Chris Leung, Ph.D., CFA, FRM

|

|

|

- Bonnie Jones

- 8 years ago

- Views:

Transcription

1 FNE 215 Financial Planning Chris Leung, Ph.D., CFA, FRM

2 Chapter 2 Planning with Personal Financial Statements

3 Chapter Objectives Explain how to create your personal cash flow statement Identify the factors that affect your cash flows Show how to create a budget based on your forecasted cash flows Describe how to create your personal balance sheet Explain how your net cash flows are related to your personal balance sheet (and therefore affect your wealth)

4 Personal Cash Flow Statement Personal cash flow statement: a financial statement that measures a person s cash inflows and outflows Cash inflows include salaries, interest, dividends Cash outflows include all expenses, both large and small

5 Personal Cash Flow Statement (cont d) Create a statement by recording your revenues and expenses over a period of time Net cash flows: cash inflows minus cash outflows

6

7 Factors That Affect Cash Flow Factors affecting cash inflows: Stage in your career path Closely related to your stage in the life cycle college, career, retirement Type of job Based on skill level and demand for those skills Number of income earners in your household

8 Factors That Affect Cash Flow (cont d) Factors affecting cash outflows: Size of family Age Personal consumption behavior Some people spend all of their income and more while others spend mainly on necessities and concentrate on saving for the future

9 Factors That Affect Cash Flow (cont d)

10 Creating a Budget Budget: a cash flow statement that is based on forecasted cash flows for a future time period Budgets are useful for anticipating either cash surpluses or cash deficiencies

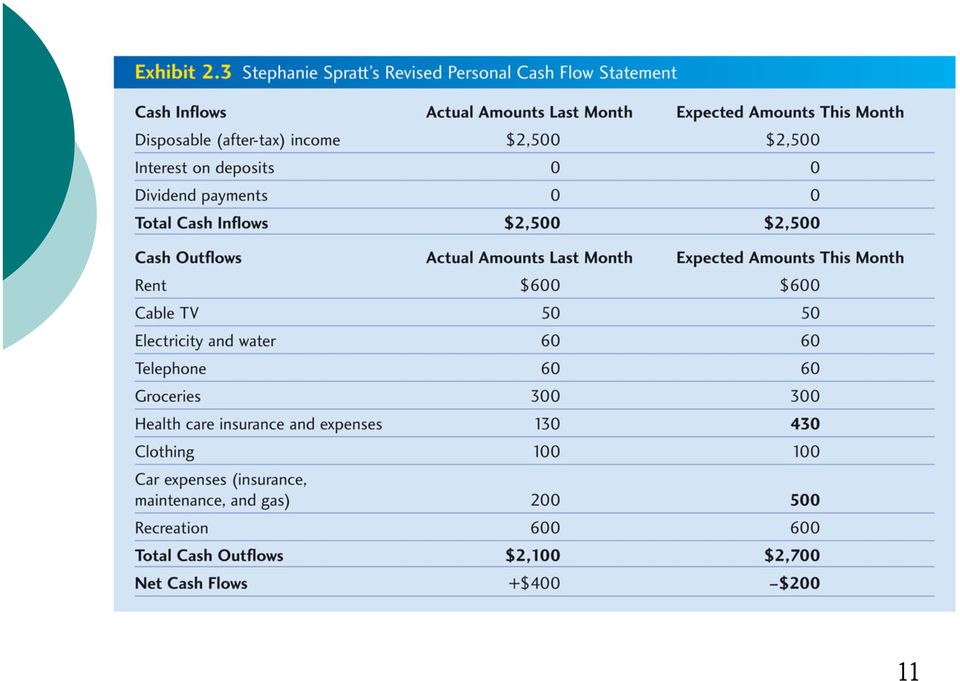

11

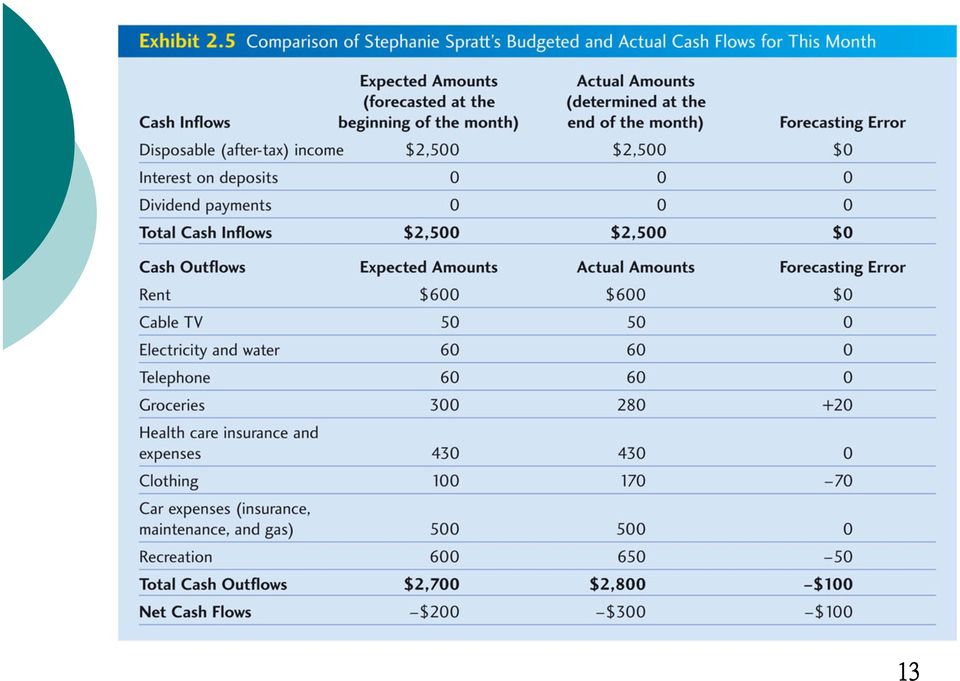

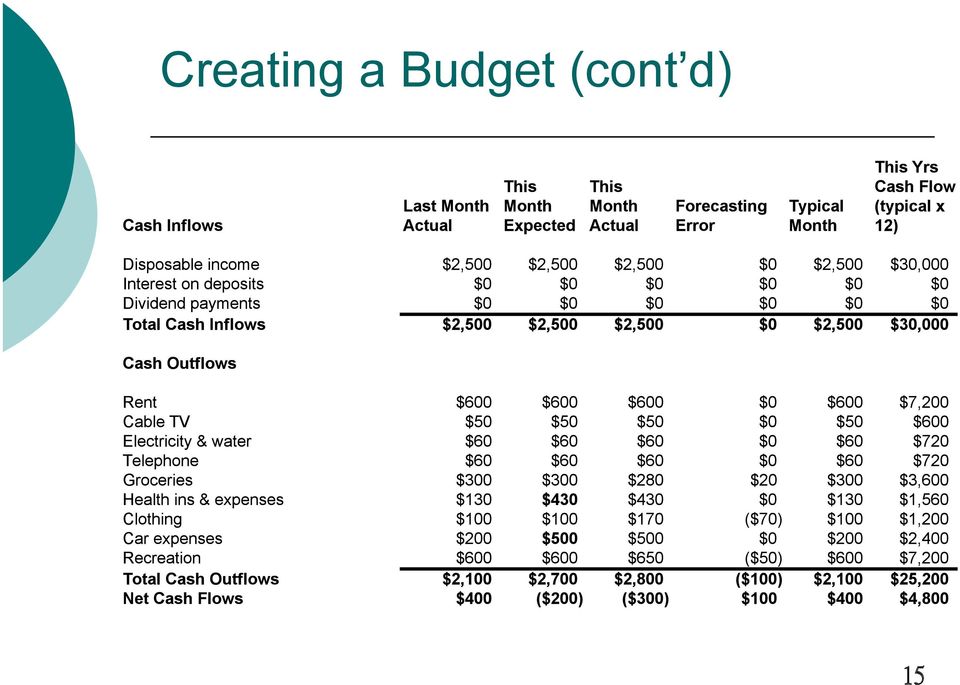

12 Creating a Budget (cont d) Anticipating cash shortages Small shortages can usually be made up from your checking account Budgets provide warning of shortages so that you can prepare for them Assessing the accuracy of the budget Compare predicted cash flows to actual cash flows Adjustment may be necessary

13

14 Creating a Budget (cont d) Forecast net cash flows over several months Use the information for a typical month and adjust it for unusual expenses such as seasonal shopping Allow for some unexpected expenses like medical care, car and home maintenance Create an annual budget by extending your budget out for longer periods

15 Creating a Budget (cont d)

16 Creating a Budget (cont d) Improving the budget Periodically review the budget to see if you are progressing toward your goals Look for areas that can be changed to improve the budget over time Focus on ethics Don t become overly dependent on others Create a budget and stay within it

17 Personal Balance Sheet Personal balance sheet: a summary of your assets (what you own), your liabilities (what you owe), and your net worth (assets minus liabilities) A balance sheet reflects your financial position at a specific point in time

18 Personal Balance Sheet Assets Liquid assets are financial assets that can be easily sold without a loss in value Household assets are items normally owned by a household, such as a home, a car, and furniture You need to establish market values for these assets the amount you would receive if you sold the asset today Investments Bonds, Stocks, Mutual Funds, Real estate

19 Personal Balance Sheet (cont d) Investments Bonds: certificates issued by borrower, usually firms and government agencies, to raise funds Stocks: certificates representing partial ownership in a firm Mutual funds: investment companies that sell shares and invest the proceeds in investment instruments Real estate: holdings in rental property and land Rental property: housing or commercial property that is rented out to others

20 Personal Balance Sheet (cont d) Liabilities Current liabilities: debts that will be paid within a year Long-term liabilities: debts that will be paid over a period longer than one year Net worth is the difference between what you own and what you owe.

21 Personal Balance Sheet (cont d) Creating a personal balance sheet Allows you to determine your net worth Update it periodically to monitor changes in your net worth over time

22

23 Personal Balance Sheet (cont d) Changes in the personal balance sheet Some changes will affect both your personal balance sheet and your net worth Other changes will affect you personal balance sheet and leave your net worth unchanged Consider the previous personal balance sheet with the purchase of a new car

24

25 Personal Balance Sheet (cont d) Analysis of the personal balance sheet Allows monitoring of liquidity, debt, and ability to save Liquidity is measured by the liquidity ratio Liquidity ratio = Liquid assets/current liabilities From personal balance sheet on previous slide 4,000/2,000 = 2 Higher result = greater liquidity

26 Personal Balance Sheet (cont d) Debt level is measured by debt-toasset ratio Debt-to-Asset Ratio = Total liabilities/total assets From personal balance sheet on previous slide 2,000/9,000 = 22.22% Higher ratio = higher debt relative to assets

27 Personal Balance Sheet (cont d) Savings rate measures savings over the period in comparison to disposable income over the period Savings rate = Savings during the period Disposable income during the period From personal balance sheet on previous slide $400/$2,500 = 16%

28 Relationship Between Cash Flows and Wealth Wealth is built by using net cash flows to invest in assets without increasing liabilities Net cash flows can be used to decrease liabilities which will increase net worth Net worth can change even if net cash flows are zero; for example, the value of an asset or investment increases or decreases

29 Relationship Between Cash Flows and Wealth

30 How Budgeting Fits within Your Financial Plan The key budgeting decisions for building your financial plan are: How can I improve my net cash flows in the near future? How can I improve my net cash flows in the distant future?

31 Chapter 3 Applying Time Value Concepts

32 Chapter Objectives Calculate the future value of a dollar amount that you save today Calculate the present value of a dollar amount that will be received in the future Calculate the future value of an annuity Calculate the present value of an annuity

33 The Importance of the Time Value of Money Can be applied to a single dollar amount also called a lump sum Can also be applied to an annuity Annuity: a series of equal cash flow payments that occur at the end of each period An example would be a monthly deposit of $50 into your savings account

34 Future Value of a Single Dollar Amount Compounding: the process by which money accumulates interest To determine the future value of an amount of money you deposit today, you must know: The amount of your deposit today The interest rate to be earned on the deposit The number of years the money will be invested

35 Future Value of a Single Dollar Amount (cont d) Future value interest factor (FVIF): a factor multiplied by today s savings to determine how the savings will accumulate over time Can be calculated using the future value table or a financial calculator Future value table shows various interest rates (i) and time periods (n)

36 Future Value of a Single Dollar Amount (cont d) Suppose you want to know how much money you will have in five years if you invest $5,000 now and earn an annual return of 9 percent The present value of money (PV) is the amount invested, or $5,000 Find the interest rate of 9 percent and a time period of five years on the table

37 Exhibit 3.1 Future Value of $1 (FVIF)

38 Exhibit 3.1 Future Value of $1 (FVIF) (cont d)

39 Future Value of a Single Dollar Amount (cont d) Using the information in the example and the table, we can determine that, in five years, your money will be worth: $5, = $7,695 This can also be determined using a financial calculator

40 Future Value of a Single Dollar Amount (cont d) Focus on ethics: delaying payments Investing money while delaying payment obligations allows you to earn interest on your funds However, delaying payments may result in late fees and penalties that may damage your credit rating Make use of your money while you can, but always make obligatory payments

41 Present Value of a Dollar Amount Discounting: the process of obtaining present values Present values tell you the amount you must invest today to accumulate a certain amount at some future time This amount is based on some interest rate you could earn over that period

42 Present Value of a Dollar Amount (cont d) To determine present values, you need to know: The amount of money to be received in the future The interest rate to be earned on the deposit The number of years the money will be invested

43 Present Value of a Dollar Amount (cont d) Using the Present Value Table Present value interest factor (PVIF): a factor multiplied by a future value to determine the present value of that amount Notice that PVIF is lower as the number of years increases and as the interest rate increases Can also be calculated using a financial calculator

44 Present Value of a Dollar Amount (cont d) You would like to accumulate $50,000 in five years by making a single investment today. You believe you can achieve a return from your investment of 8 percent annually. What is the dollar amount that you need to invest today to achieve your goal?

45 Exhibit 3.2 Present Value of $1 (PVIF)

46 Exhibit 3.2 Present Value of $1 (PVIF) (cont d)

47 Present Value of a Dollar Amount (cont d) Using the information in the example and the table we can determine that in order to have $50,000 today: $50, = $34,050 This can also be determined using a financial calculator

48 Future Value of an Annuity Annuity due: a series of equal cash flow payments that occur at the beginning of each period Timelines: diagrams that show payments received or paid over time These values can also be calculated using a table or a financial calculator

49 Future Value of an Annuity (cont d) Future value interest factor for an annuity (FVIFA): a factor multiplied by the periodic savings level (annuity) to determine how the savings will accumulate over time i is the periodic interest rate n is the number of payments in the annuity

50 Future Value of an Annuity (cont d) Suppose that you have won the lottery and will receive $150,000 at the end of every year for the next 20 years. As soon as you receive the payments, you will invest them at your bank at an interest rate of 7 percent annually. How much will be in your account at the end of 20 years, assuming you do not make any withdrawals?

51 Exhibit 3.3 Future Value of a $1 Ordinary Annuity (FVIFA)

52 Exhibit 3.3 Future Value of a $1 Ordinary Annuity (FVIFA) (cont d)

53 Future Value of an Annuity (cont d) Using our example and the table, we can determine that, at the end of twenty years, you would have: $150, = $6,149,250 This can also be determined using a financial calculator

54 Present Value of an Annuity The present value of an annuity is determined by discounting the individual cash flows of the annuity and adding them up This value also can be obtained by either using a present value of an annuity table or a financial calculator

55 Present Value of an Annuity (cont d) Present value interest factor for an annuity (PVIFA): a factor multiplied by a periodic savings level (annuity) to determine the present value of the annuity i represents various rates of interest n represents the time periods in the annuity

56 Present Value of an Annuity (cont d) Suppose you have just won the lottery. As a result of your luck, you will receive $82,000 at the end of every year for the next 25 years. Now, a financial firm offers you a lump sum of $700,000 in return for these payments. If you can invest your money at an annual interest rate of 9 percent, should you accept the offer?

57 Exhibit 3.4 Present Value of a $1 Ordinary Annuity (PVIFA)

58 Exhibit 3.4 Present Value of a $1 Ordinary Annuity (PVIFA) (cont d)

59 Present Value of an Annuity (cont d) Using our example and the previous table we can determine that the present value of the stream of $82,000 payments is: $82, = $805,486 Since this amount is more than the $700,000 offered, you would reject the offer

60 Using Time Value to Estimate Savings Estimating the future value from savings Provides motivation for regular saving Estimating the annual savings that will achieve a future amount Helps set specific goals when saving for a large purchase

61 How a Savings Plan Fits Within Your Financial Plan Key savings decisions for building your financial plan are: How much should I attempt to accumulate in savings for a future point in time? How much should I attempt to save every month or every year?

1 Tools for Financial Planning

PART 1 Tools for Financial Planning Chapter 2 Planning with Personal Financial Statements How to increase net cash flows in the near future How to increase net cash flows in the distant future Chapter

PART 1 Tools for Financial Planning Chapter 2 Planning with Personal Financial Statements How to increase net cash flows in the near future How to increase net cash flows in the distant future Chapter

Applying Time Value Concepts

Applying Time Value Concepts C H A P T E R 3 based on the value of two packs of cigarettes per day and a modest rate of return? Let s assume that Lou will save an amount equivalent to the cost of two packs

Applying Time Value Concepts C H A P T E R 3 based on the value of two packs of cigarettes per day and a modest rate of return? Let s assume that Lou will save an amount equivalent to the cost of two packs

TIME VALUE OF MONEY. In following we will introduce one of the most important and powerful concepts you will learn in your study of finance;

In following we will introduce one of the most important and powerful concepts you will learn in your study of finance; the time value of money. It is generally acknowledged that money has a time value.

In following we will introduce one of the most important and powerful concepts you will learn in your study of finance; the time value of money. It is generally acknowledged that money has a time value.

Synthesis of Financial Planning

P 7A R T Synthesis of Financial Planning 1. Tools for Financial Planning Budgeting (Chapter 2) Planned Savings (Chapter 3) Tax Planning (Chapter 4) 2. Managing Your Liquidity Bank Services (Chapter 5)

P 7A R T Synthesis of Financial Planning 1. Tools for Financial Planning Budgeting (Chapter 2) Planned Savings (Chapter 3) Tax Planning (Chapter 4) 2. Managing Your Liquidity Bank Services (Chapter 5)

Chapter 4. Time Value of Money. Copyright 2009 Pearson Prentice Hall. All rights reserved.

Chapter 4 Time Value of Money Learning Goals 1. Discuss the role of time value in finance, the use of computational aids, and the basic patterns of cash flow. 2. Understand the concept of future value

Chapter 4 Time Value of Money Learning Goals 1. Discuss the role of time value in finance, the use of computational aids, and the basic patterns of cash flow. 2. Understand the concept of future value

Chapter 4. Time Value of Money. Learning Goals. Learning Goals (cont.)

") Chapter 4 Time Value of Money Learning Goals 1. Discuss the role of time value in finance, the use of computational aids, and the basic patterns of cash flow. 2. Understand the concept of future value

Chapter 4 Time Value of Money Learning Goals 1. Discuss the role of time value in finance, the use of computational aids, and the basic patterns of cash flow. 2. Understand the concept of future value

Chapter 2 Applying Time Value Concepts

Chapter 2 Applying Time Value Concepts Chapter Overview Albert Einstein, the renowned physicist whose theories of relativity formed the theoretical base for the utilization of atomic energy, called the

Chapter 2 Applying Time Value Concepts Chapter Overview Albert Einstein, the renowned physicist whose theories of relativity formed the theoretical base for the utilization of atomic energy, called the

The Time Value of Money

The Time Value of Money Time Value Terminology 0 1 2 3 4 PV FV Future value (FV) is the amount an investment is worth after one or more periods. Present value (PV) is the current value of one or more future

The Time Value of Money Time Value Terminology 0 1 2 3 4 PV FV Future value (FV) is the amount an investment is worth after one or more periods. Present value (PV) is the current value of one or more future

Solutions to Problems

Solutions to Problems P4-1. LG 1: Using a time line Basic a. b. and c. d. Financial managers rely more on present value than future value because they typically make decisions before the start of a project,

Solutions to Problems P4-1. LG 1: Using a time line Basic a. b. and c. d. Financial managers rely more on present value than future value because they typically make decisions before the start of a project,

Chapter 6. Discounted Cash Flow Valuation. Key Concepts and Skills. Multiple Cash Flows Future Value Example 6.1. Answer 6.1

Chapter 6 Key Concepts and Skills Be able to compute: the future value of multiple cash flows the present value of multiple cash flows the future and present value of annuities Discounted Cash Flow Valuation

Chapter 6 Key Concepts and Skills Be able to compute: the future value of multiple cash flows the present value of multiple cash flows the future and present value of annuities Discounted Cash Flow Valuation

Chapter 6. Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams

Chapter 6 Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams 1. Distinguish between an ordinary annuity and an annuity due, and calculate present

Chapter 6 Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams 1. Distinguish between an ordinary annuity and an annuity due, and calculate present

Understand the relationship between financial plans and statements.

#2 Budget Development Your Financial Statements and Plans Learning Goals Understand the relationship between financial plans and statements. Prepare a personal balance sheet. Generate a personal income

#2 Budget Development Your Financial Statements and Plans Learning Goals Understand the relationship between financial plans and statements. Prepare a personal balance sheet. Generate a personal income

Chapter 4. Time Value of Money

Chapter 4 Time Value of Money Learning Goals 1. Discuss the role of time value in finance, the use of computational aids, and the basic patterns of cash flow. 2. Understand the concept of future value

Chapter 4 Time Value of Money Learning Goals 1. Discuss the role of time value in finance, the use of computational aids, and the basic patterns of cash flow. 2. Understand the concept of future value

Discounted Cash Flow Valuation

BUAD 100x Foundations of Finance Discounted Cash Flow Valuation September 28, 2009 Review Introduction to corporate finance What is corporate finance? What is a corporation? What decision do managers make?

BUAD 100x Foundations of Finance Discounted Cash Flow Valuation September 28, 2009 Review Introduction to corporate finance What is corporate finance? What is a corporation? What decision do managers make?

Solutions to Problems: Chapter 5

Solutions to Problems: Chapter 5 P5-1. Using a time line LG 1; Basic a, b, and c d. Financial managers rely more on present value than future value because they typically make decisions before the start

Solutions to Problems: Chapter 5 P5-1. Using a time line LG 1; Basic a, b, and c d. Financial managers rely more on present value than future value because they typically make decisions before the start

Week 4. Chonga Zangpo, DFB

Week 4 Time Value of Money Chonga Zangpo, DFB What is time value of money? It is based on the belief that people have a positive time preference for consumption. It reflects the notion that people prefer

Week 4 Time Value of Money Chonga Zangpo, DFB What is time value of money? It is based on the belief that people have a positive time preference for consumption. It reflects the notion that people prefer

Real estate investment & Appraisal Dr. Ahmed Y. Dashti. Sample Exam Questions

Real estate investment & Appraisal Dr. Ahmed Y. Dashti Sample Exam Questions Problem 3-1 a) Future Value = $12,000 (FVIF, 9%, 7 years) = $12,000 (1.82804) = $21,936 (annual compounding) b) Future Value

Real estate investment & Appraisal Dr. Ahmed Y. Dashti Sample Exam Questions Problem 3-1 a) Future Value = $12,000 (FVIF, 9%, 7 years) = $12,000 (1.82804) = $21,936 (annual compounding) b) Future Value

Chapter 3. Understanding The Time Value of Money. Prentice-Hall, Inc. 1

Chapter 3 Understanding The Time Value of Money Prentice-Hall, Inc. 1 Time Value of Money A dollar received today is worth more than a dollar received in the future. The sooner your money can earn interest,

Chapter 3 Understanding The Time Value of Money Prentice-Hall, Inc. 1 Time Value of Money A dollar received today is worth more than a dollar received in the future. The sooner your money can earn interest,

KENT FAMILY FINANCES

FACTS KENT FAMILY FINANCES Ken and Kendra Kent have been married twelve years and have twin 4-year-old sons. Kendra earns $78,000 as a Walmart assistant manager and Ken is a stay-at-home dad. They give

FACTS KENT FAMILY FINANCES Ken and Kendra Kent have been married twelve years and have twin 4-year-old sons. Kendra earns $78,000 as a Walmart assistant manager and Ken is a stay-at-home dad. They give

Time Value of Money Problems

Time Value of Money Problems 1. What will a deposit of $4,500 at 10% compounded semiannually be worth if left in the bank for six years? a. $8,020.22 b. $7,959.55 c. $8,081.55 d. $8,181.55 2. What will

Time Value of Money Problems 1. What will a deposit of $4,500 at 10% compounded semiannually be worth if left in the bank for six years? a. $8,020.22 b. $7,959.55 c. $8,081.55 d. $8,181.55 2. What will

Ing. Tomáš Rábek, PhD Department of finance

Ing. Tomáš Rábek, PhD Department of finance For financial managers to have a clear understanding of the time value of money and its impact on stock prices. These concepts are discussed in this lesson,

Ing. Tomáš Rábek, PhD Department of finance For financial managers to have a clear understanding of the time value of money and its impact on stock prices. These concepts are discussed in this lesson,

Time Value Conepts & Applications. Prof. Raad Jassim

Time Value Conepts & Applications Prof. Raad Jassim Chapter Outline Introduction to Valuation: The Time Value of Money 1 2 3 4 5 6 7 8 Future Value and Compounding Present Value and Discounting More on

Time Value Conepts & Applications Prof. Raad Jassim Chapter Outline Introduction to Valuation: The Time Value of Money 1 2 3 4 5 6 7 8 Future Value and Compounding Present Value and Discounting More on

Chapter 6. Time Value of Money Concepts. Simple Interest 6-1. Interest amount = P i n. Assume you invest $1,000 at 6% simple interest for 3 years.

6-1 Chapter 6 Time Value of Money Concepts 6-2 Time Value of Money Interest is the rent paid for the use of money over time. That s right! A dollar today is more valuable than a dollar to be received in

6-1 Chapter 6 Time Value of Money Concepts 6-2 Time Value of Money Interest is the rent paid for the use of money over time. That s right! A dollar today is more valuable than a dollar to be received in

2 The Mathematics. of Finance. Copyright Cengage Learning. All rights reserved.

2 The Mathematics of Finance Copyright Cengage Learning. All rights reserved. 2.3 Annuities, Loans, and Bonds Copyright Cengage Learning. All rights reserved. Annuities, Loans, and Bonds A typical defined-contribution

2 The Mathematics of Finance Copyright Cengage Learning. All rights reserved. 2.3 Annuities, Loans, and Bonds Copyright Cengage Learning. All rights reserved. Annuities, Loans, and Bonds A typical defined-contribution

MODULE: PRINCIPLES OF FINANCE

Programme: BSc (Hons) Financial Services with Law BSc (Hons) Accounting with Finance BSc (Hons) Banking and International Finance BSc (Hons) Management Cohort: BFSL/13/FT Aug BACF/13/PT Aug BACF/13/FT

Programme: BSc (Hons) Financial Services with Law BSc (Hons) Accounting with Finance BSc (Hons) Banking and International Finance BSc (Hons) Management Cohort: BFSL/13/FT Aug BACF/13/PT Aug BACF/13/FT

CHAPTER 4. The Time Value of Money. Chapter Synopsis

CHAPTER 4 The Time Value of Money Chapter Synopsis Many financial problems require the valuation of cash flows occurring at different times. However, money received in the future is worth less than money

CHAPTER 4 The Time Value of Money Chapter Synopsis Many financial problems require the valuation of cash flows occurring at different times. However, money received in the future is worth less than money

Preparing Family Net Worth and Income Statements

Family and Consumer Sciences FSFCS49 Preparing Family Net Worth and Income Statements Laura Connerly Instructor - Family Resource Management Arkansas Is Our Campus Visit our web site at: http://www.uaex.edu

Family and Consumer Sciences FSFCS49 Preparing Family Net Worth and Income Statements Laura Connerly Instructor - Family Resource Management Arkansas Is Our Campus Visit our web site at: http://www.uaex.edu

Cash Flow Forecasting & Break-Even Analysis

Cash Flow Forecasting & Break-Even Analysis 1. Cash Flow Cash Flow Projections What is cash flow? Cash flow is an estimate of the timing of when the cash associated with sales will be received and when

Cash Flow Forecasting & Break-Even Analysis 1. Cash Flow Cash Flow Projections What is cash flow? Cash flow is an estimate of the timing of when the cash associated with sales will be received and when

Discounted Cash Flow Valuation

Discounted Cash Flow Valuation Chapter 5 Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

Discounted Cash Flow Valuation Chapter 5 Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

CHAPTER 6. Accounting and the Time Value of Money. 2. Use of tables. 13, 14 8 1. a. Unknown future amount. 7, 19 1, 5, 13 2, 3, 4, 6

CHAPTER 6 Accounting and the Time Value of Money ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems 1. Present value concepts. 1, 2, 3, 4, 5, 9, 17, 19 2. Use

CHAPTER 6 Accounting and the Time Value of Money ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems 1. Present value concepts. 1, 2, 3, 4, 5, 9, 17, 19 2. Use

PRESENT VALUE ANALYSIS. Time value of money equal dollar amounts have different values at different points in time.

PRESENT VALUE ANALYSIS Time value of money equal dollar amounts have different values at different points in time. Present value analysis tool to convert CFs at different points in time to comparable values

PRESENT VALUE ANALYSIS Time value of money equal dollar amounts have different values at different points in time. Present value analysis tool to convert CFs at different points in time to comparable values

Practice Problems. Use the following information extracted from present and future value tables to answer question 1 to 4.

PROBLEM 1 MULTIPLE CHOICE Practice Problems Use the following information extracted from present and future value tables to answer question 1 to 4. Type of Table Number of Periods Interest Rate Factor

PROBLEM 1 MULTIPLE CHOICE Practice Problems Use the following information extracted from present and future value tables to answer question 1 to 4. Type of Table Number of Periods Interest Rate Factor

Present Value and Annuities. Chapter 3 Cont d

Present Value and Annuities Chapter 3 Cont d Present Value Helps us answer the question: What s the value in today s dollars of a sum of money to be received in the future? It lets us strip away the effects

Present Value and Annuities Chapter 3 Cont d Present Value Helps us answer the question: What s the value in today s dollars of a sum of money to be received in the future? It lets us strip away the effects

Discounted Cash Flow Valuation

6 Formulas Discounted Cash Flow Valuation McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter Outline Future and Present Values of Multiple Cash Flows Valuing

6 Formulas Discounted Cash Flow Valuation McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter Outline Future and Present Values of Multiple Cash Flows Valuing

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Solutions to Questions and Problems NOTE: All-end-of chapter problems were solved using a spreadsheet. Many problems require multiple steps. Due to space and readability

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Solutions to Questions and Problems NOTE: All-end-of chapter problems were solved using a spreadsheet. Many problems require multiple steps. Due to space and readability

QUIZ IV Version 1. March 24, 2004. 4:35 p.m. 5:40 p.m. BA 2-210

NAME: Student ID: College of Business Administration Department of Economics Principles of Macroeconomics O. Mikhail ECO 2013-0008 Spring 2004 QUIZ IV Version 1 This closed book QUIZ is worth 100 points.

NAME: Student ID: College of Business Administration Department of Economics Principles of Macroeconomics O. Mikhail ECO 2013-0008 Spring 2004 QUIZ IV Version 1 This closed book QUIZ is worth 100 points.

1. If you wish to accumulate $140,000 in 13 years, how much must you deposit today in an account that pays an annual interest rate of 14%?

Chapter 2 - Sample Problems 1. If you wish to accumulate $140,000 in 13 years, how much must you deposit today in an account that pays an annual interest rate of 14%? 2. What will $247,000 grow to be in

Chapter 2 - Sample Problems 1. If you wish to accumulate $140,000 in 13 years, how much must you deposit today in an account that pays an annual interest rate of 14%? 2. What will $247,000 grow to be in

Principles of Managerial Finance INTEREST RATE FACTOR SUPPLEMENT

Principles of Managerial Finance INTEREST RATE FACTOR SUPPLEMENT 1 5 Time Value of Money FINANCIAL TABLES Financial tables include various future and present value interest factors that simplify time value

Principles of Managerial Finance INTEREST RATE FACTOR SUPPLEMENT 1 5 Time Value of Money FINANCIAL TABLES Financial tables include various future and present value interest factors that simplify time value

Present Value Concepts

Present Value Concepts Present value concepts are widely used by accountants in the preparation of financial statements. In fact, under International Financial Reporting Standards (IFRS), these concepts

Present Value Concepts Present value concepts are widely used by accountants in the preparation of financial statements. In fact, under International Financial Reporting Standards (IFRS), these concepts

EXERCISE 6-4 (15 20 minutes)

") EXERCISE 6-4 (15 20 minutes) (a) (b) (c) (d) Future value of an ordinary annuity of $4,000 a period for 20 periods at 8% $183,047.84 ($4,000 X 45.76196) Factor (1 +.08) X 1.08 Future value of an annuity

EXERCISE 6-4 (15 20 minutes) (a) (b) (c) (d) Future value of an ordinary annuity of $4,000 a period for 20 periods at 8% $183,047.84 ($4,000 X 45.76196) Factor (1 +.08) X 1.08 Future value of an annuity

Chapter 6 Contents. Principles Used in Chapter 6 Principle 1: Money Has a Time Value.

Chapter 6 The Time Value of Money: Annuities and Other Topics Chapter 6 Contents Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate present and future values

Chapter 6 The Time Value of Money: Annuities and Other Topics Chapter 6 Contents Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate present and future values

Ing. Lenka Strýčková, Ph.D.

Ing. Lenka Strýčková, Ph.D. 1. Introduction to Business Financial Management (introduction to the course, basic terminology) 2. Capital Budgeting: Long-Term Decisions (capital budgeting, short-term and

Ing. Lenka Strýčková, Ph.D. 1. Introduction to Business Financial Management (introduction to the course, basic terminology) 2. Capital Budgeting: Long-Term Decisions (capital budgeting, short-term and

Module 5: Interest concepts of future and present value

Page 1 of 23 Module 5: Interest concepts of future and present value Overview In this module, you learn about the fundamental concepts of interest and present and future values, as well as ordinary annuities

Page 1 of 23 Module 5: Interest concepts of future and present value Overview In this module, you learn about the fundamental concepts of interest and present and future values, as well as ordinary annuities

STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

PowerPoint. to accompany. Chapter 5. Interest Rates

PowerPoint to accompany Chapter 5 Interest Rates 5.1 Interest Rate Quotes and Adjustments To understand interest rates, it s important to think of interest rates as a price the price of using money. When

PowerPoint to accompany Chapter 5 Interest Rates 5.1 Interest Rate Quotes and Adjustments To understand interest rates, it s important to think of interest rates as a price the price of using money. When

How to Prepare a Cash Flow Forecast

The Orangeville & Area Small Business Enterprise Centre (SBEC) 87 Broadway, Orangeville ON L9W 1K1 519-941-0440 Ext. 2286 or 2291 sbec@orangeville.ca www.orangevillebusiness.ca Supported by its Partners:

The Orangeville & Area Small Business Enterprise Centre (SBEC) 87 Broadway, Orangeville ON L9W 1K1 519-941-0440 Ext. 2286 or 2291 sbec@orangeville.ca www.orangevillebusiness.ca Supported by its Partners:

Sample Examination Questions CHAPTER 6 ACCOUNTING AND THE TIME VALUE OF MONEY MULTIPLE CHOICE Conceptual Answer No. Description d 1. Definition of present value. c 2. Understanding compound interest tables.

Sample Examination Questions CHAPTER 6 ACCOUNTING AND THE TIME VALUE OF MONEY MULTIPLE CHOICE Conceptual Answer No. Description d 1. Definition of present value. c 2. Understanding compound interest tables.

Chapter 4. The Time Value of Money

Chapter 4 The Time Value of Money 4-2 Topics Covered Future Values and Compound Interest Present Values Multiple Cash Flows Perpetuities and Annuities Inflation and Time Value Effective Annual Interest

Chapter 4 The Time Value of Money 4-2 Topics Covered Future Values and Compound Interest Present Values Multiple Cash Flows Perpetuities and Annuities Inflation and Time Value Effective Annual Interest

The Time Value of Money

C H A P T E R6 The Time Value of Money When plumbers or carpenters tackle a job, they begin by opening their toolboxes, which hold a variety of specialized tools to help them perform their jobs. The financial

C H A P T E R6 The Time Value of Money When plumbers or carpenters tackle a job, they begin by opening their toolboxes, which hold a variety of specialized tools to help them perform their jobs. The financial

FIN 3000. Chapter 6. Annuities. Liuren Wu

FIN 3000 Chapter 6 Annuities Liuren Wu Overview 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams Learning objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate

FIN 3000 Chapter 6 Annuities Liuren Wu Overview 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams Learning objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate

Chapter 7 SOLUTIONS TO END-OF-CHAPTER PROBLEMS

Chapter 7 SOLUTIONS TO END-OF-CHAPTER PROBLEMS 7-1 0 1 2 3 4 5 10% PV 10,000 FV 5? FV 5 $10,000(1.10) 5 $10,000(FVIF 10%, 5 ) $10,000(1.6105) $16,105. Alternatively, with a financial calculator enter the

Chapter 7 SOLUTIONS TO END-OF-CHAPTER PROBLEMS 7-1 0 1 2 3 4 5 10% PV 10,000 FV 5? FV 5 $10,000(1.10) 5 $10,000(FVIF 10%, 5 ) $10,000(1.6105) $16,105. Alternatively, with a financial calculator enter the

You just paid $350,000 for a policy that will pay you and your heirs $12,000 a year forever. What rate of return are you earning on this policy?

1 You estimate that you will have $24,500 in student loans by the time you graduate. The interest rate is 6.5%. If you want to have this debt paid in full within five years, how much must you pay each

1 You estimate that you will have $24,500 in student loans by the time you graduate. The interest rate is 6.5%. If you want to have this debt paid in full within five years, how much must you pay each

Important Financial Concepts

Part 2 Important Financial Concepts Chapter 4 Time Value of Money Chapter 5 Risk and Return Chapter 6 Interest Rates and Bond Valuation Chapter 7 Stock Valuation 130 LG1 LG2 LG3 LG4 LG5 LG6 Chapter 4 Time

Part 2 Important Financial Concepts Chapter 4 Time Value of Money Chapter 5 Risk and Return Chapter 6 Interest Rates and Bond Valuation Chapter 7 Stock Valuation 130 LG1 LG2 LG3 LG4 LG5 LG6 Chapter 4 Time

CHAPTER 6 DISCOUNTED CASH FLOW VALUATION

CHAPTER 6 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. The four pieces are the present value (PV), the periodic cash flow (C), the discount rate (r), and

CHAPTER 6 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. The four pieces are the present value (PV), the periodic cash flow (C), the discount rate (r), and

CHAPTER 1. Compound Interest

CHAPTER 1 Compound Interest 1. Compound Interest The simplest example of interest is a loan agreement two children might make: I will lend you a dollar, but every day you keep it, you owe me one more penny.

CHAPTER 1 Compound Interest 1. Compound Interest The simplest example of interest is a loan agreement two children might make: I will lend you a dollar, but every day you keep it, you owe me one more penny.

Determinants of Valuation

2 Determinants of Valuation Part Two 4 Time Value of Money 5 Fixed-Income Securities: Characteristics and Valuation 6 Common Shares: Characteristics and Valuation 7 Analysis of Risk and Return The primary

2 Determinants of Valuation Part Two 4 Time Value of Money 5 Fixed-Income Securities: Characteristics and Valuation 6 Common Shares: Characteristics and Valuation 7 Analysis of Risk and Return The primary

A financial statement captures a person s overall wealth at a specific point in time. In this lesson, students will:

PROJECT 3 CASH FLOW AND BALANCE SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

PROJECT 3 CASH FLOW AND BALANCE SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

A financial statement captures a person s overall wealth at a specific point in time. In this lesson, students will:

PROJECT 3 CASH FLOW AND BALANC E SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

PROJECT 3 CASH FLOW AND BALANC E SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

Key Concepts and Skills. Multiple Cash Flows Future Value Example 6.1. Chapter Outline. Multiple Cash Flows Example 2 Continued

6 Calculators Discounted Cash Flow Valuation Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

6 Calculators Discounted Cash Flow Valuation Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

Finding the Payment $20,000 = C[1 1 / 1.0066667 48 ] /.0066667 C = $488.26

![Finding the Payment $20,000 = C[1 1 / 1.0066667 48 ] /.0066667 C = $488.26](/thumbs/17/134163.jpg "Finding the Payment $20,000 = C[1 1 / 1.0066667 48 ] /.0066667 C = $488.26") Quick Quiz: Part 2 You know the payment amount for a loan and you want to know how much was borrowed. Do you compute a present value or a future value? You want to receive $5,000 per month in retirement.

Quick Quiz: Part 2 You know the payment amount for a loan and you want to know how much was borrowed. Do you compute a present value or a future value? You want to receive $5,000 per month in retirement.

Time Value of Money PAPER 3A: COST ACCOUNTING CHAPTER 2 BY: CA KAPILESHWAR BHALLA

Time Value of Money 1 PAPER 3A: COST ACCOUNTING CHAPTER 2 BY: CA KAPILESHWAR BHALLA Learning objectives 2 Understand the Concept of time value of money. Understand the relationship between present and

Time Value of Money 1 PAPER 3A: COST ACCOUNTING CHAPTER 2 BY: CA KAPILESHWAR BHALLA Learning objectives 2 Understand the Concept of time value of money. Understand the relationship between present and

Future Value. Basic TVM Concepts. Chapter 2 Time Value of Money. $500 cash flow. On a time line for 3 years: $100. FV 15%, 10 yr.

Chapter Time Value of Money Future Value Present Value Annuities Effective Annual Rate Uneven Cash Flows Growing Annuities Loan Amortization Summary and Conclusions Basic TVM Concepts Interest rate: abbreviated

Chapter Time Value of Money Future Value Present Value Annuities Effective Annual Rate Uneven Cash Flows Growing Annuities Loan Amortization Summary and Conclusions Basic TVM Concepts Interest rate: abbreviated

International Financial Strategies Time Value of Money

International Financial Strategies 1 Future Value and Compounding Future value = cash value of the investment at some point in the future Investing for single period: FV. Future Value PV. Present Value

International Financial Strategies 1 Future Value and Compounding Future value = cash value of the investment at some point in the future Investing for single period: FV. Future Value PV. Present Value

CHAPTER 8 INTEREST RATES AND BOND VALUATION

CHAPTER 8 INTEREST RATES AND BOND VALUATION Solutions to Questions and Problems 1. The price of a pure discount (zero coupon) bond is the present value of the par value. Remember, even though there are

CHAPTER 8 INTEREST RATES AND BOND VALUATION Solutions to Questions and Problems 1. The price of a pure discount (zero coupon) bond is the present value of the par value. Remember, even though there are

Mathematics. Rosella Castellano. Rome, University of Tor Vergata

and Loans Mathematics Rome, University of Tor Vergata and Loans Future Value for Simple Interest Present Value for Simple Interest You deposit E. 1,000, called the principal or present value, into a savings

and Loans Mathematics Rome, University of Tor Vergata and Loans Future Value for Simple Interest Present Value for Simple Interest You deposit E. 1,000, called the principal or present value, into a savings

Time Value of Money. 15.511 Corporate Accounting Summer 2004. Professor S. P. Kothari Sloan School of Management Massachusetts Institute of Technology

Time Value of Money 15.511 Corporate Accounting Summer 2004 Professor S. P. Kothari Sloan School of Management Massachusetts Institute of Technology July 2, 2004 1 LIABILITIES: Current Liabilities Obligations

Time Value of Money 15.511 Corporate Accounting Summer 2004 Professor S. P. Kothari Sloan School of Management Massachusetts Institute of Technology July 2, 2004 1 LIABILITIES: Current Liabilities Obligations

CHAPTER 7 MAKING CAPITAL INVESTMENT DECISIONS

CHAPTER 7 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

CHAPTER 7 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

FinQuiz Notes 2 0 1 4

Reading 5 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Reading 5 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Assist. Financial Calculators. Technology Solutions. About Our Financial Calculators. Benefits of Financial Calculators. Getting Answers.

Assist. Financial s Technology Solutions. About Our Financial s. Helping members with their financial planning should be a key function of every credit union s website. At Technology Solutions, we provide

Assist. Financial s Technology Solutions. About Our Financial s. Helping members with their financial planning should be a key function of every credit union s website. At Technology Solutions, we provide

Annuities and Sinking Funds

Annuities and Sinking Funds Sinking Fund A sinking fund is an account earning compound interest into which you make periodic deposits. Suppose that the account has an annual interest rate of compounded

Annuities and Sinking Funds Sinking Fund A sinking fund is an account earning compound interest into which you make periodic deposits. Suppose that the account has an annual interest rate of compounded

( ) ( )( ) ( ) 2 ( ) 3. n n = 100 000 1+ 0.10 = 100 000 1.331 = 133100

( )( ) ( ) 2 ( ) 3. n n = 100 000 1+ 0.10 = 100 000 1.331 = 133100") Mariusz Próchniak Chair of Economics II Warsaw School of Economics CAPITAL BUDGETING Managerial Economics 1 2 1 Future value (FV) r annual interest rate B the amount of money held today Interest is compounded

Mariusz Próchniak Chair of Economics II Warsaw School of Economics CAPITAL BUDGETING Managerial Economics 1 2 1 Future value (FV) r annual interest rate B the amount of money held today Interest is compounded

INSTRUCTIONS TO ASSIST IN COMPLETING ATTACHMENT B: PERSONAL FINANCIAL STATEMENT WORKSHEET

INSTRUCTIONS TO ASSIST IN COMPLETING ATTACHMENT B: PERSONAL FINANCIAL STATEMENT WORKSHEET This instruction sheet is intended to provide guidance on how to complete the Attachment B: Personal Financial

INSTRUCTIONS TO ASSIST IN COMPLETING ATTACHMENT B: PERSONAL FINANCIAL STATEMENT WORKSHEET This instruction sheet is intended to provide guidance on how to complete the Attachment B: Personal Financial

What three main functions do they have? Reducing transaction costs, reducing financial risk, providing liquidity

Unit 4 Test Review KEY Savings, Investment and the Financial System 1. What is a financial intermediary? Explain how each of the following fulfills that role: Financial Intermediary: Transforms funds into

Unit 4 Test Review KEY Savings, Investment and the Financial System 1. What is a financial intermediary? Explain how each of the following fulfills that role: Financial Intermediary: Transforms funds into

Accounts payable Money which you owe to an individual or business for goods or services that have been received but not yet paid for.

A Account A record of a business transaction. A contract arrangement, written or unwritten, to purchase and take delivery with payment to be made later as arranged. Accounts payable Money which you owe

A Account A record of a business transaction. A contract arrangement, written or unwritten, to purchase and take delivery with payment to be made later as arranged. Accounts payable Money which you owe

University of Rio Grande Fall 2010

University of Rio Grande Fall 2010 Financial Management (Fin 20403) Practice Questions for Midterm 1 Answers the questions. (Or Identify the letter of the choice that best completes the statement if there

University of Rio Grande Fall 2010 Financial Management (Fin 20403) Practice Questions for Midterm 1 Answers the questions. (Or Identify the letter of the choice that best completes the statement if there

Compound Interest Formula

Mathematics of Finance Interest is the rental fee charged by a lender to a business or individual for the use of money. charged is determined by Principle, rate and time Interest Formula I = Prt $100 At

Mathematics of Finance Interest is the rental fee charged by a lender to a business or individual for the use of money. charged is determined by Principle, rate and time Interest Formula I = Prt $100 At

TT03 Financial Calculator Tutorial And Key Time Value of Money Formulas November 6, 2007

TT03 Financial Calculator Tutorial And Key Time Value of Money Formulas November 6, 2007 The purpose of this tutorial is to help students who use the HP 17BII+, and HP10bll+ calculators understand how

TT03 Financial Calculator Tutorial And Key Time Value of Money Formulas November 6, 2007 The purpose of this tutorial is to help students who use the HP 17BII+, and HP10bll+ calculators understand how

Financial Management

Just Published! 206 Financial Management Principles & Practice 7e By Timothy Gallagher Colorado State University Changes to the new Seventh Edition: Updating of all time sensitive material and some new

Just Published! 206 Financial Management Principles & Practice 7e By Timothy Gallagher Colorado State University Changes to the new Seventh Edition: Updating of all time sensitive material and some new

REVIEW MATERIALS FOR REAL ESTATE ANALYSIS

REVIEW MATERIALS FOR REAL ESTATE ANALYSIS 1997, Roy T. Black REAE 5311, Fall 2005 University of Texas at Arlington J. Andrew Hansz, Ph.D., CFA CONTENTS ITEM ANNUAL COMPOUND INTEREST TABLES AT 10% MATERIALS

REVIEW MATERIALS FOR REAL ESTATE ANALYSIS 1997, Roy T. Black REAE 5311, Fall 2005 University of Texas at Arlington J. Andrew Hansz, Ph.D., CFA CONTENTS ITEM ANNUAL COMPOUND INTEREST TABLES AT 10% MATERIALS

Composition of Farm Household Income and Wealth

Composition of Farm Household Income and Wealth Today it is rare for any household to receive all of its from a single source. Even when only one household member is employed, it is possible to earn from

Composition of Farm Household Income and Wealth Today it is rare for any household to receive all of its from a single source. Even when only one household member is employed, it is possible to earn from

To understand and apply the concept of present value analysis in management decision making within the framework of the regulatory process.

Present Value Analysis Effective management decision making means making the best possible choices from the available investment alternatives consistent with the amount of funds available for reinvestment.

Present Value Analysis Effective management decision making means making the best possible choices from the available investment alternatives consistent with the amount of funds available for reinvestment.

Section 8.1. I. Percent per hundred

1 Section 8.1 I. Percent per hundred a. Fractions to Percents: 1. Write the fraction as an improper fraction 2. Divide the numerator by the denominator 3. Multiply by 100 (Move the decimal two times Right)

1 Section 8.1 I. Percent per hundred a. Fractions to Percents: 1. Write the fraction as an improper fraction 2. Divide the numerator by the denominator 3. Multiply by 100 (Move the decimal two times Right)

18. Interest on savings is calculated by multiplying the money amount times the opportunity cost times the annual interest rate. True False 19.

1 Student: 1. Financial planning has specific techniques that will be effective for every individual and household. 2. Personal financial planning is the process of managing one's money to achieve personal

1 Student: 1. Financial planning has specific techniques that will be effective for every individual and household. 2. Personal financial planning is the process of managing one's money to achieve personal

CHAPTER 5 HOW TO VALUE STOCKS AND BONDS

CHAPTER 5 HOW TO VALUE STOCKS AND BONDS Answers to Concepts Review and Critical Thinking Questions 1. Bond issuers look at outstanding bonds of similar maturity and risk. The yields on such bonds are used

CHAPTER 5 HOW TO VALUE STOCKS AND BONDS Answers to Concepts Review and Critical Thinking Questions 1. Bond issuers look at outstanding bonds of similar maturity and risk. The yields on such bonds are used

Managing Home Equity to Build Wealth By Ray Meadows CPA, CFA, MBA

Managing Home Equity to Build Wealth By Ray Meadows CPA, CFA, MBA About the Author Ray Meadows is the president of Berkeley Investment Advisors, a real estate brokerage and investment advisory firm. He

Managing Home Equity to Build Wealth By Ray Meadows CPA, CFA, MBA About the Author Ray Meadows is the president of Berkeley Investment Advisors, a real estate brokerage and investment advisory firm. He

Numbers 101: Cost and Value Over Time

The Anderson School at UCLA POL 2000-09 Numbers 101: Cost and Value Over Time Copyright 2000 by Richard P. Rumelt. We use the tool called discounting to compare money amounts received or paid at different

The Anderson School at UCLA POL 2000-09 Numbers 101: Cost and Value Over Time Copyright 2000 by Richard P. Rumelt. We use the tool called discounting to compare money amounts received or paid at different

Oklahoma State University Spears School of Business. Time Value of Money

Oklahoma State University Spears School of Business Time Value of Money Slide 2 Time Value of Money Which would you rather receive as a sign-in bonus for your new job? 1. $15,000 cash upon signing the

Oklahoma State University Spears School of Business Time Value of Money Slide 2 Time Value of Money Which would you rather receive as a sign-in bonus for your new job? 1. $15,000 cash upon signing the

DISCOUNTED CASH FLOW VALUATION and MULTIPLE CASH FLOWS

Chapter 5 DISCOUNTED CASH FLOW VALUATION and MULTIPLE CASH FLOWS The basic PV and FV techniques can be extended to handle any number of cash flows. PV with multiple cash flows: Suppose you need $500 one

Chapter 5 DISCOUNTED CASH FLOW VALUATION and MULTIPLE CASH FLOWS The basic PV and FV techniques can be extended to handle any number of cash flows. PV with multiple cash flows: Suppose you need $500 one

Time Value of Money. Background

Time Value of Money (Text reference: Chapter 4) Topics Background One period case - single cash flow Multi-period case - single cash flow Multi-period case - compounding periods Multi-period case - multiple

Time Value of Money (Text reference: Chapter 4) Topics Background One period case - single cash flow Multi-period case - single cash flow Multi-period case - compounding periods Multi-period case - multiple

Guide to Financial Statements Study Guide

Guide to Financial Statements Study Guide Overview (Topic 1) Three major financial statements: The Income Statement The Balance Sheet The Cash Flow Statement Objectives: Explain the underlying equation

Guide to Financial Statements Study Guide Overview (Topic 1) Three major financial statements: The Income Statement The Balance Sheet The Cash Flow Statement Objectives: Explain the underlying equation

CHAPTER 8 INTEREST RATES AND BOND VALUATION

CHAPTER 8 INTEREST RATES AND BOND VALUATION Answers to Concept Questions 1. No. As interest rates fluctuate, the value of a Treasury security will fluctuate. Long-term Treasury securities have substantial

CHAPTER 8 INTEREST RATES AND BOND VALUATION Answers to Concept Questions 1. No. As interest rates fluctuate, the value of a Treasury security will fluctuate. Long-term Treasury securities have substantial

Present Value (PV) Tutorial

Tutorial") EYK 15-1 Present Value (PV) Tutorial The concepts of present value are described and applied in Chapter 15. This supplement provides added explanations, illustrations, calculations, present value tables,

EYK 15-1 Present Value (PV) Tutorial The concepts of present value are described and applied in Chapter 15. This supplement provides added explanations, illustrations, calculations, present value tables,

National Standards for Personal Finance Education - Jump $tart Correlation to Virtual Business - Personal Finance

National s for Personal Finance Education - Jump $tart Correlation to Virtual Business - Personal Finance I. Financial Responsibility & Decision Making II. Income & Careers III. Planning & Money Management

National s for Personal Finance Education - Jump $tart Correlation to Virtual Business - Personal Finance I. Financial Responsibility & Decision Making II. Income & Careers III. Planning & Money Management

FinQuiz Notes 2 0 1 5

Reading 5 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Reading 5 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Finance 3130 Sample Exam 1B Spring 2012

Finance 3130 Sample Exam 1B Spring 2012 True/False Indicate whether the statement is true or false. 1. A firm s income statement provides information as of a point in time, and represents how management

Finance 3130 Sample Exam 1B Spring 2012 True/False Indicate whether the statement is true or false. 1. A firm s income statement provides information as of a point in time, and represents how management

Chapter Focus. Why Study Family finance? To Achieve Financial Success. Chapter Outline. Understanding Important Economic Trends. Your Goals in Life

Chapter Focus Chapter 1: Financial Planning-- Why It s Important This chapter puts financial planning in perspective in relation to your goals in life. The key to financial success is to know your goals

Chapter Focus Chapter 1: Financial Planning-- Why It s Important This chapter puts financial planning in perspective in relation to your goals in life. The key to financial success is to know your goals

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. Assuming positive cash flows and interest rates, the future value increases and the present value

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. Assuming positive cash flows and interest rates, the future value increases and the present value

NPV calculation. Academic Resource Center

NPV calculation Academic Resource Center 1 NPV calculation PV calculation a. Constant Annuity b. Growth Annuity c. Constant Perpetuity d. Growth Perpetuity NPV calculation a. Cash flow happens at year

NPV calculation Academic Resource Center 1 NPV calculation PV calculation a. Constant Annuity b. Growth Annuity c. Constant Perpetuity d. Growth Perpetuity NPV calculation a. Cash flow happens at year

How To Read The Book \"Financial Planning\"

Time Value of Money Reading 5 IFT Notes for the 2015 Level 1 CFA exam Contents 1. Introduction... 2 2. Interest Rates: Interpretation... 2 3. The Future Value of a Single Cash Flow... 4 4. The Future Value

Time Value of Money Reading 5 IFT Notes for the 2015 Level 1 CFA exam Contents 1. Introduction... 2 2. Interest Rates: Interpretation... 2 3. The Future Value of a Single Cash Flow... 4 4. The Future Value

Module 5: Interest concepts of future and present value

file:///f /Courses/2010-11/CGA/FA2/06course/m05intro.htm Module 5: Interest concepts of future and present value Overview In this module, you learn about the fundamental concepts of interest and present

file:///f /Courses/2010-11/CGA/FA2/06course/m05intro.htm Module 5: Interest concepts of future and present value Overview In this module, you learn about the fundamental concepts of interest and present