Homework Solutions - Lecture 2

|

|

|

- Maximilian Willis

- 9 years ago

- Views:

Transcription

1 Homework Solutions - Lecture 2 1. The value of the S&P 500 index is and the treasury rate is 3.43%. In a typical year, stock repurchases increase the average payout ratio on S&P 500 stocks to over 4%. a. Calculate the implied equity premium assuming the dividend yield in the most recent year was 4% of the current index value and dividends are expected to grow at a constant rate of 5% annually. How does this implied premium compare to the value we calculated when ignoring repurchases? Div = (.04)(1.05) = Div1 R = g + =.05 + CurrentValue = = 9.20% Implied Risk Premium = = 5.77% All of the values in this problem are the same as the problem we did in class except the dividend yield. Because the current value of the index ( ) does not change, but the forecasted dividends here are higher, the implied premium is higher than the one we calculated in class. b. Calculate the implied equity premium assuming the dividend yield in the most recent year was 4% of the current index value, dividends are expected to grow at an annual rate of 10% for the next five years, and at a constant rate of 5% thereafter (Hint: you can use the solver function in excel). How does this implied premium compare to the value we calculated when ignoring repurchases? Here you will need to use the Solver function in excel. Specifically, you should solve for the required return that sets the present value of future dividends equal to the current index value. Div = (.04)(1.10) = = /( R.05) + 5 R = 10.20% Implied Risk Premium = = 6.77% Again, all of the values in this problem are the same as the problem we did in class except the dividend yield. Because the current value of the index ( ) does not change, but the forecasted dividends here are higher, the implied premium is higher than the one we calculated in class.

2 2. An analyst at your firm comes to you with a valuation of a Greek firm done with Euro cash flows. The analyst has used the 15.85% yield on the Euro-denominated Greek government bond as the riskfree rate in the cost of equity calculation, along with a 4.5% global equity risk premium. What assumptions is this analyst making about country risk? Would it be appropriate for the analyst to add a separate country risk premium to the CAPM equation? The 15.85% yield on the Greek Euro bond includes a real risk-free rate, an expectation of inflation, and a default spread. Including the default spread is one method of estimating country risk. The implicit assumptions are that (1) the country risk premium can be approximated by the default spread on local government bonds, and (2) the sensitivity to country risk is the same across all firms in the Greece, or λ=1. Because the analyst has already implicitly incorporated country risk, an additional country risk term should not be added separately. Yields on 10-Year Government Bonds 18.0% 16.0% 13.98% default spread 15.85% 14.0% 12.0% 10.0% 8.0% 1.87% risk-free rate based on German Euro bond (including estimate of Euro inflation) 10.06% 6.0% 4.0% 2.0% 0.0% 0.21% 2.17% 3.73% 4.62% 1.87% 4.69% 2.96% 1.72% 3.92% 3.91% U.S. (Inflation Indexed) U.S. ($U.S.) Brazil C-Bond ($U.S.) Italy (Euro) Germany (Euro) Spain (Euro) Greece (Euro) Portugal (Euro) Japan (Yen) Singapore (SGD) China (Yuan) Mexico (Peso) ( Risk Premium ) Country Spread E( R) = R f + β U S % Euro risk-free rate (excluding 13.98% country default spread) 13.98% country bond default spread for Greek BB+ rated bonds %

3 3. In 1995, Time Warner Inc. had a Beta of Part of the reason for this high Beta was the debt left over from the leveraged buyout of Time by Warner in 1989, which amounted to $10 billion in The market value of equity at Time Warner in 1995 was also $10 billion. The marginal tax rate was 40%. a) Using the formula for leveraging a beta that includes tax effects (to account for the extremely high and changing leverage), we get: E 10 β u = β e = 1.61 = D(1 T ) + E 10(1.4) + 10 b) The debt/equity ratio in 1995 was 10/10 = 1.0. If the debt ratio goes from 1.0 in 1995, to 0.9 in 1996, and 0.8 in 1997, the levered betas for 1996 and 1997 would equal: D(1 T ) β e = β u 1 + = = E ( +.9(1.4)) D(1 T ) β e = β u 1 + = = E ( +.8(1.4))

Using the formula for leveraging a beta that includes tax effects (to account for the extremely high and changing leverage), we get: E 10 β u = β e = 1.61 = 1.006 D(1 T ) + E 10(1.")

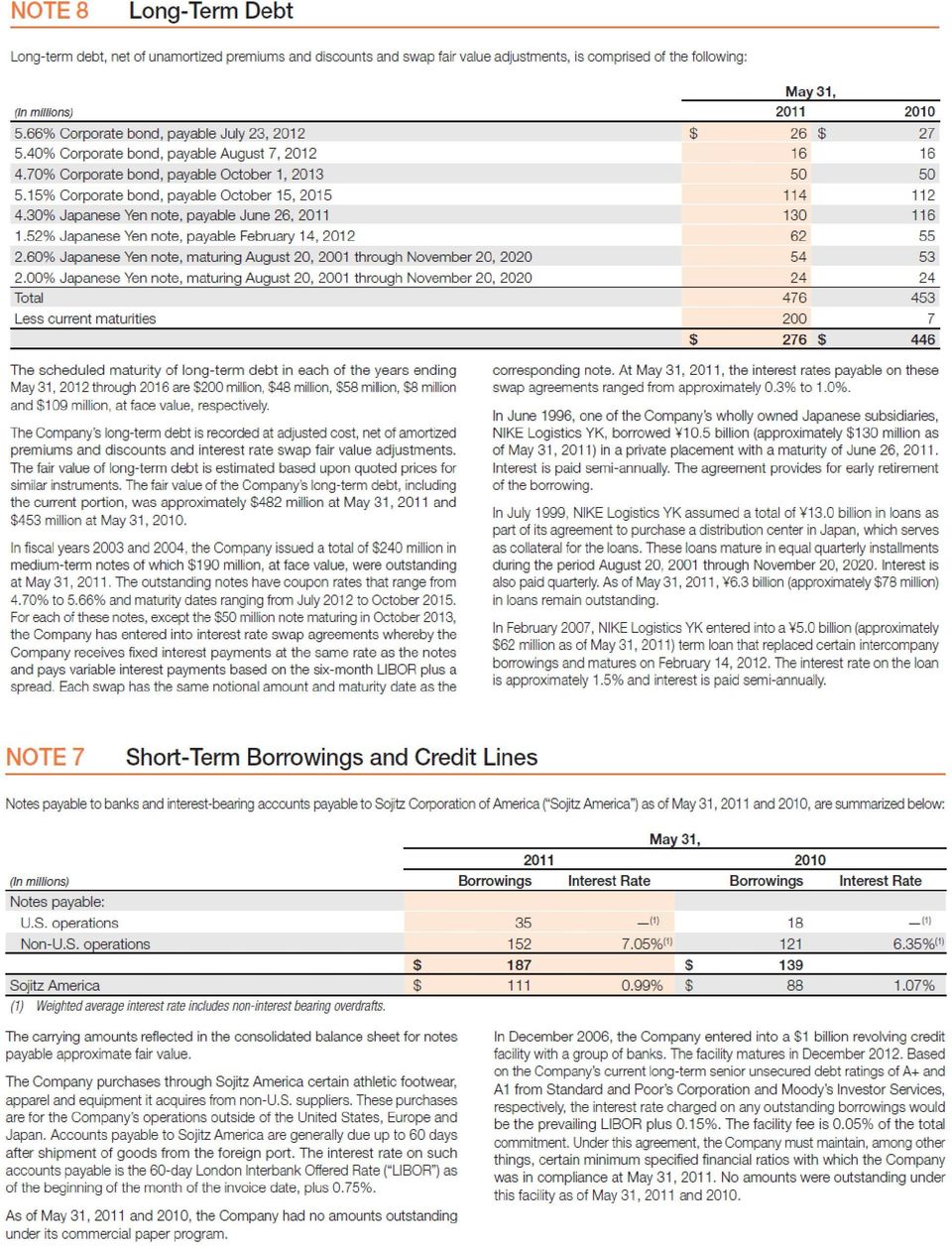

4 4. Cost of Capital for Nike: In this problem, you will calculate the cost of equity and weighted average cost of capital for Nike as of May 31, Be sure to explain any assumptions you make to arrive at your answers. a. Collect monthly return data for both Nike and the S&P 500 Index for the 60-month period ending in May Using this data, estimate the Beta for Nike based on a market model (CAPM) regression. Using this Beta estimate, calculate the cost of equity (K e ) for Nike based on the CAPM model. Note that you must choose an appropriate risk-free rate and market risk premium to use in the CAPM equation. Briefly explain your choice for each of these variables. I will assume that the risk-free rate equals the 10-year Treasury Yield as of 5/30/11, or 3.05%. The market model regression using 60-months of returns for Nike and the S&P gives a Beta estimate of (see the attached graph). I will use a market risk premium of 4.5%. This estimate reflects both the historical equity risk premium relative to U.S. Treasury Bonds and the implied equity premium calculations we discussed in class. Using this information, the cost of equity can be calculated as: K e = 3.05% (4.5%) = 7.21% b. Estimate the market value of debt and the market value of equity for Nike as of May 31, Use the firm's A+ rating and the default spreads provided in the course notes to estimate the firm's cost of debt (K d ). Using these estimates and your answer to (a), calculate the weighted average cost of capital (WACC) for Nike. Assume a marginal tax rate of 36%. Based on the default spread table provided in the class notes, the average default spread on A+ rated corporate bonds is 1.041%. Combining this with the risk-free rate from (a) gives a cost of debt equal to 4.09% (3.05% %). In the Notes to the Consolidated Financial Statements, Nike estimates the market value of longterm debt (including current installments) to be $482 million (compared to a book value of $476m). Combining this with the firm's short-term debt valued at $187 million gives a total market value for debt of $669 million. Using methods we will discuss in Lecture 3, I find that the debt value of Nike's operating leases equals $1,584.5 million (see the attached table). Together, this gives a total adjusted market value of debt equal to $2,253.5 billion. Nike's shares outstanding include 90.0 million class A shares and million class B shares. Treating these shares as identical and multiplying by the stock price as of May 31, 2011 ($84.45) gives a total equity market value of $ billion. To this, we must add the after-tax value of employee stock options (which will be discussed in more detail in Lecture 5), or $817.4 million. This gives an adjusted market value of equity equal to $ billion. Ignoring the adjustments for operating lease debt and employee stock options, the weighted average cost of capital (WACC) is calculated as: WACC = 7.21% + (4.09%)(1.36) = 7.14% After incorporating operating lease debt and employee stock options, the weighted average cost of capital (WACC) is calculated as: WACC = 7.21% + (4.09%)(1.36) = 6.97%

5 5. Synthetic Debt Ratings: c. The following information was taken from the income statement and balance sheet of a real firm. Use this information to calculate the EBITDA-to-interest ratio, the Debt-to-EBITDA ratio, the Debt-to-Capital ratio, and the Return on Capital. Based on the values you calculate, use the S&P Ratings Guide on the attached page to estimate a synthetic debt rating for this firm. EBIT = $5,839 EBITDA = $7,455 Interest Expense = $530 Total Debt = $9,749 Stockholder s Equity = $18,889 Tax Rate = 36.7% EBITDA Interest Debt EBITDA = 7455 = = = Debt Capital 9749 = = 34.04% (1.367) ROC = = 12.91% Based on these ratios, the firm is roughly similar to other firms in the low A or high BBB ratings categories. d. The firm described above has significant operating leases. The notes to the financial statements show that the firm s operating lease expenses during the period were $823, of which $289 is estimated to be interest expense. In addition, you calculate the debt value of operating leases to be $5,927. Recalculate the ratios above incorporating this new information. Based on these corrected values, use the S&P Ratings Guide to estimate a revised synthetic debt rating for this firm. EBIT = $5, = $6,128 EBITDA = $7, = $8,278 Interest Expense = = $819 Total Debt = 9, ,927 = $15,676 Stockholder s Equity = $18,889 Tax Rate = 36.7% EBITDA Interest Debt EBITDA = 8278 = = = Debt Capital = = 45.35% (1.367) ROC = = 11.22% Based on these revised ratios, the firm appears to fall at the middle or high end of BBB rated firms (or the very low end of A rated firms). Note that I assume the operating lease expense of $823 is a combination of interest expense and depreciation.

6 Question 4 Regression Output: SUMMARY OUTPUT Regression Statistics R Square Observations 60 Coefficients Standard Error t Stat P-value Lower 95% Upper 95% Intercept X Variable y = x R² = Nike Return 20.00% 15.00% 10.00% 5.00% 0.00% % % % -5.00% 0.00% 5.00% 10.00% 15.00% -5.00% % % %

7

8 Question 4 Nike Operating Lease Information: Inputs: 5/31/2011 5/31/2010 5/31/2009 Cost of Debt 4.09% 4.09% 4.09% Round Annuity Length? (1=yes, 0=no) Operating Lease Commitments (mil) 2013 (or year +1) $374.0 $334.0 $ (or year +2) $310.0 $264.0 $ (or year +3) $253.0 $220.0 $ (or year +4) $198.0 $177.0 $ (or year +5) $174.0 $148.0 $168.6 >2017 (after year ) $535.0 $466.0 $588.5 Total $1,844.0 $1,609.0 $1,797.8 Estimation (based on yr 5 pymt): Year 5 payment $174.0 $148.0 $168.6 Annuity yrs PV of Lease Pmts $1,584.5 $1, ,529.0

: Year 5 payment $174.0 $148.0 $168.6 Annuity yrs 3.1 3.")

9 Question 4 Nike Employee Stock Options Valuation: Employee Options at Nike updated 2011 Black-Scholes Option Pricing Model Inputs: Black-Scholes Option Pricing Model (with dilution) Inputs (with dilution effects): Stock Price (S) $84.45 Stock Price (S) $84.45 Strike Price (X) $51.29 Strike Price (X) $51.29 Volatility (σ) 31.50% Volatility (σ) 31.50% Risk-free Rate 3.05% 1.70% Risk-free Rate 3.05% Time to expiration (T) 6.00 yrs Time to expiration (T) 6.00 yrs Dividend Yield 1.60% Dividend Yield 1.60% # of Options (mil) 35 # of Options (mil) 35 # Shares Outstanding (mil) 468 # Shares Outstanding (mil) 468 Output: Output: Adjusted S (dilution) $81.16 D D D D N(D1) N(D1) N(D2) N(D2) Call Price $39.47 Call Price $36.87 Put Price $5.46 Put Price $5.86 Value of Call Options (mil) $1, Value of Call Options (mil) $1, After-tax Option Value (mil) $ After-tax Option Value (mil) $817.38

35 # of Options (mil) 35 # Shares Outstanding (mil) 468 # Shares Outstanding (mil) 468 Output: Output: Adjusted S (dilution) $81.16 D1 1.14483 D1 1.09328 D2 0.37324 D2 0.")

10

NIKE Case Study Solutions

NIKE Case Study Solutions Professor Corwin This case study includes several problems related to the valuation of Nike. We will work through these problems throughout the course to demonstrate some of the

NIKE Case Study Solutions Professor Corwin This case study includes several problems related to the valuation of Nike. We will work through these problems throughout the course to demonstrate some of the

I. Estimating Discount Rates

I. Estimating Discount Rates DCF Valuation Aswath Damodaran 1 Estimating Inputs: Discount Rates Critical ingredient in discounted cashflow valuation. Errors in estimating the discount rate or mismatching

I. Estimating Discount Rates DCF Valuation Aswath Damodaran 1 Estimating Inputs: Discount Rates Critical ingredient in discounted cashflow valuation. Errors in estimating the discount rate or mismatching

FINC 3630: Advanced Business Finance Additional Practice Problems

FINC 3630: Advanced Business Finance Additional Practice Problems Accounting For Financial Management 1. Calculate free cash flow for Home Depot for the fiscal year-ended February 1, 2015 (the 2014 fiscal

FINC 3630: Advanced Business Finance Additional Practice Problems Accounting For Financial Management 1. Calculate free cash flow for Home Depot for the fiscal year-ended February 1, 2015 (the 2014 fiscal

Homework Solutions - Lecture 4

Homework Solutions - Lecture 4 1. Estimate fundamental growth in EBIT for Nike based on the firm s reinvestment rate and ROC in the most recent year. Be sure to incorporate any necessary adjustments made

Homework Solutions - Lecture 4 1. Estimate fundamental growth in EBIT for Nike based on the firm s reinvestment rate and ROC in the most recent year. Be sure to incorporate any necessary adjustments made

Estimating Beta. Aswath Damodaran

Estimating Beta The standard procedure for estimating betas is to regress stock returns (R j ) against market returns (R m ) - R j = a + b R m where a is the intercept and b is the slope of the regression.

Estimating Beta The standard procedure for estimating betas is to regress stock returns (R j ) against market returns (R m ) - R j = a + b R m where a is the intercept and b is the slope of the regression.

Cost of Capital and Project Valuation

Cost of Capital and Project Valuation 1 Background Firm organization There are four types: sole proprietorships partnerships limited liability companies corporations Each organizational form has different

Cost of Capital and Project Valuation 1 Background Firm organization There are four types: sole proprietorships partnerships limited liability companies corporations Each organizational form has different

Problem 1 Problem 2 Problem 3

Problem 1 (1) Book Value Debt/Equity Ratio = 2500/2500 = 100% Market Value of Equity = 50 million * $ 80 = $4,000 Market Value of Debt =.80 * 2500 = $2,000 Debt/Equity Ratio in market value terms = 2000/4000

Problem 1 (1) Book Value Debt/Equity Ratio = 2500/2500 = 100% Market Value of Equity = 50 million * $ 80 = $4,000 Market Value of Debt =.80 * 2500 = $2,000 Debt/Equity Ratio in market value terms = 2000/4000

CHAPTER 8. Problems and Questions

CHAPTER 8 Problems and Questions 1. Plastico, a manufacturer of consumer plastic products, is evaluating its capital structure. The balance sheet of the company is as follows (in millions): Assets Liabilities

CHAPTER 8 Problems and Questions 1. Plastico, a manufacturer of consumer plastic products, is evaluating its capital structure. The balance sheet of the company is as follows (in millions): Assets Liabilities

Forecasting and Valuation of Enterprise Cash Flows 1. Dan Gode and James Ohlson

Forecasting and Valuation of Enterprise Cash Flows 1 1. Overview FORECASTING AND VALUATION OF ENTERPRISE CASH FLOWS Dan Gode and James Ohlson A decision to invest in a stock proceeds in two major steps

Forecasting and Valuation of Enterprise Cash Flows 1 1. Overview FORECASTING AND VALUATION OF ENTERPRISE CASH FLOWS Dan Gode and James Ohlson A decision to invest in a stock proceeds in two major steps

Value of Equity and Per Share Value when there are options and warrants outstanding. Aswath Damodaran

Value of Equity and Per Share Value when there are options and warrants outstanding Aswath Damodaran 1 Equity Value and Per Share Value: A Test Assume that you have done an equity valuation of Microsoft.

Value of Equity and Per Share Value when there are options and warrants outstanding Aswath Damodaran 1 Equity Value and Per Share Value: A Test Assume that you have done an equity valuation of Microsoft.

Stock Valuation: Gordon Growth Model. Week 2

Stock Valuation: Gordon Growth Model Week 2 Approaches to Valuation 1. Discounted Cash Flow Valuation The value of an asset is the sum of the discounted cash flows. 2. Contingent Claim Valuation A contingent

Stock Valuation: Gordon Growth Model Week 2 Approaches to Valuation 1. Discounted Cash Flow Valuation The value of an asset is the sum of the discounted cash flows. 2. Contingent Claim Valuation A contingent

USING THE EQUITY RESIDUAL APPROACH TO VALUATION: AN EXAMPLE

Graduate School of Business Administration - University of Virginia USING THE EQUITY RESIDUAL APPROACH TO VALUATION: AN EXAMPLE Planned changes in capital structure over time increase the complexity of

Graduate School of Business Administration - University of Virginia USING THE EQUITY RESIDUAL APPROACH TO VALUATION: AN EXAMPLE Planned changes in capital structure over time increase the complexity of

CHAPTER 15 FIRM VALUATION: COST OF CAPITAL AND APV APPROACHES

0 CHAPTER 15 FIRM VALUATION: COST OF CAPITAL AND APV APPROACHES In the last two chapters, we examined two approaches to valuing the equity in the firm -- the dividend discount model and the FCFE valuation

0 CHAPTER 15 FIRM VALUATION: COST OF CAPITAL AND APV APPROACHES In the last two chapters, we examined two approaches to valuing the equity in the firm -- the dividend discount model and the FCFE valuation

Finding the Right Financing Mix: The Capital Structure Decision

Finding the Right Financing Mix: The Capital Structure Decision Aswath Damodaran Stern School of Business Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum

Finding the Right Financing Mix: The Capital Structure Decision Aswath Damodaran Stern School of Business Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum

Chapter 13, ROIC and WACC

Chapter 13, ROIC and WACC Lakehead University Winter 2005 Role of the CFO The Chief Financial Officer (CFO) is involved in the following decisions: Management Decisions Financing Decisions Investment Decisions

Chapter 13, ROIC and WACC Lakehead University Winter 2005 Role of the CFO The Chief Financial Officer (CFO) is involved in the following decisions: Management Decisions Financing Decisions Investment Decisions

Chapter 17 Does Debt Policy Matter?

Chapter 17 Does Debt Policy Matter? Multiple Choice Questions 1. When a firm has no debt, then such a firm is known as: (I) an unlevered firm (II) a levered firm (III) an all-equity firm D) I and III only

Chapter 17 Does Debt Policy Matter? Multiple Choice Questions 1. When a firm has no debt, then such a firm is known as: (I) an unlevered firm (II) a levered firm (III) an all-equity firm D) I and III only

Corporate Finance: Final Exam

Corporate Finance: Final Exam Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. For partial credit, when discounting, please show the discount rate

Corporate Finance: Final Exam Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. For partial credit, when discounting, please show the discount rate

DUKE UNIVERSITY Fuqua School of Business. FINANCE 351 - CORPORATE FINANCE Problem Set #4 Prof. Simon Gervais Fall 2011 Term 2.

DUK UNIRSITY Fuqua School of Business FINANC 351 - CORPORAT FINANC Problem Set #4 Prof. Simon Gervais Fall 2011 Term 2 Questions 1. Suppose the corporate tax rate is 40%. Consider a firm that earns $1,000

DUK UNIRSITY Fuqua School of Business FINANC 351 - CORPORAT FINANC Problem Set #4 Prof. Simon Gervais Fall 2011 Term 2 Questions 1. Suppose the corporate tax rate is 40%. Consider a firm that earns $1,000

Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.)

") Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.) The primary focus of the next two chapters will be to examine the debt/equity choice by firms. In particular,

Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.) The primary focus of the next two chapters will be to examine the debt/equity choice by firms. In particular,

DUKE UNIVERSITY Fuqua School of Business. FINANCE 351 - CORPORATE FINANCE Problem Set #7 Prof. Simon Gervais Fall 2011 Term 2.

DUKE UNIVERSITY Fuqua School of Business FINANCE 351 - CORPORATE FINANCE Problem Set #7 Prof. Simon Gervais Fall 2011 Term 2 Questions 1. Suppose the corporate tax rate is 40%, and investors pay a tax

DUKE UNIVERSITY Fuqua School of Business FINANCE 351 - CORPORATE FINANCE Problem Set #7 Prof. Simon Gervais Fall 2011 Term 2 Questions 1. Suppose the corporate tax rate is 40%, and investors pay a tax

CHAPTER 12 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING

CHAPTER 12 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

CHAPTER 12 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

Using the Bloomberg terminal for data

Using the Bloomberg terminal for data Contents of Package 1.Getting information on your company Pages 2-31 2.Getting information on comparable companies Pages 32-39 3.Getting macro economic information

Using the Bloomberg terminal for data Contents of Package 1.Getting information on your company Pages 2-31 2.Getting information on comparable companies Pages 32-39 3.Getting macro economic information

Equity Value and Per Share Value: A Test

Equity Value and Per Share Value: A Test Assume that you have done an equity valuation of Microsoft. The total value for equity is estimated to be $ 400 billion and there are 5 billion shares outstanding.

Equity Value and Per Share Value: A Test Assume that you have done an equity valuation of Microsoft. The total value for equity is estimated to be $ 400 billion and there are 5 billion shares outstanding.

TIP If you do not understand something,

Valuing common stocks Application of the DCF approach TIP If you do not understand something, ask me! The plan of the lecture Review what we have accomplished in the last lecture Some terms about stocks

Valuing common stocks Application of the DCF approach TIP If you do not understand something, ask me! The plan of the lecture Review what we have accomplished in the last lecture Some terms about stocks

Corporate Finance, Fall 03 Exam #2 review questions (full solutions at end of document)

") Corporate Finance, Fall 03 Exam #2 review questions (full solutions at end of document) 1. Portfolio risk & return. Idaho Slopes (IS) and Dakota Steppes (DS) are both seasonal businesses. IS is a downhill

Corporate Finance, Fall 03 Exam #2 review questions (full solutions at end of document) 1. Portfolio risk & return. Idaho Slopes (IS) and Dakota Steppes (DS) are both seasonal businesses. IS is a downhill

Napoli Pizza wants to determine its optimal capital structure

Napoli Pizza wants to determine its optimal capital structure ABSTRACT Brad Stevenson Daniel Bauer David Collins Keith Richardson This case is based on an actual business decision that was made by a small,

Napoli Pizza wants to determine its optimal capital structure ABSTRACT Brad Stevenson Daniel Bauer David Collins Keith Richardson This case is based on an actual business decision that was made by a small,

CHAPTER 14 COST OF CAPITAL

CHAPTER 14 COST OF CAPITAL Answers to Concepts Review and Critical Thinking Questions 1. It is the minimum rate of return the firm must earn overall on its existing assets. If it earns more than this,

CHAPTER 14 COST OF CAPITAL Answers to Concepts Review and Critical Thinking Questions 1. It is the minimum rate of return the firm must earn overall on its existing assets. If it earns more than this,

CIS September 2012 Exam Diet. Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis

CIS September 2012 Exam Diet Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis Corporate Finance (1 13) 1. Assume a firm issues N1 billion in debt

CIS September 2012 Exam Diet Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis Corporate Finance (1 13) 1. Assume a firm issues N1 billion in debt

Finance 3130 Corporate Finiance Sample Final Exam Spring 2012

Finance 3130 Corporate Finiance Sample Final Exam Spring 2012 True/False Indicate whether the statement is true or falsewith A for true and B for false. 1. Interest paid by a corporation is a tax deduction

Finance 3130 Corporate Finiance Sample Final Exam Spring 2012 True/False Indicate whether the statement is true or falsewith A for true and B for false. 1. Interest paid by a corporation is a tax deduction

Use the table for the questions 18 and 19 below.

Use the table for the questions 18 and 19 below. The following table summarizes prices of various default-free zero-coupon bonds (expressed as a percentage of face value): Maturity (years) 1 3 4 5 Price

Use the table for the questions 18 and 19 below. The following table summarizes prices of various default-free zero-coupon bonds (expressed as a percentage of face value): Maturity (years) 1 3 4 5 Price

VALUATION JC PENNEY (NYSE:JCP)

") VALUATION JC PENNEY (NYSE:JCP) Prepared for Dr. K.C. Chen California State University, Fresno Prepared by Sicilia Sendjaja Finance 129-Student Investment Funds December 15 th, 2009 California State University,

VALUATION JC PENNEY (NYSE:JCP) Prepared for Dr. K.C. Chen California State University, Fresno Prepared by Sicilia Sendjaja Finance 129-Student Investment Funds December 15 th, 2009 California State University,

STUDENT CAN HAVE ONE LETTER SIZE FORMULA SHEET PREPARED BY STUDENT HIM/HERSELF. FINANCIAL CALCULATOR/TI-83 OR THEIR EQUIVALENCES ARE ALLOWED.

Test III-FINN3120-090 Fall 2009 (2.5 PTS PER QUESTION. MAX 100 PTS) Type A Name ID PRINT YOUR NAME AND ID ON THE TEST, ANSWER SHEET AND FORMULA SHEET. TURN IN THE TEST, OPSCAN ANSWER SHEET AND FORMULA

Test III-FINN3120-090 Fall 2009 (2.5 PTS PER QUESTION. MAX 100 PTS) Type A Name ID PRINT YOUR NAME AND ID ON THE TEST, ANSWER SHEET AND FORMULA SHEET. TURN IN THE TEST, OPSCAN ANSWER SHEET AND FORMULA

Employee Options, Restricted Stock and Value. Aswath Damodaran 1

Employee Options, Restricted Stock and Value 1 Basic Proposition on Options Any options issued by a firm, whether to management or employees or to investors (convertibles and warrants) create claims on

Employee Options, Restricted Stock and Value 1 Basic Proposition on Options Any options issued by a firm, whether to management or employees or to investors (convertibles and warrants) create claims on

E. V. Bulyatkin CAPITAL STRUCTURE

E. V. Bulyatkin Graduate Student Edinburgh University Business School CAPITAL STRUCTURE Abstract. This paper aims to analyze the current capital structure of Lufthansa in order to increase market value

E. V. Bulyatkin Graduate Student Edinburgh University Business School CAPITAL STRUCTURE Abstract. This paper aims to analyze the current capital structure of Lufthansa in order to increase market value

Financial Formulas. 5/2000 Chapter 3 Financial Formulas i

Financial Formulas 3 Financial Formulas i In this chapter 1 Formulas Used in Financial Calculations 1 Statements of Changes in Financial Position (Total $) 1 Cash Flow ($ millions) 1 Statements of Changes

Financial Formulas 3 Financial Formulas i In this chapter 1 Formulas Used in Financial Calculations 1 Statements of Changes in Financial Position (Total $) 1 Cash Flow ($ millions) 1 Statements of Changes

CHAPTER 11 Questions and Problems

1 CHAPTER 11 Questions and Problems (In the problems below, you can use a risk premium of 5.5% and a tax rate of 40% if either is not specified) 1. Stock buybacks really do not return cash to stockholders,

1 CHAPTER 11 Questions and Problems (In the problems below, you can use a risk premium of 5.5% and a tax rate of 40% if either is not specified) 1. Stock buybacks really do not return cash to stockholders,

Chapter 14 Capital Structure in a Perfect Market

Chapter 14 Capital Structure in a Perfect Market 14-1. Consider a project with free cash flows in one year of $130,000 or $180,000, with each outcome being equally likely. The initial investment required

Chapter 14 Capital Structure in a Perfect Market 14-1. Consider a project with free cash flows in one year of $130,000 or $180,000, with each outcome being equally likely. The initial investment required

Expected default frequency

KM Model Expected default frequency Expected default frequency (EDF) is a forward-looking measure of actual probability of default. EDF is firm specific. KM model is based on the structural approach to

KM Model Expected default frequency Expected default frequency (EDF) is a forward-looking measure of actual probability of default. EDF is firm specific. KM model is based on the structural approach to

SOLUTIONS. Practice questions. Multiple Choice

Practice questions Multiple Choice 1. XYZ has $25,000 of debt outstanding and a book value of equity of $25,000. The company has 10,000 shares outstanding and a stock price of $10. If the unlevered beta

Practice questions Multiple Choice 1. XYZ has $25,000 of debt outstanding and a book value of equity of $25,000. The company has 10,000 shares outstanding and a stock price of $10. If the unlevered beta

Valuation. Aswath Damodaran Home Page: http://www.stern.nyu.edu/~adamodar Email: [email protected] This presentation is under seminars.

Valuation Aswath Damodaran Home Page: http://www.stern.nyu.edu/~adamodar Email: [email protected] This presentation is under seminars. Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand

Valuation Aswath Damodaran Home Page: http://www.stern.nyu.edu/~adamodar Email: [email protected] This presentation is under seminars. Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand

Practice Exam (Solutions)

") Practice Exam (Solutions) June 6, 2008 Course: Finance for AEO Length: 2 hours Lecturer: Paul Sengmüller Students are expected to conduct themselves properly during examinations and to obey any instructions

Practice Exam (Solutions) June 6, 2008 Course: Finance for AEO Length: 2 hours Lecturer: Paul Sengmüller Students are expected to conduct themselves properly during examinations and to obey any instructions

Models of Risk and Return

Models of Risk and Return Aswath Damodaran Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for

Models of Risk and Return Aswath Damodaran Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for

( ) ( )( ) ( ) 2 ( ) 3. n n = 100 000 1+ 0.10 = 100 000 1.331 = 133100

( )( ) ( ) 2 ( ) 3. n n = 100 000 1+ 0.10 = 100 000 1.331 = 133100") Mariusz Próchniak Chair of Economics II Warsaw School of Economics CAPITAL BUDGETING Managerial Economics 1 2 1 Future value (FV) r annual interest rate B the amount of money held today Interest is compounded

Mariusz Próchniak Chair of Economics II Warsaw School of Economics CAPITAL BUDGETING Managerial Economics 1 2 1 Future value (FV) r annual interest rate B the amount of money held today Interest is compounded

] (3.3) ] (1 + r)t (3.4)

![] (3.3) ] (1 + r)t (3.4)](/thumbs/39/18539117.jpg "] (3.3) ] (1 + r)t (3.4)") Present value = future value after t periods (3.1) (1 + r) t PV of perpetuity = C = cash payment (3.2) r interest rate Present value of t-year annuity = C [ 1 1 ] (3.3) r r(1 + r) t Future value of annuity

Present value = future value after t periods (3.1) (1 + r) t PV of perpetuity = C = cash payment (3.2) r interest rate Present value of t-year annuity = C [ 1 1 ] (3.3) r r(1 + r) t Future value of annuity

Equity Analysis and Capital Structure. A New Venture s Perspective

Equity Analysis and Capital Structure A New Venture s Perspective 1 Venture s Capital Structure ASSETS Short- term Assets Cash A/R Inventories Long- term Assets Plant and Equipment Intellectual Property

Equity Analysis and Capital Structure A New Venture s Perspective 1 Venture s Capital Structure ASSETS Short- term Assets Cash A/R Inventories Long- term Assets Plant and Equipment Intellectual Property

Achievement of Market-Friendly Initiatives and Results Program (AMIR 2.0 Program) Funded by U.S. Agency for International Development

Funded by U.S. Agency for International Development") Achievement of Market-Friendly Initiatives and Results Program (AMIR 2.0 Program) Funded by U.S. Agency for International Development Equity Analysis, Portfolio Management, and Real Estate Practice Quizzes

Achievement of Market-Friendly Initiatives and Results Program (AMIR 2.0 Program) Funded by U.S. Agency for International Development Equity Analysis, Portfolio Management, and Real Estate Practice Quizzes

Call and Put. Options. American and European Options. Option Terminology. Payoffs of European Options. Different Types of Options

Call and Put Options A call option gives its holder the right to purchase an asset for a specified price, called the strike price, on or before some specified expiration date. A put option gives its holder

Call and Put Options A call option gives its holder the right to purchase an asset for a specified price, called the strike price, on or before some specified expiration date. A put option gives its holder

If you ignore taxes in this problem and there is no debt outstanding: EPS = EBIT/shares outstanding = $14,000/2,500 = $5.60

Problems Relating to Capital Structure and Leverage 1. EBIT and Leverage Money Inc., has no debt outstanding and a total market value of $150,000. Earnings before interest and taxes [EBIT] are projected

Problems Relating to Capital Structure and Leverage 1. EBIT and Leverage Money Inc., has no debt outstanding and a total market value of $150,000. Earnings before interest and taxes [EBIT] are projected

LECTURE- 4. Valuing stocks Berk, De Marzo Chapter 9

1 LECTURE- 4 Valuing stocks Berk, De Marzo Chapter 9 2 The Dividend Discount Model A One-Year Investor Potential Cash Flows Dividend Sale of Stock Timeline for One-Year Investor Since the cash flows are

1 LECTURE- 4 Valuing stocks Berk, De Marzo Chapter 9 2 The Dividend Discount Model A One-Year Investor Potential Cash Flows Dividend Sale of Stock Timeline for One-Year Investor Since the cash flows are

How To Calculate Financial Leverage Ratio

What Do Short-Term Liquidity Ratios Measure? What Is Working Capital? HOCK international - 2004 1 HOCK international - 2004 2 How Is the Current Ratio Calculated? How Is the Quick Ratio Calculated? HOCK

What Do Short-Term Liquidity Ratios Measure? What Is Working Capital? HOCK international - 2004 1 HOCK international - 2004 2 How Is the Current Ratio Calculated? How Is the Quick Ratio Calculated? HOCK

Chapter 14. Web Extension: Financing Feedbacks and Alternative Forecasting Techniques

Chapter 14 Web Extension: Financing Feedbacks and Alternative Forecasting Techniques I n Chapter 14 we forecasted financial statements under the assumption that the firm s interest expense can be estimated

Chapter 14 Web Extension: Financing Feedbacks and Alternative Forecasting Techniques I n Chapter 14 we forecasted financial statements under the assumption that the firm s interest expense can be estimated

Finance 2 for IBA (30J201) F. Feriozzi Re-sit exam June 18 th, 2012. Part One: Multiple-Choice Questions (45 points)

F. Feriozzi Re-sit exam June 18 th, 2012. Part One: Multiple-Choice Questions (45 points)") Finance 2 for IBA (30J201) F. Feriozzi Re-sit exam June 18 th, 2012 Part One: Multiple-Choice Questions (45 points) Question 1 Assume that capital markets are perfect. Which of the following statements

Finance 2 for IBA (30J201) F. Feriozzi Re-sit exam June 18 th, 2012 Part One: Multiple-Choice Questions (45 points) Question 1 Assume that capital markets are perfect. Which of the following statements

II. Estimating Cash Flows

II. Estimating Cash Flows DCF Valuation Aswath Damodaran 61 Steps in Cash Flow Estimation Estimate the current earnings of the firm If looking at cash flows to equity, look at earnings after interest expenses

II. Estimating Cash Flows DCF Valuation Aswath Damodaran 61 Steps in Cash Flow Estimation Estimate the current earnings of the firm If looking at cash flows to equity, look at earnings after interest expenses

The Weighted Average Cost of Capital

The Weighted Average Cost of Capital What Does "Cost of Capital" Mean? "Cost of capital" is defined as "the opportunity cost of all capital invested in an enterprise." Let's dissect this definition: Opportunity

The Weighted Average Cost of Capital What Does "Cost of Capital" Mean? "Cost of capital" is defined as "the opportunity cost of all capital invested in an enterprise." Let's dissect this definition: Opportunity

INTERVIEWS - FINANCIAL MODELING

420 W. 118th Street, Room 420 New York, NY 10027 P: 212-854-4613 F: 212-854-6190 www.sipa.columbia.edu/ocs INTERVIEWS - FINANCIAL MODELING Basic valuation concepts are among the most popular technical

420 W. 118th Street, Room 420 New York, NY 10027 P: 212-854-4613 F: 212-854-6190 www.sipa.columbia.edu/ocs INTERVIEWS - FINANCIAL MODELING Basic valuation concepts are among the most popular technical

Equity Valuation. Lecture Notes # 8. 3 Choice of the Appropriate Discount Rate 2. 4 Future Cash Flows: the Dividend Discount Model (DDM) 3

3") Equity Valuation Lecture Notes # 8 Contents About Valuation 2 2 Present-Values 2 3 Choice of the Appropriate Discount Rate 2 4 Future Cash Flows: the Dividend Discount Model (DDM) 3 5 The Two-Stage Dividend-Growth

Equity Valuation Lecture Notes # 8 Contents About Valuation 2 2 Present-Values 2 3 Choice of the Appropriate Discount Rate 2 4 Future Cash Flows: the Dividend Discount Model (DDM) 3 5 The Two-Stage Dividend-Growth

Review for Exam 3. Instructions: Please read carefully

Review for Exam 3 Instructions: Please read carefully The exam will have 25 multiple choice questions and 5 work problems. You are not responsible for any topics that are not covered in the lecture note

Review for Exam 3 Instructions: Please read carefully The exam will have 25 multiple choice questions and 5 work problems. You are not responsible for any topics that are not covered in the lecture note

Time allowed Formulae Sheet, Present Value and Annuity Tables are on

Fundamentals Level Skills Module Financial Management Friday 15 June 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Fundamentals Level Skills Module Financial Management Friday 15 June 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II + III

SOLUTIONS RE-EXAMS 2014 II + III") TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II III Instructions 1. Only one problem should be treated on each sheet of paper and only one side of the sheet should be used. 2. The solutions folder

TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II III Instructions 1. Only one problem should be treated on each sheet of paper and only one side of the sheet should be used. 2. The solutions folder

Test3. Pessimistic Most Likely Optimistic Total Revenues 30 50 65 Total Costs -25-20 -15

Test3 1. The market value of Charcoal Corporation's common stock is $20 million, and the market value of its riskfree debt is $5 million. The beta of the company's common stock is 1.25, and the market

Test3 1. The market value of Charcoal Corporation's common stock is $20 million, and the market value of its riskfree debt is $5 million. The beta of the company's common stock is 1.25, and the market

Web Extension: Financing Feedbacks and Alternative Forecasting Techniques

19878_09W_p001-009.qxd 3/10/06 9:56 AM Page 1 C H A P T E R 9 Web Extension: Financing Feedbacks and Alternative Forecasting Techniques IMAGE: GETTY IMAGES, INC., PHOTODISC COLLECTION In Chapter 9 we forecasted

19878_09W_p001-009.qxd 3/10/06 9:56 AM Page 1 C H A P T E R 9 Web Extension: Financing Feedbacks and Alternative Forecasting Techniques IMAGE: GETTY IMAGES, INC., PHOTODISC COLLECTION In Chapter 9 we forecasted

An Introduction to Institutions, Management, & Investments

An Introduction to Institutions, Management, & Investments TEMTH EBITIQM HERBERT B. MAYO The College of New Jersey *\ SOUTH-WESTERN t% CENGAGE Learning- Australia Brazil Japan Korea Mexico Singapore Spain

An Introduction to Institutions, Management, & Investments TEMTH EBITIQM HERBERT B. MAYO The College of New Jersey *\ SOUTH-WESTERN t% CENGAGE Learning- Australia Brazil Japan Korea Mexico Singapore Spain

CFAspace. CFA Level II. Provided by APF. Academy of Professional Finance 专 业 金 融 学 院

CFAspace Provided by APF CFA Level II Equity Investments Free Cash Flow Valuation Part I CFA Lecturer: Hillary Wang Content Free cash flow to the firm, free cash flow to equity Ownership perspective implicit

CFAspace Provided by APF CFA Level II Equity Investments Free Cash Flow Valuation Part I CFA Lecturer: Hillary Wang Content Free cash flow to the firm, free cash flow to equity Ownership perspective implicit

KEY EQUATIONS APPENDIX CHAPTER 2 CHAPTER 3

KEY EQUATIONS B CHAPTER 2 1. The balance sheet identity or equation: Assets Liabilities Shareholders equity [2.1] 2. The income statement equation: Revenues Expenses Income [2.2] 3.The cash flow identity:

KEY EQUATIONS B CHAPTER 2 1. The balance sheet identity or equation: Assets Liabilities Shareholders equity [2.1] 2. The income statement equation: Revenues Expenses Income [2.2] 3.The cash flow identity:

EMBA in Management & Finance. Corporate Finance. Eric Jondeau

EMBA in Management & Finance Corporate Finance EMBA in Management & Finance Lecture 5: Capital Budgeting For the Levered Firm Prospectus Recall that there are three questions in corporate finance. The

EMBA in Management & Finance Corporate Finance EMBA in Management & Finance Lecture 5: Capital Budgeting For the Levered Firm Prospectus Recall that there are three questions in corporate finance. The

Finding the Right Financing Mix: The Capital Structure Decision

Finding the Right Financing Mix: The Capital Structure Decision Neither a borrower nor a lender be Someone who obviously hated this part of corporate finance Aswath Damodaran 2 First Principles Invest

Finding the Right Financing Mix: The Capital Structure Decision Neither a borrower nor a lender be Someone who obviously hated this part of corporate finance Aswath Damodaran 2 First Principles Invest

CHAPTER 20. Hybrid Financing: Preferred Stock, Warrants, and Convertibles

CHAPTER 20 Hybrid Financing: Preferred Stock, Warrants, and Convertibles 1 Topics in Chapter Types of hybrid securities Preferred stock Warrants Convertibles Features and risk Cost of capital to issuers

CHAPTER 20 Hybrid Financing: Preferred Stock, Warrants, and Convertibles 1 Topics in Chapter Types of hybrid securities Preferred stock Warrants Convertibles Features and risk Cost of capital to issuers

PRACTICE EXAM QUESTIONS ON WACC

Dr. Sudhakar Raju Financial Statements Analysis (FN 6450) PRACTICE EXAM QUESTIONS ON WACC 1. The return shareholders require on their investment in a firm is called the: a. dividend yield. B. cost of equity.

Dr. Sudhakar Raju Financial Statements Analysis (FN 6450) PRACTICE EXAM QUESTIONS ON WACC 1. The return shareholders require on their investment in a firm is called the: a. dividend yield. B. cost of equity.

Leverage. FINANCE 350 Global Financial Management. Professor Alon Brav Fuqua School of Business Duke University. Overview

Leverage FINANCE 35 Global Financial Management Professor Alon Brav Fuqua School of Business Duke University Overview Capital Structure does not matter! Modigliani & Miller propositions Implications for

Leverage FINANCE 35 Global Financial Management Professor Alon Brav Fuqua School of Business Duke University Overview Capital Structure does not matter! Modigliani & Miller propositions Implications for

A Basic Introduction to the Methodology Used to Determine a Discount Rate

A Basic Introduction to the Methodology Used to Determine a Discount Rate By Dubravka Tosic, Ph.D. The term discount rate is one of the most fundamental, widely used terms in finance and economics. Whether

A Basic Introduction to the Methodology Used to Determine a Discount Rate By Dubravka Tosic, Ph.D. The term discount rate is one of the most fundamental, widely used terms in finance and economics. Whether

Chapter 7. . 1. component of the convertible can be estimated as 1100-796.15 = 303.85.

Chapter 7 7-1 Income bonds do share some characteristics with preferred stock. The primary difference is that interest paid on income bonds is tax deductible while preferred dividends are not. Income bondholders

Chapter 7 7-1 Income bonds do share some characteristics with preferred stock. The primary difference is that interest paid on income bonds is tax deductible while preferred dividends are not. Income bondholders

Determining the cost of equity

Determining the cost of equity Macroeconomic factors and the discount rate Baring Asset Management Limited 155 Bishopsgate London EC2M 3XY Tel: +44 (0)20 7628 6000 Fax: +44 (0)20 7638 7928 www.barings.com

Determining the cost of equity Macroeconomic factors and the discount rate Baring Asset Management Limited 155 Bishopsgate London EC2M 3XY Tel: +44 (0)20 7628 6000 Fax: +44 (0)20 7638 7928 www.barings.com

1 Pricing options using the Black Scholes formula

Lecture 9 Pricing options using the Black Scholes formula Exercise. Consider month options with exercise prices of K = 45. The variance of the underlying security is σ 2 = 0.20. The risk free interest

Lecture 9 Pricing options using the Black Scholes formula Exercise. Consider month options with exercise prices of K = 45. The variance of the underlying security is σ 2 = 0.20. The risk free interest

Finance Master. Winter 2015/16. Jprof. Narly Dwarkasing University of Bonn, IFS

Finance Master Winter 2015/16 Jprof. Narly Dwarkasing University of Bonn, IFS Chapter 2 Outline 2.1 Firms Disclosure of Financial Information 2.2 The Balance Sheet 2.3 The Income Statement 2.4 The Statement

Finance Master Winter 2015/16 Jprof. Narly Dwarkasing University of Bonn, IFS Chapter 2 Outline 2.1 Firms Disclosure of Financial Information 2.2 The Balance Sheet 2.3 The Income Statement 2.4 The Statement

Equity Valuation Project

Equity Valuation Project Group: Mike Altman Alison Birch Erin Burns Joe Faber Santosh Lakhan Josh Sullivan Companies: Affiliated Computer Services Apple Computer Biosite Gundle Environmental Systems Infosys

Equity Valuation Project Group: Mike Altman Alison Birch Erin Burns Joe Faber Santosh Lakhan Josh Sullivan Companies: Affiliated Computer Services Apple Computer Biosite Gundle Environmental Systems Infosys

Equity Market Risk Premium Research Summary. 12 April 2016

Equity Market Risk Premium Research Summary 12 April 2016 Introduction welcome If you are reading this, it is likely that you are in regular contact with KPMG on the topic of valuations. The goal of this

Equity Market Risk Premium Research Summary 12 April 2016 Introduction welcome If you are reading this, it is likely that you are in regular contact with KPMG on the topic of valuations. The goal of this

EMERSON AND SUBSIDIARIES CONSOLIDATED OPERATING RESULTS (AMOUNTS IN MILLIONS EXCEPT PER SHARE, UNAUDITED)

") CONSOLIDATED OPERATING RESULTS (AMOUNTS IN MILLIONS EXCEPT PER SHARE, UNAUDITED) TABLE 1 Quarter Ended March 31, Percent Change Net Sales $ 5,854 $ 5,919 1% Costs and expenses: Cost of sales 3,548 3,583

CONSOLIDATED OPERATING RESULTS (AMOUNTS IN MILLIONS EXCEPT PER SHARE, UNAUDITED) TABLE 1 Quarter Ended March 31, Percent Change Net Sales $ 5,854 $ 5,919 1% Costs and expenses: Cost of sales 3,548 3,583

How To Value A Private Firm

1 VALUING PRIVATE FIRMS So far in this book, we have concentrated on the valuation of publicly traded firms. In this chapter, we turn our attention to the thousands of firms that are private businesses.

1 VALUING PRIVATE FIRMS So far in this book, we have concentrated on the valuation of publicly traded firms. In this chapter, we turn our attention to the thousands of firms that are private businesses.

Using Bloomberg to get the Data you need

Using Bloomberg to get the Data you need 1 Contents of Package 1. Getting information on your company Pages 3-30 2. Getting information on comparable companies Pages 31-34 3. Getting macro economic information

Using Bloomberg to get the Data you need 1 Contents of Package 1. Getting information on your company Pages 3-30 2. Getting information on comparable companies Pages 31-34 3. Getting macro economic information

VALUING FINANCIAL SERVICE FIRMS

1 VALUING FINANCIAL SERVICE FIRMS Banks, insurance companies and other financial service firms pose a particular challenge for an analyst attempting to value them for two reasons. The first is the nature

1 VALUING FINANCIAL SERVICE FIRMS Banks, insurance companies and other financial service firms pose a particular challenge for an analyst attempting to value them for two reasons. The first is the nature

Chapters 3 and 13 Financial Statement and Cash Flow Analysis

Chapters 3 and 13 Financial Statement and Cash Flow Analysis Balance Sheet Assets Cash Inventory Accounts Receivable Property Plant Equipment Total Assets Liabilities and Shareholder s Equity Accounts

Chapters 3 and 13 Financial Statement and Cash Flow Analysis Balance Sheet Assets Cash Inventory Accounts Receivable Property Plant Equipment Total Assets Liabilities and Shareholder s Equity Accounts

MBA 8230 Corporation Finance (Part II) Practice Final Exam #2

Practice Final Exam #2") MBA 8230 Corporation Finance (Part II) Practice Final Exam #2 1. Which of the following input factors, if increased, would result in a decrease in the value of a call option? a. the volatility of the company's

MBA 8230 Corporation Finance (Part II) Practice Final Exam #2 1. Which of the following input factors, if increased, would result in a decrease in the value of a call option? a. the volatility of the company's

Risk and Return: Estimating Cost of Capital

Lecture: IX 1 Risk and Return: Estimating Cost o Capital The process: Estimate parameters or the risk-return model. Estimate cost o equity. Estimate cost o capital using capital structure (leverage) inormation.

Lecture: IX 1 Risk and Return: Estimating Cost o Capital The process: Estimate parameters or the risk-return model. Estimate cost o equity. Estimate cost o capital using capital structure (leverage) inormation.

Paper F9. Financial Management. Friday 6 December 2013. Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Fundamentals Level Skills Module Financial Management Friday 6 December 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Fundamentals Level Skills Module Financial Management Friday 6 December 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

HHIF Lecture Series: Discounted Cash Flow Model

HHIF Lecture Series: Discounted Cash Flow Model Alexander Remorov University of Toronto November 19, 2010 Alexander Remorov (University of Toronto) HHIF Lecture Series: Discounted Cash Flow Model 1 / 18

HHIF Lecture Series: Discounted Cash Flow Model Alexander Remorov University of Toronto November 19, 2010 Alexander Remorov (University of Toronto) HHIF Lecture Series: Discounted Cash Flow Model 1 / 18

Paper F9. Financial Management. Friday 7 June 2013. Fundamentals Level Skills Module. The Association of Chartered Certified Accountants.

Fundamentals Level Skills Module Financial Management Friday 7 June 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Fundamentals Level Skills Module Financial Management Friday 7 June 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

t = 1 2 3 1. Calculate the implied interest rates and graph the term structure of interest rates. t = 1 2 3 X t = 100 100 100 t = 1 2 3

MØA 155 PROBLEM SET: Summarizing Exercise 1. Present Value [3] You are given the following prices P t today for receiving risk free payments t periods from now. t = 1 2 3 P t = 0.95 0.9 0.85 1. Calculate

MØA 155 PROBLEM SET: Summarizing Exercise 1. Present Value [3] You are given the following prices P t today for receiving risk free payments t periods from now. t = 1 2 3 P t = 0.95 0.9 0.85 1. Calculate

A Piece of the Pie: Alternative Approaches to Allocating Value

A Piece of the Pie: Alternative Approaches to Allocating Value Cory Thompson, CFA, CIRA [email protected] Ryan Gandre, CFA [email protected] Introduction Enterprise value ( EV ) represents the sum of debt

A Piece of the Pie: Alternative Approaches to Allocating Value Cory Thompson, CFA, CIRA [email protected] Ryan Gandre, CFA [email protected] Introduction Enterprise value ( EV ) represents the sum of debt

Chapter 16 Hybrid and Derivative Securities

Chapter 16 Hybrid and Derivative Securities Solutions to Problems P16-1. LG 2: Lease Cash Flows Basic Firm Lease Payment Tax Benefit After-tax Cash Outflow [(1) (2)] Year (1) (2) (3) A 1 4 $1 00,000 $

Chapter 16 Hybrid and Derivative Securities Solutions to Problems P16-1. LG 2: Lease Cash Flows Basic Firm Lease Payment Tax Benefit After-tax Cash Outflow [(1) (2)] Year (1) (2) (3) A 1 4 $1 00,000 $

Chapter 22 Credit Risk

Chapter 22 Credit Risk May 22, 2009 20.28. Suppose a 3-year corporate bond provides a coupon of 7% per year payable semiannually and has a yield of 5% (expressed with semiannual compounding). The yields

Chapter 22 Credit Risk May 22, 2009 20.28. Suppose a 3-year corporate bond provides a coupon of 7% per year payable semiannually and has a yield of 5% (expressed with semiannual compounding). The yields

Discounted Cash Flow Valuation: The Inputs. Aswath Damodaran

Discounted Cash Flow Valuation: The Inputs Aswath Damodaran 1 The Key Inputs in DCF Valuation Discount Rate Cost of Equity, in valuing equity Cost of Capital, in valuing the firm Cash Flows Cash Flows

Discounted Cash Flow Valuation: The Inputs Aswath Damodaran 1 The Key Inputs in DCF Valuation Discount Rate Cost of Equity, in valuing equity Cost of Capital, in valuing the firm Cash Flows Cash Flows

1-3Q of FY2014 87.43 78.77 1-3Q of FY2013 74.47 51.74

January 30, 2015 Resona Holdings, Inc. Consolidated Financial Results for the Third Quarter of Fiscal Year 2014 (Nine months ended December 31, 2014/Unaudited) Code number: 8308 Stock

January 30, 2015 Resona Holdings, Inc. Consolidated Financial Results for the Third Quarter of Fiscal Year 2014 (Nine months ended December 31, 2014/Unaudited) Code number: 8308 Stock

CHAPTER 21: OPTION VALUATION

CHAPTER 21: OPTION VALUATION 1. Put values also must increase as the volatility of the underlying stock increases. We see this from the parity relation as follows: P = C + PV(X) S 0 + PV(Dividends). Given

CHAPTER 21: OPTION VALUATION 1. Put values also must increase as the volatility of the underlying stock increases. We see this from the parity relation as follows: P = C + PV(X) S 0 + PV(Dividends). Given

LOS 42.a: Define and interpret free cash flow to the firm (FCFF) and free cash flow to equity (FCFE).

and free cash flow to equity (FCFE).") The following is a review of the Equity Investments principles designed to address the learning outcome statements set forth by CFA Institute. This topic is also covered in: Free Cash Flow Valuation This

The following is a review of the Equity Investments principles designed to address the learning outcome statements set forth by CFA Institute. This topic is also covered in: Free Cash Flow Valuation This

- Once we have computed the costs of the individual components of the firm s financing,

WEIGHTED AVERAGE COST OF CAPITAL - Once we have computed the costs of the individual components of the firm s financing, we would assign weight to each financing source according to some standard and then

WEIGHTED AVERAGE COST OF CAPITAL - Once we have computed the costs of the individual components of the firm s financing, we would assign weight to each financing source according to some standard and then

Take-Home Problem Set

Georgia State University Department of Finance MBA 8622 Fall 2001 MBA 8622: Corporation Finance Take-Home Problem Set Instructors: Lalitha Naveen, N. Daniel, C.Hodges, A. Mettler, R. Morin, M. Shrikhande,

Georgia State University Department of Finance MBA 8622 Fall 2001 MBA 8622: Corporation Finance Take-Home Problem Set Instructors: Lalitha Naveen, N. Daniel, C.Hodges, A. Mettler, R. Morin, M. Shrikhande,

COST OF CAPITAL Compute the cost of debt. Compute the cost of preferred stock.

OBJECTIVE 1 Compute the cost of debt. The method of computing the yield to maturity for bonds will be used how to compute the cost of debt. Because interest payments are tax deductible, only after-tax

OBJECTIVE 1 Compute the cost of debt. The method of computing the yield to maturity for bonds will be used how to compute the cost of debt. Because interest payments are tax deductible, only after-tax

Bonds, Preferred Stock, and Common Stock

Bonds, Preferred Stock, and Common Stock I. Bonds 1. An investor has a required rate of return of 4% on a 1-year discount bond with a $100 face value. What is the most the investor would pay for 2. An

Bonds, Preferred Stock, and Common Stock I. Bonds 1. An investor has a required rate of return of 4% on a 1-year discount bond with a $100 face value. What is the most the investor would pay for 2. An