Indiana Department of Education Overview of the State Tuition Support Formula

|

|

|

- Sheila Weaver

- 8 years ago

- Views:

Transcription

1 Indiana Department of Education Overview of the State Tuition Support Formula

2 Agenda Background Formula Terms The Formula Reconciliation Other Grants Resources Contacts

3 State Tuition Support Formula Background Established by the IN General Assembly Funded through state revenues without a property tax component School corporations do, however, have the opportunity to raise operating dollars through a property tax referendum. Adopted as a two year formula during the long session in odd-numbered years Effective 7/1/13, the funding formula became a fiscal year formula Fiscal year formula runs from July 1 through June 30

4 State Tuition Support Formula Background Sets the fiscal year cap or maximum amount of dollars available for tuition support funding State tuition support Choice scholarships Mitch Daniels Early Graduation Scholarship Currently supports six categorical grants Basic tuition support Complexity Full-day kindergarten Honors Special education Career & Tech. Educ.

5 Tuition Support Stats September 2013 ADM count 989, February 2014 ADM count 983, September 2014 ADM count 988, FY14 Average TS per ADM $4, FY14 Average CI per ADM $1, FY 15 Average TS per ADM $4, FY15 Average CI per ADM $1,169.08

6 Tuition Support Stats FY14 Basic Tuition $4,560,189,077 FY14 Complexity $1,144,499,350 FY14 Ave. mo. payment (gross) $544,890,577 FY 15 Basic Tuition (est) $4,570,469,843 FY15 Complexity (est) $1,155,846,600 FY15 Ave. mo. payment (gross) $546,372,116

$1,155,846,600 FY15 Ave.")

7 Foundation CY2011- $4,505 CY2012- $4,280 CY2013- $4,505 FY2014- $4,569 FY2015- $4,587 Tuition Support Stats

8 Tuition Support Stats Full-day kindergarten per student funding: $1, $1, $2, FY $2, FY $2,472.00

9 IDOE Monitors the cap Ensuring that distributions made do not exceed funds available for the fiscal year Cap FY2013- $6,313,700,000 FY2014- $6,622,800,000 FY2015- $6,691,600,000 FY2016- TBD

10 IDOE Creates the worksheet Work with a small committee of fiscal analysts, school business officials, school associations and IDOE staff to prepare a draft worksheet Test, retests and finalizes the calculations Determines and distributes grant amounts Twelve payments per year with at least one payment occurring every forty (40) days

11 IDOE Calculates a gross monthly payment to public school corporations and charter schools Finalizes the net monthly payments after adjustments Plus and minus adjustments Common school loans Medicaid Veteran loans Other adjustments

12 DOE- ME Membership Report Used to gather average daily membership (ADM) and full-day kindergarten (FDK) counts Two counts Formula Terms September (fall count) determines July through December funding February (spring count) determines January through June funding Kindergarten students count as ½ student for purposes of the membership count used for the basic tuition support and complexity grants Kindergarten students count as 1 student for purposes of the FDK grant ME counts are used to determine basic tuition support, FDK and complexity funding

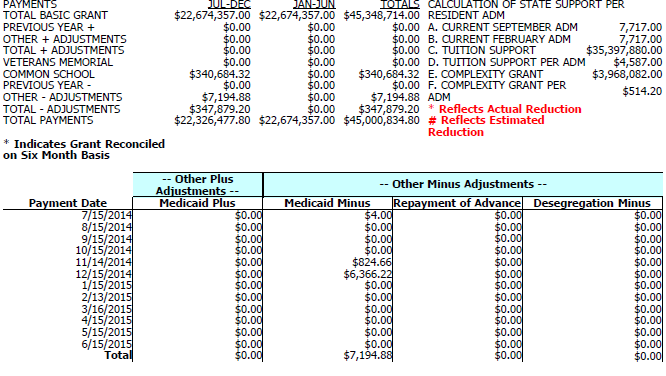

13 DPI54 - Form 54 Formula Terms Fiscal year Basic Grant Monthly Distribution worksheet found in the State Aid Program lists actual and estimated monthly state tuition support payments by grant Shows gross and net monthly payments and any plus or minus adjustments.

14 Formula Terms Inters Form 30A - Career and technical Education Report Data collected in September determines career and technical education funding for a fiscal year Uses Labor Market more than, moderate, less than moderate Wage Rates- high, moderate, less than moderate FY- fiscal year, or the period of July 1 through June 30

15 Formula Terms DOE- GR Graduate Report For FY2015, the count of students, who graduated or left school with a certificate of completion after September 30, 2013 and before October 1, The number of students who graduated with either an Academic Honors or Core 40 with Technical Honors diploma determined Honors funding in the FY2015 formula.

16 DOE-TB Textbook Formula Terms Data collection of the cost of providing textbook assistance to students who were eligible to receive a free or reduced lunch. The percentage of students that received textbook assistance in October 2013 divided by pupil enrollment was a factor used to determine FY2015 complexity grant funding.

17 Formula Terms DOE- SE Special Education Report Count of students who received special education services on December 1 and April 1 The Department uses the December 1 counts to determine special education grant funding Severe Mild and Moderate Communication and Homebound Special education preschool

18 Formula Terms Adjusted ADM The current ADM in the case of the September ADM count The current ADM or not less than ninety percent of the school corporation s September count of ADM, regardless of the actual amount of the February ADM count. IC ADM of the previous year The average of the previous year s fall and spring adjusted ADM counts.

19 Formula terms Attending Physical or virtual presence of a student with the expectation of continued services in the educational programs for which the student is registered (IC ) Current ADM Spring count (February) for distributions from January through June Fall count (September) for distributions from July through December

Current ADM Spring count (February) for distributions from January through June")

20 Formula Terms Enrolled Registered with a school corporation to attend educational programs offered by or through the school corporation; and attending their educational programs or receiving educational services. (IC )

21 The Formula

22 Variables needed FY2014 Basic Tuition Support (DOE SA54 Tuition Support, 1st Column) Prior Year Form 54 FY2014 Honors Diploma Grant Prior Year Form 54 FY2014 Special Ed Grant Prior Year Form 54 FY2014 Career and Tech Ed Grant Prior Year Form 54 FY2014 Complexity Grant Prior Year Form 54 FY2014 Full Day Kindergarten Grant Prior Year Form 54

23 Variables needed September 2013 ADM Count ( ) Prior year DOE-ME report February 2014 ADM Count ( ) Prior year DOE-ME report September 2014 ADM Count ( ) Current year DOE-ME report February 2015 ADM Count ( ) Current year DOE-ME report

24 Variables needed Number of Students-academic honors diploma Current year DOE- GR report Number of Students- Core 40 diploma w/tech honors in sch year Current year DOE-GR report Percent of Students that received or are eligible to receive free textbooks in ( textbook student count/pupil enrollment) Prior year textbook claim submission and Oct. 1 pupil enrollment data Sept Full Day Kindergarten (FDK) Count Current year Sept. ME report Feb Full Day Kindergarten (FDK) Count Current year Feb. ME report

25 Variables needed Dec 2014 Special Education Severe Disabilities Pupil Count Current year DOE-SE report Dec 2014 Special Education Mild and Moderate Disabilities Pupil Count Current year DOE-SE report Dec 2014 Special Education Communication and Homebound Pupil Count Current year DOE-SE report Dec 2014 Special Education Preschool Count Current year DOE-SE report

26 Variables needed 1. More Than Moderate Labor Market Need/High Wage 2. More Than Moderate Labor Market Need/Moderate Wage 3. More Than Moderate Labor Market Need/Less than Moderate Wage 4. Moderate Labor Market Need/High Wage 5. Moderate Labor Market Need/Moderate Wage 6. Moderate Labor Market Need/Less than Moderate Wage 7. Less Than Moderate Labor Market Need/High Wage 8. Less Than Moderate Labor Market Need/Moderate Wage 9. Less Than Moderate Labor Market Need/Less than Moderate Wage 10. Area Participation Student Count 11. Student Count for All Other Approved CTE Programs Data is from the Current year (Sept. 2014) inters Form 30A- through DWD

27 Sections A and B Previous Year Revenue Tuition support revenue for the prior fiscal year- DPI54 tuition support column total Adjusted ADM Determines three counts used in the formula: Ave. adjusted ADM, Fall count (September), and Spring count (February)

28 Section C Transition to Foundation Revenue Applies to all school corporations, charter schools, and virtual charter schools Uses the applicable fall and spring counts Lines 1-4 determine transition to foundation revenue per student Lines 5-6 multiplies the revenue per student by the applicable fall or spring count (ADM) to determine each six month period of basic tuition support funding.

29 Section C1 Virtual Charter Schools Applies to virtual charter schools only Uses the applicable fall and spring count Determines basic tuition support funding for virtual charter schools for each six month period at a rate of 90% of the transition to foundation revenue per student multiplied by the applicable fall and spring count (ADM).

30 Honors Grant Section D Applies to school corporations, charter schools and virtual charter schools Uses applicable DOE-GR counts Provides $1,000 for each student who graduated with an Academic Honors or Core 40 with Technical Honors diploma in the previous school year.

31 Section E Special Education Applies to school corporations, charter schools and virtual charter schools Uses DOE-SE and DOE-HB counts Allows school corporations funding for Severe disability students at $8,350 Mild/Moderate students at $2,265 Communication/homebound students at $533 Special ed. preschool students at $2,750

32 Section F Career and Technical Education Applies to school corporations, charter schools and virtual charter schools More than moderate labor mkt. need/high wage at $450 More than moderate labor mkt. need/moderate wage at $375 More than moderate labor mkt. need/less than moderate wage at $300

33 Section F cont d Career and Technical Education Moderate labor mkt. need/high wage at $375 Moderate labor mkt. need/moderate wage at $300 Moderate labor mkt. need/less than moderate wage at $225 Less than moderate labor mkt. need/high wage at $300 Less than moderate labor mkt. need/ moderate wage at $225 Less than moderate labor mkt. need/less than moderate wage at $150

34 Section F cont d Career and Technical Education All other career and technical education programs at $250 per student count Area participation count at $150

35 Section G Complexity Grant Applies to school corporations, charter schools and virtual charter schools Uses the percentage of students eligible to receive textbook assistance (FY15 formula) to determine complexity index funds. Multiplies the complexity index by the school corporation s foundation amount to determine funding.

36 Section H Full-day kindergarten Applies to school corporations, charter schools and virtual charter schools. Multiplies the FDK membership count by $2472 (in FY15) to determine FDK funding.

37 Section I Capital Projects Fund References the amount of allowable expenditures from the capital projects fund for utility services or property and casualty insurance Requires school corporations to advertise and adopt a CPF budget, levy and rate sufficient to cover costs Maintains the amount at 3.5% of the school corporation s 2005 calendar year distribution.

38 Sections J and K FY State Tuition Support Provides the fiscal year funding amount by grant Funding Comparison Provides a grant by grant comparison of current and previous fiscal year grant totals and the overall percentage change from one fiscal year to the next.

39 Reconciliation Grants that use two counts Basic Tuition Support Complexity Full-day kindergarten Grants that use one count Special Education Honors Career and Technical Education

40 Reconciliation with two counts The Department uses estimated ADM and FDK counts for the July through October payments. The Department then uses actual September counts to determine July through December funding and reconciles what was paid against what should have been paid. September actual counts are used to distribute funds November through March. The Department uses the February counts to determine January through June funding.

41 Reconciliation with two counts When the fall (September) count is loaded, the November and December payments increased or decreased to ensure the school corporation received the Basic Tuition Support, Complexity and FDK grant monies it was entitled to for the period of July through December.

42 Reconciliation with two counts Estimated ADM count used for July through December payments resulted in $600,000 tuition support due for six month period. July through October - DOE distributed $400,000 September (Fall) count loaded- ADM dropped School entitled to $500,000 for the six month period Amount due July through Dec. $500,000 Received July through October $400,000 Remainder $100,000 Nov. pmt. $ 50,000 Dec. pmt. $ 50,000 Jan. to June payment estimate $500,000

43 Reconciliation with two counts Estimated ADM count used for July through December payments resulted in $600,000 tuition support due for the six month period. July through October DOE distributed $400,000 September (Fall) count loaded- ADM increased School entitled to $700,000 for the six month period Amount due July through Dec. $700,000 Received July through Oct. $400,000 Remainder $300,000 Nov. pmt. $150,000 Dec. pmt. $150,000 Jan. to June payment estimate $700,000

44 Reconciliation with one count for CTE and Honors September (CTE) and October (GR) counts determine July through June funding. Prior year counts were used to distribute funds for July through November payments.

45 Reconciliation with one count for CTE and Honors When CTE and Honors counts are loaded, the December payment increased or decreased to provide school corporations with the level of funding it should have received for the period of July through December and anticipated funding for January to June (50/50 split of funds).

46 Reconciliation with one count- CTE and Honors Prior year counts were used for July through December payments and resulted in $240,000 CTE and Honors funds due for the six-month period. July through November - $200,000 distributed (40k*5) Final counts loaded- counts decreased, six month total is now $234,000 July to Dec. total $234,000 Received to date $200,000 Dec. pmt. $ 34,000 Jan. to June payment total $234,000

47 Reconciliation with one count- CTE and Honors Prior year counts were used for July through December payments and resulted in $240,000 CTE and Honors funds due for the six-month period. July through November - $200k distributed (40k*5) Final counts loaded- counts increased, six month total is now $300,000 July to December total $300,000 Received to date $200,000 Dec. pmt. $100,000 Jan. to June payment total will be $300,000

48 Reconciliation with one count for Sp. Ed. Prior year counts were used to distribute funds for July through January special education payments. The December 1 special education count determines fiscal year funding.

49 Reconciliation with one count- Sp. Ed. Final counts loaded- counts decreased School paid to date $315,000 of the $540,000 fiscal year estimate School actually entitled to $480,000 for the fiscal year February through May payments are prorated DOWN with the June payment being a normal monthly payment.

50 Reconciliation with one count- Sp. Ed. Entitled to: $480,000 Received: $315,000 (through Jan.) Remainder: $165,000 Pro-rate Feb. $ 31,250 Pro-rate Mar. $ 31,250 Pro-rate April $ 31,250 Pro-rate May $ 31,250 June pmt. $ 40,000 Total due: $480,000

51 Reconciliation with one count- Sp. Ed. Final counts loaded- counts increased School paid to date $315,000 of the $540,000 fiscal year estimate School actually entitled to $720,000 for the fiscal year Lump sum adjustment made for the February payment with March through June payments being normal monthly payments.

52 Reconciliation with one count- Sp. Ed. Entitled to: $720,000 Received: $315,000 (through Jan.) Remainder: $405,000 Feb. pmt. $165,000 Mar. pmt. $ 60,000 April pmt. $ 60,000 May pmt. $ 60,000 June pmt. $ 60,000 Total due: $480,000

53 Recap Grants are reconciled within each six month period to allow ½ of the grant to be distributed within a six-month period Exception special education Grants using two counts are membership, FDK and complexity Grants using one count are honors, career and technical education and special education

54 DPI 54 or Form 54 Provides estimated and actual tuition support gross and net monthly payment information Check your Form 54 every month July (new formula takes effect) November (Basic Tuition Support, FDK, and Complexity Grants updated) December (Honors and CTE updated) February (Special education updated) April (Basic Tuition Support, FDK and Complexity Grants updated)

55

56

57 Resources IDOE Staff Website STN Finance Application Center (State Aid) Workshops Digest of Public School Finance Learning Connection Finance Community School Associations clinics, seminars and updates Talking to peers

58 IDOE Office of School Finance Contacts Melissa Ambre at Kaitlin Boldt at Fatima Carson at LaTrice Akers at Ashley Sims at Phone: Fax: Learning Connection > Finance Community

Superintendents and Charter School Administrators. Melissa K. Ambre, Director, Office of School Finance Kathryn Roth, Program Manager

M E M O R A N D U M TO: FROM: Superintendents and Charter School Administrators Melissa K. Ambre, Director, Office of School Finance Kathryn Roth, Program Manager DATE: January 15, 2016 RE: 2016 Summer

M E M O R A N D U M TO: FROM: Superintendents and Charter School Administrators Melissa K. Ambre, Director, Office of School Finance Kathryn Roth, Program Manager DATE: January 15, 2016 RE: 2016 Summer

12/05/2014. Alaska Public School Funding Formula Overview SENATE BILL 36 THIS PRESENTATION PROVIDES AN OVERVIEW OF: Mindy Lobaugh

Alaska Public School Funding Formula Overview Presented by Mindy Lobaugh School Finance Mindy.Lobaugh@alaska.gov (907) 465-2261 http://education.alaska.gov SENATE BILL 36 The current state public school

Alaska Public School Funding Formula Overview Presented by Mindy Lobaugh School Finance Mindy.Lobaugh@alaska.gov (907) 465-2261 http://education.alaska.gov SENATE BILL 36 The current state public school

Analysis One Code Desc. Transaction Amount. Fiscal Period

Analysis One Code Desc Transaction Amount Fiscal Period 57.63 Oct-12 12.13 Oct-12-38.90 Oct-12-773.00 Oct-12-800.00 Oct-12-187.00 Oct-12-82.00 Oct-12-82.00 Oct-12-110.00 Oct-12-1115.25 Oct-12-71.00 Oct-12-41.00

Analysis One Code Desc Transaction Amount Fiscal Period 57.63 Oct-12 12.13 Oct-12-38.90 Oct-12-773.00 Oct-12-800.00 Oct-12-187.00 Oct-12-82.00 Oct-12-82.00 Oct-12-110.00 Oct-12-1115.25 Oct-12-71.00 Oct-12-41.00

Financing Education In Minnesota 2013-14. A Publication of the Minnesota House of Representatives Fiscal Analysis Department

Financing Education In Minnesota 2013-14 A Publication of the Minnesota House of Representatives Fiscal Analysis Department November 2013 Financing Education in Minnesota 2013-14 A Publication of the Minnesota

Financing Education In Minnesota 2013-14 A Publication of the Minnesota House of Representatives Fiscal Analysis Department November 2013 Financing Education in Minnesota 2013-14 A Publication of the Minnesota

CHAPTER 16-7.2 The Education Equity and Property Tax Relief Act 1

CHAPTER 16-7.2 The Education Equity and Property Tax Relief Act 1 SECTION 16-7.2-1 16-7.2-1 Legislative findings. (a) The general assembly recognizes the need for an equitable distribution of resources

CHAPTER 16-7.2 The Education Equity and Property Tax Relief Act 1 SECTION 16-7.2-1 16-7.2-1 Legislative findings. (a) The general assembly recognizes the need for an equitable distribution of resources

LEGISLATIVE SERVICES AGENCY OFFICE OF FISCAL AND MANAGEMENT ANALYSIS 301 State House (317) 232-9855

232-9855") LEGISLATIVE SERVICES AGENCY OFFICE OF FISCAL AND MANAGEMENT ANALYSIS 301 State House (317) 232-9855 FISCAL IMPACT STATEMENT LS 7482 DATE PREPARED: Mar 30, 2001 BILL NUMBER: SB 199 BILL AMENDED: Mar 29,

LEGISLATIVE SERVICES AGENCY OFFICE OF FISCAL AND MANAGEMENT ANALYSIS 301 State House (317) 232-9855 FISCAL IMPACT STATEMENT LS 7482 DATE PREPARED: Mar 30, 2001 BILL NUMBER: SB 199 BILL AMENDED: Mar 29,

Florida Education Finance Program (FEFP)

") F l o r i d a H o u s e o f R e p r e s e n t a t i v e s Florida Education Finance Program (FEFP) EDUCATION FACT SHEET 2010-11 What is the Florida Education Finance Program? The Florida Education Finance

F l o r i d a H o u s e o f R e p r e s e n t a t i v e s Florida Education Finance Program (FEFP) EDUCATION FACT SHEET 2010-11 What is the Florida Education Finance Program? The Florida Education Finance

STATE SPECIAL EDUCATION FUNDING CHANGES: FY 2014 - FY 2016

STATE SPECIAL EDUCATION FUNDING CHANGES: FY 2014 - FY 2016 Special Education Caseloads Task Force October 15, 2013 Tom Melcher, Director School Finance Division FY 2013 Funding General Education Revenue

STATE SPECIAL EDUCATION FUNDING CHANGES: FY 2014 - FY 2016 Special Education Caseloads Task Force October 15, 2013 Tom Melcher, Director School Finance Division FY 2013 Funding General Education Revenue

Essential Programs & Services State Calculation for Funding Public Education (ED279):

:") Essential Programs & Services State Calculation for Funding Public Education (ED279): Maine s Funding Formula for Sharing the Costs of PreK-12 Education between State and Local: 1. Determine the EPS Defined

Essential Programs & Services State Calculation for Funding Public Education (ED279): Maine s Funding Formula for Sharing the Costs of PreK-12 Education between State and Local: 1. Determine the EPS Defined

Understanding Senate Bill 13-213

Understanding Senate Bill 13-213 Proposed Future School Finance Act August 2013 Colorado Department of Education Public School Finance 201 E. Colfax Ave., Denver, CO 80203 UNDERSTANDING SENATE BILL 13-213

Understanding Senate Bill 13-213 Proposed Future School Finance Act August 2013 Colorado Department of Education Public School Finance 201 E. Colfax Ave., Denver, CO 80203 UNDERSTANDING SENATE BILL 13-213

School Finance 101. MASA / MASE Spring Conference Joel Sutter Ehlers Greg Crowe - Ehlers

School Finance 101 MASA / MASE Spring Conference Joel Sutter Ehlers Greg Crowe - Ehlers 3/13/2014 1 Overview Minnesota has one of the most complex school funding systems of any state It is not a logical,

School Finance 101 MASA / MASE Spring Conference Joel Sutter Ehlers Greg Crowe - Ehlers 3/13/2014 1 Overview Minnesota has one of the most complex school funding systems of any state It is not a logical,

Michigan School Loan Revolving Fund General Instructions for Completing Annual Repayment Activity Application

Michigan School Loan Revolving Fund General Instructions for Completing Annual Repayment Activity Application It is a statutory requirement that the district submit a completed Annual Repayment Activity

Michigan School Loan Revolving Fund General Instructions for Completing Annual Repayment Activity Application It is a statutory requirement that the district submit a completed Annual Repayment Activity

ROYAL REHAB COLLEGE AND THE ENTOURAGE EDUCATION GROUP. UPDATED SCHEDULE OF VET UNITS OF STUDY AND VET TUITION FEES Course Aug 1/2015

UPDATED SCHEDULE OF UNITS OF STUDY AND TUITION FEES Course Aug 1/2015 Course Name: Delivery Mode: BSB50215 Diploma of Business Online DBTEU01 01/08/2015 19/08/2015 31/10/2015 0.25 $4245 $3265 DBTEU02 01/11/2015

UPDATED SCHEDULE OF UNITS OF STUDY AND TUITION FEES Course Aug 1/2015 Course Name: Delivery Mode: BSB50215 Diploma of Business Online DBTEU01 01/08/2015 19/08/2015 31/10/2015 0.25 $4245 $3265 DBTEU02 01/11/2015

Special Education Cross-Subsidies Fiscal Year 2013. Fiscal Year 2013. Report. To the. Legislature. As required by. Minnesota Statutes,

Special Education Cross-Subsidies Fiscal Year 2013 Fiscal Year 2013 Report To the Legislature As required by Minnesota Statutes, section 127A.065 COMMISSIONER: Special Education Cross-Subsidies Brenda

Special Education Cross-Subsidies Fiscal Year 2013 Fiscal Year 2013 Report To the Legislature As required by Minnesota Statutes, section 127A.065 COMMISSIONER: Special Education Cross-Subsidies Brenda

Guide to Financing Your Williams College Education 2015-2016

Guide to Financing Your Williams College Education 2015-2016 Choosing the Best Way to Finance Your Education Whether you applied for financial aid or not, there are several ways to address the balance

Guide to Financing Your Williams College Education 2015-2016 Choosing the Best Way to Finance Your Education Whether you applied for financial aid or not, there are several ways to address the balance

MISSOURI. Gerri Ogle Coordinator, School Administrative Services Department of Elementary and Secondary Education I. GENERAL BACKGROUND.

MISSOURI Gerri Ogle Coordinator, School Administrative Services Department of Elementary and Secondary Education I. GENERAL BACKGROUND State The major portion of state funds for elementary and secondary

MISSOURI Gerri Ogle Coordinator, School Administrative Services Department of Elementary and Secondary Education I. GENERAL BACKGROUND State The major portion of state funds for elementary and secondary

FINANCING SCHOOL CHOICE IN MINNESOTA

Program Finance Division FINANCING SCHOOL CHOICE IN MINNESOTA PUBLIC SCHOOL CHOICE 1. Interdistrict Open Enrollment (Minn. Stat. 124D.03) Program allows students to attend public school in a district other

Program Finance Division FINANCING SCHOOL CHOICE IN MINNESOTA PUBLIC SCHOOL CHOICE 1. Interdistrict Open Enrollment (Minn. Stat. 124D.03) Program allows students to attend public school in a district other

uiopasdfghjklzxcvbnmqwertyuiopasdf

qwertyuiopasdfghjklzxcvbnmqwertyui opasdfghjklzxcvbnmqwertyuiopasdfgh jklzxcvbnmqwertyuiopasdfghjklzxcvb SCHOOL FINANCE PAYMENT REPORT (SFPR) ----------------------------------- Line-by-Line Explanation

qwertyuiopasdfghjklzxcvbnmqwertyui opasdfghjklzxcvbnmqwertyuiopasdfgh jklzxcvbnmqwertyuiopasdfghjklzxcvb SCHOOL FINANCE PAYMENT REPORT (SFPR) ----------------------------------- Line-by-Line Explanation

SCHOOL FINANCE 101. Presented by Brenda Burkett, CPA, SFO Chief Financial Officer Norman Public Schools. February 2015

SCHOOL FINANCE 101 Presented by Brenda Burkett, CPA, SFO Chief Financial Officer Norman Public Schools February 2015 Budget and Funding Timeline JUN JUL AUG SEP OCT NOV Final State Aid Allocation from

SCHOOL FINANCE 101 Presented by Brenda Burkett, CPA, SFO Chief Financial Officer Norman Public Schools February 2015 Budget and Funding Timeline JUN JUL AUG SEP OCT NOV Final State Aid Allocation from

Funding North Carolina s Public Schools

Funding North Carolina s Public Schools Brian Matteson Fiscal Research Division Key Takeaways State Public Schools funding is distributed to Local Education Agencies (LEAs) through allotments Allotments

Funding North Carolina s Public Schools Brian Matteson Fiscal Research Division Key Takeaways State Public Schools funding is distributed to Local Education Agencies (LEAs) through allotments Allotments

State Cashflow Management

Informational Paper 77 State Cashflow Management Wisconsin Legislative Fiscal Bureau January, 2009 State Cashflow Management Prepared by Dave Loppnow Wisconsin Legislative Fiscal Bureau One East Main,

Informational Paper 77 State Cashflow Management Wisconsin Legislative Fiscal Bureau January, 2009 State Cashflow Management Prepared by Dave Loppnow Wisconsin Legislative Fiscal Bureau One East Main,

Academic Calendar 2015-2018 Arkansas State University - Jonesboro

Shared Governance Proposal Any constituent (individual or group) may submit a proposal into the shared governance process. In order to be considered, each proposal must contain the following and be directed

Shared Governance Proposal Any constituent (individual or group) may submit a proposal into the shared governance process. In order to be considered, each proposal must contain the following and be directed

The NEVADA PLAN For School Finance An Overview

The NEVADA PLAN For School Finance An Overview Fiscal Analysis Division Legislative Counsel Bureau 2013 Legislative Session Nevada Plan for School Finance I. Overview of Public K-12 Education Finance

The NEVADA PLAN For School Finance An Overview Fiscal Analysis Division Legislative Counsel Bureau 2013 Legislative Session Nevada Plan for School Finance I. Overview of Public K-12 Education Finance

School Funding. Where does school funding come from? Where does it actually go?

SCHOOL FINANCE 101 School Funding Where does school funding come from? Where does it actually go? Basics of School Finance in Ohio: School funding in Ohio is a SHARED responsibility between the state and

SCHOOL FINANCE 101 School Funding Where does school funding come from? Where does it actually go? Basics of School Finance in Ohio: School funding in Ohio is a SHARED responsibility between the state and

School Finance How Does it Work???

School Finance How Does it Work??? March 3, 2016 Leanne Emm, Associate Commissioner Emm_l@cde.state.co.us 303-866-6202 School Finance Total Program Funding 2 1 Total Program Funding The vast majority of

School Finance How Does it Work??? March 3, 2016 Leanne Emm, Associate Commissioner Emm_l@cde.state.co.us 303-866-6202 School Finance Total Program Funding 2 1 Total Program Funding The vast majority of

THE STATE SCHOOL AID ACT OF 1979 Act 94 of 1979

THE STATE SCHOOL AID ACT OF 1979 Act 94 of 1979 AN ACT to make appropriations to aid in the support of the public schools, the intermediate school districts, community colleges, and public universities

THE STATE SCHOOL AID ACT OF 1979 Act 94 of 1979 AN ACT to make appropriations to aid in the support of the public schools, the intermediate school districts, community colleges, and public universities

NEW YORK. Description of the Formula. District-Based Components

NEW YORK NOTE: The following is a high level summary of the NYS school finance system and not an exhaustive or comprehensive description of every school aid formula used in the State. Description of the

NEW YORK NOTE: The following is a high level summary of the NYS school finance system and not an exhaustive or comprehensive description of every school aid formula used in the State. Description of the

VIRGINIA. Description of the Formula

VIRGINIA Description of the Formula The foundation formula is based on pupils in average daily membership (ADM) for the current year. Basic program funding is determined by multiplying total ADM by a per

VIRGINIA Description of the Formula The foundation formula is based on pupils in average daily membership (ADM) for the current year. Basic program funding is determined by multiplying total ADM by a per

Digest Of Public School Finance In Indiana. 2011-2013 Biennium. Indiana Department of Education Dr. Tony Bennett Superintendent of Public Instruction

Digest Of Public School Finance In Indiana 2011-2013 Biennium Indiana Department of Education Dr. Tony Bennett Superintendent of Public Instruction i Policy Notification Statement It is the policy of the

Digest Of Public School Finance In Indiana 2011-2013 Biennium Indiana Department of Education Dr. Tony Bennett Superintendent of Public Instruction i Policy Notification Statement It is the policy of the

A Guide to. NYC Public Schools Budget

A Guide to NYC Public Schools Budget Dear New York City Community Member, With 1.1 million students and over 1,700 schools, the New York City Department of Education (DOE) is the largest school system

A Guide to NYC Public Schools Budget Dear New York City Community Member, With 1.1 million students and over 1,700 schools, the New York City Department of Education (DOE) is the largest school system

Components 127th General Assembly 128th General Assembly

League of Women Voters of Ohio Comparison of the Components of the Education Provisions of Am. Sub. HB 119 (127th General Assembly) and Am. Sub. HB 1 (128th General Assembly) Updated February 2010 Components

League of Women Voters of Ohio Comparison of the Components of the Education Provisions of Am. Sub. HB 119 (127th General Assembly) and Am. Sub. HB 1 (128th General Assembly) Updated February 2010 Components

IPEDS: Collecting Information on Veteran and Servicemember Students

IPEDS: Collecting Information on Veteran and Servicemember Students Gigi Jones, Ph.D. U.S. Department of Education National Center for Education Statistics June 4, 2015 (1:45pm-2:30pm Central) Itinerary

IPEDS: Collecting Information on Veteran and Servicemember Students Gigi Jones, Ph.D. U.S. Department of Education National Center for Education Statistics June 4, 2015 (1:45pm-2:30pm Central) Itinerary

Impact of the Medicare Part D Program on the NC Medicaid Program. Fiscal Research Division December 7, 2005

Impact of the Medicare Part D Program on the NC Medicaid Program Fiscal Research Division December 7, 2005 What is Impact of the Medicare Part D Program on the NC Medicaid Program? The Medicare Prescription

Impact of the Medicare Part D Program on the NC Medicaid Program Fiscal Research Division December 7, 2005 What is Impact of the Medicare Part D Program on the NC Medicaid Program? The Medicare Prescription

Colorado s Current Use of a Single Count Day and Considerations if Average Daily Membership (ADM) is Used as a Funding Mechanism

is Used as a Funding Mechanism") Colorado s Current Use of a Single Count Day and Considerations if Average Daily Membership (ADM) is Used as a Funding Mechanism By: Audit Team, School Finance Division January 2013 Version 1.0 Audit Team,

Colorado s Current Use of a Single Count Day and Considerations if Average Daily Membership (ADM) is Used as a Funding Mechanism By: Audit Team, School Finance Division January 2013 Version 1.0 Audit Team,

State of Vermont. Patrick Flood. Commissioner Vermont Department of Disabilities, Aging and Independent Living

State of Vermont Patrick Flood Commissioner Vermont Department of Disabilities, Aging and Independent Living Shifting the Balance Act 160 Vermont Department of Disabilities, Aging, and Independent Living

State of Vermont Patrick Flood Commissioner Vermont Department of Disabilities, Aging and Independent Living Shifting the Balance Act 160 Vermont Department of Disabilities, Aging, and Independent Living

Debt Comparison by Unit Type

QUESTIONS from the COMMUNITY 1. Recently, it was put out that our school district was over $4,000,000 in debt. A website was also introduced that had some of this statistical data. What is the story with

QUESTIONS from the COMMUNITY 1. Recently, it was put out that our school district was over $4,000,000 in debt. A website was also introduced that had some of this statistical data. What is the story with

Understanding Alabama Schools Accounting System. A Guide to State Allocation Calculations 2013-2014 3/4/2014. Funding Components.

Understanding Alabama Schools Accounting System A Guide to State Allocation Calculations 2013-2014 Sonja Peaspanen State Department of Education March 5, 2014 Funding Components Total Units Total Foundation

Understanding Alabama Schools Accounting System A Guide to State Allocation Calculations 2013-2014 Sonja Peaspanen State Department of Education March 5, 2014 Funding Components Total Units Total Foundation

Health Insurance Exchange Finance Work Group Meeting August 22, 2012 Wakely Consulting Model Table Summaries - Updated

Table 3 Model Take up rate estimates 2014 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Revised 25.0% 25.0% 18.0% 3.6% 3.6% 3.6% 3.6% 3.6% 3.6% 3.6% 3.6% 3.6% Fast 12.0% 18.0% 20.0% 18.0% 6.0% 4.0% 4.0%

Table 3 Model Take up rate estimates 2014 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Revised 25.0% 25.0% 18.0% 3.6% 3.6% 3.6% 3.6% 3.6% 3.6% 3.6% 3.6% 3.6% Fast 12.0% 18.0% 20.0% 18.0% 6.0% 4.0% 4.0%

RI s Education Funding Formula. Introduction and Its Impact on Cumberland Students 02/04/2014

RI s Education Funding Formula Introduction and Its Impact on Cumberland Students 02/04/2014 Overview of the Funding Formula & Basic Education Plan (BEP) Enacted in June 2010 Regulations developed by the

RI s Education Funding Formula Introduction and Its Impact on Cumberland Students 02/04/2014 Overview of the Funding Formula & Basic Education Plan (BEP) Enacted in June 2010 Regulations developed by the

Issue Brief. Illinois School Funding Formula and General State Aid. August 2006

70 East Lake Street Suite 1700 Chicago, IL 60601 312-332-1041 www.ctbaonline.org Issue Brief Illinois School Funding Formula and General State Aid August 2006 For more information please contact Chrissy

70 East Lake Street Suite 1700 Chicago, IL 60601 312-332-1041 www.ctbaonline.org Issue Brief Illinois School Funding Formula and General State Aid August 2006 For more information please contact Chrissy

FUNDING AND FINANCIAL MANAGEMENT OF FLORIDA S PUBLIC CHARTER SCHOOLS

T TECHNICAL ASSISTANCE PAPER No: 2009-03 FUNDING AND FINANCIAL MANAGEMENT OF FLORIDA S PUBLIC CHARTER SCHOOLS This manual describes the funding of Florida s public charter schools and related budget issues.

T TECHNICAL ASSISTANCE PAPER No: 2009-03 FUNDING AND FINANCIAL MANAGEMENT OF FLORIDA S PUBLIC CHARTER SCHOOLS This manual describes the funding of Florida s public charter schools and related budget issues.

LSC Redbook. Analysis of the Executive Budget Proposal. Department of Education

LSC Redbook Analysis of the Executive Budget Proposal Department of Education Emily W. H. Gephart, Budget Analyst Andrew Plagenz, Budget Analyst Edward M. Millane, Budget Analyst Legislative Service Commission

LSC Redbook Analysis of the Executive Budget Proposal Department of Education Emily W. H. Gephart, Budget Analyst Andrew Plagenz, Budget Analyst Edward M. Millane, Budget Analyst Legislative Service Commission

Important Dates Calendar 2014-2015 FALL

Important Dates Calendar 204-205 FALL Rev. 6-8-4 st 8 H st 0 2nd 0 st 5 2nd 5 3rd 5 LSC Advanced Registration Begins May 27 May 27 May 27 May 27 May 27 May 27 May 27 May 27 May 27 Returning Students Advanced

Important Dates Calendar 204-205 FALL Rev. 6-8-4 st 8 H st 0 2nd 0 st 5 2nd 5 3rd 5 LSC Advanced Registration Begins May 27 May 27 May 27 May 27 May 27 May 27 May 27 May 27 May 27 Returning Students Advanced

Department of Health & Human Services (DHHS) Centers for Medicare & Medicaid Services (CMS) Transmittal A-03-043 Date: MAY 23, 2003

Centers for Medicare & Medicaid Services (CMS) Transmittal A-03-043 Date: MAY 23, 2003") Program Memorandum Intermediaries Department of Health & Human Services (DHHS) Centers for Medicare & Medicaid Services (CMS) Transmittal A-03-043 Date: MAY 23, 2003 SUBJECT: CHANGE REQUEST 2692 Changes

Program Memorandum Intermediaries Department of Health & Human Services (DHHS) Centers for Medicare & Medicaid Services (CMS) Transmittal A-03-043 Date: MAY 23, 2003 SUBJECT: CHANGE REQUEST 2692 Changes

SCHOOL FINANCE IN COLORADO

SCHOOL FINANCE IN COLORADO Legislative Council Staff State Capitol Building, Room 029 200 East Colfax Avenue Denver, CO 80203 Phone: (303) 866-3521 March 2011 STATE OF COLORADO LEGISLATIVE COUNCIL COLORADO

SCHOOL FINANCE IN COLORADO Legislative Council Staff State Capitol Building, Room 029 200 East Colfax Avenue Denver, CO 80203 Phone: (303) 866-3521 March 2011 STATE OF COLORADO LEGISLATIVE COUNCIL COLORADO

ASCUS Presentation: Reporting Reconciliation and 915 Processing. School Finance Arizona Department of Education

ASCUS Presentation: Reporting Reconciliation and 915 Processing School Finance Arizona Department of Education New Changes For FY 2014 Report Reconciliation for Student Detail and Student Counts Reports

ASCUS Presentation: Reporting Reconciliation and 915 Processing School Finance Arizona Department of Education New Changes For FY 2014 Report Reconciliation for Student Detail and Student Counts Reports

Legislative Brief: PAY OR PLAY PENALTIES LOOK BACK MEASUREMENT METHOD EXAMPLES. EmPowerHR

EmPowerHR Legislative Brief: PAY OR PLAY PENALTIES LOOK BACK MEASUREMENT METHOD EXAMPLES The Affordable Care Act (ACA) imposes a penalty on applicable large employers (ALEs) that do not offer health insurance

EmPowerHR Legislative Brief: PAY OR PLAY PENALTIES LOOK BACK MEASUREMENT METHOD EXAMPLES The Affordable Care Act (ACA) imposes a penalty on applicable large employers (ALEs) that do not offer health insurance

NATIONAL STUDENT AID PROFILE: OVERVIEW OF 2015 FEDERAL PROGRAMS

NATIONAL STUDENT AID PROFILE: OVERVIEW OF 2015 FEDERAL PROGRAMS Published July 2015 Table of Contents Overview... 1 The Federal Pell Grant Program... 4 Campus-Based Aid Programs... 6 The Federal Supplemental

NATIONAL STUDENT AID PROFILE: OVERVIEW OF 2015 FEDERAL PROGRAMS Published July 2015 Table of Contents Overview... 1 The Federal Pell Grant Program... 4 Campus-Based Aid Programs... 6 The Federal Supplemental

Health Insurance Premiums: Part-time Employees, Partial Unpaid Leaves and Varying Appointment Percentages

University of Wisconsin Health Insurance Premiums: Part- Employees, Partial Unpaid Leaves and Varying Appointment Percentages This policy clarifies payments for employees covered by the Wisconsin Retirement

University of Wisconsin Health Insurance Premiums: Part- Employees, Partial Unpaid Leaves and Varying Appointment Percentages This policy clarifies payments for employees covered by the Wisconsin Retirement

udget For Local Property Tax Revenues

REVENUES 37 Property Tax Revenue Trend 70,000,000 60,000,000 50,000,000 Dollars 40,000,000 30,000,000 20,000,000 10,000,000 - Note: Top part of Personal Property bar is State revenue received from Personal

REVENUES 37 Property Tax Revenue Trend 70,000,000 60,000,000 50,000,000 Dollars 40,000,000 30,000,000 20,000,000 10,000,000 - Note: Top part of Personal Property bar is State revenue received from Personal

Anchorage School District Fiscal Year 2002-2003 PROJECTED REVENUES AND EXPENDITURES SUMMARY

PROJECTED REVENUES AND EXPENDITURES SUMMARY Revenues and Fund Balance 2002-2003 2002-2003 Fund Local State Federal Revenues/Sources Expenditures Taxes Other General $ 113,758,901 $ 5,145,650 $ 224,510,449

PROJECTED REVENUES AND EXPENDITURES SUMMARY Revenues and Fund Balance 2002-2003 2002-2003 Fund Local State Federal Revenues/Sources Expenditures Taxes Other General $ 113,758,901 $ 5,145,650 $ 224,510,449

PI-1524 State Tuition Claim Instructions

PI-1524 State Tuition Claim Instructions Updated June 29, 2015 The PI-1524 State Tuition Claim is an Excel workbook used by Wisconsin school districts eligible for state tuition to submit claims to DPI.

PI-1524 State Tuition Claim Instructions Updated June 29, 2015 The PI-1524 State Tuition Claim is an Excel workbook used by Wisconsin school districts eligible for state tuition to submit claims to DPI.

POST GRADUATE DIPLOMA IN MANAGEMENT

POST GRADUATE DIPLOMA IN MANAGEMENT PROGRAMME DURATION: 12 Months + 3 Months Project Report ELIGIBILITY: 1. Graduate of any discipline, other than music and fine arts, from any recognized university. Graduates

POST GRADUATE DIPLOMA IN MANAGEMENT PROGRAMME DURATION: 12 Months + 3 Months Project Report ELIGIBILITY: 1. Graduate of any discipline, other than music and fine arts, from any recognized university. Graduates

Development of Special Education Programs. Elizabeth Compton Special Education Section ecompton@sde.idaho.edu 332-6869

Development of Special Education Programs Elizabeth Compton Special Education Section ecompton@sde.idaho.edu 332-6869 1 Agenda Welcome & Introductions Objectives Special Education Compliance & Funding

Development of Special Education Programs Elizabeth Compton Special Education Section ecompton@sde.idaho.edu 332-6869 1 Agenda Welcome & Introductions Objectives Special Education Compliance & Funding

South Carolina Unemployment Insurance Trust Fund Annual Assessment FY2015

South Carolina Unemployment Insurance Trust Fund Annual Assessment FY2015 Executive Summary For each fiscal year, the South Carolina Department of Employment and Workforce is required to submit, by October

South Carolina Unemployment Insurance Trust Fund Annual Assessment FY2015 Executive Summary For each fiscal year, the South Carolina Department of Employment and Workforce is required to submit, by October

DEBT MANAGEMENT POLICY AND PROPOSED CERTIFICATES OF PARTICIPATION (COPs) TRANSACTION

TRANSACTION") DEBT MANAGEMENT POLICY AND PROPOSED CERTIFICATES OF PARTICIPATION (COPs) TRANSACTION Los Angeles Unified School District Office of the Chief Financial Officer Background Since 1990, District has issued

DEBT MANAGEMENT POLICY AND PROPOSED CERTIFICATES OF PARTICIPATION (COPs) TRANSACTION Los Angeles Unified School District Office of the Chief Financial Officer Background Since 1990, District has issued

State Comparisons: Aspiration States

State Comparisons: Aspiration States Attainment Average Freshman Graduation Rate from NCES. Cohort Graduation Rate, 18 24 HS Completers, and 25 and Up data from ed.gov. Freshman Graduation Rate (2012)

State Comparisons: Aspiration States Attainment Average Freshman Graduation Rate from NCES. Cohort Graduation Rate, 18 24 HS Completers, and 25 and Up data from ed.gov. Freshman Graduation Rate (2012)

IEDA is charged by the Iowa General Assembly with coordinating four programs that deliver customized training to Iowa business and industry:

Workforce Programs for Iowa Business IEDA is charged by the Iowa General Assembly with coordinating four programs that deliver customized training to Iowa business and industry: 1. Industrial New Jobs

Workforce Programs for Iowa Business IEDA is charged by the Iowa General Assembly with coordinating four programs that deliver customized training to Iowa business and industry: 1. Industrial New Jobs

Dual Credit in Indiana Q & A. Version 7.8 October 30, 2012

Dual Credit in Indiana Q & A Version 7.8 October 30, 2012 Dual Credit in Indiana Q&A GENERAL INFORMATION 1. What is dual credit? In Indiana, dual credit is the term given to courses in which high school

Dual Credit in Indiana Q & A Version 7.8 October 30, 2012 Dual Credit in Indiana Q&A GENERAL INFORMATION 1. What is dual credit? In Indiana, dual credit is the term given to courses in which high school

Arizona School Finance Summary Manual

December 2014 Arizona School Finance Summary Manual A tool developed to assist you in understanding the school budget where the money comes from and where it goes www.aasbo.org Permission is granted to

December 2014 Arizona School Finance Summary Manual A tool developed to assist you in understanding the school budget where the money comes from and where it goes www.aasbo.org Permission is granted to

WAPPINGERS CENTRAL SCHOOL DISTRICT: BUDGET OVERVIEW BOE ADOPTED BUDGET 2013-2014

1 WAPPINGERS CENTRAL SCHOOL DISTRICT: BUDGET OVERVIEW BOE ADOPTED BUDGET 2013-2014 2 WCSD BOE Adopted Budget 2013-2014 IN COMPLIANCE WITH THE TAX CAP 2012-2013 Budget $196,982,040 2013-2014 Budget $205,013,864

1 WAPPINGERS CENTRAL SCHOOL DISTRICT: BUDGET OVERVIEW BOE ADOPTED BUDGET 2013-2014 2 WCSD BOE Adopted Budget 2013-2014 IN COMPLIANCE WITH THE TAX CAP 2012-2013 Budget $196,982,040 2013-2014 Budget $205,013,864

PROCEDURES FOR THE NONPUBLIC AGING SCHOOLS PROGRAM (FISCAL YEAR 2015)

") PROCEDURES FOR THE NONPUBLIC AGING SCHOOLS PROGRAM (FISCAL YEAR 2015) August 2014 These procedures are available for download at: http://www.pscp.state.md.us Applications for this program must be submitted

PROCEDURES FOR THE NONPUBLIC AGING SCHOOLS PROGRAM (FISCAL YEAR 2015) August 2014 These procedures are available for download at: http://www.pscp.state.md.us Applications for this program must be submitted

TEACHING AS A SECOND CAREER

TEACHING AS A SECOND CAREER Sponsored by the Presentation Sisters Presentation College is offering a (7-12) Secondary Education Teaching Certificate (South Dakota licensure only) program. This is a one-year,

TEACHING AS A SECOND CAREER Sponsored by the Presentation Sisters Presentation College is offering a (7-12) Secondary Education Teaching Certificate (South Dakota licensure only) program. This is a one-year,

Helbling Benefits Consulting Your Health Care Reform Partner

Helbling Benefits Consulting Your Health Care Reform Partner Will you be hit with penalties due to health care reform? Once the employer mandate becomes effective, some employers may have to pay a penalty

Helbling Benefits Consulting Your Health Care Reform Partner Will you be hit with penalties due to health care reform? Once the employer mandate becomes effective, some employers may have to pay a penalty

How Utah Public Schools are Funded. Office of Legislative Research and General Counsel February 5, 2013

How Utah Public Schools are Funded Office of Legislative Research and General Counsel February 5, 2013 Utah Public Education System State Board of Education Utah State Office of Education 41 School Districts

How Utah Public Schools are Funded Office of Legislative Research and General Counsel February 5, 2013 Utah Public Education System State Board of Education Utah State Office of Education 41 School Districts

I. GENERAL BACKGROUND

VIRGINIA Kent Dickey Brian Logwood Department of Education Commonwealth of Virginia I. GENERAL BACKGROUND State In 1998 99, 85% of state funds allocated for K 12th grade education supported the Standards

VIRGINIA Kent Dickey Brian Logwood Department of Education Commonwealth of Virginia I. GENERAL BACKGROUND State In 1998 99, 85% of state funds allocated for K 12th grade education supported the Standards

How does the Department define full-time enrollment for Title IV aid purposes?

Enrollment Status 34 CFR 668.2(b). Federal Student Aid Handbook, Vol. 1, Ch. 1. Federal Student Aid Handbook, Vol. 3, Ch. 1. 150 Percent Direct Subsidized Loan Limit Information website. Accurate as of:

Enrollment Status 34 CFR 668.2(b). Federal Student Aid Handbook, Vol. 1, Ch. 1. Federal Student Aid Handbook, Vol. 3, Ch. 1. 150 Percent Direct Subsidized Loan Limit Information website. Accurate as of:

The Basics of Quality Basic Education (QBE) Funding

Funding") The Basics of Quality Basic Education (QBE) Funding Public schools in Chatham County receive a combination of federal, state and local funds to pay for the education of public school students. Public school

The Basics of Quality Basic Education (QBE) Funding Public schools in Chatham County receive a combination of federal, state and local funds to pay for the education of public school students. Public school

IC 20-20-13 Chapter 13. Educational Technology Program and Grants

IC 20-20-13 Chapter 13. Educational Technology Program and Grants IC 20-20-13-0.5 "Fund" Sec. 0.5. As used in this chapter, "fund" refers to the Senator David C. Ford educational technology fund established

IC 20-20-13 Chapter 13. Educational Technology Program and Grants IC 20-20-13-0.5 "Fund" Sec. 0.5. As used in this chapter, "fund" refers to the Senator David C. Ford educational technology fund established

GENERAL INSTRUCTIONS: ANNUAL FINANCIAL REPORT (CNPweb) National School Lunch, School Breakfast Programs 1/09

National School Lunch, School Breakfast Programs 1/09") GENERAL INSTRUCTIONS: ANNUAL FINANCIAL REPORT (CNPweb) National School Lunch, School Breakfast Programs 1/09 These are general guidelines for the online Annual Financial Report (AFR), explaining only the

GENERAL INSTRUCTIONS: ANNUAL FINANCIAL REPORT (CNPweb) National School Lunch, School Breakfast Programs 1/09 These are general guidelines for the online Annual Financial Report (AFR), explaining only the

Arizona School Finance Understanding the System. DR. CHUCK ESSIGS Arizona Association of School Business Officials

Arizona School Finance Understanding the System DR. CHUCK ESSIGS Arizona Association of School Business Officials Funding of Schools 1900 1950 Very little state assistance Very little state control Ability

Arizona School Finance Understanding the System DR. CHUCK ESSIGS Arizona Association of School Business Officials Funding of Schools 1900 1950 Very little state assistance Very little state control Ability

HB 1843 -- MINIMUM TEACHER SALARY

Missouri General Assembly Legislative Update Cooperating School Districts of Greater Kansas City From Bert Kimble, Tom Rackers and Steven Carroll Week 9 March 6, 2014 This week the Missouri General Assembly

Missouri General Assembly Legislative Update Cooperating School Districts of Greater Kansas City From Bert Kimble, Tom Rackers and Steven Carroll Week 9 March 6, 2014 This week the Missouri General Assembly

Initiative 1351 Fiscal Impact

Initiative 1351 Fiscal Impact Initiative 1351 (I-1351) will not increase or decrease state revenues. State expenditures will increase through distributions to local school districts by an estimated $4.7

Initiative 1351 Fiscal Impact Initiative 1351 (I-1351) will not increase or decrease state revenues. State expenditures will increase through distributions to local school districts by an estimated $4.7

Postsecondary Student Financial Aid Facts

The Role of Financial Aid Administrators Financial aid administrators are dedicated to opening the doors of opportunity by making college possible. Student financial assistance for postsecondary education

The Role of Financial Aid Administrators Financial aid administrators are dedicated to opening the doors of opportunity by making college possible. Student financial assistance for postsecondary education

ILLUSTRATION 17-1 CONVERTIBLE SECURITIES CONVERTIBLE BONDS

ILLUSTRATION 17-1 CONVERTIBLE SECURITIES CONVERTIBLE BONDS Issued ten, 8%, $1,000 par value bonds at 110. Each bond is convertible into 100 shares of $5 par value common. Entry at date of issue: Cash 11,000

ILLUSTRATION 17-1 CONVERTIBLE SECURITIES CONVERTIBLE BONDS Issued ten, 8%, $1,000 par value bonds at 110. Each bond is convertible into 100 shares of $5 par value common. Entry at date of issue: Cash 11,000

SCHOOL FINANCE IN COLORADO

SCHOOL FINANCE IN COLORADO Legislative Council Staff State Capitol Building, Room 029 200 East Colfax Avenue Denver, CO 80203 Phone: (303) 866-3521 April 2012 STATE OF COLORADO LEGISLATIVE COUNCIL COLORADO

SCHOOL FINANCE IN COLORADO Legislative Council Staff State Capitol Building, Room 029 200 East Colfax Avenue Denver, CO 80203 Phone: (303) 866-3521 April 2012 STATE OF COLORADO LEGISLATIVE COUNCIL COLORADO

2014 Clerk-Treasurer s Conference. Dan Jones Asst. Director of Budget Division June 2014

2014 Clerk-Treasurer s Conference Dan Jones Asst. Director of Budget Division June 2014 1 Topics Preparing for 2015 Budget Gateway Problem Areas Most Common Reasons for Budget Problems 1782 Requirement:

2014 Clerk-Treasurer s Conference Dan Jones Asst. Director of Budget Division June 2014 1 Topics Preparing for 2015 Budget Gateway Problem Areas Most Common Reasons for Budget Problems 1782 Requirement:

QUEEN S UNIVERSITY BELFAST STUDENT FINANCE FRAMEWORK C O N T E N T S

FINAL QUEEN S UNIVERSITY BELFAST STUDENT FINANCE FRAMEWORK C O N T E N T S Section 1. Introduction 2. Tuition Fees Setting and Approval Mechanism 2.1 Approval Process 2.2 Fees set by Government 2.3 Calculation

FINAL QUEEN S UNIVERSITY BELFAST STUDENT FINANCE FRAMEWORK C O N T E N T S Section 1. Introduction 2. Tuition Fees Setting and Approval Mechanism 2.1 Approval Process 2.2 Fees set by Government 2.3 Calculation

CTE IN MINNESOTA. May 3, 2012 Minnesota Foundation for Student Organizations

CTE IN MINNESOTA May 3, 2012 Minnesota Foundation for Student Organizations Learning in the Context of Careers CTE in Minnesota Four Questions 1. What is career and technical education in Minnesota? 2.

CTE IN MINNESOTA May 3, 2012 Minnesota Foundation for Student Organizations Learning in the Context of Careers CTE in Minnesota Four Questions 1. What is career and technical education in Minnesota? 2.

Pennsylvania Association of School Business Officials

Pennsylvania Association of School Business Officials Mailing Address: Office Location: P.O. Box 6993 2608 Market Place Harrisburg, PA 17112-0993 Harrisburg, PA 17110 Telephone 717-540-9551 www.pasbo.org

Pennsylvania Association of School Business Officials Mailing Address: Office Location: P.O. Box 6993 2608 Market Place Harrisburg, PA 17112-0993 Harrisburg, PA 17110 Telephone 717-540-9551 www.pasbo.org

Kentucky s 529 College Saving Programs. What are 529 Programs? Basic Features of 529 s. Kentucky s Affordable Prepaid Tuition Plan

Kentucky s 529 College Saving Programs Kentucky s Affordable Prepaid Tuition Plan Kentucky Education Savings Plan Trust What are 529 Programs? Defined in Section 529 of the Internal Revenue Code -also

Kentucky s 529 College Saving Programs Kentucky s Affordable Prepaid Tuition Plan Kentucky Education Savings Plan Trust What are 529 Programs? Defined in Section 529 of the Internal Revenue Code -also

ILLINOIS STATE BOARD OF EDUCATION via Video Conference. Chicago Location: ISBE Video Conference Room, 14 th Floor, 100 W. Randolph Street, Chicago, IL

ILLINOIS STATE BOARD OF EDUCATION via Video Conference Chicago Location: ISBE Video Conference Room, 14 th Floor, 100 W. Randolph Street, Chicago, IL Springfield Location: ISBE Video Conference Room, 3

ILLINOIS STATE BOARD OF EDUCATION via Video Conference Chicago Location: ISBE Video Conference Room, 14 th Floor, 100 W. Randolph Street, Chicago, IL Springfield Location: ISBE Video Conference Room, 3

Teachers Superannuation Commission Room 129 3085 Albert Street Regina, Saskatchewan S4S 0B1 Phone: 787-6440 Fax: 787-1939

Teachers Superannuation Commission Room 129 3085 Albert Street Regina, Saskatchewan S4S 0B1 Phone: 787-6440 Fax: 787-1939 Information Manual Pension Contributions Teachers Group Life Insurance Plan Teachers

Teachers Superannuation Commission Room 129 3085 Albert Street Regina, Saskatchewan S4S 0B1 Phone: 787-6440 Fax: 787-1939 Information Manual Pension Contributions Teachers Group Life Insurance Plan Teachers

Sample Program Profile Table. 1. Select Administrative. 2. Select Program Profile

40 TH DAY AND 100 TH DAY COURSE ENROLLMENT REPORTING Policy Citations In alignment with A.R.S. 15-902.I CTE requires districts to report Career and Technical Education student enrollment data to the Department

40 TH DAY AND 100 TH DAY COURSE ENROLLMENT REPORTING Policy Citations In alignment with A.R.S. 15-902.I CTE requires districts to report Career and Technical Education student enrollment data to the Department

College Financial Aid Workshop for Parents (or Grandparents) Session 1

Session 1") Cannon Beach Consultants, Inc 2012 1 College Financial Aid Workshop for Parents (or Grandparents) Session 1 January 31, 2012 Cannon Beach Consultants, Inc 2012 2 1. Overview of College Financial Planning

Cannon Beach Consultants, Inc 2012 1 College Financial Aid Workshop for Parents (or Grandparents) Session 1 January 31, 2012 Cannon Beach Consultants, Inc 2012 2 1. Overview of College Financial Planning

Module 2: Preparing for Capital Venture Financing Building Pro-Forma Financial Statements

Module 2: Preparing for Capital Venture Financing Building Pro-Forma Financial Statements Module 2: Preparing for Capital Venture Financing Building Pro-Forma Financial Statements TABLE OF CONTENTS 1.0

Module 2: Preparing for Capital Venture Financing Building Pro-Forma Financial Statements Module 2: Preparing for Capital Venture Financing Building Pro-Forma Financial Statements TABLE OF CONTENTS 1.0

AT&T Global Network Client for Windows Product Support Matrix January 29, 2015

AT&T Global Network Client for Windows Product Support Matrix January 29, 2015 Product Support Matrix Following is the Product Support Matrix for the AT&T Global Network Client. See the AT&T Global Network

AT&T Global Network Client for Windows Product Support Matrix January 29, 2015 Product Support Matrix Following is the Product Support Matrix for the AT&T Global Network Client. See the AT&T Global Network

Cash Flow Forecasting & Break-Even Analysis

Cash Flow Forecasting & Break-Even Analysis 1. Cash Flow Cash Flow Projections What is cash flow? Cash flow is an estimate of the timing of when the cash associated with sales will be received and when

Cash Flow Forecasting & Break-Even Analysis 1. Cash Flow Cash Flow Projections What is cash flow? Cash flow is an estimate of the timing of when the cash associated with sales will be received and when

SCHOOL FUNDING COMPLETE RESOURCE

[Type text] LEGISLATIVE SERVICE COMMISSION SCHOOL FUNDING COMPLETE RESOURCE Updated February 2011 [Type text] TABLE OF CONTENTS INTRODUCTION... 4 STATE OPERATING REVENUE... 8 Adequacy State Model Amount...

[Type text] LEGISLATIVE SERVICE COMMISSION SCHOOL FUNDING COMPLETE RESOURCE Updated February 2011 [Type text] TABLE OF CONTENTS INTRODUCTION... 4 STATE OPERATING REVENUE... 8 Adequacy State Model Amount...

Student Financial Planning Guide College of Graduate & Extended Studies 2015-2016

Student Financial Planning Guide College of Graduate & Extended Studies 2015-2016 ATTENTION STUDENTS: Please review carefully and retain for reference. Table of Contents Financial Readiness Checklist Includes...

Student Financial Planning Guide College of Graduate & Extended Studies 2015-2016 ATTENTION STUDENTS: Please review carefully and retain for reference. Table of Contents Financial Readiness Checklist Includes...

Arizona School Finance Summary Manual

December 2010 Arizona School Finance Summary Manual A tool developed to assist your understanding of the school budget where the money comes from and where it goes www.aasbo.org Permission is granted to

December 2010 Arizona School Finance Summary Manual A tool developed to assist your understanding of the school budget where the money comes from and where it goes www.aasbo.org Permission is granted to

FY 2014 Third Quarter Financial Report FY 2015 Financial Plan Projection (Draft)

") Herbert H. Lehman College The City University of New York FY 2014 Third Quarter Financial Report FY 2015 Financial Plan Projection (Draft) April 23, 2014 (DRAFT) Division of Administration and Finance

Herbert H. Lehman College The City University of New York FY 2014 Third Quarter Financial Report FY 2015 Financial Plan Projection (Draft) April 23, 2014 (DRAFT) Division of Administration and Finance

Overview of State Funding for Public Education in Idaho

Overview of State Funding for Public Education in Idaho Idaho s public schools receive revenue from state, local, and federal sources. This brief focuses on the allocation of state funds for public education,

Overview of State Funding for Public Education in Idaho Idaho s public schools receive revenue from state, local, and federal sources. This brief focuses on the allocation of state funds for public education,

Retirement Benefit Workshop

Retirement Benefit Workshop Indiana Public Retirement System Teachers Retirement Fund Please silence your cell phone. Today s Agenda TRF s role in your Retirement Benefit Monthly Pension and Annuity Savings

Retirement Benefit Workshop Indiana Public Retirement System Teachers Retirement Fund Please silence your cell phone. Today s Agenda TRF s role in your Retirement Benefit Monthly Pension and Annuity Savings

SCHOOL FINANCE IN COLORADO

STATE OF COLORADO LEGISLATIVE COUNCIL COLORADO GENERAL ASSEMBLY STATE CAPITOL BUILDING RM 029 200 EAST COLFAX AVENUE DENVER CO 80203-1784 M110300000 SCHOOL FINANCE IN COLORADO Legislative Council Staff

STATE OF COLORADO LEGISLATIVE COUNCIL COLORADO GENERAL ASSEMBLY STATE CAPITOL BUILDING RM 029 200 EAST COLFAX AVENUE DENVER CO 80203-1784 M110300000 SCHOOL FINANCE IN COLORADO Legislative Council Staff

1783-1796 Before statehood public education needs were priority- Note: 1784- State of Franklin- Education important with sums paid by the public.

1783-1796 Before statehood public education needs were priority- Note: 1784- State of Franklin- Education important with sums paid by the public. 1789 Congress specified that title for school lands be

1783-1796 Before statehood public education needs were priority- Note: 1784- State of Franklin- Education important with sums paid by the public. 1789 Congress specified that title for school lands be

Comparison of the Executive, Assembly, and Senate Education Proposals FY 2015-2016

Comparison of the Executive, Assembly, and Senate Education Proposals FY 2015-2016 March 24, 2015 The governor s Executive Budget proposal would increase school aid by $1.07 billion. The increase in school

Comparison of the Executive, Assembly, and Senate Education Proposals FY 2015-2016 March 24, 2015 The governor s Executive Budget proposal would increase school aid by $1.07 billion. The increase in school

July 2013 Colorado Department of Education Public School Finance Unit 201 East Colfax Avenue Room 206 Denver, CO 80203 www.cde.state.co.

UNDERSTANDING COLORADO SCHOOL FINANCE AND CATEGORICAL PROGRAM FUNDING July 2013 Colorado Department of Education Public School Finance Unit 201 East Colfax Avenue Room 206 Denver, CO 80203 www.cde.state.co.us

UNDERSTANDING COLORADO SCHOOL FINANCE AND CATEGORICAL PROGRAM FUNDING July 2013 Colorado Department of Education Public School Finance Unit 201 East Colfax Avenue Room 206 Denver, CO 80203 www.cde.state.co.us

AUDIT SUMMARY ONLINE TECHNICAL MANUAL

2014-2015 STATE OF NEW JERSEY DEPARTMENT OF EDUCATION DIVISION OF ADMINISTRATION &FINANCE OFFICE OF SCHOOL FINANCE AUDIT SUMMARY ONLINE TECHNICAL MANUAL TABLE OF CONTENTS PURPOSE.. 3 SUBMISSION DATES..

2014-2015 STATE OF NEW JERSEY DEPARTMENT OF EDUCATION DIVISION OF ADMINISTRATION &FINANCE OFFICE OF SCHOOL FINANCE AUDIT SUMMARY ONLINE TECHNICAL MANUAL TABLE OF CONTENTS PURPOSE.. 3 SUBMISSION DATES..