Latin America s Debt crisis 1980 s

|

|

|

- Cecil Parker

- 10 years ago

- Views:

Transcription

1 Latin America s Debt crisis 1980 s

2 The LATAM Debt Crisis of the 80 s Why the region accumulated an unmanageable external debt? What factors precipitated the crisis? How sovereignties and international creditors responded to the crisis? What was the most important outcome of the crisis resolution and afterwards? Is Latin America vulnerable to new debt crises?

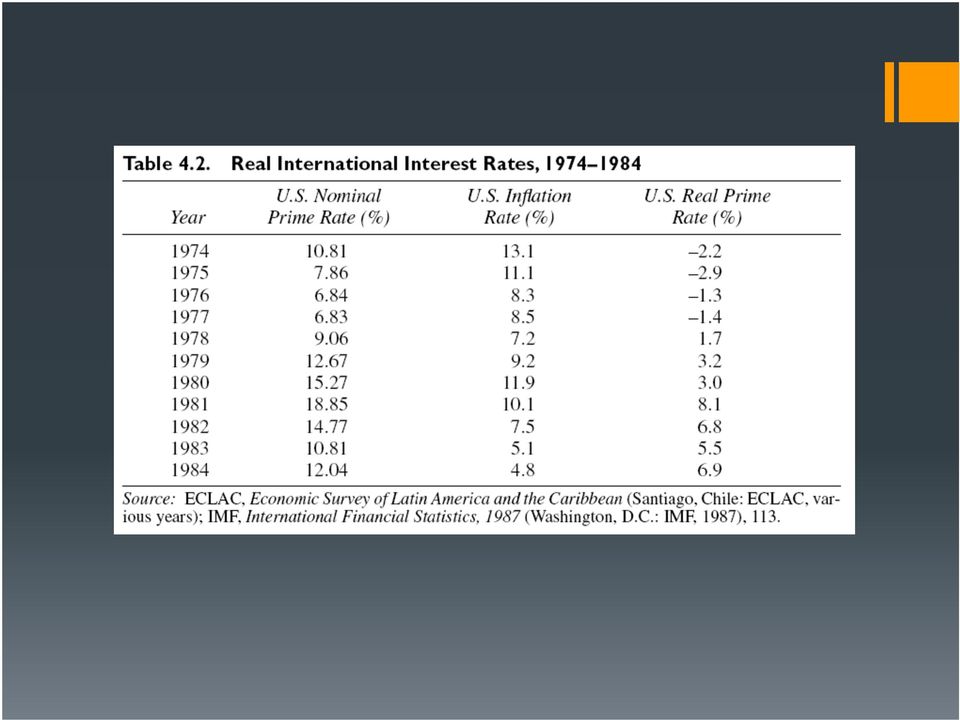

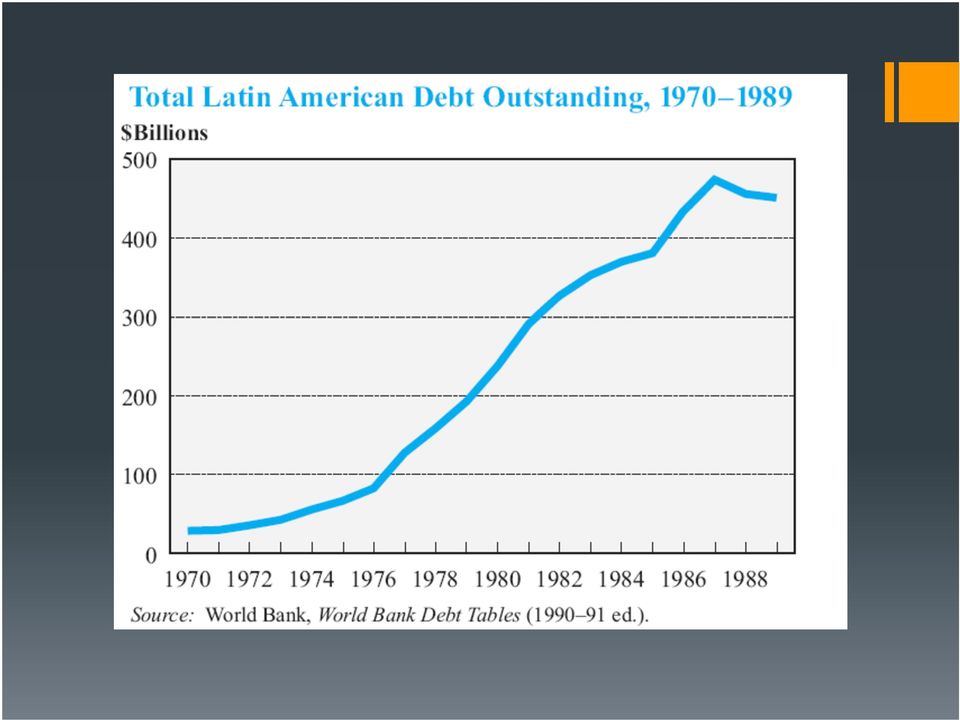

3 Origins of the crisis The debt buildup A. External factors The collapse of the Bretton Woods system was accompanied by the reemergence of international capital markets and an increase in the activity of international commercial banks. In 1973 the OPEC quadrupled the prices of oil. Oil producers countries deposited their surpluses of asses in international commercial banks. Oil-importing nations in Latin America increasingly needed capital, in part to finance the external deficits associated with oil inflation. The so called Petrodollar recycling program allowed lesser developed nations to purchase oil even as its price skyrocketed, and it was actively promoted by the United States. A drastic change in the source and composition of loans to Latin American in the 1970s, from long-term official loans with low interest rates to short-term commercial loans with variable high interest rates was a major factor which led to the debt crisis of the 1980s.

4 The debt buildup B Internal factors A good part of Latin American debt went to finance the growing trade imbalances. Many LATAM nations kept the real exchange rate strong as a measure against inflation, worsening the current account. The continuous real exchange appreciation made international interest rates (low in nominal terms) to be negative in real terms. This exacerbated indebtedness.

5

6

7 What factors precipitated the crisis? Raising interest rates Developed countries recession External shocks Capital flight Many LATAM countries allowed the liberalization of foreign trade, domestic financial markets, and international capital flows. The latter caused large private capital outflows or capital flight from the region to developed countries.

8

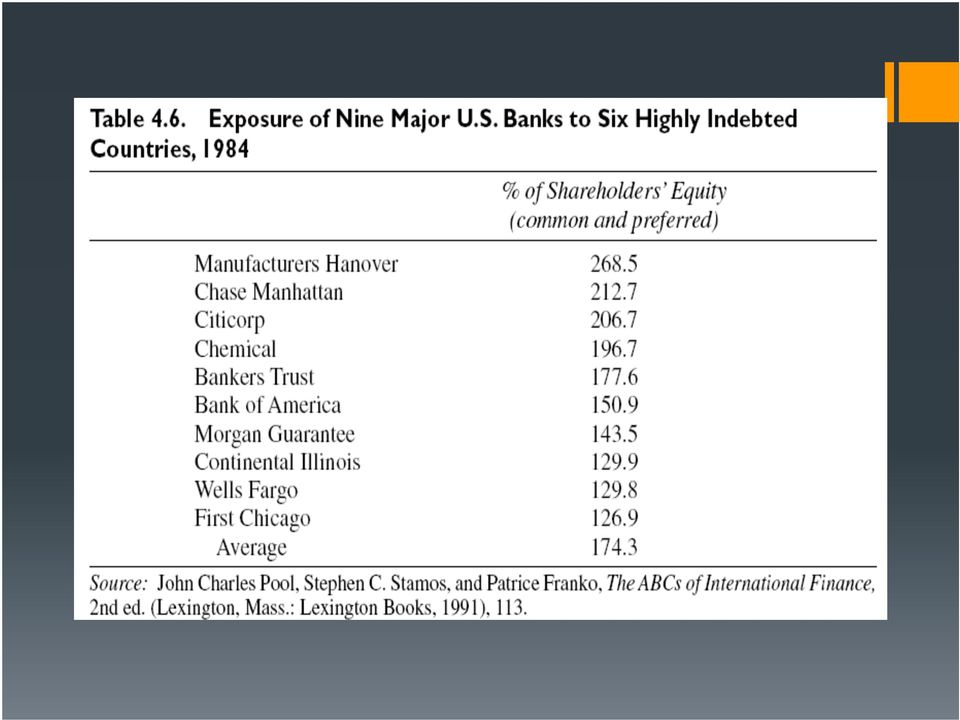

9 Responses to the debt crisis 1. The IMF Approach The absorption approach: A way of understanding the determinants of the balance of trade, noting that it is equal to income minus absorption Y A = B. If Y- A > 0 implies X-IM > 0 and NX>0 Trade surplus A trade surplus, then, would help restore financial health by decreasing the need to finance imports, leaving the balance to pay off the debt. The IMF recommended contractionary policies aimed to decrease fiscal spending and money emission. Countries that signed agreements with IMF were signaling international banks of their intentions to abide to the rules of the game. The notion of conditionality emerged with its harsh consequences for the inhabitants of the debtor countries. Lending from the IMF and international banks were used for servicing the debt. Resulting in a non-resolution of the problem.

10 2. Markets reaction to the debt crisis Secondary markets

11 Debt-for-equity swaps There are at least three parties to the transaction. Example 1. Citibank recognizes $100m of bad debt in Mexico. 2. Chrysler wants to invest in Mexico. It needs the equivalent of $75m in pesos. Chrysler could take US$75m and convert it to pesos at the prevailing exchange rate. 3.The Mexican central bank wants to help Citibank recoup some of the $100 m bad loan. That way Citibank will be willing to lend to other Mexican clients in the future. 4.The Mexican central bank approaches Citibank and Chrysler and arranges the deal. Let s say it arranges for Citibank to sell the debt at a 40% discount and agrees to purchase it from Chrysler at 75% of face value. 5.Chrysler then gives Citibank $60 (40% discount off of $100m ) and is given the $100m bad debt. Just a paper asset. 6. Chrysler immediately runs to the central bank and swaps the bad debt for the equivalent of $75m in pesos. 7. Chrysler then invests the $75m in pesos in Mexico.

12 3. Beyond Muddling Through: The Baker Plan Countries could not continue to service their debt through contractionary policies, growth must be reassumed. The Baker plan targeted fifteen less-developed countries for $29 billion of new money, $20 billion from commercial banks and $9 billion from the IMF and the World Bank. Debt came to be understood as a development problem, and the World Bank was charged with assisting in the management of the adjustment process. Too little too late. $29 billion will have no impact on obligations of near one trillion dollars The consensus was that the banks were prepared to take a realistic position on developing country debt: it would never be repaid in full. Jump-starting growth would not work until the debt burden was reduced two years later under the Brady plan.

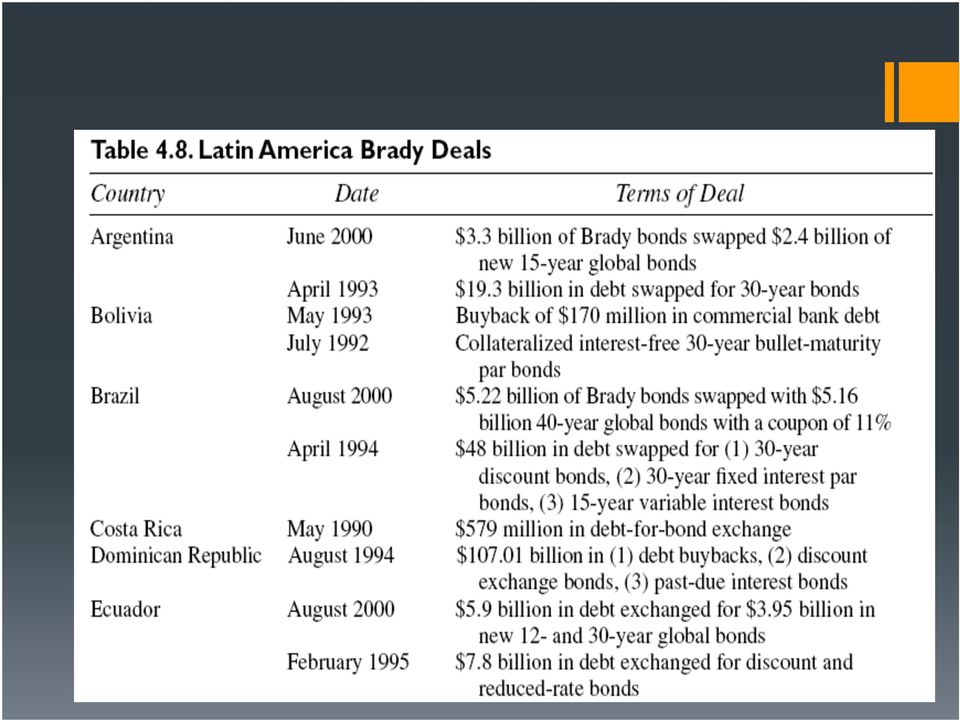

13 The 1989 Brady Plan It was aimed to debt reduction throughout 3 options: decreasing the face value of debt extending the time period of obligations Infusion of new money Mexico restructured $48 billion of its liabilities. This debt relief reduced net transfers by $4 billion per year, nearly 2 percent of the gross domestic product (GDP), from 1989 through 1994.

14

15

16

17 Lessons from the debt crisis Recovery from crisis long and painful Latin American debt crisis of the 1980s (as) a crucial dividing mark in the area s recent economic history (Rodrik, 2003). Strong economic fundamentals matter; countries must put attention to price stability and budget constrains. The burden of adjustment to the debt crisis may have fallen disproportionately on women in particular andon the poorest people in general. Rodrik s (2003), sees the debt crisis as the explosive end of a period of continued decline: the import substitution industrialization development model.

18 Is Latin America vulnerable to new debt crises? Many agree that the openness of the financial sector in emerging markets triggered the financial crises of Mexico in 1994, East Asia, Russia and Brazil at the end of the 1990 s. However, these financial crises did not caused sovereign debt crises. LATAM countries returned to the international markets, and many nations are emerging as important players in the world s debt and equity markets. The return to the markets has not reached the poorest countries in the region

Lecture 12: Benefits of International Financial Integration. Pros and Cons of Open Financial Markets

Lecture 12: Benefits of International Financial Integration Pros and Cons of Open Financial Markets Advantages of financial integration The theory of intertemporal optimization Other advantages Do financial

Lecture 12: Benefits of International Financial Integration Pros and Cons of Open Financial Markets Advantages of financial integration The theory of intertemporal optimization Other advantages Do financial

ECON 4311: The Economy of Latin America. Debt Relief. Part 1: Early Initiatives

ECON 4311: The Economy of Latin America Debt Relief Part 1: Early Initiatives The Debt Crisis of 1982 severely hit the Latin American economies for many years to come. Balance of payments deficits and

ECON 4311: The Economy of Latin America Debt Relief Part 1: Early Initiatives The Debt Crisis of 1982 severely hit the Latin American economies for many years to come. Balance of payments deficits and

Latin America s s Foreign Debt

Latin America s s Foreign Debt Causes and Effects Internal Causes of the Debt Overvalued currency associated with ISI Returns on projects in future, but payments now: Debt trap Populist economic policies:

Latin America s s Foreign Debt Causes and Effects Internal Causes of the Debt Overvalued currency associated with ISI Returns on projects in future, but payments now: Debt trap Populist economic policies:

The 1990 s Financial Crises in Nordic Countries

The 1990 s Financial Crises in Nordic Countries Seppo Honkapohja, Bank of Finland I. Introduction 19 crises in advanced countries since WWII (before the current) 1990 s crises in Finland, Norway and Sweden

The 1990 s Financial Crises in Nordic Countries Seppo Honkapohja, Bank of Finland I. Introduction 19 crises in advanced countries since WWII (before the current) 1990 s crises in Finland, Norway and Sweden

Practice Problems on Current Account

Practice Problems on Current Account 1- List de categories of credit items and debit items that appear in a country s current account. What is the current account balance? What is the relationship between

Practice Problems on Current Account 1- List de categories of credit items and debit items that appear in a country s current account. What is the current account balance? What is the relationship between

Lecture 10: International banking

Lecture 10: International banking The sessions so far have focused on banking in a domestic context. In this lecture we are going to look at the issues which arise from the internationalisation of banking,

Lecture 10: International banking The sessions so far have focused on banking in a domestic context. In this lecture we are going to look at the issues which arise from the internationalisation of banking,

Introduction to International Finance

Introduction to International Finance Barry W. Ickes Econ 434 Fall 2008 1. Introduction International macroeconomics (or international finance) as a subject covers many topical issues. What has happened

Introduction to International Finance Barry W. Ickes Econ 434 Fall 2008 1. Introduction International macroeconomics (or international finance) as a subject covers many topical issues. What has happened

FINANCIALISATION AND EXCHANGE RATE DYNAMICS IN SMALL OPEN ECONOMIES. Hamid Raza PhD Student, Economics University of Limerick Ireland

FINANCIALISATION AND EXCHANGE RATE DYNAMICS IN SMALL OPEN ECONOMIES Hamid Raza PhD Student, Economics University of Limerick Ireland Financialisation Financialisation as a broad concept refers to: a) an

FINANCIALISATION AND EXCHANGE RATE DYNAMICS IN SMALL OPEN ECONOMIES Hamid Raza PhD Student, Economics University of Limerick Ireland Financialisation Financialisation as a broad concept refers to: a) an

CHAPTER 11 INTERNATIONAL BANKING AND MONEY MARKET SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

CHAPTER 11 INTERNATIONAL BANKING AND MONEY MARKET SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Briefly discuss some of the services that international banks provide

CHAPTER 11 INTERNATIONAL BANKING AND MONEY MARKET SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Briefly discuss some of the services that international banks provide

Public Debt in Developing Countries

Public Debt in Developing Countries Has the Market-Based Model Worked? Indermit Gill and Brian Pinto The World Bank Capital Flows and Global External Imbalances Seminar April 4 2006 In Principle: Government

Public Debt in Developing Countries Has the Market-Based Model Worked? Indermit Gill and Brian Pinto The World Bank Capital Flows and Global External Imbalances Seminar April 4 2006 In Principle: Government

Managing Systemic Banking Crises. David S. Hoelscher Assistant Director Money and Credit Markets Department

Managing Systemic Banking Crises David S. Hoelscher Assistant Director Money and Credit Markets Department 2 Introduction Systemic banking crises of unprecedented scale: Argentina, East Asia, Ecuador,

Managing Systemic Banking Crises David S. Hoelscher Assistant Director Money and Credit Markets Department 2 Introduction Systemic banking crises of unprecedented scale: Argentina, East Asia, Ecuador,

MGE#12 The Balance of Payments

MGE#12 The Balance of Payments The Current Account, the Capital Account and the Balance of Payments Introduction to the Foreign Exchange Market Savings, Investment and the Current Account 1 From last session

MGE#12 The Balance of Payments The Current Account, the Capital Account and the Balance of Payments Introduction to the Foreign Exchange Market Savings, Investment and the Current Account 1 From last session

EXTERNAL DEBT MANAGEMENT: CASE STUDY ON INDIA

EXTERNAL DEBT MANAGEMENT: CASE STUDY ON INDIA \ CONTENTS 1.1 External Debt-Definition 1.2An overview 1.3 External Debt and Macro economic Considerations 1.4 Important Aspects Related To External debt Management

EXTERNAL DEBT MANAGEMENT: CASE STUDY ON INDIA \ CONTENTS 1.1 External Debt-Definition 1.2An overview 1.3 External Debt and Macro economic Considerations 1.4 Important Aspects Related To External debt Management

Fiscal consolidation: the Greek case. Dionysios A. Lalountas Directorate of Macroeconomic Policy & Forecasts Ministry of Finance

Fiscal consolidation: the Greek case Dionysios A. Lalountas Directorate of Macroeconomic Policy & Forecasts Ministry of Finance 1 Structure of the presentation Macroeconomic developments before the sovereign

Fiscal consolidation: the Greek case Dionysios A. Lalountas Directorate of Macroeconomic Policy & Forecasts Ministry of Finance 1 Structure of the presentation Macroeconomic developments before the sovereign

Naturally, these difficult external conditions have affected the Mexican economy. I would stress in particular three developments in this regard:

REMARKS BY MR. JAVIER GUZMÁN CALAFELL, DEPUTY GOVERNOR AT THE BANCO DE MÉXICO, ON THE MEXICAN ECONOMY IN AN ADVERSE EXTERNAL ENVIRONMENT: CHALLENGES AND POLICY RESPONSE, SANTANDER MEXICO DAY 2016, Mexico

REMARKS BY MR. JAVIER GUZMÁN CALAFELL, DEPUTY GOVERNOR AT THE BANCO DE MÉXICO, ON THE MEXICAN ECONOMY IN AN ADVERSE EXTERNAL ENVIRONMENT: CHALLENGES AND POLICY RESPONSE, SANTANDER MEXICO DAY 2016, Mexico

Specifics of national debt management and its consequences for the Ukrainian economy

Anatoliy Yepifanov (Ukraine), Vyacheslav Plastun (Ukraine) Specifics of national debt management and its consequences for the Ukrainian economy Abstract This article is about the specifics of the national

Anatoliy Yepifanov (Ukraine), Vyacheslav Plastun (Ukraine) Specifics of national debt management and its consequences for the Ukrainian economy Abstract This article is about the specifics of the national

Research. What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields?

Research What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields? The global economy appears to be on the road to recovery and the risk of a double dip recession is receding.

Research What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields? The global economy appears to be on the road to recovery and the risk of a double dip recession is receding.

On Corporate Debt Restructuring *

On Corporate Debt Restructuring * Asian Bankers Association 1. One of the major consequences of the current financial crisis is the corporate debt problem being faced by several economies in the region.

On Corporate Debt Restructuring * Asian Bankers Association 1. One of the major consequences of the current financial crisis is the corporate debt problem being faced by several economies in the region.

CONTAGION: HOW THE ASIAN CRISIS SPREAD

EDRC Briefing Notes Number 3 ASIAN DEVELOPMENT BANK Economics and Development Resource Center CONTAGION: HOW THE ASIAN CRISIS SPREAD W. Christopher Walker October 1998 CONTAGION: HOW THE ASIAN CRISIS SPREAD

EDRC Briefing Notes Number 3 ASIAN DEVELOPMENT BANK Economics and Development Resource Center CONTAGION: HOW THE ASIAN CRISIS SPREAD W. Christopher Walker October 1998 CONTAGION: HOW THE ASIAN CRISIS SPREAD

Factoring Exchange Rate Policy into your Investment Strategy: Risks Facing Andean Countries

Factoring Exchange Rate Policy into your Investment Strategy: Risks Facing Andean Countries September 2011 Dr. Eliot Kalter President, E M Strategies Senior Fellow, The Fletcher School [email protected]

Factoring Exchange Rate Policy into your Investment Strategy: Risks Facing Andean Countries September 2011 Dr. Eliot Kalter President, E M Strategies Senior Fellow, The Fletcher School [email protected]

Fixed Exchange Rates and Exchange Market Intervention. Chapter 18

Fixed Exchange Rates and Exchange Market Intervention Chapter 18 1. Central bank intervention in the foreign exchange market 2. Stabilization under xed exchange rates 3. Exchange rate crises 4. Sterilized

Fixed Exchange Rates and Exchange Market Intervention Chapter 18 1. Central bank intervention in the foreign exchange market 2. Stabilization under xed exchange rates 3. Exchange rate crises 4. Sterilized

Statistics Netherlands. Macroeconomic Imbalances Factsheet

Macroeconomic Imbalances Factsheet Introduction Since the outbreak of the credit crunch crisis in 2008, and the subsequent European debt crisis, it has become clear that there are large macroeconomic imbalances

Macroeconomic Imbalances Factsheet Introduction Since the outbreak of the credit crunch crisis in 2008, and the subsequent European debt crisis, it has become clear that there are large macroeconomic imbalances

Chapter 17. Preview. Introduction. Fixed Exchange Rates and Foreign Exchange Intervention

Chapter 17 Fixed Exchange Rates and Foreign Exchange Intervention Slides prepared by Thomas Bishop Copyright 2009 Pearson Addison-Wesley. All rights reserved. Preview Balance sheets of central banks Intervention

Chapter 17 Fixed Exchange Rates and Foreign Exchange Intervention Slides prepared by Thomas Bishop Copyright 2009 Pearson Addison-Wesley. All rights reserved. Preview Balance sheets of central banks Intervention

Reading the balance of payments accounts

Reading the balance of payments accounts The balance of payments refers to both: All the various payments between a country and the rest of the world The particular system of accounting we use to keep

Reading the balance of payments accounts The balance of payments refers to both: All the various payments between a country and the rest of the world The particular system of accounting we use to keep

X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/

1/ X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/ 10.1 Overview of World Economy Latest indicators are increasingly suggesting that the significant contraction in economic activity has come to an end, notably

1/ X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/ 10.1 Overview of World Economy Latest indicators are increasingly suggesting that the significant contraction in economic activity has come to an end, notably

2.5 Monetary policy: Interest rates

2.5 Monetary policy: Interest rates Learning Outcomes Describe the role of central banks as regulators of commercial banks and bankers to governments. Explain that central banks are usually made responsible

2.5 Monetary policy: Interest rates Learning Outcomes Describe the role of central banks as regulators of commercial banks and bankers to governments. Explain that central banks are usually made responsible

FISCAL POLICY: HAS BRAZIL GRADUATED FROM PRO- CYCLICAL POLICIES? Marcio Holland Secretary of Economic Policy Ministry of Finance, Brazil

FISCAL POLICY: HAS BRAZIL GRADUATED FROM PRO- CYCLICAL POLICIES? Marcio Holland Secretary of Economic Policy Ministry of Finance, Brazil XXXIX Meeting of the Network of Central Banks and Finance Ministries

FISCAL POLICY: HAS BRAZIL GRADUATED FROM PRO- CYCLICAL POLICIES? Marcio Holland Secretary of Economic Policy Ministry of Finance, Brazil XXXIX Meeting of the Network of Central Banks and Finance Ministries

Formulas for the Current Account Balance

Formulas for the Current Account Balance By Leigh Harkness Abstract This paper uses dynamic models to explain the current account balance in a range of situations. It starts with simple economies with

Formulas for the Current Account Balance By Leigh Harkness Abstract This paper uses dynamic models to explain the current account balance in a range of situations. It starts with simple economies with

Ch. 38 Practice MC 1. In international financial transactions, what are the only two things that individuals and firms can exchange? A.

Ch. 38 Practice MC 1. In international financial transactions, what are the only two things that individuals and firms can exchange? A. Currency and real assets. B. Services and manufactured goods. C.

Ch. 38 Practice MC 1. In international financial transactions, what are the only two things that individuals and firms can exchange? A. Currency and real assets. B. Services and manufactured goods. C.

Big Concepts. Balance of Payments Accounts. Financing International Trade. Economics 202 Principles Of Macroeconomics. Lecture 12

Economics 202 Principles Of Macroeconomics Professor Yamin Ahmad Big Concepts Balance of Payments Equilibrium The relationship between the current account, capital account and official settlements balance

Economics 202 Principles Of Macroeconomics Professor Yamin Ahmad Big Concepts Balance of Payments Equilibrium The relationship between the current account, capital account and official settlements balance

Globalization, IMF and Bulgaria

Globalization, IMF and Bulgaria Presentation by Piritta Sorsa * *, Resident Representative of the IMF in Bulgaria, At the Conference on Globalization and Sustainable Development, Varna Free University,

Globalization, IMF and Bulgaria Presentation by Piritta Sorsa * *, Resident Representative of the IMF in Bulgaria, At the Conference on Globalization and Sustainable Development, Varna Free University,

CAN INVESTORS PROFIT FROM DEVALUATIONS? THE PERFORMANCE OF WORLD STOCK MARKETS AFTER DEVALUATIONS. Bryan Taylor

CAN INVESTORS PROFIT FROM DEVALUATIONS? THE PERFORMANCE OF WORLD STOCK MARKETS AFTER DEVALUATIONS Introduction Bryan Taylor The recent devaluations in Asia have drawn attention to the risk investors face

CAN INVESTORS PROFIT FROM DEVALUATIONS? THE PERFORMANCE OF WORLD STOCK MARKETS AFTER DEVALUATIONS Introduction Bryan Taylor The recent devaluations in Asia have drawn attention to the risk investors face

1. Briefly discuss some of the services that international banks provide their customers and the market place.

Page 287-288 QUESTIONS 1. Briefly discuss some of the services that international banks provide their customers and the market place. Answer: International banks can be characterized by the types of services

Page 287-288 QUESTIONS 1. Briefly discuss some of the services that international banks provide their customers and the market place. Answer: International banks can be characterized by the types of services

Adjusting to a Changing Economic World. Good afternoon, ladies and gentlemen. It s a pleasure to be with you here in Montréal today.

Remarks by David Dodge Governor of the Bank of Canada to the Board of Trade of Metropolitan Montreal Montréal, Quebec 11 February 2004 Adjusting to a Changing Economic World Good afternoon, ladies and

Remarks by David Dodge Governor of the Bank of Canada to the Board of Trade of Metropolitan Montreal Montréal, Quebec 11 February 2004 Adjusting to a Changing Economic World Good afternoon, ladies and

D) surplus; negative. 9. The law of one price is enforced by: A) governments. B) producers. C) consumers. D) arbitrageurs.

surplus; negative. 9. The law of one price is enforced by: A) governments. B) producers. C) consumers. D) arbitrageurs.") 1. An open economy is one in which: A) the level of output is fixed. B) government spending exceeds revenues. C) the national interest rate equals the world interest rate. D) there is trade in goods and

1. An open economy is one in which: A) the level of output is fixed. B) government spending exceeds revenues. C) the national interest rate equals the world interest rate. D) there is trade in goods and

THE GREAT DEPRESSION OF FINLAND 1990-1993: causes and consequences. Jaakko Kiander Labour Institute for Economic Research

THE GREAT DEPRESSION OF FINLAND 1990-1993: causes and consequences Jaakko Kiander Labour Institute for Economic Research CONTENTS Causes background The crisis Consequences Role of economic policy Banking

THE GREAT DEPRESSION OF FINLAND 1990-1993: causes and consequences Jaakko Kiander Labour Institute for Economic Research CONTENTS Causes background The crisis Consequences Role of economic policy Banking

Financing the U.S. Trade Deficit

James K. Jackson Specialist in International Trade and Finance December 23, 2013 CRS Report for Congress Prepared for Members and Committees of Congress Congressional Research Service 7-5700 www.crs.gov

James K. Jackson Specialist in International Trade and Finance December 23, 2013 CRS Report for Congress Prepared for Members and Committees of Congress Congressional Research Service 7-5700 www.crs.gov

Lecture 3: Int l Finance

Lecture 3: Int l Finance 1. Mechanics of foreign exchange a. The FOREX market b. Exchange rates c. Exchange rate determination 2. Types of exchange rate regimes a. Fixed regimes b. Floating regimes 3.

Lecture 3: Int l Finance 1. Mechanics of foreign exchange a. The FOREX market b. Exchange rates c. Exchange rate determination 2. Types of exchange rate regimes a. Fixed regimes b. Floating regimes 3.

Analysis of the Impact of High Oil Prices on the Global Economy. International Energy Agency May 2004

Analysis of the Impact of High Oil Prices on the Global Economy International Energy Agency May 2004 SUMMARY Oil prices still matter to the health of the world economy. Higher oil prices since 1999 partly

Analysis of the Impact of High Oil Prices on the Global Economy International Energy Agency May 2004 SUMMARY Oil prices still matter to the health of the world economy. Higher oil prices since 1999 partly

What does the BOP Measure?

Balance of Payments - Concepts & Accounting Balance of Payments (a flow concept)» What does the BOP measure?» Accounting conventions» Important sub-categories of payments Current account Capital account

Balance of Payments - Concepts & Accounting Balance of Payments (a flow concept)» What does the BOP measure?» Accounting conventions» Important sub-categories of payments Current account Capital account

Practice Problems Mods 25, 28, 29

Practice Problems Mods 25, 28, 29 Multiple Choice Identify the choice that best completes the statement or answers the question. Scenario 25-1 First National Bank First National Bank has $80 million in

Practice Problems Mods 25, 28, 29 Multiple Choice Identify the choice that best completes the statement or answers the question. Scenario 25-1 First National Bank First National Bank has $80 million in

Markets, Investments, and Financial Management FIFTEENTH EDITION

INTRODUCTION TO FINANCE Markets, Investments, and Financial Management FIFTEENTH EDITION Ronald W. Melicher Professor of Finance University of Colorado at Boulder Edgar A. Norton Professor of Finance Illinois

INTRODUCTION TO FINANCE Markets, Investments, and Financial Management FIFTEENTH EDITION Ronald W. Melicher Professor of Finance University of Colorado at Boulder Edgar A. Norton Professor of Finance Illinois

Econ 202 Section 4 Final Exam

Douglas, Fall 2009 December 15, 2009 A: Special Code 00004 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 202 Section 4 Final Exam 1. Oceania buys $40

Douglas, Fall 2009 December 15, 2009 A: Special Code 00004 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 202 Section 4 Final Exam 1. Oceania buys $40

Macroeconomic Influences on U.S. Agricultural Trade

Macroeconomic Influences on U.S. Agricultural Trade In addition to the influence of shifting patterns of growth in foreign populations and per capita income, cyclical macroeconomic factors associated with

Macroeconomic Influences on U.S. Agricultural Trade In addition to the influence of shifting patterns of growth in foreign populations and per capita income, cyclical macroeconomic factors associated with

A Brief Research Note on. Temasek Holdings. And Singapore: Mr. Madoff Goes to Singapore

A Brief Research Note on Holdings And Singapore: Mr. Madoff Goes to Singapore Christopher Balding HSBC Business School Peking University Graduate School [email protected] Short Abstract: Holdings

A Brief Research Note on Holdings And Singapore: Mr. Madoff Goes to Singapore Christopher Balding HSBC Business School Peking University Graduate School [email protected] Short Abstract: Holdings

Chapter 17. Fixed Exchange Rates and Foreign Exchange Intervention. Copyright 2003 Pearson Education, Inc.

Chapter 17 Fixed Exchange Rates and Foreign Exchange Intervention Slide 17-1 Chapter 17 Learning Goals How a central bank must manage monetary policy so as to fix its currency's value in the foreign exchange

Chapter 17 Fixed Exchange Rates and Foreign Exchange Intervention Slide 17-1 Chapter 17 Learning Goals How a central bank must manage monetary policy so as to fix its currency's value in the foreign exchange

University of Lethbridge Department of Economics ECON 1012 Introduction to Macroeconomics Instructor: Michael G. Lanyi

University of Lethbridge Department of Economics ECON 1012 Introduction to Macroeconomics Instructor: Michael G. Lanyi CH 25 Exch Rate & BofP 1) Foreign currency is A) the market for foreign exchange.

University of Lethbridge Department of Economics ECON 1012 Introduction to Macroeconomics Instructor: Michael G. Lanyi CH 25 Exch Rate & BofP 1) Foreign currency is A) the market for foreign exchange.

Lecture 2. Output, interest rates and exchange rates: the Mundell Fleming model.

Lecture 2. Output, interest rates and exchange rates: the Mundell Fleming model. Carlos Llano (P) & Nuria Gallego (TA) References: these slides have been developed based on the ones provided by Beatriz

Lecture 2. Output, interest rates and exchange rates: the Mundell Fleming model. Carlos Llano (P) & Nuria Gallego (TA) References: these slides have been developed based on the ones provided by Beatriz

The Return of Saving

Martin Feldstein the u.s. savings rate and the global economy The savings rate of American households has been declining for more than a decade and recently turned negative. This decrease has dramatically

Martin Feldstein the u.s. savings rate and the global economy The savings rate of American households has been declining for more than a decade and recently turned negative. This decrease has dramatically

Impact of Global Financial Crisis on South Asia

Impact of Global Financial Crisis on South Asia February 17, 2009 - The global financial crisis hit South Asia at a time when it had barely recovered from severe terms of trade shock resulting from the

Impact of Global Financial Crisis on South Asia February 17, 2009 - The global financial crisis hit South Asia at a time when it had barely recovered from severe terms of trade shock resulting from the

A BRIEF HISTORY OF BRAZIL S GROWTH

A BRIEF HISTORY OF BRAZIL S GROWTH Eliana Cardoso and Vladimir Teles Organization for Economic Co operation and Development (OECD) September 24, 2009 Paris, France. Summary Breaks in Economic Growth Growth

A BRIEF HISTORY OF BRAZIL S GROWTH Eliana Cardoso and Vladimir Teles Organization for Economic Co operation and Development (OECD) September 24, 2009 Paris, France. Summary Breaks in Economic Growth Growth

European Debt Crisis and Impacts on Developing Countries

July December 2011 SR/GFC/11 9 SESRIC REPORTS ON GLOBAL FINANCIAL CRISIS 9 SESRIC REPORTS ON THE GLOBAL FINANCIAL CRISIS European Debt Crisis and Impacts on Developing Countries STATISTICAL ECONOMIC AND

July December 2011 SR/GFC/11 9 SESRIC REPORTS ON GLOBAL FINANCIAL CRISIS 9 SESRIC REPORTS ON THE GLOBAL FINANCIAL CRISIS European Debt Crisis and Impacts on Developing Countries STATISTICAL ECONOMIC AND

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Study Questions 5 (Money) MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The functions of money are 1) A) medium of exchange, unit of account,

Study Questions 5 (Money) MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The functions of money are 1) A) medium of exchange, unit of account,

THE ARGENTINEAN DEBT: HISTORY, DEFAULT AND RESTRUCTURING. Mario Damill Roberto Frenkel Martín Rapetti

THE ARGENTINEAN DEBT: HISTORY, DEFAULT AND RESTRUCTURING Mario Damill Roberto Frenkel Martín Rapetti CEDES Buenos Aires, April 2005 1 The Argentinean debt: history, default and restructuring Mario Damill,

THE ARGENTINEAN DEBT: HISTORY, DEFAULT AND RESTRUCTURING Mario Damill Roberto Frenkel Martín Rapetti CEDES Buenos Aires, April 2005 1 The Argentinean debt: history, default and restructuring Mario Damill,

MGE #13 Capital mobility and interest rates

MGE #13 Capital mobility and interest rates Loanable funds market and interest rates in the long-run Capital flows and monetary policy, with fixed exchange rates The Mexican crisis of 1994 1 From the last

MGE #13 Capital mobility and interest rates Loanable funds market and interest rates in the long-run Capital flows and monetary policy, with fixed exchange rates The Mexican crisis of 1994 1 From the last

CHAPTER 3 BALANCE OF PAYMENTS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

CHAPTER 3 BALANCE OF PAYMENTS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Define the balance of payments. Answer: The balance of payments (BOP) can be defined

CHAPTER 3 BALANCE OF PAYMENTS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Define the balance of payments. Answer: The balance of payments (BOP) can be defined

CHAPTER 32 EXCHANGE RATES, BALANCE OF PAYMENTS, AND INTERNATIONAL DEBT

CHAPTER 32 EXCHANGE RATES, BALANCE OF PAYMENTS, AND INTERNATIONAL DEBT Chapter in a Nutshell Along with the flows of goods and services being traded between countries, there are corresponding flows of

CHAPTER 32 EXCHANGE RATES, BALANCE OF PAYMENTS, AND INTERNATIONAL DEBT Chapter in a Nutshell Along with the flows of goods and services being traded between countries, there are corresponding flows of

Lessons from a comparative analysis of financial crises 1 Roberto Frenkel 2. Introduction

Lessons from a comparative analysis of financial crises 1 Roberto Frenkel 2 Introduction The paper is presented in two parts. The first part presents a comparative analysis of a set of financial crises

Lessons from a comparative analysis of financial crises 1 Roberto Frenkel 2 Introduction The paper is presented in two parts. The first part presents a comparative analysis of a set of financial crises

Econ 202 Section 2 Final Exam

Douglas, Fall 2009 December 17, 2009 A: Special Code 0000 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 202 Section 2 Final Exam 1. The present value

Douglas, Fall 2009 December 17, 2009 A: Special Code 0000 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 202 Section 2 Final Exam 1. The present value

BALANCE OF PAYMENTS AND FOREIGN DEBT

BALANCE OF PAYMENTS AND FOREIGN DEBT V 1. BALANCE OF PAYMENTS In 1997, the external current account deficit was 8.1 billion krónur, corresponding to 1. percent of GDP. It declined from 8.9 b.kr., or 1.8

BALANCE OF PAYMENTS AND FOREIGN DEBT V 1. BALANCE OF PAYMENTS In 1997, the external current account deficit was 8.1 billion krónur, corresponding to 1. percent of GDP. It declined from 8.9 b.kr., or 1.8

Monetary policy, fiscal policy and public debt management

Monetary policy, fiscal policy and public debt management People s Bank of China Abstract This paper touches on the interaction between monetary policy, fiscal policy and public debt management. The first

Monetary policy, fiscal policy and public debt management People s Bank of China Abstract This paper touches on the interaction between monetary policy, fiscal policy and public debt management. The first

Debt Forgiveness: Dangerous Trend or Absolute Necessity

A revised version appears as: "Debt Forgiveness: Dangerous Trend or Absolute Necessity?" World Link, Vol. 4, No. 5 (September/October 1991), pp. 37-39. Debt Forgiveness: Dangerous Trend or Absolute Necessity

A revised version appears as: "Debt Forgiveness: Dangerous Trend or Absolute Necessity?" World Link, Vol. 4, No. 5 (September/October 1991), pp. 37-39. Debt Forgiveness: Dangerous Trend or Absolute Necessity

External Debt and Growth

External Debt and Growth Catherine Pattillo, Hélène Poirson and Luca Ricci Reasonable levels of external debt that help finance productive investment may be expected to enhance growth, but beyond certain

External Debt and Growth Catherine Pattillo, Hélène Poirson and Luca Ricci Reasonable levels of external debt that help finance productive investment may be expected to enhance growth, but beyond certain

IV. Special feature: Foreign currency deposits of firms and individuals with banks in China

Robert N McCauley (+852) 2878 71 [email protected] YK Mo (+852) 2878 71 IV. Special feature: deposits of firms and individuals with banks in China In principle, an economy with capital controls can

Robert N McCauley (+852) 2878 71 [email protected] YK Mo (+852) 2878 71 IV. Special feature: deposits of firms and individuals with banks in China In principle, an economy with capital controls can

Why a Credible Budget Strategy Will Reduce Unemployment and Increase Economic Growth. John B. Taylor *

Why a Credible Budget Strategy Will Reduce Unemployment and Increase Economic Growth John B. Taylor * Testimony Before the Joint Economic Committee of the Congress of the United States June 1, 011 Chairman

Why a Credible Budget Strategy Will Reduce Unemployment and Increase Economic Growth John B. Taylor * Testimony Before the Joint Economic Committee of the Congress of the United States June 1, 011 Chairman

Anti-Crisis Stimulus Package for Economic Recovery

Anti-Crisis Stimulus Package for Economic Recovery (Developing Efficient State Debt Management Policy) The project is implemented in the framework of The East-West Management Institute s (EWMI) Policy,

Anti-Crisis Stimulus Package for Economic Recovery (Developing Efficient State Debt Management Policy) The project is implemented in the framework of The East-West Management Institute s (EWMI) Policy,

Agenda. Saving and Investment in the Open Economy. Balance of Payments Accounts. Balance of Payments Accounting. Balance of Payments Accounting.

Agenda. Saving and Investment in the Open Economy Goods Market Equilibrium in an Open Economy. Saving and Investment in a Small Open Economy. Saving and Investment in a Large Open Economy. 7-1 7-2 Balance

Agenda. Saving and Investment in the Open Economy Goods Market Equilibrium in an Open Economy. Saving and Investment in a Small Open Economy. Saving and Investment in a Large Open Economy. 7-1 7-2 Balance

With lectures 1-8 behind us, we now have the tools to support the discussion and implementation of economic policy.

The Digital Economist Lecture 9 -- Economic Policy With lectures 1-8 behind us, we now have the tools to support the discussion and implementation of economic policy. There is still great debate about

The Digital Economist Lecture 9 -- Economic Policy With lectures 1-8 behind us, we now have the tools to support the discussion and implementation of economic policy. There is still great debate about

Section 2 Evaluation of current account balance fluctuations

Section 2 Evaluation of current account balance fluctuations Key points 1. The Japanese economy and IS balance trends From a macroeconomic perspective, the current account balance weighs the Japanese economy

Section 2 Evaluation of current account balance fluctuations Key points 1. The Japanese economy and IS balance trends From a macroeconomic perspective, the current account balance weighs the Japanese economy

Lecture 7: Savings, Investment and Government Debt

Lecture 7: Savings, Investment and Government Debt September 18, 2014 Prof. Wyatt Brooks Problem Set 1 returned Announcements Groups for in-class presentations will be announced today SAVING, INVESTMENT,

Lecture 7: Savings, Investment and Government Debt September 18, 2014 Prof. Wyatt Brooks Problem Set 1 returned Announcements Groups for in-class presentations will be announced today SAVING, INVESTMENT,

Asian Development Bank

ERD POLICY BRIEF SERIES Economics and Research Department Number 7 Causes of the 1997 Asian Financial Crisis: What Can an Early Warning System Model Tell Us? Juzhong Zhuang Malcolm Dowling Asian Development

ERD POLICY BRIEF SERIES Economics and Research Department Number 7 Causes of the 1997 Asian Financial Crisis: What Can an Early Warning System Model Tell Us? Juzhong Zhuang Malcolm Dowling Asian Development

28.10.2013. The recovery of the Spanish economy XVI Congreso Nacional de la Empresa Familiar/Instituto de la Empresa Familiar Luis M.

28.10.2013 The recovery of the Spanish economy XVI Congreso Nacional de la Empresa Familiar/Instituto de la Empresa Familiar Luis M. Linde Governor Let me begin by thanking you for inviting me to take

28.10.2013 The recovery of the Spanish economy XVI Congreso Nacional de la Empresa Familiar/Instituto de la Empresa Familiar Luis M. Linde Governor Let me begin by thanking you for inviting me to take

Mexico: The challenges of capital inflows. Manuel Sánchez, Deputy Governor

Manuel Sánchez, Deputy Governor Adam Smith Seminar, Schloss Spiez, Switzerland, June 26, 2013 Contents 1 Taxonomy of capital inflows 2 Risks and the prevention of problems 3 Economic outlook 2 Like other

Manuel Sánchez, Deputy Governor Adam Smith Seminar, Schloss Spiez, Switzerland, June 26, 2013 Contents 1 Taxonomy of capital inflows 2 Risks and the prevention of problems 3 Economic outlook 2 Like other

Reducing public debt: Turkey

Reducing public debt: Turkey Abstract Turkey halved the ratio of public debt to GDP from almost 80 percent in 2001 to less than 40 percent before the global crisis of 2009. Several factors helped. First,

Reducing public debt: Turkey Abstract Turkey halved the ratio of public debt to GDP from almost 80 percent in 2001 to less than 40 percent before the global crisis of 2009. Several factors helped. First,

Economics 101 Multiple Choice Questions for Final Examination Miller

Economics 101 Multiple Choice Questions for Final Examination Miller PLEASE DO NOT WRITE ON THIS EXAMINATION FORM. 1. Which of the following statements is correct? a. Real GDP is the total market value

Economics 101 Multiple Choice Questions for Final Examination Miller PLEASE DO NOT WRITE ON THIS EXAMINATION FORM. 1. Which of the following statements is correct? a. Real GDP is the total market value

THE GROUP OF 8 EXTERNAL DEBT CANCELLATION Effects and implications for Guyana

THE GROUP OF 8 EXTERNAL DEBT CANCELLATION Effects and implications for Guyana Introduction Guyana is one of the most indebted emerging market economies in the world. In 2004, its total public external

THE GROUP OF 8 EXTERNAL DEBT CANCELLATION Effects and implications for Guyana Introduction Guyana is one of the most indebted emerging market economies in the world. In 2004, its total public external

Pre-Test Chapter 11 ed17

Pre-Test Chapter 11 ed17 Multiple Choice Questions 1. Built-in stability means that: A. an annually balanced budget will offset the procyclical tendencies created by state and local finance and thereby

Pre-Test Chapter 11 ed17 Multiple Choice Questions 1. Built-in stability means that: A. an annually balanced budget will offset the procyclical tendencies created by state and local finance and thereby

A proposal for debt relief among Caribbean SIDS. 17th Meeting of the Monitoring Committee of the CDCC

A proposal for debt relief among Caribbean SIDS Emerging challenges Region has experienced lower GDP growth since the post crisis period with an average of 1.2% in 2014. ECLAC projects that in 2015 growth

A proposal for debt relief among Caribbean SIDS Emerging challenges Region has experienced lower GDP growth since the post crisis period with an average of 1.2% in 2014. ECLAC projects that in 2015 growth

Economics 380: International Economics Fall 2000 Exam #2 100 Points

Economics 380: International Economics Fall 2000 Exam #2 100 Points Name (ID) YOU SHOULD HAVE 7 PAGES FOR THIS EXAM. EXAM WILL END AT 1:50. MAKE SURE YOUR NAME IS ON THE FIRST AND LAST PAGE OF THE EXAM.

Economics 380: International Economics Fall 2000 Exam #2 100 Points Name (ID) YOU SHOULD HAVE 7 PAGES FOR THIS EXAM. EXAM WILL END AT 1:50. MAKE SURE YOUR NAME IS ON THE FIRST AND LAST PAGE OF THE EXAM.

THE IMPORTANCE OF RISK MANAGEMENT

THE IMPORTANCE OF RISK MANAGEMENT Andrew L. T. Sheng* I have a terribly difficult task, because I have very little to add after such excellent presentations by three wise men, Stanley Fischer, whom I worked

THE IMPORTANCE OF RISK MANAGEMENT Andrew L. T. Sheng* I have a terribly difficult task, because I have very little to add after such excellent presentations by three wise men, Stanley Fischer, whom I worked

Financial Crisis and the fluctuations of the global crude oil prices and their impacts on the Iraqi Public Budget Special Study

Financial Crisis and the fluctuations of the global crude oil prices and their impacts on the Iraqi Public Budget Special Study Dr.Ahmed-Al-Huseiny* ABSTRACT The Iraqi economy is not isolated from the

Financial Crisis and the fluctuations of the global crude oil prices and their impacts on the Iraqi Public Budget Special Study Dr.Ahmed-Al-Huseiny* ABSTRACT The Iraqi economy is not isolated from the