Fehmarnbelt Business Barometer

|

|

|

- Arthur Kelly

- 10 years ago

- Views:

Transcription

1 Fehmarnbelt Business Barometer Summary report Survey #1 Autumn 2012 Roskilde University ENSPAC Per Homann Jespersen Jean Endres Marianne Jakobsen Clément Guasco

2 Table of Contents Introduction... 4 Method... 5 Reach... 5 Fehmarn Business Barometer - Participants according to region and sector... 6 Results... 7 The near future... 7 Fehmarn Business Barometer Short term expectations by sector... 8 The future after the fixed link... 8 Cooperation across the border... 8 Fehmarn Business Barometer - Current, strategic and after the fixed link cross-border cooperation... 9 Cooperation activities Barriers Fehmarn Business Barometer Barriers for increased cooperation Millibars and Hectopascals Selected excerpts from the Barometer Survey Conclusion Appendix Appendix Appendix

3 Preamble The following report is the first of an annual series and it summarises the results of a survey carried out during the 3 rd quarter of 2012 by Roskilde University s ENSPAC Institute, in cooperation with Femern A/S and the Green STRING Corridor project, which is part of the European Union s INTERREG IV A programme. The information contained in this report highlights the main results obtained by the survey; for in depth information please refer to the appendices. 3

4 Introduction When the Fehmarnbelt Fixed Link between Germany and Denmark opens, it will create considerable potential for growth, regional development, business opportunities and increased cross-border cooperation between companies and institutions because of the ease of access between Central and Northern Europe. The regions closest to the underwater tunnel across the Fehmarnbelt and the companies that are active in them, are the ones with the greatest potential to be affected. Although there is the positive potential for growth, development and cooperation, there is also the possibility that differences between the regions such as the tax system, labour costs, purchasing power and other variables may cause an imbalance in the relative attractions of doing business, company migration and market competition. It is extremely important to attempt to assess in advance, which of these effects will occur, the extent to which different business sectors are preparing themselves and what their expectations are for the future. The ENSPAC Institute of Roskilde University has, in partnership with Femern A/S and the INTERREG IV-A project Green STRING Corridor, carried out a survey among businesses located in the regions of Scania in Sweden; the Capital Region of Denmark and Region Zealand in Denmark; and the Länder Schleswig-Holstein and Hamburg in Germany in order to understand GDP per capita and population Quick Demographics: The population in the five affected regions totals 8,447,000 inhabitants distributed as follows: The Capital Region of Denmark 1,730,000; Zealand Region 821,000; Scania Region 1,250,000; Schleswig-Holstein 2,839,000 and Hamburg 1,806,900. The total GDP for all the regions in 2009 was 304,685 million EUR. Hamburg had the highest with 83,736 million EUR while Region Zealand had the lowest with 24,300 million EUR. GDP per capita in EUR Inhabitants X 100 Source: Europa.eu how local businesses, and ultimately the regions themselves, will be affected by the future fixed link. Values of 2009, Source Europa.eu 4

5 Method 1 The Fehmarnbelt Business Barometer is an internet based survey consisting of 10 main questions and corelated sub-questions, which was distributed to companies with more than 100 employees in the regions of Scania, Capital Region of Denmark, Region Zealand, Schleswig-Holstein and Hamburg. In order to complete the questionnaire, knowledge of past, present and future company strategy and perspectives is required; therefore it has been addressed to the top tier of management of the businesses (CFO or CEO). 2 Apart from taking a snapshot of the companies, the objective of the survey is to observe the changes in strategy and perspectives over time towards when the Fehmarnbelt tunnel opens. As a result, the survey is distributed and the data collected and analysed once a year in such a way that the figures from the previous surveys can be compared with the new data. In order to optimise the comparison of results over time, the intention is that, in each succeeding questionnaire, the respondents are able to see their answers from the previous year. For the first survey, the questionnaires were sent to businesses during August 2012 with the data being examined over the following month. The handling of data has been done using the Systat program. Reach The questionnaires have been distributed to a total of 2,095 companies in the five interest regions. The number of questionnaires distributed to each region was the following: Questionnaires distributed per region: Region Scania Zealand Capital Denmark Hamburg Questionnaires Schleswig- Holstein The proportion of respondents who completed the questionnaire was 3.53%, i.e. 74 in total, distributed in the five regions in this manner: Respondents per region: Region Scania Zealand Capital Denmark Hamburg Schleswig- Holstein Respondents 3.93% 9.09% 5.18% 0.86% 3.91% 1 For the complete methodology, refer to appendix 1 2 For the complete questionnaire, refer to appendix 2 5

6 When answering the background information part of the questionnaire, the respondents were able to indicate the sector in which their company operated. It was also possible to choose more than one sector and give each an equivalent weight, for example: Company X operates in the field of communication, but part of its work is related to consulting. In this case, the respondent could indicate, in percentage values, which of the activities predominated in the operation. The relative values have been considered in the analysis and the sectors to which the questionnaires were distributed were: Food and agriculture; Life-Science and health; Transport and logistics; Manufacturing; Energy, water and waste; Tourism; Real estate services; Knowledge production and education; Culture leisure and sport; Building and construction; Wholesale and retail; Information and communication. The ENSPAC Institute The Department for Environmental, Social and Spatial Change of the Roskilde University conducts research and offers undergraduate and graduate programmes in the fields of Geography, Technological and Socio-Economic Planning, City Planning, Work Life and Health Promotion. For more information visit: Fehmarnbelt Business Barometer Participants according to region and sector Inform. Communication Wholesale retail Building construction Culture leisure sport Knowledge education Real estate Tourism Energy water waste Manufacturing Transp Life Food and agriculture In this graph, the sector to which each company belongs was indicated by the respondent and relative values were given when a company belonged to more than one sector. 6

7 Results The following section presents an overview of the current situation regarding turnover, export, import and employment; and then the future expectations of businesses with the same variables at the time of the expected opening of the Fehmarnbelt Fixed Link. This section also touches upon the current and foreseeable challenges for companies in the five different regions. For more graphics and raw data, please refer to appendices 4 and 5. Due to the low response rate, the results must be interpreted with great care, and cannot be seen as representative of either the regions or the industrial sectors they simply say something about the companies who actually responded. The near future Regarding the short term expectations for turnover, import, export and employment for the next 12 months, the companies in all the regions expect growth from 1% to 7.5% on average. The only exception is Region Zealand, which expects a reduction in job offers for the participating businesses on average. Region Zealand is also the one which presents the lowest results for expected turnover for the next year with below average, 2.5% growth. On the other hand, the two German regions, Hamburg 7.5% and Schleswig- Holstein 6.5%, expect above average growth in turnover. Taking into consideration the same variables but this time regarding the business sector, there are more rational differences. Life Sciences and Health show good short term perspectives, especially with regard to volume of business (turnover) and export. In contrast, there are poor expectations in tourism, energy, water and waste, culture, leisure and sport, wholesale and retail as well as information and communication. 7

8 Fehmarnbelt Business Barometer Short term expectations by sector 20,0% 15,0% 10,0% 5,0% TURNOVER EXPORT IMPORT EMPLOYMENT 0,0% -5,0% The size of the sample for each sector is important when interpreting the graph above and might explain some of the spikes The future after the fixed link opens In this section we put the current situation side by side with the perspectives on cross-border cooperation after the tunnel has opened. On the question of cross-border cooperation, the Capital Region of Denmark, Region Zealand and Scania have responded in the context of their cooperation with Northern Germany. For the regions of Hamburg and Schleswig Holstein, the response was in the context of the Øresund Region. 3 Cross-border cooperation Taking into account the current situation, the strategic importance of cooperation between the companies and the expected crossborder cooperation after the tunnel opens; the various sectors seem to expect an increase in cross-border cooperation to a considerable extent. Femern A/S The Danish Transport Ministry owns Femern A/S which is the enterprise responsible for the fixed link across the Fehmarnbelt. The enterprise operates under the name Sund&Bælt Holding A/S, which is also responsible for the Great Belt Bridge. For more information visit: 3 Øresund Region is a transnational region formed by Region Zealand and Capital Region of Denmark in Denmark and Region Scania in Sweden. 8

9 According to the respondents, knowledge and educational institutions are the ones with the highest degree of cooperation nowadays and this sector is expected to have the largest growth in the years following the fixed link inauguration. On a 7 point scale, zero being no cooperation at all and 6 being a very high degree of cooperation, the knowledge production and education sector currently shows almost 3 points for cross-border cooperation with an expected increase to 5 points. The manufacturing sector also presents a considerable increase in cooperation in the years following the opening of the fixed link. The energy, water and waste sector presented extremely high results for increase in cooperation, but this finding is based on a very small number of responses. If we ignore the sectors and only take into account the region in which the companies are located, we can see general expectations for increased cross-border cooperation. Hamburg, which along with Capital Region of Denmark, could be considered as the most global of the regions, is the place where crossborder cooperation is regarded as the most strategically important. The Capital Region of Denmark, on the other hand, is back in 4 th place among the five for the same set of findings. More conclusions can be drawn from the following graph: Fehmarnbelt Business Barometer Cross-border cooperation: current; strategic; and after the fixed link opens 3,50 3,00 2,50 2,00 1,50 1,00 0,50 0,00 Cooperation now Cooperation strategically important Cooperation expected after the link Note the Capital Region of Denmark with the lowest current cross-border cooperation, as considered by the companies 9

10 Cooperation activities The respondents were able to choose from a list and/or name one or more activities that represent their collaboration with partners across the border. They were also asked to name an activity that was strategically important to them as well as activities that are expected to increase or decrease after the tunnel opens. From the three perspectives (current, strategic and future), the volume of cooperation does not seem to vary much across the different activities. The current, strategic and future activity valued as the most important was export. To be able to have meetings across the border was also considered an important activity, but there was no change regarding the before/after the tunnel opening in any of the above. Other activities mentioned were: Import; Marketing; Knowledge Exchange; and Workforce and Agency (subsidiary office). The Green String Corridor The EU Interreg IV A project intends to facilitate cooperation between businesses and public institutions in the STRING region, while promoting innovative transport and logistics solutions. For more information please visit: Barriers In the previous section, we saw that cross-border activity, as considered by the companies today, does not seem to vary much in the future. On this issue, the respondents were asked to identify the barriers to cooperation. The companies considered transport to be the most important barrier. Although legal issues and language barriers between the regions were also considered, the transport time over the Fehmarnbelt and, in consequence, the increased cost appears to be a deciding factor. Other barriers mentioned were the labour market and commercial irrelevance. 10

11 Fehmarnbelt Business Barometer Barriers against increased cooperation A fixed link can tackle directly the largest barrier for cross-border cooperation Millibars and Hectopascals Selected excerpts from the Barometer Survey 4 This section highlights some of the answers given by the respondents to open questions in the survey. Due to the fact that the open questions did not entail a mandatory answer, these inputs are random but can contribute to a better understanding of companies expectations and needs. How will a fixed link across the Fehmarnbelt contribute to your company s cooperation with Northern Germany/Øresund Region? Maybe slightly cheaper transport Easier transport Increase in construction activities Do you have any suggestions for actions to be implemented that could make the upcoming fixed link contribute to the success of your company? Common activities could be arranged in the field of culture and sports Collaboration between the Royal Danish Theatre and the Elbe Symphony, Cooperation between the zoos, Hamburg Technical Museum and the Danish Experimentarium Make common exhibitions 4 The statements were given in the respondents original language and freely translated for this report. 11

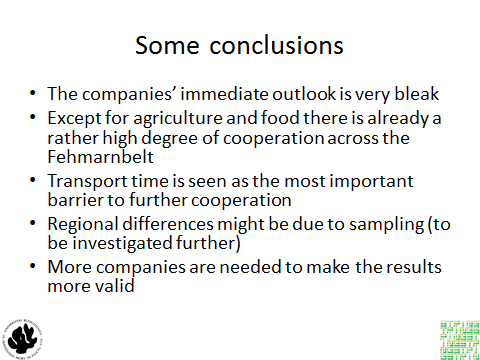

12 Transport should be synchronised with the Øresund link, price is very important There is no clarity about how the long-term use of the local area around the Fehmarnbelt link will be affected. No overall framework is reported. One might fear a collapse of the structure and lack of organisation. There seems to be no vision about the long-term and lasting growth opportunities combined with the necessary actions in the area to house crews, etc. during the construction phase. Branch specific forums should be organised to get to know each-other No, our business is not dependent on a Fehmarnbelt Fixed Link. But the region would benefit from such, and our company may do too in the long term through secondary effects. Eventually open a subsidiary in Northern Germany More flexibility regarding labour market relations/taxes We look forward to being suppliers for the construction phase More information about suppliers/deliverers from Northern Germany Quick implementation Highway to Næstved Conclusion There are different ways in which the survey can be interpreted. One sort of meta-interpretation would take into account the low number of respondents. Although more than 2,000 companies were contacted, around 200 responded and 100 replied that they would NOT like to participate. All in all, around 90% of the contacted companies did not even take any notice of the survey. The explanation for that can probably be found on the time span between now and the opening of the fixed link which is expected in The construction phase has yet to start and, as a consequence, significant media coverage, word of mouth and serious planning by the companies has yet to begin. From the response rates, it can also be seen that the companies in the Øresund Region are more interested than the German companies. The fixed link across the Fehmarnbelt is still seen as a mainly Danish project. From the data that has been collected and analysed, it can be said that the fate of the companies in the different regions regarding the opening of the fixed link, does not yet seem to be defined. The only concrete exceptions are transport time and transport cost, which are factors that already, although the length of time before the tunnel opens, is being treated by the companies as something that can influence their operations in a material way. 12

13 What can be seen today is that there is already a considerable amount of activity across the Fehmarnbelt. Apart from the Agriculture and Food sector, other areas already work together to some extent and the tendency is for cooperation and cross-border activity to increase. It is possible to identify rational differences from one region to another, especially when that data is crossreferenced with sector-specific findings. These major differences are inconclusive and, because of the size of the sample, it is possible that some of the very specific cross-references are not entirely reliable. In this regard, a greater number of respondents participating is needed and this is expected for the future rounds of the Fehmarnbelt Business Barometer. Once the tunnel construction phase approaches and the anticipation of an opening becomes more concrete, the interest of the companies will tend to increase and respondents will be able to have more tangible expectations. 13

14 Appendix 1 Aim: To identify strategic and commercial considerations regarding the future Fehmarnbelt tunnel among top executives within the business environment in the Øresund Region, Holstein and Hamburg. The aim is to learn about the business areas, which are of strategic interest within the context of a fixed link across the Fehmarnbelt with a view to meeting their expectations. The method: The survey was conducted as an internet-based questionnaire sent to senior executives in the STRING region (CEOs or CFOs). The business barometer is structured so that it can be repeated every year as required. Roskilde University is responsible for the design and for carrying out the first round. Choice of companies: Initially, company data was collected through various commercial databases; Orbis for Germany, Greens Erhvervsinformation for Denmark (Business Information for Denmark) and Upplysningscentralens register WebSelect for Scania. In the next phase, some previously excluded companies were added within the following business areas: energy supply; information and communication; property; accountancy and consultancy; and personal services. The data collected includes: name, location, number of employees, turnover and primary sector. The criteria for the selected companies was set at >100 employees. Initially the limit was set at large companies according to the EU definition (>250 employees). This definition did not produce enough companies in Denmark to achieve a good overview. The limit was, therefore, reduced to 100 employees in line with the model from Denmark s Trade Council. The EU definition is not suitable for Denmark because Danish companies generally have fewer employees than equivalent foreign companies. Using the EU model, almost all Danish companies would be SMEs. The 100 employee limit enables enough firms in each region to be able to generalise and to exclude small companies where the probability of not having an interest in a fixed link is considered greatest. A minimum limit of 50 employees was considered, but this could not be completed within the project s timetable and economic framework because of an excessive number of companies with over 50 employees in the German lands (states). Some industry sectors, which were assumed not to have an interest in a Fehmarnbelt fixed link and border trade at regional level, were excluded beforehand. These sectors are finance, insurance, temporary employment agencies and home help agencies. Those companies that did not disclose their number of employees were excluded because we were unable to assess whether they were over or under the limit of 100 employees. 14

15 Companies close to the Danish/German border were excluded because their regional cross-border strategy is seen as focusing on trade with Southern Jutland. The excluded areas are Nordfriesland district, Schleswig- Flensborg district and Flensburg. Selection of respondents: The respondent in each company was an individual at strategic level (CEO or CFO). As far as possible, the survey was sent directly to the respondent s mailbox. If it was not possible to find the respondent s own address, the survey was sent to the company s general address (e.g. info@...) Collecting s: Missing contact details from the databases used were collected manually from the companies respective websites. Where the respondent s address was not available the survey was sent to the company s general address with a request to pass on the survey to the respondent. Companies with and without the respondent s address were put on separate lists in order to check whether this affected the outcome. The company was excluded if it proved impossible to find their website, or if the website failed to provide any address. Around 22% of the companies were deleted as a result. Test: Before the survey was sent to respondents, it was tested on selected test persons from RUC and Femern A/S on several occasions to check whether the questions were understood as intended, whether there were any technical errors in the questionnaire and whether the collected data could be processed. After three test runs, the questionnaire was sent to all respondents. 15

16 Appendix 2 Complete Survey Questionnaire: 1/10 Fehmarnbelt Business Barometer Roskilde University carries out an annual survey of top business leaders in Northern Germany, East Denmark and Skåne with a view to identifying expectations for the fixed link across the Fehmarnbelt. Do you wish to participate? (1) Yes (2) No 2/10 Thank you for your participation in the Fehmarnbelt Business Barometer. In order that we can target future communications appropriately, please provide the following information: Name of contact person address of contact person Title of contact person The company s annual turnover (in EUR) Number of employees in the company 16

17 3/10 Within which sector(s) does your company/organisation operate? Please check one or several x (1) Agriculture and food (2) Life sciences/health (3) Transport and logistics (4) Manufacturing (5) Energy, water and waste (6) Tourism (7) Real estate, consultancy service (8) Knowledge creation and education (9) Culture, entertainment and sport (10) Building and construction (11) Wholesale and retail trade (12) Information and communication (13) Other A (what?) (14) Other B (what?) 3.1/10 If you have indicated that you are more involved in more than sector, please provide more details as to how large a percentage of your business/organisation is accounted for by each. (approximate values) 20% 40% 60% 80% 100% Agriculture and food (1) (2) (3) (4) (5) Life sciences/health (1) (2) (3) (4) (5) Transport and logistics (1) (2) (3) (4) (5) Manufacturing (1) (2) (3) (4) (5) Energy, water and waste (1) (2) (3) (4) (5) 17

18 20% 40% 60% 80% 100% Tourism (1) (2) (3) (4) (5) Real estate, consultancy service Knowledge creation and education Culture, entertainment and sport (1) (2) (3) (4) (5) (1) (2) (3) (4) (5) (1) (2) (3) (4) (5) Building and construction (1) (2) (3) (4) (5) Wholesale and retail trade (1) (2) (3) (4) (5) Information and communication (1) (2) (3) (4) (5) Other A (1) (2) (3) (4) (5) Other B (1) (2) (3) (4) (5) 4/10 Your company s expectations for the future What expectations does your company/organisation have in terms of its turnover over the next 12 months? (1) Increase of more than 10% (2) Increase of around 10% (3) Increase of around 5% (4) Unchanged (5) Decrease of around 5% (6) Decrease of around 10% 18

19 (7) Decrease of more than 10% (8) Don t know What expectations do you have with regard to developments in your company/organisation s exports over the next 12 months? (1) Increase of more than 10% (2) Increase of around 10% (3) Increase of around 5% (4) Unchanged (5) Decrease of around 5% (6) Decrease of around 10% (7) Decrease of more than 10% (8) Don t know What expectations do you have with regard to developments in your company/organisation s imports over the next 12 months? (1) Increase of more than 10% (2) Increase of around 10% (3) Increase of around 5% (4) Unchanged (5) Decrease of around 5% (6) Decrease of around 10% (7) Decrease of more than 10% (8) Don t know 19

20 What expectations do you have concerning developments in your company/organisation s headcount over the next 12 months? (1) Increase of more than 10% (2) Increase of around 10% (3) Increase of around 5% (4) Unchanged (5) Decrease of around 5% (6) Decrease of around 10% (7) Decrease of more than 10% (8) Don t know 5/10 Current situation To what extent does your company/organisation cooperate with companies/organisations in North Germany? (1) 1 To a large extent (2) 2 - (3) 3 - (4) 4 To some extent (5) 5 - (6) 6 - (7) 7 Not at all 6/10 Current situation What form does this cooperation take? Insert one or several x (1) Import (2) Export 20

21 (3) Head office, branch office, sales office (4) Knowledge sharing/exchange (5) Meetings with partners (6) Manpower/key employees (7) Sales promotions (8) Other: 6.1/10 Current situation What barriers do you see to possible cooperation? Check one or several x (1) Legislation (2) Language (3) Transport time (4) Labour market conditions (5) Uninteresting in business terms (6) Other: 7/10 Current situation To what extent is Northern Germany strategically interesting to your company? (1) 1 To a large extent (2) 2 - (3) 3 - (4) 4 To some extent (5) 5 - (6) 6 - (7) 7 Not at all 21

22 7.1/10 What sort of cooperation with the North German market could be of interest? Check one or several x (1) Import (2) Export (3) Head office, branch office, sales office (4) Knowledge sharing/exchange (5) Meetings with partners (6) Manpower/key employees (7) Sales promotions (8) Other: 8/10 The future To what extent will a fixed link across the Fehmarnbelt support your company/organisation s cooperation with Northern Germany? (1) 1 To a great extent (2) 2 - (3) 3 - (4) 4 To some extent (5) 5 - (6) 6 - (7) 7 Not at all 9/10 The future How will a fixed link across the Fehmarnbelt support your company/organisation s co-operation with Northern Germany? Insert one or several x (1) More imports (2) More exports 22

23 (3) Head office, branch offices, sales office (4) More knowledge sharing/exchange (5) More meetings with partners (6) Manpower/key employees (7) More sales promotions (8) Other: 10/10 The future Do you have any suggestions for actions to be implemented that could make the upcoming fixed link contribute to the success of your company? May we contact you for more information about your answer? Please insert your contact details below. Thank you for your answer. We will contact you again next year. Thank you for your answer. We will not contact you again. 23

24 Appendix 3 24

25 25

26 26

27 27

28 28

29 29

30 30

31 31

THE JUTLAND ROUTE CORRIDOR

THE JUTLAND ROUTE CORRIDOR FACTS AND FIGURES 4 th June 2014, Vejle 1 THE JUTLAND ROUTE CORRIDOR FACTS AND FIGURES 1 Introduction 2 The Corridor Area and its Geo-Strategic Framework 3 Demographic and Economic

THE JUTLAND ROUTE CORRIDOR FACTS AND FIGURES 4 th June 2014, Vejle 1 THE JUTLAND ROUTE CORRIDOR FACTS AND FIGURES 1 Introduction 2 The Corridor Area and its Geo-Strategic Framework 3 Demographic and Economic

A new strong growth corridor in Northern Europe

A new strong growth corridor in Northern Europe OSLO STOCKHOLM COPENHAGEN HAMBURG Öresund Hamburg a new strong growth corridor When the fixed link under the Green growth is no longer an alterna- Fehmarn

A new strong growth corridor in Northern Europe OSLO STOCKHOLM COPENHAGEN HAMBURG Öresund Hamburg a new strong growth corridor When the fixed link under the Green growth is no longer an alterna- Fehmarn

The Danish Transport System. Facts and Figures

The Danish Transport System Facts and Figures 2 The Ministry of Transport Udgivet af: Ministry of Transport Frederiksholms Kanal 27 DK-1220 København K Udarbejdet af: Transportministeriet ISBN, trykt version:

The Danish Transport System Facts and Figures 2 The Ministry of Transport Udgivet af: Ministry of Transport Frederiksholms Kanal 27 DK-1220 København K Udarbejdet af: Transportministeriet ISBN, trykt version:

Financial Analysis, Traffic Forecast and Analysis of Railway Payment

FIXED LINK ACROSS FEHMARNBELT Trafikministeriet, København Bundesministerium für Verkehr, Bau- und Wohnungswesen, Berlin Financial Analysis, Traffic Forecast and Analysis of Railway Payment Summary Report

FIXED LINK ACROSS FEHMARNBELT Trafikministeriet, København Bundesministerium für Verkehr, Bau- und Wohnungswesen, Berlin Financial Analysis, Traffic Forecast and Analysis of Railway Payment Summary Report

Innovation Survey Into the Cornish Marine Sector 2006 to 2008 www.nea2.eu

Innovation Survey Into the Cornish Marine Sector 2006 to 2008 www.nea2.eu Contents 1. Executive Summary 2. Introduction and Background 3. Results: About Activities that Support Innovation 4. Results: About

Innovation Survey Into the Cornish Marine Sector 2006 to 2008 www.nea2.eu Contents 1. Executive Summary 2. Introduction and Background 3. Results: About Activities that Support Innovation 4. Results: About

Draft guidelines and measures to improve ICT procurement. Survey results

Draft guidelines and measures to improve ICT procurement Survey results Europe Economics Chancery House 53-64 Chancery Lane London WC2A 1QU Tel: (+44) (0) 20 7831 4717 Fax: (+44) (0) 20 7831 4515 www.europe-economics.com

Draft guidelines and measures to improve ICT procurement Survey results Europe Economics Chancery House 53-64 Chancery Lane London WC2A 1QU Tel: (+44) (0) 20 7831 4717 Fax: (+44) (0) 20 7831 4515 www.europe-economics.com

A Greener Transport System in Denmark. Environmentally Friendly and Energy Efficient Transport

A Greener Transport System in Denmark Environmentally Friendly and Energy Efficient Transport Udgivet af: Ministry of Transport Frederiksholms Kanal 27 DK-1220 København K Udarbejdet af: Transportministeriet

A Greener Transport System in Denmark Environmentally Friendly and Energy Efficient Transport Udgivet af: Ministry of Transport Frederiksholms Kanal 27 DK-1220 København K Udarbejdet af: Transportministeriet

A9. What is the total number of employees worldwide including Denmark by headcount?

SURVEY OF EMPLOYMENT PRACTICES OF MULTINATIONAL COMPANIES OPERATING IN DENMARK Home-based English version Please select a language: SECTION A: INTRODUCTION English... 1 Danish... 2 First page: EMPLOYMENT

SURVEY OF EMPLOYMENT PRACTICES OF MULTINATIONAL COMPANIES OPERATING IN DENMARK Home-based English version Please select a language: SECTION A: INTRODUCTION English... 1 Danish... 2 First page: EMPLOYMENT

How To Calculate The Number Of Private Sector Businesses In The Uk

STATISTICAL RELEASE STATISTICAL RELEASE BUSINESS POPULATION ESTIMATES FOR THE UK AND REGIONS 2011 12 October 2011 Issued by: BIS Level 2, 2 St Paul s Place, Sheffield, S1 2FJ For more detail: http://stats.bis.gov.

STATISTICAL RELEASE STATISTICAL RELEASE BUSINESS POPULATION ESTIMATES FOR THE UK AND REGIONS 2011 12 October 2011 Issued by: BIS Level 2, 2 St Paul s Place, Sheffield, S1 2FJ For more detail: http://stats.bis.gov.

Powering Up the Network: A Report on Small Business Use of E-business Solutions in Canada

Powering Up the Network: A Report on Small Business Use of E-business Solutions in Canada February 2010 Overview Canada is a world leader in many areas: energy, natural resources and the financial services

Powering Up the Network: A Report on Small Business Use of E-business Solutions in Canada February 2010 Overview Canada is a world leader in many areas: energy, natural resources and the financial services

Internationalization a driver for business performance

ization a driver for business performance January 2013 DHL ization a driver for business performance 2 Table of contents 1. Introduction 3 1.1. Background 4 1.2. Methodology 5 2. Analysis 7 2.1. SMEs 8

ization a driver for business performance January 2013 DHL ization a driver for business performance 2 Table of contents 1. Introduction 3 1.1. Background 4 1.2. Methodology 5 2. Analysis 7 2.1. SMEs 8

Innovation in New Zealand: 2011

Innovation in New Zealand: 2011 Crown copyright This work is licensed under the Creative Commons Attribution 3.0 New Zealand licence. You are free to copy, distribute, and adapt the work, as long as you

Innovation in New Zealand: 2011 Crown copyright This work is licensed under the Creative Commons Attribution 3.0 New Zealand licence. You are free to copy, distribute, and adapt the work, as long as you

Project to the Interreg IV B Baltic Sea Region Programme Scandinavian Adriatic Corridor for Growth and Innovation (SCANDRIA)

") Kick off Meeting 3 5 September 2009 SCANDRIA Kick Off Meeting 3 5 September 2009 Berlin and Potsdam 3rd 4th 5th Venue 3rd: 4th: 5th: Plenary Open for Professional Public, Berlin Working Groups for Project

Kick off Meeting 3 5 September 2009 SCANDRIA Kick Off Meeting 3 5 September 2009 Berlin and Potsdam 3rd 4th 5th Venue 3rd: 4th: 5th: Plenary Open for Professional Public, Berlin Working Groups for Project

Commercial Non-Life Insurance Brokers in Northern and Central Europe

Brochure More information from http://www.researchandmarkets.com/reports/1194948/ Commercial Non-Life Insurance Brokers in Northern and Central Europe Description: Finaccord s report titled Commercial

Brochure More information from http://www.researchandmarkets.com/reports/1194948/ Commercial Non-Life Insurance Brokers in Northern and Central Europe Description: Finaccord s report titled Commercial

Survey on the access to finance of enterprises (SAFE) Analytical Report 2014

Analytical Report 2014") Survey on the access to finance of enterprises (SAFE) Analytical Report 2014 Written by Sophie Doove, Petra Gibcus, Ton Kwaak, Lia Smit, Tommy Span November 2014 LEGAL NOTICE This document has been prepared

Survey on the access to finance of enterprises (SAFE) Analytical Report 2014 Written by Sophie Doove, Petra Gibcus, Ton Kwaak, Lia Smit, Tommy Span November 2014 LEGAL NOTICE This document has been prepared

1 Sustainable Development Strategy of Latvia until 2030. Browser SAEIMA OF THE REPUBLIC OF LATVIA SAEIMA

1 Sustainable Strategy of Latvia until 2030 Browser SAEIMA OF THE REPUBLIC OF LATVIA SAEIMA A group of experts led by associate professor Roberts Ķīlis, in accordance with the task of the Ministry of Regional

1 Sustainable Strategy of Latvia until 2030 Browser SAEIMA OF THE REPUBLIC OF LATVIA SAEIMA A group of experts led by associate professor Roberts Ķīlis, in accordance with the task of the Ministry of Regional

Small Business Survey Scotland 2012

Small Business Survey Scotland 2012 March 2013 Office of the Chief Economic Adviser Small Business Survey Scotland 2012 Office of the Chief Economic Adviser http://www.scotland.gov.uk/topics/economy/ Small

Small Business Survey Scotland 2012 March 2013 Office of the Chief Economic Adviser Small Business Survey Scotland 2012 Office of the Chief Economic Adviser http://www.scotland.gov.uk/topics/economy/ Small

Statistical Data on Women Entrepreneurs in Europe

Statistical Data on Women Entrepreneurs in Europe September 2014 Enterprise and Industry EUROPEAN COMMISSION Directorate-General for Enterprise and Industry Directorate D SMEs and Entrepreneurship Unit

Statistical Data on Women Entrepreneurs in Europe September 2014 Enterprise and Industry EUROPEAN COMMISSION Directorate-General for Enterprise and Industry Directorate D SMEs and Entrepreneurship Unit

DEUTSCHE BANK RESPONSE TO THE REPORT OF THE EXPERT GROUP ON CUSTOMER MOBILITY IN RELATION TO BANK ACCOUNTS

Deutsche Bank Dr. Bernhard Speyer/Dr. Stefan Schäfer Deutsche Bank AG/DB Research P.O. Box 60272 Frankfurt, Germany e-mail: [email protected] Tel. +49 (0)69 910 31832 Fax +49 (0)69 910 31743 03.09.2007

Deutsche Bank Dr. Bernhard Speyer/Dr. Stefan Schäfer Deutsche Bank AG/DB Research P.O. Box 60272 Frankfurt, Germany e-mail: [email protected] Tel. +49 (0)69 910 31832 Fax +49 (0)69 910 31743 03.09.2007

Central and Eastern Europe Information Society Benchmarks

Central and Eastern Europe Survey Results Objective 2 Investing in People and Skills September 2004 2.A EUROPEAN YOUTH INTO THE DIGITAL AGE 2.A.1 Number of computers per 100 pupils in primary/secondary/tertiary

Central and Eastern Europe Survey Results Objective 2 Investing in People and Skills September 2004 2.A EUROPEAN YOUTH INTO THE DIGITAL AGE 2.A.1 Number of computers per 100 pupils in primary/secondary/tertiary

CASI: Public Participation in Developing a Common Framework for Assessment and Management of Sustainable Innovation

CASI: Public Participation in Developing a Common Framework for Assessment and Management of Sustainable Innovation THEME SiS.2013.1.2-1 Mobilisation and Mutual Learning (MML) Action Plans: Mainstreaming

CASI: Public Participation in Developing a Common Framework for Assessment and Management of Sustainable Innovation THEME SiS.2013.1.2-1 Mobilisation and Mutual Learning (MML) Action Plans: Mainstreaming

E-commerce in Europe 2014

E-commerce in Europe 2014 Contents Introduction About Europe Increasingly borderless Product categories Payment Delivery Shopping abroad In focus Detailed results PostNord 3 4 6 8 10 14 15 16 17 18 19

E-commerce in Europe 2014 Contents Introduction About Europe Increasingly borderless Product categories Payment Delivery Shopping abroad In focus Detailed results PostNord 3 4 6 8 10 14 15 16 17 18 19

Road freight transport across a fixed Fehmarn Belt link

Road freight transport across a fixed Fehmarn Belt link Per Homann Jespersen 1 Draft version Introduction A fixed link between Denmark and Germany was agreed upon by the Danish and German governments on

Road freight transport across a fixed Fehmarn Belt link Per Homann Jespersen 1 Draft version Introduction A fixed link between Denmark and Germany was agreed upon by the Danish and German governments on

Operational Companies VAT Indirect Taxes. Why Luxembourg: VAT advantages for commercial companies*

Operational Companies VAT Indirect Taxes Why : VAT advantages for commercial companies* Why : VAT advantages for commercial companies as an international decision-making, financing or distribution hub:

Operational Companies VAT Indirect Taxes Why : VAT advantages for commercial companies* Why : VAT advantages for commercial companies as an international decision-making, financing or distribution hub:

The Community Innovation Survey 2010 (CIS 2010)

") The Community Innovation Survey 2010 (CIS 2010) THE HARMONISED SURVEY QUESTIONNAIRE The Community Innovation Survey 2010 FINAL VERSION July 9, 2010 This survey collects information on your enterprise s

The Community Innovation Survey 2010 (CIS 2010) THE HARMONISED SURVEY QUESTIONNAIRE The Community Innovation Survey 2010 FINAL VERSION July 9, 2010 This survey collects information on your enterprise s

Contents. Key points from the 2014 Q4 Survey 4. General economic environment 5. Market conditions and the economy 6. Cash flow and risk 9 M&A 11

The Deloitte CFO Survey 2014 Q4 Results 2 Contents Key points from the 2014 Q4 Survey 4 General economic environment 5 Market conditions and the economy 6 Cash flow and risk 9 M&A 11 A note on methodology

The Deloitte CFO Survey 2014 Q4 Results 2 Contents Key points from the 2014 Q4 Survey 4 General economic environment 5 Market conditions and the economy 6 Cash flow and risk 9 M&A 11 A note on methodology

Bulgaria: The IT and Telecommunications Sector. Sector: IT and Telecommunications. Prepared by the Royal Danish Embassy in Sofia

MINISTRY OF FOREIGN AFFAIRS OF DENMARK THE TRADE COUNCIL ICT SECTOR BULGARIA Bulgaria: The IT and Telecommunications Sector Date: September, 2014 Sector: IT and Telecommunications Prepared by the Royal

MINISTRY OF FOREIGN AFFAIRS OF DENMARK THE TRADE COUNCIL ICT SECTOR BULGARIA Bulgaria: The IT and Telecommunications Sector Date: September, 2014 Sector: IT and Telecommunications Prepared by the Royal

Skills & Demand in Industry

Engineering and Technology Skills & Demand in Industry Annual Survey www.theiet.org The Institution of Engineering and Technology As engineering and technology become increasingly interdisciplinary, global

Engineering and Technology Skills & Demand in Industry Annual Survey www.theiet.org The Institution of Engineering and Technology As engineering and technology become increasingly interdisciplinary, global

Survey report on Nordic initiative for social responsibility using ISO 26000

Survey report on Nordic initiative for social responsibility using ISO 26000 2013 Contents SUMMARY... 3 1. INTRODUCTION... 4 1.1 Objective of the survey... 4 1.2 Basic information about the respondents...

Survey report on Nordic initiative for social responsibility using ISO 26000 2013 Contents SUMMARY... 3 1. INTRODUCTION... 4 1.1 Objective of the survey... 4 1.2 Basic information about the respondents...

Dialogue between the Government and stakeholders a crucial factor for improving Business Environment

Dialogue between the Government and stakeholders a crucial factor for improving Business Environment Anrijs Matīss Deputy State Secretary Ministry of Economics of the Republic of Latvia Brivibas street

Dialogue between the Government and stakeholders a crucial factor for improving Business Environment Anrijs Matīss Deputy State Secretary Ministry of Economics of the Republic of Latvia Brivibas street

THE ELECTRONIC CUSTOMS IMPLEMENTATION IN THE EU

Flash Eurobarometer THE ELECTRONIC CUSTOMS IMPLEMENTATION IN THE EU REPORT Fieldwork: April-May 214 Publication: October 214 This survey has been requested by the European Commission, Directorate-General

Flash Eurobarometer THE ELECTRONIC CUSTOMS IMPLEMENTATION IN THE EU REPORT Fieldwork: April-May 214 Publication: October 214 This survey has been requested by the European Commission, Directorate-General

Labour Market Brief September Quarter 2015

Labour Market Brief September Quarter 2015 Key Message Overall the labour market continues to remain relatively tight, with both full time and part time employment continuing to increase since the beginning

Labour Market Brief September Quarter 2015 Key Message Overall the labour market continues to remain relatively tight, with both full time and part time employment continuing to increase since the beginning

Chamber SME E-Business Survey 2002

Chamber SME E-Business Survey 2002 Prepared for Chambers of Commerce of Ireland September 2002 Chambers of Commerce of Ireland 17 Merrion Square Dublin 2 Ireland W: www.chambersireland.ie E: [email protected]

Chamber SME E-Business Survey 2002 Prepared for Chambers of Commerce of Ireland September 2002 Chambers of Commerce of Ireland 17 Merrion Square Dublin 2 Ireland W: www.chambersireland.ie E: [email protected]

Language Technologies in Europe: trends and future perspectives

Language Technologies in Europe: trends and future perspectives European Commission Márta Nagy-Rothengass, DG CONNECT Data Value Chain Unit Berlin, 24 January 2013 META - Creation of language resources

Language Technologies in Europe: trends and future perspectives European Commission Márta Nagy-Rothengass, DG CONNECT Data Value Chain Unit Berlin, 24 January 2013 META - Creation of language resources

Broadband Mapping 2013

Broadband Mapping 2013 Broadband Mapping 2013 Summary Publisher: The Danish Business Authority A full Danish edition can be downloaded from the website of the Danish Business Authority: www.erst.dk BROADBAND

Broadband Mapping 2013 Broadband Mapping 2013 Summary Publisher: The Danish Business Authority A full Danish edition can be downloaded from the website of the Danish Business Authority: www.erst.dk BROADBAND

Mario Torres Jarrín Director European Institute of International Studies Associate Lecturer Department of Romance Studies and Classics and Associate

Mario Torres Jarrín Director European Institute of International Studies Associate Lecturer Department of Romance Studies and Classics and Associate Researcher, Institute of Latin American Studies Stockholm

Mario Torres Jarrín Director European Institute of International Studies Associate Lecturer Department of Romance Studies and Classics and Associate Researcher, Institute of Latin American Studies Stockholm

Lu.Be.C. Lucca, 21 e 22 ottobre 2010

Tekes the Finnish Funding Agency for Technology and Innovation Tekes Agenzia Finlandesa per la Promozione di Tecnologia ed Innovazione Lu.Be.C. Lucca, 21 e 22 ottobre 2010 1. Facts - and figures 2. Tekes

Tekes the Finnish Funding Agency for Technology and Innovation Tekes Agenzia Finlandesa per la Promozione di Tecnologia ed Innovazione Lu.Be.C. Lucca, 21 e 22 ottobre 2010 1. Facts - and figures 2. Tekes

It s not just about the environment

Supply Chain Consultancy It s not just about the environment Sustainable Supply Chains Paul Goose discusses the need to take a wider, more integrated view of operations to ensure long term growth. A great

Supply Chain Consultancy It s not just about the environment Sustainable Supply Chains Paul Goose discusses the need to take a wider, more integrated view of operations to ensure long term growth. A great

Adult Education Survey 2006, European comparison

Education 2009 Adult Education Survey 2006, European comparison Adults in the Nordic countries actively participate in education and training Persons aged 25 to 64 who live in the Nordic countries (Finland,

Education 2009 Adult Education Survey 2006, European comparison Adults in the Nordic countries actively participate in education and training Persons aged 25 to 64 who live in the Nordic countries (Finland,

UK Government Information Economy Strategy

Industrial Strategy: government and industry in partnership UK Government Information Economy Strategy A Call for Views and Evidence February 2013 Contents Overview of Industrial Strategy... 3 How to respond...

Industrial Strategy: government and industry in partnership UK Government Information Economy Strategy A Call for Views and Evidence February 2013 Contents Overview of Industrial Strategy... 3 How to respond...

Study on the Sharing of Information and Reporting of Suspicious Sports Betting Activity in the EU 28

Study on the Sharing of Information and Reporting of Suspicious Sports Betting Activity in the EU 28 A study for the DIRECTORATE-GENERAL EDUCATION AND CULTURE, Directorate Youth and Sport, Unit Sport By

Study on the Sharing of Information and Reporting of Suspicious Sports Betting Activity in the EU 28 A study for the DIRECTORATE-GENERAL EDUCATION AND CULTURE, Directorate Youth and Sport, Unit Sport By

Nordic Co-operation Programme for Innovation and Business Policy 2014 2017

Nordic Co-operation Programme for Innovation and Business Policy 2014 2017 NORDISK MILJØMÆRKNING Nordic Co-operation Programme for Innovation and Business Policy 2014 2017 ISBN 978-92-893-2739-8 http://dx.doi.org/10.6027/anp2014-722

Nordic Co-operation Programme for Innovation and Business Policy 2014 2017 NORDISK MILJØMÆRKNING Nordic Co-operation Programme for Innovation and Business Policy 2014 2017 ISBN 978-92-893-2739-8 http://dx.doi.org/10.6027/anp2014-722

10. STUDENT LOANS IN EUROPE: AN OVERVIEW 1

90 10. STUDENT LOANS IN EUROPE: AN OVERVIEW 1 Marianne Guille Education is expensive. In 1995 the average global effort in favour of education represented 6.7% of GDP in OECD countries, and this effort

90 10. STUDENT LOANS IN EUROPE: AN OVERVIEW 1 Marianne Guille Education is expensive. In 1995 the average global effort in favour of education represented 6.7% of GDP in OECD countries, and this effort

Fehmarnbelt Forecast 2014 - Update of the FTC-Study of 2002

Fehmarnbelt Forecast 2014 - Update of the FTC-Study of 2002 for Femern A/S 2014 Intraplan Consult GmbH Orleansplatz 5a Wentzingerstr. 19 81667 München 79106 Freiburg BVU Beratergruppe Verkehr + Umwelt

Fehmarnbelt Forecast 2014 - Update of the FTC-Study of 2002 for Femern A/S 2014 Intraplan Consult GmbH Orleansplatz 5a Wentzingerstr. 19 81667 München 79106 Freiburg BVU Beratergruppe Verkehr + Umwelt

INNOVATION IN THE PUBLIC SECTOR: ITS PERCEPTION IN AND IMPACT ON BUSINESS

Flash Eurobarometer INNOVATION IN THE PUBLIC SECTOR: ITS PERCEPTION IN AND IMPACT ON BUSINESS REPORT Fieldwork: February-March 22 Publication: June 22 This survey has been requested by the European Commission,

Flash Eurobarometer INNOVATION IN THE PUBLIC SECTOR: ITS PERCEPTION IN AND IMPACT ON BUSINESS REPORT Fieldwork: February-March 22 Publication: June 22 This survey has been requested by the European Commission,

ACER scoping document for Rules for Trading

ENTSOG response to ACER questionnaire on scoping for Rules for 12 May 2014 Final ACER scoping document for Rules for ENTSOG response to the ACER questionnaire Since some of the questions are addressed

ENTSOG response to ACER questionnaire on scoping for Rules for 12 May 2014 Final ACER scoping document for Rules for ENTSOG response to the ACER questionnaire Since some of the questions are addressed

TTIP AND CULTURE. what are 'cultural sectors' from the trade perspective? how do trade talks deal with the so-called 'cultural exception'?

TTIP AND CULTURE In 2013, the European Union (EU) started negotiations for a free trade agreement (FTA) the Transatlantic Trade and Investment Partnership or TTIP with the United States (US), the largest

TTIP AND CULTURE In 2013, the European Union (EU) started negotiations for a free trade agreement (FTA) the Transatlantic Trade and Investment Partnership or TTIP with the United States (US), the largest

The Economic Impact of Long Distance Cycle Routes North Sea Cycle Route (NSCR)

") The Economic Impact of Long Distance Cycle Routes North Sea Cycle Route (NSCR) Les Lumsdon and Paul Downward CAST, Staffordshire University Stoke-on-Trent SK10 1LT, UK [email protected] Summary

The Economic Impact of Long Distance Cycle Routes North Sea Cycle Route (NSCR) Les Lumsdon and Paul Downward CAST, Staffordshire University Stoke-on-Trent SK10 1LT, UK [email protected] Summary

Implementation of the Bologna Goals in Denmark

Note Implementation of the Bologna Goals in Denmark The Bologna Process A reform of higher education programmes, known as the Bologna Process, is taking place in several European countries for the purpose

Note Implementation of the Bologna Goals in Denmark The Bologna Process A reform of higher education programmes, known as the Bologna Process, is taking place in several European countries for the purpose

ARE THE POINTS OF SINGLE CONTACT TRULY MAKING THINGS EASIER FOR EUROPEAN COMPANIES?

ARE THE POINTS OF SINGLE CONTACT TRULY MAKING THINGS EASIER FOR EUROPEAN COMPANIES? SERVICES DIRECTIVE IMPLEMENTATION REPORT NOVEMBER 2011 EUROPEAN COMPANIES WANT WELL-FUNCTIONING POINTS OF SINGLE CONTACT

ARE THE POINTS OF SINGLE CONTACT TRULY MAKING THINGS EASIER FOR EUROPEAN COMPANIES? SERVICES DIRECTIVE IMPLEMENTATION REPORT NOVEMBER 2011 EUROPEAN COMPANIES WANT WELL-FUNCTIONING POINTS OF SINGLE CONTACT

How To Study Employment Practices Of Multinational Companies In An Organizational Context

Employment Practices of Multinational Companies in an Organizational Context Summary of Research Project This project is the first based on a representative sample of MNCs operating in Denmark. In this

Employment Practices of Multinational Companies in an Organizational Context Summary of Research Project This project is the first based on a representative sample of MNCs operating in Denmark. In this

Mortgage Distribution Channels: Estimates of lending

Mortgage Distribution Channels: Estimates of lending Dean Garratt, Economist, Council of Mortgage Lenders Deregulation and technological advancement have contributed to a multi-channel approach. The competitiveness

Mortgage Distribution Channels: Estimates of lending Dean Garratt, Economist, Council of Mortgage Lenders Deregulation and technological advancement have contributed to a multi-channel approach. The competitiveness

Instruments to control and finance the building of healthcare infrastructure in other countries of the European Union

Summary and conclusions This report describes the instruments by which the respective authorities of eight important European Union members control the building, financing and geographical distribution

Summary and conclusions This report describes the instruments by which the respective authorities of eight important European Union members control the building, financing and geographical distribution

ESTABLISHED GERMAN MARZIPAN COMPANY CONTINUES SUSTAINABLE HEALTH PROMOTION 1. Case metadata

ESTABLISHED GERMAN MARZIPAN COMPANY CONTINUES SUSTAINABLE HEALTH PROMOTION 1. Case metadata Country of origin: Germany Year of publication by agency: 2012 Sector: C10 Manufacture of food products Keywords:

ESTABLISHED GERMAN MARZIPAN COMPANY CONTINUES SUSTAINABLE HEALTH PROMOTION 1. Case metadata Country of origin: Germany Year of publication by agency: 2012 Sector: C10 Manufacture of food products Keywords:

The MetLife Survey of

The MetLife Survey of Challenges for School Leadership Challenges for School Leadership A Survey of Teachers and Principals Conducted for: MetLife, Inc. Survey Field Dates: Teachers: October 5 November

The MetLife Survey of Challenges for School Leadership Challenges for School Leadership A Survey of Teachers and Principals Conducted for: MetLife, Inc. Survey Field Dates: Teachers: October 5 November

RETAIL FINANCIAL SERVICES

Special Eurobarometer 373 RETAIL FINANCIAL SERVICES REPORT Fieldwork: September 211 Publication: April 212 This survey has been requested by the European Commission, Directorate-General Internal Market

Special Eurobarometer 373 RETAIL FINANCIAL SERVICES REPORT Fieldwork: September 211 Publication: April 212 This survey has been requested by the European Commission, Directorate-General Internal Market

Second Quarter Results 2014 Investor presentation

Second Quarter Results 2014 Investor presentation Second Fourth Quarter and Results 2015 Full Year Results 2014 Press conference Christian Investor Clausen, presentation President and Group CEO Christian

Second Quarter Results 2014 Investor presentation Second Fourth Quarter and Results 2015 Full Year Results 2014 Press conference Christian Investor Clausen, presentation President and Group CEO Christian

Business Operations Survey

Image description. Hot Off The Press. End of image description. Embargoed until 10:45am 27 April 2007 Business Operations Survey 2006 Highlights Ninety-one percent of businesses use the Internet. Seventy-seven

Image description. Hot Off The Press. End of image description. Embargoed until 10:45am 27 April 2007 Business Operations Survey 2006 Highlights Ninety-one percent of businesses use the Internet. Seventy-seven

QUESTIONNAIRE ON CONTRACT RULES FOR ONLINE PURCHASES OF DIGITAL CONTENT AND TANGIBLE GOODS

QUESTIONNAIRE ON CONTRACT RULES FOR ONLINE PURCHASES OF DIGITAL CONTENT AND TANGIBLE GOODS Information about the respondent 1. Please enter your full name OR the name of the organisation / company / institution

QUESTIONNAIRE ON CONTRACT RULES FOR ONLINE PURCHASES OF DIGITAL CONTENT AND TANGIBLE GOODS Information about the respondent 1. Please enter your full name OR the name of the organisation / company / institution

Opportunities for Growth in the UK Events Industry

Opportunities for Growth in the UK Events Industry Roles & responsibilities A report to the All Party Parliamentary Group For Events Presented jointly by the October 2011 1 Contents 1.0 The UK events industry

Opportunities for Growth in the UK Events Industry Roles & responsibilities A report to the All Party Parliamentary Group For Events Presented jointly by the October 2011 1 Contents 1.0 The UK events industry

Executive Summary, 21 January 2015

January 2015 Study by the Ifo Institute, Munich, and the Institute for Applied Economic Research (IAW), Tübingen commissioned by the German Federal Ministry for Economic Cooperation and Development (BMZ)

January 2015 Study by the Ifo Institute, Munich, and the Institute for Applied Economic Research (IAW), Tübingen commissioned by the German Federal Ministry for Economic Cooperation and Development (BMZ)

Pan-European opinion poll on occupational safety and health

PRESS KIT Pan-European opinion poll on occupational safety and health Results across 36 European countries Press kit Conducted by Ipsos MORI Social Research Institute at the request of the European Agency

PRESS KIT Pan-European opinion poll on occupational safety and health Results across 36 European countries Press kit Conducted by Ipsos MORI Social Research Institute at the request of the European Agency

Preparation of a new EU Disability Strategy 2010-2020 Summary of the main outcomes of the public consultation

Preparation of a new EU Disability Strategy 2010-2020 Summary of the main outcomes of the public consultation European Commission 2 Table of Contents 1. Background of the public consultation...5 2. Questionnaire...5

Preparation of a new EU Disability Strategy 2010-2020 Summary of the main outcomes of the public consultation European Commission 2 Table of Contents 1. Background of the public consultation...5 2. Questionnaire...5

Briefing on Personnel Leasing in the European Union

Annex 13 Briefing on Personnel Leasing in the European Union 1. Economic significance In the EU (15 Member States; there are not yet any figures of the 10 new Member States) there are about 1,4 million

Annex 13 Briefing on Personnel Leasing in the European Union 1. Economic significance In the EU (15 Member States; there are not yet any figures of the 10 new Member States) there are about 1,4 million

International Education in the Comox Valley: Current and Potential Economic Impacts

International Education in the Comox Valley: Current and Potential Economic Impacts FINAL REPORT March 2012 Prepared by: Vann Struth Consulting Group Inc. Vancouver, BC www.vannstruth.com Prepared for:

International Education in the Comox Valley: Current and Potential Economic Impacts FINAL REPORT March 2012 Prepared by: Vann Struth Consulting Group Inc. Vancouver, BC www.vannstruth.com Prepared for:

Gerry Byrne Country Head Poland

Gerry Byrne Country Head Poland Bank Zachodni WBK S.A. ( BZ WBK ) and Banco Santander, S.A. ("Santander") both caution that this presentation contains forward-looking statements. These forward-looking

Gerry Byrne Country Head Poland Bank Zachodni WBK S.A. ( BZ WBK ) and Banco Santander, S.A. ("Santander") both caution that this presentation contains forward-looking statements. These forward-looking

CONSULTATION ON A POSSIBLE STATUTE FOR A EUROPEAN PRIVATE COMPANY (EPC)

") EUROPEAN COMMISSION Internal Market and Services DG MARKT/ 19.07.2007 CONSULTATION ON A POSSIBLE STATUTE FOR A EUROPEAN PRIVATE COMPANY (EPC) Consultation by the Services of the Internal Market Directorate

EUROPEAN COMMISSION Internal Market and Services DG MARKT/ 19.07.2007 CONSULTATION ON A POSSIBLE STATUTE FOR A EUROPEAN PRIVATE COMPANY (EPC) Consultation by the Services of the Internal Market Directorate

Toronto Employment Survey 2014

This bulletin summarizes the highlights of the 2014 City of Toronto annual Survey, marking its 32 nd consecutive year. This information resource presents a picture of change in Toronto s economy throughout

This bulletin summarizes the highlights of the 2014 City of Toronto annual Survey, marking its 32 nd consecutive year. This information resource presents a picture of change in Toronto s economy throughout

REPORT ON LANGUAGE MANAGEMENT STRATEGIES AND BEST PRACTICE IN EUROPEAN SMES: THE PIMLICO PROJECT

REPORT ON LANGUAGE MANAGEMENT STRATEGIES AND BEST PRACTICE IN EUROPEAN SMES: THE PIMLICO PROJECT EXECUTIVE SUMMARY AND RECOMMENDATIONS The Directorate-General for Education and Culture is launching an

REPORT ON LANGUAGE MANAGEMENT STRATEGIES AND BEST PRACTICE IN EUROPEAN SMES: THE PIMLICO PROJECT EXECUTIVE SUMMARY AND RECOMMENDATIONS The Directorate-General for Education and Culture is launching an

Statement on G7 Topic Trade and Supply Chain Standards

Statement on G7 Topic Trade and Supply Chain Standards Together, the G7 states produce 32 per cent of the global gross domestic product. A large number of companies located in the G7 countries are active

Statement on G7 Topic Trade and Supply Chain Standards Together, the G7 states produce 32 per cent of the global gross domestic product. A large number of companies located in the G7 countries are active

BUSINESS STATISTICS SNAPSHOT UPDATE April 2015

BUSINESS STATISTICS SNAPSHOT UPDATE April 2015 Australian Overview 1 Australian Businesses 1 The number of actively trading businesses in Australia was 2 100 162 at June 2014, increased by 1 per cent (20

BUSINESS STATISTICS SNAPSHOT UPDATE April 2015 Australian Overview 1 Australian Businesses 1 The number of actively trading businesses in Australia was 2 100 162 at June 2014, increased by 1 per cent (20

Investors in People Impact Assessment. Final report August 2004

Final report Investors in People Impact Assessment 2004 Final report Investors in People Impact Assessment By: Charles Michaelis Michelle McGuire Final report Contents 1 EXECUTIVE SUMMARY... 5 1.1 BACKGROUND...5

Final report Investors in People Impact Assessment 2004 Final report Investors in People Impact Assessment By: Charles Michaelis Michelle McGuire Final report Contents 1 EXECUTIVE SUMMARY... 5 1.1 BACKGROUND...5

Family Law. Analytical Report

Flash Eurobarometer European Commission Family Law Analytical Report Fieldwork: June 2006 Report: October 2006 Flash Eurobarometer 188 The Gallup Organization This survey was requested by Directorate-General

Flash Eurobarometer European Commission Family Law Analytical Report Fieldwork: June 2006 Report: October 2006 Flash Eurobarometer 188 The Gallup Organization This survey was requested by Directorate-General

Wystąpienie Rzecznika Praw Obywatelskich - Bruksela, 15 września 2008 r.

1 Wystąpienie Rzecznika Praw Obywatelskich - Bruksela, 15 września 2008 r. Two years ago, during the European Year of Workers Mobility, we realised the unprecedented scale of economic migration today.

1 Wystąpienie Rzecznika Praw Obywatelskich - Bruksela, 15 września 2008 r. Two years ago, during the European Year of Workers Mobility, we realised the unprecedented scale of economic migration today.

Directors & Officers Liability (D&O) Insurance. Benchmarking Report 2013

Insurance. Benchmarking Report 2013") Directors & Officers Liability (D&O) Insurance Benchmarking Report 2013 Contents 1. Executive Summary...4 2. D&O benchmarking survey...6 3. D&O insurance arrangements...8 4. Risk manager role and responsibilities...10

Directors & Officers Liability (D&O) Insurance Benchmarking Report 2013 Contents 1. Executive Summary...4 2. D&O benchmarking survey...6 3. D&O insurance arrangements...8 4. Risk manager role and responsibilities...10

World Tourism Organization RECOMMENDATIONS TO GOVERNMENTS FOR SUPPORTING AND/OR ESTABLISHING NATIONAL CERTIFICATION SYSTEMS FOR SUSTAINABLE TOURISM

World Tourism Organization RECOMMENDATIONS TO GOVERNMENTS FOR SUPPORTING AND/OR ESTABLISHING NATIONAL CERTIFICATION SYSTEMS FOR SUSTAINABLE TOURISM Introduction Certification systems for sustainable tourism

World Tourism Organization RECOMMENDATIONS TO GOVERNMENTS FOR SUPPORTING AND/OR ESTABLISHING NATIONAL CERTIFICATION SYSTEMS FOR SUSTAINABLE TOURISM Introduction Certification systems for sustainable tourism