Credit Cycles and House Prices

|

|

|

- Gerard Williams

- 10 years ago

- Views:

Transcription

1 Credit Cycles and House Prices Workshop on The Financial Sector and the Macro Economy, Danmarks Nationalbank, September 29, 2015 Svend E. Hougaard Jensen, Ph.D. Professor, Department of Economics Director, PeRCent Copenhagen Business School (CBS)

2 Structure: Deleveraging? Credit cycles House prices in Denmark

3 Recent debt developments Looking at the world as a whole: there has been no aggregate deleveraging since 2008 Looking at high-income economies, viewed as a single bloc: there has been no deleveraging since 2008 Looking at emerging market economies: there has been no deleveraging since 2008 Looking at the financial sectors: they have deleveraged in the US and UK Looking at the household sectors: they have deleveraged in the US and, to a lesser degree, in the UK liabilities of households have converged between the US and the Eurozone as a whole

4 Global debt (% of GDP)

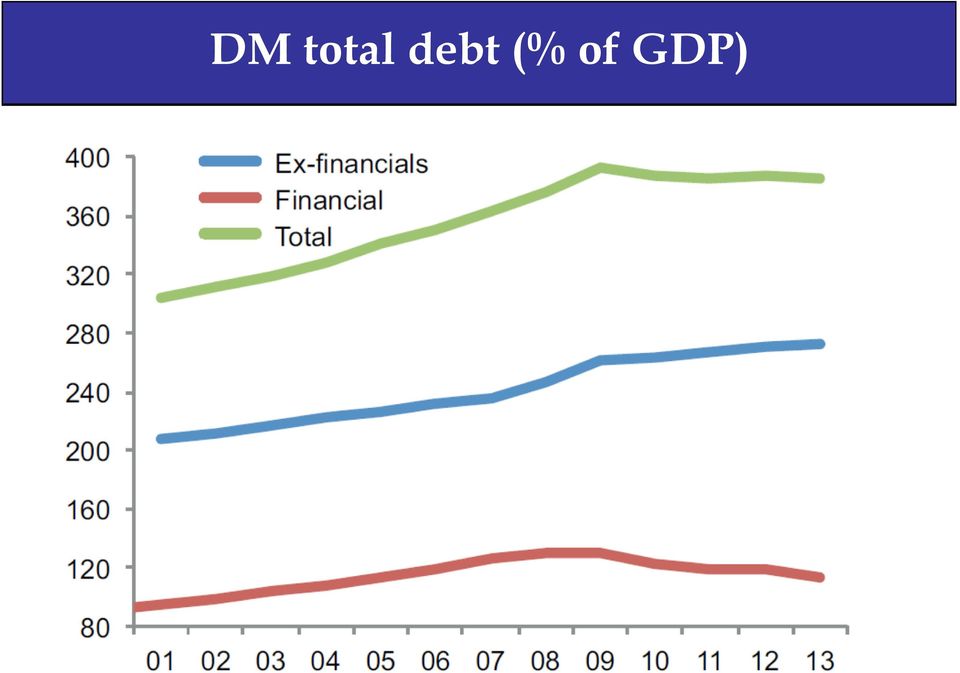

5 DM total debt (% of GDP)

6 Households liabilities (% of disposable income)

7 Eurozone private debt: household (% of GDP)

8 Eurozone private debt: corporate (% of GDP)

9 Government debt (% of GDP)

10 The leverage cycle: A conceptual framework Absorption of innovation Innovation Optimism on growth Credit expansion Reduction in growth prospects Default (inflation) Slow deleveraging Crisis Scaling back of expected credit Structural reforms

11 Do credit cycles matter? A typology of different output paths Type 1: such as Sweden in the early 1990s, the level of output falls, never to regain its pre-crisis trend, but the growth rate recovers. Type 2: more damaging, as in Japan since the 1990s, there is no absolute fall in output, but potential growth falls far short of the pre-crisis rate. Type 3: as in the eurozone now and probably the US and UK, there is both a fall in output and a permanent fall in potential growth.

12 Poisonous combination of high/rising debt and slowdown in GDP growth in advanced economies

13 Do we observe a pattern: Huge expansions in credit, followed by crises and attempts to manage the aftermath? A credit boom in Japan that collapsed after 1990; A credit boom in (some) Nordic countries in the early 1990s, followed by crisis; A credit boom in Asian emerging economies that collapsed in 1997; A credit boom in the north Atlantic economies that collapsed after 2007; and finally in China??? Each is greeted as a new era of prosperity, to collapse into crisis and post-crisis malaise

14 Alternative scenarios for real GDP

15 Recession? Yes but not a crisis

16 Type 1 crisis: permanent loss of output, but potential growth unchanged

17 Type 2 crisis: persistent fall in output growth

18 Type 3 crisis: fall in output and lower growth rate

19 Possible reasons: Do credit cycles matter? The pre-crisis trend was unsustainable Damage to confidence and so investment and innovation from a financial crisis Debt overhang - and deleveraging is hard: may generate a vicious circle from high debt to low growth and back to even higher debt Policy implication: Don t to let debt run ahead of the long-term capacity of an economy to support it in the first place The hope is that macro-prudential policy will achieve this outcome

20 Upsurge in house prices in the noughties For fundamental drivers: Interest rate too low New mortgage products (example of financial innovation) Interest-only (IO) loans adjustable-rate loan/mortgage Fiscal policy too expansionary Freeze on property value tax

21 Importance of new mortgage products for upsurge in house prices in Denmark,

22 Outstanding Mortgage Debt (mio. DKK)

23 Factual and Counterfactual House Prices in Denmark (importance of IO loans)

24 Factual and Counterfactual House Prices in Denmark (importance of IO loans) The graph labeled Denmark shows the house prices index in Denmark using data from DST. The graph labelled Synthetic Control, based on data from BIS, shows the estimated house price index in a counterfactual setting, where Denmark did not introduce IO loans. The Synthetic control is estimated using a sample of countries which (a) did not have IO-mortgages available, but (b) still experienced a housing boom. This is the best estimate of what house prices in Denmark would have been in the absence of the reform.

25 Income distribution of buyers: before and after reform

26 Income distribution of buyers: before and after reform The graph shows the income distribution for buyers of housing in Denmark in 2002 and In 2002 the reform had yet to be announced, so we use 2002 to examine buyers income prior to the introduction of IO mortgages is the first full year where IO mortgages were available. The graph shows that the income distribution of buyers did not significantly change between 2002 and The main point of the graph is to show that we do not see a shift towards low income buyers.

27 Introduction of IO mortgages in Denmark: Main take-home message The introduction of IO mortgages amplified the housing boom and bust in Denmark. House prices jumped an additional percent during the boom compared to a counterfactual that also experienced a housing boom but for which IO loans did not exist. House prices declined an additional percent compared to the counterfactual that did not have IO mortgages available.

28 References: Buttiglione, Luigi, Philip R. Lane, Lucrezia Reichlin and Vincent Reinhart (2014), Deleveraging? What Deleveraging?, Geneva Reports on the World Economy, 16. Bäckman, Claes and Chandler Lutz (2015), The Consequences of Interest Only Loans for the Housing Boom and Bust, mimeo, CBS (contact:

THE RETURN OF CAPITAL EXPENDITURE OR CAPEX CYCLE IN MALAYSIA

PUBLIC BANK BERHAD ECONOMICS DIVISION MENARA PUBLIC BANK 146 JALAN AMPANG 50450 KUALA LUMPUR TEL : 03 2176 6000/666 FAX : 03 2163 9929 Public Bank Economic Review is published bi monthly by Economics Division,

PUBLIC BANK BERHAD ECONOMICS DIVISION MENARA PUBLIC BANK 146 JALAN AMPANG 50450 KUALA LUMPUR TEL : 03 2176 6000/666 FAX : 03 2163 9929 Public Bank Economic Review is published bi monthly by Economics Division,

The Employment Crisis in Spain 1

The Employment Crisis in Spain 1 Juan F Jimeno (Research Division, Banco de España) May 2011 1 Paper prepared for presentation at the United Nations Expert Meeting The Challenge of Building Employment

The Employment Crisis in Spain 1 Juan F Jimeno (Research Division, Banco de España) May 2011 1 Paper prepared for presentation at the United Nations Expert Meeting The Challenge of Building Employment

How To Be Cheerful About 2012

2012: Deeper into crisis or the long road to recovery? Bart Van Craeynest Hoofdeconoom Petercam [email protected] 1 2012: crises looking for answers Global slowdown No 2008-0909 rerun Crises

2012: Deeper into crisis or the long road to recovery? Bart Van Craeynest Hoofdeconoom Petercam [email protected] 1 2012: crises looking for answers Global slowdown No 2008-0909 rerun Crises

The 1990 s Financial Crises in Nordic Countries

The 1990 s Financial Crises in Nordic Countries Seppo Honkapohja, Bank of Finland I. Introduction 19 crises in advanced countries since WWII (before the current) 1990 s crises in Finland, Norway and Sweden

The 1990 s Financial Crises in Nordic Countries Seppo Honkapohja, Bank of Finland I. Introduction 19 crises in advanced countries since WWII (before the current) 1990 s crises in Finland, Norway and Sweden

Annual Economic Report 2015/16 German council of economic experts. Discussion. Lucrezia Reichlin, London Business School

Annual Economic Report 2015/16 German council of economic experts Discussion Lucrezia Reichlin, London Business School Bruegel Brussels, December 4 th 2015 Four parts I. Euro area economic recovery and

Annual Economic Report 2015/16 German council of economic experts Discussion Lucrezia Reichlin, London Business School Bruegel Brussels, December 4 th 2015 Four parts I. Euro area economic recovery and

a) Aggregate Demand (AD) and Aggregate Supply (AS) analysis

Aggregate Demand (AD) and Aggregate Supply (AS) analysis") a) Aggregate Demand (AD) and Aggregate Supply (AS) analysis Determinants of AD: Aggregate demand is the total demand in the economy. It measures spending on goods and services by consumers, firms, the

a) Aggregate Demand (AD) and Aggregate Supply (AS) analysis Determinants of AD: Aggregate demand is the total demand in the economy. It measures spending on goods and services by consumers, firms, the

PROJECTION OF THE FISCAL BALANCE AND PUBLIC DEBT (2012 2027) - SUMMARY

- SUMMARY") PROJECTION OF THE FISCAL BALANCE AND PUBLIC DEBT (2012 2027) - SUMMARY PUBLIC FINANCE REVIEW February 2013 SUMMARY Key messages The purpose of our analysis is to highlight the risks that fiscal policy

PROJECTION OF THE FISCAL BALANCE AND PUBLIC DEBT (2012 2027) - SUMMARY PUBLIC FINANCE REVIEW February 2013 SUMMARY Key messages The purpose of our analysis is to highlight the risks that fiscal policy

THE GREAT DEPRESSION OF FINLAND 1990-1993: causes and consequences. Jaakko Kiander Labour Institute for Economic Research

THE GREAT DEPRESSION OF FINLAND 1990-1993: causes and consequences Jaakko Kiander Labour Institute for Economic Research CONTENTS Causes background The crisis Consequences Role of economic policy Banking

THE GREAT DEPRESSION OF FINLAND 1990-1993: causes and consequences Jaakko Kiander Labour Institute for Economic Research CONTENTS Causes background The crisis Consequences Role of economic policy Banking

Joint Economic Forecast Spring 2013. German Economy Recovering Long-Term Approach Needed to Economic Policy

Joint Economic Forecast Spring 2013 German Economy Recovering Long-Term Approach Needed to Economic Policy Press version Embargo until: Thursday, 18 April 2013, 11.00 a.m. CEST Joint Economic Forecast

Joint Economic Forecast Spring 2013 German Economy Recovering Long-Term Approach Needed to Economic Policy Press version Embargo until: Thursday, 18 April 2013, 11.00 a.m. CEST Joint Economic Forecast

China s Economic Reforms and Growth Prospects. Nicholas Lardy. Anthony M Solomon Senior Fellow. Peterson Institute for International Economics

China s Economic Reforms and Growth Prospects Nicholas Lardy Anthony M Solomon Senior Fellow Peterson Institute for International Economics Paper Prepared for the CF-40 PIIE 2014 Conference Beijing May

China s Economic Reforms and Growth Prospects Nicholas Lardy Anthony M Solomon Senior Fellow Peterson Institute for International Economics Paper Prepared for the CF-40 PIIE 2014 Conference Beijing May

2013 global economic outlook: Are promising growth trends sustainable? Timothy Hopper, Ph.D., Chief Economist, TIAA-CREF January 24, 2013

2013 global economic outlook: Are promising growth trends sustainable? Timothy Hopper, Ph.D., Chief Economist, TIAA-CREF January 24, 2013 U.S. stock market performance in 2012 * +12.59% total return +6.35%

2013 global economic outlook: Are promising growth trends sustainable? Timothy Hopper, Ph.D., Chief Economist, TIAA-CREF January 24, 2013 U.S. stock market performance in 2012 * +12.59% total return +6.35%

3 Macroeconomics LESSON 8

3 Macroeconomics LESSON 8 Fiscal Policy Introduction and Description Fiscal policy is one of the two demand management policies available to policy makers. Government expenditures and the level and type

3 Macroeconomics LESSON 8 Fiscal Policy Introduction and Description Fiscal policy is one of the two demand management policies available to policy makers. Government expenditures and the level and type

Be prepared Four in-depth scenarios for the eurozone and for Switzerland

www.pwc.ch/swissfranc Be prepared Four in-depth scenarios for the eurozone and for Introduction The Swiss economy is cooling down and we are currently experiencing unprecedented levels of uncertainty in

www.pwc.ch/swissfranc Be prepared Four in-depth scenarios for the eurozone and for Introduction The Swiss economy is cooling down and we are currently experiencing unprecedented levels of uncertainty in

Danish mortgage bonds provide attractive yields and low risk

JANUARY 2015 Danish mortgage bonds provide attractive yields and low risk New European Union legislation favours Danish mortgage bonds KEY CONCEPTS New legislation favours Danish mortgage bonds Attractive

JANUARY 2015 Danish mortgage bonds provide attractive yields and low risk New European Union legislation favours Danish mortgage bonds KEY CONCEPTS New legislation favours Danish mortgage bonds Attractive

China's debt - latest assessment SUMMARY

China's debt - latest assessment SUMMARY China s debt-to-gdp ratio continues to increase despite the slowing economy. A convincing case can be made that the situation is manageable: the rate of credit

China's debt - latest assessment SUMMARY China s debt-to-gdp ratio continues to increase despite the slowing economy. A convincing case can be made that the situation is manageable: the rate of credit

Spain Economic Outlook. Rafael Doménech EUI-nomics 2015 Debating the Economic Conditions in the Euro Area and Beyond Firenze, 24th of April, 2015

Spain Economic Outlook Rafael Doménech EUI-nomics 2015 Debating the Economic Conditions in the Euro Area and Beyond Firenze, 24th of April, 2015 The outlook one year ago: the risks were to the upside for

Spain Economic Outlook Rafael Doménech EUI-nomics 2015 Debating the Economic Conditions in the Euro Area and Beyond Firenze, 24th of April, 2015 The outlook one year ago: the risks were to the upside for

Lecture 4: The Aftermath of the Crisis

Lecture 4: The Aftermath of the Crisis 2 The Fed s Efforts to Restore Financial Stability A financial panic in fall 2008 threatened the stability of the global financial system. In its lender-of-last-resort

Lecture 4: The Aftermath of the Crisis 2 The Fed s Efforts to Restore Financial Stability A financial panic in fall 2008 threatened the stability of the global financial system. In its lender-of-last-resort

INFLATION REPORT PRESS CONFERENCE. Thursday 4 th February 2016. Opening remarks by the Governor

INFLATION REPORT PRESS CONFERENCE Thursday 4 th February 2016 Opening remarks by the Governor Good afternoon. At its meeting yesterday, the Monetary Policy Committee (MPC) voted 9-0 to maintain Bank Rate

INFLATION REPORT PRESS CONFERENCE Thursday 4 th February 2016 Opening remarks by the Governor Good afternoon. At its meeting yesterday, the Monetary Policy Committee (MPC) voted 9-0 to maintain Bank Rate

Supplemental Unit 5: Fiscal Policy and Budget Deficits

1 Supplemental Unit 5: Fiscal Policy and Budget Deficits Fiscal and monetary policies are the two major tools available to policy makers to alter total demand, output, and employment. This feature will

1 Supplemental Unit 5: Fiscal Policy and Budget Deficits Fiscal and monetary policies are the two major tools available to policy makers to alter total demand, output, and employment. This feature will

FINANCIALISATION AND EXCHANGE RATE DYNAMICS IN SMALL OPEN ECONOMIES. Hamid Raza PhD Student, Economics University of Limerick Ireland

FINANCIALISATION AND EXCHANGE RATE DYNAMICS IN SMALL OPEN ECONOMIES Hamid Raza PhD Student, Economics University of Limerick Ireland Financialisation Financialisation as a broad concept refers to: a) an

FINANCIALISATION AND EXCHANGE RATE DYNAMICS IN SMALL OPEN ECONOMIES Hamid Raza PhD Student, Economics University of Limerick Ireland Financialisation Financialisation as a broad concept refers to: a) an

Household debt and consumption in the UK. Evidence from UK microdata. 10 March 2015

Household debt and consumption in the UK Evidence from UK microdata 10 March 2015 Disclaimer This presentation does not necessarily represent the views of the Bank of England or members of the Monetary

Household debt and consumption in the UK Evidence from UK microdata 10 March 2015 Disclaimer This presentation does not necessarily represent the views of the Bank of England or members of the Monetary

Debt and (not much) deleveraging

deleveraging") Debt and (not much) deleveraging Peterson Institute for International Economics Susan Lund, McKinsey Global Institute Global debt has increased by $57 trillion since the crisis began with $25 trillion

Debt and (not much) deleveraging Peterson Institute for International Economics Susan Lund, McKinsey Global Institute Global debt has increased by $57 trillion since the crisis began with $25 trillion

NEWS FROM NATIONALBANKEN

1ST QUARTER 2016 NO. 1 NEWS FROM NATIONALBANKEN PROSPERITY IN DENMARK IS KEEPING UP Since the crisis in 2008, the Danish economy has generated an increase in prosperity, which is actually slightly higher

1ST QUARTER 2016 NO. 1 NEWS FROM NATIONALBANKEN PROSPERITY IN DENMARK IS KEEPING UP Since the crisis in 2008, the Danish economy has generated an increase in prosperity, which is actually slightly higher

chapter: Solution Fiscal Policy

Fiscal Policy chapter: 28 13 ECONOMICS MACROECONOMICS 1. The accompanying diagram shows the current macroeconomic situation for the economy of Albernia. You have been hired as an economic consultant to

Fiscal Policy chapter: 28 13 ECONOMICS MACROECONOMICS 1. The accompanying diagram shows the current macroeconomic situation for the economy of Albernia. You have been hired as an economic consultant to

International competition will change mortgage lending

Pentti Hakkarainen Deputy Governor, Bank of Finland International competition will change mortgage lending Nordic Mortgage Council Helsinki, 28 August 2015 28.8.2015 Unrestricted 1 Financial stability

Pentti Hakkarainen Deputy Governor, Bank of Finland International competition will change mortgage lending Nordic Mortgage Council Helsinki, 28 August 2015 28.8.2015 Unrestricted 1 Financial stability

Forecasting Chinese Economy for the Years 2013-2014

Forecasting Chinese Economy for the Years 2013-2014 Xuesong Li Professor of Economics Deputy Director of Institute of Quantitative & Technical Economics Chinese Academy of Social Sciences Email: [email protected]

Forecasting Chinese Economy for the Years 2013-2014 Xuesong Li Professor of Economics Deputy Director of Institute of Quantitative & Technical Economics Chinese Academy of Social Sciences Email: [email protected]

SRAS. is less than Y P

KrugmanMacro_SM_Ch12.qxp 11/15/05 3:18 PM Page 141 Fiscal Policy 1. The accompanying diagram shows the current macroeconomic situation for the economy of Albernia. You have been hired as an economic consultant

KrugmanMacro_SM_Ch12.qxp 11/15/05 3:18 PM Page 141 Fiscal Policy 1. The accompanying diagram shows the current macroeconomic situation for the economy of Albernia. You have been hired as an economic consultant

Euro Zone s Economic Outlook and What it Means for the United States

WELCOME TO THE WEBINAR WEBINAR LINK: HTTP://FRBATL.ADOBECONNECT.COM/ECONOMY/ DIAL-IN NUMBER (MUST USE FOR AUDIO): 855-377-2663 ACCESS CODE: 71032685 Euro Zone s Economic Outlook and What it Means for the

WELCOME TO THE WEBINAR WEBINAR LINK: HTTP://FRBATL.ADOBECONNECT.COM/ECONOMY/ DIAL-IN NUMBER (MUST USE FOR AUDIO): 855-377-2663 ACCESS CODE: 71032685 Euro Zone s Economic Outlook and What it Means for the

The effects of the recent oil price shock on the U.S. and global economy 1. Nouriel Roubini Stern School of Business, NYU. and

The effects of the recent oil price shock on the U.S. and global economy 1 Nouriel Roubini Stern School of Business, NYU and Brad Setser Research Associate, Global Economic Governance Programme, University

The effects of the recent oil price shock on the U.S. and global economy 1 Nouriel Roubini Stern School of Business, NYU and Brad Setser Research Associate, Global Economic Governance Programme, University

Chapter 9 Aggregate Demand and Economic Fluctuations Macroeconomics In Context (Goodwin, et al.)

") Chapter 9 Aggregate Demand and Economic Fluctuations Macroeconomics In Context (Goodwin, et al.) Chapter Overview This chapter first introduces the analysis of business cycles, and introduces you to the

Chapter 9 Aggregate Demand and Economic Fluctuations Macroeconomics In Context (Goodwin, et al.) Chapter Overview This chapter first introduces the analysis of business cycles, and introduces you to the

ECON 201: Introduction to Macroeconomics Final Exam December 13, 2012 NAME:

ECON 201: Introduction to Macroeconomics Final Exam December 13, 2012 NAME: Circle your TA s name: Amy Thiago Samir Circle your section time: 9 a.m. 3 p.m. INSTRUCTIONS: 1) The exam lasts 2 hours. 2) The

ECON 201: Introduction to Macroeconomics Final Exam December 13, 2012 NAME: Circle your TA s name: Amy Thiago Samir Circle your section time: 9 a.m. 3 p.m. INSTRUCTIONS: 1) The exam lasts 2 hours. 2) The

SMEs in London s economy

SMEs in London s economy Kit Malthouse Overview The size of the SME presence in London s economy The economic situation Economic forecasts for the UK and London Some of the issues faced by SMEs How might

SMEs in London s economy Kit Malthouse Overview The size of the SME presence in London s economy The economic situation Economic forecasts for the UK and London Some of the issues faced by SMEs How might

M C A S S E T M A N A G E M E N T H O L D I N G S, L L C

M C A S S E T M A N A G E M E N T H O L D I N G S, L L C 6 Landmark Square, Stamford, CT 06901 Phone (203) 487-6700 Fax: (203) 487-6720 A Global Economy that Sisyphus Would Understand 2013 AAAIM National

M C A S S E T M A N A G E M E N T H O L D I N G S, L L C 6 Landmark Square, Stamford, CT 06901 Phone (203) 487-6700 Fax: (203) 487-6720 A Global Economy that Sisyphus Would Understand 2013 AAAIM National

The IMF believes that Latvia will be able to pay back the loan

The IMF believes that Latvia will be able to pay back the loan The International Monetary Fund (IMF) has not started any particular talks with Latvia about the repayment of the international loan, which

The IMF believes that Latvia will be able to pay back the loan The International Monetary Fund (IMF) has not started any particular talks with Latvia about the repayment of the international loan, which

Answers to Text Questions and Problems in Chapter 11

Answers to Text Questions and Problems in Chapter 11 Answers to Review Questions 1. The aggregate demand curve relates aggregate demand (equal to short-run equilibrium output) to inflation. As inflation

Answers to Text Questions and Problems in Chapter 11 Answers to Review Questions 1. The aggregate demand curve relates aggregate demand (equal to short-run equilibrium output) to inflation. As inflation

Relationship of Macroeconomic Variables and Growth of Insurance in India: A Diagnostic Study

International Journal of Advances in Management and Economics ISSN: 2278-3369 RESEARCH ARTICLE Relationship of Macroeconomic Variables and Growth of Insurance in India: A Diagnostic Study Bunny Singh Bhatia

International Journal of Advances in Management and Economics ISSN: 2278-3369 RESEARCH ARTICLE Relationship of Macroeconomic Variables and Growth of Insurance in India: A Diagnostic Study Bunny Singh Bhatia

Bank credit developments in Spain European Association of Public Banks (EAPB) Annual Congress

Annual Congress") 10.11.2015 Bank credit developments in Spain European Association of Public Banks (EAPB) Annual Congress Fernando Restoy Deputy Governor 1. Introduction Good morning everyone. It is a pleasure for me

10.11.2015 Bank credit developments in Spain European Association of Public Banks (EAPB) Annual Congress Fernando Restoy Deputy Governor 1. Introduction Good morning everyone. It is a pleasure for me

Deficits as far as the eye can see

Testimony of Mark A. Calabria, Ph.D. Director, Financial Regulation Studies, Cato Institute Submitted to the Subcommittee on Insurance, Housing, & Community Opportunity House Committee on Financial Services

Testimony of Mark A. Calabria, Ph.D. Director, Financial Regulation Studies, Cato Institute Submitted to the Subcommittee on Insurance, Housing, & Community Opportunity House Committee on Financial Services

Factoring: A n Effective Financing Option to SMEs in China

Factoring: A n Effective Financing Option to SMEs in China FENG Yue Economics and Management Department, Nanjing Institute of Technology, P.R.China, 211167 [email protected] Abstract: Factoring is a

Factoring: A n Effective Financing Option to SMEs in China FENG Yue Economics and Management Department, Nanjing Institute of Technology, P.R.China, 211167 [email protected] Abstract: Factoring is a

The Impact of the Financial Crisis on Developing Countries. Justin Yifu Lin Senior Vice President & Chief Economist, The World Bank

The Impact of the Financial Crisis on Developing Countries Justin Yifu Lin Senior Vice President & Chief Economist, The World Bank Outline Why was the global economy so dynamic in 2002-07? Why has that

The Impact of the Financial Crisis on Developing Countries Justin Yifu Lin Senior Vice President & Chief Economist, The World Bank Outline Why was the global economy so dynamic in 2002-07? Why has that

Unemployment. AS Economics Presentation 2005

Unemployment AS Economics Presentation 2005 Key Issues The meaning of unemployment Different types of unemployment Consequences of unemployment Unemployment and economic growth Recent trends in UK unemployment

Unemployment AS Economics Presentation 2005 Key Issues The meaning of unemployment Different types of unemployment Consequences of unemployment Unemployment and economic growth Recent trends in UK unemployment

U.S. Fixed Income: Potential Interest Rate Shock Scenario

U.S. Fixed Income: Potential Interest Rate Shock Scenario Executive Summary Income-oriented investors have become accustomed to an environment of consistently low interest rates. Yields on the benchmark

U.S. Fixed Income: Potential Interest Rate Shock Scenario Executive Summary Income-oriented investors have become accustomed to an environment of consistently low interest rates. Yields on the benchmark

Recent U.S. Economic Growth In Charts MAY 2012

Recent U.S. Economic Growth In Charts MAY 212 GROWTH SINCE 29 The Growth Story Since 29 Despite the worst financial crisis since the Great Depression and a series of shocks in its aftermath, the economy

Recent U.S. Economic Growth In Charts MAY 212 GROWTH SINCE 29 The Growth Story Since 29 Despite the worst financial crisis since the Great Depression and a series of shocks in its aftermath, the economy

Research. What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields?

Research What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields? The global economy appears to be on the road to recovery and the risk of a double dip recession is receding.

Research What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields? The global economy appears to be on the road to recovery and the risk of a double dip recession is receding.

UK Government s Public Finance Plans and Fiscal Targets

UK Government s Public Finance Plans and Fiscal Targets Scottish Government June 2015 Overview This paper analyses the scope to make different choices about the UK s public finances, within the fiscal

UK Government s Public Finance Plans and Fiscal Targets Scottish Government June 2015 Overview This paper analyses the scope to make different choices about the UK s public finances, within the fiscal

Demystifying the Chinese Housing Boom

Demystifying the Chinese Housing Boom Hanming Fang University of Pennsylvania & NBER Paper presented at the International Symposium on Housing and Financial Stability in China. Hosted by the Chinese University

Demystifying the Chinese Housing Boom Hanming Fang University of Pennsylvania & NBER Paper presented at the International Symposium on Housing and Financial Stability in China. Hosted by the Chinese University

Note: This feature provides supplementary analysis for the material in Part 3 of Common Sense Economics.

1 Module C: Fiscal Policy and Budget Deficits Note: This feature provides supplementary analysis for the material in Part 3 of Common Sense Economics. Fiscal and monetary policies are the two major tools

1 Module C: Fiscal Policy and Budget Deficits Note: This feature provides supplementary analysis for the material in Part 3 of Common Sense Economics. Fiscal and monetary policies are the two major tools

Macroprudential Policies in Korea

1 IMF-Riksbank Conference Stockholm, November 13~14, 2014 Macroprudential Policies in Korea Tae Soo Kang Disclaimer This presentation represents the views of the author and not necessarily those of the

1 IMF-Riksbank Conference Stockholm, November 13~14, 2014 Macroprudential Policies in Korea Tae Soo Kang Disclaimer This presentation represents the views of the author and not necessarily those of the

Jarle Bergo: Monetary policy and the outlook for the Norwegian economy

Jarle Bergo: Monetary policy and the outlook for the Norwegian economy Speech by Mr Jarle Bergo, Deputy Governor of Norges Bank, at the Capital markets seminar, hosted by Terra-Gruppen AS, Gardermoen,

Jarle Bergo: Monetary policy and the outlook for the Norwegian economy Speech by Mr Jarle Bergo, Deputy Governor of Norges Bank, at the Capital markets seminar, hosted by Terra-Gruppen AS, Gardermoen,

MACROECONOMIC AND INDUSTRY ANALYSIS VALUATION PROCESS

MACROECONOMIC AND INDUSTRY ANALYSIS VALUATION PROCESS BUSINESS ANALYSIS INTRODUCTION To determine a proper price for a firm s stock, security analyst must forecast the dividend & earnings that can be expected

MACROECONOMIC AND INDUSTRY ANALYSIS VALUATION PROCESS BUSINESS ANALYSIS INTRODUCTION To determine a proper price for a firm s stock, security analyst must forecast the dividend & earnings that can be expected

New Monetary Policy Challenges

New Monetary Policy Challenges 63 Journal of Central Banking Theory and Practice, 2013, 1, pp. 63-67 Received: 5 December 2012; accepted: 4 January 2013 UDC: 336.74 Alexey V. Ulyukaev * New Monetary Policy

New Monetary Policy Challenges 63 Journal of Central Banking Theory and Practice, 2013, 1, pp. 63-67 Received: 5 December 2012; accepted: 4 January 2013 UDC: 336.74 Alexey V. Ulyukaev * New Monetary Policy

Fiscal sustainability, long-term interest rates and debt management

Fiscal sustainability, long-term interest rates and debt management Fabrizio Zampolli Bank for International Settlements Basel A presentation at the Dubrovnik Economic Conference 13-14 June 2013 The opinions

Fiscal sustainability, long-term interest rates and debt management Fabrizio Zampolli Bank for International Settlements Basel A presentation at the Dubrovnik Economic Conference 13-14 June 2013 The opinions

SAN DIEGO S ROAD TO RECOVERY

SAN DIEGO S ROAD TO RECOVERY June 2012 Like all American cities, San Diego suffered from the 2008 financial crisis and ensuing recession. Gradual and positive trends in unemployment, real estate, tourism

SAN DIEGO S ROAD TO RECOVERY June 2012 Like all American cities, San Diego suffered from the 2008 financial crisis and ensuing recession. Gradual and positive trends in unemployment, real estate, tourism

Sweden 2013 Article IV Consultation: Concluding Statement of the Mission Stockholm May 31, 2013

Sweden 2013 Article IV Consultation: Concluding Statement of the Mission Stockholm May 31, 2013 Sweden s economy performed well through the crisis, but growth has moderated recently 1. Growth has slowed

Sweden 2013 Article IV Consultation: Concluding Statement of the Mission Stockholm May 31, 2013 Sweden s economy performed well through the crisis, but growth has moderated recently 1. Growth has slowed

European Debt Crisis and Impacts on Developing Countries

July December 2011 SR/GFC/11 9 SESRIC REPORTS ON GLOBAL FINANCIAL CRISIS 9 SESRIC REPORTS ON THE GLOBAL FINANCIAL CRISIS European Debt Crisis and Impacts on Developing Countries STATISTICAL ECONOMIC AND

July December 2011 SR/GFC/11 9 SESRIC REPORTS ON GLOBAL FINANCIAL CRISIS 9 SESRIC REPORTS ON THE GLOBAL FINANCIAL CRISIS European Debt Crisis and Impacts on Developing Countries STATISTICAL ECONOMIC AND

European office rental struggle amidst subdued demand

The Jones Lang LaSalle Office Property Clock - Q2 2012 European office rental struggle amidst subdued demand The European rental index records a second successive modest fall (-0.2%) The European vacancy

The Jones Lang LaSalle Office Property Clock - Q2 2012 European office rental struggle amidst subdued demand The European rental index records a second successive modest fall (-0.2%) The European vacancy

Vol 2014, No. 10. Abstract

Macro-prudential Tools and Credit Risk of Property Lending at Irish banks Niamh Hallissey, Robert Kelly, & Terry O Malley 1 Economic Letter Series Vol 2014, No. 10 Abstract The high level of mortgage arrears

Macro-prudential Tools and Credit Risk of Property Lending at Irish banks Niamh Hallissey, Robert Kelly, & Terry O Malley 1 Economic Letter Series Vol 2014, No. 10 Abstract The high level of mortgage arrears

2.If actual investment is greater than planned investment, inventories increase more than planned. TRUE.

Macro final exam study guide True/False questions - Solutions Case, Fair, Oster Chapter 8 Aggregate Expenditure and Equilibrium Output 1.Firms react to unplanned inventory investment by reducing output.

Macro final exam study guide True/False questions - Solutions Case, Fair, Oster Chapter 8 Aggregate Expenditure and Equilibrium Output 1.Firms react to unplanned inventory investment by reducing output.

CHAPTER 3 THE LOANABLE FUNDS MODEL

CHAPTER 3 THE LOANABLE FUNDS MODEL The next model in our series is called the Loanable Funds Model. This is a model of interest rate determination. It allows us to explore the causes of rising and falling

CHAPTER 3 THE LOANABLE FUNDS MODEL The next model in our series is called the Loanable Funds Model. This is a model of interest rate determination. It allows us to explore the causes of rising and falling

Liability Claims Trends: Emerging Risks and Rebounding Economic Drivers

Liability Claims Trends: Emerging Risks and Rebounding Economic Drivers Roman Lechner 17 th Meeting of The Geneva Association s Annual Circle of Chief Economists Insurance Prospects in a Changing Risk

Liability Claims Trends: Emerging Risks and Rebounding Economic Drivers Roman Lechner 17 th Meeting of The Geneva Association s Annual Circle of Chief Economists Insurance Prospects in a Changing Risk

Managing Systemic Banking Crises. David S. Hoelscher Assistant Director Money and Credit Markets Department

Managing Systemic Banking Crises David S. Hoelscher Assistant Director Money and Credit Markets Department 2 Introduction Systemic banking crises of unprecedented scale: Argentina, East Asia, Ecuador,

Managing Systemic Banking Crises David S. Hoelscher Assistant Director Money and Credit Markets Department 2 Introduction Systemic banking crises of unprecedented scale: Argentina, East Asia, Ecuador,

Insurance Market Outlook

Munich Re Economic Research May 2014 Premium growth is again slowly gathering momentum After a rather restrained 2013 (according to partly preliminary data), we expect growth in global primary insurance

Munich Re Economic Research May 2014 Premium growth is again slowly gathering momentum After a rather restrained 2013 (according to partly preliminary data), we expect growth in global primary insurance

Long-term macroeconomic forecasts Key trends to 2050

A special report from The Economist Intelligence Unit www.eiu.com Contents Overview 2 Top ten economies in 5 at market exchange rates 3 The rise of Asia continues 4 Global dominance of the top three economies

A special report from The Economist Intelligence Unit www.eiu.com Contents Overview 2 Top ten economies in 5 at market exchange rates 3 The rise of Asia continues 4 Global dominance of the top three economies

Economic Overview. East Asia managed to weather the global recession by relying on export-oriented

Economic Overview Economic growth remains strong in East Asia and retains healthy momentum thanks to strong commodity prices and increases in exports. leads the region in growth and its GDP is expected

Economic Overview Economic growth remains strong in East Asia and retains healthy momentum thanks to strong commodity prices and increases in exports. leads the region in growth and its GDP is expected

The French Public Debt Worries and. Solutions

The French Public Debt Worries and Solutions Vesselina Spassova Pierre Garello Abstract: In the context of debt crisis in the European Union, the French public debt finally attracts the attention of the

The French Public Debt Worries and Solutions Vesselina Spassova Pierre Garello Abstract: In the context of debt crisis in the European Union, the French public debt finally attracts the attention of the

Lecture 2. Output, interest rates and exchange rates: the Mundell Fleming model.

Lecture 2. Output, interest rates and exchange rates: the Mundell Fleming model. Carlos Llano (P) & Nuria Gallego (TA) References: these slides have been developed based on the ones provided by Beatriz

Lecture 2. Output, interest rates and exchange rates: the Mundell Fleming model. Carlos Llano (P) & Nuria Gallego (TA) References: these slides have been developed based on the ones provided by Beatriz

When Will the U.S. Job Market Recover?

March 2012 In this newsletter, we focus on the U.S. job market. The economic recovery post-2008 is often referred to as a "jobless recovery" given the persistently high unemployment rate. In this paper

March 2012 In this newsletter, we focus on the U.S. job market. The economic recovery post-2008 is often referred to as a "jobless recovery" given the persistently high unemployment rate. In this paper

Consumer Credit Worldwide at year end 2012

Consumer Credit Worldwide at year end 2012 Introduction For the fifth consecutive year, Crédit Agricole Consumer Finance has published the Consumer Credit Overview, its yearly report on the international

Consumer Credit Worldwide at year end 2012 Introduction For the fifth consecutive year, Crédit Agricole Consumer Finance has published the Consumer Credit Overview, its yearly report on the international

Consumer Over-indebtedness and Financial Vulnerability: Evidence from Credit Bureau Data

KDI International Conference on Household Debt from an International Perspective: Issues and Policy Directions Consumer Over-indebtedness and Financial Vulnerability: Evidence from Credit Bureau Data By

KDI International Conference on Household Debt from an International Perspective: Issues and Policy Directions Consumer Over-indebtedness and Financial Vulnerability: Evidence from Credit Bureau Data By

S&P 500 Composite (Adjusted for Inflation)

") 12/31/1820 03/31/1824 06/30/1827 09/30/1830 12/31/1833 03/31/1837 06/30/1840 09/30/1843 12/31/1846 03/31/1850 06/30/1853 09/30/1856 12/31/1859 03/31/1863 06/30/1866 09/30/1869 12/31/1872 03/31/1876 06/30/1879

12/31/1820 03/31/1824 06/30/1827 09/30/1830 12/31/1833 03/31/1837 06/30/1840 09/30/1843 12/31/1846 03/31/1850 06/30/1853 09/30/1856 12/31/1859 03/31/1863 06/30/1866 09/30/1869 12/31/1872 03/31/1876 06/30/1879

Macroeconomics Instructor Miller Fiscal Policy Practice Problems

Macroeconomics Instructor Miller Fiscal Policy Practice Problems 1. Fiscal policy refers to changes in A) state and local taxes and purchases that are intended to achieve macroeconomic policy objectives.

Macroeconomics Instructor Miller Fiscal Policy Practice Problems 1. Fiscal policy refers to changes in A) state and local taxes and purchases that are intended to achieve macroeconomic policy objectives.

Econ 330 Exam 1 Name ID Section Number

Econ 330 Exam 1 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If during the past decade the average rate of monetary growth

Econ 330 Exam 1 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If during the past decade the average rate of monetary growth

A BRIEF HISTORY OF BRAZIL S GROWTH

A BRIEF HISTORY OF BRAZIL S GROWTH Eliana Cardoso and Vladimir Teles Organization for Economic Co operation and Development (OECD) September 24, 2009 Paris, France. Summary Breaks in Economic Growth Growth

A BRIEF HISTORY OF BRAZIL S GROWTH Eliana Cardoso and Vladimir Teles Organization for Economic Co operation and Development (OECD) September 24, 2009 Paris, France. Summary Breaks in Economic Growth Growth

A Model of Financial Crises

A Model of Financial Crises Coordination Failure due to Bad Assets Keiichiro Kobayashi Research Institute of Economy, Trade and Industry (RIETI) Canon Institute for Global Studies (CIGS) Septempber 16,

A Model of Financial Crises Coordination Failure due to Bad Assets Keiichiro Kobayashi Research Institute of Economy, Trade and Industry (RIETI) Canon Institute for Global Studies (CIGS) Septempber 16,