhang Ying, Senior Economist In recent years, as the internationalization of the RMB has been steadily carrying out,

General Certificate of Education Advanced Level Examination January 2010

General Certificate of Education Advanced Level Examination January 2010 Economics ECON4 Unit 4 The National and International Economy Tuesday 2 February 2010 1.30 pm to 3.30 pm For this paper you must

General Certificate of Education Advanced Level Examination January 2010 Economics ECON4 Unit 4 The National and International Economy Tuesday 2 February 2010 1.30 pm to 3.30 pm For this paper you must

Recent Developments and Outlook for the Mexican Economy Credit Suisse, 2016 Macro Conference April 19, 2016

Credit Suisse, Macro Conference April 19, Outline 1 Inflation and Monetary Policy 2 Recent Developments and Outlook for the Mexican Economy 3 Final Remarks 2 In line with its constitutional mandate, the

Credit Suisse, Macro Conference April 19, Outline 1 Inflation and Monetary Policy 2 Recent Developments and Outlook for the Mexican Economy 3 Final Remarks 2 In line with its constitutional mandate, the

What Determines Exchange Rates? In the Short Run In the Long Run

What Determines Exchange Rates? In the Short Run In the Long Run Selected Exchange Rates Selected Exchange Rates Determinants of the Exchange Rate in the Short Run In the short run, movements of currency

What Determines Exchange Rates? In the Short Run In the Long Run Selected Exchange Rates Selected Exchange Rates Determinants of the Exchange Rate in the Short Run In the short run, movements of currency

India s Services Exports

Markus Hyvonen and Hao Wang* Exports of services are an important source of demand for the Indian economy and account for a larger share of output than in most major economies. The importance of India

Markus Hyvonen and Hao Wang* Exports of services are an important source of demand for the Indian economy and account for a larger share of output than in most major economies. The importance of India

Monthly Economic Dashboard

RETIREMENT INSTITUTE SM Economic perspective Monthly Economic Dashboard Modest acceleration in economic growth appears in store for 2016 as the inventory-caused soft patch ends, while monetary policy moves

RETIREMENT INSTITUTE SM Economic perspective Monthly Economic Dashboard Modest acceleration in economic growth appears in store for 2016 as the inventory-caused soft patch ends, while monetary policy moves

Wisconsin's Exports A Special Report on Wisconsin's Economy

Wisconsin's Exports A Special Report on Wisconsin's Economy April 2011 Wisconsin Department of Revenue Division of Research and Policy AT A GLANCE Wisconsin's goods exports increased 18.3% to $19.8 billion

Wisconsin's Exports A Special Report on Wisconsin's Economy April 2011 Wisconsin Department of Revenue Division of Research and Policy AT A GLANCE Wisconsin's goods exports increased 18.3% to $19.8 billion

A Strong U.S. Dollar Changes Everything

Schwab Center for Financial Research A Strong U.S. Dollar Changes Everything A white paper by Kathy A. Jones, Senior Vice President, Chief Fixed Income Strategist The U.S. dollar is near its highest level

Schwab Center for Financial Research A Strong U.S. Dollar Changes Everything A white paper by Kathy A. Jones, Senior Vice President, Chief Fixed Income Strategist The U.S. dollar is near its highest level

Weiqiao Textile Announces its 2015 Interim Results

Weiqiao Textile Announces its 2015 Interim Results Seize new opportunities in new normal development phase Continued leadership against the backdrop of industry changes Financial Summary Revenue was approximately

Weiqiao Textile Announces its 2015 Interim Results Seize new opportunities in new normal development phase Continued leadership against the backdrop of industry changes Financial Summary Revenue was approximately

Future drivers and trends in dairy and food markets

Future drivers and trends in dairy and food markets IAL 2011 August 2011 Michael Harvey, Senior Analyst Road map Topic 1 Future drivers and trends in dairy and food markets Topic 2 Where is the dairy sector

Future drivers and trends in dairy and food markets IAL 2011 August 2011 Michael Harvey, Senior Analyst Road map Topic 1 Future drivers and trends in dairy and food markets Topic 2 Where is the dairy sector

Measuring Beef Demand

Measuring Beef Demand James Mintert, Ph.D. Professor & Extension State Leader Department of Agricultural Economics Kansas State University www.agmanager.info/livestock/marketing jmintert@ksu.edu A Picture

Measuring Beef Demand James Mintert, Ph.D. Professor & Extension State Leader Department of Agricultural Economics Kansas State University www.agmanager.info/livestock/marketing jmintert@ksu.edu A Picture

Explaining Russia s New Normal

Explaining Russia s New Normal Chris Weafer of Macro-Advisory This Op- Ed appeared on BNE.eu on September 11 2015 One of the slogans now regularly deployed to describe Russia s current economic condition

Explaining Russia s New Normal Chris Weafer of Macro-Advisory This Op- Ed appeared on BNE.eu on September 11 2015 One of the slogans now regularly deployed to describe Russia s current economic condition

Global growth rates Macroeconomic indicators CEDIGAZ Reference Scenario

Medium and Long Term Natural Gas Outlook CEDIGAZ February 215 Global growth rates Macroeconomic indicators CEDIGAZ Reference Scenario 4 3 %/year 199-213 213-235 6 Main consuming markets - %/year (213-235)

Medium and Long Term Natural Gas Outlook CEDIGAZ February 215 Global growth rates Macroeconomic indicators CEDIGAZ Reference Scenario 4 3 %/year 199-213 213-235 6 Main consuming markets - %/year (213-235)