News Trading and Speed

|

|

|

- Jonah Richardson

- 10 years ago

- Views:

Transcription

1 News Trading and Speed Thierry Foucault, Johan Hombert, and Ioanid Rosu (HEC) High Frequency Trading Conference

High Frequency")

2 Plan Plan 1. Introduction - Research questions 2. Model 3. Is news trading different? 4. Implications 5. Conclusions

3 News Trading and Speed Introduction

4 Introduction News trading Market effi ciency: securities prices reflect all publicly available information instantaneously. Implication: Trading on news (corporate announcements, macro announcements, newswire, market data etc.) cannot be profitable. Yet, it is profitable Empirical evidence: Tetlock, Saar-Tsechansky, and Mackassy (2008), Engelberg (2008), Tetlock (2010), Engleberg, Reed and Ringgenberg (2011). 2. High-Frequency Trading on News: some investors make massive technological investments to trade on "news" (orders, quotes, etc.).

, Engelberg (2008), Tetlock (2010), Engleberg, Reed and Ringgenberg")

5 Introduction High Frequency News Trading (HFTNs) Math-loving traders are using powerful computers to speed-read news reports, editorials, company Web sites, blog posts and even Twitter messages and then letting the machines decidewhat it all means for the markets.["computers that trade on news"-new-york-times, December 22,2010.

6 Introduction High Frequency News Trading (HFTNs) Authorities are exploring potential holes in the system, including new algorithms referred to as news aggregation that search the internet, news sites and social media for selected keywords, and fire off orders in milliseconds. The trades are so quick, often before the information is widely disseminated, that authorities are debating whether they violate insider trading rules, [...].["FBI joins SEC in computer trading probe"-financial Times, 2013.]

7 Introduction Why is news trading profitable? 1. Greater processing capacity of vast amount of information: #messages (orders) per second in U.S. equity markets 100,000 [Hendershott (2011)]. Only computers can process such vast amount of data to generate trading signals OR/AND 2. Faster access to information (co-location, real-time data feed etc.) Models of informed trading usually focus on the first type of advantage. Does this matter? What is the optimal trading strategy of an informed investor who is both (i) a fast and (ii) skilled information processor?

Models of informed trading usually focus on the first type of advantage.")

8 Introduction Why are these questions important? Disentangling the relative contributions of speed and information processing capacity is important to: 1. Identify the exact sources (speed vs accuracy) of news traders profitability. Could be important for regulation (unfair access to information vs. skilled processing of information). 2. Make predictions about trades of high frequency news traders and relate these trades to returns. 2.1 Many empirical papers relate returns to order imbalances from high frequency traders (e.g., Kirilenko et al.(2011), Brogaard, Hendershott, Riordan (2012), Hirschey (2011), etc.). 2.2 How to interpret these findings? Need of structural foundations 3. Understand the process by which news get impounded into prices (trades or quote updates?)

, Brogaard, Hendershott, Riordan (2012), Hirschey (2011), etc.). 2.2 How to interpret these findings? Need of structural foundations 3.")

9 Introduction Our approach We use the dynamic version of Kyle (1985) with news arrivals. The informed investor in our model has two advantages: 1. A greater ability to process information: he extracts more precise signals than dealers from news. 2. A faster reaction than dealers to news. To isolate the effect of speed: we compare the equilibrium with and without a speed advantage for the informed investor. Main finding: The equilibrium trading strategy of the informed investor is significantly different when he has a speed advantage and when he has not.

.")

10 Introduction Equilibrium holdings and trades Left panel: informed investor s holdings of the risky asset, x t (red in the benchmark model; blue in the fast model). Right Panel: informed investor s trade (dx t )

.")

11 Introduction Literature Continuous time Kyle (1985) with news for the informed investor: 1. Back and Pedersen (1998): No news for dealers = No news trading (a special case of our model). 2. Chau and Vayanos (2008): News for dealers but no speed advantage for the informed investor = No news trading. 3. Martinez and Rosu (2012): No news for dealers but ambiguity aversion for the informed investor = News trading but for a different reason than in our paper.

: No news for dealers but ambiguity aversion for the informed investor = News trading but")

12 Introduction Literature Theoretical literature on HFTs: Biais, Foucault, and Moinas (2011), Pagnotta and Phillipon (2011), Jovanovic and Menkveld (2011), Cvitanic and Kirilenko (2011), Cartea and Penalva (2012), Hoffman (2012). 1. Our contribution: optimal dynamic strategy for an investor who has both a fast access to news and a greater information processing ability. Empirical literature on HFTs, especially Brogaard, Hendershott, and Riordan (2012) Public information and volume (Kim and Verrecchia (1992, 1994)

13 Introduction Plan 1. Introduction - Research questions 2. Model 3. Implications 4. Conclusions

14 Model Model Kyle (1985) with: 1. Public information: A flow of news 2. Speed: The possibility for the informed investor to observe news before dealers. Fundamental value of the asset at date T, v T = v 0 + t=t t=1 v t where v 0 N(0, Σ 0 ) and v t N(0, σ v t) v t = E (v T v s s=t s=1 ) (Brownian motion) and σ v =Fundamental Volatility.

and v t N(0, σ v t) v t = E (v T v s s=t s=1 ) (Brownian motion) and σ v")

15 Model Participants One risk neutral informed trader:he knows v 0 and NEWS: z i t = v t + e t where de t N(0, σ e t). 1. Position at date t : x t. 2. Strategy: market order for x t shares traded at date t. Noise traders: 1. Exogenous trade at date t: u t N(0, σ u t) 2. u t contains no information on the asset value. Competitive Market-makers: 1. Dealers NEWS: z t = v t + e t, where e t N(0, σ e t) and e t e t. 2. At date t, they absorb the net order imbalance y t = x t + u t at a price equal to the expected payoff of the asset conditional on their information.

and e t e t. 2.")

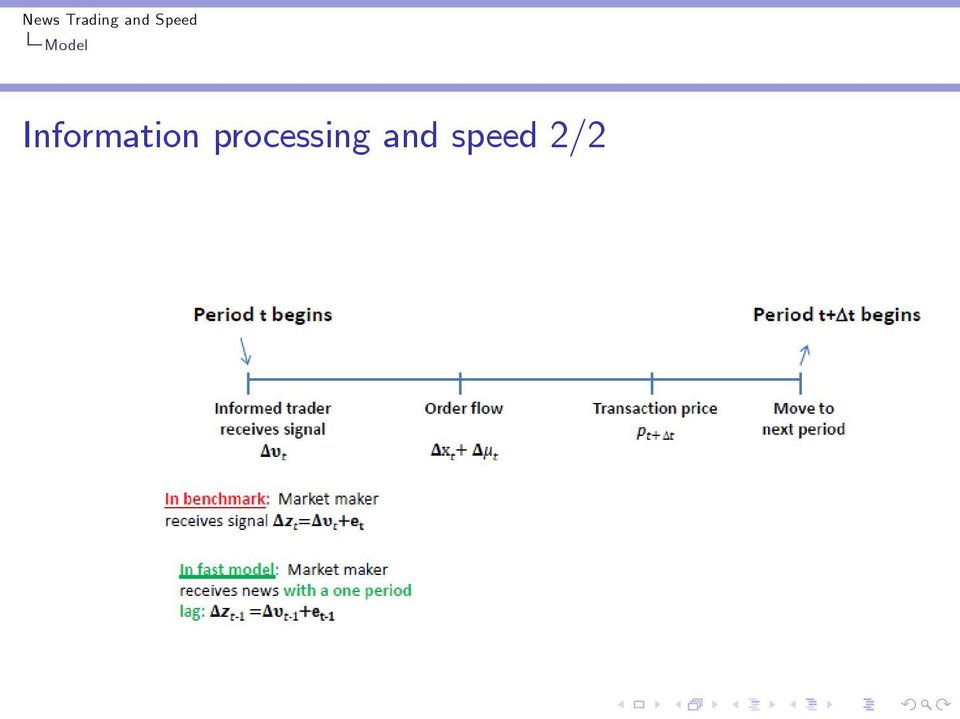

16 Model Information processing and speed 1/2 Information processing: The informed investor has a greater information processing capacity than dealers: σ e σ e. To simplify, σ e = 0 = z i t = v t. Speed of access to information: 1. Fast model:market-makers observe news with a one period delay relative to the informed investor. 2. Benchmark case:market-makers observe news without delay: the informed investor only has only an information processing advantage.

17 Model Information processing and speed 2/2

18 Model Interpretation and Particular Cases 1/σ e = a measure of news informativeness for dealers. σ e = 0. The informed investor and the dealer observe the same news. σ e : market-makers never receive news.

19 Model News Trading: Definition. State variables for the informed investor at date t: 1. The dealer s forecast of the asset value before trading ("the midquote"): q t 2. The informed investor s forecast of the asset value after receiving news: v t 3. News: v t = v t v t 1 DEFINITION: There is news trading if the investor s optimal strategy depends on news ( v t ), and not just v t and q t.

20 Model Equilibrium Definition Same as in Kyle (1985): At any point in time: 1. Prices are equal to dealers forecast of the asset liquidation value given their information and the optimal trading policy of the informed investor ( x ). 2. The trading policy of the informed investor is optimal at any point time given dealers pricing policy. To obtain a closed form solution, we focus on the continuous time version of the model: NOT KEY. Is it important that the problem is dynamic? YES: no news trading in the "static" (one period) model.

21 Model Equilibrium There is a linear equilibrium in which: 1. The informed investor s optimal trade at date t is: dx t = β t (v t q t )dt } {{ } Pricing error + γ dv t } {{ } News Trading where q t is market-maker s expectation of the asset payoff before observing the order flow at date t. 2. Transaction prices are linear in the order flow (dy t ).The sensitivity of prices to the order flow, λ, is a measure of market illiquidity. (as in Kyle (1985)): p t+dt = q t + λ dy t We characterize in closed form β t, γ and λ both when the informed investor has a speed advantage and when he has not.

22 Model Equilibrium trading strategy for the informed investor 1/2 The trading strategy has two components: 1. Forecast or pricing error component (β t (v t q t )dt):the informed investor buys (sells) the asset if the dealer undervalues (overvalues) it. Standard in Kyle s type of model. 2. News Trading component (γdv t ):The informed investor trades on news because dealers quote updates are correlated with news. If the informed investor observes good news, he anticipates an increase in dealers quotes Buy more before buying becomes more expensive.

23 Model Equilibrium trading strategy for the informed investor 2/2 Result 1: Responsiveness of the investor s holdings to news (γ). 1. No news trading without a speed advantage: γ > 0 iff the informed investor has a speed advantage An information processing advantage (σ e > 0) is not suffi cient to generate aggressive trading on news. 2. More aggressive trading on informative news for dealers: γ is positively related to 1/σ e. 3. No news trading if dealers do not receive public information: γ goes to zero if σ e. Result 2: Responsiveness of the investor s holdings to mispricing (β t ). 1. It is lower when the informed investor has a speed advantage ("substitution effect").

24 Model Liquidity Illiquidity = λ = Price impact of trades. The ability of the informed investor to exploit news before market-makers is an additional source of adverse selection for market-makers (they are more likely to sell the asset when good news arrive and buy it when bad news arrive). Hence, liquidity is smaller with news trading than without. Not surprising.

25 Model Plan 1. Introduction - Research questions 2. Model 3. Is news trading different? 4. Empirical Implications 5. Conclusions

26 Is news trading different? News Traders Footprints High participation rate: The fraction of total trading volume due to the informed investor is an order of magnitude higher when he has a speed advantage (consistent with the large fraction of trading volume due to high frequency traders). Anticipatory trading: The informed informed investor trades are positively correlated with very short term returns. "Possibly due to their speed advantage or superior ability to predict price changes, HFTs are able to buy right as the prices are about to increase." (Kirilenko et al.(2012)) None of these properties are obtained if the informed investor has no speed advantage. Why?

27 Is news trading different? Informed Investor s Participation Rate (circle= fast model; crosses=benchmark) Informed investor s participation rate = Fraction of trading volume due to the informed investor at various sampling frequency. Intuition: Var( x t )=γ 2 σ 2 v dt and Var( u t )=σ 2 udt: same order of magnitude.

28 Is news trading different? Anticipatory Trading The covariance between the informed investor s trade rate at date t and the subsequent return over various horizons [Blue line: Fast model. Green line: Benchmark]

29 Is news trading different? News Trading and Price discovery 1/2 Let s t = p t v t = Pricing error at date t. Measure of informational effi ciency: Average pricing error at date t: We have: Σ t = E (s 2 t Dealers Information Set at date t). dσ t = 2Cov(dp t, s t ) 2Cov(dp t, dv t ) + (2σ 2 v + Σ 0 )dt } {{ } } {{ } <0 >0 Hence, informational effi ciency is higher when price changes are: 1. more positively correlated with news(cov(dp t, dv t ) higher). 2. more negatively correlated with pricing errors (i.e., correct pricing errors)(cov(dp t, s t ) smaller)

30 Is news trading different? News Trading and Price discovery 2/2 Two effects of granting a speed advantage to the informed investor: Price changes are 1. more positively correlated with news(cov(dp t, dv t ) is higher in the fast model). 2. but less negatively correlated with pricing errors due to the substitution effect(cov(dp t, v t p t ) is smaller in the fast model). Net effect on informational effi ciency/price discovery ( t ): zero at any date.

31 Is news trading different? News Trading and the Sources of Volatility Prices changes because dealers receive information. Two sources of information: 1. Trades ( y t ) 2. Public signals ( z t ) Volatility of returns can be decomposed in two components (q t =dealer s quote after receiving public information): Var( p t ) = Var(p t+ t q t ) + Var(q t p t ), } {{ } } {{ } Trades News The first component is higher in the fast model and the second smaller; Net effect: zero: Volatility is identical whether or not the informed investor has a speed advantage. However, the contribution of news (trades) to volatility is smaller (higher) in the fast model.

32 Is news trading different? Plan 1. Introduction - Research questions 2. Model 3. Is news trading different? 4. Empirical Implications 5. Conclusions

33 Is news trading different? News Informativeness, Volume and Liquidity An increase in news informativeness for dealers results in: 1. A higher participation rate for the informed investor 2. A higher trading volume 3. A more liquid market (λ declines). = Risk of spurious positive correlation between measures of news traders activity and liquidity [liquidity is lower (λ higher) when the informed investor has a speed advantage.]

34 Is news trading different? How does trading on news affect returns? Brogaard, Hendershott and Riordan (2012) decompose transaction prices into a permanent and a transitory component ("pricing error"): p t }{{} Transaction prices = m t }{{} Effi cient price + s }{{} t. Pricing error and relate (a) innovations in m t to innovations in order imbalances from high frequency traders and (b) pricing errors to order imbalances from high frequency traders.

35 Is news trading different? How does trading on news affect returns? If we set m t = v t (and assume β constant), we obtain (in the discrete time version): m t = κ x t s t+ t = φs t + ψ x t + η t The model predicts: κ > 0, φ < 1, and ψ < 0. Consistent with Brogaard, Hendershott and Riordan (2012) s findings who estimate κ = 4.13bps, φ = 0.47bps and ψ = 1.97bps (/$10, 000).

36 Is news trading different? Interpretation The model implies that: 1. κ = 1 γ Estimate of κ can be viewed as a measure of high-frequency traders responsiveness to news. 2. Slow trading on the forecast error = 0 < φ < ψ < 0, even though, strictly speaking news trading is not trading on the pricing error: Suppose s t = 0 (p t = v t ). Positive news ( v t > 0)= Informed investor buys x t > 0 but the price does not fully adjust because order flow is noisy = s t+1 = p t+1 v t+1 < 0.

37 Is news trading different? Do we really need a dynamic model? Suppose only one period ( t = 1). At date 0: 1. The informed investor knows v 0 and observes news: v = v 1 v 0 AND, 2. The dealer observes news: z 0 = v + e 0 before trading in the benchmark model and after trading in the Fast model. Benchmark: No news trading...informed investor s optimal trading strategy: x B 0 = β B (v 0 + v q 0 ) just as in Kyle (85) = Same weights on v 0 and news. Fast model: No news trading again...: x F 0 = β F (v 0 + v q 0 ); Only difference: β F > β B. = News trading really requires multiple trading opportunities.

38 Is news trading different? Conclusion Speed of access to information has effects distinct from greater processing capacity of information. Slowing down high frequency traders may have no effect on volatility or price discovery (they will simply trade more aggressively on their long-run forecast of the asset value) but it will reduce their profits. Dynamic models of high frequency trading help to interpret relationships between HFTs flows and returns.

News Trading and Speed

News Trading and Speed Thierry Foucault, Johan Hombert, Ioanid Roşu (HEC Paris) 6th Financial Risks International Forum March 25-26, 2013, Paris Johan Hombert (HEC Paris) News Trading and Speed 6th Financial

News Trading and Speed Thierry Foucault, Johan Hombert, Ioanid Roşu (HEC Paris) 6th Financial Risks International Forum March 25-26, 2013, Paris Johan Hombert (HEC Paris) News Trading and Speed 6th Financial

News Trading and Speed

News Trading and Speed Thierry Foucault Johan Hombert Ioanid Roşu September 5, 01 Abstract Informed trading can take two forms: (i) trading on more accurate information or (ii) trading on public information

News Trading and Speed Thierry Foucault Johan Hombert Ioanid Roşu September 5, 01 Abstract Informed trading can take two forms: (i) trading on more accurate information or (ii) trading on public information

News Trading and Speed

News Trading and Speed THIERRY FOUCAULT, JOHAN HOMBERT, and IOANID ROŞU June 30, 2015 Abstract We compare the optimal trading strategy of an informed speculator when he can trade ahead of incoming news

News Trading and Speed THIERRY FOUCAULT, JOHAN HOMBERT, and IOANID ROŞU June 30, 2015 Abstract We compare the optimal trading strategy of an informed speculator when he can trade ahead of incoming news

Toxic Arbitrage. Abstract

Toxic Arbitrage Thierry Foucault Roman Kozhan Wing Wah Tham Abstract Arbitrage opportunities arise when new information affects the price of one security because dealers in other related securities are

Toxic Arbitrage Thierry Foucault Roman Kozhan Wing Wah Tham Abstract Arbitrage opportunities arise when new information affects the price of one security because dealers in other related securities are

Equilibrium High Frequency Trading

Equilibrium High Frequency Trading B. Biais, T. Foucault, S. Moinas Fifth Annual Conference of the Paul Woolley Centre for the Study of Capital Market Dysfunctionality London, June 2012 What s High Frequency

Equilibrium High Frequency Trading B. Biais, T. Foucault, S. Moinas Fifth Annual Conference of the Paul Woolley Centre for the Study of Capital Market Dysfunctionality London, June 2012 What s High Frequency

Algorithmic trading Equilibrium, efficiency & stability

Algorithmic trading Equilibrium, efficiency & stability Presentation prepared for the conference Market Microstructure: Confronting many viewpoints Institut Louis Bachelier Décembre 2010 Bruno Biais Toulouse

Algorithmic trading Equilibrium, efficiency & stability Presentation prepared for the conference Market Microstructure: Confronting many viewpoints Institut Louis Bachelier Décembre 2010 Bruno Biais Toulouse

Fast Aggressive Trading

Fast Aggressive Trading Richard Payne Professor of Finance Faculty of Finance, Cass Business School Global Association of Risk Professionals May 2015 The views expressed in the following material are the

Fast Aggressive Trading Richard Payne Professor of Finance Faculty of Finance, Cass Business School Global Association of Risk Professionals May 2015 The views expressed in the following material are the

High frequency trading

High frequency trading Bruno Biais (Toulouse School of Economics) Presentation prepared for the European Institute of Financial Regulation Paris, Sept 2011 Outline 1) Description 2) Motivation for HFT

High frequency trading Bruno Biais (Toulouse School of Economics) Presentation prepared for the European Institute of Financial Regulation Paris, Sept 2011 Outline 1) Description 2) Motivation for HFT

HFT and Market Quality

HFT and Market Quality BRUNO BIAIS Directeur de recherche Toulouse School of Economics (CRM/CNRS - Chaire FBF/ IDEI) THIERRY FOUCAULT* Professor of Finance HEC, Paris I. Introduction The rise of high-frequency

HFT and Market Quality BRUNO BIAIS Directeur de recherche Toulouse School of Economics (CRM/CNRS - Chaire FBF/ IDEI) THIERRY FOUCAULT* Professor of Finance HEC, Paris I. Introduction The rise of high-frequency

High-frequency trading and execution costs

High-frequency trading and execution costs Amy Kwan Richard Philip* Current version: January 13 2015 Abstract We examine whether high-frequency traders (HFT) increase the transaction costs of slower institutional

High-frequency trading and execution costs Amy Kwan Richard Philip* Current version: January 13 2015 Abstract We examine whether high-frequency traders (HFT) increase the transaction costs of slower institutional

How To Understand The Role Of High Frequency Trading

High Frequency Trading and Price Discovery * by Terrence Hendershott (University of California at Berkeley) Ryan Riordan (Karlsruhe Institute of Technology) * We thank Frank Hatheway and Jeff Smith at

High Frequency Trading and Price Discovery * by Terrence Hendershott (University of California at Berkeley) Ryan Riordan (Karlsruhe Institute of Technology) * We thank Frank Hatheway and Jeff Smith at

Financial Markets. Itay Goldstein. Wharton School, University of Pennsylvania

Financial Markets Itay Goldstein Wharton School, University of Pennsylvania 1 Trading and Price Formation This line of the literature analyzes the formation of prices in financial markets in a setting

Financial Markets Itay Goldstein Wharton School, University of Pennsylvania 1 Trading and Price Formation This line of the literature analyzes the formation of prices in financial markets in a setting

Need for Speed: An Empirical Analysis of Hard and Soft Information in a High Frequency World

Need for Speed: An Empirical Analysis of Hard and Soft Information in a High Frequency World S. Sarah Zhang 1 School of Economics and Business Engineering, Karlsruhe Institute of Technology, Germany Abstract

Need for Speed: An Empirical Analysis of Hard and Soft Information in a High Frequency World S. Sarah Zhang 1 School of Economics and Business Engineering, Karlsruhe Institute of Technology, Germany Abstract

Fast Trading and Prop Trading

Fast Trading and Prop Trading B. Biais, F. Declerck, S. Moinas (Toulouse School of Economics) December 11, 2014 Market Microstructure Confronting many viewpoints #3 New market organization, new financial

Fast Trading and Prop Trading B. Biais, F. Declerck, S. Moinas (Toulouse School of Economics) December 11, 2014 Market Microstructure Confronting many viewpoints #3 New market organization, new financial

High-Frequency Trading and Price Discovery

High-Frequency Trading and Price Discovery Jonathan Brogaard University of Washington Terrence Hendershott University of California at Berkeley Ryan Riordan University of Ontario Institute of Technology

High-Frequency Trading and Price Discovery Jonathan Brogaard University of Washington Terrence Hendershott University of California at Berkeley Ryan Riordan University of Ontario Institute of Technology

Goal Market Maker Pricing and Information about Prospective Order Flow

Goal Market Maker Pricing and Information about Prospective Order Flow EIEF October 9 202 Use a risk averse market making model to investigate. [Microstructural determinants of volatility, liquidity and

Goal Market Maker Pricing and Information about Prospective Order Flow EIEF October 9 202 Use a risk averse market making model to investigate. [Microstructural determinants of volatility, liquidity and

Financial Market Microstructure Theory

The Microstructure of Financial Markets, de Jong and Rindi (2009) Financial Market Microstructure Theory Based on de Jong and Rindi, Chapters 2 5 Frank de Jong Tilburg University 1 Determinants of the

The Microstructure of Financial Markets, de Jong and Rindi (2009) Financial Market Microstructure Theory Based on de Jong and Rindi, Chapters 2 5 Frank de Jong Tilburg University 1 Determinants of the

Working Paper SerieS. High Frequency Trading and Price Discovery. NO 1602 / november 2013. Jonathan Brogaard, Terrence Hendershott and Ryan Riordan

Working Paper SerieS NO 1602 / november 2013 High Frequency Trading and Price Discovery Jonathan Brogaard, Terrence Hendershott and Ryan Riordan ecb lamfalussy fellowship Programme In 2013 all ECB publications

Working Paper SerieS NO 1602 / november 2013 High Frequency Trading and Price Discovery Jonathan Brogaard, Terrence Hendershott and Ryan Riordan ecb lamfalussy fellowship Programme In 2013 all ECB publications

Trading Fast and Slow: Colocation and Market Quality*

Trading Fast and Slow: Colocation and Market Quality* Jonathan Brogaard Björn Hagströmer Lars Nordén Ryan Riordan First Draft: August 2013 Current Draft: November 2013 Abstract: Using user-level data from

Trading Fast and Slow: Colocation and Market Quality* Jonathan Brogaard Björn Hagströmer Lars Nordén Ryan Riordan First Draft: August 2013 Current Draft: November 2013 Abstract: Using user-level data from

Do retail traders suffer from high frequency traders?

Do retail traders suffer from high frequency traders? Katya Malinova, Andreas Park, Ryan Riordan November 15, 2013 Millions in Milliseconds Monday, June 03, 2013: a minor clock synchronization issue causes

Do retail traders suffer from high frequency traders? Katya Malinova, Andreas Park, Ryan Riordan November 15, 2013 Millions in Milliseconds Monday, June 03, 2013: a minor clock synchronization issue causes

On the Efficiency of Competitive Stock Markets Where Traders Have Diverse Information

Finance 400 A. Penati - G. Pennacchi Notes on On the Efficiency of Competitive Stock Markets Where Traders Have Diverse Information by Sanford Grossman This model shows how the heterogeneous information

Finance 400 A. Penati - G. Pennacchi Notes on On the Efficiency of Competitive Stock Markets Where Traders Have Diverse Information by Sanford Grossman This model shows how the heterogeneous information

Trading Fast and Slow: Colocation and Market Quality*

Trading Fast and Slow: Colocation and Market Quality* Jonathan Brogaard Björn Hagströmer Lars Nordén Ryan Riordan First Draft: August 2013 Current Draft: December 2013 Abstract: Using user-level data from

Trading Fast and Slow: Colocation and Market Quality* Jonathan Brogaard Björn Hagströmer Lars Nordén Ryan Riordan First Draft: August 2013 Current Draft: December 2013 Abstract: Using user-level data from

Do High-Frequency Traders Anticipate Buying and Selling Pressure?

Do High-Frequency Traders Anticipate Buying and Selling Pressure? Nicholas H. Hirschey London Business School November 2013 Abstract High-frequency traders (HFTs) account for a substantial fraction of

Do High-Frequency Traders Anticipate Buying and Selling Pressure? Nicholas H. Hirschey London Business School November 2013 Abstract High-frequency traders (HFTs) account for a substantial fraction of

Do High Frequency Traders Need to be Regulated? Evidence from Algorithmic Trading on Macro News

Do High Frequency Traders Need to be Regulated? Evidence from Algorithmic Trading on Macro News Tarun Chordia, T. Clifton Green, and Badrinath Kottimukkalur * March 2015 Abstract Stock index ETF and futures

Do High Frequency Traders Need to be Regulated? Evidence from Algorithmic Trading on Macro News Tarun Chordia, T. Clifton Green, and Badrinath Kottimukkalur * March 2015 Abstract Stock index ETF and futures

What do we know about high-frequency trading? Charles M. Jones* Columbia Business School Version 3.4: March 20, 2013 ABSTRACT

What do we know about high-frequency trading? Charles M. Jones* Columbia Business School Version 3.4: March 20, 2013 ABSTRACT This paper reviews recent theoretical and empirical research on high-frequency

What do we know about high-frequency trading? Charles M. Jones* Columbia Business School Version 3.4: March 20, 2013 ABSTRACT This paper reviews recent theoretical and empirical research on high-frequency

Low-Latency Trading and Price Discovery without Trading: Evidence from the Tokyo Stock Exchange Pre-Opening Period

Low-Latency Trading and Price Discovery without Trading: Evidence from the Tokyo Stock Exchange Pre-Opening Period Preliminary and incomplete Mario Bellia, SAFE - Goethe University Loriana Pelizzon, Goethe

Low-Latency Trading and Price Discovery without Trading: Evidence from the Tokyo Stock Exchange Pre-Opening Period Preliminary and incomplete Mario Bellia, SAFE - Goethe University Loriana Pelizzon, Goethe

High-Frequency Trading Competition

High-Frequency Trading Competition Jonathan Brogaard and Corey Garriott* May 2015 Abstract High-frequency trading (HFT) firms have been shown to influence market quality by exploiting a speed advantage.

High-Frequency Trading Competition Jonathan Brogaard and Corey Garriott* May 2015 Abstract High-frequency trading (HFT) firms have been shown to influence market quality by exploiting a speed advantage.

Where is the Value in High Frequency Trading?

Where is the Value in High Frequency Trading? Álvaro Cartea and José Penalva November 5, 00 Abstract We analyze the impact of high frequency trading in financial markets based on a model with three types

Where is the Value in High Frequency Trading? Álvaro Cartea and José Penalva November 5, 00 Abstract We analyze the impact of high frequency trading in financial markets based on a model with three types

Liquidity Cycles and Make/Take Fees in Electronic Markets

Liquidity Cycles and Make/Take Fees in Electronic Markets Thierry Foucault (HEC, Paris) Ohad Kadan (Washington U) Eugene Kandel (Hebrew U) April 2011 Thierry, Ohad, and Eugene () Liquidity Cycles & Make/Take

Liquidity Cycles and Make/Take Fees in Electronic Markets Thierry Foucault (HEC, Paris) Ohad Kadan (Washington U) Eugene Kandel (Hebrew U) April 2011 Thierry, Ohad, and Eugene () Liquidity Cycles & Make/Take

Should Exchanges impose Market Maker obligations? Amber Anand. Kumar Venkataraman. Abstract

Should Exchanges impose Market Maker obligations? Amber Anand Kumar Venkataraman Abstract We study the trades of two important classes of market makers, Designated Market Makers (DMMs) and Endogenous Liquidity

Should Exchanges impose Market Maker obligations? Amber Anand Kumar Venkataraman Abstract We study the trades of two important classes of market makers, Designated Market Makers (DMMs) and Endogenous Liquidity

Execution Costs. Post-trade reporting. December 17, 2008 Robert Almgren / Encyclopedia of Quantitative Finance Execution Costs 1

December 17, 2008 Robert Almgren / Encyclopedia of Quantitative Finance Execution Costs 1 Execution Costs Execution costs are the difference in value between an ideal trade and what was actually done.

December 17, 2008 Robert Almgren / Encyclopedia of Quantitative Finance Execution Costs 1 Execution Costs Execution costs are the difference in value between an ideal trade and what was actually done.

Market Microstructure & Trading Universidade Federal de Santa Catarina Syllabus. Email: [email protected], Web: www.sfu.ca/ rgencay

Market Microstructure & Trading Universidade Federal de Santa Catarina Syllabus Dr. Ramo Gençay, Objectives: Email: [email protected], Web: www.sfu.ca/ rgencay This is a course on financial instruments, financial

Market Microstructure & Trading Universidade Federal de Santa Catarina Syllabus Dr. Ramo Gençay, Objectives: Email: [email protected], Web: www.sfu.ca/ rgencay This is a course on financial instruments, financial

Asset Management Contracts and Equilibrium Prices

Asset Management Contracts and Equilibrium Prices ANDREA M. BUFFA DIMITRI VAYANOS PAUL WOOLLEY Boston University London School of Economics London School of Economics September, 2013 Abstract We study

Asset Management Contracts and Equilibrium Prices ANDREA M. BUFFA DIMITRI VAYANOS PAUL WOOLLEY Boston University London School of Economics London School of Economics September, 2013 Abstract We study

How Does Algorithmic Trading Improve Market. Quality?

How Does Algorithmic Trading Improve Market Quality? Matthew R. Lyle, James P. Naughton, Brian M. Weller Kellogg School of Management August 19, 2015 Abstract We use a comprehensive panel of NYSE limit

How Does Algorithmic Trading Improve Market Quality? Matthew R. Lyle, James P. Naughton, Brian M. Weller Kellogg School of Management August 19, 2015 Abstract We use a comprehensive panel of NYSE limit

UBS Global Asset Management has

IIJ-130-STAUB.qxp 4/17/08 4:45 PM Page 1 RENATO STAUB is a senior assest allocation and risk analyst at UBS Global Asset Management in Zurich. [email protected] Deploying Alpha: A Strategy to Capture

IIJ-130-STAUB.qxp 4/17/08 4:45 PM Page 1 RENATO STAUB is a senior assest allocation and risk analyst at UBS Global Asset Management in Zurich. [email protected] Deploying Alpha: A Strategy to Capture

High-frequency trading, flash crashes & regulation Prof. Philip Treleaven

High-frequency trading, flash crashes & regulation Prof. Philip Treleaven Director, UCL Centre for Financial Computing UCL Professor of Computing www.financialcomputing.org [email protected] Normal

High-frequency trading, flash crashes & regulation Prof. Philip Treleaven Director, UCL Centre for Financial Computing UCL Professor of Computing www.financialcomputing.org [email protected] Normal

Bene ts and Costs of Organised Trading for Non Equity Products

Bene ts and Costs of Organised Trading for Non Equity Products Thierry Foucault, HEC, Paris I Background I Market Transparency I Electronic Trading I Conclusions Introduction Background I "We rea rm our

Bene ts and Costs of Organised Trading for Non Equity Products Thierry Foucault, HEC, Paris I Background I Market Transparency I Electronic Trading I Conclusions Introduction Background I "We rea rm our

Adaptive Arrival Price

Adaptive Arrival Price Julian Lorenz (ETH Zurich, Switzerland) Robert Almgren (Adjunct Professor, New York University) Algorithmic Trading 2008, London 07. 04. 2008 Outline Evolution of algorithmic trading

Adaptive Arrival Price Julian Lorenz (ETH Zurich, Switzerland) Robert Almgren (Adjunct Professor, New York University) Algorithmic Trading 2008, London 07. 04. 2008 Outline Evolution of algorithmic trading

High Frequency Quoting, Trading and the Efficiency of Prices. Jennifer Conrad, UNC Sunil Wahal, ASU Jin Xiang, Integrated Financial Engineering

High Frequency Quoting, Trading and the Efficiency of Prices Jennifer Conrad, UNC Sunil Wahal, ASU Jin Xiang, Integrated Financial Engineering 1 What is High Frequency Quoting/Trading? How fast is fast?

High Frequency Quoting, Trading and the Efficiency of Prices Jennifer Conrad, UNC Sunil Wahal, ASU Jin Xiang, Integrated Financial Engineering 1 What is High Frequency Quoting/Trading? How fast is fast?

The Rise of Machines and Liquidity Patterns in Markets

The Rise of Machines and Liquidity Patterns in Markets Vasant Dhar Professor and Co-Director, Center for Business Analytics Stern School of Business Editor-in-Chief, Big Data Journal April 25, 2014 Key

The Rise of Machines and Liquidity Patterns in Markets Vasant Dhar Professor and Co-Director, Center for Business Analytics Stern School of Business Editor-in-Chief, Big Data Journal April 25, 2014 Key

This paper is not to be removed from the Examination Halls

~~FN3023 ZB d0 This paper is not to be removed from the Examination Halls UNIVERSITY OF LONDON FN3023 ZB BSc degrees and Diplomas for Graduates in Economics, Management, Finance and the Social Sciences,

~~FN3023 ZB d0 This paper is not to be removed from the Examination Halls UNIVERSITY OF LONDON FN3023 ZB BSc degrees and Diplomas for Graduates in Economics, Management, Finance and the Social Sciences,

Need For Speed? Low Latency Trading and Adverse Selection

Need For Speed? Low Latency Trading and Adverse Selection Albert J. Menkveld and Marius A. Zoican April 22, 2013 - very preliminary and incomplete. comments and suggestions are welcome - First version:

Need For Speed? Low Latency Trading and Adverse Selection Albert J. Menkveld and Marius A. Zoican April 22, 2013 - very preliminary and incomplete. comments and suggestions are welcome - First version:

Rise of the Machines: Algorithmic Trading in the Foreign Exchange Market. Alain Chaboud, Benjamin Chiquoine, Erik Hjalmarsson, and Clara Vega

Rise of the Machines: Algorithmic Trading in the Foreign Exchange Market Alain Chaboud, Benjamin Chiquoine, Erik Hjalmarsson, and Clara Vega 1 Rise of the Machines Main Question! What role do algorithmic

Rise of the Machines: Algorithmic Trading in the Foreign Exchange Market Alain Chaboud, Benjamin Chiquoine, Erik Hjalmarsson, and Clara Vega 1 Rise of the Machines Main Question! What role do algorithmic

René Garcia Professor of finance

Liquidity Risk: What is it? How to Measure it? René Garcia Professor of finance EDHEC Business School, CIRANO Cirano, Montreal, January 7, 2009 The financial and economic environment We are living through

Liquidity Risk: What is it? How to Measure it? René Garcia Professor of finance EDHEC Business School, CIRANO Cirano, Montreal, January 7, 2009 The financial and economic environment We are living through

Asymmetric Information (2)

") Asymmetric nformation (2) John Y. Campbell Ec2723 November 2013 John Y. Campbell (Ec2723) Asymmetric nformation (2) November 2013 1 / 24 Outline Market microstructure The study of trading costs Bid-ask

Asymmetric nformation (2) John Y. Campbell Ec2723 November 2013 John Y. Campbell (Ec2723) Asymmetric nformation (2) November 2013 1 / 24 Outline Market microstructure The study of trading costs Bid-ask

High Frequency Trading An Asset Manager s Perspective

NBIM Discussion NOTE #1-2013 High Frequency Trading An Asset Manager s Perspective In this note we review the rapidly expanding literature in the area of market microstructure, high frequency and computer-based

NBIM Discussion NOTE #1-2013 High Frequency Trading An Asset Manager s Perspective In this note we review the rapidly expanding literature in the area of market microstructure, high frequency and computer-based

Rise of the Machines: Algorithmic Trading in the Foreign. Exchange Market

Rise of the Machines: Algorithmic Trading in the Foreign Exchange Market Alain Chaboud Benjamin Chiquoine Erik Hjalmarsson Clara Vega February 20, 2013 Abstract We study the impact of algorithmic trading

Rise of the Machines: Algorithmic Trading in the Foreign Exchange Market Alain Chaboud Benjamin Chiquoine Erik Hjalmarsson Clara Vega February 20, 2013 Abstract We study the impact of algorithmic trading

FIN 500R Exam Answers. By nature of the exam, almost none of the answers are unique. In a few places, I give examples of alternative correct answers.

FIN 500R Exam Answers Phil Dybvig October 14, 2015 By nature of the exam, almost none of the answers are unique. In a few places, I give examples of alternative correct answers. Bubbles, Doubling Strategies,

FIN 500R Exam Answers Phil Dybvig October 14, 2015 By nature of the exam, almost none of the answers are unique. In a few places, I give examples of alternative correct answers. Bubbles, Doubling Strategies,

The Need for Speed: Minimum Quote Life Rules and Algorithmic. Trading

The Need for Speed: Minimum Quote Life Rules and Algorithmic Trading Alain Chaboud Erik Hjalmarsson Clara Vega [PRELIMINARY AND INCOMPLETE. PLEASE DO NOT CITE.] May 4, 2015 Abstract We study the impact

The Need for Speed: Minimum Quote Life Rules and Algorithmic Trading Alain Chaboud Erik Hjalmarsson Clara Vega [PRELIMINARY AND INCOMPLETE. PLEASE DO NOT CITE.] May 4, 2015 Abstract We study the impact

High Frequency Trading around Macroeconomic News Announcements. Evidence from the US Treasury market. George J. Jiang Ingrid Lo Giorgio Valente 1

High Frequency Trading around Macroeconomic News Announcements Evidence from the US Treasury market George J. Jiang Ingrid Lo Giorgio Valente 1 This draft: November 2013 1 George J. Jiang is from the Department

High Frequency Trading around Macroeconomic News Announcements Evidence from the US Treasury market George J. Jiang Ingrid Lo Giorgio Valente 1 This draft: November 2013 1 George J. Jiang is from the Department

THE EFFECTS OF STOCK LENDING ON SECURITY PRICES: AN EXPERIMENT

THE EFFECTS OF STOCK LENDING ON SECURITY PRICES: AN EXPERIMENT Steve Kaplan Toby Moskowitz Berk Sensoy November, 2011 MOTIVATION: WHAT IS THE IMPACT OF SHORT SELLING ON SECURITY PRICES? Does shorting make

THE EFFECTS OF STOCK LENDING ON SECURITY PRICES: AN EXPERIMENT Steve Kaplan Toby Moskowitz Berk Sensoy November, 2011 MOTIVATION: WHAT IS THE IMPACT OF SHORT SELLING ON SECURITY PRICES? Does shorting make

How aggressive are high frequency traders?

How aggressive are high frequency traders? Björn Hagströmer, Lars Nordén and Dong Zhang Stockholm University School of Business, S 106 91 Stockholm July 30, 2013 Abstract We study order aggressiveness

How aggressive are high frequency traders? Björn Hagströmer, Lars Nordén and Dong Zhang Stockholm University School of Business, S 106 91 Stockholm July 30, 2013 Abstract We study order aggressiveness

High-frequency trading: towards capital market efficiency, or a step too far?

Agenda Advancing economics in business High-frequency trading High-frequency trading: towards capital market efficiency, or a step too far? The growth in high-frequency trading has been a significant development

Agenda Advancing economics in business High-frequency trading High-frequency trading: towards capital market efficiency, or a step too far? The growth in high-frequency trading has been a significant development

Dark trading and price discovery

Dark trading and price discovery Carole Comerton-Forde University of Melbourne and Tālis Putniņš University of Technology, Sydney Market Microstructure Confronting Many Viewpoints 11 December 2014 What

Dark trading and price discovery Carole Comerton-Forde University of Melbourne and Tālis Putniņš University of Technology, Sydney Market Microstructure Confronting Many Viewpoints 11 December 2014 What

This paper sets out the challenges faced to maintain efficient markets, and the actions that the WFE and its member exchanges support.

Understanding High Frequency Trading (HFT) Executive Summary This paper is designed to cover the definitions of HFT set by regulators, the impact HFT has made on markets, the actions taken by exchange

Understanding High Frequency Trading (HFT) Executive Summary This paper is designed to cover the definitions of HFT set by regulators, the impact HFT has made on markets, the actions taken by exchange

Finance 400 A. Penati - G. Pennacchi Market Micro-Structure: Notes on the Kyle Model

Finance 400 A. Penati - G. Pennacchi Market Micro-Structure: Notes on the Kyle Model These notes consider the single-period model in Kyle (1985) Continuous Auctions and Insider Trading, Econometrica 15,

Finance 400 A. Penati - G. Pennacchi Market Micro-Structure: Notes on the Kyle Model These notes consider the single-period model in Kyle (1985) Continuous Auctions and Insider Trading, Econometrica 15,

A Stock Trading Algorithm Model Proposal, based on Technical Indicators Signals

Informatica Economică vol. 15, no. 1/2011 183 A Stock Trading Algorithm Model Proposal, based on Technical Indicators Signals Darie MOLDOVAN, Mircea MOCA, Ştefan NIŢCHI Business Information Systems Dept.

Informatica Economică vol. 15, no. 1/2011 183 A Stock Trading Algorithm Model Proposal, based on Technical Indicators Signals Darie MOLDOVAN, Mircea MOCA, Ştefan NIŢCHI Business Information Systems Dept.

Shifting Sands: High Frequency, Retail, and Institutional Trading Profits over Time

Shifting Sands: High Frequency, Retail, and Institutional Trading Profits over Time Katya Malinova University of Toronto Andreas Park University of Toronto Ryan Riordan University of Ontario Institute

Shifting Sands: High Frequency, Retail, and Institutional Trading Profits over Time Katya Malinova University of Toronto Andreas Park University of Toronto Ryan Riordan University of Ontario Institute

INTERNATIONAL EVIDENCE ON ALGORITHMIC TRADING

INTERNATIONAL EVIDENCE ON ALGORITHMIC TRADING Ekkehart Boehmer Kingsley Fong Julie Wu March 14, 2012 Abstract We use a large sample from 2001 2009 that incorporates 39 exchanges and an average of 12,800

INTERNATIONAL EVIDENCE ON ALGORITHMIC TRADING Ekkehart Boehmer Kingsley Fong Julie Wu March 14, 2012 Abstract We use a large sample from 2001 2009 that incorporates 39 exchanges and an average of 12,800

From Traditional Floor Trading to Electronic High Frequency Trading (HFT) Market Implications and Regulatory Aspects Prof. Dr. Hans Peter Burghof

Market Implications and Regulatory Aspects Prof. Dr. Hans Peter Burghof") From Traditional Floor Trading to Electronic High Frequency Trading (HFT) Market Implications and Regulatory Aspects Prof. Dr. Hans Peter Burghof Universität Hohenheim Institut für Financial Management

From Traditional Floor Trading to Electronic High Frequency Trading (HFT) Market Implications and Regulatory Aspects Prof. Dr. Hans Peter Burghof Universität Hohenheim Institut für Financial Management

Anticipatory Traders and Trading Speed

Anticipatory Traders and Trading Speed Raymond P. H. Fishe Richard Haynes and Esen Onur* This version: March 26, 2015 ABSTRACT We investigate whether there is a class of market participants who follow

Anticipatory Traders and Trading Speed Raymond P. H. Fishe Richard Haynes and Esen Onur* This version: March 26, 2015 ABSTRACT We investigate whether there is a class of market participants who follow

END OF CHAPTER EXERCISES - ANSWERS. Chapter 14 : Stock Valuation and the EMH

1 EN OF CHAPTER EXERCISES - ANSWERS Chapter 14 : Stock Valuation and the EMH Q1 oes the dividend discount model ignore the mass of investors who have bought their shares with the intention of selling them

1 EN OF CHAPTER EXERCISES - ANSWERS Chapter 14 : Stock Valuation and the EMH Q1 oes the dividend discount model ignore the mass of investors who have bought their shares with the intention of selling them

Media-Driven High Frequency Trading:

Media-Driven High Frequency Trading: Evidence from News Analytics Bastian von Beschwitz* INSEAD Donald B. Keim** Wharton School Massimo Massa*** INSEAD October 2, 2013 Abstract We investigate whether providers

Media-Driven High Frequency Trading: Evidence from News Analytics Bastian von Beschwitz* INSEAD Donald B. Keim** Wharton School Massimo Massa*** INSEAD October 2, 2013 Abstract We investigate whether providers

Why Do Firms Announce Open-Market Repurchase Programs?

Why Do Firms Announce Open-Market Repurchase Programs? Jacob Oded, (2005) Boston College PhD Seminar in Corporate Finance, Spring 2006 Outline 1 The Problem Previous Work 2 3 Outline The Problem Previous

Why Do Firms Announce Open-Market Repurchase Programs? Jacob Oded, (2005) Boston College PhD Seminar in Corporate Finance, Spring 2006 Outline 1 The Problem Previous Work 2 3 Outline The Problem Previous

A new model of a market maker

A new model of a market maker M.C. Cheung 28786 Master s thesis Economics and Informatics Specialisation in Computational Economics and Finance Erasmus University Rotterdam, the Netherlands January 6,

A new model of a market maker M.C. Cheung 28786 Master s thesis Economics and Informatics Specialisation in Computational Economics and Finance Erasmus University Rotterdam, the Netherlands January 6,

Algorithmic Trading and the Market for Liquidity

JOURNAL OF FINANCIAL AND QUANTITATIVE ANALYSIS Vol. 48, No. 4, Aug. 2013, pp. 1001 1024 COPYRIGHT 2013, MICHAEL G. FOSTER SCHOOL OF BUSINESS, UNIVERSITY OF WASHINGTON, SEATTLE, WA 98195 doi:10.1017/s0022109013000471

JOURNAL OF FINANCIAL AND QUANTITATIVE ANALYSIS Vol. 48, No. 4, Aug. 2013, pp. 1001 1024 COPYRIGHT 2013, MICHAEL G. FOSTER SCHOOL OF BUSINESS, UNIVERSITY OF WASHINGTON, SEATTLE, WA 98195 doi:10.1017/s0022109013000471

Department of Economics and Related Studies Financial Market Microstructure. Topic 1 : Overview and Fixed Cost Models of Spreads

Session 2008-2009 Department of Economics and Related Studies Financial Market Microstructure Topic 1 : Overview and Fixed Cost Models of Spreads 1 Introduction 1.1 Some background Most of what is taught

Session 2008-2009 Department of Economics and Related Studies Financial Market Microstructure Topic 1 : Overview and Fixed Cost Models of Spreads 1 Introduction 1.1 Some background Most of what is taught

Markus K. Brunnermeier

Institutional tut Finance Financial Crises, Risk Management and Liquidity Markus K. Brunnermeier Preceptor: Dong BeomChoi Princeton University 1 Market Making Limit Orders Limit order price contingent

Institutional tut Finance Financial Crises, Risk Management and Liquidity Markus K. Brunnermeier Preceptor: Dong BeomChoi Princeton University 1 Market Making Limit Orders Limit order price contingent

The Flash Crash: The Impact of High Frequency Trading on an Electronic Market

The Flash Crash: The Impact of High Frequency Trading on an Electronic Market Andrei Kirilenko Mehrdad Samadi Albert S. Kyle Tugkan Tuzun January 12, 2011 ABSTRACT The Flash Crash, a brief period of extreme

The Flash Crash: The Impact of High Frequency Trading on an Electronic Market Andrei Kirilenko Mehrdad Samadi Albert S. Kyle Tugkan Tuzun January 12, 2011 ABSTRACT The Flash Crash, a brief period of extreme

Need for Speed? Exchange Latency and Liquidity

Duisenberg school of finance - Tinbergen Institute Discussion Paper TI 14-097/IV//DSF78 Need for Speed? Exchange Latency and Liquidity Albert J. Menkveld Marius A. Zoican Faculty of Economics and Business

Duisenberg school of finance - Tinbergen Institute Discussion Paper TI 14-097/IV//DSF78 Need for Speed? Exchange Latency and Liquidity Albert J. Menkveld Marius A. Zoican Faculty of Economics and Business

Herding, Contrarianism and Delay in Financial Market Trading

Herding, Contrarianism and Delay in Financial Market Trading A Lab Experiment Andreas Park & Daniel Sgroi University of Toronto & University of Warwick Two Restaurants E cient Prices Classic Herding Example:

Herding, Contrarianism and Delay in Financial Market Trading A Lab Experiment Andreas Park & Daniel Sgroi University of Toronto & University of Warwick Two Restaurants E cient Prices Classic Herding Example:

Intraday Trading Invariance. E-Mini S&P 500 Futures Market

in the E-Mini S&P 500 Futures Market University of Illinois at Chicago Joint with Torben G. Andersen, Pete Kyle, and Anna Obizhaeva R/Finance 2015 Conference University of Illinois at Chicago May 29-30,

in the E-Mini S&P 500 Futures Market University of Illinois at Chicago Joint with Torben G. Andersen, Pete Kyle, and Anna Obizhaeva R/Finance 2015 Conference University of Illinois at Chicago May 29-30,